bank of finland bulletin 2/2014: financial stability

DESCRIPTION

Bank of Finland Bulletin 2/2014: Financial stability. Pentti Hakkarainen, Deputy Governor. Themes of the stability report. Owing to the weak outlook for the real economy, particular attention needs to be devoted to the vulnerabilities of the domestic financial system. - PowerPoint PPT PresentationTRANSCRIPT

Bank of Finland Bulletin 2/2014: Financial stabilityPentti Hakkarainen, Deputy Governor

15.5.2014

Themes of the stability report

• Owing to the weak outlook for the real economy, particular attention needs to be devoted to the vulnerabilities of the domestic financial system.

• Risks can be created by: housing price developments and households’ considerable debt levels, effects of low interest rates and transmission of bank lending.

• As demonstrated by the financial crisis, Finland also needs internationally comparable instruments for prevention of systemic risks.

• Banking union marks an important step forward. Supervision and resolution should be on the same cross-border level as the actual operations of financial institutions.

15.5.2014 2

315.5.2014

Risks related to economic and credit cycles

415.5.2014

-200

0

200

400

600

800

2007 2008 2009 2010 2011 2012 2013 2014

Basis points

Public sector*, peripheral countries**Public sector*, Countries with good credit ratingsFinancial institutions, peripheral countries**Financial institutions, countries with good credit ratings

* Public-sector bonds refer to bonds issued by local government and centralgovernment-guaranteed bonds.** Peripheral countries: Italy, Spain, Greece, Ireland and Portugal.Sources: Bloomberg and BofA Merrill Lynch.

Risk premia on bonds issued by financial institutions andpublic-sector entities*

Improved access to finance supports euro area’s gradual recovery from the crisis

515.5.2014

0

100

200

300

400

500

0

5

10

15

20

25

1998 2001 2004 2007 2010 2013

Numer of issues (right-hand scale) Risk premium

%

Source: Bloomberg.

Number

Issues of bonds by high-risk non-financial corporations and risk premia on yields

Increased risk appetite may distort prices on securities markets

6

Share prices on the increase

15.5.2014

60

100

140

180

220

2009 2010 2011 2012 2013 2014

S & P 500 index Tokyo, Nikkei 225 index Total euro area: Dow Jones Euro Stoxx (Broad) index MSCI emerging markets index

Beginning of period = 100

Source: Bloomberg.

Stock indices of major countries

Risks transmitted from abroad to Finland

• The development of the international economy and financial markets has a great impact on the prospects and risks for the Finnish economy and financial system.

Risks of key concern for Finland: Emergence of renewed instability on international financial markets. Long-sustained low level of interest rates and excessive rise in

asset prices. Impact of geopolitical tensions on the Finnish economic outlook.

15.5.2014 7

8

Domestic economy, non-financial corporations, households, public finances

15.5.2014

Makrotalous

Asuntojen hinnat

VelkaantuneisuusRiskipreemiot

Pankkien kestävyys

IV/2009 I/2012 III/2012

Suomen rahoitusjärjestelmän vakauskartta

Lähteet: NASDAQ OMX Helsinki, pankit, Tilastokeskus ja Suomen Pankki.

Makrotalous

Asuntojen hinnat

VelkaantuneisuusRiskipreemiot

Pankkien kestävyys

IV/2009 I/2012 III/2012

Suomen rahoitusjärjestelmän vakauskartta

Lähteet: NASDAQ OMX Helsinki, pankit, Tilastokeskus ja Suomen Pankki.

June 2012 June 2013 May 2014

Makrotalous

Asuntojen hinnat

VelkaantuneisuusRiskipreemiot

Pankkien kestävyys

IV/2009 I/2012 III/2012

Suomen rahoitusjärjestelmän vakauskartta

Lähteet: NASDAQ OMX Helsinki, pankit, Tilastokeskus ja Suomen Pankki.

The outer values reflect higher systemic risks.Sources: NASDAQ OMX Helsinki, banks, Statistics Finland and Bank of Finland.

9

Housingprices

Real economy

Banks’viability

IndebtednessRisk premia

Indebtedness and development of the real economy pose the main risks to the Finnish financial system

15.5.2014

1015.5.2014

-20

-10

0

10

20

30

0

2

4

6

8

10

2005 2007 2009 2011 2013

1 Average interest rate on corporate loan stock* (left-hand scale) 2 Average interest rate on new corporate loans* (left-hand scale) 3 Corporate loans, annual growth rate** (right-hand scale)

12

3

%

* Includes housing corporations. ** Excludes housing corporations.Source: Bank of Finland.

