breaking down federal investments in clean energy

TRANSCRIPT

Breaking Down Federal Investments in Clean Energy BY MEGAN NICHOLSON AND MATTHEW STEPP | MARCH 2013

The United States has failed to create a comprehensive energy policy that provides robust and consistent support for innovation. Although the Recovery and Reinvestment Act of 2009 stimulated public investments in energy innovation, many of these programs and incentives have since expired or concluded, leaving the energy innovation ecosystem underfunded and skewed towards supporting deployment incentives over technology R&D, demonstration, and manufacturing.

This report assembles a series of articles first published on Energy Trends Insider, featuring data captured in the Energy Innovation Tracker.1 ITIF’s Energy Innovation Tracker is a publically available, transparent, and accessible database of federal investments in energy innovation at the project level.2 It was developed to inform the clean energy policy debate by defining federal investments in clean energy innovation by technology, innovation phase, and investment type. Energy policy in the United States is only as good as its innovation-based goals, framing, and emphasis, so clarifying past and current support for energy innovation is fundamental to creating the policies of the future.

The structure of the report breaks down the major areas of energy innovation investment.3 The first section defines energy innovation by identifying the necessary pieces of a comprehensive innovation ecosystem. The second section details total investment trends since 2009. The third section takes a closer look at investment trends for energy demonstration projects, and the fourth section does the same for deployment incentive costs. The fifth section describes investment trends in support for clean energy manufacturing.

DEFINING THE ENERGY INNOVATION ECOSYSTEM

A pervasive problem persists in the clean energy policy debate: innovation policy is often misrepresented as only research, or largely ignored by advocates to support rigid

ENERGY INNOVATION TRACKER MARCH 2013

2

economic doctrines or policy goals that divert attention from addressing climate change (e.g. short-term green job creation).4 This type of clean energy policy fundamentalism de-emphasizes the need for cheap, new, clean energy technologies and muddles innovation’s foundational role in U.S. clean energy policy. By extension, the process inhibits America’s abilities to drastically cut carbon emissions as quickly as possible.

Providing clarity on what characterizes clean energy innovation policy is critically important to understanding the components of a healthy innovation ecosystem. The first step towards improving the nation’s energy innovation system is defining the individual but linked stages of technology innovation.

Basic Science Basic energy science is fundamental scientific research in fields like chemistry, biology, and physics that often don’t have an obvious commercial outcome but could enable a suite of energy solutions. The National Science Foundation invested $43 million in basic energy science projects through university grants in FY2013 covering a wide gamut of science issues potentially related to energy, such as developing fundamentally new ways to grow nano-crystals which could have significant impact for fuel cells and biomedical technologies. The Department of Energy Office of Science, on the other hand, conducts basic energy research in high-energy physics, nuclear energy, super-computing and chemistry both through University grants, but also through the National Laboratory system. Projects include fundamental research in plasma technology, quantum physics, and the creation of new materials and biochemistries, to name a few.

Research and Development As basic science progresses in the lab and potential uses and outcomes become more apparent, additional research and development (R&D) is necessary. R&D is specific research that addresses explicit technological needs through creating proof-of-concept prototypes.5 In many ways this research is still early-stage, but often with more focused purpose and goals. For instance, the Department of Agriculture invests in several different feedstock and conversion process R&D projects in order to target the most cost-effective and efficient combination for creating next-generation biofuels ($11 million in FY2011), while the Department of Transportation’s NextGen Aircraft Technologies program supports the development of alternative jet fuels and low-carbon aviation systems and technologies through early-stage prototyping ($20.1 million in FY2011).6

DOE’s Advanced Research Projects Agency–Energy (ARPA-E) offers the most comprehensive picture of laudable public R&D investments; the agency funds early-stage research through prototyping of potentially “transformative” energy technologies that would otherwise be too risky for private investors.7 ARPA-E was initially funded by the Recovery Act, and was appropriated $143 million in FY2011 and $243 million in FY2012.

DOE’s Advanced Research Projects Agency–Energy (ARPA-E) funds early-stage research through prototyping of potentially “transformative” energy technologies that would otherwise be too risky for private investors.

ENERGY INNOVATION TRACKER MARCH 2013

3

Technology Demonstration Demonstration projects offer the opportunity to show users the practical utility of a new technology, while enabling researchers to collect data on its technical and economic characteristics under realistic conditions and address any remaining research gaps.8 Because of the capital-intensive nature of energy technologies, demonstration projects are often expensive and are underfunded by the private sector, however despite the high cost of these projects, they are highly valuable because they offer increased access to information to all stakeholders. In fact, for many energy technologies like utility-scale solar, wind, and carbon capture projects, demonstrating its first-of-kind commercial potential is absolutely necessary to gain private sector support for the technology.

Examples of this kind of investment include the American Recovery and Reinvestment Act (ARRA) investment of $685 million in the demonstration of competitively selected, large-scale grid projects to measure performance and cost in a realistic market. The Pacific Northwest Division Smart Grid Demonstration Project installed industrial smart metering, electricity storage technologies, and direct load control devices to distribute power to more than 60,000 customers across five states to validate technology readiness and assess costs and benefits of the enhanced grid system. DOD also supports projects demonstrating advancements in energy technology in pursuit of achieving greater operational capabilities – their Great Green Fleet project equips tanks and other combat vehicles with a variety of energy technologies including fuel cell engines and energy storage and power electronics systems.9 Investment in the suite of projects contributing to the Great Green Fleet demonstration totaled about $82 million in FY2012.

Siting and Permitting Support for siting and permitting offers technical and regulatory assistance for planning and management within current policies. Projects focused on siting and permitting often conduct market research for technology commercialization prior to the deployment stage; this kind of research can be as procedural as Department of Commerce research on coastal and marine spatial planning for potential offshore wind locations (which cost $1.5 million in FY2011) or as objective as DOE’s market transformation and systems integration programs within the Office of Energy Efficiency and Renewable Energy (EERE) (which totaled $31 million in FY2011) that research other non-hardware barriers to technology commercialization such as potential regional or industry collaborations, addressing concerns for the wide-spread adoption of emerging energy technologies.

Technology Deployment Even after a technology has been demonstrated at full-scale, financing for its full commercialization may not be easily attained because of the nature of the energy industry and the low (often subsidized) cost of fossil fuels. Technology deployment

ENERGY INNOVATION TRACKER MARCH 2013

4

investments can help create economies of scale for technologies by creating an initial customer base, promoting information sharing about the technology, allowing producers to streamline manufacturing processes, and permitting installers to lower costs.10 Deployment support can directly apply to either commercial “off-the-shelf” technologies that are readily available in the marketplace, or emerging technologies that are not widely available in commercial markets.

The Department of the Treasury is in charge of administering a number of deployment programs through tax incentives that support both clean and conventional energy technologies – the much-discussed Energy Production Tax Credit is one such incentive available to producers of clean energy technologies (wind, solar, biomass, etc.) that provides a subsidy to any eligible clean energy project. In a parallel way the Department of Interior supports the deployment of energy technologies through the department-wide New Energy Frontier initiative, which funds the deployment of renewable and conventional energy on public lands.11

Government Procurement An additional way that public investments can promote the innovation of clean energy technologies is through acquisition of technologies by the federal government acquiring technologies. Like deployment incentives, government procurement can create early markets for emerging technologies that are too risky for commercial markets, but show future promise. For example, early government purchasing of the microchip allowed produces to quickly lower costs and eventually take the product to market, revolutionizing the electronic industry. In energy, General Services Administration (GSA) and DOD procurement are the top agencies capable of creating early markets for breakthrough technologies. ITIF’s recent report, Lean, Mean, and Green II: Assessing DOD Investments in Clean Energy Innovation suggested that DOD’s operational energy challenges drove the department to invest $540 million in FY2012 in the procurement of energy technologies, and about 70 percent of this investment was for acquiring emerging technologies.12 DOD’s procurement process provides the demand and the capital for the production of these emerging technologies, which in turn offers potential for bringing the technologies to commercial markets.

Manufacturing The future of a competitive clean energy industry in the United States hinges on significant investments in clean energy technology manufacturing. While the previous innovation phases are integral in developing advanced technologies, without a significant manufacturing sector the country continues to rely on the manufacturing capacities of other countries, losing its competitive advantage as an innovator of breakthrough energy solutions. The Section 48C Advanced Energy Manufacturing Tax Credit, for example, awarded funds to energy producers to update or build facilities for

DOD’s operational energy challenges drove the department to invest $540 million in FY2012 in the procurement of energy technologies, and about 70 percent of this investment was for acquiring emerging technologies.

ENERGY INNOVATION TRACKER MARCH 2013

5

the manufacture of advanced wind, solar, geothermal, and other renewable energy technologies.13

Improving the pathway towards competitive clean energy in the United States lies in improving the quality of our innovation system – but these improvements can only begin with a full understanding of the innovation ecosystem itself. Defining energy innovation at this level of detail exposes the features of a working ecosystem more thoroughly, and defining public investments according to these phases can uncover white spaces that require additional funding, areas of policy weakness, or areas where there may be over-funding.

In the following sections, we’ll look more deeply into the public investment profiles of individual innovation phases to give a better sense of what U.S. clean energy policy really looks like, and to provide a sense of how these investments are shaping America’s clean energy future and what additional policy support is needed. This report is complimentary to previous reports taking a deep-dive into U.S. Clean energy R&D funding. 14

TRENDS IN PUBLIC INVESTMENTS IN CLEAN ENERGY INNOVATION

Clean energy innovation encompasses more than any one policy, whether it is R&D, tax incentives, regulation, or an economy-wide carbon price. Well-designed public investments impact the entire energy innovation ecosystem and fill gaps in next-generation technology development and deployment.

Figure 1 details federal investments in energy innovation since FY2009, which are divided into ‘technology development’ and ‘technology deployment’ categories. In this case, technology development captures all investments in basic science, research and development, demonstration; technology deployment investments facilitate the installation and procurement of clean energy technologies in commercial markets, along with supporting investments in siting and permitting and training and education.

During the past four years, the balance between development and deployment has evolved dramatically, driven in part by increased procurement of emerging and commercial off-the-shelf energy technologies by the Department of Defense, as well as expanded deployment initiatives and tax incentives through the Department of Energy and the U.S. Treasury Department. Between 2009 and 2011, investment in deployment and procurement of clean energy technologies nearly quadrupled, while investment in R&D and demonstration projects remained relatively steady or declined. All told, technology deployment and procurement now captures about 63.8 percent of the clean energy innovation budget, while technology development captures 36.1 percent.

Technology deployment and procurement now captures about 63.8 percent of the clean energy innovation budget, while technology development captures 36.1 percent.

ENERGY INNOVATION TRACKER MARCH 2013

6

Loan guarantee programs also contributed to the demonstration and deployment of clean energy technologies during the last four years and through the Recovery Act by providing temporary financing for projects and technological systems close to commercialization. The impacts of these investments on the development of technologies has high value, but the cost to the government to back loan guarantees is only a fraction of the actual loan amount. Because of this distinction from direct government spending, loan guarantees are not counted in this section. Costs and impacts of loan guarantees are explained in further detail in the subsequent sections on demonstration projects and deployment incentives.

Figure 1: Total investment in clean energy innovation between FY2009 and FY2012, and from the American Recovery and Reinvestment Act (ARRA) (billions, USD); does not include loan guarantees

The impact of significant investments in clean energy innovation through the American Recovery and Reinvestment Act (ARRA) cannot be overstated. The Recovery Act directly increased federal funding of research and demonstration projects through a series of new programs and initiatives, and also established many tax incentives for the adoption of energy efficiency and renewable energy technologies that were extended into FY2012. While some critics accuse the Recovery Act of coming up short in its effort to reverse the effects of the Great Recession on the American economy, it super-charged energy innovation with public investments in new programs, and created new opportunities for funding of advanced energy R&D through ARPA-E.

Between 2009 and 2011, investment in deployment and procurement of clean energy technologies nearly quadrupled, while investment in R&D and demonstration projects remained relatively steady or declined.

