aviva uk: the aviva family finances report 5 - january 2012

TRANSCRIPT

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 1/32

The Aviva FamilyFinances ReportJanuary – 2012

FAM_REP_V4_33760_BRO.indd 1 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 2/32FAM_REP_V4_33760_BRO.indd 2 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 3/32

The typical UK family

While 84% of the UK population lives as part of a family, theconcept of the ‘traditional’ family is now outmoded. In theFamily Finances Report, Aviva recognises there are variousdifferent types of modern families (see page four for groupstracked) and looks at their individual approaches to financesincluding wealth, debt and expenditure.

In addition, this January 2012 report looks at why finances can be a taboo topic for families,

and also the implications for those who don’t discuss ‘what if?’ scenarios with their loved

ones. Here Aviva encourages families to overcome these taboos and think about how their

families might cope financially, if their circumstances were to change.

Overview:

l Income – Average incomes rise but are hit by the impact of inflation (pg 5).

l Sourcesofincome– Sources of income remain steady over the year (pg 7).

l Expenditure – Spending levels remain steady as families juggle priorities (pg 9).

l Familywealth – Cost of living impacts on savings (pg 12).

l Housingwealth– Family house prices rise but housing wealth lags behind (pg 15).

l Familyborrowing– Level of unsecured debts doubles in a year (pg 18).

l Looktothefuture – Inflation fears top list of family concerns for 2012 (pg 20).

l Spotlight– Failure to discuss the ‘what ifs’ leaves families open to potential problems

(pg 22).

l AcrosstheUK – Regional data shows Londoners have it all – highest incomes but

also highest debts (pg 28).

The Aviva Family Finances Report 3

FAM_REP_V4_33760_BRO.indd 3 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 4/32

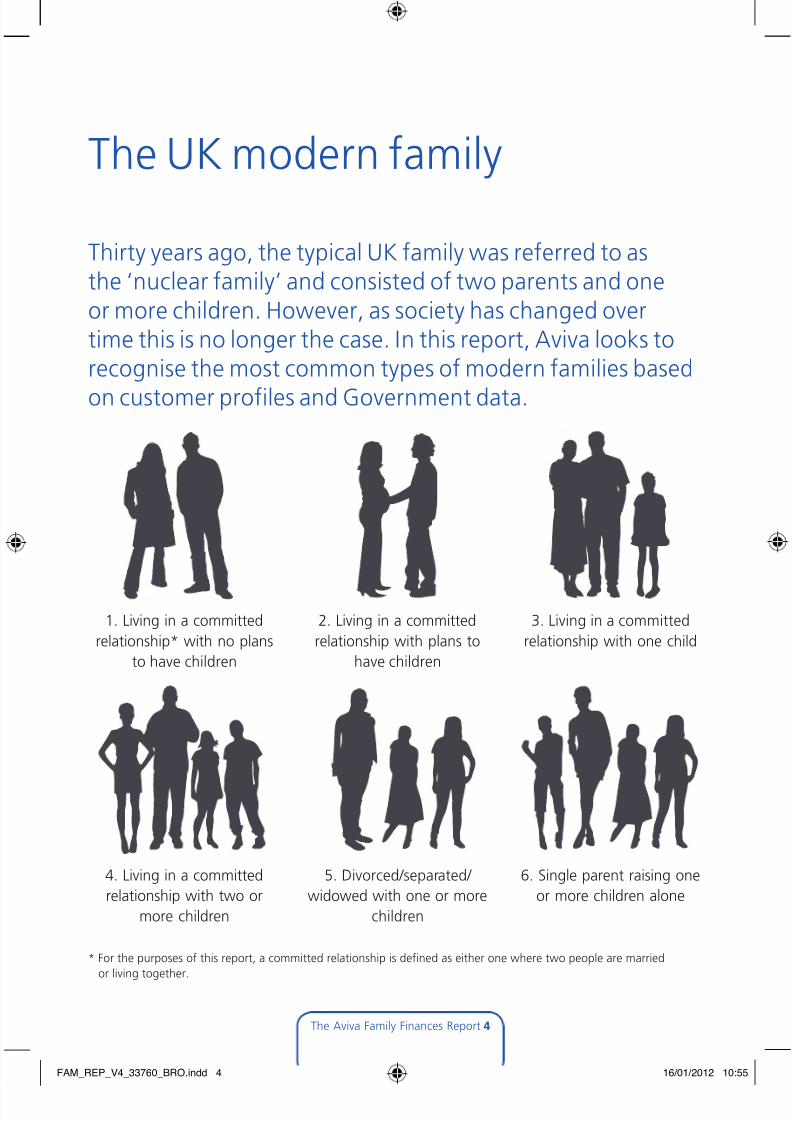

The UK modern family

The Aviva Family Finances Report 4

1. Living in a committed

relationship* with no plans

to have children

2. Living in a committed

relationship with plans to

have children

3. Living in a committed

relationship with one child

4. Living in a committed

relationship with two or

more children

5. Divorced/separated/

widowed with one or more

children

6. Single parent raising one

or more children alone

* For the purposes of this report, a committed relationship is defined as either one where two people are married

or living together.

Thirty years ago, the typical UK family was referred to asthe ‘nuclear family’ and consisted of two parents and oneor more children. However, as society has changed overtime this is no longer the case. In this report, Aviva looks torecognise the most common types of modern families based

on customer profiles and Government data.

FAM_REP_V4_33760_BRO.indd 4 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 5/32

Income

Averageincomesrisebutareabsorbedbytheimpactofinflation

The typical (i.e. the ‘median’ family in the

middle of the sample) monthly net income

of a family in the UK is now £2,066, which is

up (4%) on the previous quarter (November

2011 – £1,983), and up 7% compared to the

same time last year (January 2011 – £1,937).

The main factor behind this increase is the

rise in incomes experienced by those families

in committed relationships without children.

Those couples who are planning to have

children reported an 11% increase (year-

on-year) in monthly income from £2,187

(January 2011) to £2,433 (January 2012),and those living with a partner who do

not plan to have children reported a 10%

increase (year-on-year) in monthly income

from £2,010 (January 2011) to £2,220

(January 2012).

These two groups have the highest number of

people who derive an income from a ‘primary

job’ – i.e. income as a result of full timeemployment for the main breadwinner. Eighty

per cent of those families who plan to have

children, and 72% of those who do not plan

to have children, report this type of income.

The Aviva Family Finances Report 5

FAM_REP_V4_33760_BRO.indd 5 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 6/32

The Aviva Family Finances Report 6

Previous Family Finances Reports have noted the negative impact that children – especially

young children – can have on a family’s income and parents’ earning capacities, and this

appears to be the case still. Most family units with children also reported a slight year-on-year

increase in incomes, however divorced/separated/widowed parents reported a year-on-year

decrease from £1,387 (January 2011) to £1,075 (January 2012) per month. This decrease

has possibly been exacerbated by the changes to benefit payments which came into force in

2011, and also the impact of rising unemployment over the year.

