board matters quarterly - building a better working world - · pdf file ·...

TRANSCRIPT

1AGM

Preparing toface investorswith yourannual reportcard

12SingaporeBudget 2016− Wehighlightsome of thekey changes

17Finally, thenew leasesstandard

24Sustainabilityreporting

30Hong KongBudget2016-17

32Regulatoryupdates

35Changes toFRS effectivein 2016

Issue 27, March 2016 | Singapore

Board MattersQuarterly

EditorialAGM is governed by an ever increasing number oflegislative and regulatory requirements. With growinginvestor scrutiny and shareholder activism, it isimportant that companies are well prepared for theirAGM. AGM also offers the Boards the opportunity tocommunicate their vision for the company, explain thecompany’s recent performance and to hear fromshareholders without the filter of intermediaries. In thisissue of Board Matters Quarterly, we look at theforthcoming AGMs with questions and topics the Boardshould consider, and some suggestion for AGMpreparation.

We highlight some of the key changes announced in theSingapore Budget 2016. We also look at the new leasesstandard - What is the new leases accounting model?How different will your financials look? Lastly, we lookat sustainability reporting the SGX is expected toimplement in 2017.

We hope you find Board Matters Quarterly useful, andshare it with others. If you have feedback or ideas forfuture issues, please contact us [email protected].

Tan Seng Choon

Assurance Partner and Professional Practice Director

Ernst & Young LLP

Section or Chapter title

Board Matters Quarterly | March 2016 1

Section or Chapter title

Board Matters Quarterly | March 2016 2

AGMPreparing to face investors with your annual report card

AGM has become increasingly challengingThe AGM is the pinnacle of the corporategovernance process. The board, in guidingand monitoring the company, is responsiblefor ensuring proper accountability, probityand openness in the conduct of the company’sbusiness – the corporate governanceenvironment.

Traditionally, AGM is the one day of the yearwhen shareholders of listed companies havethe legal right, as owners, to query the Boardon its role and performance in a public forum.AGM also offers the Boards the opportunity tocommunicate their vision for the company,explain the company’s recent performanceand to hear from shareholders without thefilter of intermediaries.

The scrutiny placed upon Boards of listedcompanies continues to intensify against abackdrop of increasing corporate governanceand financial reporting issues. Stakeholders,from regulators to shareholders to corporatesocial responsibility advocates, have become

more vocal, sophisticated, and assertive,while the business environment has becomemore challenging and competitive.

Both investor representative bodies and thepress may draw greater attention togovernance related issues than companiesmay necessarily wish. In extremecircumstances, this can potentially lead to theembarrassment of resolutions beingwithdrawn or voted down at AGM. All thesemean that the underprepared Board will facea challenging time during the AGM. Apoorly−run AGM will reflect badly on thegovernance of the company, erode confidencein the Board and ultimately impactshareholder value.

This article highlights potential areas of focusfor shareholders at the forthcoming AGM withquestions or topics that you should consider,and a reminder of some of the basic rules ofAGM preparation.

6. Selection ofauditor

7. ACRA’sFRSP

8. Reporting offinancialresults,generalbusiness andperformanceissues

3. Tenure of directorshipand multiple directorships

4. Dividends

5. Board composition

In this issue:

1. Basic rules forAGM

2. Directors andexecutiveremuneration

Section or Chapter title

Board Matters Quarterly | March 2016 3

2.Determine howto respond toshareholdersduring AGM

1 Basic rules for AGM

► AGM held in Singapore - Issuer which is primary−listed on Singapore Exchange (SGX) is required to holdits general meetings in Singapore, unless prohibited by the relevant laws and regulations in the jurisdictionof their incorporation.

► Voting by poll - All resolutions at general meetings are to be voted by poll, and at least one scrutineer isto be appointed for each general meeting.

Preparation is key to success — A little homework goes a long way

Planning should always begin with a debrief on last year’s meeting (number of attendees and questionsasked), and consider any major developments during the financial year (FY). In presentations by theChairman or CEO, events that should be covered include major acquisitions, divestment or restructuring,legal or media issues, significant changes to products or services and impacts as a result of the industrydevelopments or competition. One should also be prepared to answer questions to the extent that are notcovered by the Chairman or CEO in the annual report.

Strategic preparation for AGM involves these considerations:

3.Anticipatequestionsand issuesduring AGM

4.Decide the natureof questions to be

directed to specificdirectors

5.Contact

institutionalinvestors

prior to AGM

6.Attendance bythe key service

advisors andsenior

management

7.Updated

shareholderregister

8.Know yourcorporate

governancedisclosures

9.Fixing AGMdate early

10.Plan to stayafter AGM to

mingle with theshareholders

1.Engage thefull Board

Section or Chapter title

Board Matters Quarterly | March 2016 4

► Companies that engage the full Board to discuss issues and plan itsstrategy will be better positioned to deal with surprises on AGM day,especially if the meeting is expected to be controversial in any way.

Conversations should include a debrief on the prior year’s AGM, theexperiences of peer companies, and procedural matters includingwhether to have the Chairman announce the results of proxy votesbefore the shareholders voting.

► The Board should determine how to respond to shareholders duringAGM. AGM follow a standard format which typically begins with theChairman's address, followed by the tabling of proposed resolutions,consequential shareholder questions, and any special business.

Once AGM as commenced, the Chairman has the power and duty toensure that the meeting is conducted properly and smoothly. To ensurethat each motion is given sufficient time and attention, the Chairmancan:

► Require full debate on one topic at a time, and refer back to earlierdiscussion on that topic.

► Setting protocol (e.g., giving different shareholders opportunities toraise questions) so that others have a fair chance to speak.

What if the shareholder ignores it? The Chairman could politely waitfor an opening − ”Let me make sure that I understand correctly”, or“Let me sum up what you said” − Let them know that the Board haveheard them, and know what they are saying, while at the same timetaking the floor away from them.

► Quickly answer or decline repetitive questions that have beenanswered.

► Tactfully decline or defer questions that are irrelevant to theresolution being considered.

► End the debate by exercising the Chairman’s right to keep anydiscussion within reasonable bounds.

► Seek the vote of the meeting to bring the discussion to a close.

► Anticipate questions and issues, and plan the best responses to them.The Board may decide to conduct a pre−emptive presentation if there isa topic of wide−spread interest, e.g., future plans following arestructuring or reverse takeover, etc.

Prepare an internal FAQ so that all concerned are on the same page.

► Decide the nature of questions to be directed to specific directors.For example, it may be inappropriate for the CEO to answercompensation−related questions, especially if the CEO is the highest paidBoard member. The Chairman of the Remuneration Committee orChairman of the Board might be a better choice. Ensure that eachdirector knows how fellow directors will respond to questions.

► Contact institutional investors prior to AGM to gauge their supportfor the proposed resolutions. Prior warning of a lack of support inparticular areas allows the Board to consider if and how it will proceed,and how it may amend resolutions. Remember that motions defeated atan AGM may send a message of a lack of confidence in the Board.

To preventembarrassing andavoidable pitfalls

It is important that theBoards and companysecretaries get the basicsright. The entity shouldensure that AGM is not leftshort by:

► A shortage of seats forall of the Board to sit atthe top table, or havingname cards in the wrongpositions.

► Being unable to dealwith difficult questionsor complex points of lawdue to a lack of availableadvice.

► Allowing the meeting tobe derailed by anunexpected issue raisedby a key interest group.

► A technology failure(audio or visual) forexplanatory slideshowsor presentations, or notmaking adequateprovision for therecording ofproceedings.

► Not having a microphoneready to those not at thetop table who canreasonably be expectedto speak, for example,the CFO who is not adirector.

Section or Chapter title

Board Matters Quarterly | March 2016 5

► Attendance by the key service advisors and senior management likecompany secretary, senior managers as well as legal and other advisorscan support directors’ responses. Also consider attendance byremuneration consultants, especially if concerns about remunerationhave been raised in the past.

► Updated shareholder register ensures smooth process for shareholdersvoting. Decide whether there should be electronic voting or poll voting.

► Know your corporate governance disclosures. The annual reportalready reported how the company performed against the corporategovernance recommendations. However, it is worth preparing specificanswers to questions which may arise on what shareholders would seeas boilerplate explanations to non−compliance. In addition, having amanagement presentation on the state of the company at the outset ofAGM may help pre−empt many questions that could otherwise comefrom the floor.

► Fixing AGM date early so that shareholders and directors with interestsin multiple companies can plan their schedules.

► Plan to stay after AGM to mingle with the shareholders. It is anopportunity to hear from shareholders directly without the filter ofintermediaries.

2 Directors and executiveremunerationAccording to the Board Remuneration and Practice in Singapore20151 released by the global management consultancy Hay Group in 2015,the non-executive directors in Singapore listed companies received anincrease of 7.1 percent in the median of the average director’s fee (or$60,000 per annum) in Financial Year 2013/2014, compared to $56,000in the previous financial years.

