‘bank challengers’ in payments - kpmg · ‘bank challengers’ in payments ... (retail) bank...

TRANSCRIPT

Financial ServiceS & Finance adviSory

‘Bank Challengers’ in Paymentsresults of a survey of banks and payment service providers on the market challenges for payment service providers

Study

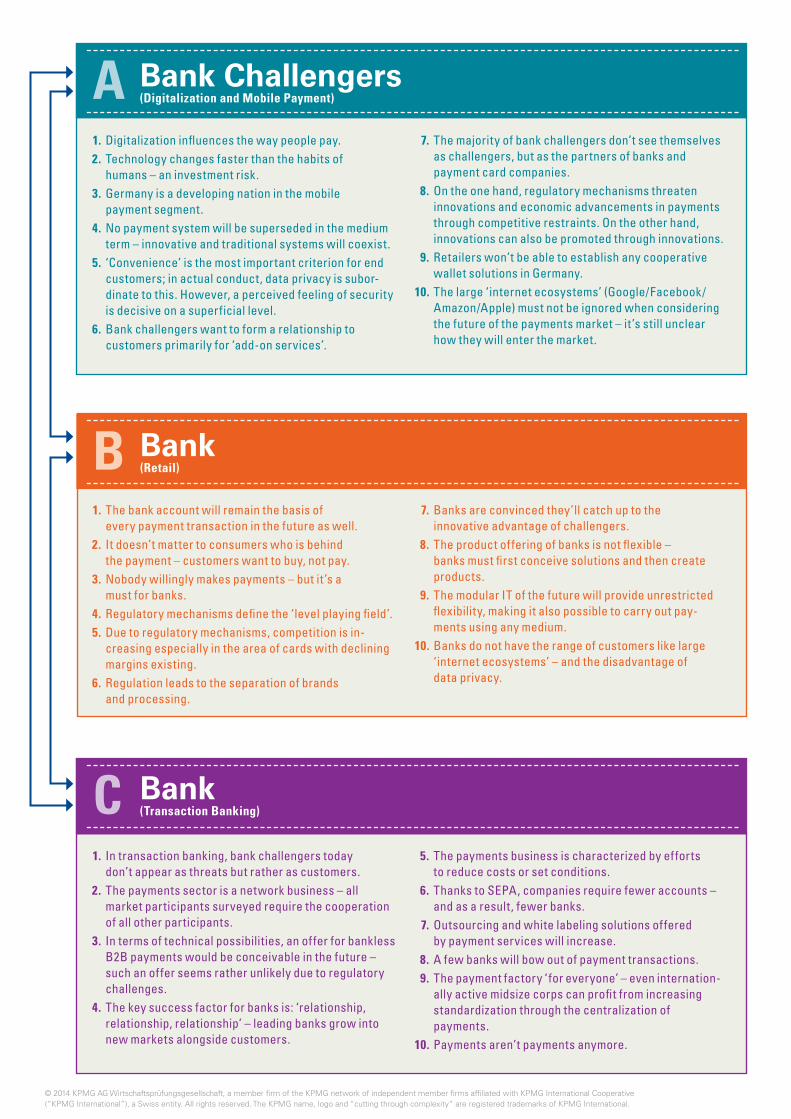

1. Digitalization influences the way people pay. 2. Technology changes faster than the habits of

humans – an investment risk. 3. Germany is a developing nation in the mobile

payment segment. 4. No payment system will be superseded in the medium

term – innovative and traditional systems will coexist. 5. ‘Convenience’ is the most important criterion for end

customers; in actual conduct, data privacy is subordinate to this. However, a perceived feeling of security is decisive on a superficial level.

6. Bank challengers want to form a relationship to customers primarily for ‘addon services’.

7. The majority of bank challengers don’t see themselves as challengers, but as the partners of banks and payment card companies.

8. On the one hand, regulatory mechanisms threaten innovations and economic advancements in payments through competitive restraints. On the other hand, innovations can also be promoted through innovations.

9. Retailers won’t be able to establish any cooperative wallet solutions in Germany.

10. The large ‘internet ecosystems’ (Google/Facebook/Amazon/Apple) must not be ignored when considering the future of the payments market – it’s still unclear how they will enter the market.

1. The bank account will remain the basis of every payment transaction in the future as well.

2. It doesn’t matter to consumers who is behind the payment – customers want to buy, not pay.

3. Nobody willingly makes payments – but it’s a must for banks.

4. Regulatory mechanisms define the ‘level playing field’. 5. Due to regulatory mechanisms, competition is in

creasing especially in the area of cards with declining margins existing.

6. Regulation leads to the separation of brands and processing.

7. Banks are convinced they’ll catch up to the inno vative advantage of challengers.

8. The product offering of banks is not flexible – banks must first conceive solutions and then create products.

9. The modular IT of the future will provide unrestricted flexibility, making it also possible to carry out payments using any medium.

10. Banks do not have the range of customers like large ‘internet ecosystems’ – and the disadvantage of data privacy.

1. In transaction banking, bank challengers today don’t appear as threats but rather as customers.

2. The payments sector is a network business – all market participants surveyed require the cooperation of all other participants.

3. In terms of technical possibilities, an offer for bankless B2B payments would be conceivable in the future – such an offer seems rather unlikely due to regulatory challenges.

4. The key success factor for banks is: ‘relationship, relationship, relationship’ – leading banks grow into new markets alongside customers.

5. The payments business is characterized by efforts to reduce costs or set conditions.

6. Thanks to SEPA, companies require fewer accounts – and as a result, fewer banks.

7. Outsourcing and white labeling solutions offered by payment services will increase.

8. A few banks will bow out of payment transactions. 9. The payment factory ‘ for everyone’ – even inter na tion

ally active midsize corps can profit from increasing stan dard ization through the centralization of payments.

10. Payments aren’t payments anymore.

A

B

C

Bank Challengers(Digitalization and Mobile Payment)

Bank(Retail)

Bank(Transaction Banking)

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

ContentsIntroduction 05

Study Approach design, participants and concepts 06

The Market Perception “We feel challenged, not threatened.” 08

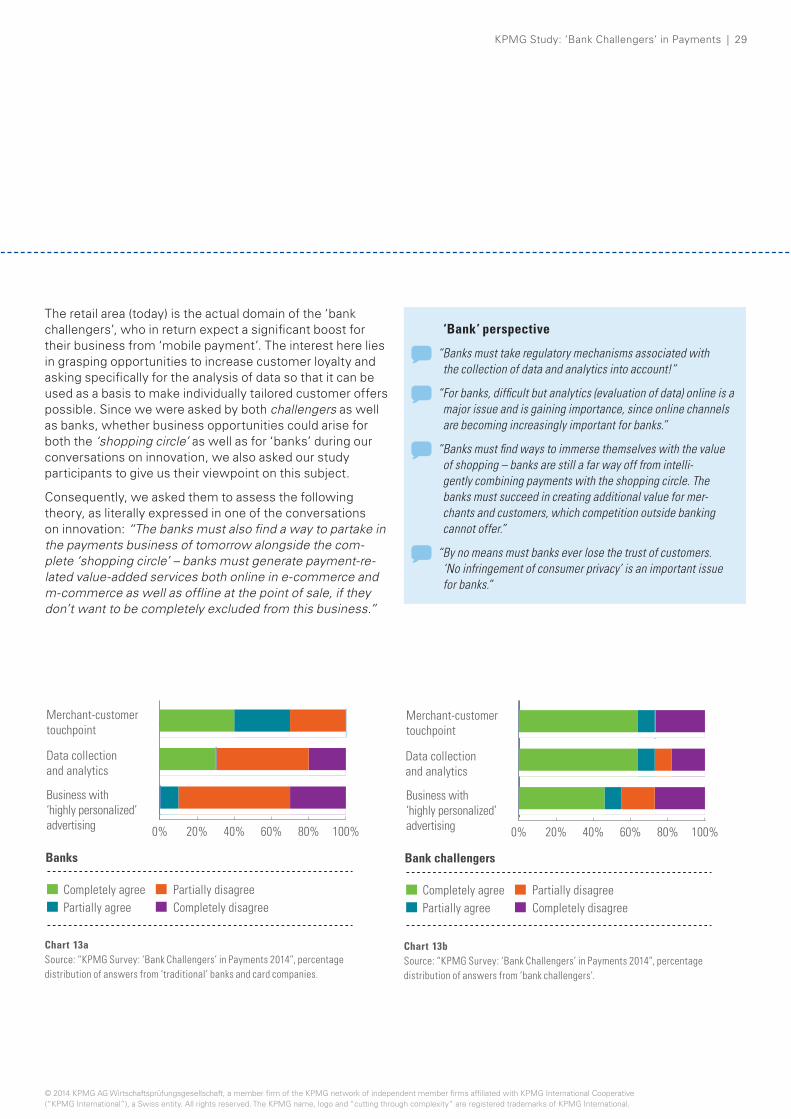

The Market Development “The market will have completely changed in ten years.” 14

The Market Evaluation “digitalization influences the way people pay.” 20

The Market Regulation “regulatory mechanisms serve as a playing field for everyone.” 31

The Market – KPMG’s Conclusion “Payments aren't payments anymore.” 36

1

2

3

4

5

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

4 | KPMG Study: ‘Bank challengers’ in Payments

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 5

Introduction

due to a variety of technical innovations and ever-changing customer needs, the market for payment services is in a phase of upheaval. new market participants are entering this market, which up until now has been dominated by ‘traditional’ financial service companies such as banks and credit and debit card companies. These new participants, who stand out above all thanks to their innovative concepts and products, are not only in fierce competition with each other, but quite a few also seek to directly compete with traditional providers in the payments market. KPMG there-fore classifies these new market participants as ‘bank challengers’.

