basic calculation - asppa > news calculation 2 basic calculation –pre 62 –the limit at any...

TRANSCRIPT

1

2014 Actuarial Symposium

Session 3: IRS Section 415

Limitations on Defined

Benefit Plans

James E. Holland, Jr.Cheiron, Inc.

Thomas J. FinneganThe Savitz Organization

August 15, 2014

5178448v3

Basic Calculation

2

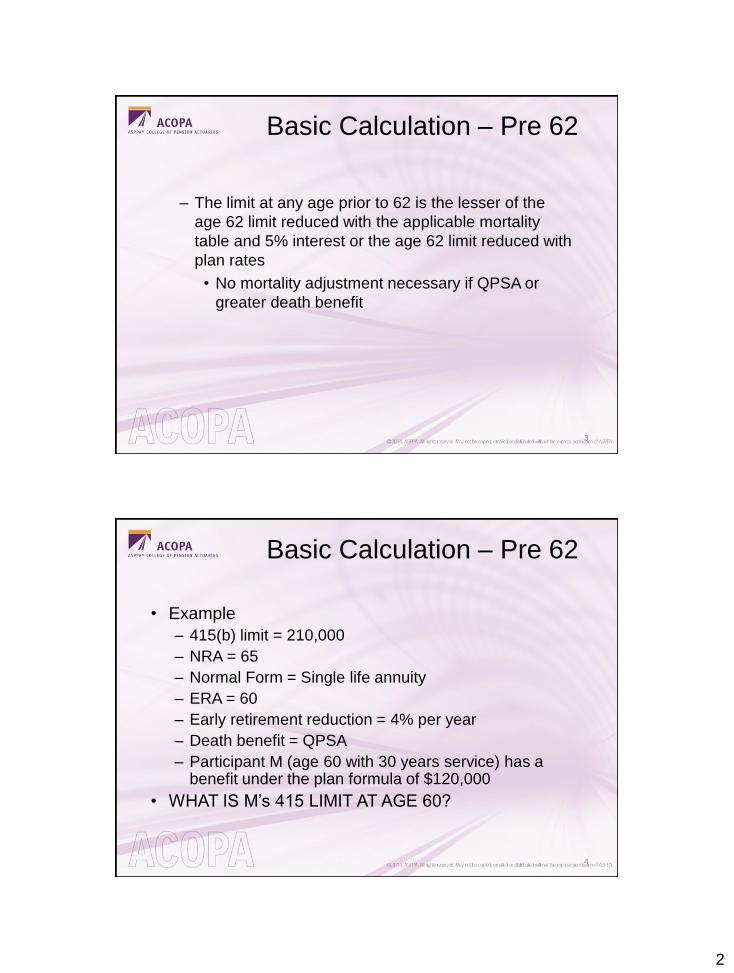

Basic Calculation – Pre 62

– The limit at any age prior to 62 is the lesser of the

age 62 limit reduced with the applicable mortality

table and 5% interest or the age 62 limit reduced with

plan rates

• No mortality adjustment necessary if QPSA or

greater death benefit

3

Basic Calculation – Pre 62

• Example

– 415(b) limit = 210,000

– NRA = 65

– Normal Form = Single life annuity

– ERA = 60

– Early retirement reduction = 4% per year

– Death benefit = QPSA

– Participant M (age 60 with 30 years service) has a benefit under the plan formula of $120,000

• WHAT IS M’s 415 LIMIT AT AGE 60?

