bir reliefdocshare02.docshare.tips/files/31405/314058265.pdf · accomplished vat relief transmittal...

TRANSCRIPT

BIR RELIEFSummary List of Sales and Purchases

WHAT IS RELIEF?• Reconciliation of Listings for Enforcement. • created by BIR to capture the monthly summary

of sales, purchases and importations required to be submitted by VAT-registered taxpayers on a quarterly basis in magnetic form based on a prescribed electronic format.

• The consolidation and matching of information with other externally sourced data will detect underdeclaration of revenues/overdeclaration of expenses resulting in greater tax potential.

MAIN FEATURES • Data maintenance of Sales, Purchases and

Importations • Data import / export capability across multiple

PCs • Purging and Archiving facility • Database back-up and recovery facility • Reports generation

Who are required to submit Summary List of Sales?

• All VAT taxpayers are required to submit the quarterly summary list of sales (SLS).

• The requirement previously applies to VAT-registered taxpayers with total quarterly sales/ receipts (net of VAT) exceeding P2.5 M

Who are required to submit Summary List of Purchases?• All VAT taxpayers are required to submit the

quarterly summary list of purchases (SLP).

• The requirement previously applies to VAT-registered taxpayers with total quarterly total purchases (net of VAT) exceeding P1M.

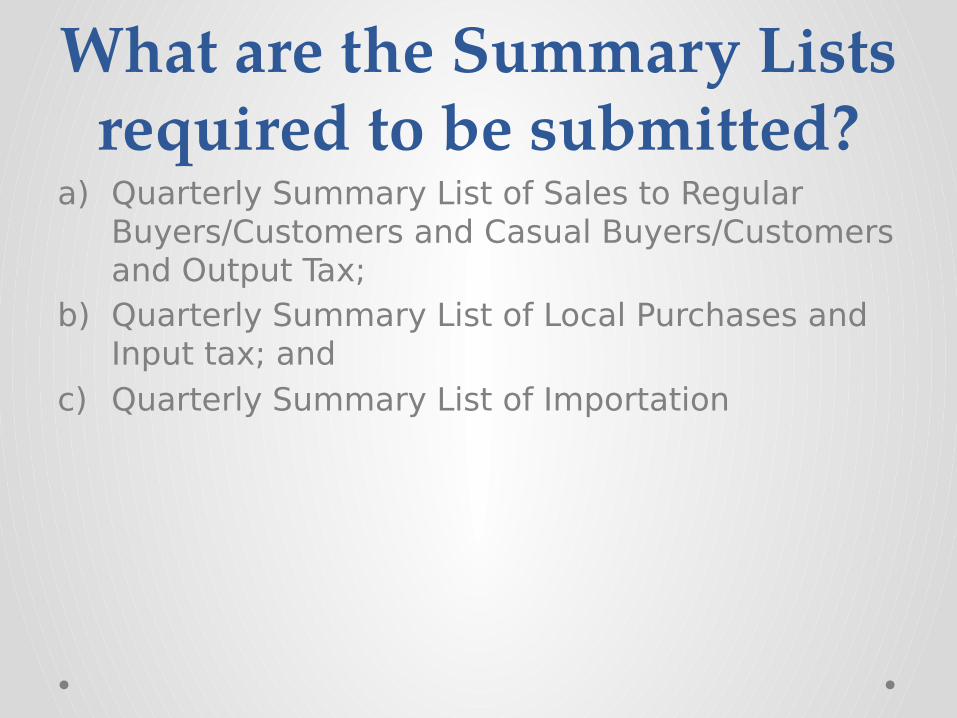

What are the Summary Lists required to be submitted?

