banking the poor getting finance 2008 thailand launch the world bank november 2008

TRANSCRIPT

Banking the Poor Getting Finance 2008 Thailand Launch

The World Bank November 2008

2

Access to Banking Services

How many persons have access to banking services? What matters for access to banking services?

Reform oriented indicators - 54 countries Africa (35 countries) South and East Asia (6 and 8 countries), respectively, Central America (4 countries) and Mexico.

Survey Instruments 2 questionnaires: Commercial Banks and Central Banks

3

Numbers of Accounts Vary Widely…

Barely 9 bank accounts per 000 adults in Chad. Fewer than 35 accounts per 000 adults in Rwanda,

Liberia and Madagascar 550 accounts per 000 adults in South Africa, the richest

African county, with a per capita income more than tenfold that of Chad

But 2,010 accounts per 000 adults in Mauritius, the second richest country in Africa, which has the most financial access

1,352 accounts per 000 in Thailand (5th best), compared to 83 in Vietnam and 464 in Indonesia.

4

Main Measures Explored and Findings

1. Accounts per 000: income is a key factor

2. Complexity: documents to open an account, days to open

an account, loan application processes - associated with reduced access

3. Costs: opening charges, maintenance costs - recurring charges and complex fee structures matter

4. Quality and Convenience Features: enhance banking services for the already banked but are not likely to bring new entrants

