brics outlook - degroof petercam · pdf fileimportant political events ahead in brics and...

TRANSCRIPT

BRICS outlook December 2017

BRICS outlook - overview

• Brazil • Russia • India • China (see here for recent update) • South-Africa

2

BRICS continue to be the biggest contributors to world GDP growth

3

July ‘18

•General election (Mexico)

Aug ‘18

•Official start election (Brazil)

Oct ‘18

•1st & 2th round (Brazil)

Nov ‘18

•ASEAN summit

Nov ‘18

•New CB governor (Mexico)

Nov ‘18

•General election (Thailand)

Nov ‘18

•General election (Chile)

H1 ‘19

•General election (S.Africa)

Nov ‘19

•Legislative election (Poland)

Nov ‘19

•General elections (Turkey)

Jan ‘18

•Presidential election (Czech R.)

March ‘18

•Presidential election (Russia)

March ‘18

•Leadership transition incl. PBOC (China)

March ‘18

•Legislative election (Colombia)

March ‘18

•General election (Malaysia)

April ‘18

•ASEAN summit

April ‘18

•General election (Hungary)

H1 ‘18

•Legislative elections (India)

May ‘18

•Presidential election (Colombia)

June ‘18

•Regional elections (Indonesia)

Important political events ahead in BRICS and other EM

4

Brazil

Economic recovery set to strengthen next year…

6

… driven by a more optimistic consumer.

7

Retail sales picking up strongly…

8

… while consumer surveys still pointing to much room for improvement.

9

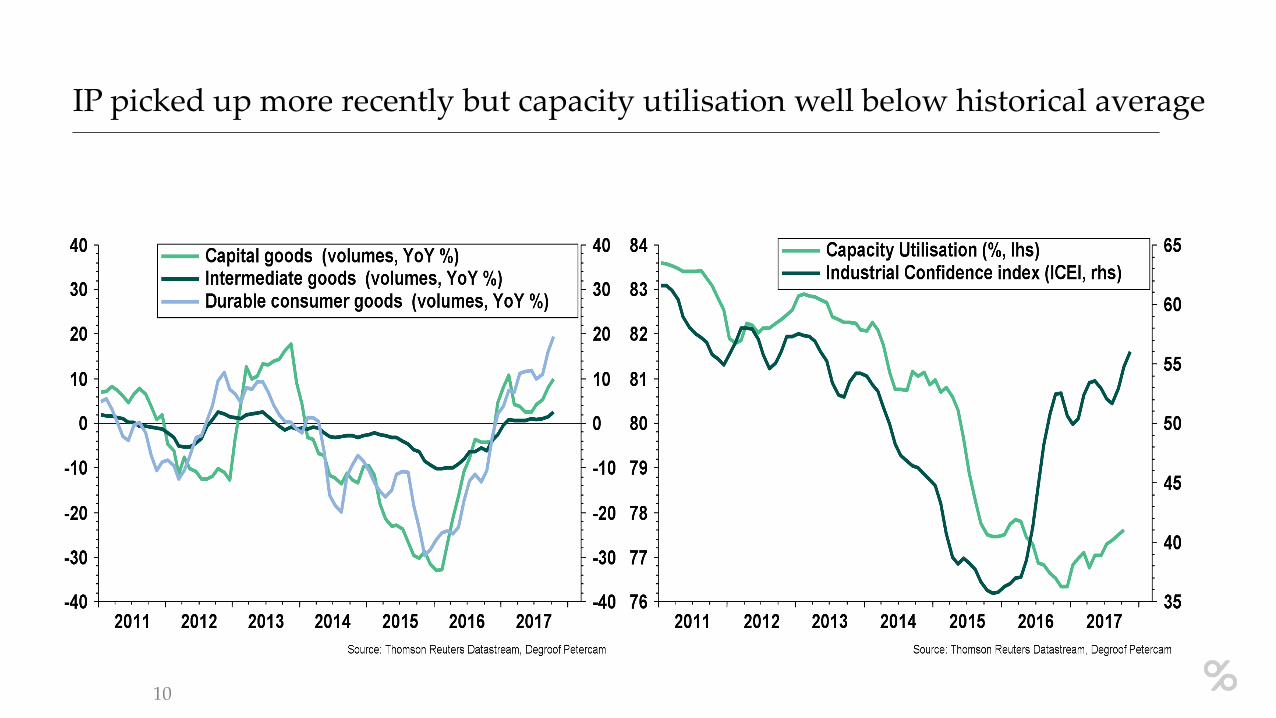

IP picked up more recently but capacity utilisation well below historical average