Average interest rates on MFI corporate loans and annual growth rate in Finland

%

Growth rate of MFI corporate loans has remained subdued

11

Interest rates on corporate loan stock in euro area countries

15.5.2014

0

1

2

3

4

5

6

7

2009 2010 2011 2012 2013 2014

Finland Germany France Italy Spain Euro area

%

Sources: European Central Bank and Bank of Finland calculations.

1215.5.2014

0

20

40

60

80

100

2009 2010 2011 2012 2013 2014

Got everything Got part of itRefused to withdraw because cost too high Application rejectedDon't know

Source: European central bank.

%

* October–March.** April–September.

* *** ** * **

Access to finance has remained good in the corporate sector in Finland

1315.5.2014

Bankruptcies increasing slightly, but still at a moderate level

0

2

4

6

8

0

2

4

6

8

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Bankruptcy filings for non-financial corportaions, 12-month moving sum (left-hand scale)Banks' non-performing assets* (right-hand scale)

Number, 1,000

* Assets due and unpaid for at least 90 days.Sources: Statistics Finland, Financial Supervisory Authority and Bank of Finland calculations.

Bankruptices and non-performing assets in Finland

EUR billion

1415.5.2014

0

1

2

3

4

5

6

7

0

20

40

60

80

100

120

140

2000 2002 2004 2006 2008 2010 2012

Other loans (left-hand scale)Housing corporation loans* (left-hand scale)Housing loans (left-hand scale)Interest expenditure (right-hand scale)

% of disposable income

* Statistics Finland’s estimate of the loan stock of household-owned housing corporations.Sources: Statistics Finland and Bank of Finland calculations.

Household indebtedness and interest burden in Finland

% of disposable income

Household indebtedness continued to grow but at a slower pace

1515.5.2014

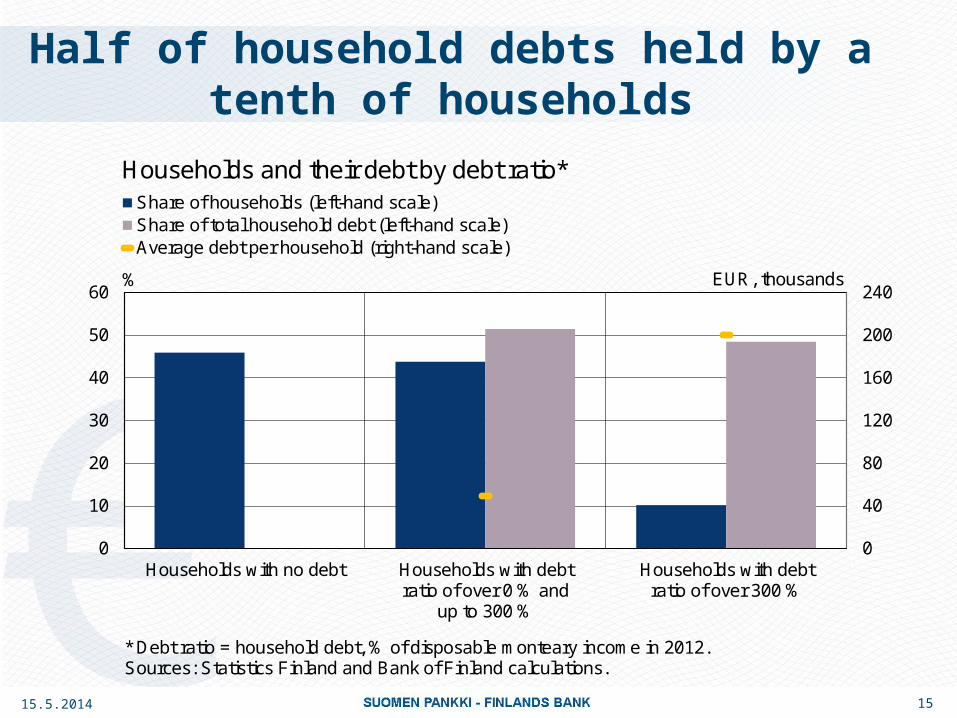

Half of household debts held by a tenth of households

0

40

80

120

160

200

240

0

10

20

30

40

50

60

Households with no debt Households with debtratio of over 0 % and

up to 300 %

Households with debtratio of over 300 %

Share of households (left-hand scale)Share of total household debt (left-hand scale)Average debt per household (right-hand scale)

%

* Debt ratio = household debt, % of disposable monteary income in 2012.Sources: Statistics Finland and Bank of Finland calculations.

