bayernlb fixed income conference - talanx · munich re generali 2 axa 2 ... group (“best...

TRANSCRIPT

Alik Hertel, Head of TreasuryMarcus Sander, Senior Investor Relations Manager Munich, 18 May 2015

BayernLB Fixed Income Conference

2 BayernLB Fixed Income Conference, Munich, 18 May 2015

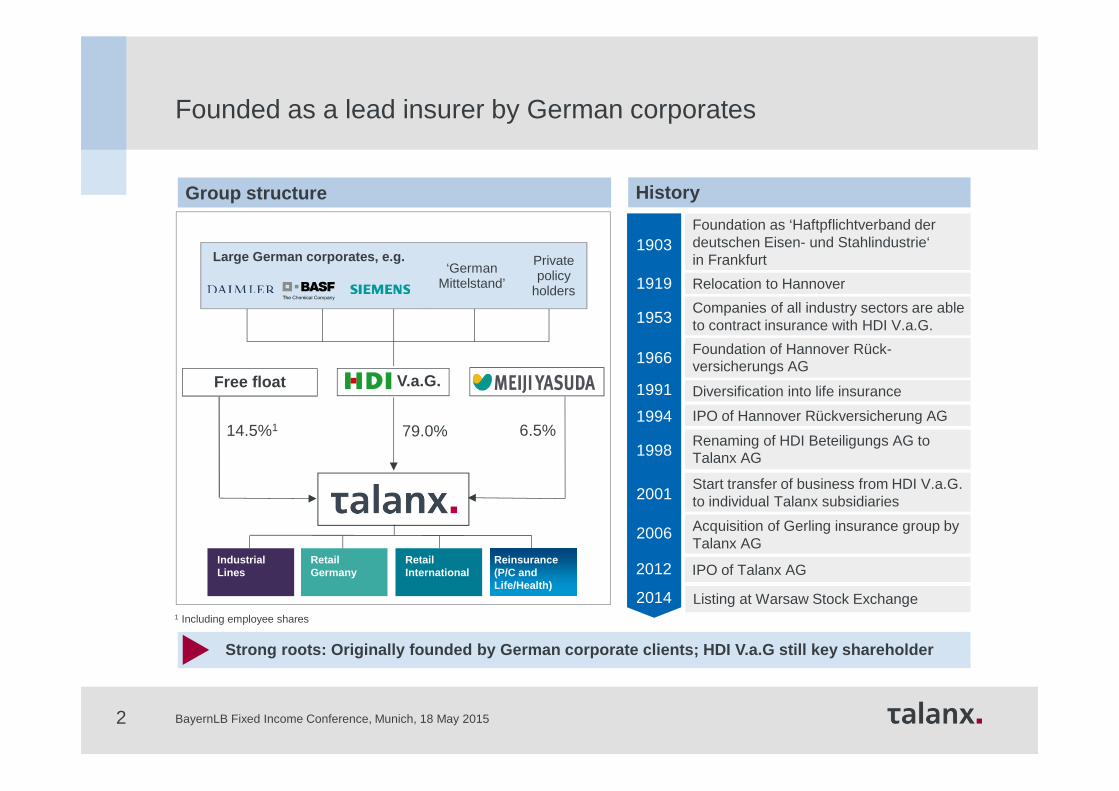

‘German Mittelstand’

Private policy

holders

Large German corporates, e.g.

V.a.G.

79.0%

Strong roots: Originally founded by German corporat e clients; HDI V.a.G still key shareholder

Group structure

Free float

1903

1919

1953

1966

1991

1994

1998

2001

2006

2012

Foundation as ‘Haftpflichtverband der deutschen Eisen- und Stahlindustrie‘in Frankfurt

Relocation to Hannover

Companies of all industry sectors are ableto contract insurance with HDI V.a.G.

Foundation of Hannover Rück-versicherungs AG

Diversification into life insurance

IPO of Hannover Rückversicherung AG

Renaming of HDI Beteiligungs AG to Talanx AG

Start transfer of business from HDI V.a.G. to individual Talanx subsidiaries

Acquisition of Gerling insurance group by Talanx AG

IPO of Talanx AG

History

14.5%1 6.5%

1 Including employee shares

IndustrialLines

RetailGermany

Reinsurance (P/C and Life/Health)

RetailInternational

Founded as a lead insurer by German corporates

Listing at Warsaw Stock Exchange2014

3

IndustrialLines

RetailGermany

Reinsurance(P/C andLife/Health)

RetailInternational

CorporateOperations

Four divisions with a strong portfolio of brands

Integrated international insurance group following a multi-brand approach

BayernLB Fixed Income Conference, Munich, 18 May 2015

4

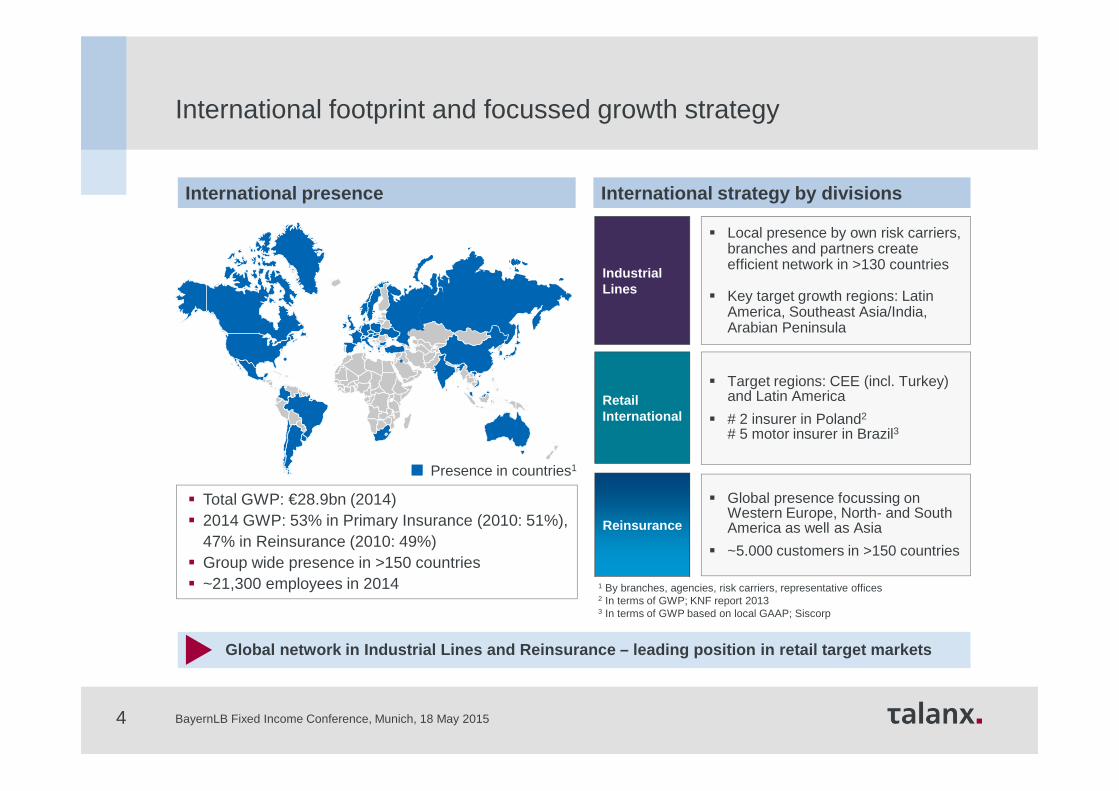

Industrial Lines

Retail International

Reinsurance

� Local presence by own risk carriers, branches and partners create efficient network in >130 countries

� Key target growth regions: Latin America, Southeast Asia/India, Arabian Peninsula

� Target regions: CEE (incl. Turkey) and Latin America

� # 2 insurer in Poland2

# 5 motor insurer in Brazil3

� Global presence focussing on Western Europe, North- and South America as well as Asia

� ~5.000 customers in >150 countries

Presence in countries1

1 By branches, agencies, risk carriers, representative offices2 In terms of GWP; KNF report 20133 In terms of GWP based on local GAAP; Siscorp

International presence International strategy by divisions

� Total GWP: €28.9bn (2014)� 2014 GWP: 53% in Primary Insurance (2010: 51%),

47% in Reinsurance (2010: 49%)� Group wide presence in >150 countries� ~21,300 employees in 2014

Global network in Industrial Lines and Reinsurance – leading position in retail target markets

International footprint and focussed growth strategy

BayernLB Fixed Income Conference, Munich, 18 May 2015

5

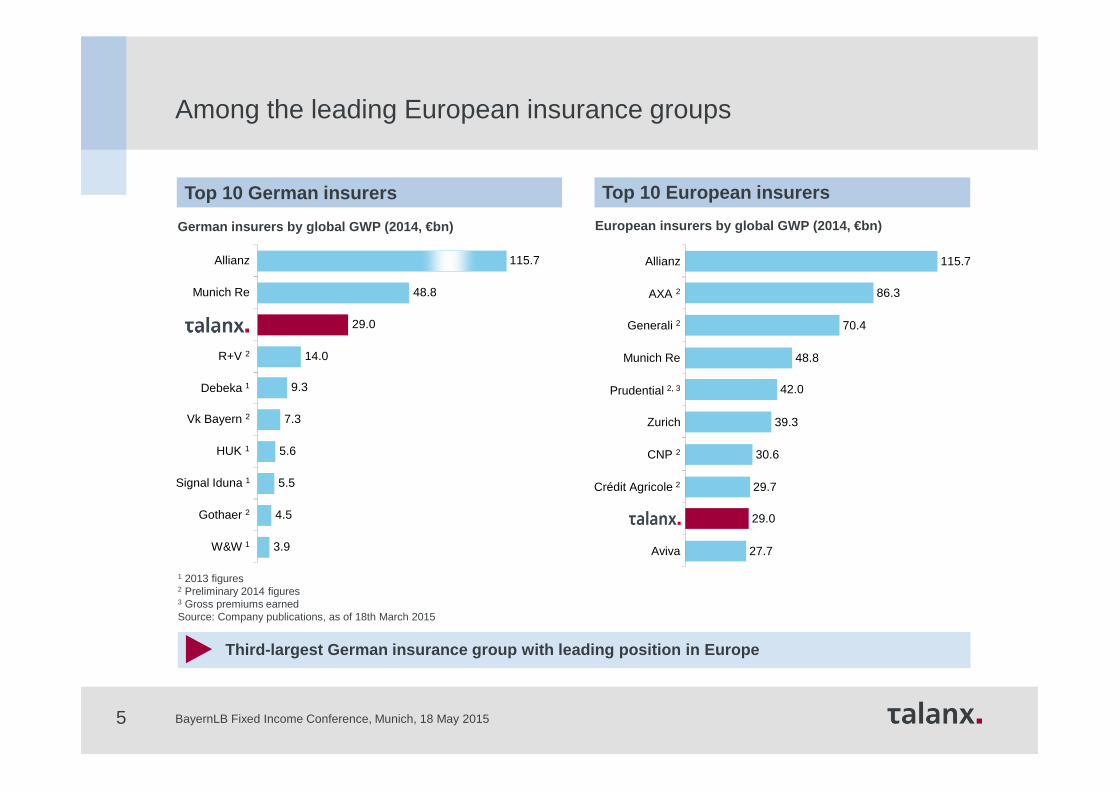

European insurers by global GWP (2014, €bn)German insurers by global GWP (2014, €bn)

Listed insurers

1 2013 figures2 Preliminary 2014 figures3 Gross premiums earnedSource: Company publications, as of 18th March 2015

