bill davidson sr. vp firethorn mobile, inc., sales and...

TRANSCRIPT

1

25th Annual Roth Conference March 19, 2013

Bill Davidson

Sr. VP Firethorn Mobile, Inc., Sales and Marketing

and Qualcomm Investor Relations

2

Safe Harbor and corporate structure In addition to the historical information contained herein, this presentation contains forward-looking statements that are inherently subject to risks and uncertainties, including but not limited to statements regarding our our fiscal 2013 outlook, including revenue and EPS targets; continued adoption of smartphones and connected devices; forecasted smartphone shipments and sales; 3G and 3G/4G growth in emerging regions; 3G/LTE adoption; increased device capabilities; 3G/4G device average selling prices; estimated 3G/4G replacement rates; key initiatives for the Company’s growth; expanding areas for smartphone innovation; new mobile computing growth opportunities; mobile data traffic growth; and growth in small cell deployment. Forward-looking statements are generally identified by words such as “estimates,” “guidance” and similar expressions. Actual results may differ materially from those referred to in the forward-looking statements due to a number of important factors, including but not limited to risks associated with the commercial deployment of our technologies and our customers’ and licensees’ sales of equipment, products and services based on these technologies; competition; our dependence on a small number of customers and licensees; attacks on our licensing business model; our dependence on third-party suppliers; the enforcement and protection of our intellectual property rights; claims by third parties that we infringe their intellectual property; global economic conditions that impact the communications industry and the potential impact on demand for our products and our customers’ and licensees’ products; our stock price and earnings volatility; strategic transactions and investments; foreign currency fluctuations; and failures, defects or errors in our products and services or in the products of our customers and licensees. These and other risks are set forth in our most recent Form 10-K and Form 10-Q filed with the SEC, copies of which are available on our website at www.qualcomm.com. We undertake no obligation to update any forward-looking statements.

Throughout today’s presentations we refer to “Qualcomm” for ease of reference. However, please note that in connection with our recent reorganization, Qualcomm Incorporated continues to operate QTL and own the vast majority of our patent portfolio, while Qualcomm Technologies, Inc., its wholly-owned subsidiary, now operates, along with its subsidiaries, substantially all of our products and services businesses, including QCT, and substantially all of our research and development functions.

3

Qualcomm’s unique business model A technology enabler for the entire mobile value chain

SUBSCRIBERS WIRELESS

ECOSYSTEM

4

Qualcomm: a communications systems company Innovation across entire wireless value chain

Standardization Innovative technologies Productization Commercialization

5

$0.025 $0.035

$0.05 $0.07

$0.09

$0.12 $0.14

$0.16 $0.17

$0.19

$0.215

$0.25

$0.35

Feb '03 Jul '03 Mar '04 Jul '04 Mar '05 Mar '06 Mar '07 Mar '08 Mar '09 Mar '10 Mar'11 Mar'12 Mar'13

Quarterly dividend increased by 40% Record $1.40 per share annualized payout

40% Increase, Board

Approved*

Qu

art

erl

y d

ivid

en

d p

er

sh

are

**

Note: The Company effected a two-for-one stock split in August 2004. All references to per share data have been adjusted to refl ect the stock split.

*As of March 5, 2013

**Based on announcement date of increase

6

FY'03 FY'04 FY'05 FY'06 FY'07 FY'08 FY'09 FY'10 FY'11 FY'12 FY'13 YTD**

Cumulative return of capital to stockholders New $5 billion stock repurchase program*

$19.9B** Returned to stockholders

Stock repurchases

Cash dividends

*Announced March 5, 2013

**As of December 30, 2012

7

Continued adoption of smartphones

Growth of 3G in emerging regions

QCT:

− Technology leadership

− Roadmap breadth and depth

− New computing and connectivity opportunities

QTL: Industry-leading licensing program

Double-digit revenue and EPS CAGR targets

over the next five years*

~27% pre-revenue R&D**

Fiscal 2013 Outlook

*Estimates as of November 15, 2012 for the five year period from FY’12-FY’17

**Estimates as of November 15, 2012

8

$194 $192 $205 $215 $214 $214 $219 $205

$186 $206

$219 $220

$-

$100

$200

$300

$400

$500

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13e

3G/4G estimated wholesale device midpoint ASP trend(1)(2)

Learning curves

’97–’13 est. 85%

’99–’13 est. 96%

’07–’13 est. 99%

Fiscal years

Midpoint of $214–$226*

estimate for FY’13

*Guidance as of November 7, 2012.

(1) and (2) See notes included at the end of the presentation.

Voice

• Transition to data

• Ramp in WCDMA and EV-DO

• Significant growth in emerging

regions

• DOrA, HSPA+

• Increased device

capabilities

• 2G to 3G migration

• Growth in smartphones &

connected devices

• 3G/LTE adoption

• Increased device capabilities;

memory, display, camera...

