binnenlandse francqui leerstoel vub 2004-2005 1. black scholes and beyond andré farber solvay...

Post on 21-Dec-2015

215 views

TRANSCRIPT

Binnenlandse Francqui Leerstoel VUB 2004-20051. Black Scholes and beyond

André Farber

Solvay Business School

University of Brussels

VUB 01 Black Scholes and beyond |2August 23, 2004

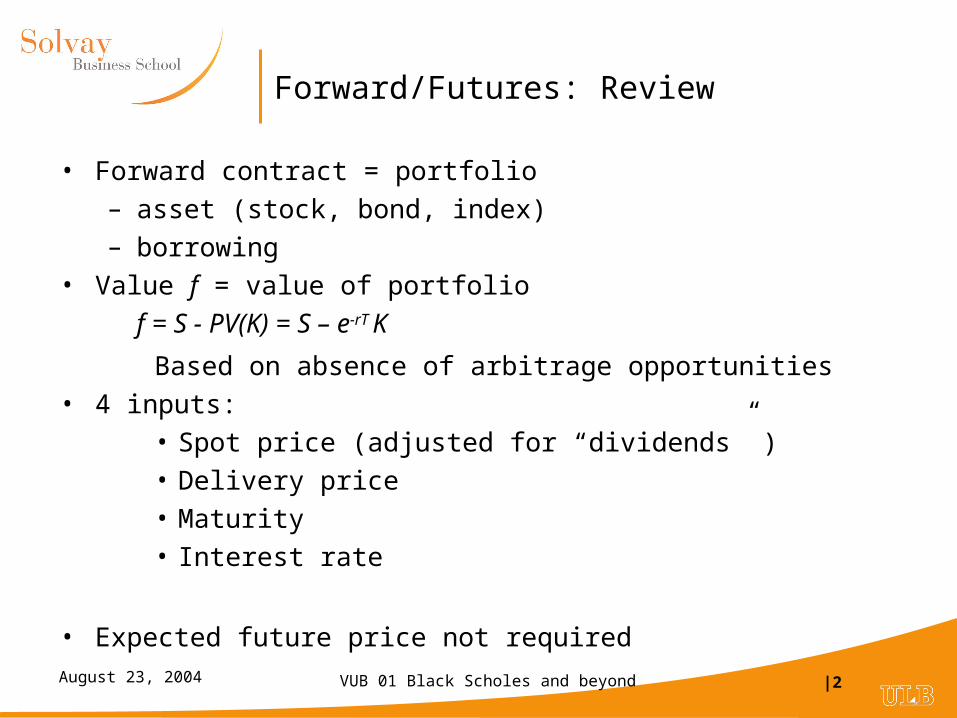

Forward/Futures: Review

• Forward contract = portfolio

– asset (stock, bond, index)

– borrowing

• Value f = value of portfolio

f = S - PV(K) = S – e-rT K

Based on absence of arbitrage opportunities

• 4 inputs:

• Spot price (adjusted for “dividends” )

• Delivery price

• Maturity

• Interest rate

• Expected future price not required

VUB 01 Black Scholes and beyond |3August 23, 2004

Discount factors and interest rates

• Review: Present value of Ct

• PV(Ct) = Ct × Discount factor

• With annual compounding:

• Discount factor = 1 / (1+r)t

• With compounding n times per year:

• Discount factor = 1/(1+r/n)nt

• With continuous compounding:

• Discount factor = 1 / ert = e-rt

n

en

r rn

)1(

VUB 01 Black Scholes and beyond |4August 23, 2004

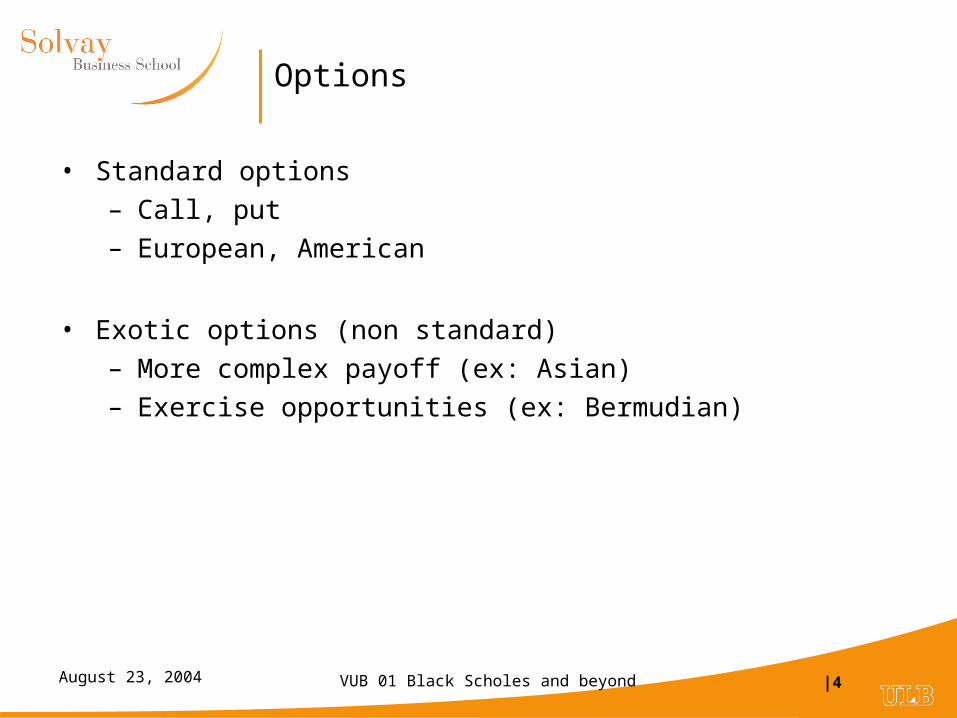

Options

• Standard options

– Call, put

– European, American

• Exotic options (non standard)