5. Special Schemes – basic banking, special savings vehicles: – hard to find a measurable impact upon access

6. Mobile technology, retail payments services: increase convenience / depth

7. Transparency, information, institutions, competition: associated with better access

5

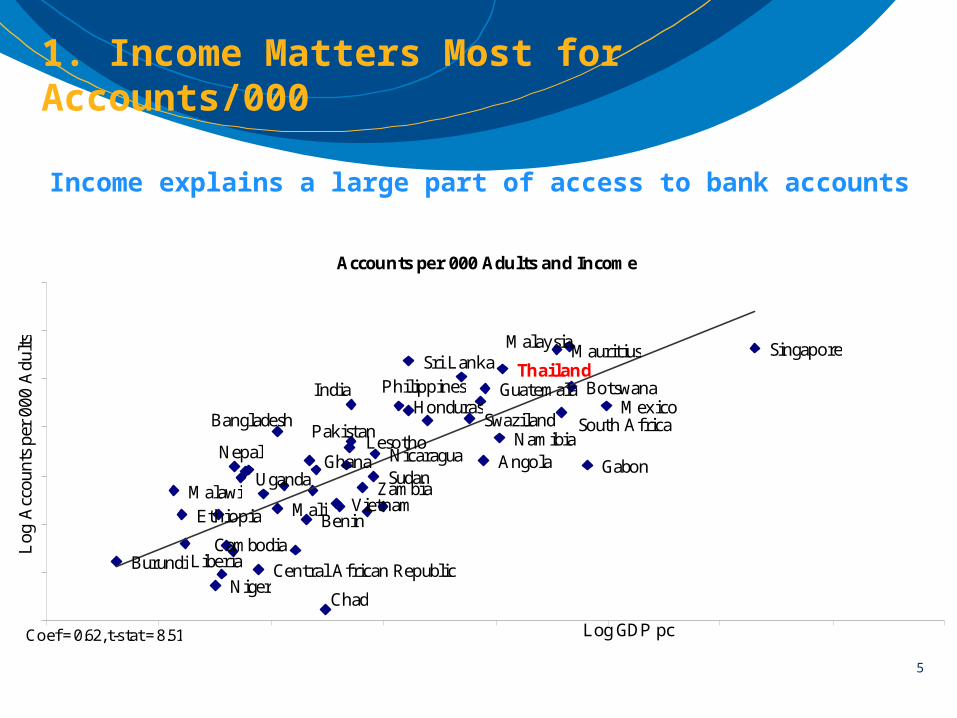

1. Income Matters Most for Accounts/000

Income explains a large part of access to bank accounts

Accounts per 000 Adults and Income

Philippines

NepalNamibia

Malawi

Lesotho

Honduras

Ghana Angola

Chad

Gabon

Malaysia

India

Bangladesh

BeninCambodia

Liberia

NicaraguaPakistan

Botswana

Burundi Central African Republic

Ethiopia

Guatemala

Mali

Mauritius

Mexico

Niger

Singapore

South Africa

Sri Lanka

Sudan

Swaziland

Thailand

UgandaVietnam

Zambia

Coef = 0.62, t-stat = 8.51 Log GDP pc

Log

Acc

ount

s pe

r 00

0 A

dults

6

2. More complexity, less access for individuals

Documents Needed to Open an Account : 5 in Cote d’Ivoire, Nicaragua Only 1 in Singapore, Thailand

Documents Required to O pen an Account and Access

Thailand

Tanzania Nicaragua

Mauritius

Indonesia Chad

Burundi

ZambiaSudanRwandaPakistan

NamibiaMexicoLesotho Cote d'Ivoire

Burkina Faso

Cape VerdeSri Lanka

South Africa

Gambia

Cambodia

BotswanaSierra Leone

Malaysia

Honduras

GabonAngola

NepalLiberia

Kenya

IndiaBenin Bangladesh

Coef = -153.5, t-stat = -3.3 Documents Required

Acc

coun

ts p

er 0

00 A

dults

7

Opening an Account can be complex…

Days to Open an Account•More days, less access

Country Days Country Days

Mexico 3.0 Thailand 0.5Pakistan 2.8 Cameroon 0.5South Africa 2.8 Chad 0.5Gabon 2.5 Malaysia 0.5Botswana 2.3 Ethiopia 0.6

Longest wait Shortest Wait

8

More complexity, less access for firms…

More complex business loan applications mean fewer small firms use working capital credit…

