bpz5b/bpg5a/bpw5a practical auditing unit i … · methods of internal check includes...

TRANSCRIPT

BPZ5B/BPG5A/BPW5A

PRACTICAL AUDITING

UNIT I - V

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING 2

UNIT I – SYLLABUS

Meaning of Auditing

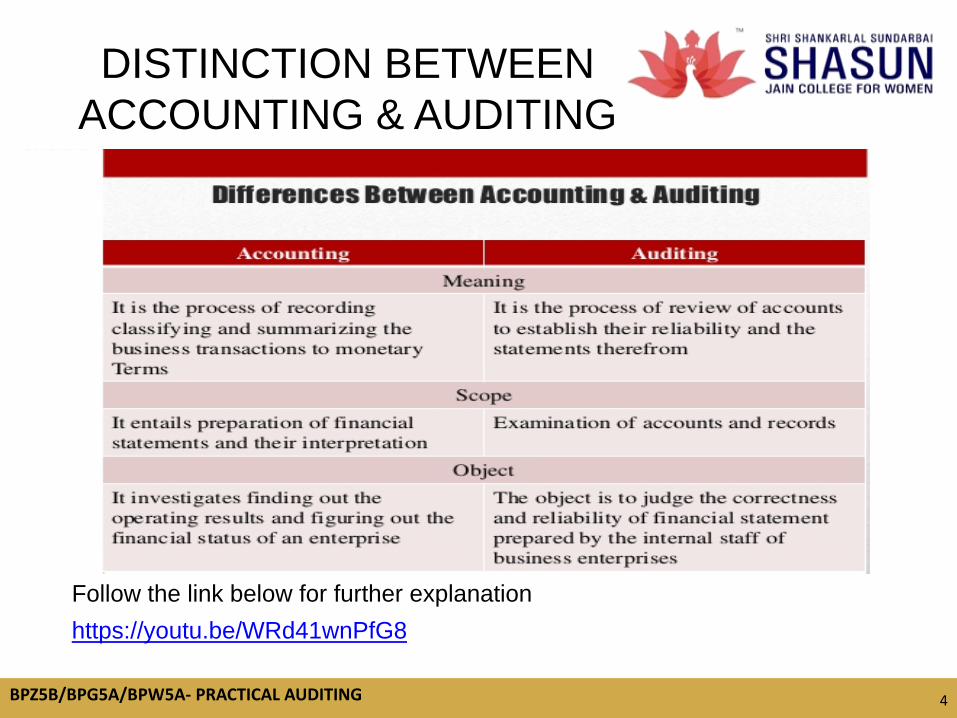

Distinction between Auditing & Accounting

Objectives of Auditing

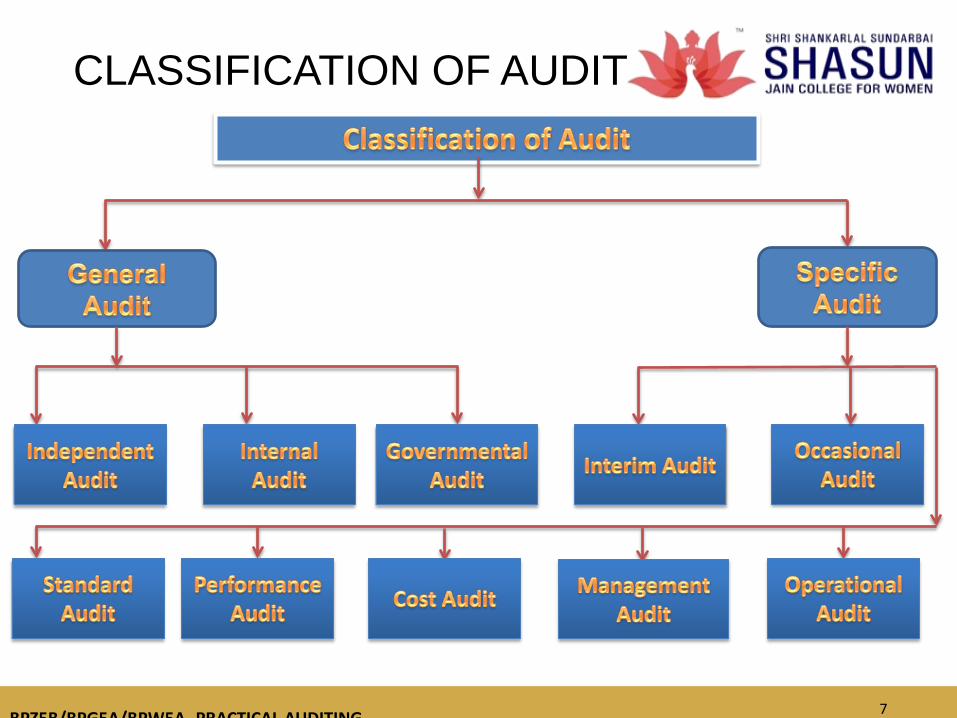

Classification of Audit

Audit Planning

Audit Programme

Audit Notebook

Audit Working Papers

Internal Control

Internal Check

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING 3

AUDITING

The Institute of Chartered Accountants of India describes auditing as

“the independent examination of financial information of any entity,

whether profit oriented or not, and irrespective of its size or legal form,

when such examination is conducted with a view to expressing an

opinion thereon”.

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

4

https://youtu.be/WRd41wnPfG8

Follow the link below for further explanation

DISTINCTION BETWEEN ACCOUNTING & AUDITING

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

5

AUDIT FRAMEWORK

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

6

I) Main Objective : Expression of expert opinion.

II) Secondary Objectives :

• Detection and prevention of errors - Error of omission, Error of

Commission, Error of Principle, Errors of Duplication

• Detection and prevention of frauds- Embezzlement of cash,

Misappropriation of goods, Fraudulent of manipulation of accounts.

III) Specific Objectives:

• Review of Operations

• Performance Management Policy

• Cost records

OBJECTIVES OF AUDITING

TM

BPZ5B/BPG5A/BPW5A PRACTICAL AUDITING

CLASSIFICATION OF AUDIT

7

TM

8

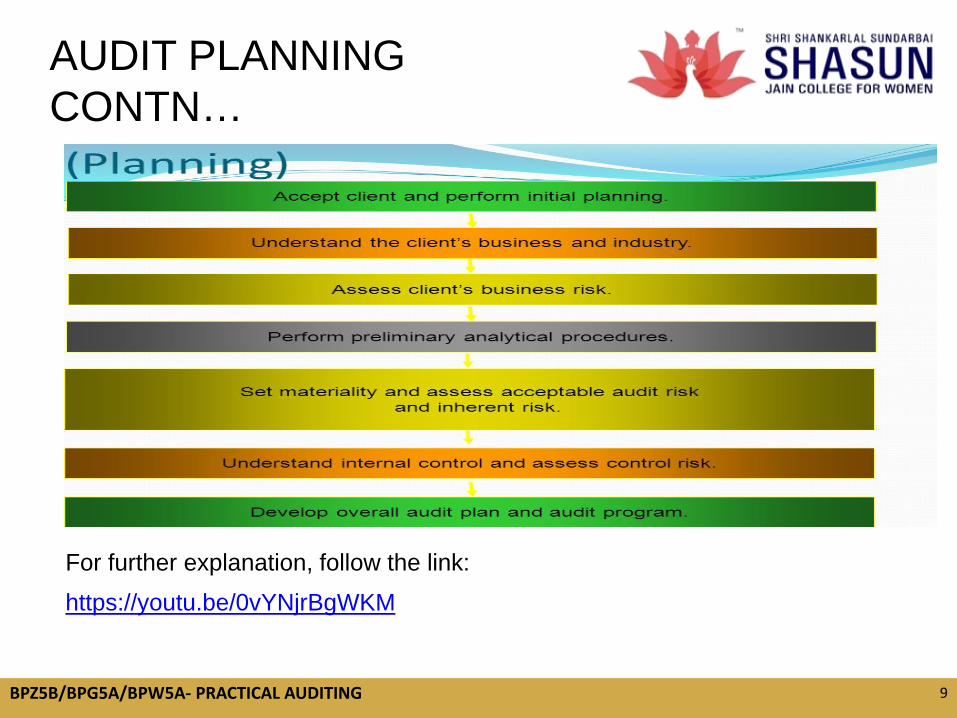

Audit Planning is a planned performance, meaningful and well-covered

reporting and with a sense of time, cost and above all quality.

Auditing and Assurance Standard (AAS1) states that the auditor should

plan his work to enable him to conduct an effective audit in an efficient

manner.

Benefits of Audit Planning:

Appropriate attention to important areas.

Potential problems promptly identified.

Time bound progress and completion

Man power utilization.

Coordination of work of auditor and experts.

AUDIT PLANNING

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

9

AUDIT PLANNING CONTN…

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

For further explanation, follow the link:

https://youtu.be/0vYNjrBgWKM

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

10

AUDIT PROGRAMME

Audit Programme is a plan of action translated into specific areas of

audit works with check list of actions to be performed.

Entails specific listing of audit area components in terms of related

procedures.

Specifies the time or date by which the work should have been

completed.

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

11

A written record of queries made, replies received thereto,

correspondence entered into etc. Audit notebook is maintained by the audit clerk.

Also known as Audit Memoranda.

Great help to the auditor for preparing audit report.

Examples of notes made in the audit notebook:

28-8-2016 Receipt for Rs.10000 paid to Messrs. XYZ vide C.B.Folio

69, not available.

2-2-2017 Receipt for Rs.25000 paid to Messrs. XYZ, seen and

cancelled.

AUDIT NOTEBOOK

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

12

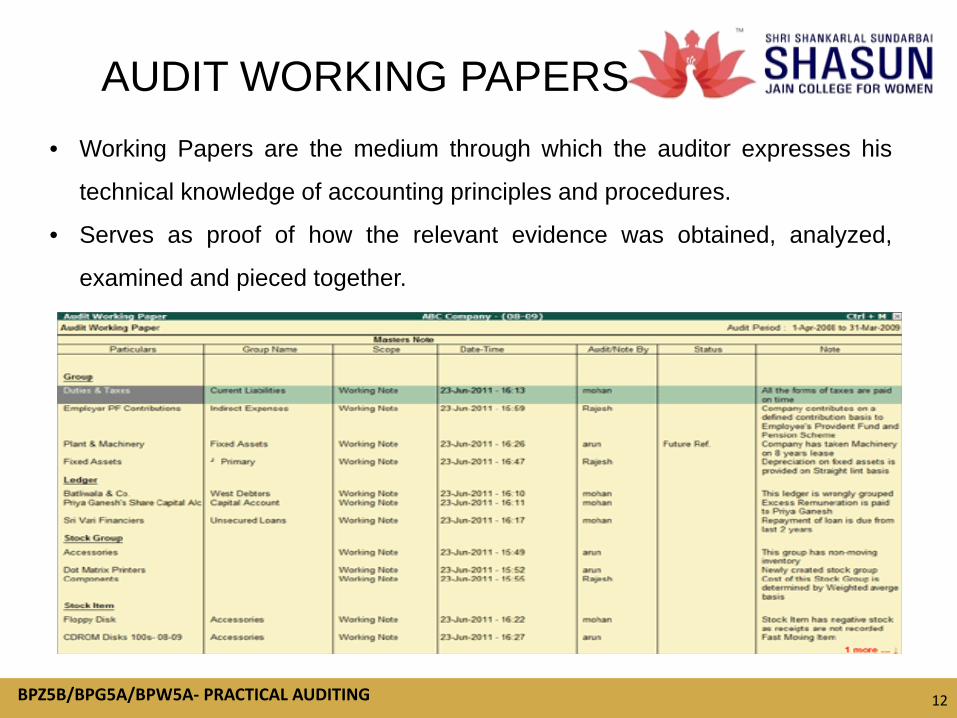

AUDIT WORKING PAPERS • Working Papers are the medium through which the auditor expresses his

technical knowledge of accounting principles and procedures.

• Serves as proof of how the relevant evidence was obtained, analyzed,

examined and pieced together.

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

13

OBJECTIVES OF WORKING PAPER • Planning, organisation and review of audit work.

• Support for Auditor’s opinion.

• Basis for review and revision of internal control.

• Basis for evaluation and training of audit staff.

• Division of Labour.

• Use as permanent record.

• Bridge between original transactions and financial statements.

• Basis for further work.

Contn…..

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

14

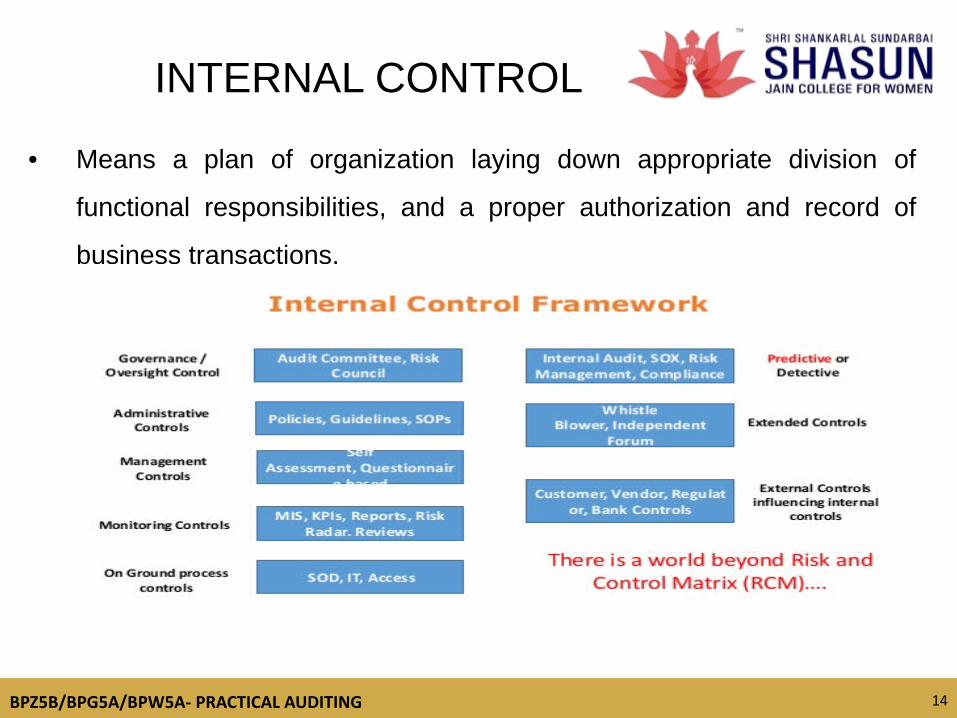

• Means a plan of organization laying down appropriate division of

functional responsibilities, and a proper authorization and record of

business transactions.

INTERNAL CONTROL

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

15

TECHNIQUES OF INTERNAL CONTROL SYSTEM

NARRATIVE RECORD – Complete written description of the internal control system, employed in a small business. QUESTIONNAIRE METHOD – Contains a set of questions, the answers to which provide an insight into the internal control system.

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

16

FLOWCHART METHOD- Internal control system is depicted with the help of symbols, figures and code references with minimum narration.

Contn……

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

17

Arrangement of book-keeping routine to prevent errors and frauds.

A continuous internal audit carried on by the staff itself.

Methods of internal check includes Self-balancing ledger system, time-

recording clocks regarding wages. OBJECTIVES Proper division of work.

Fixation of responsibility.

Minimisation of errors and frauds.

Early detection of errors and frauds.

Reliability of books of accounts.

Early preparation of final accounts.

INTERNAL CHECK

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

UNIT II – SYLLABUS

Vouching

Trading Transactions

Vouching of Cash receipts & Payments

Vouching of Outstanding Assets and Liabilities

Verification & its process

Valuation of assets and liabilities

Distinction between assets & liabilities

18

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

Meaning : Vouching is an examination of the ledger entries in which the

entries are supported by documentary evidence.

It Includes an inquiry into the genuineness of the transaction, accuracy of

the amount involved and proper posting in the relevant accounts.

VOUCHING

19

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

20

Vouching of Trading transactions should be preceded by a thorough

evaluation of the existing system of internal check and control.

Involves careful enquiry into the policies and procedures relating to

authorisation as to:

Ordering of goods.

Receipts and inspection of goods.

Return of defective goods.

Processing of invoices for payment.

VOUCHING OF TRADING TRANSACTIONS

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

21

Purchase Transactions

Invoices should be addressed to the client.

Date and amount of invoice should be checked with its record in

Purchase book.

Invoices should be signed by the Authorised clerk

All purchases in the preceding weeks should be recorded in the

Purchase book at the end of relevant financial periods.

Castings and carry forwards in the purchase book should be carefully

checked.

After an invoice has been vouched, it should be “cancelled”.

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

22

Entries in the Sales Day Book should be checked with the duplicates of

sales invoices and originals of customers orders.

Entries in the Sales Day book should be checked with postings to Sales

Ledger.

Must ascertain whether goods represented as sales in the books of

account have been actually sold.

Amount of Sales tax should be shown in separate column in the Sales

Day book. OTHER TRADING BOOKS The auditor should check the:

Consignment Book, Bills Receivable book, Bills Payable book, Purchase

Ledger and Sales ledger.

SALES TRANSACTIONS

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

23

CASH SALES Cash memos are to be printed.

It should be in quadruplicate.

COLLECTION FROM DEBTORS

Copies of sales invoice.

Settlement of accounts received from debtors.

RENT RECEIPTS

Rent agreements.

Counterfoils of rent receipts.

INCOME FROM INVESTMENTS

Dividend/interest warrants received.

Certificates showing purchase of shares.

Vouching of Cash Receipts

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

24

LOAN RECEIVED The loan agreement.

The sanction ticket issued by the lender.

BILLS RECEIVABLE

Verify the bills receivable book, cash book and bank statement.

Verify if any bills are dishonored.

SALE OF FIXED ASSET

Fixed asset register.

Sale Agreement.

ROYALITIES RECEIVED

Verify the due date of royalty, rate of royalty etc.

Verify the calculation of recoupment of short working.

Contn…..

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

25

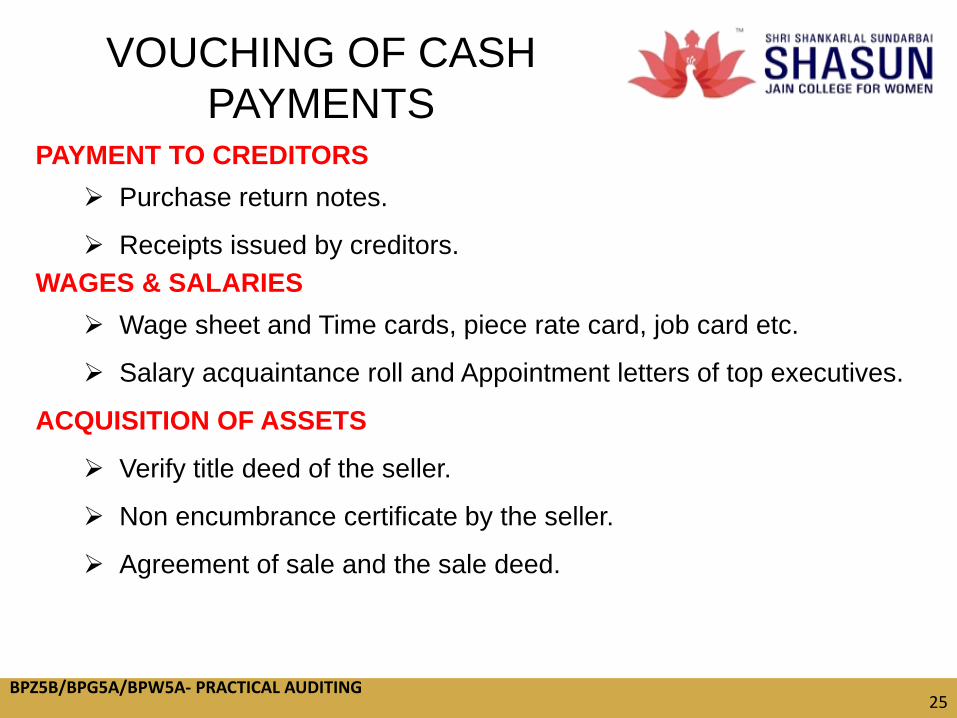

PAYMENT TO CREDITORS Purchase return notes.

Receipts issued by creditors. WAGES & SALARIES

Wage sheet and Time cards, piece rate card, job card etc.

Salary acquaintance roll and Appointment letters of top executives.

ACQUISITION OF ASSETS

Verify title deed of the seller.

Non encumbrance certificate by the seller.

Agreement of sale and the sale deed.

VOUCHING OF CASH PAYMENTS

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

26

PAYMENT OF INCOME TAX Verify the statement prepared to calculate the advance tax.

Ensure that the advance tax is paid within due date.

ASSETS ACQUIRED UNDER HIRE PURCHASE

Description of assets.

Cost of the assets.

Hire purchase charges.

ADVERTISEMENT EXPENSE

Verify the vouchers relating to advertisement expenses.

Copy the advertisement should be enclosed with the payment voucher.

ACQUISITION OF ASSETS

Verify title deed of the seller.

Agreement of sale and the sale deed.

Contn…

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

27

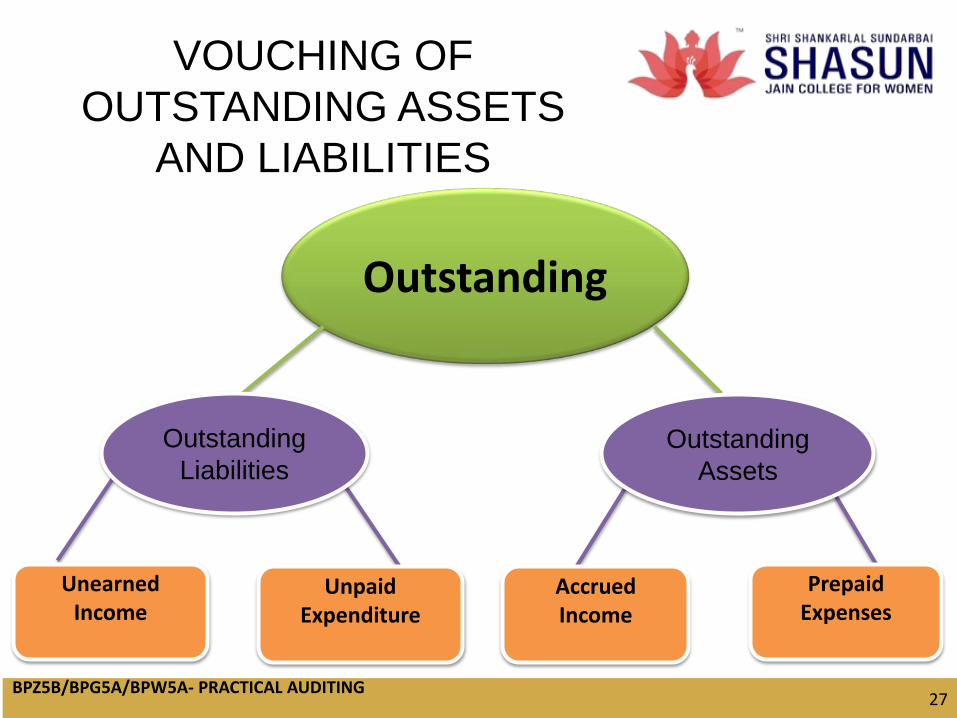

VOUCHING OF OUTSTANDING ASSETS

AND LIABILITIES

Outstanding

Outstanding Liabilities

Outstanding Assets

Unearned Income

Unpaid Expenditure

Accrued Income

Prepaid Expenses

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

28

I) OUTSTANDING LIABILITIES: UNPAID EXPENDITURE Employee stock options and deferred compensation plans.