a) Quarterly Summary List of Sales to Regular Buyers/Customers and Casual Buyers/Customers and Output Tax;

b) Quarterly Summary List of Local Purchases and Input tax; and

c) Quarterly Summary List of Importation

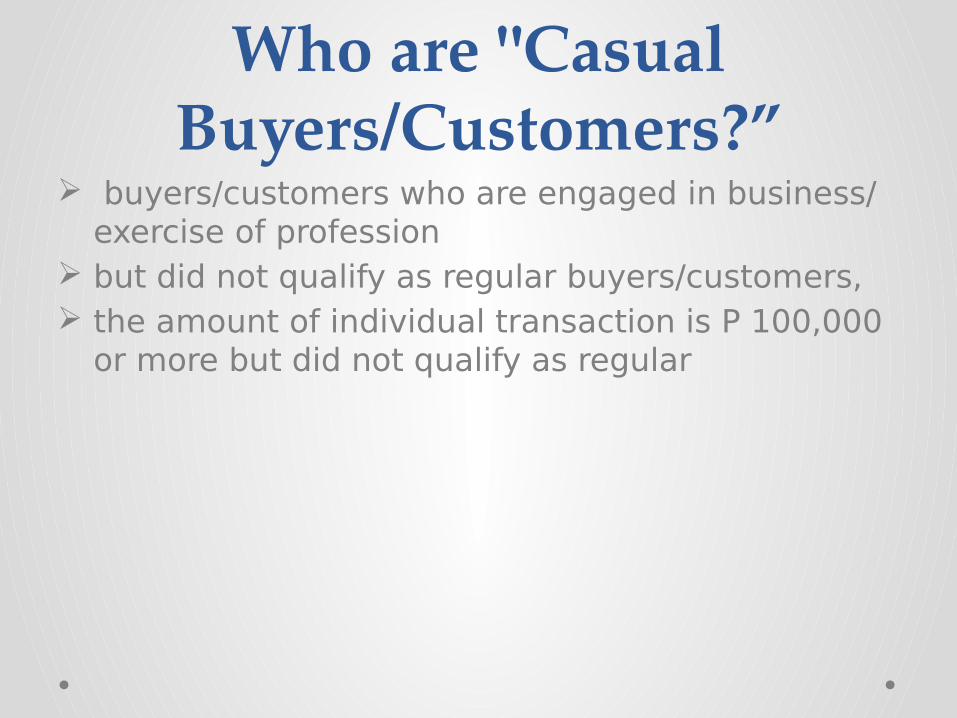

Who are "Casual Buyers/Customers?”

buyers/customers who are engaged in business/ exercise of profession

but did not qualify as regular buyers/customers, the amount of individual transaction is P 100,000

