bachelor of commerce programme - kbp college, vashi · 2019-07-31 · bachelor of commerce...

TRANSCRIPT

BACHELOR OF COMMERCE

PROGRAMME

Under Choice Based Credit, Grading and

Semester System

To be implemented from Academic Year 2019-2020

Faculty of Commerce

Board of Studies of Accountancy

Rayat Shikshan Sanstha’s

Karmaveer Bhaurao Patil College, Vashi

Three Years Full Time Under Graduate Programme.

Semester Pattern with Credit System, Structure For Second Year

S

e

m

Course Type

Course

Codes

Course Title WL Cr. CE TE Total

III

Discipline Specific Elective

(DSE)Courses

UCOM301 Accountancy and Financial

Management III 4 3 40 60 100

UCOM302 Introduction to Management

Accounting

Discipline Related

Elective(DRE) Courses

UCOM303 Commerce III 3 3 40 60 100

UCOM304 Business Economics III 3

3

40 60 100

Ability Enhancement

Compulsory Courses (AECC)

UCOM305 Advertising

Computer Application

Entrepreneurship

Development

4

4

4

3

3

3

40

40

40

60

60

60

100

100

100 UCOM305

*Skill Enhancement Courses

(SEC)

UCOM306 *Foundation Course –II

( Gen/NSS/PE) 3

2

40 60 100

Core Courses (CC) UCOM307 Business Law 4 3 40 60 100

20

IV Discipline Specific Elective

Course

UCOM401 Accountancy and Financial

Management IV 4 3 40 60 100

UCOM402 Auditing

Discipline Related

Elective(DRE) Courses

UCOM403 Commerce – IV 3

3

40

60

100

Discipline Related

Elective(DRE) Courses

UCOM404 Business Economics IV

3

3

40 60 100

Ability Enhancement

Compulsory Courses (AECC)

UCOM405 Advertising 4 3

40 60 100

Ability Enhancement

Compulsory Courses (AECC)

UCOM405 Computer Application 4 3

40 60 100

*Skill Enhancement Courses

(SEC)

UCOM406 *Foundation Course –I

( Gen/NSS/PE) 3

2

40 60 100

Core Courses (CC) UCOM407 Business Law 4 3 40 60 100

20

* General/National service Scheme/Physical Education

Rayat Shikshan Sanstha’s

Karmaveer Bhaurao Patil College Vashi, Navi Mumbai

Autonomous College

[University of Mumbai]

Syllabus for Approval

Sr.

No. Heading Particulars

1 Title of Course S.Y.B.Com. Accounting &

Financial Management III & IV

2 Eligibility for

Admission

3 Passing Marks

4 Ordinances/Regulations

(if any)

5 No. of Years/Semesters One year/Two semester

6 Level U.G.

7 Pattern Semester

8 Status New

9 To be implemented

from Academic year 2019-2020

AC- 02/ 03/ 2019

Item No- 2.12

Rayat Shikshan Sanstha’s KARMAVEER BHAURAO PATIL COLLEGE, VASHI.

NAVI MUMBAI (AUTONOMOUS COLLEGE)

Sector-15- A, Vashi, Navi Mumbai - 400 703

Syllabus for S.Y.B.Com.

Accounting & Financial Management III & IV

Program: B.Com.

Course: S.Y.B. Com.

Accounting & Financial Management III & IV

(Choice Based Credit, Grading and Semester System

with effect from the academic year 2019‐2020)

Semester III

Accountancy and Financial Management Paper-III

Modules at a Glance

Sr.

No.

