blueknight investor presentation august 2020 downstream

TRANSCRIPT

Private & Confidential

Blueknight Investor Presentation August 2020

Downstream Terminalling Solutions for Tomorrow’s Infrastructure and Transportation End Markets

2Private & Confidential

Legal Disclaimer

Forward-Looking Statements

This presentation includes forward-looking statements. Statements included in this presentation that are not historical facts (including, without limitation, anystatements about future financial and operating results, guidance, projected or forecasted financial results, objectives, project timing, expectations and intentionsand other statements that are not historical facts) are forward-looking statements. Such forward-looking statements are subject to various risks and uncertainties.These risks and uncertainties include, among other things, the Partnership’s ability to pay future distributions, uncertainties relating to the Partnership’s debt levelsand restrictions in its credit facility, its exposure to the credit risk of our third-party customers, the Partnership’s future cash flows and operations, future marketconditions, current and future governmental regulation, future taxation and other factors discussed in the Partnership’s filings with the Securities and ExchangeCommission. If any of these risks or uncertainties materializes, or should underlying assumptions prove incorrect, actual results or outcomes may vary materiallyfrom those expected. The Partnership undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information,future events or otherwise.

This presentation contains the non-GAAP financial measures of Adjusted EBITDA and total operating margin, excluding depreciation and amortization. AdjustedEBITDA is defined as earnings before interest, income taxes, depreciation and amortization, non-cash equity-based compensation, asset impairment charges, gainsand losses on asset sales and other select items which management feels decreases the comparability of results among periods. Operating margin, excludingdepreciation and amortization is defined as revenues from related parties and external customers less operating expenses, excluding depreciation and amortization.The use of Adjusted EBITDA and operating margin, excluding depreciation and amortization should not be considered as alternatives to GAAP measures such asoperating income, net income or cash flows from operating activities. Adjusted EBITDA and operating margin, excluding depreciation and amortization arepresented because the Partnership believes they provide additional information with respect to its business activities and are used as supplemental financialmeasures by management and external users of the Partnership’s financial statements, such as investors, commercial banks and others to assess, among otherthings, the Partnership’s operating performance and return on capital as compared to those of other companies in the midstream energy sector, without regard tofinancing or capital structure.

Blueknight does not provide GAAP financial measures, including reconciliations, on a forward-looking basis because the partnership is unable to predict withreasonable certainty impairments, depreciation and amortization, non-cash equity based compensation, the ultimate outcome of legal proceedings and acquisitionrelated expenses.

3Private & Confidential

Blueknight’s Robust and Unique Platform

Asphalt Terminalling

• 8.8 million barrels of asphaltand residual fuel oil storage

• 53 terminals across 26 states• Largest independently

owned asphalt network

Pipeline and Trucking

• OK pipeline system withcombined capacity of50,000 bpd

• 63 trucks• XTO crude oil dedication

and minimum volumecommitment

Downstream Terminalling Solutions for Tomorrow’s Infrastructure and Transportation End Markets

Asphalt TerminallingCrude Oil Terminalling

Pipeline Trucking

• Master limited partnership established in 2007 andheadquartered in Tulsa, Oklahoma

• Geographically-diversified, high-quality assets in26 states

• Stable cash flows underpinned by long-term, take-or-pay contracts and over 50% of revenue frominvestment grade customers

• Common and preferred units on NASDAQ under“BKEP” and “BKEPP”, respectively

2019 Operating Margin Contribution

2019 TerminallingRevenue %

Take-Or-Pay

AsphaltTerminalling 80%

16%Crude Oil

Terminalling

93%

Crude Oil Terminalling

• 6.6 million barrels ofCushing, OK storage

• Operate additional 1.0million barrels forTransMontaigne

• Strong connectivity andblending capability

Take-Or-Pay

Source: Company reports; note operating margin excludes depreciation and amortization

4Private & Confidential

Ergon, Inc., a Leading Asphalt Marketer and Blueknight Sponsor

A Leading Energy Company With Over Six

Decades of Market Experience

Diversified Portfolio

• Private, family-owned, diversified company in petroleum, road construction materials and real estate

• Formed in 1954 and based in Jackson, Mississippi

• Largest customer of Blueknight with commercial services in 28 of the 53 asphalt facilities

• General partner of Blueknight since 2016

High Quality, Supportive Sponsor

Midstream and Logistics Oil and GasAsphalt and EmulsionsRefining and Marketing

• Presence in over 12 countries worldwide; over 2,500 employees globally

• One of the largest asphalt emulsion marketers in the U.S.