In addition, the SGX announced in October 2015 that it is carrying out areview of how listed companies abide by the “comply or explain”requirement for principles and guidelines of the Singapore Code ofCorporate Governance 2012 (the Code). Examples of key Code principlescovered in the review include board composition, risk management andinternal controls and disclosure on remuneration. According to theSingapore Directorship Report2 launched in November 2014, less than athird (31%) of entities discloses the precise remuneration of their directors,although the Code Guideline 9.2 requires this disclosure. This is the mostsignificant non−compliance of the Code. In view of these, companies can

1 The report examined 229 listed companies on the SGX, provides insights into current trendsin NED remuneration and board governance (board composition, structure and meetings)among listed companies.

2 The report was jointly launched by the Singapore Institute of Directors (SID) and the Instituteof Singapore Chartered Accountants (ISCA). It examines the structure of boards and theircomposition, director tenure, remuneration, meeting attendance, gender diversity and multipledirectorships, and provides answers to questions that are frequently asked regardingdirectorships. It also documents elements of compliance with key aspects of the Code.

Section or Chapter title

Board Matters Quarterly | March 2016 6

expect shareholders’ scrutiny over the reasons forthis reluctance of Boards to comply with theremuneration disclosure requirement.

Alignment of Company Performance andRemuneration Outcomes

Shareholders and the media will continue to focus onkey management personnel (KMP), particularly theCEO, and the remuneration structure and quantum ofemoluments. This is particularly challenging whencompany performance has been disappointing orwhere a decline in share price results in significantincrease in the number of share awards proposed.

The key challenge lies in shifting the focus from “howmuch directors and executives are paid” to the basisof “how” and “why” directors and executives are paidthe way they are.

Companies should be well−prepared to support theperformance metrics in their incentive plans includingcomparable groups (listed peer companies) used fortesting of relative performance, and vesting scalesused in long−term incentive plans.

Remuneration of Non−Executive Directors(NED)

The Statement of Good Practice (SGP) issued by SIDindicated that fee rates for NED can be approached intwo directions:

► A consideration of the time spent by directors toensure that fees are compelling.

► An external reference provides the necessaryinput to ensure that fee levels are in line withmarket practices.

The SGP also issued a guideline on a fee structure,which is based on a multiple of a base fee in relationto the different work levels and responsibilities ofvarious NED. Companies should take intoconsideration this SGP as a comparison basis whenestablishing NED fee.

An early and proactive approach to shareholderengagement should have a positive influence on yourremuneration report and related resolution votingoutcomes. Alignment of reward with companyperformance, together with clear and objectivecommunications, will set your company up for asmoother ride through AGM.

Elaborate on yourcompany’sperformance andsignificant events,such as Mergers &Acquisitions (M&A)and capital raisingoccurred during theyear and followingthe year end.Consider their impacton the pay−out orvesting of short− andlong−term incentiveplans.

Be able to justifydirectors’remunerationvis−a−visdividend policy.

Prior to the voting resolutions on the remunerationand directors’ equity…

Section or Chapter title

Board Matters Quarterly | March 2016 7

3 Tenure of directorship andmultiple directorshipsThe widely−held beliefs

The length of service of directors and number of Board seats held bydirectors has always been one of the key concerns among shareholders:

► There has been argument that Independent Directors who have stayedtoo long on the Board may develop too cozy a relationship with themanagement or the majority shareholders and thus may affect theirindependence.

► Having multiple directorships may affect the level of commitmentrequired of a director.

The findings

While the SID−ISCA Singapore Directorship Report confirmed somewidely−held beliefs, the report had a few surprise findings:

► Multiple directorships do not appear to be a major problem as iscommonly perceived. More than 82% of all directors only sit on oneBoard, and merely 12.3% of IDs sit on more than two Boards. Thisshows that there is a significant breadth in the pool of IDs.

► Directors with multiple directorships had a better attendance record atBoard meetings. Over 90% of them attended more than three−quartersof all Board meetings, compared to 80% of single−seat directors. Thissuggests that directors with multiple directorships take the effort todedicate sufficient time and attention to their directorships.

Shareholders are questioning whether they have the right people on theirBoards for the challenges ahead. As such, providing comprehensiveinformation can assist in making the case for the election and re−election ofdirectors who have the Board’s endorsement. Boards can also assistshareholders in understanding the process for nominating and selectingdirectors by:

► Being explicit about the skills and expertise the Board is seeking andshowing heightened awareness of systemic risk.

► Building shareholder confidence in the effectiveness and suitability ofthe Board’s candidates through a rigorous appointment process. Boardscould conduct a performance appraisal for each director seekingre−election and communicate this to shareholders as part of theinformation provided in support of the election process.

► Communicate to the institutional shareholders about the strength of theBoard team and their skills for leading the company through difficulttimes.

Questionsfor the Boardsand AuditCommittee (AC)to considerIt is also necessary toreflect on the followingquestions in preparation foran AGM:

► Communicating theBoard’s rationale fordirector nominations. Dothe directors,particularly the NEDhave the relevantindustry experience tosit on the Board? If thenominees do not havethe relevant industryknowledge, what valuecan these nomineesbring to the Board?

► How does the Boardassess the independenceof their directors?

► Are fresh perspectivesintroduced among theBoard?

► Is the companyconsidering moves tolimit directorships andcommittee membershipsin the future? Why hasthe Board chosen adirector who also holdsdirectorship on multipleother Boards?

► How the nominatingcommittee assesses theability of directors tocommit their time toeffectively dischargetheir responsibilities?

► If the CEO is also a NEDof an unrelatedcompany, is the CEOable to fulfill the roleeffectively as well as actas a NED?

► Directors who have notattended substantiallyall of the meetings mayhave their attendancerecord challenged andshould be able toaccount for theirabsences.

Section or Chapter title

Board Matters Quarterly | March 2016 8

4 DividendsOne of the simplest ways for companies to communicate financial well−beingand shareholder value is to say "the dividend will be credited to youraccount". Dividends send a clear, powerful message about future prospectsand performance. A company's willingness and ability to pay steadydividends over time provides good indicator about its fundamentals.Shareholders are likely to hold strong expectations of companies with whichthey have shared a history of reliable, consistent dividend payments. Theywill want to know what dividend payments they can expect in future.

For companies where dividends are not common practice, the fall in equityvalues has similarly created concern among shareholders and reduced theirinvestments. For this group of shareholders, the yield on their stock is muchmore important than the asset value. The bottom line is that dividendsmatter. Profits on paper say one thing about a company’s prospects; profitsthat produce cash dividends say another thing entirely.

We recommend that the company communicate with shareholders about thecompany’s broad dividend strategy, and how any downturn is being dealtwith. This would assist shareholders in understanding the pressurescompanies are facing and the need for dividend reductions. In addition,letters from the Chairman in the annual report can be effective incommunicating the Board’s message to shareholders.

5 Board compositionThe SID−ISCA Singapore Directorship Report shows that about 97% of allBoards comply with the requirement to have IDs making up one−third oftheir composition.Moving forward, in situations where (i) the Chairman and CEO is the sameperson or they are immediate family members, (ii) the Chairman is part ofthe management team, or (iii) the Chairman is not independent, the newGuideline 2.2 requires ID to make up at least half of the Board composition.Listed companies need to comply with this new guideline at AGM followingthe end of the FY commencing from 1 May 2016 onwards (i.e., latest by 30April 2018 for 31 December year−end listed companies).Although this new guideline does not come into effect yet, the SID−ISCASingapore Directorship Report shows that 54.5% of all Boards alreadyhaving ID comprise at least half of their Board.

However, this also shows that the lack of SID−ISCA Singapore DirectorshipReport independent Chairman on Boards remains one of the moreprominent corporate governance gaps which could or should be improved.Although the Code recommends that Boards have ID as their Chairmen, only18.4% have independent Chairmen. Nearly a third has Chairmen who areCEO, and 57% have executive Chairmen.

Given investors’ increasing focus on Board composition, the Board shouldstart its transition plan and process to ensure compliance with the Code.

Questionsfor the Boardsand AC toconsider► What factors have driven

the company’s shareprice performance?

► What action, if any, isbeing taken to arrestpoor performance?

► Can the current Boardand managementillustrate an ability toexecute statedstrategy?

► Why is share pricetrading below net assetvalue per share orcomparable listedcompanies?

Board with independent chairman18%

Board with non-independent chairman84%

The Code recommends that Boards have IDas their Chairmen.

Source: SID−ISCA Singapore DirectorshipReport

Section or Chapter title

Board Matters Quarterly | March 2016 9

6 Selection of auditorBy opining on the true and fairness of financial statements, the auditorplays a key role in preserving and strengthening confidence in Singapore’sbusiness and financial markets. However, the audit opinion is only oneaspect of the value derived from an audit. The shareholders may be keen tounderstand the key factors the AC considered when deciding on theappointment and reappointment of auditor. For instance, did the ACconsider the following:

► How have the AC assessed the suitability of the auditor forappointment/ reappointment?

► Had the AC used the Audit Quality Indicators (AQIs) DisclosureFramework released by ACRA in October 2015 as part of the aboveevaluation? The AQIs provide AC with a comparable basis on which toconduct a conversation on the effort, experience and resources that anaudit firm will bring to bear on a particular audit.

An effective and high-quality external audit framework promotes confidencein the integrity of financial information and assists investors in their capitalallocation decisions.