– More complex payoff (ex: Asian)

– Exercise opportunities (ex: Bermudian)

VUB 01 Black Scholes and beyond |5August 23, 2004

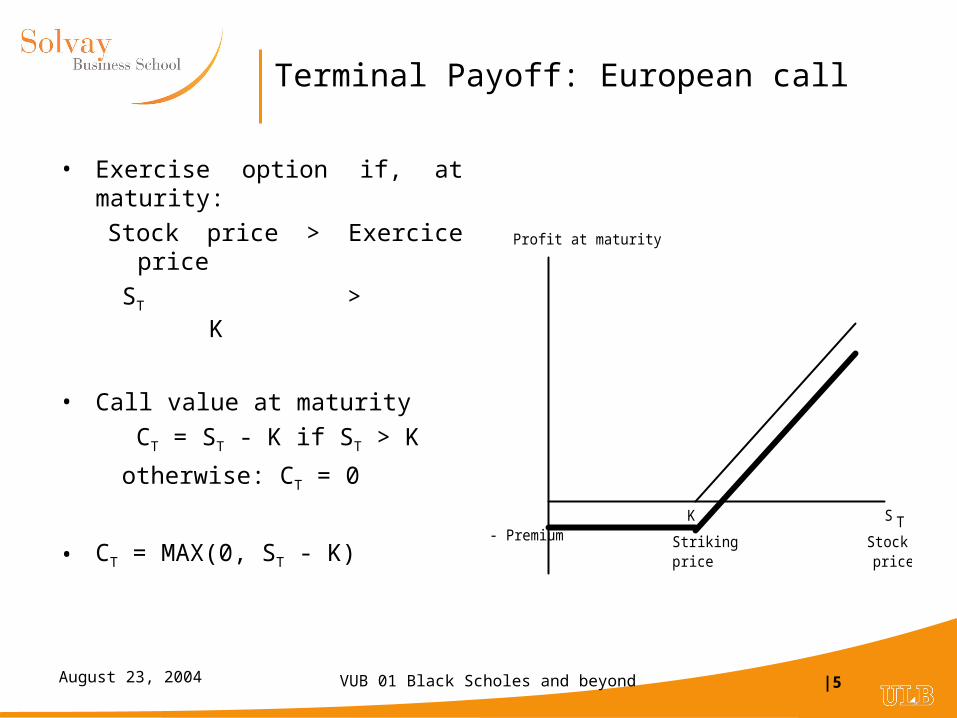

Terminal Payoff: European call

• Exercise option if, at maturity:

Stock price > Exercice price

ST > K

• Call value at maturity

CT = ST - K if ST > K

otherwise: CT = 0

• CT = MAX(0, ST - K)

Profit at maturity

K S TStrikingprice

Stockprice

- Premium

VUB 01 Black Scholes and beyond |6August 23, 2004

Terminal Payoff: European put

• Exercise option if, at maturity:

Stock price < Exercice price

ST < K

• Put value at maturity

PT = K - ST if ST < K

otherwise: PT = 0

• PT = MAX(0, K- ST )

Value / profit at maturity

K S T

Strikingprice

Stockprice

Value

Profit

Premium

VUB 01 Black Scholes and beyond |7August 23, 2004

The Put-Call Parity relation

• A relationship between European put and call prices on the same stock

• Compare 2 strategies:

• Strategy 1. Buy 1 share + 1 put

At maturity T: ST<K ST>K

Share value ST ST

Put value (K - ST) 0

Total value K ST

• Put = insurance contract

K

ST

Value at maturity

K

VUB 01 Black Scholes and beyond |8August 23, 2004

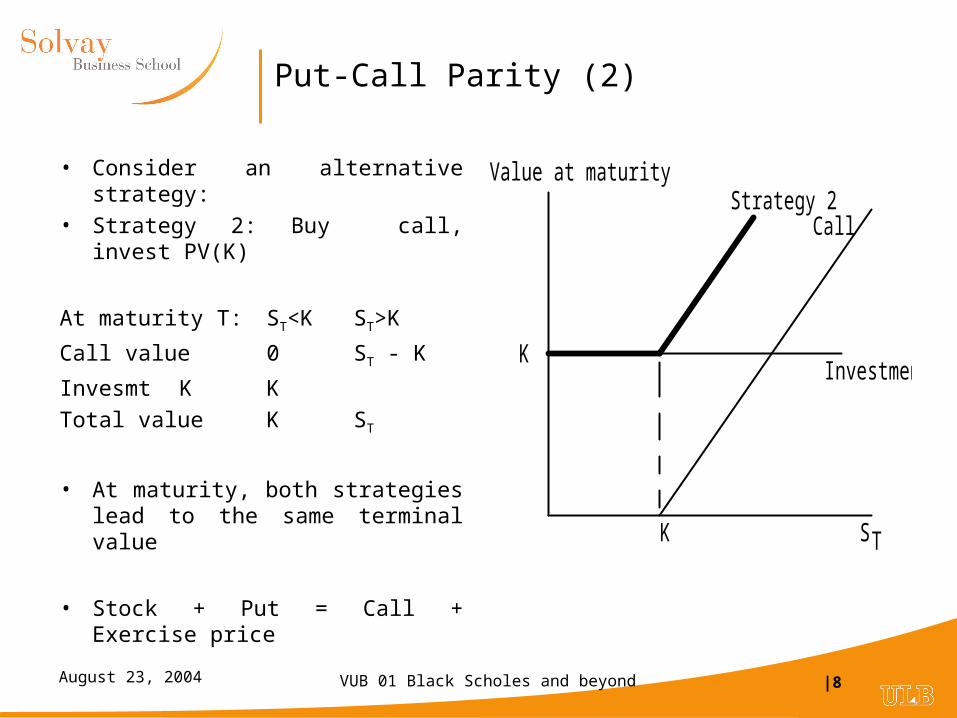

Put-Call Parity (2)

