bengin the intangible evaluation the service version 2.0 draft, not for distribution bengin - the...

TRANSCRIPT

bengin

The Intangible Evaluation

The Service

Version 2.0

Draft, not for Distributionbengin - The Intangible Evaluation – The Service V2.0_e.ppt

Index

• The new Business World

• The bengin.com approach

• The Benefit for the customers

• The MindSet: how does it work?

• Some examples from the market

• More ways to use the analysis

• Additional Types of analysis

Complexity of the new Business World rises and the Business Models have to reflect this

Valueto be

Mapped

Valueto be

Mapped

Business ModelBusiness Model

intangibleintangible

tangibletangible

newnewoldold T

Real Economy

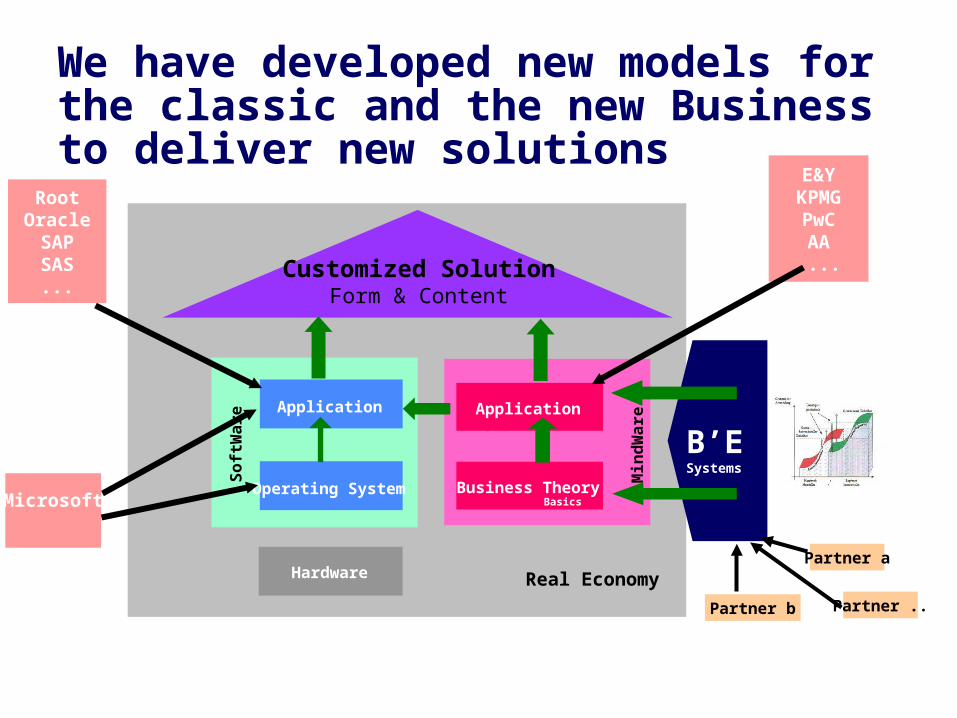

We have developed new models for the classic and the new Business to deliver new solutions

Customized SolutionForm & Content

So

ftW

are

Application

Operating System

Hardware

Min

dW

areApplication

Business TheoryBasics

RootOracleSAPSAS

...

RootOracleSAPSAS

...

MicrosoftMicrosoft

E&YKPMGPwCAA....

B’ESystems

Partner b

Partner a

Partner ..

1. Structure

2. Quantity

3. Direction

4. Optimization

We developed the original know-how, the procedures and the instruments to analyze the new Business World and to find the needed Solutions.

We developed the original know-how, the procedures and the instruments to analyze the new Business World and to find the needed Solutions.

We concentrate on the evaluation of the total assets of a company, because.... „YOU CANNOT MANAGE WHAT YOU CANNOT MEASURE“!

2. Quantity

The total value of a company is the sum of its Tangible and Intangible Assets.

Only by managing the Tangible Assets

(money based) and the Intangible Assets (Knowledge, Skills, Market Position, etc.) the company can achieve their goals successfully.

