bridging macro to micro: gs top-down stock...

TRANSCRIPT

June 11, 2012

Bridging macro to micro: GS

top-down stock selection

Portfolio Strategy Research

A tool to translate macro views into stock ideas

We introduce a top-down stock picking framework which builds upon

macro factor mapping, micro-specific comparisons, and business-cycle-

based investing, aiming to connect macro views to micro implementation.

Macro and micro are both important to returns

Macro factors such as global growth, local growth and financial conditions

are important return drivers for around 60% of market cap in Asia.

Additionally, micro specifics such as valuations, consensus EPS changes,

and technical indicators have strong links with ensuing 3-month returns.

Macro + Micro = Alpha

Using the four phases of the business cycle as defined by our Global

Leading Indicator (GLI), we select stocks based on their macro and micro

characteristics. Backtests suggest that such an approach would help

produce returns that exceed those of traditional buy/hold strategies.

Stock picks in a contraction phase: Lower beta and growth

exposure; and buy easing beneficiaries

Our GLI suggests that we are currently in a contraction phase (since April).

Against this backdrop, we highlight stocks with appropriate macro

exposure and micro support: NAB, Orica, Hengan, PetroChina, Tencent,

CK, HSB, HDFC, ITC, BRI, LS Corp, Shinhan, CIMB, SM Inv., JCC, Delta,

TSMC and BK Bank. We intend to refresh our stock ideas on a regular

basis.

Top-down analysis works for select economic groups but not all

Source: FactSet, MSCI, CEIC, Goldman Sachs Global ECS Research.

Kinger Lau, CFA

+852-2978-1224 [email protected] Goldman Sachs (Asia) L.L.C.

Timothy Moe, CFA

+852-2978-1328 [email protected] Goldman Sachs (Asia) L.L.C.

Caesar Maasry

+852-2978-7213 [email protected] Goldman Sachs (Asia) L.L.C.

Richard Tang

+852-2978-0722 [email protected] Goldman Sachs (Asia) L.L.C.

Sunil Koul

+852-2978-0924 [email protected] Goldman Sachs (Asia) L.L.C.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investorsshould be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and otherimportant disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed bynon-US affiliates are not registered/qualified as research analysts with FINRA in the U.S. This report is intended fordistribution to GS institutional clients only.

The Goldman Sachs Group, Inc. Goldman Sachs Global Economics, Commodities and Strategy Research

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 2

Introducing GS top-down stock picking framework

In this report, we introduce a framework to help connect the macro environment to

single stock selection.

Specifically, we believe this framework would be helpful to:

Formalize our existing top-down stock picking logic and approach in a disciplined

and statistically-tested manner that is also intuitively appealing

Better comprehend how macro factors influence individual stock returns and help

connect macro trends to actionable stock ideas

Expand our implementation focus to include more single stock ideas as well as

theme baskets and derivative overlays

Complement our sector analysts’ views and our bottom-up stock selection

processes such as Asia-Pacific Conviction Lists and GS Sustain, which focus

principally on operating returns and industry position

Provide a tool which can add further perspective to investors’ own stock selection

processes

The exhibit below summarizes the key building blocks and logic flow in this report.

The key building blocks and approach of our stock-selection framework

Source: FactSet, I/B/E/S, Goldman Sachs Global ECS Research estimates.

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 3

Executive summary

Top-down and bottom-up are the two prevalent approaches to securities analysis.

However, neither is perfect— macro-focused investors may overlook micro factors and

industry dynamics while stock pickers may sometimes miss the big picture.

With an objective of combining the two approaches and translating macro views into

actionable stock ideas (and, hopefully, good returns), we introduce a top-down stock

selection framework which builds upon macro factor profiling, micro specific

comparisons, and business-cycle-based investing.

Key conclusions and investment implications in this report are:

1. Macro analysis is important, even to stock pickers. Our regression model

shows select macroeconomic factors are statistically significant return drivers

(R²>40%) for around 250 stocks in Asia, representing 58% of MXAPJ market cap.

This underscores the importance of macro analysis even to bottom-up-oriented

investors. Macro analysis is particularly effective in Hong Kong, China, Singapore,

and sectors including energy, financials, and materials.

2. Some macro variables are more important than others. Investors can be

overwhelmed by macro data, but many macroeconomic variables are highly

correlated. Stock pickers can simplify the process of macro monitoring by

focusing on six factors, namely, market risk, local growth, policy/liquidity, CPI,

oil prices, and global growth.

3. Micro specifics have linked well with ensuing returns. Empirically, micro

considerations such as valuation, consensus EPS and target price changes, and

technical entry levels have shown very strong relationships with ensuing 3-

month returns. These micro considerations complement the macro perspective

and address the extent to which fundamentals are discounted in share prices.

4. Our two-tier stock selection strategy may help performance. We have

established a trading algorithm based on our global leading indicator and its

derived business cycle— expansion, slowdown, contraction, and recovery— to

implement our macro and micro analysis. Backtests of our two-tier strategy

suggest performance can be enhanced to a meaningful extent by considering

these macro and micro factors.

5. Useful tool. This framework is flexible and can complement the investment

process for different types of investors.

Caveats: A tool, not a cure-all

We believe this approach adds value, but we also recognize its limitations. Regression

models are static and assume mean-reversion, and need to be updated and refined to

adapt to changing fundamentals.

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 4

Stock ideas: Investing in a contraction phase The latest GLI reading suggests the global economy has entered a contraction phase.

Against this backdrop, we would:

a. Reduce market risk “beta”;

b. Buy stocks with low sensitivity to local growth;

c. Accumulate policy easing beneficiaries;

d. Own stocks that may outperform in a disinflationary environment;

e. Buy stocks that may benefit from lower oil prices;

f. Overweight stocks that are less sensitive to global growth momentum.

Stocks which have these macro characteristics and have shown favorable micro readings

are shown in Exhibit 1.

Exhibit 1: We like these stocks because of their favorable macro exposure and compelling micro profile relative to their

regional peers Stock recommendations for June 2012 (Priced as of June 5)

Note (1): These stocks are rated Buy or Neutral by Goldman Sachs Research except SM Investments which is NC. We use consensus estimates for SM Investments. Note (2): * denotes the stock is on our regional Conviction List. “Tick” indicates stock that ranks top-30 percentile within each factor relative to its market peers and they perform well in our specified macro environment. Revisions and sentiment are based on forward 12-month consensus EPS.

Source: Factset, I/B/E/S, Goldman Sachs Global ECS Research estimates.

Key exhibits for chart lovers

We highlight the important exhibits (takeaways) as follows:

Exhibit 7: Where top-down analysis may be more applicable in terms of markets

and sectors.

Exhibit 8: Stocks that are the most and least sensitive to different macro factors

across markets.

Exhibit 17: The empirical relationships between micro parameters and ensuing

returns.

Exhibits 28 to 38: Market summary pages which detail the factor loading for each

stock under our study universe.

Ticker Name MarketMkt. cap

(US$mn)

6m

ADVT

GS

Rating

Global

growth

13E

P/E

13E

P/B

13E

D/Y

13E

EPSg

EPS

rev.

EPS

sent.

14d

RSI%b

NAB AT National Australia Bank Australia 49,179 156.9 B √ √ √ 8.4 1.2 8.6% 5% -1% 17% 35 14%

ORI AT Orica Australia 8,473 34.8 B* √ √ 10.8 2.1 4.7% 16% 3% 13% 28 9%

1044 HK Hengan Int'L Group Co China 6,748 20.1 N √ √ √ 19.9 5.7 3.2% 21% 4% 43% 32 -4%

857 HK Petrochina Co H China 26,240 89.1 N √ √ √ 8.6 1.2 5.2% 8% 3% 0% 28 5%

700 HK Tencent Holdings Lim(Cn) China 27,186 98.2 B √ 19.2 5.5 0.6% 27% 4% 22% 37 13%

1 HK Cheung Kong Holdings Hong Kong 15,492 51.2 B √ √ √ 7.7 0.6 3.9% 16% 2% 6% 28 8%

11 HK Hang Seng Bank Hong Kong 9,866 19.6 N √ √ √ 10.6 2.1 5.2% 9% 2% 15% 38 26%

HDFC IS Housing Dev Finance Corp India 12,601 57.4 N √ √ √ 14.8 3.2 2.2% 15% 15% -15% 44 44%

ITC IS ITC India 8,867 33.4 B √ √ √ 21.5 8.0 2.8% 17% 4% 23% 41 0%

BBRI IJ Bank Rakyat Indonesia Indonesia 6,253 24.4 N √ √ √ 7.2 1.7 2.8% 13% 3% -5% 23 8%

006260 KP LS Corp Korea 1,162 9.2 B √ √ 6.4 0.9 1.6% 23% 5% 50% 47 23%

055550 KP Shinhan Financial Group Korea 13,742 40.0 N √ √ √ 6.3 0.7 2.9% 4% 1% 19% 39 31%

CIMB MK CIMB Group Holdings Bhd Malaysia 11,204 23.8 N √ √ 11.6 1.8 4.1% 12% 2% -8% 52 60%