10

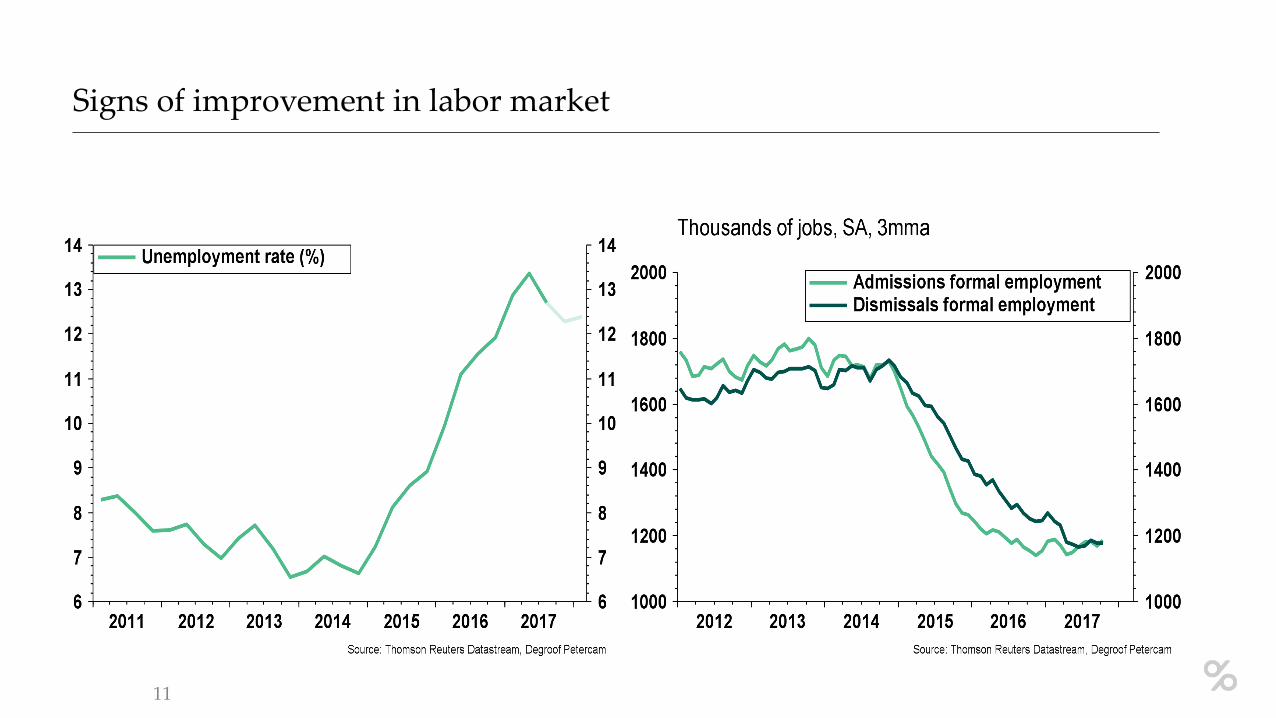

Signs of improvement in labor market

11

Wage growth remains modest but inflation drag has faded.

