basic course on public-private partnerships (ppp) for ... · basic cities development initiative...

TRANSCRIPT

Cities Development Initiative for Asia

Basic Course on Public-Private Partnerships (PPP) for

Municipalities:

Training for Facilitators

Trainer’s Materials

17-20 July 2012 in Bangkok, Thailand

CDIA

© The Cities Development Initiative for Asia (CDIA)

CDIA is a multi-donor Programme established in 2007 to assist medium sized Asian cities to bridge the gap between their development plans and the implementation of their infrastructure investments. CDIA uses a demand driven approach to support the identification and development of urban investment projects in the framework of existing city development plans that emphasize with focus on environmental improvement, pro-poor development, good governance, and climate change.

All rights reserved.

Basic Course on Public-Private Partnerships (PPP) for

Municipalities: Training for Facilitators

Trainer’s Materials

© Cities Development Initiative for Asia (CDIA)

July 2012

Disclaimer This document is part of a training course on Municipal Public Private Partnerships, and has been developed for pedagogical purposes only. Its use or citation in any other context without the prior written authorization from CDIA is not permitted. Information from several reputable sources was used in the elaboration of this document to serve as examples for illustration of concepts or as case studies. However, CDIA cannot guarantee the accuracy of the information provided by those sources. The views expressed in this document are solely those of the authors and do not necessarily reflect the position or policy of the CDIA Funding Agencies.

CDIA’s Short PPP Training for Facilitators i

TABLE OF CONTENTS

TABLE OF CONTENTS ......................................................................................................................................... I

TABLE OF FIGURES ........................................................................................................................................... II

TABLE OF BOXES .............................................................................................................................................III

FOREWORD ..................................................................................................................................................... 2

1 WHAT IS AND WHAT IS NOT A PPP ........................................................................................................... 6

2 WHAT IS IMPORTANT............................................................................................................................... 8

3 URBAN DEVELOPMENT AND BROADER DEVELOPMENT GOALS ............................................................. 10

4 PPPS ARE PARTNERSHIP PROJECTS ........................................................................................................ 14

5 THE PPP STAKEHOLDERS ........................................................................................................................ 16

6 BENEFITS AND DOWNSIDES ................................................................................................................... 18

6.1 Infrastructure Challenges ......................................................................................................................... 19

7 THE IMPORTANCE OF BANKABILITY ....................................................................................................... 24

8 VALUE FOR MONEY ................................................................................................................................ 26

8.1 Quantitative value for money assessment ............................................................................................... 27

8.2 Qualitative value for money assessment.................................................................................................. 28

9 MAKING PROJECTS ATTRACTIVE ............................................................................................................ 30

10 TYPES OF URBAN PPP PROJECTS......................................................................................................... 36

10.1 Types of PPPs ............................................................................................................................................ 36

10.2 Sectors where PPPs can be applied .......................................................................................................... 37 10.2.1 Urban Transport ..................................................................................................................... 38 10.2.2 Public utilities ......................................................................................................................... 41 10.2.3 Public Services and Social and Public Infrastructures ............................................................ 44

11 IDENTIFYING PPP PROJECTS ............................................................................................................... 50

11.1 Project ideas ............................................................................................................................................. 51

11.2 Project selection ....................................................................................................................................... 51

12 WHAT IS NEEDED TO UNDERTAKE A PPP ............................................................................................ 52

13 LEGAL CONSIDERATIONS .................................................................................................................... 54

13.1 Civil law ..................................................................................................................................................... 55

13.2 Common law ............................................................................................................................................. 56

14 RISK MANAGEMENT ........................................................................................................................... 60

14.1 Risk identification ..................................................................................................................................... 60 14.1.1 Project Risk ............................................................................................................................. 60 14.1.2 Country-specific risks ............................................................................................................. 61 14.1.3 Municipal risk ......................................................................................................................... 62

14.2 Risk management ..................................................................................................................................... 62 14.2.1 Risk Qualification .................................................................................................................... 63 14.2.2 Risk Mitigation ........................................................................................................................ 64 14.2.3 Risk allocation ......................................................................................................................... 66

15 THE SPONSORS ................................................................................................................................... 72

15.1 Identification of projects .......................................................................................................................... 74

15.2 Consortia formation ................................................................................................................................. 74

CDIA’s Short PPP Training for Facilitators ii

15.3 Offer preparation...................................................................................................................................... 75

16 PROJECT FUNDING ............................................................................................................................. 76

16.1 SPV’s financial structure ........................................................................................................................... 76

16.2 Financing structure ................................................................................................................................... 77

17 LENDERS ............................................................................................................................................. 82

17.1 Loan characteristics .................................................................................................................................. 82

17.2 Project Finance ......................................................................................................................................... 83

17.3 Project Finance’s risk management .......................................................................................................... 84

18 THE PROJECT CYCLE ............................................................................................................................ 88

18.1 The project cycle stages ............................................................................................................................ 89

18.2 Project logistics ......................................................................................................................................... 90

18.3 Project team and governance structure ................................................................................................... 91

18.4 External advisors....................................................................................................................................... 91

18.5 Project plan and time-table ...................................................................................................................... 91

18.6 Project preparation .................................................................................................................................. 91 18.6.1 Pre-Feasibility Study ............................................................................................................... 92 18.6.2 Feasibility study ...................................................................................................................... 92 18.6.3 Tendering documents ............................................................................................................ 92

18.7 Project procurement ................................................................................................................................ 92 18.7.1 Prequalification of bidders ..................................................................................................... 93 18.7.2 Requests for Proposal (RFPs) ................................................................................................. 93 18.7.3 Bid evaluation ......................................................................................................................... 94

18.8 Project follow-up ...................................................................................................................................... 94

18.9 Project ending ........................................................................................................................................... 95

TABLE OF FIGURES

Figure 1. PPP Stakeholders ................................................................................................................... 16

Figure 2. Relationship between stakeholders ....................................................................................... 17

Figure 3. Source: PPP Reference Guide. World Bank Institute and PPIAF ............................................ 19

Figure 4: Project Finance vs Corporate Finance.................................................................................... 25

Figure 5. Value for Money .................................................................................................................... 27

Figure 6: PPP readiness in Asia-Pacific: ................................................................................................. 55

Figure 7: Civil Law and Common Law main features ............................................................................ 55

Figure 8: Different laws can affect PPP projects .................................................................................. 56

