boeing financial analysis

TRANSCRIPT

1

Performance management .................................................................................... 2

1.1. Revenue ..................................................................................................................................................... 2

1.1.1. PROFITABILITY RATIOS .................................................................................................................. 3

1.1.2. Efficiency ................................................................................................................................................. 5

1.1.3. Management Effectiveness ............................................................................................................. 6

1.2. Cost .............................................................................................................................................................. 7

1.2.1. Interest Cover Ratio ........................................................................................................................... 9

1.2.2. GEARING ................................................................................................................................................. 9

1.2.3. WACC vs. ROIC ................................................................................................................................... 10

1.2.4. Operation Cash Flow ...................................................................................................................... 10

Corporation strategy ............................................................................................ 12

1.3. Macro-‐environmental ....................................................................................................................... 12

1.3.1. Political ................................................................................................................................................ 12

1.3.2. Economic ............................................................................................................................................. 12

1.3.3. Social ..................................................................................................................................................... 13

1.3.4. Technological .................................................................................................................................... 14

1.3.5. Porter’s five forces ........................................................................................................................... 14

1.4. SWOT ........................................................................................................................................................ 17

1.4.1. Strength ............................................................................................................................................... 17

1.4.2. Weaknesses: ....................................................................................................................................... 17

1.4.3. Opportunities ..................................................................................................................................... 18

1.4.4. Threats ................................................................................................................................................. 18

Conclusion ........................................................................................................... 18

References ........................................................................................................... 19

2

Performance management

Boeing is the world’s largest aerospace company and leading manufacturer of commercial airplanes

and defense, space and security systems. Boeing’s products and tailored services include commercial

military aircraft, satellites, weapons, electronic and defense system, launch system, advanced

information and communication system, and performance-based logistical and training. The company

is organized into two business units: Boeing Commercial Airplanes and Boeing Defense, Space &

Security.(Boeing Official Website,2015 )

1.1. Revenue

To classify the revenue from the different business Boeing has, we divide the revenue into three parts:

! Commercial Airplanes;

! Our Defense, Space & Security (BDS) business comprises three segments: Boeing Military

Aircraft (BMA), Network & Space Systems (N&SS) and Global Services & Support (GS&S);

and

! Boeing Capital (BCC).

Revenues in 2014 increased by $4,139 million or 5% compared with 2013. Commercial Airplanes

revenues increased by $7,009 million primarily due to higher new airplane deliveries. BDS revenue

decreased by $2,316 million is due to lower revenues in all three segments. Revenues in 2013 increased

by $4,925 million or 6% compared with 2012.

Commercial Airplanes revenues increased by $3,854 million due to higher new airplane deliveries.

BDS revenues increased by $590 million due to higher revenues in the Network & Space Systems

(N&SS) and Global Services & Support (GS&S) segments, partially offset by lower revenues in the

Boeing Military Aircraft (BMA) segment. The change in unallocated items, eliminations and other in

2014, 2013 and 2012 primarily reflects the timing of eliminations for intercompany aircraft deliveries.

(Boeing annul report,2014).

3

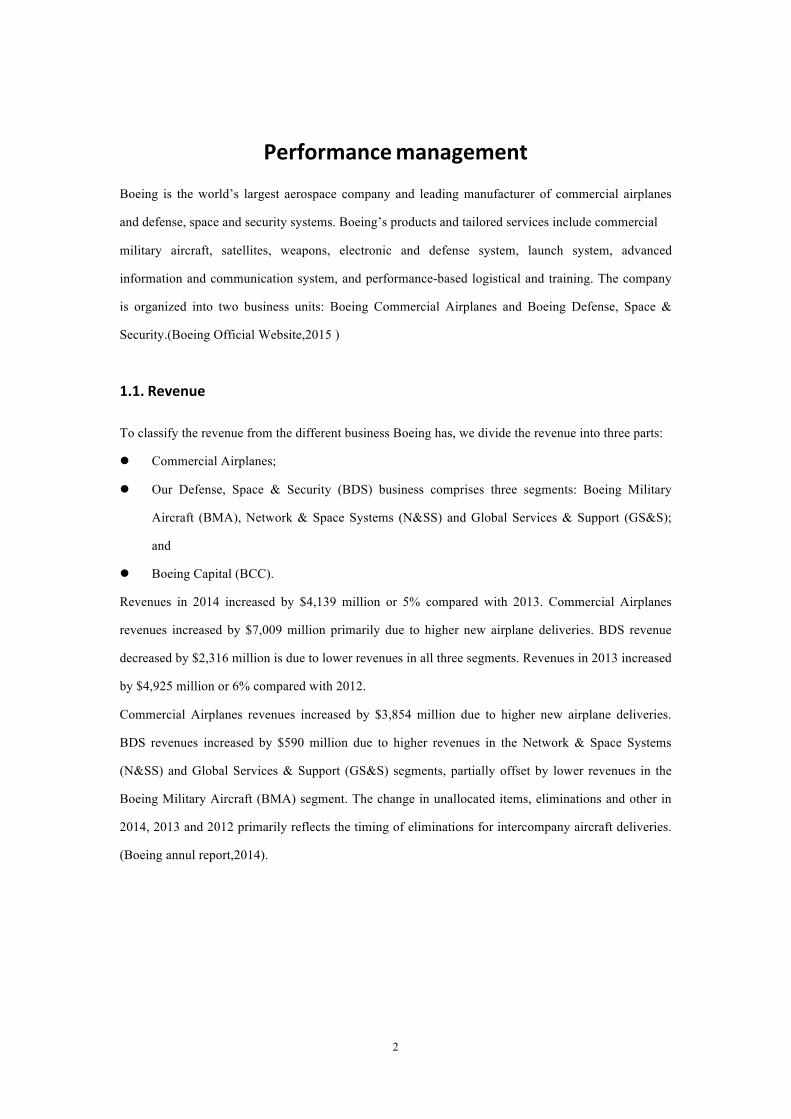

And we can see from the graph, the increase of revenue is predominantly the result of the increase of