• Refining & Marketing: refinery operations and marketing of crude oil and various refined products includingspecialty naphthenic and paraffinic products

• Asphalt & Emulsions: production, marketing and distribution of paving and specialty asphalt products

• Midstream & Logistics: logistics support including a fleet of river, road and rail transportation equipment alongwith numerous terminal locations and pipelines

• Oil & Gas: retail distribution network for propane, mid-river fleeting, refueling & supply, and oil & gasexploration and development

5Private & Confidential

MLP Organizational Structure with Two Public Securities

• Blueknight General Partnerownership: Ergon, Inc.

• Two classes of publicly tradedequity (NASDAQ):

─ Series A Preferred Units: BKEPP

─ Common Units: BKEP

Blueknight Energy Partners G.P., L.L.C. (DE)

BKEP Operating Subsidiaries

Blueknight Energy Partners, L.P. (DE)

Blueknight GP Holding, LLC (DE)

1.6% General Partner Interest

100.0% Ownership Interest

100.0% Ownership Interest

71.2% Limited Partner Interest

Ergon Asphalt & Emulsions, Inc.

100.0% Ownership Interest

Ergon, Inc.

27.2% Limited Partner Interest

Ergon Asphalt Holding, LLC

Public Unitholders

$400 million Senior Secured Credit Facility

(1) Market capitalization includes BKEP and BKEPP(2) Market data as of 8/11/20(3) Unit count and balance sheet data as of Q2 2020 filings

NASDAQ Tickers BKEP & BKEPP

Market Capitalization ($ millions) (1,2,3) $270

Enterprise Value ($ millions) (2,3) $538

Annual BKEP Distribution ($/unit) $0.16

Annual BKEPP Distribution ($/unit) $0.72

Source: Company reports

Highlights and Strategy

7Private & Confidential

Blueknight Investment Highlights

• Robust, geographically-diversified system of logistics terminalling solutions focused on niche end markets

• Largest independently-owned network of 53 asphalt terminals across the U.S. in major markets

• Highly strategic terminal at Cushing Interchange with 6.6 million barrels of crude oil storage

Unique Platformof High-Quality Terminal Assets

1

• Target long-term leverage of 3.5x and coverage on all distributions greater than 1.2x

• 2020 guidance with adjusted EBITDA outlook in-line with 2019; internally generated cash flow to fully fund 2020distribution payments with expected coverage greater than 1.2x and debt leverage between 4.0x-4.25x

Disciplined Financial Principles and 2020 Guidance

3

• Stable earnings underpinned by 90%+ take-or-pay revenue, over 50% revenue from investment grade customers

• Minimal direct commodity exposure or dependence on U.S. upstream drilling activity and productionStrong Fee-BasedCash Flow Profile

2

• Core Asphalt Terminalling business driven more by infrastructure/road construction trends than oil & gascommodity markets; steady growth expected ahead for state and federal infrastructure spending

• Crude Oil Terminalling business in Cushing benefitting from deep 2020 crude oil contango market

FavorableIndustry Trends

Driving Continued Market Growth

4

• Leverage existing asset footprint to grow alternative specialty terminalling business in niche product markets

• Focus on opportunistic consolidation of competitor non-core asphalt facilities in key strategic markets

Focused Strategic Growth

Opportunities

5

• Seasoned management team with extensive and complementary industry experience

• Deep knowledge base and strong entrenched relationships within the highly specialized asphalt industryExperienced

Management Team

6

8Private & Confidential

($20.0)

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

2014 2015 2016 2017 2018 2019

Asphalt Terminalling Services Crude Oil Terminalling Services Crude Oil Pipeline Services Crude Oil Trucking Services

48% 63%

25%

68%

24%

5%

80%

22%

93%

12%

80%

16%

2015 Crude Oil Contango Environment

53%

24%

Unique and Stable Platform of High-Quality Terminal Assets1

• Diversified provider of downstream terminalling solutions for infrastructure and niche transportation end markets─ Robust platform of geographically diversified, high-quality terminal assets, representing 96% of total operating margin in 2019─ Over 90% of terminalling revenues supported by take-or-pay contractual agreements─ Minimal direct commodity exposure or dependence on U.S. upstream drilling activity and production─ Reviewing strategic options for crude oil pipeline and trucking businesses, including potential joint venture or sale

Blueknight Operating Margin Contribution ($ in Millions)

Source: Company reports; note operating margin excludes depreciation and amortization

