bridge to india - global solar demand conference - 2013 - tobias engelmeier

TRANSCRIPT

www.bridgetoindia.com

Global Demand Conference VII, Munich

Where is the Indian solar market headed?

Tobias Engelmeier New Delhi,June 18th 2013 [email protected]

© BRIDGE TO INDIA, 2011 2

About us

Our business BRIDGE TO INDIA specializes in supporting international solar companies and investors in India

• Founded in 2008 • Based in New Delhi,

Hamburg and Munich • German competency

and local expertise • Entrepreneurial

approach • Solar PV as a core

knowledge area • Three mutually

supportive business segments

BRIDGE TO INDIA’s key fields of expertise are:

Policy

Projects Financing Industry

Market Entry

Market Potential Competitor Landscape

Market Strategy

Capital Investments

Remittance PD Due Diligence

© BRIDGE TO INDIA, 2011 3

Overall context India is rich, poor, democratic, chaotic – 1/6thof the global population – in a league of its own…

© BRIDGE TO INDIA, 2011 4

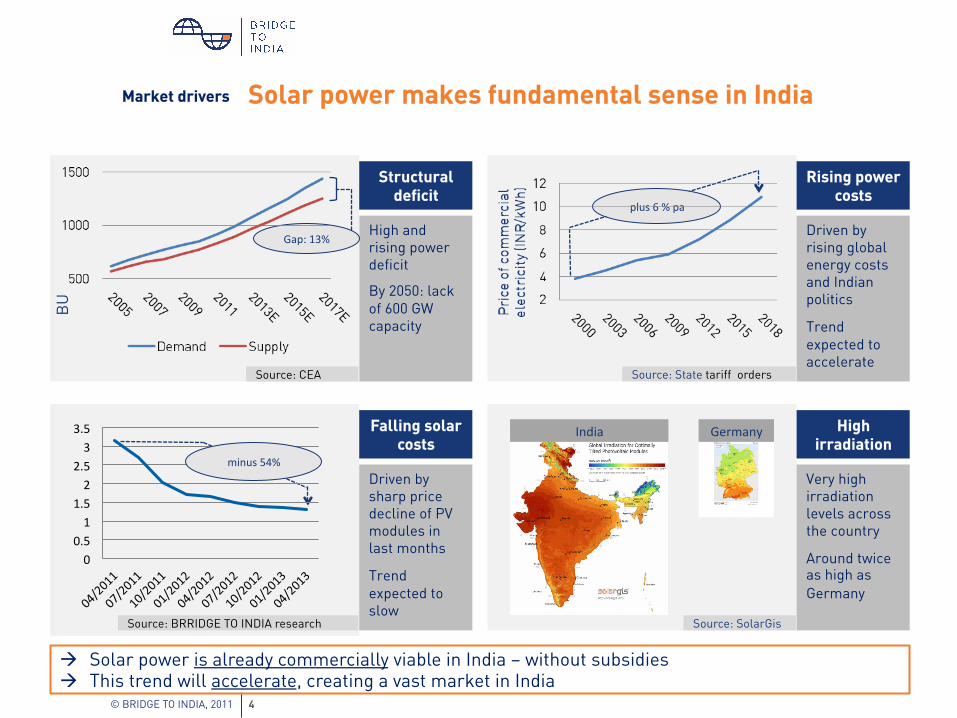

Solar power makes fundamental sense in India

High and rising power deficit

By 2050: lack of 600 GW capacity

Driven by sharp price decline of PV modules in last months

Trend expected to slow

Market drivers

à Solar power is already commercially viable in India – without subsidies à This trend will accelerate, creating a vast market in India

Driven by rising global energy costs and Indian politics

Trend expected to accelerate

Very high irradiation levels across the country

Around twice as high as Germany

Structural deficit

Rising power costs

Falling solar costs

High irradiation

Source: State tariff orders Source: CEA

Source: BRRIDGE TO INDIA research Source: SolarGis

plus 6 % pa

India Germany

Gap: 13%

BU

0 0.5 1

1.5 2

2.5 3

3.5

minus 54%

© BRIDGE TO INDIA, 2011 5

Installed PV capacity India has more than 1.7 GW of installed capacity already

Key Facts

• Currently market growth centres on grid-connected plants (FiT)