KPMG addressed this topic outlined above in the form of a survey, examining both the perspective of the ‘bank challengers’ as well as the traditional payment providers – who, for the purpose of simplicity and memorability, were repeatedly referred to as ‘the banks’, also by our respon-dents. our comparative survey of conceptually fundamental perspectives of ‘banks versus bank challengers’ allows trends, chances, risks and recommended actions to be derived for both groups in the payments market.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

6 | KPMG Study: ‘Bank challengers’ in Payments

Design, participants and concepts

Study Approach

This KPMG publication evaluates the results of a primarily qualitative-based survey carried out in personal interviews. in the first survey phase, KPMG employees engaged in open conversations on innovation with a few selected market participants representing payment service pro vid-ers. Based on these previous conversations on innovation, a questionnaire was then developed, serving as the basis upon which further talks with market participants were conducted in a second survey phase. Thanks to the struc-ture of the questionnaire, the talks of this second survey phase then unlocked possibilities to quantitatively evaluate the recorded results.

With regard to the design of this study, our survey was not regarded as a conventional field study making statistically grounded general claims; therefore, the statements de-scrib ing trends and tendencies made in our study results do not make any claims to accuracy as based on statistical evidence.1 rather, the “KMPG Study: ‘Bank challengers’ in Payments” collects the opinions of the different ‘parties’ active in today’s payments market and evaluates them by way of comparison, analysis, drawing conclusions and asking further questions. Subjective evaluations made on the part of KPMG have been identified as such.

The selection of our respondents includes representatives from different fields of business activity in payment trans-actions. This comprehensive range is intended to gain a qualitatively representative picture of the undertakings being carried out in the different areas of this market in all its current facets – in other words, the entire ecosystem of payments in its various forms of usage: We didn’t just survey credit- or e-money institutions, credit and debit card issuers and acquirers, online or mobile payment providers, payment processors and financial platforms, but also contacts from the telecommunications industry, a banking association as well as a standardization organization. a total of 25 interviewees participated in our study – and despite this seemingly limited number of participants, we can state that a significant share of the players most important to this market participated in the KPMG Study.2

‘Bank challenger’ perspective

“ ‘Bank challengers’– this term is actually funny, because we are not concerned with challenging banks. In contrast: We often work with banks – right from the very beginning in fact. We see ourselves more as ‘bank enablers’.”

on this basis, the KPMG Study has conceptually different objectives and areas of classification: For one, it was our primary objective to juxtapose the subject matter from two different perspectives – on the one hand, the partici-pant perspective of ‘traditional’ payment service providers (i.e. ‘traditional’ banks and card companies), on the other hand, the perspective of KPMG’s so-called ‘bank chal-lengers’. The same set of mainly qualitatively based, but also quantitatively oriented questions were asked to the representatives of both perspectives. For reasons of practicality, we have included all participants who are not ‘traditional’ banks and card companies under the category of ‘bank challenger’ in our graphical evaluations – for one, because we can easily distinguish the ‘traditional’ market participants, but also because we didn’t want to form any subgroups for evaluation beforehand due to the relatively small number of participants. in accordance with our defined nomenclature, 11 ‘banks’ and 14 ‘bank chal-lengers’ partook in our study.3

of course, these two groups are by no means homoge-neous. This is already apparent in that the ‘bank chal-lengers’ surveyed by KPMG only partially see themselves as such – some of them even specifically emphasized that they consider themselves primarily as the ‘cooperation partners of banks’. only a minority actually enter the mar-ket to pursue being a ‘creative destroyer’, with the intent of decreasing the market shares of ‘the banks’ in payments to a partially substantial degree over the medium to long term. in addition, different survey participants repeatedly indi-cated that the business, already being generated online and now also through mobile payment, is for the most

1 Studies in other subject areas, which are are grounded in statistically verifiable survey results, exist in great numbers; examples of such include the initiative d21 / Fiducia: “online – Banking 2014” (June 2014); GS1 Germany / eHi retail institute: “Mobile in retail 2014” (May 2014); capgemini / royal Bank of Scotland: “World Payments report 2013” (September 2013); efma: “innovation in retail Banking” (5th annual edition, September 2013); a.T. Kearney: “Winning the Growth challenge in Payments” (June 2013); deutsche Bank research: “The Future of (Mobile) Payment: new (online) Players competing with Banks.” [“Banken im Wettbewerb mit neuen internet-dienstleistern”](February 2013).

2 We gratefully thank all survey participants for their willingness to communicate and for taking the time to extensively inform us about their own business, discuss market fore casts and talk about future perspectives. KMPG has promised the study participants not to refer to the study participants by name in the publication. Moreover, the survey results should be anonymized so that it is not possible for outside observers to draw conclusions as to the respective response of an individually identifiable institute or company. everything, identified as a ‘statement’ in this publication (through the use of quotation marks and italics), nevertheless represents authentic quotes from survey participants who – as agreed – have been anonymized by KPMG.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 7

3 For the purpose of memorability as well as because of background affiliation, we kindly ask credit and debit card companies to see that we have ‘assigned’ them to the ‘banks’ in the charts – here this collective term is used to differentiate ‘bank challengers’ from all ‘traditional’ banks and credit and debit card companies which participated in our survey. Since not all study participants always answered each individual question, percentage values are provided in the graphical evaluations for the total number of respondents who actually answered the respective question, for the sake of clarity as well as comparability.

4 cf. KPMG: “consumer Barometer – 2/2014 – Mobile Payment” (July 2014); BiTKoM: “Position Paper on Mobile Payment” [“Positionspapier Mobile Payment”] (February 2013) or the surveys and statistics from BiTKoM research, for example, “Trends in online Shopping” [“Trends im online-Shopping”] (June 2014).

part ‘new business’, which previously did not exist in this form in the ‘traditional’ world: it is not so much the personal aim of innovative payment providers to just ‘have a slice of the cake’ but rather to be ‘the icing on the cake in future’ – above all, to gain better access to customers, for example, for the possibilities of personalized information, specifically tailored advertising and products, etc.

our pool of participants is heterogeneous, not only in terms of fields of business activity but also in terms of size and regional focus. even among the ‘challengers’, there are large established companies with thousands of employees in addition to small start-ups with only a handful of workers. among the ‘traditional’ respondents on the other side, KPMG interviewed nationally as well as internationally active banks and card companies, whose business models apply to both the retail as well as the corporate sector (i.e. end customer and corporate customer segments). it should be noted that there are clear differ ences in the significance and rating of answers provided by ‘banks’ – between ‘retail’ (i.e. private customers) and ‘wholesale’ or ‘transaction banking’ (i.e. corporate clients, with a focus on mass pay-ments or processing) – to which explicit reference is respectively made in the study publication.

‘Bank’ perspective

“ Do we feel challenged by bank challengers? In transaction banking (mass payments) – no. In business-to-consumer relations – yes. A risk for banks, to lose the loyalty of customers here, only becoming pure processors.”

‘Bank challenger’ perspective

“ The basic attitude of banks can be described as ‘conser-vative’; ‘change’ is perceived as a threat and danger. With this attitude, it is difficult to start something new, to open up to new partnerships or even to contemplate a new business model. On the other hand, the openness to change in par tic-ular financial institutions is also strongly related to individ-uals in particular financial institutions, since there are also interviewees who are concerned with the question of future viability in light of rapid developments. The interesting part here is that classifications can be assigned to specific areas of business: in retail – no! In wholesale – already more open to new developments.”

in the contexts addressed, some of our questions dealt with mobile payment, which – thanks to technological innovations and social developments – are notably being awarded substantial growth potential.4 Since there are different definitions of ‘mobile payment’ circulating around the market and because we wanted to ensure that all respondents discuss this subject with the same prior understanding in mind, we provided a definition in the survey: in terms of ‘mobile payment’, we mean payment transactions which can be processed in ‘real time’ basically anywhere and at any time using mobile devices (smart-phones, tablets, etc.) – no matter the technical means (near field communication [nFc], Bluetooth low energy [Ble], etc.). Moreover, when ‘payment methods’ or ‘pay-ment schemes’ are mentioned, both technological innova-tive payment options (nFc, Ble, quick response codes [Qr code] or bar codes, etc.) as well as traditional forms of payment (cash, billing, direct debit, debit/card cards, prepaid cards) are meant.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

8 | KPMG Study: ‘Bank challengers’ in Payments

1“We feel challenged, not threatened.”