SM PM SM Investments Philippines 3,334 9.2 NC √ √ √ 15.5 2.1 1.7% 12% 2% 0% 48 36%

JCNC SP Jardine Cycle & Carriage Singapore 3,467 7.8 N √ 8.3 - 5.1% 24% 9% 0% 33 17%

2308 TT Delta Electronics Taiwan 4,749 21.5 B √ √ 12.7 2.0 5.8% 10% 8% 67% 36 11%

2330 TT Taiwan Semiconductor Mfg Taiwan 64,204 101.0 N √ √ √ 11.5 2.5 3.8% 10% 10% 56% 41 11%

BBL/F TB Bangkok Bank Fgn Thailand 4,617 7.7 B* √ √ √ 8.6 1.1 4.4% 17% 4% 38% 31 -13%

Median 9,366 28.9 10.7 2.0 3.9% 14% 3% 16% 37 12%

MXAPJ 9.3 1.3 4.0% 11% 0% -6% 30 16%

Factor loading Valuations Fundamentals Technical

Market

risks

Local

growth

Policy/

liquidityInflation Oil

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 5

Part 1: Mapping stock returns to macro exposure

Defining our study universe

To ensure the practicability of the regression results, we choose to focus on MXAPJ

constituents with at least US$1bn of index market cap, over US$5mn of average daily value

traded (ADVT) in the past 6 months, and at least 5 years of listing history. There are 412

stocks in MXAPJ which fit these requirements (as of April 30, 2012) and they represent

86% of MXAPJ index market cap. These stocks are mostly located in Australia, China,

Korea and India, with a sector concentration in financials, IT and telecoms (Exhibits 2 and

3).

Exhibit 2: Liquid, large-cap stocks are mostly found in

Australia, China, Korea and India Free-float market cap distribution by markets

Exhibit 3: ...and they are concentrated in sectors including

financials, IT, and telecoms Free-float market cap distribution by sectors

Source: FactSet, MSCI, Goldman Sachs Global ECS Research.

Source: FactSet, MSCI, Goldman Sachs Global ECS Research.

Defining the dependent variables (returns)

We choose 3-month price returns as the dependent variable in our regression model as

we attempt to strike a balance between high frequency trading and the “buy-and-hold”

approach. Returns are quoted in local currency, on our assumption that foreign

investors should treat the currency decisions separately from the stock selection decisions

and the impact of FX changes could be partly reflected/captured in the underlying macro

trends (e.g. exports in CAI and FCI).

Choosing and testing independent variables (macro factors)

While there are a large number of macro variables that equity investors could focus on, we

elect to limit our independent variables to 14 macro factors which theoretically should

drive stock prices. In other words, this is not an exhaustive list of macro variables which

might influence stock returns but what we have found to be generally influential at a

market level. See Asia Pacific: Portfolio Strategy: What macro indicators matter for Asian

markets?, May 7, for details.

We also test the statistical significance of 2nd derivatives and lead/lags for each of the

factors in our multi-factor regression model to ensure statistically important relationships

will be accounted for.

Given many of these variables are inter-correlated and are essentially linked to similar sets

of fundamental drivers, we run a correlation matrix to eliminate those with strong

Australia20%

China23%

Hong Kong8%

India11%

Indonesia2%

Korea16%

Malaysia2%

Philippines0%

Singapore5%

Taiwan9%

Thailand4%

Banks23%

Information Technology

14%

Telecom11%

Materials10%

Energy9%

Industrials7%

Cons Disc7%

Cons Stap6%

Property6%

Insurance and other financial

services4%

Utilities2%

Health Care1%

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 6

directional relationships to improve the ensuing regression results (Appendix 1). In cases

where macro factors are strongly correlated among each other within a category (e.g.

growth), we prefer our proprietary indexes such as Current Activity Index (CAI), Financial

Conditions Index (FCI), and Global Leading Indicator (GLI) given their broader

representation and statistically-tested robustness (see Exhibit 4).

Following the above steps, we conclude that a significant part of an individual stock’s

return variations can be reasonably explained by 6 broad macro measurements: Market

risk (MXAPJ), domestic growth (CAI), domestic liquidity/policy (FCI), domestic

inflation (CPI), oil prices (WTI), and global growth (GLI).

The final step is to establish linkages between returns and these macro factors by using

regression techniques, namely simple linear and multiple factor regression models.

Recognizing the advantages and deficiencies of these modeling techniques, we choose to

base our stock selection analysis on the former and the market analysis on the latter.

Simple linear regression by a single factor (e.g. six separate regression models)

allows us to estimate the factor loadings for the independent variables without

running into multicollinearity issues. This approach may work better in capturing

the maximum total exposure to a single factor. That said, it doesn't account for the

impact of other significant variables and therefore is not robust to changes in the

relationship between macro factors over time. Even if we run a number of single

factor regressions, the resulting individual R²s from this are not additive and we

cannot statistically prove the explanatory power of each factor for returns.

Multiple factor regression with stepwise elimination helps form a quantifiable

relationship (equation) as to what factors are important and to what extent they,

when all treated as independent variables, have historically affected stock returns

(when one factor changes and others are held constant). The drawback is that the

(high) correlation among macro variables lowers the precision of the regression

estimates, which is likely to lead to estimates being very inaccurate for some

stocks when the regressions are carried out across a large universe of single

stocks. If we subsequently use the analysis to pick stocks with the highest/lowest

sensitivities there is a risk that we will also end up maximizing exposure to

estimation errors.

Exhibit 4: The independent variables in our regression model are representative of the principal macro categories that

tend to influence stock returns Macro variables and the inputs to our regression model

Note: We use the next 3 month yoy growth for CAI (local/US/EU) as they show significantly higher correlations with returns, which provides better indicative power on returns and fits our purpose of mapping returns to macro exposure better. See Appendix 1 for details.

Source: FactSet, I/B/E/S, Goldman Sachs Global ECS Research estimates.

Input specifications

Chosen

variablesRegional index returns Log P(t)‐Log P(t‐3)

Country index returns Log P(t)‐Log P(t‐3)Regional sector index returns Log P(t)‐Log P(t‐3)

Local IP Log (Avg. of last 3 monthly yoy growth)

Local export growth Log (Avg. of last 3 monthly yoy growth)

Local retail sales Log (Avg. of last 3 monthly yoy growth)

Local CAI Log (Avg. of next 3 monthly yoy growth)

Local PMI Log (Avg. of latest 3 mom growth)

Local CPI Log (Avg. of last 3 monthly yoy growth) Local CPI

Local FCI Log (Avg. of last 3 monthly yoy growth) Local FCI

WTI Price Log WTI(t)‐Log WTI(t‐3)US CAI Log (Avg. of next 3 monthly yoy growth)

EU CAI Log (Avg. of next 3 monthly yoy growth)

EM GDP Log (Avg. of last 3 monthly yoy growth)

GLI momentum Log (latest 3 mom changes)

MXAPJ returns

Local CAI

WTI

GLI

Indep

enden

t variab

les

Stock beta

Domestic growth

Domestic

liquidity/policy

Global growth

• Correlationmatrix

• Multi‐collinearity

check

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 7

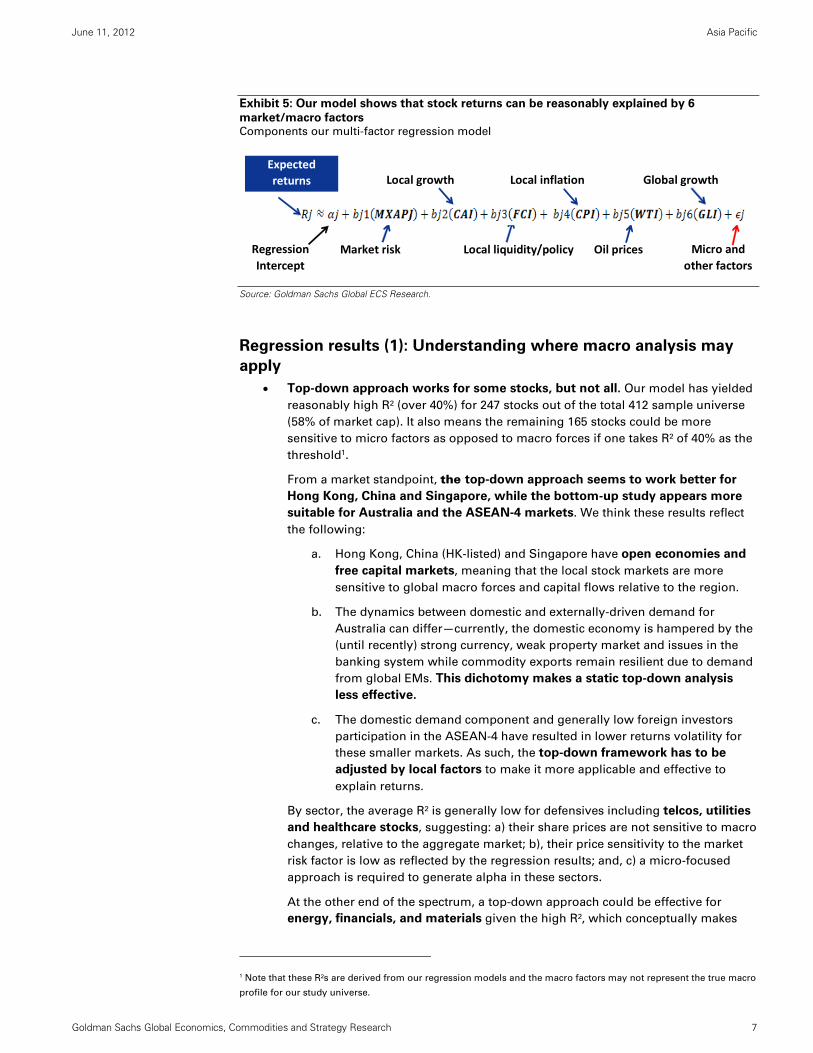

Exhibit 5: Our model shows that stock returns can be reasonably explained by 6

market/macro factors Components our multi-factor regression model

Source: Goldman Sachs Global ECS Research.