Households and their debt by debt ratio*

EUR, thousands

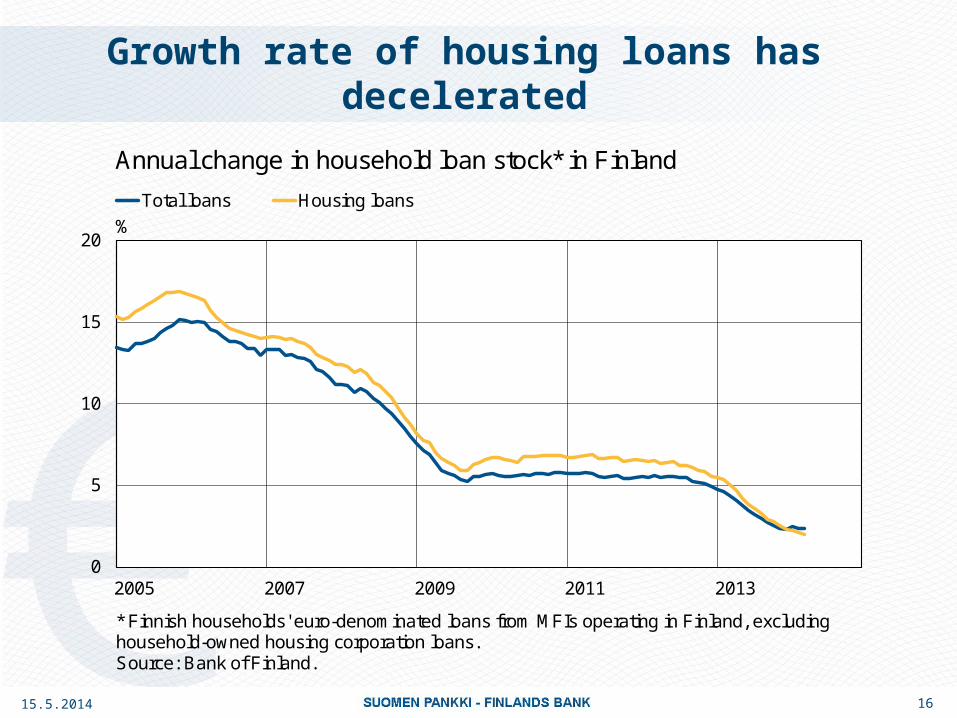

1615.5.2014

0

5

10

15

20

2005 2007 2009 2011 2013

Total loans Housing loans%

* Finnish households' euro-denominated loans from MFIs operating in Finland, excluding household-owned housing corporation loans.Source: Bank of Finland.

Annual change in household loan stock* in Finland

Growth rate of housing loans has decelerated

1715.5.2014

80

100

120

140

160

2000 2003 2006 2009 2012

Whole country Greater Helsinki area Rest of Finland

Index, 2000 = 100

Nominal housing price indices are converted into real indices, using the consumer price indexfor the whole country.Source: Statistics Finland.

Real housing prices in Finland

Real housing prices have declined, regional differences in price developments

1815.5.2014

Financial system risk resilience and structural risks

1915.5.2014

0

5

10

15

20

25

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013

Loss buffer* (left-hand scaleMinimum requirement for own funds (left-hand scale)Capital adequacy ratio (Tier 1 and Tier 2) (right-hand scale)Common Equity Tier 1 ratio (CET1) (right-hand scale)

EUR bn

* Own funds surplus = own funds − minimum requirement for own funds.Source: Financial Supervisory Authority.

Own funds and capital adequacy in the Finnish banking sector

%

Finnish banking sector’s risk resilience has remained good

2015.5.2014

Banking sector performance unchanged and loan losses small

-8

-4

0

4

8

2007 2008 2009 2010 2011 2012 2013

Net interest income Net fee incomeNet income from trading and investment Other incomeExpenses and depreciations Net impairment lossesPre-tax profit

EUR bn

Source: Financial Supervisory Authority.

Finnish banking sector performance

2115.5.2014

-2

0

2

4

6

1999 2001 2003 2005 2007 2009 2011 2013

Overall margin (average interest rate on loan stock - average interest rate on deposit stock)3-month Euribor

%

Finnish MFI loans to and deposits from the public.Sources: Reuters and Bank of Finland.

Overall margin and 3-month Euribor

Low interest rates and slower growth of lending stock strain profitability

2215.5.2014

Dependency on international wholesale funding increases vulnerability

0

50

100

150

200

2006 2008 2010 2012 2014

Issues of long-term debt securitiesIssues of short-term debt securitiesLoans to households and non-financial corporationsDeposits from households and non-financial corporationsStructural financial deficit (loan stock - deposit stock)

EUR bn

Deposit banks, mortgage banks and other credit institutions in the same group.Source: Bank of Finland.

Finnish banking sector’s dependency on wholesale funding

Banking sector sensitive to contagion

• Finnish banking sector’s degree of concentration among the highest in the EU.

• Strong interconnectedness within the Nordic banking system. Large amount of assets in the Nordic countries, only small amount in the higher-risk countries.