• The average project size in India is 6.8 MW

• Around 50% of installations are in the Indian state of Gujarat, another 30% in Rajasthan – both in the West

Total installed capacity: 1.7 GW Average size of project: 6.8 MW

© BRIDGE TO INDIA, 2011 6

Installed PV capacity New agreements for 2.5 GW to be signed in India in 2013. Of this, allocation process for 1.7 GW is under way

Key Facts • A capacity of 1,745

MW is being allocated or has been recently allocated in Tamil Nadu, Andhra Pradesh, Uttar Pradesh, Karnataka, Punjab and Rajasthan

• More than 1,100 MW of this 1,700 MW is in the southern states of Tamil Nadu, Andhra Pradesh and Karnataka

• A capacity allocation of 750 MW under the NSM will begin in July 2013

Note: some agreements are only Memorandums of Understanding (MoUs) and the indicated capacity is not expected to be completely installed. Some policy based projects also get delayed or cancelled.

1,718 MW

315 MW

1,745 MW

750 MW

654 MW

Installed capacity

Projects under development

Recently allocated projects (under allocation process)

New allocations expected in 2013

Existing agreements that have not been formalized or are likely to be cancelled

Snapshot of policy based projects in India (2013)

© BRIDGE TO INDIA, 2011 7

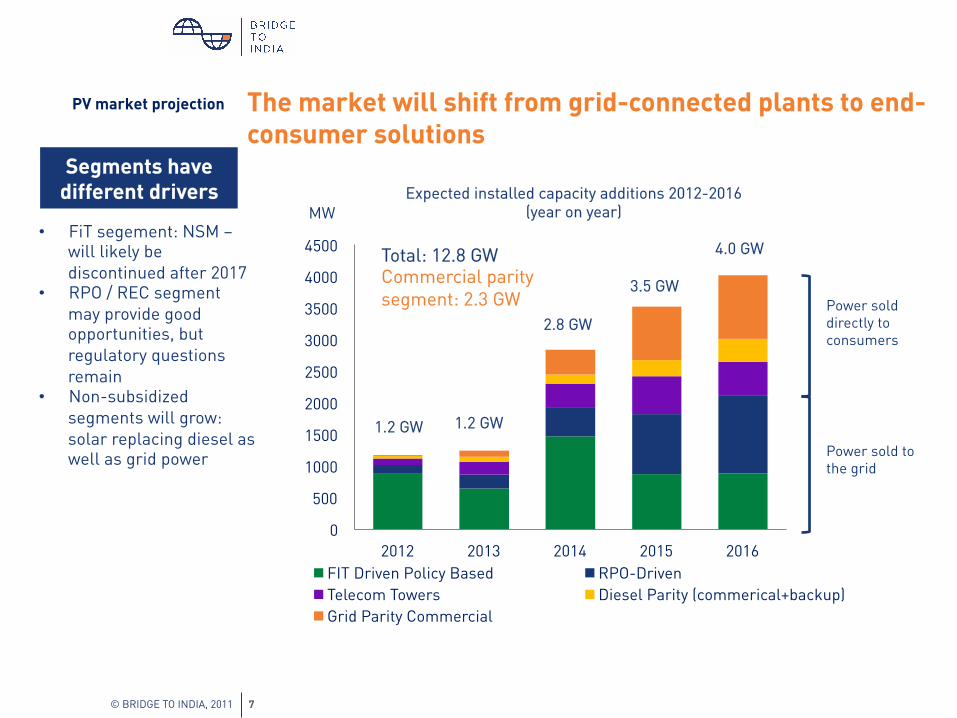

PV market projection The market will shift from grid-connected plants to end-consumer solutions

• FiT segement: NSM – will likely be discontinued after 2017

• RPO / REC segment may provide good opportunities, but regulatory questions remain

• Non-subsidized segments will grow: solar replacing diesel as well as grid power

Segments have different drivers

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2012 2013 2014 2015 2016 FIT Driven Policy Based RPO-Driven Telecom Towers Diesel Parity (commerical+backup) Grid Parity Commercial

Expected installed capacity additions 2012-2016 (year on year)

