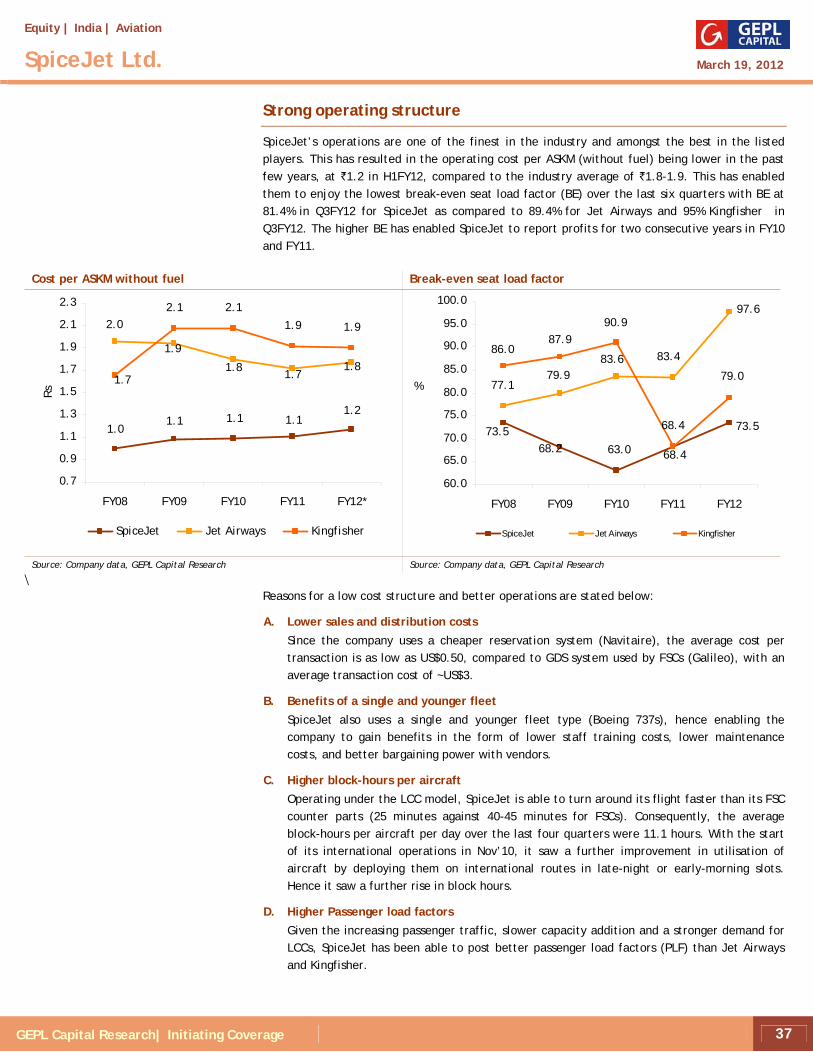

aviation industry - sector review - myirisbreport.myiris.com/geplcap1/jetairpr_20120319.pdf · the...

TRANSCRIPT

Equity | India | Aviation

Aviation Industry

Yields fail to rise despite traffic growth and ATF spike

March 19, 2012

Analyst Sunil Sewhani

+91-22- 6618 2690 [email protected] GEPL Capital Research 1

Sector Review

Domestic Aviation Industry

12.719.4

99.3

45.3

0

20

40

60

80

100

120

FY00

FY05

FY10

FY15

E

mn

visi

ts

0

5

10

15

20

%

Domestic traffic CAGR growth

International Aviation Industry

23.7

5.33.7

11.6

0

5

10

15

20

25

FY00

FY05

FY10

FY15

E

mn

visi

ts

0

5

10

15

20

%

International traffic CAGR growth

ATF Prices

40.7

48.8

54.9

60.6

66.1

62.7

44.6

58.656.2

64.665.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

Oct

-10

Feb-

11

Jun-

11

Oct

-11

Feb-

12

Rs/

litr

e

FY11 Market share

Jet Airways

(incl JetLite),

26.2

Kingfisher

(incl Air

Deccan)

16.5

NACIL, 19.9

SpiceJet, 13.5

Indigo, 17.5

GoAir, 6.3

Passenger traffic to double in the next four years

The passenger traffic in India has grown by 18% in FY11 and 15% in FY10. We expect India’s passenger traffic to nearly double in the next five years from 67 mn passengers in FY11 to 123 mn passengers (domestic - 99 mn and international – 23.7 mn) in FY15E, led by:

a) Higher GDP growth expectations and plenty of room for growth: Total passenger traffic in India has shown a GDP multiplier effect of 2.2x, over the last ten years. Despite this, there is still plenty of room for growth with number of trips per person in India (0.3) being much lower than other nations (0.15 in China 0.25 and 2.0 in USA).

b) Growth beyond metros led by better infrastructure facilities and connectivity: Passenger traffic in non-metros has seen 21% CAGR in the last five years with Tier –I cities witnessing a CAGR of 18%; Mumbai-Delhi witnessing a CAGR of 15% in the same period. This has been possible due to better infrastructure facilities and better connectivity.

c) Rising air travel affordability with the emergence of LCCs: The emergence of Low Cost Carriers (LCC) has led to affordable ticket pricing. With a growth in disposable income and stagnant ticket prices, a decline in average ticket price as a percentage of per-capita income has led to an increase in the air travel affordability. Consequently, we expect the share of LCC’s in the domestic traffic to rise to 56% by FY13E from 45% in FY11.

Demand-supply mismatch a blessing in disguise

The aviation industry has witnessed a relatively slow capacity addition due to stretched balance sheets and tight supply of aircrafts. Only LCCs have placed fresh orders for aircrafts and we do not expect fleet addition of over 15 aircraft per year for the next three years. Consequently, the passenger load factors are expected to remain above 70%.

Higher ATF prices a major cause of worry ATF prices have risen 62% since Oct’10 and 32% in CY11. Increased crude price is one of the biggest risks for profitability with a 1% rise in crude prices impacting EBITDAR by 3-5%. However, a 1% rise in load factor can negate the impact of a US$3-4/bbl rise in crude prices.

Yields under pressure with high competition despite demand supply mismatch Despite a sharp rise in ATF prices, the yields (Revenue/RPKM) have not been able to improve. While SpiceJet has seen a 6.7% rise in yields in Q2FY12, Jet’s domestic segment saw mere 1% rise in yields and Kingfisher’s yields declined by 10% in the same period. This has been due to an environment of intense competition leading to irrational pricing consequently resulting in deeper losses for most airline operators.

Lowering debt, improving cash flows a key for survival The rise in ATF prices and a decline in yields have resulted in a cash drain for most operators. To add to this the higher leverage by most operators results in a huge interest outflow even if a company is able to break even on the BITDAR front. Hence, the sector has not been in the best of health and needs to improve its debt position if it wishes to survive, compete and capture the growing pie of the Indian passenger traffic.

Valuation and views

We initiate coverage on the in the Indian aviation sector with a BUY rating on Jet Airways with a target price of `397 per share, BUY rating on SpiceJet with a target price of `28.3 per share, and a SELL rating on Kingfisher Airlines with a target price of `16 per share.

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 2

Passenger traffic to double in the next five years

Our analysis indicates that the performance of aviation stocks’ is correlated to traffic growth and earnings momentum. The domestic passenger traffic has witnessed a 14.7% CAGR in FY01-11 to 54 mn and the international traffic has grown at a 13.4% CAGR to 13.4 mn passengers in the same period. The growth rate is higher in the last five years led by government initiatives, better infrastructure and the emergence of LCC’s all of which have helped domestic passenger traffic grow at 16.5% CAGR in FY06-11 while international passenger traffic has seen a 15.5% CAGR in the same period.

The passenger traffic (PAX) in India has grown by 18% in FY11 and 15% in FY10. We expect India’s passenger traffic to nearly double in the next five years from 67 mn passengers in FY11 to 123 mn passengers (domestic - 99 mn and international - 19.3 mn) in FY15E assuming a 16.5% CAGR in domestic traffic and 15.5% CAGR in international traffic.

Domestic passenger traffic

12.7 13.7 14.0 15.7 19.425.2

35.844.4

39.5

62.973.2

85.3

99.3

12.9

45.3

54.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

E

FY13

E

FY14

E

FY15

E

mn

visi

ts

(20)

(10)

0

10

20

30

40

50

%

Domestic traffic Y-o-Y growth

Source: DGCA, GEPL Capital Research

International passenger traffic

4.2 4.5 5.36.5

7.69.1

17.8

20.6

23.7

15.4

10.0

3.83.7

13.4

11.6

3.7

0.0

5.0

10.0

15.0

20.0

25.0

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

E

FY13

E

FY14

E

FY15

E

mn

visi

ts

(5)

0

5

10

15

20

25

%

International traffic Y-o-Y growth

Source: DGCA, GEPL Capital Research

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 3

The growth in the passenger traffic industry is expected to be driven by three main factors

1. Strong GDP growth with 2.2 x multiplier effect Total passenger traffic in India has shown a GDP multiplier effect of 2.2x, (domestic 2.3x and international 1.9x) over the last eight years (FY04-FY11). Passenger traffic has grown at an average of 18.4% in the same period (from 20.2 mn to 67.3 mn) compared to real average GDP growth of 8.5% in the same period. The growth in passenger traffic has been driven by a 16.5% CAGR in FY06-FY11 in domestic passenger traffic to 54 mn and a 15.5% CAGR in international passenger traffic at 13.4 mn.

