bakery research - bord · pdf filebakery research june 2014 ... total value of the bakery...

TRANSCRIPT

Bakery Research June 2014

Growing the success of Irish food & horticulture

Alternative Solutions

Shifting Patterns

Lack of Innovation

The Liquid Shopper

Health Agenda

Fresh & Natural

Education Needed

Category Growth

Key Bakery Themes

2%+ value growth expected for the category but…… Issues around health and health perceptions of category will severely dent this if not managed. Disproportionate share of category and future growth likely to go towards unbranded/own label solutions if relevant solutions and dialogue are not championed by brands.

Category Primed for Growth…..but

Category Growth

Bread and Morning Goods Market Value Snapshot – Ireland

€ 393,338m

Value (Yoy)

Volume (Yoy)

Source: Kantar/ Canadean

Total Value of The Bakery Market (Jan 2013 - Jan 2014)

3.7%

2.1%

Growth Forecasts: average year-over-year growth in the next three years

Total Value of Bread and Morning Goods Market (Jan 2013 - Jan 2014)

+2.2% Per annum

+2.9% Per annum

Bread and Rolls Morning Goods

Category Growth

78%

22%

Market Value Share By Sector

Bread Morning Goods

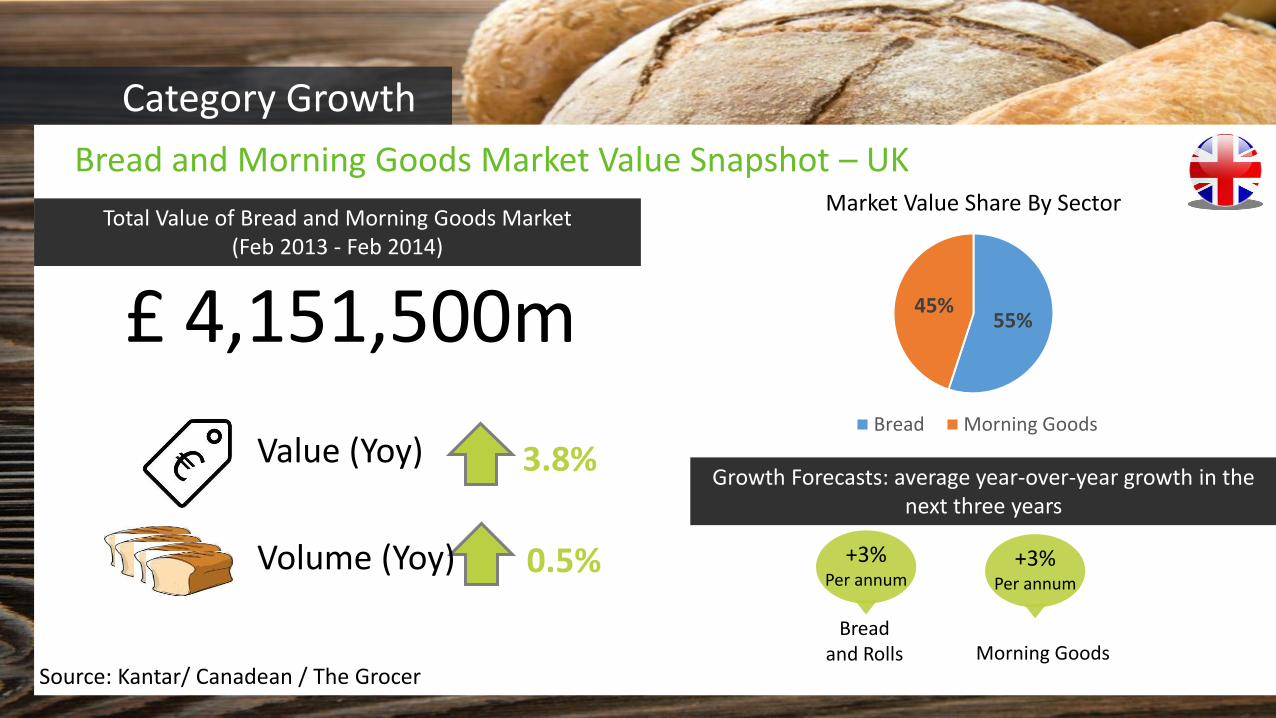

Bread and Morning Goods Market Value Snapshot – UK

Source: Kantar/ Canadean / The Grocer

Total Value of The Bakery Market (Jan 2013 - Jan 2014)

3.8%

0.5%

Growth Forecasts: average year-over-year growth in the next three years

+3% Per annum

+3% Per annum

Bread and Rolls Morning Goods

Category Growth

£ 4,151,500m

Value (Yoy)

Volume (Yoy)

Total Value of Bread and Morning Goods Market (Feb 2013 - Feb 2014)

55% 45%

Market Value Share By Sector

Bread Morning Goods

71%

45% 43% 37% 26%

11%

25% 14%

16% 25%

19% 30%

43% 48% 49%

Packagedsliced pan

French breads- Baguettes

Soda/stoneground

bread

Wraps Rolls/ Buns /Baps

Regularly (at least weekly) Occasionally (at least quarterly) Less often or never

What’s In the Bread Bin? – Top 5 Purchases Types of baked goods purchased for the household:

73%

44% 34% 29% 29%

9%

23% 23%

14% 14%

18% 33%

43% 57% 58%

Packagedsliced loaf

Rolls/ Buns /Baps

French breads/Baguettes

Unsliced loaf/bloomer

Wraps

Base: All Grocery Shoppers N=1,000; England N=1,000

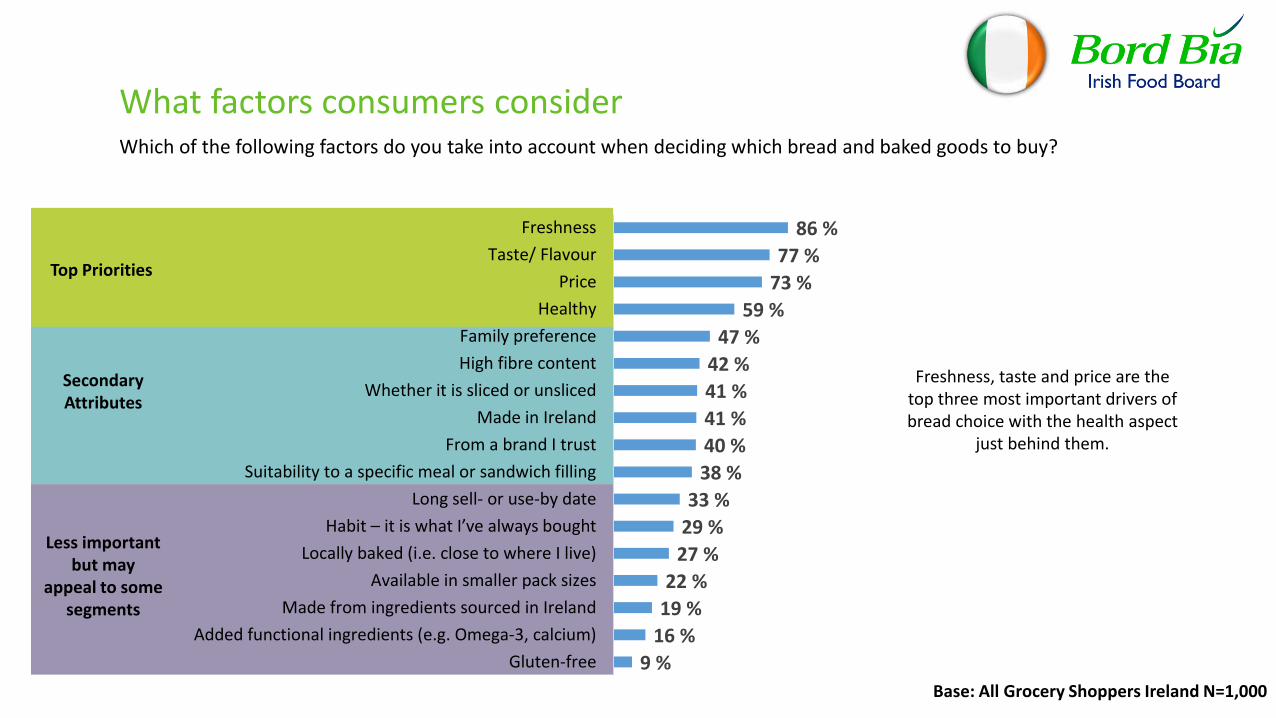

Which of the following factors do you take into account when deciding which bread and baked goods to buy?

What factors consumers consider

Base: All Grocery Shoppers Ireland N=1,000

Top Priorities

Secondary Attributes

Less important but may

appeal to some segments

9 %

16 %

19 %

22 %

27 %

29 %

33 %

38 %

40 %

41 %

41 %

42 %

47 %

59 %

73 %

77 %

86 %

Gluten-free

Added functional ingredients (e.g. Omega-3, calcium)

Made from ingredients sourced in Ireland

Available in smaller pack sizes

Locally baked (i.e. close to where I live)

Habit – it is what I’ve always bought

Long sell- or use-by date

Suitability to a specific meal or sandwich filling

From a brand I trust

Made in Ireland

Whether it is sliced or unsliced

High fibre content

Family preference

Healthy

Price

Taste/ Flavour

Freshness

Freshness, taste and price are the top three most important drivers of bread choice with the health aspect

just behind them.

Which of the following factors do you take into account when deciding which bread and baked goods to buy?

What factors consumers consider

Base: All Grocery England N=1,000

Top Priorities

Secondary Attributes

Less important but may

appeal to some segments

2 % 6 %

10 % 16 %

23 % 24 % 25 %

33 % 34 %

43 % 45 % 46 %

51 % 51 % 51 %

75 % 81 %

86 %

Other, specify:

Gluten-free

Added functional ingredients (e.g. Omega-3, calcium)

Made from ingredients sourced in England

Available in smaller pack sizes

Locally baked (i.e. close to where I live)

Made in England

High fibre content

Habit – it is what I’ve always bought

Suitability to a specific meal or sandwich filling

Long sell- or use-by date

Family preference

Whether it is sliced or unsliced

From a brand I trust

Healthy

Price

Taste/ Flavour

Freshness

When it comes to the brand of bread you buy most often, which of the following best describes what you do?

The Role of Branding and Loyalty in the Category

Base: All Grocery Shoppers N=1,000; England N=1,000

4%

21%

33%

42%

5%

26%

30%

39%

I buy whatever bread is on special offer, nomatter what brand that is

I have a couple of favourite brands I likeand usually buy one of them

I tend to switch from my main brand ifanother brand is on special offer

I almost always buy the same brand, myfavourite one

IRL UK

You mentioned that you buy a supermarket own brand bread, which of the following best describes the reasons why?

12%

7%

30%

27%

61%

5%

13%

37%

38%

57%

Other, (specify)

I’d prefer buying a well-known brand of bread but I simply can’t afford it

I only buy it because it’s cheaper

The taste is similar to a well-knownbread brand

The quality is comparable with well-known brands

Base: Grocery Shoppers who buy own brand bread ROI N=265; ENG N=278

Eroding personal permission to consume bread and baked goods. Driven by health concerns and also rise in alternative solutions within the category. Moving towards a broader based repertoire overall but with this shoppers need assistance. Assistance in discovering new varieties. Assistance in understanding how and when to use (occasions and ideas).

Everyday Solutions Under Threat

Alternative solutions

41% Buying a wider variety of baked goods overall, while also actively

reducing white bread consumption.

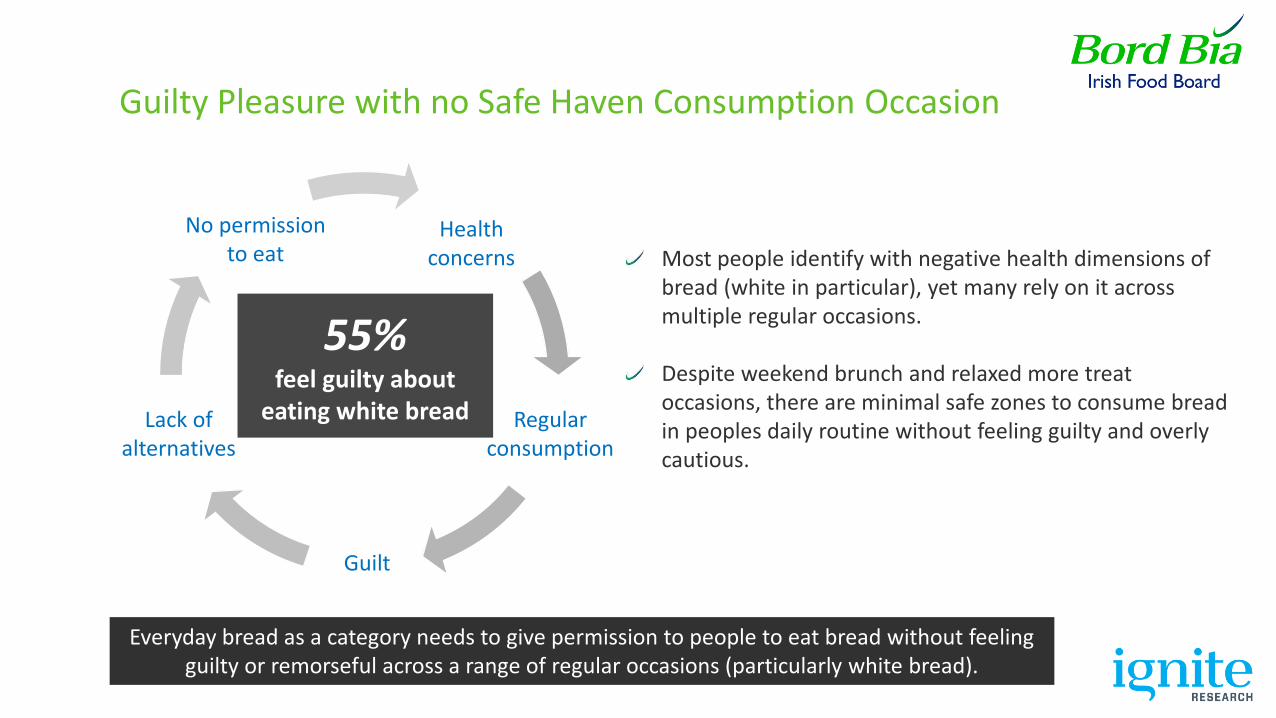

Guilty Pleasure with no Safe Haven Consumption Occasion

Everyday bread as a category needs to give permission to people to eat bread without feeling guilty or remorseful across a range of regular occasions (particularly white bread).

Health concerns

Regular consumption

Guilt

Lack of alternatives

No permission to eat

55% feel guilty about

eating white bread

Most people identify with negative health dimensions of bread (white in particular), yet many rely on it across multiple regular occasions. Despite weekend brunch and relaxed more treat occasions, there are minimal safe zones to consume bread in peoples daily routine without feeling guilty and overly cautious.

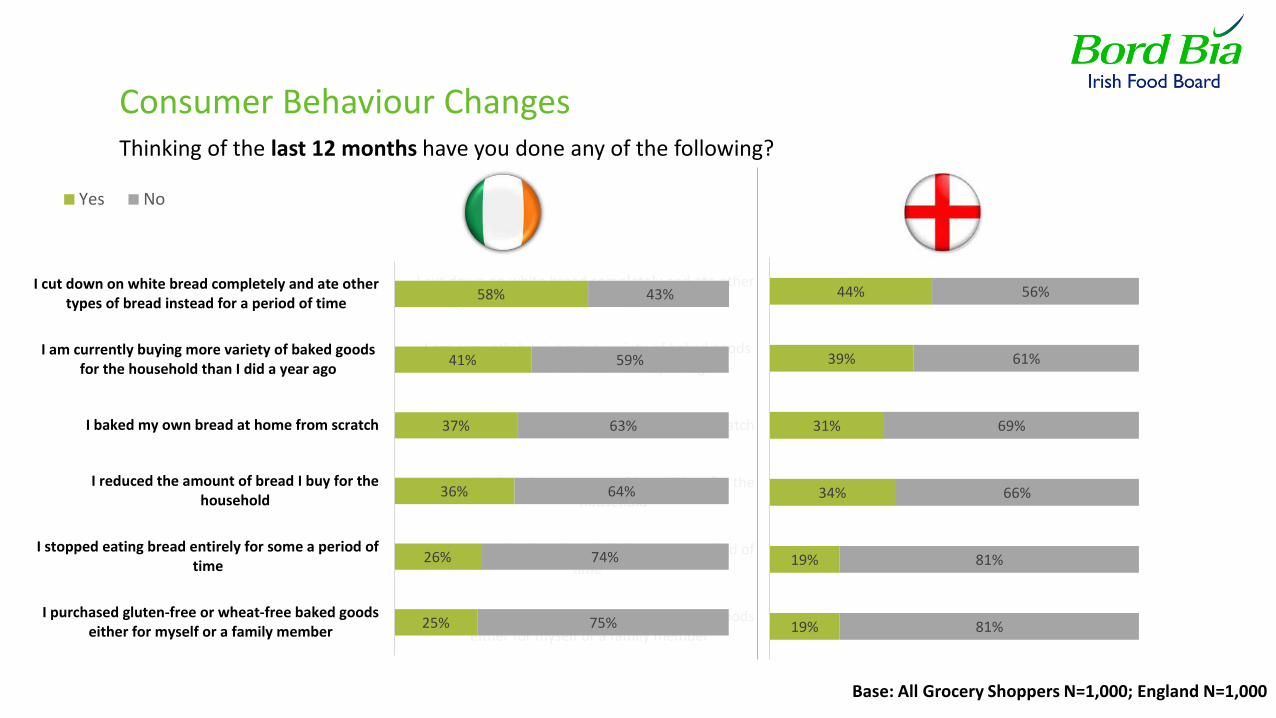

19%

19%

34%

31%

39%

44%

81%

81%

66%

69%

61%

56%

I purchased gluten-free or wheat-free baked goodseither for myself or a family member

I stopped eating bread entirely for some a period oftime

I reduced the amount of bread I buy for thehousehold

I baked my own bread at home from scratch

I am currently buying more variety of baked goodsfor the household than I did a year ago

I cut down on white bread completely and ate othertypes of bread instead for a period of time

Consumer Behaviour Changes Thinking of the last 12 months have you done any of the following?

25%

26%

36%

37%

41%

58%

75%

74%

64%

63%

59%

43%

I purchased gluten-free or wheat-free baked goodseither for myself or a family member

I stopped eating bread entirely for some a period oftime

I reduced the amount of bread I buy for thehousehold

I baked my own bread at home from scratch

I am currently buying more variety of baked goodsfor the household than I did a year ago

I cut down on white bread completely and ate othertypes of bread instead for a period of time

Yes No

Base: All Grocery Shoppers N=1,000; England N=1,000

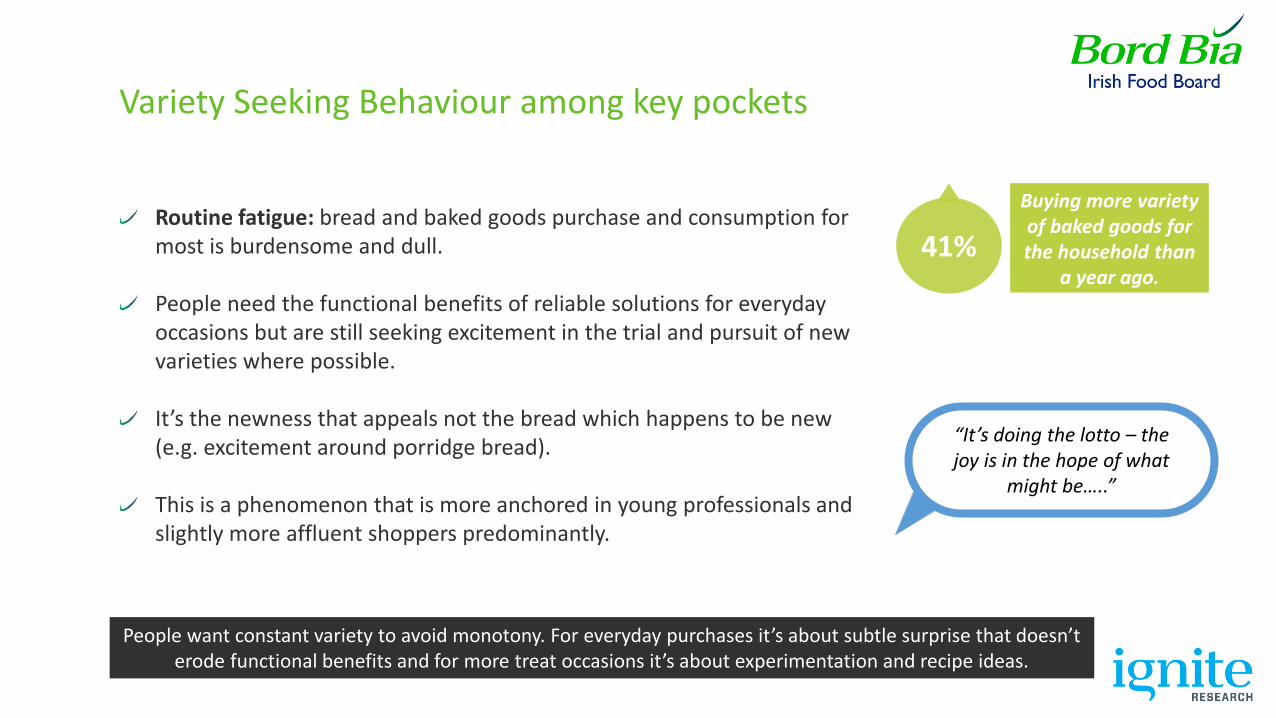

Variety Seeking Behaviour among key pockets

People want constant variety to avoid monotony. For everyday purchases it’s about subtle surprise that doesn’t erode functional benefits and for more treat occasions it’s about experimentation and recipe ideas.

41%

Buying more variety of baked goods for the household than

a year ago.

“It’s doing the lotto – the joy is in the hope of what

might be…..”

Routine fatigue: bread and baked goods purchase and consumption for most is burdensome and dull. People need the functional benefits of reliable solutions for everyday occasions but are still seeking excitement in the trial and pursuit of new varieties where possible. It’s the newness that appeals not the bread which happens to be new (e.g. excitement around porridge bread). This is a phenomenon that is more anchored in young professionals and slightly more affluent shoppers predominantly.

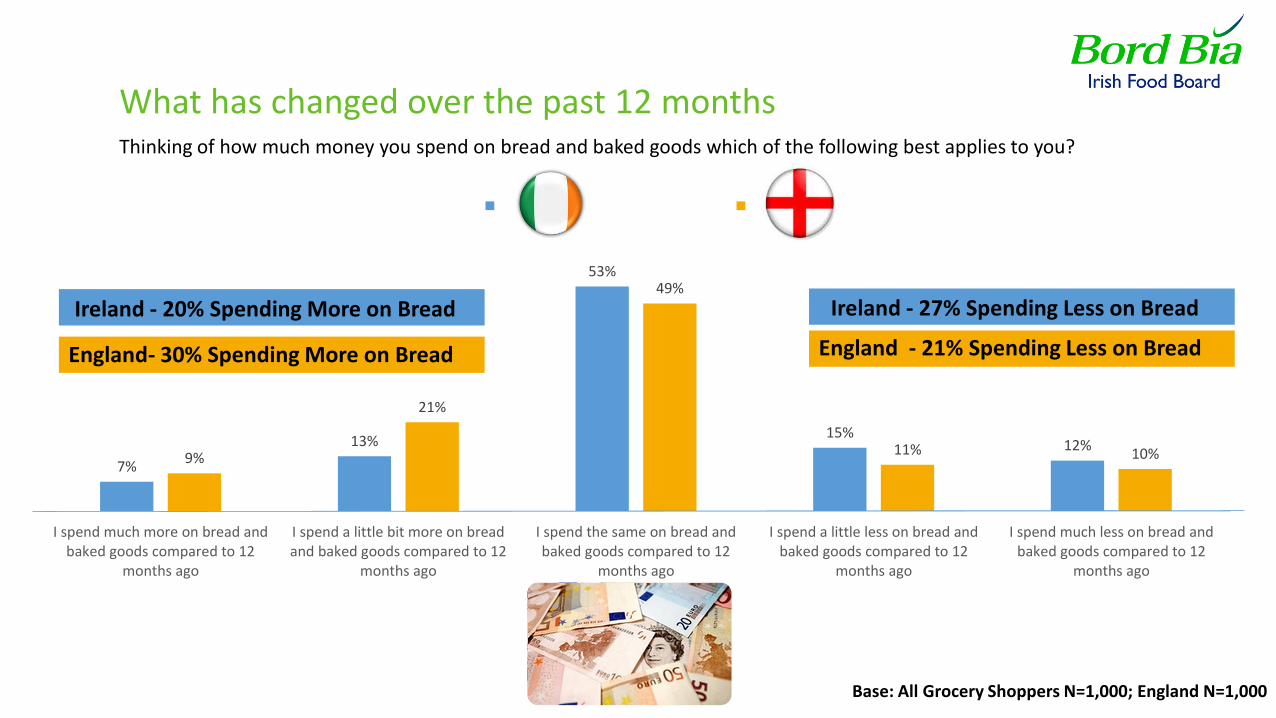

Almost half of all shoppers are changing their baked goods category spend over the past 12 months. Almost equal proportions are increasing and decreasing spend. This is a strong indication of the change and shifting patterns of behaviour that are occurring in the category. This flux can be viewed as an opportunity or threat but represents a sizable space for disruption in the category where winners and losers will be made.

Opportunities & Threats Around the Fringes

Shifting patterns

47% Have changed their level of spend in the category

in the past 12 months

7%

13%

53%

15% 12%

9%

21%

49%

11% 10%

I spend much more on bread andbaked goods compared to 12

months ago

I spend a little bit more on breadand baked goods compared to 12

months ago

I spend the same on bread andbaked goods compared to 12

months ago

I spend a little less on bread andbaked goods compared to 12

months ago

I spend much less on bread andbaked goods compared to 12

months ago

IRL UK

Thinking of how much money you spend on bread and baked goods which of the following best applies to you?

What has changed over the past 12 months

Base: All Grocery Shoppers N=1,000; England N=1,000

Ireland - 27% Spending Less on Bread England - 21% Spending Less on Bread

Ireland - 20% Spending More on Bread

England- 30% Spending More on Bread

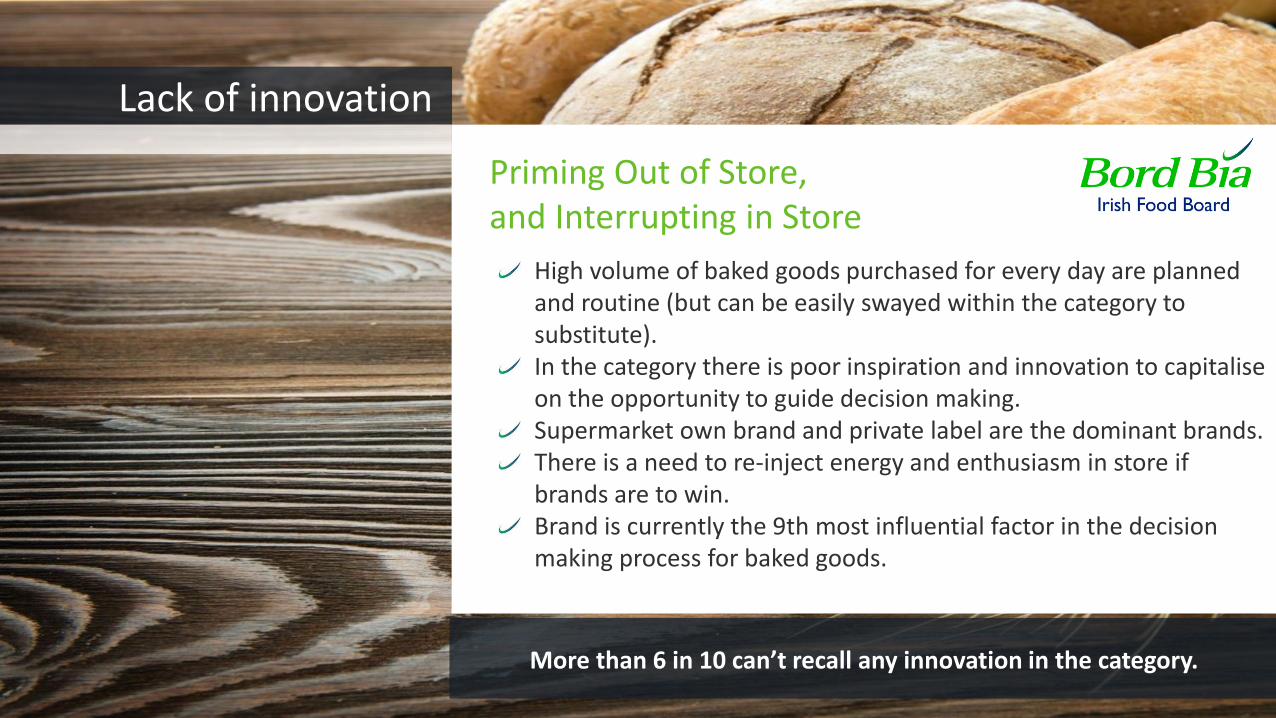

High volume of baked goods purchased for every day are planned and routine (but can be easily swayed within the category to substitute). In the category there is poor inspiration and innovation to capitalise on the opportunity to guide decision making. Supermarket own brand and private label are the dominant brands. There is a need to re-inject energy and enthusiasm in store if brands are to win. Brand is currently the 9th most influential factor in the decision making process for baked goods.

Priming Out of Store, and Interrupting in Store

Lack of innovation

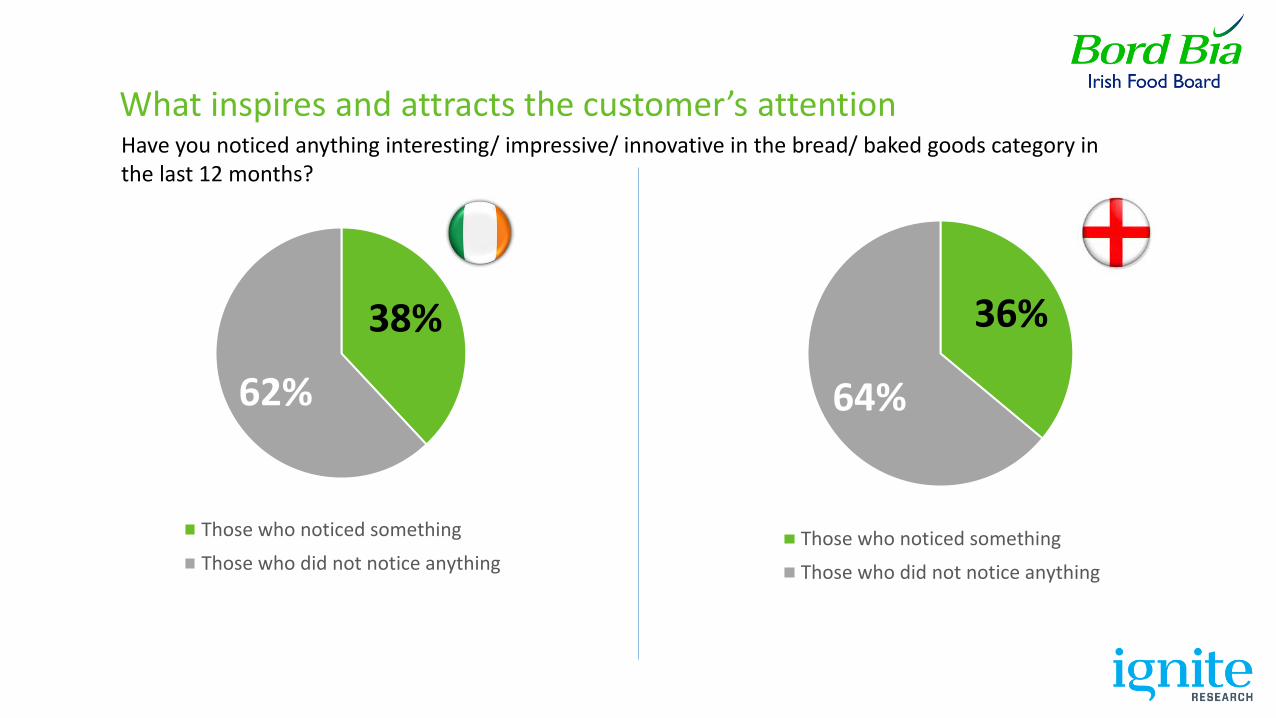

More than 6 in 10 can’t recall any innovation in the category.

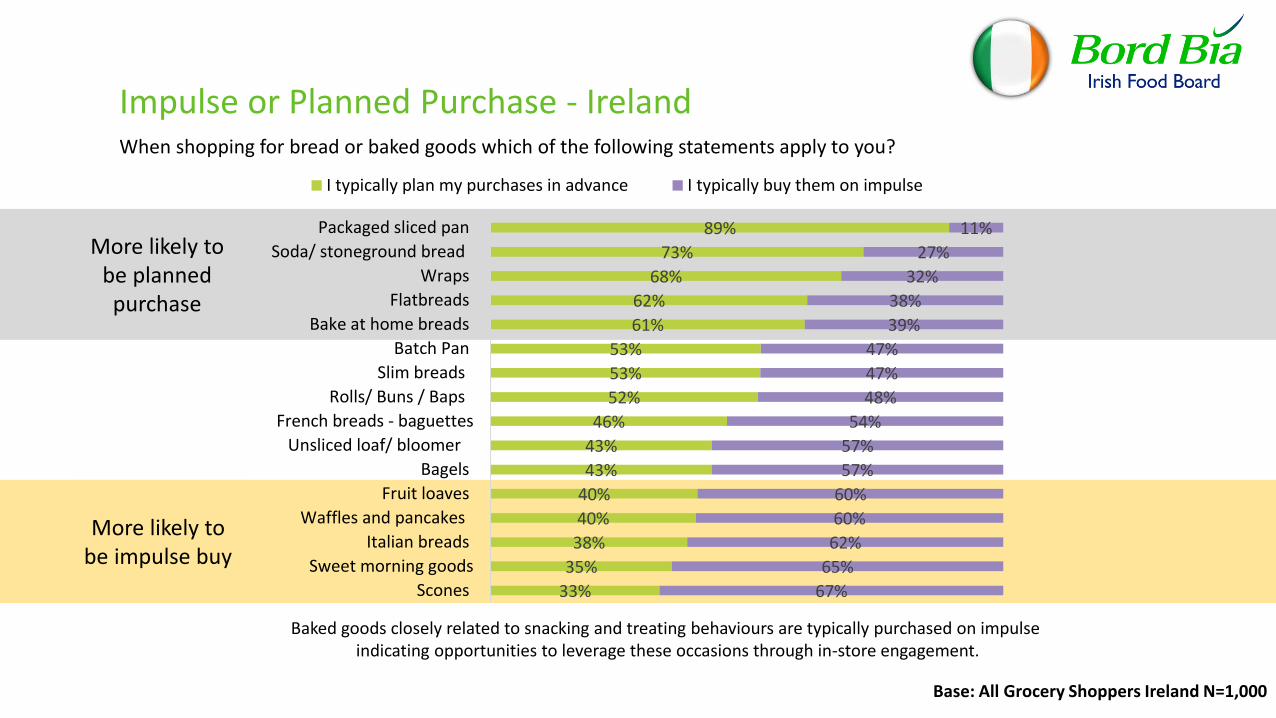

When shopping for bread or baked goods which of the following statements apply to you?

Impulse or Planned Purchase - Ireland

Base: All Grocery Shoppers Ireland N=1,000

33%

35%

38%

40%

40%

43%

43%

46%

52%

53%

53%

61%

62%

68%

73%

89%

67%

65%

62%

60%

60%

57%

57%

54%

48%

47%

47%

39%

38%

32%

27%

11%

Scones

Sweet morning goods

Italian breads

Waffles and pancakes

Fruit loaves

Bagels

Unsliced loaf/ bloomer

French breads - baguettes

Rolls/ Buns / Baps

Slim breads

Batch Pan

Bake at home breads

Flatbreads

Wraps

Soda/ stoneground bread

Packaged sliced pan

I typically plan my purchases in advance I typically buy them on impulse

More likely to be planned purchase

More likely to be impulse buy

Baked goods closely related to snacking and treating behaviours are typically purchased on impulse indicating opportunities to leverage these occasions through in-store engagement.

When shopping for bread or baked goods which of the following statements apply to you?

Impulse or Planned Purchase - England

Base: All Grocery Shoppers England N=1,000

More likely to be planned purchase

More likely to be impulse buy

28%

36%

37%

39%

39%

44%

48%

48%

54%

54%

57%

58%

59%

62%

64%

81%

72%

64%

63%

61%

61%

56%

52%

52%

46%

46%

43%

42%

41%

38%

36%

19%

Scones

Sweet morning goods – e.g. …

Waffles and pancakes

Italian breads

Fruit loaves

Bagels

Batch Pan

French breads

Soda/ stoneground bread

Bake at home breads

Slim breads

Unsliced loaf/ bloomer

Flatbreads

Wraps

Rolls/ Buns / Baps

Packaged sliced pan

I typically plan my purchases in advance I typically buy them on impulse

What inspires and attracts the customer’s attention Have you noticed anything interesting/ impressive/ innovative in the bread/ baked goods category in the last 12 months?

38%

62%

Those who noticed something

Those who did not notice anything

36%

64%

Those who noticed something

Those who did not notice anything

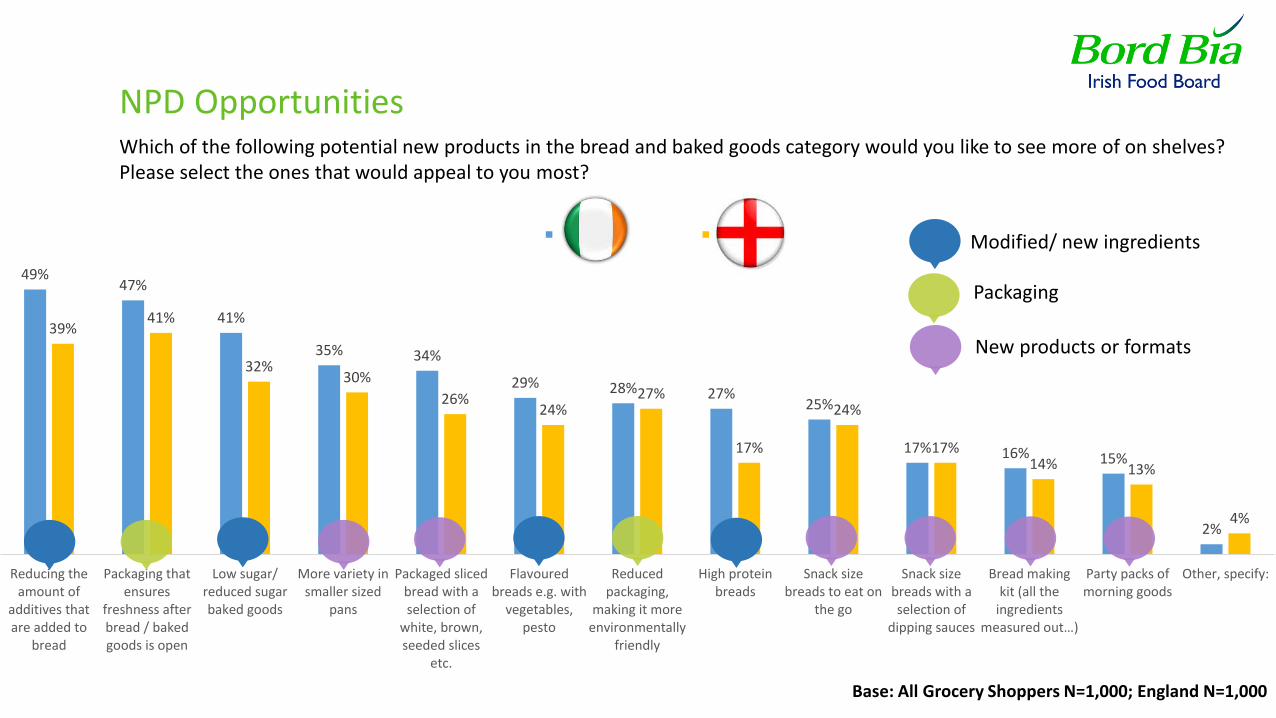

49% 47%

41%

35% 34%

29% 28% 27% 25%

17% 16% 15%

2%

39% 41%

32% 30%

26% 24%

27%

17%

24%

17% 14% 13%

4%

Reducing theamount of

additives thatare added to

bread

Packaging thatensures

freshness afterbread / bakedgoods is open

Low sugar/reduced sugarbaked goods

More variety insmaller sized

pans

Packaged slicedbread with aselection of

white, brown,seeded slices

etc.

Flavouredbreads e.g. with

vegetables,pesto

Reducedpackaging,

making it moreenvironmentally

friendly

High proteinbreads

Snack sizebreads to eat on

the go

Snack sizebreads with aselection of

dipping sauces

Bread making kit (all the

ingredients measured out…)

Party packs ofmorning goods

Other, specify:

IRL UK

Which of the following potential new products in the bread and baked goods category would you like to see more of on shelves? Please select the ones that would appeal to you most?

NPD Opportunities

Base: All Grocery Shoppers N=1,000; England N=1,000

Modified/ new ingredients

Packaging

New products or formats

24%

40%

41%

44%

47%

49%

34%

40%

45%

47%

49%

52%

Added health benefits

Looks freshly baked

Small trial packages available to purchase

Reduced price

On special offer

Getting a sample to taste

IRL UK

7%

12%

14%

24%

18%

25%

9%

16%

20%

23%

28%

30%

If I was shown how it is made

Accompanied with serving suggestions/ recipes(what the bread goes with)

Made from ingredients sourced in Ireland

From a brand I trust

Contains ingredients that I have heard goodthings about

Well presented in store

What would make you more likely to buy a new type/ variety of bread / baked goods that you haven’t tried before?

New product trial

Base: All Grocery Shoppers N=1,000; England N=1,000

Shoppers are characterised by a desire for weekday convenience and weekend experience. The category needs to understand this and tailor not only solutions but also messaging. When speaking to the same target, they are likely to want something entirely different from the category depending upon the time of day or week. Suppliers need to have the correct conversations at the correct time so that they are aligned with what shoppers are actually seeking at that moment.

The Shopper is not Fixed

The Liquid Shopper

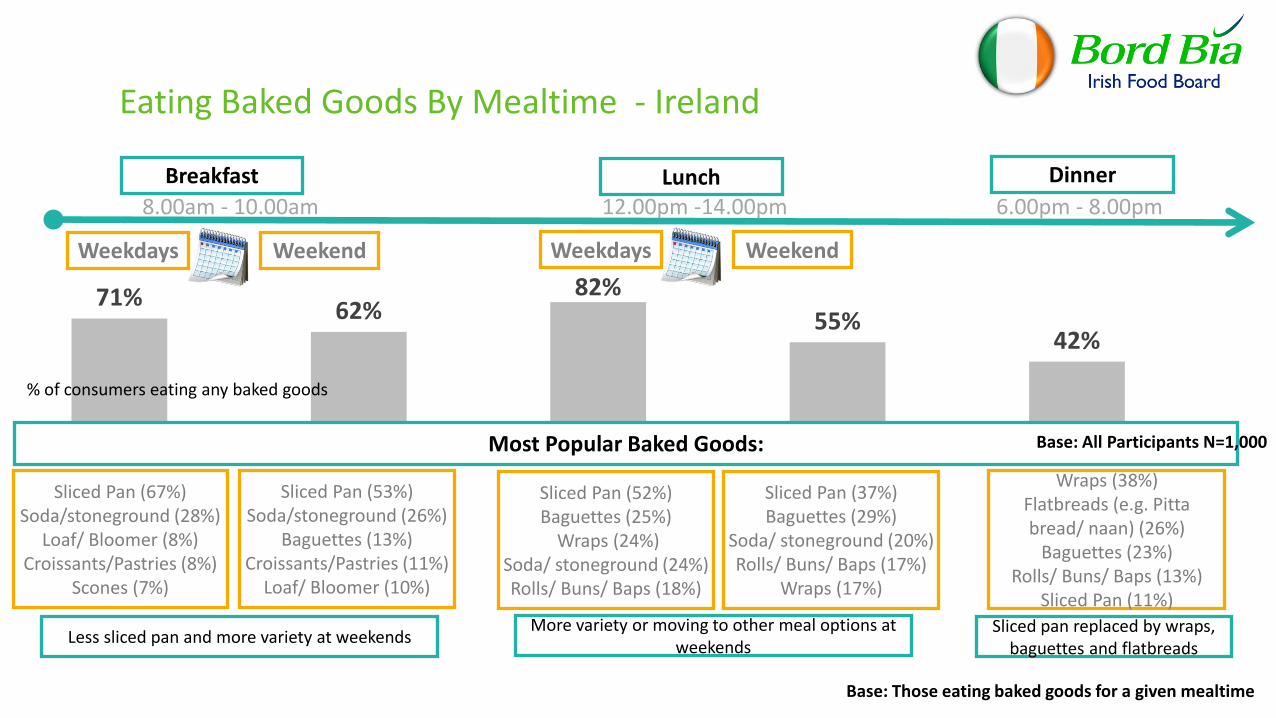

Circa 20% Fall in white sliced pan consumption at the weekend

with rise in more artisan options

71% 62%

82%

55% 42%

Eating Baked Goods By Mealtime - Ireland

8.00am - 10.00am 12.00pm -14.00pm 6.00pm - 8.00pm

Dinner Lunch Breakfast

Weekdays Weekend Weekdays Weekend

Most Popular Baked Goods:

Sliced Pan (67%) Soda/stoneground (28%)

Loaf/ Bloomer (8%) Croissants/Pastries (8%)

Scones (7%)

Sliced Pan (53%) Soda/stoneground (26%)

Baguettes (13%) Croissants/Pastries (11%)

Loaf/ Bloomer (10%)

Sliced Pan (52%) Baguettes (25%)

Wraps (24%) Soda/ stoneground (24%) Rolls/ Buns/ Baps (18%)

Sliced Pan (37%) Baguettes (29%)

Soda/ stoneground (20%) Rolls/ Buns/ Baps (17%)

Wraps (17%)

Wraps (38%) Flatbreads (e.g. Pitta bread/ naan) (26%)

Baguettes (23%) Rolls/ Buns/ Baps (13%)

Sliced Pan (11%)

Less sliced pan and more variety at weekends More variety or moving to other meal options at

weekends Sliced pan replaced by wraps,

baguettes and flatbreads

Base: All Participants N=1,000

% of consumers eating any baked goods

Base: Those eating baked goods for a given mealtime

60% 59% 78%

60% 48%

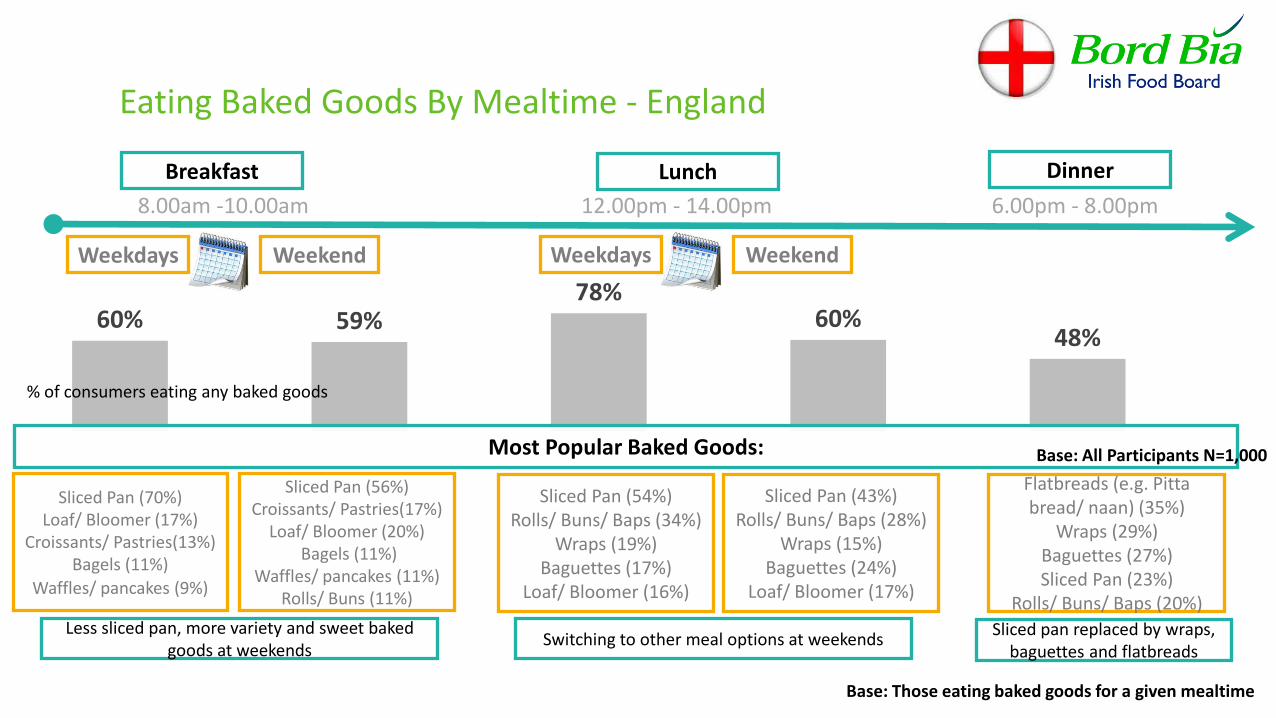

Eating Baked Goods By Mealtime - England

8.00am -10.00am 12.00pm - 14.00pm 6.00pm - 8.00pm

Dinner Lunch Breakfast

Weekdays Weekend Weekdays Weekend

Most Popular Baked Goods:

Sliced Pan (70%) Loaf/ Bloomer (17%)

Croissants/ Pastries(13%) Bagels (11%)

Waffles/ pancakes (9%)

Sliced Pan (56%) Croissants/ Pastries(17%)

Loaf/ Bloomer (20%) Bagels (11%)

Waffles/ pancakes (11%) Rolls/ Buns (11%)

Sliced Pan (54%) Rolls/ Buns/ Baps (34%)

Wraps (19%) Baguettes (17%)

Loaf/ Bloomer (16%)

Sliced Pan (43%) Rolls/ Buns/ Baps (28%)

Wraps (15%) Baguettes (24%)

Loaf/ Bloomer (17%)

Flatbreads (e.g. Pitta bread/ naan) (35%)

Wraps (29%) Baguettes (27%) Sliced Pan (23%)

Rolls/ Buns/ Baps (20%) Less sliced pan, more variety and sweet baked

goods at weekends Switching to other meal options at weekends

Sliced pan replaced by wraps, baguettes and flatbreads

% of consumers eating any baked goods

Base: All Participants N=1,000

Base: Those eating baked goods for a given mealtime

Weekday Convenience & Weekend Experience

• Busy during the week – less time; more of a functional task and seeking to primarily satisfy a lower order physiological need for sustenance rather than taste and enjoyment.

• Quick and practical solutions which are familiar, convenient and good value sought.

• Becomes routine, repetitive and boring – being able to inject excitement as an additional benefit, while not compromising on the convenience or value needs, would be welcome.

The needs of the same individuals shift considerably in terms of what they seek from the bakery category from mid week to weekend

The increase in speciality breads consumed at the

weekend

The decline in consumption of

white slice pan at the weekend

• Weekend brings more time for most and means there is less rushing – seeking more enjoyment and reward after a week of hard work.

• Experiential, exploratory and more sophistication consumption occasions and needs sought to be catered for.

• More experiential and sensory stimulating solutions which are different to the norm (purchase and consumption).

• Value is important but willing to pay premium for the experience and variety.

Weekday Weekend

Discounter

Supermarket

Convenience

Artisan Bakery

Category Management: Key Success Factors

Shopper Behaviour: On the front lines

The squeeze: importance of touch and texture, with most shoppers testing softness before selecting.

Hidden choice is best: Never take from the front is

the mantra of shoppers as they feel others have done “the squeeze” and retailers stock freshest to

the back.

Uncovered bread: considered ok for individuals themselves or staff to touch but not others.

Care in transit: bread placed carefully in

trolley/basket to avoid damage to carefully selected item.

In Store Experience

Well stocked: neat and tidy, no sparse shelves and good selection

Clean and hygienic: particularly for unwrapped

baked goods.

Odour: fresh and homely (ideally smell of freshly baked)

Provenance cues: wood, baskets, parchment, cloth etc. to build theatre and perception of

natural goodness.

Category info: ideas and information – currently quite poor in store.

Online Category Management

As online grows in adoption opportunities and threats for bread and baked goods will become more prominent and potentially drive disruptive innovations in the category.

Online grocery shopping in England has 3 times the population reach than in Ireland (Periscope 2013). Buying fresh produce of any nature, including baked goods online has different challenges than in bricks and mortar stores.

Freshness cues. Variability in batches and across days. Selection of “best” bread rather than any bread.

Online baked goods face new challenges which need to be considered when selling online to shoppers.

A key driver of current thinking and behaviour in the category is anchored around health. The health agenda is not being managed effectively by the category at an overall level and there are many gaps in understanding leading to shopper confusion and misunderstanding. 1 in 4 shoppers buying gluten free but just a minority of these have any intolerance, and very few understand the specific benefits of gluten free overall. Information on health and the category is coming mostly from word of mouth and online. This is focused on diets and health tips mostly, and much is getting lost in translation between the original source (quite often based on sound science) and the decisions being made in store in the baked goods category.

Health is a Central Driver of Category Future

Health agenda

55% feel guilty about eating white bread

Healthy Eating Please tell us how much you agree or disagree with the following statements:

13%

11%

7%

3%

12%

17%

11%

13%

10%

10%

32%

21%

16%

20%

17%

29%

38%

42%

43%

34%

11%

19%

22%

24%

27%

People often turn to me for advice regarding healthy eating

I am actively trying to control how many calories I eat each day

I carefully read all labels on all the food items I buy

I’m up to date with the latest findings on what food is good for you

I’m currently trying to lose weight

Disagree a lot Disagree a little Neither agree or disagree Agree a little Agree a lot

17%

10%

8%

5%

13%

17%

8%

12%

8%

8%

34%

26%

21%

26%

21%

23%

35%

39%

39%

35%

10%

22%

21%

22%

24%

People often turn to me for advice regarding healthy eating

I am actively trying to control how many calories I eat each day

I carefully read all labels on all the food items I buy

I’m up to date with the latest findings on what food is good for you

I’m currently trying to lose weight

Top 2

61%

67%

64%

57%

40%

59%

61%

60%

57%

33%

Base: All Grocery Shoppers N=1,000; England N=1,000

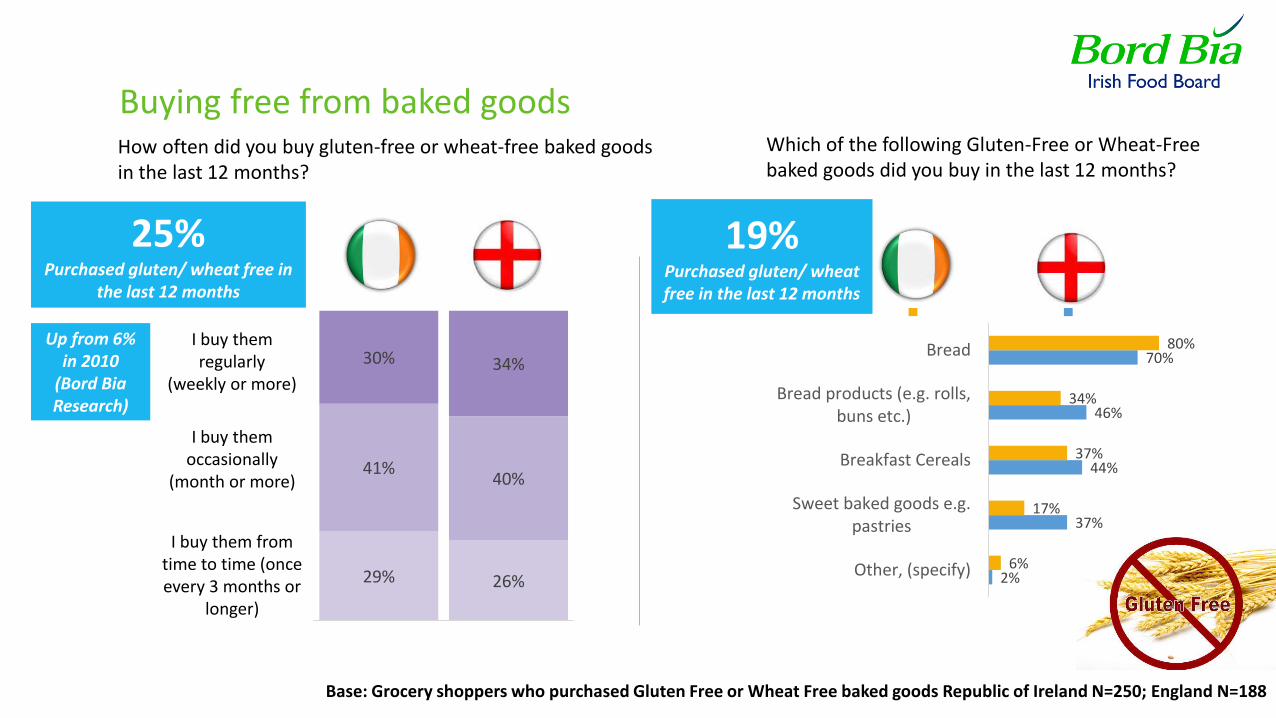

2%

37%

44%

46%

70%

6%

17%

37%

34%

80%

Other, (specify)

Sweet baked goods e.g.pastries

Breakfast Cereals

Bread products (e.g. rolls,buns etc.)

Bread

IRL UK

How often did you buy gluten-free or wheat-free baked goods in the last 12 months?

Buying free from baked goods

Base: Grocery shoppers who purchased Gluten Free or Wheat Free baked goods Republic of Ireland N=250; England N=188

Which of the following Gluten-Free or Wheat-Free baked goods did you buy in the last 12 months?

I buy them regularly

(weekly or more)

I buy them occasionally

(month or more)

I buy them from time to time (once every 3 months or

longer)

29% 26%

41% 40%

30% 34%

IRL UK

25% Purchased gluten/ wheat free in

the last 12 months

19% Purchased gluten/ wheat free in the last 12 months

Up from 6% in 2010

(Bord Bia Research)

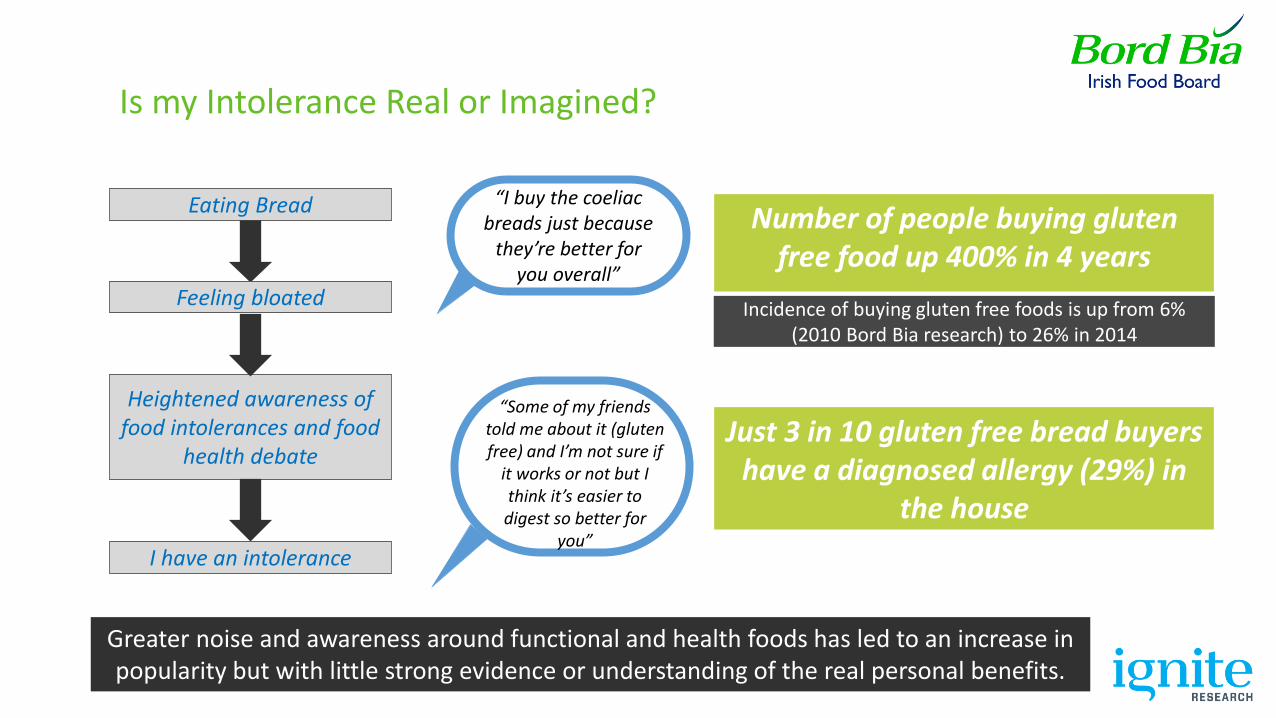

Is my Intolerance Real or Imagined?

Greater noise and awareness around functional and health foods has led to an increase in popularity but with little strong evidence or understanding of the real personal benefits.

Eating Bread

Feeling bloated

Heightened awareness of food intolerances and food

health debate

I have an intolerance

Incidence of buying gluten free foods is up from 6% (2010 Bord Bia research) to 26% in 2014

Number of people buying gluten free food up 400% in 4 years

Just 3 in 10 gluten free bread buyers have a diagnosed allergy (29%) in

the house

“Some of my friends told me about it (gluten free) and I’m not sure if

it works or not but I think it’s easier to digest so better for

you”

“I buy the coeliac breads just because

they’re better for you overall”

0%

10%

20%

30%

40%

50%TV programmes

Social media (e.g. Facebook)

Word of mouth (friends/colleagues)

Searching on the internet(Google)

Blogs

Government organisations (e.g.Food Standards Agency)

Initiatives in schools

Newspapers, magazines

0%

10%

20%

30%

40%

50%TV programmes

Social media (e.g.Facebook)

Word of mouth (friends/colleagues)

Searching on the internet(Google)

Blogs

Government organisations(e.g. Bord Bia, safefood)

Initiatives in schools

Newspapers, magazines

What sources of information do you typically use to get information on the nutrition and health aspects of food?

How consumers source health information

Base: All Grocery Shoppers N=1,000; England N=1,000

Searching on the internet (Google) 43%

TV programmes 38%

Word of mouth (friends/ colleagues) 38%

Searching on the internet (Google) 48%

TV programmes 47%

Word of mouth (friends/ colleagues) 37%

21% 15%

9%

37% 35%

4%

6% 7%

37% 38%

12%

38%

43% 48%

37%

15%

Bread as collateral damage & not a key protagonist

Fast food

Fat

Sugar

Soft drinks

Calories

Carbs

Bread (via carbs primarily)

Alcohol

Salt

Processed

Confectionary

Portion control

Balanced diet

There is a wide ranging debate around health and wellness underway within which bread is a lower order (yet present) focal point

There is an ongoing discussion around health and nutrition which many people are engaged with, but for whom few have a detailed understanding. Most focus of attention is on what are perceived to be the worst offenders of “bad food” and this is where much of the volume of discussion is occurring. Most individuals are focused on what are the rules of good and bad nutrition and are immediately concerned with removing/controlling the worst offenders in the diet.

Bread as collateral damage & not a key protagonist

Fast food

Fat

Sugar

Soft drinks

Calories

Carbs

Bread (via carbs primarily)

Alcohol

Salt

Processed

Confectionary

Portion control

Balanced diet

Bread is on the periphery of “bad agents” in this debate. There is much heresy and misinformation about the

nutritional values of bread (white in particular), which is driving a negative attitude towards bread overall in

terms of health.

There has been no context given to what constitutes good and bad practices in eating a balanced diet

containing bread, and the industry has been particularly quiet on this front from a consumers perspective.

There needs to be a unified industry voice to push back

on the overly negative portrayal of bread in the consumers mind and education is paramount on this

front. Currently much of the information driving consumer knowledge is based loosely on facts and being

shared via WOM.

Bread as a category has done little in the consumers mind to inform and guide the debate around its health credentials and as such is vulnerable to having overly negative perceptions associated with it (particularly white bread).

Mystical Language of Health

• They are aware of many of the health terms

and hot button topics, but have a shallow knowledge of what these are specifically and how/why they impact on health.

Despite much talk about health, shoppers are relatively poorly equipped and educated to navigate the volume of technical terms and metrics used within the health debate – they then default to short cuts for forming opinions

which are driven and shaped by WOM and pop culture rather than hard fact or industry guidance.

Breath of understanding

Depth of understanding

• Shoppers and consumers spend a lot of time and metal energy thinking and talking about health.

• However the technicality of terms and information is confusing to

shoppers.

• Shoppers lack a bigger picture understand or

framework where they can compare and understand the health and nutritional quality of all the options open to them.

• Complex and detailed – could understand if wanted to invest time and energy.

• WOM, social and entertainment/lifestyle chatter drives much of the urban and consensus wisdom – not always accurate or fully formed views, but no challenges from industry to contextualise and empower the debate. May be more an issue for Government policy rather than any one sector, but impacts all sectors – NB education within your category to mitigate against this is critical.

• Easier to look for clues and short cuts (heuristics) which will help them make acceptable decisions (nb key hooks and what’s in fashion drive a lot of the debate).

These are the two most important factors which will command a premium from shoppers. These issues are the ones which shoppers are most interested in within the category. Ironically these are the issues which the category should be very strong in, but recent health debates have called much of what shoppers believed to be true into question and now there is a need to re-connect – those who re-connect best (while keeping an eye on value) will be the big winners in the category.

Freshly Baked and Natural Ingredients are Key

Fresh & Natural

Freshly baked (60%) & only natural ingredients (50%) most

likely to command premium

26%

27%

27%

33%

38%

58%

34%

35%

24%

33%

50%

60%

Containing ingredients with specific health benefits

No added sugar

Made in a traditional manner

Locally baked (i.e. close to where I live)

Only natural ingredients (no artificial additives)

Freshly baked

UK

Which of the following attributes would make you more likely to pay a bit more for bread or baked goods?

What consumers will pay more for

Base: All Grocery Shoppers N=1,000; England N=1,000

7%

13%

14%

20%

21%

22%

25%

12%

16%

22%

21%

29%

35%

24%

Gluten free

If I know exactly how it’s made

Fortified bread (e.g. with vitamins,calcium etc.)

Reduced, more environmentally friendlypackaging

Baked from ingredients sourced in[England / Ireland]

Baked in [England / Ireland]

Hand crafted, artisan

Pseudo Science Shaping Motivations

People’s shallow depth of specific understanding leads to an uninformed thinking process around bread and baked goods.

The Problem The Solution

Strong vilification of white bread in particular based on “pop science” WOM and fad celebrity diets mostly.

Lack of deep and real understanding of nutritional impact of bread and how and why this is good/bad or should fit in

the diet

The perceived problems with white bread are then solved in the consumers mind through various cues and hooks which are

used to counteract the perceived failings of breads health dimensions. (seeds, Gluten free etc all strong hooks here).

There is however little understanding of why or how these

cues have specific benefits that negate the perceived health failings.

Pseudo science and bread: Posing the answer to the question that was never really asked.

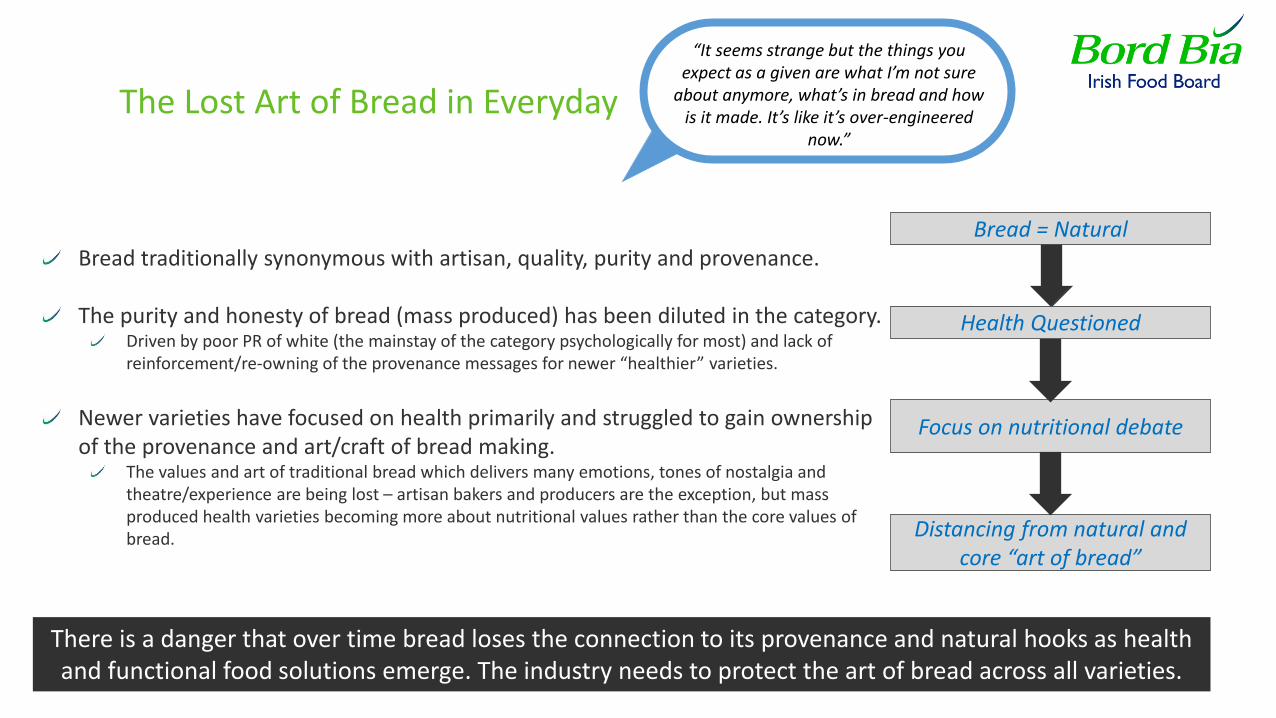

The Lost Art of Bread in Everyday

There is a danger that over time bread loses the connection to its provenance and natural hooks as health and functional food solutions emerge. The industry needs to protect the art of bread across all varieties.

Bread = Natural

Health Questioned

Focus on nutritional debate

Distancing from natural and core “art of bread”

“It seems strange but the things you expect as a given are what I’m not sure

about anymore, what’s in bread and how is it made. It’s like it’s over-engineered

now.”

Bread traditionally synonymous with artisan, quality, purity and provenance. The purity and honesty of bread (mass produced) has been diluted in the category.

Driven by poor PR of white (the mainstay of the category psychologically for most) and lack of reinforcement/re-owning of the provenance messages for newer “healthier” varieties.

Newer varieties have focused on health primarily and struggled to gain ownership of the provenance and art/craft of bread making.

The values and art of traditional bread which delivers many emotions, tones of nostalgia and theatre/experience are being lost – artisan bakers and producers are the exception, but mass produced health varieties becoming more about nutritional values rather than the core values of bread.

Heuristics in Decision Making and The Power of Seeds

We are making decisions in store to buy baked goods based on short cuts that help us estimate how each product will solve our problems/satisfy our needs. These shortcuts are currently being dominated by a combination of price and health heuristics in the category.

Heuristics

A heuristic is a mental shortcut that allows people to solve problems and make judgments quickly and efficiently.

These rule-of-thumb strategies shorten decision-making time and allow people to function without constantly stopping to

think about their next course of action.

While heuristics are helpful in many situations, they can also lead to biases.

(Source:psychology.about.com)

Low levels of conscious thinking or understanding about the ingredients or processing of bread (unless in a negative context when thinking of poor health cues for white bread).

With a latent perception that bread is not healthy, shoppers are looking for ways to mitigate the poor health credentials.

Shoppers want to reduce and avoid the “bad breads” and are looking for cues to help them select “good breads”.

Two key heuristics short cuts used:

Seeds and tangible visible additions that are considered healthy. Functional food dimensions: Low, GI, Celiac, Gluten/wheat free etc.

There is a strong need and appetite for education in category. Shoppers have key issues top of mind which bring many questions. They have a health challenge to the category which they are looking for assistance in solving. Currently poor information and poor understanding leads to weak choices in category, where shoppers do not feel empowered and have doubt over whether they have made, and continue to make, the right choice for them.

Category Education is Urgently Needed

Education needed

56% Interested in learning more about the actual health benefits

of some of the ingredients added to bread.

Lack of Information

Despite the volume and frequency of bread consumption and the discussions around the health impact of bread, there is a notable dearth of real understanding about bread………… How much bread is ok to eat each day?

How much bread is it recommended that I eat each day?

What are the positive nutritional benefits of bread? What are the negative nutritional drawbacks of bread? How does the nutritional value of different breads vary?

42% Feel confused about the health benefits

of different types of bread

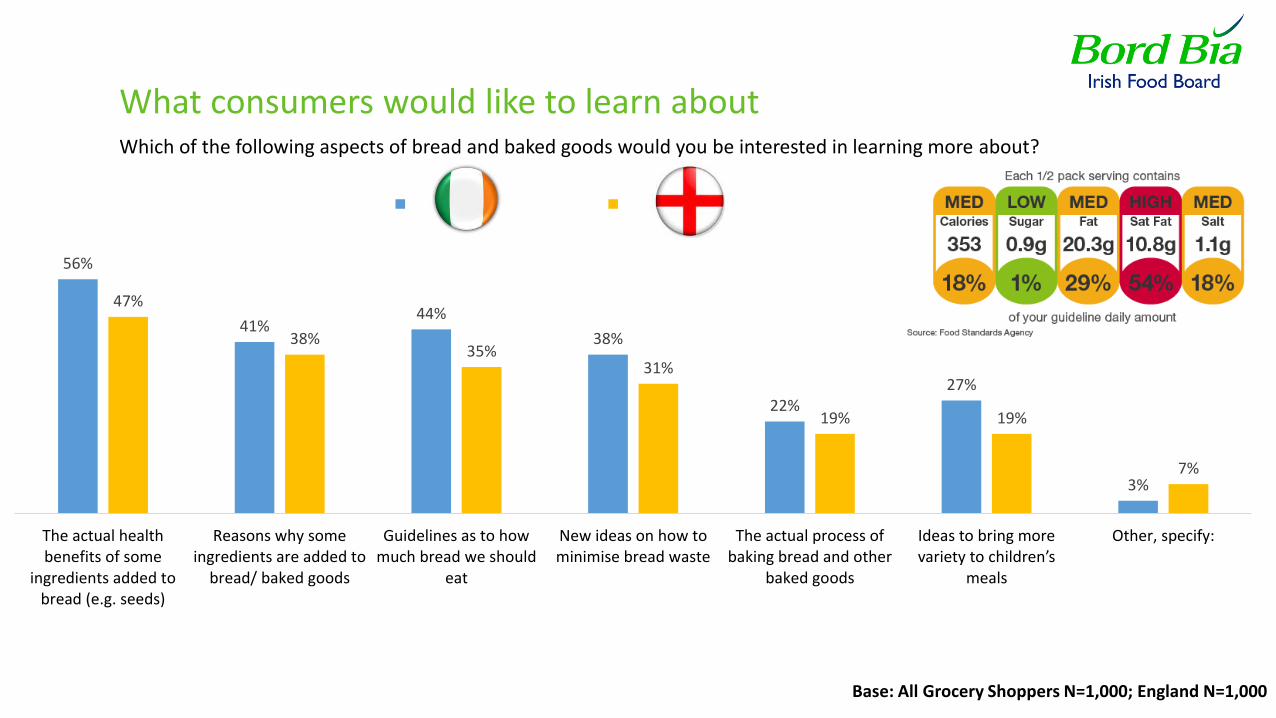

Which of the following aspects of bread and baked goods would you be interested in learning more about?

What consumers would like to learn about

Base: All Grocery Shoppers N=1,000; England N=1,000

56%

41% 44%

38%

22% 27%

3%

47%

38% 35%

31%

19% 19%

7%

The actual healthbenefits of some

ingredients added tobread (e.g. seeds)

Reasons why someingredients are added to

bread/ baked goods

Guidelines as to howmuch bread we should

eat

New ideas on how tominimise bread waste

The actual process ofbaking bread and other

baked goods

Ideas to bring more variety to children’s

meals

Other, specify:

IRL UK

Build a factual and consistent narrative and view of the category which will satisfy the current need for health solutions but also provides clarity on what the category does and does not offer.

Final Thoughts

Health & Education are key:

In store inspiration: The opportunity to influence behaviour in store is significant. Retailers and own label are managing this well to their own effect. Brands need to be more engaged in a conversation with shoppers in store to increase success.

Moving Targets: Same Shopper, multiple needs Shoppers want many different baked goods at many different times. Brands need to acknowledge this, build relevant solutions and position them in not only the right locations but at the correct times. Constant innovation and variety is a must Variety seeking behaviour is strong and likely to be a feature of the category into the future. Brands must have the agility to constantly engage and surprise shoppers to satisfy their needs, while having an omnipresent and excellent core range which satisfies their core everyday needs. Without this variety, the core solutions lose traction and stickiness with shoppers and become easily replaceable and substitutable at point of sale.

Some Quick Wins

Freshness cues and information (provenance, when baked and landed in store)

Innovation and variety (constant and incremental NPD to excite and inspire)

Brand values and essence (define what you stand for and commit)

Have conversations across the customer journey (out of store, and in store)

Educate and Inspire (meal solutions, occasion ideas and recipes)

Category Management in store (layout and shelf position, stock levels and availability across the day)

1. Education via Pack Design (nutritional info & brand visibility in store)

2.

3.

4.

5.

6.

7.