12

The end of a disinflationary period

13

Historical low selic rate supports activity going into 2018

14

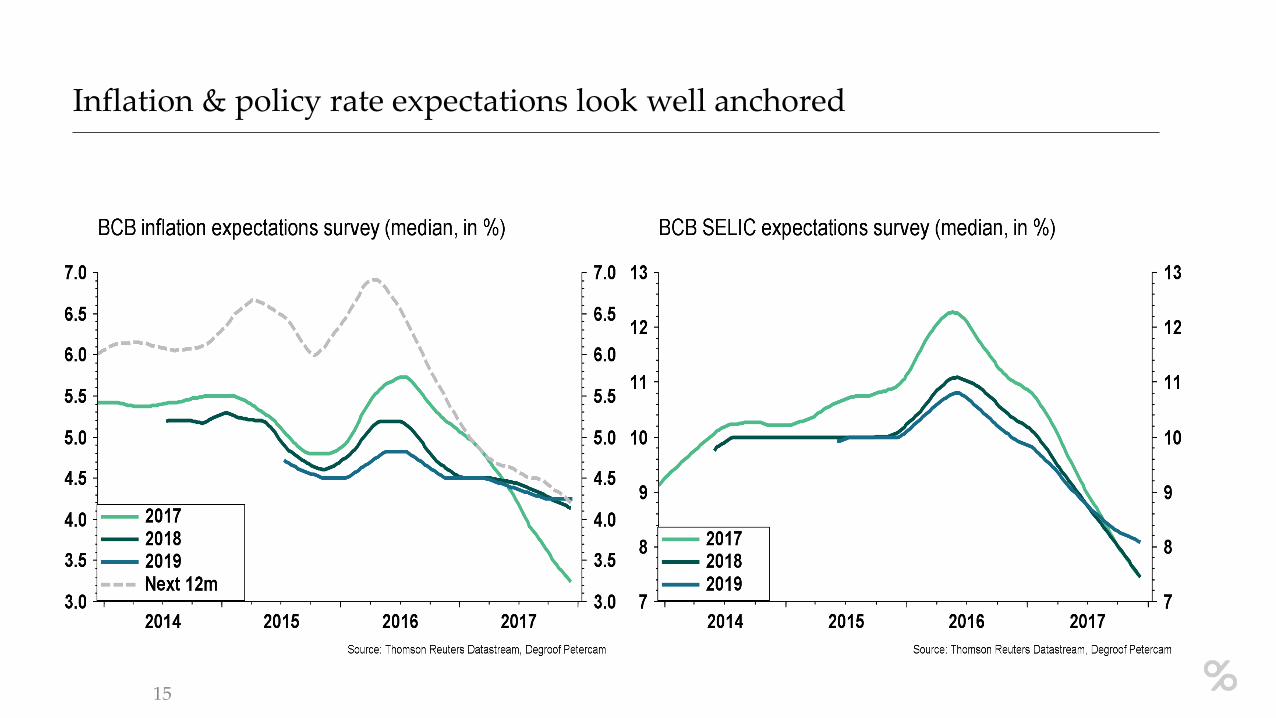

Inflation & policy rate expectations look well anchored

15

Current account deficit likely to persist

16

Continuation of fiscal reforms required after important election (October 7)

17

Brazil - Conclusion

• The Brazilian economy is leaving recession driven by a more optimistic consumer, with confidence indicators pointing to more good news ahead.

• Despite the recent improvements, there is much slack left in the economy and wage growth

remains modest. • The disinflationary period is over, with inflation moving towards target and inflation

expectations well anchored. • The current monetary policy stance is very accommodative with SELIC at historical low. • On the contrary, fiscal policy needs to be tightened to avoid an unsustainable path, which

will be challenging considering the upcoming elections.

18

Russia

Economic activity moving in the right direction…

20

… supported by more than just the energy sector.