Pax growth 2.2x of Real GDP growth

8.58.06.99.29.79.5

7.58.5

11.0

22.3

28.3

36.8

23.418.3

15.0

(7.4)(10.0)

(5.0)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

%

Real GDP growth PAX growth Source: CMIE, DGCA, GEPL Capital Research

With an estimated 8% growth in GDP over the next 5 years and therefore we expect passenger traffic to double in the next four years and reach 123 mn trips by FY15E with domestic passengers accounting for over 80% of the total travels (99 mn) and the remaining being contributed by international passenger (23 mn).

Small base in global scenario offers plenty of room for growth

India is currently the world’s ninth largest civil aviation market in terms of passenger traffic and fourth largest market in terms of domestic passenger traffic. However, there is still plenty of room for growth as the number of trips per person is negligible at 0.05 compared to 0.15 in China 0.25 in Brazil and 2 per person in USA and other developed nations. With an increase in disposable income and strong GDP growth, we expect Indians to fly more and lead to a growth in traffic. . Moreover, the fact that India offers a mere 1/10th number of seats as compared to USA, the case for capacity addition and absorption remains highly lucrative.

Average trips per person across Nations

2.4

2.1

0.5

0.30.2

0.1

0.0

0.5

1.0

1.5

2.0

2.5

Australia USA Malaysia Brazil China India

Tri

ps p

er P

erso

n

Source: DGCA, GEPL Capital Research

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 4

2. Infrastructure- Improvement visible but long way to go

The government’s infrastructure facilities in support of aviation are clearly visible with the opening of the new terminal in New Delhi. Moreover, the other measures include the Green field airports in Hyderabad, Bengaluru and New Delhi and the on-going upgradation of terminals in Mumbai. The improved infrastructure facilities and modernization of technology have enabled faster turnaround of aircrafts and improved the flying experience for passengers.

The no of airports have increased 6% in FY06-10 to 116 (domestic 1% and international 21%) while the flights per day have risen by 90% (domestic 101% and international 51%). The operational efficiency has enabled PAX handled per day witness a 115% growth in the same period (domestic 142% and international 54%) highlighting the improvement in turnaround of aircrafts, higher take-offs and better load factors

Flights per day Passenger per day

1,8142,391

2,931 2,9183,638

509

586

674 840

768

0

1,000

2,000

3,000

4,000

5,000

CY06 CY07 CY08 CY09 CY10

Flig

hts

per

day

Domestic International

140194

238 212

33861

7081 94

94

0

100

200

300

400

500

CY06 CY07 CY08 CY09 CY10

Pass

enge

r pe

r da

y

Domestic International Source: DGCA, GEPL Capital Source: DGCA, GEPL Capital

Strong growth in Tier- II and tier – III cities

The improved connectivity has enabled strong growth in passenger traffic from tier-II and tier- III cities, with daily passenger traffic (DPT) in these airports growing at 21% CAGR, against 18% CAGR in tier-I cities and 15% CAGR in the top two cities, Delhi and Mumbai, in FY06-11. Consequently, the contribution of tier-II and tier-III airports to DPT has increased from 26% in FY06 to 31% in FY11.

With a rise in disposable income, faster and economical mode due to emergence of LCC’s and better connectivity to non-metros, the tier-II and III routes have changed course, to become profitable routes as compared to a government obligation a few years back.

City-wise growth in passenger traffic City-wise traffic contribution

(14)

(12)

27

20

30

16

2334 45

10

(7)

21

28

45

22

(20)

(10)

0

10

20

30

40

50

CY06 CY07 CY08 CY09 CY10

%

Top 2 Top 3-6 Tier II & III

43.4 40.6 39.6 39.3 39.5

30.6 32.1 31.9 31.0 29.5

26.0 27.3 28.4 29.7 31.0

0.0

20.0

40.0

60.0

80.0

100.0

CY06 CY07 CY08 CY09 CY10

%

Top 2 Top 3-6 Tier II & III

Source: DGCA, GEPL Capital Source: DGCA, GEPL Capital

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 5

3. Emergence of LCC’s – additional wings for the aviation sector

FY04 saw the emergence of the first Indian low-cost carrier (LCC), Air Deccan, followed by three more LCC’s: SpiceJet, Indigo and Go Air till FY07. With affordable pricing the LCC’s have been able to capture a bigger pie of the Indian domestic aviation market. LCC’s accounted for nearly 45% of the total domestic traffic in FY11 as compared to a mere 16% in FY06.

The share is much higher, at 60%, if we consider Kingfisher airlines (flies 75% of its passengers through Kingfisher Red). The rise in LCC’s has led to better operational efficiencies due to competition and led to a rise in affordability, hence we expect this share to rise to 56% by FY15E.

Share of LCC in domestic passenger traffic

22

29

34

40

45

0 10 20 30 40 50

FY07

FY08

FY09

FY10

FY11

%

Source: DGCA, GEPL Capital Research

Rising affordability

Air fares have remained more or less stagnant over the last 5 years (Jet airways: Mumbai-Delhi airfare). This has been mainly due to the entry of LCC’s and their quest to capture a higher market share. In the same period, per capita income has increased by 85% to `66487 from `35844 in FY06-11. This has made air travel more affordable, with the average ticket price as a percentage of per capita income declining to 7 2% in FY11 from 13.5% in FY06.

Average ticket price as percentage of per capita income

17.8

16.9

13.5

11.9

10.9

11.8

7.7

7.2

0.0 5.0 10.0 15.0 20.0

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

%

Source: CMIE, DGCA, GEPL Capital Research

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 6

Demand supply mismatch a blessing in disguise

The mismatch in the Available seat kms (ASKM) or capacity and passenger traffic growth has been a blessing in disguise for the Indian aviation industry. While the ASKM saw a 10.6% CAGR (Domestic: 11.8% and International: 9.6%) in FY06-FY11, the Revenue passenger km (RPKM) witnessed an 11.7% CAGR (Domestic: 13.2% and International: 10.3%) in the same period. This helped the PLF rise from 68.3% in FY06 to 71.5% (Domestic: 71.9% and International: 71.1%) in FY11.

RPKM growth to outpace ASKM growth It is due to the stretched balance-sheets and tight supply (delivery slots from Boeing for new orders available only from FY13E) that we expect the capacity addition to increase at a relatively slow pace of 10.4% CAGR in ASKM as against 10.9% CAGR in RPKM.

Domestic ASKM, RPKM and PLF

71.5

68.968.0

66.3

70.7 71.1

72.9 72.4 72.3 72.8

65.5

0

10

20

30

40

50

60

70

80

90

100FY

05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

E

FY13

E

FY14

E

FY15

E

bn

60.0

62.0

64.0

66.0

68.0

70.0

72.0

74.0

%

ASKM RPKM PLF

Source: DGCA, GEPL Capital Research

While the domestic passenger traffic is expected to witness a 16.5% CAGR in FY11-FY15E, the ASKM is expected to witness a mere 10.4% CAGR in the same period. The total ASKM is expected to rise from 125 bn in FY11 to 186 bn (Domestic: 94 bn and International: 92 bn) in FY15E. While the total RPKM is expected to rise from 89 bn in FY11 to 136 bn (Domestic: 69 bn and International: 67 bn) in FY15E. Consequently, we expect the Passenger Load Factor (PLF) to improve to 72.8% in FY15E from 71.5% in FY11.

International ASKM, RPKM and PLF

64.9

67.768.9 68.8

71.9 71.9

73.8 74.3 73.8

63.6

72.9

0

10

20

30

40

50

60

70

80

90

100

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

E

FY13

E

FY14

E

FY15

E

bn

58.0

60.0

62.0

64.0

66.0

68.0

70.0

72.0

74.0

76.0

%

ASKM RPKM PLF Source: DGCA, GEPL Capital Research

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 7

High debt to restrict new fleet addition

The Indian aviation industry is much more mature now than it was during FY05-08 and we believe that risk of sharp increase in capacity is lower in this cycle given the stretched balance sheets of the big carriers (mainly Indian Airlines, Jet Airways and Kingfisher Airlines).

Since companies such as Air India and Kingfisher have been making huge losses over the last couple of years, and are highly leveraged, not many aircraft leasing companies are interested in leasing out planes to them, since there is a risk of default on regular lease payments (which is the case for Paramount Airlines).

While Kingfisher and Air India will find it difficult to add further aircraft to its existing fleet due to a stretched balance sheet, Jet Airways is looking to add 17 Boeing 737s over the next one and a half year. This however should restrict JetLite to add aircraft especially given the intent of the management to merge the LCC business of JetLite and Jet Konnect.