Top 10 European insurersTop 10 German insurers

Third-largest German insurance group with leading p osition in Europe

Among the leading European insurance groups

3.9

4.5

5.5

5.6

7.3

9.3

14.0

29.0

48.8

115.7

W&W 1

Gothaer 2

Signal Iduna 1

HUK 1

Vk Bayern 2

Debeka 1

R+V 2

Munich Re

Allianz

27.7

29.0

29.7

30.6

39.3

42.0

48.8

70.4

86.3

115.7

Aviva

Crédit Agricole 2

CNP 2

Zurich

Prudential 2, 3

Munich Re

Generali 2

AXA 2

Allianz

BayernLB Fixed Income Conference, Munich, 18 May 2015

6

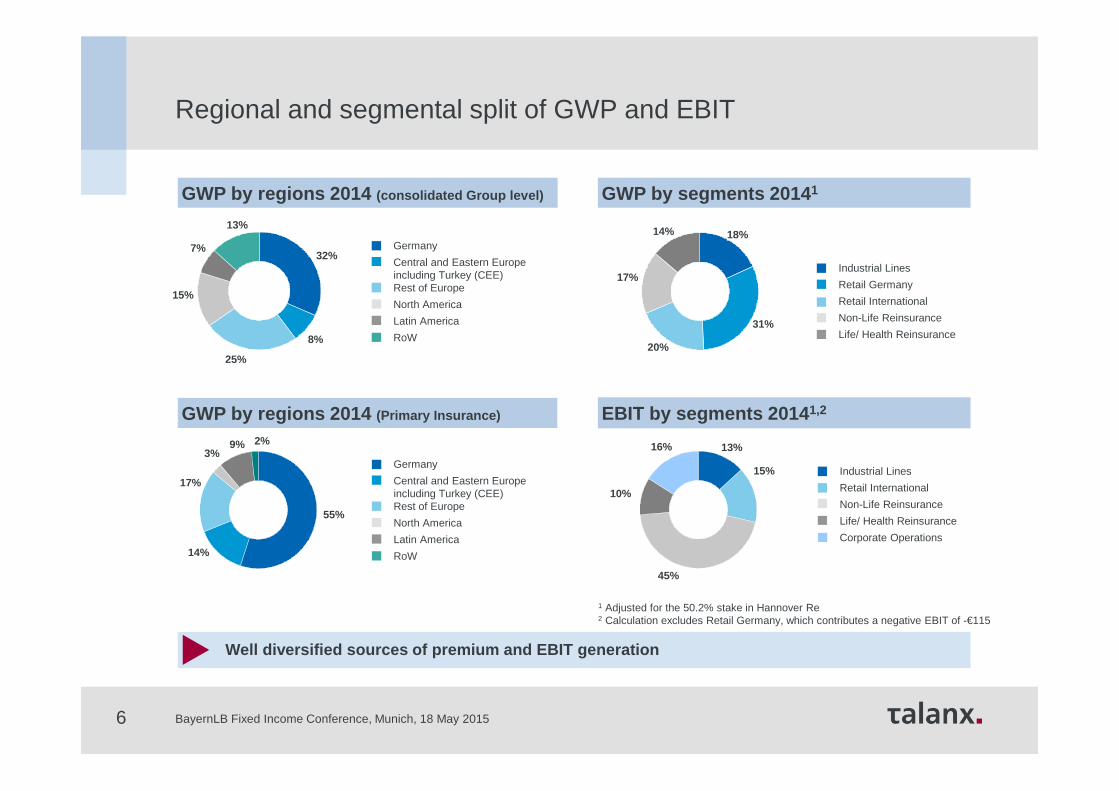

GWP by regions 2014 (Primary Insurance)

Regional and segmental split of GWP and EBIT

GWP by regions 2014 (consolidated Group level)

Germany

Central and Eastern Europe including Turkey (CEE)Rest of Europe

North America

Latin America

RoW

GWP by segments 2014 1

Industrial Lines

Retail Germany

Retail International

Non-Life Reinsurance

Life/ Health Reinsurance

EBIT by segments 2014 1,2

Industrial Lines

Retail International

Non-Life Reinsurance

Life/ Health Reinsurance

Corporate Operations

Well diversified sources of premium and EBIT genera tion

31%

13%

15%

45%

10%

16%

1 Adjusted for the 50.2% stake in Hannover Re2 Calculation excludes Retail Germany, which contributes a negative EBIT of -€115

18%

20%

17%

14%

Germany

Central and Eastern Europe including Turkey (CEE)Rest of Europe

North America

Latin America

RoW

32%

8%

25%

15%

7%

13%

55%

14%

17%

3%9% 2%

BayernLB Fixed Income Conference, Munich, 18 May 2015

7

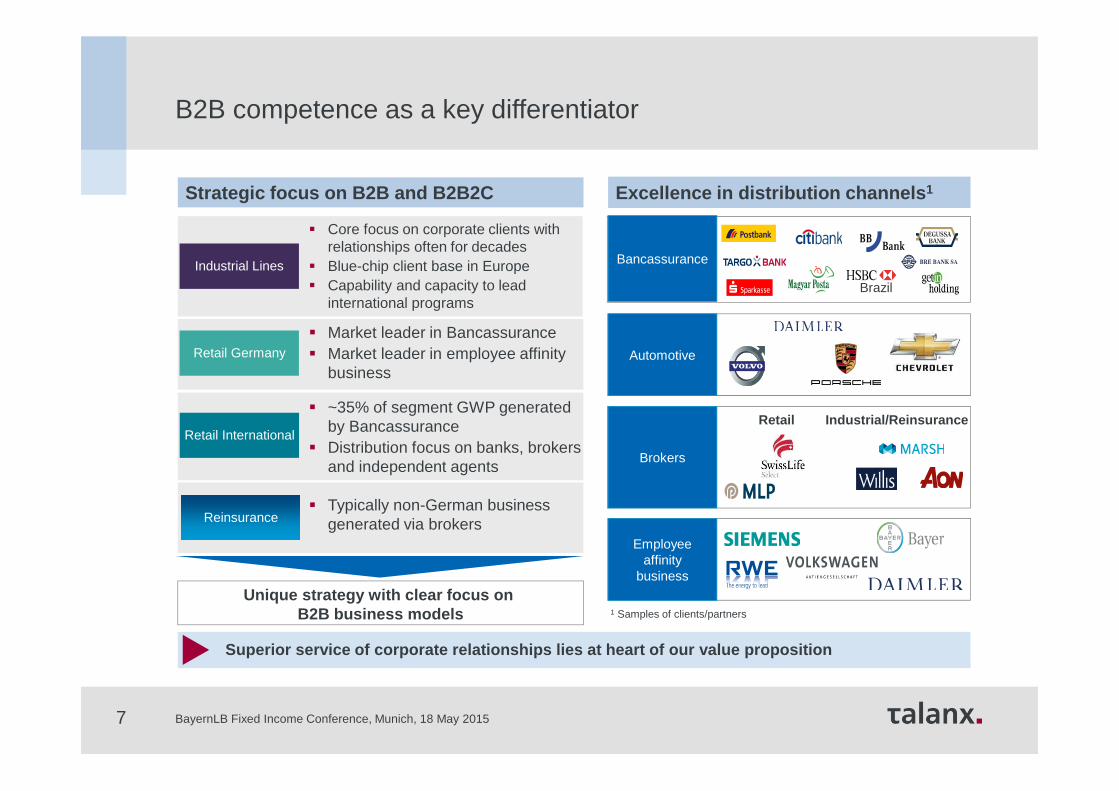

Industrial Lines

Retail Germany

Retail International

Reinsurance

� Market leader in Bancassurance� Market leader in employee affinity

business

� Core focus on corporate clients with relationships often for decades

� Blue-chip client base in Europe� Capability and capacity to lead

international programs

� ~35% of segment GWP generatedby Bancassurance

� Distribution focus on banks, brokers and independent agents

� Typically non-German business generated via brokers

Unique strategy with clear focus on B2B business models

Strategic focus on B2B and B2B2C Excellence in distribution channels 1

Brokers

Bancassurance

Automotive

Employee affinity

business

Retail Industrial/Reinsurance

Brazil

Superior service of corporate relationships lies at heart of our value proposition

B2B competence as a key differentiator

1 Samples of clients/partners

BayernLB Fixed Income Conference, Munich, 18 May 2015

8

Industrial Lines Retail Germany Retail International Reinsurance Selected examples

Right of first choice for Hannover Re to underwrite business from Talanx’s primary insurance companies

Opportunity for higher retention on Group level

Retail International acting as entry pointand (licensed) platform to write industrial risk in new markets

Business relationships by Industrial Lines help to sell retail policies (employee affinity business, auto dealerships)

Leveraging expertise across Talanx Group (“best practice”), e.g. productdevelopment, underwriting capabilities, Bancassurance know-how

Opportunities for Group-wide synergies

Group-wide cooperation and “best practice” approach c reates value for Talanx Group

Group-wide asset management unit (Talanx Asset Management)

Securing reinsurance support

Fronting arrangements to expand global footprint

Market entry support

Support acquisition and product distribution

Leveraging expertise across the Group

Synergy benefits from shared back-office, IT and reinsurance procurement

BayernLB Fixed Income Conference, Munich, 18 May 2015

9

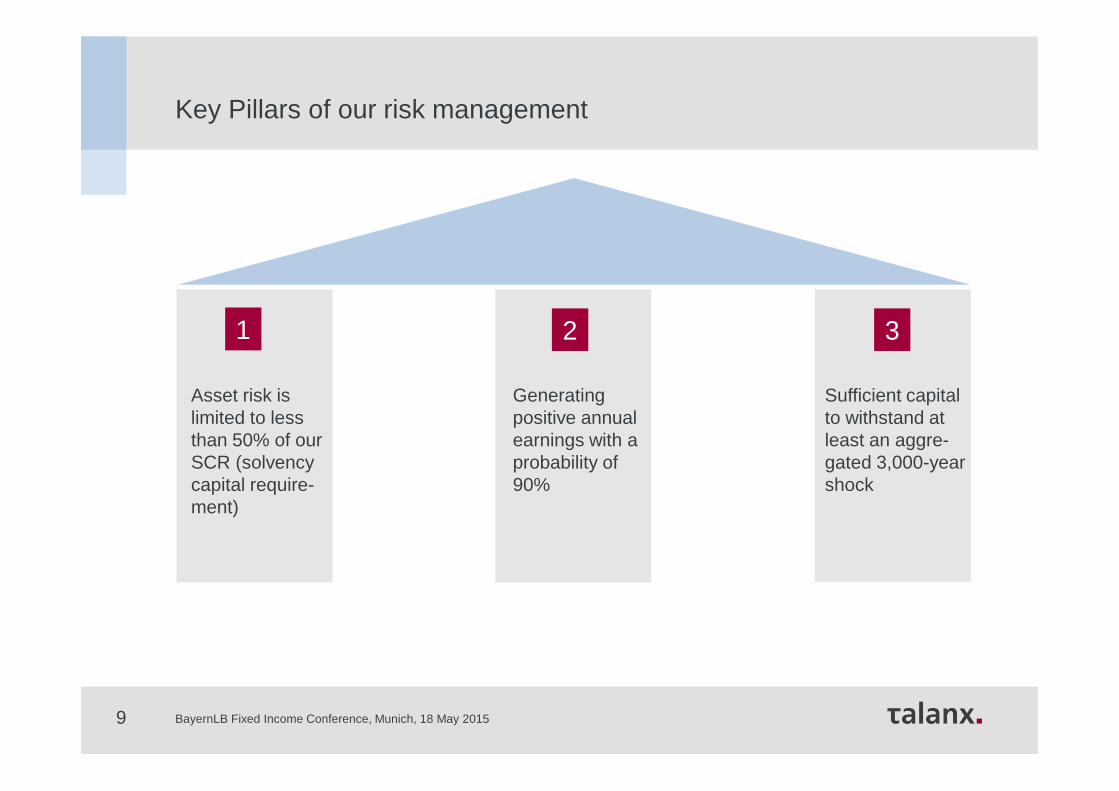

Key Pillars of our risk management

Asset risk is limited to less than 50% of our SCR (solvency capital require-ment)

Generating positive annual earnings with a probability of 90%

Sufficient capital to withstand at least an aggre-gated 3,000-year shock

1 2 3

BayernLB Fixed Income Conference, Munich, 18 May 2015

10

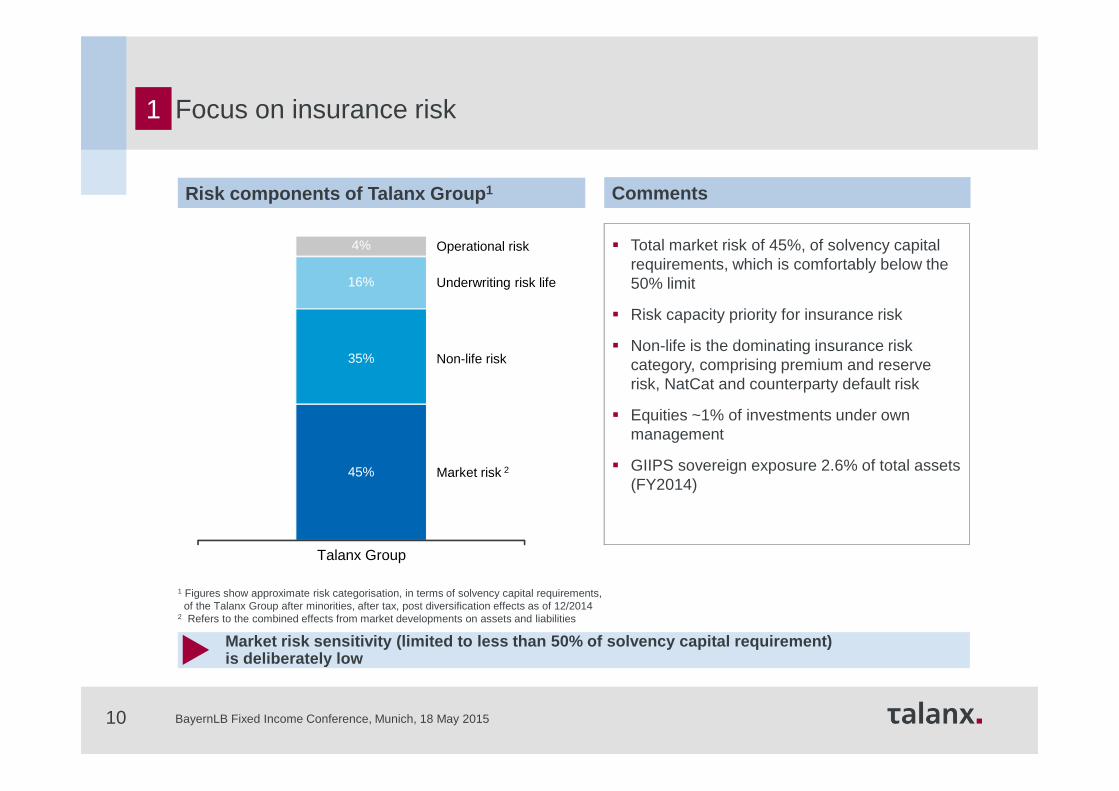

Market risk 2

Non-life risk

Underwriting risk life

Operational risk � Total market risk of 45%, of solvency capital requirements, which is comfortably below the 50% limit