Section or Chapter title

Board Matters Quarterly | March 2016 10

7 ACRA’s Financial ReportingSurveillance ProgrammeOn the financial reporting front, the Accounting and Corporate RegulatoryAuthority (ACRA) issued its inaugural report on key findings on FY2013financial statements of listed companies under its Financial ReportingSurveillance Programme (FRSP) in September 2015. The report revealedthat there is still room for improvement as a number of instances of non-compliance with the accounting standards were identified. Out of a total of49 sets of financial statements reviewed, only two companies went throughthe review with no enquiries raised. In fact, directors of four companiesreceived warning letters from ACRA, arising from instances of severe non-compliance. The FSRP review focused on areas that would significantlyimpact revenue, profit and operating cash flows. Key findings in the reportpointed to companies misclassifying operating cash flows, inappropriateaccounting for mixed-use property and revenue recognition, andinappropriate consolidation.

In addition, ACRA also published the FRSP areas of review focus for theFY2015 Financial Statements in December 2015 whereby it is bringingtougher corporate governance rules and possible enforcement actionagainst directors for violations under the Companies Act. For companiesthat were subjected to the FRSP review, companies can expect shareholders’scrutiny over ACRA’s findings, if any. The Board should determine how torespond to shareholders during AGM.

8 Reporting of financial resultsand performance issuesHaving read the annual reports, shareholders may come prepared to querythe directors on details of the Chairman’s statement and operations andfinancial review for the FY. Leading up to AGM, the directors should be fullybriefed on the likely questions that may be raised. The following arefinancial and operational considerations that are likely to be top of mind forshareholders.

Causes ofnon-compliance by

directors asidentified by ACRA

Over-relianceon accounting team

who may lackcompetence or diligence

Insufficientscrutiny

of financialstatements

Management’sjudgement not

adequatelychallenged

The ACRA’s FRSPrevealed that there isstill room forimprovement as anumber of instancesof non-compliancewith the accountingstandards wereidentified.

The FRSP Keyfindings under ACRA’sFRSP pointed tocompanies► misclassifying

operating cashflows,

► inappropriateaccounting formixed-useproperty

► revenuerecognition, and

► inappropriateconsolidation.

Section or Chapter title

Board Matters Quarterly | March 2016 11

Questions for the Boards and AC to consider

Concernedwith debtmanagementissues

For entities with debt management issues, the following can be of concern toshareholders:

► Does the company have any plans to go to market for additional capital raising and ifso, will it be made available to all classes of shareholder?

► Has it been necessary to strengthen debt management processes by re−negotiatingdebt covenants; negotiating extended payment terms with suppliers; or assessingaccess to short−term capital?

► Have all triggers of covenant default been reviewed and assessed across allagreements, business activities and group entities to address the risk of contagion?

► What is the current performance against banking covenants?

► How has the company sought to build transparent relationships with debt providers,equity analysts and rating agencies?

Operationaland financialreview

► What is the business outlook for the new FY and its impact on the entity’s business?

► Has management considered the new tax measures proposed under SingaporeBudget 2015, and its impact on the entity’s operations?

► What are the recent changes in laws and regulations (such as the Listing Rules andthe Code), and their impact on the entity’s business? Is the entity already incompliance?

► Where does the company stand within the respective business segments orgeography, e.g., market share, price positioning and brand positioning?

Plannedexpenditureof resource

Are there areas (country or region, product or process) which the Board or topmanagement envisages that:

► Management will have to spend more time?

► Will see additional manpower (headcount) deployed?

► Will require more financial resources? For example, capacity expansion andacquisitions.

► Will see a reduction in resources? For example, capacity reduction and assetdivestments.

Internalcontrols andriskmanagement

► Is the Board or a specific sub−committee responsible for risk management oversight?

► Has an enterprise’s risk management evaluation been performed? If yes, what are thekey areas of concern? What is management doing to deter and detect fraud?

► Is the focus of risk management largely on financial risks or does the company alsoconsider operational, strategic and compliance risk?

► Has the Board received a report from management as to the effectiveness of riskmanagement efforts? How does the CEO and CFO gain comfort over the adequacy offinancial records, the system of internal control and risk management over financialstatements?

► What are the deficiencies in internal controls, instances of fraud or illegal acts (if any)communicated by either the independent or internal auditors?

► What changes in internal control have been made, or are planned, to address thedeficiencies identified?

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 12

Over

the

last

few

years,

we

have

seen

significant

cha

nges

and

developments

on

the

accounting

fronw

financi

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 13

Singapore Budget2016Singapore’s Minister for Finance, Mr. Heng SweeKeat, delivered the 2016 Budget for the financialyear 1 April 2016 to 31 March 2017 inParliament on 24 March 2016.We highlight some of the key changes.

The 2016 Budget focuses on transforming theeconomy through enterprise and innovation, andbuilding a caring and resilient society with a strongspirit of partnership.

While tackling the immediate cyclical downturn,2016 Budget aims to steer Singapore towardseconomic transformation to ensure its continuedrelevance amidst the rapidly changing globaleconomic and competitive landscape, catalysed bytechnological disruptions. These objectives will beachieved by supporting enterprises and industries totransform, and driving transformation throughinnovation with targeted measures, investing inskills development, and enhancing and investing insocial infrastructure and care measures.

A number of tax changes were announced to helpbusinesses address their near-term concerns arisingfrom the cyclical slowdown and to supportbusinesses and industries in transformation andinnovation so as to be well-placed to compete in thechanging global economic environment whenbroader global recovery happens.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 14

Addressing near-term concerns

1. Enhancing the Corporate Income Tax (CIT)rebate for year of assessment (YA) 2016 andYA 2017: The CIT rebate will be raised from30% to 50% for YA 2016 and YA 2017, subjectto a cap of S$20,000 rebate per YA.

Transforming enterprises

2. Automation Support Package: SPRING willimplement an Automation Support Packagecomprising four components to support firms toautomate, drive productivity and scale up:

a) Capability Development Grant: TheCapability Development Grant will beexpanded to support the roll-out or scalingup of automation projects at up to 50% ofthe qualifying cost. The grant is capped atS$1m.

b) Investment Allowance (IA): Qualifyingprojects may be eligible for an IA of 100%on the amount of approved capitalexpenditure, net of grants. This IA is inaddition to the existing capital allowance forplant and machinery. The approved capitalexpenditure is capped at S$10m perproject.

c) Enhanced financing support: Thegovernment will increase the risk-share withparticipating financial institutions underSPRING’s Local Enterprise Finance Schemeequipment loan, from 50% to 70% forqualifying projects undertaken by Small andMedium Enterprises (SMEs). The LocalEnterprise Finance Scheme will also beexpanded to cover equipment loan for non-SMEs at 50% risk-share with participatingfinancial institutions.

d) IE Singapore and SPRING will work togetherwhere relevant to help businesses to accessoverseas markets.

3. Enhancing the Mergers and Acquisitions(M&A) scheme: To support more M&As, theexisting cap for qualifying M&A deals will bedoubled from S$20m to S$40m such that:

a) Tax allowance of 25% will be granted for upto S$40m of consideration paid forqualifying M&A deals per YA; and

b) Stamp duty relief will be granted for up toS$40m of consideration paid for qualifyingM&A deals per financial year.

This change will take effect for qualifying M&Adeals made from 1 April 2016 to 31 March2020. IRAS will release further details by June2016.

4. Extending the upfront certainty of non-taxation of companies’ gains on disposal ofequity investments under section 13Z of theIncome Tax Act (ITA): The scheme under section13Z will be extended until 31 May 2022 (tocover disposal of equity investments from 1June 2017 to 31 May 2022). All conditions ofthe scheme remain unchanged.

5. Extending the Double Tax Deduction (DTD) forInternationalisation scheme: The DTD forInternationalisation scheme will be extended foranother four years from 1 April 2016 to 31March 2020. The existing automatic DTD onexpenses up to S$100,000 will also beextended to qualifying expenditure incurredduring this period (1 April 2016 to 31 March2020). All other conditions of the schemeremain unchanged. IE Singapore will releasefurther details by June 2016.

6. Enhancing the Land Intensification Allowance(LIA) scheme: The LIA scheme grants an initialallowance of 25% and an annual allowance of 5%on the qualifying capital expenditure incurredfor the construction or renovation of aqualifying building or structure. To encouragehigher industrial land productivity, the schemewill be extended to buildings used by a user ormultiple users, who are related, for one ormultiple qualifying trades or businesses, ifcertain conditions are met. In addition, a newcriterion requiring LIA applicants to be relatedto the qualifying user or users of the buildingwill be introduced. These changes will takeeffect for LIA applications if:

a) The application for LIA is made from 25March 2016; and

b) The application for planning permission orconservation permission for theconstruction or renovation is made from25 March 2016.