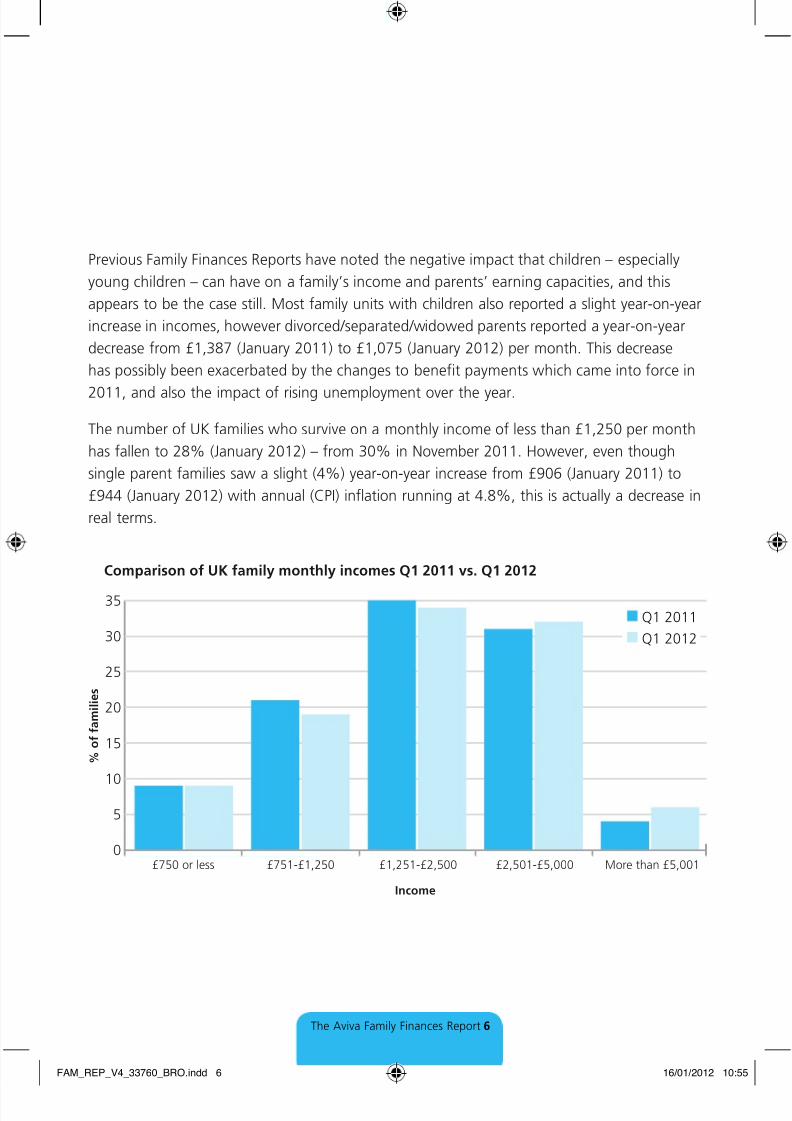

The number of UK families who survive on a monthly income of less than £1,250 per month

has fallen to 28% (January 2012) – from 30% in November 2011. However, even though

single parent families saw a slight (4%) year-on-year increase from £906 (January 2011) to

£944 (January 2012) with annual (CPI) inflation running at 4.8%, this is actually a decrease in

real terms.

0

5

10

15

20

25

30

35

Comparison of UK family monthly incomes Q1 2011 vs. Q1 2012

% o

f f a m i l i e s

Income

£750 or less £751-£1,250 £1,251-£2,500 £2,501-£5,000 More than £5,001

Q1 2011

Q1 2012

FAM_REP_V4_33760_BRO.indd 6 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 7/32

Sourcesofincome

The most common source of income for UK families is still the salary from a primary income

earner (69% – January 2012), although this has been falling over the past few quarters from a

high of 72% in August 2011 to 70% in November 2011. Government labour market statistics

for December 2011 support this declining trend as they show the unemployment rate is the

highest since 1996 and the number of unemployed people is the highest since 1994.

The number of families who obtain an income from spousal earnings remains relatively steady

(33% – January 2012 compared to 32% – November 2011), as does the number of families

who receive contributions from part-time or second jobs (18% – January 2012 compared to

18% – November 2011). The families most likely to report a part-time or second job are those

who are married with two or more children. More than one in five of these families (22% –

January 2012) are reliant on income from a second job to supplement their monthly income.

More than a fifth of families (22% – January 2012) rely on benefits to provide a

proportion of their monthly income. This has remained fairly steady over the last year(20% – January 2011). However, we have seen the number of single parents (50% – January

2012 vs. 54% – January 2011) and the number of divorced/separated/widowed parents

(47% – January 2012 vs. 54% – January 2011) claiming benefits fall. This suggests that the

Government’s benefit reforms have had an impact on some areas – a view supported by the

monthly income levels of these groups mentioned earlier.

Despite a year of low interest rates, volatile stock markets and falling bond yields, five per

cent of UK families still receive an income from savings and investments, although it is not

clear whether this is income from interest or from dipping into the capital. Families without

children are the most likely to receive an income from savings and investments, with 9% of

couples planning children, and 7% in a committed relationship with no plans to have children

reporting this.

The Aviva Family Finances Report 7

FAM_REP_V4_33760_BRO.indd 7 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 8/32

Spendingremainssteadyasfamiliesjugglepriorities

Despite the impact of inflation over the year, the average monthly family expenditure has

remained steady over the last 12 months. However there has been a notable drop in the

amount spent on children’s activities from 4% of monthly income in January 2011 to 1% in

January 2012.

There has been a slight dip in the amount spent on energy bills since the last quarter (6% –November 2011 compared to 5% – January 2012) which may be due to unseasonably mild

weather. There has also been a slight increase in the amount being spent on entertainment,

recreation and holidays (3% – November 2011 compared to 4% – January 2012) which could

be as a result of the festive period.

As a percentage of expenditure, debt repayment is also slightly higher than a year ago (8%

– January 2011 compared to 9% – January 2012), although lower than a peak seen in the

second quarter of 2011 (10%).