• Significant share of the Finnish banking sector in the ownership of Nordic parent banks.

• Domestic banks’ foreign assets and liabilities have increased in the 2000s.

15.5.2014 23

24

Insurance sector has maintained its solvency

15.5.2014

• Insurance sector profitability and solvency have remained good, but considerable differences between companies can be observed.

• Insurance companies have been able to adjust their business models in the low interest rate environment.

• Unexpected shocks in the investment market pose the main risk to profitability and solvency.

25

Infrastructure has operated reliably

• A reliable infrastructure that functions under all circumstances is a key part of a stable financial system – International cooperative oversight plays an important role

• Fragmentation of functions can endanger continuity – National contingency arrangements important

• Finland migrated to SEPA on schedule, development continues – New cooperation groups have been established: the Euro

Retail Payments Board (ERPB) in Europe and the Payments Council in Finland

15.5.2014

2615.5.2014

Measures to ensure financial stability

27

The macroprudential tools to be introduced in Finland

• Countercyclical capital buffer requirement: 2015

• Binding maximum loan-to-value (LTV) ratio for housing loand (loan-to-value cap): 7/2016

• Minimum risk weights for housing loans: 2015

• Additional capital requirement for domestic systemically important credit institutions (O-SII requirement): 2016

15.5.2014

28

…. should be supplemented

• Use of the systemic risk buffer should also be made possible in Finland – Additional capital requirement permitted by the Capital

Requirements Directive if the national banking sector is structurally vulnerable

– There should not be big differences in regulation and supervision in an integrated banking market

– Nearly all EU countries will incorporate the requirement in their legislation

• An internationally comparable set of instruments is necessary; use of the instruments to be determined separately.

15.5.2014

29

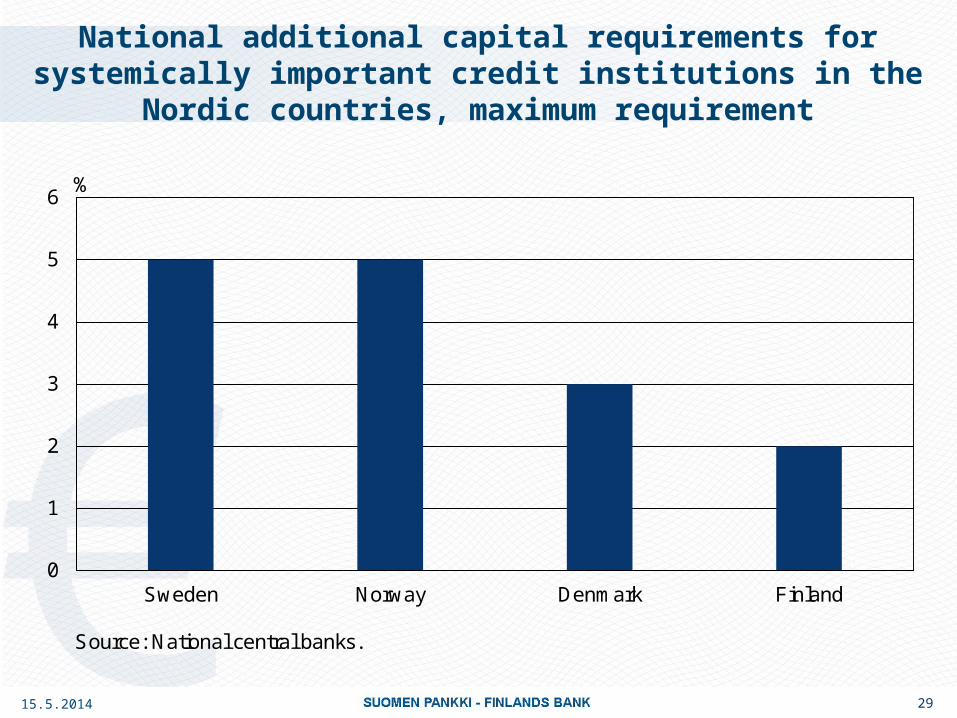

National additional capital requirements for systemically important credit institutions in the Nordic countries, maximum

requirement

0

1

2

3

4

5

6

Sweden Norway Denmark Finland

National additional capital requirements for systemically important credit institutions in the Nordic countries, maximum amount

%

Source: National central banks.

15.5.2014

Banking union about to start

• The two key elements of banking union – single supervision of banks and single resolution – are about to start.

• The resolution mechanism and bail-in remove/reduce the costs of banking crises to taxpayers.

• Also in Finland, resolution legislation and the related powers for authorities must be implemented promptly in all respects.

15.5.2014 30

31

Single Resolution Mechanism

15.5.2014

3215.5.2014

Thank you!