9Private & Confidential

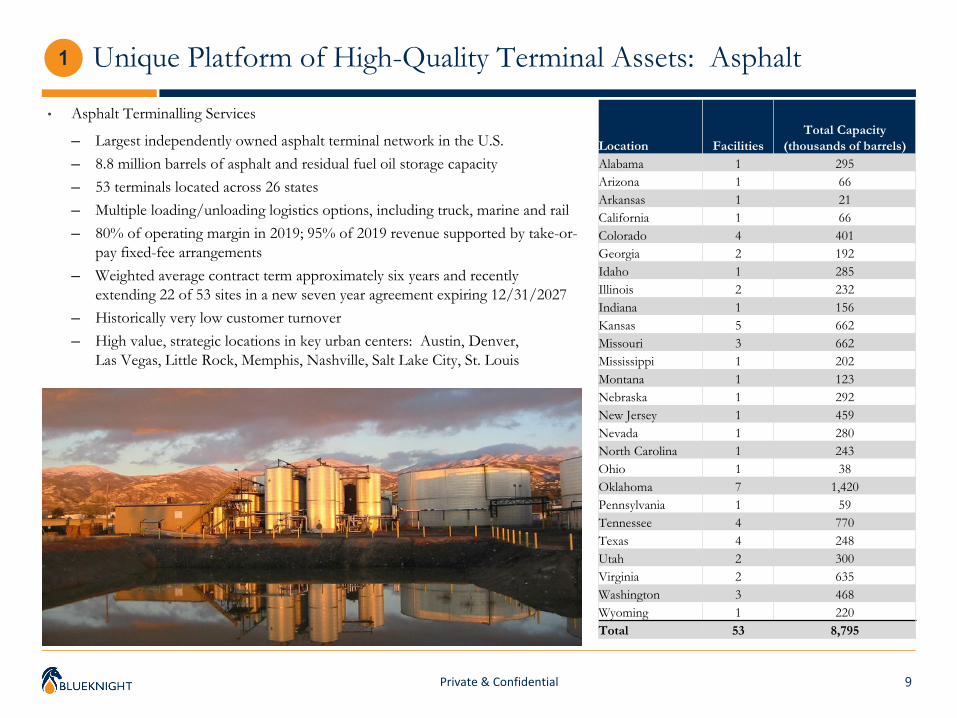

Unique Platform of High-Quality Terminal Assets: Asphalt 1

• Asphalt Terminalling Services

─ Largest independently owned asphalt terminal network in the U.S.─ 8.8 million barrels of asphalt and residual fuel oil storage capacity─ 53 terminals located across 26 states─ Multiple loading/unloading logistics options, including truck, marine and rail─ 80% of operating margin in 2019; 95% of 2019 revenue supported by take-or-

pay fixed-fee arrangements─ Weighted average contract term approximately six years and recently

extending 22 of 53 sites in a new seven year agreement expiring 12/31/2027─ Historically very low customer turnover─ High value, strategic locations in key urban centers: Austin, Denver,

Las Vegas, Little Rock, Memphis, Nashville, Salt Lake City, St. Louis

Location FacilitiesTotal Capacity

(thousands of barrels)Alabama 1 295 Arizona 1 66 Arkansas 1 21 California 1 66 Colorado 4 401 Georgia 2 192 Idaho 1 285 Illinois 2 232 Indiana 1 156 Kansas 5 662 Missouri 3 662 Mississippi 1 202 Montana 1 123 Nebraska 1 292 New Jersey 1 459 Nevada 1 280 North Carolina 1 243 Ohio 1 38 Oklahoma 7 1,420 Pennsylvania 1 59 Tennessee 4 770 Texas 4 248 Utah 2 300 Virginia 2 635 Washington 3 468 Wyoming 1 220 Total 53 8,795