21

The recession was long and shallow in historical perspective

22

Consumption growth gradually recovering

23

Retail trade activity moving up

24

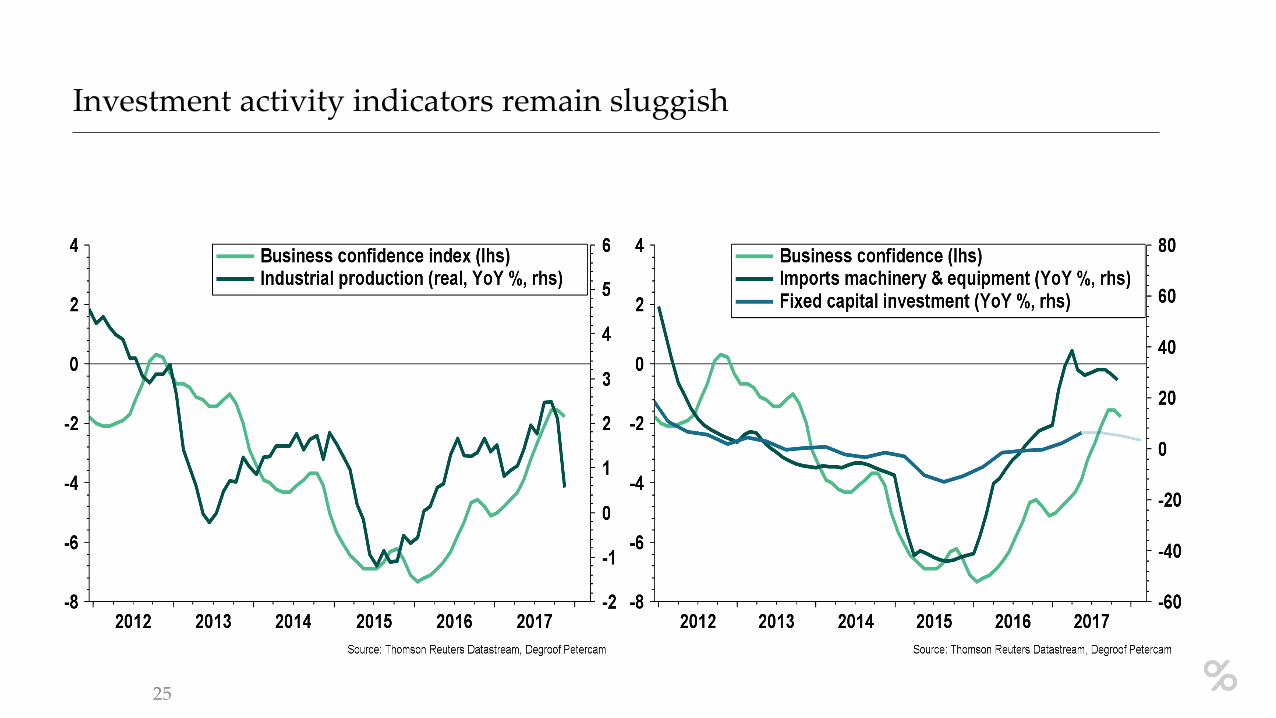

Investment activity indicators remain sluggish

25

Increasing capacity utilisation in manufacturing

26

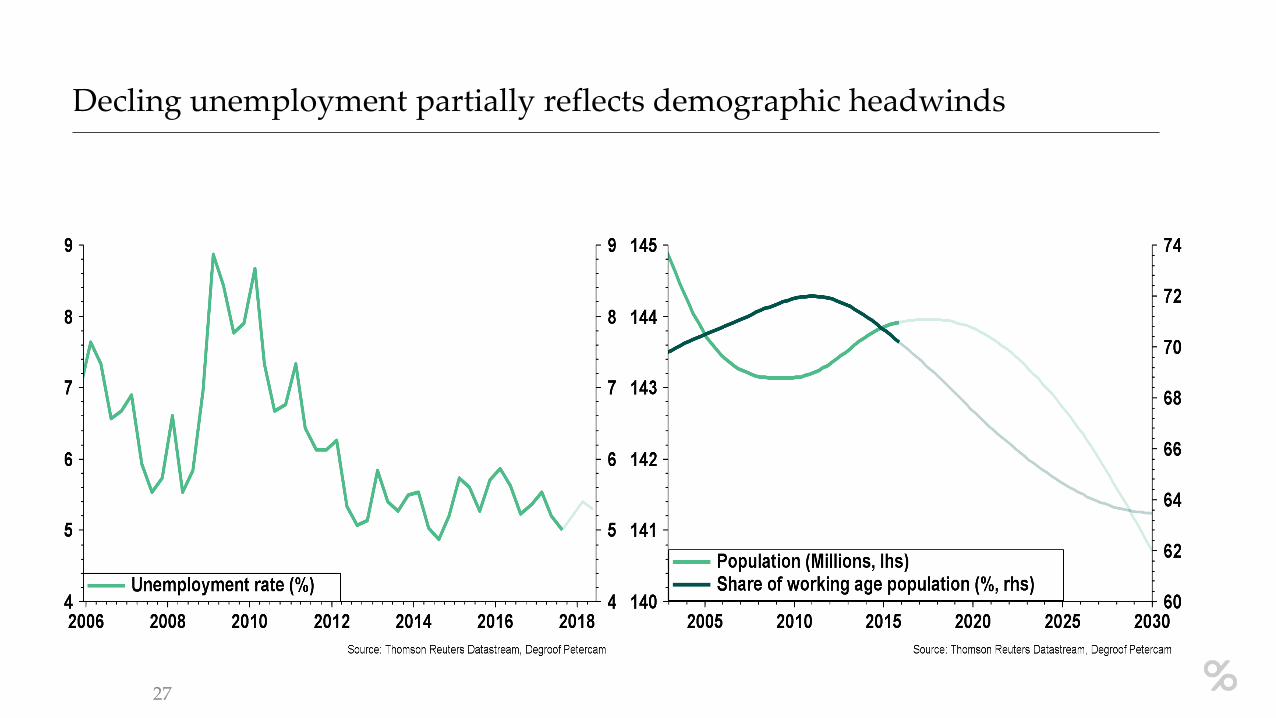

Decling unemployment partially reflects demographic headwinds

27

Wage growth remains largely constrained

28

External factors and lower food prices driving inflation...