Expenditure

The Aviva Family Finances Report 8

FAM_REP_V4_33760_BRO.indd 8 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 9/32

The Aviva Family Finances Report 9

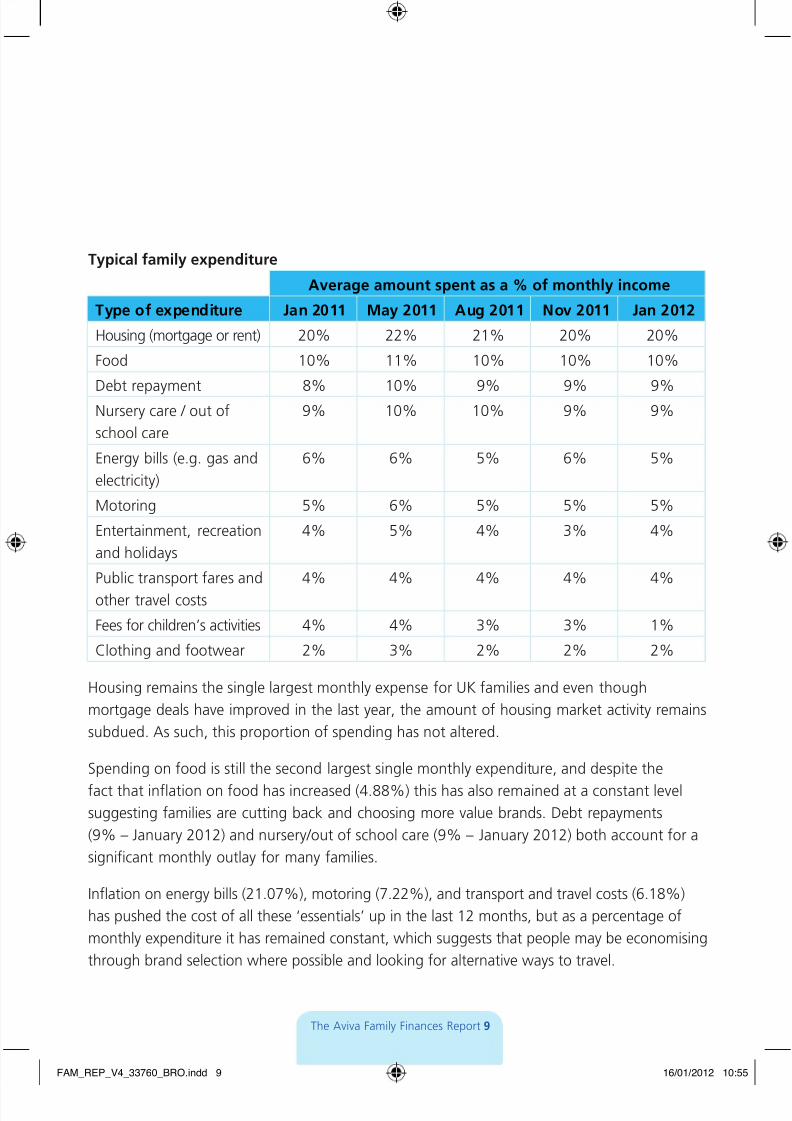

Typicalfamilyexpenditure

Averageamountspentasa%ofmonthlyincome

Typeofexpenditure Jan2011 May2011 Aug2011 Nov2011 Jan2012

Housing (mortgage or rent) 20% 22% 21% 20% 20%

Food 10% 11% 10% 10% 10%

Debt repayment 8% 10% 9% 9% 9%Nursery care / out of

school care

9% 10% 10% 9% 9%

Energy bills (e.g. gas and

electricity)

6% 6% 5% 6% 5%

Motoring 5% 6% 5% 5% 5%

Entertainment, recreation

and holidays

4% 5% 4% 3% 4%

Public transport fares and

other travel costs

4% 4% 4% 4% 4%

Fees for children’s activities 4% 4% 3% 3% 1%

Clothing and footwear 2% 3% 2% 2% 2%

Housing remains the single largest monthly expense for UK families and even though

mortgage deals have improved in the last year, the amount of housing market activity remains

subdued. As such, this proportion of spending has not altered.

Spending on food is still the second largest single monthly expenditure, and despite the

fact that inflation on food has increased (4.88%) this has also remained at a constant level

suggesting families are cutting back and choosing more value brands. Debt repayments

(9% – January 2012) and nursery/out of school care (9% – January 2012) both account for a

significant monthly outlay for many families.

Inflation on energy bills (21.07%), motoring (7.22%), and transport and travel costs (6.18%)

has pushed the cost of all these ‘essentials’ up in the last 12 months, but as a percentage of

monthly expenditure it has remained constant, which suggests that people may be economising

through brand selection where possible and looking for alternative ways to travel.

FAM_REP_V4_33760_BRO.indd 9 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 10/32

Spendingtrends

It is just as telling to see where families are not spending money, and the Family Finances

Report also tracks where UK families are cutting back and which expenses are vital. This

indicates what the fixed costs are for families and how their spending habits are affected by thestate of their finances.

Housing is an essential need, but the number of UK families who claim they do not spend

money on housing has been rising slowly over the last six months. In August 2011 20% said

they didn’t spend money on housing. By November 2011 this had risen to 21%, and in January

2012 22% of families said they are not spending any income on housing. This suggests that

they either own their own home outright, receive accommodation through employment, or are

supported by the State. In addition, some younger families may be economising by living with

extended family members.

The trend towards cutting back on non-essential items has continued into 2012, with 22%

of families (January 2012) claiming they are not spending money on personal goods (up from

17% in August 2011) and 30% saying they do without entertainment/recreation/holidays

(compared to 21% in August 2011). Almost half (42%) of families say they have cut out

spending on leisure goods completely (as opposed to 36% in August 2011).

The Aviva Family Finances Report 10

“UK families are determined to maintain their standard

of living despite the increases to the costs of goods and

services. Value for money is the watchword for many

families who have maintained spending on non-essential

items. Although with prices still rising, families may belooking to make further cutbacks in 2012.”

Louise Colley, head of protection sales and marketing, Aviva

FAM_REP_V4_33760_BRO.indd 10 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 11/32

However, while the percentage of monthly income spent on fees for children’s activities has

fallen in the last 12 months, the number of families spending money on these pursuits has

grown compared to a year ago. This might suggest that while families are paring back their

spending where possible, some are now having to spend money on low cost activities for their

children as there are fewer`free’ activities being provided.

PercentageoffamilieswhospendmoneyonthisexpenseonamonthlybasisTypeofexpenditure Nov2011 Jan2012

Housing (mortgage or rent) 79% 78%

Debt repayment 52% 52%

Entertainment, recreation and holidays 75% 70%

Public transport fares and other travel costs 67% 66%

Fees for children’s activities 48% 50%

Leisure goods 61% 58%

Eating out and takeaways 80% 77%

The Aviva Family Finances Report 11

FAM_REP_V4_33760_BRO.indd 11 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 12/32

Family wealth

Costoflivingimpactsonsavings

The rising cost of living in the last 12 months has meant UK families are finding it progressively

harder to set aside money each month. This report found the typical amount now being saved

on a monthly basis is £21 (January 2012), down from £22 in January 2011 – although there

was a spike in August when this reached £34.

Nevertheless, families are showing their resolve to maintain savings wherever possible and 70%of families say that they have some form of savings. There is no change from the last quarter in

terms of how many families have nothing set aside in savings (30% January 2012), but looking

over the last 12 months this has improved from 33% in January 2011.