Regression results (1): Understanding where macro analysis may

apply

Top-down approach works for some stocks, but not all. Our model has yielded

reasonably high R² (over 40%) for 247 stocks out of the total 412 sample universe

(58% of market cap). It also means the remaining 165 stocks could be more

sensitive to micro factors as opposed to macro forces if one takes R² of 40% as the

threshold1.

From a market standpoint, the top-down approach seems to work better for

Hong Kong, China and Singapore, while the bottom-up study appears more

suitable for Australia and the ASEAN-4 markets. We think these results reflect

the following:

a. Hong Kong, China (HK-listed) and Singapore have open economies and

free capital markets, meaning that the local stock markets are more

sensitive to global macro forces and capital flows relative to the region.

b. The dynamics between domestic and externally-driven demand for

Australia can differ—currently, the domestic economy is hampered by the

(until recently) strong currency, weak property market and issues in the

banking system while commodity exports remain resilient due to demand

from global EMs. This dichotomy makes a static top-down analysis

less effective.

c. The domestic demand component and generally low foreign investors

participation in the ASEAN-4 have resulted in lower returns volatility for

these smaller markets. As such, the top-down framework has to be

adjusted by local factors to make it more applicable and effective to

explain returns.

By sector, the average R² is generally low for defensives including telcos, utilities

and healthcare stocks, suggesting: a) their share prices are not sensitive to macro

changes, relative to the aggregate market; b), their price sensitivity to the market

risk factor is low as reflected by the regression results; and, c) a micro-focused

approach is required to generate alpha in these sectors.

At the other end of the spectrum, a top-down approach could be effective for

energy, financials, and materials given the high R², which conceptually makes

1 Note that these R²s are derived from our regression models and the macro factors may not represent the true macro

profile for our study universe.

Market risk Local liquidity/policy Oil prices

Local inflation Global growthExpected

returns

Regression

Intercept

Local growth

Micro and

other factors

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 8

sense as these sectors are closely linked with global dynamics via real demand

and financial channels.

Exhibit 6: Macro factors appear important return drivers (R² more than 40%) for 60% of the

stocks and 58% of market cap in MXAPJ

Accumulated distribution of R² based on our study universe

Source: Goldman Sachs Global ECS Research estimates.

Exhibit 7: Top-down analysis works for select economic groups but not all Average R² based on our multi-factor regression

Source: FactSet, I/B/E/S, Goldman Sachs Global ECS Research estimates.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Top‐down approach may work better

Macro factors explain >40% of return variations

% of market cap

R2

Bottom‐up approach may work better

Macro factors explain<40% of return variations

Utilities

Health

care Telecom Con. Stp. Con. Disc. Industrials IT Materials Financials Energy Average

Hong Kong 0.16 ‐ ‐ ‐ 0.45 0.60 0.64 ‐ 0.63 ‐ 0.55

China 0.31 0.51 0.50 0.42 0.48 0.61 0.53 0.59 0.66 0.57 0.55

Singapore ‐ ‐ 0.27 0.47 0.41 0.56 ‐ ‐ 0.58 ‐ 0.52

India 0.48 0.25 0.55 0.29 0.50 0.52 0.56 0.53 0.47 0.41 0.46

Indonesia 0.42 ‐ 0.47 0.43 0.39 0.46 ‐ 0.28 0.39 0.51 0.40

Thailand ‐ ‐ 0.05 0.21 ‐ ‐ ‐ 0.75 0.46 0.52 0.44

Taiwan ‐ ‐ 0.25 0.26 0.34 0.30 0.49 0.44 0.41 0.48 0.43

Philippines ‐ ‐ 0.25 ‐ ‐ 0.36 ‐ ‐ 0.45 ‐ 0.35

Korea 0.31 0.26 0.15 0.27 0.42 0.42 0.33 0.46 0.48 0.28 0.40

Malaysia 0.16 ‐ 0.16 0.38 0.41 0.25 ‐ ‐ 0.41 ‐ 0.33

Australia 0.03 0.11 0.15 0.29 0.37 0.28 0.15 0.41 0.36 0.38 0.32

Average 0.34 0.31 0.35 0.38 0.46 0.47 0.49 0.49 0.50 0.51

Bottom 25 percentile

Top 25 percentile

Bottom‐up may work better

Bottom‐up may work better

Top downmay work better

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 9

Regression results (2): Making sense of it

We ran macro-factor regressions for more than 400 stocks in Asia and the results are

organized by their factor loadings in each market in Exhibit 8 (we show the top-3 stocks

under each market factor only; regression results for the full universe are shown in the

country summary pages).

Exhibit 8: We group stocks under different macro buckets based on their factor loadings Stocks with highest/lowest factor loadings by market

Note (*): Highest (positive) coefficients for FCI means stocks have historically performed better relative to their benchmark when financial conditions tighten. Note (1): We rank stocks by their factor loadings based on the output from our simple linear regression model. Multiple factor regression models using specific independent variables are required to estimate the relative significance of variables and their explanatory power on returns. Note (2): We only show stocks which rank in the top-80 percentile in terms of R² ranking for that particular factor.

Note (3): We exclude Philippines because only 4 stocks satisfy our liquidity requirements.

Source: Goldman Sachs Global ECS Research estimates.

Highest Lowest Highest Lowest Highest Lowest Highest Lowest Highest Lowest Highest Lowest

Lynas Corporation

Westfield Group Goodman Group Telstra Corp Origin Energy OZ Minerals Metcash WorleyparsonsFortescue

Metals GroupTatts Group

Lynas Corporation

Westfield Group

Fortescue Metals Group

Westpac Banking

Fortescue Metals Group

CFX retail SantosLynas

CorporationOrigin Energy Goodman Group OZ Minerals Coca-Cola Amatil Goodman Group

Westpac Banking

OZ MineralsNational

Australia BankLynas

CorporationNational

Australia BankIluka Resources Goodman Group

Ramsay Health Care

Lynas Corporation Goodman Group Westfield GroupFortescue

Metals GroupNational

Australia BankNine Dragons

PaperBeijing

Enterprises HldgNine Dragons

PaperTingyi Holding

Corp(Cn)China Resources

PowerNine Dragons

PaperChina Unicom

Nine Dragons Paper

China COSCO H China MobileNine Dragons

PaperHengan Int'L

Group Co

China COSCO HHengan Int'L

Group CoChina Cosco Holdings H

Beijing Enterprises Hldg

China MobileIntime

Department CNOOC

Shimao Property Hldgs

China Coal Energy H

China Telecom Corp H

Intime Department

Tsingtao Brewery H

Agile Property Hldgs

China Resources Power

China Coal Energy H

Tsingtao Brewery H

China Telecom Corp H

China Coal Energy H

China Overseas Land &Inv

Agile Property Hldgs

Nine Dragons Paper

China Resources Land

China Coal Energy H

China Mobile

Galaxy Entertainment

Link REITFoxconn

InternationalCLP Holdings

Foxconn International

Cheung Kong Infrastruct.