4

3

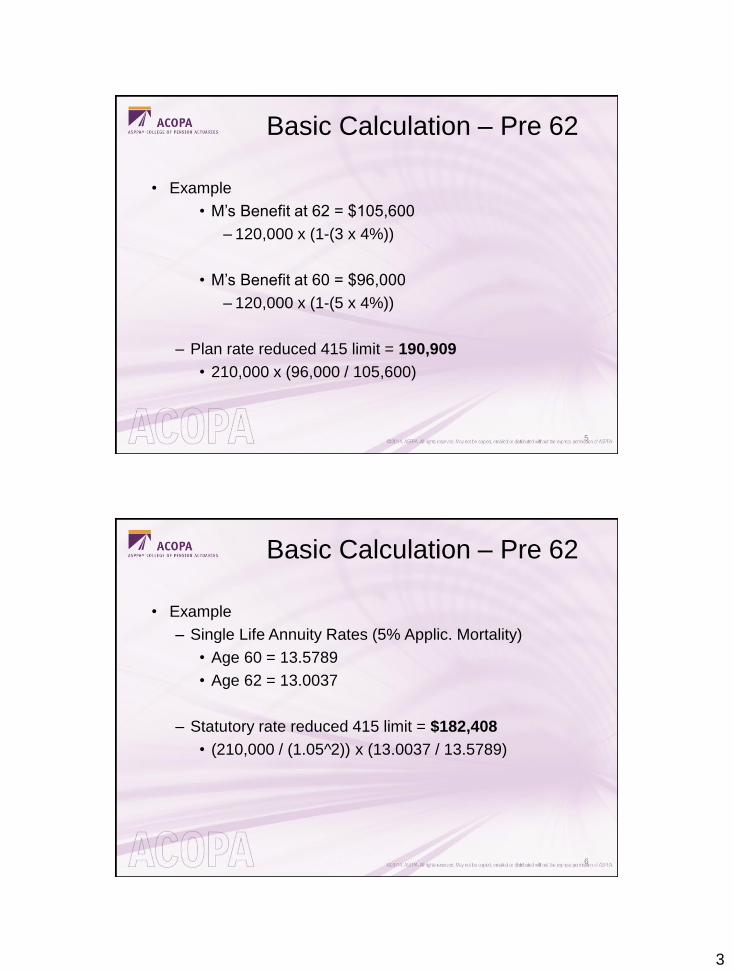

Basic Calculation – Pre 62

• Example

• M’s Benefit at 62 = $105,600

– 120,000 x (1-(3 x 4%))

• M’s Benefit at 60 = $96,000

– 120,000 x (1-(5 x 4%))

– Plan rate reduced 415 limit = 190,909

• 210,000 x (96,000 / 105,600)

5

Basic Calculation – Pre 62

• Example

– Single Life Annuity Rates (5% Applic. Mortality)

• Age 60 = 13.5789

• Age 62 = 13.0037

– Statutory rate reduced 415 limit = $182,408

• (210,000 / (1.05^2)) x (13.0037 / 13.5789)

6

4

Basic Calculation – Pre 62

• Example

– Age 60 415 limit is the lesser of

• Plan rate reduced 415 limit = 190,909

• Statutory rate reduced 415 limit = 182,408

• $182,408

7

Effect of ERFs

• Z’s benefit by plan formula is well in excess of $210,000

• Z is retiring at age 62 with 15 years plan participation

• All other provisions the same

– 415(b) limit = 210,000

– NRA = 65

– Normal Form = Single life annuity

– ERA = 60

– Early retirement reduction = 4% per year

– Death benefit = QPSA

8

5

Effect of ERFs

• What is Z’s 415 limit at age 62?

– The 415(b) limit at age 62 is the same as the 415(b)

limit at age 65…..$210,000

• What is the maximum benefit the plan can Z at age 62?

– Post 2007 415 regs the plan must limit the accrued

benefit (as opposed to just the benefit payable) to the

415(b) limit or $210,000 as a life annuity at 65

– The plan reduces benefits payable at age 62 by 12%

– The benefit payable at age 62 is $184,800

• 210,000 x .88 = 184,800 (less than the 415 limit)

• Not all agree, but IRS Gray Book

9

Effect of ERFs

• What if the plan said that Z, or people at the 415 limit, get

unreduced benefits at 62?