or more but did not qualify as regular

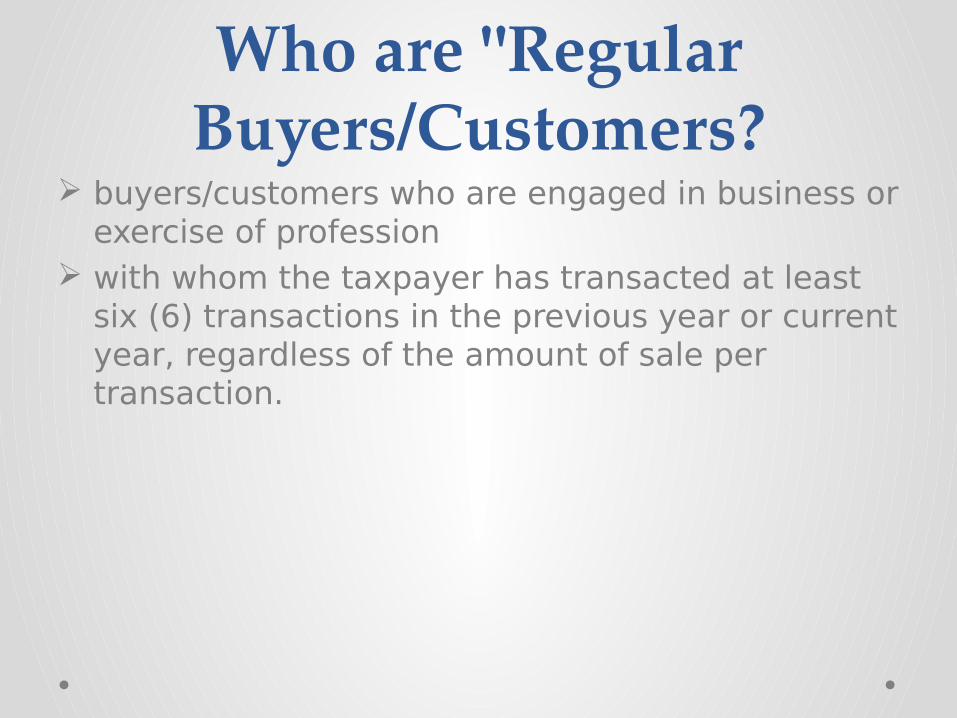

Who are "Regular Buyers/Customers?

buyers/customers who are engaged in business or exercise of profession

with whom the taxpayer has transacted at least six (6) transactions in the previous year or current year, regardless of the amount of sale per transaction.

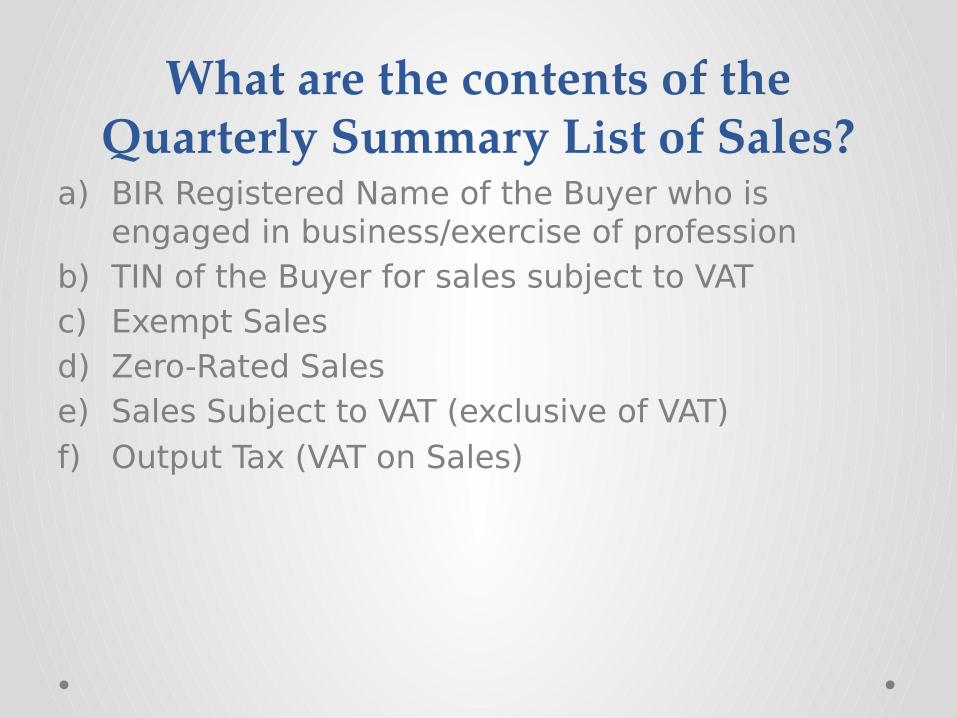

What are the contents of the Quarterly Summary List of Sales?

a) BIR Registered Name of the Buyer who is engaged in business/exercise of profession

b) TIN of the Buyer for sales subject to VATc) Exempt Salesd) Zero-Rated Salese) Sales Subject to VAT (exclusive of VAT)f) Output Tax (VAT on Sales)