HongKong China Gas

Foxconn International

Galaxy Entertainment

CLP HoldingsGalaxy

Entertainment Link REIT

New World Development

HongKong China Gas

Galaxy Entertainment

Link REITHong Kong

Exch.&ClearingPower Assets

HoldingsHang Seng Bank

Orient Overseas Intl

Foxconn International

Link REITFoxconn

InternationalHongKong China

GasFoxconn

InternationalHang Seng Bank

Hong Kong Exch.&Clearing

HongKong China Gas

New World Development

Hang Seng Bank Link REIT BOCHKASM Pacific Technology

HongKong China Gas

ASM Pacific Technology

MTR Corp

Jaiprakash Associates

NTPCJaiprakash Associates

ITCInfrastructure

Dev FinBharti Airtel

Dr Reddy'S Laboratories

Jaiprakash Associates

JSW Steel ITC JSW Steel ITC

Adani Enterprises

Asian PaintsInfrastructure

Dev FinHindustan Unilever

Wipro Lupin Asian Paints Bharti Airtel Tata Steel Gail IndiaSterlite

IndustriesBharti Airtel

Sterlite Industries

Sun Pharmaceutical

Tata Consultancy Hdfc BankHindalco

IndustriesHindustan Unilever

Axis Bank United SpiritsAdani

EnterprisesAsian Paints Tata Steel

Sun Pharmaceutical

Bumi ResourcesTelekomunikasi

IndonesiaIndofood Sukses

MakmurBank Negara

IndonesiaPerusahaan Gas

NegaraBumi Resources

Perusahaan Gas Negara

Bumi Resources Bumi Resources Gudang Garam Bumi ResourcesTelekomunikasi

Indonesia

United Tractors Gudang Garam IndocementBank Rakyat

IndonesiaBank Negara

IndonesiaBank Mandiri

Telekomunikasi Indonesia

United Tractors United TractorsPerusahaan Gas

NegaraUnited Tractors Semen Gresik

Bank Negara Indonesia

Bank Rakyat Indonesia

Bank Mandiri Gudang GaramIndofood Sukses

MakmurUnited Tractors

Indofood Sukses Makmur

Bank Rakyat Indonesia

Indofood Sukses Makmur

Bank Rakyat Indonesia

SK HynixKepco Korea Elect. Power

SK HynixAmorepacific Corp (New)

Doosan Heavy Industries

NCsoft Corp CelltrionDoosan Infracore

CoSK Hynix

LG Household & Health

SK HynixKepco Korea Elect. Power

Hanwha Chemical Corp

Samsung Fire & Marine

Industrial Bank Of Korea

LG Household & Health

Doosan Corp Celltrion NCsoft CorpWoori Finance

HoldingsWoori Finance

HoldingsOrion Corp

Korea Exchange Bank

Cheil Industrial

Dongbu Insurance Co

Kangwon LandHana Financial

HoldingsLG Electronics

Hyundai Heavy Industries

Samsung Electro-Mech. Co

S-Oil Corp SK HynixDaewoo

ShipbuildingLS Corp

Woori Finance Holdings

LG Display

AMMB Holdings Sime Darby AMMB Holdings Genting AirAsiaBumiputra-Commerce

Tenaga Nasional IOI Corp IOI Corp UMW Holdings AMMB Holdings Tenaga Nasional

Genting Public Bank Fgn IOI CorpBumiputra-Commerce

DiGi.com Public Bank Fgn Umw Holdings AMMB Holdings AMMB Holdings Public Bank Fgn IOI Corp UMW Holdings

Bumiputra-Commerce

Malayan Banking Kuala Lumpur

Kepong Malayan Banking AMMB Holdings Genting Resorts World

Kuala Lumpur Kepong

Genting Tenaga Nasional Genting Public Bank Fgn

Keppel LandSingapore Telecom

Keppel LandSingapore Press

HldgSingapore Telecom

Noble GroupSingapore Telecom

Keppel Land Keppel LandSingapore Press

HldgKeppel Land

Singapore Telecom

Golden Agri Resources

Singapore Press Hldg

Golden Agri Resources

Singapore Telecom

OCBC BankOlam

InternationalSingapore Press

HldgOlam International

SembCorp Marine

Singapore Telecom

Golden Agri Resources

Singapore Press Hldg

Wilmar International

Fraser And Neave

Olam International

Ascendas Real Estate Inv

Fraser And Neave

Keppel Corp OCBC Bank Noble Group Noble GroupSingapore

AirlinesKeppel Corp

Singapore Airlines

Chimei Innolux Corp

Far Eastone Telecom. Co

Chimei Innolux Corp

Taiwan Mobile HTCChimei Innolux

CorpHTC

Chimei Innolux Corp

Chimei Innolux Corp

Chunghwa Telecom Co

WPG HoldingsChunghwa Telecom Co

WPG Holdings Taiwan Mobile WPG HoldingsFar Eastone Telecom. Co

Taiwan Mobile WPG HoldingsPresident Chain

StoreEPISTAR WPG Holdings

President Chain Store

Chimei Innolux Corp

Far Eastone Telecom. Co

Novatek Microelectrs

Formosa Petrochemical

Novatek Microelectrs

Chunghwa Telecom Co

Formosa Petrochemical

EPISTAR Taiwan Mobile Wpg Holdings Co Wistron CorpQuanta

ComputerEPISTAR Taiwan Mobile

PTT Global Chemical

PTT Exploration&Pro

PTT Global Chemical

Bangkok Bank Fgn

Bank Of Ayudhya

Charoen Pokphand Foods

Advanced Info Service

PTT Global Chemical

PTT Global Chemical

Charoen Pokphand Foods

PTT Global Chemical

Charoen Pokphand Foods

Thai OilSiam

Commercial Thai Oil

Siam Commercial

Thai Oil PTTPTT

Exploration&ProThai Oil Thai Oil

Kasikornbank Fgn

IRPC PCLSiam

Commercial

IRPC PCLBangkok Bank

FgnBanpu Bangkok Bank

PTT Global Chemical

Bangkok BankSiam

Commercial Banpu Banpu

Bangkok Bank Fgn

BanpuBangkok Bank

Fgn

Korea

Malaysia

Singapore

Taiwan

Thailand

Global growth

Australia

China

Hong Kong

India

Inflation Oil

Indonesia

Linear regression cofficient

Market risks Local growth Policy/ liquidity *

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 10

To better interpret and make sense of the regression output, we think it is useful to look at

a few examples below.

Example 1: Samsung Electronics (005930 KR)

The regression R² is low for Samsung Electronics (33%), suggesting the stock’s

returns could be more sensitive to specific micro factors than the high-level macro

variables that we test.

While Samsung is perceived by investors as a DM growth proxy, its share does not

appear to be well linked with global growth momentum (GLI is eliminated in the

stepwise regression). This coincides with the stock’s substantial outperformance in

the past few years due to its improved competiveness and strong product cycle

(e.g. Galaxy smartphones).

It is positively correlated with domestic growth and liquidity conditions, which

seems normal, although their statistical significance is lower than the market risk

factor.

Exhibit 9: The low R² for Samsung suggests that micro factors could be more important in driving the stock price

Stepwise regression results (Samsung Electronics)

Source: FactSet, CEIC, MSCI, Goldman Sachs Global ECS Research estimates.

Example 2: ICBC (1398 HK)

Our model shows 74% of ICBC’s share price variations can be explained by the

four factors in the stepwise regression model.

ICBC’s sensitivity to the market risk factor is high (high beta), partly reflecting the

relatively high growth and policy volatility (or market concerns) in China.

It is positively correlated with inflation and policy easing as the bank may benefit

from loan pricing and higher loan quota when these macro conditions move in its

favor.

The share prices tend to outperform (underperform) the aggregate market when

global growth decelerates (accelerates), as the stock is not as sensitive as the

MXAPJ aggregate to global growth momentum.

# of obs. 142

R² 33%

Significant variables Eliminated variables

Variable

Estimated

coefficient P value Variable Partial R² P value

Intercept ‐0.02 0.45 GLI Momentum 0.0004 0.76

MXAPJ 0.87 <.0001 CPI 0.0008 0.69

CAI 1.04 0.03

FCI ‐2.25 0.02

WTI ‐0.17 0.05

Low R² ≈ more micro driven

Low "beta" vs. MXAPJ; statistically significant

Positively correlated with local growth and easing; unfavorably

exposed to high oil prices

Eliminated by stepwise process

Low incrementalexplanatory power to the regression

GLI is not a significant return driver although the stock is regarded as

DM proxy

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 11

Exhibit 10: Policy easing should bode well for ICBC but its GDP growth exposure may not be as high as many have

perceived Stepwise regression results (ICBC)

Source: FactSet, CEIC, MSCI, Goldman Sachs Global ECS Research estimates.

Example 3: WesFarmers (WES AU)

The regression R² is high compared with other Australian stocks in our study

sample, meaning that top-down approach may make more sense for WES relative

to other Australian stocks.

The stock has showed low sensitivity to MXAPJ returns in local currency terms.

Higher CPI tends to bode well for stock returns, as high inflation may allow the

company to raise prices more easily.

While the local exposure of its business operations may suggest high sensitivity to

domestic growth activities, domestic CAI is omitted from the regression. This may

reflect the hybrid structure of the Australian economy as discussed on page 7.

Exhibit 11: The market risk sensitivity is generally low for AU stocks due possibly to the omission of FX beta; domestic

activities link well with export growth cycles, adding complications when interpreting regression results Stepwise regression results (WesFarmers)

Source: FactSet, CEIC, MSCI, Goldman Sachs Global ECS Research estimates.