– Z can be paid a 210,000 benefit at 62

– Assuming Z is the sole participant, no problems

– But our example had M receiving reduced ER benefits

– If different early retirement factors apply to different

groups, each of the sets of factors is subject to BeRF

testing

– A group covering a single HCE is discriminatory

• A group covering those at the 415 limit is almost

certainly discriminatory

10

6

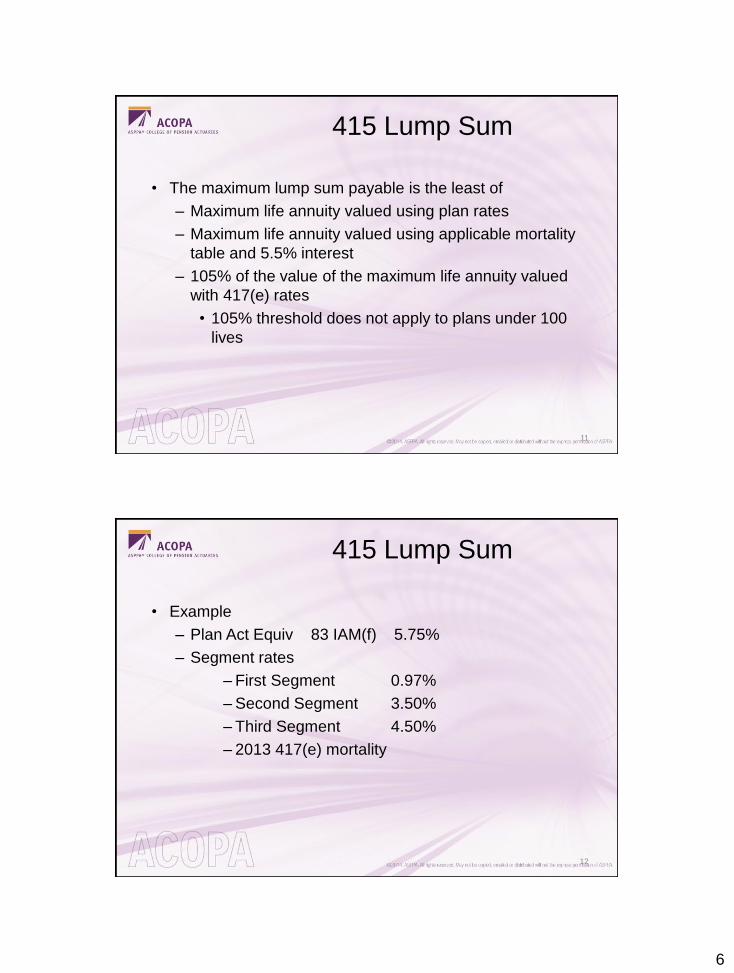

415 Lump Sum

• The maximum lump sum payable is the least of

– Maximum life annuity valued using plan rates

– Maximum life annuity valued using applicable mortality

table and 5.5% interest

– 105% of the value of the maximum life annuity valued

with 417(e) rates

• 105% threshold does not apply to plans under 100

lives

11

415 Lump Sum

• Example

– Plan Act Equiv 83 IAM(f) 5.75%

– Segment rates

– First Segment 0.97%

– Second Segment 3.50%

– Third Segment 4.50%

– 2013 417(e) mortality

12

7

415 Lump Sum

• Example

• Plan Act Equiv

• 83 IAM(f) 5.75% APR = 13.1323

• Applicable Mortality 5.5% APR = 12.6409

• 1st Segment (0.97%)

– N60=11522489; N65=8927518; D60=538633

• 2nd Segment (3.50%)

– N65=1379128; N80=324922; D60=122015

• Third Segment (4.50%)

– N80=142890; D60=68526

13

415 Lump Sum

• Example

• Value of maximum benefit

– Plan rates

• 182,408 x 13.1323= 2,395,437

– Applicable Mortality and 5.5%

• 182,408 x 12.6409= 2,305,801

14

8

415 Lump Sum

• Example

• Value of maximum benefit

– First segment piece

• 182,408 x (N60-N65) / D60 =

• 182,408 x (11522489 – 8927518) / 538633 =

• 878,787

– Second segment piece

• 182,408 x (N65-N80) / D60 =

• 182,408 x (1379128-324922) / 122015 =

• 1,575,999

15

415 Lump Sum

• Example

• Value of maximum benefit

– Third segment piece

• 182,408 x N80 / D60 =

• 182,408 x 142890 / 68526 =

• 380,356

16

9

415 Lump Sum

• Example

• Value of maximum benefit

– 417(e) max benefit value

• 878,787 + 1,575,999 + 380,356 = 2,835,142

– 105% of 417(e) value

• 2,835,142 x 1.05 = 2,976,899

17

415 Lump Sum

• Example

• Max lump sum

– Least of

• Plan rates 2,395,437

• Applic Mortality 5.5% 2,305,801

• 105% of 417(e) result 2,976,899

18

10

Employee Contributions

Employee Contributions

• In general, the annual benefit attributable to after-tax

employee contributions is not included in the annual

benefit for § 415(b) purposes.

• The benefit attributable to mandatory contributions is

calculated and excluded.

• Voluntary contributions are treated as separate defined

contribution plan and is subject to the DC plan limits

11

Employee Contributions

• Employee contributions does not include contributions

that are “picked-up” by a governmental employer pursuant

to IRC § 414(h)(2).

• Also, employee contributions do not include certain

repayments of loans, withdrawn employee contributions,

or previously distributed amounts.

Employee Contributions

• Annual benefit attributable to mandatory employee

contributions is

– Determined using the rules of § 411(c)(2) and §

1.411(c)-1(c)(4).

– If plan provides a higher benefit, then excess is

included in benefit to be tested.

– § 411(c)(2) rules used even if plan is not subject to that

section (such as a governmental plan).