ENERGY INNOVATION TRACKER MARCH 2013

7

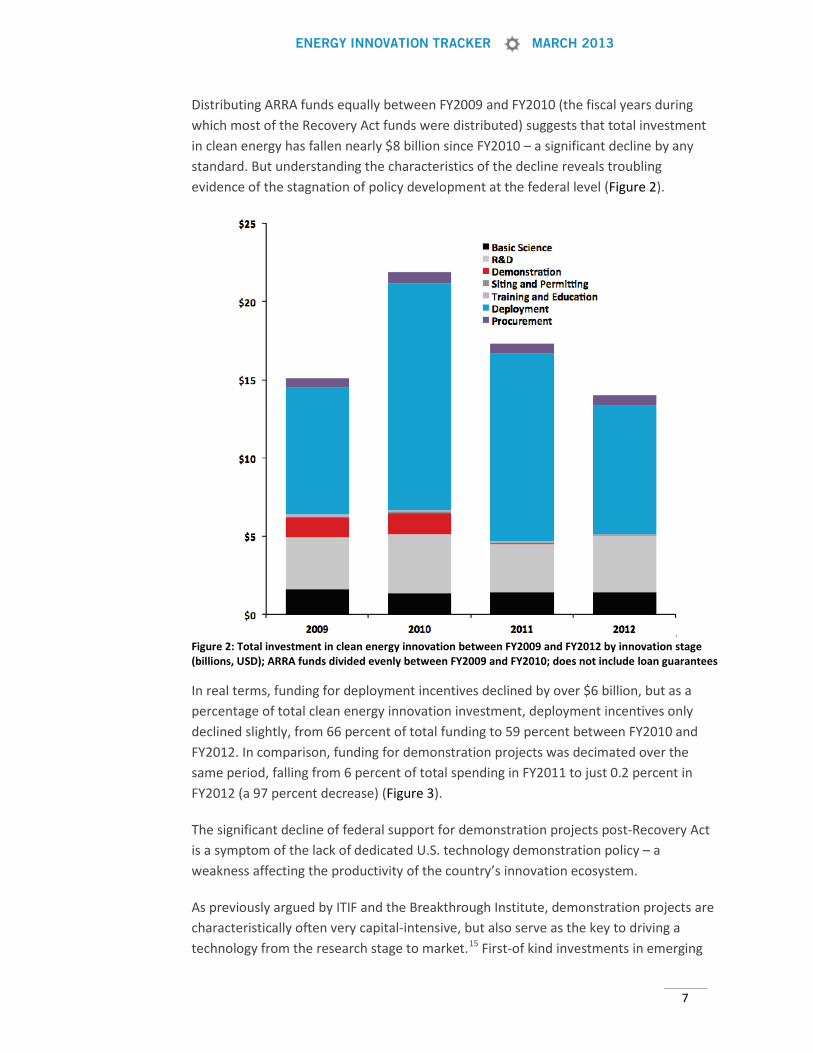

Distributing ARRA funds equally between FY2009 and FY2010 (the fiscal years during which most of the Recovery Act funds were distributed) suggests that total investment in clean energy has fallen nearly $8 billion since FY2010 – a significant decline by any standard. But understanding the characteristics of the decline reveals troubling evidence of the stagnation of policy development at the federal level (Figure 2).

Figure 2: Total investment in clean energy innovation between FY2009 and FY2012 by innovation stage (billions, USD); ARRA funds divided evenly between FY2009 and FY2010; does not include loan guarantees

In real terms, funding for deployment incentives declined by over $6 billion, but as a percentage of total clean energy innovation investment, deployment incentives only declined slightly, from 66 percent of total funding to 59 percent between FY2010 and FY2012. In comparison, funding for demonstration projects was decimated over the same period, falling from 6 percent of total spending in FY2011 to just 0.2 percent in FY2012 (a 97 percent decrease) (Figure 3).

The significant decline of federal support for demonstration projects post-Recovery Act is a symptom of the lack of dedicated U.S. technology demonstration policy – a weakness affecting the productivity of the country’s innovation ecosystem.

As previously argued by ITIF and the Breakthrough Institute, demonstration projects are characteristically often very capital-intensive, but also serve as the key to driving a technology from the research stage to market.15 First-of kind investments in emerging

ENERGY INNOVATION TRACKER MARCH 2013

8

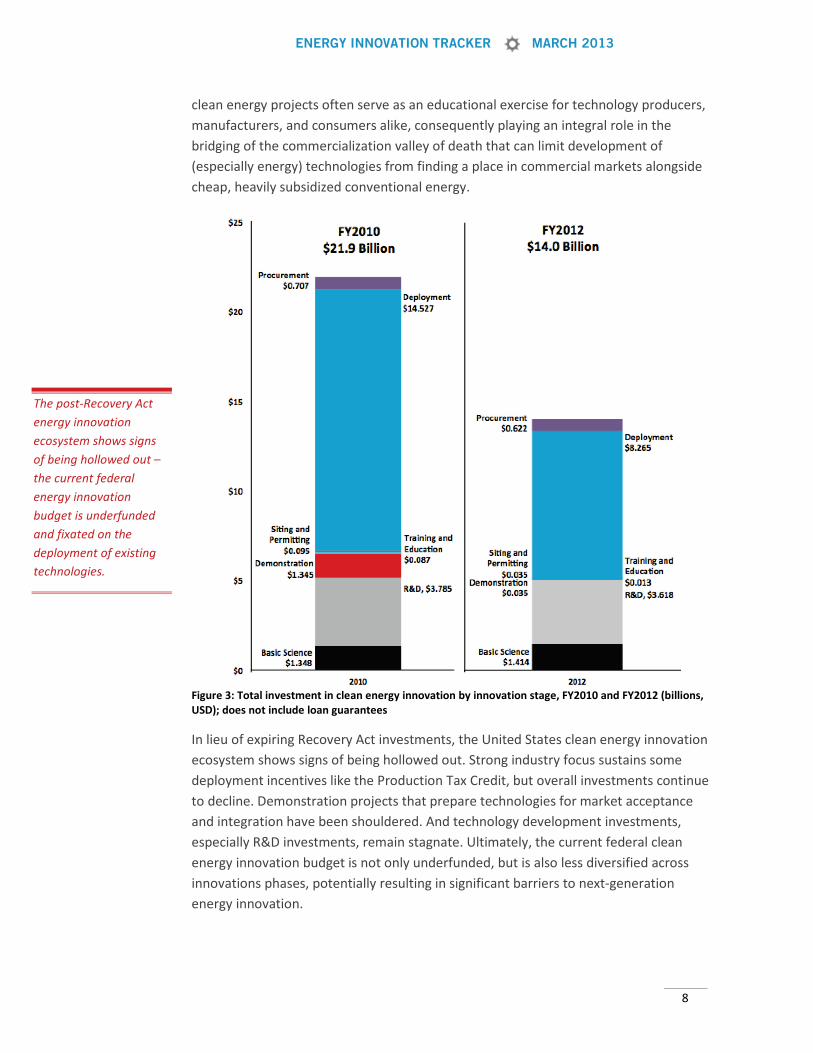

clean energy projects often serve as an educational exercise for technology producers, manufacturers, and consumers alike, consequently playing an integral role in the bridging of the commercialization valley of death that can limit development of (especially energy) technologies from finding a place in commercial markets alongside cheap, heavily subsidized conventional energy.

Figure 3: Total investment in clean energy innovation by innovation stage, FY2010 and FY2012 (billions, USD); does not include loan guarantees

In lieu of expiring Recovery Act investments, the United States clean energy innovation ecosystem shows signs of being hollowed out. Strong industry focus sustains some deployment incentives like the Production Tax Credit, but overall investments continue to decline. Demonstration projects that prepare technologies for market acceptance and integration have been shouldered. And technology development investments, especially R&D investments, remain stagnate. Ultimately, the current federal clean energy innovation budget is not only underfunded, but is also less diversified across innovations phases, potentially resulting in significant barriers to next-generation energy innovation.