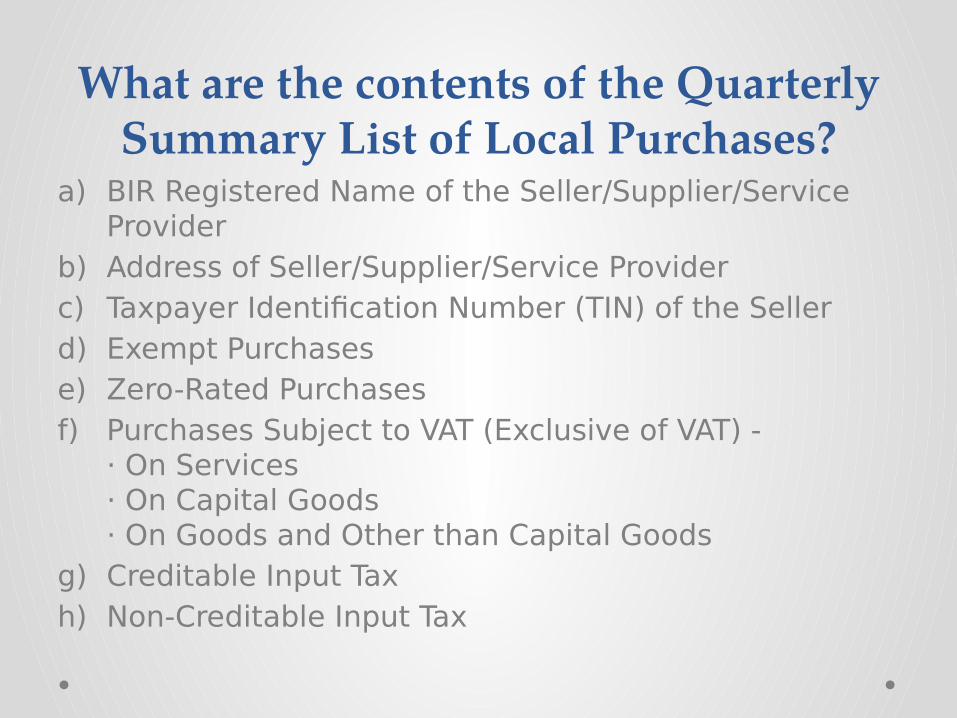

What are the contents of the Quarterly Summary List of Local Purchases?

a) BIR Registered Name of the Seller/Supplier/Service Provider

b) Address of Seller/Supplier/Service Providerc) Taxpayer Identification Number (TIN) of the Sellerd) Exempt Purchasese) Zero-Rated Purchasesf) Purchases Subject to VAT (Exclusive of VAT) -