10Private & Confidential

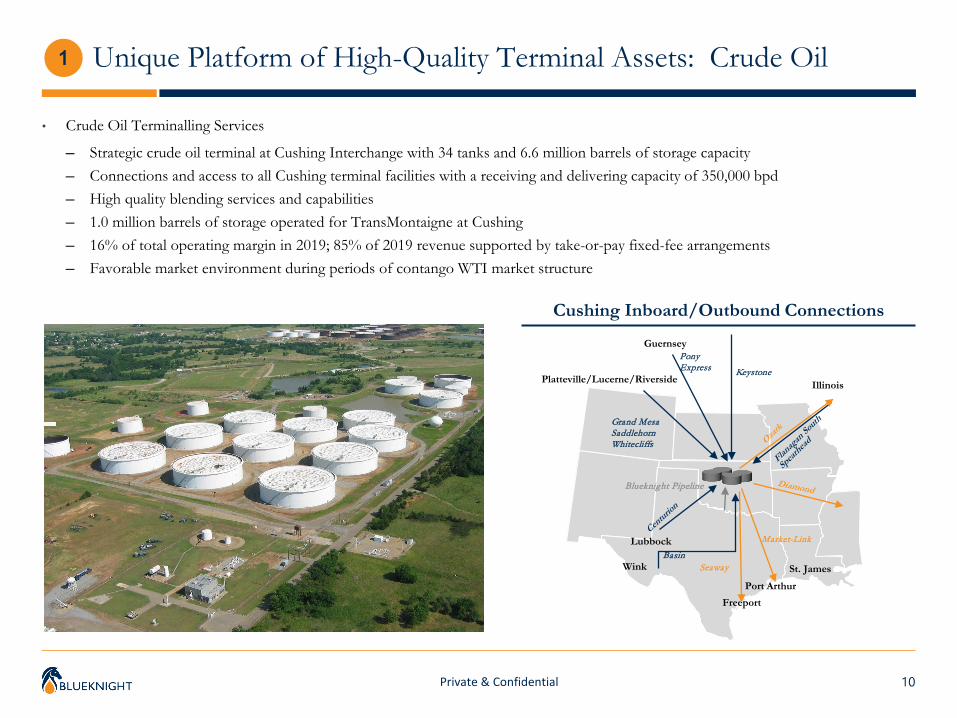

Unique Platform of High-Quality Terminal Assets: Crude Oil 1

• Crude Oil Terminalling Services

─ Strategic crude oil terminal at Cushing Interchange with 34 tanks and 6.6 million barrels of storage capacity─ Connections and access to all Cushing terminal facilities with a receiving and delivering capacity of 350,000 bpd─ High quality blending services and capabilities─ 1.0 million barrels of storage operated for TransMontaigne at Cushing─ 16% of total operating margin in 2019; 85% of 2019 revenue supported by take-or-pay fixed-fee arrangements ─ Favorable market environment during periods of contango WTI market structure

Cushing Inboard/Outbound Connections

Illinois

Wink

Lubbock

Platteville/Lucerne/Riverside

Guernsey

St. James

Port ArthurFreeport

Keystone

PonyExpress

Grand MesaSaddlehornWhitecliffs

Basin

Blueknight Pipeline

Seaway

Market-Link

11Private & Confidential

$0

$20

$40

$60

$80

$100

$120

$140

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

2014 2015 2016 2017 2018* 2019

WT

I ($

/bbl

)

BK

EP

Free

Cas

h Fl

ow ($

mill

ion)

Adjusted EBITDA WTI Price

Strong Fee-Based Cash Flow Profile 2

• Blueknight’s high-quality terminal assets generate stable, steady free cashflow generation despite oil price volatility

• Asset base positioned for minimal direct commodity exposure ordependence on upstream drilling activity and production

• Asphalt and Crude Oil Terminalling services underpinned by 95% and 85%contracted take-or-pay fixed-fees, respectively

Source: Company reports, FactSet

Adjusted EBITDA vs. WTI

* 2018: BKEP divested three asphalt terminals and its producer field services business

2019 Terminalling Segments Revenue Mix

Take-or-Pay 95%

Variable5%

Asphalt Terminalling

Take-or-Pay85%

Variable15%

Crude Oil Terminalling

12Private & Confidential

Strong Fee-Based Cash Flow Profile: High-Quality Customer Base 2

Select Crude Oil Terminalling CustomersSelect Asphalt Terminalling Customers Select Transportation Customers

• Strong support from high-quality, stable customer base across all businesses

• Over 50% of revenue from terminalling customers are investment grade entities

• Asphalt Terminalling customers typically significant players in the industry

─ Weighted average contract term of approximately 6 years─ Contract terms range from 5 to 10 years

• Crude Oil Terminalling customers typically trading and marketing firms and midstream entities

─ No upstream producers among customer base, minimal upstream counterparty risks

• XTO Energy primary customer of pipeline business, supported by minimum volume commitments and dedications