Reduced Access for Small Firms

South Africa

TanzaniaSwazilandSenegal

Rwanda

PhilippinesMali Madagascar

Sri Lanka

Indonesia

Honduras CameroonVietnam

Thailand

El SalvadorNicaraguaNiger

Mauritius

Cambodia

Kenya

Gambia Ghana

Ethiopia

Cape VerdeBotswana

Burkina Faso

Benin

Angola

Coef = -31, t-stat = -2.11 Business Loan Complexity of Loan Procedures

`% o

f sm

all m

icro

firm

s w

ith

loan

s fo

r wor

king

cap

ital

9

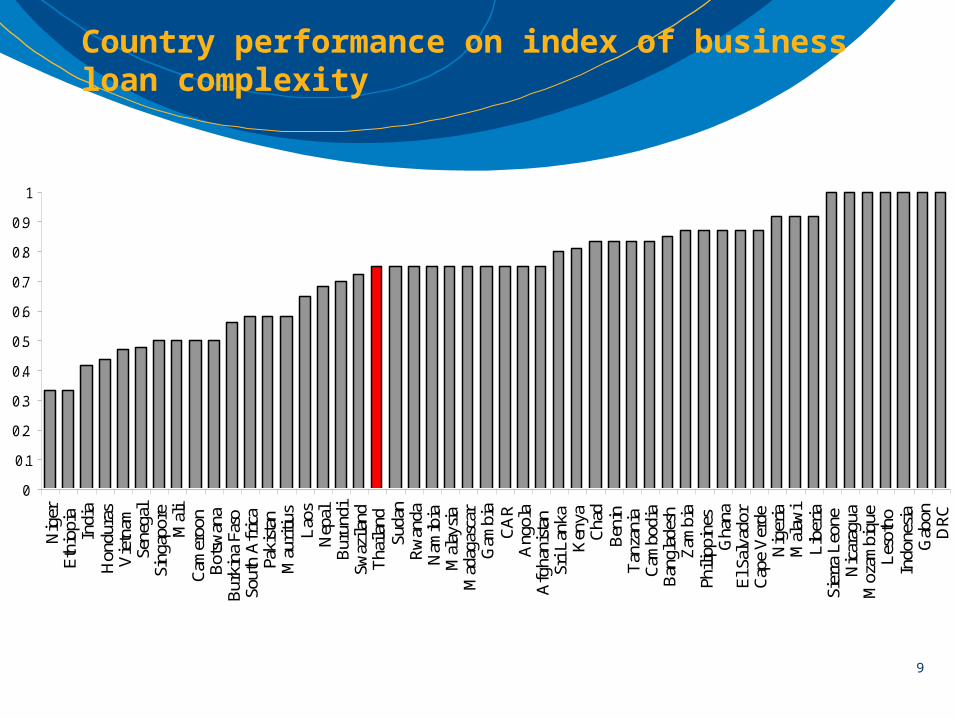

Country performance on index of business loan complexity

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Nig

erE

thio

pia

Indi

aH

ondu

ras

Vie

tnam

Sene

gal

Sing

apor

eM

ali

Cam

eroo

nB

otsw

ana

Bur

kina

Fas

oSo

uth

Afr

ica

Paki

stan

Mau

ritiu

sL

aos

Nep

alB

urun

diSw

azila

ndT

haila

ndSu

dan

Rw

anda

Nam

ibia

Mal

aysi

aM

adag

asca

rG

ambi

aC

AR

Ang

ola

Afg

hani

stan

Sri L

anka

Ken

yaC

had

Ben

inT

anza

nia

Cam

bodi

aB

angl

ades

hZ

ambi

aPh

ilipp

ines

Gha

naE

l Sal

vado

rC

ape

Ver

deN

iger

iaM

alaw

iL

iber

iaSi

erra

Leo

neN

icar

agua

Moz

ambi

que

Les

otho

Indo

nesi

aG

abon

DR

C

10

3. Some Costs Matter – Ongoing Costs

Monthly maintenance fee, as a % monthly wage is: 51.5% in Rwanda; 0.05% in Singapore

Over half of all sampled banks charge monthly fees Fees in Africa tend to be higher ($4, vs. 0.50c in Asia) 20% of banks report other charges such as fees for a checkbook or an ATM People dislike paying fragmented fees

11

Annual fees for cash and debit cards

Annual Fee for Cash and Debit Cards (US$)

0 1 2 3 4 5 6 7

South Asia

East Asia

CentralAmerica

Africa

12

Periodic monthly fee for current account maintenace in Thailand is 1.39 USD

Lowest Fees USD Highest Fees USD

Sudan 14.93 Pakistan 0.27Mexico 11.49 Angola 0.22Cote d'Ivoire 11.04 Cambo-dia 0.21Senegal 9.00 Nigeria 0.16Liberia 7.82 Gambia 0.05Ethiopia 6.83 Afghanistan 0.00Niger 6.08 India 0.00Kenya 5.86 Namibia 0.00Zambia 5.76 Nepal 0.00DRC 5.64 Vietnam 0.00

Source: Getting Finance Database

Periodic monthly fees for current account maintenance (USD)

13

Remittance Costs Also Matter…

Higher Costs for Receiving a Banker’s Draft - Lower Financial Access

Financial Access and the Cost of Receiving a Banker's Draft

Namibia

Ghana

Sri Lanka

Niger

Mexico

Malaysia

ZambiaUganda

Thailand Tanzania

South Africa

Mauritius

Laos

IndiaEthiopia

Côte d'IvoireChad

Cape verde

CameroonCambodia

BotswanaMalawi

Burundi

Benin

Cost of Receiving a Banker's Draft Coef=-269.557 , t=-2.13

14

4. What Doesn’t Seem to Influence Access?...Convenience Features…

Index of convenience features (0-1)

Higher End Index Lower End Index

Senegal 0.81 Sri Lanka 0.35Kenya 0.79 Thailand 0.33CAR 0.75 Afghanistan 0.31India 0.75 Laos 0.30Malawi 0.75 Bangladesh 0.29Mexico 0.75 Cote d'Ivoire 0.25Nicaragua 0.75 Malaysia 0.25Botswana 0.70 Ethiopia 0.15Burkina Faso 0.70 Liberia 0.10Nepal 0.70 Guatemala 0.00

Source: Getting Finance Databasenote: The index of usage convenience is an equally weighted mean of responses to: passbook not required, after hours access available, overdraft provision and whether a customer is notified of overdraft.