29

... lower below target…

30

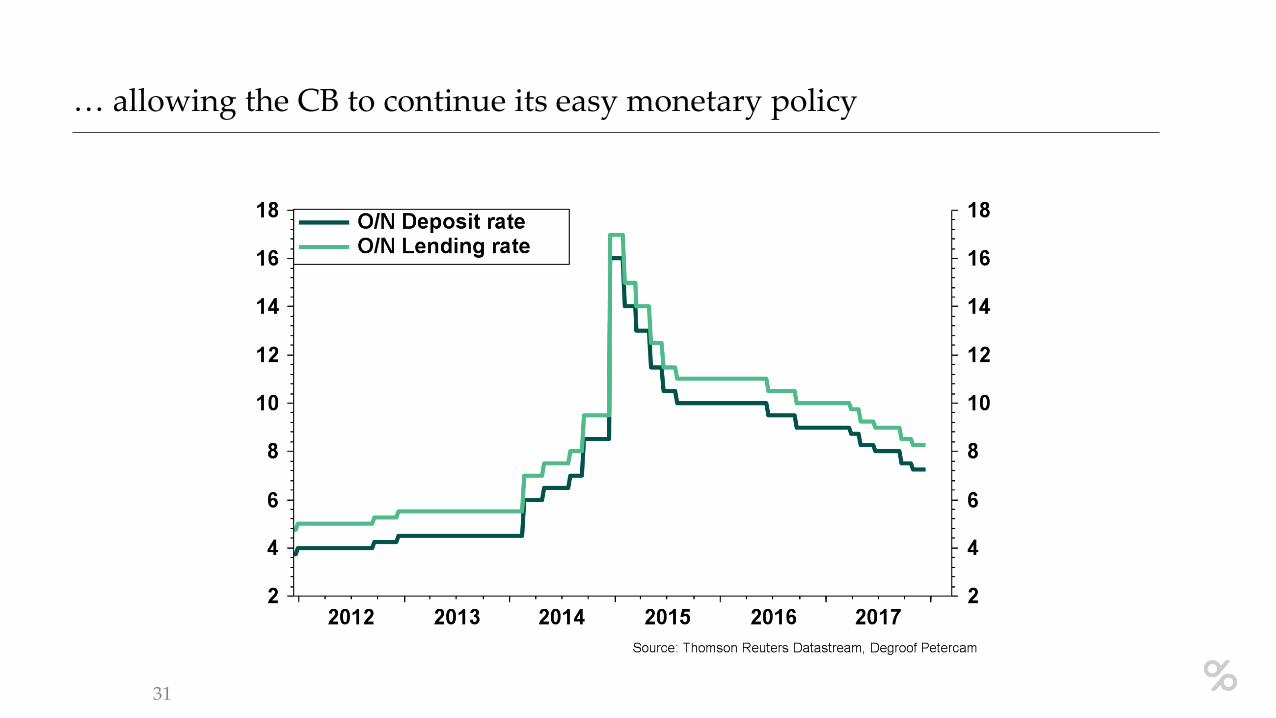

… allowing the CB to continue its easy monetary policy

31

Current account strongly influenced by oil…

32

… as is the fiscal outlook, hence the introduction of new budget rule…

33

… to lower the budget’s oil & gas dependence (~ Dutch disease)

• Mechanism to save difference between actual and projected revenues • Excess revenues are used to buy FX with proceeds deposited in Reserve Fund

(actual oil price >$40 pb) • Shortages are withdrawn from Reserve Fund (actual oil price <$40 pb) • Primary structural deficit should be ≤ 0%

34

Russia - Conclusion

• The Russian economy is recovering from a long but shallow recession, supported by efforts to shift the economy away from the energy sector.

• Consumption growth is gradually improving, although investment activity indicators

remain sluggish. • Wage growth remains constrained and volatile food prices put downward pressure on

consumer prices. In this context monetary policy remains supportive. • The fiscal constraints will be challenging given demographic headwinds, despite measures

that increase fiscal discipline and lower the impact from the energy sector.

35

India

Steady economic recovery continues…

37

… driven mainly by consumpion…

38

… with investment activity interrupted by drastic reforms.

39

Consumption surveys remain cautiously optimistic

40

Services lagging manufacturing

41

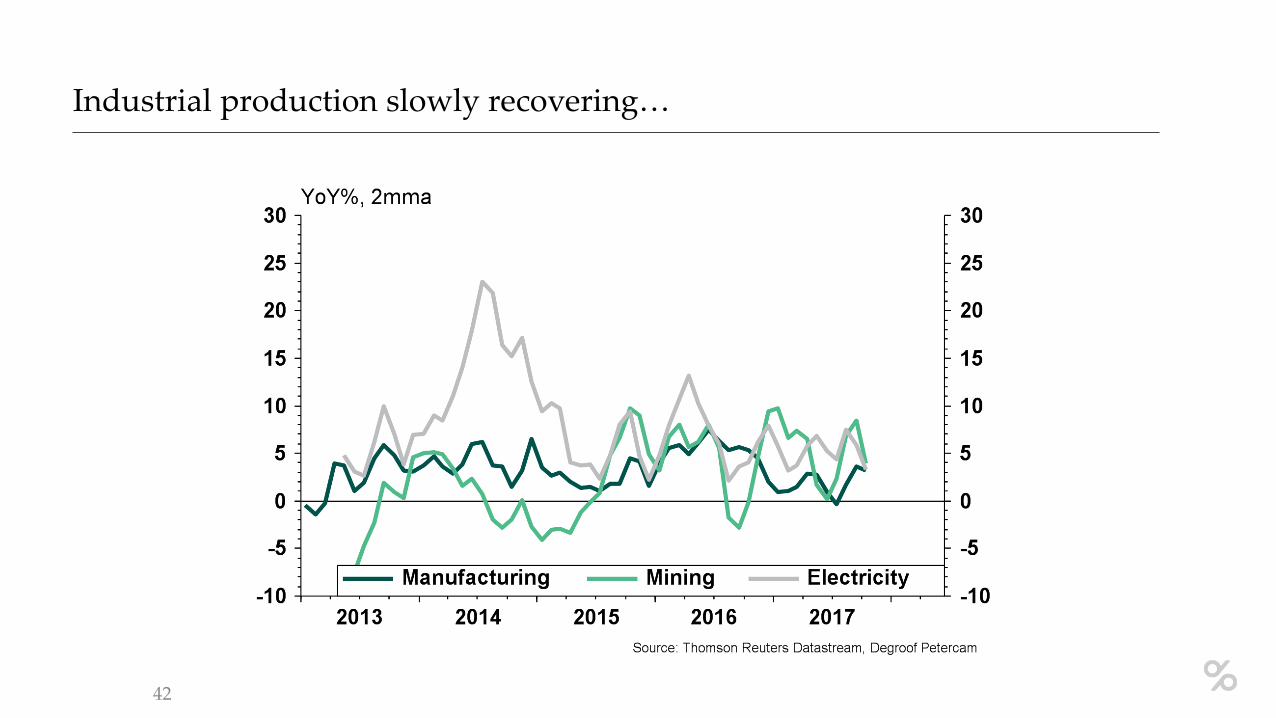

Industrial production slowly recovering…

42

… in line with exports after a period of weakness on the back of commodities.