Contingent liabilities.

UNEARNED INCOME

Subscriptions.

Advance in respect of sale of goods/ services.

II) OUTSTANDING ASSETS:

PREPAID EXPENSES

Prepaid advances or commission to employees.

Deferred revenue expenditure.

ACCRUED INCOME Interest and dividend.

Contn….

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

29

Means “providing the truth” or “confirmation”.

Involves the following points: Comparing the ledger accounts with the balance sheet. Verifying the existence of assets on the date of balance sheet. Satisfying that they are free from any charge. Verifying their proper value.

VERIFICATION

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

30

LEASEHOLD LAND Leasehold land is subject to diminution in value.

Depreciation should be provided (write off total cost).

BUILDING

Building should always be valued at cost less depreciation at a

reasonable rate.

Depreciation to be provided even building is not under use.

PLANT & MACHINERY

Plant & machinery is valued at cost less depreciation at reasonable rate.

Necessary adjustments for additions or sales should be appropriately

made.

VALUATION OF ASSETS

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

31

GOODWILL Goodwill to be valued by the specified method.

Calculation of normal profit.

INVENTORIES Value Raw materials, Finished goods and Goods on consignment. VERIFICATION OF LIABILITIES

TRADE CREDITORS Verify the purchase ledger.

Verify creditor’s schedule of the management with the statement of accounts. DEBENTURES Verify debenture trust deed & debenture a/c.

Verify debenture redemption reserve a/c and the authorisation in the Articles

of Association.

Contn…

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

32

INCOME RECEIVED IN ADVANCE Verify the schedule of incomes received in advance and confirm these are

fully disclosed in the Balance sheet.

According to Sec 418, a company is required to make the payment of the

PF dues by the due date i.e within 15 days from the date of deduction from

salaries. CONTINGENT LIABILITY Inspection of minutes book of meetings of the board of directors.

Inquiry and discussions with the staff of the company.

Contn….

https://youtu.be/XrnbqfrZHYI

For further explanation, refer the link below

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

33

DISTINCTION BETWEEN VERIFICATION & VALUATION

TM

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

UNIT III – SYLLABUS

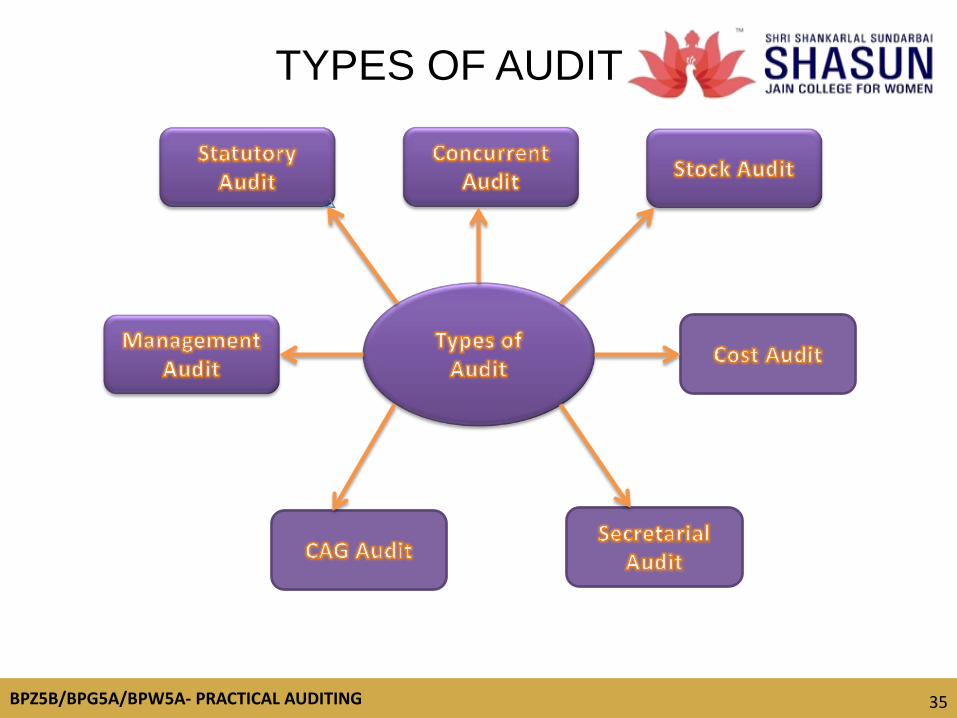

Types of Audit - Statutory Audit, Concurrent Audit, Stock Audit,

Cost Audit, Secretarial Audit, CAG Audit, Management Audit

Accounting Standards

Standards on Auditing

Standards on Internal Audit

Penal Provisions

Role of National Finance Reporting Authority

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

35

TYPES OF AUDIT

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

36

I. STATUTORY AUDIT – Determines whether an organization is providing

a fair and accurate representation of its financial position by examining

book keeping records.

II. CONCURRENT AUDIT – Examination of financial transactions at the

time of happening or parallel with the transaction.

III. STOCK AUDIT - Refers to the physical verification of the inventory.

Involves the counting of physical stock presenting the specified premises

and verifying the same with computed stock maintained by the company.

IV. COST AUDIT – Verification of cost accounts and check on the adherence

to cost accounting plan.

TYPES OF AUDIT

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

37

V. SECRETARIAL AUDIT – To Check compliance of various legislations

including the Companies Act and other corporate and economic laws

applicable to the company.

VI. CAG AUDIT - Audit of government accounts (including the accounts of

the State Governments) in India. Involves auditing all expenditure and

revenues from the Consolidated Fund of the Union or State

Governments, whether incurred within India or outside India.

VII. MANAGEMENT AUDIT – Assessment of methods and policies of an

organization’s management in strategic planning and employee

improvement.

TYPES OF AUDIT -Contn….

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

38

Also known as Indian Accounting Standard (Ind-AS).

Adopted by Companies in India and issued under the supervision and

control of Accounting Standard Board (ASB).

AS are numbered in the same way as the corresponding International

Financial Reporting Standards (IFRS).

Companies shall follow Ind AS voluntarily or mandatorily.

Mandatory Applicability on or after 1st April 2017:

Every Listed company.

Unlisted companies with Net worth of not less than Rs.2.5 billion

and not more than Rs.5 billion.

ACCOUNTING STANDARDS

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

39

Contn….

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

40

Contn….

https://youtu.be/Y1BV8iP_PDk For further details, follow the link:

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

41

Issued by Auditing Practices Committee formed by ICAI in 1982.

Standards carried the numbers SAP-1, SAP-2 and so on.

Renamed as Auditing and Assurance Standards Board (ASAB).

Also numbered as AAS-1, AAS-2 and so on.