· On Services· On Capital Goods· On Goods and Other than Capital Goods

g) Creditable Input Taxh) Non-Creditable Input Tax

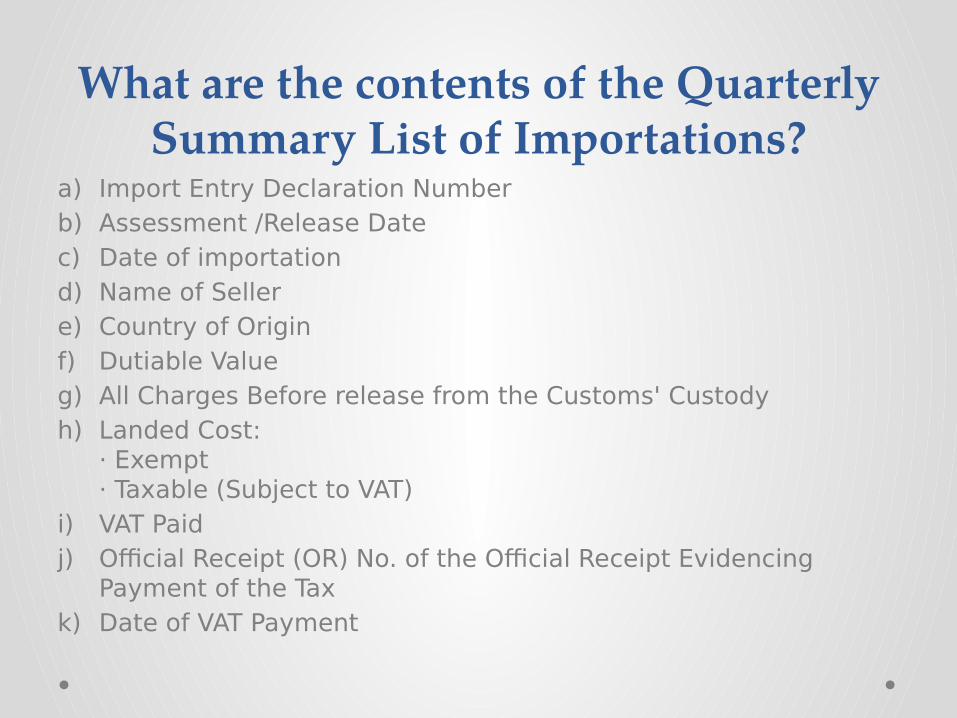

What are the contents of the Quarterly Summary List of Importations?

a) Import Entry Declaration Numberb) Assessment /Release Datec) Date of importationd) Name of Sellere) Country of Originf) Dutiable Valueg) All Charges Before release from the Customs' Custodyh) Landed Cost:

· Exempt· Taxable (Subject to VAT)

i) VAT Paidj) Official Receipt (OR) No. of the Official Receipt Evidencing

Payment of the Taxk) Date of VAT Payment

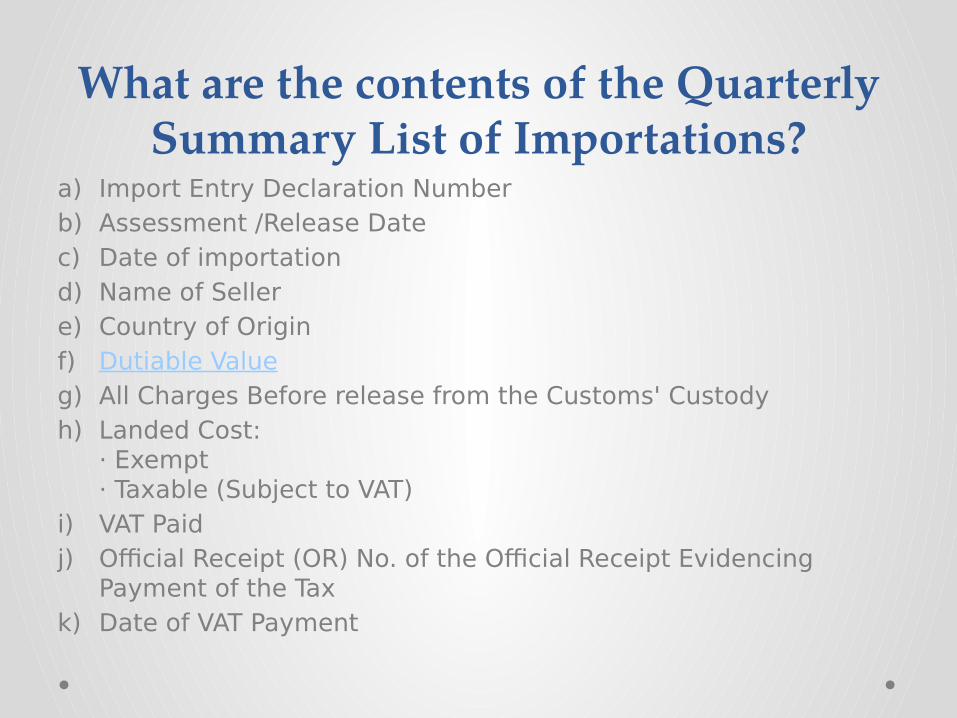

What are the contents of the Quarterly Summary List of Importations?

a) Import Entry Declaration Numberb) Assessment /Release Datec) Date of importationd) Name of Sellere) Country of Originf) Dutiable Valueg) All Charges Before release from the Customs' Custodyh) Landed Cost:

· Exempt· Taxable (Subject to VAT)

i) VAT Paidj) Official Receipt (OR) No. of the Official Receipt Evidencing

Payment of the Taxk) Date of VAT Payment

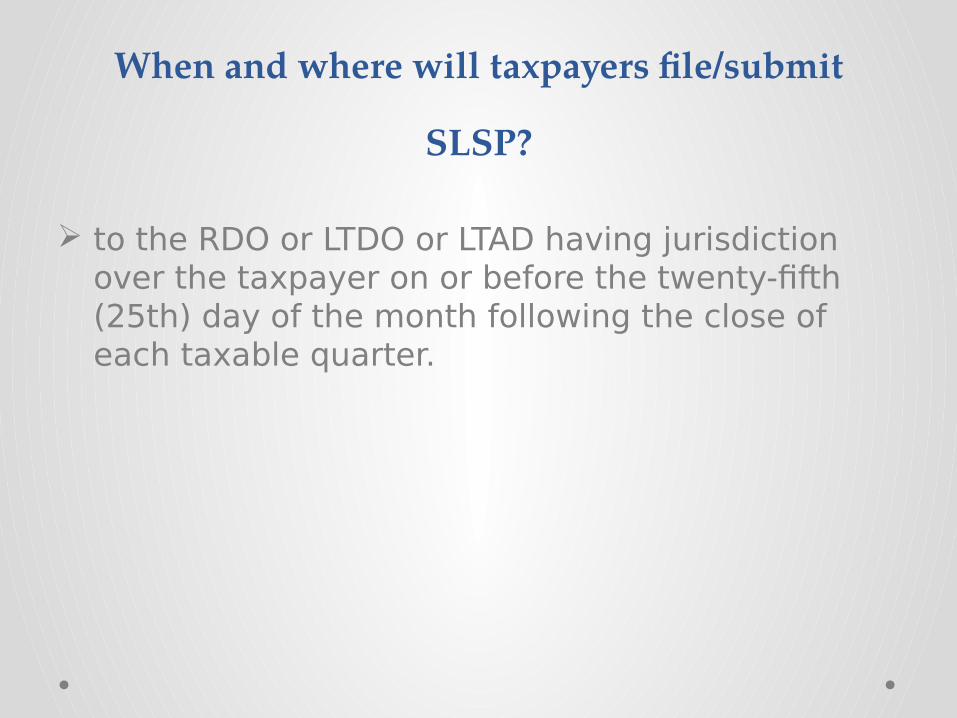

When and where will taxpayers file/submit

SLSP?

to the RDO or LTDO or LTAD having jurisdiction over the taxpayer on or before the twenty-fifth (25th) day of the month following the close of each taxable quarter.

How to file/submit the SLSP?

• can be submitted manually to BIR office in magnetic form using 3.5 inch floppy diskette, CD or USB following the format provided under Section 4.114 of RR No.16-2005 together with the accomplished VAT RELIEF transmittal form.

• Through electronic filing facility for taxpayers under the jurisdiction of Large Taxpayers Service (LTS) and those enrolled under the EFPS. The VAT relief dat files can be emailed to [email protected] subject for verification and approval of BIR.

PENALTY

(RR 16-2005)• Administrative Penalty

P 1,000 - For each failure to file, keep or supply the required documentsAggregate amount not to exceed P 25,000 for the taxable year

• Criminal Penalty

Willful failure to keep any record or to supply the information at the time or times required shall be subject to the criminal penalty under the Tax Code of 1997.

• *Compromise on such violation SHALL NOT relieve the violating taxpayer from the obligation to submit the required documents.