commercial airplanes revenue. Boeing has continually been in a strong grow in commercial airplane

area, which has driven its revenue to a successful growth. In 2010,Boeing delivered 462 commercial

airplanes, but in 2014,it has broken the record and delivered 723 commercial jets. Also Boeing has

increased its record backlog to nearly 5,800 airplanes worth $440 billion.

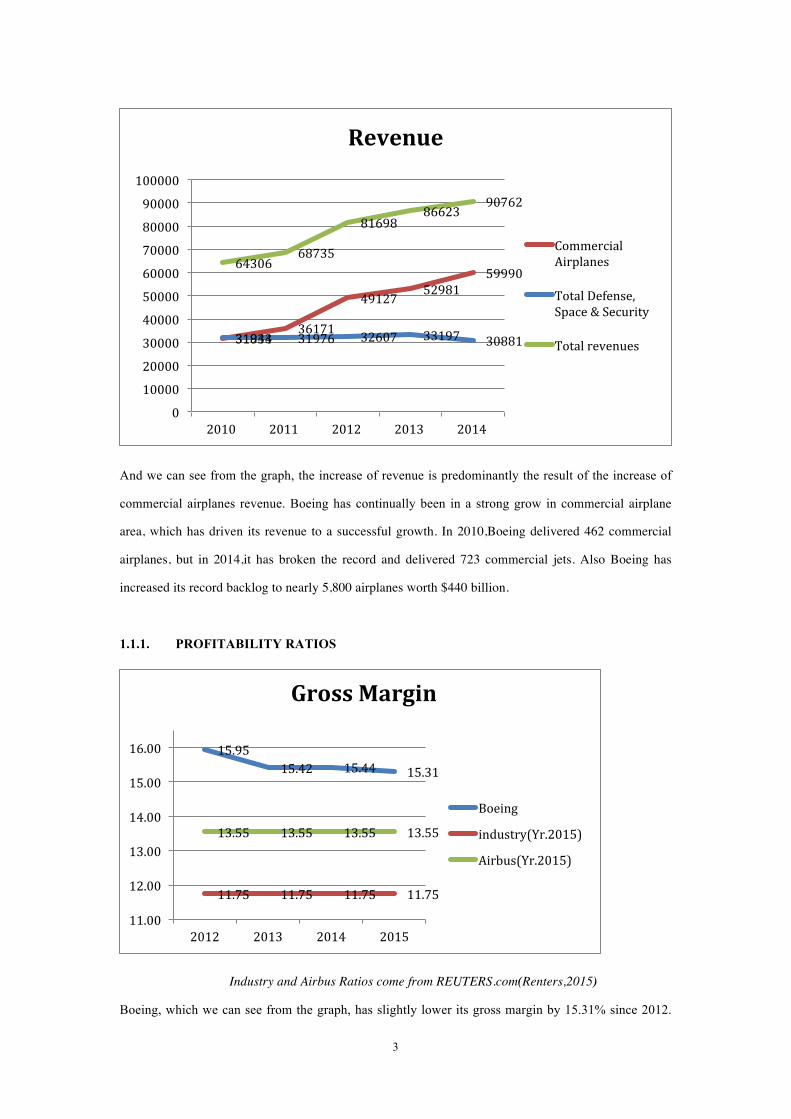

1.1.1. PROFITABILITY RATIOS

Industry and Airbus Ratios come from REUTERS.com(Renters,2015)

Boeing, which we can see from the graph, has slightly lower its gross margin by 15.31% since 2012.

31834 36171

49127 52981

59990

31943 31976 32607 33197 30881

64306 68735

81698 86623

90762

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2010 2011 2012 2013 2014

Revenue

Commercial Airplanes

Total Defense, Space & Security

Total revenues

15.95 15.42 15.44 15.31

11.75 11.75 11.75 11.75

13.55 13.55 13.55 13.55

11.00

12.00

13.00

14.00

15.00

16.00

2012 2013 2014 2015

Gross Margin

Boeing

industry(Yr.2015)

Airbus(Yr.2015)

4

That probably because of the program accounting that Boeing is using. Program accounting requires

the demonstrated ability to reliably estimate the relationship of sales to costs for the defined program

accounting quantity. At the beginning of a program, such as the 787 program, it required a higher unit

production costs and substantial investment. This will raise the operating cost and drop Gross margin

down. But compared to industry and the biggest competitor Airbus Group, Boeing is still much higher

than them, which indicates its perfect job on manufacture process.