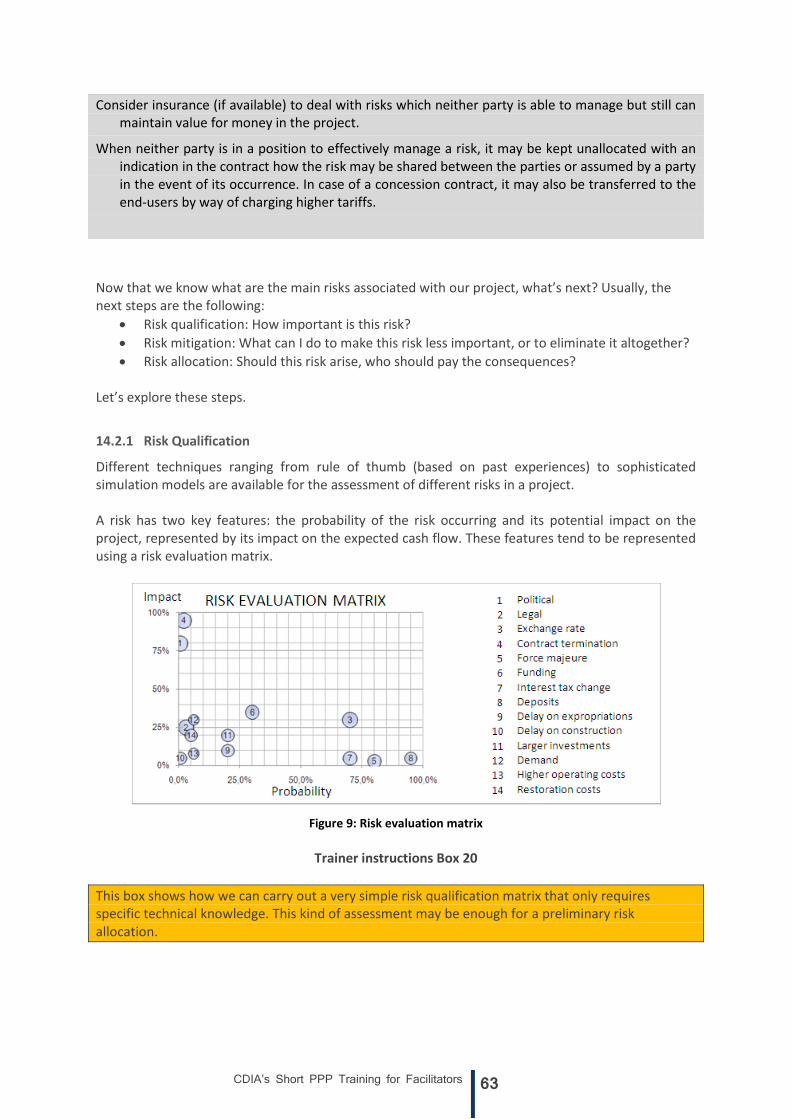

Figure 9: Risk evaluation matrix ............................................................................................................ 63

Figure 10: Risk allocation in an urban tunnel........................................................................................ 67

Figure 11: Risk allocation in a housing project ..................................................................................... 68

Figure 12: Cash Flow and Project Finance I .......................................................................................... 83

Figure 13: Cash Flow and Project Finance II ......................................................................................... 83

Figure 14: Stages of a PPP project ........................................................................................................ 89

CDIA’s Short PPP Training for Facilitators iii

TABLE OF BOXES

Box 1: Is this a PPP agreement? ............................................................................................................ 7

Box 2: How can PPP help urban development? .................................................................................... 11

Box 3: How can PPP be a successful partnership? ................................................................................ 15

Box 4: Parking in Medolang: Who are the stake-holders? ................................................................... 18

Box 5: Is PPP a good solution? .............................................................................................................. 20

Box 6: SPV's characteristics ................................................................................................................... 25

Box 7: Example of bankability and capital structure. Alandur Sewerage Project ................................. 26

Box 8: Is PPP procurement superior to the PSC? .................................................................................. 28

Box 9: Are the benefits-costs easy to measure? ................................................................................... 29

Box 10: Parking in Medolang: Making the project attractive ............................................................... 31

Box 11: Mass Rapid Transit: Bangkok Skytrain. Thailand ..................................................................... 39

Box 12: Infrastructure: Kuala Lumpur Smart Tunnel, Malaysia ............................................................ 40

Box 13: Alandur Sewerage System, India.............................................................................................. 42

Box 14: Water Supply Metro Manila, Philippines ................................................................................ 43

Box 15: Please try to identify ................................................................................................................ 46

Box 16: How does project analysis answer the following questions? .................................................. 52

Box 17: Making a PPP come true ......................................................................................................... 53

Box 18: Regulation by the law or by the contract................................................................................. 56

Box 19: UNESCAP principles in risk management ................................................................................. 62

Box 20: Risk qualification in a Subway PPP project .............................................................................. 64

Box 21: Asian Development Bank (ADB) Credit Enhancement Products .............................................. 65

Box 22: Infrastructure Debt Fund (IIDF) ................................................................................................ 65

Box 23: Risk mitigation measures ......................................................................................................... 66

Box 24: Risk sharing .............................................................................................................................. 67

Box 25: Risk allocation .......................................................................................................................... 68

Box 26: What are the sponsors’ tasks? ................................................................................................. 73

Box 27: Consortium formation ............................................................................................................. 75

Box 28: SPV’s characteristics ................................................................................................................. 76

Box 29: Capital structure: Who comes last? ......................................................................................... 77

Box 30: What is more expensive? ......................................................................................................... 78

Box 31: What are the main stages in a project cycle? .......................................................................... 88

Box 32: PPP development and implementation process according to PPIAF (World Bank) ................ 89

Box 33: How does the project cycle in your country differ? ................................................................. 90

Box 34: Prequalification of bidders in social housing ........................................................................... 93

Box 35: Follow-up of the social housing PPP project ............................................................................ 94

CDIA’s Short PPP Training for Facilitators 1

CDIA’s Short PPP Training for Facilitators 2

FOREWORD

PURPOSE, TARGET AUDIENCE, AND KEY MESSAGES

CDIA’s PPP Guidelines for Municipalities has received all kinds of compliments and positive recognition among its users and peer organizations for its clarity and simplicity. However, our goal was not only to make it easy to read and understand, but also make it an instrument for readers to learn how to deal with the opportunities that PPPs can bring to small and medium size cities in Asia in a safe and sound manner.

The training was designed to complement the Guidelines providing more than just words and additional readings but also practical and real-situation exercises for participants to have a drill on the concepts.

This training was not designed for PPP practitioners or people who will devote their careers entirely to the development of PPP projects, but for those that have not been exposed to this contractual scheme before or those with little knowledge of it. It was designed for city officials at the municipal level with different concerns and anxieties in the implementation of this model from the ones that were traditionally using PPP.

The objective of this training for facilitators is to present as it would be presented to its final users. In this way they can see themselves in the role of final participants evaluating the effectiveness that this training can bring to their particular context.

ORGANIZATION OF THIS GUIDEBOOK

Following the structure of CDIA’s PPP Guidelines for Municipalities, the training is divided in different sessions covering three parts:

In “Basis”, the fundamentals of the PPP model, including definitions and key principles, are described in a practical manner. It provides guided questions and exercises for participants to understand and get familiarized with the concepts, and their translation to the circumstances of the local governments.

In “Approach”, insights on how local governments can go about deciding whether or not to pursue a PPP approach are provided. A review is given on how a PPP scheme is different from a traditional publicly-financed project. It also describes the different positions of each individual player participating in the process.

In “Process”, the training provides a complement to the Guideline and an introduction to what the real process of engaging in a project under a PPP scheme entails.

B A S I S A P P R O A C H P R O C E S S

SECTION 1

PART 1

B A S I S

CDIA’s Short PPP Training for Facilitators 4

SESSION 1

BASIS I

CDIA’s Short PPP Training for Facilitators 5

CDIA’s Short PPP Training for Facilitators 6

Trainer general instructions

This session is an introduction to PPPs and the course. Main ideas that should be delivered to participants are: • Not all procurement involving a private partner is a PPP • PPP procurement involves financing from the private sector as well as risk sharing between the local authorities and the private partner • To make a successful PPP there are many necessary ingredients – all participants must obtain something • Even though PPP transfers many duties to the private partner, local authorities remain at all times responsible for the project, the services provided and its outcome • PPP procurement can be very helpful to local authorities as an urban development tool – stretching public funds, bringing private sector efficiency…

Public Private Partnership (PPP) is not a new concept, but as old as the need for infrastructures. Public Authorities have traditionally engaged with the private sector to develop public services and infrastructures using typical supply contracts or other forms of procurement instruments that share budgetary funding as a common characteristic. PPP procurements, in turn, demand from private participants not only their managing and implementation abilities but also their financing capacity. Public infrastructures, in general, require a significant investment and subsequently long-term agreements to make them commercially viable. That makes PPP contracts far more complex than traditional procurement contracts, demanding from the participants’ additional experience and capacities.