43

Trade balance and current account in deficit

44

Base effects and food prices driving up inflation more recently…

45

… leading the RBI to slow down or stop easing cycle.

46

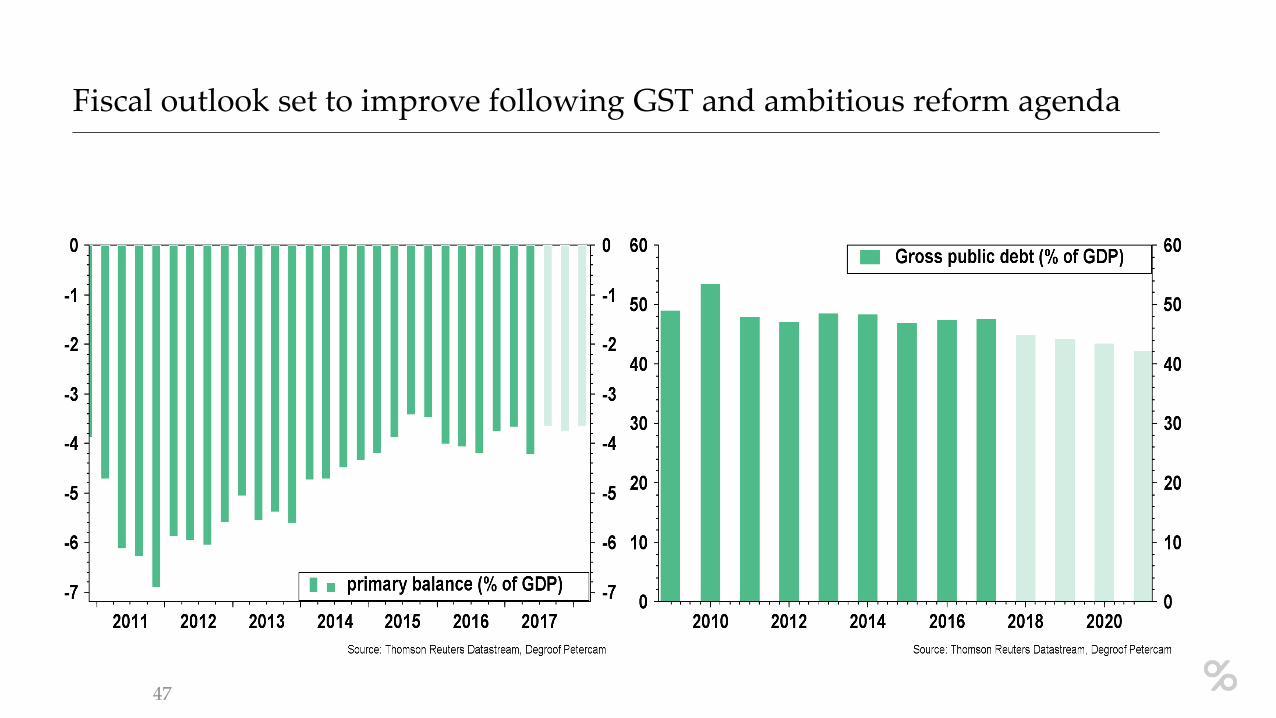

Fiscal outlook set to improve following GST and ambitious reform agenda

47

India - Conclusion

• The Indian economy is positioned on a high growth trajectory, with drastic reforms such as demonetisation and Goods and Services Tax reform (GST) weighing on ST growth.

• Consumption growth is main driver of recovery with investment activity, industrial

production and net exports improving more recently. • With inflation moving higher, the RBI is expected to remain on hold for now.

• Fiscal outlook is set to improve following ambitious reforms, as is the LT growth potential.