• Consider an alternative strategy:

• Strategy 2: Buy call, invest PV(K)

At maturity T: ST<K ST>K

Call value 0 ST - K

Invesmt K K

Total value K ST

• At maturity, both strategies lead to the same terminal value

• Stock + Put = Call + Exercise price

K

ST

Value at maturity

K

Call

Investment

Strategy 2

VUB 01 Black Scholes and beyond |9August 23, 2004

Put-Call Parity (3)

• Two equivalent strategies should have the same cost

S + P = C + PV(K)

where S current stock price

P current put value

C current call value

PV(K) present value of the striking price

• This is the put-call parity relation

• Another presentation of the same relation:

C = S + P - PV(K)

• A call is equivalent to a purchase of stock and a put financed by borrowing the PV(K)

VUB 01 Black Scholes and beyond |10August 23, 2004

Option Valuation Models: Key ingredients

• Model of the behavior of spot price

new variable: volatility

• Technique: create a synthetic option

• No arbitrage

• Value determination

– closed form solution (Black Merton Scholes)

– numerical technique

VUB 01 Black Scholes and beyond |11August 23, 2004

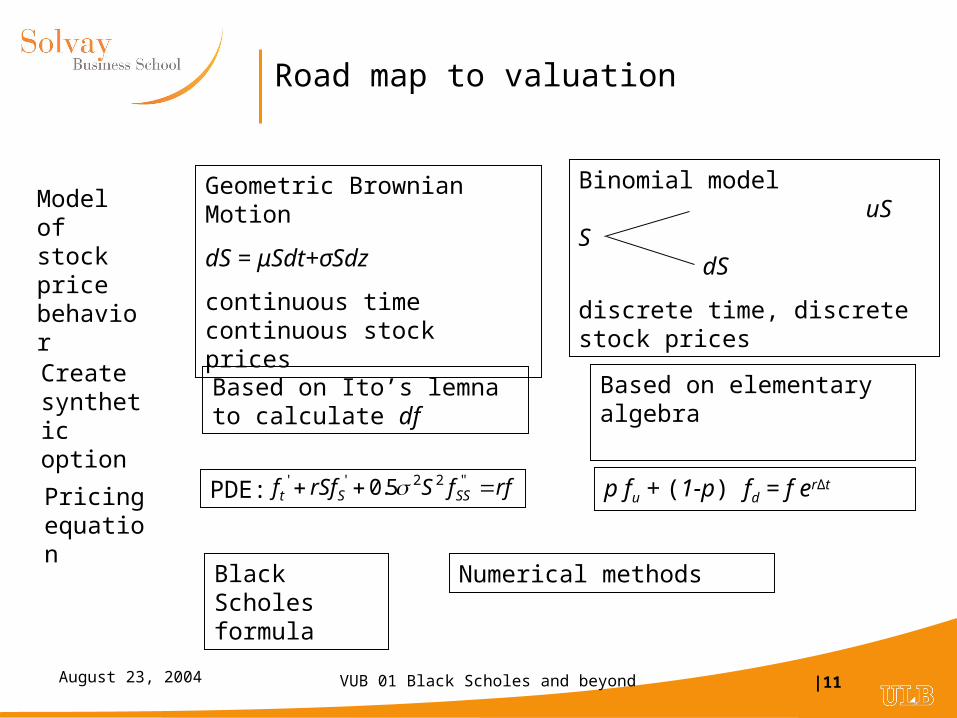

Road map to valuation

Geometric Brownian Motion

dS = μSdt+σSdz

continuous timecontinuous stock prices

Binomial model uSS dS

discrete time, discrete stock prices

Model of stock price behavior

Create synthetic option

Based on Ito’s lemna to calculate df

Based on elementary algebra

Pricing equation

PDE: rffSrSff SSSt "22'' 5.0 p fu + (1-p) fd = f erΔt

Black Scholes formula

Numerical methods

VUB 01 Black Scholes and beyond |12August 23, 2004

Modelling stock price behaviour

• Consider a small time interval t: S = St+t - St

• 2 components of S:– drift : E(S) = S t [ = expected return (per year)]

– volatility:S/S = E(S/S) + random variable (rv)

• Expected value E(rv) = 0

• Variance proportional to t

– Var(rv) = ² t Standard deviation = t– rv = Normal (0, t)– = Normal (0,t)– = z z :

Normal (0,t)– = t : Normal(0,1)

z independent of past values (Markov process)

VUB 01 Black Scholes and beyond |13August 23, 2004

Geometric Brownian motion illustrated

Geometric Brownian motion

-100.00

-50.00

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

0 8 16

24

32

40

48

56

64

72

80

88

96

104

112

120

128

136

144

152

160

168

176

184

192

200

208

216

224

232

240

248

256

Drift Random shocks Stock price

VUB 01 Black Scholes and beyond |14August 23, 2004

Geometric Brownian motion model

S/S = t + z S = S t + S z

• = S t + S t

• If t "small" (continuous model)