1 WHAT IS AND WHAT IS NOT A PPP

Trainer suggested readings

• “CDIA PPP Guide for Municipalities,” City Development Initiative Asia, June 2010. Section 1: Introduction to Public Private Partnerships (PPP) (page 4) • “Public-Private Partnership Handbook”, ADB, 2008. Section 1: Public Private Partnerships (PPPs) – An Overview (page 1) • “Public-Private Partnerships Reference Guide, Version 1.0”, PPIAF, 2012 Key Definitions: What is a PPP? (page 11) Section 1.2.1: PPP Contract Types (page 36)

PPP are long term contracts between a Public Authority and a private partner to provide a public infrastructure or service in which the private partner bears significant financial and management responsibility. PPP contracts share the following features:

Risks are shared between the public and private participants

Risks are allocated through contracts between the partners and/or the specific legislation, if any

The private partner is expected to finance and/or operate a public infrastructure or to provide a public service

The private partner expects to recover his investment and to obtain a reasonable return

CDIA’s Short PPP Training for Facilitators 7

The Public Authority retains property, service responsibility and the right to terminate the contract

The Public Authority is expected to assure that the PPP contract provides the best possible return on the investment made amongst all the available procurement alternatives

The PPP concept encompasses many different procurement alternatives itself, depending on what its role is (duties, responsibilities, rights…). Consider, for instance, the following examples:

A toll road that must be built from scratch: the private sponsor has to finance, design, build and operate the infrastructure.

A toll road that is already built but needs an upgrade: the design and construction aspects are less relevant than on the previous example.

A toll road that has already been built and upgraded by the Local Authorities, who decide to lease it to the private sector for a certain period of time: the private sponsor needs only to finance and operate the infrastructure.

PPPs are usually not limited to obtaining financing from the private sector – some responsibilities (as well as the associated risks) are, in many cases, transferred as well. The following contractual agreements between the public and private sectors are, in most cases, not considered PPP contracts:

Service contracts, regardless the payment mechanisms, where the private partner assumes no operating responsibilities

Management contracts, where the private partner assumes no financial risk

Divestiture or privatization of public assets, where property is transferred

Assignment of management to a publicly owned enterprise, where there is no private partner assuming operational and financial risks.

Trainer instructions Box 1

The first box is a very easy one, but is important in order to introduce some basic concepts (risk transfer, collaboration, private and public active participation). It is suggested that the box is solved collectively during the session, one question at a time. To make the session more participative, the trainer can ask for a volunteer to provide an answer and provide the reasons. Other participants can then give their opinions.

Take your time to explain each answer and resolve all doubts; the course can be speeded up later.

Box 1: Is this a PPP agreement?

In your local town, there is a Public Bureau in charge of water supply on exclusive terms. In accordance with your legislation, the local government could allow private companies to supply water.

The water supply infrastructure requires significant investment and better management, and your local government is evaluating different alternatives. Please provide some advice pointing out whether the following alternatives are a form of PPP or not:

CDIA’s Short PPP Training for Facilitators 8

Transforming the Water Supply Bureau into a state-owned company that will borrow money from the banks and provide the service on a commercial basis.

Yes No . The Water Supply Bureau is still owned by a Public Authority

Carrying out the investment with public funds and reaching an agreement with a private partner for the management of the water supply service.

Yes No This is an example of a management contract where the private partner assumes no financial risk. Some PPP guides may consider it a PPP if remuneration is subject to performance indicators. Transferred risks, however, are limited.

Transforming the Water Supply Bureau into a publicly and privately owned company (the shareholders being the local authority and a private partner selected by public tendering). The company will borrow money from the banks and provide the service on a commercial basis.

Yes No The private partner bears significant financial and operational risks a as part of a mix capital company.

Reaching an agreement with a private partner for the construction of the needed infrastructure and the management of the water supply service. Funds will be provided by the local government and by the private partner.

Yes No This is a typical PPP agreement. The existence of a certain level of public finance does not change this fact. The private partner still bears some financial risk as well as operational risk.

Selling the Water Supply Body to a private investor together with an allowance to supply water.

Yes No This is an example of a divesture. Privatizations are not considered PPP. The relationship between the Authority and the private investor after the sale is a normal Authority/private enterprise relationship.

The CDIA’s PPP Guide for Municipalities includes broader definitions of PPP and a list of relationships between the Public Authority and private partners that are not considered PPPs.

2 WHAT IS IMPORTANT

Trainer instructions

In this section we are going to present some basic topics that will be explained in detail in the course of the succeeding sessions. It is important that participants understand what is important and why. Participants can be asked to determine what elements they consider important in PPP procurement, although normally they will not be able to do it. It may be easier to have them help justify why the topics outlined by the trainer are important.

Trainer suggested readings

• “CDIA PPP Guide for Municipalities,” City Development Initiative Asia, June 2010. Section 2: What are the main principles of PPPs? (page 5) • “Public-Private Partnership Handbook”, ADB, 2008. Section 1: Public Private Partnerships (PPPs) – An Overview (page 1) Section 3.1: Requirements and expectations (page 11)

CDIA’s Short PPP Training for Facilitators 9

In a PPP agreement, the Public Authority transfers management and decision- making powers to the private partner during a normally long period of time, and the private partner bears significant risks and assumes long-term commitments. The Public Authority and the private sector need to build up a different type of association beyond the classical client-procurer relationship. They must become longtime partners sharing the risks and revenues of the project. When identifying, appraising and developing a PPP project, there are many things that must be taken into consideration. Some of them have to do with basic urban development needs, therefore:

PPP should help achieving public goals. PPP agreements are a powerful and efficient tool which local governments have at their disposal. But still only a tool. If the usage of PPP in a certain project does not help urban development, does not support broader development goals or does not answer to users’ and citizens’ needs better than normal procurement, then said project may not succeed.

There is a more or less formal procedure that helps in deciding whether PPP is the better procurement option for a certain project: Value for Money.

PPP requires private partners. PPP agreements need the participation of private parties. To ensure that participation, the local authority must identify the potential partners, arouse their interest and design attractive and balanced PPP projects that take their needs and worries into consideration.

PPP requires private funds. One of the main features of PPP contracts is that they aim to raise private funds for public needs. Private lenders analyze carefully any potential investment, especially large and risky investments such as those required by PPP projects.

In order to be financed, PPP projects must be bankable, meaning they are capable of providing sufficient profit to the potential lenders to appear as a good investment option. In order to attract both private partners and private funds, PPP projects must go through an efficient and consistent risks identification, allocation and mitigation process.

Public Authority keeps responsibility and liability. The Granting Authority maintains in, all cases, the responsibility for delivering the services under its authority, and should make sure that the project is properly carried on in its behalf. Furthermore, even if the private partner assumes the complete financial risk, the Public Authority usually maintains economic liability.

The Public Authority must carry out a constant and efficient supervision and monitoring of the private partner performance throughout the project. All these concepts will be explained in detail in the following chapters, with examples to make them more comprehensive.

CDIA’s Short PPP Training for Facilitators 10

3 URBAN DEVELOPMENT AND BROADER DEVELOPMENT GOALS

Trainer suggested readings

• “CDIA PPP Guide for Municipalities,” City Development Initiative Asia, June 2010. Section 3: Do PPPs support broader development goals? (page 9) • “Public-Private Partnership Handbook”, ADB, 2008. Section 1.2: Motivation for engaging in PPPs (page 3) • “Public-Private Partnerships Reference Guide, Version 1.0”, PPIAF, 2012 Section 1.1: Infrastructure challenges and how PPPs can help (page 15)

The CDIA’s PPP Guide for Municipalities describes, in its introduction, the infrastructure needs and the public services shortfalls common to most Asian cities. It also exposes the main reasons for local governments’ inefficiency in providing adequate urban services and infrastructures. The Guide also describes how PPP procurement, by means of their many potential advantages, can support broader development goals such as reducing poverty, improving living conditions and providing environmental improvements. It focuses on the positive environmental impact of financial, management and technical improvement provided by efficient PPP agreements. PPPs have experimented a continuous growth in the last decades as they seem to be an effective answer to some of these public sector’s difficulties. Some of the reasons for this success are that PPPs:

reduce public deficit and debt. Concessional PPP contracts allow investing with limited indebtedness and impact on public accounts.

reduce public risks and liabilities. PPP agreements transfer significant risks to private partners reducing risks and liabilities supported by the Authority.

use private efficiency. Incorporating market criteria into the procurement results in better managed projects.

stretch public funds further. Local Authorities can make the most out of limited funds by taking advantage of private financial capacity, as shown in Figure 5 of CDIA PPP Guide for Municipalities.

bring investments forward. Stretching public funds permits providing more and better services

are implemented faster. Contractors are incentivized to implement projects faster to bring revenues forward.

have costs that are more predictable. Projects have a turn-key approach. The project financial plan includes the whole life costing for the fixed period including upgrade requirements, thus costs are extremely predictable.