Intangible Value

Tangible ValueT

ITotal Value

The Value Vector

Evaluating the Intangible, our customers can gain in various ways

Large, international companies, mid-sized companies and governamental Departments and Institution:

To analyze their current position and development over time To plan internal changes To plan mergers and acquisitions To plan spin offs and oursoucing To evaluate the market position (benchmark) To evaluate the productivity of various Business Units To evaluate new projects (integration in the company assets) ........

Investment companies and Venture Capitals:

To evaluate the potential of an investment (e.g. in a start up, etc) To plan the future „exit strategy“ ........

Start up companies:

To explain (calibrate) their own potential to an Investor To show the development over time of their own potential ........

Evaluating the Intangible, our customers can gain in various ways

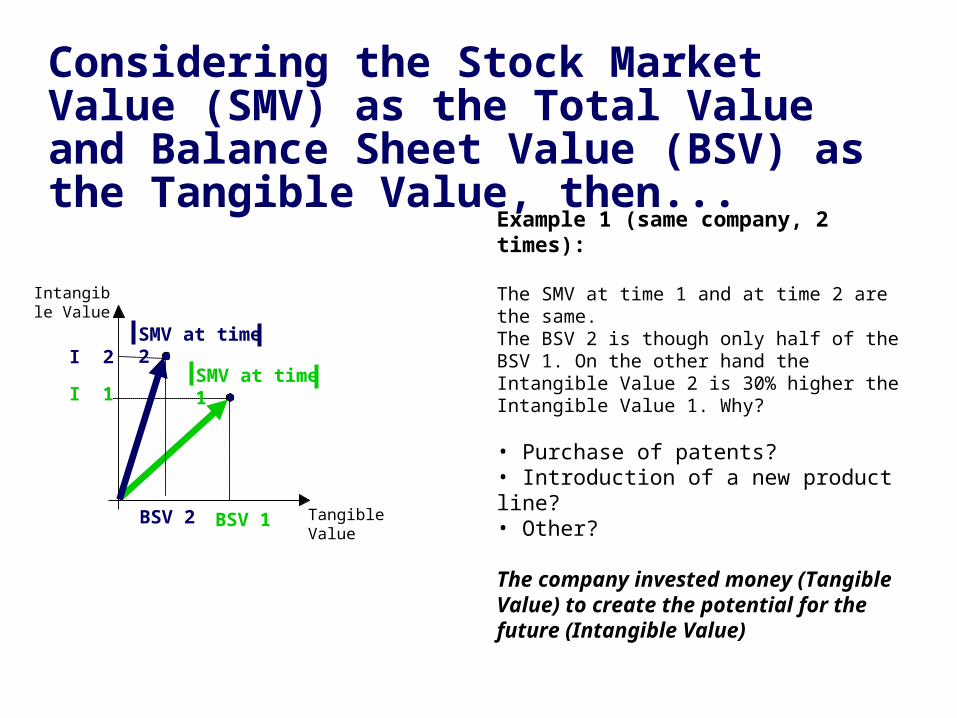

Considering the Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value, then...

Example 1 (same company, 2 times):

The SMV at time 1 and at time 2 are the same.The BSV 2 is though only half of the BSV 1. On the other hand the Intangible Value 2 is 30% higher the Intangible Value 1. Why?

• Purchase of patents?• Introduction of a new product line?• Other?

The company invested money (TangibleValue) to create the potential for the future (Intangible Value)

Intangible Value

Tangible ValueBSV 1

I 1SMV at time 1

BSV 2

I 2SMV at time 2

Intangible Value

Tangible ValueBSV 1

I 1SMV 1

SMV 3

BSV 3

I 3

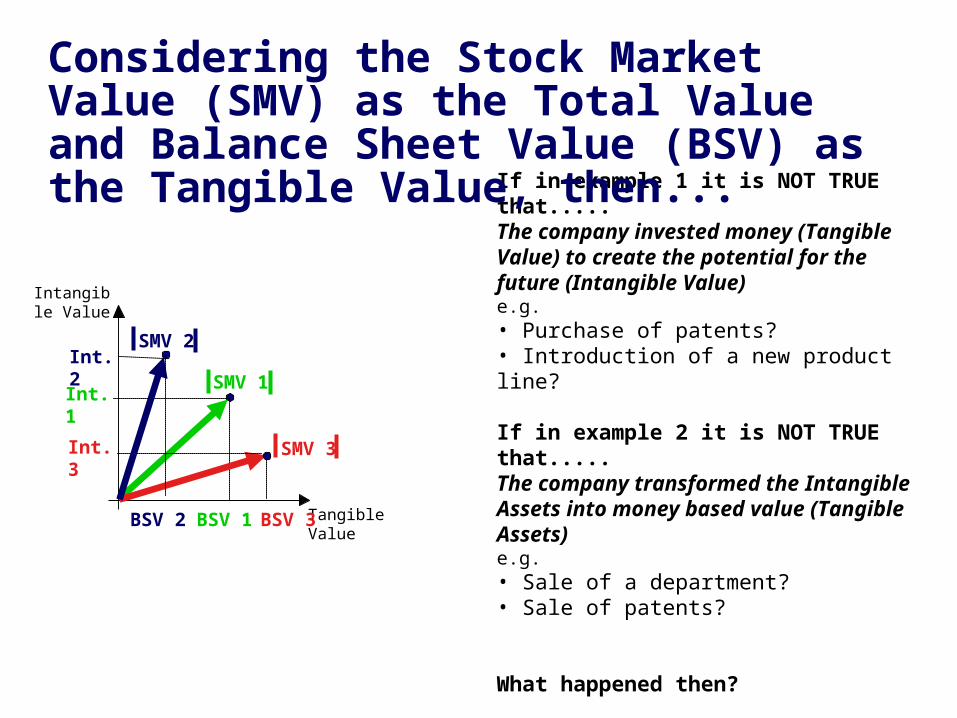

Example 2 (same company, 2 times):

The SMV at time 1 and at time 2 are the same.The Balance Value 3 increased by 20% compared to the Balance Value 1. On the other hand the Intangible Value 3 is less than half of the Intangible Value 1. Why?

• Sale of a department?• Sale of patents?• Other?

The company transformed Intangible Assets into money based value (Tangible Assets)

Considering the Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value, then...

If in example 1 it is NOT TRUE that.....The company invested money (TangibleValue) to create the potential for the future (Intangible Value)e.g. • Purchase of patents?• Introduction of a new product line?

If in example 2 it is NOT TRUE that.....The company transformed the Intangible Assets into money based value (Tangible Assets)e.g.• Sale of a department?• Sale of patents?

What happened then?

Considering the Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value, then...

Intangible Value

Tangible ValueBSV 1

Int. 1

BSV 3

Int. 3

SMV 2Int. 2

BSV 2

SMV 1

SMV 3

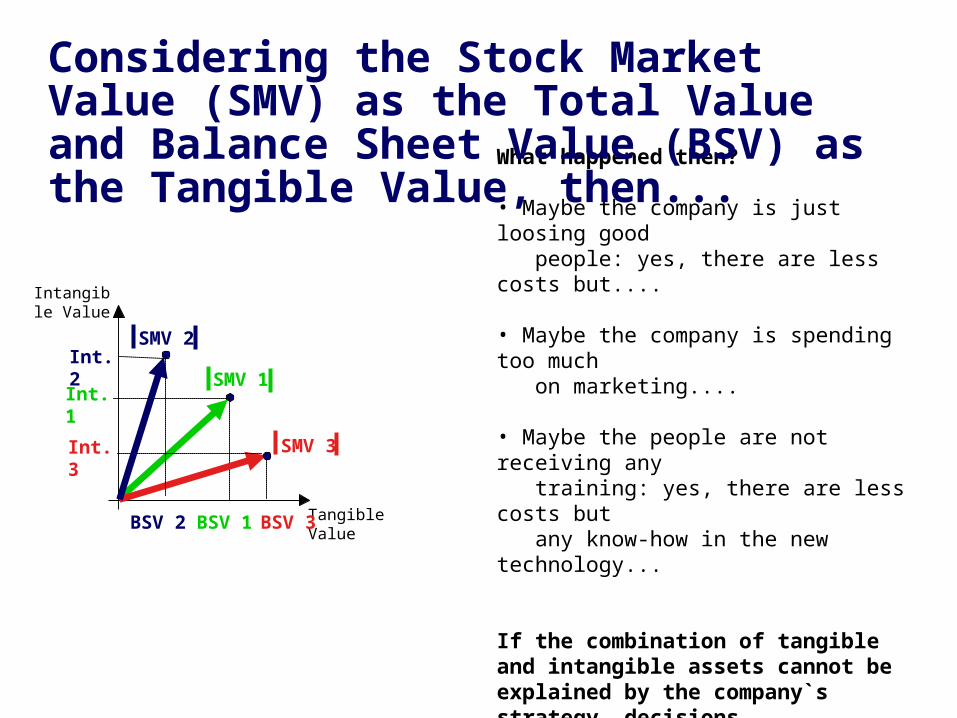

What happened then?

• Maybe the company is just loosing good people: yes, there are less costs but....

• Maybe the company is spending too much on marketing....

• Maybe the people are not receiving any training: yes, there are less costs but any know-how in the new technology...

If the combination of tangible and intangible assets cannot be explained by the company`s strategy, decisions, actions......then we must look deeper. The causes need to be discovered in order to better manage the company

Considering the Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value, then...

Intangible Value

Tangible Value

Int. 1

Int. 3

Int. 2SMV 2

SMV 1

SMV 3

BSV 1 BSV 3BSV 2

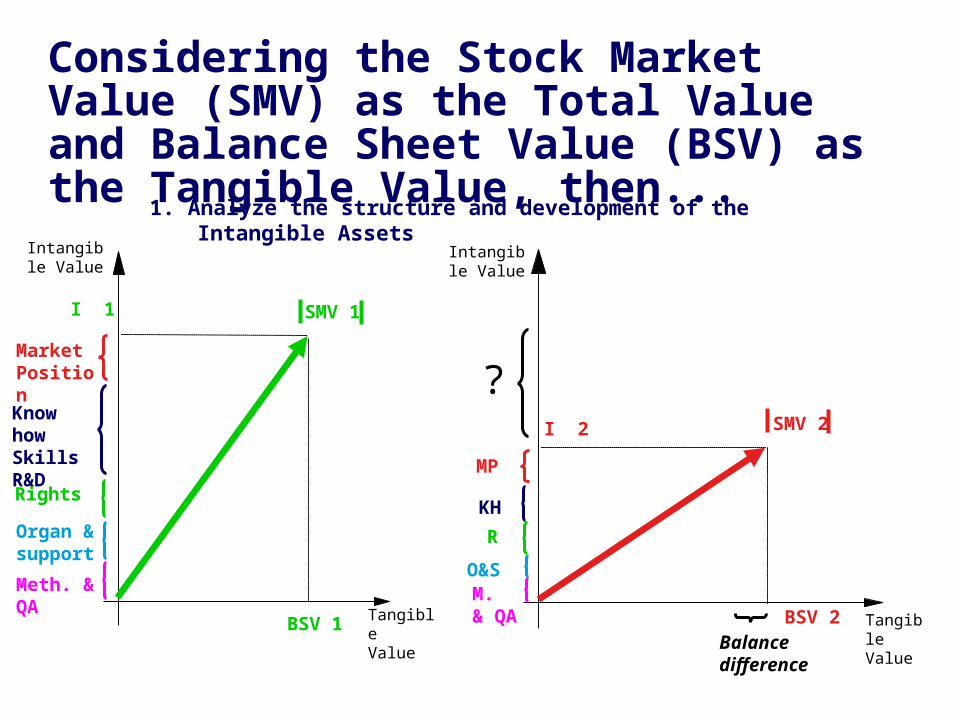

1. Analyze the structure and development of the Intangible Assets

Considering the Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value, then...

Intangible Value

Rights

Intangible Value

Tangible Value

BSV 1

I 1

Market Position

Know howSkillsR&D

Organ &support

Meth. &QA

TangibleValue

BSV 2

I 2

MP

KH

R

O&SM. & QA

?

Balancedifference

SMV 1

SMV 2

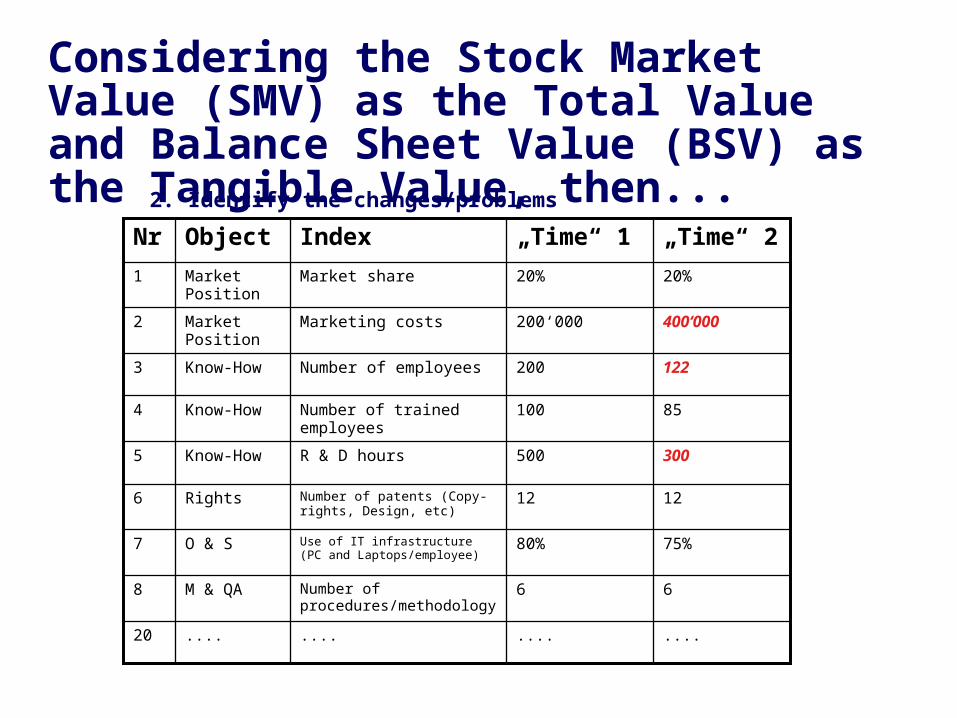

2. Identify the changes/problems

................20

66Number of procedures/methodology

M & QA8

75%80%Use of IT infrastructure (PC and Laptops/employee)

O & S7

1212Number of patents (Copy- rights, Design, etc)

Rights6

300500R & D hoursKnow-How5

85100Number of trained employees

Know-How4

122200Number of employeesKnow-How3

400‘000200‘000Marketing costsMarket Position

2

20%20%Market shareMarket Position

1

„Time“ 2„Time“ 1IndexObjectNr

Considering the Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value, then...

3. Discover the reasons

People left – see Nr 3

Reason not clear!

Organized event to launch new products

Reasons

Consequence of Nr 3

Yes, it need to be solved!

no

Actions needed?

300

122

400‘000

„Time“ 2

500R & D hoursKnow-How5

200Number of employees

Know-How3

200‘000Marketing costsMarket Position

2

„Time“ 1IndexObjectNr

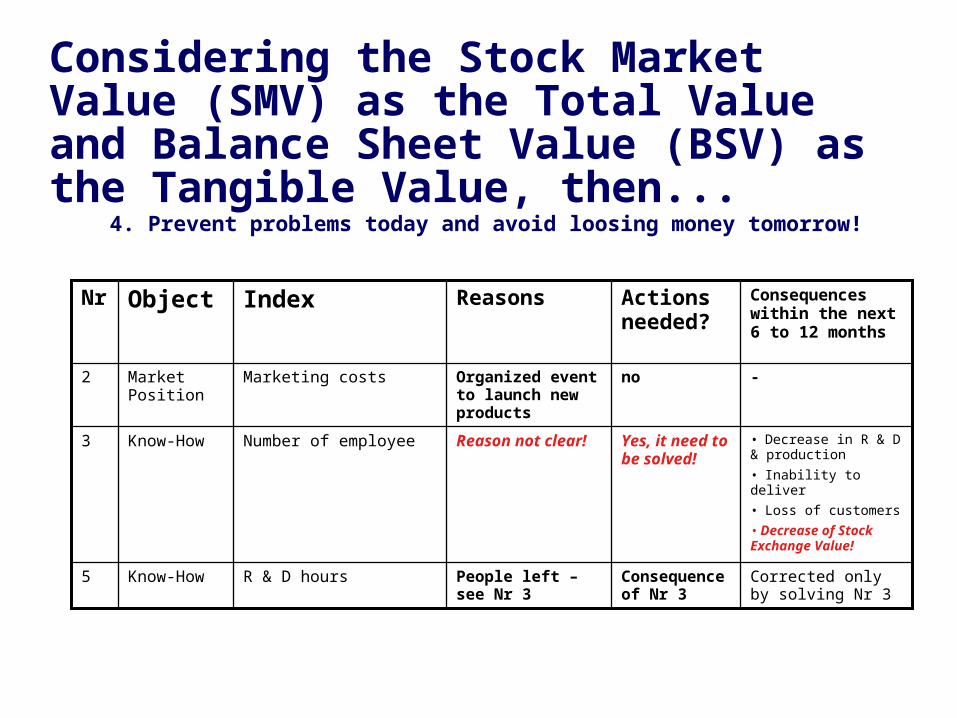

Considering the Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value, then...

4. Prevent problems today and avoid loosing money tomorrow!

Corrected only by solving Nr 3

• Decrease in R & D & production

• Inability to deliver

• Loss of customers

• Decrease of Stock Exchange Value!

-

Consequences within the next 6 to 12 months

Consequence of Nr 3

Yes, it need to be solved!

no

Actions needed?

People left – see Nr 3

R & D hoursKnow-How5

Reason not clear!Number of employeeKnow-How3

Organized event to launch new products

Marketing costsMarket Position

2

ReasonsIndexObjectNr

Considering the Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value, then...

By analyzing only the Tangible Assets (money based) you would recognize the problems TOO LATE.

The Intangible Assets of today represent the TangibleAssets of tomorrow, therefore knowing them will help you manage the total assets of the company better.

In this example:Knowing the possible internal problems 6 to 12 months in advance will allow you to correct the problems before they effect the company Market Value!

Considering the Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value, then...

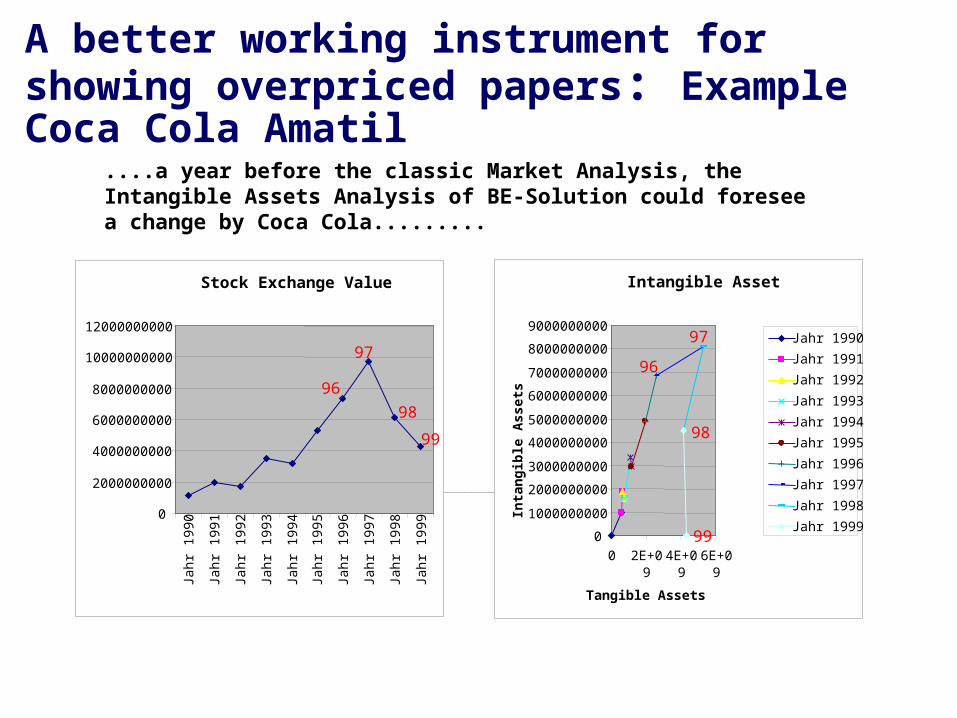

A better working instrument for showing overpriced papers: Example Coca Cola Amatil

Intangible Asset

0

1000000000

2000000000

3000000000

4000000000

5000000000

6000000000

7000000000

8000000000

9000000000

0 2E+09

4E+09

6E+09

Tangible Assets

Inta

ng

ible

Ass

ets

Jahr 1990

Jahr 1991

Jahr 1992

Jahr 1993

Jahr 1994

Jahr 1995

Jahr 1996

Jahr 1997

Jahr 1998

Jahr 1999

96

97

98

99

Stock Exchange Value

0

2000000000

4000000000

6000000000

8000000000

10000000000

12000000000

Jahr

199

0

Jahr

199

1

Jahr

199

2

Jahr

199

3

Jahr

199

4

Jahr

199

5

Jahr

199

6

Jahr

199

7

Jahr

199

8

Jahr

199

9

96

97

98

99

....a year before the classic Market Analysis, the Intangible Assets Analysis of BE-Solution could foresee a change by Coca Cola.........

It is possible to analyze the development of the company‘s asset. Example: a part of ABB

Pointer of vector for five years

0 200 400 600 800 1'000 1'200

1'400

1'600

material axis [Mio sFr]

0

200

400

600

800

1'000

1'200

1'400

inta

ng

ible

axi

s [

i -

Mio

]

96

93 94

92 95 The answer for the question – "What happens in the year 1996?" – is easy:

Part of enterprise sold.It is after all a question of the quality of Management if this loss of intangible values is compensated by the price received for the sold enterprise.

Intagible assets or Shareholder Value Expectation?

5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80

80

75

70

65

60

55

50

45

40

35

30

25

20

15

10

5

Intangible Value [i - Mia]

Tangible Value [Mia]

-

McDonald's

The Tangible Value and the Intangible Value together gives a complete picture about the company value and its development.

The question remain:Are all Intangible Assets or part of it is only Shareholder Value Expectation?

Microsoft IBM

Ford

Coca Cola

Valuepoints of 75 enterprises

0

1'000

2'000

3'000

4'000

5'000

6'000

7'000

8'000

9'000

10'000

0 1'000 2'000 3'000 4'000 5'000 6'000 7'000 8'000 9'000 10'000

tangible Values

inta

ng

ible

Va

lue

s

Analyzing enterprises with the above mentioned instruments leads to fundamentally new decisions on the side of the managers as well as of the side of shareholders, which have nowadays a better/good working instrument for showing overpriced papers.

A better model for new decisions

Investors: Attention!

Management should use potential more effective

More ways to use the analysis: Stock Market Value (SMV) as the Total Value and Balance Sheet Value (BSV) as the Tangible Value

• To evaluate and decide if it is better to „Make“ or „Buy“• To evaluate and decide for an acquisition (Tangible and Intangible)• To evaluate productivity, e.g. the „transformation“ of Intangible into Tangible• To Benchmark• To evaluate the benefits of a merge• .........

This can be done at various levels: Whole Company, Business Unit, department, process or project.

Additional types of analysis

Turnover (Total value) vs. Total costs (Tangible)

e.g. knowing the Total Value (Turnover) and the Tangible Value of a company (Total costs) it is possible to analyze what value is generated by the company (know how, etc.)

To analyze productivityTo analyze resource allocation (intangible ROI)To analyze Value Chain profitabilityTo evaluate a possible spin off or mergeTo compare the values of different departments

This can be done at various levels: Whole Company, Business Unit, department, process or project.

Additional types of analysis

Total costs (Total Value) vs. „Total costs minus Personal costs“ (Tangible)

e.g. knowing the Total Value (Total costs) and the Tangible Value („All cost minus Personal costs“) it is possible to analyze what value is generated by the people (know how, etc.)

To analyze the productivity of employeesTo analyze the value of trainingTo compare the values of different departments

This can be done at various levels: Whole Company, Business Unit, department, process or project.

Contact:

Peter BretscherIngenieurbüro für WirtschaftsentwicklungAlpsteinstrasse 4, CH-9034 [email protected]++41 (0)79 650 49 04