• dS = S dt + S dz

VUB 01 Black Scholes and beyond |15August 23, 2004

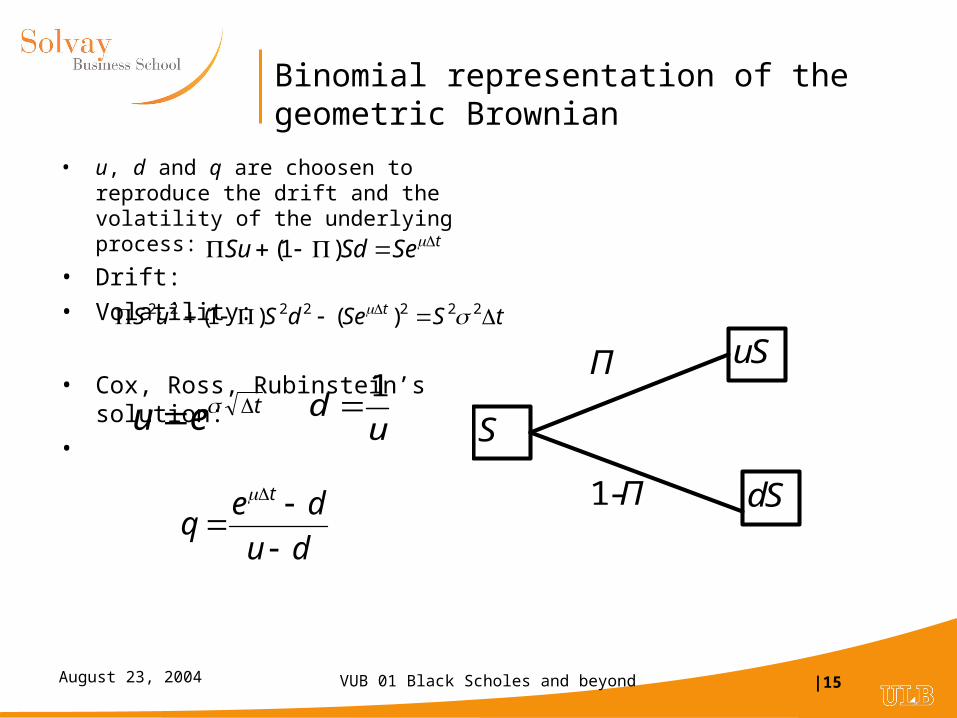

Binomial representation of the geometric Brownian

• u, d and q are choosen to reproduce the drift and the volatility of the underlying process:

• Drift:

• Volatility:

• Cox, Ross, Rubinstein’s solution:

•

S

uS

dS

Π

1-Π

teu u

d1

du

deq

t

tSeSdSu )1(

tSSedSuS t 2222222 )()1(

VUB 01 Black Scholes and beyond |16August 23, 2004

Binomial process: Example

• dS = 0.15 S dt + 0.30 S dz ( = 15%, = 30%)

• Consider a binomial representation with t = 0.5

u = 1.2363, d = 0.8089, Π = 0.6293

• Time 0 0.5 1 1.5 2 2.5• 28,883• 23,362• 18,897 18,897• 15,285 15,285• 12,363 12,363 12,363• 10,000 10,000 10,000• 8,089 8,089 8,089• 6,543 6,543• 5,292 5,292• 4,280• 3,462

VUB 01 Black Scholes and beyond |17August 23, 2004

Call Option Valuation:Single period model, no payout

• Time step = t• Riskless interest rate = r • Stock price evolution

• uS

• S

• dS

• No arbitrage: d<er t <u

• 1-period call option

• Cu = Max(0,uS-X)

• Cu =?

• Cd = Max(0,dS-X)

Π

1- Π

Π

1- Π

VUB 01 Black Scholes and beyond |18August 23, 2004

Option valuation: Basic idea

• Basic idea underlying the analysis of derivative securities

• Can be decomposed into basic components possibility of creating a synthetic identical security

• by combining:

• - Underlying asset

• - Borrowing / lending

Value of derivative = value of components

VUB 01 Black Scholes and beyond |19August 23, 2004

Synthetic call option

• Buy shares

• Borrow B at the interest rate r per period

• Choose and B to reproduce payoff of call option

u S - B ert = Cu

d S - B ert = Cd

Solution:

Call value C = S - B

dSuS

CC du

trdu

edu

uCdCB

)(

VUB 01 Black Scholes and beyond |20August 23, 2004

Call value: Another interpretation

Call value C = S - B

• In this formula:

+ : long position (buy, invest)

- : short position (sell borrow)

B = S - C

Interpretation:

Buying shares and selling one call is equivalent to a riskless investment.