# of obs. 60

R² 74%

Significant variables Eliminated variables

Variable

Estimated

coefficient P value Variable Partial R² P value

Intercept ‐0.03 0.19 WTI 0.0049 0.32

MXAPJ 1.64 <.0001 CAI 0.0053 0.30

CPI 1.66 0.02

FCI ‐1.85 0.04

GLI ‐7.91 0.01

High R² ≈ more macro driven

High "beta" vs. MXAPJ; statistically significant

High CPI may improve loan pricing and easing could mean better loan

growth and lower NPL risksChinese banks may not offer high GDP growth exposure as many would have thought

# of obs. 142

R² 50%

Significant variables Eliminated variables

Variable

Estimated

coefficient P value Variable Partial R² P value

Intercept ‐0.18 <.0001 GLI 0.0001 0.84

MXAPJ 0.61 <.0001 CAI 0.0069 0.17

CPI 6.39 <.0001

FCI ‐2.74 <.0001

WTI 0.24 <.0001

High R² compared with other AU stocks

Low "beta" vs. MXAPJ; may reflect the omission

of FX beta

Higher inflation may lead to higher ASP and liquidity easing is positive

to the local economyAlthough the company is focusing on the domestic market, CAI is heavily influenced by commodity exports

cycles

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 12

Example 4: TATA Consultancy Services (TCS IN)

It has one of the highest R² (74%) among the Indian stocks in the MXAPJ universe

(average 46%).

The stock can be classified as a low-beta stock given its low return coefficient with

MXAPJ (c.0.67).

The stock has tended to move very closely with GLI momentum (1% of GLI

momentum change has historically led to 15% of share price movement),

consistent with TCS’s business concentration in global developed markets.

Exhibit 12: TATA consultancy’s share prices seem very sensitive to global growth given the company’s geographic

exposure

Stepwise regression results (TATA Consultancy Services)

Source: FactSet, CEIC, MSCI, Goldman Sachs Global ECS Research estimates.

# of obs. 86

R² 74%

Significant variables Eliminated variables

Variable

Estimated

coefficient P value Variable Partial R² P value

Intercept ‐0.09 0.00 WTI 0.0031 0.33

MXAPJ 0.67 <.0001 CAI 0.0076 0.12

CPI 1.48 0.0002

FCI ‐1.01 0.0017

GLI 15.68 <.0001

Reasonably high R²

Low "beta" vs. MXAPJ; statistically significant

Strong (weak) relationship with global growth momenutm (localgrowth), reflecting its business

concentration in DM

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 13

Part 2: Adding micro overlays—valuation, micro fundamentals and

technical indicators—to enhance returns

Part 1 aims to match individual equities’ returns to select macro factors. However, the

return attribution exercise is insufficient to build a sensible trading strategy on its own,

because:

a. No market or stock in our sample universe has close to a 100% fit (R²) in our

regression model, suggesting some unobserved or uncaptured variables, which

we believe are mostly micro-related, are also significant performance drivers;

b. Stock returns are essentially a joint function of earnings growth and valuation

changes. Our analysis helps partly explain returns variations using macro factors

but does not take into account the returns that macro drivers have on risk premia

and therefore the willingness of investors to pay for equities for a given level of

earnings.

c. In some cases, share prices may have already reflected stock-specific

themes/exposure; and pricing signals (especially shorter-term ones) are difficult to

capture in macro-factor regression models.

As such, we incorporate valuation parameters, micro fundamental variables, and

various technical indicators into our broader framework. We believe these additional

considerations could help us form an objective view on stocks’ micro profile and help

answer the questions of “how much is priced in” and “entry level”, which have shown

strong relationships with price returns (more on this later).

Valuation parameters

We focus on the stock’s current valuations to gauge how the stock’s fundamentals are

being priced by the market and to avoid buying/selling at full/depressed valuation levels.

Specifically, taking the conclusions from our recent work: Asia Pacific: Portfolio Strategy:

Global Strategy Paper: No. 3: AsiaPac Valuation: What works, and when, March 12, 2012,

we have chosen forward P/E, trailing D/Y, and trailing P/B, which are proven to be

significant returns indicators (higher significance to medium-term returns) according to our

analysis, as the key metrics.

While we have also proved that P/CF has strong predictive power on forward returns at a

market level, we deliberately exclude this in our analysis given its short and unstable time

series at an individual stock level.

Micro fundamentals

While we have established relationships between macro factors and stock returns in Part 1,

stocks react to macro forces because they tend to impact earnings or earnings expectations,

which can be quantified and captured by the changes of consensus EPS and expected

returns (target price). In this vein, we look at following indicators to assess stock’s micro

dynamics using consensus data:

Earnings revision (magnitude)—percentage of month-on-month forward 12-

month EPS changes;

Earnings sentiment (breadth)—percentage of net earnings

upgrades/downgrades versus the total number of consensus estimates (mom);

Consensus target price—percentage changes (mom).

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 14

Technical indicators

Broadly speaking, technical indicators can be grouped into four categories—momentum,

volatility, trend and volume. Given the numerous forms of technical indicators, we focus

on those that are most commonly used and are comparable from a time series standpoint.

The key objective here is to form a view on short-term entry levels.

1. RSI (momentum): We use 14-day RSI to gauge the near-term price momentum of

particular stocks. We prefer 14-day over longer-dated RSIs given its higher

volatility relative to longer-dated RSIs, which better fits our objective of evaluating

entry point for shorter-term investing.

2. Bollinger bands (volatility): For computational purpose, we look at %b, as

opposed to the actual moving averages and the two bands (upper and lower) to

quantify where the current price is relative to its recent range in standard deviation

terms. Low %b indicates current prices are closer to the lower Bollinger band and

vice versa.

3. Moving Average Convergence/Divergence (MACD) (trend): We take the

differentials between MACD line (12 day-26 day exponential moving average

(EMA)) and MACD signal line (9-day EMA), which is the histogram on a typical

MACD chart, to gauge the short-term trend and price momentum of the stock. High

positive values reflect strong price momentum in recent trading periods and vice

versa.

4. Volume: Most volume-based indicators require a time-series perspective to form

trading signals; hence, an absolute number often does not tell us much. Volume

signals can vary so decision-making is not stable. As such, we exclude volume-

related indicators in our micro score calculation.

Exhibit 13: We use these micro parameters to form a view on the stocks’ fundamentals, aiming to enhance the

risk/reward of our top-down stock recommendations A summary of micro parameters

Source: FactSet, I/B/E/S, Goldman Sachs Global ECS Research estimates.

Input specifications

Forward P/E P(t)/fEPS(t)

Trailing P/B P(t)/tBPS(t)

Trailing D/Y P(t)/tDPS(t)

EPS revisions fEPS(t)/fEPS(t‐1)‐1

EPS sentiment{#up rev(t)‐#down

rev(t)}/#estimate(t)

Consensus target price TP(t)/TP(t‐1)‐1

Momentum 14‐day RSI

Volatility Bollinger Bands (%b)

Trend MACD line ‐ MACD signal line

Composite micro score

Micro param

eters

Valuations

Micro

fundamentals

Technical

indicators

Valuation

MicroTechnical

Z‐score standardization

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 15

The effectiveness of micro overlays—an empirical study

While these micro parameters are commonly regarded as important elements to potential

returns, their actual implications and contribution to returns are unclear to us up to this

point.

As such, we test the conditions and formats under which these micro factors matter most

to potential returns, and design our trading strategies accordingly.

First, we aggregate and organize ex-ante, subsequent 3-month stock returns based on the

nominal values of these parameters. The sample size is statistically significant as there are

more than 50,000 datapoints for each parameter, given our study universe contains over

400 stocks with more than 12 years of monthly history (i.e. 400*144). The results support

the conventional wisdom of buying stocks at low valuations and technically sound

entry levels, and when consensus expectations rise, ensuing returns tend to be

strong and vice versa. Details are shown in Appendix 2.

We then standardize all the parameters based on their z-scores to ensure comparability and

compatibility of the dataset, and to allow us to form an objective view of the stock’s micro

attractiveness with existing (ex-ante) data-points. Key points to note:

Forms of standardization: Time series and cross-sectional analysis are commonly

used data standardization methods. While they have their own analytical

advantages and drawbacks, we choose the forms under which the parameters

have historically generated more differentiated (higher or lower) returns. In this

vein, we take time series z-scores for valuations and micro revision data, and

cross-sectional z-scores for technical indicators.

Valuations—Extreme valuations usually lead to significant subsequent

returns: In our recent research, Global Strategy Paper: No. 3 - AsiaPac Valuation:

What works, and when, we found that the levels of valuation, on a standalone

basis, have low correlation with ensuing returns over a relatively short time

horizon (3-6 months) at the regional/market level. However, the picture looks

slightly different at the stock level. We note that when prevailing stock valuations

are close to 1.5 to 2 standard deviations (s.d.) to the attractive side (3-year rolling z-

scores), subsequent 3-month performance tends to be strong (Exhibit 14). The

opposite is not very obvious, unless when valuations are extremely demanding (2

s.d. to the unattractive side).

Micro fundamentals—Consensus view changes are a reasonably good

indicator of short-term returns: Unsurprisingly, upgrades of consensus earnings

(both magnitude and breadth) and/or target prices usually lead to favorable price

returns. However, it is noteworthy that we are comparing ex-ante earnings and

target price changes with subsequent 3-month returns, meaning that: a)

observable consensus view changes do drive actual stock returns; and, b) it may

take some time for the market to discount the incremental new consensus

expectations (Exhibit 15).