The qualifying capital expenditure for which anallowance may be made excludes anyexpenditure incurred before 25 March 2016.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 15

Transforming through innovation

7. Providing an election for the writing-downperiod for intellectual property rights (IPRs)under section 19B of the ITA: Under section19B of the ITA, companies or partnerships canclaim writing-down allowance (WDA) on theacquisition cost of qualifying IPRs over a periodof five years. To recognise the varying usefullives of IPRs, while maintaining a simple andcertain tax regime, companies or partnershipsmay elect for their section 19B WDA to beclaimed over a writing-down period of five, 10or 15 years. The election must be made at thepoint of submitting the tax return of the YArelating to the basis period in which thequalifying costs is first incurred. The election,once made, is irrevocable. This change willapply to qualifying IPR acquisitions made withinthe basis periods for YA 2017 to YA 2020. IRASwill release further details by 30 April 2016.

8. Introducing an anti-avoidance mechanism forIPR transfers under section 19B of the ITA: Ananti-avoidance mechanism for IPR transfers willbe included under section 19B to empower theComptroller to make the following adjustmentsto the transacted price of the IPR, if the IPR isnot transacted at open market value (OMV):

a) If the acquisition price of the IPR is higherthan the OMV of the IPR, the Comptrollermay substitute the acquisition price withthe OMV of the IPR and restrict the WDAbased on the OMV of the IPR; and

b) If the disposal price of the IPR is lower thanthe OMV of the IPR, the Comptroller maysubstitute the disposal price with the OMVof the IPR for the purpose of computingbalancing charge.

This change will apply to acquisitions, sales,transfers or assignments of IPRs that are madefrom 25 March 2016.

Shift from broad-based support

9. Allowing the Productivity and InnovationCredit (PIC) scheme to lapse and lowering thecash payout rate: Under the PIC scheme,businesses can convert qualifying expenditureinto a non-taxable cash payout at a cash payoutrate of 60% on up to S$100,000 of expenditureacross six qualifying activities per YA. The cashpayout rate will be lowered from 60% to 40% forqualifying expenditure incurred from 1 August2016.

The PIC scheme was extended in Budget 2014for three years (YA 2016 to YA 2018). It willexpire and will not be available from YA 2019.

Strengthening the competitiveness of themaritime sector

10. Enhancing the Maritime Sector Incentive(MSI): To further develop Singapore as anInternational Maritime Centre, the MSI will beenhanced as follows:

a) The MSI-Shipping Enterprise (SingaporeRegistry of Ships) (MSI-SRS) and MSI-Approved International Shipping Enterprise(MSI-AIS) award will cover income derivedfrom operation of ships used for explorationor exploitation of offshore energy oroffshore minerals, or ancillary activityrelating to exploration or exploitation ofoffshore energy or offshore minerals.

b) The MSI-Maritime Leasing (Ship) [MSI-ML(Ship)] award will cover income derivedfrom leasing of ships used for exploration orexploitation of offshore energy or offshoreminerals, or ancillary activity relating toexploration or exploitation of offshoreenergy or offshore minerals.

c) The restriction on the qualifyingcounterparty’s requirement under MSI-ML(Ship) award will be removed. Therefore, taxexemption will be granted on incomederived from leasing of ships used forqualifying activities to any counterpartiesfor use outside the port limits of Singapore.

The above changes will take effect from 25March 2016. MPA will release further details ofthe change in (a) and (b) above by June 2016.

Nurturing a caring and resilient society

11. Introducing the Business and IPC PartnershipSchemes (BIPS): To incentivise employeevolunteerism through businesses, a pilot BIPSwill be introduced from 1 July 2016 to 31December 2018. Under BIPS, businesses willenjoy an additional 150% tax deduction onwages and incidental expenses when they sendtheir employees to volunteer and provideservices to Institutions of a Public Character(IPCs), including secondments. This will besubject to the receiving IPCs’ agreement, with ayearly cap of S$250,000 per business andS$50,000 per IPC on the qualifying costs. MOFand IRAS will release further details byJune 2016.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 16

Other changes

12. Introducing mandatory electronic-filing (e-Filing) for CIT returns (including EstimatedChargeable Income, Form C and Form C-S):Mandatory e-Filing of CIT returns will beimplemented in stages as follows:

► YA 2018: Companies with turnover ofmore than S$10m in YA 2017

► YA 2019: Companies with turnover ofmore than S$1m in YA 2018

► YA 2020: All companies

13. Introducing mandatory electronic-filing (e-Filing) for PIC cash payout application:Mandatory e-Filing of PIC cash payoutapplications will be introduced. The mandatorye-Filing of PIC cash payout applications will beeffective from 1 August 2016.

Business Grants Portal

14. Business Grants Portal: To improve access tothe range of incentive schemes administered byvarious government agencies, a BusinessGrants Portal will be launched for grantapplication. The portal will start with grants

from IE Singapore, SPRING, STB and DesignSingapore and progressively expand to includegrants from other government agencies.

National Trade Platform

15. National Trade Platform: To supportbusinesses, particularly in the logistics andtrade finance sectors, a National TradePlatform will be developed as the next-generation platform. This platform will serveas a one-stop trade informationmanagement system to allow electronic datasharing amongst businesses andgovernment agencies and aims to becomean open innovation platform to allow serviceproviders to formulate value-added servicesand apps in areas such as operations,visibility and trade finance. This platform willeventually replace the current TradeNet andTradeXchange systems.

Read more about this year's budget measuresand the business implications in EY’s SingaporeBudget 2016 Synopsis and our SingaporeBudget 2016 website.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 17

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 18

Finally, the newleases standardIt’s more than bringing leases on balance sheet

In January 2016, the International AccountingStandards Board issued the new InternationalFinancial Reporting Standard (IFRS) 16 Leases,which will replace the existing InternationalAccounting Standard 17 that was introduced morethan 30 years ago. IFRS 16 is mandatorily effectivefor annual periods beginning on or after 1 January2019. Early adoption is permitted, provided that thenew revenue standard IFRS 15 is adopted at thesame time. In Singapore, the Accounting StandardsCouncil is expected to adopt IFRS 16 soon.

Essentially, the new leases standard seeks to addresscriticisms that the existing off-balance sheetaccounting for operating leases does not portray thetrue economics of leases.

We look at what is the new leases accounting model,and how different will your financials look.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 19

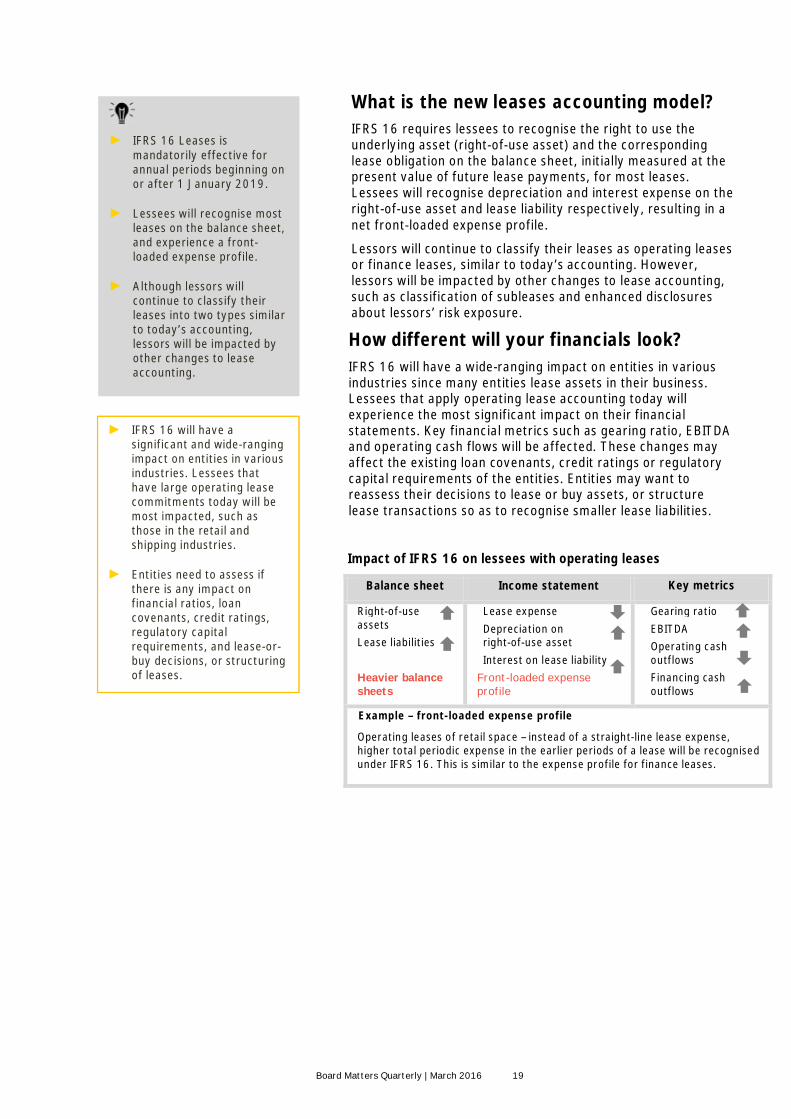

What is the new leases accounting model?IFRS 16 requires lessees to recognise the right to use theunderlying asset (right-of-use asset) and the correspondinglease obligation on the balance sheet, initially measured at thepresent value of future lease payments, for most leases.Lessees will recognise depreciation and interest expense on theright-of-use asset and lease liability respectively, resulting in anet front-loaded expense profile.