The post-Recovery Act energy innovation ecosystem shows signs of being hollowed out – the current federal energy innovation budget is underfunded and fixated on the deployment of existing technologies.

ENERGY INNOVATION TRACKER MARCH 2013

9

The next sections identify the contributing sources of this decline by examining investment trends within the demonstration, deployment, and manufacturing innovation stages.

FEDERAL SUPPORT FOR DEMONSTRATION PROJECTS

Transforming the U.S. (and global) energy system from fossil fuels to low-carbon technologies requires a healthy, publicly supported innovation ecosystem that invests in and supports research, development, demonstration, and deployment. But as discussed in the last section, America’s energy innovation ecosystem is hollowed out, particularly because of reduced investment in technology demonstration projects.

Controversy of Public Funding for Demonstration Projects At its very basic level, technology demonstration projects exhibit full-scale models of first-of-kind technologies and systems, as opposed to pilot projects (e.g. an ARPA-E project), which aim to simply prove a technical idea. Demonstration projects aim to prove a technology at commercial scale. Clean energy demonstration projects are an area of policy debate and controversy for two reasons:

Clean energy demonstration projects are often capital-intensive projects that require significant investment and public-private collaboration, typically invoking considerable attention because of large budgets.

Clean energy demonstration projects are often viewed as too close to market and not an appropriate role of government investment. As such, it’s a turbulent area of clean energy innovation policy.

Purpose of Demonstration Projects Criticisms aside, clean energy demonstration projects serve a number of important innovation-related purposes. Demonstration projects communicate potential commercial applications to consumers and manufacturers. They also provide energy producers with the opportunity to collect and evaluate data on technology performance under commercial-scale conditions.

Good demonstration projects efficiently showcase the technology to maximize interest, and all demonstration projects look different depending on the technology and can vary from large-scale smart grid technology installations to model homes showcasing emerging building technologies, plus everything in between. Historically, a common characteristic across the board is that demonstration projects represent a crucial role in technology development because of the opportunity they offer to accelerate technologies across the commercialization valley of death and into the market.

ENERGY INNOVATION TRACKER MARCH 2013

10

Impacts of the Recovery Act on Investment in Demonstration The Recovery Act alone increased demonstration project investment to almost $2.6 billion, and was complimented by scant fiscal year appropriations. In the absence of direct spending on Recovery Act-backed programs, the loan guarantee programs (particularly the Title XVII Section 1705 and the Advanced Technology Vehicle Manufacturing loan programs) provided support for these projects in FY2011.16

The cost of a loan guarantee to the government – called the “subsidy cost” – is the estimated cost to the government if the loan recipient should default. Subsidy costs are appropriated by fiscal year (or through the Recovery Act, in the case of the Title 17 Section 1705 Loan Program), but are not available to the public on a project-by-project basis. Consequently presented in this report are the full loan amounts for loan programs, counted within the fiscal year of the projects’ agreement dates.17 The Title XVII Section 1705 Loan Program expired in 2011 and consequently the program did not grant additional loan guarantees after this point.18 Many of the funded projects are still ongoing, but they are no longer receiving federal funds. The loan guarantee programs are counted here according agreement date.

Figure 4: Total investment in clean energy demonstration projects (loan guarantees counted according to agreement date), FY2009-FY2012 (billions, USD); ARRA funds divided evenly between FY2009 and FY2010

Direct spending and loan programs are obviously not immediate substitutes for each other – direct spending describes federal appropriations and grants for clean energy

Transforming the U.S. (and global) energy system from fossil fuels to low-carbon technologies requires a healthy, publicly supported innovation ecosystem that invests in and supports research, development, demonstration, and deployment.

ENERGY INNOVATION TRACKER MARCH 2013

11

projects, while loan guarantee programs only support the temporary financing of debt. The federally appropriated funds for the loan guarantee programs are essentially only enough to cover the possible cost of loan defaults. After the Recovery Act, in other words, direct spending on clean energy demonstration projects fell from $1.3 billion in FY2009 to only $56 million in FY2011.

While DOE ARRA funds and loan guarantees provided about 80 percent of the financial support for clean energy demonstration projects in FY2009-10, the Department of Transportation’s Funding for Transportation Electrification Initiative provided $400 million during the two fiscal years – the program awarded eight projects with funding for the demonstration of “grid-connected vehicle and infrastructure” projects, including charging stations, to accelerate large-scale data collection of these technological impacts to the grid (Figure 5).

Figure 5: Total investment in clean energy demonstration projects by agency, (loan guarantees counted according to agreement date) FY2009-FY2012 (billions, USD); ARRA funds divided evenly between FY2009 and FY2010

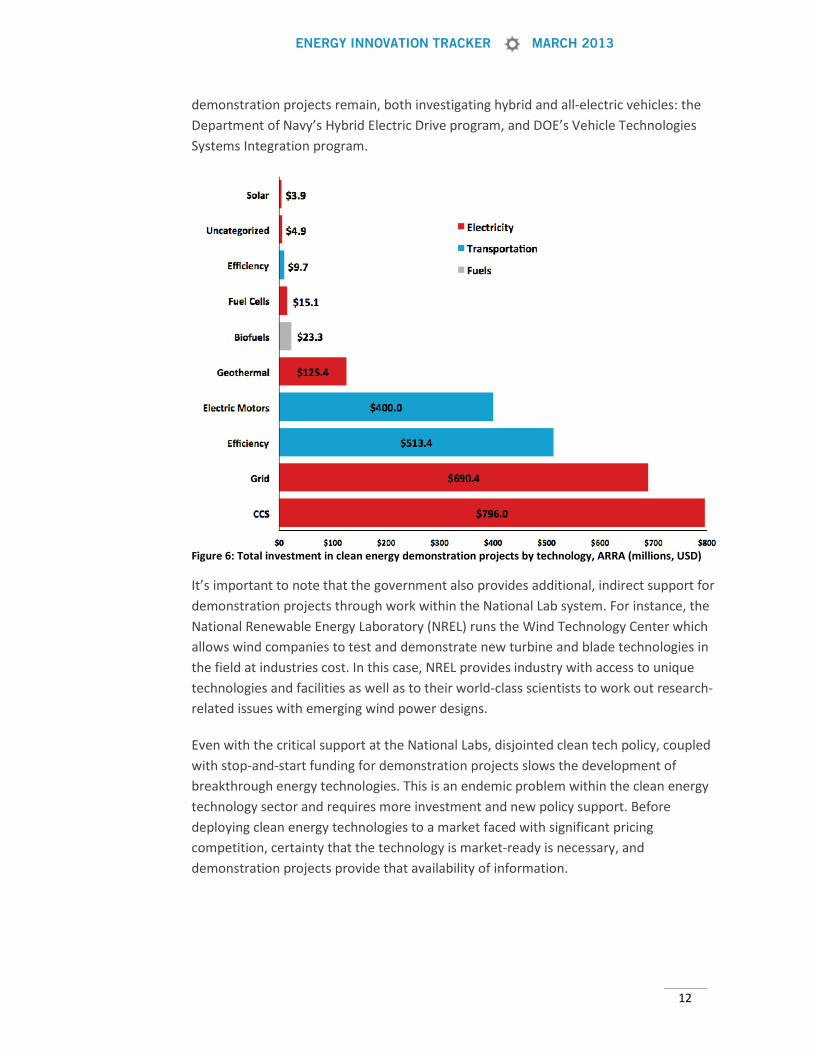

The Recovery Act diversified investment in demonstration projects across at least ten technology categories (Figure 6), although significant funding was awarded to larger projects like the Department of Energy’s Clean Coal Power Initiative demonstration project which supplemented an existing project with funds for exploring emerging carbon sequestration technologies, as well as the Smart Grid Regional Energy Storage demonstration project which invested in several large-scale grid demonstration projects that installed emerging battery, flywheel, and compressed air storage technologies to electricity grids across the country. In FY2012, only two publically supported

After the Recovery Act, direct spending on clean energy demonstration projects fell from $1.3 billion in FY2009 to only $56 million in FY2011.

ENERGY INNOVATION TRACKER MARCH 2013

12

demonstration projects remain, both investigating hybrid and all-electric vehicles: the Department of Navy’s Hybrid Electric Drive program, and DOE’s Vehicle Technologies Systems Integration program.

Figure 6: Total investment in clean energy demonstration projects by technology, ARRA (millions, USD)

It’s important to note that the government also provides additional, indirect support for demonstration projects through work within the National Lab system. For instance, the National Renewable Energy Laboratory (NREL) runs the Wind Technology Center which allows wind companies to test and demonstrate new turbine and blade technologies in the field at industries cost. In this case, NREL provides industry with access to unique technologies and facilities as well as to their world-class scientists to work out research-related issues with emerging wind power designs.

Even with the critical support at the National Labs, disjointed clean tech policy, coupled with stop-and-start funding for demonstration projects slows the development of breakthrough energy technologies. This is an endemic problem within the clean energy technology sector and requires more investment and new policy support. Before deploying clean energy technologies to a market faced with significant pricing competition, certainty that the technology is market-ready is necessary, and demonstration projects provide that availability of information.

ENERGY INNOVATION TRACKER MARCH 2013

13

DEEP DIVE INTO DEPLOYMENT INCENTIVES

For the last few years, the lion’s share of debate on U.S. clean energy policy has focused on encouraging deployment – or large-scale construction and installation – of low-carbon technologies. By significantly deploying clean energy technologies, supporters say, the United States can encourage integration of emerging technologies in an energy market dominated by entrenched fossil fuel interests, spur cost-cutting economies of scale, and get started on lowering greenhouse gas emissions in the process. However, others argue that there is a necessity to designing well-constructed deployment incentives aimed at directly spurring innovation to address climate change.19

Typology of Deployment Policies Federal clean energy deployment incentives can be made available through grants and other annually appropriated programs. For instance, the State and Tribal Energy Programs at the Department of Energy (DOE) deploy building efficiency and renewable energy technologies within communities. The New Energy Frontier initiative at the Department of the Interior (DOI) deploys renewable and energy efficiency technologies on federal lands. While direct spending on deployment incentives of this type is typically minor in comparison to other direct spending programs, the Recovery Act significantly increased direct spending for deployment by funding the Advanced Battery Manufacturing Grants program, which awarded funding to projects that accelerated the manufacture and deployment of batteries for electric vehicles (Figure 7).

.

Figure 7: Total investment in deployment of clean energy technologies by investment type (loan guarantees counted according to agreement date), FY2009-FY2012, and ARRA investment (billions, USD)

ENERGY INNOVATION TRACKER MARCH 2013

14

More commonly, federal deployment incentives are driven by consumer and corporate tax credits, and through loan programs that help finance construction of large-scale technology installations. Investment in deployment programs was highest in FY2011 at $22.3 billion because of large tax and loan guarantee expenditures. In fact, the most significant deployment investment nearly every year between FY2009-2012 came from tax expenditures, which accounted for 80 percent of total investment in FY2010, 51 percent in FY2011, and 87 percent in FY2012.

Tax expenditures support a multitude of technology priorities including the production of low-carbon electricity, the installation of energy efficiency and renewable energy retrofits on homes and commercial buildings, and the production of low-carbon fuels (Figure 8). Many of the loan guarantee expenditures awarded during FY2011 were from the Recovery Act’s Title XVII Section 1705 Loan Program, which supported deployment of mainly solar and wind technologies.

Figure 8: Total investment in deployment of clean energy technologies by technology (loan guarantees counted according to agreement date), FY2009-FY2012 (billions, USD); ARRA funds divided evenly between FY2009 and FY2010

Commercial and Emerging Technologies An important distinction often overlooked in the clean energy deployment policy debate is whether public investment supports existing or emerging technologies. As the figure

ENERGY INNOVATION TRACKER MARCH 2013

15

below shows, federal deployment investments are historically directed at supporting commercial off-the-shelf technologies (i.e. technologies that are readily available in commercial markets), rather than emerging technologies (i.e. nascent technologies being introduced to commercial markets for the first time), with loan guarantees and tax incentives (Figure 9).

This difference is particularly important in determining whether deployment policies are linked to research investments and provide a strong pipeline for emerging technologies to reach market. Today, most clean energy technologies are not cost- and performance- competitive compared to conventional energy technologies. By deploying these technologies at a larger-scale, the nation is focusing its resources on making clean energy competitive by subsidizing the cost to producers and consumers, with the hope that (1) economies of scale will drive costs below that of fossil fuels and allow subsidies to lapse and (2) by providing existing clean energy technologies a niche footprint in the market, deployment policies are providing an opening for emerging technologies close to the commercialization phase.20

Figure 9: Total investment in deployment of clean energy technologies by investment type and technology generation (loan guarantees counted according to agreement date), FY2009-FY2012 (billions, USD); ARRA funds divided evenly between FY2009 and FY2010

Today, most clean energy technologies are not cost- and performance-competitive compared to conventional energy technologies.

ENERGY INNOVATION TRACKER MARCH 2013

16

Creating an Innovation-Centric National Deployment Policy Deployment incentives are an integral part of the innovation ecosystem because they help reduce costs, eliminate information and infrastructure barriers to achieving market introduction, and create new markets for next-generation technologies. Unfortunately the nation’s current system of subsidization and financing is chiefly focused on deploying mature technologies, instead of providing a direct pipeline for emerging technologies to reach market. Implementing deployment tools that only support the most mature technology options can potentially help pull emerging technologies into the market. In fact, wind turbine companies constructing wind fields because of the Production Tax Credit are also now able to work with researchers, such as those the National Renewable Energy Laboratory, on next-generation turbine designs. But the connection between research and market for other industries like solar and battery storage is not so clear.

Well-structured deployment policies with innovation in mind – such as those that leverage performance standards to foster companies to innovate, or those that spur regional collaborations that tie research with deployment options – are needed to move these industries to competitiveness as quickly as possible. Even the wind industry could better utilize incentives to ensure that the most innovative wind turbines, and not just the most mature, are installed using public investment.

Public investments in deploying emerging technologies are at an all-time low; an innovation ecosystem absent this investment stifles technological change and directly impacts America’s response to climate change. Emerging technologies are what ultimately will drive carbon emissions to zero as quickly as possible by providing low-cost, high-performance alternatives to fossil fuels. The imperative to accelerate the development and deployment of these technologies is quickly growing. In other words, not only must we increase public investment in deployment, we must also ensure complementary reforms to the policies themselves to emphasize support for emerging technologies in the context of improving our innovation ecosystem. This is a taller task for sure, but one that is desperately needed if we are to meet our climate goals.

THE CLEAN ENERGY MANUFACTURING SECTOR

There is an eminent need for supporting a well-developed and funded clean energy manufacturing sector as part of a robust innovation ecosystem. The feedback loops between manufacturing and research are explicitly linked.21 Even with all the R&D, demonstration, and deployment of clean energy, the United States could lose its competitive advantage over production resulting in the industry (and future innovation) to move overseas without strong policy support for advanced manufacturing. But like many other parts of America’s energy innovation budget, support for advanced manufacturing is rapidly declining.

An innovation ecosystem absent public investments in deploying emerging technologies stifles technological change and directly impacts America’s response to climate change – emerging technologies will drive carbon emissions to zero.

ENERGY INNOVATION TRACKER MARCH 2013

17

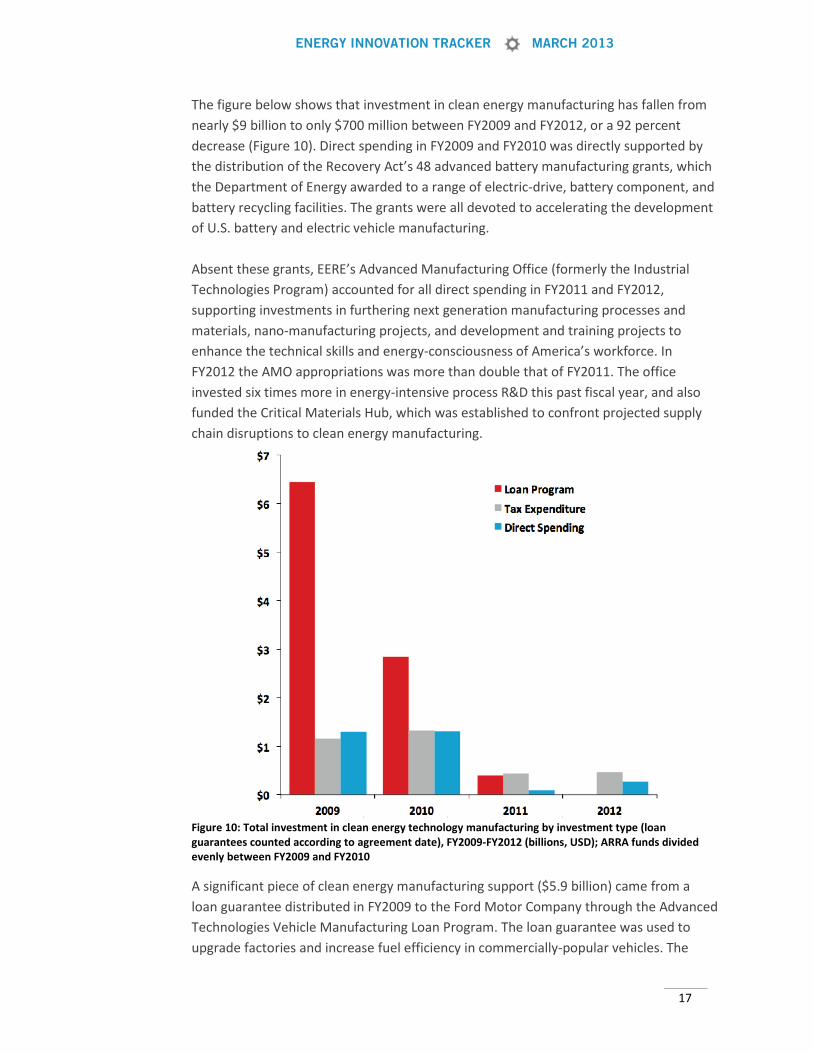

The figure below shows that investment in clean energy manufacturing has fallen from nearly $9 billion to only $700 million between FY2009 and FY2012, or a 92 percent decrease (Figure 10). Direct spending in FY2009 and FY2010 was directly supported by the distribution of the Recovery Act’s 48 advanced battery manufacturing grants, which the Department of Energy awarded to a range of electric-drive, battery component, and battery recycling facilities. The grants were all devoted to accelerating the development of U.S. battery and electric vehicle manufacturing. Absent these grants, EERE’s Advanced Manufacturing Office (formerly the Industrial Technologies Program) accounted for all direct spending in FY2011 and FY2012, supporting investments in furthering next generation manufacturing processes and materials, nano-manufacturing projects, and development and training projects to enhance the technical skills and energy-consciousness of America’s workforce. In FY2012 the AMO appropriations was more than double that of FY2011. The office invested six times more in energy-intensive process R&D this past fiscal year, and also funded the Critical Materials Hub, which was established to confront projected supply chain disruptions to clean energy manufacturing.

Figure 10: Total investment in clean energy technology manufacturing by investment type (loan guarantees counted according to agreement date), FY2009-FY2012 (billions, USD); ARRA funds divided evenly between FY2009 and FY2010

A significant piece of clean energy manufacturing support ($5.9 billion) came from a loan guarantee distributed in FY2009 to the Ford Motor Company through the Advanced Technologies Vehicle Manufacturing Loan Program. The loan guarantee was used to upgrade factories and increase fuel efficiency in commercially-popular vehicles. The

ENERGY INNOVATION TRACKER MARCH 2013

18

program made three other guarantees to electric vehicle manufacturers in FY2010, which amounted to $2.4 billion.