Modules No. of

Lectures

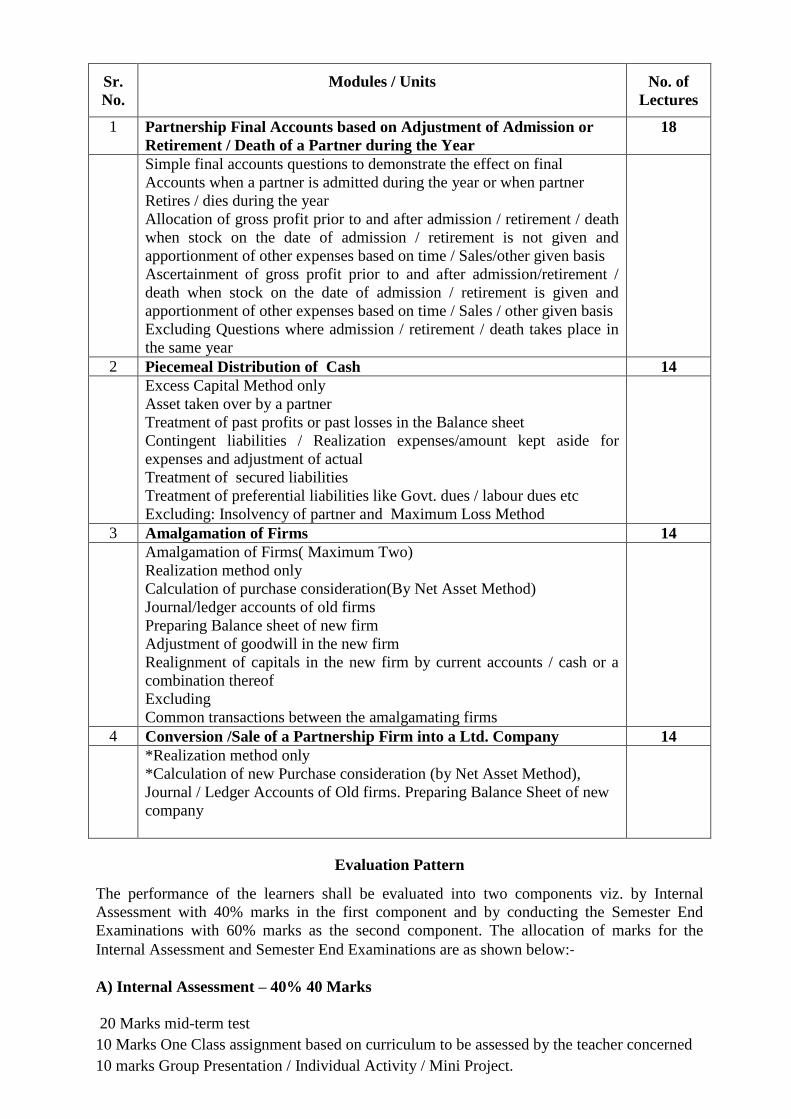

1 Partnership Final Accounts based on Adjustment of Admission or

Retirement / Death of a Partner during the Year

18

2 Piecemeal Distribution of Cash 14

3 Amalgamation of Firms 14

4 Conversion / Sale of a Partnership Firm into a Ltd. Company 14

Total 60

Course Outcomes:

1. Identify net profit of the firm prior/after admission, retirement or death of a partner.

2. Adjust the value of goodwill at the time of admission, retirement or death of a partner.

3. Understands the concepts of admission and retirement of the partners.

4. Understand the order of payment of liabilities at the time of dissolution.

5. Calculate the Excess Capital of a partner under surplus capital method.

6. Prepares the statement of cash distribution.

7. Calculate the Purchase Consideration under Net Asset Method.

8. Adjust the capitals of partners in new firm as per the terms and conditions in new firm.

9. Closes the books of amalgamating firms and opens books of new firm.

Sr.

No.

Modules / Units No. of

Lectures

1 Partnership Final Accounts based on Adjustment of Admission or

Retirement / Death of a Partner during the Year

18

Simple final accounts questions to demonstrate the effect on final

Accounts when a partner is admitted during the year or when partner

Retires / dies during the year

Allocation of gross profit prior to and after admission / retirement / death

when stock on the date of admission / retirement is not given and

apportionment of other expenses based on time / Sales/other given basis

Ascertainment of gross profit prior to and after admission/retirement /

death when stock on the date of admission / retirement is given and

apportionment of other expenses based on time / Sales / other given basis

Excluding Questions where admission / retirement / death takes place in

the same year

2 Piecemeal Distribution of Cash 14

Excess Capital Method only

Asset taken over by a partner

Treatment of past profits or past losses in the Balance sheet

Contingent liabilities / Realization expenses/amount kept aside for

expenses and adjustment of actual

Treatment of secured liabilities

Treatment of preferential liabilities like Govt. dues / labour dues etc

Excluding: Insolvency of partner and Maximum Loss Method

3 Amalgamation of Firms 14

Amalgamation of Firms( Maximum Two)

Realization method only

Calculation of purchase consideration(By Net Asset Method)

Journal/ledger accounts of old firms

Preparing Balance sheet of new firm

Adjustment of goodwill in the new firm

Realignment of capitals in the new firm by current accounts / cash or a

combination thereof

Excluding

Common transactions between the amalgamating firms

4 Conversion /Sale of a Partnership Firm into a Ltd. Company 14

*Realization method only

*Calculation of new Purchase consideration (by Net Asset Method),

Journal / Ledger Accounts of Old firms. Preparing Balance Sheet of new

company

Evaluation Pattern

The performance of the learners shall be evaluated into two components viz. by Internal

Assessment with 40% marks in the first component and by conducting the Semester End

Examinations with 60% marks as the second component. The allocation of marks for the

Internal Assessment and Semester End Examinations are as shown below:‐

A) Internal Assessment – 40% 40 Marks

20 Marks mid-term test

10 Marks One Class assignment based on curriculum to be assessed by the teacher concerned

10 marks Group Presentation / Individual Activity / Mini Project.

Test Paper Pattern

Maximum Marks: 20

Questions to be set 3

Q.No. 1 Choose the correct alternatives. (Any Five) (5 Marks.)

Q. No. 2 Answer in one sentence. (Any Five) (5 Marks.)

Q.No. 3. Answer the following. (Any Two) (10 Marks.)

B) Semester End Examinations – 60% 60 Marks

Question Paper Pattern

Maximum Marks: 60

Questions to be Set: 04

Duration: 2 Hrs.

All Questions are Compulsory Carrying 15 Marks each.

Q-1

Q-1

Full Length Practical Question

OR

Full Length Practical Question

15 Marks

15 Marks

Q-2

Q-2

Full Length Practical Question

OR

Fill Length Practical Question

15 Marks

15 Marks

Q-3

Q-3

Full Length Practical Question

OR

Full Length Practical Question

15 Marks

15 Marks

Q-4

Q-4

Objective Questions*

(*Multiple choice / True or False / Match the columns / fill in the blanks)

OR

Theory questions*

(*Short notes / short questions)

15 Marks

15 Marks

Note: Full length question of 15 marks may be divided into two sub questions of 08 and 07

marks

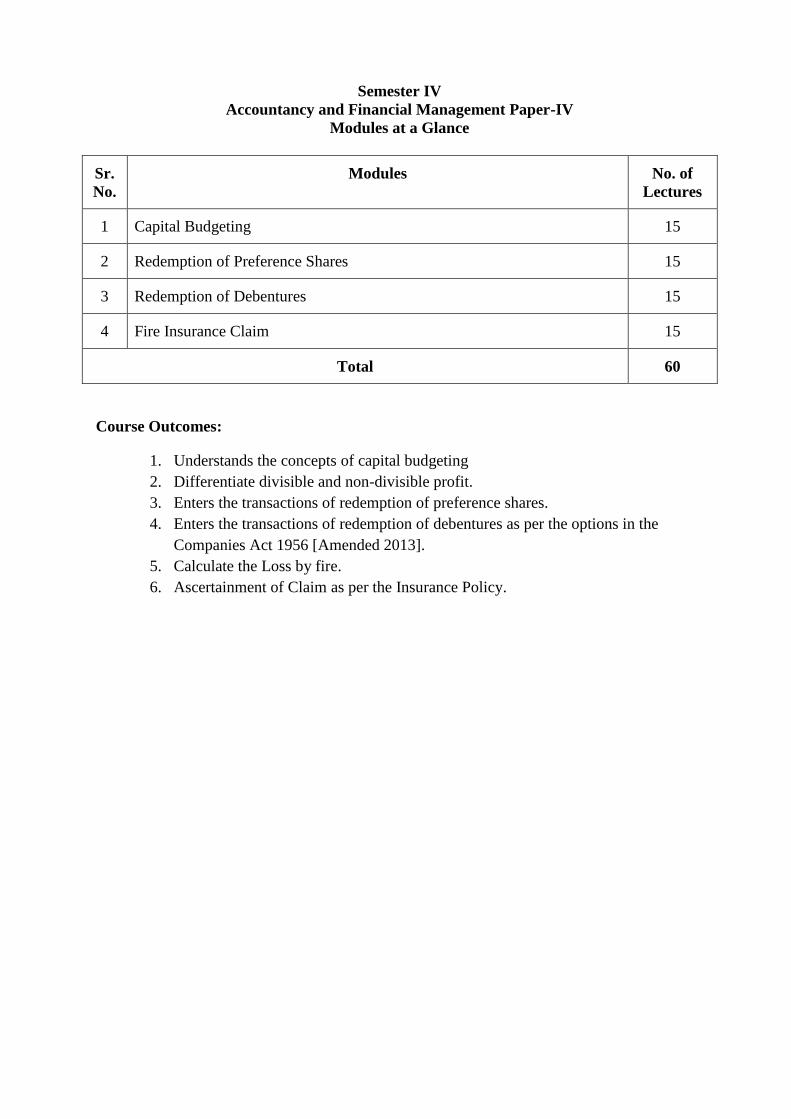

Semester IV

Accountancy and Financial Management Paper-IV

Modules at a Glance

Sr.

No.

Modules No. of

Lectures

1 Capital Budgeting 15

2 Redemption of Preference Shares 15

3 Redemption of Debentures 15

4 Fire Insurance Claim 15

Total 60

Course Outcomes:

1. Understands the concepts of capital budgeting

2. Differentiate divisible and non-divisible profit.

3. Enters the transactions of redemption of preference shares.

4. Enters the transactions of redemption of debentures as per the options in the

Companies Act 1956 [Amended 2013].

5. Calculate the Loss by fire.

6. Ascertainment of Claim as per the Insurance Policy.

Sr.

No.

Modules / Units No. of

Lectures

1 Capital Budgeting 15

A. Introduction:

B. The classification of capital budgeting projects

C. Capital budgeting process

D. Capital budgeting techniques - Payback Period, Accounting Rate

of Return, Net Present Value, The Profitability Index, Discounted

Payback. (Excluding calculation of cash flow)

2 Redemption of Preference Shares 15

Issue of Shares: Different modes IPO, private Placement , Preferential

, Rights, ESO, SWEAT and ESCROW account, issue of shares at par,

premium and discount, Book Building Process

Company Law / Legal Provisions for redemption of preference

shares in Companies Act

Sources of redemption including divisible profits and proceeds of

fresh issue of shares

Premium on redemption from security premium and profits of

company

Capital Redemption Reserve Account - creation and use

3 Redemption of Debentures 15

Issue of Debentures: Issue of debentures at par, premium and discount

Redemption of debentures by payment from sources including out of

capital and / or out of profits.

Debenture redemption reserve and debenture redemption sinking fund

excluding insurance policy.

Redemption of debentures by conversion into new class of shares or

debentures with options- including at par, premium and discount.

4. Fire Insurance Claim 15

Computation of Loss of Stock by Fire

Ascertainment of Claim as per the Insurance Policy

Exclude: Loss of Profit and consequential Loss

Evaluation Pattern

The performance of the learners shall be evaluated into two components viz. by Internal

Assessment with 40% marks in the first component and by conducting the Semester End

Examinations with 60% marks as the second component. The allocation of marks for the

Internal Assessment and Semester End Examinations are as shown below:‐

A) Internal Assessment – 40% 40 Marks

20 Marks mid-term test

10 Marks One Class assignment based on curriculum to be assessed by the teacher concerned

10 marks Group Presentation / Individual Activity / Mini Project.

Test Paper Pattern

Maximum Marks :20

Questions to be set 3

Q.No. 1 Choose the correct alternatives. (Any Five) (5 Marks.)

Q. No. 2 Answer in one sentence. (Any Five) (5 Marks.)

Q.No. 3. Answer the following. (Any Two) (10 Marks.)

B) Semester End Examinations – 60% 60 Marks

Question Paper Pattern

Maximum Marks: 60

Questions to be Set: 04

Duration: 2 Hrs.

All Questions are Compulsory Carrying 15 Marks each.

Q-1

Q-1

Full Length Practical Question

OR

Full Length Practical Question

15 Marks

15 Marks

Q-2

Q-2

Full Length Practical Question

OR

Fill Length Practical Question

15 Marks

15 Marks

Q-3

Q-3

Full Length Practical Question

OR

Full Length Practical Question

15 Marks

15 Marks

Q-4

Q-4

Objective Questions*

(*Multiple choice / True or False / Match the columns / fill in the blanks)

OR

Theory questions*

(*Short notes / short questions)

15 Marks

15 Marks

Note: Full length question of 15 marks may be divided into two sub questions of 08 and 07

marks

Rayat Shikshan Sanstha’s

Karmaveer Bhaurao Patil College Vashi, Navi Mumbai

Autonomous College

[University of Mumbai]

Syllabus for Approval

Sr.

No. Heading Particulars

1 Title of Course S.Y.B.Com. Introduction to

Management Accounting and

Introduction to Auditing

2 Eligibility for

Admission

3 Passing Marks

4 Ordinances/Regulations

(if any)

5 No. of Years/Semesters One year/Two semester

6 Level U.G.

7 Pattern Semester

8 Status New

9 To be implemented

from Academic year 2019-2020

AC- 02/ 03/ 2019

Item No- 2.12

RayatShikshanSanstha’s KARMAVEER BHAURAO PATIL COLLEGE, VASHI.

NAVI MUMBAI (AUTONOMOUS COLLEGE)

Sector-15- A, Vashi, Navi Mumbai - 400 703

Syllabus for S.Y.B.Com.

Introduction to Management Accounting

and Introduction to Auditing

Program: B.Com.

Course: S.Y.B. Com.

Introduction to Management Accounting and

Introduction to Auditing

(Choice Based Credit, Grading and Semester System

with effect from the academic year 2019‐2020)

SEM III

Introduction to Management Accounting

Modules at a Glance

No. Modules No. of Lectures

1 Introduction to Management Accounting 10 2 Analysis and Interpretation of Financial

Statements 13

3 Ratio Analysis and Interpretation 12 4 Working Capital Management 10

Total 45

Course Outcomes

Understands about conceptual knowledge and evolution of Management Accounting.

Familiarize the learners with the functions in Management Accounting.

Getting the idea of Analysis and Interpretation of Financial Statements.

Acquires knowledge and techniques of financial statement analysis.

Prepares Proforma of Vertical Balance Sheet and revenue Statement.

Calculates various Formulas which give assistance in futuristic decisions.

Understands the calculation of Working Capital and its Management.

Sr.

No.

Modules No. of

Lectures

1 Introduction to Management Accounting

Meaning-Nature, Scope, Function of management accounting- Role of

management accounting in decision making, Decision Making Process,

Financial Accounting V/S Management Accounting

10

2 Analysis and Interpretation of Financial Statements (a) Study of Balance Sheet and Income Statement/ Revenue Statements

in Vertical from suitable for analysis

(b) Relationship between items in Balance Sheet Trend Analysis &

Revenue Statement

(c) Tools of Analysis of Financial Statements-

i. Trend Analysis

ii. Comparative Statement

iii. Common Size Statement Note: i. Problems based on trend analysis ii. short problems on Comparative and Common Sized Statements iii. Comments on Short term and long financial position and comment on Profitability.

13

3 Ratio Analysis and Interpretation

(Based on Vertical Form of Financial Statements – Meaning,

Classification, Du Point Chart, Advantages and Limitations)

A. Balance Sheet Ratios: i) Current Ratio ii) Liquid Ratio iii) Stock

Working Capital Ratio iv) Proprietary Ratio v) Debt Equity Ratio vi)

Capital Gearing Ratio

B. Revenue Statement Ratio: i) Gross Profit Ratio ii) Expenses Ratio iii)

Operating Ratio iv) Net Profit Ratio v) Net Operating Profit Ratio vi)

Stock Turnover Ratio

C. Combined Ratio: i) Return on capital employed (Including Long Term

Borrowings) ii) Return on proprietor's Fund (Shareholders Fund and

Preference Capital) iii) Return on Equity Capital iv) Dividend Payout Ratio

v) Debt Service Ratio vi) Debtors Turnover vii) Creditors Turnover

(Practical Question on Ratio Analysis and Comments on that)

12

4 Working Capital Management

A. Concept, Nature of Working Capital , Planning of Working Capital

B. Estimation / Projection of Working Capital Requirement in case of

Trading and Manufacturing Organization

C. Operating Cycle

10

Evaluation Pattern

The performance of the learners shall be evaluated into two components viz. by Internal

Assessment with 40% marks in the first component and by conducting the Semester End

Examinations with 60% marks as the second component. The allocation of marks for the

Internal Assessment and Semester End Examinations are as shown below:‐

A) Internal Assessment – 40% 40 Marks

20 Marks mid-term test

10 Marks One Class assignment based on curriculum to be assessed by the teacher concerned

10 marks Group Presentation / Individual Activity / Mini Project.

Test Paper Pattern

Maximum Marks :20

Questions to be set 3

Q.No. 1 Choose the correct alternatives. (Any Five) (5 Marks.)

Q. No. 2 Answer in one sentence. (Any Five) (5 Marks.)

Q.No. 3. Answer the following. (Any Two) (10 Marks.)

B) Semester End Examinations – 60% 60 Marks

Question Paper Pattern

Maximum Marks: 60

Questions to be Set: 04

Duration: 2 Hrs.

All Questions are Compulsory Carrying 15 Marks each.

Q-1

Q-1

Full Length Practical Question

OR

Full Length Practical Question

15 Marks

15 Marks

Q-2

Q-2

Full Length Practical Question

OR

Fill Length Practical Question

15 Marks

15 Marks

Q-3

Q-3

Full Length Practical Question

OR

Full Length Practical Question

15 Marks

15 Marks

Q-4

Q-4

Objective Questions*

(*Multiple choice / True or False / Match the columns / fill in the blanks)

OR

Theory questions*

(*Short notes / short questions)

15 Marks

15 Marks

Note: Full length question of 15 marks may be divided into two sub questions of 08 and 07

marks

SEM IV

Introduction to Auditing

Modules at a Glance

No. Modules No. of Lectures

1 Introduction to Auditing 10 2 Audit Planning, Procedures and Documentation 10 3 Auditing Techniques and Internal Audit Introduction 15 4 Auditing Techniques : Vouching & Verification 10

Total 45

Course Outcomes:

Aware about conceptual knowledge and evolution of Auditing. Familiarizes the learners with the process of Auditing

Understand the concept of error and frauds.

Understands the duty of auditor regarding fraud and error.

Define and explain the planning and Documentation in Auditing.

Assists in getting the Standards on Auditing.

Understands various methods and techniques of Auditing.

Sr. No. Modules No. of Lectures

1 Introduction to Auditing A. Basics – Financial Statements, Users of

Information, Definition of Auditing, Objectives of Auditing, Inherent limitations of Audit, Difference between Accounting and Auditing, Investigation and Auditing.

B. Errors & Frauds – Definitions, Reasons and Circumstances, Types of Error, Types of frauds, Risk of fraud and Error in Audit, Auditors Duties and Responsibilities in case of fraud.

C. Principles of Audit, Materiality, True and Fair view

D. Types of Audit – Meaning, Advantages, Disadvantages of Balance sheet Audit, Interim Audit, Continuous Audit, Concurrent Audit and Annual Audit, Statutory Audit

10

2 Audit Planning, Procedures and Documentation A. Audit Planning – Meaning, Objectives, Factors to

be considered, Sources of obtaining information, Discussion with Client, Overall Audit Approach

B. Audit Program – Meaning, Factors, Advantages and Disadvantages, Overcoming Disadvantages, Methods of Work, Instruction before commencing Work, Overall Audit Approach.

C. Audit Working Papers – Meaning, importance, Factors determining Form and Contents, Main Functions / Importance, Features, Contents of Permanent Audit File, Temporary Audit File, Ownership, Custody, Access of Other Parties to Audit Working Papers, Auditors Lien on Working Papers, Auditors Lien on Client’s Books.

10

3 Auditing Techniques and Internal Audit Introduction

A. Test Check – Test Checking Vs Routing Checking,

test Check meaning, features, factors to be

considered, when Test Checks can be used,

advantages, disadvantages, precautions.

B. Audit Sampling – Audit Sampling, meaning,

purpose, factors in determining sample size –

Sampling Risk, Tolerable Error and expected error,

methods of selecting Sample Items Evaluation of

Sample Results auditors Liability in conducting

audit based on Sample

C. Internal Control – Meaning and purpose, review of

internal control, advantages, auditors duties, review

of internal control, Inherent Limitations of Internal

control, internal control samples for sales and

debtors, purchases and creditors, wages and salaries.

Internal Checks Vs Internal Control, Internal Checks

Vs Test Checks.

D. Internal Audit : Meaning, basic principles of

establishing Internal audit, objectives, evaluation of

internal Audit by statutory auditor, usefulness of

15

Internal Audit, Internal Audit Vs External Audit,

Internal Checks Vs Internal Audit

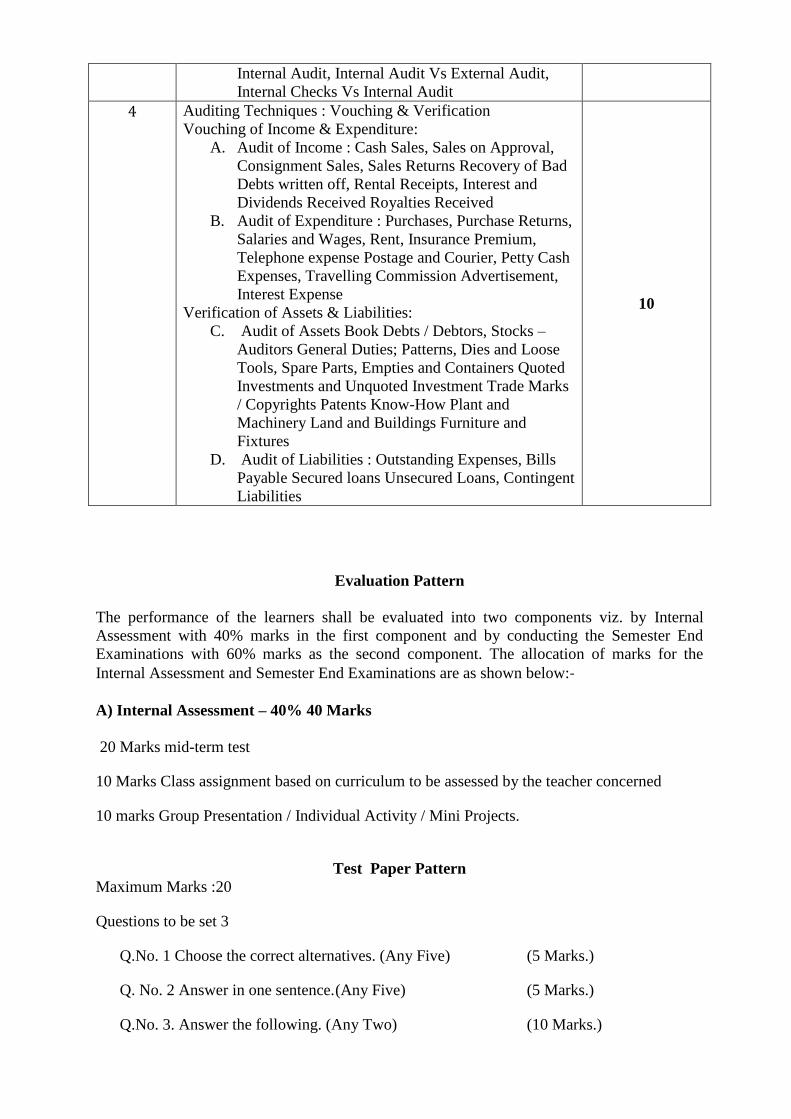

4 Auditing Techniques : Vouching & Verification

Vouching of Income & Expenditure:

A. Audit of Income : Cash Sales, Sales on Approval,

Consignment Sales, Sales Returns Recovery of Bad

Debts written off, Rental Receipts, Interest and

Dividends Received Royalties Received

B. Audit of Expenditure : Purchases, Purchase Returns,

Salaries and Wages, Rent, Insurance Premium,

Telephone expense Postage and Courier, Petty Cash

Expenses, Travelling Commission Advertisement,

Interest Expense

Verification of Assets & Liabilities:

C. Audit of Assets Book Debts / Debtors, Stocks –

Auditors General Duties; Patterns, Dies and Loose

Tools, Spare Parts, Empties and Containers Quoted

Investments and Unquoted Investment Trade Marks

/ Copyrights Patents Know-How Plant and

Machinery Land and Buildings Furniture and

Fixtures

D. Audit of Liabilities : Outstanding Expenses, Bills

Payable Secured loans Unsecured Loans, Contingent

Liabilities

10

Evaluation Pattern

The performance of the learners shall be evaluated into two components viz. by Internal

Assessment with 40% marks in the first component and by conducting the Semester End

Examinations with 60% marks as the second component. The allocation of marks for the

Internal Assessment and Semester End Examinations are as shown below:‐

A) Internal Assessment – 40% 40 Marks

20 Marks mid-term test

10 Marks Class assignment based on curriculum to be assessed by the teacher concerned

10 marks Group Presentation / Individual Activity / Mini Projects.

Test Paper Pattern

Maximum Marks :20

Questions to be set 3

Q.No. 1 Choose the correct alternatives. (Any Five) (5 Marks.)

Q. No. 2 Answer in one sentence. (Any Five) (5 Marks.)

Q.No. 3. Answer the following. (Any Two) (10 Marks.)

B) Semester End Examinations – 60% 60 Marks

Question Paper Pattern

Maximum Marks: 60

Questions to be Set: 04

Duration: 2 Hrs.

All Questions are Compulsory Carrying 15 Marks each.

Q-1

Q-1

Full Length Practical Question

OR

Full Length Practical Question

15 Marks

15 Marks

Q-2

Q-2

Full Length Practical Question

OR

Fill Length Practical Question

15 Marks

15 Marks

Q-3

Q-3

Full Length Practical Question

OR

Full Length Practical Question

15 Marks

15 Marks

Q-4

Q-4

Objective Questions*

(*Multiple choice / True or False / Match the columns / fill in the blanks)

OR

Theory questions*

(*Short notes / short questions)

15 Marks

15 Marks

Note: Full length question of 15 marks may be divided into two sub questions of 08 and 07

marks