Technical indicators—The trend is your friend: Exhibit 16 shows, fairly

consistently, stocks with high technical scores (low RSI, MACD, %b compared with

peers) tend to outperform those that embrace demanding technical entry levels.

However, the extent to which stocks have historically outperformed/

underperformed is lower on our technical scores (vs. valuation and micro scores),

reflecting that valuations and fundamentals have comparatively higher

contributions to return variations than technical indicators.

Composite micro score—an objective view on stock’s micro attractiveness:

While the each of the three categories of micro parameters appear to be significant

determinant of short-term returns on its own, we believe a combined

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 16

measurement (simple average of the three z-scores) could be even more helpful

for investors to gauge risk/reward because: a) it gives a comprehensive and

objective assessment of stocks’ micro profile using observable market data,

without involving stocks’ specific operating and industry-wide expectations; b) it

gives higher alpha (positive and negative) than the individual scores may reflect,

meaning that it is probably a better variable to consider in our stock-picking

framework (Exhibit 17).

Exhibit 14: Levels of valuations seem to have strong

impact on returns, especially when valuations are at

extremes 3-month price returns (loc) vs. valuation z-scores

Exhibit 15: Positive earnings revisions (in terms of both

magnitude and breadth) and target price upgrades do bode

well for performance 3-month price returns (loc) vs. micro fundamentals z-scores

Note: High z-scores mean lower fP/E, tP/B and high tD/Y. Note: High z-scores mean positive EPS revisions, EPS sentiment, and consensus target price upgrades.

Source: FactSet, Goldman Sachs Global ECS Research.

Source: FactSet, Goldman Sachs Global ECS Research.

Exhibit 16: Technical factors are helpful to explain returns

variations, although not as much as valuations and

fundamentals 3-month price returns (loc) vs. technical z-scores

Exhibit 17: Our composite z-scores provide an objective

assessment on stocks’ micro profile and reasonably

strong indications to forward returns 3-month price returns (loc) vs. composite micro z -cores

Note: High z -scores mean low RSI, MACD and %b.

Source: Bloomberg, Goldman Sachs Global ECS Research.

Source: FactSet, Bloomberg, Goldman Sachs Global ECS Research.

2.7%

6.6% 6.6%

4.8%4.6%4.2%

5.6%

8.1%

10.1%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-2 -1.5 -1 -0.5 0 0.5 1 1.5 2

Valuation score at different entry levels (z score)

Average returns in our study universe

Avg. subsequent 3m returns

2.7%

5.9%

3.2%3.7%

4.2%

6.7%7.1%

7.5%

9.9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-2 -1.5 -1 -0.5 0 0.5 1 1.5 2

Micro fundamentals score at different entry levels (z score)

Avg. subsequent 3m returns

Average returns in our study universe

1.6%

2.8%

3.6%4.2%

4.9%

6.4% 6.4%6.8% 7.1%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-2 -1.5 -1 -0.5 0 0.5 1 1.5 2

Technical score at different entry levels (z score)

Average returns in our study universe

Avg. subsequent 3m returns

2.0%

3.9% 2.9%

4.5% 4.8%5.7%

8.2%

9.5%

15.2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-2 -1.5 -1 -0.5 0 0.5 1 1.5 2

Composite micro score at different entry levels (z score)

Avg. subsequent 3m returns

Average returns in our study universe

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 17

Part 3: Back-testing our strategies—Cycle-based trading algorithms

may help performance

Building trading algorithms around the GLI

Parts 1 and 2 form the core analytical foundations for our stock selection process. The next

step revolves around designing a trading algorithm and testing (and refining) its

effectiveness.

Leveraging the work by our global team in its recent paper: Global Economics Paper No:

214, Acceleration Matters: Asset Returns and the Business Cycle, May 16, 2012, we define

the macro business cycle using our proprietary Global Leading Indicator (GLI), which

also serves as a signal for our trading strategies.

Simply put, our global team uses the interaction of GLI growth (mom) with GLI acceleration

(changes of mom growth) to define four phases of the business cycle (Exhibit 18):

1. Expansion: Positive growth and positive acceleration.

2. Slowdown: Positive growth and negative acceleration.

3. Contraction: Negative growth and negative acceleration.

4. Recovery: Negative growth and positive acceleration.

In each of the four phases, we examine past market returns (MXAPJ) and historical trends

of macro variables in our regression model to understand how investors should position in

the different periods of the economic cycle. Key insights (and our decision rules) are:

In an expansion phase, investors should turn aggressive by going long stock

beta and growth proxies (including oil-related exposure). Policy tends to stay

neutral during this phase given the lagged effect of growth on inflation.

During an economic slowdown, equity returns may stay positive although they are

less obvious than in the expansion phase. Investors should focus on late-cycle

plays including inflation beneficiaries and commodity stocks as

growth/inflation tradeoff deteriorates. Policy tends to become tighter, so stocks

that are sensitive (insensitive) to liquidity may underperform (outperform).

Defensive is the core theme during economic contraction periods as high beta

equities and growth proxies are likely to be under pressure. Policymakers tend to

loosen monetary policy as growth is challenged, and stocks with favorable

exposure to liquidity should trade well relative to the benchmark.

Easing starts to take effect and growth begins to accelerate into the recovery stage.

Equities returns are mixed as valuation compression tends to overpower the

impact of nascent growth and earnings upgrades. In other words, investors should

own growth proxies but not necessarily overweight beta. Financial conditions tend

to stay very easy and asset/rate-sensitive slices may outperform.

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 18

Exhibit 18: GLI mom growth and acceleration define the four phases of the business cycle

and our stock selection decision process GS GLI momentum and our trading algorithms

Note: “1” means owning the top-40 percentile (by factor sensitivity) of stocks under each market factor and owning the bottom-40 for “-1”. “0” means owning 30 to 70 percentile of the distribution.

Source: Goldman Sachs Global ECS Research estimates.

Back-testing our trading strategy

We test this strategy based on the following procedures:

a. Create a benchmark portfolio which includes top-80 percentile of stocks by their R²

ranking in each of the six macro factors in order to include stocks to which the top-

down approach may apply. We also believe this is a better performance proxy

than MXAPJ because of survivorship bias in our study universe.

b. Take the latest GLI reading as input and allocate macro exposure (1, 0 or -1) based

on the trading algorithm we defined in Exhibit 18. Specifically, “1” means owning

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 19

the top-40 percentile of stock (based on their factor loadings) under that particular

factor for each market, “-1” means buying the bottom-40 percentile, and “0”

refers to the 30th to 70th percentile of the distribution.

c. We then rank stocks by their macro attractiveness, as defined by the simple

average of their ranking in all 6 macro factors (depending on the business cycle),

to filter stocks with reasonably compelling macro exposure (i.e. these stocks may

not score well in all six macro filters but they have relatively high ranking in all

categories on average.) This forms our “macro-only” portfolio.

d. From (c), we select stocks in each market with the highest aggregate micro z-

scores (top-15 percentile) and form our “macro + micro” portfolio. The portfolio is

rebalanced on a quarterly basis and the price returns are measured in local

currency.

Exhibit 19: The logic flow/mechanism of our top-down selection framework

Source: Goldman Sachs Global ECS Research estimates.

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 20

Evaluating the back-test results: It is an alpha, not beta strategy

Performance: Over the past ten years, our “macro + micro” portfolio has gained

326%, versus benchmark of 165% on a market-cap-weighted basis, translating into

11.4pp average annualized outperformance according to our backtest (as of May

31). The portfolio has generated accumulated price return of 1914% since 2002 on

an equal-weighted basis, outperforming the benchmark (672%) by 1232pp. This

translates into 88pp average outperformance per annum versus the benchmark

(Exhibit 20). “Macro” and “macro + micro” portfolios outperformed the

benchmark 29 and 24 out of 42 quarters since 2002 respectively.

Representation: Our portfolio has consisted of at least 23 stocks across the full

study period, representing around 5% of the universe by number of stocks and 5%

by free-float market cap. Portfolio constituents are proportionately distributed

across markets according to their representation in the universe as designed by

our constraints. 295 stocks have been included in our portfolio at least once.

Volatility: Realized volatility (annualized) of our portfolio has been tracking in line

with the benchmark except during 1H09 and 1H12 when the overall market

volatility was high. Given the size (number of stocks in the portfolio) of the

portfolio, we consider its realized volatility as reasonable.

Alpha or beta?: As shown in Exhibit 23, both portfolios have outperformed the

benchmark (on average) in all the economic phases since 2002 on an equal-

weighted basis, suggesting that: a) our strategies are not entirely driven by beta

exposure; b) Some elements of alpha are embedded in our portfolios as they have

outperformed in both expansion and contraction phases2.

Macro vs. micro: Interestingly, the returns differentials between our “macro only”

and “macro + micro” portfolios reflect that one strategy might outperform the

other under different market conditions. For example, “macro” fared better than

“macro + micro” during the bull market from 2005 to 2007 but underperformed in

2009, and we believe this can be explained by the micro filters that we have put in

place to screen out high-valuation and momentum stocks during that period3. In

the case of 2009, given many stocks were trading at undemanding valuations and

technical levels post the Global Financial Crisis, our micro filters were generally

not binding constraints (Exhibit 24). This shows that investors may be better off if

they can relax their valuation/micro standards at the onset of a market

uptrend; however, micro disciplines still add alpha over time.