The Market Perception

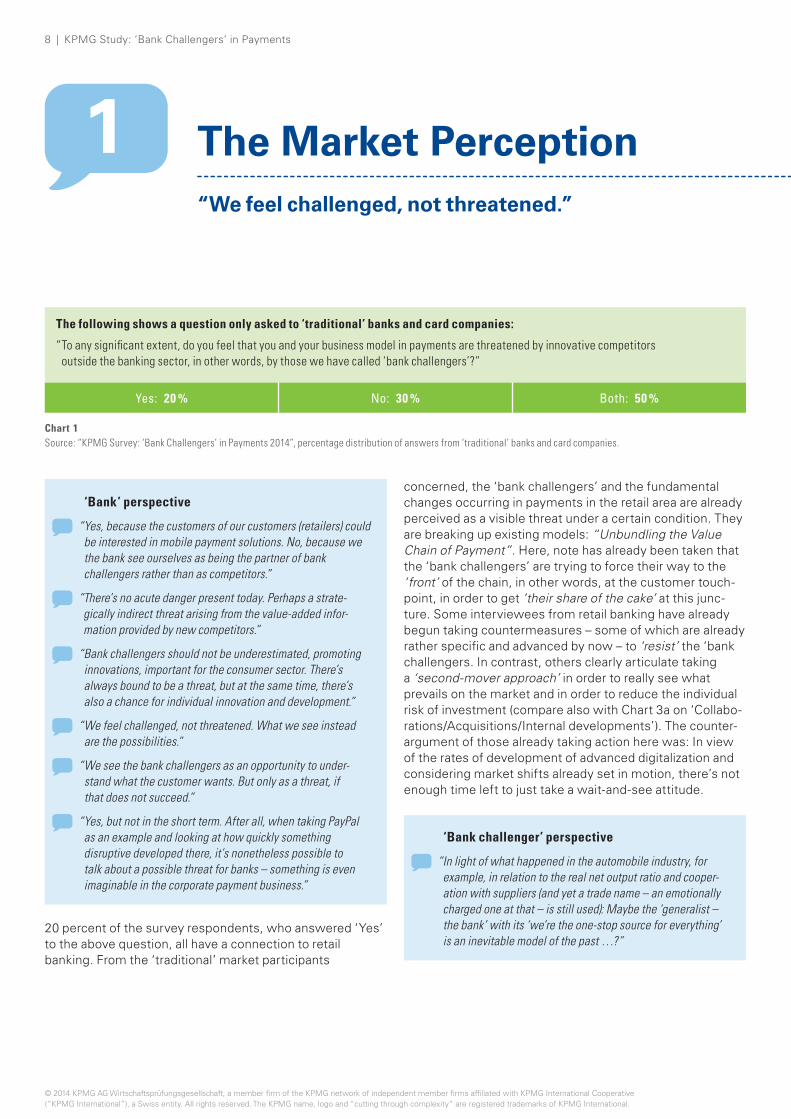

The following shows a question only asked to ‘traditional’ banks and card companies:

“ To any significant extent, do you feel that you and your business model in payments are threatened by innovative competitors outside the banking sector, in other words, by those we have called ‘bank challengers’?”

Yes: 20 % No: 30 % Both: 50 %

Chart 1Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of answers from ‘traditional’ banks and card companies.

‘Bank’ perspective

“ Yes, because the customers of our customers (retailers) could be interested in mobile payment solutions. No, because we the bank see ourselves as being the partner of bank challengers rather than as competitors.”

“ There’s no acute danger present today. Perhaps a strate-gically indirect threat arising from the value-added infor-mation provided by new competitors.”

“ Bank challengers should not be underestimated, promoting innovations, important for the consumer sector. There’s always bound to be a threat, but at the same time, there’s also a chance for individual innovation and development.”

“ We feel challenged, not threatened. What we see instead are the possibilities.”

“ We see the bank challengers as an opportunity to under-stand what the customer wants. But only as a threat, if that does not succeed.”

“ Yes, but not in the short term. After all, when taking PayPal as an example and looking at how quickly something disruptive developed there, it’s nonetheless possible to talk about a possible threat for banks – something is even imaginable in the corporate payment business.”

20 percent of the survey respondents, who answered ‘yes’ to the above question, all have a connection to retail banking. From the ‘traditional’ market participants

concerned, the ‘bank challengers’ and the fundamental changes occurring in payments in the retail area are already perceived as a visible threat under a certain condition. They are breaking up existing models: “Unbundling the Value Chain of Payment”. Here, note has already been taken that the ‘bank challengers’ are trying to force their way to the ‘front’ of the chain, in other words, at the customer touch-point, in order to get ‘their share of the cake’ at this junc-ture. Some interviewees from retail banking have already begun taking countermeasures – some of which are already rather specific and advanced by now – to ‘resist’ the ‘bank challengers. in contrast, others clearly articulate taking a ‘second-mover approach’ in order to really see what prevails on the market and in order to reduce the individual risk of investment (compare also with chart 3a on ‘collabo-rations/acquisitions/internal developments’). The counter-argument of those already taking action here was: in view of the rates of development of advanced digitalization and considering market shifts already set in motion, there’s not enough time left to just take a wait-and-see attitude.

‘Bank challenger’ perspective

“ In light of what happened in the automobile industry, for example, in relation to the real net output ratio and coope r-ation with suppliers (and yet a trade name – an emotionally charged one at that – is still used): Maybe the ‘generalist – the bank’ with its ‘we’re the one-stop source for everything’ is an inevitable model of the past …?”

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 9

accordingly, there’s a view in transaction banking, from which 30 percent of the survey respondents, who an-swered with a clear ‘no’, come from, that the ‘bank chal-lengers’ are to be treated with a wait-and-see attitude, but nevertheless also with a certain degree of respect. al-though ‘knowledge’ was expressed several times here that ‘something must be done’, it cannot be argued from KPMG’s point of view that this problem is to be regarded as urgent or even dramatic. as a reason for the relatively nonchalant position or hesitant behavior taken – depending on individually assessed evaluations – attention is to be paid to the characteristic of the payments, in particular, in the B2B area: as a network business, complexity is an inherent part of payments, which makes it extremely difficult for ‘new players’ to enter this market. Thus, for large cus -tomers, the aspect of payment processing capability and assurance plays a central role, especially when several million SePa direct debit transactions must be quickly, safely and completely transferred and processed in the settlement of payments. The condition required for a functional mass payment system does not only require highly complex processes, but also requires highly specific risk management in the face of regulatory and security requirements: all these aspects represent significant barriers to ‘bank challengers’ entering the market.

‘Bank’ perspective

“ The competition in the business of payments is really very fierce. The reason for this is that volumes are extremely important.”

With regard to the German payments market in transaction banking, multiple references were also made, that in com-parison to the rest of the eU, payments were already highly efficient long before SePa, especially in Germany. There’s also the issue that the business of payments is generally a business with very tight margins, in which, given the high costs of investment, adequate revenues can only be generated by reaching massive volumes.

From this perspective, in transaction banking, ‘traditional’ financial service providers will only initially be affected by ‘bank challengers’ in the medium term. insofar that pay-ments continue to be processed ‘behind the end-customer touchpoint’ through traditional means, and companies continue to pass on the processing and clearing of their own customers’ payments, the current developments in mobile payment also do not represent a threat to trans-action banking – in the current opinion of our study partici-pants. “But will that be the case tomorrow?” it’s not with-out reason that explicit considerations are being made by banks to which extent ‘PayPal’ might be imagin able for the corporate world.

With this in mind, we asked the study participants if they “see potential for bank challengers in business-to-business payments?” The principle answer on a whole was: “Yes, unlikely, but B2B is possible.” Banks, in particular, ex-pressed concerns here that regulatory and (risk) capital hurdles must be overcome. Moreover, it is questionable whether ‘bank challengers’ are capable of reaching the service level of a bank, offering the necessary convenience as well as fulfilling leverage and margin requirements. “How should corporate customers use the technical opportunities of new providers?” limited potential is seen here at best, on the one hand, for large online ecosystems and, on the other hand, for ‘niches’ or ‘very exceptional cases’. For instance, the payment services offered by amazon for vendors (‘Payment collection’ ) or for ‘B2B payments with commercial cards’, with which small companies such as craftsmen, for example, can make online orders for materials. even from the side of the ‘bank challengers’ various imaginable services are used for ‘small companies’ in the ‘SME sector’ generally as a replacement for cash. nevertheless, one of our respon-dents from the ‘bank’ survey group has even greater trust in the innovative capacity of the ‘bank challengers’: “In terms of their potential, such scenarios for B2B business may be much closer than people wish to believe.”

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

10 | KPMG Study: ‘Bank challengers’ in Payments

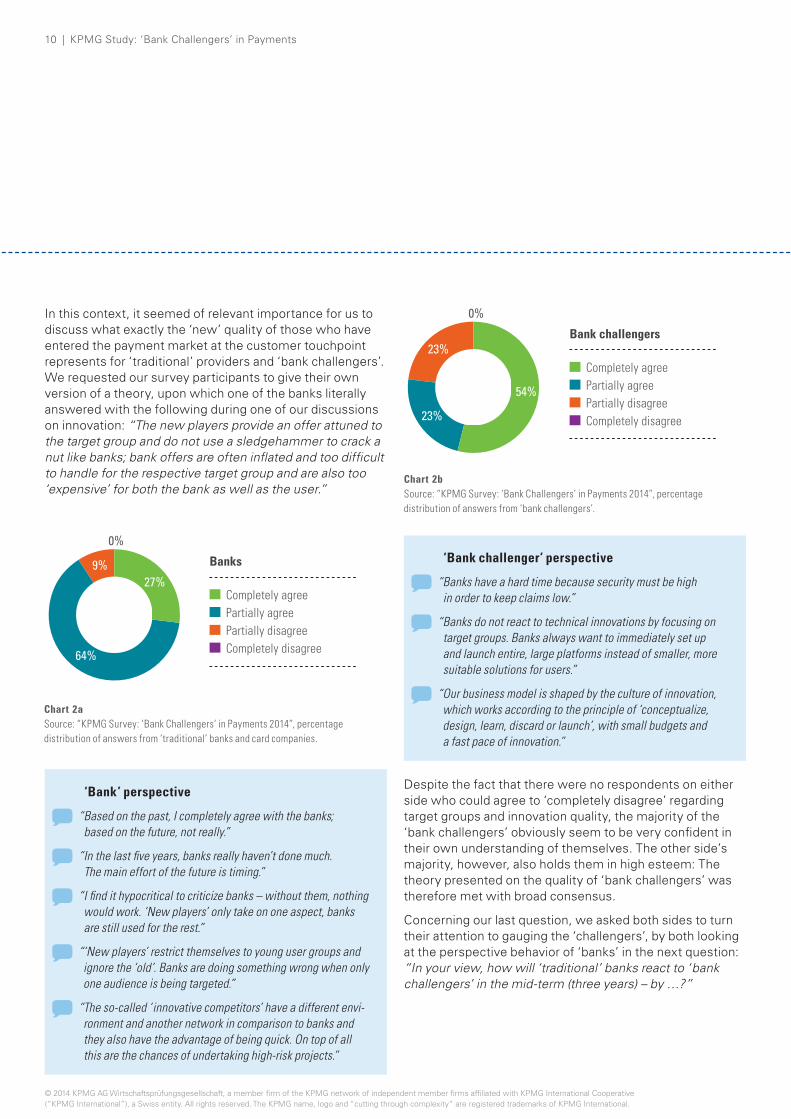

in this context, it seemed of relevant importance for us to discuss what exactly the ‘new’ quality of those who have entered the payment market at the customer touchpoint represents for ‘traditional’ providers and ‘bank challengers’. We requested our survey participants to give their own version of a theory, upon which one of the banks literally answered with the following during one of our discussions on innovation: “The new players provide an offer attuned to the target group and do not use a sledgehammer to crack a nut like banks; bank offers are often inflated and too difficult to handle for the respective target group and are also too ‘expensive’ for both the bank as well as the user.”

‘Bank’ perspective

“ Based on the past, I completely agree with the banks; based on the future, not really.”

“ In the last five years, banks really haven’t done much. The main effort of the future is timing.”

“ I find it hypocritical to criticize banks – without them, nothing would work. ‘New players’ only take on one aspect, banks are still used for the rest.”

“ ‘New players’ restrict themselves to young user groups and ignore the ‘old’. Banks are doing something wrong when only one audience is being targeted.”

“ The so-called ‘ innovative competitors’ have a different envi-ron ment and another network in comparison to banks and they also have the advantage of being quick. On top of all this are the chances of undertaking high-risk projects.”

‘Bank challenger’ perspective

“ Banks have a hard time because security must be high in order to keep claims low.”

“ Banks do not react to technical innovations by focusing on target groups. Banks always want to immediately set up and launch entire, large platforms instead of smaller, more suitable solutions for users.”

“ Our business model is shaped by the culture of innovation, which works according to the principle of ‘conceptualize, design, learn, discard or launch’, with small budgets and a fast pace of innovation.”

despite the fact that there were no respondents on either side who could agree to ‘completely disagree’ regarding target groups and innovation quality, the majority of the ‘bank challengers’ obviously seem to be very confident in their own understanding of themselves. The other side’s majority, however, also holds them in high esteem: The theory presented on the quality of ‘bank challengers’ was therefore met with broad consensus.

concerning our last question, we asked both sides to turn their attention to gauging the ‘challengers’, by both looking at the perspective behavior of ‘banks’ in the next question: “In your view, how will ‘traditional’ banks react to ‘bank challengers’ in the mid-term (three years) – by …?”

27%

64%

9%

0%

Banks

Completely agreePartially agreePartially disagreeCompletely disagree

Chart 2a Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of answers from ‘traditional’ banks and card companies.

54%

23%

23%

0%

Bank challengers

Completely agreePartially agreePartially disagreeCompletely disagree

Chart 2b Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of answers from ‘bank challengers’.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 11

‘Bank’ perspective

“ Bank challengers = innovators; banks = adapters. Banks will buy bank challengers in the long run.”

“ Acquisition, but within limits. Development of own models, but also in cooperation.”

“ Internal developments will only be undertaken by a few banks.”

“ Acquisitions and the development of own models are actually only a response to the potential (negative) threat. The only way of really suitably tackling the challenge is a cooperation.”

“ Innovation is key – a necessity of joint ventures and takeovers of start-ups in order to pick up momentum and speed.”

“ Bank challengers offer different chances for banks. Invest-ments in companies are plausible when they bring returns. So far it is questionable as to how banks can yield profits with bank challenger models – a business case?”

“ The business of payments is a network business. Collabora-tions – even with competitors – are the only way if you wish to succeed.”

“ The banks enter into partnerships as soon as they’ve realized where the market is heading. They have the customers and the network.”

‘Bank challenger’ perspective

“ The banks will try many things, but will not succeed and therefore cooperate.”

“ Collaborations require the least investment and solve all problems. Optionally, participation models are also conceivable.”

“ In the payments market, when one includes payments, there’s a long value chain and the companies work in cooperation – even when they are partly in competition with each other.”

“ The bank challengers are seen as rivals. That’s why banks don’t collaborate with them. Only once they are too large do they receive attention and then they are bought.”

The remarkable feature about the answers from both sides is that opinions are split in ‘three’ among the three prede-fined answer options: “Everything is possible in the mid-term. We’ll see,” as one bank officer put it in a nutshell. This ‘deadlock’ of opinions on the potential reaction of traditional providers also corresponds to the requirement expressed in the views of many respondents, more than the selection of one of the predefined options does. With-out wanting to over-interpret the data available, a slight preference for ‘cooperation’ still exists; between the two groups, there are also small shifts in relation to the other two answer categories: The challengers tend to believe in acquisitions more than the banks, and the challengers trust banks less in ‘developing their own models’ than banks do themselves.

26%

35%39%

Banks

CollaborationsAcquisitionsDevelopment of own model

Chart 3a Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of answers from ‘traditional’ banks and card companies.

32%

28%

40%

Bank challengers

CollaborationsAcquisitionsDevelopment of own model

Chart 3b Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of answers from ‘bank challengers’.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

12 | KPMG Study: ‘Bank challengers’ in Payments

The prevailing attitude, especially in relation to transaction banking, seems to be that the ‘banks’ can take a ‘wait-and-see’ position as it were knowing their investment strength. after all, with the future in mind, it would be the big banks and card companies that are financially well equipped to strengthen their position in any kind of market develop-ment.

Furthermore, consensus exists between the ‘bank chal-lengers’ and classical providers about the fundamental im-portance of collaborations in ‘network business payments’. in each of the two groups, around 80 percent of the respon-dents see cooperation as being at least ‘very important’ or even as ‘indispensable’ – and that’s the way they also see it being for the future of the payments market. Further larger collaborations, especially when data security is concerned, are more or less desired: “This makes business easier.”

The obvious question to be asked here is why the ‘bank challengers’ selected a field such as the payments market for their business operations where in fact it is very difficult to earn money: “Nobody willing makes payments.” The possible responses to this question are multifaceted. The ‘official’ answer most widely given was that within the ‘value chain of payment’, many small specialist provid ers of payment services for retail customers apparently rely on their innovative services proving so successful in the medium term, that different cooperation models with banks, credit card companies or others (i.e. larger payment service providers) will eventually present themselves. only behind closed doors does talk also center on the topic that quite a few start-ups hope to be bought up one day. other ‘bank challengers’ are so convinced of the quality of their payment solution that they firmly believe they’ll come out on top in this difficult market (see also chapter 2 ‘Market development’). at any rate, KPMG also holds the view that only a few of the many smaller players and payment models currently existing in this market can survive over the long term.

The answer probably most worth considering as to why the ‘bank challengers’ want in on this market, points in another dimension of the future, however. “The new providers only want to gain access to customer data or rather liquidity. They don’t actually want to engage in payments.” With the global mega-trend of ever-expanding rapid digitalization, the ‘value chain’ (conventionally understood as payment until now) is merging with so-called ‘value-added services’ from upstream or downstream areas or is crossing over into areas completely unknown to payments in the past. For the drivers behind electronic innovations and their eco-nom ic implications, catchwords, such as ‘big data’ and ‘data analytics’, to ‘e-commerce and m-commerce’, to ‘brands’ as well as to pretty much everything which is associated or which could be associated with ‘social networks’, were often mentioned. consequently, the first thoughts here are about any transaction data as well as about any customer data connected with transactions that could have any value in the age of digitalization. Following this logic, money is no longer primarily earned through actual payments but rather through the data generated as a result (see also chapter 3, chart 13).

in this respect, many of the respondents show serious concern, but nevertheless declare this as ‘unlikely’ or ‘theoretically only conceivable’: it’s plausible that the large ‘internet ecosystems’ from amazon to apple to Facebook and Google could offer comprehensive services to their customers or the market, notably without having to gen-erate revenue from payments at first. Therefore, it is a recurring issue in the industry that those companies, which already have the ‘brand’ and thus also the ‘custom ers’ in the age of the internet, could also offer payments as an additional service and customer retention instrument, which they could then operate single-handedly. Given a common underlying uncertainty, this situation seems a little like the popular saying ‘whistling in the dark’, when one sees themselves as being the future ‘potential cooperation partner’ for internet giants or believes that their business model can adjust itself to the actions of the others ‘de-pending on the case’. Thus, assuming there could even tu-ally be completely different and suddenly relevant players in the payments market of tomorrow:

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 13

“In relation to your business or business model, do you see the large ‘ internet ecosystems’ (Google/Facebook/Amazon/Apple) as being …“

‘Bank’ perspective

“ They bring us business – they grow, we grow.”

“ We see them as clients. We also see them as competitors, however, if they were to offer new solutions.”

“ In principle, Google/Facebook/Apple could definitely develop B2B solutions.”

“ Something new may arise; in the end, it’s all about acceptance.”

‘Bank challenger’ perspective

“ They have potential thanks to the high number of users. When they do something, then it’s done thoroughly, meaning it will be relevant for the market.”

“ We are payment providers. The corporates need payments in order to populate their own ecosystem. A critical eye must be kept on this.”

“ We don’t expect that Google wants to enter into regulated banking. If Google, Apple or Facebook want to establish independent ecosystems, they’ll strive to operate far away from banking supervisors.”

“ Do we know whether Facebook or Google is a long-term friend or foe …? No! We live with this situation. Can Facebook or Google decide otherwise tomorrow: Yes!”

drawing on the ‘deadlock’ of answers provided, there’s a certain degree of uncertainty, not only about the behavior of internet giants, but also about the upheavals in the ‘value chain of payment’ which might emanate from the customer touchpoint. concerning our questions on how the ‘men-tality’ behind the large internet ecosystems is perceived – as well as during our talks on what drives the ‘bank chal-lengers’ (see chart 2a and 2b) – it was made very apparent just how far awareness has spread among ‘the banks’ that there is another predominant type of customer and market perception among the ‘new players’. Based on the previous actions of ‘Apple, Google & Co.’, traditional financial service providers have clearly realized that in comparison to their previous customer understanding, there has been a change in perspective: The internet companies as well as the ‘bank challengers’ first ask “What does the customer want?” and then develop their products for the market. in contrast, the traditional players up until now have asked “What does the market want?” and then based on a step conceived upstream on the conveyance of marketability, they then develop their products which they offer to their (potential) customers.

50%

4% 15%

31%

All answers

Potential competitorsPotential cooperation partnersVariableCompanies that do not affect my business

Chart 4 Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of all answers.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

14 | KPMG Study: ‘Bank challengers’ in Payments

2“ The market will have completely changed

in ten years!”

The Market Development

How and in which direction is the payments market de vel-op ing? That the market is changing and will continue to change is something all respondents say. But not by leaps and bounds or ‘non-disruptively’ within the next three years. in the medium term, banks will lose moderate market shares at most – but to whom: This is where opinions diverge, above all, in respect to card and telecommuni-cations companies. However, the opinion given here – not in response to a question asked, but instead as a long-term view repeatedly raised in the comments of the study par-ticipants – takes a much more aggressive stance.

‘Bank’ perspective

“ A shift within the banks shall occur.”

“ In Western Europe, card companies together with payment service providers will significantly expand their market shares.”

“ Card companies will be the big losers. No future- oriented product portfolio or range of products.”

“ Telecommunications companies don’t stand a chance in this market and have no prospects to grow.”

“ Telecommunications companies will grow considerably.”

‘Bank challenger’ perspective

“ The trend is moving from banks to card companies.”

“ Banks will lose big time. Card companies will increase transaction volumes, but fees will drop. Payment providers for internet and mobile payment will grow.”

“ We are convinced that the German market will continue to be dominated by providers with a banking license.”

While the forecast for the future generally only predicts relatively small shifts in the medium term, one group of survey respondents used this question about the future to – in our opinion – spark an insightful and in-depth discus-sion about what will define their business in the mid-term: the business in transaction banking.

“ From the total transaction volume in Germany, how do you think the distribution of market shares for payment services or payment methods is today? And how will these market shares distribute in the medium term (in three years) …?”

Each competitor’s market share of the total transaction volume of payment services

Today as percent of the total German market

Medium term (three years) as percent of the total German market

Banks 79% 72%

Card companies 13% 15%

Payment providers for internet and mobile payment

5% 9%

Telecommunications providers

1% 2%

Other 1% 1%

Chart 5 Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of all answers.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 15

‘Bank’ perspective

“ The European map will change in the medium term: Things will get less clearer in respect to the clearing of payments, but instead there will be greater standardization; it will be quicker and cheaper to process payments; XML formats in other currencies, not only in EUR, driven by customer re quire ments and by standardization, too; the per spec tive focuses primarily on fees, in terms of pressure exerted on margins; cost-efficient infrastructures, after all, IT is the main driver of synergies, costs and margins.”

For example, specific trends identified by participants include further standardized, consistently structured formats in place of financial information (e.g. in the case of payments: today = SePa, tomorrow = Global XMl/cGi) and thus also include better exploitation of the opportuni-ties offered through digitalization. This also includes trends such as electronic bank account management (eBaM), standardized bank billing services (TWiST) or ‘virtual accounts’, which reduce the number of accounts for corporates. inter na tion ally active institutions, above all, don’t only emphasize cost-effectiveness and process efficiency as factors of success, but also international harmonization as well as flexibility in particular.

a specific example here are the currently much-discussed customer benefits of a ‘payment factory for everyone’: if ‘ large caps’ in particular have a payment factory (i.e. cen-tralization of outgoing payments) in place today, it’s also worth setting up a payment factory for international midsize corps active in various countries by way of SePa, uniform regulations and high-performance treasury systems. Thanks to SePa, cross-border direct debit also exists for the first time, upon which the centralization of incoming payments is also achieving greater attention under the heading of ‘collection factory’.

‘Bank’ perspective

“ Internationally, we see a trend towards payment factories and shared service centers.”

“ Our business model today in the area of payments is aimed at setting up a comprehensive support approach (e.g. payment factory). The increasing harmonization of formats in payments and the standardization/simplification are leading to the need for connectivity (e.g. SWIFT) and are making payment factories increasingly attractive even for SMEs.”

“ Payment factories will come, but not within the next three years.”

“ A payment factory for everyone – even for smaller corporates.”

Such trends are likely to make further waves in the trans-action banking market, although a number of established providers would actually prefer to shy way from the costs associated with some initiatives (e.g. eBaM, TWiST): “Something like this only costs money at the moment …” interestingly enough, some corporates are calling for de vel-op ments such as these so intensively right now that banks feel forced to address the wishes of their customers. in this sense, the transition already mentioned above also leads to an increased focus on customers in transaction banking. customers benefit from added value, in particular, for the processing of payments and the treasury function on a whole, not just apparently because of a ‘change in attitude’ here, but also because of tangible initiatives.

in relation to actual feasibility, we ventured to ask our respondents just once for the requirements they’d like to see: “If tomorrow you could build a payments company from the ground up: How would your IT environment look …?”

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

16 | KPMG Study: ‘Bank challengers’ in Payments

‘Bank’ perspective

“ Actually, a new bank would have to be established with completely new IT in order to have an innovative platform. But in order to do this, a whole lot of money is needed, and nobody is really ready to risk that …”

“ It’s not only essential to have great ideas; a bank must also be able to realize these ideas – one’s own IT is usually more of a hindrance here …”

“ A core banking scheme in Germany and the EU, a payment platform, a set of solution components which can be used in a customer-oriented manner (plug & play), no legacy systems, just pure digitalization.”

“ Custom-made IT, tailored to your own needs. Expansion for the payments of upstream and downstream products. Image of the entire value chain from the customer’s order right through to transaction completion.”

in response to the question, what is the basis for the iT environment of the future, there’s a common answer: ‘end the suffering from legacy systems’. almost all pay-ment service pro viders dream of the moment when they’ll be allowed to quickly and efficiently offer new or adapted products which really meet customer needs through a freely scalable new iT platform: “What does the corporate client need in order to reliably carry out their specific business, and then afterward to design their own IT, to the latest state-of-the-art specifications …” Module iT of the future will provide unrestricted flexibility, making it also possible to initiate payments using any medium.

With such wishes in mind, the reality of payments in corporate banking is not so much about real ‘ large’ inno-vations in the medium term but ultimately about gradual inventions for corporates. on the other hand, the changes predicted to take place through innovations in ‘mobile pay-ment’ are universally regarded as being promising for the future growth market in the retail sector. But here, too, a few individuals give careful consideration that – in con trast to over-optimistic outlooks – there may be a ‘transition market’ only generating a few ‘new’ transactions, but whose growth is much more the result of shifts in the entire market.

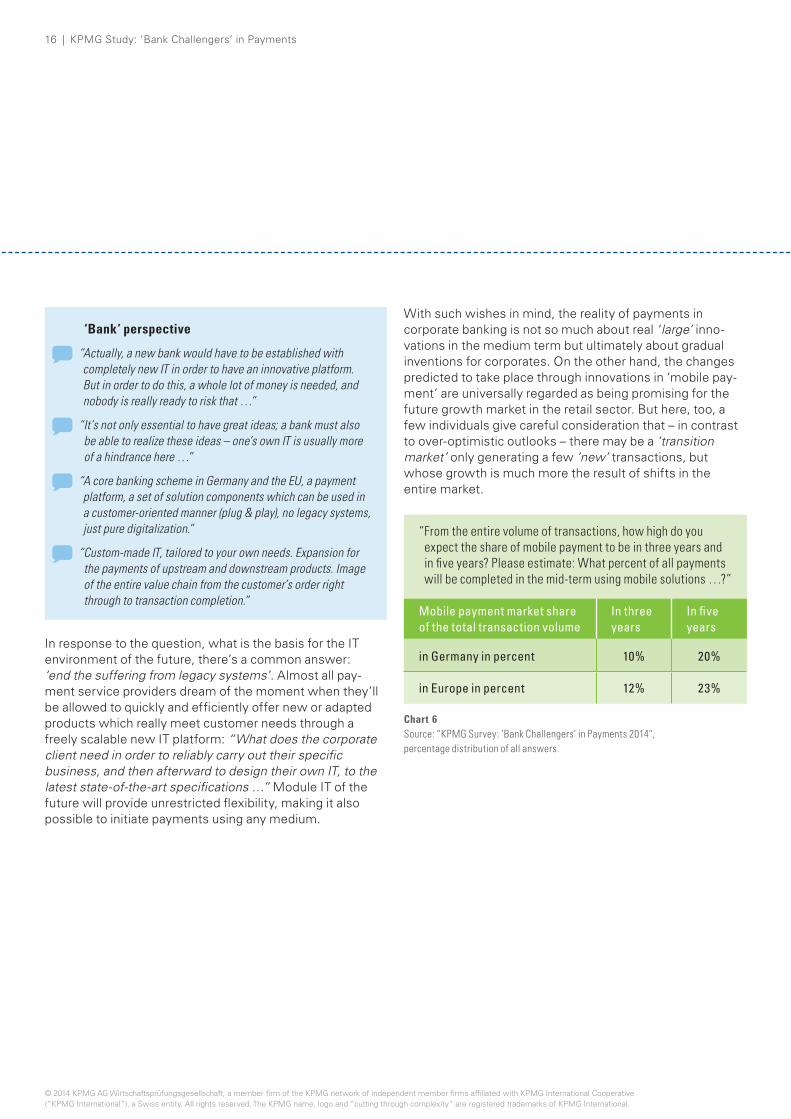

“ From the entire volume of transactions, how high do you expect the share of mobile payment to be in three years and in five years? Please estimate: What percent of all payments will be completed in the mid-term using mobile solutions …?”

Mobile payment market share of the total transaction volume

In three years

In five years

in Germany in percent 10% 20%

in Europe in percent 12% 23%

Chart 6 Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of all answers.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 17

‘Bank’ perspective

“ The growth rates are rather high. The use of mobile payment will drastically increase.”

“ Huge growth will occur quickly among the younger gen er a-tion; the older generation will soon follow thereafter.”

“ Germany trails behind in comparison to Anglo-Saxons. There’s a skeptical mentality toward mobile payment in Germany – no trust.”

“ I haven’t yet seen a successful mobile payment project.”

‘Bank challenger’ perspective

“ No German bank today is capable of realizing mobile payment!”

“ Loss of market shares does not occur overnight; this however will be the case for future generations because they are growing up differently.”

“ The increase in Europe will be greater in five years, due to the fact that regulatory requirements are lower in other countries than as in Germany and solutions prevail quicker and therefore usage expands more quickly.”

after all: Growth in ‘mobile payment’ is emphasized by everyone – ‘bank challengers’, as it is to be expected, have considerably more optimistic expectations of growth rates than established providers.

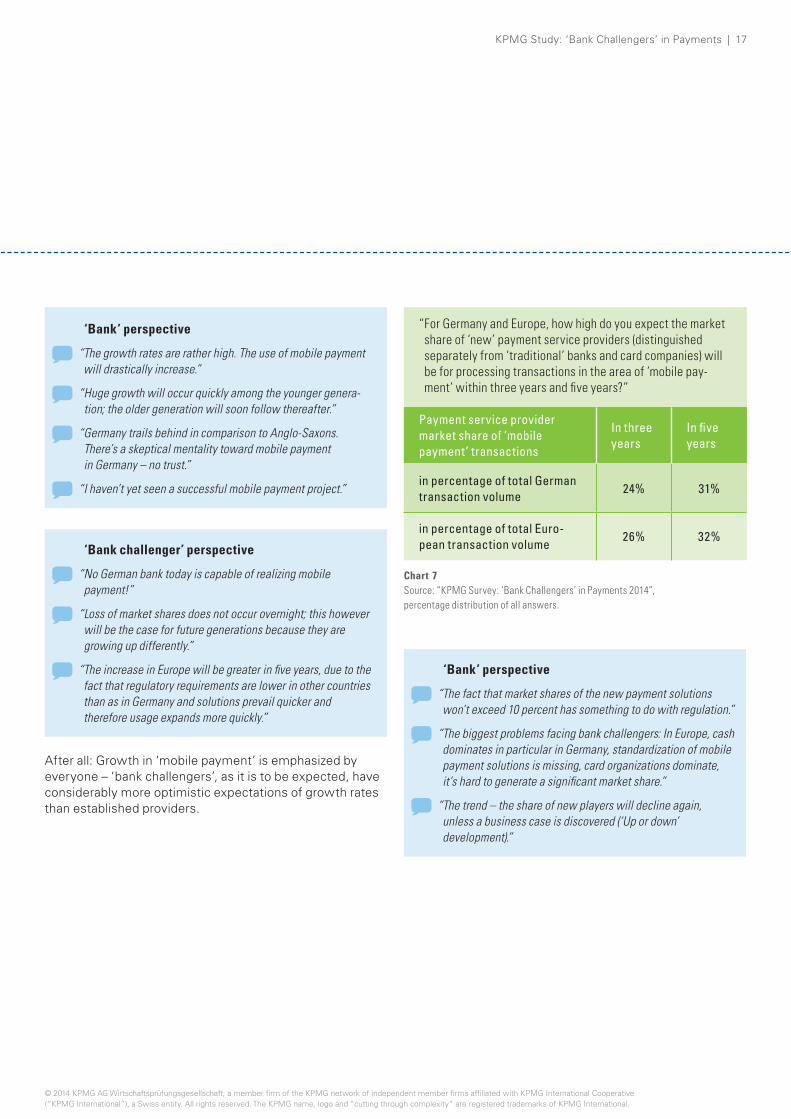

“ For Germany and Europe, how high do you expect the market share of ‘new’ payment service providers (distinguished separately from ‘traditional’ banks and card companies) will be for processing transactions in the area of ‘mobile pay-ment’ within three years and five years?”

Payment service provider market share of ‘mobile payment’ transactions

In three years

In five years

in percentage of total German transaction volume

24% 31%

in percentage of total European transaction volume

26% 32%

Chart 7 Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of all answers.

‘Bank’ perspective

“ The fact that market shares of the new payment solutions won’t exceed 10 percent has something to do with regulation.”

“ The biggest problems facing bank challengers: In Europe, cash dominates in particular in Germany, standardization of mobile payment solutions is missing, card organizations dominate, it’s hard to generate a significant market share.”

“ The trend – the share of new players will decline again, unless a business case is discovered (‘Up or down’ development).”

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

18 | KPMG Study: ‘Bank challengers’ in Payments

‘Bank challenger’ perspective

“ A steady rise can be expected in Germany; in some countries the rise will be steeper.”

“ The banks won’t gather the momentum to develop adequate solutions. That’s why payment service providers will proliferate.”

“ In Germany and internationally, banks will have to jump on the bandwagon, if they want to mean anything in the world of mobile payment.”

“ In terms of acceptance, the new payment service providers will process a high percentage of transactions: +80 percent. As far as issuing is concerned, card companies and banks will continue to stay in control, but also here new payment service providers will be able to achieve a relevant market share.”

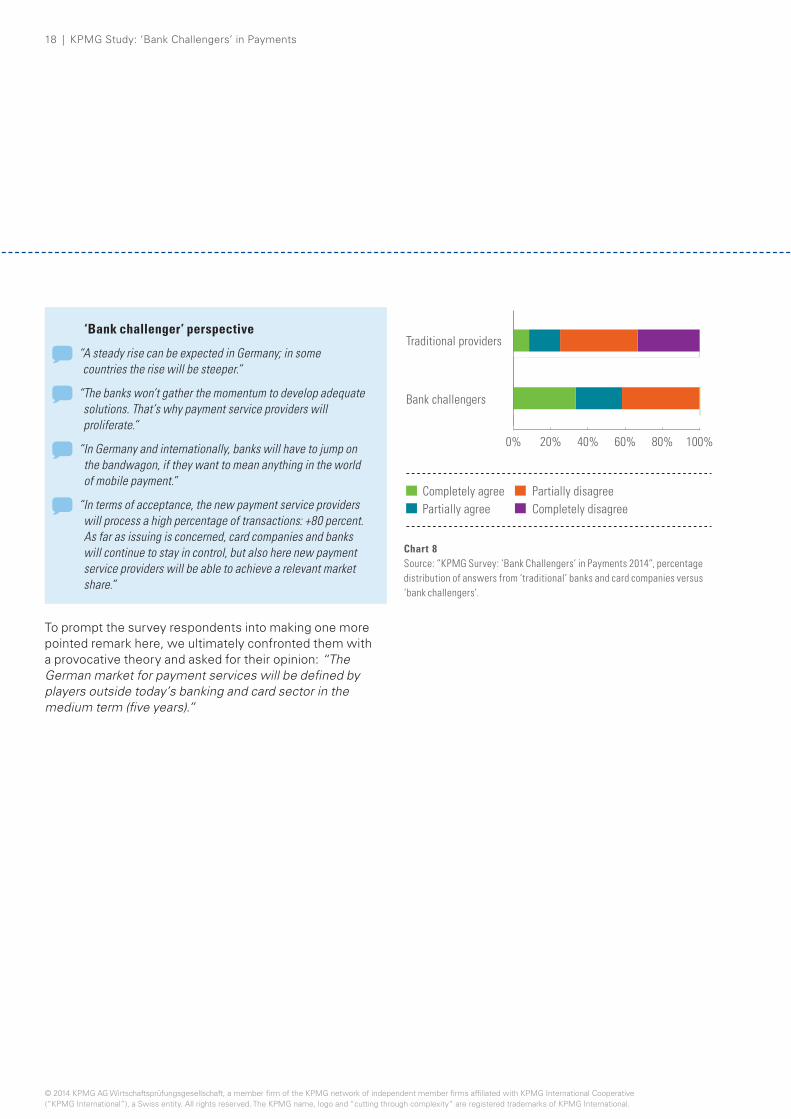

To prompt the survey respondents into making one more pointed remark here, we ultimately confronted them with a provocative theory and asked for their opinion: “The German market for payment services will be defined by players outside today’s banking and card sector in the medium term (five years).”

Partially disagreeCompletely disagree

0% 20% 40% 60% 80% 100%

Bank challengers

Traditional providers

Completely agreePartially agree

Chart 8Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of answers from ‘traditional’ banks and card companies versus ‘bank challengers’.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 19

‘Bank’ perspective

“ Overall, this doesn’t really apply to Germany. The market, however, is diverse, and some aspects could already be covered by innovative approaches.”

“ National schemes lose, international schemes win. There won’t be any overarching solutions any time soon.”

“ Payment is the business of banks. Without banks, it just won’t work!”

“ Five years is too short a period of time. The new players are still far away from the critical mass required to define this market.”

“ It will be difficult for ‘players’ outside the current banking and card sector, because their network and infrastructure cannot be compared to the traditional sector.”

“ There is great impetus in the market for payments, with clear potential for players outside the banking sector; at least, at present.”

“ I agree that bank challengers have huge potential when it comes to the way we see payments in the future. But I still think, that they will only gain a limited market share. At least, I hope that the banks will wake up in the meantime and prepare themselves.”

“ The market will have completely changed in ten years.”

‘Bank challenger’ perspective

“ There will be new providers, but they won’t be any main decision-makers, since the old players will continue to stay in business.”

“ Others will shape the future, but banks will still provide the bank account.”

“ Banks will continue to be there with the bank account, but they’re going to lose the payments market.”

“ It doesn’t matter to consumers who is behind the payment.”

The ‘banks’ strong rejection of this theory stems from the self-confident attitude of some banks towards ‘bank challengers’. This group is entering the market to change it under new conditions and circumstances – a market in which technical solutions rapidly intensify and consumer behavior changes business.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

20 | KPMG Study: ‘Bank challengers’ in Payments

The Market Evaluation“Digitalization influences the way people pay.”

3

To gain an overview of the market opinions of our survey participants, we asked them to give their own point of view by evaluating and rating the three drivers most com-monly mentioned in the discussions on innovation as being relevant to the mid-term development of payments: ‘customer behavior and demands’, ‘technological inno-vations’ as well as ‘regulations’. it’s worth noting here, that these three drivers were largely confirmed (partially explicitly) to us as being relevant for future market devel-opment, in the comments provided alongside the survey answers. (The subject of ‘regulations’ is referred to in detail once again – see chapter 4.) Survey participants also men-tioned ‘transaction costs’, ‘merchant acceptance’ and ‘competition’ as being other notable drivers of development.

The answers to the question whether mid-term develop-ment in payments will be driven by three defined factors and which one of them is ‘the most important’ are dis -tributed as follow:

‘Bank’ perspective

“ The most important driver is the customer. Everything else is just ‘tactical maneuvering’; added value must exist. Today, however, development is driven by technical achievements.”

“ A small number of customers is very active. The majority however behaves conservatively.”

“ Only when business models are developed beyond tech nology will they survive a term of three years.”

“ Money and innovation always go hand in hand. Unfor tunate ly, none of the customers are willing to pay for innovations.”

0% 20% 40% 60% 80% 100%

Regulations

Technological innovations

Customer behavior and demands

Banks

Partially disagreeCompletely disagree

Completely agreePartially agree

75%

25%

0%

Banks: most important driver

Customer behavior and demands

Technological innovationsRegulations

Chart 9aSource: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of answers from ‘traditional’ banks and card companies.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 21

‘Bank challenger’ perspective

“ Only what customers will use makes sense.”

“ The customer is the key to penetrating the market against traditional payment providers.”

“ The risks lie in technical development. These develop faster than human habits change. Technical achievements are currently way ahead of habits and thus the willingness to use new solutions.”

Perhaps the most striking result from the evaluation of the questions is a significant difference in the rating of the ‘most important’ drivers for mid-term development: ‘technological development’, despite being seen by the majority as a driver with ratings ranging between ‘com-pletely’ agree to ‘moderately’ agree, is given no preference by ‘traditional’ payment service providers as the ‘most im-portant’ driver. Three-quarters of the traditional providers rate ‘customer behavior’ as being the most important; in

principle, this result also matches the general rating of the ‘bank challengers’, but with the difference that they give technological development a much higher rating. The astonishing part here is that while it may be true that all ‘bank challengers’ prioritize customers and stipulate ‘added value’ and ‘benefits’, at least one-third still than switched to technology when answering the question about the ‘most important’ drivers.

With regard to technical innovations in payments, many ‘traditional’ respondents ask the question whether they must lead the way as the ‘pioneer’ in the market or whether it’s not enough if they react as the ‘follower’ and then first adopt innovations once they have demonstrated their mar-ket maturity. “Germany is more sluggish, that’s why ‘speed-boats’ can be calmly observed racing along.” others are concerned whether there’s enough time left in the future to behave so cautiously given the imminent cycles of inno-vation which will most likely occur in the next few years.

Bank challengers

0% 20% 40% 60% 80% 100%

Regulations

Technological innovations

Customer behavior and demands

Partially disagreeCompletely disagree

Completely agreePartially agree

42%

25%

33%

Bank challengers: most important driver

Customer behavior and demands

Technological innovationsRegulations

Chart 9bSource: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of answers from ‘bank challengers’.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

22 | KPMG Study: ‘Bank challengers’ in Payments

‘Bank’ perspective

“ Digitalization is on the rise – this is influencing the way people pay.”

“ Innovative products will prevail given adequate customer education and advertising.”

“ Innovation has advanced, awareness has been established, more and more people are concerned with innovation – and the generational transition takes care of the rest.”

‘Bank challenger’ perspective

“ Technology is not decided by usability. Retailer requirements are relevant when it comes to the question of the capabilities of technology. Crucial factors are the customer’s needs as well as the retail expenses.”

“ It’s a supplier market today in mobile payment; the need for education among consumers and retailers exists.”

Technological and product innovations in payments are relevant factors in interplay with digitalization and demo-graphic development, provided that – from all sides – the focus is really directed towards ‘proximity to customers’ and ‘customer benefits’. Whether the customer here knows what their ‘needs’ are, or whether they must first be told, is – as the case may be – an ‘all too familiar’ discussion on the ‘gullibility’ and ‘clarification’ of consumers: at any rate, the general agreement here is that such innovations will first lead to gradually increasing numbers of users, espe-cially among the younger generations. This is accompanied by a change in cultural attitudes towards payment behavior, which in turn should then positively affect the accelerated implementation of mobile payment. especially from the side of bank challengers, it’s assumed in this context that the rate of innovation will definitely continue to rise and that it’s a crucial competitive advantage in the future to be able to quickly react as a payment service provider.

in this context, we asked the respondents for their opinions on a theory about the behavior of consumers today and requested them to give possible opportunities for further development:

“What is your personal opinion of the following theory: Most consumers already have a sound portfolio of payment methods they are using and show little or no interest in expanding it in the future.”

‘Bank’ perspective

“ Yet, consumers do want different ways to pay. They just have to be ensured that they can make payments anywhere using the payment means of their choice: hence, the infrastructures for contactless payments must be established, retailers must participate, and the banks must offer the solutions.”

“ Consumers don’t know what they really want, because they can’t imagine which products and solutions are possible.”

“ People in general don’t like change. But the people who like change are the front-runners – and a study found: In the customer’s mind, a product must be around ten times better than the old one …”

31%

35%

30%

4% All answers

Completely agreePartially agreePartially disagreeCompletely disagree

Chart 10Source: “KPMG Survey: ‘Bank Challengers’ in Payments 2014”, percentage distribution of all answers.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 23

‘Bank challenger’ perspective

“ Yes, but both interact with each other: the existing port-folio PLUS prospective, new methods.”

“ No customer needs, no change. Only things that make sense will convince customers.”

“ Additional value must be created. This can be done through the price, coupons or something else – trust and security as conditions.”

“ From the user’s perspective, there’s one guiding principle: ‘I want to have it simply easy.’”

The majority of survey participants believe that the current ‘fixed portfolio of utilized payment methods’ represents a clear obstacle to innovation in the payments market. The request to give their opinion on this theory was followed-up by asking an additional question: “And what in your opinion must happen so that consumers – regardless of how – change their payment behavior …?” in order to get cus-tomers to change their payment behavior, it’s obvious to all respondents that customers must be able to clearly iden-tify some kind of additional value in the new appli cation: Whether it’s pecuniary advantages such as low costs, coupons, a loyalty program or vouchers; whether it’s basic ‘convenience’ such as ‘the customer not wanting to queue up while shopping, for example.’; whether it’s value-added services such as ‘monitoring of expenditures’; or wheth er it’s basic ‘simplicity (usability)’ in the use of new products. consequently, real ‘problem solutions’ combined with ‘value-added services’ must be generated, offered and ad-vertised so that consumers are motivated to use new pay-ment methods. “This can also be achieved through tech nol-ogy and the removal of barriers.” Finally, it was noted that a new procedure must also be ‘fun’ and seem ‘cool’ to younger generations.

However, the basic prerequisite for everything remains that the customer can trust in the security of the procedure, because: the ‘perception of security’ is important. “For Germans, banks will remain the first choice when it comes to the question of trust,”: a statement made by banks, to which we more or less heard something similar on multiple occasions. Trust is your ‘core asset’.

Beyond a doubt, the big advantage of ‘traditional’ providers is that they have built up confidence in the security of their payment solutions over decades through their relations to customers. The question is only whether they can also fundamentally set themselves apart on the market in future.

‘Bank’ perspective

“ Payments service is a product of convenience. Customers don’t think so much about risks of fraud or trust; the topic of security is not at the top either. This is not critical in payments; it’s about convenience: ‘How can I make payments without much effort.’ (e.g. entering credit card number or a PIN, etc. is already too much).”

‘Bank challenger’ perspective

“ In future, it will be more and more about convenience. The factor of convenience is extremely important. And this means that a cross-channel offer must really be able to be used everywhere. At the same time, the benefit must also be put to the fore. A solution, which comes from a completely different direction and which is laden with ‘payment’, won’t win recognition.”

There is a broad consensus among all study participants regarding the success factors essential for a product’s market acceptance (from the point of users as well as vendor outlets) in the payments area; only in respect to the ratings and the hierarchization of such factors are there divergences. While ‘security’, ‘usability’ and ‘processing time’ are named as the most common criteria for cus-tomers, ‘costs’ (transparency of costs and low costs), ‘process efficiency’ (simple integration of iT, terminals, retailer process as well as payment guarantee) and ‘cus-tomer loyalty/market penetration’ are the most common criteria for vendor outlets or retailers.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

24 | KPMG Study: ‘Bank challengers’ in Payments

as expected, the subject of ‘convenience versus security’ was brought up to such a frequent extent during our dis cus-sions on innovation, that we requested our participants to comment on the following: “How do you judge ‘security’ with respect to the tension between convenience and user acceptance of new payment methods? Keywords, for exam-ple: regulatory requirements versus ‘shopping experience’. How could both requirements be reconciled with each other?” Without security, it’s not possible – for regulatory reasons alone – that’s something everybody agrees on. in addition, a common denominator among all answers is that there must be a ‘balance between security and conve-nience’ for the users. interestingly enough, in relation to this balance, it’s plain to see that something like a state of push and pull exists between the objections made by the different sides: ‘The banks’ always prefer the aspect of security, whereas most ‘bank challengers’ argue from the point of the user and see convenience as being more important.

‘Bank’ perspective

“ Compared with bank challengers, banks can offer the highest security standards. After all, they’ve dealt intensively with the issue of security for years.”

“ Security is the most important thing: The difference between technical security, objective security and perceived security is that the latter must be high. The user must be convinced that the payment is secure. This applies, above all, to Germany.”

“ Security is fundamental. When something’s not convenient, then the products aren’t used. The regulatory system points the way, but isn’t the showstopper.”

‘Bank challenger’ perspective

“ A certain level of security is necessary, but convenience wins. Take a look at Facebook/WhatsApp.”

“ Data privacy is important for providers. Convenience for users.”

“ Regulation must exist, but it must specify a realistic objec-tive. The idea of ‘strong authentication’ and the inconvenient requirement of having ‘something additional’ with me and having to use it, is not accepted by users: user acceptance is not low, but non-existent.”

a different reference made was that the subjective percep-tion is what matters for users. in the realm of regulatory provisions given, data privacy depends on the person and situation: “Some are very careless with this.” as the expe-rience of our study participants shows, the common set of beliefs supposedly prevailing across Germany about secu-rity concerns frequently takes a secondary role when it comes to specific payments. “If the customer wants a bargain, then they want to have it quickly.” Whether it’s an auction or whether it’s a limited special offer – the customer is readily using mobile payment already today, despite all the concerns raised about security in surveys.

Based on practical experience, it was therefore recom-mended to look at security as depending on the amount in question: if data security in payment can be defined as the authorization of a transaction, the tension between ‘secu-rity versus convenience’ can be handled in a flexible man-ner in this respect. different security levels and require-ments, for example, could be assigned according to amounts so that no authorization is required when pur-chasing small amounts. and the customer should also be able to have a say in which level of security (and the value of the amount) they want to have, so that additional secu-rity features can be offered to ‘very safety-conscious’ customers.

in relation to the development of the usage of payment methods, all respondents expect that the use of cash will continuously decline in coming years (estimated at around 1.5 percent p.a.). it may be true that cash won’t be replaced ‘overnight’, but it’s presumed that this gradual decline will be accelerated over time given the mega-trends of digitali-zation and demographic development.

Both sides agree that hardly any payment method will ‘disappear’ within the next three years. according to the majority, however, cash cards, checks and cash on deliv-ery also don’t have a future anymore. Moreover, our study participants all share the same view that it’s only a matter of time until contactless payment – in any form what so-ever – takes hold.

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks of KPMG International.

KPMG Study: ‘Bank challengers’ in Payments | 25

‘Bank challenger’ perspective

“ Bank accounts will always exist. The focus will continue to be on debit and credit cards, but at some point the smart-phone will replace the card as the carrier medium.”

“ Plastic cards will decline and be replaced by mobile phones/wearables (watches/eyeglasses, other interfaces). Credit cards will disappear, but not the companies, since they connect bank accounts to retailers.”

“ Traditional credit transfers and direct debits will suffer because of the increased complexity through SEPA. Online bank transfers for the checkout will also be less marketable.”

“ New payment methods will be introduced by traditional instruments. The essential factor of success thereby will be ‘usability’ (i.e. the ease of use) for both retailers as well as for consumers. For retailers, the cost model from card providers will represent a significant risk to the already low margins. Here, new payment providers with lower cost structures will establish themselves.”

Which products will come out on top in payments over the long run, is in the opinion of the study participants, still debatable. The majority agree that direct debit as well as prepaid solutions will decline. For some respondents, quick credit transfers and direct transfers appear as being ‘viable for the future’. although opposite responses were also given, a clear majority of the participants think that credit cards and debit cards – which up until now have under-performed in Germany as compared with other european countries – will gain greater acceptance in their range of functions: “Customers want to increasingly pay by card.” The only thing is that there is often serious doubt as to if ‘plastic’ will survive as a carrier medium.

The extent to which the implementation of products in payments is tied to a specific technology is an open topic. The software and hardware channels used are of secondary importance to the survey participants – what matters is that one or two solutions are widely accepted by cus tomers and retailers. in relation to this primary requirement for accep-tance, reference was repeatedly made that technology itself – current topics of discussion: near field communica-tion (nFc), Bluetooth low energy, Qr codes, Beacon – is actually ‘only a channel’. as to whether nFc – which is

acknowledged as standing the greatest chance – will really gain acceptance is where a divergence of opinions occurs; in total, based on our answers, it’s the skeptics who outweigh the clear supporters.

‘Bank challenger’ perspective

“ NFC won’t come out on top. It’s a technology, not a strategy. Internet, cloud-based, that’s the future.”

“ Think about the applications in terms of the checkout pro-cess: No additional charges must exist and it must be able to be used everywhere (tickets, food, restaurants, textiles, etc.)”

“ Channel access and seamless media continuity ensure customer acceptance and thereby market acceptance as well.”

“ Consumer behavior is constantly changing – from a so-called technical point of view through mobile phones, smartphones and technical gadgets. I can’t tell customers what they should use or do and not do.”

From the respondents’ point of view, there is no dispute that the bank account will remain the ‘nucleus’ of all pay-ment methods – which services will be connected to it, however, is the subject of many deliberations.