VUB 01 Black Scholes and beyond |21August 23, 2004

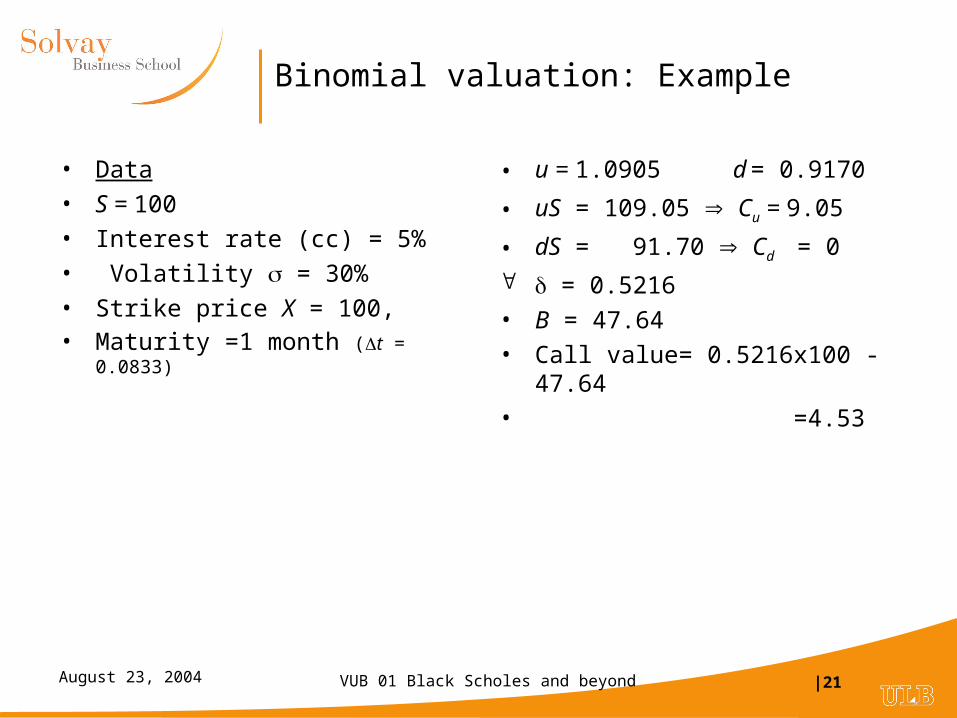

Binomial valuation: Example

• Data

• S = 100

• Interest rate (cc) = 5%

• Volatility = 30%

• Strike price X = 100, • Maturity =1 month (t = 0.0833)

• u = 1.0905 d = 0.9170

• uS = 109.05 Cu = 9.05

• dS = 91.70 Cd = 0

= 0.5216

• B = 47.64

• Call value= 0.5216x100 - 47.64

• =4.53

VUB 01 Black Scholes and beyond |22August 23, 2004

1-period binomial formula

• Cash value = S - B

• Substitue values for and B and simplify:

• C = [ pCu + (1-p)Cd ]/ ert where p = (ert - d)/(u-d)

• As 0< p<1, p can be interpreted as a probability

• p is the “risk-neutral probability”: the probability such that the expected return on any asset is equal to the riskless interest rate

VUB 01 Black Scholes and beyond |23August 23, 2004

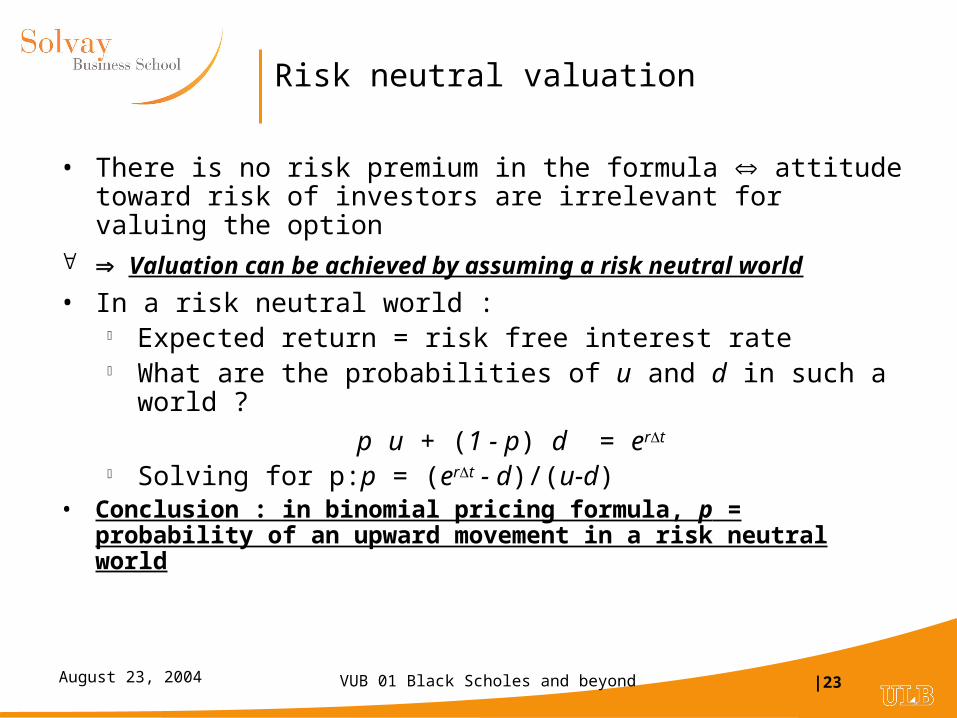

Risk neutral valuation

• There is no risk premium in the formula attitude toward risk of investors are irrelevant for valuing the option

Valuation can be achieved by assuming a risk neutral world

• In a risk neutral world : Expected return = risk free interest rate What are the probabilities of u and d in such a world ?

p u + (1 - p) d = ert

Solving for p:p = (ert - d)/(u-d)• Conclusion : in binomial pricing formula, p = probability of an upward

movement in a risk neutral world

VUB 01 Black Scholes and beyond |24August 23, 2004

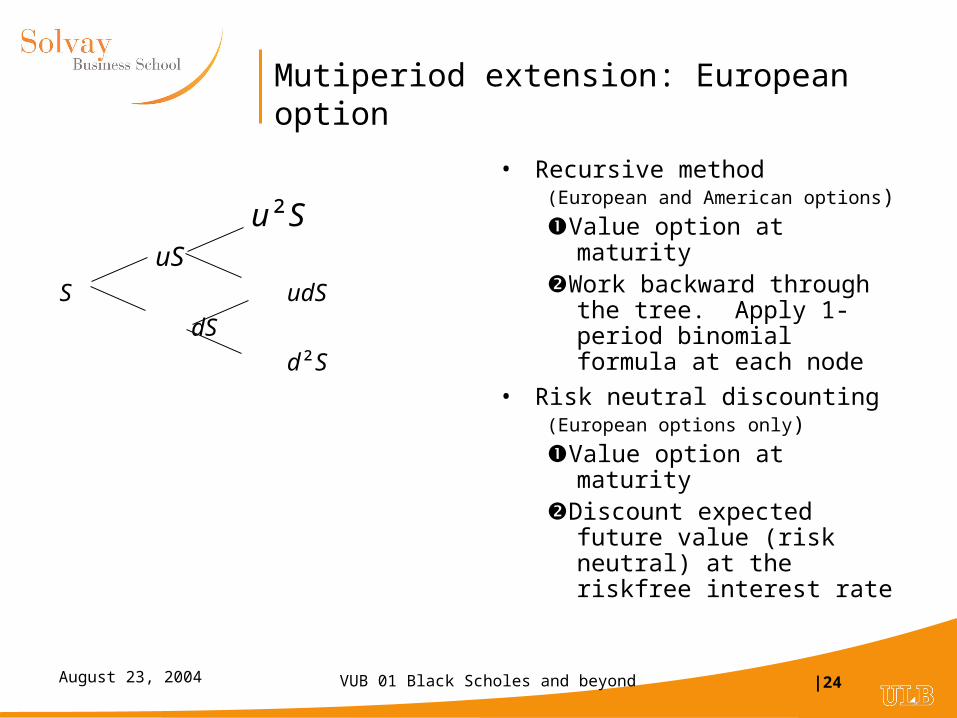

Mutiperiod extension: European option

u²SuS

S udS

dS

d²S

• Recursive method (European and American options)

Value option at maturityWork backward through the tree.

Apply 1-period binomial formula at each node

• Risk neutral discounting(European options only)

Value option at maturityDiscount expected future value

(risk neutral) at the riskfree interest rate

VUB 01 Black Scholes and beyond |25August 23, 2004

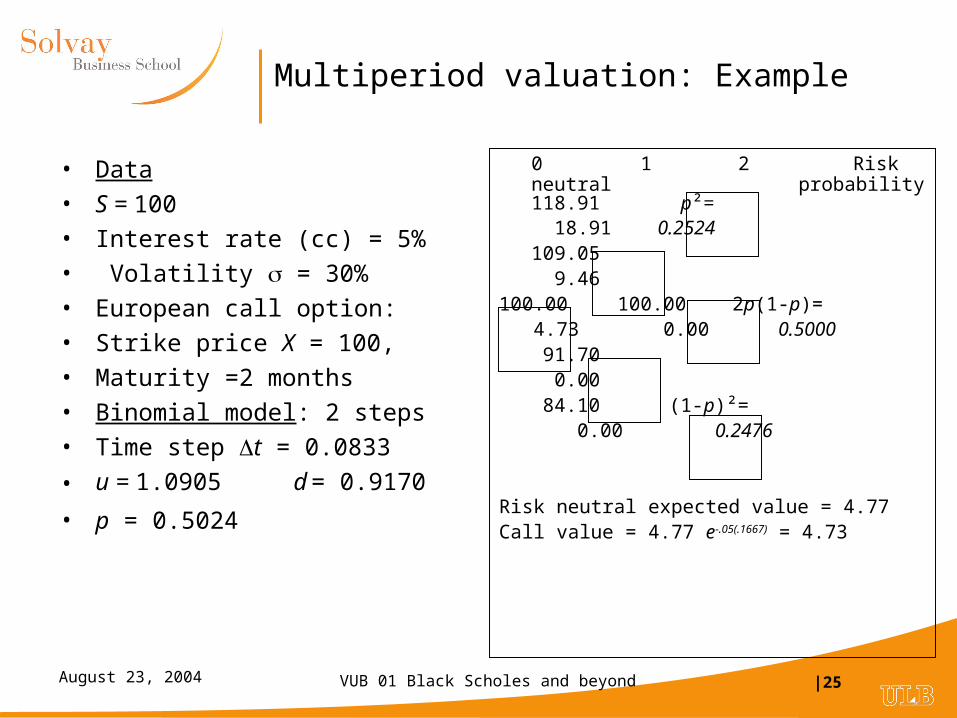

Multiperiod valuation: Example

• Data

• S = 100

• Interest rate (cc) = 5%

• Volatility = 30%

• European call option:

• Strike price X = 100,

• Maturity =2 months

• Binomial model: 2 steps

• Time step t = 0.0833

• u = 1.0905 d = 0.9170

• p = 0.5024

0 1 2 Risk neutral probability118.91 p²= 18.91 0.2524

109.05 9.46

100.00 100.00 2p(1-p)= 4.73 0.00 0.5000

91.70 0.00

84.10 (1-p)²= 0.00 0.2476

Risk neutral expected value = 4.77Call value = 4.77 e-.05(.1667) = 4.73

VUB 01 Black Scholes and beyond |26August 23, 2004

From binomial to Black Scholes

• Consider:

• European option

• on non dividend paying stock

• constant volatility

• constant interest rate

• Limiting case of binomial model as t0

Stock price

Timet T

VUB 01 Black Scholes and beyond |27August 23, 2004

Convergence of Binomial Model

Convergence of Binomial Model

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1 4 7 10

13

16

19

22

25

28

31

34

37

40

43

46

49

52

55

58

61

64

67

70

73

76

79

82

85

88

91

94

97

100

Number of steps

Op

tio

n v

alu

e

VUB 01 Black Scholes and beyond |28August 23, 2004

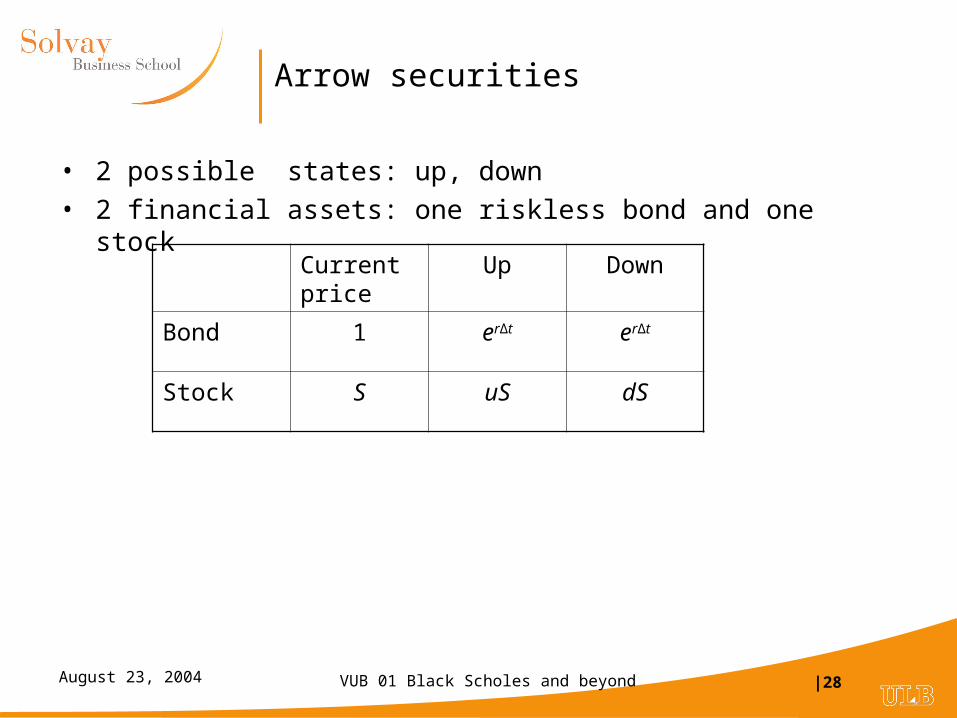

Arrow securities

• 2 possible states: up, down

• 2 financial assets: one riskless bond and one stock

Current price

Up Down

Bond 1 erΔt erΔt

Stock S uS dS

VUB 01 Black Scholes and beyond |29August 23, 2004

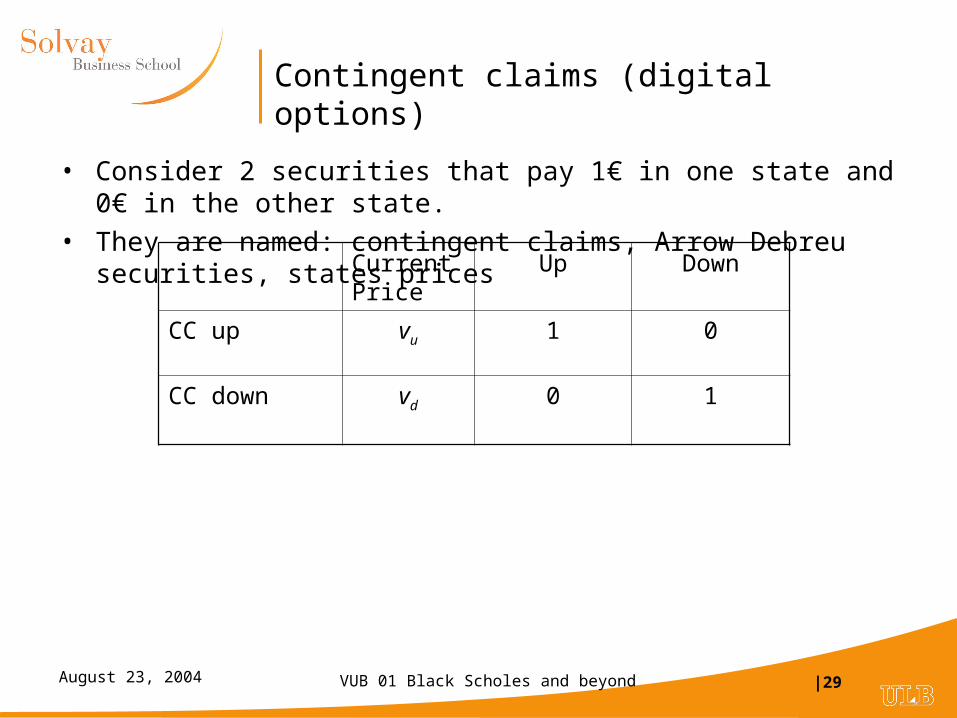

Contingent claims (digital options)

• Consider 2 securities that pay 1€ in one state and 0€ in the other state.