12

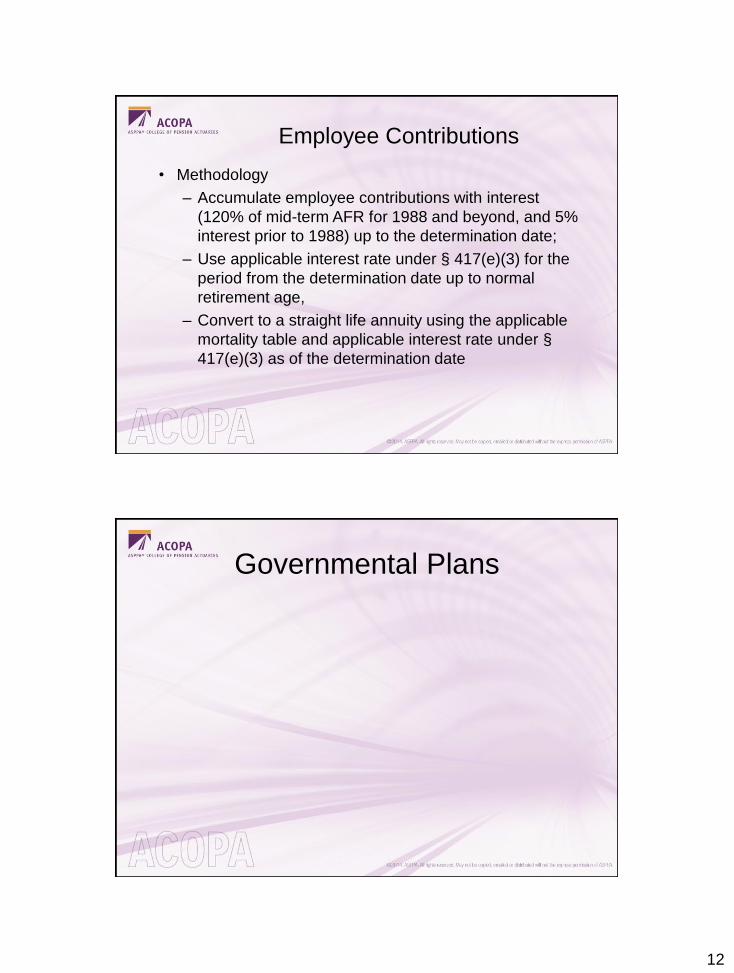

Employee Contributions

• Methodology

– Accumulate employee contributions with interest

(120% of mid-term AFR for 1988 and beyond, and 5%

interest prior to 1988) up to the determination date;

– Use applicable interest rate under § 417(e)(3) for the

period from the determination date up to normal

retirement age,

– Convert to a straight life annuity using the applicable

mortality table and applicable interest rate under §

417(e)(3) as of the determination date

Governmental Plans

13

Governmental Plans

• Generally, same limitation apply as for private sector plans

• However, some special rules

– Accrued benefit does not need to be limited but benefit

payable does (no 411(d)(6) protection for governmental

plans)

• So Z from earlier example could get full 210,000

benefit at age 62 regardless of plan ERFs between

65 and 62

Governmental Plans

• Form adjustment uses the same rules

• Note preamble language

– Section 415(b)(2)(E) applies based on the form of the

benefit, and not the status of the plan, and therefore

the final regulations provide that these rules also apply

to plans that are not subject to the requirements of

section 417.

14

Governmental Plans

• Special rules

– 100% compensation limit does not apply

– No reduction in dollar limit for commencement before age

62 for a “qualified participant” who is a participant

• In a DB maintained by a State, Indian tribal govt., or

any political subdivision thereof with respect to whom

the service taken into account includes at least 15

years as

– A full-time employee of a police or fire department,

or

– As a member of Armed Forces of the United States

Governmental Plans

• Special Rules – (cont.)

– Reduction for commencement below age 62, or for

less than 10 years of service or participation do not

apply to annuity benefit

• payable on account of disability by reason of

personal injuries or sickness, or

• received by a beneficiary on account of death.

15

Governmental Plans

• Special Rules – (cont.)

– Grandfather election - For a participant who

commenced participation in a governmental plan

before 1/1/1990, the limitation shall not be less than

the AB under the plan determined without regard to

any amendment after October 14, 1987.

– Election prior to 1990 plan year.

Governmental Plans

• Special Rules – (cont.)

– Purchase of service credit under § 415(n)

• Employee contribution to buy “permissive service

credit” either meets DC rules or benefit purchased

treated as provided by Employer and tested under

DB rules.

• May include up to 5 years of “air time” or other

nonqualified service, once has 5 years of

participation.

• Limits of 5 years of nonqualified service credit do

not apply for transfer subject to 403(b)(13)(A) or

457(e)(17)(A) plan.

16

Adjustments for QJSA

Adjustments for QJSA

• No adjustment for benefit paid to surviving spouse in a

QJSA

• If combined form, then adjustment for other death benefits

or features but not for survivor annuity to surviving spouse

• Example – Plan provides a joint and survivor benefit with

a 10-year certain feature. Adjustment is made for the 10-

year certain feature, but no adjustment made for the

benefit to the surviving spouse.

17

Adjustments for QJSA

• Example – Plan provides a joint and survivor benefit with a 10-year certain feature. Adjustment is made for the 10-year certain feature, but no adjustment made for the benefit to the surviving spouse.

– Same result would obtain if joint and survivor benefit included features such as cash refund (of employee contributions) or a “pop-up” upon death of spouse. (See Q&A 30 of 2014 EA Gray Book with respect to “pop-up.”)

• Example – lump sum plus QJSA on remaining annuity

– Lump sum adjusted under lump sum rules

– QJSA adjusted under annuity rules so that survivor annuity not taken into account

§ 401(a)(17) Application

18

§ 401(a)(17) Application

• Old Law

– The compensation limit under Section 401(a)(17) of

the Code applied for purposes of nondiscrimination

and benefit determination

– It did not apply for purposes of determining the 100%

of pay 415 limit

– The 100% of pay limit applies at any age to any form,

it is NOT increased for delayed commencement

35

§ 401(a)(17) Application

• 2007 Final Regulation

– The compensation limit under Section 401(a)(17) of

the Code applies for purposes of determining the

100% of pay 415 limit

36

19

§ 401(a)(17) Application

• Impact on older employees

– The primary impact of the application of the 401(a)(17) limit for 415 purposes will be the elimination of most of the adjustment to 415 for deferral of benefit commencement past age 65

– Under current law the 415(b) limitation is adjusted if benefit commencement is beyond age 65

• The adjustment is made using the lesser of the plan’s interest rate or 5%

• Because the 415 and 401(a)(17) limits are so close, the elimination of the deferred commencement adjustment occurs at age 68

37

§ 401(a)(17) Application-2014(** 255,000 is the average of 250,000; 255,000 and 260,000)

Age Prior Law Final Reg

62 205,000 205,000

63 205,000 205,000

64 205,000 205,000

65 205,000 205,000

66 220,882 220,882

67 238,192 238,192

68 257,121 255,000**

69 277,903 255,000**

70 300,791 255,000**

20

§ 401(a)(17) Application-2014

• What happens if benefits do not start at age 68, and no

suspension?