The average (mean) amount UK families have in savings and investments (excluding pensions

and property) has increased significantly, but this is because the mean average is skewed by the

five per cent of families (January 2012) who have savings and investments worth more than

£100,000. Taking these people out of the equation brings the average down considerably.

The typical UK family (i.e. the family in the middle of the sample) has savings of £928 (January2012) which is actually up a more modest 9% from £849 in January 2011. This means that the

typical UK family has savings totalling less than half (45%) of the average (median) monthly

income of £2,066.

The majority of families classed as single parents (59%) and parents who are divorced/

separated/widowed (61%) say they do not manage to save anything each month.

These figures are significantly higher than the UK average, which shows that 42% of all

families save nothing on a monthly basis (January 2012). This figure is now at its highest level

for 12 months (40% in January 2011) and suggests that it is getting harder for families to save,

and also that there is a core group of families who are unable or unwilling to save.

It is notable that while the number of men who do not save regularly has fallen from 36%

(January 2011) to 33% (January 2012), for women the opposite is true and now 47% (January

2012) do not save on a monthly basis compared to 42% in January 2011. This trend is mirrored

by the typical (median) amounts being saved, with the typical monthly amount saved by a man

standing at £47 (January 2012) – up from £39 in January 2011 – while for women it has halved

over the same period from £16 a month to just £8 a month.

The Aviva Family Finances Report 12

FAM_REP_V4_33760_BRO.indd 12 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 13/32

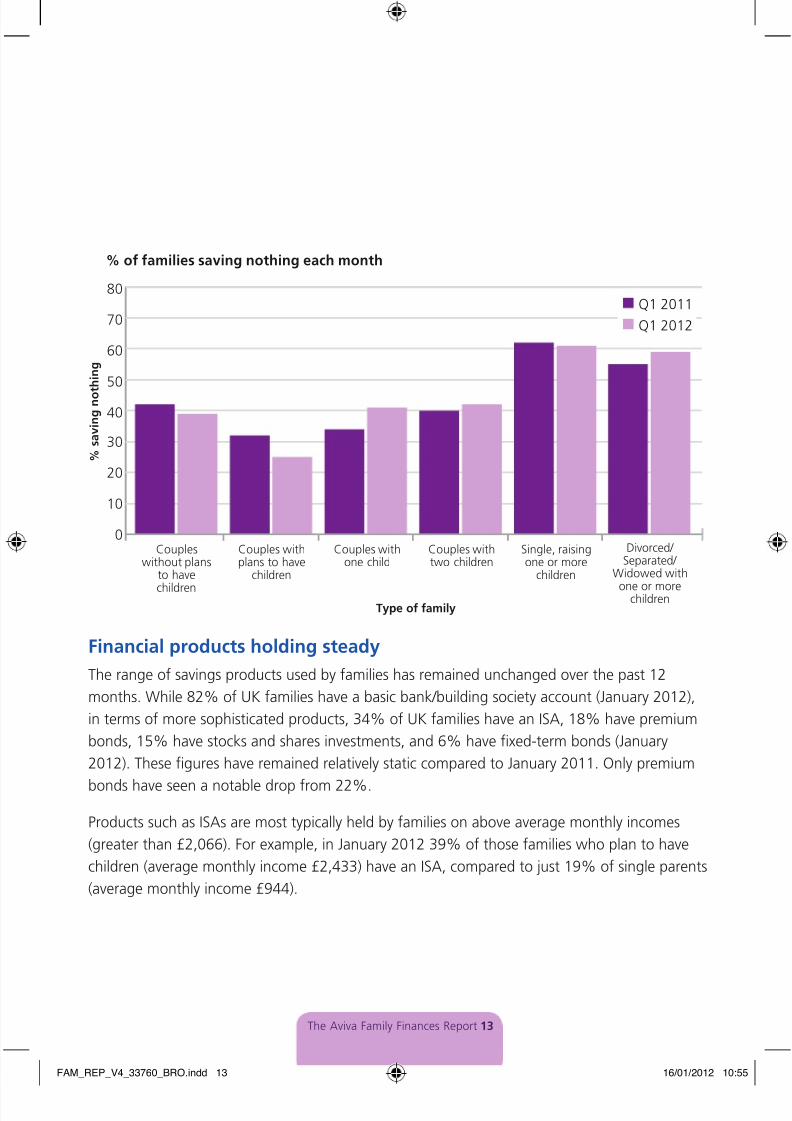

Financialproductsholdingsteady

The range of savings products used by families has remained unchanged over the past 12

months. While 82% of UK families have a basic bank/building society account (January 2012),

in terms of more sophisticated products, 34% of UK families have an ISA, 18% have premium

bonds, 15% have stocks and shares investments, and 6% have fixed-term bonds (January

2012). These figures have remained relatively static compared to January 2011. Only premium

bonds have seen a notable drop from 22%.

Products such as ISAs are most typically held by families on above average monthly incomes

(greater than £2,066). For example, in January 2012 39% of those families who plan to have

children (average monthly income £2,433) have an ISA, compared to just 19% of single parents

(average monthly income £944).

The Aviva Family Finances Report 13

0

10

20

30

40

50

60

70

80

% of families saving nothing each month

% s

a v i n g n o t h i n g

Type of family

Coupleswithout plans

to have

children

Couples withplans to have

children

Couples withone child

Couples withtwo children

Single, raisingone or more

children

Divorced/ Separated/

Widowed with

one or morechildren

Q1 2011

Q1 2012

FAM_REP_V4_33760_BRO.indd 13 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 14/32

This trend is similar for those who hold private pensions, with 33% of UK families (January

2012) holding a pension set up by their employer and 20% holding a personal private pension.

In January 2012, 30% of those families planning to have children (average monthly income

£2,433) have an employer pension, compared to just 21% of those divorced/separated/

widowed parents raising one or more children alone (average monthly income £1,075).

The number of families with protection insurance has also fallen over the last 12 months.While families with life insurance was up from 39% (January 2011) to 40% (January 2012),

the number with private health insurance is down from 15% (January 2011) to 12% (January

2012), and those with critical illness policies has fallen from 13% (January 2011) to 12%

(January 2012), with income protection down from 11% to 10%.

The Aviva Family Finances Report 14

“The latest Family Finances Report demonstrates that UK

families are feeling the pinch and as such are trying to

build and maintain a savings ‘buffer’ to protect themselves.However, at the same time the number of families who

have some type of protection insurance has declined. While

savings are clearly important, families should be aware that

protection products provide signicantly more nancial

security, should the unexpected happen.”

Louise Colley, head of protection sales and marketing, Aviva

FAM_REP_V4_33760_BRO.indd 14 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 15/32

Housing wealth

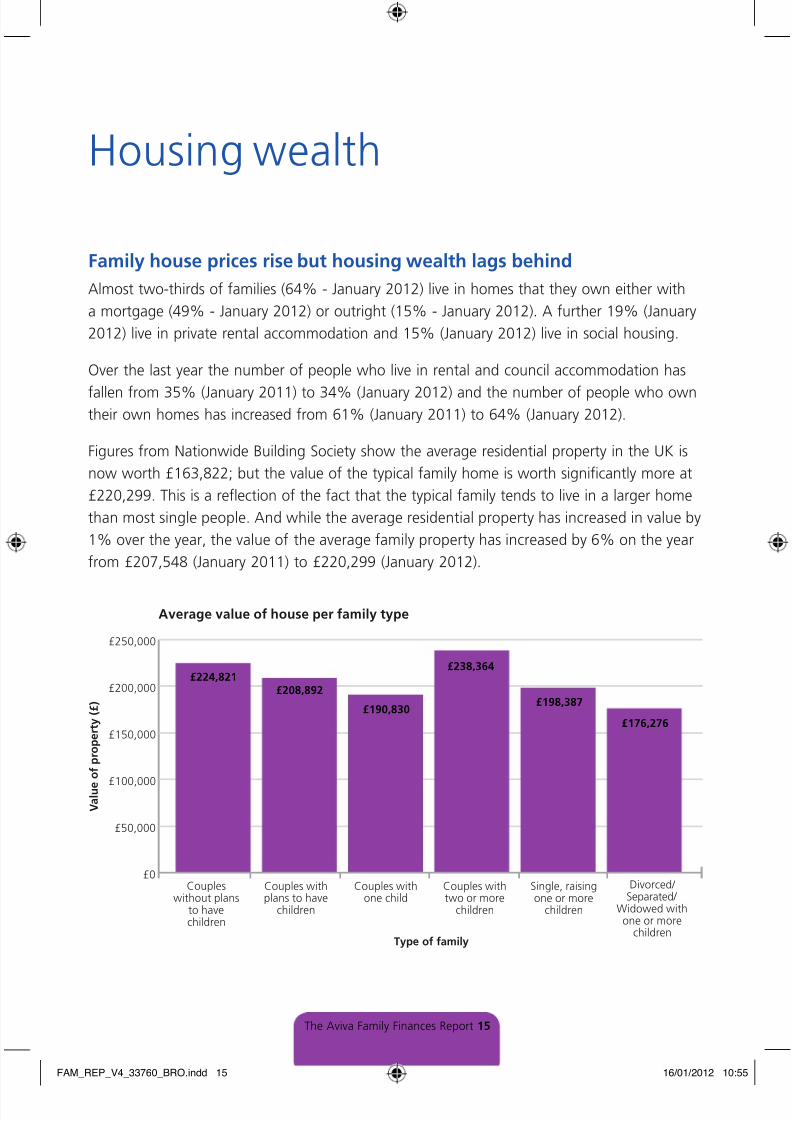

Familyhousepricesrisebuthousingwealthlagsbehind

Almost two-thirds of families (64% - January 2012) live in homes that they own either with

a mortgage (49% - January 2012) or outright (15% - January 2012). A further 19% (January

2012) live in private rental accommodation and 15% (January 2012) live in social housing.

Over the last year the number of people who live in rental and council accommodation has

fallen from 35% (January 2011) to 34% (January 2012) and the number of people who owntheir own homes has increased from 61% (January 2011) to 64% (January 2012).

Figures from Nationwide Building Society show the average residential property in the UK is

now worth £163,822; but the value of the typical family home is worth significantly more at

£220,299. This is a reflection of the fact that the typical family tends to live in a larger home

than most single people. And while the average residential property has increased in value by

1% over the year, the value of the average family property has increased by 6% on the year

from £207,548 (January 2011) to £220,299 (January 2012).

The Aviva Family Finances Report 15

£0

£50,000

£100,000

£150,000

£200,000

£250,000

Average value of house per family type

V a l u e

o f p r o p e r t y

( £ )

Type of family

Coupleswithout plans

to havechildren

Couples withplans to have

children

Couples withone child

Couples withtwo or more

children

Single, raisingone or more

children

Divorced/ Separated/

Widowed withone or more

children

£224,821£208,892

£190,830

£238,364

£198,387

£176,276

FAM_REP_V4_33760_BRO.indd 15 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 16/32

The average amount of equity families have in their homes has not risen at the same

pace however, increasing just 2% in the last 12 months from £139,218 (January 2011) to

£141,889 (January 2012). And the average family mortgage has increased from £89,018

(January 2011) to £101,538 (January 2012).

This tallies with data from the Council of Mortgage Lenders which has predicted that the

number of borrowers who could lose their homes because they cannot afford to pay theirmortgage will rise from 37,000 in 2011 to 45,000 in 2012. And tenants are not immune from

financial pressures either as they have seen rents rise significantly in 2011 to stand at a UK

average of £717 a month in December 2011.

Separate research from housing charity Shelter claimed in January 2012 that almost one

million people have resorted to payday loans (short-term loans with high rates of interest) to

cover their mortgage or rent in the last year.

Single people raising one or more children alone are the most likely to be living in social

housing (46% - January 2012) compared to single couples who plan to have children

(6% - January 2012).

The Aviva Family Finances Report 16

“Families tend to live in properties worth signicantly

more than the national average. However with nancestight for many it is a concern to see industry bodies

predicting more families will nd it difcult to maintain

repayments in 2012. Planning for contingencies affords

families the peace of mind that should the unexpected

happen, they will be able to cover their mortgage or rent,

and can have the stability of staying in their home.”

Louise Colley, head of protection sales and marketing, Aviva

FAM_REP_V4_33760_BRO.indd 16 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 17/32

Those families who are married/in a committed relationship with two or more children are the mostlikely to own their own home with a mortgage (56% - January 2012) and those who don’t plan to

have children are the most likely to live in a home they own outright (25% - January 2012).

The number of families who own a second property has increased from 13% to 16%

since January 2011 with those couples not planning children being the most likely to

do so (19% - January 2012).

“Following the death of a parent at a young age, we atGrief Encounter try and encourage families to keep as

much stability as possible for the bereaved child. Being

able to stay in their existing family home and at the same

school will provide a little comfort when their world has

been blown apart.”

Shelley Gilbert, CEO of Grief Encounter

The Aviva Family Finances Report 17

FAM_REP_V4_33760_BRO.indd 17 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 18/32

Family borrowing

Levelofunsecureddebtssoarsinayear

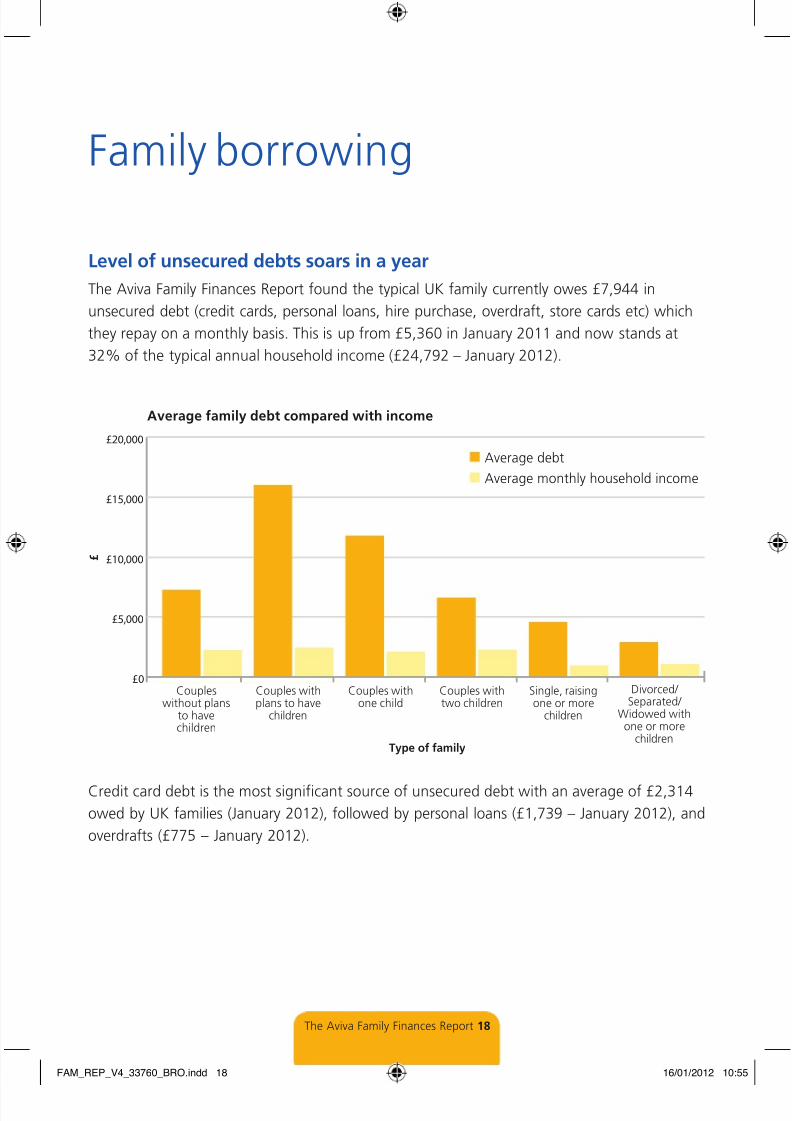

The Aviva Family Finances Report found the typical UK family currently owes £7,944 in

unsecured debt (credit cards, personal loans, hire purchase, overdraft, store cards etc) which

they repay on a monthly basis. This is up from £5,360 in January 2011 and now stands at

32% of the typical annual household income (£24,792 – January 2012).

Credit card debt is the most significant source of unsecured debt with an average of £2,314

owed by UK families (January 2012), followed by personal loans (£1,739 – January 2012), and

overdrafts (£775 – January 2012).

£0

£5,000

£10,000

£15,000

£20,000

Average family debt compared with income

£

Type of family

Coupleswithout plans

to havechildren

Couples withplans to have

children

Couples withone child

Couples withtwo children

Single, raisingone or more

children

Divorced/ Separated/

Widowed withone or more

children

Average debt

Average monthly household income

The Aviva Family Finances Report 18

FAM_REP_V4_33760_BRO.indd 18 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 19/32

The largest source of unsecured debt for the typical single parent family is credit cards,

with an average of £1,455 owed. Divorced/separated/widowed parents have the smallest

average overdraft (£243 – January 2012) compared to committed couples planning a family

(£3,839 – January 2012).

Divorced /separated/widowed parents owe the least (on average) in personal loans

(£573 – January 2012) compared to couples with one child (£2,452 – January 2012).

However, worries over inabilities to keep up with debt repayments have fallen over the year,

and only 12% of families cite this as a concern compared to 13% in January 2011.

“Families are now used to living with a certain level of

debt; however it has continued to increase over the last

12 months. As long as people are able to service their

debts, they remain manageable, but borrowings can be

another layer of pressure on a family’s nances.”

Louise Colley, head of protection sales and marketing, Aviva

The Aviva Family Finances Report 19

FAM_REP_V4_33760_BRO.indd 19 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 20/32

Look to the future

Inflationfearstoplistoffamilyconcernsfor2012

The top three biggest fears for UK families

over the next six months are: a significant

increase in the price of the basic necessities

(e.g. food or utilities) (62% - January 2012),

followed by losing job/s (i.e. redundancy)

(46% - January 2012), and unexpected

expenses (e.g. major repairs to home)

(41% - January 2012).

There has been no change to either the types

of financial concerns or to their rankings since

January 2011. However, in each case more

families are now more concerned about them

than they were this time last year.

UK families are slightly less concerned

about negative impacts caused by a

loss of/changes to Government benefits

(22% - January 2012 compared to

24% - January 2011). This suggests that

changes made and announced by the

Government in 2011 have now been

factored in to most families’ budgets.

A new category introduced in the last quarter

of 2011 found that 8% of families were

concerned about continued unemployment

(November 2011), and in January 2012 this

has increased to 10%. This indicates that

those people who are currently without jobs

are becoming less confident about their

prospects of re-entering the workplace.

The Aviva Family Finances Report 20

FAM_REP_V4_33760_BRO.indd 20 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 21/32

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 22/32

Spotlight – Financial taboos and

the potential impact on the familyIn this report Aviva looks specifically at the implications forfamilies who avoid facing up to their finances or are reluctantto plan for how they would protect their family in a worstcase scenario.

“It’s understandable that discussing awkward ‘taboo’ topics

can make many people feel uncomfortable. As a rule,

people don’t like to talk about the state of their nances

and it’s even less palatable to discuss how their families

would cope without them should they suffer a serious

accident or illness, or even a fatality. But by choosing to

bury their heads in the sand and ignore these subjects,

people potentially risk making a bad situation worse.”

Louise Colley, head of protection sales and marketing, Aviva

The Aviva Family Finances Report 22

FAM_REP_V4_33760_BRO.indd 22 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 23/32

Tabootopics

The Family Finances Report found 27% of families say they would be uncomfortable discussing

their debts with relatives, and 24% don’t like to discuss even general finances with them. There

are also major taboos around people’s own mortality – and with this what would happen if

they were no longer able to provide for their family.

Sixteen percent said they would avoid discussions about their funeral arrangements and

14% said they wouldn’t be prepared to talk about a will. Meanwhile one in 10 parents

(9%) are unwilling to discuss who might look after their children if they weren’t around, a

crucial consideration, particularly given the growing number of families who don’t conform

to the traditional ‘nuclear’ model. Significantly, the only topic seen as more taboo for family

discussions was ‘sex’ – a no-go area for 56% of respondents.

As many families feel uncomfortable discussing these topics, it is understandable that there

is a lack of understanding over what would happen and who would provide support to their

family, should the unexpected happen. As such, 9% of families reported that they did not

think they needed life insurance. Similarly nearly a third (30%) said they didn’t need income

protection and more than a quarter (26%) thought they didn’t need critical illness cover.

Monthlyoutgoings

As a result of this mindset, there are currently more families (50% - January 2012) who report

paying for a monthly satellite TV package than those who have life insurance

(40% - January 2012) which provides a cash lump sum in the event of the death of the insured.

This highlights that UK families seem more willing to prioritise spending on immediatepurchases and luxuries, than facing up to the need to protect their families financially.

The Aviva Family Finances Report 23

FAM_REP_V4_33760_BRO.indd 23 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 24/32

Protectionpriorities

The report also found that families are likely to attach more importance to vet’s bills and

protecting electrical goods and gadgets than their own health and the financial wellbeing of

their family.

More UK families have taken out insurance policies for their pets (17% – January 2012) and

mobile phones (14% – January 2012), than have taken out insurance to protect themselvesand their family in the event they suffer a critical illness (13% – January 2012). And more

people have taken out an extended warranty on electrical items (13% – January 2012) than

have income protection insurance (10% – January 2012) which would potentially pay them an

income for life should they be unable to work due to accident or sickness.

The Aviva Family Finances Report 24

0%

20%

40%

60%

80%

100%

% of families in possession of certain products/services

% w

h o o w n

Products/Service

I n c o

m e p r o t e c t i o

n i n s

u r a n

c e

E x t e

n d e d

w a r r a n t y o

n c a r

C r i t i

c a l i l l n e

s s i n

s u r a n c e

E x t e

n d e d

w a r r a n t y

o n e l e c t r i

c a l i t

e m s

P e t i

n s u r a n

c e

M o b i l e

p h o

n e i n s u r a n c

e

L i f e i n s u r a n

c e A w i l l

S a t e l l i t

e T V

p a c k a g

e

H o m e c

o m p u t e

r

H o m e i n t

e r n e t a

c c e s s

86% 86%

50%

40%

32%

17%14% 13% 13%

10%5%

FAM_REP_V4_33760_BRO.indd 24 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 25/32

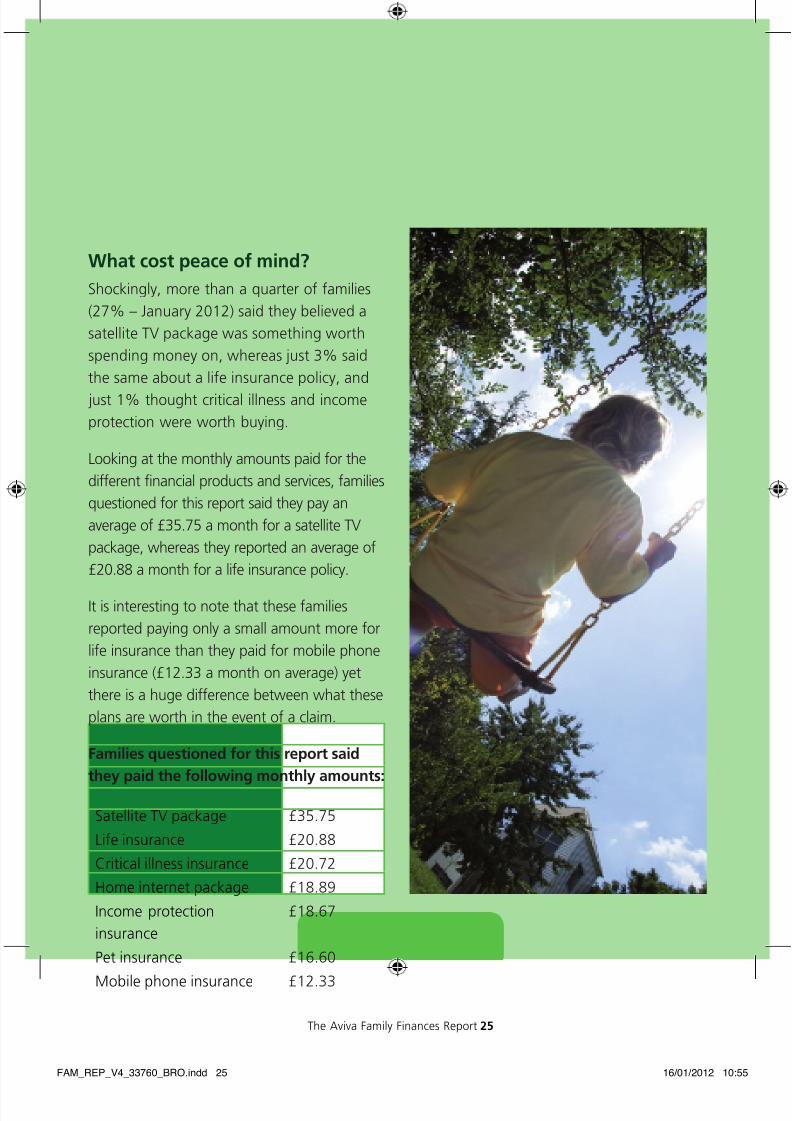

Whatcostpeaceofmind?

Shockingly, more than a quarter of families

(27% – January 2012) said they believed a

satellite TV package was something worth

spending money on, whereas just 3% said

the same about a life insurance policy, and

just 1% thought critical illness and income

protection were worth buying.

Looking at the monthly amounts paid for the

different financial products and services, families

questioned for this report said they pay an

average of £35.75 a month for a satellite TV

package, whereas they reported an average of

£20.88 a month for a life insurance policy.

It is interesting to note that these families

reported paying only a small amount more for

life insurance than they paid for mobile phone

insurance (£12.33 a month on average) yet

there is a huge difference between what these

plans are worth in the event of a claim.

Familiesquestionedforthisreportsaid

theypaidthefollowingmonthlyamounts:

Satellite TV package £35.75

Life insurance £20.88

Critical illness insurance £20.72

Home internet package £18.89

Income protection

insurance

£18.67

Pet insurance £16.60

Mobile phone insurance £12.33

The Aviva Family Finances Report 25

FAM_REP_V4_33760_BRO.indd 25 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 26/32

With the rising cost of goods and services causing UK families to look at their outgoings

and re-examine their financial priorities in 2012, the two most important financial steps

UK families believe they will take this year are cutting back on their spending

(39% – January 2012) and paying off their debts (35% – January 2012).

However, despite this, it seems other financial ‘safety checks’ are way down the priorities

list. More families are focusing on booking their annual holiday (21% – January 2012) thanbuying life insurance (3%) or making a will (13%) in 2012.

The Aviva Family Finances Report 26

FAM_REP_V4_33760_BRO.indd 26 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 27/32

The Aviva Family Finances Report 27

“While families know life insurance is something they

‘should’ think about, it’s more pleasurable to think about

things like planning holidays – so it’s no surprise to see

people putting it off. However our research also shows

that a third of people feel ‘frustrated’ with things ontheir to do list and a fth feel stressed by them. On the

ip side we know that customers report feeling reassured

when they have taken out life insurance, knowing their

affairs are in order. With this in mind it’s important to

look at ways providers and advisers can help customers

to understand the benets of protection insurance andthe peace of mind it can afford.”

Louise Colley, head of protection sales and marketing, Aviva

“We cannot begin to explain the devastation to a family

when a Mum or Dad dies young. At Grief Encounter we

see the impact on families when a nancial safety nethas not been put in place. Taking a short time to secure

life insurance now means that your family may have a

little comfort in their darkest times.”

Shelley Gilbert, CEO of child bereavement charity Grief Encounter

FAM_REP_V4_33760_BRO.indd 27 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 28/32

Region

% of people in the

region who are

living in a committed

relationship and

want children

% of people living

in the region living

in a committed

relationship with

one child

Monthly

incomeDebt

House

prices

1 East 8% 24% £1,923 £12,295 £235,875

2 London 14% 20% £2,845 £16,680 £340,023

3 East Midlands 6% 21% £2,055 £6,392 £195,546

4 West Midlands 7% 23% £2,027 £6,325 £191,927

5 North East 7% 25% £1,232 £3,640 £152,412

6 North West 7% 17% £1,981 £6,323 £174,831

7 Scotland 11% 15% £2,074 £4,459 £182,558

8 South East 9% 22% £2,314 £5,712 £263,242

9 South West 8% 17% £1,949 £9,263 £233,289

10 Wales 7% 19% £1,892 £6,333 £190,691

11 Yorkshire 8% 18% £1,964 £4,806 £169,875

UK 8% 20% £2,066 £7,944 £220,299

The Aviva Family Finances Report 28

The view across the UK

Families in London continue to have the highest average incomes of anywhere in the country.

The typical family in the capital has an average monthly income of £2,845 (compared with

£2,625 – January 2011), followed by those in the South East (£2,314).

The lowest monthly income can be found in the North East, where the typical family takes

home £1,232 each month. Family houses in this region are also valued at significantly less

than the average (£154,412 compared with £220,299). Families in London once again findthemselves at the top end of the scale, with the average house valued at £340,023.

They are also most likely to have built up their savings, with the typical family having stored

£3,124 away, followed by families in the East (£1,544) and South East (£1,199). In contrast,

families in the North East have the smallest savings pots of any region, with just £161 stashed

away. This is perhaps to be expected, with half (50%) of the region saving nothing each

month. Families in Yorkshire (52%) and Wales (52%) are the most likely to save nothing each

month, whereas this falls to just 34% of families in London.

FAM_REP_V4_33760_BRO.indd 28 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 29/32

The Aviva Family Finances Report 29

However, while

families in the capital

have higher incomes,

more valuable homes,

and more saved than

elsewhere in the country,

they have also incurred moredebt than anyone else.

The typical family in

this region owes

£16,680, whereas

this figure stands

at just £3,640 in

the North East (UK

average - £7,944).

Families in London are also least likely to be

financially protected. Thirty-six per cent of

families in the capital have life insurance

– yet almost half (48%) have a satellite

television package. In contrast, families in

the East (49%) and Scotland (49%)

are most likely to have taken out

life insurance. Meanwhile, less than

one in ten (9%) families in the West

Midlands has taken out insurance to protect

them in the event of a critical illness.

FAM_REP_V4_33760_BRO.indd 29 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 30/32

“

The Aviva Family Finances Report 30

So what does this tell us?

In this edition of the Family Finances Report, Aviva discovered just how

many families in the UK are unwilling to broach certain topics that deal

with their nancial and general health.

It can be uncomfortable for families to discuss how they would cope

nancially with a distressing event that leaves someone unable towork or worse, but not talking about it could be much more serious.

Unfortunately, statistics show one in four women and one in ve men

will suffer a serious illness before retirement age. This could leave them

permanently disabled and unable to work or worse, and if families have

not planned for this scenario then they are likely to end up suffering

nancially on top of the emotional distress.

I believe families need to take time out to consciously consider thepotential risks they are exposing their families to. As soon as I became a

mum the ‘what ifs’ were always at the back of my mind, and knowing I

have a responsibility to my children made me respond and take action.

For any families who aren’t protected, the ‘what if?’ conversation should

be top of their to do lists. By having the discussion, families can have

an appreciation of the nancial consequences they face and as a result

actually take the steps to make a difference.

The average costs of protecting a family are usually less than people think

– and often less than monthly charges that families pay out for other

goods and services. Plus, the younger a person is when they take out life

insurance, the less they tend to pay on a monthly basis.

FAM_REP_V4_33760_BRO.indd 30 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 31/32

“

The Aviva Family Finances Report 31

Buying a house and having children are just two major life events that

should act as a stimulus to encourage families to talk about how they

would protect themselves should the unexpected happen.

We know that around a quarter of families feel awkward talking about

money matters but this shouldn’t stop them having the discussions.And on a positive note, this also means that the remaining three

quarters feel comfortable raising the subject – so there’s no excuse not

to have the conversations!

Families owe it to themselves to discuss all eventualities, good and bad.

While we all hope for the best, we need to plan for the worst.

Louise Colley, head of protection sales and marketing, Aviva

LouiseColley,headofprotectionsalesandmarketingforAviva

andmumtoAmeliaandAlexander

FAM_REP_V4_33760_BRO.indd 31 16/01/2012 10:55

8/3/2019 Aviva UK: The Aviva Family Finances Report 5 - January 2012

http://slidepdf.com/reader/full/aviva-uk-the-aviva-family-finances-report-5-january-2012 32/32

SupportingBritish athletes

Methodology

The Aviva Family Finances Report was designed and produced by Wriglesworth Research.

As part of this 10,098* UK consumers – aged between 18 and 55 – who live as part of one

of six family groups were interviewed by Opinion Matters between December 2010 and

December 2011. This data was combined with additional information from the sources listed

below and used to form the basis of the Aviva Family Finances Report.

Additional data sources include:

l Unemployment Figures – Office of National Statistics – December 2011

l Nationwide – December House Price Figures

Technicalnotes

l A median is described as the numeric value separating the upper half of a sample, a

population, or a probability distribution, from the lower half. Thus for this report, the

median is the person who is the utter middle of a sample.

l An average or mean is a single value that is meant to typify a list of values. This is derived

by adding all the values on a list together and then dividing by the number of items on

said list. This can be skewed by particularly high or low values.

For further information on the report or for a comment, please contact Sarah Poulter at the

Aviva Press Office on 01904 452828 or [email protected]

* = Minimum of 2,000 per quarter