48

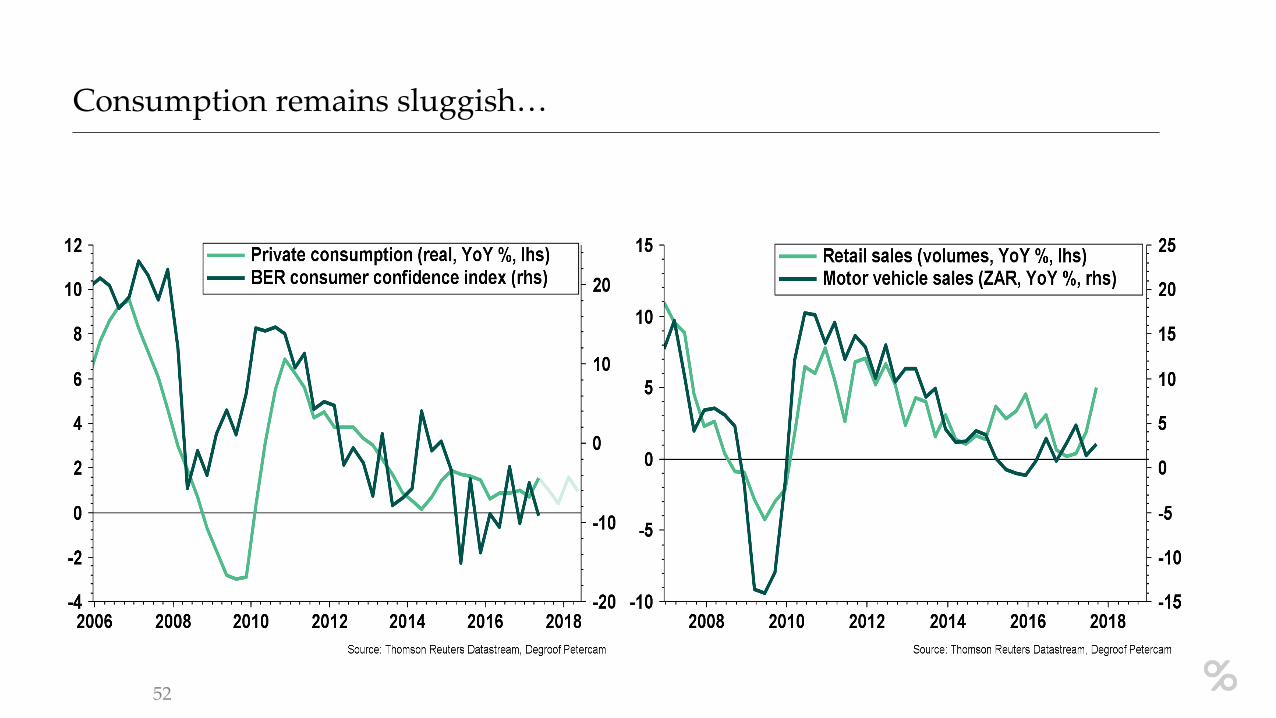

South-Africa

Economic activity continues to struggle…

50

… leaving S. Africa out of the current global cyclical upswing.

51

Consumption remains sluggish…

52

… across most regions.

53

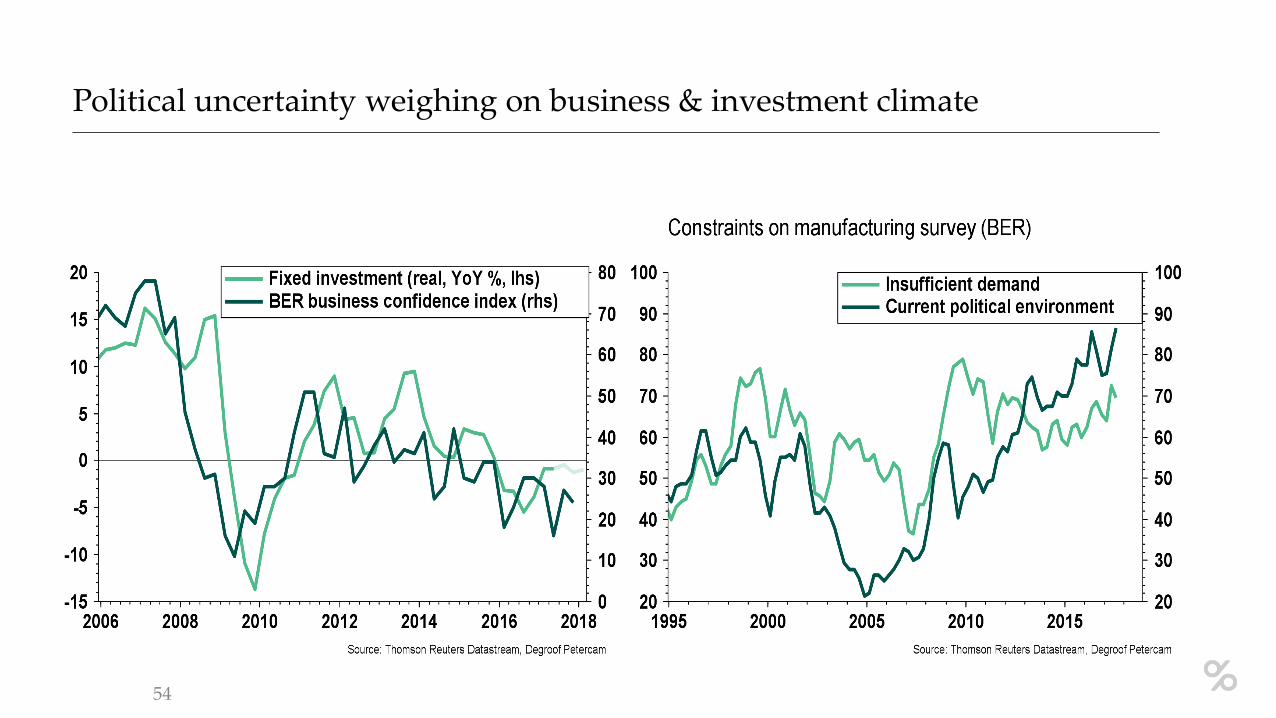

Political uncertainty weighing on business & investment climate

54

Extreme inequality likely topic in upcoming elections (H1 ‘19)