Lessors will continue to classify their leases as operating leasesor finance leases, similar to today’s accounting. However,lessors will be impacted by other changes to lease accounting,such as classification of subleases and enhanced disclosuresabout lessors’ risk exposure.

How different will your financials look?IFRS 16 will have a wide-ranging impact on entities in variousindustries since many entities lease assets in their business.Lessees that apply operating lease accounting today willexperience the most significant impact on their financialstatements. Key financial metrics such as gearing ratio, EBITDAand operating cash flows will be affected. These changes mayaffect the existing loan covenants, credit ratings or regulatorycapital requirements of the entities. Entities may want toreassess their decisions to lease or buy assets, or structurelease transactions so as to recognise smaller lease liabilities.

Impact of IFRS 16 on lessees with operating leases

Balance sheet Income statement Key metrics

Right-of-useassetsLease liabilities

Heavier balancesheets

Lease expenseDepreciation onright-of-use assetInterest on lease liability

Front-loaded expenseprofile

Gearing ratioEBITDAOperating cashoutflowsFinancing cashoutflows

Example – front-loaded expense profile

Operating leases of retail space – instead of a straight-line lease expense,higher total periodic expense in the earlier periods of a lease will be recognisedunder IFRS 16. This is similar to the expense profile for finance leases.

► IFRS 16 Leases ismandatorily effective forannual periods beginning onor after 1 January 2019.

► Lessees will recognise mostleases on the balance sheet,and experience a front-loaded expense profile.

► Although lessors willcontinue to classify theirleases into two types similarto today’s accounting,lessors will be impacted byother changes to leaseaccounting.

► IFRS 16 will have asignificant and wide-rangingimpact on entities in variousindustries. Lessees thathave large operating leasecommitments today will bemost impacted, such asthose in the retail andshipping industries.

► Entities need to assess ifthere is any impact onfinancial ratios, loancovenants, credit ratings,regulatory capitalrequirements, and lease-or-buy decisions, or structuringof leases.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 20

More about the new leases standardIn this section, we have identified some key aspects of IFRS 16, and highlight our preliminaryobservations on the considerations that the directors or management should take note of.

Considerations for directors or management

1. Lease versus servicecontracts?

► Although the concept underlying the definition of a lease is broughtforward from the existing standard, the distinction between lease andservice contracts will become more important under IFRS 16 because

(1) Leases will be recognised on the balance sheet while service contractsare not.

(2) Expense recognition pattern for leases will be front-loaded whileexpenses incurred for services are generally recognised on a straight-line basis.

► Similarly, the identification of the non-lease components (e.g. sale of goodor service) in multi-element contracts will become more important underIFRS 16, since only the lease component will be recognised on balancesheet. The practical expedient that permits lessees to account for thelease and non-lease components as a single lease will be useful where thenon-lease component is not significant.

► Examples of contracts that may require closer examination of whether itis a lease or service contract include contracts for the use of ships,aircraft, or network services. The contract qualifies as a lease if itconveys the right to control the use of an identified asset to the customerover a period of time.

2. Can any leases beexempted?

► Lessees can be exempted from capitalising leases and recognise lease expenseon a straight-line basis for the following leases:

(1) Short-term leases (by class of underlying asset) - with lease terms of 12months or less, or

(2) Leases of low-value assets (on a lease-by-lease basis) – where thelessee can benefit from using the asset on its own or together withother readily available resources, and the asset is not highly dependenton, or highly interrelated with other assets.

► The determination of whether a lease term is short-term is not merelybased on the non-cancellable lease period, and has to consider the effectsof extension options and purchase options.

► The assessment of ‘low-value assets’ is based on the value of the assetwhen it is new, and on an absolute basis.

Examples of leases that qualify for exemption:

► Leases of low-value assets such as tablets and personal computers,small items of office furniture and telephones.

► 9-month lease of an apartment, with a 3-month lease extension optionthat the lessee is reasonably certain to exercise.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 21

Considerations for directors or management

3. What are includedin the leasepayments?

► Currently minimum lease payments mainly comprise fixed lease payments.IFRS 16 requires variable lease payments that depend on an index or a rate(initially measured using the index or rate at the commencement date) anddisguised in-substance fixed payments, to be included in the lease paymentsto be capitalised on the balance sheet.

► Other types of non-index based variable payments, such as those that arelinked to future use or sales, will not be included in the capitalised leasepayments.

Examples of lease payments to be included:

► Variable payments linked to consumer price index or benchmarkinterest rate (e.g. LIBOR).

► In-substance fixed payments that may, in form, contain variability (e.g.dependent on production volume), but are subject to an annual minimumpayment.

4. What are theongoingreassessmentrequirements?

► IFRS 16 imposes ongoing reassessment requirements on lessees, for instance,when there are changes to index-based lease payments, or significant changesin circumstances that is within the lessee’s control and will impact theassessment of the lease term (e.g. significant change in business decision thataffects the lessee’s decision to extend a lease).

5. Are sale andleasebacktransactionsimpacted?

► Since sale and leaseback transactions will almost always be on thebalance sheet, there may be reduced incentive for sellers to enterinto these transactions under IFRS 16.

► Determining whether a sale has occurred in a sale and leasebacktransaction depends on whether control of the underlying asset istransferred to the buyer, as opposed to today’s accounting which focuseson whether it is an operating or finance leaseback.

► After adjusting for off-market terms, any gain on the sale recognised underIFRS 16 will be smaller than that recognised today, since the gain isrecognised only on the rights transferred to the buyer-lessor.

6. Are subleasesimpacted?

► In sublease arrangements, the head lease and sublease are accounted foras separate transactions consistent with other lease arrangements.

► The intermediate lessor, being the lessee of the head lease, will experiencechanges to its balance sheet and income statement profiles, similar toother lessees.

► With respect to the sublease, the intermediate lessor will classify the subleasewith reference to the right-of-use asset arising from the head lease, ratherthan the underlying asset as currently required. Hence, there may be moresubleases classified as finance leases that are currently classified asoperating leases in the books of the intermediate lessor.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 22

Towards a smooth implementationIFRS 16 takes effect on 1 January 2019. Earlyadoption is possible if the new revenue standardIFRS 15 is also applied.

Transition► Lessees can choose to use a full retrospective

approach to restate comparative figures, or amodified retrospective approach. Under thelatter approach, the lessee recognises thecumulative effect of initially applying IFRS 16as an adjustment to equity. There are also anumber of practical expedients provided, forexample, the new leases requirements need notbe applied to leases ending within 12 months.

► Lessors are not required to make adjustmentson transition, except for intermediate lessors insubleases.

► IFRS 16 provides transitional relief in a numberof areas. For example, entities can choose not

to reassess whether existing contracts containa lease. Entities are not required to reassessexisting sale and leaseback transactions todetermine whether a sale has occurred.

Next stepsAs a critical first step towards successfulimplementation, entities should gain a thoroughunderstanding of the effects of IFRS 16. Given thewide-ranging and significant impact of IFRS 16 onmany entities, the three-year implementationtimeframe is not a long time for entities to startassessing the impact of the new standard andestablishing processes and systems to capture theinformation needed. In fact, an early assessmentwill be the key to managing the implementationprocess for the adoption of the new leasesstandard. In addition, early communication to bothinternal and stakeholders are also important toensure a smooth implementation process.

How can EY help you?Through our Financial & Accounting Advisory Services (FAAS), we can provide assistance on your currentcritical accounting and related issues, including managing and implementation of the new leases standard,complex accounting and reporting issues, GAAP conversion support, accounting processes and controlssupport. For more information, please contact Mr. Ronald Wong at +65 6309 6155 | [email protected],or contact your audit partners.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 23