All in all, PPP procures powerful tools for local governments to face their increasing needs and to improve urban development. Among many others, the following goals can be achieved:

Reduce transportation costs and increase efficiency

Provide clean water and sanitation to more people at a lower cost

Improve the quality of public services and public equipment

Find original tailor-made solutions for urban development challenges

CDIA’s Short PPP Training for Facilitators 11

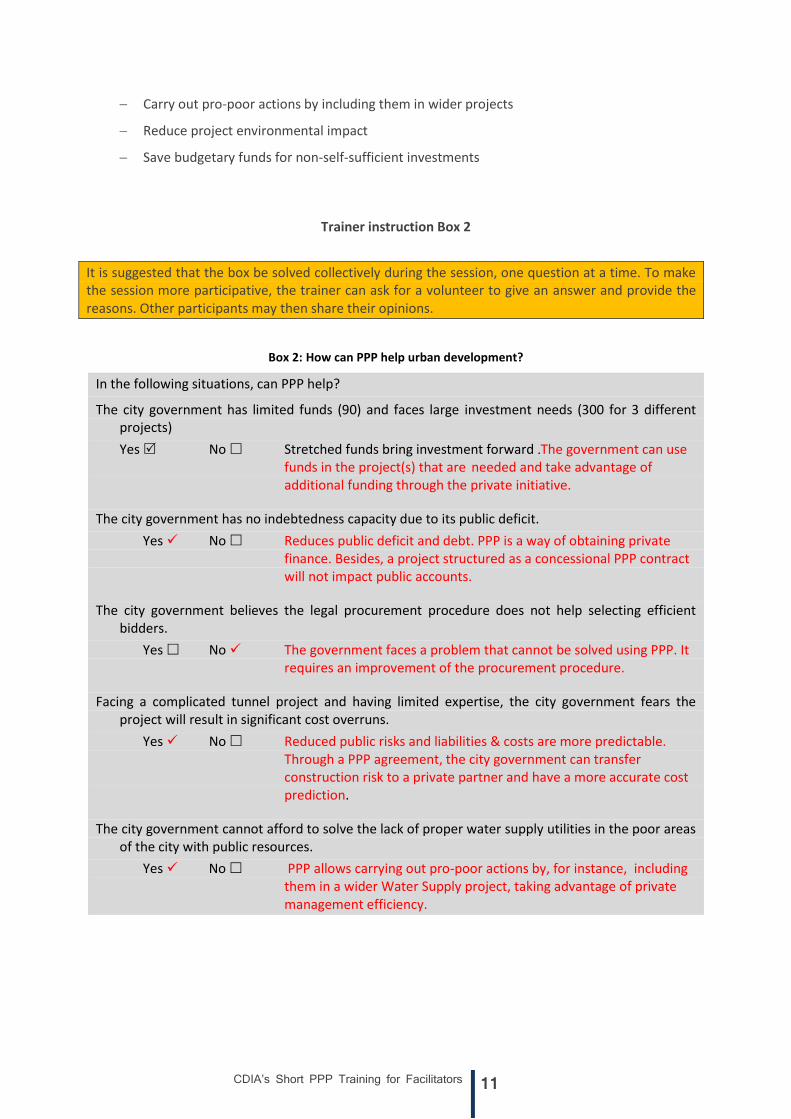

Carry out pro-poor actions by including them in wider projects

Reduce project environmental impact

Save budgetary funds for non-self-sufficient investments

Trainer instruction Box 2

It is suggested that the box be solved collectively during the session, one question at a time. To make the session more participative, the trainer can ask for a volunteer to give an answer and provide the reasons. Other participants may then share their opinions.

Box 2: How can PPP help urban development?

In the following situations, can PPP help?

The city government has limited funds (90) and faces large investment needs (300 for 3 different projects)

Yes No Stretched funds bring investment forward .The government can use funds in the project(s) that are needed and take advantage of additional funding through the private initiative.

The city government has no indebtedness capacity due to its public deficit.

Yes No Reduces public deficit and debt. PPP is a way of obtaining private finance. Besides, a project structured as a concessional PPP contract will not impact public accounts.

The city government believes the legal procurement procedure does not help selecting efficient bidders.

Yes No The government faces a problem that cannot be solved using PPP. It requires an improvement of the procurement procedure.

Facing a complicated tunnel project and having limited expertise, the city government fears the project will result in significant cost overruns.

Yes No Reduced public risks and liabilities & costs are more predictable. Through a PPP agreement, the city government can transfer construction risk to a private partner and have a more accurate cost prediction.

The city government cannot afford to solve the lack of proper water supply utilities in the poor areas of the city with public resources.

Yes No PPP allows carrying out pro-poor actions by, for instance, including them in a wider Water Supply project, taking advantage of private management efficiency.

CDIA’s Short PPP Training for Facilitators 12

SESSION 2

BASIS II

CDIA’s Short PPP Training for Facilitators 13

CDIA’s Short PPP Training for Facilitators 14

Trainer general instructions

This session is focused on PPP basic issues. Main ideas that should be delivered to participants are: • PPPs are partnership projects and should be faced in a much more collaborative way than traditional public procurement projects. • There are many actors involved in a PPP project, and they should all be taken into account. • PPPs have potential benefits and downsides. We should try to take advantage of benefits and avoid downsides. Knowing them will help to determine if PPP procurement is the best option for a certain project.

4 PPPS ARE PARTNERSHIP PROJECTS

Trainer suggested readings

• “CDIA PPP Guide for Municipalities,” City Development Initiative Asia, June 2010. Section 2.1: The importance of the third “P” - Partnership (page 5) • “Public-Private Partnership Handbook”, ADB, 2008. Section 3.7: Clear Sector Strategy and Road Map (page 24) Section 3.8: Clear Government Commitment and a Designated Champion (page 26) • “Public-Private Partnerships in Housing and Urban Development”, United Nations Human

Settlements Program, 2011. Building strong relationships through Clear Communication (page 17)

PPP projects are based on collaboration between a public partner, who is responsible for the procurement of a certain infrastructure or public service, and a private partner, who is willing to play an active role in the procurement process by means of assuming some significant operational and financial responsibilities. PPP relationships require cooperative contracts. The public and private partners must work together all the way through the project, and that stretches over a long period of time. Given the long duration of PPP contracts, previously identified, or even unexpected risks, will eventually arise. The private sector and the Authority must work together to overcome the difficulties when they arise, doing it in a creative and flexible way. CDIA’s PPP Guide for Municipalities includes a typical tasks distribution between the public and private partner, but in truth there are limitless possibilities on the distribution of tasks and responsibilities. What should be always taken into consideration is that PPP projects involve several stakeholders with different objectives and capacities. The PPP agreement should try to involve all stakeholders, align their objectives with those of the project and provide a proper framework for a collaborative performance.

Trainer instruction Box 3

This box focuses on building up confidence between partners - a basic requirement in order to develop a successful PPP project. It is suggested that the box be solved collectively during the session, one question at a time. To make the session more participative, the trainer can ask for a volunteer to give an answer and provide the reasons. Other participants may then share their opinions.

CDIA’s Short PPP Training for Facilitators 15

Box 3: How can PPP be a successful partnership?

PPP agreements should take into consideration the main principles of collaborative agreements:

Mutual trust: Transparency and capacity

Commitment:

Solid long term PPP programs with wide politic support. Budgetary and fiscal commitment. Understanding of PPP projects

Dialogue:

Flexible contractual agreements that include provisions for unexpected situations

Constructive approach:

PPP permits imaginative and creative solutions. Take advantage of having private firms searching for the best possible one.