55

Weak job growth not sufficient to keep pace with increased participation

56

Significant interest payments to foreign debt holders…

57

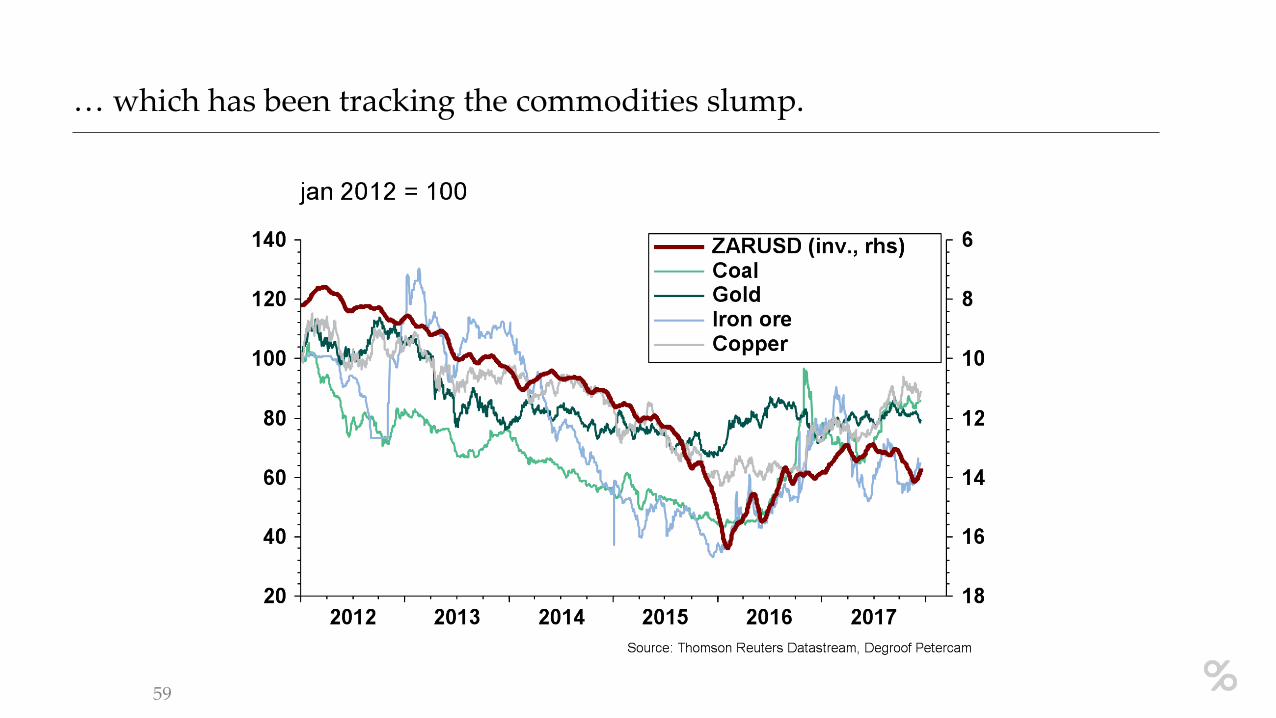

… are contributing to a widening CA deficit, despite a low ZAR…

58

… which has been tracking the commodities slump.

59

Pass-through effects on inflation remain limited

60

Core inflation remains moderate…

61

… and close to target, despite inflation expectations anchoring higher.

62

SARB remains put and cautious for higher inflation prints

63

Government debt set to increase further

64

South Africa - Conclusion

• Despite the global cyclical recovery, the growth outlook in S.Africa remains subdued. • Consumption growth remains modest and current political environment seems to be

weighing on confidence and investment. • Levels of external debt remain high, contributing to the CA deficit

• Inflation remains moderate and close to target while inflation expectations are anchoring

higher, prompting the SARB to be patient and cautious.

• The general election in H1 2019 will be closely watched, as structural problems need to be addressed and the traditional political landscape could fundamentally change.

65

BRICS outlook - Conclusion

• The Brazilian economy is leaving recession strongly on a disinflationary trend, with fiscal outlook and election biggest uncertainty

• Russia is set to grow with a reduced dependency on oil, struggling with fiscal constraints

and demographic headwinds in the LT • India is on one of the highest growth trajectories of all EM, with ambitious reforms weighing

on short-term growth while increasing LT growth potential • China (see here for recent update) • South-Africa risks missing out of global upswing on the eve of important elections that

could address its structural problems such as inequality

66

Contact

Michiel Verstrepen Economist

Bank Degroof Petercam

Tel.: +32 (0)2 662 81 32

Follow our blog posts at blog.degroofpetercam.com

Follow me on Twitter: @michielverstrep

Discover our website at www.degroofpetercam.com

67