Voice/data transition Voice & enhanced data Smartphones

• Voice-centric devices

• Growth in CDMA 2000

• Focus on developed

regions

9

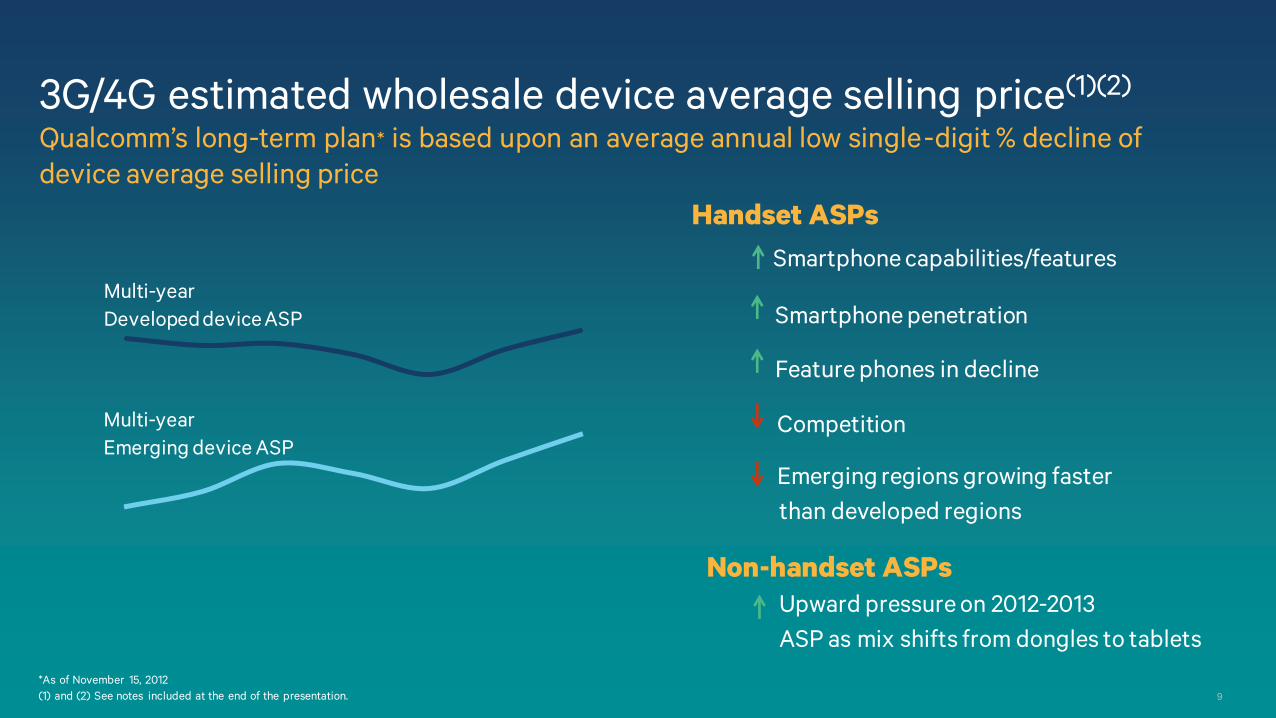

3G/4G estimated wholesale device average selling price(1)(2)

Qualcomm’s long-term plan* is based upon an average annual low single-digit % decline of

device average selling price

Multi-year

Developed device ASP

Multi-year

Emerging device ASP

Smartphone capabilities/features

Smartphone penetration

Feature phones in decline

Competition

Emerging regions growing faster

than developed regions

Upward pressure on 2012-2013

ASP as mix shifts from dongles to tablets

Handset ASPs

Non-handset ASPs

*As of November 15, 2012

(1) and (2) See notes included at the end of the presentation.

10

Key initiatives for sustained, long-term growth Qualcomm innovations underpin industry dynamics

Drive smartphone

growth and innovation

Create new

mobile computing

opportunities

Solve the 1000x

data challenge Enable growth

in emerging regions

Deliver the Internet

of Everything

11

Our most important device Immediacy, portability, connectedness

Source: Google/Sterling Brands/Ipsos Multi-Screen Research, Aug. ’12

1/3+ of daily media interactions occur

on a smartphone

~1/2 of smartphone owners use them

while watching TV

4/5 of all searches on a smartphone

are spontaneous, compared to 52% on PC

12

2011 2012 2013 2014 2015 2016

Annual forecasted smartphone unit shipments

24% CAGR 2011–2016

Continued smartphone momentum Displacing feature phones

Cumulative smartphone unit sales

forecast between 2012–2016 ~5B Source: Average of Gartner, Oct. ’12; Strategy Analytics, Aug. ’12

13

Expanding areas for smartphone innovation

GPU

CPU

DSP/Multimedia

Sensors

Connectivity

Displays

Modems

14

GPU

Expanding areas for smartphone innovation

2MB L2 (8064 only) aSMP Custom krait Web Tech innovations High performance floating point Custom system interconnect

FlexRenderTM technology GPGPU compute for imaging/video (Renderscript, OpenCL, LLVM) Unified shader architecture Low power innovations Stereoscopic rendering Accelerated WebGL Profiling tools

21 MPix 20x digital zoom Zero shutter lag Ultrasound 7.1 surround playback 5.1 surround camcorder

Stereo 3D video 1080p HD video Browser with HTML5 and 1080p flash Computational camera Noise cancellation

LTE world mode LTE broadcast

LTE TDD RF multi-band

TD-SCDMA

Coexistence with connectivity VoLTE/SRVCC

Advanced receivers Power optimization

BT Miracast

Multiband FM

Coexistence with WWAN Indoor location

GPS/GNSS .11ac

Temperature Gyroscope IR sensing Humidity

Magnetometer

Accelerometer Proximity Pressure

Ambient light Gestures

3D Wireless display

MEMS

Color correction Content adaptive backlight Frame buffer compression

Sensors

Connectivity

Displays

Modems CPU

DSP/Multimedia

15

Qualcomm Snapdragon processor leadership

*Includes Qualcomm reference design

Source: Qualcomm data

85+ manufacturers shipping

550+ designs in development*

770+ devices announced*

16

Snapdragon Processors

Snapdragon 800

Premium smartphones, Smart

TVs, digital media adapters

and tablets.

Snapdragon 600

Mid-high tier smartphones

and tablets.

Snapdragon 400

High volume smartphones

and tablets.

Snapdragon 200

Entry level smartphones.

17

Mobile is redefining computing

High resolution screens Responsive devices

Fast, always-on connectivity Rich multimedia experience

High performance computing

Sleek, ultra-light

Longer battery life

Thermal efficiency

Without compromising mobility

18

New mobile computing growth opportunities Tablets to lead growth of new generation of mobile computing devices

41% CAGR (2011-2016)

Tablets: Average of Gartner, Dec. ’12; Strategy Analytics, Jan. ’12;

19

3G/4G growth in emerging regions

2.7B

2011 2016

3G/4G Connections

0.8B

Source: Wireless Intelligence, Nov. ’12

+255% Expected growth

20

Qualcomm reference designs Accelerating global growth of 3G smartphones

Source: Qualcomm data

170+ devices launched

13 countries

40+ OEMs

21

~2x from 2010–2011*

Mobile data traffic growth

Network efficiency Small cells More spectrum

Source: Cisco, Feb ‘11

Global data traffic growth

1000x data traffic growth

Preparing for

22

Qualcomm LTE leadership and scale

Source: Qualcomm data

700+ LTE OEM devices based on Qualcomm LTE chips:

300+ OEM LTE devices accepted by carriers

400+ more OEM LTE designs in the pipeline

23

Connectivity Wi-Fi BT GPS

The unique Qualcomm advantage Hiding the complexity underneath the most seamless mobile connectivity

22 33

27

35 36 37 38

39 40 41 42 43 1 2 8 3 4 5 6 9

28

34

7 10 11 12

13 14 17 44 18

19

20

21

23 24

25

26 Radio Frequency Bands

GERAN CDMA 1x UMTS TD-SCDMA LTE TDD/FDD EV-DO

LTE

2G/3G

System Selection

Blind Redirection

Redirection w/ Measurements

Reselection

PS Handover

CS Fallback

CSFB w/ SI Tunneling

Single Radio VCC

Handover Techniques (Multiple Can Apply in Each Case) Handover Combinations (Hypothetical Examples)

24

Qualcomm RF360 Front End Solution The First Truly Global Solution for 4G LTE Devices

Single SKU

Power

Performance

Size

Time to market

Advantages

25

Demand driving extreme densification

26

Small cells everywhere Low cost, small size and ease of deployment

3G 4G

Wi-Fi

27

Internet of everything Everything around us is becoming intelligent & connected

Health &

fitness

Automotive Industrial

Home

28

Digital 6th sense

29

Key initiatives for sustained, long-term growth Qualcomm innovations underpin industry dynamics

Drive smartphone

growth and innovation

Create new

mobile computing

opportunities

Solve the 1000x

data challenge

Technology leadership and financial strength

Enable growth

in emerging regions

Deliver the Internet

of Everything

30

Footnotes

1. Total reported device sales is the sum of all reported sales in U.S. dollars (as reported to us by our licensees) of all licensed CDMA-based, OFDMA-based and

multimode CDMA/OFDMA subscriber devices (including handsets, modules, modem cards and other subscriber devices) by our licensees during a particular

period (collectively, “3G/4G devices”). The reported quarterly estimated ranges of ASPs and unit shipments are determined based on the information as reported

to us by our licensees during the relevant period and our own estimates of the selling prices and unit shipments for licensees that do not provide such

information. Not all licensees report sales, selling prices and/or unit shipments the same way (e.g., some licensees report selling prices net of permitted

deductions, such as transportation, insurance and packing costs, while other licensees report selling prices and then identify the amount of permitted deductions

in their reports), and the way in which licensees report such information may change from time to time. Total reported device sales, estimated unit shipments and

estimated ASPs for a particular period may include prior period activity that was not reported by the licensee until such particular period.

2. The midpoints of the estimated ranges are identified for comparison purposes only and do not indicate a higher degree of confidence in the midpoints.

31

For more information on Qualcomm, visit us at:

www.qualcomm.com & www.qualcomm.com/blog

Qualcomm is a trademark of Qualcomm Incorporated, registered in the United States and other countries.

Other products and brand names may be trademarks or registered trademarks of their respective owners

Thank you Follow us on: