bachelor thesis web viewbachelor thesis. cultural impact on ... due to the growth of multinational...

TRANSCRIPT

Bachelor Thesis

Cultural Impact on Accounting Practices

Does it disappear after the introduction of IFRS?

Supervisors: dr C.D. Knoops and drs H.J. Bouwer

ERASMUS UNIVERSITY ROTTERDAM

Erasmus School of Economics

Section: Accounting, Auditing and Control

Name : Bebi Merinda

Student number : 326348

E-mail address : [email protected]

Table of ContentsTable of Contents............................................................................................................................................2

1. Introduction............................................................................................................................................4

1.1. Background.....................................................................................................................................4

1.2. Problem definition..........................................................................................................................5

1.3. Relevance........................................................................................................................................5

1.5. Methodology..................................................................................................................................8

2. International Financial Reporting Standards..........................................................................................9

2.1. Introduction....................................................................................................................................9

2.2. History of IFRS.................................................................................................................................9

2.3. Characteristics of IFRS standards..................................................................................................10

2.4. IFRS adoption................................................................................................................................11

2.5. Conclusion.....................................................................................................................................12

3. Relationships of culture and accounting..............................................................................................13

3.1. Introduction..................................................................................................................................13

3.2. Prior the Hofstede-Gray framework.............................................................................................13

3.3. Hofstede’s cultural dimensions....................................................................................................15

3.4. The Hofstede-Gray’s Framework..................................................................................................17

3.5. Evaluation of the Hofstede-Gray framework on theoretical basis...............................................19

3.6. Conclusion.....................................................................................................................................20

4. Findings.................................................................................................................................................21

4.1. Introduction..................................................................................................................................21

4.2. No IAS / IFRS in research design...................................................................................................21

4.2.1. Authority and enforcement..................................................................................................21

2

4.2.2. Measurement practices........................................................................................................22

4.2.3. Disclosure practices..............................................................................................................23

4.2.4. Other Findings......................................................................................................................24

4.3. IAS / IFRS in research design.........................................................................................................25

4.3.1. Authority and enforcement..................................................................................................25

4.3.2. Measurement practices........................................................................................................26

4.3.3. Disclosure practices..............................................................................................................29

4.3.4. Other findings.......................................................................................................................30

5. Analysis.................................................................................................................................................31

5.1. Introduction..................................................................................................................................31

5.2. Analysis of findings.......................................................................................................................31

5.3. Conclusion.....................................................................................................................................32

6. Conclusion.............................................................................................................................................33

References....................................................................................................................................................34

Appendix.......................................................................................................................................................38

3

1. Introduction

1.1. Background

Due to the growth of multinational companies and an increasing trend in globalization, there is a

need for a single set of accounting standards that facilitates the process of exchanging, sharing and

reporting financial results for international business activities. The trend towards harmonization of

international accounting standards has evolved in the past three decades. Most common obstacles of

harmonization process are listed by Elnathan and Krlich (1992). The three common obstacles are the

differences in national accounting systems, nationalism and language differences. The first obstacle is

related to the differences in the users of financial reporting and legal systems, the second obstacle is

related to cultural differences and national pride and the third one is related to proper communication

channels in interpretation of different terminology.

Despite of these obstacles, the International Accounting Standards Board (IASB) prevails to

develop a single set of high-quality reporting standards called International Financial Reporting

Standards (IFRS). The publicity of IFRS is an important milestone in the harmonization process of

accounting practices. Nowadays, IFRS is the basis of the financial reporting standards of most countries

and encouraged improvement and convergence of accounting standards.

Several years further away since the introduction of IFRS, it seems that systematic differences in

the accounting practices between countries which applied IFRS still exist (Ball, 2006; Kvaal and Nobes,

2010). It seems that even after IFRS adoption, many companies are still preserved their national

accounting practices in a way that minimizes as far as possible changes in the form of financial reporting

that they applied under their previous national GAAPs (Ernst&Young, 2006).

There are many relevant literatures related to international differences in financial reporting

prior to IFRS adoption. Few reasons of IFRS implementation differences have been suggested such as

legal system, providers of finance, taxation, culture and other external factors (Nobes and Parker, 2004,

ch. 2). Harrison and McKinnon (1986) list some elements of a general theoretical model, but there is no

specification which factors are major explanatory variables for accounting practices. In 1988, Gray

develops a model based on Hofstede’s (1980) cultural / societal values related to accounting practices. In

his model, he draws a link between societal values and accounting values, and how both values reinforce

accounting practices in a particular country. The framework was extended by Doupnik and Salter (1995)

who developed a general model of accounting development which links external environment, culture

4

and institutional structures to accounting practices. Culture has been established by former researchers

to be one of the major reasons of differences in accounting practices (Doupnik and Salter, 1995; Nobes,

1998).

1.2. Problem definitionRelated to the evidence found in previous investigation of cultural influences on accounting

practices, this paper tries to analyze whether cultural differences across countries can be an explanation

for differences in accounting practices across countries. The goal of this paper is not to examine

accounting differences prior to IFRS adoption, but rather to use evidence found in the previous research

as a guidance to find cultural impacts on IFRS implementation. It aims to answer the research question:

“Does culture have an influence on accounting practices especially IFRS practices?”

Theory suggests that cultural impact on accounting practices will disappear due to the

standardization of accounting practices after the introduction of IFRS (Nobes and Parker, 2004; Deegan,

2009). I will try to answer the question whether the impact of culture is different in studies that

incorporate IFRS in their research design as compared to studies that do not. The focus is on studies

which use the Hofstede-Gray framework (1988) that relates culture and accounting values to accounting

systems and practices. The accounting systems / practices are concerned with four different areas

namely authority, enforcement, measurements and information disclosures. Below are the sub-

questions which help to answer the research question:

1. Do societal and accounting values influence the authority of professional assurance and the

enforcement of accounting standards especially IFRS?

2. Do societal and accounting values influence differences in the application of accounting

measurements especially IFRS measurement?

3. Do societal and accounting values influence the information disclosure especially IFRS

disclosures?

1.3. RelevanceIn perspective of financial markets, high quality of financial statements contributes to lowering

cost of capital since trustworthiness of an investor to financial reports appeals them to provide capital at

a lower cost. Therefore countries which adopt an internationally recognized and understood accounting

standard for financial statement will gain significant advantages to those who do not (Sharpe, 1998). The

harmonization of financial reporting is expected to increase market efficiency by reducing monitoring

5

costs and decreasing cost of raising capital. Some empirical studies suggest positive effects of IFRS

adoption on financial markets efficiency. Daske et al. (2008) investigate the economic consequences of

compulsory IFRS adoption around the world. Using a large sample of firms which are obligated to adopt

IFRS, they found an increase in average market liquidity around the time of the IFRS introduction, a

decrease in firm’s cost of capital and an increase in equity valuations.

Investors believe that the benefit of IFRS adoption outweighs the implementation cost . This is

affirmed by an empirical study of market reaction to events surrounding the adoption of IFRS in Europe

(Armstrong et al., 2010). They found significant positive market reactions to events that increased the

likelihood of IFRS adoption and vice versa. Another empirical study suggests strong positive abnormal

returns of IFRS adoption and a substantial long-run reduction in the cost of capital (Karamanou et al.,

2005). From an economic point of view, early evidences indicate that the harmonization process

appears to bear its fruit which is to accommodate financial markets with high quality information and

improve capital market efficiency by increasing accessibility of global capital and lowering cost of capital

(Guggiola, 2010).

Despite of the evidence that IFRS adoption has positive economic consequences, there are still

some aspects to be improved in comparability and consistency of financial statements that comply with

IFRS. By focusing on one factor i.e. culture, this paper analyzes the extent of cultural impact, if there is

any, on accounting practices when IFRS is incorporated in the research design. It investigates whether

culture is a possible cause of international differences in the standardization of accounting practices. By

understanding the underlying reason of differences in accounting practices, standard-setting bodies can

take into account the societal and accounting values in the agenda of IFRS implementation. Furthermore,

this paper contributes in informing users that the claim of consistent and full comparability of financial

statements under IFRS standards have not yet been accomplished and culture may be an important

explanatory variable. It also reminds standard setters to take into account that inevitable cultural

differences may influence the implementation of proposed accounting standards.

6

External InfluencesForces of nature

TradeInvestmentConquest

Ecological InfluencesGeographicEconomic

DemographicGenetic / Hygiene

HistoricalTechnologicalUrbanization

Institutional ConsequencesLegal system

Corporate ownershipCapital markets

Professional associationsEducationReligion

Societal Values

Accounting SystemsAccounting Values

REINFORCEMENT

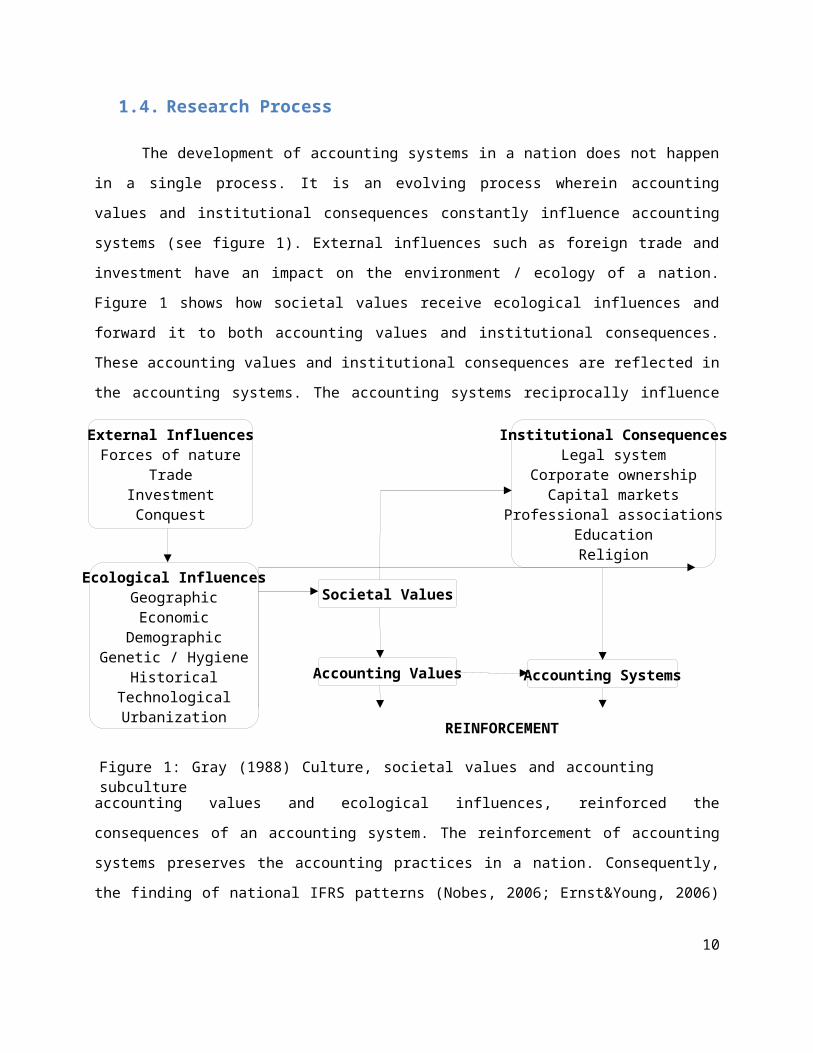

Figure 1: Gray (1988) Culture, societal values and accounting subculture

1.4. Research Process

The development of accounting systems in a nation does not happen in a single process. It is an

evolving process wherein accounting values and institutional consequences constantly influence

accounting systems (see figure 1). External influences such as foreign trade and investment have an

impact on the environment / ecology of a nation. Figure 1 shows how societal values receive ecological

influences and forward it to both accounting values and institutional consequences. These accounting

values and institutional consequences are reflected in the accounting systems. The accounting systems

reciprocally influence accounting values and ecological influences, reinforced the consequences of an

accounting system. The reinforcement of accounting systems preserves the accounting practices in a

nation. Consequently, the finding of national IFRS patterns (Nobes, 2006; Ernst&Young, 2006) is not

surprising because accounting values are implanted in the root of accounting practices of a country.

After the introduction of a new standard, that is IFRS, accounting practices should comply with

that new standard. The development of accounting systems at the sub-cultural level is related to societal

values orientations, since such values pervade a nation’s social system (Gray, 1988). If societal values do

not change, correspondingly it is expected that accounting values also do not change. Since societal

7

values remain unchanged and likewise accounting values, therefore IFRS practice is inevitably impacted

by the culture of the related country.

Using three sub-questions which have been mentioned before, a comparison will be made

between accounting practices before and after the introduction of IFRS. However, due to the absence of

empirical literature about cultural influences on IFRS implementation, this kind of comparison cannot be

made. Therefore I review empirical studies that incorporate accounting rules based on IAS / IFRS in their

research design and discuss these studies further in the section of analysis. There are three accounting

practices to be examined: authority and enforcement, measurement practices, and information

disclosure. These three accounting practices are expected to be similar or converged when a uniform set

of accounting standards i.e. IFRS is applied. If convergence in the accounting practices does not happen,

the extent of culture as a possible explanation on this divergence will be investigated. Empirical

literatures are used to identify whether influences of cultural values through accounting values of a

nation appear in these three accounting practices.

1.5. Methodology

The methodology of this thesis is based on literature review. This exploratory study relies on the

work of former researchers and takes logical inferences based on their studies. There are two theories

that will be used i.e. a theory of Hofstede (1980) on societal values and a theory of Gray (1988) that links

Hofstede’s societal values to accounting values and accounting systems / practices. The latter is known

as the so-called Hofstede-Gray framework and my literature review studies consist of studies that make

use of this framework.

The structure of this paper proceeds as follows: section one defines the problem statement and

relevancy of this paper to the readers; section two describes the history of IFRS, its characteristics and

the adoption of IFRS around the world; section three explains the relationship between culture and

accounting using the Hofstede-Gray framework; section four presents some empirical studies that use

the Hofstede-Gray framework since Gray (1988) never did empirical test on his own framework. These

empirical studies are presented in three parts: authority and enforcement, measurement practices and

disclosures; section five provides analysis of empirical findings from section four; finally section six

provides conclusions of the whole thesis and some suggestions for further research.

8

2. International Financial Reporting Standards

2.1. Introduction

This section provides a brief description of the history of IFRS, the characteristics of IFRS

standards and the meaning of IFRS as a principle-based standard and the lists of countries which decided

to adopted IFRS as their accounting standards, suggesting the success of IFRS towards its goal as a set of

globally accepted financial reporting standards.

2.2. History of IFRS

The history of accounting standards and rules began in 1966. The objective was to create an

International Study Group containing several accounting groups from different countries such as the

American Institute of Certified Public Accountants, the Canadian Institute of Chartered Accountants and

the Institute of Chartered Accountants of England and Wales. In 1967 the study group was created,

under the name of Accounting International Study Group. Six years later, these groups established an

international body writing accounting standards under the name of International Accounting Standards

Committee (IASC) through an agreement by professional accounting bodies from Australia, Canada,

France, Germany, Japan, Mexico, the Netherlands, the United Kingdom and Ireland, and the United

States. The main reason behind the setting up of IASC was to develop accounting standards to be

accepted around the world for the improvement of financial reporting internationally. Throughout the

years, there were some changes to its structure and functioning. The most notable one is the increase in

IASC’s sponsorship from nine original accounting bodies to 152 accounting bodies from 112 countries

(Ankarath et al., 2010). This fundamental change drew the attention of governments, standard-setting

bodies, securities regulators and the business community on the effort of IASC to develop a single set of

accounting standards to be adopted by most countries worldwide. In 2001, the IASC was replaced by the

International Accounting Standard Board (IASB).

The IASB is an independent standard-setting body under the IFRS foundation. The objective of

IFRS foundation is “to develop a single set of high-quality, understandable, enforceable and globally

accepted financial reporting standards based upon clearly articulated principles” (see IASB website). The

new accounting standards published in a set of standards called International Financial Reporting

Standards (IFRS).

9

2.3. Characteristics of IFRS standards

In the development of IFRS, the IASB emphasized on sound and clearly stated principles from

which an interpretation is important. It is also referred to as a principle-based standard. In a principle-

based standard, there are fundamental understandings about transactions and economics events which

lead any other rules established in the standard. Because it does not address every accounting issue, the

implementation of a principles-based standard requires professional judgments from accountants in

making estimation of certain events and transactions (Carmona et al., 2008). In contrary a rule-based

standard such as U.S. GAAP consists considerably more application guidance (or rules). In general, IFRS

do not give clear guidelines when distinguishing among circumstances in which different accounting

requirements are specified (Ankarath et al., 2010). This reduces the opportunities to arranging

transactions to attain particular accounting effects, as what happened at the famous accounting scandal

during year 2002 in the United States. The principle-based approach reduces the length of the text of the

IFRS which is about 2000 to 3000 pages in length, in contrast with U.S. GAAP which covers more than

20.000 pages of literatures (Ankarath et al., 2010).

From 1973 until 2000, the IASC has established International Accounting Standards (IAS). Since

the replacement of its predecessor IASC, the IASB has made some amendments to IAS by replacing some

IAS with new IFRS and proposing new IFRS on topic for which has not been covered in the previous IAS.

In broad term, IFRS refers the entire body of IASB publications including standards and interpretations

approved by the IASB and its predecessor IASC. Next to IFRS, the IASB also issued the IASB framework

which addresses accounting issues that are not stated directly in the standards. The framework is the

underlying concepts in the preparation and presentation of financial statements i.e. the objectives,

assumptions, characteristics, definitions and criteria that guide financial reporting. The framework is

referred to as the ‘conceptual framework’ and does not have the force as a standard. Thus in case of a

conflict, the requirements of IFRS prevail over the conceptual framework. The IASB revises the

conceptual framework from time to time according to the new information and future development.

As addressed in IAS 1, the information provided in financial statements should be useful to the

users and has attributes of the qualitative characteristics. In the framework, there are four principal of

qualitative characteristics: understandability, relevance, reliability and comparability. IASB acknowledges

that there is likely a trade-off between different characteristics of information. Therefore in such case, a

proper balance among these characteristics must be pursued in order to satisfy the objective of financial

10

statements for example a tradeoff between providing reliable information by taking time to ensure a

right judgment in estimating the transactions and reporting relevant information in a timely manner.

Information may lack of its relevancy to the users if it is not reported in a timely manner. Information

which is subject to measurement uncertainty (e.g. the fair value of financial instruments) is difficult to

present them in a reliable way. It may be represent in a reliable way (e.g. through historical cost of

financial instruments) but not essentially relevant.

2.4. IFRS adoption

The collapsed of Enron followed by other accounting fraud cases which erupted in 2002 exposed

the shortcomings of the U.S. ‘rules-based’ standard. The rules-based approach which is common in U .S.

GAAP has been criticized, contrasting it with the principles-based standards such as IFRS. Shortly after

the major accounting scandals in the United States, a Convergence Project between IASB and the U.S.

accounting standards board i.e. Financial Accounting Standards Board (FASB) started which aims to

narrow the differences between U.S. GAAP and IFRS. In 2007, the US Securities and Exchange

Commission (SEC) allowed non-U.S. companies registered in the United States to comply with IFRS

without any necessity to reconcile with U.S. GAAP. SEC also published a proposed roadmap on IFRS

adoption for domestic U.S. companies. The assessment of these convergence milestones will determine

whether to mandate the adoption of IFRS in the United States. The decision of the adoption will be made

in 2011 (see IASB website). The U.S. involvement in the harmonization of accounting standards fosters

the global acceptance of IFRS given that the U.S. constitutes the world’s major capital market (Deegan,

2009, p. 121).

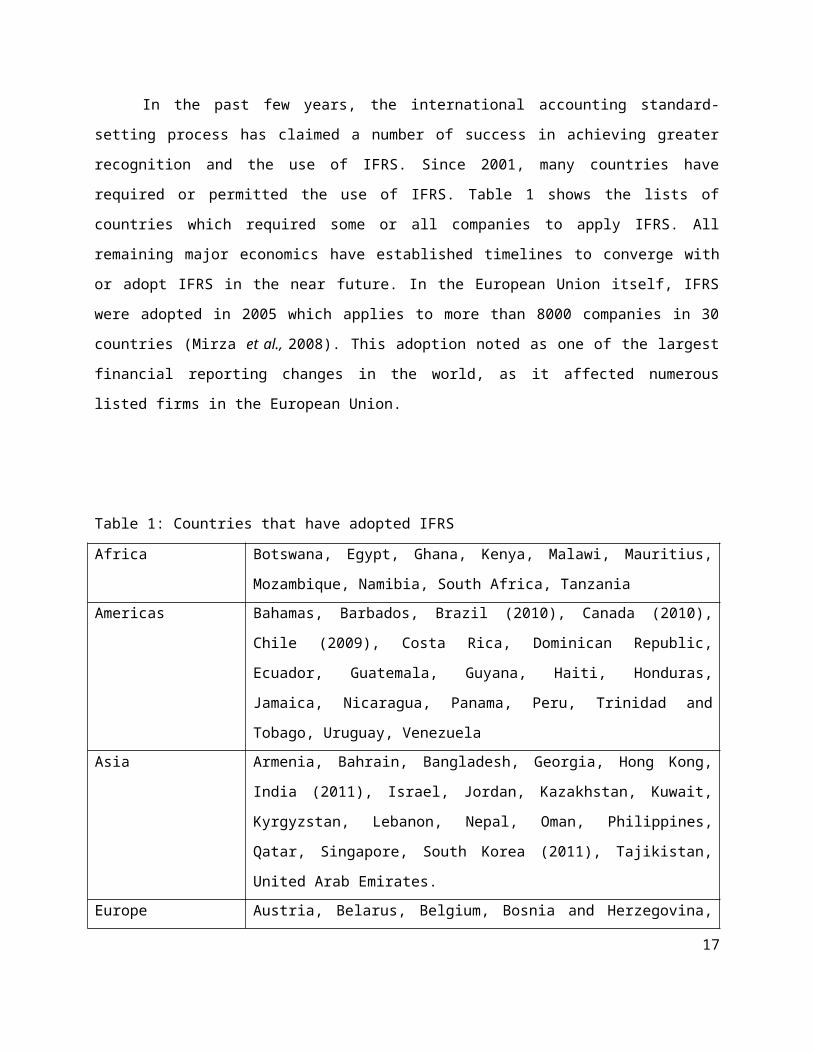

In the past few years, the international accounting standard-setting process has claimed a

number of success in achieving greater recognition and the use of IFRS. Since 2001, many countries have

required or permitted the use of IFRS. Table 1 shows the lists of countries which required some or all

companies to apply IFRS. All remaining major economics have established timelines to converge with or

adopt IFRS in the near future. In the European Union itself, IFRS were adopted in 2005 which applies to

more than 8000 companies in 30 countries (Mirza et al., 2008). This adoption noted as one of the largest

financial reporting changes in the world, as it affected numerous listed firms in the European Union.

11

Table 1: Countries that have adopted IFRS

Africa Botswana, Egypt, Ghana, Kenya, Malawi, Mauritius, Mozambique, Namibia,

South Africa, Tanzania

Americas Bahamas, Barbados, Brazil (2010), Canada (2010), Chile (2009), Costa Rica,

Dominican Republic, Ecuador, Guatemala, Guyana, Haiti, Honduras, Jamaica,

Nicaragua, Panama, Peru, Trinidad and Tobago, Uruguay, Venezuela

Asia Armenia, Bahrain, Bangladesh, Georgia, Hong Kong, India (2011), Israel,

Jordan, Kazakhstan, Kuwait, Kyrgyzstan, Lebanon, Nepal, Oman, Philippines,

Qatar, Singapore, South Korea (2011), Tajikistan, United Arab Emirates.

Europe Austria, Belarus, Belgium, Bosnia and Herzegovina, Bulgaria, Croatia, Cyprus,

Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece,

Hungary, Iceland, Ireland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg,

Macedonia, Malta, Montenegro, Netherlands, Norway, Poland, Portugal,

Romania, Russia, Russia, Serbia, Slovakia, Slovenia, Spain, Sweden, Turkey,

Ukraine, United Kingdom.

Oceania Australia, Fiji, New Zealand, Papua New Guinea

Source: Wiley IFRS: practical implementation guide and workbook. John Wiley & Sons Inc. (Mirza et al., 2008).

2.5. ConclusionThe harmonization of accounting standards was started by the establishment of IASC that strives

for an improvement in financial reporting internationally. The increase in IASC’s sponsorship drew

attention of various parties on the effort of IASC to develop a single set of accounting standards to be

adopted by most countries worldwide. The major accounting scandals in the United States expose the

shortcomings of the U.S. rule-based accounting standards and therefore accelerate the acceptance of

IFRS internationally. The amount of countries which has adopted IFRS indicates the promising future of

IFRS as a single set of globally accepted accounting standards. The next section presents an overview

from international accounting research before the introduction of IFRS. The next section describes the

importance of culture in explaining differences in accounting practices / systems across countries and

how the Hofstede-Gray framework captures adequately the relationships between culture and

accounting.

12

3. Relationships of culture and accounting

3.1. IntroductionThe impact of culture on financial accounting has become an increasing interest to accounting

researchers. The relevance of culture on accounting practices has been a long debate particularly in the

field of international accounting (Burchell et al., 1980 and Meyer, 1986). Previous research has shown

the existence of different patterns in accounting systems internationally. One of the reasons is the

environmental factors which tend to have great impact on the development of national systems. Many

researchers have tried to identify and establish the environmental factors involved (Radebaugh, 1975;

Nair and Frank, 1980; Nobes, 1983; Doupnik and Salter, 1993). This section gives an overview of

international accounting research associated with culture prior to the Hofstede-Gray framework,

conceptualization of culture based on Hofstede (1980), a brief description of the Hofstede-Gray

framework and some attempts to refine the Hofstede-Gray framework on theoretical basis from

subsequent researchers. Other researcher such as Bik (2010) uses House et al.’ cultural dimensions1

(2004) in his cross-cultural study of assurance professionals behaviors. House et al.’ cultural dimensions

are the outcomes of 10-year research project called GLOBE (Global Leadership and Organizational

Behavior Effectiveness) by measuring cultural practice and cultural values from 62 societies.

Nevertheless, this cultural framework will not be used in this paper since it is not used as a framework in

accounting.

3.2. Prior the Hofstede-Gray frameworkCulture is one factor which helps to explain the differences in accounting systems across

countries. Violet (1983) is the earliest author who explicitly recognized culture as a cause of differences

in international accounting. He examined accounting system as a social function (a product of its culture)

and therefore the success of international accounting standards (IAS) is limited by cultural variables

because cultural relativism exists even in the most basic of societies. Cultural relativism implies that one

group should not judge other group’s activities based on its criteria because the fundamental attributes

are different from one society to another (Hofstede and Hofstede, 2005). Nevertheless, Violet (1983) did

not attempt to classify different patterns of culture-specific factors which allow a better understanding of

the influence of environmental factors on accounting development.

1 House et al.’ (2004) social dimensions are power distance, uncertainty avoidance, assertiveness, institutional collectivism, in-group collectivism, future orientation, performance orientation, human orientation, and gender egalitarianism.

13

Historically, comparative accounting research has two major directions in its effort on

international classification of accounting systems; they are deductive approach and inductive approach

(Gray, 1988). The deductive approach identifies relevant environmental factors and linking those to

national accounting practices. Based on judgments of different environmental factors, the international

classifications or development patterns are proposed (e.g. Mueller, 1967, 1968; Nobes 1983, 1984). The

environmental analysis by Mueller (1967) considered four categories of accounting development in

western nations with market oriented economic systems: a microeconomics pattern where accounting is

closely interrelated to national policies, a macroeconomic pattern where accounting is viewed as a

separate branch of business economics, the independent discipline approach where accounting is

viewed as a service function of business practice and the uniform accounting approach where accounting

is viewed as part of administration and control.

Mueller’s method was extended by Nobes (1983) who based his classification on an evolutionary

approach. He distinguished between business economics practice orientations under a microeconomic

based classification and government / tax / legal orientations under a macroeconomic based

classification. The major features which are used in the identification of accounting practices are the

importance of tax rules, the use of conservative valuation procedures, the strictness of historical costs

application, the making of replacement cost adjustments, the use of consolidation techniques, the

generous use of provisions, and the uniformity between companies in the application of rules. Based on

judgmental analysis of accounting systems in fourteen countries, his results however did not go beyond

providing support for either microeconomics or macroeconomics based classification.

The inductive approach starts by examining development patterns and analyzing accounting

practices and thereafter proposed explanations by referring to a variety of economic, social, political and

cultural factors (e.g. Frank, 1979; Nair and Frank, 1980). In their analysis, Nair and Frank (1980) discerned

accounting practices between measurement and disclosure practices as they assumed these practices to

have different patterns of development. Using data from Price Waterhouse, they conducted a statistical

analysis of accounting practices in forty-four countries. They identified five groups of countries in terms

of measurement practices and seven groups in terms of disclosure practices. The language variable was

used as a proxy for culture, as it was perceived to capture similarities in legal systems particularly in the

disclosure patterns. Based on a number of explanatory variables including language, they found clear

evidence that there were differences between the measurement and disclosure groupings. Nevertheless

14

their hypotheses that (a) cultural and economic variables might be more closely related to disclosure

practices and (b) trading variables might be more closely related to measurement practices were not

supported.

The researches using both approaches are interesting and may provide useful explanations for

international classifications using empirical research. They established relationships, although very

general, between environmental factors and accounting patterns. Each approach notwithstanding has its

own shortcoming. The deductive approach has been criticized of its broad set of influences without

providing precise specification2. The shortcoming of inductive approach is found in its data. The Price

Waterhouse data was criticized for its suitability of purpose, misleading cases and errors (Nobes, 1992).

Nevertheless, most importantly these approaches did not provide explicit recognition on culture as an

explanatory variable but rather apparently incorporated culture in the set of identified environmental

factors.

The importance of culture was recognized in a methodological framework proposed by Harrison

and McKinnon (1986). The framework was used to evaluate the impact of culture on the form and

functioning of accounting in corporate financial reporting regulation at the nation specific level. In his

framework, culture is an essential factor in explaining how societal systems change since ‘culture

influences (1) the norms and values of such systems; and (2) the behavior of groups in their interactions

within and across systems’ (Harrison and McKinnon, 1986).

3.3. Hofstede’s cultural dimensionsCulture is a complicated topic to address because it has no exact definition, it is continuously

affecting and affected by many contextual factors and it is hard to objectify and assess (Papamarcos et

al., 2006). A research conducted by Hofstede (1980) is one of a path-breaking research in conceptualized

differences between national cultures and suggesting ways in which cultural factors may have

consequences on people and organizations. Hofstede (1980) defines culture as ‘the collective

programming of the mind which distinguishes the members of one human group from another’ . He uses

the word “culture” to describe the entire societies and “sub-culture” for groups within societies. His

work appeals to many researchers in social science fields such as behavioral and organizational research.

2 Nobes (1992) specified six important factors which may cause international differences between financial reporting systems: legal systems, business ownership, stock exchanges, tax systems, profession and other factors.

15

The data were collected between 1967 and 1973 and again between 1971 and 1973 from about

117.000 attitude surveys which completed by 88,000 employees at a large multinational corporation IBM

from 72 countries (reduced to 40 countries that had more than 50 responses each) in 20 languages

(Hofstede, 1980). The questionnaire which is used in the IBM study called value survey model (VSM) 3 has

been revised several times for research purpose. The questions included in the VSM are related to these

following aspects: social inequality comprising the relationship with authority, the relationship between

the individual and the group, concepts of gender equality, and ways of dealing with uncertainty and

ambiguity which related to the control of emotions and aggression (Hofstede and Hofstede, 2005).

Country-level factor analysis led to the identification of four societal values dimensions along which

countries could be positioned. The four societal values (culture) dimensions are as follows:

Large versus Small Power Distance

Power Distance is the extent to which the members in a society accept that power in organizations is

distributed unequally. People in Large Power Distance societies accept a hierarchical order in which

everybody has a place which needs no further justification. People in Small Power Distance societies

strive for power equalization and demand justification for power inequalities.

Individualism versus Collectivism

Individualism stands for a preference for a loosely knit social framework in society wherein individuals

should take care of themselves and their immediate families only. Collectivism as its opposite stands for

a preference for a tightly knit social framework in which individuals can expect their relatives or other in-

group to look after them.

Strong versus Weak Uncertainty Avoidance

Uncertainty Avoidance is the extent to which the members of a society feel towards uncertainty and

ambiguity. A Strong Uncertainty Avoidance society preserves rigid codes of belief and behavior and is

inflexible towards deviant ideas. Weak Uncertainty Avoidance societies maintain a more relaxed

atmosphere where practice counts more than principles and deviance is more easily tolerated.

Masculinity versus Femininity

Masculinity refers to a preference in society for achievement, heroism, assertiveness, and material

success. Femininity, as opposite, refers to a preference for relationships, modesty, caring for the weak,

and the quality of life.

3 Hofstede’s VSM is available at www.geert-hofstede.com and may be freely used for research purposes.16

3.4. The Hofstede-Gray’s Framework

Gray (1988) advanced the idea that culture might have influences on accounting practices by

exploring the extent of cultural differences identified by Hofstede (1980) may explain differences in

accounting systems. He used the societal values dimensions of Hofstede (1980) as cultural factors which

might influence accounting practices through the accounting values. He proposed specific hypothesis to

examine the form of these relationships. His proposition was the first literature which attempted to link

societal values with accounting practices in the international accounting literature (Chanchani and

MacGregor, 1999). Although he did not examine his framework on empirical basis, subsequent

researchers evaluated his framework both from a theoretical basis and empirical evidences.

Gray’s model (1988) which extends the framework of Hofstede provides an apparent link

between societal values and accounting practices. He developed a framework which links accounting

values and practices to Hofstede’s (1980) cultural dimensions. Accounting values refers to accounting

subculture of a society which directly influenced by societal values possessed by that society. On a

judgmental basis, he identified four accounting value dimensions that are reflected in a country’s

accounting system. These four accounting values and his hypotheses of the relationships between

Hofstede’s (1980) culture dimensions and accounting values are as follows (Gray, 1988):

Professionalism versus Statutory Control:

“A preference for the exercise of individual professional judgment and the maintenance of

professional self-regulation as opposed to compliance with prescriptive legal requirements and

statutory control”. He hypothesized that “The higher a country ranks in terms of individualism and the

lower it ranks in terms of uncertainty avoidance and power distance then the more likely it is to rank

highly in terms of professionalism”.

Uniformity versus Flexibility:

“A preference for the enforcement of uniform accounting practices between companies and for the

consistent use of such practices over time as opposed to flexibility in accordance with the perceived

circumstances of individual companies”. He hypothesized that “The higher a country ranks in terms of

uncertainty avoidance and power distance and the lower it ranks in terms of individualism then the

more likely it is to rank highly in terms of uniformity”.

17

Conservatism versus Optimism

“A preference for a cautious approach to measurement so as to cope with the uncertainty of future

events as opposed to a more optimistic, laissez-faire, risk-taking approach”. He hypothesized that

“The higher a country ranks in terms of uncertainty avoidance and the lower it ranks in terms of

individualism and masculinity then the more likely it is to rank highly in terms of conservatism”.

Secrecy versus Transparency

“A preference for confidentiality and the restriction of disclosure of information about the business

only to those who are closely involved with its management and financing as opposed to a more

transparent, open, and publicly accountable approach”. He hypothesized that “The higher a country

ranks in terms of uncertainty avoidance and power distance and the lower it ranks in terms of

individualism and masculinity then the more likely it is to rank highly in terms of secrecy”.

The hypotheses of societal values and accounting values can be summarized as follows:

Table 2: relationships of accounting values with societal values

Societal values Accounting values

Professionalism Uniformity Conservatism Secrecy

Individualism Positive Negative Negative Negative

Large power distance Negative Positive n/a Positive

Strong uncertainty avoidance Negative Positive Positive Positive

Masculinity n/a n/a Positive Negative

After formulated hypotheses relating societal values to accounting values, Gray (1988) stated

that the most important societal values at the level of the accounting subcultures / values are

uncertainty avoidance and individualism. While power distance is significant to some extent and

masculinity appears to be lesser importance in the system of accounting values. Figure 2 represents the

relations of societal values, accounting values and accounting practices.

Furthermore, Gray (1988) proposed cultural area classifications of accounting systems using

combinations of accounting values. He distinguished between authority and enforcement of accounting

systems, that is, the extent to which the systems are enforced by statutory control or professional

judgments on the one hand, and the measurement and disclosure characteristics of accounting systems

on the other. He argued that accounting values professionalism and uniformity are mostly relevant to

the authority and enforcement of accounting system, while accounting values conservatism and secrecy

18

ReinforcementReinforcement

Societal values:

Individualism / collectivismPower distanceUncertainty avoidanceMasculinity / femininty

Authority and enforcementProfessionalism / statutory controlUniormity / flexibility

Secrecy / transparency

Conservatism / optimism Measurement of assets and profits

Information disclsosure

are relevant to the measurement practices used and the extent of information disclosed. On judgmental

basis, Gray (1988) developed the classification of culture areas hypothesized (see figure 1 and 2 in the

appendix). In formulating these cultural areas, he refers to the relevant correlations between value

dimensions and the resultant cluster of countries identified from the statistical analysis carried out by

Hofstede (1980).

Figure 2: Gray’s framework: Culture and accounting systems

3.5. Evaluation of the Hofstede-Gray framework on theoretical basisThere have been some literatures that attempt to extend or refine the Hofstede-Gray framework

on a theoretical basis. Perera (1989) and Perera and Matthews (1990) suggest that accounting values

have a considerable influence on accounting practices. He provided an analysis relating accounting

values to certain aspects of accounting practices particularly in the context of developing countries’

accounting systems.

Fechner and Kilgore (1994) proposed a modified framework to explain cultural influence on

accounting. They suggested that culture dimensions (i.e. societal values) and economic factors have

moderating influence on the relationships between accounting values and accounting practices. In their

modified framework, societal values have no direct influence on accounting values which is different

from the Hofstede-Gray framework. Similarly to Gray, these subsequent studies provided no indication

of how the numerous variables in the framework may be operationalized, the extent to which they may

interact, and how statistical test might be conducted to examine the interactions between the variables

(Chanchani and MacGregor, 1999).

19

Using Germany as a case study, Heidhues and Patel (2011) criticized the Hofstede-Gray

framework as misleading and fail to enhance the understanding of differences in accounting

practices/systems. Using Hofstede’s value scores for Germany, they evaluated the graphical mapping of

Germany in cultural areas of Gray and concluded it as being imprecise and too simplistic. They apply a

‘more holistic approach’ in examining the factors that distinguished German accounting system from

other accounting models. This approach provides additional insights such as specific characteristics in

Germany accounting systems i.e. strictly confidential which has major complications with the adoption of

IFRS. They recommend that further cultural research should lie on ‘a critical examination of contextual

environments of countries rather than a focus on measurement, quantification, simplification and

categorization’ (Heidhues and Patel, 2011, p. 282).

3.6. Conclusion

Prior to the Hofstede-Gray framework, inductive and deductive approaches have been used to

explain differences in international accounting practices/systems. Both approaches are useful in

identifying some explanatory factors; nevertheless these approaches cannot be used to explain the

mechanism in the relationship between culture and differences in accounting practice/systems. The

Hofstede-Gray framework fills this gap by proposing specific hypothesis, ready to be tested, between

societal values and accounting values. Gray (1988) also developed cultural areas which help subsequent

researchers in choosing country samples and to test his hypotheses empirically. Following researchers

attempt to refine the Hofstede-Gray framework and criticized the framework as being imprecise and too

simplistic. The Hofstede-Gray framework is nevertheless a useful tool in understanding the influence of

culture on accounting practices/systems. The next section provides overview of empirical studies that

use the Hofstede-Gray framework.

20

4. Findings

4.1. IntroductionThere are only limited amounts of empirical research which specifically study cultural

implications using the Hofstede-Gray framework. This section provides empirical studies that use the

Hofstede-Gray framework. The first sub-section briefly discusses the empirical research that did not use

IAS or IFRS in their research instrument. The second sub-section provides an overview of the empirical

research that incorporated IAS or IFRS in their research instrument. The researchers try to simulate the

implementation of IFRS on individual professional accountants as the unit of analysis by incorporating

the financial reporting rules based on IAS or IFRS in their research instrument.

Until now, there is no empirical study available that examines the influence of culture after the

implementation of IFRS due to the recentness of IFRS adoption. Therefore analysis is only possible by

comparing empirical research between using and not using IAS or IFRS within their research instrument.

Table 1 and 2 in the appendix provides summary of empirical studies used in this section. For

convenience sake, the sub-section will be divided based on three areas i.e. authority and enforcement,

measurement and disclosure. Comparison based on these three areas will be made in the analysis in

order to examine the implication of including IAS or IFRS in the research instrument on these three

areas. Authority and enforcement of accounting practices are related to accounting values

professionalism / statutory control and uniformity / flexibility. Measurements in accounting practices are

related to accounting value of conservatism. Disclosure practices in accounting are related to accounting

value of secrecy.

4.2. No IAS / IFRS in research design

4.2.1. Authority and enforcement

Robert and Salter (1999) examine the drivers behind accountants’ attitudes towards uniformity

in accounting rules. They hypothesized as follows: (1) ‘The strength of desire for a single mandatory

treatment for an accounting issue in a country is related to the culture of a country and (2) The strength

of desire for a single mandatory treatment for an accounting issue in a country is positively related to the

importance of the stock market in that country’ (Robert and Salter, 1999, p. 6) . They administered a

questionnaire comprised of 14 accounting issues to the sample of auditors employed in the Big 6

21

accounting firms4 in 23 countries5. The countries were selected based on the size of stock markets at the

end of 1993. Each respondent was asked to respond with a yes/no on the statement whether they

wanted a single mandatory treatment respectively for 14 different accounting issues 6. The dependent

variable is the response of whether or not a single mandatory method is preferred. The independent

variables consist of the importance of capital market (MKTCAP) and two societal culture dimensions

(CULT 1 and CULT 2). CULT 1 has positive loadings on power distance and negative loadings on

individualism while CULT 2 has positive loadings for both uncertainty avoidance and masculinity.

The results show that the respondents tend to favor a mandatory single treatment in 66% of the

cases analyzed. Related to the first hypothesis, CULT 1 appears to be positively related to preferences for

a single treatment but CULT 2 is negatively related which is in contrast to the expectation. The result of

CULT 1 is consistent with Gray’s (1988) hypothesis that uniformity has a positive relation to power

distance and a negative relation to individualism. In terms of CULT 2, the result is contrary to Gray’s

uniformity hypothesis. Robert and Salter (1999) suggest that the involvement of masculinity component

in CULT2 may distort the relation between uncertainty avoidance and uniformity. Gray (1988) did not

propose any relation between masculinity and uniformity. Moreover, the results provide strong support

related to the second hypothesis means that auditors prefer a single treatment as the role of stock

markets as a source of finance increases. They concluded that the preference of a single mandatory

treatment in accounting is influenced by certain aspects of culture and the importance of stock markets.

4.2.2. Measurement practicesSchultz and Lopez (2001) examine the consistency in the judgments made by accountants in the

United States, France and Germany given same economic facts and similar financial reporting standards.

They hypothesized that (1) ‘American accountants will resolve warranty estimates lower dollar

magnitudes than individual French and German accountants, (2) The warranty estimates of participants

that were given a low to high order of monetary amounts will be greater for French than German

4 The Big 6 accounting firms are Arthur Andersen, Ernst & Young, Coopers and Lybrand, Deloitte & Touche, Peat Marwick Mitchell (now is KPMG) and Price Waterhouse.

5 The countries included in the sample are Australia, Austria, Belgium, Brazil, Canada, Denmark, France, Germany, Hong Kong, Italy, Japan, Korea, Malaysia, Mexico, Netherlands, Singapore, Spain, Sweden, Switzerland, Taiwan, Thailand, U.K., and the U.S.

6 The specific issues concern of ‘the initial valuation of property, plant or equipment acquired in exchange for a similar asset; valuation of investment properties; the correction of fundamental errors, omissions or accounting policy changes; revenue recognition on construction contracts; the benefit valuation method used when valuing retirement benefits; gains or losses on long-term monetary items due to exchange rate changes; the exchange rate used to translate income statements; accounts of subsidiaries located in countries with hyper-inflation; development costs; inventory flow assumptions; borrowing costs on assets under construction; merger accounting method; positive goodwill; and, negative goodwill’ (Robert and Salter, 1999, p. 9).

22

accountants and greater for German than American accountants’ (Schultz and Lopez, 2001, p. 8-9).

Based on the score of uncertainty avoidance of each country, they speculate that French accountants

will behave more conservatively (i.e. more cautious in their warranty expense estimation and therefore

provide higher number) than German accountants and German accountants will be more conservative

than American accountants respectively.

The samples are professional accountants of a large international accounting firm from each of

the three countries. The respondents were presented with two cases of manufacturing companies and

were asked to calculate the amount of warranty expense they would recognize. Each set of cases

included three levels of probability (i.e. low, medium and high) and two monetary amounts (i.e. large

and small) and each respondent should exercise judgment for each combination of probability level and

monetary amount. In total, each respondent made six judgments for every case.

The results provide support for both hypotheses that French and German accountants recognize

higher amount of warranty estimates (i.e. more cautious or conservative) than the accountants in the

United States. The outcomes suggest that accountants in high uncertainty avoidance countries are more

sensitive to framing effects (i.e. the level of probability and monetary amount) than those in low

uncertainty avoidance. They concluded that the cultural dimension of uncertainty avoidance influences

the process of judgment-making of professional accountants even if same economic facts and uniform

accounting standards are given.

4.2.3. Disclosure practicesGray and Vint (1995), Zarzeski (1996), Wingate (1997), Jaggi and Low (2000) and Hope (2003) are

empirical studies that examine only the secrecy hypothesis of Gray (1988). All these studies use countries

as unit of analysis. Gray and Vint (1995) regress mean disclosure scores of 27 countries as the dependent

variable and Hofstede’s (1980) societal values indices as independent variables. The mean disclosure

scores are obtained from a database of a project conducted by Gray et al. (1984). The results show that

masculinity and individualism have a positive relation to the amount of information disclosed and power

distance and uncertainty avoidance have negative relation to the amount of information disclosed.

Zarzeski (1996) examines the influence of both culture and market forces which are measured by

foreign sales, debt ratio and size of a company on disclosure practice. The results provide direction

consistent with Gray’s hypothesis for uncertainty avoidance, masculinity and individualism. The results

indicated that the relation between uncertainty avoidance and disclosure depends upon the

internationality of the firm. Uncertainty avoidance has more influence on disclosure when the firm is less

23

international dependent. He concludes that ‘local firms disclose more like their culture than do

international firms’ (Zarzeski, 1996, p. 35)

Wingate (1997) investigates whether culture has influence on the required amount of disclosure

in 39 sample countries. Using CIFAR’s7 1991disclosure index as the dependent variable and Hofstede’s

cultural indices, she found that uncertainty avoidance and individualism are significantly related to the

disclosure index.

Jaggi and Low (2000) construct an international financial disclosure model which involved

culture, legal systems and accounting disclosures and test it by using CIFAR’s 1993 disclosure index as

dependent variable. Independent variables comprise Hofstede’s indices, legal system and market force

variables (i.e. firm size, debt ratio and market share). Their sample consists of three common law

countries and three code law countries. Four societal values have a significant relation to disclosure in

code law countries but only individualism is in the expected direction. For common law countries, none

of the societal values has significant influence on disclosure. In conformity to their expectation, cultural

values have more influence than market forces on disclosure in code law countries, while in common law

countries market forces dominate culture in influencing disclosure. Jaggi and Low (2000) criticize Gray’s

secrecy hypothesis as invalid and Hofstede’s indices as outdated.

Hope (2000) continued the Jaggi and Low (2000) study using CIFAR’s disclosure indices from

1993 until 1995 as the dependent variable. Using a larger sample from 39 countries, he found a

significant relation of societal values individualism and masculinity to disclosure, but the direction

masculinity is opposite to expectation. When he separated his analysis into common law and code law

countries, he got mixed results contrary to Jaggi and Low (2000). Nonetheless, he concludes that culture

still has explanatory power on disclosure levels.

4.2.4. Other FindingsEddie (1990) tests all four hypotheses of the Hofstede-Gray framework for thirteen countries of

the Asia-Pacific region. He used Hofstede’s index score (1980) for societal values dimension and

constructed a subjective index for Gray’s values based on information available in 1991. His empirical

study confirmed all predicted signs of association between societal values and accounting values.

Nevertheless, the results should be viewed with caution because his method of measurement was not

rigorous, the index were subjectively determined, and he used two different sets of data based on

information from twenty years apart (Chanchani and Macgregor, 1998; Finch, 2007).

7 CIFAR stands for Center for International Financial Analysis and Research.24

Salter and Niswander (1995) operationalized Gray’s hypotheses using collected data from 29

countries. A variety of cultures in terms of language, geographical location, colonial antecedents, and

economic development were included in their samples. They found significant support only for six out of

thirteen of Gray’s predicted relationships between societal values dimensions and accounting values.

The correlation between the uncertainty avoidance dimension and uniformity is the only significant

relationship that is in contrast to Gray’s proposition.

4.3. IAS / IFRS in research design

4.3.1. Authority and enforcement

No empirical study has used the Hofstede-Gray framework to examine cultural influence on the

implementation of IFRS in terms of authority and enforcement by incorporating IAS or IFRS in its

research instrument. In terms of IFRS enforcement, not every company that claims compliance to IAS

standards (predecessor of IFRS) in financial reporting is actually in full compliance with IAS (Street and

Bryant, 2000; Asbaugh and Pincus, 2001; Chatham, 2008). The IASB had made some effort to reduce this

possibility in IAS 1 by compelling companies to disclose any material departure from IAS and not to claim

that they are in compliance with IAS unless it is full compliance. Some researchers argued that the level

of enforcement of accounting standards is as necessary as the standards themselves (e.g. Hope, 2003).

Some empirical studies suggest that weak enforcement in the IFRS implementation have caused

lower degree of compatibility and comparability and thus lower quality of financial reports (Byard et al.,

2009; Armstrong et al., 2010). Byard et al. (2009) examine the impact of the mandatory adoption of IFRS

in the European Union on analysts’ information environment8. Their results demonstrate that mandatory

adoption of IFRS enhances analysts’ information environment only when the implementation is

substantial and rigorously enforced. Armstrong et al. (2010) investigate the European equity market

reaction to sixteen events associated with the adoption of IFRS in Europe. Their findings demonstrate a

substantial negative reaction for firms located in code law countries which are consistent with investors’

concern over weaker IFRS enforcement in those countries.

Nevertheless, given that these empirical literatures are useful in revealing and identifying the

importance of rigorous enforcement of IFRS standards, it is still not clear whether accounting values are

the drivers behind these international differences. This area still needs further investigation.

8 Analysts’ information environment was measured by forecast errors, forecast dispersion and analyst following (Byard et al., 2009).

25

4.3.2. Measurement practices

An Empirical study from Doupnik and Richter (2004) investigated the effect of national culture on

the interpretation of “in context” verbal probability expressions. The hypotheses were tested by using a

survey of accountants in Germany and the United States. They made three hypotheses as follows: (1)

German accountants will assign a higher numerical probability than U.S. accountants to positively framed

verbal probability expressions associated with assets recognition and increases in net income, (2)

German accountants will assign a lower numerical probability than U.S. accountants to positively framed

verbal probability expressions associated with liabilities recognition and decreases in net income, (3)

German accountants will assign a higher numerical probability than U.S. accountants to negatively

framed verbal probability expressions associated with assets recognition and increases in net income.

To test the hypotheses, Doupnik and Richter (2004) selected 14 excerpts from IAS containing 16

verbal probability expressions and included the excerpts in a research instrument. Professional

accountants in the U.S. and Germany were asked to assign a numerical probability from 0% to 100% to

each verbal probability expression. Eleven of the expressions are positively framed (e.g. likely, sufficient

certainty) and five of the expressions are negatively framed (e.g. insufficient certainty). The results

provide support for the first and second hypotheses but not for the third hypothesis. The results were

mixed in terms of negatively framed expressions. These outcomes show that culture affects the

interpretation of positively framed verbal probability expressions9. This study provides evidence that

through accounting value of conservatism, culture affects the interpretation of probability expressions in

IAS by U.S. and German accountants. The outcomes are consistent with Gray’s conservatism hypothesis

(1988) which posits Germanic (Germany) as conservative countries and Anglo (United States) as optimist

countries (see figure 2 in the appendix).

An empirical study from Doupnik and Ricio (2006) examine whether differences in culture cause

accountants in different countries to interpret and apply the same accounting standards differently. To

do that, they use the same approach as Doupnik and Richter (2004). Doupnik and Ricio (2006) asked a

sample of accountants in the U.S. and Brazil to interpret verbal probability expressions used in IFRS as

thresholds for both recognition and disclosure decisions. In Gray’s (1988) cultural areas, Brazil is

categorized in the more developed Latin area that scores high on conservatism (see figure 2 in the

appendix). They hypothesized that (1) Brazilian accountants will assign a higher numerical probability to

9 Most probability expressions used in IAS are positively framed (Doupnik and Richter, 2004).26

verbal probability expressions that determine the recognition of items that increase net income than

American accountants and (2) Brazilian accountants will assign a lower numerical probability to verbal

probability expressions that determine the recognition of items that decrease income than American

accountants.

Hofstede’s VSM was included in the research instrument to ensure that the U.S. and Brazilian

accountants’ samples differed on Hofstede’s cultural values and in the direction expected. To test the

hypothesis, Doupnik and Ricio (2006) selected 11 excerpts from IFRS containing five different verbal

probability expressions. From the eleven excerpts being used, 6 excerpts are used to test the first

hypothesis (H1) and 3 excerpts to test the second hypothesis (H2). The other two excerpts were used to

test hypothesis related to another topic i.e. disclosure (secrecy). The respondents were asked to assign a

numerical probability expression from 0% to 100% to each verbal probability expression. Doupnik and

Ricio (2006) did not make any distinction in framing verbal probability expression in such a way as

Doupnik and Richter (2004) did.

The differences in VSM cultural values scores from both samples provide direction which is

consistent with Hofstede’s scores except for masculinity. Their sample of Brazilian accountants has

higher scores on power distance and uncertainty avoidance and a lower score on individualism than the

sample of U.S. accountants. Nevertheless, due to Gray’s judgments in his proposition that masculinity

has only a weak relation with the accounting values of conservatism, they concluded that the cultural

value scores obtained from the respondents are consistent with their assumptions that Brazil is more

conservative than the United States.

The outcomes provide significant evidence with regard to H1 but not for H2. The differences in

the mean probabilities assigned by the two groups are in the predicted direction for four of the six

excerpts being used to test H1 and indicate significant differences between Brazilian and the U.S.

accountants’ response to the recognition of items that increase net income. Adversely, all probability

expressions related to H2 are not statistically significant and in the opposite direction of what was

predicted.

Tsakumis (2007) examines the influence of national culture on accountant’s application of

accounting rules using profession accountants from Greece and the U.S. To test the influence of

accounting value conservatism, he hypothesized that ‘Greek accountants are more likely to recognize

27

contingent liabilities and less likely to recognize contingent assets than U.S. accountants’ (Tsakumis,

2007, p.33). In Gray’s cultural areas (1988) Anglo countries (the U.S.) score high on optimism and Near

Eastern countries (Greece) rank high on conservatism (see figure 2 in the appendix).

The independent variables of this hypothesis consist of national culture (Greek versus U.S.) and

the nature of contingency (assets versus liability) while dependent variables consist of participants’

recognition (conservatism) and disclosure decisions (secrecy). Each participant received questionnaires in

which two litigation cases were presented and guidelines of an accounting standard that they were

asked to apply in making financial judgments. Each litigation scenario comprises of one recognition

scenario to test the conservatism hypothesis and one disclosure scenario to test another hypothesis

related to secrecy. Conservatism was apprehended as a decision to recognize or not recognize a

contingent asset or liability (and respective gain or loss) and measured on a 10-point scale. The

accounting standard in the questionnaire was formulated after IAS 37 provisions, contingent liabilities

and contingent assets, which addresses both measurement and disclosure of accounting information.

Hofstede’s VSM was included in the questionnaire in order to calculate scores for each subject group’s

societal values dimensions. The research instrument attempted to control for factors other than culture

such as current accounting practice, taxation and litigation risk.

Related to the conservatism hypothesis, the results are insignificant for both independent

variables indicating no support for the hypothesis. In contrast to expectation, the direction in mean

differences indicates that Greek accountants are less conservative than U.S. accountants although not in

a statistically significant level. Tsakumis (2007) further analyzed about this phenomenon by including

additional test in his research instrument. The respondents were asked to indicate their agreement with

six statements associated with conservatism. Three significant differences in the mean responses were

found. The results indicate that U.S. accountants agreed mostly with statements related to recognizing

expenses, losses and liabilities earlier and at higher amounts than Greek accountants. This additional test

provides further confirmation of U.S. participants’ conservatism.

4.3.3. Disclosure practices

Doupnik and Ricio (2006) test hypothesis related to the level of secrecy of U.S. and Brazilian

accountants. To test their hypothesis, they use verbal probability expressions in IAS 37 (i.e. remote and

probable) regarding contingent liabilities and contingent assets. The professional accountants both from

the U.S. and Brazil were asked to assign a numerical probability on a scale 0% - 100% to each probability 28

expression. They hypothesized that Brazilian accountants will assign a higher numerical probability to

verbal probability expressions that determine the disclosure of an item than American accountants.

The results are consistent with the hypothesis. The mean difference assigned to the term

“remote” related to contingent liability is highly significant and to the term “probable” related to

contingent asset is significant. These outcomes indicate significant differences between Brazilian and U.S.

accountants across two expressions related to the hypothesis of secrecy. Consistent with Gray’s (1988)

proposition, Brazilian accountants score higher than American accountants in the level of secrecy and

are less likely to provide disclosures.

The second study comes from Tsakumis (2007) which examines whether Greek accountants are

more likely to exhibit secrecy compared to U.S. accountants. Greece ranks high in secrecy (Gray, 1988)

means that Greek accountants are less likely to disclose the existence of both liabilities and assets in

order to keep inside parties’ confidentiality. Tsakumis (2007) hypothesized that ‘Greek accountants are

less likely to disclose the existence of contingent liabilities and contingent assets than U.S. accountants’

(Tsakumis, 2007, p. 33). Using the same participants and scenarios, as what has been mentioned in the

previous sub-section, the results demonstrate that both independent variables i.e. ‘culture’ and ‘nature

of contingency’ have significant effects on participants’ disclosure decisions as the dependent variable.

The outcomes indicate that ‘culture’ main effect is significant, providing strong support for the

hypothesis. The significant mean differences from a within-groups t-test reveal that Greek accountants

are less likely to disclose both contingent assets and contingent liabilities. These results confirmed the

hypothesis with regard to cultural influence on accounting disclosure practices.

4.3.4. Other findings

Ding et al. (2004) examine the role of culture in the way national accounting systems of 52

sample countries10 may differ from IAS. They claim that the difference between national GAAP and IAS

can be classified into: (1) divergence if national GAAP prescribes a different method than IAS and (2)

absence if national GAAP does not cover an accounting issue regulated by IAS. Their study focuses on the

cultural values of each country as the explanatory variables for the differences between each national

GAAP and IAS. With regard to divergence, they hypothesized that a country with a higher level of

individualism and uncertainty avoidance and a lower level of masculinity and power distance is likely to

10 The samples of 52 countries are selected based on the study from “GAAP 2001” (Nobes, 2001) executed by several international accounting firms.

29

have accounting standards that diverge from IAS. In terms of absence, they hypothesized that a country

with a higher level of masculinity and uncertainty avoidance and a higher level of individualism and

power distance is likely to have accounting standards that are less extensive than IAS.

The results show that societal values of individualism, power distance and uncertainty avoidance

are significant in explaining divergence from IAS while the level of absence appears to be less related to

cultural factors. Ding et al. (2004) argued that the level of absence is more likely related to economic

development and capital market issues11. They concluded that discrepancy from IAS is ‘not exclusively

driven by contractual motives or a claimed technical superiority but also by diversity in cultural factors’

(Ding et al., 2004, p. 2).

11 An analysis of the items included in IAS but not in national rules shows that these items are depending more on the level of economic development and the size of capital market rather than national culture (Ding et al, 2004).

30

5. Analysis

5.1. IntroductionIn this section, the previous findings will be discussed and relates them to the three sub-

questions in the first chapter. Herewith, cultural impacts are the focus while IFRS can be seen as an

instrument included in the research design to examine if culture still plays a role in the accounting

practices / systems.

5.2. Analysis of findingsIn terms of authority and enforcement, no judgment can be made whether culture has an

influence on the implementation of IFRS. Previous findings from Robert and Salter (1999) show that