1.2 GW

4.0 GW

3.5 GW

2.8 GW

1.2 GW

Total: 12.8 GW Commercial parity segment: 2.3 GW

MW

Power sold to the grid

Power sold directly to consumers

© BRIDGE TO INDIA, 2011 8

Parity in 2013

Source: BTI market analysis, based on data from various state tariff orders

Key assumptions

Three states have already reached commercial parity , 40% of the states have reached parity with MNRE subsidy

2013 scenario

Key assumptions: • System size 100 kWp • Interest rate: 13% • Debt-equity ratio:

70:30 • System cost: INR 82/

Wp (EUR 1.2/Wp) • MNRE capital

subsidy at 30% • Solar LCOE varies by

irradiation across states

• Diesel LCOE varies by diesel prices at state level, taken in May 2013

• Commercial grid tariffs for states taken from various state tariff orders as of May 2013

Three Indian states with a poten?al of 728 MW of solar installa?ons ?ll 2016 have already reached parity.

© BRIDGE TO INDIA, 2011 9

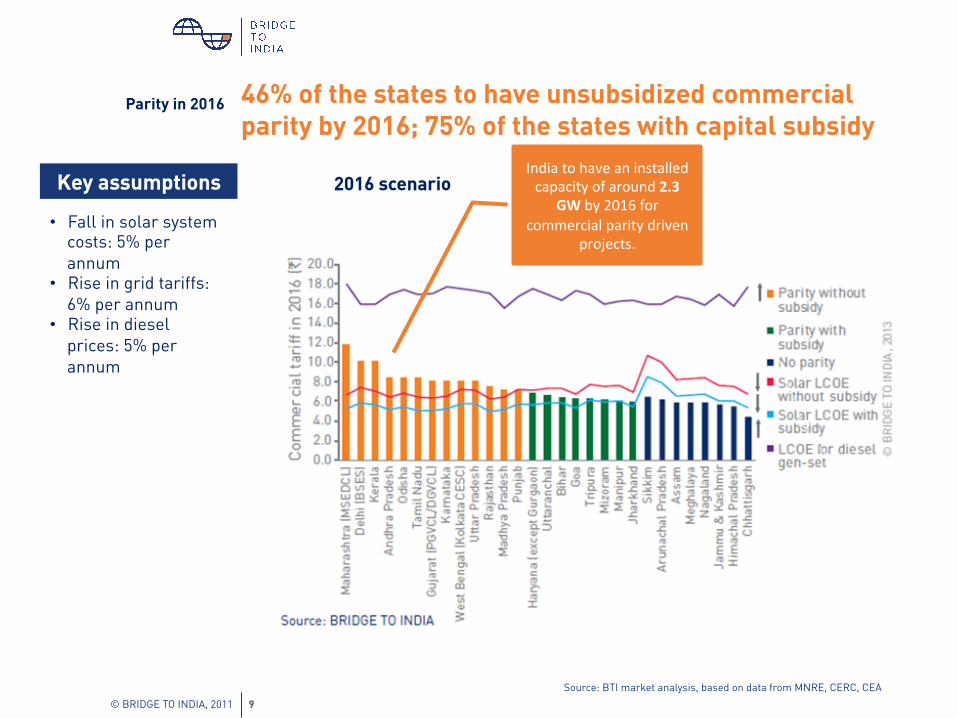

Parity in 2016

Source: BTI market analysis, based on data from MNRE, CERC, CEA

Key assumptions

46% of the states to have unsubsidized commercial parity by 2016; 75% of the states with capital subsidy

• Fall in solar system costs: 5% per annum

• Rise in grid tariffs: 6% per annum

• Rise in diesel prices: 5% per annum

2016 scenario India to have an installed capacity of around 2.3

GW by 2016 for commercial parity driven

projects.