SpiceJet also plans to add 30 Bombardiers to its fleet over the course of the next two years, however, the capacity addition would remain low seat configuration (78 seats) of the aircraft and Indigo though has placed an order for 180 Airbus, they would be deliverable over the course of the next 10 years. Hence, we expect and average addition of 10-12 aircraft per year in the entire industry.

To add to this a decision to stop operating flights from Mumbai and Delhi airports from strong players like American Airlines and Air Asia should keep the ASKM growth for the international segment under check. This should allow Indian carriers to benefit and help maintain the PLF above 70% over the next three years.

Less chances of organic ASKM growth due to high block hours and load factors Moreover, the possibility of capacity addition by increasing the use of aircraft also seems to be low as most airlines are already operating aircraft with block-hours of 10-12 hours per day. Consequently, we expect the load factors across the industry to remain above 70%.

Block hours per aircraft

10.611.2

11.8

8.99.5

10.2

12.1 11.9

11.1

6

7

8

9

10

11

12

13

FY10 FY11 H1FY12

Hou

rs

Jet Airways Kingfisher Airlines SpiceJet

Source: Various companies, GEPL Capital Research

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 8

Higher ATF prices a major cause of concern

Crude prices have been on the rise since Oct’10 due to various factors like the Middle-East crisis, uncertainty of the economy, and lower stock piles. This has resulted in Brent crude prices remaining above US$110/bbl for most part of CY11 forcing Oil Marketing Companies (OMC’s) to raise ATF prices. ATF prices hence rose 62% since Oct’10 and 32% in CY11 itself to `66/litre currently.

Moreover, to add to the existing woes, Western trade sanctions against Iran have begun to strangle its oil exports. This is on account of Iran being locked in a diplomatic row with major Western powers over its nuclear programme, which as per USA is aimed at building an atomic bomb. Meanwhile, traders noted positive economic data from the United States signaling a rising demand to the World's largest oil consumers. With oil inventories and spare OPEC production capacity running low, consumers don't have much buffer against additional disruptions in supply. This has led to Brent crude rising to a two year high of US$127/bbl resulting in a 13% rise in ATF prices in CY12 so far.

ATF Prices

40.7

48.8

54.9

60.6

66.1

62.7

44.6

58.6

56.2

64.665.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-

11

Aug

-11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Rs/

litr

e

Source: HPCL,BPCL, GEPL Capital Research

Despite the sharp rise in ATF prices, airline operators have been unable to pass on the rise to the end customers. Given the fact that a) fuel costs account for ~35-40% of the total sales of the company (35% for FSCs like Jet Airways, Kingfisher and over 40% for SpiceJet and JetLite) and b) airlines operate on low margins; a stark rise in ATF prices has severely impacted the profitability of companies. Consequently, Jet Airways (standalone) and SpiceJet have reported net losses for the third consecutive quarter while the losses for Kingfisher have widened.

Increased crude price is one of the biggest risks to profitability with a 10% rise in crude prices impacting EBITDAR by 15%. However, a 1% rise in load factor can negate the impact of a 2.5% rise in crude prices.

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 9

Do not see any near term positives from ATF imports The failure to hike prices and improve yields coupled with the rise in ATF cost has resulted in the Q3FY12 net losses for the three listed players mounting to `6.06 bn as compared to `153 mn in Q3FY11. Considering the high debt, low margins and rise in crude prices; airlines have seen constant erosion to their net worth over the last four quarters. Hence, Jet Airways and SpiceJet both have reported a net loss for the fourth consecutive quarter which has led to a sharp wipeout in its consolidated net worth. Kingfisher on the other hand has failed to record a profitable quarter yet again making survival even more difficult for itself.

The airline operators have therefore asked the government to allow import of ATF as currently taxes on ATF range from 4-35% (all inclusive) which severely dents their margins; considering fuel costs account for 40-45% of the total cost of airlines. Acceding to the demands of cash-strapped domestic aviation firms, a government panel on 8th Feb’12 allowed individual airlines to import ATF. Though the Cabinet will take a final call on the issue later, we believe the move will not be of much help to the airline operators.

No real savings from ATF imports

Airline operators believe that while OMCs will still levy marketing, handling and distribution charges for handling the fuel directly imported India, but the base price of oil (on which these additional charges will be levied) will be lower than what these companies set otherwise.

Though direct imports theoretically should result in savings of 20%- 25% on fuel cost, there is no clarity yet on the contours of ATF import making the savings calculation nearly impossible. However, in the real world, airlines would save only on sales tax which varies from 15-28% across the country, which would be offset by various facets such as

1. Airlines will have to import ATF in huge a quantity which is not viable If airlines do end up importing ATF, they would need to do so in large quantities with a parcel size of minimum 10,000-15,000 tonnes which is equivalent to 3-6 months of supplies. Doing so, would result in a large inventory for a long time, as compared to fuel derived from OMCs on just in time basis.

2. Lower credit period Airlines will avail only a 30 day credit facility due to the import of ATFs. Currently, airlines enjoy a 60-90 day credit from OMCs. Given the current cash crunch scenario across the industry this would lead to a stress on working capital of these companies hence making the move less lucrative.

3. Terminalling expenses Even if airlines are able to import from ports like Mumbai and Kandla in the west coast, and Kochi, Chennai and Haldia in the east coast, they would need to make arrangement for terminalling and pay for terminalling charge.

4. Storage and transportation cost

Even if somebody offers them terminalling facility, tanker and storage facility, they will have to transport it either through pipeline or transport system. This would once again make them dependable on OMCs for the infrastructure support.

Hence it would be more viable for airline operators if the various states adopted the Andhra Pradesh model of charging 4% tax of fuel. This suggestion was however not responded to favorably by most states. To add to this, even in the best case scenario, only a portion of the total ATF consumption would be imported and hence dependence on OMCs would remain.

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 10

Yields under pressure despite demand-supply mismatch and sharp rise in ATF prices

Despite a strong growth in the total passenger traffic in India, the yields (Revenue/RPKM) have failed to see a rise. Jet Airways has witnessed a 2% CAGR de-growth in yields in FY07-FY11 in its domestic business. Similarly SpiceJet has seen its yields stagnate over the last three years despite a 9% CAGR growth in FY07-FY11 due to a low base at the start of its operations. Kingfisher too has not been an exception to the rule and witnessed a 2% CAGR de-growth in its overall yields from FY09-FY11. This has been due to an environment of intense competition leading to irrational pricing consequently resulting in deeper losses for most airline operators.

Yields continue to remain under pressure

3.9 3.63.8

3.6

4.14.0

3.33.4 3.3

4.2

4.6

4.9

4.5

5.1

4.7

3.53.2 3.7

3.5

4.1

3.0

3.5

4.0

4.5

5.0

5.5

Q3FY11 Q4FY11 Q1FY12 Q2FY12 Q3FY12

Rs

Jet Airways JetLite Kingfisher SpiceJet Source: Various companies, GEPL Capital Research

The yields on a quarterly basis also have failed to show an improvement. Yields for the listed universe in Q2FY11 stood at a stagnant `4.2 as compared to `4.18 in Q2FY11 and declined by 6% Q-o-Q due to the seasonality impact on prices. While yields for Jet Airways grew by 2% Y-o-Y to `4.4, it fell 10% Y-o-Y for JetLite to `3.3 in Q2FY12. Similarly the yields for SpiceJet grew by 7% Y-o-Y and declined by 2% Y-o-Y for Kingfisher to `3.5 and `4.6 respectively in Q2FY12.

The stagnant yield is a major cause of concern for the industry given

A. The sharp rise in ATF prices over the last one year

B. Demand supply mismatch due to a stretched balance sheet

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 11

Lowering debt, improving cash flow: a key for survival

The aviation industry has witnessed turbulent times over the last one year with a sharp rise in fuel prices. This has led to losses for players across the board mounting over the last six quarters. Consequently, the companies have been burdened by higher debt and interest liabilities and seen their profits nose-dive.

We expect debt of the three listed players to witness a 2.3% CAGR in FY11-14E to `223.2 bn from `208.2 bn due to a 12.3% CAGR rise in debt for Kingfisher to `100.1 bn. Jet Airways’ net debt is expected to decline by 5.1% CAGR in FY11-FY14E to `116.8 bn led by a debt repayment of `16 bn of its aircraft related long-term debt. The purchase of Bombardier aircraft by SpiceJet should result in its debt rising to `6.4 bn in FY14E as compared to ~`4.4 bn in FY12E.

Due to the rise in debt we expect the interest outflow to witness a 2.8% CAGR in FY11-FY14E for the listed players to `26.2 bn despite a 14.7% CAGR in cash flow from operations which should partially aid debt repayment for SpiceJet and Jet Airways. Consequently, with the improvement in EBIT of all three companies we expect the interest coverage ratio to improve from 0.37 in FY11 to 0.54 in FY14E.

Debt of airline industry Cash of airline industry

142.8136.8 132.8

126.8116.8

79.270.6

80.689.6

100.1

4.4 0.9 4.4 7.9 6.4

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

FY10 FY11 FY12E FY13E FY14E

Rs

bn

Jet Airways Kingfisher Airlines SpiceJet

13.6 14.3

18.7

7.5

18.4

(10.4)

8.9

6.38.7 9.7

3.1

(2.3)(3.0)

0.03.2

(15.0)

(10.0)

(5.0)

0.0

5.0

10.0

15.0

20.0

25.0

FY10 FY11 FY12E FY13E FY14E

Rs

bn

Jet Airways Kingfisher Airlines SpiceJet

Source: Various companies, GEPL Capital Research Source: Various companies, GEPL Capital Research

Net interest outflow Interest coverage ratio

10.510.9

10.0 9.5 8.8

11.0

13.113.7

15.217.0

0.10.1

0.4 0.5 0.4

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY10 FY11 FY12E FY13E FY14E

Rs

bn

Jet Airways Kingfisher Airlines SpiceJet

0.4 0.8 0.4 1.1

(0.8)

0.2

6.5

12.0

(10.4)

(2.1)

4.6

(0.7)

(0.0)

(0.1)(0.5)

(15.0)

(10.0)

(5.0)

0.0

5.0

10.0

15.0

FY10 FY11 FY12E FY13E FY14E

Rs

bn

Jet Airways Kingfisher Airlines SpiceJet Source: Various companies, GEPL Capital Research Source: Various companies, GEPL Capital Research

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 12

Global Valuations

The Indian aviation industry is trading at 7.5x its one-year forward EV/EBITDAR which is a significant premium to players across the globe. However the figures remain skewed due to the presence of Kingfisher Airlines which despite its recent losses continues to command a strong premium. Jet Airways and SpiceJet together trade at an average of 5.5x its one-year forward EV/EBITDAR. We believe this premium is justified considering the strong growth in the passenger traffic in India over the next few years and the scope for growth.

Yields continue to remain under pressure

Name Country Price Mkt Cap (`mn) Revenue Growth EV/EBITDAR

Global Average 2.11

Jet Airways Ltd India 319.1 27,545 20.7 5.97

Kingfisher Airlines Ltd India 20.9 12,073 23.0 26.93

SpiceJet Ltd India 23.4 10,330 32.0 3.14

India Average 7.51

Allegiant Travel Co USA 50.7 48,521 17.4 4.63

Skywest Inc USA 11.1 28,379 32.2 2.37

Hawain Holdings Inc USA 5.1 12,976 26.0 1.25

Republican Airways Holding USA 4.7 11,417 7.9 3.40

AMR Corp USA 0.5 8,256 8.2 2.34

Air Canada Canada 0.9 12,957 7.7 2.10

Chorus Aviation Inc Canada 3.6 22,574 12.0 2.47

USA and Canada Average 2.44

Air New Zealand New Zealand 0.9 39,890 6.4 2.18

Rehional Express Holdings Australia 1.1 7,343 2.0 2.45

Australia and New Zealand Average 2.20

AER Lingus Ireland 0.9 32,336 6.0 2.06

Norwegian Air Shuttle Norway 98.3 29,730 25.3 3.54

SAS Ab Sweden 9.2 22,389 1.7 2.77

Finnair Finland 2.4 19,898 11.6 3.52

Dart Group UK 71.0 8,041 24.9 0.09

Flybe Group UK 63.0 3,763 4.4 0.45

Europe Average 2.52

Cebu Air Inc Phillipines 67.2 47,545 16.7 5.10

Skymark Airlines Japan 649.0 35,584 40.0 1.08

Tiger Airways Holdings Ltd Singapore 0.8 25,670 28.0 8.76

Asia Average 3.55 Source: Bloomberg, GEPL Capital Research

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 13

FDI in aviation: a step in the right direction

The Group of Ministers in a meeting reviewed the civil aviation ministry’s proposal to allow foreign airlines to pick up 49% in local airlines. The decision would require the Union Cabinet’s concurrence and will be moved to the Cabinet soon as per the Aviation Minister, Mr Ajit Singh.

We believe this is a step in the right direction and approval for the same could be a potential positive catalyst for the stock as this decision will allow a foreign partner to provide Indian airline operators the much needed lifeline of equity infusion.

We believe that the India aviation industry remains highly attractive with air travel penetration being one of the lowest among developing nations and almost 70% less than China’s. Further, we believe the strong macro economic factors like a) burgeoning middle-class, b) strong corporate travel, c) high youth working population, d) better connectivity and e) better affordability all offer ample growth opportunities.

Kingfisher Airline’s large net debt makes it less attractive as compared to the other listed players. The series of issues currently surrounding the company which include non-payment of taxes, salaries to employees and leasing disputes make its case further weak. While Jet Airways has a strong presence in the domestic (both FSC and LCC) and international travel, Mr Naresh Goyal’s (promoter of Jet Airways) 80% stake in Jet is considered as a foreign holding. This is also a key reason why the Foreign Investment Promotion Board (FIPB) had denied approval to Jet for an additional qualified institutional placement (QIP) unless foreign holding was brought down to 49%.

Hence we believe, SpiceJet which is largely a domestic player with the second highest market share in the LCC space would be the biggest beneficiary of an FDI approval. Given the low debt on books and capacity expansion of SpiceJet it seems more likely for investors to be interested in SpiceJet than any other listed airline operator

India: FDI policy on air transport and allied services

FDI ceiling on air transport services

• Scheduled air transport services: This includes scheduled operations by passenger airlines. FDI up to 49% and investment by non-resident Indians (NRIs) up to 100% is allowed through the automatic route.

• Foreign airlines cannot invest directly or indirectly in scheduled air transport services in India.

• Non-scheduled air transport services: It includes operations by non-scheduled airlines, chartered carriers and cargo airlines. FDI up to 74% and investment by NRI up to 100% is allowed through the automatic route.

• Foreign airlines cannot invest directly or indirectly in non-scheduled and chartered airlines, but they can invest up to 74% in cargo airlines in India.

• Helicopter services: FDI, including that from foreign companies, is allowed up to 100% through the automatic route.

FDI ceiling in other services under civil aviation sector

• Ground handling services: FDI up to 74% and investment by NRIs up to 100% is allowed through the automatic route, subject to sectoral regulations and security clearance.

• Maintenance, repair organisations, flying training institutes, technical training institutes. FDI up to 100% is allowed through the automatic route.

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 14

Evolution of domestic aviation industry

Duopoly (FY03-05): The industry was dominated by two major players, NACIL and Jet Airways with more than 90% market share. It also saw the entry of the first Indian low-cost carrier (LCC), Air Deccan, launched in FY04.

Entry of new players (FY05-07): Three more LCCs (SpiceJet, Indigo and Go Air) and two more FSCs (Kingfisher Airlines and Paramount Airways), entered the industry. Consequently, the number of players increased from three in FY03 to nine in FY07.

Intense competition (FY07-08): This period was marked by the beginning of intense competition in a bid to capture market share, with rapid fleet expansions by both new and incumbent players. This resulted in a sharp drop in profitability and the deterioration of balance-sheets. By the end of FY08 the top-three players’ market share dropped to 69% and the share of LCC’s increased to 31%.

Consolidation phase (FY08-11): The subsequent significant erosion in net worth resulted in merger/acquisition of the financially weak companies with the stronger ones and the halting of fleet additions. Jet Airways acquired Air Sahara (now Jet-Lite), Kingfisher acquired Air Deccan, and Indian Airlines merged with Air India to form NACIL. However, the market share of LCC’s increased to 45%, by FY11.

In the next five years, we expect LCC’s to gain control of more than half of the domestic aviation market because of LCCs’ relatively faster fleet addition; compared to FSCs. FSCs’ are increasing focus on serving tier-II and tier-III cities through their LCC arms. The relatively fast growth in leisure travel (compared with business travel), is more advantageous for LCC’s due to the cost consciousness of the Indian consumer.

Equity | India | Aviation

Aviation Industry March 19, 2012

GEPL Capital Research | Sector Review 15

Player-wise market share in FY03 Player-wise market share in FY07

Jet Lite,

10

NACIL, 42

Jet

Airways,

48

Jet Airways,

28.4

NACIL, 20.3

Paramount,

1Go Air, 3.6

SpiceJet,

7.4

Indigo, 2.6

JetLite, 8.4

Kingfisher,

9.3Air Deccan,

19

Source: DGCA, GEPL Capital Research Source: DGCA, GEPL Capital Research

Player-wise market share in FY08 Player-wise market share in FY11

Jet Airways

(incl JetLite),

29.4

Kingfisher

(incl Air

Deccan)

29

NACIL, 17.8

SpiceJet, 9.3

Indigo, 8.8

GoAir, 4.1

Paramount,

1.3

Jet Airways

(incl JetLite),

26.2

Kingfisher

(incl Air

Deccan)

16.5

NACIL, 19.9

SpiceJet, 13.5

Indigo, 17.5

GoAir, 6.3

Source: DGCA, GEPL Capital Research Source: DGCA, GEPL Capital Research

Equity | India | Aviation

Jet Airways (India) Ltd.