� Risk capacity priority for insurance risk

� Non-life is the dominating insurance risk category, comprising premium and reserve risk, NatCat and counterparty default risk

� Equities ~1% of investments under own management

� GIIPS sovereign exposure 2.6% of total assets (FY2014)

45%

35%

16%

4%

Talanx Group

Market risk sensitivity (limited to less than 50% o f solvency capital requirement) is deliberately low

1 Figures show approximate risk categorisation, in terms of solvency capital requirements,of the Talanx Group after minorities, after tax, post diversification effects as of 12/2014

2 Refers to the combined effects from market developments on assets and liabilities

CommentsRisk components of Talanx Group 1

1 Focus on insurance risk

BayernLB Fixed Income Conference, Munich, 18 May 2015

11

2005 2006 2007 2008 2009 2010 2011 2012

7 1 2- - - 3 2

2013

2

+ Net profit – Net loss

1 Net income of Talanx after minorities, after tax based on restated figures as shown in annual reports (2004–2013 according to IFRS)2 Adjusted on the basis of IAS 83 Top 20 European listed peers, each year measured by GWP;on group level; IFRS standardsSource: Bloomberg, annual reports

Tal

anx

Gro

up a

ndpr

edec

esso

rs n

et in

com

e1

Talanx Group net income 1 (€m)

# of

loss

mak

ing

com

petit

ors3

+ + + + + + + + + +

Talanx Group net income

Robust cycle resilience due to diversification of s egments

Diversification of business model leads to earnings resilience 2

2014

-

245

394

477

183

4852

2162

5152

6262

7322 769

BayernLB Fixed Income Conference, Munich, 18 May 2015

12

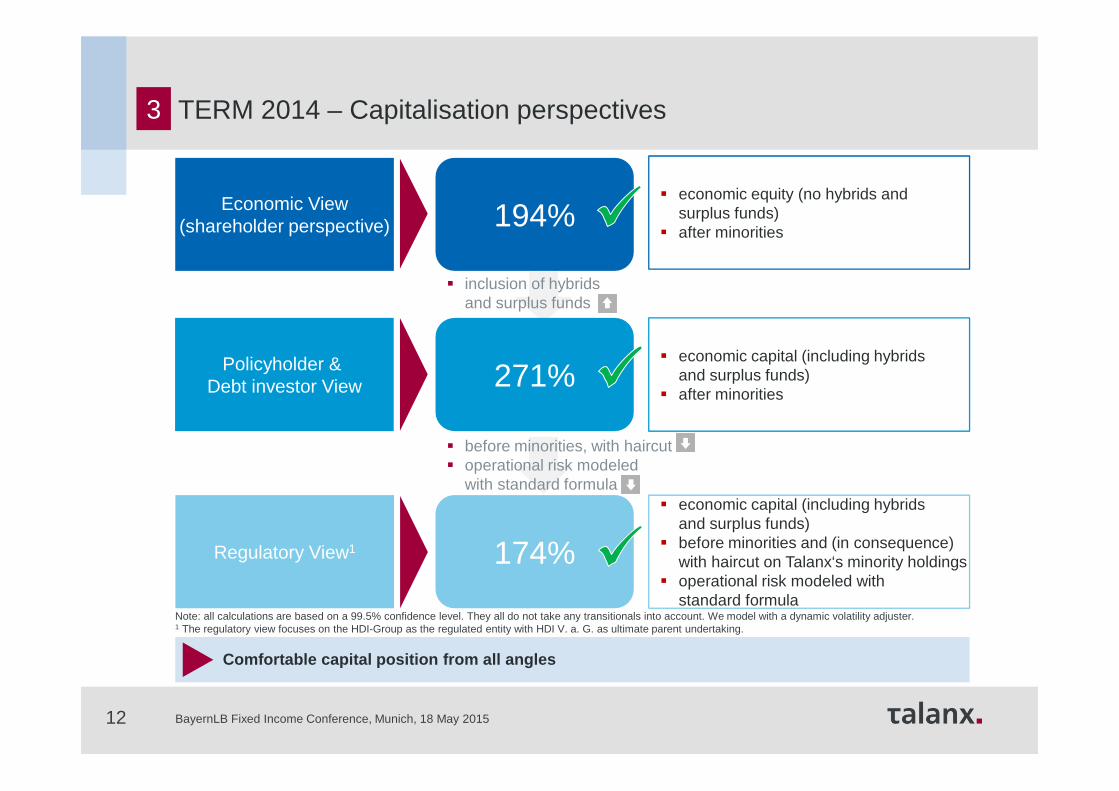

3

� before minorities, with haircut� operational risk modeled

with standard formula

Policyholder & Debt investor View 271%

� economic capital (including hybrids and surplus funds)

� after minorities

174%

TERM 2014 – Capitalisation perspectives

Comfortable capital position from all angles

Economic View(shareholder perspective)

Regulatory View1

Note: all calculations are based on a 99.5% confidence level. They all do not take any transitionals into account. We model with a dynamic volatility adjuster.1 The regulatory view focuses on the HDI-Group as the regulated entity with HDI V. a. G. as ultimate parent undertaking.

194%� economic equity (no hybrids and

surplus funds)� after minorities

� economic capital (including hybrids and surplus funds)

� before minorities and (in consequence)with haircut on Talanx‘s minority holdings

� operational risk modeled with standard formula

� inclusion of hybridsand surplus funds

BayernLB Fixed Income Conference, Munich, 18 May 2015

13

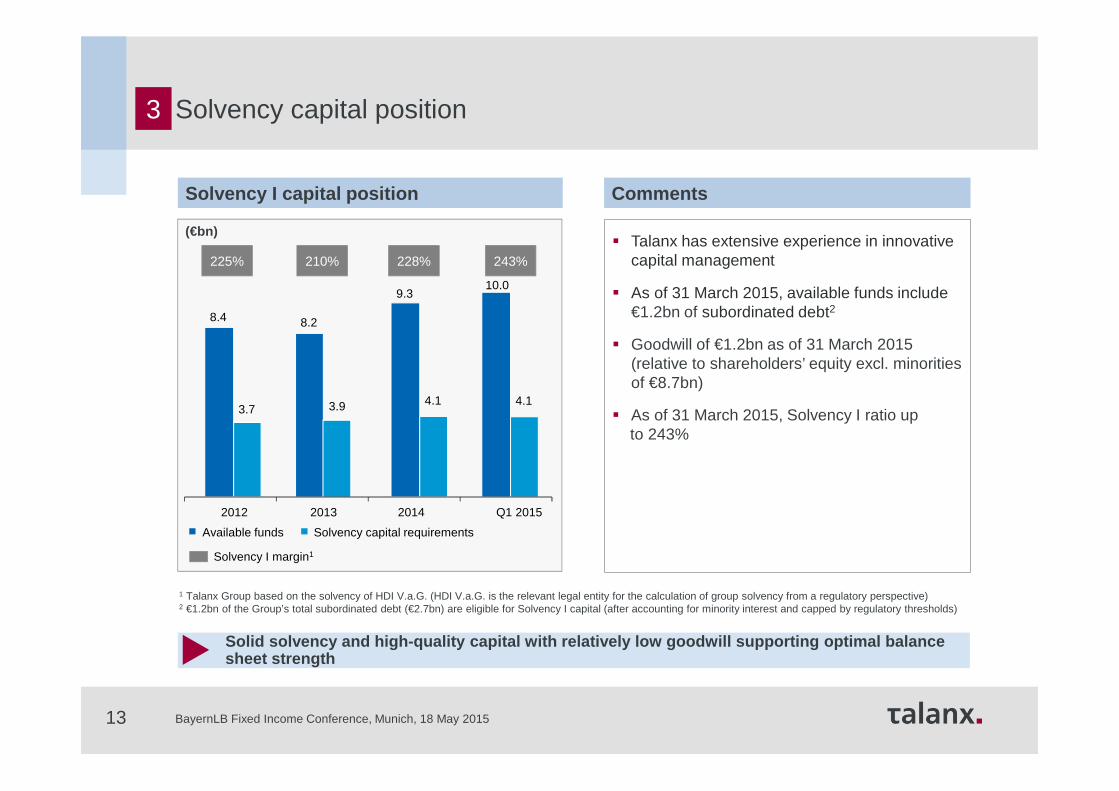

� Talanx has extensive experience in innovative capital management

� As of 31 March 2015, available funds include €1.2bn of subordinated debt2

� Goodwill of €1.2bn as of 31 March 2015(relative to shareholders’ equity excl. minorities of €8.7bn)

� As of 31 March 2015, Solvency I ratio up to 243%

(€bn)

Solid solvency and high-quality capital with relati vely low goodwill supporting optimal balance sheet strength

1 Talanx Group based on the solvency of HDI V.a.G. (HDI V.a.G. is the relevant legal entity for the calculation of group solvency from a regulatory perspective)2 €1.2bn of the Group’s total subordinated debt (€2.7bn) are eligible for Solvency I capital (after accounting for minority interest and capped by regulatory thresholds)

CommentsSolvency I capital position

Solvency I margin1

225% 210% 228% 243%

8.2

10.0

3.9 4.1

2012 2013 2014 Q1 2015

Available funds Solvency capital requirements

8.4

3.7

Solvency capital position3

9.3

4.1

BayernLB Fixed Income Conference, Munich, 18 May 2015

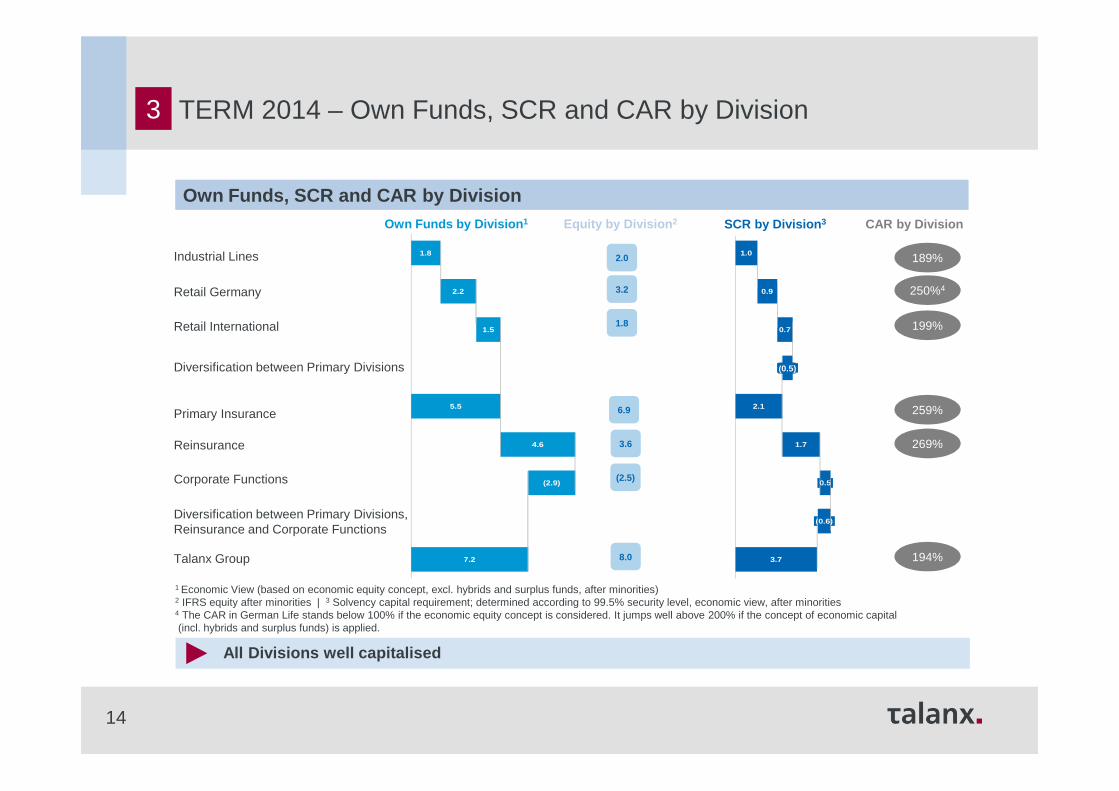

1.0

0.9

0.7

(0.6)

2.1

1.7

0.5

(0.6)

3.7

189%

250%4

199%

259%

269%

2.0

3.2

1.8

6.9

3.6

(2.5)

8.0 194%

Industrial Lines

Retail Germany

Retail International

Diversification between Primary Divisions

Primary Insurance

Reinsurance

Corporate Functions

Diversification between Primary Divisions, Reinsurance and Corporate Functions

Talanx Group

14

All Divisions well capitalised

Equity by Division 2 CAR by Division

1 Economic View (based on economic equity concept, excl. hybrids and surplus funds, after minorities)2 IFRS equity after minorities | 3 Solvency capital requirement; determined according to 99.5% security level, economic view, after minorities4 The CAR in German Life stands below 100% if the economic equity concept is considered. It jumps well above 200% if the concept of economic capital(incl. hybrids and surplus funds) is applied.