For further explanation, follow the link:

https://www.icai.org/new_post.html?post_id=450&c_id=141

STANDARDS ON AUDITING

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

42

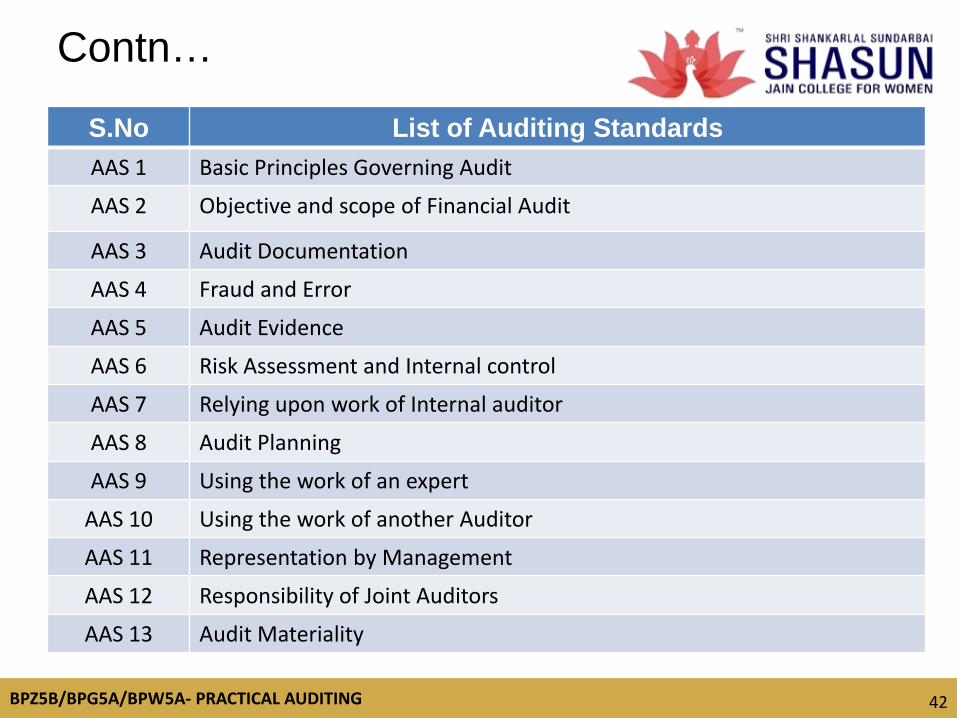

Contn…

S.No List of Auditing Standards AAS 1 Basic Principles Governing Audit

AAS 2 Objective and scope of Financial Audit

AAS 3 Audit Documentation

AAS 4 Fraud and Error

AAS 5 Audit Evidence

AAS 6 Risk Assessment and Internal control

AAS 7 Relying upon work of Internal auditor

AAS 8 Audit Planning

AAS 9 Using the work of an expert

AAS 10 Using the work of another Auditor

AAS 11 Representation by Management

AAS 12 Responsibility of Joint Auditors

AAS 13 Audit Materiality

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

43

Contn… S.No List of Accounting Standards

AAS 14 Analytical Procedure

AAS 15 Audit Sampling

AAS 16 Going Concern

AAS 17 Quality Control for Audit work

AAS 18 Auditing of Accounting Estimates

AAS 19 Subsequent Events

AAS 20 Knowledge of the Business

AAS 21 Consideration of the Laws and Regulations in an Audit

AAS 22 Initial Engagements

AAS 23 Related parties

AAS 24 Audit Considerations relating to Entities using Service Organisations

AAS 25 Comparatives

AAS 26 Terms of Audit Engagement

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

44

content: font size 20

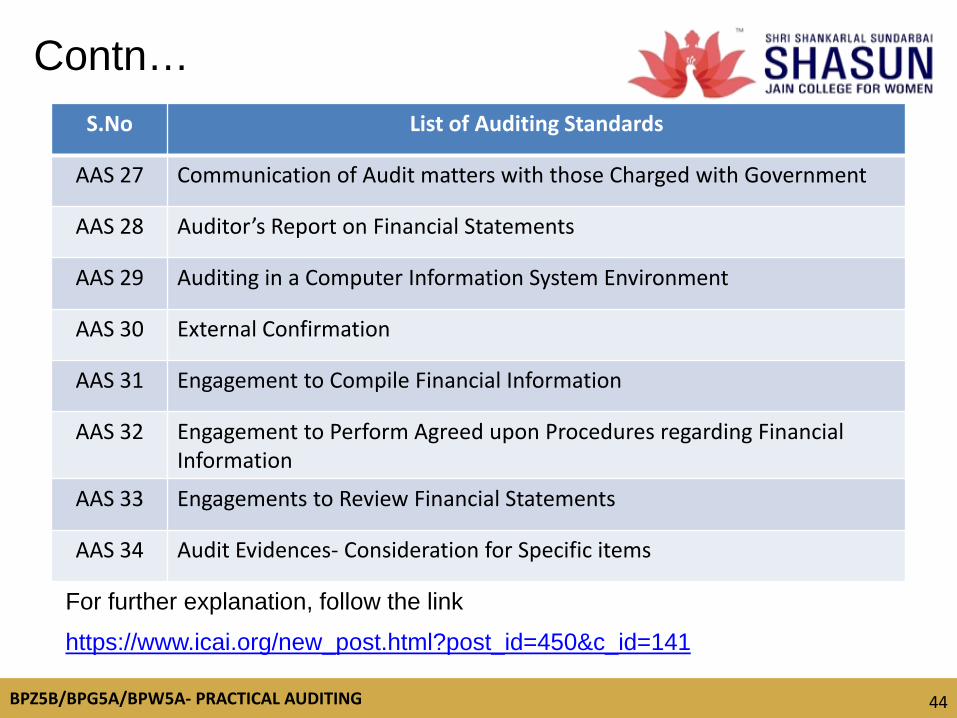

Contn… S.No List of Auditing Standards

AAS 27 Communication of Audit matters with those Charged with Government

AAS 28 Auditor’s Report on Financial Statements

AAS 29 Auditing in a Computer Information System Environment

AAS 30 External Confirmation

AAS 31 Engagement to Compile Financial Information

AAS 32 Engagement to Perform Agreed upon Procedures regarding Financial Information

AAS 33 Engagements to Review Financial Statements

AAS 34 Audit Evidences- Consideration for Specific items

For further explanation, follow the link

https://www.icai.org/new_post.html?post_id=450&c_id=141

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

45

STANDARDS OF INTERNAL AUDIT

S.No List of Standards

SIA 1 Planning an Internal Audit

SIA 2 Basic Principles governing Internal Audit

SIA 3 Documentation

SIA 4 Reporting

SIA 5 Sampling

SIA 6 Analytical Procedures

SIA 7 Quality Assurance in Internal Audit

SIA 8 Terms of Internal Audit Engagement

SIA 9 Communication with Management

SIA 10 Internal Audit Evidence

SIA 11 Consideration of Fraud in an Internal Audit

SIA 12 Internal Control Evaluation

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

46

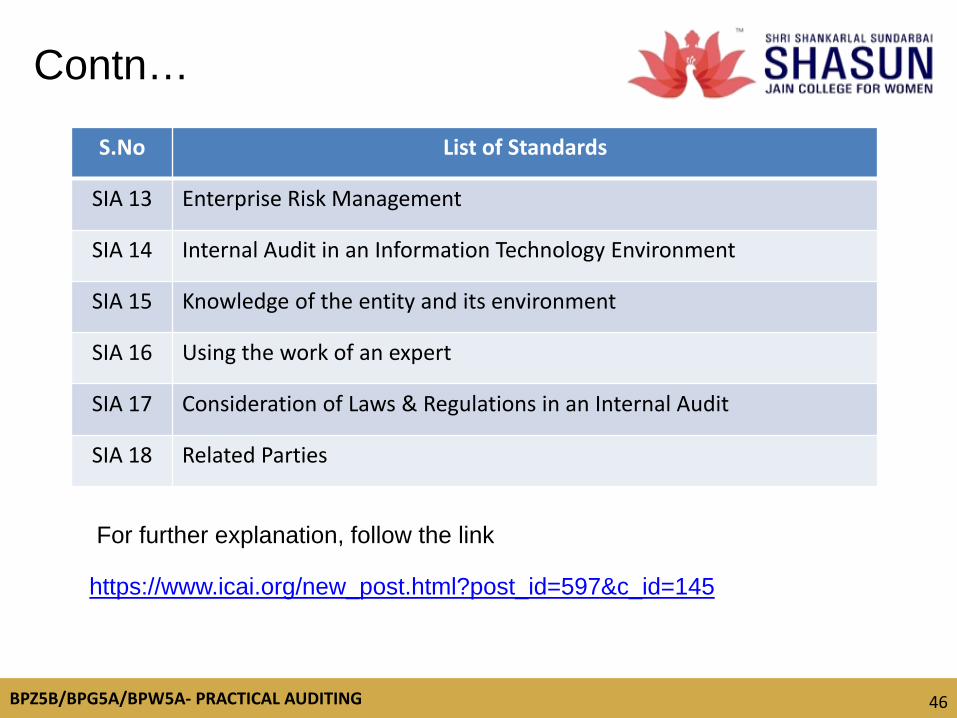

Contn…

S.No List of Standards

SIA 13 Enterprise Risk Management

SIA 14 Internal Audit in an Information Technology Environment

SIA 15 Knowledge of the entity and its environment

SIA 16 Using the work of an expert

SIA 17 Consideration of Laws & Regulations in an Internal Audit

SIA 18 Related Parties

For further explanation, follow the link

https://www.icai.org/new_post.html?post_id=597&c_id=145

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

47

I) Under Law of Agency – Failing to comply with Provisions, the auditor is

liable to a fine upto Rs.1000 provided the default is wilfull.