When separated from fiscal year appropriations, Recovery Act funds are accountable for a significant portion of investment in manufacturing during the last four years, both because of the loan guarantee program mentioned previously, and because of the advanced battery manufacturing grants for producers of electric vehicle batteries and components ($2.4 billion). The third major piece of clean energy manufacturing investment was the Section 48(c) Advanced Energy Manufacturing Tax Credit ($2.3 billion), which supported creation and updating of manufacturing facilities for renewable energy technology producers by allowing producers up to a 30 percent tax credit.

Figure 11: ARRA investment in clean energy manufacturing (billions, USD) (loan guarantees counted according to agreement date)

The Administration has tried repeatedly to extend the 48(c) tax credit, but has been unsuccessful to date. Combined, these three manufacturing policies accounted for 82 percent of total U.S. manufacturing investment since 2009. While they may individually have long-lasting impacts, intermittent funding opportunities like these encourage investment in the short-term. Significant growth in the clean energy manufacturing sector will only be stimulated by a strong policy commitment over time.

A strong clean energy manufacturing sector acts as an integral vehicle for producing clean energy technologies at economies of scale in order to drive down their costs and increase their competitiveness with conventional energy technologies.

ENERGY INNOVATION TRACKER MARCH 2013

19

While clean energy manufacturing is not often characterized as part of the energy innovation ecosystem, a strong manufacturing sector acts as an integral vehicle for producing clean energy technologies at economies of scale to drive down costs as well as acting as a key source for future research. America’s declining support for manufacturing is troubling, but new ideas are being worked on, though funding concerns still continue.

Strong support for a manufacturing sector in the United States is not only necessary to develop and deploy cost-effective clean energy technologies, it is also significant to ensuring the nation’s manufacturing competitiveness on the global scale. ITIF has written extensively (and recently) on why the administration’s National Network for Manufacturing Innovation (NNMI) plan should be put to action.22 While the health of U.S. manufacturing has planed off dramatically during the past decade, an NNMI could coordinate a recovery that leads to increases in productivity and job growth, and the recovery of America’s innovation ecosystem. To grow the clean energy economy and reduce carbon emissions in the in the United States, the importance of the manufacturing sector must not be forgotten.

CONCLUSION

Public investments in innovation are essential to advancing technologies from early-stage research through commercialization. This principle, proven by historical evidence, is especially important for the development of clean energy technologies because the process is more capital intensive, and technologies must compete within a current energy system running on cheap fossil fuels. Recognition of the need for public investments in support of energy innovation on its own, however, is not enough. Knowing where to direct those investments – for basic science, R&D, demonstration, deployment, and manufacturing of clean energy technologies – is even more significant.

Appreciating the state of the U.S. clean energy innovation ecosystem is the first step in recognizing ways to improve it. The analysis presented here suggests that in many ways the American Recovery and Reinvestment Act of 2009 elevated public investments in clean energy innovation to record levels. Unfortunately most of these investments were short-lived. Since the expiration of Recovery Act programs and tax credits supporting demonstration and manufacturing of clean energy technologies, in addition to continued budget cuts, the energy innovation ecosystem has been hollowed out.

Constructing a successful and enduring energy innovation ecosystem requires significant public investment, substantial policy commitment to the development of clean energy technologies, and considerable, smart policy options that can continue to drive energy innovation forward. A comprehensive strategy for meeting these challenges in the future is incomplete without a thorough understanding of current policy.

ENERGY INNOVATION TRACKER MARCH 2013

20

Appendix

Methodology

The Energy Innovation Tracker database has been compiled using only publicly available data from U.S. government budget documents, and the source of each line item within the EIT is identified in the database. All investments captured in the EIT reflect appropriations. EIT categorizes projects by innovation phase, investment type, technology, sub-technology and organizes entries by agency and program. All entries include a description and citation.

This analysis was performed using the current version of the database – ‘v01232013.’ The EIT captures all investments in energy innovation, but this report specifically considers clean energy innovation (i.e. it excludes tax incentives and other policies encouraging R&D and deployment of conventional energy technologies.)

This report accounts for loan guarantees by fiscal year according to project date of agreement, rather than by fiscal year in which total subsidy costs per loan program (which cover the cost of the loan in the case of default) were appropriated by Congress. Additionally, the loan guarantees captured here are for the entire loan amount, rather than the actual cost of the loans to the government. This kind of accounting allows for more project-level transparency and clarification for trends analysis, but it is different than the current version of the Tracker (‘v03052013’), which reports loan guarantees at the project level, counted within the fiscal year in which the subsidy cost of the program was appropriated.

ENERGY INNOVATION TRACKER MARCH 2013

21

Endnotes

All of the original posts in the series were initially published by Energy Trends Insider by Matthew 1.Stepp, and were featured in the following order: Matthew Stepp, “Clarifying Public Investments in Clean Energy Innovation,” Energy Trends Insider, January 3, 2013, http://www.energytrendsinsider.com/2013/01/03/clarifying-public-investments-in-clean-energy-innovation/. Matthew Stepp, “Breaking Down the Federal Clean Energy Innovation Budget,” Energy Trends Insider, January 10, 2013, http://www.energytrendsinsider.com/2013/01/10/breaking-down-the-federal-clean-energy-innovation-budget/. Matthew Stepp, “Breaking Down the Federal Clean Energy Innovation Budget: Demonstration Projects,” Energy Trends Insider, January 17, 2013, http://www.energytrendsinsider.com/2013/01/17/breaking-down-the-federal-clean-energy-innovation-budget-demonstration-projects/. Matthew Stepp, “Breaking Down the Federal Clean Energy Innovation Budget: Deployment Incentives,” Energy Trends Insider, January 24, 2013, http://www.energytrendsinsider.com/2013/01/24/breaking-down-the-federal-clean-energy-innovation-budget-deployment-incentives/. Matthew Stepp, “Breaking Down the Federal Clean Energy Innovation Budget: Manufacturing Investments,” Energy Trends Insider, February 7, 2013, http://www.energytrendsinsider.com/2013/02/07/breaking-down-the-federal-clean-energy-budget-manufacturing-investments/.

Energy Innovation Tracker, “The Energy Innovation Tracker: An Introduction,” (December 2.2010), http://energyinnovation.us/wordpress/wp-content/uploads/2010/08/EIT-Introduction.pdf.

All investment data mentioned in this report is directly available at the Energy Innovation 3.Tracker (v01232013), http://www.energyinnovation.us.

Jewel Samada, “Dear Mr. President: Time to Deal with Climate Change,” MIT Tech Review, 4.January 2, 2013, http://www.technologyreview.com/featuredstory/508841/dear-mr-president-time-to-deal-with-climate-change/.

Charles Weiss and William Bonvillian, Structuring an Energy Technology Revolution. Cambridge, 5.Mass.: MIT Press, 2009.