© BRIDGE TO INDIA, 2011 10

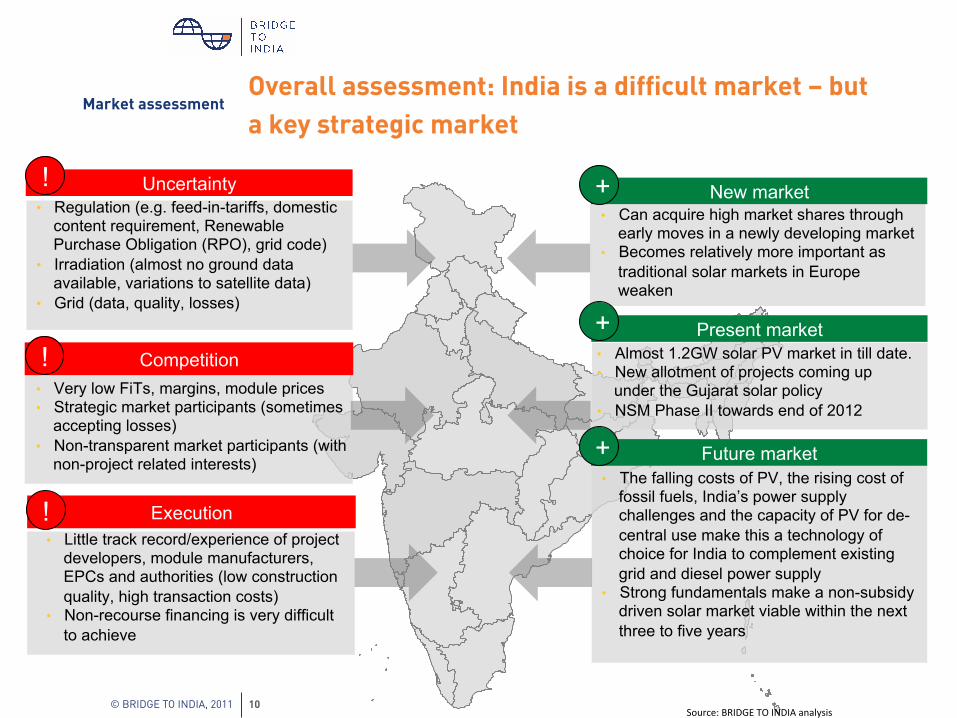

Market assessment Overall assessment: India is a difficult market – but a key strategic market

• Regulation (e.g. feed-in-tariffs, domestic content requirement, Renewable Purchase Obligation (RPO), grid code)

• Irradiation (almost no ground data available, variations to satellite data)

• Grid (data, quality, losses)

Uncertainty

• Very low FiTs, margins, module prices • Strategic market participants (sometimes

accepting losses) • Non-transparent market participants (with

non-project related interests)

Competition

• Little track record/experience of project developers, module manufacturers, EPCs and authorities (low construction quality, high transaction costs)

• Non-recourse financing is very difficult to achieve

Execution

• Can acquire high market shares through early moves in a newly developing market

• Becomes relatively more important as traditional solar markets in Europe weaken

New market

• The falling costs of PV, the rising cost of fossil fuels, India’s power supply challenges and the capacity of PV for de-central use make this a technology of choice for India to complement existing grid and diesel power supply

• Strong fundamentals make a non-subsidy driven solar market viable within the next three to five years

Future market

!

!

!

+

• Almost 1.2GW solar PV market in till date. • New allotment of projects coming up

under the Gujarat solar policy • NSM Phase II towards end of 2012

Present market +

+

Source: BRIDGE TO INDIA analysis

© BRIDGE TO INDIA, 2011 11

Our publications We help you understand and track the Indian solar market

Reports

INDIA SOLAR HANDBOOK

INDIA SOLAR COMPASS

INDIA SOLAR DECISION BRIEF

INDIA SOLAR POLICY BRIEF

IndiaSolarMarket.com IndiaSolarHomes.com

Social Media

www. facebook.com/ bridgetoindia

Write to us at [email protected] for any further information.

Our LinkedIn group,

‘India Solar Future’

www. twitter.com/

bridgetoindia

The BRIDGE TO INDIA Blog

Weekly market update (newsletter)

© BRIDGE TO INDIA, 2011 12

Our customers We have serviced many international solar players with our Indian market knowledge

Conglomerates

Solar Companies

Institutions

Government of Madhyapradesh

© BRIDGE TO INDIA, 2011

Contact www.bridgetoindia.com Follow us on facebook.com/bridgetoindia

We are happy to support you in any further queries