Own Funds, SCR and CAR by DivisionOwn Funds by Division 1 SCR by Division 3

1.8

2.2

1.5

5.5

4.6

(2.9)

7.2

(0.5)

3 TERM 2014 – Own Funds, SCR and CAR by Division

Results Presentation FY2014, 23 March 2015151515

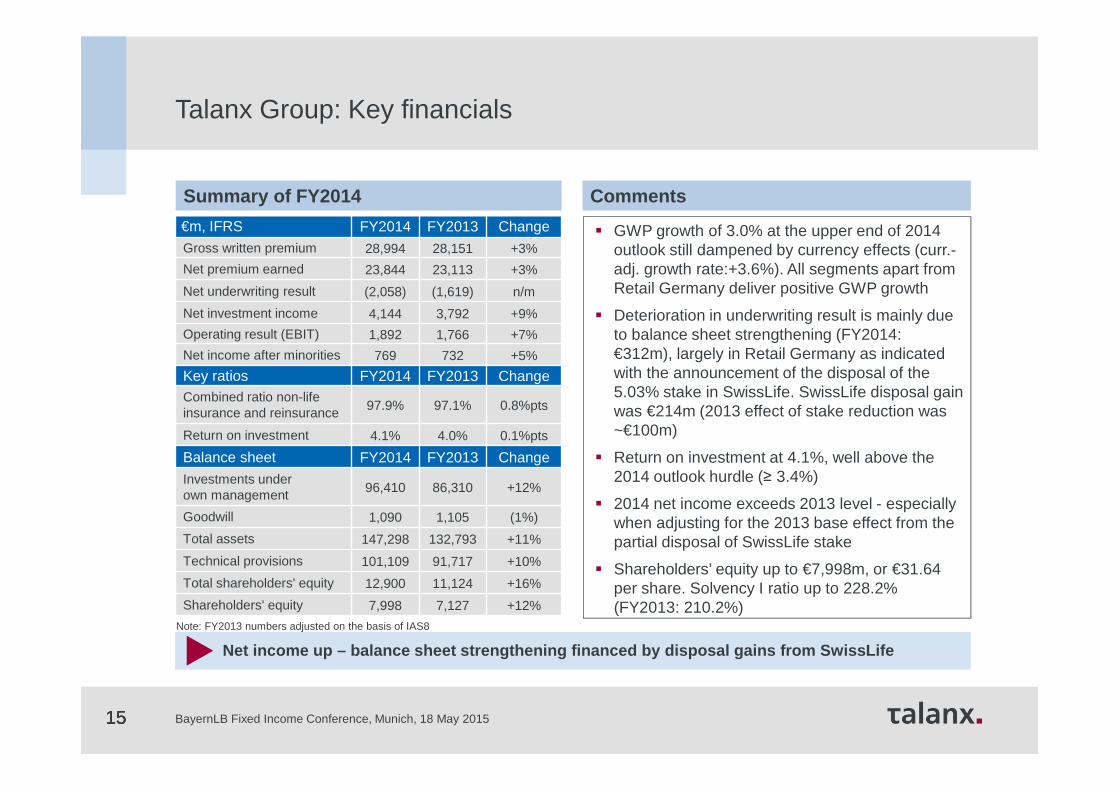

Summary of FY2014

Net income up – balance sheet strengthening financed by disposal gains from SwissLife

€m, IFRS FY2014 FY2013 ChangeGross written premium 28,994 28,151 +3%

Net premium earned 23,844 23,113 +3%

Net underwriting result (2,058) (1,619) n/m

Net investment income 4,144 3,792 +9%

Operating result (EBIT) 1,892 1,766 +7%

Net income after minorities 769 732 +5%

Key ratios FY2014 FY2013 ChangeCombined ratio non-life insurance and reinsurance 97.9% 97.1% 0.8%pts

Return on investment 4.1% 4.0% 0.1%pts

Balance sheet FY2014 FY2013 Change

Investments under own management 96,410 86,310 +12%

Goodwill 1,090 1,105 (1%)

Total assets 147,298 132,793 +11%

Technical provisions 101,109 91,717 +10%

Total shareholders' equity 12,900 11,124 +16%

Shareholders' equity 7,998 7,127 +12%

Comments

Note: FY2013 numbers adjusted on the basis of IAS8

� GWP growth of 3.0% at the upper end of 2014 outlook still dampened by currency effects (curr.-adj. growth rate:+3.6%). All segments apart from Retail Germany deliver positive GWP growth

� Deterioration in underwriting result is mainly due to balance sheet strengthening (FY2014: €312m), largely in Retail Germany as indicated with the announcement of the disposal of the 5.03% stake in SwissLife. SwissLife disposal gain was €214m (2013 effect of stake reduction was ~€100m)

� Return on investment at 4.1%, well above the 2014 outlook hurdle (≥ 3.4%)

� 2014 net income exceeds 2013 level - especially when adjusting for the 2013 base effect from the partial disposal of SwissLife stake

� Shareholders’ equity up to €7,998m, or €31.64 per share. Solvency I ratio up to 228.2% (FY2013: 210.2%)

Talanx Group: Key financials

BayernLB Fixed Income Conference, Munich, 18 May 2015

Results Presentation FY2014, 23 March 20151616

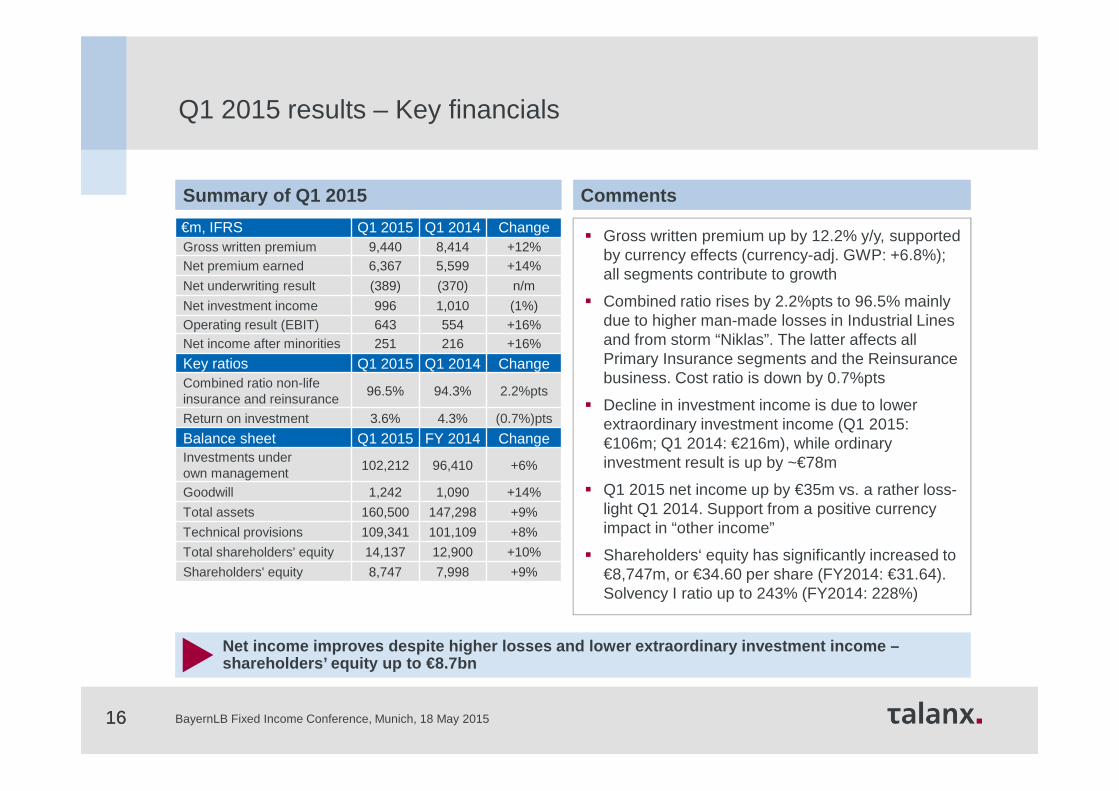

Summary of Q1 2015

Net income improves despite higher losses and lower extraordinary investment income –shareholders’ equity up to €8.7bn

€m, IFRS Q1 2015 Q1 2014 ChangeGross written premium 9,440 8,414 +12%Net premium earned 6,367 5,599 +14%

Net underwriting result (389) (370) n/m

Net investment income 996 1,010 (1%)Operating result (EBIT) 643 554 +16%Net income after minorities 251 216 +16%

Key ratios Q1 2015 Q1 2014 ChangeCombined ratio non-life insurance and reinsurance

96.5% 94.3% 2.2%pts

Return on investment 3.6% 4.3% (0.7%)pts

Balance sheet Q1 2015 FY 2014 ChangeInvestments under own management

102,212 96,410 +6%

Goodwill 1,242 1,090 +14%

Total assets 160,500 147,298 +9%

Technical provisions 109,341 101,109 +8%

Total shareholders' equity 14,137 12,900 +10%

Shareholders' equity 8,747 7,998 +9%

Comments

� Gross written premium up by 12.2% y/y, supported by currency effects (currency-adj. GWP: +6.8%); all segments contribute to growth

� Combined ratio rises by 2.2%pts to 96.5% mainly due to higher man-made losses in Industrial Lines and from storm “Niklas”. The latter affects all Primary Insurance segments and the Reinsurance business. Cost ratio is down by 0.7%pts

� Decline in investment income is due to lower extraordinary investment income (Q1 2015: €106m; Q1 2014: €216m), while ordinary investment result is up by ~€78m

� Q1 2015 net income up by €35m vs. a rather loss-light Q1 2014. Support from a positive currency impact in “other income”

� Shareholders‘ equity has significantly increased to €8,747m, or €34.60 per share (FY2014: €31.64). Solvency I ratio up to 243% (FY2014: 228%)