15

5. Special Measures don’t seem to promote access…

‘Basic’ or simplified accounts? However, experiments are small and new Commercial banks schemes also don’t show association

Matched savings may work Require governments to make matching contributions to private

savings, in some agreed proportion But such schemes require subsidies Only offered in Singapore in our sample

Yet 22 countries offer tax incentives for savings Many governments prefer to forgo revenue through tax waivers

instead of spending on subsidies

Door Step Collection Schemes India, Philippines, Indonesia, Ghana

16

6. Phone, Internet and Mobile Technologies overview

Banking services can be offered via ATMs, Internet, Cell Phones

No association with number of accounts All banks in Thailand offer balance

inquiries over Internet About 50% of banks in Thailand offer

balance inquieries via cell phones M-banking holds promise

17

Mobile Technologies increase financial depth but not access

Private Credit/GDP and Mobile Technology

Angola

BotswanaCape verde

DRC

Gabon

Guatemala

Honduras

Indonesia

KenyaMalawi

Malaysia

Nicaragua

Nigeria

Singapore South AfricaThailand

Vietnam

Mobile Technology IndexCoef=25.36, t=1.75

18

The network quality and interoperability index for Thailand is 0.88

Network quality and interoperability index (0-1)

Higher End Index Lower End Index

Honduras 1.00 Cambodia 0.20India 1.00 Ethiopia 0.20Indonesia 1.00 Laos 0.20Malaysia 1.00 Sierra Leone 0.20Mauritius 1.00 Burundi 0.12Mexico 1.00 Niger 0.08Nicaragua 1.00 CAR 0.00Nigeria 1.00 Chad 0.00Pakistan 1.00 Gambia 0.00Philippines 1.00 Liberia 0.00

Source: Getting Finance Database

note: The Network quality and interoperability index comprises 2 variables assessing the interoperability of payments networks: (i) whether debit cards can be used at ATMs belonging to other banks which share the banks' network; and (ii) whether debit cards can be used at merchants through Points of Sale devices.

19

7. What Else Matters? Increased competition, transparency, creditors rights…

Banks in countries with more competitive banking sectors are less bureaucratic.

Thailand: Asset share of top three banks: less than 45% Documents required to open an account: 1 on average

Nicaragua: Asset share of top 3 banks: 95% Documents required to open an account: 5 on average

20

Increasing disclosure can increase access

Clear, transparent bank regulations Transparent fees Informed customers Procedures for complaints Clear credit application guidelines Financial literacy programs

21

Increasing disclosure

Working Capital Loans and Credit Guidelines

Angola

Lesotho

ZambiaSouth Africa

Uganda

Thailand

El SalvadorNicaragua

Malawi

Mauritius

Mexico

Sri Lanka

KenyaGhana

Benin

Cape VerdeGambiaGuatemala

Mali

P akistan

Rwanda

Swaziland

Coef. = 16.76, t=3.2 Credit Application Guidelines Index

22

Banking the Poor Snapshots

1.24

61.38

3.54

28

50.64

1.593.88

16.87

28.227.2325.31

10.31

0

10

20

30

40

50

60

70

Annual Debit CardFee US$

Fee to receive $250remittance

Small firms withbank loans %

Firms that use loansfor investments %

Thailnd

East Asia

54 Countries

23

Banking the Poor Snapshots

2.00

0.50

1.001.00

2.00

0.50

0.800.540.46 0.48

0.67

3.05

0

1

1

2

2

3

3

4

Transparency andconsumer protection

index (0-1)

Index of collateralflexibility (0-1)

Start-up loanprocessing fee %

Documents to openan account

Thailand

East Asia

54 Countries

24

Next Steps

New Regulators Survey in 140 countries Measuring broader access to finance:

Commercial Banks Microfinance Institutions Development Banks Credit Unions, Cooperatives

Part of the new CGAP initiative

25

Questions?