International business to aid growth March 19, 2012

BUY

Analyst Sunil Sewhani

+91-22- 6614 2690 [email protected] GEPL Capital Research 16

Initiating Coverage

CMP (`) Target (`)

318.9 397

Potential Upside Absolute Rating

24% BUY

Market Info (as on 16th March, 2012)

BSE Sensex 17466

Nifty S&P 5317

Stock Detail

BSE Group A

BSE Code 532617

NSE Code JETAIRWAYS

Bloomberg Code JETIN IN

Market Cap (`bn) 27.53

Free Float (%) 20%

52wk Hi/Lo 517 / 167

Avg. Daily Volume (NSE) 2347833

Face Value / Div. per share (`) 10.00 / 0.00

Shares Outstanding (mn) 86.3

Shareholding Pattern (in %) Promoters FIIs DII Others

80.00 5.42 6.28 8.30

Financial Snapshot (`mn)

Y/E Mar FY10 FY11 FY12E FY13E

Net Sales 145,226 167,787 206,240 224,488

EBITDA 15,692 982 11,348 16,870

PAT (858) (10,688) (3,560) 333

EPS (10) (124) (41) 4

ROE (%) (3) (32) (20) 18

ROCE (%) 9 (3) 2 5

P/E (45) (1) (4) 48

EV/EBITDA 11 148 12 7

Share Price Performance

20

30

40

50

60

70

80

90

100

110

120

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-

11

Aug

-11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Jet Airways BSE SENSEX

Rel. Perf. 1Mth 3 Mths 6Mths 1Yr

Jet Air (%) (7.5) 55.9 17.1 (31.8)

SENSEX (%) (3.8) 12.7 3.1 (4.9)

Source: Company data, GEPL Capital Research

Investment Rationale

Unique business model with presence across segments We believe Jet Airways India Ltd (Jet) is best placed to capture the 16.5% CAGR in domestic passenger traffic and 15.5% CAGR in international passenger traffic in FY11-FY15E. Jet offers a host of benefits due to flexible business model such as a) dominant market share in both the domestic (~26%) and international market (~36%) allowing it to reshuffle part of its fleet depending on the seasonality in demand, b) presence in the FSC (Jet Airways) and LCC segments (JetLite and Jet Konnect) which enables to successfully divert part of its fleet based on the demand supply scenario, and hence maintain the yields and load factors, and c) varied fleet type (Boeing and ATR), size (capacity of 777s is 312 while that of ATR is 65) and ownership making pilot poaching difficult, accommodating demand across sectors easier and leasing out owned fleet to capitalise on the demand-supply mismatch.

Focus on International segment- key driver for profitability The international business of Jet Airways has seen a sharp turnaround in operations; from being a loss making until FY08 (EBITDA level) to contributing 74% to the consolidated EBITDA in FY11. The international division has not only led to higher margins and profitability for the company but also aids growth by providing synergies like a) ready customer base to its domestic segment, and b) creates diversified passenger traffic leading to demand throughout the year.

Improving domestic business Due to the strong brand image, operational synergies and flexible business model, the domestic business of Jet Airways has witnessed a sharp improvement in operations. The company plans to add 17 Boeing 737-800 to its existing fleet over the next one and a half year, to increase its domestic capacity and capture a greater share of the demand supply mismatch present in the domestic aviation industry in India.

Merger of JetLite and Jet Konnect to boost LCC segment growth

The company has also successfully managed to improve JetLite’s operational efficiency over the years with a rise in block hours despite the reduction in ASKM which has helped improve efficiencies and reduce costs. Jet plans to merge its two LCCs JetLite and Jet Konnect and operate under the brand name of the latter. The higher brand perception for Jet Konnect as compared to JetLite, higher operating efficiencies by the former, tie-up synergies and improved connectivity are some of the benefits that the company would witness with the re-branding and merger of JetLite.

Balance sheet concerns overdone The company has successfully reduced its debt position to `1.36 bn in FY11 as compared to `1.42 bn in FY10. With `9 bn of this debt being aircraft-related dollar denominated debt and 4.5% rate of interest, the debt situation is much better for Jet when compared to its peers. Moreover, the company has converted part of its rupee debt which has helped reduce interest outgo. With a series of steps like a) refinancing high-cost debt, b) the sale and leaseback of aircraft, and c) the sale of non-core assets, we expect Jet’s interest burden to decline by 18% over the next two years.

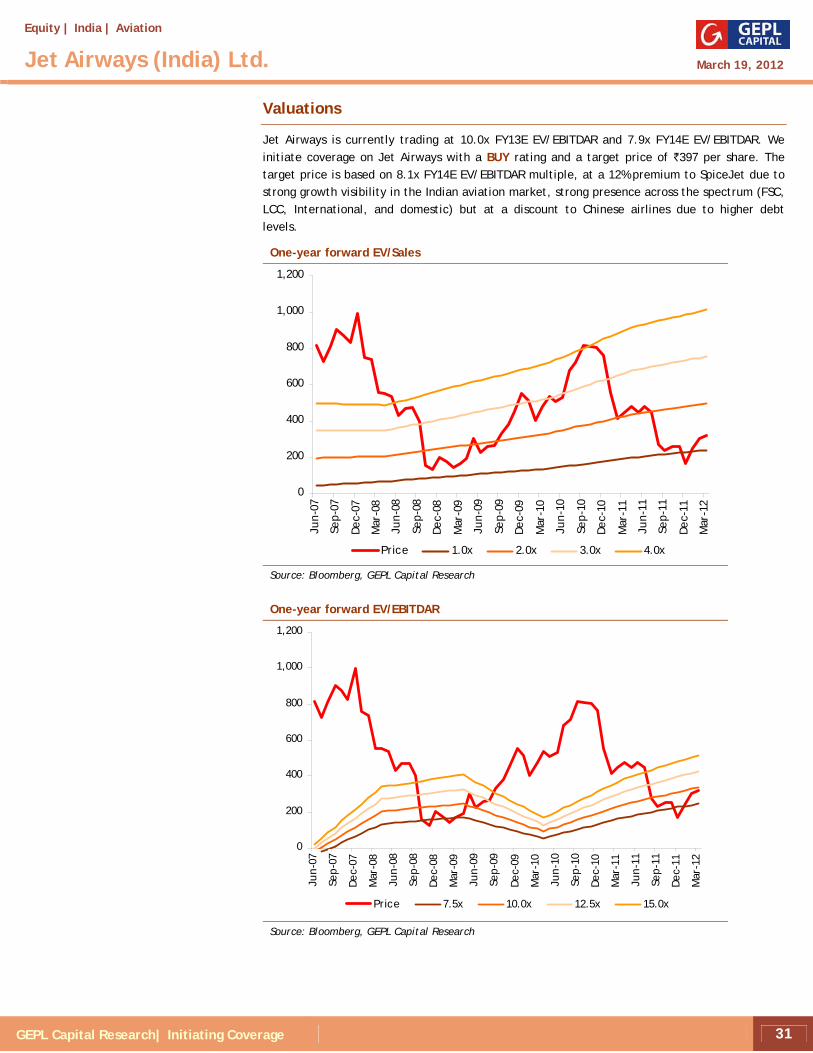

Valuation

Jet Airways is currently trading at 10.0x FY13E EV/EBITDAR and 7.9x FY14E EV/EBITDAR. We initiate coverage on Jet Airways with a BUY rating and a target price of `397 per share. The target price is based on 8.1x FY14E EV/EBITDAR multiple, at a 12% premium to SpiceJet due to strong growth visibility in the Indian aviation market, strong presence across the spectrum (FSC, LCC, International, and domestic) but at a discount to Chinese airlines due to higher debt levels.

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 17

Investment Rationale Unique business model with presence across segments

We believe Jet Airways India Ltd (Jet) is best placed to capture the 16.5% CAGR in domestic passenger traffic and 15.5% CAGR in international passenger traffic in FY11-FY15E due to its unique business model and the benefits attached to the same.

A. Presence in domestic as well as international market The domestic passenger traffic has witnessed a 16.5% CAGR in FY06-FY11 to 54 mn trips. We assume similar growth trend in the future considering a) rising GDP over the next five years with a 2.2x multiplier effect, b) improving infrastructure with new airports and expansion of existing airports, and c) rising per capita income in India and comparatively lower rise in ticket prices hence improving the affordability of Indian travelers. With a 16.5% CAGR in FY11-FY15E we expect the domestic passenger traffic to grow to 99 mn trips.