Q1 2015 results – Key financials

BayernLB Fixed Income Conference, Munich, 18 May 2015

17

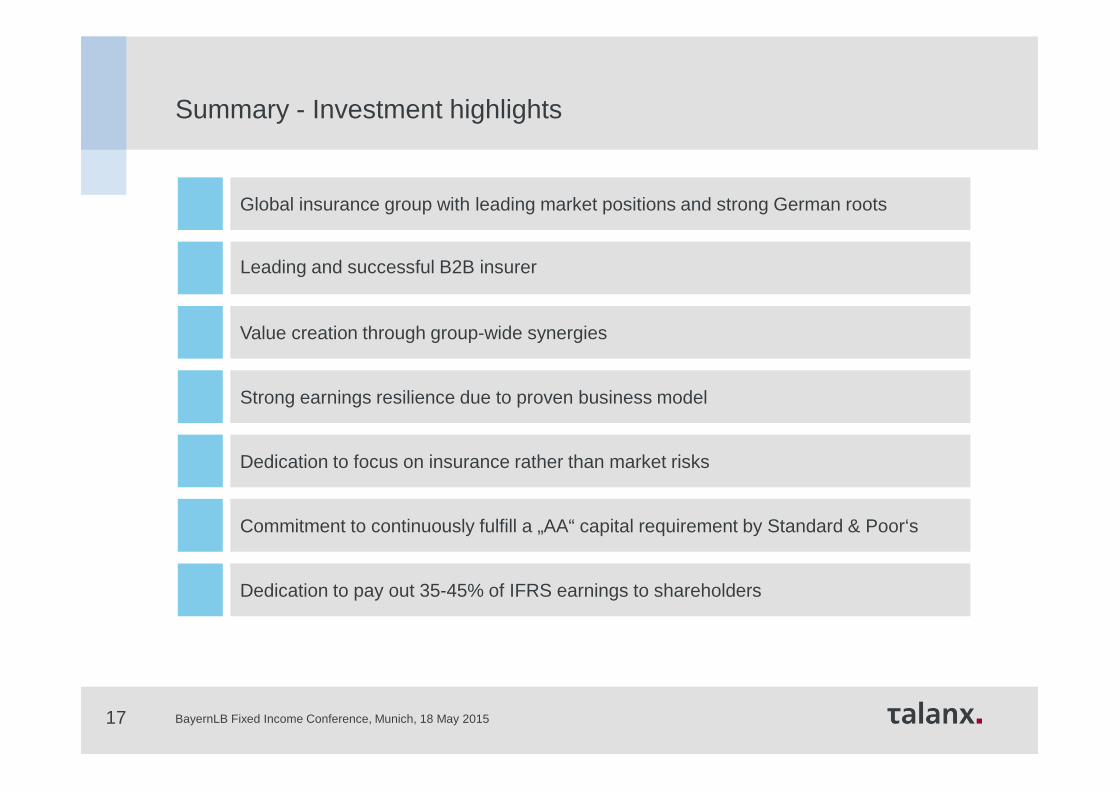

Summary - Investment highlights

Global insurance group with leading market positions and strong German roots

Dedication to focus on insurance rather than market risks

Value creation through group-wide synergies

Strong earnings resilience due to proven business model

Leading and successful B2B insurer

Commitment to continuously fulfill a „AA“ capital requirement by Standard & Poor‘s

Dedication to pay out 35-45% of IFRS earnings to shareholders

BayernLB Fixed Income Conference, Munich, 18 May 2015

1818

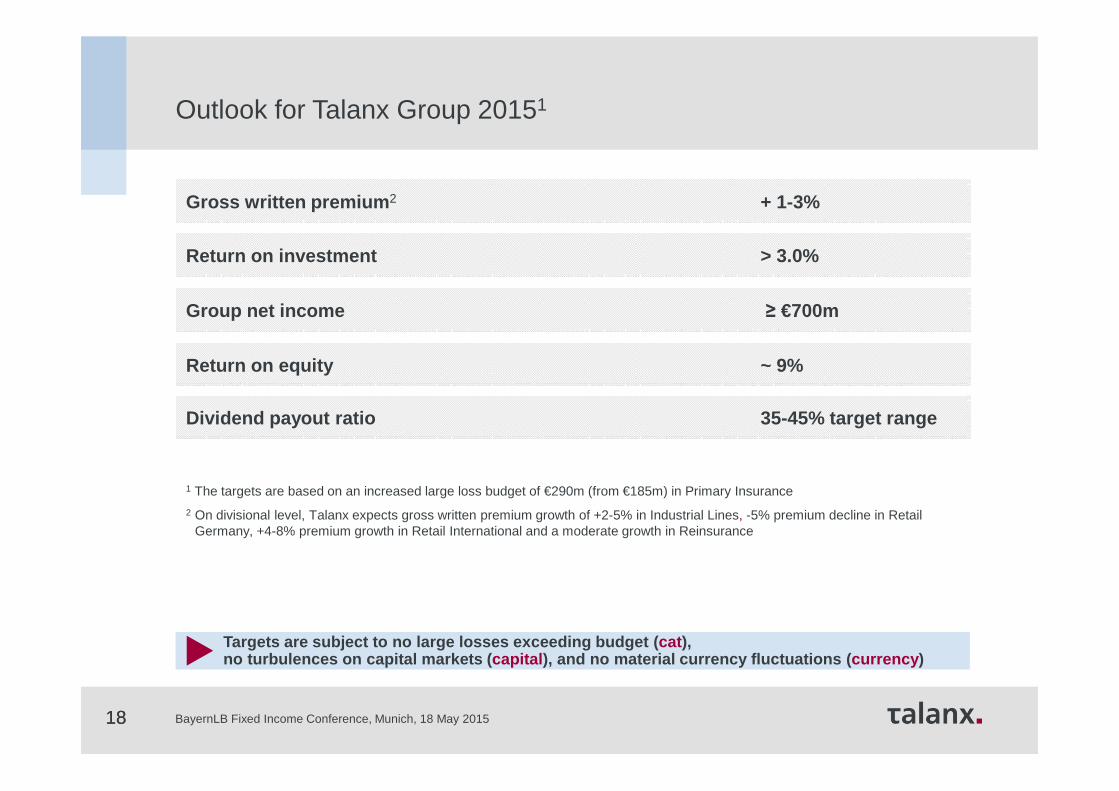

Targets are subject to no large losses exceeding bu dget ( cat ), no turbulences on capital markets ( capital ), and no material currency fluctuations ( currency )

Gross written premium 2 + 1-3%

Return on investment > 3.0%

Group net income ≥ €700m

Return on equity ~ 9%

Dividend payout ratio 35-45% target range

1 The targets are based on an increased large loss budget of €290m (from €185m) in Primary Insurance

2 On divisional level, Talanx expects gross written premium growth of +2-5% in Industrial Lines, -5% premium decline in Retail Germany, +4-8% premium growth in Retail International and a moderate growth in Reinsurance

Outlook for Talanx Group 20151

BayernLB Fixed Income Conference, Munich, 18 May 2015

19

- Debt Financing Overview -

BayernLB Fixed Income Conference, Munich, 18 May 2015

CommentsOrganisational overview

� One central function for capital and liquidity management

� Secure a comfortable level of liquidity at Talanx AG

� Active capital and liquidity management

� Know-how centre for capital market instruments

� Central steering of all capital markets processes in the group

� Financing of group companies at-arms-lengths

� Cost reduction in consequence of concentration of all bank relations in one function

� FX / Interest rate hedging

� Investment of Liquidity buffers

Capital markets

Treasury

capital/liquidity

dividend/interests

Banks/Investors

Subordinated Bonds

Senior Bonds

Equities

Convertibles

Credit lines

Realisation of efficiency and scale effects through central state-of-the-art treasury function.

Capital / liquidity management (excluding Hannover Re)

BayernLB Fixed Income Conference, Munich, 18 May 201520

Subordinated bond 8.367%, 30-NC-10

2012

2013

Liability management exercise

Strengthening of capitalisation of Talanx

Group

Reduction of external debt

IPO

Senior bond 3.125%, 10 years

Financing of organic and inorganic growth and partially

repay amounts outstanding under two credit facilities

Refinancing of internal debt

500

(204)

517

750

300

Latest capital market transactions (excluding Hanno ver Re)

1 conversion of the Tier 1 Meiji Yasuda bond.

April

July

Oct

€m

Capital market appearances established by liquid in struments in major market segments

April

July

Oct

Feb

April

July

Oct

Feb

Senior bond 2.50%, 12 years

2014 500Refinancing

of internal debtJuly

1

Historic market transactions

BayernLB Fixed Income Conference, Munich, 18 May 201521

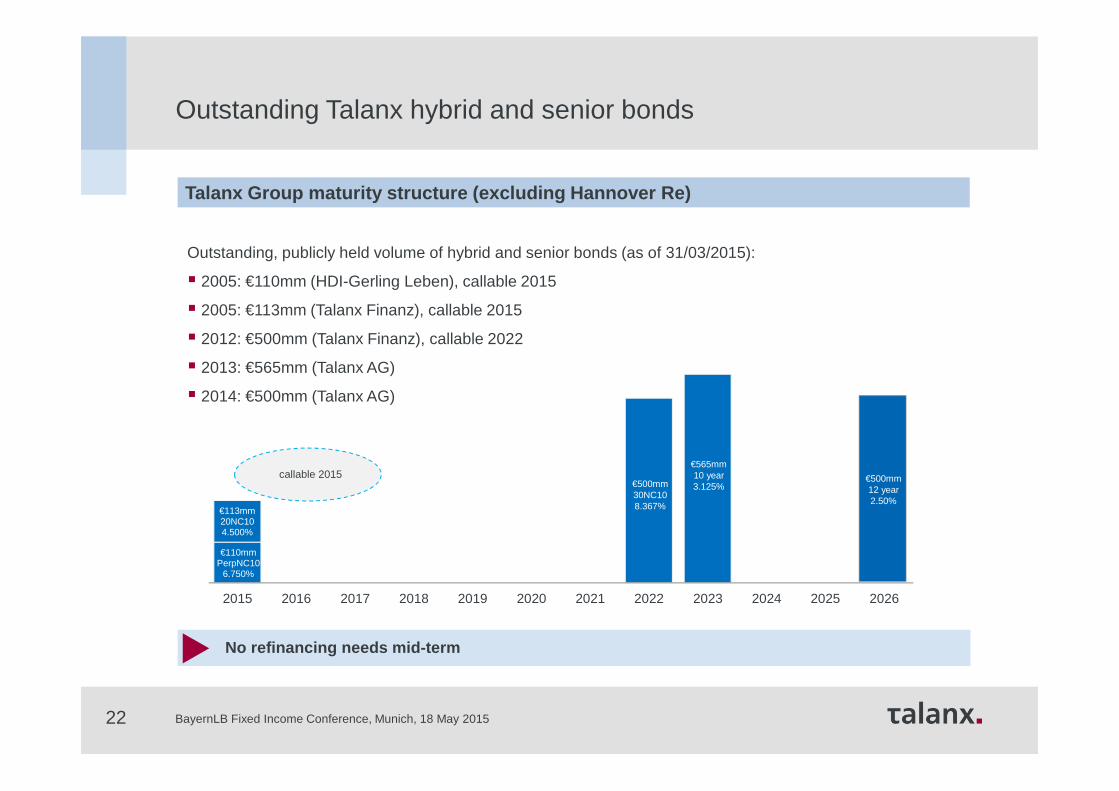

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

No refinancing needs mid-term

Talanx Group maturity structure (excluding Hannover Re)

Outstanding, publicly held volume of hybrid and senior bonds (as of 31/03/2015):

� 2005: €110mm (HDI-Gerling Leben), callable 2015

� 2005: €113mm (Talanx Finanz), callable 2015

� 2012: €500mm (Talanx Finanz), callable 2022

� 2013: €565mm (Talanx AG)

� 2014: €500mm (Talanx AG)

€500mm 30-nc-108.367%

€113mm 20NC104.500%

€110mm PerpNC10

6.750%

€500mm 30NC108.367%

callable 2015€565mm 10 year3.125%

€500mm 12 year 2.50%

Talanx Group maturity structure (excluding Hannover Re)

Outstanding Talanx hybrid and senior bonds

BayernLB Fixed Income Conference, Munich, 18 May 201522

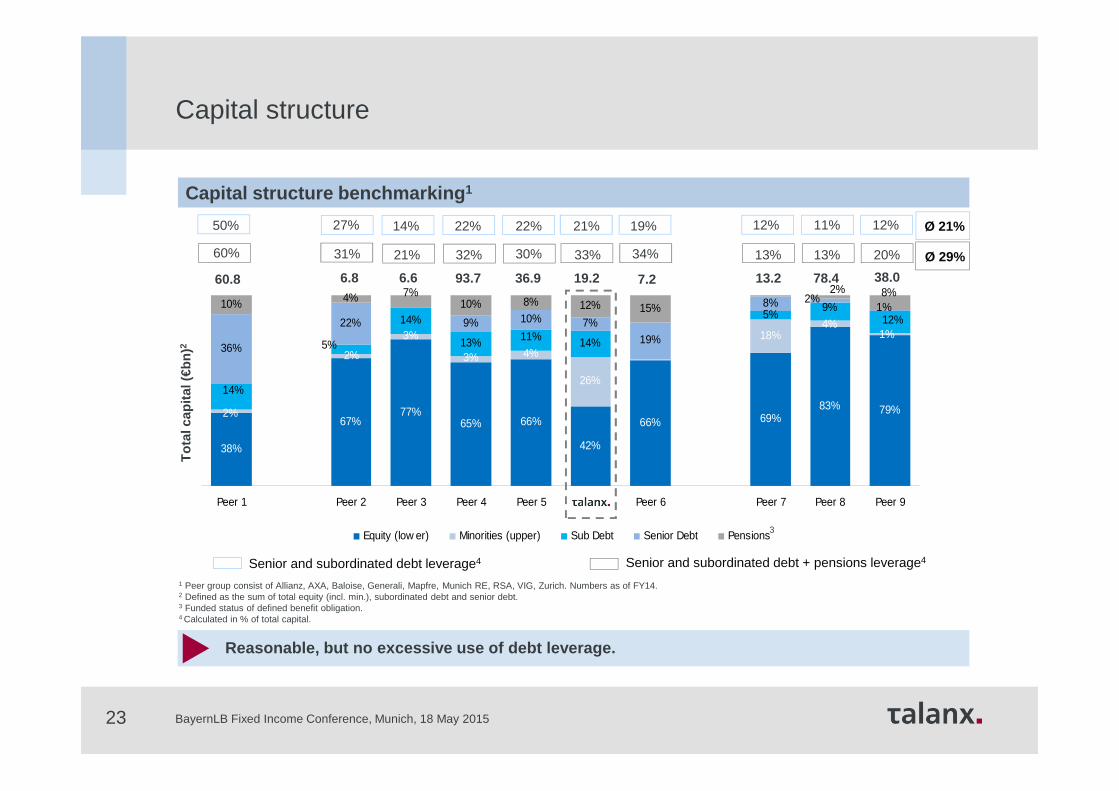

Capital structure benchmarking 1

Reasonable, but no excessive use of debt leverage.