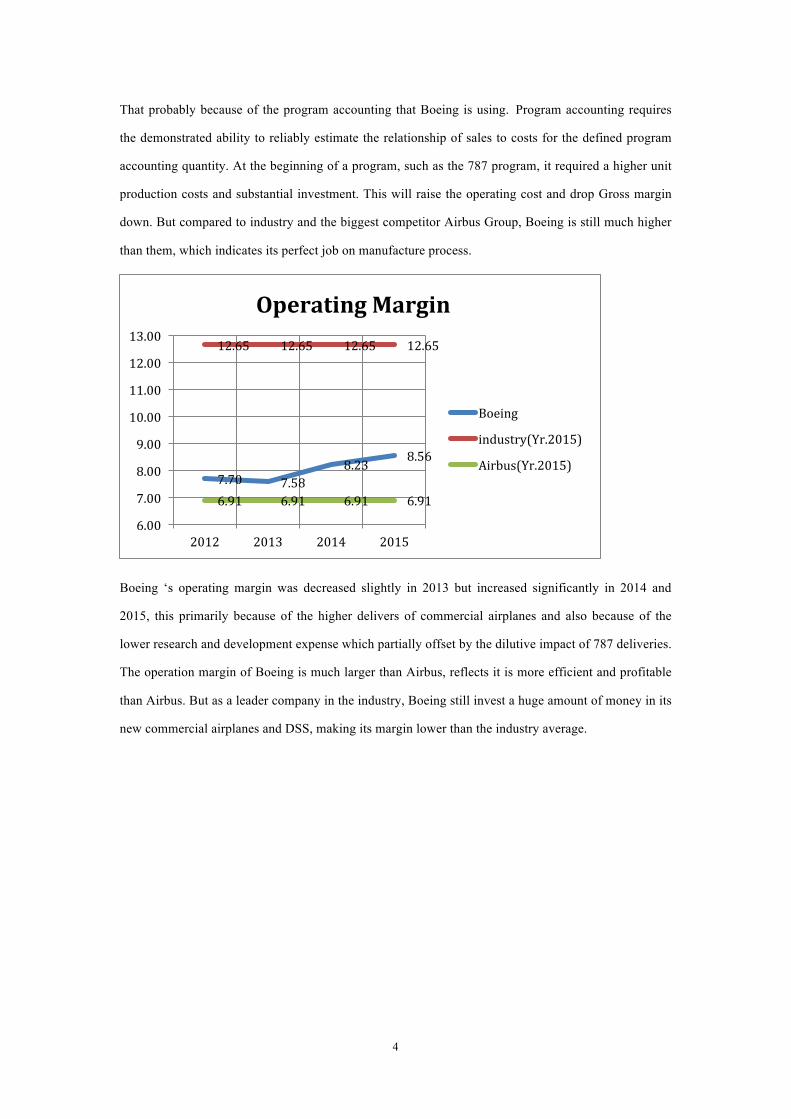

Boeing ‘s operating margin was decreased slightly in 2013 but increased significantly in 2014 and

2015, this primarily because of the higher delivers of commercial airplanes and also because of the

lower research and development expense which partially offset by the dilutive impact of 787 deliveries.

The operation margin of Boeing is much larger than Airbus, reflects it is more efficient and profitable

than Airbus. But as a leader company in the industry, Boeing still invest a huge amount of money in its

new commercial airplanes and DSS, making its margin lower than the industry average.

7.70 7.58 8.23 8.56

12.65 12.65 12.65 12.65

6.91 6.91 6.91 6.91

6.00

7.00

8.00

9.00

10.00

11.00

12.00

13.00

2012 2013 2014 2015

Operating Margin

Boeing

industry(Yr.2015)

Airbus(Yr.2015)

5

1.1.2. Efficiency

To compare the efficiency of the company, we compare Boeing Airbus and the industry in three

dimensions: Receivable Turnover, Inventory Turnover and Asset Turnover. As for receivable turnover,

Boeing has the highest in 11.65, which is much higher than the industry average. That means Boeing

has a high proportion of quality customers that pay off their debts quickly. And it may also indicate

that the company’s collection of accounts receivable is efficient. The company, which has a

conservative policy, will filters out customers who may be more likely to take a long time in paying

their debts, but it also may drive away potential customers and give business to competitors because

the credit is too tight.

Inventory turnover is a ratio showing how many times a company's inventory is sold and replaced over

a period. Boeing’s inventory turnover shows that it can replace its inventory 1.72 times in a year, which

is lower than the industry average ratio. This is a bad sign for company because it shows that the hold

cost is high, and because Boeing is mainly sold the jets through contact, in some point it can prevent

the inventory being deteriorated, and make the company have high ability to stable the price.

Boeing’s asset turnover is much beyond the average as well as its biggest competitor. This reflects the

company is so efficient at making revenue by its asset.

11.65

1.72 1.01

3.53 2.51

0.43

10.26

1.87 0.64

0

2

4

6

8

10

12

14

Receivable Turnover Inventory Turnover Asset Turnover

Ef4iciency

Boeing

industry

Airbus

6

1.1.3. Management Effectiveness

When we compare Boeing’s management effectiveness with industry level and its competitor, we can

see Boeing did quite well in ROA, ROI and ROE. Both return on asset and return on investment show

that Boeing is good at using its asset and investment to make net income. The company manages to

earn more money on less investment. And the high return on equity ratio shows Boeing is worthy to

hold the shares because its very profitable and it can generate a lot of profit with the money

shareholders have invested. And next we compare these three ratios in a vertical way.

Seeing from the graph, Boeing’s ROA and ROIC are almost increased yearly from 2012 to 2015, this

mainly due to the increasing selling of the commercial airplanes. But when we look at ROE, we will

find something interesting. There was a big drop of ROE in 2013 and then its back to normal again not

reaching 2012 level.