II) Under Statute (Misfeasance):

Under Companies Act,1956 – The auditor shall be punishable with

imprisonment for a term which may extend to seven years and shall

also be liable to fine for any breach of duty.

Under Indian Penal Code – If the auditor signs any certificate which is

false, he shall be punishable with an imprisonment for a period of two

years and a fine.

PENAL PROVISIONS

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

48

Contn…

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

49

For further explanation, follow the link below www.taxmann.com/.../NFRA%20Draft%20National%20Financial%20Reporting%20A...

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

UNIT IV- SYLLABUS

Appointment, procedure, eligibility and qualifications of auditors

Powers and Duties of auditor

Rotation and Removal of auditor

Resignation of auditor

Remuneration of auditors

Audit report preparation and presentation

Auditor's responsibility and liabilities towards shareholders board

and Audit committee

Restriction on other service

50

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

Section Reference

Description

Sec 224 Appointment and remuneration of Auditors Sec 224 A Appointment of auditor by special resolution Sec 225 Removal, resignation of auditor and giving of special notice

Sec 226 Eligibility, Qualifications and disqualifications of auditors

Sec 227 Powers and Duties of auditors Sec 228 Audit of accounts of any branch office of a company Sec 229 Signature of audit report Sec 230 Reading & Inspection of auditors report Sec 231 Rights of auditor to attend general meeting Sec 232 Penalty for non compliance with sec 225 to 231

51

LIST OF SECTIONS UNDER COMPANY LAW

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

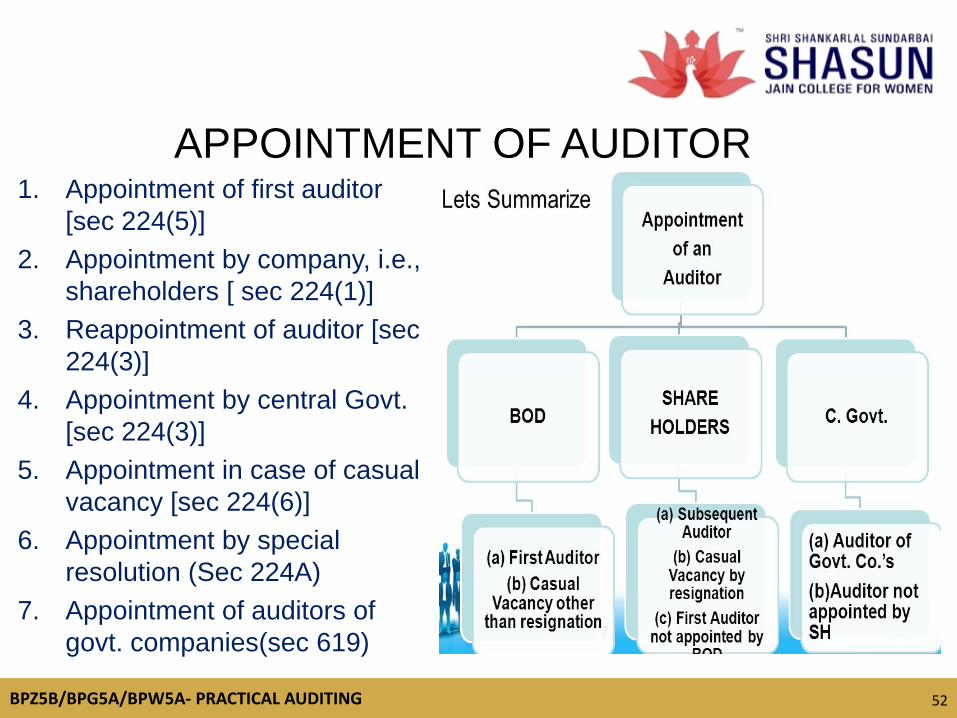

APPOINTMENT OF AUDITOR 1. Appointment of first auditor

[sec 224(5)] 2. Appointment by company, i.e.,

shareholders [ sec 224(1)] 3. Reappointment of auditor [sec

224(3)] 4. Appointment by central Govt.

[sec 224(3)] 5. Appointment in case of casual

vacancy [sec 224(6)] 6. Appointment by special

resolution (Sec 224A) 7. Appointment of auditors of

govt. companies(sec 619)

52

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

ELIGIBILITY & QUALIFICATION OF AN AUDITOR SEC 226

1. Practicing Chartered Accountants with his individual capacity

2. Deemed to be in practice 3. Holding certificate of practice & a partner of

charted accountant firm. 4. Offers to performs the services involving the

auditing or verifications of financial institution books, records , accounts , verification or certification of financial accounting

https://vakilsearch.com/advice/role-of-auditor-company/

53

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

54

DISQUALIFICATION OF AUDITORS SEC 226(3),(4) AND (5)

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

55

DUTIES/RESPONSIBILITIES OF COMPANY AUDITORS

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

56

DUTIES OF COMPANY AUDITORS 1.Statutory duties : Certifying report as to vital matters, Reporting the

members , Enquiring into specific matter, Assisting investigation , Assistant

Public Prosecutor, Certifying directors insolvencies, Signing report in the

prospectus, Certifying accounting standards

2.Common law: Representing client on tax matters, Offering advise in

company law matter , Conducting inter cost, Performing managerial activity

3.Professional ethics : Responsibilities, Public Interest , Standard of care,

Integrity, honesty &Engagement duties

4. General duties : Ensuring trust fullness of financial statement , Taking

reasonable care , Arriving at independent opinion , Reporting violation,

Ensuring in case of doubt

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

57

1. Right of access to books, accounts and vouchers (sec 227(1))

2. Right to obtain information and explanations (sec 227(1))

3. Right to receive notice and to attend general meeting(sec 231)

4. Right to indemnified

5. Right to report to members

6. Right to sign audit report

7. Right to visit branches

8. Right to have legal and technical advice

9. Right to receive remuneration

10. Right of lien

RIGHTS AND POWERS OF AUDITOR

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

58

REMOVAL OF AUDITOR

https://www.icsi.edu/portals/0/AUDIT%20AND%20AUDITORS.pdf

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

59

RESIGNATION OF AUDITOR

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

60

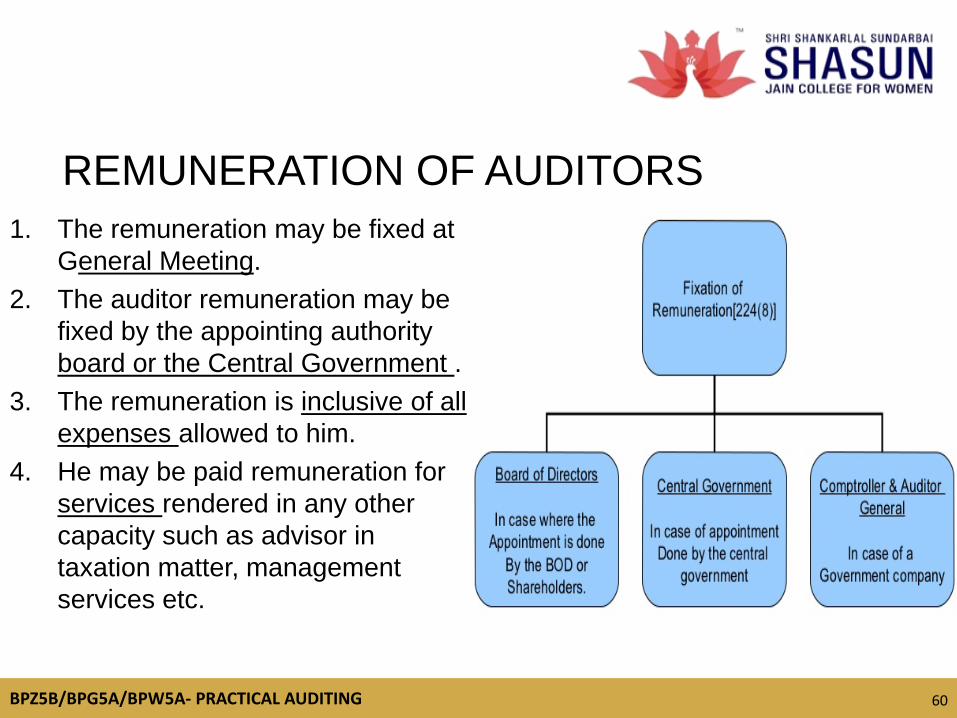

REMUNERATION OF AUDITORS 1. The remuneration may be fixed at

General Meeting. 2. The auditor remuneration may be

fixed by the appointing authority board or the Central Government .

3. The remuneration is inclusive of all expenses allowed to him.

4. He may be paid remuneration for services rendered in any other capacity such as advisor in taxation matter, management services etc.

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

61

AUDIT REPORT PREPARATION Basic elements of the Report 1. Title 2. Addressee 3. Identification of financial statements 4. Reference to auditing standards and

practices 5. Opinion on the financial statements 6. Signing of Audit Report 7. Address of the Auditor 8. Dating of the report 9. Place of signature 10. Reading and inspection of auditor’s report

Types of Audit Report 1. Clean Report 2. Qualified Report 3. Disclaimer 4. Negative Report

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

62

Statutory liabilities Liabilities for misstatement in prospectus False statement in return and in the report Liability for false statement upon examination by the

official liquidator Delinquency Destruction, Alternation and Manipulation Liabilities under chartered accountant act Liabilities under special Act Banking Regulation Act 1949 Insurance Act 1956 Indian Penal Code Income Tax Act Consumer Protection Act 1986

AUDITOR'S LIABILITIES &

RESPONSIBILITIES

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

63

Civil liability on account of Misfeasance Criminal liability For misstatement in prospectus Liability penalty for false statements Failure to assist in an investigation Other liabilities Liability to third party Liability for unlawful act of the client Liability for unaudited statement Liability resulting from negligence of audit assistance Liability to Articled clerks

AUDITOR'S LIABILITIES &

RESPONSIBILITIES

CONTN…..

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

EDP Audit - Meaning

Division of auditing in EDP environment

Impact of computerization on audit approach

CAAT

Audit around with computers

Procedure of Audit under EDP system

UNIT V-SYLLABUS

64

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

65

EDP AUDIT

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

66

APPROACHES TO EDP AUDITING

Approach to EDP

Auditing

Auditing Through

the computer

Auditing Around the Computer

Auditing with the

Computer

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

67

FEATURES OF AUDITING THROUGH

COMPUTER SYSTEM

Real Time Processing

Online Data Entry

Elimination of printouts

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

68

CHARACTERISTICS OF AUDITING THROUGH

THE COMPUTER

Organizational Structure

Nature of Processing

Design and Procedural Aspects

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

69

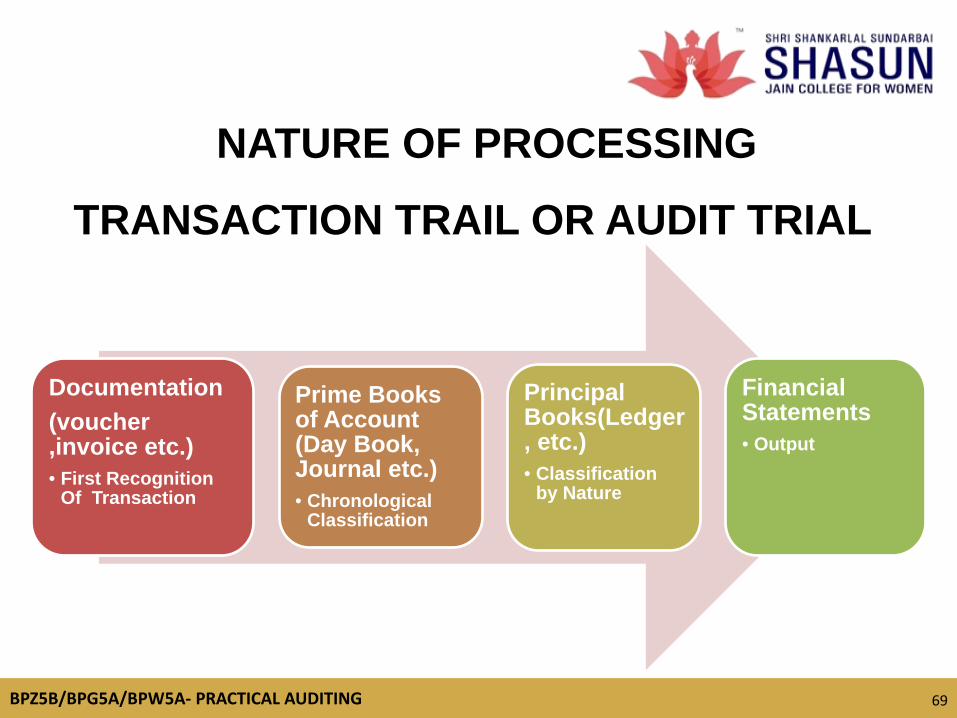

NATURE OF PROCESSING

TRANSACTION TRAIL OR AUDIT TRIAL

Documentation (voucher ,invoice etc.) • First Recognition

Of Transaction

Prime Books of Account (Day Book, Journal etc.) • Chronological

Classification

Principal Books(Ledger, etc.) • Classification

by Nature

Financial Statements • Output

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

70

INTERNAL CONTROL IS AN AUDITING

THROUGH THE ENVIRONMENT

Internal control

Accuracy

Completeness

Non-redundancy

Asset safeguarding

Existence of audit trail

Authenticity

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

71

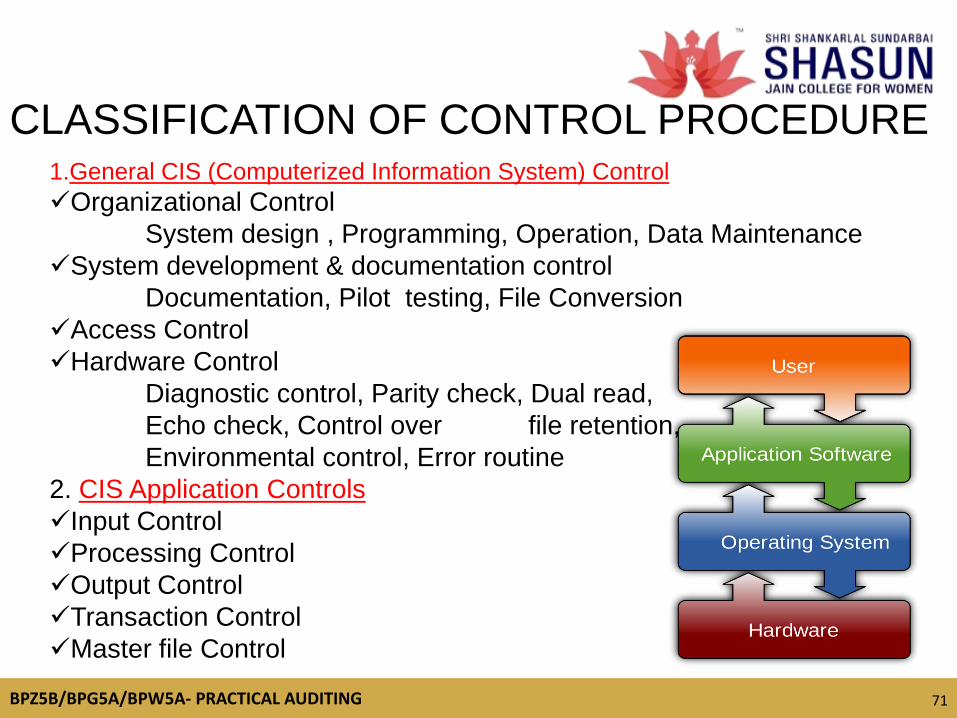

CLASSIFICATION OF CONTROL PROCEDURE 1.General CIS (Computerized Information System) Control Organizational Control System design , Programming, Operation, Data Maintenance System development & documentation control Documentation, Pilot testing, File Conversion Access Control Hardware Control Diagnostic control, Parity check, Dual read, Echo check, Control over file retention, Environmental control, Error routine 2. CIS Application Controls Input Control Processing Control Output Control Transaction Control Master file Control

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

72

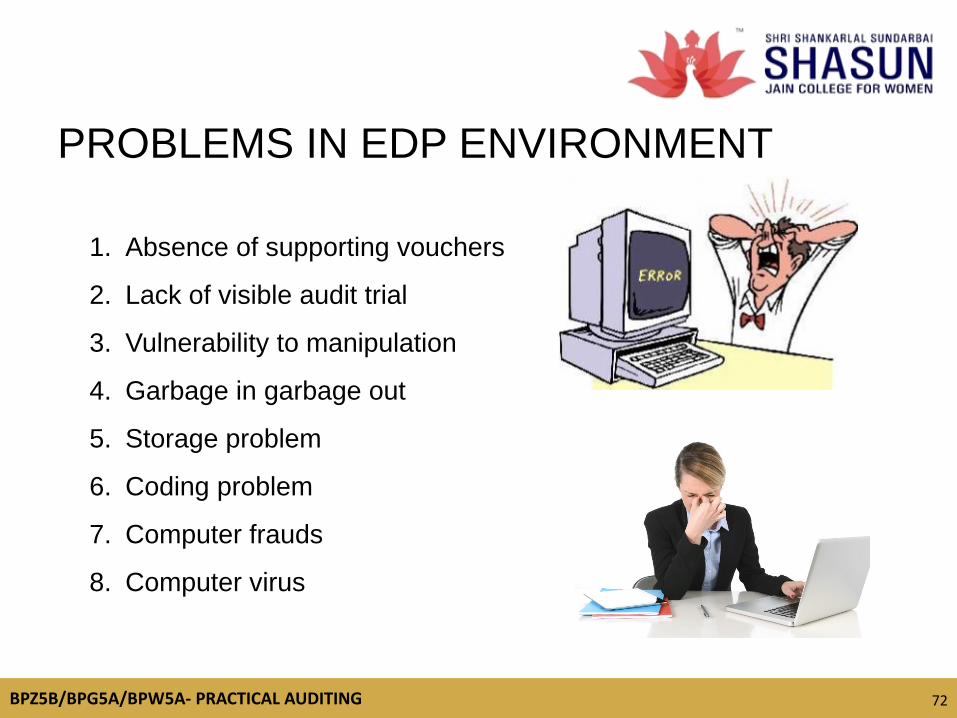

PROBLEMS IN EDP ENVIRONMENT

1. Absence of supporting vouchers

2. Lack of visible audit trial

3. Vulnerability to manipulation

4. Garbage in garbage out

5. Storage problem

6. Coding problem

7. Computer frauds

8. Computer virus

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

73

ADMINISTRATIVE CONTROL

(Operators, Files, Input) DIVISION OF RESPONSIBILITIES

1. Operator should not have access to the documents containing original data. They should not have access to clerically maintained financial records.

2. Operators are not to be authorised to alter any data. 3. Access to the computer room and to the computers should be restricted

to authorised persons only. 4. Operating instructions should be provided in a manual. 5. The work schedule should be strictly adhered to. 6. There should be atleast two operators per shift. 7. The duty timings should be frequently changed among the operators. 8. A log is to be maintained for each operator as to time and usage of

computers.

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

74

ADMINISTRATIVE CONTROL

(Operators, Files, Input)

CONTN…..

DIVISION OF RESPONSIBILITIES Only correct files should be used. No files should be used for unauthorised purposes. Access should be allowed only for authorised persons by the use of

passwords To ensure physical security, copies of important file should be stored

in a different place. Adequate reconstruction procedure should be made available to

save the corrupt files. Only corrected data is entered Data is entered only once Data is converted correctly into machine readable form.

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

75

COMPUTER ASSISTED AUDIT

TECHNIQUE

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

76

IMPACT OF COMPUTERIZATION ON

AUDIT APPROACH 1. Feasibility study 2. Size and nature 3. Planning and installation 4. Unforeseen circumstances 5. Training and exposure to employees 6. Software and hardware should be reliable 7. Flexible 8. Scope and limitations of the package 9. Organization change –Facilities, Staffing, Centralization of data and

segregation of duties 10.Methods of authorization 11.Visibility -Input data, Processing, Transaction trail

BPZ5B/BPG5A/BPW5A- PRACTICAL AUDITING

TM

77

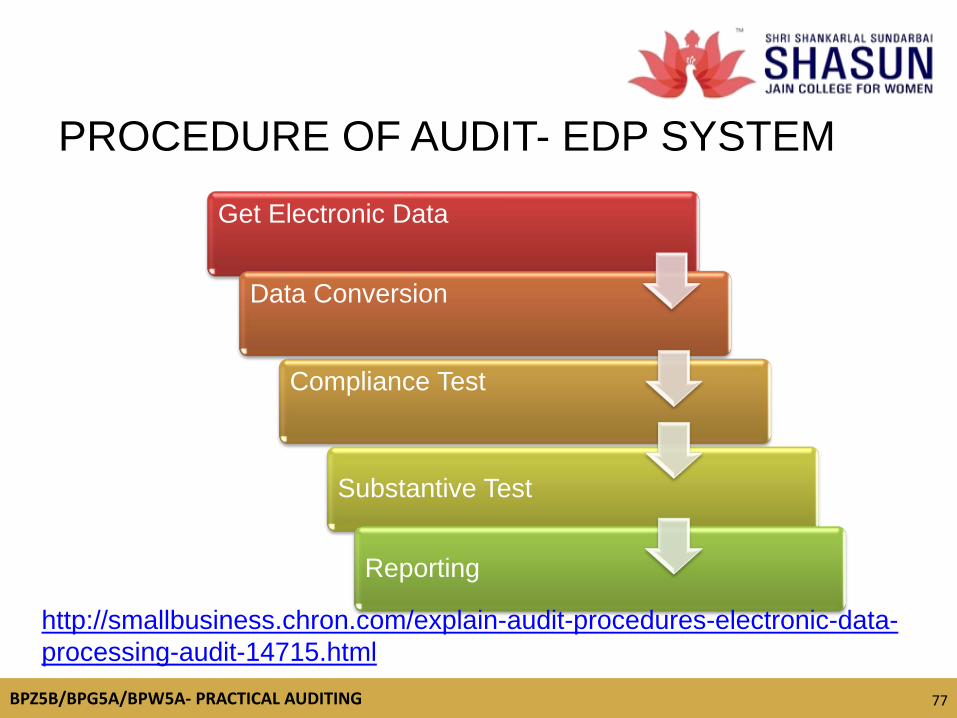

PROCEDURE OF AUDIT- EDP SYSTEM

Get Electronic Data

Data Conversion

Compliance Test

Substantive Test

Reporting

http://smallbusiness.chron.com/explain-audit-procedures-electronic-data-processing-audit-14715.html