Caveats: Risks and limitations

1. Our backtest is conducted on an in-sample basis (i.e. regression for factor loading

and backtest start at the same time), a less preferred approach to out-of-sample

test from a statistical standpoint. However, we are constrained by data availability

which is prevalent for Asian stocks where listing history is generally short.

2. Historical GLI readings are subject to revision risk. As such, the indication of

economic turning points by the GLI is more accurate on an ex-post basis.

3. We have not assumed any trading and transaction costs in our backtest returns

calculations. Realized returns could be meaningfully different from the results.

4. Our trading algorithms could be subject to data-mining risk (e.g. we favor certain

macro exposures in different business-cycle phases based on historical pattern).

2 We use monthly rebalancing returns to calculate our portfolios’ performance in different business-cycle phases to

better capture the changes in GLI-derived trading signals.

3 We take the simple average of the valuation, micro fundamentals, and technical scores. Investors may adjust the

weighting of each category depending on market conditions.

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 21

Exhibit 20: Our two-tier strategy has outperformed the benchmark in both equal-weighted and market-cap-weighted

terms Indexed price performance (loc for equal weighted and USD for market-cap weighted), as of May 31

Source: Bloomberg, MSCI, FactSet, Goldman Sachs Global ECS Research.

Exhibit 21: Our portfolio accounts for around 5% of the

benchmark by number of stocks and 5.3% (avg.) by cap Percentage of stock and market cap

Exhibit 22: Our strategy has higher realized volatility than

the benchmark in 1H09 and 1H12 Annualized monthly return volatility

Source: Bloomberg, MSCI, FactSet, Goldman Sachs Global ECS Research.

Source: FactSet, MSCI, Goldman Sachs Global ECS Research.

Exhibit 23: Our strategy has outperformed benchmark in

different phases in the business cycle Average monthly price returns in different business-cycle

phases since 2002 (Equal weighted)

Exhibit 24: Micro considerations appeared less effective

during 2005 to 2007 when the markets were on a strong

run Annual price returns (Equal weighted)

Source: Bloomberg, MSCI, Goldman Sachs Global ECS Research.

Source: FactSet, MSCI, Goldman Sachs Global ECS Research.

0

400

800

1200

1600

2000

2400

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

EW benchmark

EW macro only

EW macro and micro

Macro and Micro: 2014

Macro: 1667

Benchmark: 783

0

100

200

300

400

500

600

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

CW benchmark

CW macro only

CW macro and micro

Macro and Micro: 426

Macro: 417

Benchmark: 265

0%

2%

4%

6%

8%

10%

12%

0

5

10

15

20

25

30

35

Ja

n/0

2

Ma

y/0

2

Se

p/0

2

Ja

n/0

3

Ma

y/0

3

Se

p/0

3

Ja

n/0

4

Ma

y/0

4

Se

p/0

4

Ja

n/0

5

Ma

y/0

5

Se

p/0

5

Ja

n/0

6

Ma

y/0

6

Se

p/0

6

Ja

n/0

7

Ma

y/0

7

Se

p/0

7

Ja

n/0

8

Ma

y/0

8

Se

p/0

8

Ja

n/0

9

Ma

y/0

9

Se

p/0

9

Ja

n/1

0

Ma

y/1

0

Se

p/1

0

Ja

n/1

1

Ma

y/1

1

Se

p/1

1

Ja

n/1

2

% of market cap (RHS)

Number of stocks

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

EW benchmark

EW macro only

EW macro and micro

4.7%

1.2%

-5.7%

1.1%

5.8%

1.3%

-4.1%

1.3%

5.9%

1.2%

-3.6%

3.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Expansion Slowdown Contraction Recovery

benchmark

macro only

macro and micro

-100%

-50%

0%

50%

100%

150%

200%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

benchmark

macro only

macro and micro

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 22

Part 4: Stock ideas- Investing in a contraction phase; reduce market

beta and go long easing beneficiaries

The latest GLI reading (final) for May 2012, which was released on June 1, suggests that

the global economy has ventured into a contraction phase starting from April (Exhibit

25). See Global Leading Indicator (GLI): May Final GLI - Momentum In Negative Territory,

June 1, 2012.

Exhibit 25: GS GLI suggests the global economy has entered the contraction phase GLI momentum and momentum changes

Source: Goldman Sachs Global ECS Research estimates.

Adhering to our stock selection process, we would focus on the following macro

characteristics when investing in a contraction phase:

Low “beta”;

Low sensitivity to local growth;

Favorable exposure to policy easing;

Disinflationary outperformers;

Stocks that may benefit from lower oil prices;

Low sensitivity to global growth momentum.

Stocks which have these macro characteristics and rank well with respect to their

composite micro scores include (organized by macro factors) are shown in Exhibit 26.

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 23

Exhibit 26: We like these stocks because of their favorable macro exposure and compelling micro profile relative to their

regional peers Stock recommendations for June 2012 (Priced as of June 5)

Note (1): These stocks are rated Buy or Neutral by Goldman Sachs Research except SM Investments which is NC. We use consensus estimates for SM Investments. Note (2): * denotes the stock is on our regional Conviction List. “Tick” indicates stock that ranks top-30 percentile within each factor relative to its market peers and they perform well in our specified macro environment. Revisions and sentiment are based on forward 12-month consensus EPS.

Source: FactSet, I/B/E/S, Goldman Sachs Global ECS Research estimates.

Ticker Name MarketMkt. cap

(US$mn)

6m

ADVT

GS

Rating

Global

growth

13E

P/E

13E

P/B

13E

D/Y

13E

EPSg

EPS

rev.

EPS

sent.

14d

RSI%b

NAB AT National Australia Bank Australia 49,179 156.9 B √ √ √ 8.4 1.2 8.6% 5% -1% 17% 35 14%

ORI AT Orica Australia 8,473 34.8 B* √ √ 10.8 2.1 4.7% 16% 3% 13% 28 9%

1044 HK Hengan Int'L Group Co China 6,748 20.1 N √ √ √ 19.9 5.7 3.2% 21% 4% 43% 32 -4%

857 HK Petrochina Co H China 26,240 89.1 N √ √ √ 8.6 1.2 5.2% 8% 3% 0% 28 5%

700 HK Tencent Holdings Lim(Cn) China 27,186 98.2 B √ 19.2 5.5 0.6% 27% 4% 22% 37 13%

1 HK Cheung Kong Holdings Hong Kong 15,492 51.2 B √ √ √ 7.7 0.6 3.9% 16% 2% 6% 28 8%

11 HK Hang Seng Bank Hong Kong 9,866 19.6 N √ √ √ 10.6 2.1 5.2% 9% 2% 15% 38 26%

HDFC IS Housing Dev Finance Corp India 12,601 57.4 N √ √ √ 14.8 3.2 2.2% 15% 15% -15% 44 44%

ITC IS ITC India 8,867 33.4 B √ √ √ 21.5 8.0 2.8% 17% 4% 23% 41 0%

BBRI IJ Bank Rakyat Indonesia Indonesia 6,253 24.4 N √ √ √ 7.2 1.7 2.8% 13% 3% -5% 23 8%

006260 KP LS Corp Korea 1,162 9.2 B √ √ 6.4 0.9 1.6% 23% 5% 50% 47 23%

055550 KP Shinhan Financial Group Korea 13,742 40.0 N √ √ √ 6.3 0.7 2.9% 4% 1% 19% 39 31%

CIMB MK CIMB Group Holdings Bhd Malaysia 11,204 23.8 N √ √ 11.6 1.8 4.1% 12% 2% -8% 52 60%

SM PM SM Investments Philippines 3,334 9.2 NC √ √ √ 15.5 2.1 1.7% 12% 2% 0% 48 36%

JCNC SP Jardine Cycle & Carriage Singapore 3,467 7.8 N √ 8.3 - 5.1% 24% 9% 0% 33 17%

2308 TT Delta Electronics Taiwan 4,749 21.5 B √ √ 12.7 2.0 5.8% 10% 8% 67% 36 11%

2330 TT Taiwan Semiconductor Mfg Taiwan 64,204 101.0 N √ √ √ 11.5 2.5 3.8% 10% 10% 56% 41 11%

BBL/F TB Bangkok Bank Fgn Thailand 4,617 7.7 B* √ √ √ 8.6 1.1 4.4% 17% 4% 38% 31 -13%

Median 9,366 28.9 10.7 2.0 3.9% 14% 3% 16% 37 12%

MXAPJ 9.3 1.3 4.0% 11% 0% -6% 30 16%

Factor loading Valuations Fundamentals Technical

Market

risks

Local

growth

Policy/

liquidityInflation Oil

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 24

Part 5: Potential usage—Broad-based

We recognize that many investors use some form of macro input to their stock selection

process, ranging from general awareness of the macro environment to pure model-driven

strategies. While our approach may not suit everyone, we do think it is a useful

complement to different types of investors, notably:

Macro investors: This framework can help pick stocks, implement themes, and devise

various forms of strategies based on their macro expectations expressed in observable and

quantifiable variables.

Relative-return-focused fund managers: Fund managers running regional or country

funds can use this tool to attribute returns to macro factors and better understand what

their portfolio’s effective exposure is relative to the benchmark, thereby helping tactical

allocation and portfolio risk management.

Bottom-up stock pickers: This group of investors may not pay much attention to macro

trends but our analysis can help them identify stocks where top-down (or bottom-up)

approaches may (or may not) work, and therefore improve their internal resource

allocation.

Hedgers: Investors may be assisted in formulating targeted, factor-hedging strategies

based on our outlined risk parameters at the regional, market or stock level.

General market participants: As stated earlier, our model by no means has captured all

significant return drivers, especially at the sector and stock levels where specific micro

factors play a more important role in driving returns. Nevertheless, investors can add

and/or substitute independent variables to/from our default regression setup to explore

investment implications according to their mandate and interest areas.

For example, an ASEAN-focused fund manager can replace MXAPJ by MSCI ASEAN index

and add local factors such as palm oil prices to the model, and a tech specialist can put

Taiwan exports order and monthly revenue growth as independent variables. In a nutshell,

the framework is flexible and expandable.

Exhibit 27: Our framework may be helpful to a diverse group of investors Potential users and usage of our stock picking framework

Source: Goldman Sachs Global ECS Research.

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 25

Market summary: Australia

Exhibit 28: Factor loadings for MXAU constituents which pass our liquidity and market filters

Note (1): We show stepwise regression coefficient and p-value for each macro variable at the market index level but we show simple linear regression coefficient at the stock level given the multicollinearity issue we discussed earlier in this report. Note (2): Dark-blue (light-blue) shading means top-15 (bottom-15) percentile of stocks that have historically performed well when macro indicators move positively (including our FCI which means tightening of financial conditions),

Note (3): (1) and (2) apply to all market summary pages from page 25 to 32.

Source: FactSet, I/B/E/S, Goldman Sachs Global ECS Research estimates.

Market risks Local growth Policy/liquidity Inflation Oil Global growthMXAU Multiple regression R²= 0 7396 0 53 (<0 01) 1 94 (<0 01) -0 03 (0 93) 1 6 (<0 01) 0 02 (0 55) 1 11 (0 4)BHP AU BHP Billiton Ltd. 0.8 6.6 -1.5 -3.2 0.3 9.4CBA AU Commonwealth Bank of Australia 0.6 5.6 -2.9 -2.8 0.2 10.3WBC AT Westpac Banking Corp. 0.5 4.5 -1.9 -2.2 0.1 7.7ANZ AU Australia & New Zealand Banking Group Ltd. 0.4 4.9 -2.9 -2.3 0.1 8.2NAB AT National Australia Bank Ltd. 0.5 4.3 -2.1 -1.0 0.1 7.8WOW AT Woolworths Ltd. 0.1 1.8 -0.1 1.5 0.0 0.1WES AT Wesfarmers Ltd. 0.6 5.8 -2.6 -0.3 0.3 10.8RIO AT Rio Tinto Ltd. 1.1 10.6 -3.1 -3.9 0.6 20.2WPL AT Woodside Petroleum Ltd. 0.7 6.7 -0.8 -3.0 0.5 11.4WDC AT Westfield Group Australia 0.5 7.1 -1.7 -4.1 0.1 7.4NCM AT Newcrest Mining Ltd. 0.6 6.1 -1.8 -2.5 0.1 5.8CSL AU CSL Ltd. 0.4 2.4 1.1 -0.4 0.1 2.4TLS AT Telstra Corp. Ltd. 0.2 3.0 0.3 -1.0 0.0 2.6QBE AT QBE Insurance Group Ltd. 0.5 5.0 0.8 0.9 0.1 4.2ORG AT Origin Energy Ltd. 0.0 -0.3 1.7 4.1 0.1 -0.6STO AT Santos Ltd. 0.3 1.6 1.6 -0.2 0.3 3.7AMP AU AMP Ltd. 0.5 3.8 -2.1 -1.0 0.1 7.4BXB AU Brambles Ltd. 0.5 5.8 -1.3 -2.6 0.1 8.8SUN AT Suncorp Group Ltd. 0.6 7.6 -2.2 -0.8 0.2 10.7MQG AT Macquarie Group Ltd. 1.1 9.6 -3.8 -4.1 0.4 16.2ORI AT Orica Ltd. 1.0 10.9 -4.6 -7.0 0.3 16.9AMC AU Amcor Ltd. 0.2 2.7 -1.6 0.0 -0.1 3.5TCL AT Transurban Group 0.0 1.9 0.1 -0.2 -0.1 0.9SGP AT Stockland Australia 0.4 7.3 -2.1 -1.9 0.2 9.8IAG AT Insurance Australia Group Ltd. 0.3 3.1 -0.5 -0.2 0.0 2.9CCL AU Coca‐Cola Amatil Ltd. 0.0 0.7 -1.0 0.2 -0.1 -0.5FMG AU Fortescue Metals Group Ltd. 2.4 25.9 -2.0 -9.6 0.9 37.0AGK AU AGL Energy Ltd. 0.0 -0.2 0.7 -0.2 0.0 -0.4ILU AT Iluka Resources Ltd. 0.2 -1.1 1.4 0.5 0.0 0.8GPT AT GPT Group 0.6 11.5 -2.9 -3.3 0.2 15.7ASX AU ASX Ltd. 0.7 6.0 -1.4 -3.0 0.2 7.9IPL AT Incitec Pivot Ltd. 1.2 15.9 -1.0 -6.8 0.7 23.4WOR AT WorleyParsons Ltd. 1.7 15.7 -3.8 -16.2 0.8 23.0GMG AT Goodman Group 1.8 27.1 -6.2 -15.5 0.8 37.8SHL AT Sonic Healthcare Ltd. 0.2 2.4 0.9 -1.4 0.1 2.0CPB AU Campbell Brothers Ltd. 1.0 9.7 -2.7 -4.2 0.4 18.5MGR AT Mirvac Group 1.0 12.1 -4.6 -4.3 0.4 20.1DXS AT Dexus Property Group 0.9 9.7 -2.1 -6.5 0.4 13.5LLC AT Lend Lease Group 0.8 8.8 -3.5 -6.3 0.2 13.9TOL AT Toll Holdings Ltd. 0.3 5.1 -3.0 0.2 0.0 5.7CPU AU Computershare Ltd. 0.6 5.3 -0.2 -4.2 0.2 8.6COH AU Cochlear Ltd. 0.2 0.4 -0.3 -0.4 0.0 -1.3CFX AT CFS Retail Property Trust 0.1 3.1 -0.5 -0.9 0.0 3.1TTS AT Tatts Group Ltd. 0.0 2.1 -0.6 -1.7 -0.2 -1.4JHX AU James Hardie Industries SE 0.5 4.5 -3.7 -1.9 0.1 7.8MTS AT Metcash Ltd. 0.1 2.0 -1.4 4.7 -0.1 -2.8LEI AT Leighton Holdings Ltd. 1.0 11.7 -3.0 -3.5 0.4 18.2BLD AU Boral Ltd. 0.6 7.0 -2.5 -1.6 0.3 11.6OZL AT OZ Minerals Ltd. 1.9 21.4 -7.4 -7.5 0.8 32.8BEN AU Bendigo & Adelaide Bank Ltd. 0.3 5.3 -0.5 0.3 0.0 6.1AWC AU Alumina Ltd. 1.3 13.6 -3.9 -4.2 0.5 25.1RHC AT Ramsay Health Care Ltd. 0.1 -0.5 0.1 3.9 -0.1 -1.0APA AT APA Group 0.2 1.3 -0.6 -0.4 0.0 1.3SGM AT Sims Metal Management Ltd. 1.0 9.0 -1.9 -3.3 0.6 15.5TAH AT TABCorp Holdings Ltd. 0.5 8.9 -2.9 -3.5 0.2 10.2CTX AU Caltex Australia Ltd. 1.0 10.5 -2.2 -7.3 0.4 14.9LYC AT Lynas Corp. Ltd. 2.5 23.7 -6.5 -10.3 0.7 44.5QAN AT Qantas Airways Ltd. 0.8 9.8 -3.9 -3.9 0.1 12.6FXJ AU Fairfax Media Ltd. 1.0 12.3 -4.1 -4.7 0.4 18.4SYD AT Sydney Airport 0.7 9.8 -3.1 -8.9 0.2 10.9HVN AT Harvey Norman Holdings Ltd. 0.9 9.1 -3.3 -4.1 0.2 12.9

June 11, 2012 Asia Pacific

Goldman Sachs Global Economics, Commodities and Strategy Research 26

Market summary: China

Exhibit 29: Factor loadings for MXCN constituents which pass our liquidity and market filters

Source: FactSet, I/B/E/S, Goldman Sachs Global ECS Research estimates.

Market risks Local growth Policy/liquidity Inflation Oil Global growth