• Cannot forfeit, and cannot pay more than $255,000.

• Can self-correct. (See Q&A 26 of 2014 EA Gray Book.)

39

§ 401(a)(17) Application

• Effective Date

– Limitation years beginning on or after 7/01/07

– Accrued benefits as of last day of limitation year prior to effective date, based on the plan as of 4/5/07, are grandfathered

– Calendar year plan grandfathers 12/31/07 accrued benefit based on plan as of 4/5/07

• Continued to accrue grandfathered benefits until 12/31

• Actuarial increases to grandfathered accrued benefits in accordance with the 4/5/07 plan doc are covered by grandfather

40

21

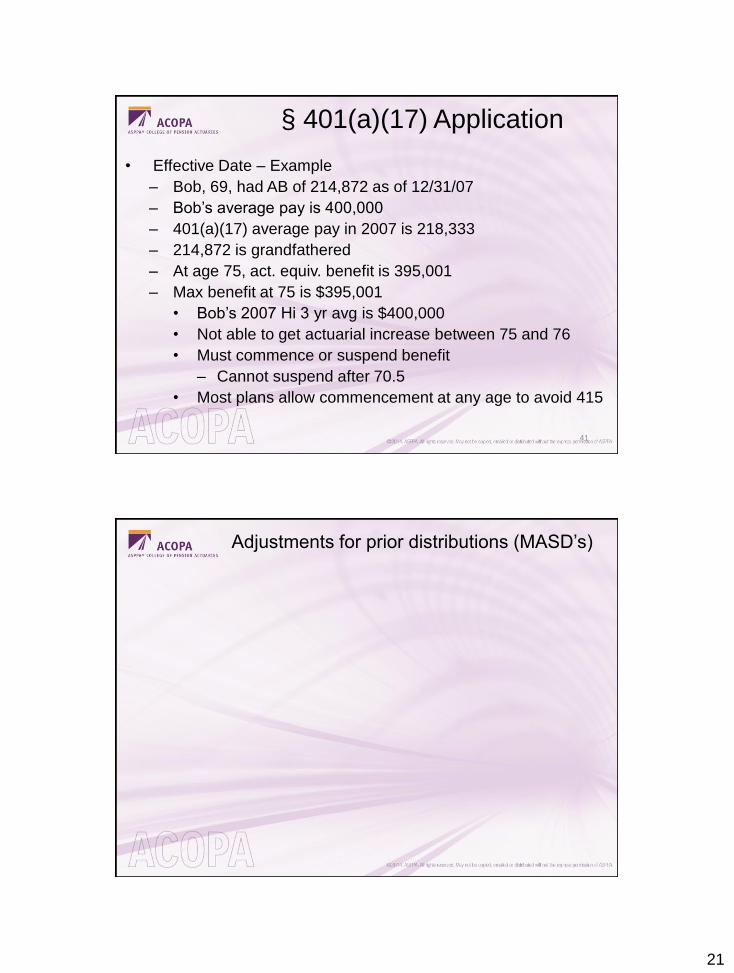

§ 401(a)(17) Application

• Effective Date – Example

– Bob, 69, had AB of 214,872 as of 12/31/07

– Bob’s average pay is 400,000

– 401(a)(17) average pay in 2007 is 218,333

– 214,872 is grandfathered

– At age 75, act. equiv. benefit is 395,001

– Max benefit at 75 is $395,001

• Bob’s 2007 Hi 3 yr avg is $400,000

• Not able to get actuarial increase between 75 and 76

• Must commence or suspend benefit

– Cannot suspend after 70.5

• Most plans allow commencement at any age to avoid 415

41

Adjustments for prior distributions (MASD’s)

22

Adjustments for prior distributions

(MASD’s)

– Common situations in which prior distributions occur:

• Divorce

• Required minimum distributions

• Distribution from a prior DB plan

• Rehired participants with a prior payout

• Elective partial distributions

• Changes to existing payment streams

– Changes in the Form of Benefit

– Additional accruals while still employed

– COLA’s

43

Adjustments for prior distributions

(MASD’s)

• Regulatory history

– Proposed § 415 regulations issued in 2005 contained proposed MASD rule.

• The proposed rules were not included in the final regulations.

– § 1.415(b)-1(b)(1)(iii) refers to overall need to adjust but lacks any detailed guidance and is essentially a good-faith standard.

• The detailed guidance is to be specified later in the reserved section 415(b)-2.

• COLA adjustments – have rules of their own, which can avoid MASD rules.