Domestic market share International market share

35.9

29.1 28.125.7 26.2

0

5

10

15

20

25

30

35

40

FY07 FY08 FY09 FY10 FY11

%14.3

19.9

32.9 3435.9

0

5

10

15

20

25

30

35

40

FY07 FY08 FY09 FY10 FY11

%

Source: DGCA, GEPL Capital Research Source: DGCA, GEPL Capital Research

Ability to reshuffle part of its fleet across geographies Jet Airways currently has 54 aircraft allocated in the domestic skies, 5 sub leased aircrafts, and the reaming 41 aircraft routed to fly international. Its presence in the international and domestic markets has enabled the company to re-shuffle its fleet to international skies based on the seasonal demand and vice versa. During the Oct-Jan period international tourist arrivals are at its peak while Apr-June period is the peak season for Indian domestic travelers. The presence across geographies helps reduce its dependence on a particular market and helps improve fleet efficiency.

The presence in the international segment has helped improve the block hours for the company as well improve revenues with a higher revenue per RPKM (yield) seen from the international business.

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 18

B. Presence in the FSC and LCC segment

The company is the best bet in the Indian aviation space, to capture the robust growth in the domestic passenger traffic due to its presence in both the LCC and FSC segment. The company caters to the lower end of the spectrum with its brands, Jet Konnect and JetLite, and to the premium end with its own brand-name, Jet Airways. This enables the company to provide a range of ticket prices and is able to cater to premium and economy travelers. The presence in the LCC segment allows it to capture the relatively strong growth in the domestic skies and also leads to improvement in blended load factors. On the other hand the FSC segment has helped Jet maintain its yields.

Passenger load factors (PLF) Yields

69.5 69.5 67.7

77.1 78.7

68.8 68.863.7

72.177.4

68.0 66.3 65.5 70.7 73.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

FY07 FY08 FY09 FY10 FY11

%

Jet (consolidated) Domestic Industry

International Industry

5.7 5.8

6.8

5.3 5.2

2.9 3.03.3

2.8 2.94.63.4 3.4 3.6 3.7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

FY07 FY08 FY09 FY10 FY11

Rs

Jet Domestic Jet International JetLite

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Diverting part of its fleet under the FSC/LCC model Due to the advantage of having a presence in both the LCC and FSC model, the company has been able to successfully divert part of its fleet based on the demand supply scenario, and hence maintain the yields and load factors.

It has a vast fleet of 119 aircrafts (19 Jet Lite and 100 Jet Airways ) and has a competitive advantage due to operations under FSC and LCC models which enables it to divert part of its fleet under the LCC/ FSC model depending on the economic scenario.

For example, in the downturn of FY09, Jet reconfigured two-thirds of its domestic fleet by converting premium seats to economy seats which helped maintain demand and load factors despite the lower yields. Similarly, when the demand for premium travel had revived in FY10, it started reconfiguring its seats by adding premium seats again. This has given a significant boost to their yields considering that passenger yield for business class is 2.5x that of economy class.

Moreover, the company is able to evaluate the possibility of deploying the higher capacity (Airbus A330 aircraft with 220 seats) in place of the current Boeing 737s (with 175 seats) on the Mumbai-Delhi route, due to strong demand and limited slots available at Mumbai airport.

Such flexibility places Jet in a better scenario than its competitors and hence the company is able to capture a greater share of wallet spend during good time as well as maintain its PLF during lean seasons.

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 19

C. Varied fleet size and type

Jet Airways (standalone) currently has a fleet of 100 aircraft (12 Boeing 777 series, 12 Airbus A330-200, 56 Boeing 737 series and 20 ATR 72-500 turboprops). Its fleet also comprises of 19 aircraft (10 Boeing 737-700 series and 9 Boeing 737-80- series) under its fully owned subsidiary Jet Lite (previously Air-Sahara). Due to the difference in fleet (Boeing for Jet and Airbus for Kingfisher and Indigo) poaching of pilots becomes difficult and hence the attrition rate is maintained.

Moreover, a varied fleet size (capacity of Boeing 777s is 312 seats while that of ATR is 65 seats) helps to accommodate demand across sectors. This has led to the company being able to constantly maintain and improve its load factors. The move has also led to better utilisation of its fleet as per the needs of the sector and the cyclical and seasonal demand.

Jet Airways Fleet type

Type Size Capacity

Boeing 737-700 11 118

Boeing 737-800 43 160

Boeing 737-900 2 138

ATR 72-500 20 65

Airbus 330-200 12 235

Boeing 777-300 12 312

Source: Company data, GEPL Capital Research

Jet-Lite Fleet type

Type Size Capacity

Boeing 737-700 10 145

Boeing 737-800 5 186

Boeing 737-800W 4 186

Source: Company data, GEPL Capital Research

Leasing out owned fleet to capitalise on the demand-supply mismatch

With a fleet mix of owned (42) and leased (58) aircraft Jet is able to capitalise on the demand-supply mismatch and earn additional revenues. Such flexibility gives Jet a strong competitive advantage in terms of its ability to withstand a downturn in the economy and also makes it best placed to capture a growth opportunity during times of revival or during festive seasons. Moreover, since 42 of the total 100 aircraft are owned while the remaining 58 are leased, Jet is able to generate the highest EBITDA margins in the industry as lease rentals are low.

The company sub- leased 4 aircraft (Boeing 777’s) to Turkish Airlines for a period of 25 months in CY09 and subleased 3 aircraft to Thai Airways for a period of 36 months in CY10. This has been an additional source of revenue for the company over the last three years with the company earning `1.8 bn in FY09, `7.2 bn in FY10 and `5.2 bn in FY11. Hence due to presence of owned fleet the company was able to reduce the downturn effect with revenues straight away positively impacting the EBITDA. We expect this feature of Jet Airways to be one of its strongest edges over competitors and make it best poised in times of industry slowdown.

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 20

Focus on international segment – key driver for profitability

Jet started its international operations in FY05 and since then has seen a stark improvement in its financials and operations. The International division has seen a successful turnaround from being loss making until FY08 (EBITDA level). It turned EBITDA positive in FY09, EBIT positive in FY10 and PBT positive in FY11. With a 3.5 times increase in market share in last five years (10% in FY06 to 36% in FY11).

Jet Airways is currently the second largest international operator in India. The company’s international business accounts for 46% of its consolidated passenger revenues in FY11 and 57% of its consolidated ASKM. With a strong presence in the international business the company has been able to aid growth of the domestic traffic as well due to synergies like a) the international passengers acting as a ready customer base to its domestic segment, b) creating a diversified passenger traffic leading to demand throughout the year, and c) stability of its business model.

Passenger revenue mix in FY11 ASKM mix in FY11 International,

46

Domestic, 40

JetLite, 14

International,

57

Domestic, 29

JetLite, 14

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Synergies of International travel

The average ticket costs on international routes are nearly 20% higher than on domestic routes, for the same distance travelled, due to the lack of severe competition, leading to pricing power for international route operators. Moreover, Fuel cost, which accounts for 40-45% of revenue, is 25-30% cheaper on international soil (due to low government taxes) which leads to higher margins. To add to this, the international business reduces the cyclicality in demand as the lean season in India of July-Oct ends up being a strong season for the international markets and a lean season for the international market of Apr-July is a strong demand season for domestic travel.

Such synergies have ensured that the profitability of international operations remains significantly higher than domestic business. The EBITDAR margins too for the international business in FY11 were 24% as compared to 15% in the domestic business.

We expect the international business passenger revenue and EBITDAR to record 17.3% and 11.2% CAGR respectively in FY11-14E led by 12% CAGR in RPKM, 7.3% CAGR in passenger yields and 21.7% CAGR in fuel cost over the next three years.

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 21

International ASKM, RPKM and PLF International passenger revenues and revenue per RPKM

80.080.0

80.380.4

80.4

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

FY10

FY11

FY12

E

FY13

E

FY14

E

bn

79.7

79.8

79.9

80.0

80.1

80.2

80.3

80.4

80.5

%

ASKM RPKM PLF

2.8

2.9

3.1

3.3

3.6

0.0

20.0

40.0

60.0

80.0

100.0

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

2.5

2.7

2.9

3.1

3.3

3.5

3.7

Rs

Revenues Revenue per RPKM

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

International cost per ASKM (with and without fuel) International EBITDAR and EBITDAR margin

2.582.72

2.98 2.92 3.01

1.51 1.57 1.46 1.45 1.54

1.00

1.50

2.00

2.50

3.00

3.50

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

Cost per ASKM (with fuel)

Cost per ASKM (without fuel)

27.1

24.0

12.8

17.6

19.3

10

12

14

16

18

20

22

24

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

%

EBITDAR EBITDAR margin Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 22

Improving domestic business and merger of Jetlite and Jet Konnect

Due to the strong brand image of Jet Airways, operational synergies, a flexible and unique business model, and a strong growth in passenger traffic, the domestic business of Jet Airways has witnessed a sharp improvement in operations.