5.86

13.96

52.8

2.33 4.05

12.38

2.9 5.8

38.06

0

10

20

30

40

50

60

ROA ROI ROE

Management Effectiveness

Boeing

industry

Airbus

4.4 4.9 5.5 5.68

11.9 11.4 11.8

13.9

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2012 2013 2014 2015

ROA&ROIC

ROA

ROIC

66.5

30.8

62.9

52.8

20.0

30.0

40.0

50.0

60.0

70.0

ROE

ROE

7

From 2012 to 2014,there is a stability increase in net earning. But the shareholder’s equity had

increased a lot in 2013.One reason is that Boeing had passed benefit pension plans that cover the

majority of our employees. Potential pension contributions include both mandatory amounts required

under the Employee Retirement Income Security Act and discretionary contributions to improve the

plans' funded status. The company also provided other postretirement benefits to certain of its

employees, consisting principally of health care coverage for eligible retirees and qualifying

dependents. These new politic resulted in a significant change to Shareholders' equity. The other reason

is about the purchasing. On October 29, 2007, the Board approved the repurchase of up to $7,000 of

common stock (the 2007 Program). At December 31, 2013, $810 in shares may still be repurchased

under the Program. On December 16, 2013, the Board approved a new repurchase plan (the 2013

Program) for up to $10,000 of common stock that commences following the completion of the 2007

Program. Unless terminated earlier by a Board resolution, the Program will expire when boing had

used all authorized funds for repurchase. As of December 31, 2013 and 2012, there were 1,200,000,000

shares of common stock and 20,000,000 shares of preferred stock authorized.

1.2. Cost

The cost part consist two kind of cost, Variable cost which usually float with revenue and Fixed cost

which refer to General and administrative expense and Research and development expense.

Variable cost (cost of sales) is combined with the cost of products and services, consists primarily of

raw materials, parts, sub-assemblies, labor, overhead and subcontracting costs.

And the cost is accounted in two ways; The Commercial Airplanes segment predominantly uses

program accounting to account for cost of sales. Program accounting is a method of accounting

applicable to products manufactured for delivery under production-type contracts where profitability is

realized over multiple contracts and years, Under program accounting, cost of sales for each

commercial airplane program equals the product of the revenue recognized in connection with

Dec 31, 2014 Dec 31, 2013 Dec 31, 2012

Selected Financial Data (USD $ in

millions)

Net earnings related to parent 5,446 4,585 3,900

Shareholders’ equity 8,665 14,875 5,867

Ratio

ROE 62.85% 30.82% 66.47%

8

customer deliveries and the estimated cost of sales percentage applicable to the total remaining

program. And the BDS mainly use contract counting, under which circumstance the cost of sales is

determined by applying the estimated cost of sales percentage to the amount of revenue recognized.

The cost of service reminds stable and the cost of product increase almost with the same speed as the

increase of revenue.

There is a continually small decrease in fix cost, mainly contributed by the decrease in research and

development expense. Boeing is trying to lower the devotement cost to become more competitive.

Engineering teams are focusing on designs that are more producible, using more common systems and

parts, and adhering to our disciplined, gated development process.

-‐46,642

-‐60,309 -‐65,640 -‐68,551

-‐9,097 -‐8,247 -‐7,553 -‐8,132

-‐55,739

-‐68,556 -‐73,193 -‐76,683

-‐90,000 -‐80,000 -‐70,000 -‐60,000 -‐50,000 -‐40,000 -‐30,000 -‐20,000 -‐10,000

0 2011 2012 2013 2014

Variable cost

Cost of products

Cost of services

Variable cost

-‐3,644 -‐3,408 -‐3,717 -‐3,956 -‐3,767 -‐4,121 -‐3,918 -‐3,298 -‐3,071 -‐3,047

-‐7,765 -‐7,326 -‐7,015 -‐7,027 -‐6,814

-‐9,000 -‐8,000 -‐7,000 -‐6,000 -‐5,000 -‐4,000 -‐3,000 -‐2,000 -‐1,000

0 2010 2011 2012 2013 2014

Fix cost

General and administrative expense

Research and development expense, net

Fix cost

9

1.2.1. Interest Cover Ratio

Year 2012 2013 2014

Earnings Before Interest And Taxes 6,352 6,618 7,470

Interest Expense 442 386 333

Interest Cover Ratio 14.37 17.15 22.43

Interest cover ratio of Boeing is increasing every year which means Boeing can pay interest on

outstanding debt easily. This happens both because the increasing of EBIT and the decreasing of

interest expense. BCC’s earnings from operations are presented net of interest expense, provision for

(recovery of) losses, asset impairment expense, depreciation on leased equipment and other operating

expenses, drop the interest expense.

And when we check the table below, we can find the Boeing’s ratio is more than 8.5. So it’s rating is

AAA, so we can get that the spread is 0.5%.