Megan Nicholson, “Role of Government in Energy Innovation: Boeing’s ecoDemonstrator 6.Project ‘Takes Off,’” Energy Innovation Tracker, September 19, 2012, http://energyinnovation.us/2012/09/role-of-government-in-energy-innovation-boeings-ecodemonstrator-project-takes-off/.

Matthew Hourihan and Matthew Stepp, A Model for Innovation: ARPA-E Merits Full Funding, 7.(Information Technology and Innovation Foundation, July 2011), http://www.itif.org/publications/model-innovation-arpa-e-merits-full-funding.

For more discussion on the definition of ‘demonstration,’ see: Ambuj Sagar and Kelly Sims 8.Gallagher, “Energy Technology Demonstration and Deployment,” Belfer Center for Science & International Affairs, JFK School of Government, Harvard University, December 2004, http://belfercenter.hks.harvard.edu/publication/2596/energy_technology_demonstration_and_deployment.html.

Megan Nicholson, “Army’s Green Warrior Convoy Emphasizes DOD’s Role in Energy 9.Innovation,” Energy Innovation Tracker, May 15, 2012, http://energyinnovation.us/2012/05/armys-green-warrior-convoy-emphasizes-dods-role-in-energy-innovation/.

Ambuj Sagar and Kelly Sims Gallagher, “Energy Technology Demonstration and Deployment,” 10.Belfer Center for Science & International Affairs, JFK School of Government, Harvard

ENERGY INNOVATION TRACKER MARCH 2013

22

University, December 2004, http://belfercenter.hks.harvard.edu/publication/2596/energy_technology_demonstration_and_deployment.html.

Megan Nicholson, “Tracker Public Clean Energy Innovation Investments: DOI’s New Energy 11.Frontier,” Energy Innovation Tracker, March 6, 2012, http://energyinnovation.us/2012/03/tracking-public-clean-energy-innovation-investments-dois-new-energy-frontier/.

Megan Nicholson and Matthew Stepp, Lean, Mean, and Clean II: Assessing DOD Investments in 12.Clean Energy Innovation, (Information Technology and Innovation Foundation, October 2012), http://www2.itif.org/2012-lean-mean-clean-dod-energy.pdf.

Robert Atkinson, “Clean Technology Manufacturing Competitiveness: The Role of Tax 13.Incentives,” before the Senate Finance Committee; Subcommittee on Energy, Natural Resources, and Infrastructure, May 20, 2010, http://www.itif.org/files/2010-testimony-clean-tech-tax-credits.pdf.

A deep dive into energy R&D is not included in this report because the Tracker has released 14.previous reports on this subject. For more information on R&D-specific trends, please see: Energy Innovation Tracker, “United States Energy Innovation Investments: Trends Analysis,” (December 2010), http://energyinnovation.us/wordpress/wp-content/uploads/2010/12/EIT-TrendsAnalysis.pdf.

Jesse Jenkins and Sara Mansur, Bridging the Clean Energy Valleys of Death, (Breakthrough 15.Institute, November 2011), http://thebreakthrough.org/archive/bridging_the_clean_energy_vall.

Loan guarantees are counted in this analysis by project in the fiscal year of the date of agreement, 16.as opposed to counting them by the fiscal year in which the subsidy cost of the loans was appropriated.

Subsidy costs for the main DOE loan programs are as follows: the Advanced Technology Vehicle 17.Manufacturing Loan Program was appropriated $7.5 billion in 2009 as a subsidy cost for several projects proposed to strengthen the advanced vehicle manufacturing sector in the United States; the Innovative Technologies Loan Guarantee Program, Section 1703 was appropriated $169 million in FY2012 to cover subsidy costs of loans for major energy projects, and the Innovative Technologies Loan Guarantee Program, Section 1705 was appropriated $4 billion to cover subsidy costs to loans made through the American Recovery and Reinvestment Act.

For more discussion of why some technologies fail in the development stage, see these pieces: 18.Matthew Stepp, “A123, Solyndra, and EV Battery Innovation,” Innovation Files, October 17, 2012, http://www.innovationfiles.org/a123-solyndra-and-ev-battery-innovation/; Matthew Stepp and Matthew Hourihan, “Energy Innovation: If You Don’t Occasionally Fail, You’re Doing It Wrong,” Innovation Files, September 1, 2011, http://www.innovationfiles.org/energy-innovation-if-you-don%E2%80%99t-occasionally-fail-you%E2%80%99re-doing-it-wrong/.

For a review of this policy debate, see: Matthew Stepp, “A Note to Joe Romm and Tom 19.Friedman: Sorry, We Need an RD&D, RD&D, RD&D, RD&D, Deploy Clean Energy Strategy,” Innovation Files, March 22, 2012, http://www.innovationfiles.org/a-note-to-joe-romm-and-tom-friedman-sorry-we-need-an-rdd-rdd-deploy-rdd-rdd-deploy-clean-energy-strategy/.

Jesse Jenkins, Mark Muro, Ted Nordhaus, Michael Shellenberger, Letha Tawney, and Alex 20.Trembath, Beyond Boom and Bust: Putting Clean Tech on a Path to Subsidy Independence, (Breakthrough Institute, Brookings Institute, and World Resources Institute, April 2012), http://www.thebreakthrough.org/blog/Beyond_Boom_and_Bust.pdf.

Stephen Ezell and Robert Atkinson, The Case for a National Manufacturing Strategy, (Information 21.Technology and Innovation Foundation, April 2011), http://www.itif.org/publications/case-national-manufacturing-strategy.

ENERGY INNOVATION TRACKER MARCH 2013

23

David Hart, Stephen Ezell, and Robert Atkinson. Why America Needs a National Network for 22.

Manufacturing Innovation, (Information Technology and Innovation Foundation, December 2012) http://www.itif.org/publications/why-america-needs-national-network-manufacturing-innovation.

ENERGY INNOVATION TRACKER MARCH 2013

About

The Energy Innovation Tracker (EIT) is a comprehensive database that catalogues federal energy innovation spending from FY2009 to FY2012 (inclusive of the American Recovery and Reinvestment Act spending) across nine federal agencies. Through a publicly available website and database, EIT allows the public to quickly access query, segment, and filter federal energy innovation programs and download detailed sets of program line-items to facilitate a variety of

analysis and in-depth assessments of federal research efforts. The project is run by the Information Technology and Innovation Foundation (ITIF).

The Information Technology and Innovation Foundation (ITIF) is a Washington, D.C.-based think tank at the cutting edge of designing innovation strategies and technology policies to create economic opportunities and improve quality of life in the United States and around the world. Founded in 2006, ITIF is a 501(c)(3) nonprofit, non-partisan organization that documents the beneficial role technology plays in our lives and provides pragmatic ideas for improving technology-driven productivity, boosting competitiveness, and meeting today’s global challenges through innovation.