44

23

Adjustments for prior distributions

(MASD’s)

• There are generally 3 types of adjustment calcs:

– (1) Plan benefit adjustments

– Benefit limit adjustments

• (2) Dollar limit

• (3) Comp limit

• All three are different problems and must be considered separately.

• The proposed § 415 regs. made the mistake of lumping the dollar limit and comp limit calculations together.

45

Adjustments for prior distributions (MASD’s)

• Why are MASD adjustment calculations so problematic?

• Answer: Presence of Early Retirement Factors (or Late

Retirement Factors) that are not based on “normal” A.E.

• Quick Tip: if there are no ERF’s or LRF’s applicable, then

just use “normal” A.E. methods.

46

24

Adjustments for prior distributions (MASD’s)

Why it’s problemtic: MASD Example 1

• Plan has early retirement at age 62 with no reduction in benefit.

• A participant takes early retirement at age 62, but returns to work at age 65 and benefit payments cease.

• The participant then retires a second time after working a single day.

• The plan requires that benefits under the formula be reduced actuarially for prior distributions, as is typical.

• There will then be a substantial offset to the benefit payable at the 2nd (age 65) retirement, when common sense suggests there should not be, and that the age 62 benefit should continue.

47

Adjustments for prior distributions (MASD’s)

Why it’s problematic: MASD Example 2

• Suppose “normal” retirement at age 65

• Unreduced early retirement allowed between 62-65.

• Early Retirement Factor (ERF) = 1.0 for 62-65 only.

• Compare John, who takes an annuity at 62, and Bill, who takes partial distributions during 62-65 and then retires at 65.

• Bill and John are otherwise identical in every way.

• The plan requires that benefits under the formula be reduced actuarially for prior distributions, as is typical.

48

25

Adjustments for prior distributions (MASD’s)Why it’s problematic: MASD Example 2

John Life Annuity

Age 62 63 64 65 66 ----

Pmt $160K $160K $160K $160K $160K $160K

Bill Prior Distributions + Reduced Benefit

Age 62 63 64 65 66 ----

Pmt $100K $100K $100K <$160K <$160K <$160K

Adjustments for prior distributions (MASD’s)

Why it’s problematic: MASD Example 2 Notes

• Bill is treated unfairly relative to John.

– He gets less just because he has MASD’s.

– But nothing in the IRC says or implies that participants with prior distribs should be discriminated against.

• Plan of Example 2 is the maximum benefit “dollar” limit of IRC 415.

• The offset “error” can be as high as approx $500K for a single participant!

• Even larger errors possible for maximum “comp” limit

– (ERF = 1.0 for all ages)!

• Proposed 2005 IRS 415 Regs imposed such offsets (not included in final regulations).

50

26

MASD Problem Summary

• Counterintuitive, unreasonable results arise when “normal” actuarial equivalence is applied in the presence of early retirement factors.

• Early retirement factors impose their own actuarial equivalence structure.

• Ignoring this actuarial equivalence structure of early retirement factors leads to unequal treatment of participants.

• Not just a “fat cat” limit adjustment problem (consider 415 comp limit and plan benefit adjustments)

51

Adjustments for prior distributions (MASD’s)

How to do the calc

• Technical Resources:

– ASPPA Feb 2006 letter to IRS, Comments on Multiple Annuity Starting Dates

• Referred to hereafter as the “ASPPA approach”.

– ASPPA method gives a “pass/fail” answer and addresses 415 only.

– Does not determine “offset” amounts at points in time.

– Less technical than David MacLennan’s approach (next slide).

52

27

Adjustments for prior distributions

(MASD’s)

How to do the calc

• Technical Resources:

– Benefit Adjustments for Multiple Annuity Starting Dates

• Known as BERF = WERF approach

– Published 2007 in Journal of Pension Benefits

– Published Jan 2006 in SOA Pension Section News

– By David MacLennan

– Paper was awarded 2010 Hanson Memorial Prize, but has no official approval or recognition.

• Derives results from basic math principles

– addresses both 415 and plan offsets.

• Actual offset amount determined at different points in time (not just “pass/fail”).

53

Adjustments for prior distributions

(MASD’s)

How to do the calc

– David’s method and the ASPPA approach generally give answers consistent with each other.

54

28

Adjustments for prior distributions (MASD’s)

How to do the calc

• Presumably you could also use a method of your own during the “Interim” period

– Method must be reasonable and take into account prior and future payments

– Cannot permit make up for missed COLAs

• Note “normal” A.E. method will be grossly conservative if ERF’s are present.

– The adjustment “error” can be > $500,000

• should not be used when ERF’s are present, unless you just want to use it to arrive at a “pass” result.

• “Percentage Used” method also can be overly conservative

– Also not recommended unless you just use it to arrive at a “pass” result.

55

Adjustments for prior distributions (MASD’s)

How to do the calc (ASPPA approach)• ASPPA Method (from Feb 2006 Comment Ltr)

– Step 1: The entire stream of payments (including both the original payment stream and the revised payment, or stream of payments) must satisfy IRC § 415 as of the initial ASD (with appropriate adjustments for COLAs); and

– Step 2: As of each successor ASD, the payments to be made on or after such successor ASD must satisfy §415 as of the successor ASD.

– In other words, you test “prospectively” at each ASD. Simple, but the devil is in the details.

56

29

Adjustments for prior distributions (MASD’s)

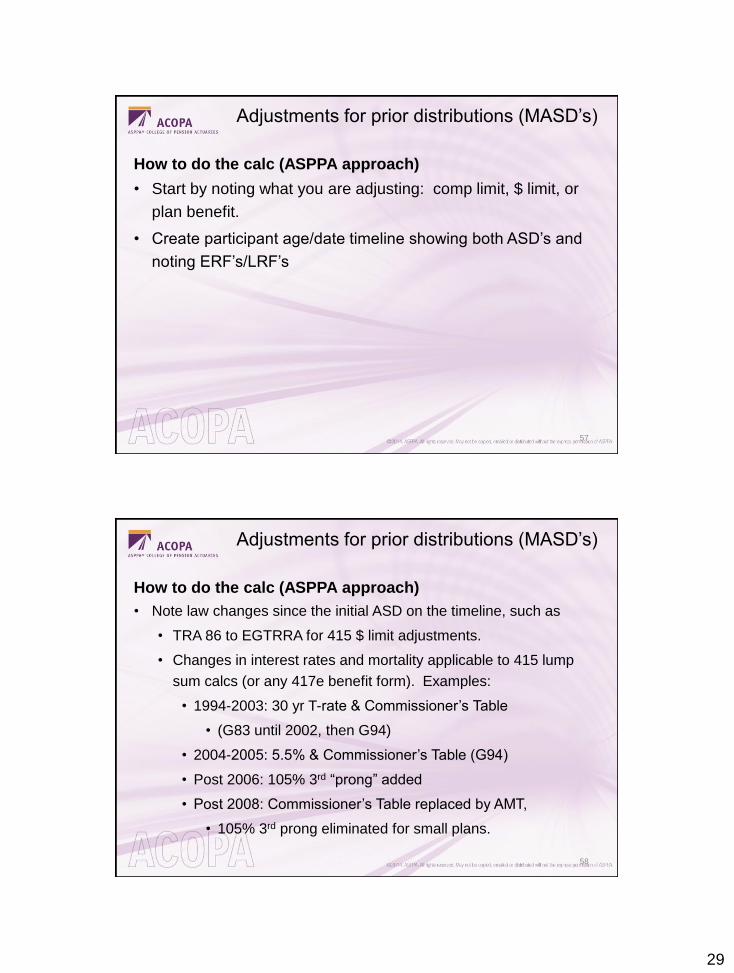

How to do the calc (ASPPA approach)

• Start by noting what you are adjusting: comp limit, $ limit, or

plan benefit.

• Create participant age/date timeline showing both ASD’s and

noting ERF’s/LRF’s

57

Adjustments for prior distributions (MASD’s)

How to do the calc (ASPPA approach)

• Note law changes since the initial ASD on the timeline, such as

• TRA 86 to EGTRRA for 415 $ limit adjustments.

• Changes in interest rates and mortality applicable to 415 lump

sum calcs (or any 417e benefit form). Examples:

• 1994-2003: 30 yr T-rate & Commissioner’s Table

• (G83 until 2002, then G94)

• 2004-2005: 5.5% & Commissioner’s Table (G94)

• Post 2006: 105% 3rd “prong” added

• Post 2008: Commissioner’s Table replaced by AMT,

• 105% 3rd prong eliminated for small plans.

58

30

Adjustments for prior distributions (MASD’s)

How to do the calc (ASPPA approach)

• “Normalize” lump-sums

• by converting to annuities

• reflecting applicable 415 lump sum interest and mortality

• see examples

• Assumptions:

• Use mortality discount only if payment would have been

forfeited upon death after ASD

• Use A.E. assumptions effective as of the ASD. Why?

Because otherwise the offset, and hence the statutory limit,

will not be definitely determinable. 59

Adjustments for prior distributions

(MASD’s)How to do the calculation (ASPPA approach)

Assumptions:

Example: if calculation involves a prior plan distribution,

apply the prior plan A.E. assumptions and 415 assumptions, effective as of the ASD, to the prior plan distribution.

Otherwise, the offset, and hence the 415 limit, cannot even be determined after the prior plan ASD because the adjusted 415 limit depends on the future plan’s A.E. and future § 417(e) rates!

60

31

Adjustments for prior distributions (MASD’s)

How to do the calc. (ASPPA approach) Example 1, Comp Limit

1st ASD: $200,000 lump sum at age 60 in 2003.

2nd ASD: $1,000,000 lump sum at age 67 in 2010.

Hi-3 AMC = $8,000

As of 1st ASD (2003), Plan A.E. was 5% I83F, lookback month is 5th

and stability period is plan year (so 30-yr T rate is 5.08%).

Normalize lump sums at different points in time to annuities

1st ASD: $200,000/157.79831 (Age 60 APR G94 5.08%) = $1,267.44/mo.