• They are named: contingent claims, Arrow Debreu securities, states prices

Current Price

Up Down

CC up vu 1 0

CC down vd 0 1

VUB 01 Black Scholes and beyond |30August 23, 2004

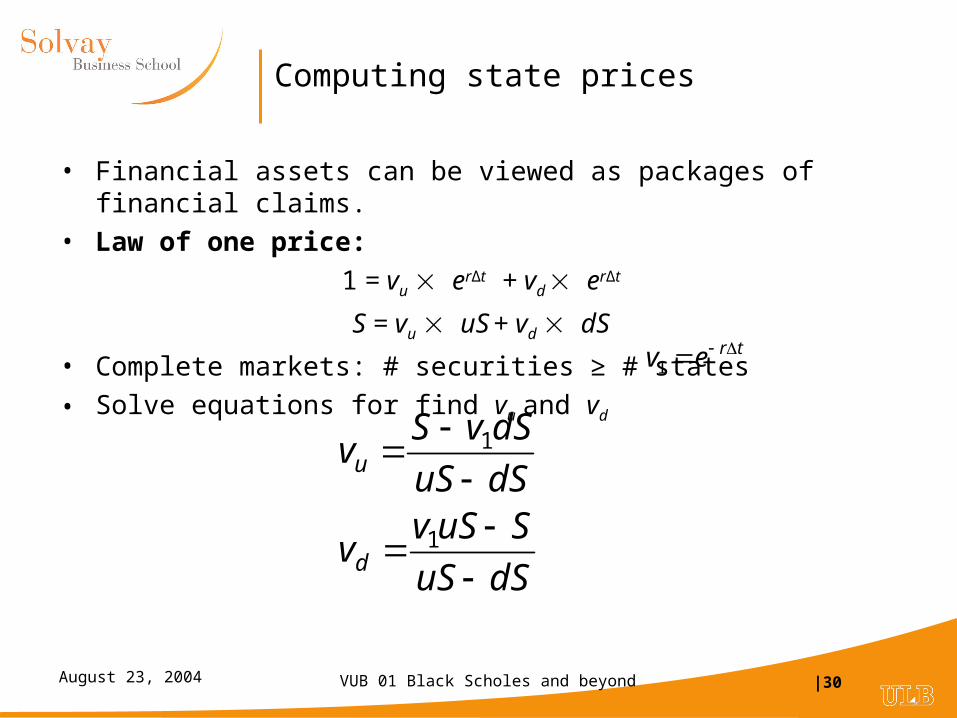

Computing state prices

• Financial assets can be viewed as packages of financial claims.

• Law of one price:

1 = vu erΔt + vd erΔt

S = vu uS + vd dS

• Complete markets: # securities ≥ # states

• Solve equations for find vu and vd

dSuS

SuSvv

dSuS

dSvSv

d

u

1

1

trev 1

VUB 01 Black Scholes and beyond |31August 23, 2004

Pricing a derivative security

trdu

e

fppff

)1(dduu fvfvf

pve

pv

tru 1

Using state prices: Using binomial option pricing model:

)1(1

1 pve

pv

trd

State prices are equal to discounted risk-neutral probabilities

VUB 01 Black Scholes and beyond |32August 23, 2004

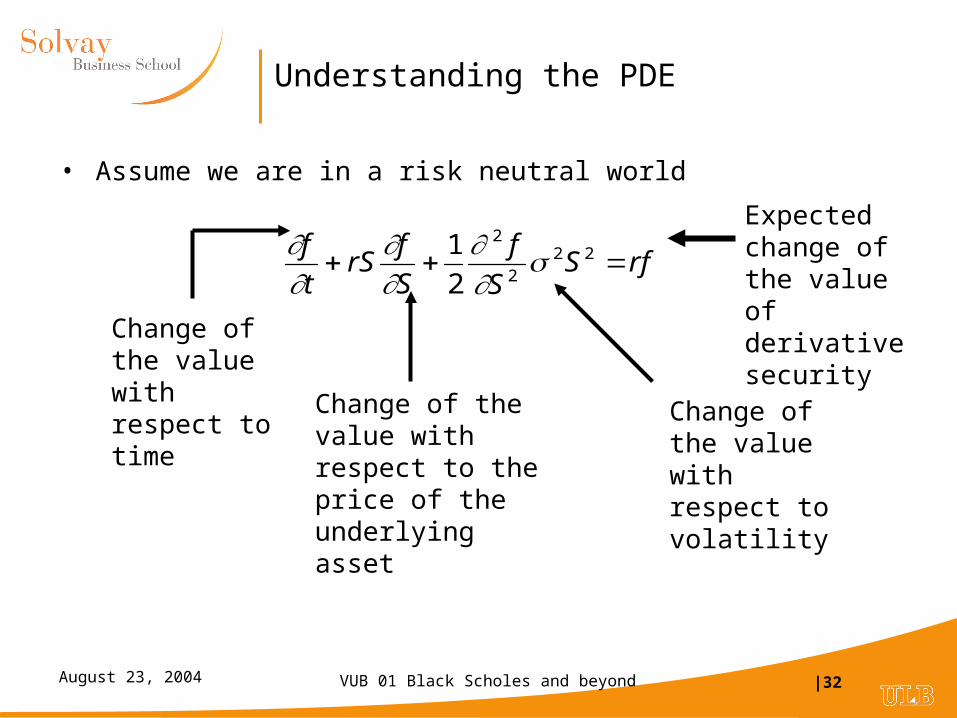

Understanding the PDE

• Assume we are in a risk neutral world

rfSS

f

S

frS

t

f 22

2

2

2

1

Expected change of the value of derivative security

Change of the value with respect to time Change of the value

with respect to the price of the underlying asset

Change of the value with respect to volatility

VUB 01 Black Scholes and beyond |33August 23, 2004

Black Scholes’ PDE and the binomial model

• We have:

• Binomial model: p fu + (1-p) fd = ert

• Use Taylor approximation:

• fu = f + (u-1) S f’S + ½ (u–1)² S² f”SS + f’t t

• fd = f + (d-1) S f’S + ½ (d–1)² S² f”SS + f’t t

• u = 1 + √t + ½ ²t

• d = 1 – √t + ½ ²t

• ert = 1 + rt

• Substituting in the binomial option pricing model leads to the differential equation derived by Black and Scholes

• BS PDE : f’t + rS f’S + ½ ² f”SS = r f