13Private & Confidential

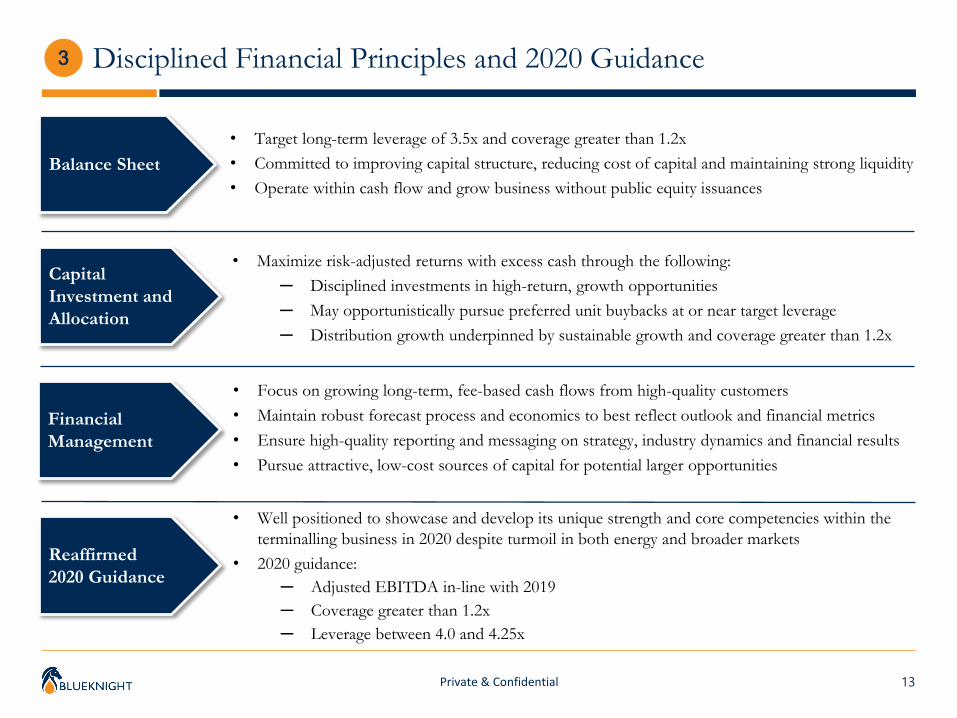

• Target long-term leverage of 3.5x and coverage greater than 1.2x• Committed to improving capital structure, reducing cost of capital and maintaining strong liquidity• Operate within cash flow and grow business without public equity issuances

• Maximize risk-adjusted returns with excess cash through the following:─ Disciplined investments in high-return, growth opportunities─ May opportunistically pursue preferred unit buybacks at or near target leverage─ Distribution growth underpinned by sustainable growth and coverage greater than 1.2x

Balance Sheet

Capital Investment and Allocation

Financial Management

• Focus on growing long-term, fee-based cash flows from high-quality customers• Maintain robust forecast process and economics to best reflect outlook and financial metrics• Ensure high-quality reporting and messaging on strategy, industry dynamics and financial results• Pursue attractive, low-cost sources of capital for potential larger opportunities

3 Disciplined Financial Principles and 2020 Guidance

Reaffirmed2020 Guidance

• Well positioned to showcase and develop its unique strength and core competencies within theterminalling business in 2020 despite turmoil in both energy and broader markets

• 2020 guidance:─ Adjusted EBITDA in-line with 2019─ Coverage greater than 1.2x─ Leverage between 4.0 and 4.25x

14Private & Confidential

Favorable Industry Trends Driving Continued Market Growth4

• Blueknight’s asphalt terminal business drivenlargely by transportation construction trends atfederal, state and local levels

• Terminal usage not dependent on E&P drillingor oil production activity

• ARTBA forecasting steady 3.9% CAGR of U.S.asphalt-related transportation construction from2018-24 to $164.6 billion for:─ Public highway and street work─ Private highway work─ Private driveway and parking lot work

• New federal infrastructure spending legislationproposed─ U.S. Senate: July 2019 vote to authorize

$287 billion for surface transportation needs─ Congressional Democrats: proposed $329

billion surface transportation spending plan─ Trump Administration: considering $2

trillion infrastructure stimulus plan in response to coronavirus pandemic market impacts

Source: American Road & Transportation Builders Association

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

E

2020

E

2021

E

2022

E

2023

E

2024

E

Public Highway, Street & Related Work Private Driveway & Parking LotPrivate Highway & Bridge Work

2020 Asphalt Transportation Construction Activity ($ in Billions)

15Private & Confidential

Focused Strategic Growth Opportunities5

• Strategic focus to transition towards a pure-playterminalling entity─ 2019 operating margin contribution