If plan A.E. 5% I83F age 60 APR was smaller, it would be used instead.

Note we are “going back in time” to do this calc and applying the 2003 rules.

2nd ASD: $1,000,000/131.52678 (Age 67 APR 5.5% 2010 AMT) = $7,603.01 (as above, 5% I83F APR is larger).

61

Adjustments for prior distributions (MASD’s)

How to do the calc (ASPPA approach)

Example 1, Comp Limit, Continued

Step 2 check @ 2nd ASD:

Determine whether a life annuity of $7603.01 meets the 415 limit

Clearly $7,603.01 is less than $8,000 Comp limit, so passes

62

32

Adjustments for prior distributions (MASD’s)

How to do the calc (ASPPA approach)

Example 1, Comp Limit, Continued

Step 1 check @ 1st ASD:

Determine whether a payment stream of $200,000 immediately and $1,000,000 at age 67 meets 415 limit at age 60

We need to determine equivalent annuity at age 60 of 2nd

ASD age 67 annuity using 2003 assumptions and statute.

Presumably 2010 lump-sum was not at risk of forfeiture on death during 2003-2010 so it must be discounted with interest only.

63

Adjustments for prior distributions (MASD’s)

How to do the calc (ASPPA approach)

Example 1, Comp Limit, Continued

Step 1 check @ 1st ASD (cont’d):

Plan A.E. adj (5% I83F):

$7,603.01 x 146.56073 / 169.85889 / (1.05)7 = $4,662.19

415 A.E. adj (5% G94):

$7,603.01 x 134.29164 / 159.00981 / (1.05)7 = $4,563.37

Taking the lesser amount above, the age 60 combined annuity attributable to the 2 lump-sum distributions is

$1,267.44 + $4,563.37 = $5,830.81.

Step 1 check passes, since $5,830.81 is less than $8,000 comp limit.

64

33

Adjustments for prior distributions

(MASD’s)

How to do the calc (ASPPA approach)

Example 1, Comp Limit, Continued

Notes on Example 1 Calc:

We could have known in advance that the Step 1 check would be a pass,

since the $200,000 lump sum in 2003 creates a temporary annuity between 60 and 67 that is much less than $8,000 ($64,000 annualized) comp limit.

Under the BERF = WERF method

Rather than discount the 2nd ASD age 67 annuity to age 60, the approach would be to determine the offset at age 67 due to the age 60 distribution

using whatever assumptions and statute are appropriate during the age 60-67 time period.

Depending on the assumptions chosen, these yield the same results.

65

Adjustments for prior distributions (MASD’s)

• Mary Ann is 63 years old as of 12/31/13.

• She has participated in a DB plan for the past 2 years.

• The plan calls for her to accrue the 415 dollar limit each yr

• NRA under the plan is age 62.

• The plan allows for in-service distributions on or after NRA.

• Actuarial Equivalency is 5½% 94GAR.

APRs: 62-145.47 63-142.27

D62=33676.03 D63=31669.96 D62/D63=1.063343

• For 2012, Mary Ann accrued the maximum benefit and

– She took a lump sum settlement of that benefit on 12/31/12

• ($1,666.67 x 145.47=$242,450).

34

Adjustments for prior distributions (MASD’s)

What is the maximum lump sum Mary Ann can take in 2013?

1. (2 x 1,708.33 x 142.27) – (242,250 x 1.055)=230,514

2. (2 x 1,708.33 - 1666.67) x 142.27 = 248.971

3. 1666.67 x 142.27 = 237,117

4. (2 x 1,708.33 x 142.27) – (242,250 x 1.063343) = 228,493

5. (2 x 1,708.33 - 1666.67) x 145.47 x 1.055 = 268,572

6. 1,708.33 x 142.27 = 243,044

And the winner is???

Adjustments for prior distributions (MASD’s)

• ASPPA comment letter on MASDs suggested

– 3 requirements for MASDs

• Entire payment stream must satisfy 415 limits as of

the first annuity starting date, including payments on

or after 2nd and later ASDs

• Payments on or after the 2nd ASD must satisfy 415

limits as of the 2nd ASD, including payments on or

after 3rd and later ASDs,

– but ignoring payments prior to 2nd ASD

• In above calcs, COLA’s are only recognized as they

occur

35

Adjustments for prior distributions (MASD’s)

What is the maximum lump sum Mary Ann can take in 2013?

1) (2 x 1,708.33 x 142.27) – (242,250 x 1.055)=230,514

• Satisfies 415

2) (2 x 1,708.33 - 1666.67) x 142.27 = 248.971

• Fails 415 at 2nd ASD

3) 1666.67 x 142.27 = 237,117

• Satisfies 415

4) (2 x 1,708.33 x 142.27) – (242,250 x 1.063343) = 228,493

• Satisfies 415

5) (2 x 1,708.33 - 1666.67) x 145.47 x 1.055 = 268,572

• Fails 415 at 2nd ASD

6) 1,708.33 x 142.27 = 243,044

• Max amount that satisfies 415 at 2nd ASD