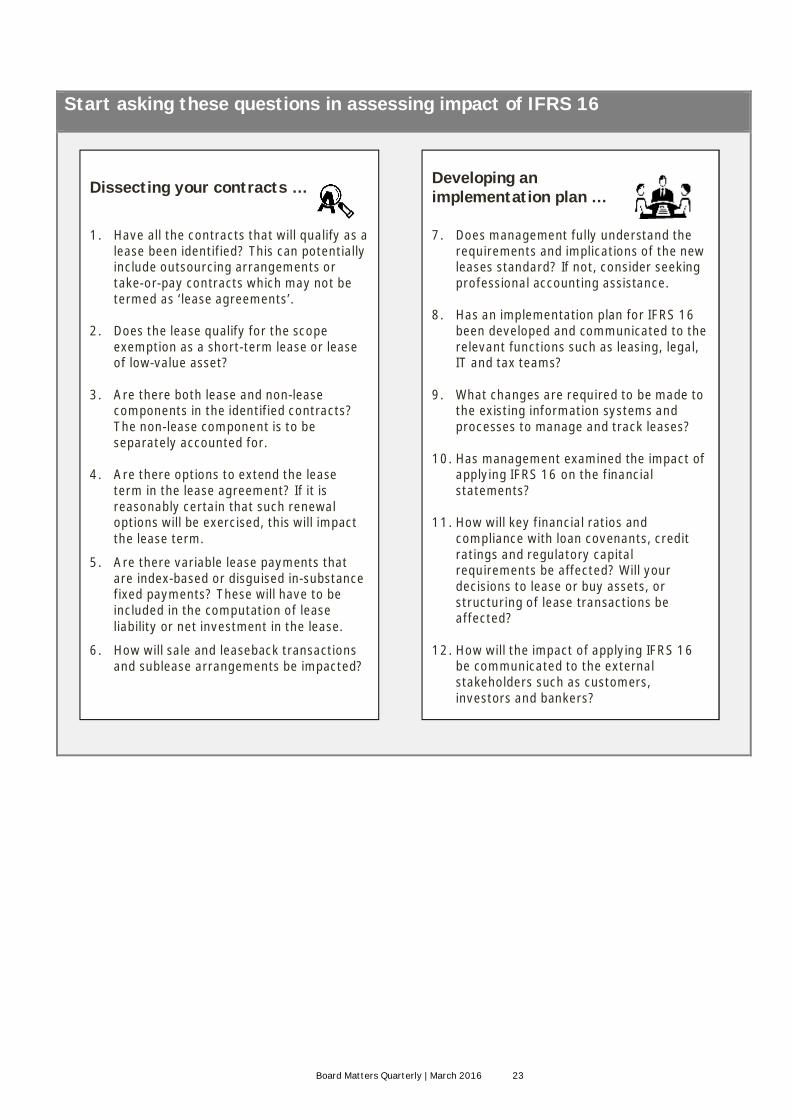

Start asking these questions in assessing impact of IFRS 16

Developing animplementation plan …

7. Does management fully understand therequirements and implications of the newleases standard? If not, consider seekingprofessional accounting assistance.

8. Has an implementation plan for IFRS 16been developed and communicated to therelevant functions such as leasing, legal,IT and tax teams?

9. What changes are required to be made tothe existing information systems andprocesses to manage and track leases?

10. Has management examined the impact ofapplying IFRS 16 on the financialstatements?

11. How will key financial ratios andcompliance with loan covenants, creditratings and regulatory capitalrequirements be affected? Will yourdecisions to lease or buy assets, orstructuring of lease transactions beaffected?

12. How will the impact of applying IFRS 16be communicated to the externalstakeholders such as customers,investors and bankers?

Dissecting your contracts …

1. Have all the contracts that will qualify as alease been identified? This can potentiallyinclude outsourcing arrangements ortake-or-pay contracts which may not betermed as ‘lease agreements’.

2. Does the lease qualify for the scopeexemption as a short-term lease or leaseof low-value asset?

3. Are there both lease and non-leasecomponents in the identified contracts?The non-lease component is to beseparately accounted for.

4. Are there options to extend the leaseterm in the lease agreement? If it isreasonably certain that such renewaloptions will be exercised, this will impactthe lease term.

5. Are there variable lease payments thatare index-based or disguised in-substancefixed payments? These will have to beincluded in the computation of leaseliability or net investment in the lease.

6. How will sale and leaseback transactionsand sublease arrangements be impacted?

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 24

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 25

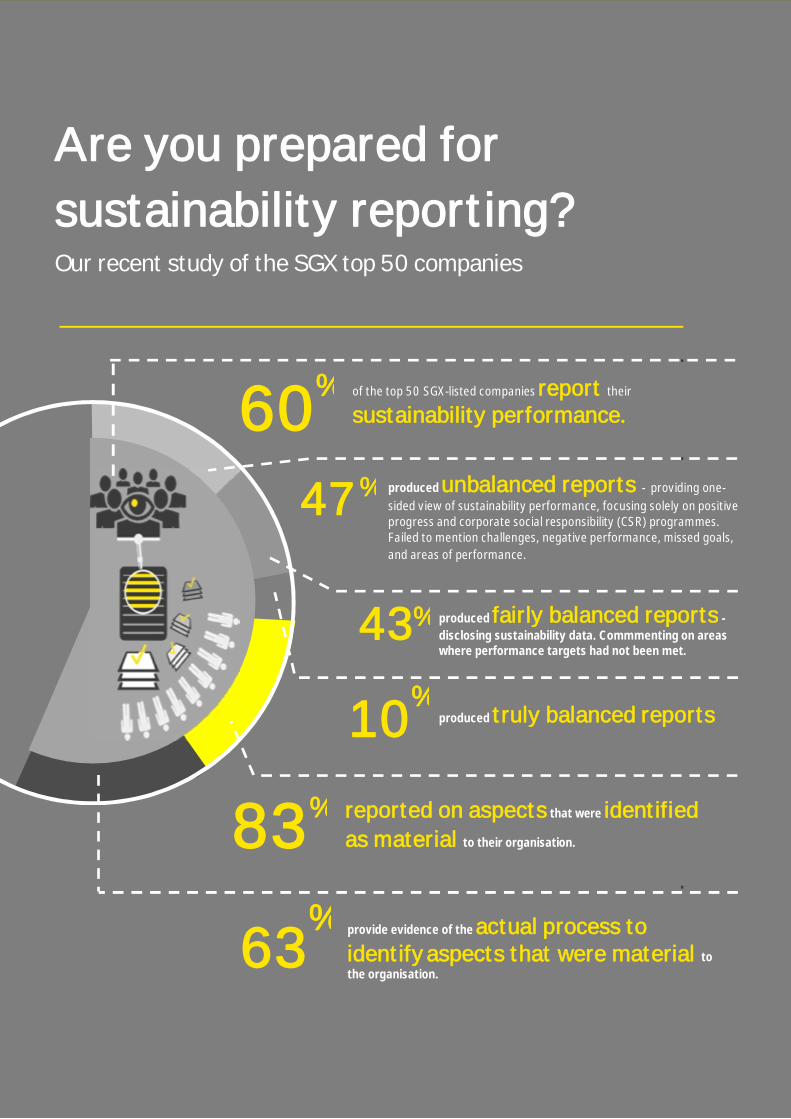

SustainabilityreportingOur recent study of the SGX top 50 companies revealed that only 60% oftop 50 SGX-listed companies report their sustainability performance, andclose to half produce one-sided, unbalanced report. Are we there yet?

In 2017, the SGX is expected to implement the “comply orexplain” rule to sustainability reporting and disclosures.Globally there is clear evidence of a growing reliance on non-financial information by investors, who more than ever, areconsidering non-financial performance to draw conclusions onvalue and better inform and underpin their decisions.

Yet, many organisations still fail to meet investor expectationsin terms of availability – and quality — of their reporting onenvironmental, social and economic sustainability performance.

Although sustainability practices and reporting has seen muchintegration over the years, there’s no “holy grail” to thereporting, with some companies doing it in Singapore but manyothers still not. Further, it may be easy to demonstratenumbers and achievements in sustainability but the crux lies inthe materiality and quality of disclosures, and how thosedisclosures ultimately add value to the readers in lendingbusiness insights.

A 2015 EY study of the top 50 companies on the SGX revealedthat there is significant room for improvement in sustainabilityreporting in Singapore: only 60% of the top 50 SGX-listedcompanies report their sustainability performance. Of these, 47%produced unbalanced reports – providing one-sided view of theirsustainability performance, focusing solely on positive progressand corporate social responsibility (CSR) programmes and failingto mention challenges, negative performance, missed goals andareas of performance.

Forty-three percent produced reports that were fairly balanced,with many disclosing sustainability data and commenting on areaswhere performance targets had not been met. Just 10% producedreports that could be considered truly balanced – providing a widerange of performance data, disclosure on whether specific targetswere met and any negative impact of the company’s operationsand how these impacts were managed.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 26

Some businesses may think that a report should onlytell pink stories. A quality report should disclose facts,be transparent and concise, and tell it as it is. Forexample, companies with previous slip-ups can takethe chance to rectify and improve on them whilesimultaneously outlining to stakeholders thecorrective policy being put in place. This presents agreat branding and communication opportunity torestore and boost credibility.

There is also a need to debunk the misconceptionabout the difficulty in producing qualitysustainability reports. Many think that the processis complicated, costly, time-consuming and requiresa lot of effort. However, the curve is actually notthat insurmountable. With a logical concept andintuitive planning, it is easier than one thinks.

Indeed, the quality of sustainability reporting is acontinuum. Different companies are on differentparts of this continuum – some have yet to start;others are disclosing some information but far fromreporting what truly matters.

Placing emphasis on materialityTo ensure quality in their sustainability reporting,companies must first need to know what aspects ofsustainability are considered as material to them.

The emphasis on materiality in recent times signalsa clear change from sustainability reporting of thepast — where companies, aiming to report on the“triple bottom line” of social, environmental andeconomic aspects, often released a mass ofinformation covering everything from paperrecycling to human rights. In those cases, therewas little regard to the relative importance of thesedisclosures to their business’ performance, or to

the relative importance of each aspect to theirstakeholders.

The definition of “material” is based on thethreshold at which an issue becomes importantenough to a company and its stakeholders. Mattersthat cross that threshold are treated as materialand these may include matters of qualitativeimportance – not just tangible units – too.Companies should capture those matters thatimpact their largest stakeholders, discuss withindepartments and report these in details.

Despite reporters investing significant time andeffort in preparing increasingly larger reports,investors and other key stakeholders were leftfrustrated by the need to sift through volumes ofinformation to find the aspects of most importanceto them. Their dissatisfaction is highlighted in EY’s2015 Global Investor Survey which found thatinvestors face a sever deficit of useful non-financialinformation.

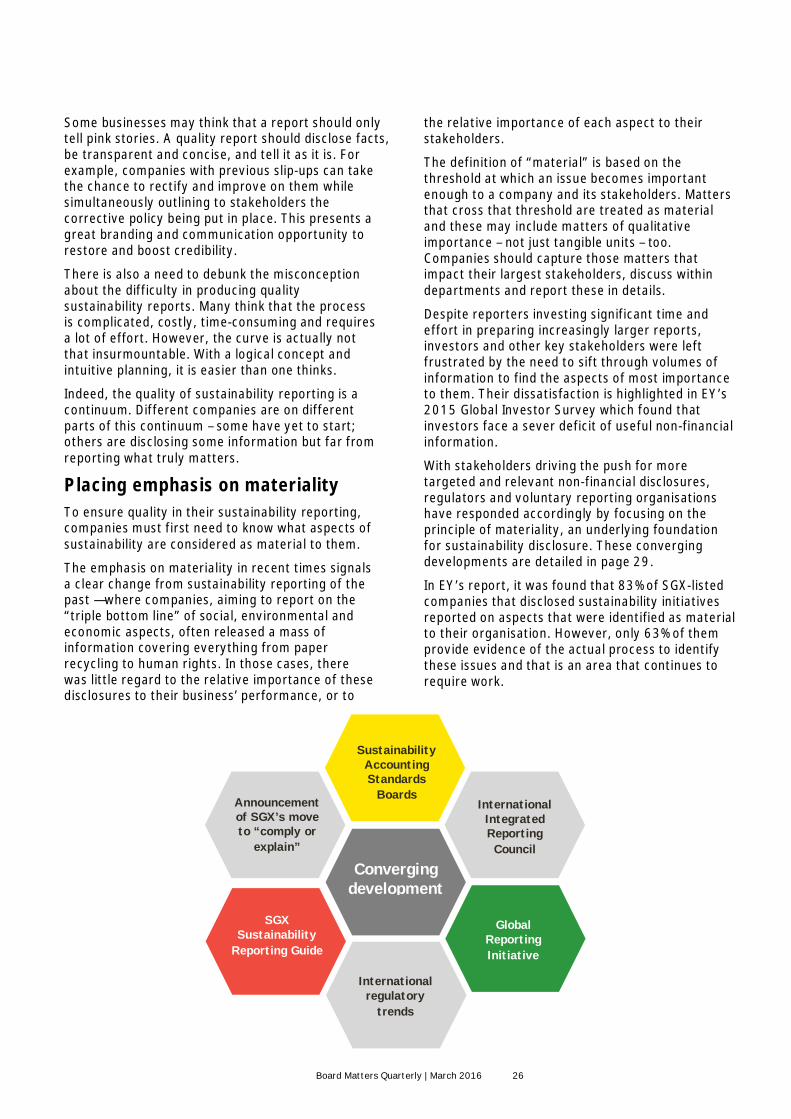

With stakeholders driving the push for moretargeted and relevant non-financial disclosures,regulators and voluntary reporting organisationshave responded accordingly by focusing on theprinciple of materiality, an underlying foundationfor sustainability disclosure. These convergingdevelopments are detailed in page 29.

In EY’s report, it was found that 83% of SGX-listedcompanies that disclosed sustainability initiativesreported on aspects that were identified as materialto their organisation. However, only 63% of themprovide evidence of the actual process to identifythese issues and that is an area that continues torequire work.

Convergingdevelopment

InternationalIntegratedReportingCouncil

GlobalReportingInitiative

Internationalregulatory

trends

SGXSustainability

Reporting Guide

Announcementof SGX’s moveto “comply or

explain”

SustainabilityAccountingStandards

Boards

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 27

producedtruly balanced reports

reported on aspects that were identifiedas material to their organisation.

Are you prepared forsustainability reporting?Our recent study of the SGX top 50 companies

of the top 50 SGX-listed companiesreport their

sustainability performance.60%

47%

63%

10%

producedunbalanced reports - providing one-sided view of sustainability performance, focusing solely on positiveprogress and corporate social responsibility (CSR) programmes.Failed to mention challenges, negative performance, missed goals,and areas of performance.

producedfairly balanced reports -disclosing sustainability data. Commmenting on areaswhere performance targets had not been met.

43%

83%

provide evidence of theactual process toidentifyaspects that were material tothe organisation.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 28

Getting ready for “comply or explain”With SGX implementing the “comply or explain”rule to sustainability reporting and disclosures by2017, it is expected that there will be a substantialshift in the level of sustainability disclosures inSingapore.

However, compliance in itself cannot be the onlymotivation. The bigger reason for companies toinvest in quality sustainability reporting must bethat the world is now more sensitive tosustainability issues and that Singapore companiesare now very much a part of the global supplychain.

Whether it is of their own accord or succumbing tobusiness operations, businesses have to embracesustainability practices. Once they start to operatemore sustainably, they will naturally have more toreport on.

As more organisations integrate sustainabilityconcerns into their core business strategy, it isexpected that there will be greater alignment offinancial and non-financial reporting. Integratedreporting that links financial results with thebusiness context will continue to gain popularity ascompanies respond to growing demands bysophisticated investors for such information.

SGX consults on “comply or explain” sustainability reporting rules and guide

SGX will be introducing sustainability reporting on a “comply or explain” basis and is inviting public comment onthe proposed rules and guide. This marks further progress from the voluntary reporting that has been in placesince 2011. SGX expects the new rules and guide on sustainability reporting to apply to companies from thefinancial year ending on, or after 31 December 2017, with reports published from 2018.

Sustainability reporting complements financial reporting with the environmental, social and governance (ESG)aspects of business and strategy, to give investors better insight into the companies they invest in. This enablesinvestors to more comprehensively assess a company’s prospects and quality of management. The increaseddisclosure enhances transparency and builds investor understanding and trust over time.

SGX’s survey of institutional investors in June 2015 found that over 90% of respondents consider ESG factorswhen investing.

The “comply or explain” approach to sustainability reporting gives companies the latitude of reporting in the waywhich best suits their industry and circumstances. In the reports, companies describe what they do to managematerial ESG risks and business opportunities.

In its consultation, SGX is seeking comments on several proposals. Specifically, issuers will have to include fiveprimary components in a sustainability report, as follows:

1. Identification of material ESG factors, giving reasons for their choice and a description of the process ofselection.

2. Policies, practices and performance of the company in relation to each of the material ESG factors, in bothdescriptive and quantitative terms. Performance should be discussed in the context of any previouslydisclosed targets.

3. Targets for the forthcoming year.4. A chosen reporting framework to guide the disclosure of relevant information on the ESG factors. Using an

internationally recognised or industry-relevant framework enhances acceptance and comparability.5. A statement of the board confirming compliance with the primary components or description of any

alternative practices with reasons for preferring them.

SGX is also consulting on the following:

1. That companies report only material ESG factors.2. That reports be published within five months from the end of each financial year.3. Whether anti-corruption and diversity aspects, which are receiving global attention, should be included as a

primary component in a sustainability report.4. The roles and responsibilities assigned to the Board with regards to sustainability reporting.

This public consultation ended in February 2016.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 29

Converging developments

SGX Sustainability ReportingGuidelines Move to ‘comply or explain’ basis International Integrated Reporting

Council

The SGX released their Guide toSustainability Reporting for ListedCompanies in 2011 (the Guide) toincrease their transparency inreporting on sustainability issues.While reporting is not mandatory, theguide provides the suggestion that allcompanies should disclose theirsustainability performance, andprovides basic actions regarding howto report and what to report on.

SGX will be introducing sustainabilityreporting on a “comply or explain”basis and is inviting public commenton the proposed rules and guide.

This marks further progress from thevoluntary reporting that has been inplace since 2011. SGX expects thenew rules and guide on sustainabilityreporting to apply to companies fromthe financial year ending on, or after31 December 2017, with reportspublished from 2018.

The International IntegratedReporting Council (IIRC) wasestablished in 2010 and released theInternational <IR> Framework inDecember 2013. Adoption of theframework is gathering momentumwith materiality underpinning itsvision to report on the factors criticalto value creation across six ‘capitals’– financial, manufactured,intellectual, human, social andrelationship and natural.

International regulatory trends Global Reporting Initiative andAccountAbility AA1000

Sustainability AccountingStandards Board

The SGX Guide to SustainabilityReporting for Listed Companies andthe move to a ‘comply or explain’basis are reflective of aninternational trend towards non-financial sustainability disclosure.Research released in 2013 by theGlobal Reporting Initiative (GRI)reviewed reporting requirementsfrom 45 countries and found 180policies specific to sustainabilitydisclosures, of which 72 per centwere mandatory. In September 2014the EU published its requirements fornon-financial disclosures with a focuson environment, social andemployee-related aspects.

The Global Reporting Initiative (GRI)is the most commonly usedinternational framework forsustainability reporting. The latestiteration of its guidelines, GRI G4,was released in 2013 withmateriality as a fundamental guidingprinciple.

The Sustainability AccountingStandards Board (SASB) wasestablished at Harvard University in2011 and is aimed at developingsustainability accounting standardswhich include analysis of materialaspects for a range of industries.

AccountAbility produces widely-usedstandards and leading research onsustainability. Their AA1000Assurance Standard is used globally,and is complemented by theirGuidance Note on the Principles ofMateriality, Completeness andResponsiveness.

About the studyEY’s Materiality and sustainability disclosure: Keyinsights from the SGX top 50 studies the sustainabilitydisclosure of the top 50 SGX-listed companies by marketcapitalisation. The research took the form of a desktopanalysis in which we examined publicly available annualreports, sustainability reports and company websites.The companies included in this research were thoseforming the SGX top 50 as at 20 August 2015. Thisinformation was reviewed as at 29 September 2015.Download the report here.

Let’s continue the conversationFind out how we can help you tackle your sustainabilitychallenges atey.com/SG/en/Services/Assurance/Climate-Change-and-Sustainability-Services

ContactMr. K. Sadashiv, Singapore and Asean Leader, ClimateChange and Sustainability ServicesTel: +65 6309 8813Mob: +65 9008 [email protected]

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 30

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 31

Hong Kong Budget2016-17The Financial Secretary, John Tsang, delivered hisBudget speech on 24 February 2016. We highlightsome of the key proposals that affect businesses.

DownloadHong Kong 2016-17Budget Insights

Hong Kong 2016-17Budget Tax Facts

Highlights► Reduce profits tax, salaries tax and tax

under personal assessment for 2015-16 by75%, capped at $20,000

► Waive government rates for 2016-17,capped at $1,000 per quarter for eachrateable property

► Waive business registration fees for 2016-17

► Waive licence fees for tourism-relatedindustries including food outlets for a year

► Extend tax deductions for capitalexpenditure on the purchase of intellectualproperty rights to cover layout-design ofintegrated circuits, plant varieties and rightsin performance

► Issue “inflation-linked retail bond” (iBond)worth up to $10 billion; issue “Silver Bond”(targeting at Hong Kong residents aged 65or above)

Details of the Hong Kong Budget 2016−17 areavailable on the Hong Kong Budget website. Youcan also read more about EY’s detailed commentson our website.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 32

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 33

Regulatory updates

1. Forty-one companiesplaced on SGX watch-list dueto Minimum Trading Price(MTP) requirementsForty-one Mainboard companies will beplaced on Singapore Exchange’s (SGX)watch-list from 3 March 2016 becausethey do not comply with the MTPrequirement. These companies have 3years to carry out actions to improvetheir share price. The full list ofcompanies on the watch-list is found onthe SGX website.

2. SGX revised calculationmethodology for MTPSGX is changing the methodology usedto determine whether a company shareprice meets the minimum trading price(MTP) requirement. The change comesafter SGX’s extension to 1 September2016 to review the volume weightedaverage price (VWAP) of shares ofcompanies which consolidate theirshares before 1 March 2016.In addition, SGX is granting the sameextension to 1 September 2016 forcompanies which have experienced - forthe first time - a dip in their VWAP belowS$0.20 due to the extreme marketvolatility in January 2016. The extensionwill allow these companies – which numberabout 20 as at end-January 2016 – time toevaluate their options and take action tocomply with the MTP requirement.The VWAP of shares following a shareconsolidation will now be computed basedon historical prices adjusted for theconsolidation ratio. Previously, the VWAP

was computed based on the total value ofsecurities traded for the 6 months underreview divided by the total volume tradedfor the 6 months. The VWAP of the shareswill now reflect fully the impact of acompleted share consolidation. This willreduce the risk of companies having toconsolidate shares at extremely highratios, or for repeated corporate action.SGX introduced an MTP for shares ofMainboard companies in March 2015 toreduce the risk of excessive speculationfollowing the extreme volatility of low-capitalisation stocks in October 2013. Therequirement takes effect from 1 March2016 after a 1-year transition period.More details are available on the SGXwebsite.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 34

3. SGX sought feedback onproposed amendments toalign Listing Rules withCompanies ActSGX is consulting the public on proposedMainboard and Catalist Listing Ruleschanges, including the electronictransmission of notices and documents toshareholders. The proposals are to alignthe Rules with the amended Companies Actpassed in October 2014.SGX is also seeking feedback on policypositions highlighted by other recentstatutory changes.On the transmission of electronic noticesand documents such as circulars andannual reports, SGX seeks feedback on:► Whether there are concerns if

companies are allowed to electronicallytransmit these materials toshareholders with their impliedconsent. Implied consent means thecompany’s articles of associationprovide for electronic communicationand shareholders will not have theoption to receive physical copies ofmaterials; and

► Whether companies should be allowedto do so when consent fromshareholders is expressly, or deemedto have been, obtained.

In addition to the above, SGX also seeksviews and comments on:► Safeguards for electronic transmission

of notices and documents

► Insurance coverage and indemnities fordirectors

► Restraint on exercise of voting rights► Treatment of shares held by a

subsidiary in its holding companyConsultation period has ended on 12February 2016.

4. SGX proposedintroducing 10% allocationof Mainboard IPO sharesfor retail investorsSGX is proposing that Mainboardcompanies allocate to retail investors aminimum 10% of shares in their initialpublic offers (IPOs), up to a maximum ofS$100 million. This is aimed at givingindividuals more investing opportunities inthe Singapore equities market.This is the second consultation on theintroduction of a mandated minimum IPOallocation to retail investors. The firstconsultation in 2012 proposed a 5% retailallocation.The increase in the proposed retail IPOallocation percentage follows positivefeedback for a minimum allocation ofshares in IPOs to retail investors from the2012 consultation. In addition, over 90% ofIPOs which occurred in 2010 to 2015 hadretail investor application rates which weregreater than 10% of the total offer size,indicating retail demand for IPO shares.More details are available on the SGXwebsite.

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 35

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 36

Changes to FRS effective in 2016The following new or revised Financial Reporting Standards (FRS) and interpretations are effective for financialperiods beginning on or after 1 January 2016. Listed companies with December financial year−end mustconsider the impact of the following in 2016.

The following new or revised FRS and interpretations that are available for early adoption in 2016.

The Accounting Standards Council is expected to adopt IFRS 16 Leases soon. IFRS 16 is mandatorily effectivefor annual periods beginning on or after 1 January 2019.

New or revised FRS Details in EY publications

Amendments to FRS 16 and FRS 41: Agriculture− Bearer Plants IFRS Developments Issue 84

Amendments to FRS 27: Equity Method in Separate Financial Statements

Amendments to FRS 16 and FRS 38: Clarification of Acceptable Methods of Depreciationand Amortisation

IFRS Developments Issue 78

Amendments to FRS 111: Accounting for Acquisitions of Interests in Joint Operations

Improvements to FRSs (November 2014)

► Amendments to FRS 105: Changes in methods of disposal

► Amendments to FRS 107: Servicing contracts; applicability of the amendments toFRS 107 to condensed interim financial statements

► Amendments to FRS 19: Regional market issue regarding discount rate

► Amendments to FRS 34: Disclosure of information elsewhere in the interim financialreport

IFRS Developments Issue 91

Amendments to FRS 1: Disclosure Initiative IFRS Developments Issue 98

Amendments to FRS 110, FRS 112 and FRS 28: Investment Entities: Applying theConsolidation Exception

IFRS Developments Issue 97

New or revised FRS Effective date(financial periodbeginning on orafter)

Details in EY publications

Amendments to FRS 7: Disclosure Initiative 1 January 2017 −

Amendments to FRS 12: Recognition ofDeferred Tax Assets for Unrealised Losses

−

FRS 115 Revenue from Contracts withCustomers

1 January 2018 IFRS Developments Issue 80Applying IFRS: A Closer Look at the New RevenueRecognition Standard

FRS 109 Financial Instruments IFRS Developments Issue 86IFRS Developments Issue 87Applying IFRS: Hedge accounting under IFRS 9Applying IFRS: Impairment of financial instrumentsunder IFRS 9

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | March 2016 37

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction andadvisory services. The insights and quality services wedeliver help build trust and confidence in the capitalmarkets and in economies the world over. We developoutstanding leaders who team to deliver on ourpromises to all of our stakeholders. In so doing, we playa critical role in building a better working world for ourpeople, for our clients and for our communities.

EY refers to the global organisation, and may refer to oneor more, of the member firms of Ernst & Young GlobalLimited, each of which is a separate legal entity.Ernst & Young Global Limited, a UK company limitedby guarantee, does not provide services to clients.For more information about our organisation,please visit ey.com.

EY | Assurance | Tax | Transactions | Advisory

© 2016 Ernst & Young LLP.

All Rights Reserved.

Ernst & Young LLP (UEN T08LL0859H) is a limitedliability partnership registered in Singapore under theLimited Liability Partnerships Act (Chapter 163A).

APAC no. 12000731

ED None

Ernst & Young LLP (UEN T08LL0859H) is a limited liability partnershipregistered in Singapore under the Limited Liability Partnerships Act (Chapter 163A).

This material has been prepared for general informational purposes onlyand is not intended to be relied upon as accounting, tax, or otherprofessional advice. Please refer to your advisors for specific advice.

www.ey.com