• Asphalt Terminalling: 80%• Crude Oil Terminalling: 16%

• Asphalt Terminalling system well optimizedoperationally─ Consistent, stable annual operating margin

contribution per site─ 3Q strongest seasonal period from peak paving

demand in summer months• Future growth prospects

─ Leverage existing assets to further develop advanced, customized terminalling solutions

─ Focus on growing terminalling business in new, specialty niche product markets

─ Heated storage tank infrastructure in place to leverage into renewable diesel and heavy oil markets

─ Evaluate opportunistic terminal acquisitions

Asphalt Segment Operating Margin Per Terminal($ thousand/terminal)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2016 2017 2018 2019** 2019: Asphalt Terminalling results negatively impacted by severe weather events in 2Q19

Quarterly Seasonality2016-19

(% of annual total)1Q 22%2Q 23%3Q 30%4Q 25%

Source: Company reports; note operating margin excludes depreciation and amortization

16Private & Confidential

Focused Strategic Growth Opportunities: Acquisition Targets5

• Blueknight operates the largest independently-owned U.S. network of 53 asphalt terminals

• Blueknight has a long history of successful asphalt terminal acquisitions, totaling approximately $175 million and representing 26% ofcurrent system facilities since May 2015

• Asphalt market characteristics─ Highly fragmented ownership: refiners, midstream entities, construction materials companies, paving contractors─ Terminals generally either (1) standalone, asphalt-only facilities, or (2) integrated into broader product terminals

• Opportunistic acquisition targets─ Refiner-owned, standalone facilities─ Materials company-owned, standalone facilities─ Standalone, non-integrated facilities

Blueknight Historical Asphalt AcquisitionsPurchase Price

Date Terminal Facility Seller ($ millions)Mar 2018 Muskogee, OK Frontier Terminal, LLC $22.0

Cummins Investment Corp.Dec 2017 Bainbridge, GA Ergon $10.2

Oct 2016 Birmingport, AL Nashville, TN Ergon $108.8 Chandler, AZ Ennis, TXWolcott, KS Mt. Pleasant, TXYellow Creek, MS Pleasanton, TXMemphis, TN

Feb 2016 Dumfries, VA Axeon Specialty Products $19.0 Wilmington, NC

May 2015 Cheyenne, WY Simon Contractors $13.9

Source: Company reports

17Private & Confidential

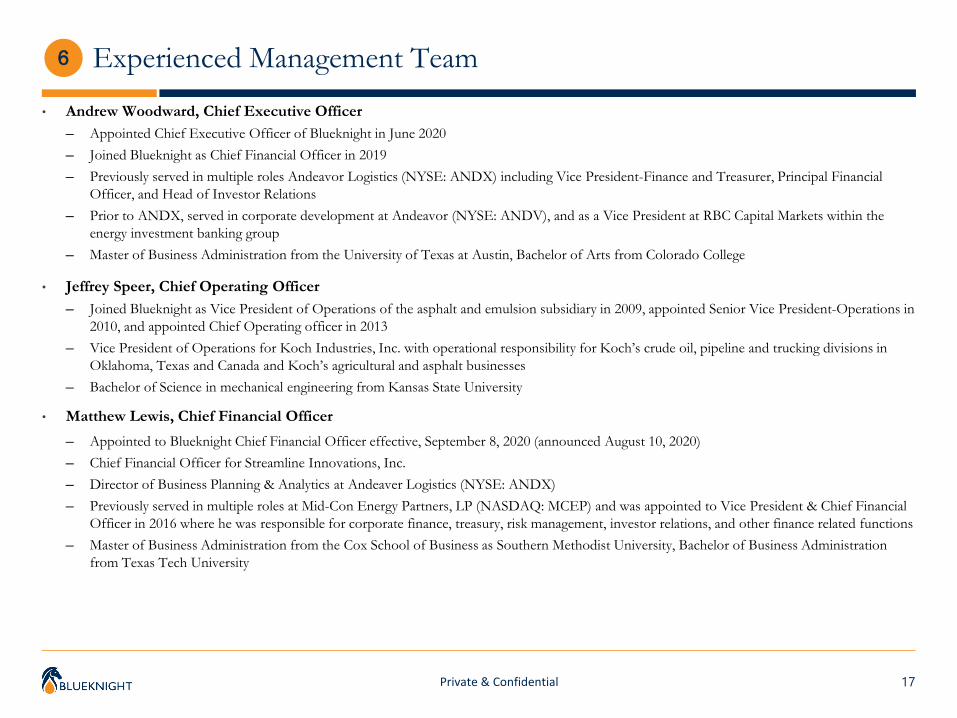

Experienced Management Team6

• Andrew Woodward, Chief Executive Officer─ Appointed Chief Executive Officer of Blueknight in June 2020─ Joined Blueknight as Chief Financial Officer in 2019─ Previously served in multiple roles Andeavor Logistics (NYSE: ANDX) including Vice President-Finance and Treasurer, Principal Financial