If interest coverage ratio is

> ≤ to Rating is Spread is

-100000 0.199999 D 15.00%

0.2 0.649999 C 12.00%

0.65 0.799999 CC 10.00%

0.8 1.249999 CCC 8.50%

1.25 1.499999 B- 5.50%

1.5 1.749999 B 5.25%

1.75 1.999999 B+ 4.25%

2 2.2499999 BB 4.00%

2.25 2.49999 BB+ 3.50%

2.5 2.999999 BBB 2.00%

3 4.249999 A- 1.50%

4.25 5.499999 A 1.25%

5.5 6.499999 A+ 1.00%

6.5 8.499999 AA 0.75%

8.50 100000 AAA 0.50%

1.2.2. GEARING

When we look at the gearing, we can see the Boeing’s gearing is very high(more than 100%), that

normally means the company is at a high risk. A lot of debt is used to finance increased operations. the

10

company could potentially generate more earnings than it would have without this outside financing. If

this were to increase earnings by a greater amount than the debt cost, then the shareholders benefit as

more earnings are being spread among the same amount of shareholders.(Investopedia,2015)

However, if the cost of this debt financing ends up losing money stakeholders’ share values may be

more harmfully hit. So this might be a boom in the future if Boeing’s revenue starts to drop.

1.2.3. WACC vs. ROIC

In %

CAPM 10.887 Total Equity 14,997

Cost of debt 4.5 Long-term Debt 8,141

WACC 8.64

First, we calculate the cost of debt=risk free rate (which is 4%) plus spread (0.5%)=4.5%. Then we

calculate the CAPM =risk free rate+β*equity risk premium=4%+0.97*7.1%=10.89%. Finally we use

WACC formula: WACC=E/LD*CAPM+LD/E*Cost of debt=8.64.

As we have mentioned before, the ROIC of Boeing is 11.7 in 2014 larger than WACC. So we can

assume that growth adds value, for every dollar of investment the company attracts it earns with more

than it pays out. And as the ROIC is always higher than WACC in Boeing’s case, it probably means

there is a moat in this company and make it continually generate value for its shareholders. We will

discuss about the moat in strategy part.

1.2.4. Operation Cash Flow

OCF (CAGR 10Y) 2012 2013 2014 2015 2016 2017 2018 2019 2020

REV 81,698 86,623 90,762 95,877 101,280 106,988 113,017 119,386 126,114

Net Profit 3,900 4,584 5,446 5,753 6,077 6,420 6,781 7,164 7,567

D&A 1,811 1,844 1,906 1,906 1,906 1,906 1,906 1,906 1,906

OCF 5,711 6,428 7,352 7,659 7,983 8,326 8,687 9,070 9,473

Discount factor

0.920 0.847 0.780 0.718 0.661 0.608

PV of OCF

2015-2020 7,050 6,764 6,493 6,236 5,993 5,762

First we use the revenue of 2004(52,457) and the revenue of 2014(90,762) to calculate the 10 years

GAGR, which is 0.06. Then we use it to estimate the year 2015-2020’s operation cash flow. And we

use discount factor to make the operating cash flow into present value. Next we use the number of

2020, long-term growth and WACC to calculate the terminal value. We add present value and terminal

11

value to figure out the firm value.

However, the firm value still omits a company’s debt on the one hand and its cash reserves on the other,

when the firm is sold to a new owner, buyer has to pay the equity value and also repay the firm’s debts

and cash, which is net debt. So we use firm value plus net debt to get enterprise value. At last we

compare the enterprise value with the stock market value to see Boeing’s performance.

Sum of PV of OCF 2015-2020 38,298

Terminal Value 102,166

Net Debt -4,186

Firm value 140,463.72

Enterprise Value 136,277.72

Stock Market Value 99,117.38

So if we estimate the operation cash flow using the 10 years GAGR, we get the enterprise value is 35%

higher than the stock market value. And if we want to estimate the OCF based on recent year, we use

the GAGR of 3 years (0.04), through this we get another table.

Sum of PV of OCF 2015-2020 36,377

Terminal Value 93,044

Net Debt -4,186

Firm value 129,421.45

Enterprise Value 125,235.45

Stock Market Value 99,117.38

From this table we can see even if we use a lower GAGR, the enterprise value is still about 25% higher

than stock market value.

From the stock market view, it might be a chance for investors because Boeing’s stock is under valued,

and the stock price still has a large room to climb. But, in Boeing’s view, this might be a bad news

because it reflects the market’s mistrust of Boeing Company. They do not trust Boeing can still have a

high revenue growth in the future. This will make the company’s decision makers think more about

how to persuade investors to come with more money.

12

Corporation strategy

The global airline industry has grown significantly consisting of over 2,000 carriers worldwide,

operating over 23,000 aircraft, and servicing over 3,700 airports. On the average annually, world

airlines flew approximately about twenty eight million (28 million) scheduled flights carrying over 2

billion passengers (IATA, 2006). While air travel has become commonplace as it is becoming more

and more affordable to various income classes of the society, more and more jets are needed today,

especially in the emerging market. The airplane manufacture industry still has a huge growth even in

today. Through Boeing is one of the leading companies, how to survive and be competitive is always a

primary issue on the table.

1.3. Macro-‐environmental

The external environment consists of external influences that affect the firm’s decision-making process

and performance. As an airplane manufacture company, the external marketing environment has a

great influence on Boeing. It is in an area fulfilled with fierce competition and government and politic

also playing a very important role in Boeing’s business. To have a look at what this company is facing

in nowadays world first we analysis the PEST of the market, which refer to P-Political, E – Economic,

S – Social and T – Technological.

1.3.1. Political

Prior to 1970’s, the airline industry was mainly owned and controlled by the governments in different

countries. There was no free market competition, as travelers have to make do with the services and

prices available to them from the few airlines. Now thought things become different. As in commercial

airplane area, because of its large profit that can bring to a country, government now has promoted the

development of the airline industry by providing infrastructure, research and development, subsidies,

protective regulation and outright ownership of airlines. For Boeing, it has deep relations and strong

agreements with US Government and Federal Aviation Administration (FAA), so the policies of the

US government may be a major driving force in accepting new orders of aircrafts. A good side is that

trading of large commercial jetliners has been tariff free since 1979 (GATT, 1994) and ‘Open Skies’

agreement of US government with other countries (US Department of State, 2011). A bad side is the

government have come out a restrictions of selling specific equipment or airplanes to particular

countries like Iran, Iraq, Afghanistan and Pakistan, in which case drive down Boeing’s sales.

1.3.2. Economic

First the cost of jet aircraft depends heavily on raw materials and fuels. A higher price of fuel and the

security equipment is due to terrorism threat especially after 2001 will intensively increase the cost of

13

capital. And another very important economy factor about these kinds of companies is the governments’

subsidies. This is mainly reflects on the competition between Boeing and airbus group. Boeing is

subsided a lot by U.S. government, According to Monday's ruling, the WTO's appellate body said

Boeing received between $3 billion and $4 billion in U.S. subsidies over a period of 8 years. And

Airbus also received a large deal of subsidies owned by European Aeronautic Defense & Space Co.

(EADS) from EU governments like Germany, France, the United Kingdom, and Spain. In 2012 The

World Trade Organization issued a ruling Monday to settle a dispute between the European Union and

United States over subsidies received by Boeing. (Ben Rooney, 2012) But until now the conflict still

remind between these two companies as a part of their fight.

1.3.3. Social

The primary social influence is the global population growth in developing countries. As more and

more people born in these countries and air travel has become more usually and affordable, in

emerging market has developed a lot in recent years. And the big players like Boeing and airbus are

fight hardly for their oversea market.

And as we can see from the graph, for a simple Asia country like China, Boeing has delivered 27

aircraft in a short period of 6 months in 2015. The increasing demand of commercial aircraft in these

14

countries can bring in large revenues for Boeing.

1.3.4. Technological

Boeing has an edge over Airbus and other competitors in using composite lightweight material in the

development of commercial airplanes (Cohan, 2011). And also Boeing is focus on use technology to

develop aircraft more efficiency. To break the upward spiral of development costs, its engineering

teams are focusing on designs that are more producible, using more common systems and parts, and

adhering to our disciplined, gated development process. Tangible benefits of these efforts are evident

on 787, 737 MAX and 777X development programs. For example, more than 90 percent of the 787-10

will be common with the 787-9, which will drive significant efficiencies through the development

process, production system and supply chain. (Boeing annual report, 2014).

1.3.5. Porter’s five forces

The five forces of Porter’s model are threat of new entrants, threat of substitute products, the

bargaining power of suppliers, the bargaining power of customers, and rivalry among competitors. It

shows that how Boeing’s long-term business strategy meet opportunities and threats in the external

environment.

1.3.5.1. Threat of new entrance:

Though the barriers of aircraft manufacture company is very high. One reason is to start a company

like this, you need a lot of money and recourse and also your own technology, and it’s not a company

that you can simply copy the counterparts. The other reason is even you have the resource and money

to build this kind of company, you can’t be a threat in a short time. It will cost a longtime to get to the

break-even point and become profitable.

But now there is indeed a new threat appears. China is also arming into aviation market. The first plane

produced by a Chinese government initiative to compete in the market for large passenger jetliners has

been unveiled in Shanghai. The Commercial Aircraft Corporation of China (COMAC) showed off its

twin-engine C919 in a ceremony on Monday attended by some 4,000 government officials and other

guests at a hangar near the Pudong International Airport. (ALJAZEERA, 2015). Though today the

China's aviation market is still shared by Boeing and Airbus equitably. The ruling Communist Party

wants to claw back some of the commercial benefits that flow to foreign suppliers. And with its power

of manufacturing and the government’s support, China is expected to add 6,330 new aircraft worth

$950bn to its commercial fleet by 2034, Boeing estimates. (ALJAZEERA, 2015).

1.3.5.2. Threat of substitutes:

The substitutes of airplane mainly refer to other transport like cars, trains and ships, and as trains

nowadays become faster and cheaper. In short travel, it may have an influence on airplane. But

15

consider of long distance travel, plane is still the main transport because it ignores the influence of

topography and save a lot more time than train.

1.3.5.3. Bargaining power of suppliers:

The bargaining power of suppliers is high in Boeing as well as the total aircraft industry. The

company’s new planes depend a lot on the suppliers, and in some case like Boeing’s 787 Dreamliner

project, the plane is delayed because of its supplies and cause a big problem to Boeing as it lost

effective control.

1.3.5.4. Bargaining power of customers:

The bargaining power of customer is low in this kind of companies because customer do not have

many choice, the only two big commercial plane made companies are Boeing and Airbus. And as an

airline company, it has to take the price if it wants to have more planes. And the switch cost between

these two companies is also very high. Because of the different control system, the airline companies

can’t afford to change the crews if they want to change the company if planes.

1.3.5.5. Competitive between competitors:

16

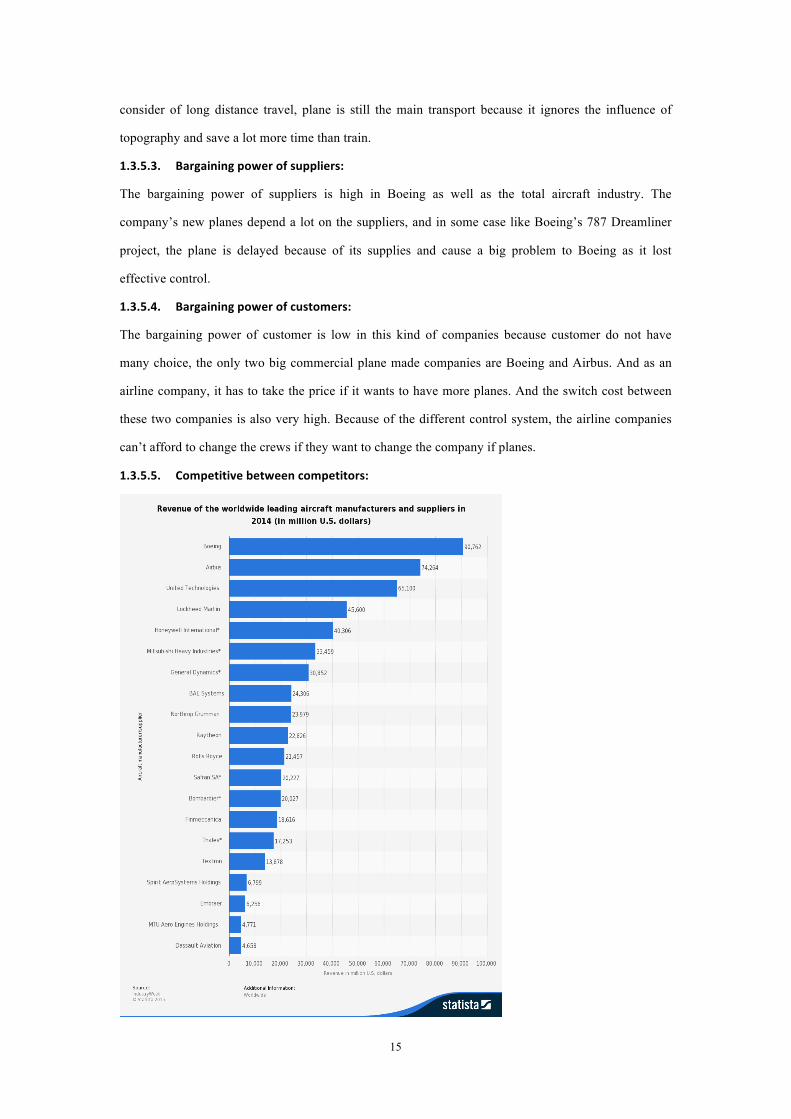

Looking at the table of the revenue of worldwide aircraft manufacturers and suppliers, Airbus is no

doubt to be the leading competitor of Boeing. And the competition with Airbus in the commercial

airplane has a significant influence of Boeing.

This graph shows more clearly how fierce is the competition between these two companies. Boeing and

Airbus is playing a race with each other and people can’t tell who is the winner at last. As in 2014,

Boeing delivered more passenger jets than its European rival, but Airbus crossed the finish line with a

higher level of orders. In detail, Airbus hit a record to supply 629 aircraft in 2014, marking 13

consecutive years of increased deliveries. This fell short of Boeing’s 723 deliveries in the period,

however, making the US group the world’s largest manufacturer of aircraft for the third year in a row.

(Peggy Hollinger, 2015).

And also the competition reflects in take more amount in the new market, with the rapid growth of

market in China and Latin American, these two companies are targeting at the international airplane

market.

In hard numbers, Boeing expects Latin American buyers to buy 3,020 new airplanes over the next 20

years, and to spend perhaps $350 billion acquiring them. About 340 of these aircraft will be

long-distance wide body jets, costing as much as $400 million a pop, and 160 or so will be much

cheaper small regional aircraft, carrying 90 passengers or less. (Rich Smith, 2015)

17

Region Population in 2015 Plane Demand (Through

2034)

Inhabitants per Plane

China 1.364 billion 6,330 215,481

South America 525 million 3,050 172,131

Mideast 357 million 3,180 112,264

1.4. SWOT

SWOT is a method for us to analysis the internal strength, weakness of the company and also the

potential opportunities and threats in the external environment.

1.4.1. Strength

The major strength of Boeing is that it’s still the leader of Innovation and Technical Expertise, and the

company has worldwide strong reputation of quality and industry leadership. With the large share of

commercial airplanes and also the business in Defense, Space & Security and Boeing Military Aircraft,

Boeing is not a normal airplane manufacturer but like the symbol of high tech and explorer of the

future airplanes. It’s a company that has an international market of the whole world providing its

products and services to over 90 countries. And its large revenue comes from not only commercial

airplanes but more than 6 divisions. A tight support from the US government also enhances the

strength of the company.

Another strength is reflected by the company’s perfect performance, we can see from the management

effectiveness that the company has a higher ROE, ROA and ROIC than industry average. Strong core

operating performance companywide raised core earnings, and make the company has a higher

enterprises value than its stock market value.

1.4.2. Weaknesses:

One of the weakness is that Boeing depends too much on it suppliers. The company is highly

dependent on the availability of essential materials, parts and subassemblies from our suppliers and

subcontractors. Although alternative sources generally exist for these raw materials, qualification of the

sources could take one year or more. Many major components and product equipment items are

procured or subcontracted on a sole-source basis with a number of companies.

While Boeing maintain an extensive qualification and performance surveillance system to control risk

associated with such reliance on third parties, failure of suppliers or subcontractors to meet

commitments could adversely affect production schedules and program/contract profitability. (Boeing

annul report, 2014)

18

1.4.3. Opportunities

The biggest opportunity is the growing market of airplane in emerging countries especially like

countries in Asia and Latin America. Also the surge of spending heavy amounts on defense and

security because of the tourists these days also increases Boeing’s market in military aircraft. Another

opportunity is new technology making Boeing save more cost in develop new jets and build lighter,

longer-range aircraft. Like Airbus is wooing new customers by increasing the number of seats in the

cabin (Peggy Hollinger, 2015), Boeing also has the opportunity to attract more customers after its new,

fuel-efficient 737 MAX delivered in 2017 and The 787-10 Dreamliner, the third and longest member of

the 787 family being delivered in 2018. (Boeing annual report, 2014)

1.4.4. Threats

One of the threats is a Boeing’s commercial airplane business depends heavily on the airline companies.

Because the it usually does business by longtime contact, the macroeconomic influence such as

sustained economic growth and political stability will both affect deliveries over a long period.

Commercial aircraft sales contracts are often entered into years before the aircraft are delivered.

Because the contracts are usually signed with a fixed-price, if the company has cost overruns or if

increases in its costs exceed the applicable escalation rate, the company will have a loss in its profit.

The other threat is new competitor coming from the emerging countries such as China, these may not

happen in a short term, but someday, with airplane become a common transport and technical barriers

is not that strong, Boeing has to deal with the new competitors joining this big market.

Conclusion

In this research, first we analysis the financial performance of Boeing company, the ratios are healthy

and stable (except the equity floating in 2013 because of the new pension project and the repurchase of

the stock). The company has a good gross profit margin above average and an increasing operating

profit margin. The company is managed efficient with a high and rising ROA and ROIC ratio. The

gearing is high which can bring shareholders a lot of profit but also with a high risk.And the WACC is

lower than ROIC which means the return on capital is more than the cost of capital, Boeing is using its

capital to earn money. At last we calculated the enterprise value and compare it to the stock market

value, the higher enterprise value indicates two thing, one is the company is underestimate by investors.

Or it might be the market’s lack of confidence about Boeing’s ability to keep that growth of profit.

Then we analysis both the internal and external environment of the company. Thought the aerospace

industry id full of competition, Boeing has kept its leading position by its large scale, leading

technology and the support from US government. But we can see the threats of the companying are

19

also coming, one is from the competition with Airbus, and also the new companies from developing

countries like China could also be a big threat.

The way to go out first is to enhance the company’s performance especially the control of the suppliers

and subcontractors to avoid the risk of being delay or over cost. The second is widening its

international business, catching the opportunity of fast market growth in the East Asia and Latin

America.

References

[1] Boeing Official Website,(2015). Boeing in brief. Available from:

<http://www.boeing.com/company/general-info/> [27 November 2015]

[2] The Boeing company,(2014) Annual Report,2014 ,Available from:

<http://www.boeing.com/assets/pdf/companyoffices/financial/finreports/annual/2014/annual_rep

ort.pdf> [31 December 2014]

[3] Reuters, (2015). Financials: Boeing Co (BA.N). Available from

<http://www.reuters.com/finance/stocks/financialHighlights?symbol=BA.N#Rj8DkqOXcIVbIUb

G.97> [27 November 2015]

[4] Reuters, (2015). Financials: Airbus Group SE (AIR.PA). Available from <

http://www.reuters.com/finance/stocks/financialHighlights?symbol=AIR.PA#1j1GTY4QdPeJIT7

B.97 > [27 November 2015]

[5] Investopedia,(2015). Debt/Equity Ratio, Available from:

<http://www.investopedia.com/terms/d/debtequityratio.asp> [27 November 2015]

[6] US Department of State, (2011). Open Skies Partners, Bureau of Economic and Business

Affairs, Washington, [online]. Available from:

<http://www.state.gov/e/eb/rls/othr/ata/114805.htm> [23 April 2012]

[7] Ben Rooney,(2012). U.S. and EU claim victory in Boeing subsidy case, CNN money.

Available from: <http://money.cnn.com/2012/03/12/markets/boeing-airbus-wto/> [12 March

2012]

[8] Cohan, P., (2011). Boeing's Dreamliner Delays: outsourcing goes too far, Daily Finance, [21

January 2011]

[9] ALJAZEERA, (2015). First China-made passenger jet leaves production line, BUSINESS &

ECONOMY, Available from:

<http://www.aljazeera.com/news/2015/11/china-passenger-jet-leaves-production-line-151102054

428051.html> [02 Nov 2015]

20

[10] Peggy Hollinger,(2015), Boeing beats Airbus to title of largest jet maker in 2014, financial

time, Available from

<http://www.ft.com/intl/cms/s/0/a2f9121c-9aa0-11e4-86c2-00144feabdc0.html#axzz3saEWODJ

s> [13 January 2015]

[11] Rich Smith,(2015). Boeing Sees a Brave "New World" for Planes Business, Fool.com,

Available from:

<http://www.fool.com/investing/general/2015/11/25/boeing-sees-a-brave-new-world-for-planes-

business.aspx?source=eogyholnk0000001&utm_source=yahoo&utm_medium=feed&utm_camp

aign=article> [25 November 2015]

[12] Statista, (2015). Statistics and Market Data about Aerospace Manufacturing, Aerospace

Manufacturing, Available from:

<http://www.statista.com/markets/407/topic/939/aerospace-manufacturing/> [27 November

2015]