1 Peer group consist of Allianz, AXA, Baloise, Generali, Mapfre, Munich RE, RSA, VIG, Zurich. Numbers as of FY14. 2 Defined as the sum of total equity (incl. min.), subordinated debt and senior debt.3 Funded status of defined benefit obligation.4 Calculated in % of total capital.

Senior and subordinated debt + pensions leverage4

Tot

al c

apita

l (€b

n)2

Senior and subordinated debt leverage4

50%

60%

27%

31%

14%

21%

22%

32%

22%

30%

21%

33%

19%

34%

12%

13%

11%

13%

12%

20%

Ø 21%

Ø 29%

60.8 6.8 6.6 93.7 36.9 19.2 7.2 13.2 78.4 38.0

38%

67%77%

65% 66%

42%

66% 69%83% 79%

3%

26%

18%14%

13% 14%

5%

36%

22% 9% 10% 7%

19%

8%10% 4% 10% 8% 12% 15%

1%4%

4%3%2%

2%

14%

11%5%

9%12%

1%2% 8%7% 2%

Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Talanx Peer 6 Peer 7 Peer 8 Peer 9

Equity (low er) Minorities (upper) Sub Debt Senior Debt Pensions3

Capital structure

BayernLB Fixed Income Conference, Munich, 18 May 201523

24

- Segments -

BayernLB Fixed Income Conference, Munich, 18 May 2015

25

Key figures Comments

� GWP grew by +5.1% y/y in FY2014 (currency-adjusted:+5.9%)

� Sustainable growth resulting from international activities, incl. North America and Asia Pacific

� Increased retention rate of 50.9% in FY2014 (FY2013: 44.5%) despite reinstatement premiums of €127m

� Profitability impacted by reinstatement premium (€127m in FY2014) and large losses, e.g. storm Ela in Q2 and various man-made losses

1 Based on total GWP adjusted for 50.2% share in Hannover Re2 Net, including income from interest on deposits

2014 GWP:geographic split

Share in 2014 group GWP 1

Key financials (€m) FY2011 FY2012 FY2013 FY2014 Change

Gross written premium 3,138 3,572 3,835 4,031 +5%

Net premium earned 1,375 1,608 1,744 2,022 +16%

Net underwriting result 155 79 (42) (61) n/m

Net investment income 204 247 240 268 +12%

Operating result (EBIT) 321 259 129 182 +41%

Combined ratio2 in % 88.6 95.1 102.4 103.0 +0.6%pts

Return on Equity in % 12.4 8.8 4.2 6.3 +2.1%pts

18%

2014 GWP: split by line

Industrial Lines: Overview

Talanx is a leading European industrial lines insur er with global ambitions

20%

37%

43%

GermanyEurope (excl. Germany)RoW

1%4%10%

13%

30%

42%

Property + EngineeringLiabilityMotor

MarineAccidentAviation

€4.0 bn €4.0 bn

BayernLB Fixed Income Conference, Munich, 18 May 2015

26

Relationships with large listed German companies 1 (DAX-30)

1 Lead insurer in liability or property line; Lead insurer at least in one line

Selected client acquisitions since 2013

Industrial Lines: Client relationships

Preferred lead insurer for large corporates

BayernLB Fixed Income Conference, Munich, 18 May 2015

27

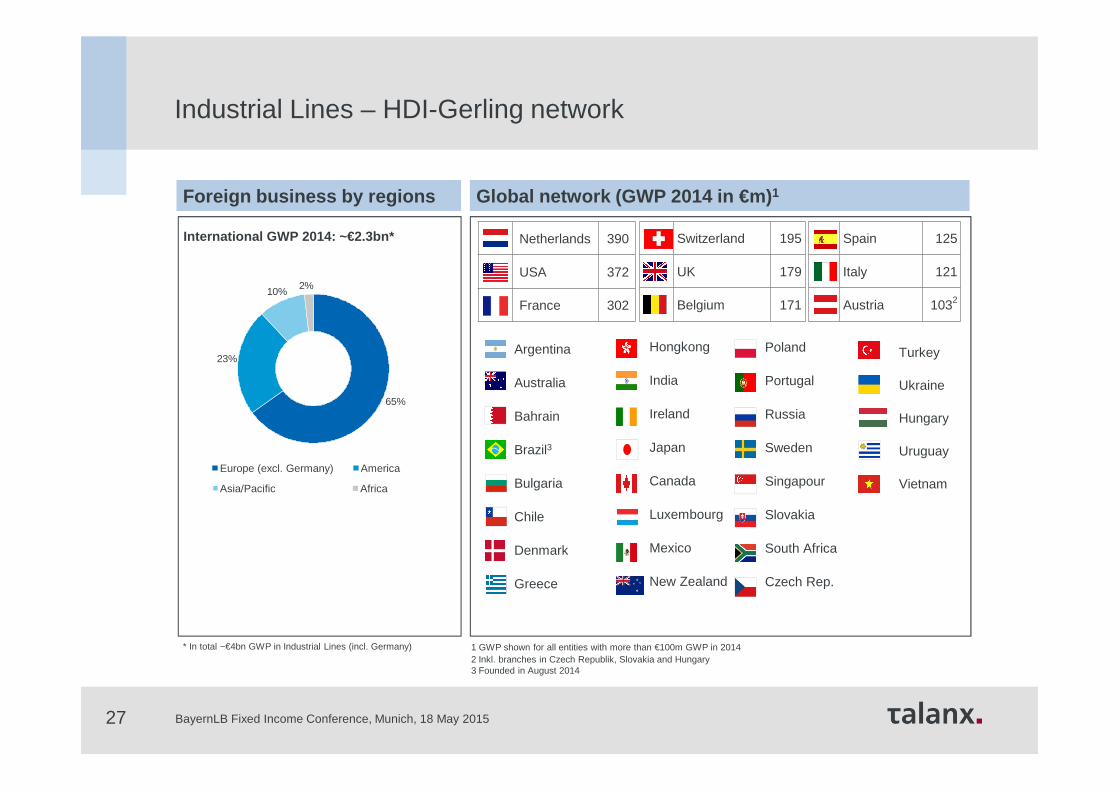

Industrial Lines – HDI-Gerling network

Global network (GWP 2014 in €m) 1Foreign business by regions

1 GWP shown for all entities with more than €100m GWP in 2014

International GWP 2014: ~€2.3bn*

* In total ~€4bn GWP in Industrial Lines (incl. Germany)

Europe (excl. Germany) America

Asia/Pacific Africa

65%

23%

10%2%

Netherlands 390

USA 372

France 302

2 Inkl. branches in Czech Republik, Slovakia and Hungary3 Founded in August 2014

Switzerland 195

UK 179

Belgium 171

Spain 125

Italy 121

Austria 1032

Argentina

Australia

Bahrain

Brazil3

Bulgaria

Chile

Denmark

Greece

Hongkong

India

Ireland

Japan

Canada

Luxembourg

Mexico

New Zealand

Poland

Portugal

Russia

Sweden

Singapour

Slovakia

South Africa

Czech Rep.

Turkey

Ukraine

Hungary

Uruguay

Vietnam

BayernLB Fixed Income Conference, Munich, 18 May 2015

28

Life GWP 2014: split by business

Share in 2014 group GWP 1

Key figures Comments

� In line with targets, slight reduction in GWP, primarily reflecting a decline in traditional Life business(FY2014: -1.4%)

� FY2014 included balance sheet strengthening of ~€290m. Adjusting for this effect, FY2014 combined ratio stood at 100.8% (Q4 2014: 103.6%)

� Adjusted FY2014 EBIT stood at €175m

� Decline in underwriting result due to balance sheet strengthening and higher capital gains (~€110m) to finance ZZR. Higher ordinary investment income contributed to bottom line

� 2014 ZZR allocation – according to HGB - of €358m (Q4 2014: €92m). In FY2014 total ZZR stock rose to ~€1.1bn

Key financials (€m) FY2011 FY2012 FY2013 FY2014 Change

Gross written premium 6,710 6,829 6,954 6,890 (1%)

Net premium earned 5,461 5,501 5,605 5,630 +0%

Net underwriting result (1,258) (1,425) (1,515) (1,953) n/m

Net investment income 1,530 1,621 1,786 1,899 +6%

Operating result (EBIT) 110 100 161 (115) n/m

Combined ratio2 in % 101.6 100.6 102.4 108.6 +6.2%pts

Return on Equity in % 2.7 4.8 3.0 (2.9) n/m1 Based on total GWP adjusted for 50.2% share in Hannover Re2 Including interest income on funds withheld and contract deposits; net, property/casualty only

32%

P&C GWP 2013: split by line

Retail Germany: Overview

Profitability numbers in Retail Germany affected by balance sheet strengthening measures

20%

18%

48%6%

8%

PropertyAccident

OtherCasualtyMotor

€1.5bn€5.4 bn

Unit-linked OtherRisk ProductsTraditional

53%2%

32%

13%

BayernLB Fixed Income Conference, Munich, 18 May 2015

29

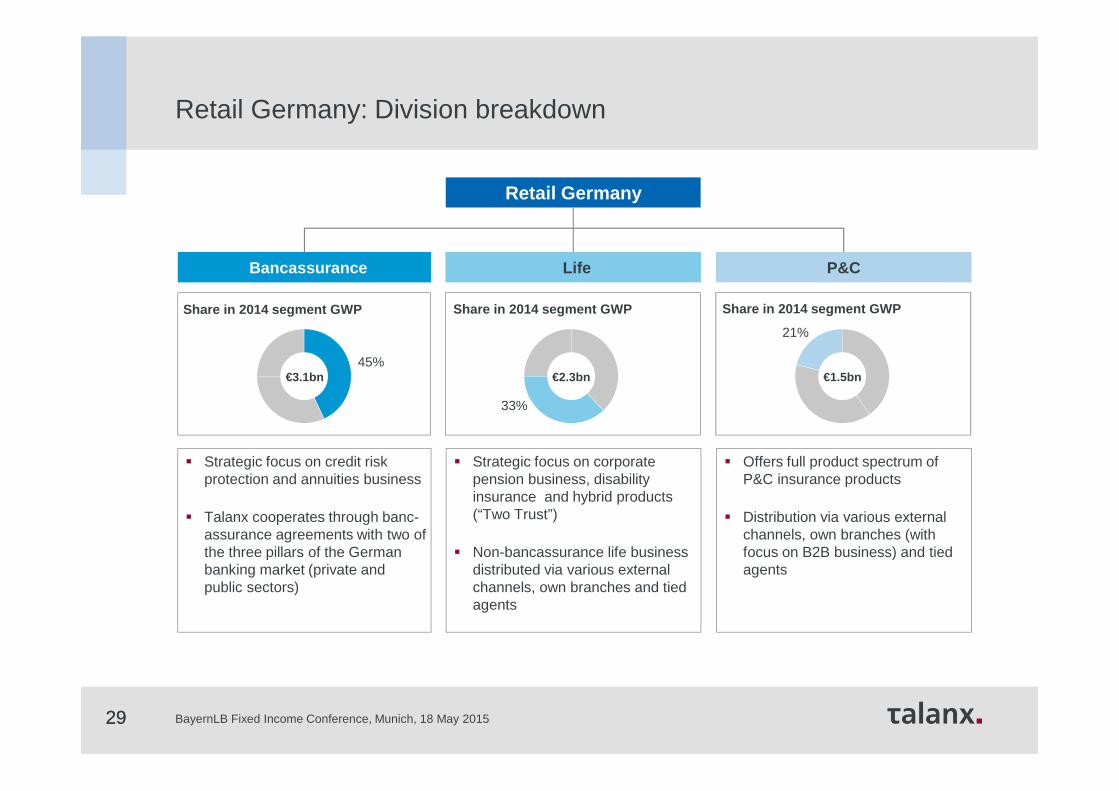

Retail Germany

� Offers full product spectrum of P&C insurance products

� Distribution via various external channels, own branches (with focus on B2B business) and tied agents

� Strategic focus on corporate pension business, disability insurance and hybrid products (“Two Trust”)

� Non-bancassurance life business distributed via various external channels, own branches and tied agents

� Strategic focus on credit risk protection and annuities business

� Talanx cooperates through banc-assurance agreements with two of the three pillars of the German banking market (private and public sectors)

Bancassurance P&CLife

€2.3bn€3.1bn €1.5bn45%

33%

21%

29

Retail Germany: Division breakdown

Share in 2014 segment GWP Share in 2014 segment GWP Share in 2014 segment GWP

BayernLB Fixed Income Conference, Munich, 18 May 2015

30

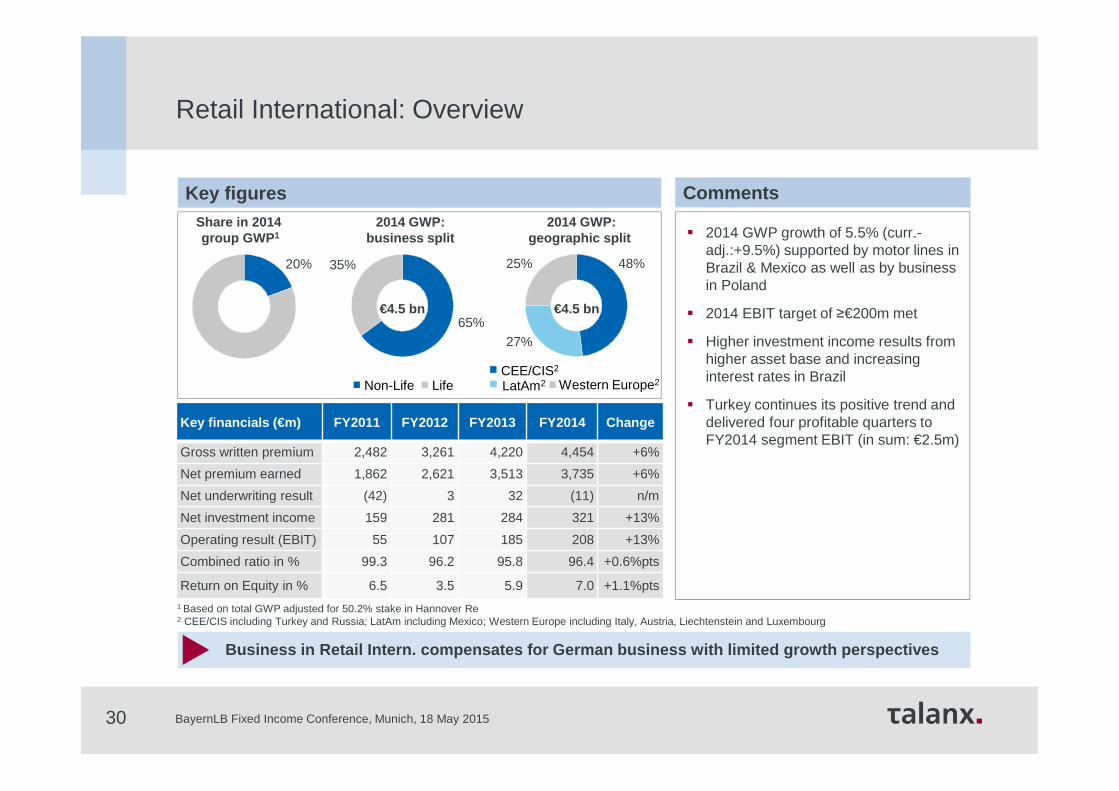

Retail International: Overview

Key figures

Key financials (€m) FY2011 FY2012 FY2013 FY2014 Change

Gross written premium 2,482 3,261 4,220 4,454 +6%

Net premium earned 1,862 2,621 3,513 3,735 +6%

Net underwriting result (42) 3 32 (11) n/m

Net investment income 159 281 284 321 +13%

Operating result (EBIT) 55 107 185 208 +13%

Combined ratio in % 99.3 96.2 95.8 96.4 +0.6%pts

Return on Equity in % 6.5 3.5 5.9 7.0 +1.1%pts

2014 GWP:geographic split

LatAm2 Western Europe2CEE/CIS2

� 2014 GWP growth of 5.5% (curr.-adj.:+9.5%) supported by motor lines in Brazil & Mexico as well as by business in Poland

� 2014 EBIT target of ≥€200m met

� Higher investment income results from higher asset base and increasing interest rates in Brazil

� Turkey continues its positive trend and delivered four profitable quarters to FY2014 segment EBIT (in sum: €2.5m)

1 Based on total GWP adjusted for 50.2% stake in Hannover Re2 CEE/CIS including Turkey and Russia; LatAm including Mexico; Western Europe including Italy, Austria, Liechtenstein and Luxembourg

Share in 2014 group GWP 1

20%

2014 GWP: business split

65%

35%

Non-Life Life

48%

27%

25%

Comments

Business in Retail Intern. compensates for German b usiness with limited growth perspectives

€4.5 bn €4.5 bn

BayernLB Fixed Income Conference, Munich, 18 May 2015

31

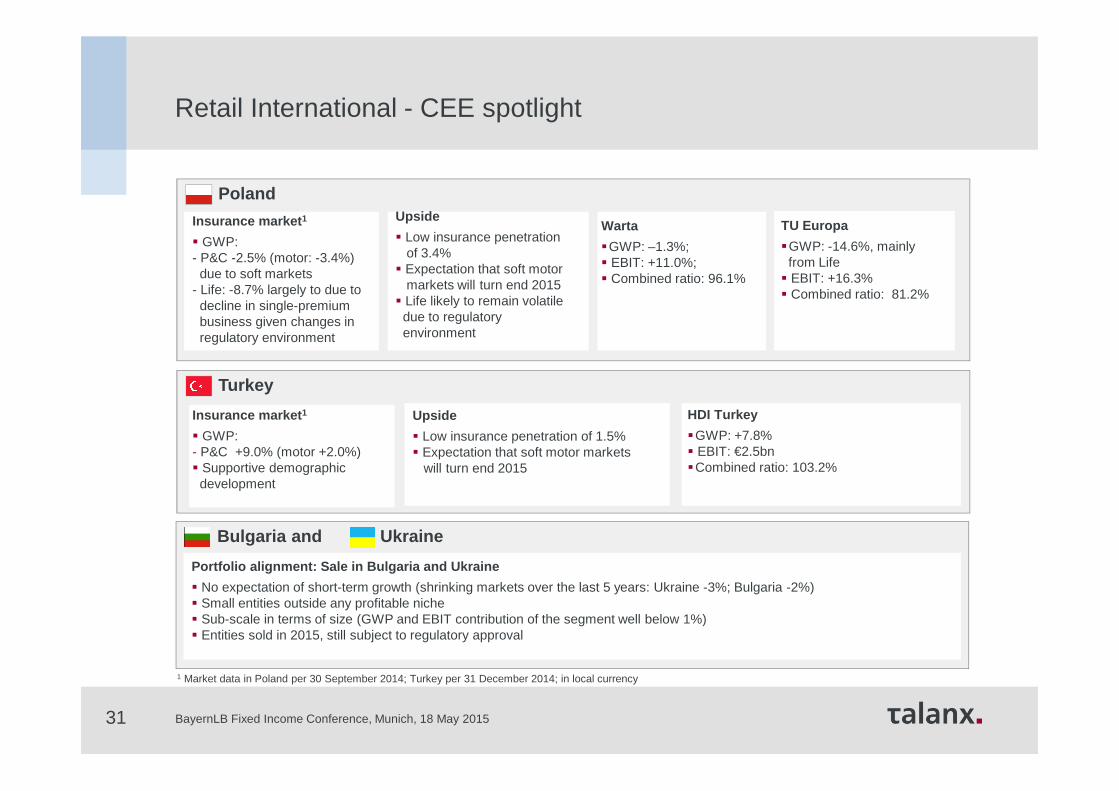

Retail International - CEE spotlight

Poland

Insurance market 1

� GWP:- P&C -2.5% (motor: -3.4%)due to soft markets

- Life: -8.7% largely to due todecline in single-premiumbusiness given changes inregulatory environment

Upside

� Low insurance penetrationof 3.4%

� Expectation that soft motormarkets will turn end 2015

� Life likely to remain volatiledue to regulatoryenvironment

TU Europa

�GWP: -14.6%, mainly from Life

� EBIT: +16.3%� Combined ratio: 81.2%

Warta

�GWP: –1.3%; � EBIT: +11.0%; � Combined ratio: 96.1%

Turkey

Insurance market 1

� GWP:- P&C +9.0% (motor +2.0%)� Supportive demographicdevelopment

Upside

� Low insurance penetration of 1.5%� Expectation that soft motor markets

will turn end 2015

HDI Turkey

�GWP: +7.8% � EBIT: €2.5bn�Combined ratio: 103.2%

Bulgaria and Ukraine

Portfolio alignment: Sale in Bulgaria and Ukraine

� No expectation of short-term growth (shrinking markets over the last 5 years: Ukraine -3%; Bulgaria -2%) � Small entities outside any profitable niche� Sub-scale in terms of size (GWP and EBIT contribution of the segment well below 1%)� Entities sold in 2015, still subject to regulatory approval

1 Market data in Poland per 30 September 2014; Turkey per 31 December 2014; in local currency

BayernLB Fixed Income Conference, Munich, 18 May 2015

32

Retail International – Latin America spotlight

Chile

Take-over of Inversiones Magallanes� Signing of contract with majority owner in December 2014� Fully consolidated from 13 February 2015 � Talanx achieves a market-leading position in Chile:

- No. 5 in P&C insurance- No. 2 in motor insurance

Brazil

Insurance market 1

� P&C: GWP growthof 11.1% (motor: 10.1%)

Upside

� Low insurancepenetration:- ~60% of vehiclesnot insured

- ~90% of privatehouseholds not insured

HDI Brazil

� GWP: +4.1%; currency-adj. +13.1%

� EBIT up by 12.6%; currrency-adj.+22.3%

� Combined ratio of 98.8%

� Fifth-largest motor insurer in Brazil� „Hermes“ award for the best motor insurer in the country

Mexico

Insurance market 1

� P&C: decline in GWP by -1.2% (motor 2.2%)

Upside

� Low insurance penetration: - More than 70% of vehicles not insured

- ~90% of privatehouseholds not insured

HDI Mexico

� GWP +7.8%; currency-adj. +11.4%

� EBIT up by 12.2%; currency-adj. +15.9%

� Combined ratio of 92.4%

� Ninth-largest motor insurer in Mexico

1 Market data per 30 September 2014 in local currency

BayernLB Fixed Income Conference, Munich, 18 May 2015

33

Key figures Comments

Key financials (€m)Non-Life Life / Health

FY2011 FY2012 FY2013 FY2014 Change FY2011 FY2012 FY2013 FY2 014 Change

Gross written premium 6,826 7,717 7,818 7,903 +1% 5,270 6,058 6,145 6,459 +5%

Net premium earned 5,961 6,854 6,866 7,011 +2% 4,789 5,426 5,359 5,411 +1%

Net investment income 880 982 811 867 +7% 512 684 611 613 +0%

Operating result (EBIT) 637 1,133 1,097 1,219 +11% 213 270 139 268 +93%

Comb.Ratio2 in % 104.2 95.8 94.9 94.7 (0.2%pts) - - - - -

GWP development (total, €bn)Share in 2014 group GWP 1

1 Based on total GWP adjusted for 50.2% share in Hannover Re2 Incl. expenses on funds withheld and contract deposits; net3 EBIT margins reflect a Talanx Group view

31%

Reinsurance

FY2011 FY2012 FY2013 FY2014 Change

Return on Equity in % 14.1 16.5 15.9 15.8 (0.1%pts)

Non Life: � Growth effects mainly from structured Reinsurance in Asia

and facultative business� Major losses of €426m (6.1% of NPE) below budget of

€670m; conservative loss reserving policy maintained� FY2014 EBIT margin3 of 17.4% (FY2013:16%) is well above

target

Life/Health:� Growth effects mainly from Australia and Longevity BATs� Improved technical result due to normalised result from

Australian disability business

Reinsurance: Overview

Hannover Re is one of the largest and most profitab le reinsurers globally

2012 2013 2014

13.8

14.0

14.3

BayernLB Fixed Income Conference, Munich, 18 May 2015

34

Hannover Re keeps its leading position in RoE ranking

Source: Hannover Re company presentation as of 10 March 2015; reflects Hannover Re’s reported numbers on a stand-alone basis

BayernLB Fixed Income Conference, Munich, 18 May 2015

35

- Appendix -

BayernLB Fixed Income Conference, Munich, 18 May 2015

3636

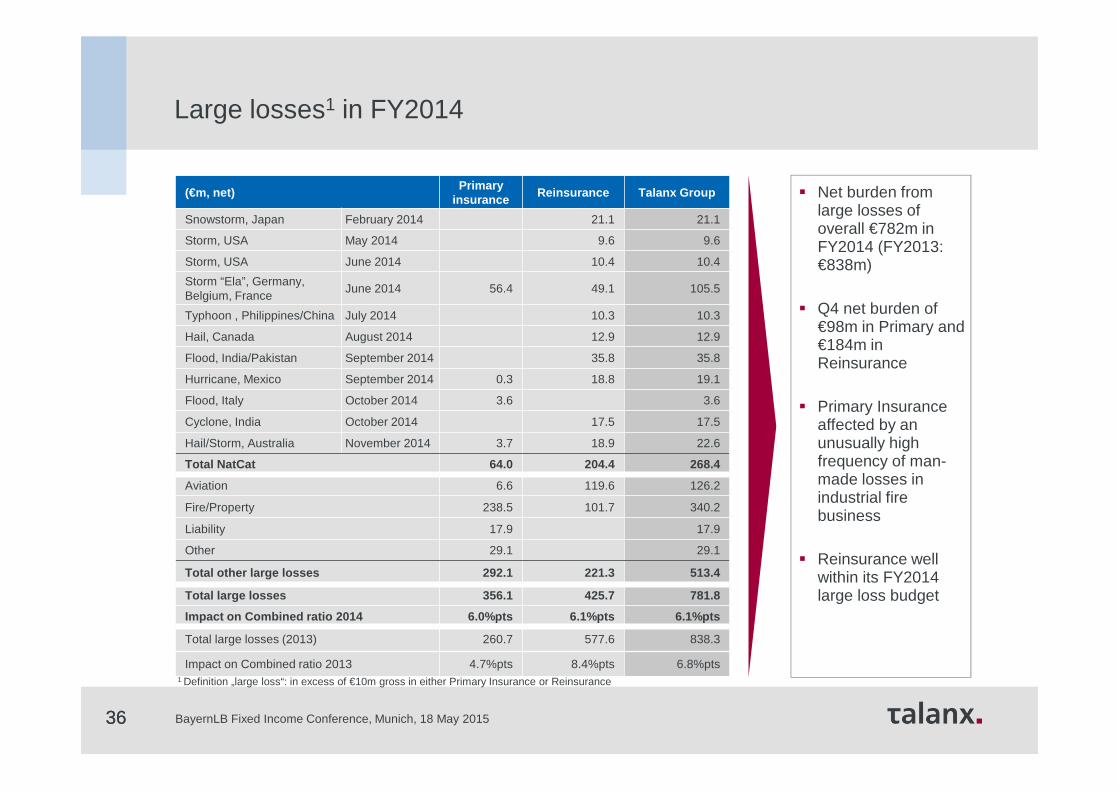

� Net burden from large losses of overall €782m in FY2014 (FY2013: €838m)

� Q4 net burden of €98m in Primary and €184m in Reinsurance

� Primary Insurance affected by an unusually high frequency of man-made losses in industrial fire business

� Reinsurance well within its FY2014 large loss budget

1 Definition „large loss“: in excess of €10m gross in either Primary Insurance or Reinsurance

Large losses1 in FY2014

(€m, net)Primary

insuranceReinsurance Talanx Group

Snowstorm, Japan February 2014 21.1 21.1

Storm, USA May 2014 9.6 9.6

Storm, USA June 2014 10.4 10.4

Storm “Ela”, Germany, Belgium, France

June 2014 56.4 49.1 105.5

Typhoon , Philippines/China July 2014 10.3 10.3

Hail, Canada August 2014 12.9 12.9

Flood, India/Pakistan September 2014 35.8 35.8

Hurricane, Mexico September 2014 0.3 18.8 19.1

Flood, Italy October 2014 3.6 3.6

Cyclone, India October 2014 17.5 17.5

Hail/Storm, Australia November 2014 3.7 18.9 22.6

Total NatCat 64.0 204.4 268.4

Aviation 6.6 119.6 126.2

Fire/Property 238.5 101.7 340.2

Liability 17.9 17.9

Other 29.1 29.1

Total other large losses 292.1 221.3 513.4

Total large losses 356.1 425.7 781.8

Impact on Combined ratio 2014 6.0%pts 6.1%pts 6.1%pts

Total large losses (2013) 260.7 577.6 838.3

Impact on Combined ratio 2013 4.7%pts 8.4%pts 6.8%pts

BayernLB Fixed Income Conference, Munich, 18 May 2015

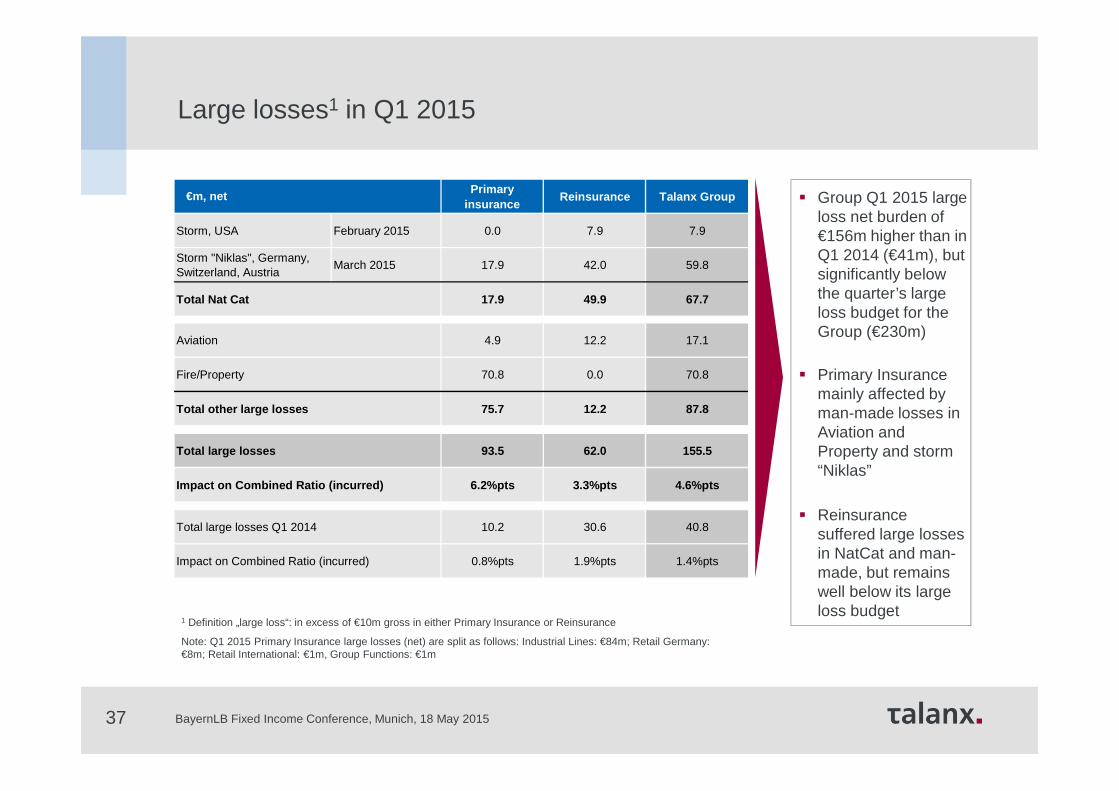

37

� Group Q1 2015 large loss net burden of €156m higher than in Q1 2014 (€41m), but significantly below the quarter’s large loss budget for the Group (€230m)

� Primary Insurance mainly affected by man-made losses in Aviation and Property and storm “Niklas”

� Reinsurance suffered large losses in NatCat and man-made, but remains well below its large loss budget

Large losses1 in Q1 2015

1 Definition „large loss“: in excess of €10m gross in either Primary Insurance or Reinsurance

Note: Q1 2015 Primary Insurance large losses (net) are split as follows: Industrial Lines: €84m; Retail Germany: €8m; Retail International: €1m, Group Functions: €1m

Primary insurance

Reinsurance Talanx Group

Storm, USA February 2015 0.0 7.9 7.9

Storm "Niklas", Germany, Switzerland, Austria

March 2015 17.9 42.0 59.8

Total Nat Cat 17.9 49.9 67.7

Aviation 4.9 12.2 17.1

Fire/Property 70.8 0.0 70.8

Total other large losses 75.7 12.2 87.8

Total large losses 93.5 62.0 155.5

Impact on Combined Ratio (incurred) 6.2%pts 3.3%pts 4. 6%pts

Total large losses Q1 2014 10.2 30.6 40.8

Impact on Combined Ratio (incurred) 0.8%pts 1.9%pts 1.4%pts

€m, net

BayernLB Fixed Income Conference, Munich, 18 May 2015

38

Rating overview

Standard & Poor’s A. M. Best

Grade Outlook Grade Outlook

last update 30/06/14 16/05/14

Talanx Group1 - - A Stable

Talanx Primary Group2 A+ Stable - -

last update 28/05/14 19/09/14

Hannover Re subgroup3 AA– Stable A+ Stable

rating of Talanx Primary GroupCurrent financial strength ratings

Financial strength underpinned by S&P and A.M. Best ratings

1 The designation used by A. M. Best for the Group is “Talanx AG and its leading non-life direct insurance operation and its leading life insurance operation”2 This rating applies to the core members of Talanx Primary Group (the subgroup of primary insurers in Talanx Group)3 This rating applies to Hannover Re and its major core companies. The Hannover Re subgroup corresponds to the Talanx Reinsurance segment4 Insurance Industry and Country Risk Assessment

Business Risk Profile

Strong

Financial Risk Profile

Very Strong

ERM

Strong

Management & Governance

Satisfactory

Capital & Earnings

Very Strong

IICRA 4)

Intermediate Risk

Risk Position

Intermediate

Competitive Position

Strong

Financial Flexibility

Strong

Liquidity

Exceptional

Anchor rating a+ Modifiers

Modifiers

Neutral

BayernLB Fixed Income Conference, Munich, 18 May 2015

39

Financial Calendar

12 August 2015Interim Report 6M 2015

17 September 2015Capital Markets Day

12 November 2015Interim Report 9M 2015

21 March 2016Annual Report 2015

11 May 2016Annual General Meeting

13 May 2016Interim Report 3M 2016

Contact

Talanx AGRiethorst 230659 [email protected]

Carsten Werle, CFAPhone: +49 511 3747 [email protected]

Marcus Sander, CFAPhone: +49 511 3747 [email protected]

Wiebke ErlerPhone: +49 511 3747 [email protected]

Christian MarxPhone: +49 511 3747 [email protected]

39

Talanx Investor Relations

BayernLB Fixed Income Conference, Munich, 18 May 2015

40

Disclaimer

This presentation contains forward-looking statements which are based on certain assumptions, expectations and opinions of the management of Talanx AG (the "Company") or cited from third-party sources. These statements are, therefore, subject to certain known or unknown risks and uncertainties. A variety of factors, many of which are beyond the Company’s control, affect the Company’s business activities, business strategy, results, performance and achievements. Should one or more of these factors or risks or uncertainties materialize, actual results, performance or achievements of the Company may vary materially from those expressed or implied as being expected, anticipated, intended, planned, believed, sought, estimated or projected.in the relevant forward-looking statement.

The Company does not guarantee that the assumptions underlying such forward-looking statements are free from errors nor does the Company accept any responsibility for the actual occurrence of the forecasted developments. The Company neither intends, nor assumes any obligation, to update or revise these forward-looking statements in light of developments which differ from those anticipated.

Where any information and statistics are quoted from any external source, such information or statistics should not be interpreted as having been adopted or endorsed by the Company as being accurate. Presentations of the company usually contain supplemental financial measures (e.g., return on investment, return on equity, gross/net combined ratios, solvency ratios) which the Company believes to be useful performance measures but which are not recognised as measures under International Financial Reporting Standards, as adopted by the European Union ("IFRS"). Therefore, such measures should be viewed as supplemental to, but not as substitute for, balance sheet, statement of income or cash flow statement data determined in accordance with IFRS. Since not all companies define such measures in the same way, the respective measures may not be comparable to similarly-titled measures used by other companies. This presentation is dated as of 12 May 2015. Neither the delivery of this presentation nor any further discussions of the Company with any of the recipients shall, under any circumstances, create any implication that there has been no change in the affairs of the Company since such date. This material is being delivered in conjunction with an oral presentation by the Company and should not be taken out of context.

40 BayernLB Fixed Income Conference, Munich, 18 May 2015