Officer, and Head of Investor Relations ─ Prior to ANDX, served in corporate development at Andeavor (NYSE: ANDV), and as a Vice President at RBC Capital Markets within the

energy investment banking group─ Master of Business Administration from the University of Texas at Austin, Bachelor of Arts from Colorado College

• Jeffrey Speer, Chief Operating Officer─ Joined Blueknight as Vice President of Operations of the asphalt and emulsion subsidiary in 2009, appointed Senior Vice President-Operations in

2010, and appointed Chief Operating officer in 2013─ Vice President of Operations for Koch Industries, Inc. with operational responsibility for Koch’s crude oil, pipeline and trucking divisions in

Oklahoma, Texas and Canada and Koch’s agricultural and asphalt businesses─ Bachelor of Science in mechanical engineering from Kansas State University

• Matthew Lewis, Chief Financial Officer─ Appointed to Blueknight Chief Financial Officer effective, September 8, 2020 (announced August 10, 2020)─ Chief Financial Officer for Streamline Innovations, Inc.─ Director of Business Planning & Analytics at Andeaver Logistics (NYSE: ANDX)─ Previously served in multiple roles at Mid-Con Energy Partners, LP (NASDAQ: MCEP) and was appointed to Vice President & Chief Financial

Officer in 2016 where he was responsible for corporate finance, treasury, risk management, investor relations, and other finance related functions─ Master of Business Administration from the Cox School of Business as Southern Methodist University, Bachelor of Business Administration

from Texas Tech University

Appendix

19Private & Confidential

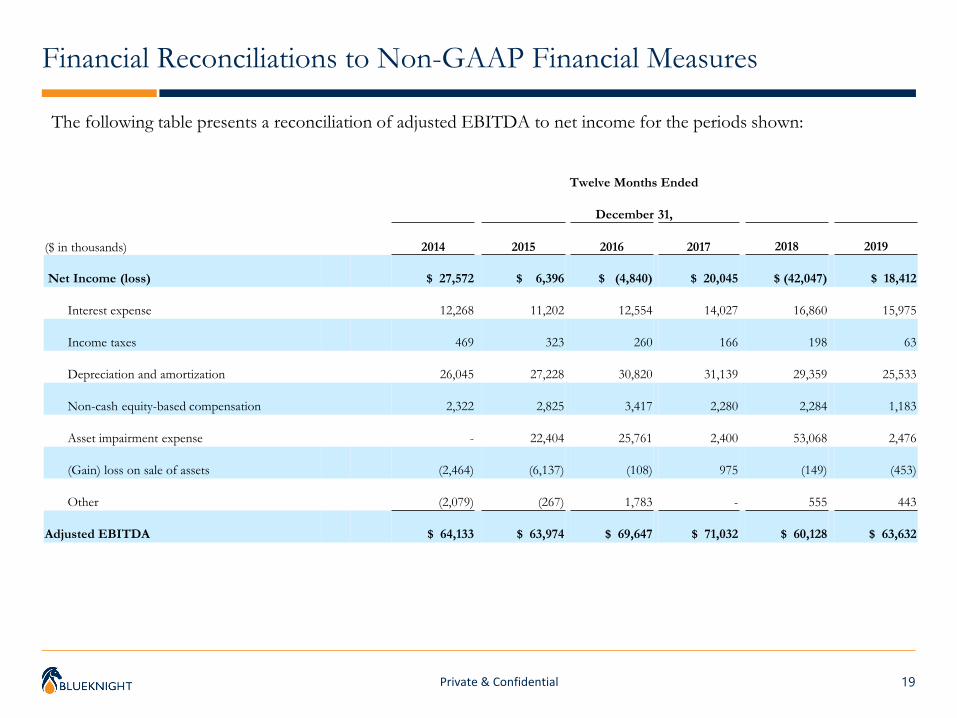

Financial Reconciliations to Non-GAAP Financial Measures

The following table presents a reconciliation of adjusted EBITDA to net income for the periods shown:

Twelve Months Ended

December 31,

($ in thousands) 2014 2015 2016 2017 2018 2019

Net Income (loss) $ 27,572 $ 6,396 $ (4,840) $ 20,045 $ (42,047) $ 18,412

Interest expense 12,268 11,202 12,554 14,027 16,860 15,975

Income taxes 469 323 260 166 198 63

Depreciation and amortization 26,045 27,228 30,820 31,139 29,359 25,533

Non-cash equity-based compensation 2,322 2,825 3,417 2,280 2,284 1,183

Asset impairment expense - 22,404 25,761 2,400 53,068 2,476

(Gain) loss on sale of assets (2,464) (6,137) (108) 975 (149) (453)

Other (2,079) (267) 1,783 - 555 443

Adjusted EBITDA $ 64,133 $ 63,974 $ 69,647 $ 71,032 $ 60,128 $ 63,632

20Private & Confidential

Financial Reconciliations to Non-GAAP Financial Measures

Twelve Months Ended

December 31,

($ in thousands) 2014 2015 2016 2017 2018 2019

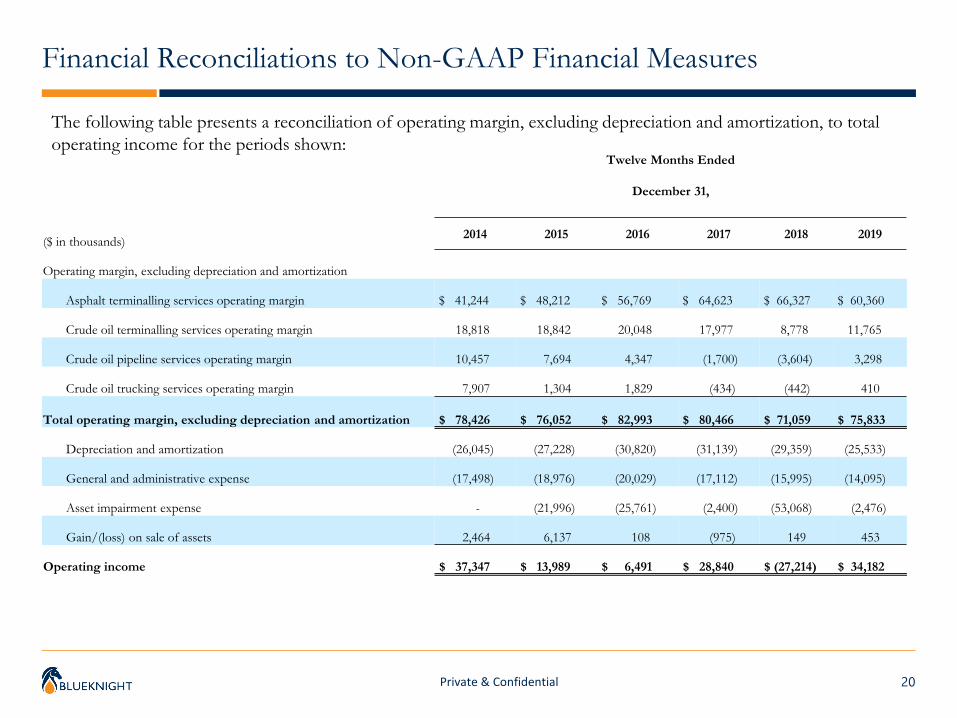

Operating margin, excluding depreciation and amortization

Asphalt terminalling services operating margin $ 41,244 $ 48,212 $ 56,769 $ 64,623 $ 66,327 $ 60,360

Crude oil terminalling services operating margin 18,818 18,842 20,048 17,977 8,778 11,765

Crude oil pipeline services operating margin 10,457 7,694 4,347 (1,700) (3,604) 3,298

Crude oil trucking services operating margin 7,907 1,304 1,829 (434) (442) 410

Total operating margin, excluding depreciation and amortization $ 78,426 $ 76,052 $ 82,993 $ 80,466 $ 71,059 $ 75,833

Depreciation and amortization (26,045) (27,228) (30,820) (31,139) (29,359) (25,533)

General and administrative expense (17,498) (18,976) (20,029) (17,112) (15,995) (14,095)

Asset impairment expense - (21,996) (25,761) (2,400) (53,068) (2,476)

Gain/(loss) on sale of assets 2,464 6,137 108 (975) 149 453

Operating income $ 37,347 $ 13,989 $ 6,491 $ 28,840 $ (27,214) $ 34,182

The following table presents a reconciliation of operating margin, excluding depreciation and amortization, to total operating income for the periods shown: