bank bonds: regulatory issues

TRANSCRIPT

BANK BONDS: REGULATORY ISSUES

Senior bail-in and TLAC/MREL - Update

Natalie Tehrani Monfared, Senior Credit Analyst (UniCredit Bank)

18 October 2016

2

AGENDA

• TLAC AND MREL

• SENIOR BAIL-IN

3

Introduction

• On 1 January 2015, the Bank Recovery and Resolution Directive (BRRD) took effect • The BRRD requires banks in the EU to fulfill minimum requirements for own funds and eligible liabilities (MREL) • Currently, the following applies: ‒ MREL applies to all banks in the EU that are not global systemically important banks ‒ MREL is a Pillar 2 requirement ‒ The requirements have to be fulfilled since 1 January 2016 with a possible transitional period of 48 months ‒ MREL(%) = (own funds + eligible liabilities) / (total assets) ‒ MREL is determined by the resolution authority on a individual level and on the highest EU consolidation level

• However, it is already known that the MREL requirements will be amended by the European Commission

• In November 2015, the Financial Stability Board (FSB) published principles for the total loss-absorbing capacity (TLAC) of global systemically important banks (G-SIBs)

• The main principles are as follows: ‒ TLAC applies to G-SIBs (consolidated group) ‒ TLAC is a Pillar 1 requirement, however, an bank-specific Pillar 2 add-on is possible ‒ The requirements have to fulfilled as of 1 January 2019 (respectively 1 January 2022) ‒ The TLAC calculation is based on risk-weighted assets (RWAs) and the leverage ratio denominator ‒ External TLAC must be at least 16% (18%) of RWAs as of 2019 (2022) and 6% (6.75%) of the leverage ratio

denominator as of 2019 (2022)

TLAC and MREL

4

TLAC and MREL

• TLAC

• MREL

5

TLAC term sheet

• The TLAC requirements are set out in a detailed set of principles and a term sheet • TLAC incorporates existing Basel III minimum capital requirements and excludes Basel III capital buffers, i.e. capital

that counts towards a buffer cannot count towards satisfying the TLAC requirements • TLAC is a Pillar 1 requirement, however, an bank-specific add-on is possible (Pillar 2) • TLAC will be set on a (consolidated) group-basis subject to minimum requirements ‒ The external minimum requirements apply for each resolution entity within a G-SIB group ‒ The internal minimum requirements apply to material subsidiaries in the group

• The minimum external TLAC requirements are as follows: ‒ as of 1 January 2019: 16% of the group’s RWAs and 6% of the Basel III leverage ratio denominator ‒ as of 1 January 2022: 18% of the group’s RWAs and 6.75% of the Basel III leverage ratio denominator

• Material subsidiaries must meet an internal TLAC that is pre-positioned on-balance sheet and is 75-90% of the external TLAC requirement

• According to the FSB, there is an expectation that at least a third of TLAC consists of debt instruments

TLAC and MREL

6

TLAC-eligible instruments

• TLAC-eligible instruments are: ‒ All regulatory capital instruments, i.e. CET1, AT1 and T2 ‒ Particular debt instruments

• TLAC-eligible debt instruments must fulfill several conditions, e.g. be paid-in, be unsecured and have a minimum remaining contractual maturity of at least one year or are perpetual

• Moreover, TLAC-eligible debt instruments must absorb losses prior to liabilities excluded from TLAC • To fulfill the latter condition, TLAC-eligible debt instruments must be: ‒ contractually subordinated to excluded liabilities on the balance sheet of the resolution entity; or ‒ junior in the statutory creditor hierarchy to excluded liabilities on the balance sheet of the resolution entity

(statutory subordination); or ‒ issued by a resolution entity that does not have excluded liabilities (structural subordination)

• Excluded from TLAC are, among others: liabilities arising from derivatives, insured deposits and covered bonds

• Note: ‒ On the one hand, all TLAC-eligible senior unsecured bonds can also be bailed-in ‒ On the other hand, a senior unsecured bond might not be TLAC-eligible (because it is not subordinated to excluded

liabilities) but can still be bailed-in

TLAC and MREL

7

TLAC-eligible instruments

Subordination

Statutory subordination

Structural subordination

Contractual subordination

The subordination of the debt is determined

in the insolvency hierarchy of the

respective country law

The subordination of the debt is given by the structure of the bank, i.e. the debt is issued

by a holding company

The subordination of the debt is determined

in the debt contract, just as is the case for subordinated bonds

Example: Germany Germany has

subordinated several senior unsecured debt

instruments by changing the German insolvency hierarchy

for banks

Example: UK Banks in the UK most often have a HoldCo

structure. Senior unsecured debt issued by a HoldCo is TLAC-eligible because a HoldCo has no excluded liabilities on its

balance sheet

Source: FSB, UniCredit Research

Example: Spain Spain has implemented a new asset class (Tier-

3) that is senior to regulatory own funds and junior to senior

unsecured debt

TLAC and MREL

8

Exemptions from the subordination requirement

• The TLAC term sheet provides for some exemptions from the subordination requirement

• The "de minimis" exemption to the subordination applies if the following conditions are fulfilled ‒ The amount of excluded liabilities that rank pari passu or junior to TLAC-eligible liabilities does not exceed 5% of the

resolution entities eligible external TLAC ‒ It can be differentiated among pari passu creditors in resolution ‒ This differentiation would not give rise to the risk of successful legal challenges or valid compensation claims ‒ There are no material adverse impacts on resolvability

• Another exemption applies in jurisdictions where liabilities excluded from TLAC are statutorily (via law) excluded from bail-in (i.e. no writedown or conversion possible), provided that: ‒ Liabilities that rank pari passu to excluded liabilities are included in the bail-in tool and meet the eligibility criteria

for TLAC, they would qualify for TLAC ‒ The terms of TLAC-eligible liabilities specify that these instruments are subject to the bail-in tool ‒ This does not give rise to the risk of successful legal challenges or valid compensation claims

• The third exemption applies to liabilities that would otherwise count as external TLAC but rank pari passu with excluded liabilities (and are not subordinated) ‒ Such liabilities may contribute to TLAC up to an equivalent of 2.5% RWA in 2016 ‒ This allowance rises to 3.5% RWA equivalent when the TLAC RWA minimum is 18% in 2022

TLAC and MREL

9

Deductions of TLAC holdings

• According to the TLAC term sheet, G-SIBs must deduct holdings of TLAC-eligible instruments issued by other G-SIBs from their own TLAC or regulatory capital

• In October 2016, the Basel Committee on Banking Supervision (BCBS) published a standard on the treatment of such TLAC holdings

• TLAC holdings refer to holdings of TLAC-eligible debt instruments (TLAC liabilities) issued by other G-SIBs • According to the standard, the following is required: ‒ All internationally active banks (G-SIBs and non-G-SIBs) are required to deduct their TLAC holdings ‒ TLAC holdings have to be deducted from the T2 capital of the investing bank ‒ When a G-SIB holds its own TLAC liabilities, it must deduct them from its own TLAC resources ‒ When an investing bank owns <10% of the common shares of the issuer, then the deduction of TLAC holdings is

subject to a 5% threshold • If total holdings in TLAC liabilities – in aggregate and on a gross long basis – exceed 5% of the bank’s common

equity, the amount above 5% has to be deducted; amounts below the threshold are risk-weighted ‒ When an investing bank is a G-SIB, the 5% threshold can only be used for TLAC holdings in the trading book that are

sold within 30 business days ‒ If an investing bank owns >10% of the common shares of the issuer, then TLAC holdings must be fully deducted

from the investing bank’s T2 capital ‒ Reciprocal cross-holdings of TLAC between G-SIBs must be fully deducted from T2 capital

TLAC and MREL

10

Total capital requirements for G-SIBs

Source: CRR, FSB, UniCredit Research

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

CET1 (4.5%)

AT1 (1.5%) T2 (2.0%)

Capital conservation buffer (2.5%)

Countercyclical buffer (up to 2.5%)

Systemic buffer

Possible Pillar 2 add-on

Other TLAC-eligible capital (8.0 – 10.0 %)

TLAC 16.0-18.0% (Pillar 1)

Minimum capital

requirement (8%)

Combined buffer

requirement

TLAC and MREL

Buffer for G-SIBs, O-SIBs and systemic risks

11

TLAC and MREL

• TLAC

• MREL

12

Status quo: MREL versus TLAC

MREL TLAC

Application date 1 January 2016 (possible transitional period of 48 months) 1 January 2019 to 1 January 2022

Scope All banks in the EU G-SIBs (30 as of November 2015)

Approach Bank-specific (Pillar 2) Minimum standard (Pillar 1) and individual add-on

Standard setter European Commission FSB, mandated by the G20 countries

Status Passed (but amendments announced) Finalized

Application Individual level and highest EU consolidation level Resolution entities (external TLAC) and subsidiaries of resolution entities (internal TLAC)

Minimum requirement

None (but de facto 8%)

At least 16% of RWA from 1 January 2019 and 18% from 1 January 2022, and 6% of the Basel III leverage ratio denominator from 1 January 2019 and 6.75% from 1 January 2022

Basel III capital buffer

Included Required additionally

Eligible liabilities

Eligible instruments are not necessarily subordinated, but the resolution authority may require that part of MREL be met with contractual bail-in instruments, which must be subordinated to other eligible instruments Further specifications, e.g. issued and fully paid up, not owed by the bank itself, purchase not funded by the bank, remaining maturity at least one year, liability does not arise from derivatives or secured deposits

Eligible instruments must be unsecured and subordinated to excluded liabilities, i.e. contractual subordination, statutory subordination or structural subordination Further specifications, e.g. issued and fully paid up, remaining maturity at least one year, liability does not arise from derivatives or secured deposits

Deductions No deductions of MREL instruments held by other banks Deduction of TLAC-eligible instruments held by other banks

Source: BRRD, FSB, UniCredit Research

TLAC and MREL

13

Planned amendments to MREL

• The European Commission aims to overhaul the MREL requirements to align them more with the TLAC requirements • A proposal for these amendments is expected in November 2016 • The following is (currently) expected: ‒ Merging of TLAC and MREL requirements into a single framework, i.e. for G-SIBs in the EU, MREL requirements will

be the same as the TLAC requirements ‒ Splitting MREL into a minimum Pillar 1 requirement (in accordance with TLAC) and a firm-specific Pillar 2

requirement ‒ Implementation of the concepts of resolution entity and resolution group into EU law, i.e. internal and external

MREL requirements ‒ Calculation of MREL as a percentage of RWA and the leverage ratio denominator (instead of total assets) ‒ Implementation of TLAC subordination criteria for MREL-eligible instruments into EU law ‒ Amendment to the supervisory regime regarding a breach of capital requirements ‒ Implementation of the TLAC-holding deduction requirements

TLAC and MREL

14

AGENDA

• TLAC AND MREL

• SENIOR BAIL-IN

15

Introduction

• Beside MREL, the BRRD provides a minimum set of resolution tools that can be used in the event of a bank failure • One of these tools is the bail-in tool ‒ The tool was already implemented in each EU member state as of 1 January 2016 ‒ According to the bail-in tool, debt instruments can be converted into equity or the principle amount can be reduced

partially or in full (called "senior bail-in") ‒ The tool applies to all liabilities that are not exempt, such as covered deposits and covered bonds

• Implementation in the EU ‒ The BRRD (including the bail-in tool) has to be transferred into national law by each EU member state ‒ When implementing the BRRD into national law, the member states have some flexibility ‒ As a result of this flexibility, the insolvency hierarchy for liabilities is not the same across the EU

Senior bail-in

16

OpCo versus HoldCo

• According to senior bail-in rules, one needs to differentiate between ‒ a holding company group structure (HoldCo) and ‒ an operating company group structure (OpCo)

• OpCo structure ‒ In countries where banks are mainly structured as OpCos (e.g. Germany and France), a multiple-point-of-entry

approach (MPE approach) is common ‒ Losses have to be absorbed by the company that incurred them

• HoldCo structure ‒ In countries where banks are mainly structured as HoldCos (e.g. the UK and the US), a single-point-of-entry approach

(SPE approach) is often preferred ‒ Losses that occurred at the level of a subsidiary are transferred to the HoldCo ‒ Senior unsecured debt issued by the HoldCo is structurally subordinated to other senior unsecured debt issued in the

group

Senior bail-in

17

Bail-in hierarchy according to the BRRD Minimum set of resolution (since 1 January 2016)

Source: BRRD, UniCredit Research

Subordinated debt

Secured claims

Other liabilities

Unsecured deposits of small and medium entities (SMEs) and

natural persons

writedown or conversion

excluded from bail-in

according to Art. 108 BRRD

senior unsecured debt, derivatives, bank deposits and wholesale deposits

for example, covered bonds and covered deposits (i.e. deposits up to EUR 100,000)

Senior bail-in

Regulatory own funds (CET1, AT1 and T2)

18

Implementation of the bail-in tool by country

Country (Expected) implementation date*

Details of implementation Insolvency hierarchy

Germany Implemented (effective as of

1 January 2017)

Subordination of several senior unsecured

liabilities

Own funds → senior unsecured debt and simple structured instruments→ bank and wholesale deposits and complex structured

instruments → unsecured deposits of SMEs and natural persons

Italy Implemented (effective as of

1 January 2019)

Full depositor preference

Own funds → senior unsecured debt and derivatives → bank and wholesale deposits → unsecured deposits of SMEs and natural persons

France Not yet implemented Split of liabilities into "preferred" and "non-preferred" liabilities

Own funds → non-preferred liabilities → preferred liabilities → unsecured deposits of SMEs and natural persons

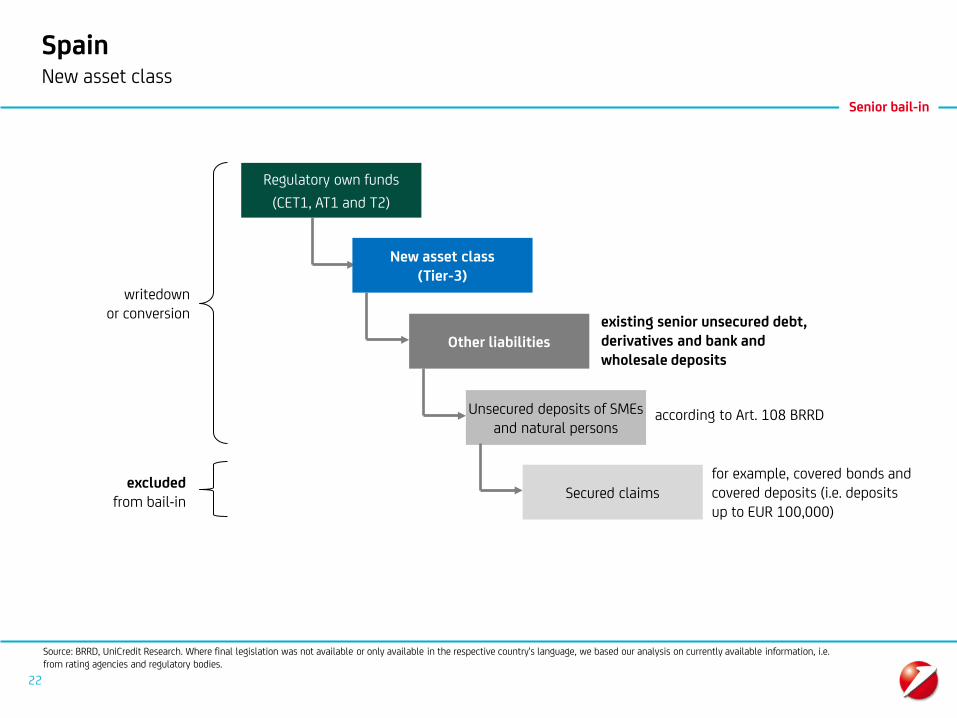

Spain Implemented Implementation of a new asset class (Tier-3)

Own funds → subordinated debt → senior unsecured debt, derivatives, bank and wholesale deposits → unsecured deposits of

SMEs and natural persons

Scandinavia Implemented in Denmark, Finland and Sweden According to the BRRD Own funds → senior unsecured debt, derivatives, bank and wholesale

deposits → unsecured deposits of SMEs and natural persons

Benelux Implemented According to the BRRD Own funds → senior unsecured debt, derivatives, bank and wholesale deposits → unsecured deposits of SMEs and natural persons

UK, Switzerland and the US Implemented Mainly holding company

(HoldCo) structure

Losses at the level of subsidiaries are channeled to the Holdco. The Holdco then settles with its shareholders (write down) and with its debt-

holders (write down or converting)

Source: BRRD, Rating agencies, regulatory bodies, UniCredit Research

* Bail-in is already applicable in every EU member state as the BRRD has already been implemented into the respective national law. However, some countries introduced special provisions with respect to the bail-in hierarchy of liabilities (e.g. Germany and Italy).

Senior bail-in

19

Germany Subordination of several senior unsecured liabilities (as of 1 January 2017)

Source: BRRD, AbwMechG, UniCredit Research

Senior bail-in

Regulatory own funds (CET1, AT1 and T2)

Secured claims

Other liabilities

Unsecured deposits of SMEs and natural persons

for example, covered bonds and covered deposits (i.e. deposits up to EUR 100,000)

* Including callable bonds, floaters linked to Euribor, Eonia or Libor (including inverse floaters), floaters with a 0% floor, and any bonds with contractually agreed interest payments and redemption amounts (such as bonds with and amortizing structure and foreign currency bonds)

** Including credit-linked notes, equity and inflation-linked bonds, bonds with caps, floors (except 0% floors) and corridors, dual-currency bonds, floaters linked to not standardized rates (e.g. CMS) and bonds with variable interest payments due to voting rights of the issuer or linked to an index

excluded from bail-in

Simple structured instruments* Bearer bonds, order bonds, promissory

note loans and registered bonds

Complex structured instruments** Money market instruments

Bank and wholesale deposits

20

Italy Preference to deposits (as of 1 January 2019)

Source: BRRD, UniCredit Research. Where final legislation was not available or only available in the respective country's language, we based our analysis on currently available information, i.e. from rating agencies and regulatory bodies.

excluded from bail-in

Senior unsecured debt and derivatives

Bank and wholesale deposits

according to Art. 108 BRRD

for example, covered bonds and covered deposits (i.e. deposits up to EUR 100,000)

Senior bail-in

Regulatory own funds (CET1, AT1 and T2)

Secured claims

Other liabilities

Unsecured deposits of SMEs and natural persons

writedown or conversion

21

France Split of liabilities into "preferred" and "non-preferred"

existing senior unsecured debt, derivatives and bank and wholesale deposits

Source: BRRD, UniCredit Research. Where final legislation was not available or only available in the respective country's language, we based our analysis on currently available information, i.e. from rating agencies and regulatory bodies.

Senior bail-in

excluded from bail-in

Non-preferred liabilities

Preferred liabilities

according to Art. 108 BRRD

for example, covered bonds and covered deposits (i.e. deposits up to EUR 100,000)

Regulatory own funds (CET1, AT1 and T2)

Secured claims

Other liabilities

Unsecured deposits of SMEs and natural persons

writedown or conversion

22

Spain New asset class

Regulatory own funds (CET1, AT1 and T2)

Secured claims

Other liabilities

Unsecured deposits of SMEs and natural persons

writedown or conversion

excluded from bail-in

New asset class (Tier-3)

according to Art. 108 BRRD

for example, covered bonds and covered deposits (i.e. deposits up to EUR 100,000)

Source: BRRD, UniCredit Research. Where final legislation was not available or only available in the respective country's language, we based our analysis on currently available information, i.e. from rating agencies and regulatory bodies.

Senior bail-in

existing senior unsecured debt, derivatives and bank and wholesale deposits

23

Bail-in in a HoldCo

HoldCo

Subsidiary A Subsidiary B Subsidiary C

• The assets of a HoldCo comprise, among others, the equity of its operational subsidiaries • The liabilities of the subsidiaries, consist of the debt issued to outside investors and the equity held by the HoldCo • The balance sheet of the HoldCo is decisive for all bail-in activities in the group

‒ The creditors of the HoldCo bear the losses of subsidiaries, allowing for the entire group to be recapitalized ‒ Loss that exceed the own funds of a subsidiary are absorbed by the liabilities of the HoldCo ‒ The HoldCo settles the losses of its subsidiaries with its own shareholders (writedown of equity) and with its own

debtholders (writedown or conversion of debt, i.e. senior bail-in)

Source: UniCredit Research

Single point-of-entry

• However, the here explained approach is ideally in a perfect world • In practice, many issues arise, for example:

‒ In some countries, HoldCo and OpCo structures exist for different bank groups ‒ A different approach can be defined in the resolution plan of a group ‒ Groups have subsidiaries outside the EU and difficulties arise between the resolution authorities

Losses incurred at a subsidiary are absorbed by the HoldCo

Senior bail-in

24

Your contacts

Corporate & Investment Banking UniCredit Bank AG Natalie Tehrani Monfared Senior Credit Analyst Regulatory & Accounting Service (RAS) UniCredit Research Tel. +49 89 378-12242 [email protected] Imprint Corporate & Investment Banking UniCredit Bank AG Arabellastraße 12 D-81925 Munich

25

This publication is presented to you by: Corporate & Investment Banking UniCredit Bank AG Arabellastr. 12 D-81925 München

The information in this publication is based on carefully selected sources believed to be reliable. However we do not make any representation as to its accuracy or completeness. Any opinions herein reflect our judgement at the date hereof and are subject to change without notice. Any investments presented in this report may be unsuitable for the investor depending on his or her specific investment objectives and financial position. Any reports provided herein are provided for general information purposes only and cannot substitute the obtaining of independent financial advice. Private investors should obtain the advice of their banker/broker about any investments concerned prior to making them. Nothing in this publication is intended to create contractual obligations. Corporate & Investment Banking of UniCredit Group consists of UniCredit Bank AG, Munich, UniCredit Bank Austria AG, Vienna, UniCredit S.p.A., Rome and other members of the UniCredit Group. UniCredit Bank AG is regulated by the German Financial Supervisory Authority (BaFin), UniCredit Bank Austria AG is regulated by the Austrian Financial Market Authority (FMA) and UniCredit S.p.A. is regulated by both the Banca d'Italia and the Commissione Nazionale per le Società e la Borsa (CONSOB). Note to UK Residents: In the United Kingdom, this publication is being communicated on a confidential basis only to clients of Corporate & Investment Banking of UniCredit Goup (acting through UniCredit Bank AG, London Branch) who (i) have professional experience in matters relating to investments being investment professionals as defined in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (“FPO”); and/or (ii) are falling within Article 49(2) (a) – (d) (“high net worth companies, unincorporated associations etc.”) of the FPO (or, to the extent that this publication relates to an unregulated collective scheme, to professional investors as defined in Article 14(5) of the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemptions) Order 2001 and/or (iii) to whom it may be lawful to communicate it, other than private investors (all such persons being referred to as “Relevant Persons”). This publication is only directed at Relevant Persons and any investment or investment activity to which this publication relates is only available to Relevant Persons or will be engaged in only with Relevant Persons. Solicitations resulting from this publication will only be responded to if the person concerned is a Relevant Person. Other persons should not rely or act upon this publication or any of its contents. The information provided herein (including any report set out herein) does not constitute a solicitation to buy or an offer to sell any securities. The information in this publication is based on carefully selected sources believed to be reliable but we do not make any representation as to its accuracy or completeness. Any opinions herein reflect our judgement at the date hereof and are subject to change without notice. We and/or any other entity of Corporate & Investment Banking of UniCredit Group may from time to time with respect to securities mentioned in this publication (i) take a long or short position and buy or sell such securities; (ii) act as investment bankers and/or commercial bankers for issuers of such securities; (iii) be represented on the board of any issuers of such securities; (iv) engage in “market making” of such securities; (v) have a consulting relationship with any issuer. Any investments discussed or recommended in any report provided herein may be unsuitable for investors depending on their specific investment objectives and financial position. Any information provided herein is provided for general information purposes only and cannot substitute the obtaining of independent financial advice. UniCredit Bank AG, London Branch is regulated by the Financial Services Authority for the conduct of business in the UK as well as by BaFIN, Germany. Notwithstanding the above, if this publication relates to securities subject to the Prospectus Directive (2005) it is sent to you on the basis that you are a Qualified Investor for the purposes of the directive or any relevant implementing legislation of a European Economic Area (“EEA”) Member State which has implemented the Prospectus Directive and it must not be given to any person who is not a Qualified Investor. By being in receipt of this publication you undertake that you will only offer or sell the securities described in this publication in circumstances which do not require the production of a prospectus under Article 3 of the Prospectus Directive or any relevant implementing legislation of an EEA Member State which has implemented the Prospectus Directive. Note to US Residents: The information provided herein or contained in any report provided herein is intended solely for institutional clients of Corporate & Investment Banking of UniCredit Group acting through UniCredit Bank AG, New York Branch and UniCredit Capital Markets, LLC (together “UniCredit”) in the United States, and may not be used or relied upon by any other person for any purpose. It does not constitute a solicitation to buy or an offer to sell any securities under the Securities Act of 1933, as amended, or under any other US federal or state securities laws, rules or regulations. Investments in securities discussed herein may be unsuitable for investors, depending on their specific investment objectives, risk tolerance and financial position. In jurisdictions where UniCredit is not registered or licensed to trade in securities, commodities or other financial products, any transaction may be effected only in accordance with applicable laws and legislation, which may vary from jurisdiction to jurisdiction and may require that a transaction be made in accordance with applicable exemptions from registration or licensing requirements. All information contained herein is based on carefully selected sources believed to be reliable, but UniCredit makes no representations as to its accuracy or completeness. Any opinions contained herein reflect UniCredit's judgement as of the original date of publication, without regard to the date on which you may receive such information, and are subject to change without notice. UniCredit may have issued other reports that are inconsistent with, and reach different conclusions from, the information presented in any report provided herein. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them. Past performance should not be taken as an indication or guarantee of further performance, and no representation or warranty, express or implied, is made regarding future performance. UniCredit and/or any other entity of Corporate & Investment Banking of UniCredit Group may from time to time, with respect to any securities discussed herein: (i) take a long or short position and buy or sell such securities; (ii) act as investment and/or commercial bankers for issuers of such securities; (iii) be represented on the board of such issuers; (iv) engage in “market-making” of such securities; and (v) act as a paid consultant or adviser to any issuer. The information contained in any report provided herein may include forward-looking statements within the meaning of US federal securities laws that are subject to risks and uncertainties. Factors that could cause a company's actual results and financial condition to differ from its expectations include, without limitation: Political uncertainty, changes in economic conditions that adversely affect the level of demand for the company‘s products or services, changes in foreign exchange markets, changes in international and domestic financial markets, competitive environments and other factors relating to the foregoing. All forward-looking statements contained in this report are qualified in their entirety by this cautionary statement. This product is offered by UniCredit Bank AG who is solely responsible for the Product and its performance and/or effectiveness. UEFA and its affiliates, member associations and sponsors (excluding UniCredit) do not endorse, approve or recommend the Product and accept no liability or responsibility whatsoever in relation thereto.

Corporate & Investment Banking UniCredit Bank AG, Munich as of 18 October 2016

Disclaimer

26

Our recommendations are based on information obtained from, or are based upon public information sources that we consider to be reliable but for the completeness and accuracy of which we assume no liability. All estimates and opinions included in the report represent the independent judgment of the analysts as of the date of the issue. This report may contain links to websites of third parties, the content of which is not controlled by UniCredit Bank. No liability is assumed for the content of these third-party websites. We reserve the right to modify the views expressed herein at any time without notice. Moreover, we reserve the right not to update this information or to discontinue it altogether without notice. This analysis is for information purposes only and (i) does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for any financial, money market or investment instrument or any security, (ii) is neither intended as such an offer for sale or subscription of or solicitation of an offer to buy or subscribe for any financial, money market or investment instrument or any security nor (iii) as an advertisement thereof. The investment possibilities discussed in this report may not be suitable for certain investors depending on their specific investment objectives and time horizon or in the context of their overall financial situation. The investments discussed may fluctuate in price or value. Investors may get back less than they invested. Changes in rates of exchange may have an adverse effect on the value of investments. Furthermore, past performance is not necessarily indicative of future results. In particular, the risks associated with an investment in the financial, money market or investment instrument or security under discussion are not explained in their entirety. This information is given without any warranty on an "as is" basis and should not be regarded as a substitute for obtaining individual advice. Investors must make their own determination of the appropriateness of an investment in any instruments referred to herein based on the merits and risks involved, their own investment strategy and their legal, fiscal and financial position. As this document does not qualify as an investment recommendation or as a direct investment recommendation, neither this document nor any part of it shall form the basis of, or be relied on in connection with or act as an inducement to enter into, any contract or commitment whatsoever. Investors are urged to contact their bank's investment advisor for individual explanations and advice. Neither UniCredit Bank nor any of their respective directors, officers or employees nor any other person accepts any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith. This analysis is being distributed by electronic and ordinary mail to professional investors, who are expected to make their own investment decisions without undue reliance on this publication, and may not be redistributed, reproduced or published in whole or in part for any purpose. Responsibility for the content of this publication lies with: UniCredit Group and its subsidiaries are subject to regulation by the European Central Bank a) UniCredit Bank AG (UniCredit Bank), Am Tucherpark 16, 80538 Munich, Germany, (also responsible for the distribution pursuant to §34b WpHG). The company belongs to UniCredit Group. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Lurgiallee 12, 60439 Frankfurt, Germany. b) UniCredit Bank AG London Branch (UniCredit Bank London), Moor House, 120 London Wall, London EC2Y 5ET, United Kingdom. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Lurgiallee 12, 60439 Frankfurt, Germany and subject to limited regulation by the Financial Conduct Authority, 25 The North Colonnade, Canary Wharf, London E14 5HS, United Kingdom and Prudential Regulation Authority 20 Moorgate, London, EC2R 6DA, United Kingdom. Further details regarding our regulatory status are available on request. c) UniCredit Bank AG Hong Kong Branch (UniCredit Bank Hong Kong), 25/F Man Yee Building, 68 Des Voeux Road Central, Hong Kong. Regulatory authority: Hong Kong Monetary Authority, 55th Floor, Two International Financial Centre, 8 Finance Street, Central, Hong Kong d) UniCredit Bank AG Singapore Branch (UniCredit Bank Singapore), Prudential Tower, 30 Cecil Street, #25-01, Singapore 049712 Regulatory authority: Monetary Authority of Singapore, 10 Shenton Way MAS Building, Singapore 079117 e) UniCredit Bank AG Tokyo Branch (UniCredit Tokyo), Otemachi 1st Square East Tower 18/F, 1-5-1 Otemachi, Chiyoda-ku, 100-0004 Tokyo, Japan Regulatory authority: Financial Services Agency, The Japanese Government, 3-2-1 Kasumigaseki Chiyoda-ku Tokyo, 100-8967 Japan, The Central Common Government Offices No. 7.

POTENTIAL CONFLICTS OF INTERESTS Aareal Bank 3; ABN Amro Bank 3; Allied Irish Banks 3; Assicurazioni Generali 3; AXA 3, 8a; Banca P. Emilia Romagna 3; Banca Popolare di Milano 3, 8a; Banco de Sabadell 3; Banco Popolare Scarl 3; Banco Popular Espanol 3; Banco Santander 8a; Bank of America 3; Bank of Montreal 3; Bankinter 3; Barclays 3; BBVA 3, 8a; BNP Paribas 8a; Citigroup 3; Commerzbank 8a; Credit Suisse 2; Danske Bank 3; Deutsche Bank 3, 8a; Deutsche Postbank 3; DNB 3; Eika BoligKreditt 3; Exor 3; General Electric 3; Goldman Sachs 3; HSBC 3; HypoVereinsbank 3; ING 8a; Intesa Sanpaolo 3, 8a; Landesbank Berlin 3; Lloyds Banking Group 3; Mediobanca 1a, 3, 6a; Morgan Stanley 3; Münchener Hypothekenbank 3; Nord/LB 3; Nordea 3; PKO Bank 3; PZU 3; Raiffeisen Bank Int. 3; Royal Bank of Canada 3; SEB 3; Société Générale 3, 8a; Svenska Handelsbanken 3; Swedbank 3; UBI Banca 3; UBS 3; Unibail-Rodamco 8a; UniCredit 2, 3; UniCredit Bank Austria 3; Wells Fargo & Co 3; Key 1a: UniCredit Bank AG and/or any related legal person owns at least 2% of the capital stock of the analyzed company. Key 1b: The analyzed company owns at least 2% of the capital stock of UniCredit Bank AG and/or any related legal person. Key 2: UniCredit Bank AG and/or any related legal person has been lead manager or co-lead manager over the previous 12 months of any publicly disclosed offer of financial instruments of the analyzed company, or in any related derivatives. Key 3: UniCredit Bank AG and/or any related legal person administers the securities issued by the analyzed company on the stock exchange or on the market by quoting bid and ask prices (i.e. acts as a market maker or liquidity provider in the securities of the analyzed company or in any related derivatives). Key 5: The analyzed company and UniCredit Bank AG and/or any related legal person have concluded an agreement on the preparation of analyses. Key 6a: Employees or members of the Board of Directors of UniCredit Bank AG and/or any other employee that works for UniCredit Research (i.e. the joint research department of the UniCredit Group) and/or members of the Group Board (pursuant to relevant domestic law) are members of the Board of Directors of the analyzed company. Members of the Board of Directors of the analyzed company hold office in the Board of Directors of UniCredit Bank AG (pursuant to relevant domestic law). The application of this Key 6a is limited to persons who, although not involved in the preparation of the analysis, had or could reasonably be expected to have access to the analysis prior to its dissemination to customers or the public. Key 6b: The analyst is on the Supervisory Board/Board of Directors of the company they cover. Key 8a: UniCredit Bank AG and/or any related legal person hold a net long position exceeding 0.5% of the total issued share capital of the issuer. Key 8b: UniCredit Bank AG and/or any related legal person hold a net short position exceeding 0.5% of the total issued share capital of the issuer.

Disclaimer Credit Research

27

RECOMMENDATIONS, RATINGS AND EVALUATION METHODOLOGY ACAFP 5/12/2016 Marketweight BFCM 11/10/2015 In transition EXOIM 2/12/2016 Marketweight RBIAV 5/13/2016 Marketweight ACAFP 4/7/2016 Restricted BNP 10/30/2015 Marketweight EXOIM 11/20/2015 Restricted RBIAV 11/10/2015 In transition AEGON 5/12/2016 Underweight BPCEGP 5/11/2016 Marketweight EXOIM 11/12/2015 Marketweight RBS 8/8/2016 Underweight AIG 8/3/2016 Marketweight BPCEGP 11/10/2015 In transition GARAN 5/30/2016 In transition RBS 4/29/2016 Marketweight AIG 6/2/2016 Restricted BPEIM 8/5/2016 no rec. GARAN 12/18/2015 Hold RBS 3/31/2016 Restricted ANNGR 8/2/2016 Overweight BPEIM 5/13/2016 Marketweight LBBER 11/10/2015 In transition SNSBNK 8/19/2016 no rec. ANNGR 6/6/2016 Restricted BZLNZ 5/9/2016 no rec. MONTE 5/6/2016 Underweight SNSBNK 11/10/2015 In transition ANNGR 5/12/2016 Overweight BZLNZ 11/10/2015 In transition NAB 5/9/2016 Marketweight SOCGEN 8/16/2016 Restricted ANNGR 3/3/2016 Marketweight CBAAU 5/9/2016 Marketweight NAB 11/10/2015 In transition STANLN 4/27/2016 Marketweight ANNGR 2/10/2016 no rec. CBAAU 11/10/2015 In transition NDB 9/26/2016 Restricted STANLN 11/10/2015 In transition ANNGR 12/9/2015 Restricted CMZB 11/2/2015 Marketweight NDB 11/27/2015 Marketweight SWEDA 2/2/2016 Marketweight ANNGR 11/3/2015 Marketweight CRH 11/18/2015 Restricted NYKRE 5/13/2016 Marketweight SWEDA 11/10/2015 In transition ANZ 5/9/2016 Marketweight CS 2/4/2016 Marketweight NYKRE 11/10/2015 In transition UBS 5/3/2016 Marketweight ANZ 11/10/2015 In transition CS 11/19/2015 Restricted PBBGR 3/3/2016 Marketweight UBS 3/14/2016 Restricted ANZNZ 5/9/2016 no rec. DAA 5/12/2016 Marketweight PBBGR 1/19/2016 Restricted UOBSP 2/26/2016 Marketweight ANZNZ 11/10/2015 In transition DAA 11/10/2015 In transition PMIIM 5/11/2016 Marketweight UOBSP 11/10/2015 In transition ASBBNK 5/9/2016 no rec. DANBNK 5/2/2016 Marketweight PMIIM 11/10/2015 In transition VAKBN 5/30/2016 In transition ASBBNK 11/10/2015 In transition DANBNK 11/10/2015 In transition POPSM 5/2/2016 Marketweight VAKBN 12/18/2015 Sell ASSGEN 5/12/2016 Restricted DPB 11/10/2015 In transition POPSM 11/10/2015 In transition WSTP 5/9/2016 Marketweight AXASA 5/4/2016 Marketweight DWNIGY 11/10/2015 Marketweight RABOBK 8/19/2016 Marketweight WSTP 11/10/2015 In transition AXASA 3/23/2016 Restricted EXOIM 9/26/2016 Overweight RABOBK 11/10/2015 In transition

Disclaimer Credit Research

28

Overview of our ratings You will find the history of rating regarding recommendation changes as well as an overview of the breakdown in absolute and relative terms of our investment ratings on our website http://www.disclaimer.unicreditmib.eu/credit-research-rd/Recommendations_CR_e.pdf . Note on the evaluation basis for interest-bearing securities: Recommendations relative to an index: For high grade names the recommendations are relative to the "iBoxx EUR Benchmark" index family, for sub investment grade names the recommendations are relative to the "iBoxx EUR High Yield" index family. Marketweight: We recommend having the same portfolio exposure in the name as the respective iBoxx index. We expect that the average total return of the instruments of the issuer is equal to the total return of the index. Overweight: We recommend having a higher portfolio exposure in the name as the respective iBoxx index. We expect that the average total return of the instruments of the issuer is greater than the total return of the index. Underweight: We recommend having a lower portfolio exposure in the name as the respective iBoxx index. We expect that the average total return of the instruments of the issuer is less than the total return of the index Outright recommendations: Hold: We recommend holding the respective instrument for investors who already have exposure. We expect that the total return of the instruments of the issuer is equal to the yield. Buy: We recommend buying the respective instrument for investors who already have exposure. We expect that the total return of the instruments of the issuer is greater than the yield. Sell: We recommend selling the respective instrument for investors who already have exposure. We expect that the total return of the instruments of the issuer is less than the yield. We employ three further categorizations for interest-bearing securities in our coverage: Restricted: A recommendation and/or financial forecast is not disclosed owing to compliance or other regulatory considerations such as a blackout period or a conflict of interest. Coverage in transition: Due to changes in the research team, the disclosure of a recommendation and/or financial information are temporarily suspended. The interest-bearing security remains in the research universe and disclosures of relevant information will be resumed in due course. Not rated: Suspension of coverage. Trading recommendations for fixed-interest securities mostly focus on the credit spread (yield difference between the fixed-interest security and the relevant government bond or swap rate) and on the rating views and methodologies of recognized agencies (S&P, Moody’s, Fitch). Depending on the type of investor, investment ratings may refer to a short period or to a 6 to 9-month horizon. Please note that the provision of securities services may be subject to restrictions in certain jurisdictions. You are required to acquaint yourself with local laws and restrictions on the usage and the availability of any services described herein. The information is not intended for distribution to or use by any person or entity in any jurisdiction where such distribution would be contrary to the applicable law or provisions. If not otherwise stated daily price data refers to pre-day closing levels and iBoxx bond index characteristics refer to the previous month-end index characteristics. Coverage Policy A list of the companies covered by UniCredit Bank is available upon request. Frequency of reports and updates It is intended that each of these companies be covered at least once a year, in the event of key operations and/or changes in the recommendation. SIGNIFICANT FINANCIAL INTEREST UniCredit Bank AG and/or other related legal persons with them regularly trade shares of the analyzed company. UniCredit Bank AG and/or other related legal persons may hold significant open derivative positions on the stocks of the company which are not delta-neutral. UniCredit Bank AG and/or other related legal persons have a significant financial interest relating to the analyzed company or may have such at any future point of time. Due to the fact that UniCredit Bank AG and/or any related legal person are entitled, subject to applicable law, to perform such actions at any future point in time which may lead to the existence of a significant financial interest, it should be assumed for the purposes of this information that UniCredit Bank AG and/or any related legal person will in fact perform such actions which may lead to the existence of a significant financial interest relating to the analyzed company. Analyses may refer to one or several companies and to the securities issued by them. In some cases, the analyzed companies have actively supplied information for this analysis. INVESTMENT SERVICES The analyzed company and UniCredit Bank AG and/or any related legal person concluded an agreement on the provision of investment services in the previous 12 months, in return for which the Bank and/or such related legal person received a consideration or promise of consideration or intends to do so. Due to the fact that UniCredit Bank AG and/or any related legal person are entitled to conclude, subject to applicable law, an agreement on the provision of investment services with the analyzed company at any future point in time and may receive a consideration or promise of consideration, it should be assumed for the purposes of this information that UniCredit Bank AG and/or any related legal person will in fact conclude such agreements and will in fact receive such consideration or promise of consideration. ANALYST DECLARATION The author’s remuneration has not been, and will not be, geared to the recommendations or views expressed in this study, neither directly nor indirectly. ORGANIZATIONAL AND ADMINISTRATIVE ARRANGEMENTS TO AVOID AND PREVENT CONFLICTS OF INTEREST To prevent or remedy conflicts of interest, UniCredit Bank has established the organizational arrangements required from a legal and supervisory aspect, adherence to which is monitored by its compliance department. Conflicts of interest arising are managed by legal and physical and non-physical barriers (collectively referred to as “Chinese Walls”) designed to restrict the flow of information between one area/department of UniCredit Bank and another. In particular, Investment Banking units, including corporate finance, capital market activities, financial advisory and other capital raising activities, are segregated by physical and non-physical boundaries from Markets Units, as well as the research department. Disclosure of publicly available conflicts of interest and other material interests is made in the research. Analysts are supervised and managed on a day-to-day basis by line managers who do not have responsibility for Investment Banking activities, including corporate finance activities, or other activities other than the sale of securities to clients. ADDITIONAL REQUIRED DISCLOSURES UNDER THE LAWS AND REGULATIONS OF JURISDICTIONS INDICATED You will find a list of further additional required disclosures under the laws and regulations of the jurisdictions indicated on our website www.cib-unicredit.com/research-disclaimer.

Disclaimer Credit Research

29

Notice to Austrian investors: This analysis is only for distribution to professional clients (Professionelle Kunden) as defined in article 58 of the Securities Supervision Act. Notice to investors in Bosnia and Herzegovina: This report is intended only for clients of UniCredit in Bosnia and Herzegovina who are institutional investors (Institucionalni investitori) in accordance with Article 2 of the Law on Securities Market of the Federation of Bosnia and Herzegovina and Article 2 of the Law on Securities Markets of the Republic of Srpska, respectively, and may not be used by or distributed to any other person. This document does not constitute or form part of any offer for sale or subscription for or solicitation of any offer to buy or subscribe for any securities and neither this document nor any part of it shall form the basis of, or be relied on in connection with or act as an inducement to enter into, any contract or commitment whatsoever. Notice to Brazilian investors: The individual analyst(s) responsible for issuing this report represent(s) that: (a) the recommendations herein reflect exclusively the personal views of the analysts and have been prepared in an independent manner, including in relation to UniCredit Group; and (b) except for the potential conflicts of interest listed under the heading “Potential Conflicts of Interest” above, the analysts are not in a position that may impact on the impartiality of this report or that may constitute a conflict of interest, including but not limited to the following: (i) the analysts do not have a relationship of any nature with any person who works for any of the companies that are the object of this report; (ii) the analysts and their respective spouses or partners do not hold, either directly or indirectly, on their behalf or for the account of third parties, securities issued by any of the companies that are the object of this report; (iii) the analysts and their respective spouses or partners are not involved, directly or indirectly, in the acquisition, sale and/or trading in the market of the securities issued by any of the companies that are the object of this report; (iv) the analysts and their respective spouses or partners do not have any financial interest in the companies that are the object of this report; and (v) the compensation of the analysts is not, directly or indirectly, affected by UniCredit’s revenues arising out of its businesses and financial transactions. UniCredit represents that: except for the potential conflicts of interest listed under the heading “Potential Conflicts of Interest” above, UniCredit, its controlled companies, controlling companies or companies under common control (the “UniCredit Group”) are not in a condition that may impact on the impartiality of this report or that may constitute a conflict of interest, including but not limited to the following: (i) the UniCredit Group does not hold material equity interests in the companies that are the object of this report; (ii) the companies that are the object of this report do not hold material equity interests in the UniCredit Group; (iii) the UniCredit Group does not have material financial or commercial interests in the companies or the securities that are the object of this report; (iv) the UniCredit Group is not involved in the acquisition, sale and/or trading of the securities that are the object of this report; and (v) the UniCredit Group does not receive compensation for services rendered to the companies that are the object of this report or to any related parties of such companies. Notice to Canadian investors: This communication has been prepared by UniCredit Bank AG, which does not have a registered business presence in Canada. This communication is a general discussion of the merits and risks of a security or securities only, and is not in any way meant to be tailored to the needs and circumstances of any recipient. The contents of this communication are for information purposes only, therefore should not be construed as advice and do not constitute an offer to sell, nor a solicitation to buy any securities. Notice to Cyprus investors: This document is directed only at clients of UniCredit Bank who are persons falling within the Second Appendix (Section 2, Professional Clients) of the law for the Provision of Investment Services, the Exercise of Investment Activities, the Operation of Regulated Markets and other Related Matters, Law 144(I)/2007 and persons to whom it may otherwise lawfully be communicated who possess the experience, knowledge and expertise to make their own investment decisions and properly assess the risks that they incur (all such persons together being referred to as “relevant persons”). This document must not be acted on or relied on by persons who are not relevant persons or relevant persons who have requested to be treated as retail clients. Any investment or investment activity to which this communication related is available only to relevant persons and will be engaged in only with relevant persons. This document does not constitute an offer or solicitation to any person to whom it is unlawful to make such an offer or solicitation. Notice to Hong Kong investors: This report is for distribution only to “professional investors” within the meaning of Schedule 1 to the Securities and Futures Ordinance (Chapter 571, Laws of Hong Kong) and any rules made thereunder, and may not be reproduced, or used by or further distributed to any other person, in whole or in part, for any purpose. This report does not constitute or form part of an offer or solicitation of any offer to buy or sell any securities, nor should it or any part of it form the basis of, or be relied upon in connection with, any contract or commitment whatsoever. By accepting this report, the recipient represents and warrants that it is entitled to receive such report in accordance with, and on the basis of, the restrictions set out in this “Disclaimer” section, and agrees to be bound by those restrictions. Notice to investors in Ivory Coast: The information contained in the present report have been obtained by Unicredit Bank AG from sources believed to be reliable, however, no express or implied representation or warranty is made by Unicredit Bank AG or any other person as to the completeness or accuracy of such information. All opinions and estimates contained in the present report constitute a judgement of Unicredit Bank AG as of the date of the present report and are subject to change without notice. They are provided in good faith but without assuming legal responsibility. This report is not an offer to sell or solicitation of an offer to buy or invest in securities. Past performance is not an indicator of future performance and future returns cannot be guaranteed, and there is a risk of loss of the initial capital invested. No matter contained in this document may be reproduced or copied by any means without the prior consent of Unicredit Bank AG. Notice to New Zealand investors: This report is intended for distribution only to persons who are “wholesale clients” within the meaning of the Financial Advisers Act 2008 (“FAA”) and by receiving this report you represent and agree that (i) you are a “wholesale client” under the FAA (ii) you will not distribute this report to any other person, including (in particular) any person who is not a “wholesale client” under the FAA. This report does not constitute or form part of, in relation to any of the securities or products covered by this report, either (i) an offer of securities for subscription or sale under the Securities Act 1978 or (ii) an offer of financial products for issue or sale under the Financial Markets Conduct Act 2013. Notice to Omani investors: This communication has been prepared by UniCredit Bank AG. UniCredit Bank AG does not have a registered business presence in Oman and does not undertake banking business or provide financial services in Oman and no advice in relation to, or subscription for, any securities, products or financial services may or will be consummated within Oman. The contents of this communication are for the information purposes of sophisticated clients, who are aware of the risks associated with investments in foreign securities and neither constitutes an offer of securities in Oman as contemplated by the Commercial Companies Law of Oman (Royal Decree 4/74) or the Capital Market Law of Oman (Royal Decree 80/98), nor does it constitute an offer to sell, or the solicitation of any offer to buy non-Omani securities in Oman as contemplated by Article 139 of the Executive Regulations to the Capital Market Law (issued vide CMA Decision 1/2009). This communication has not been approved by and UniCredit Bank AG is not regulated by either the Central Bank of Oman or Oman’s Capital Market Authority. Notice to Pakistani investors: Investment information, comments and recommendations stated herein are not within the scope of investment advisory activities as defined in sub-section I, Section 2 of the Securities and Exchange Ordinance, 1969 of Pakistan. Investment advisory services are provided in accordance with a contract of engagement on investment advisory services concluded with brokerage houses, portfolio management companies, non-deposit banks and the clients. The distribution of this report is intended only for informational purposes for the use of professional investors and the information and opinions contained herein, or any part of it shall not form the basis of, or be relied on in connection with or act as an inducement to enter into, any contract or commitment whatsoever. Notice to Polish Investors: This document is intended solely for professional clients as defined in Art. 3.39b of the Trading in Financial Instruments Act of 29 July 2005 (as amended). The publisher and distributor of the document certifies that it has acted with due care and diligence in preparing it, however, assumes no liability for its completeness and accuracy. This document is not an advertisement. It should not be used in substitution for the exercise of independent judgment. Notice to Serbian investors: This analysis is only for distribution to professional clients (profesionalni klijenti) as defined in article 172 of the Law on Capital Markets. Notice to UK investors: This communication is directed only at clients of UniCredit Bank who (i) have professional experience in matters relating to investments or (ii) are persons falling within Article 49(2)(a) to (d) (“high net worth companies, unincorporated associations, etc.”) of the United Kingdom Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or (iii) to whom it may otherwise lawfully be communicated (all such persons together being referred to as “relevant persons”). This communication must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this communication relates is available only to relevant persons and will be engaged in only with relevant persons. CR e 10

Disclaimer Credit Research