Win-win basis:

In a PPP project success is impossible to achieve alone. If the private partner does not do well, the project is a potential failure.

CDIA’s Short PPP Training for Facilitators 16

5 THE PPP STAKEHOLDERS

Trainer suggested readings

• “CDIA PPP Guide for Municipalities,” City Development Initiative Asia, June 2010. Who are the stakeholders in a PPP? (page 20) • “Public-Private Partnership Handbook”, ADB, 2008. Table 2: Role of Different Stakeholders in the PPP Process (page 21) Figure 3: The Range of Stakeholder Interests in PPPs (page 22) • “Public-Private Partnerships in Housing and Urban Development”, United Nations Human

Settlements Program, 2011. Relationships with lenders and other parties (page 8)

CDIA’s PPP Guide for Municipalities identifies the typical stakeholders involved in a PPP process:

Figure 1. PPP Stakeholders

Since no two PPPs are alike, other stakeholders may be involved as well: construction companies, service managers, insurance companies, labor unions… Some specific aspects to PPP procurement (the need to focus on partnership; the way market rules affect project feasibility; the often complicated bidding process; bidder selection criteria…) oblige to take all parties involved into consideration in all phases, starting from project identification. Broadly speaking, the main players in a PPP and their role are the following:

Local Authority (or Public entity): The entity responsible for the facility or service object of the agreement. Sometimes Public Authorities contribute to the project with assets (ie. providing parking space for trucks on a waste transportation concession) or funds (becoming share-holders in the concession)

Sponsors: usually private companies. It is common practice that sponsors gather in groups (consortia) – Several consortia then enter the bidding process and can leverage on the

CDIA’s Short PPP Training for Facilitators 17

strengths of the sponsors behind it. Once the project is awarded, they constitute what is called a Special Purpose Vehicle (SPV), a company for the only purpose of developing the project. Sponsors governs the SPV, provide its equity and receive the eventual dividends.

Financial Institutions: the lenders that provide enough funds to the SPV to face the investment, usually in the form of debt. Local authorities may also require funding from financial institutions in the event the project requires public financial support to achieve bankability.

Contractor: the specialized companies responsible for the construction and/or management of the project. Often they are also sponsors of the SPV.

Users: the final users of the facility or service.

National or Regional Government: Responsible for issuing regulations and laws that affect the PPP agreement. They may eventually have to approve the project or provide public funds.

Dealing with parties that have such different natures and pursue such different goals adds complexity to PPP agreements. However, all of those stakeholders are necessary in order to achieve success and a poor performance by any of them can result on the project failure. The following chart represents the relations between the main stakeholders in a typical PPP project.

Figure 2. Relationship between stakeholders

In the graph above all the depicted stakeholders are related to the Special Purpose Vehicle (SPV), which stands in the center. SPVs and their characteristics will be described in detail later on.

Trainer instructions Box 4

This box is the first one that refers to the “Parking in Medolang” case study. Consider if you should make a summary or let the participants review the information provided. Participants should name all possible stakeholders apart from the main ones, which we have already detailed. The objective is to realize how many stakeholders can be affected by a PPP project, how complex the relationships between them can be and how that affects the project.

CDIA’s Short PPP Training for Facilitators 18

Box 4: Parking in Medolang: Who are the stake-holders?

Please refer to the “Parking in Medolang” case study.

Can you identify the project’s stakeholders, assuming that a PPP is used for procurement? Focus specially in those that do not figure on the graph above.

Business owners close to the new parking

Granting authority

Concession company

Lenders

Construction companies

Business owners close to the new parking (construction phase and operation phase)

Other parking facilities owners in the area

People living nearby that may be affected by the public works or the noise…

6 BENEFITS AND DOWNSIDES

Trainer suggested readings

• “CDIA PPP Guide for Municipalities,” City Development Initiative Asia, June 2010. Section 4: Are there downsides to PPPs? (page 10) • “Public-Private Partnerships Reference Guide, Version 1.0”, PPIAF, 2012 Section 1.1: Infrastructure challenges and how PPPs can help (page 15) • “Public-Private Partnerships in Housing and Urban Development”, United Nations Human

Settlements Program, 2011. Chapter 3: The Advantages and Disadvantages of PPPs (page 3)

Most potential benefits of PPP have been already exposed so far in this document and on CDIA’s PPP Guide for Municipalities. The following figure summarizes challenges faced by local authorities when facing infrastructure procurement, how PPP procurement can help overcoming these challenges, and how traditional procurement deals with these challenges.

CDIA’s Short PPP Training for Facilitators 19

6.1 Infrastructure Challenges

Figure 3. Source: PPP Reference Guide. World Bank Institute and PPIAF

So, if PPP has so many potential advantages, are there any downsides to PPPs? We shall review some key aspects that make PPP procurement complex:

Mindset change in Local Authorities: with more traditional procurement alternatives Public Administrations act as “buyers” – hiring contractors to build a road for instance. When using a PPP scheme, the public sector needs to become a “seller”, that is, to convince sponsors of the attractiveness of the project – focusing on cash-flows and risks.

Additional studies: compared to traditional procurement, PPPs require extra-work on the Local Authorities side. Besides developing the project’s technical aspects, a study showing the business behind and its attractiveness needs to be carried out.

Complex implementation: Going from a PPP in paper to a real PPP is a complicated task. Even when an Administration knows what it wants, still it must ensure that nothing is left out, that risk allocation is efficient, that contracts reflect the risk allocation that was planned, and so on.

Local Authorities capacities: The mindset change and the “business case” above mentioned require special capabilities, which are not always present on the Public Sector. Is there an expert on risk allocation in the office? Does anyone know how to put that optimal risk allocation in the contract? Who can tell the correct price for this infrastructure and this level of risk? Do we have contacts in the market to test our ideas?

In short, PPPs are essentially more complex than traditional procurement. The potential benefits are great, but PPP projects which aren’t well prepared may attract an inefficient or opportunistic private partner, and turn potential advantages into effective disadvantages: construction cost over-runs, delays, poor service for the user… PPP procurement, as any other powerful tool, is dangerous if poorly used. Many PPP contracts end up in disputes, re-negotiation, exorbitant revenues or bankruptcy. Let us expose some basic recommendations to keep in mind when developing a PPP project:

Insufficient funds

Poor planning and project selection

Inefficient management

Inadequate maintenance

Additional sources of funding and financing

Improving project and service delivery

Improving maintenance

How PPPs can Help

What’s wrong with infrastructure?

Increasing fiscal resources

Improving public decision-making

Improving governance

Improving regulation

Non-PPP Alternatives or Complements

Low coverage, low quality, low reliability

Better infrastructure performance

Private sector analysis and innovation

CDIA’s Short PPP Training for Facilitators 20

Be informed. Every city is different and every project needs a tailor made solution, but positive experiences in other cities are always a good starting point. Do not try to be too innovative at once if you lack the experience.

Be pragmatic. PPP is no magic wand. Do not forget that a society has a limited payment capacity. Make the most out of it.

Be moderate. PPP schemes where too much risk is transferred (or kept) or too much private funds are attracted (or too few) will probably not work.

Get involved. Do not expect the private partner to do your job. Supervision and monitoring is essential for achieving success.

Trainer instruction Box 5

The objective of this box is to show that project analysis is important to take advantage of potential PPP benefits and avoid PPP downsides. It is suggested that the box be solved collectively during the session, one question at a time. To make the session more participative, the trainer can ask for a volunteer to give an answer and provide the reasons. Other participants may then share their opinions.

Box 5: Is PPP a good solution?

In the following situations, is PPP a good solution?

The city government needs funds for a project but wants to carry out project management directly during both construction and operation

Yes No Only seeking private funding

The city government has repeatedly failed to tender good quality projects even with help from private consultants.

Yes No PPP can help in developing better projects: the specialized private partners can usually provide better solutions and comprehensive projects

The city government needs funds for a project but there are no potential private partners that can manage project risks better than the authority.

Yes No A PPP awarded to a mixed capital company can be a good solution, as the concession company would have both the managing ability from the authority and the private finance.

Private parties are reluctant to bear significant risks and demand wider government guarantees.

Yes No If the PPP contract does not transfer significant risks to the private partner, the potential benefits of PPP will not be reached.

The city government is facing reelection and the main opposite candidate has rejected the usage of PPP.

Yes No The potential private participants may be reluctant to bid for a project that does not have wider political support.

CDIA’s Short PPP Training for Facilitators 21

CDIA’s Short PPP Training for Facilitators 22

SESSION 3

BASIS III

CDIA’s Short PPP Training for Facilitators 23

CDIA’s Short PPP Training for Facilitators 24

Trainer general instructions

This session is also focused on PPP basic issues. Main ideas that should be delivered to participants are: • BANKABILITY: Project’s revenues and cost structure must be enough to convince lenders to finance the project. • VALUE FOR MONEY: In order to be used, PPP procurement should be superior to other procurement alternatives. A Qualitative assessments is relatively easy to carry out, intuitive and, in most cases, sufficient. • MAKING PROJECTS ATTRACTIVE: A bankable project that provides Value for Money cannot be developed if private partners do not participate. Projects must be structured in order to arouse stakeholders’ interest. In some cases that will require consultation.

7 THE IMPORTANCE OF BANKABILITY

Trainer suggested readings

• “Public-Private Partnership Handbook”, ADB, 2008. Section 6.4.1 Project Financing (page 56) • “Public-Private Partnerships Reference Guide, Version 1.0”, PPIAF, 2012 Section 1.3.2.1 Bankability (page 48) • “The Guide to Guidance”. EPEC, 2011 Section 1.2.3 Bankability (page 11)

PPP schemes are an interesting and useful solution for solving one of urban development main challenges: overcoming the lack of finance by opening to private participation and financing. But where does the money that the private sector brings come from? There are two main categories, which together make the “capital structure” of the SPV:

Equity: These are the funds that belong to sponsors, and that they decide to allocate into the SPV.

Debt: The funds that sponsors have are usually not enough to cover all the investments and initial costs. They need to convince external financiers (usually banks) to give a loan to the SPV.

When granting a loan, banks need guarantees in order to make sure it will be repaid. In PPPs, banks would require as a guarantee the cash flow generated by the project alone, plus the fact that when money comes into the SPV they are paid before the SPV’s shareholders. This scheme is known as “Project Finance”, since the project is the only guarantee banks rely on to be re-paid. If the project goes wrong, banks cannot turn to the SPV’s sponsors to get their money back. The following figure shows the difference between project finance and corporate finance

CDIA’s Short PPP Training for Facilitators 25

Figure 4: Project Finance vs Corporate Finance

So, if lenders will rely on the project alone to be repaid, they will want proof that the project is very robust, that it is a good business, which even if things do not go as well as initially forecasted, they will still get their dues.

Box 6: SPV's characteristics

Special Purpose Vehicles are companies with a set of very particular characteristics:

They can only pursue the objective they’ve been initially set-up for (for example the financing, construction, operations and maintenance of a road).

They are created after the PPP contract has been awarded –and thus have no previous track-record

In their capital structure lenders have usually much more weight than sponsors (ratios of 60%-40% or even 80%-20% are not uncommon).

SPVs are insulated from their parent companies: They are not for example affected by the bankruptcy of the parent company, or the parent company is not responsible for the SPV’s debt.

A project is “bankable” when, thanks to analysis and studies, it is capable of convincing lenders to make a loan to the SPV. Lenders take several aspects into consideration when analyzing projects, aspects related with the expected return (that depends on future cash flows) and the project risks. Lenders will study every aspect of the project to make sure it is a safe bet. They will then make a decision of whether or not they want to put money into it, how much should they charge (that is, what should be the interest rate) and how much money are they willing to lend. Project preparation is crucial to help a project be bankable: a realistic operative, economic and financial plan, a balanced risk allocation, and above all the certainty (bear in mind that nothing is 100% sure) that the cash flows will be enough to re-pay lenders, even should some contingencies arise. It should be pointed out that lenders’ expectations can be very volatile – this means that a project that is bankable at one point in time may suddenly become un-bankable because lenders are no longer sure they will get their money back and ask for more guarantees (this can happen for instance if a similar PPP in the region goes bankrupt and lenders experience losses). These additional guarantees can sometimes be beyond those offered by the SPV in traditional “Project Finance” schemes – guarantees that the lenders will put more money into the SPV under certain circumstances, or that the public sector will pay them back if the project fails for instance.

CDIA’s Short PPP Training for Facilitators 26

Box 7: Example of bankability and capital structure. Alandur Sewerage Project

The Alandur Sewerage Project was the first sewerage system and waste water treatment facility developed in India as a PPP project.

This project managed to obtain a loan from private sector financial institutions amounting to 59% of the capital needs – the project was thus bankable.

The project’s capital structure was the following:

Equity 12%

Term loan 59%

Public contribution 29%

Said Public contribution refers to one-time deposits in the form of connection charges collected from the citizens prior to the construction.

It should be noted that lenders are paid BEFORE sponsors, thus reducing effectively the risk they assume.

8 VALUE FOR MONEY

Trainer suggested readings

• “CDIA PPP Guide for Municipalities,” City Development Initiative Asia, June 2010. Section 2.3 “Value for money” – the many advantages of PPPs (page 7) • “Public-Private Partnerships Reference Guide, Version 1.0”, PPIAF, 2012 Section 3.2.3 Assessing Value for Money (page 138) • “The Guide to Guidance”. EPEC, 2011 Section 1.2.4 Value for money analysis (page 12)

In order to decide if a project should be developed as a PPP, the local authority should first find out if the infrastructure project itself is sound. Value for money is a practical way of deciding whether a project should be procured by means of a PPP agreement or using a different type of procurement agreement In any way, it does not replace the project pre-feasibility and feasibility studies that should be carried out simultaneously if they are considered necessary1. Obtaining Value for Money in a certain project means achieving the optimal combination of benefits and costs when delivering the expected facility or service, once we have stated that said investment has a positive impact in the city development.

1 For more information about feasibility analysis for urban development projects please refer to CDIA Pre-

Feasibility Study Guidelines and CDIA City Infrastructure Investment Programming & Prioritisation Toolkit. Obviously the procurement alternative affects the feasibility study. Feasibility and Value for Money analysis are usually developed simultaneously following an interactive methodology.

CDIA’s Short PPP Training for Facilitators 27

CDIA’s PPP Guide for Municipalities includes a very intuitive definition of the concept base on comparing the potential advantages provided by PPP procurement and those linked to traditional direct procurement.

Figure 5. Value for Money

This definition helps understanding how Value for Money can be analyzed, that is by comparing the advantages provide by each possible procurement alternative. Also it must not be forgotten that usually there is not a single PPP procurement option but several ones. Thus Value for Money analysis can also help finding out which PPP procurement option suits a certain project better. Most of the advantages provided by both PPP procurement and direct procurement are difficult to measure in a way they can be compare with each other. There are several approaches to measuring and compare Value for Money. All of them are either quantitative assessment, qualitative assessment or a mixture of both. 8.1 Quantitative value for money assessment

The most common and widely used tool for Value for Money quantitative analysis is the Public Sector Comparator (PSC)2. The PSC is based on comparing the fiscal cost of the PPP procurement option with that of the traditional public procurement option. In some regards PPP procurement is superior to the PSC, and in others not.

Trainer instruction Box 8

The objective of this box is to point out in which aspects PPP procurement is more economically efficient than traditional procurement alternatives, and the complexity of PSC analysis. After solving the box, ask participants if they think they could efficiently measure the costs detailed when analyzing a potential PPP project.

2 PSC was originally developed in the United Kingdom for the assessment of the Private Finance Initiative

program in the early 1990s.

CDIA’s Short PPP Training for Facilitators 28

Box 8: Is PPP procurement superior to the PSC?

For the following cost items in a project, is PPP procurement cheaper than the PSC?

Transaction cost

Yes No PPP procurement involves additional preparation and effort (external advisors…)

Investment cost

Yes No The private partner will tend to minimize investment needs and will not be able to take advantage of project mistakes and deficiencies.

Operating cost

Yes No The concession company will take operation costs into consideration when designing the infrastructure in a more efficient way than the authority or a private designer.

Overseeing by the Authority

Yes No Supervision needs to be more efficient in PPP projects, as they tend to transfer wider management and decision making responsibilities.

Maintenance cost

Yes No As in operating costs

Financing cost

Yes No Since the private partners are bearing more risks, they will also demand a higher remuneration which will result in higher financing costs.

In some occasions, there will be no public procurement option for a project. That is the case if the city has public indebtedness constrains. In other cases PPP procurement may have previously proved to be a more (or less) efficient way of procurement for a certain type of services in a certain type of cities, such as public waste management. In those cases there may be no real need to carry out a complex quantitative value for money assessment. This type of analysis requires specific expertise on a Public Administration or its consultants, which is not always available. Quantitative value for money analysis are extremely complex, costly and of dubious efficiency. Thus, they may not always be needed or worth the cost. 8.2 Qualitative value for money assessment

Besides the financial benefits that quantitative Value for Money Analysis tries to reflect, a PPP project can provide important benefits and costs that are hard to measure.

Trainer instruction Box 9

The objective of this box is to understand what kind of benefits and costs are analyzed in a quantitative value for money analysis.

CDIA’s Short PPP Training for Facilitators 29

Projects may provide other benefits and suffer other costs as seen in the box below. The box should be considered a non-exhaustive list.

Box 9: Are the benefits-costs easy to measure?

Identify in the following chart, for the proposed infrastructure, the financial and non-financial benefits and costs (regardless of procurement alternative).

Source: EPEC, “The non-financial benefits of PPPs”.

Are those benefits and costs easy or hard to quantify?

Amongst the most important non-financial benefits of PPP procurement are the following: Accelerated delivery: Projects can be brought forward in time when using a PPP procurement alternative. The reasons behind are:

- Transfer of construction risk to the private sector: When the construction risk is correctly transferred to the private sector, construction delays are usually assumed by the SPV’s sponsors – “no service – no payment”.

- Non-reliance on public funding: Since PPPs are financed thanks to private sector funding they do not need to wait for an opening in the public budget.

- Enhanced delivery: This refers to the enhanced quality of the infrastructure and associated services delivered. There are three reasons why PPP procurement can enhance procurement:

- Applied life-cycle approach and assured maintenance: The project is analyzed in a wide time-frame, encompassing the construction and the operation and maintenance phases. This helps to better assess the real cost of the project and prepare for it.

- Transfer of operation and maintenance risk: PPP projects usually involved a clear definition of expected quality standards to be delivered by the private sector, ways to measure them, and the penalties (or bonuses) to be applied in case they are not reached (or surpassed).

Financial benefits

Financial costs Non-financial benefits Non-financial costs

Roads Toll revenues Capital and maintenance

costs

Time savings Reduced accident

costs

Noise and pollution from

generated traffic Light rail

Fare-box revenues

Capital and maintenance

costs

Reduced commuter time

Congestion during

construction Prisons

Reduced revenue costs

Capital and maintenance

costs

Less overcrowding No rioting

Improved security

Local property prices

Schools Energy cost

savings

Capital and maintenance

costs

Improved educational outcomes

Increased congestion

around schools

CDIA’s Short PPP Training for Facilitators 30

- Strict governance structure: As compared to more traditional procurement alternatives, PPP projects have not only the Local Authorities but at least the sponsors and the lenders to keep an eye on the project. This can result in better management.

- Wider-social impacts: The benefits associated with PPP procurement can affect non-users as well as users of the infrastructure and related services. Some examples are the increased capacities developed by Local Authorities to implement these complex projects, the development of business opportunities for domestic companies, public funds are stretched further allowing other projects to be carried out…

These benefits are difficult to quantify but can be very important nevertheless. Qualitative value for money assessments can be very helpful pointing out these benefits. Qualitative value for money assessment can thus be an alternative or a complement to quantitative analysis.

9 MAKING PROJECTS ATTRACTIVE

Trainer suggested readings

• “CDIA PPP Guide for Municipalities,” City Development Initiative Asia, June 2010. Section 6.2 How would potential investors view the project? (page 14) • “Public-Private Partnership Handbook”, ADB, 2008. Section 3.6 Stakeholder Consultation (page 20) Section 6.7 Stakeholder Involvement (page 67) • “Public-Private Partnerships Reference Guide, Version 1.0”, PPIAF, 2012 Section 3.2.2 Assessing Commercial Viability (page 137)

Successful PPP urban development projects rely, to a large extent, in the ability of local authorities to develop an attractive project. Private sponsors cannot be forced to participate on a certain PPP, but rather must be persuade. If enough qualified private companies are willing to participate in the project as sponsors and financiers, the project can face the tendering and execution phases with confidence: It is easier to select the desired bidder among a large amount of qualified tenderers. A competitive tendering process usually results on lower project costs and a more robust agreement. Project supervision and monitoring tasks are normally eased and less problematic with the right sponsors and financiers. But what must the local authority or city government do in order to develop attractive projects? Let’s try to step into the private sponsor’s shoes and focus on some of the key elements they may consider, and what the Local Authorities can do to help:

Cost of analyzing the opportunity: For a private company to study a PPP project and to enter the bidding process can have very important costs. The Local Authorities should do their best to lower these costs as much as possible, preparing and facilitating relevant information, presented in a professional way and mistake free. Also, potential bidders must be certain that if they present a good offer they have possibilities of winning (they will not be “cheated out”).

CDIA’s Short PPP Training for Facilitators 31

Uncertainties: Uncertainties are aspects of the project that are not defined, or situations and events that may have a very negative impact on the project but that are difficult to quantify (as opposed to risk, which can be measured and priced). Local Authorities should make the project uncertainty-free.

Risk allocation: Can the sponsors manage effectively the risks that Local Authorities want to assign them? If not, they will either refuse to bid, or put such a high price to the project that it may not be affordable for the Local Authorities or users.

Remuneration: Sponsors are willing to participate into a PPP to make money. The higher the risks they assume, the more money they will demand. If too little compensation is offered by Local Authorities, then most likely they will not be interested.

Bankability: Even if all the above requirements are met, sponsors still need to convince lenders to give them money. The project must be attractive not only to sponsors, but to lenders as well (as described in a previous chapter).

Trainer instruction Box 10

The objective of this box is to make participants conscious of the many different problems a project can face in order to attract private interest and to teach them how to face said problems in a constructive way.

Participants may realize that problems often have to do with the efficiency and capacity of the public administration and the lack of commitment of the involved or affected stakeholders. The exercise can lead to a discussion, preferably related to said topic.

Box 10: Parking in Medolang: Making the project attractive

Please refer to the “Parking in Medolang” case study.

After adopting the decision to use a PPP as a procurement alternative for the parking, the following issues have been identified:

Medolang Municipal Government has a reputation for awarding contracts to four local contractors, without a transparent tendering process.

Establishing a public, transparent and non-discriminatory procedure is crucial. Involving a Multilateral agency to ensure the tendering is fair could be a strong guarantee for potential bidders.

The parking lies on terrains that belong to the Local Authorities, but which are currently occupied by a public school.

Having clear plans about where will the public school be transferred, when and how is the project going to be financed seems necessary. Public commitment from local authorities is a plus.

There are elections coming up in two years, and the opposition party has shown its discontent with this project.

The opposition party needs to be boarded into the project. Consult with them to understand their issues and how the project could be modified to find a solution.

There was an earthquake five years ago that destroyed several buildings.

Local authorities need to assume force-majeure risks, or else require the concession company to insure against this risk and include the cost of said insurance in the PPPs financial plan.

CDIA’s Short PPP Training for Facilitators 32

Some neighbors, which will be affected by the project in several ways, are very well organized. In the past they’ve organized many public acts and manifestations, even forcing the city major to reconsider some of the decisions already taken

Have these citizens manifest their concerns about the project in the public consultation stage. Have a meeting with them to point out the project’s advantages.

How can these issues be overcome to make the project attractive?

CDIA’s Short PPP Training for Facilitators 33

PART 2

A P P R O A C H

CDIA’s Short PPP Training for Facilitators 34

SESSION 4

APPROACH I

CDIA’s Short PPP Training for Facilitators 35

CDIA’s Short PPP Training for Facilitators 36

Trainer general instructions

This session is devoted to showing examples of PPP projects. It should not be consider as an exhaustive list of sectors and projects in which PPP can be applied. The objective is to pass on to participants the idea that PPP is a flexible procurement option that can be used for almost any kind of PPP project, not just for the ones listed here. Some other important ideas are: • Similar projects in similar countries are always a useful reference, but each project is unique, especially when we are talking about PPP projects. It is not recommended to copy project structure due to the complexity of PPP procurement. • If you are not a PPP expert, do not try to be too innovative at the beginning. It is recommended to start to use PPP with simple projects that have already worked in the country or the region, and to develop them in a similar way, taking local circumstances into consideration. • Similar projects have common features and you should know them. Reviewing successful projects is useful, but reviewing unsuccessful projects can be even more useful, as similar projects tend to fail due to the same kind of problems. • There are some types of risks that private partners fear the most, such as expropriation or demand risk. Even experienced administration fail to manage such risks correctly so you must be especially careful with projects involving these kinds of risks, such as urban transport projects.

10 TYPES OF URBAN PPP PROJECTS

Trainer suggested readings

• “CDIA PPP Guide for Municipalities,” City Development Initiative Asia, June 2010. Section 5: In what sectors can PPPs be applied? (page 12) • “Public-Private Partnership Handbook”, ADB, 2008. Section 1: Specific Pro-Poor Activities in PPPs (page 81) • “Public-Private Partnerships in Housing and Urban Development”, United Nations Human

Settlements Program, 2011. Chapter 11: Patterns in applying the PPP model to housing and urban development

(page 22) • “Cities PPPs”, Handshake #4, International Finance Corporation, 2012. Public Transport (page 40) and Urban water (page 54)

PPPs are a very powerful and flexible procurement alternative. As such, there are many different types of PPPs which can, in turn, be applied to many sectors.

In this chapter we shall explore these two aspects.

10.1 Types of PPPs

PPP contracts were originally applied in projects where users paid tariffs or tolls generating enough return for the investments made. This is the case of a toll road.

Later on, they were applied in projects where the Public Authority assumed payment obligations on behalf of the users, known as “shadow toll”. This was due to the fact that sometimes citizens have a limited payment capacity, but the project generates benefits to society that justify the public resources that are allocated (such is the case, for instance, of many public transportation systems like subways).

CDIA’s Short PPP Training for Facilitators 37

In both cases payments are linked to the usage of the infrastructure or service provided and revenues are determined by the usage, which is related to the performance of the private partner as operator.

PFI is another kind of PPP contractual scheme3, where the Public Authority assumes repayment obligations based on prefixed project milestones and/or performance standards. This allows extending the scope of PPP agreements to a wider range of sectors (like public buildings to host administrative offices).

In summary, and just to illustrate the flexibility of PPP procurement, we’ve pointed out the different types of PPPs one can have considering:

If sponsors assume demand risk, or are paid a fixed amount (minus penalties) depending on the quality of services provided.

If sponsors are paid by the citizens or Local Authorities

10.2 Sectors where PPPs can be applied

Almost any urban infrastructure project could be developed under a PPP modality in a more or less creative way; legal restrictions being the ultimate boundary.

Each urban infrastructure sector has, however, its own characteristics, opportunities and challenges. PPPs are easier to implement in some sectors than in others, depending on social, economic and financial parameters. For instance, the PPP will need to clearly define in a simple way, easy to verify, some quality parameters – this can be easily done in a road project, but is much more complex in a hospital project.

Broadly speaking, PPPs can be categorized in three different sectors: Transportation, Utilities and Services. As a reference we enclose a table with different kinds of projects for which PPPs have been used within each sector category:

Transportation Utilities Services

Roads & Bridges

Rails (urban and non-urban)

Ferries

Bus Rapid Transit

Transport hubs and terminals

Ports

Airports

Water treatment and distribution

Sewage system and wastewater treatment

Solid waste treatment

Power generation and distribution

Central heating and cooling systems

Hospitals and jails

City government offices

Sports facilities and auditoriums

Police and fire stations

Libraries

Schools and University dormitories

We will review these sectors and their characteristics in the following chapters, with a special focus on the urban environment.

3 Private Finance Initiative (PFI) developed initially by the governments of Australia and United Kingdom in the

1990s.

CDIA’s Short PPP Training for Facilitators 38

10.2.1 Urban Transport

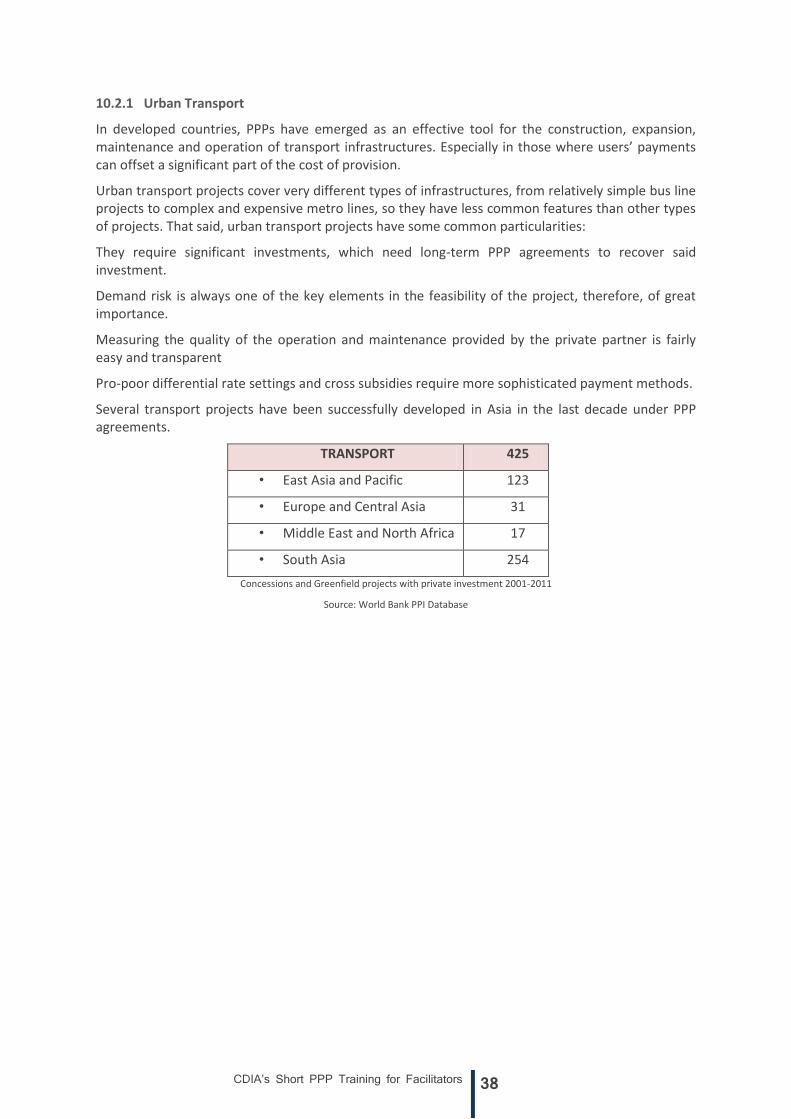

In developed countries, PPPs have emerged as an effective tool for the construction, expansion, maintenance and operation of transport infrastructures. Especially in those where users’ payments can offset a significant part of the cost of provision.