The improvement in operations is clearly highlighted by the rise in PLF to 75.1% in FY11 as compared to 71.6% in FY10 even as the ASKM rose by 17.5% in FY11. Even in Q2FY12 the domestic business has seen load factors rise to 72.1% from 71.4% in Q2FY11 as the ASKM grew by 7% Y-o-Y. In fact the yields have also seen a rise in the current fiscal with revenue/RPKM rising by 10% in Q1FY12 and 1% Q2FY12. The operational efficiencies have resulted in a better financial standing with the EBITDAR margins having improved from 15% in FY10 to 18% in FY11 and an EBITDA margins rising to of 7.8% in FY11 as compared to EBITDA margin of 3% in FY10 and an EBITDA loss in FY09.

Quarterly domestic PLF Quarterly domestic yields

73

77.5

64.5 67

.3 69.7

75.4

72.174

.6 76.9

71.4

79.1

72.9

60

65

70

75

80

85

Jan-

Mar

Apr

-Jun

July

-Spe

t

Oct

-Dec

%

CY11 CY10 CY09

5.3

5.96.

2

5.7

4.5

5.45.

6

4.9

5.5

5.1

4.8

5.7

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Jan-

Mar

Apr

-Jun

July

-Spe

t

Oct

-Dec

Rs

CY11 CY10 CY09

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

The company also plans to add 17 Boeing 737-800 to its existing fleet over the next one and a half year, a move that should help to increase its domestic capacity and capture a greater share of the demand supply mismatch present in the domestic aviation industry in India.

Given the company’s track record of bucking the trend, withstanding downtrends and turning around faster than the industry pace, we expect the domestic business passenger revenue and EBITDAR to record 15.9% and -7.9% CAGR respectively in FY11-14E led by 10.7% CAGR in RPKM, 4.8% CAGR in passenger yields and 24.2% CAGR in fuel cost over the next three years.

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 23

Domestic ASKM, RPKM and PLF Domestic passenger revenues and revenue per RPKM

71.6

75.1

74.2

75.0 75.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY10

FY11

FY12

E

FY13

E

FY14

E

bn

69.0

70.0

71.0

72.0

73.0

74.0

75.0

76.0

%

ASKM RPKM PLF

5.3 5.2

5.4

5.7

6.0

10

20

30

40

50

60

70

80

90

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

4.8

5.0

5.2

5.4

5.6

5.8

6.0

6.2

Rs

Revenues Revenue per RPKM Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Domestic cost per ASKM (with and without fuel) Domestic EBITDAR and EBITDAR margin

4.26 4.294.56 4.66 4.77

2.972.78

2.55 2.53 2.64

2.00

2.50

3.00

3.50

4.00

4.50

5.00

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

Cost per ASKM (with fuel)

Cost per ASKM (without fuel)

13.1

15.4

3.35.5

8.0

0

1

2

3

4

5

6

7

8

9

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

%

EBITDAR EBITDAR margin Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 24

Merger of JetLite and Jet Konnect to boost LCC segment growth

JetLite was formed with the acquisition of Air Sahara by Jet Airways for a sum of US$340 mn in FY08, with a fleet of 26 aircraft. Jet positioned this new subsidiary as a LCC and has been working on various integrated measures to improve its efficiency. The company has been closely working towards operational efficiency and has reduced the fleet size to 19 which has resulted in a mere 1% CAGR reduction in ASKM since its acquisition.

The company has successfully managed to improve its operational efficiency over the years with a rise in block hours per aircraft and in passengers carried despite the reduction in ASKM. This has helped improve efficiencies and reduce costs. With refurbished seats and better food, the preference for the airline has increased and the 9W code has been put on all Jet Lite aircraft to enable it to sell its seats through the GDS system, helping it to achieve ~25% of its traffic from the company’s international network. Consequently, JetLite has witnessed revenue CAGR of 4.6% in FY09-FY11 with EBITDAR profit of `2.2 bn each in FY10 and FY11. The EBITDA loss has also reduced to `762 mn in FY11 as compared to an EBITDA loss of `1.01 bn in FY10 as a result of the cost per ASKM falling to `1.65 in FY11 from `1.67 in FY10.

Quarterly block hours per aircraft per day Quarterly revenue passengers

10.8 11

.6

9.0

8.9

11.7

10.6

11.8

11.6

11.0

8.8

8.6

10.6

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

Jan-

Mar

Apr

-Jun

July

-Spe

t

Oct

-Dec

%

CY11 CY10 CY09

1.15 1.

2

0.8 0.

9

0.9

1.0

1.2

1.19

0.89

1.11

0.95

1.12

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

Jan-

Mar

Apr

-Jun

July

-Spe

t

Oct

-Dec

Rs

CY11 CY10 CY09

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

The company plans to merge its two LCC JetLite and Jet Konnect and operate under the brand name of the latter. The move to arrest losses and compete with other low-cost airlines had been in the management's mind for some time, but the decision has been taken now. Though no formal date has been announced regarding the re-branding exercise we expect the move to be positive for the company. The higher brand perception for Jet Konnect as compared to JetLite, higher operating efficiencies by the former, tie-up synergies and improved connectivity are some of the benefits that the company would witness with the re-branding and merger of JetLite.

We expect the revenues to witness 10.0% CAGR in FY11-13E driven by 4.2% CAGR in RPKM and a 5.8% CAGR In passenger yields in the same period. However, with a rise in fuel cost of 15.4% CAGR in the same period we expect the profitability of this division to remain under pressure and we expect the EBITDAR to witness 0.9% CAGR decline in FY11-FY14E.

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 25

JetLite ASKM, RPKM and PLF JetLite passenger revenues and revenue per RPKM

75.0

79.2

77.6 78.077.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

FY10

FY11

FY12

E

FY13

E

FY14

E

bn

72.0

73.0

74.0

75.0

76.0

77.0

78.0

79.0

80.0

%

ASKM RPKM PLF

3.63.7

4.1 4.3 4.4

10

12

14

16

18

20

22

24

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Rs

Revenues Revenue per RPKM

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

JetLite cost per ASKM (with and without fuel) JetLite EBITDAR and EBITDAR margin

2.93.1

3.7 3.8 3.8

1.7 1.6 1.8 1.9 1.9

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

Cost per ASKM (with fuel)

Cost per ASKM (without fuel)

14.912.8

8.79.4

1.6

0.0

0.5

1.0

1.5

2.0

2.5

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

%

EBITDAR margin EBITDA margin

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 26

Balance sheet concerns overdone

India's airlines are reeling under a US$20 bn debt load and struggling to make profits. The debt picture of Kingfisher is already making waves with a current debt of ~`89 bn. Investors are thus concerned with the high debt of Jet which stands at ~`133 bn. However, Jet’s debt consists of ~`76 bn of long-term debt related to aircraft acquisition which accounts for 57% of the total debt. Moreover, the company has managed to lower its debt even in the past.

Jet’s debt surged to `166 bn in FY09 after witnessing a severe cash-flow crunch during the downturn FY08-09. However the company was able to reduce the debt by `30 bn over the next two years due to a series of initiatives which included

a) Sale and leaseback of aircraft: Jet recognized `4.9 bn on sale and lease back of aircraft in FY08-09 which reduced its cash crunch burden.

b) Refinancing of high-cost debt: Jet refinanced its long-term debt related to aircraft acquisition of `90 bn (66% of total). The company also refinanced `25 bn of its remaining ~`47 bn loan in to dollar terms at a significantly lower interest rate of 6.5% (compared to 12 5% in the case of rupee loans). This resulted in savings of interest outflow.

c) Monetising Bandra-Kurla Complex (BKC) land: Jet signed a preliminary agreement with Godrej properties to jointly develop its BKC land. The deal entailed a) an upfront payment of `5 bn (`3.6 bn for debt repayment and `1.4 bn for cost already incurred), b) development of 1.6 mn sq ft (msf) of office space, with complete ownership of 0.25 msf given to the company, and c) a 50:50 share of the profits from the land developed.

Such steps helped reduce the debt position of Jet. Over the next three years we expect the following debt reduction measures from the company

a) Sale and leaseback of aircraft: The Company can earn `8-10 mn per aircraft through this route as the rate of depreciation charged is 5% which the diminishing value is ~2.5%. With an owned fleet of 40 aircraft the company can earn good profits from such transactions and is looking at this route to reduce its debt position over the next two years

b) Repayment of high-cost debt: The average rate of interest on long-term debt is ~4% and has a repayment obligation of `10 bn per annum. Moreover, any further conversion of the rupee denominated debt to dollar terms can be beneficial can be beneficial to the company as the latter a lower rate of interest.

c) Monetising Bandra-Kurla Complex (BKC) land: The jointly develop BKC land should result in a 50:50 share of the profits from the development of the land. However we have not factored this deal into our estimates and any positive news could result in further potential upside.

d) Equity dilution: The Company has received clearance from the Cabinet Committee on Economic Affairs (CCEA) to raise US$400 mn (`18.5 bn) from foreign investors through Qualified Institutional Placement (QIP). However, given the current market conditions we do not expect the company to dilute equity

Given the various debt reduction measures and the annual repayment schedule for the aircraft related debt, we expect the total debt to decline by `20 bn till FY14E to `116.8 bn. This should help improve the interest coverage ratio from 1.4x in FY11 to 0.7x in FY14E

With a 5.1% CAGR decline in total debt in FY11-14E, we expect the interest outflow to witness a 12.4% CAGR decline and reduce to `8.8 bn in FY14E from `10.9 bn in FY11. This should help improve the EBITDA to interest ratio to 1.9x in FY14E from 1.45x in FY11.

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 27

Gross and Net Debt Cash flow from operations

142.8 136.8 132.8126.8

116.8

134.5 130.0 129.2 119.6 108.4

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0FY

10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

Debt Net debt

5.3

143.9

1.8

(326.9)

(47.3)

0.0

40.0

80.0

120.0

160.0

200.0

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

(400.0)

(300.0)

(200.0)

(100.0)

0.0

100.0

200.0

%

Cash flow from operations Y-o-Y growth

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Interest outflow EBITDA/Interest ratio

30.6

3.7

(4.5)(7.9)

(8.3)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

(20.0)

(10.0)

0.0

10.0

20.0

30.0

40.0

%

Interest outflow Y-o-Y growth

1.16

1.45

0.10

1.19

1.93

0.00

0.50

1.00

1.50

2.00

2.50

FY10 FY11 FY12E FY13E FY14E

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 28

Financial overview

Revenues to witness a 15.6% CAGR in FY11-FY14E

We expect 15.6% CAGR in revenue in FY11-FY14E to `224.5 bn, driven by 10.6% CAGR in RPKM from 31.3 bn in FY11 to 42.4 bn in FY14E and 3.6% CAGR in passenger yield (revenue/RPKM), from `3.9 in FY11 to `4.3 in FY14E.

We expect the ASKM to witness a 10.9% CAGR in FY11-FY14E driven by 8.4% CAGR in seat capacity as the number of aircraft is expected to rise from 119 in FY11 to 130 in FY14E with the addition of Boeing 737s. We expect a marginal 50bps decline in the Passenger Load Factors (PLF), with lower than industry seat addition. However, given the strong demand for its LCC and international business, we expect the blended PLF to remain above 75% over the next two years.

We expect the company to maintain its focus on the international business with the addition of fresh fleet (8-10 in the next two years) which should lead to a 12.2% CAGR in ASKM from FY11-14E to 32.1 bn and load factors above 80%. This led by a 7.3% CAGR in passenger yields should result in international revenues witnessing 17.3% CAGR in FY11-14E to `119.4 bn. Consequently the share of international revenues is expected to rise from 51% in FY11 to 54% in FY14E.

ASKM, RPKM and PLF Revenue and Revenue per RPKM

78.7

78.178.3

77.1

78.2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

FY10

FY11

FY12

E

FY13

E

FY14

E

bn

76.0

76.5

77.0

77.5

78.0

78.5

79.0

%

ASKM RPKM PLF

3.93.8

4.1

3.8

4.3

0.0

50.0

100.0

150.0

200.0

250.0

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

bn

3.4

3.6

3.8

4.0

4.2

4.4

Rs

Revenues Revenue per RPKM Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Higher ATF prices to impact cost structure

ATF prices have seen a sharp surge over the last one year. Led by the Middle East crisis ATF prices have surged by 62% since Oct’10. Post an improvement in the scenario as well, ATF prices have refused to decline and with the falling rupee and stubborn Brent crude prices, ATF prices have risen by 332% in CY11 and 13% in CY12.

The cost structure of airlines, which operate on thin margins have hence gone for a toss given the fact that fuel costs account for over 50% of the total costs. With the surge, airlines across India are finding it difficult to break-even on an operational basis. This is visible in the cost structure where by the ASKM with fuel has risen from `2.85 in Q1FY11 to `3.63 in Q3FY12

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 29

ATF prices Cost per ASKM (with and without fuel)

40.7

48.8

54.9

60.6

66.165.064.6

56.258.6

44.6

62.7

40.0

45.0

50.0

55.0

60.0

65.0

70.0

Oct

-10

Nov

-10

Dec-

10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-

11

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Dec-

11

Jan-

12

Feb-

12

Mar

-12

Rs/l

itre

3.14 3.253.74 3.73 3.83

2.05 1.96 2.02 2.01 2.11

0.00

1.00

2.00

3.00

4.00

5.00

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

Cost per ASKM (with fuel)

Cost per ASKM (without fuel) Source: HPCL, BPCL, GEPL Capital Research Source: Company data, GEPL Capital Research

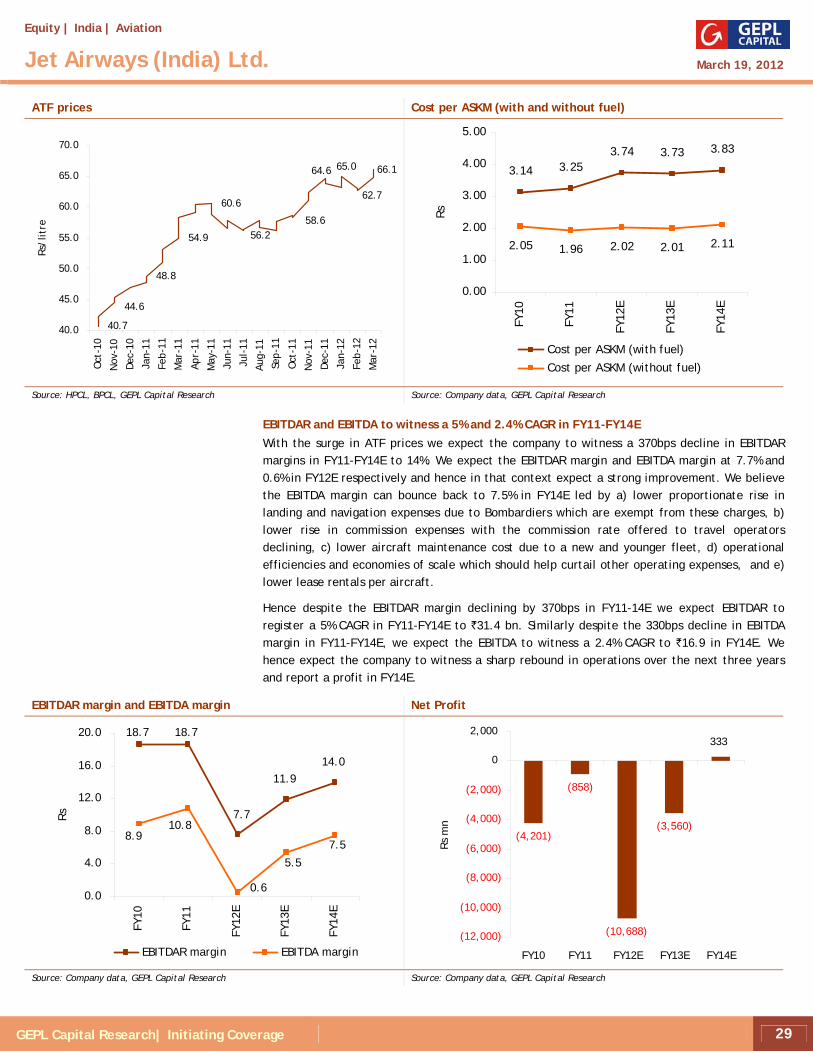

EBITDAR and EBITDA to witness a 5% and 2.4% CAGR in FY11-FY14E With the surge in ATF prices we expect the company to witness a 370bps decline in EBITDAR margins in FY11-FY14E to 14%. We expect the EBITDAR margin and EBITDA margin at 7.7% and 0.6% in FY12E respectively and hence in that context expect a strong improvement. We believe the EBITDA margin can bounce back to 7.5% in FY14E led by a) lower proportionate rise in landing and navigation expenses due to Bombardiers which are exempt from these charges, b) lower rise in commission expenses with the commission rate offered to travel operators declining, c) lower aircraft maintenance cost due to a new and younger fleet, d) operational efficiencies and economies of scale which should help curtail other operating expenses, and e) lower lease rentals per aircraft.

Hence despite the EBITDAR margin declining by 370bps in FY11-14E we expect EBITDAR to register a 5% CAGR in FY11-FY14E to `31.4 bn. Similarly despite the 330bps decline in EBITDA margin in FY11-FY14E, we expect the EBITDA to witness a 2.4% CAGR to `16.9 in FY14E. We hence expect the company to witness a sharp rebound in operations over the next three years and report a profit in FY14E.

EBITDAR margin and EBITDA margin Net Profit

18.7 18.7

11.914.0

7.7

8.9

0.6

5.5

7.5

10.8

0.0

4.0

8.0

12.0

16.0

20.0

FY10

FY11

FY12

E

FY13

E

FY14

E

Rs

EBITDAR margin EBITDA margin

(4,201)

(858)

(10,688)

(3,560)

333

(12,000)

(10,000)

(8,000)

(6,000)

(4,000)

(2,000)

0

2,000

FY10 FY11 FY12E FY13E FY14E

Rs

mn

Source: Company data, GEPL Capital Research Source: Company data, GEPL Capital Research

Equity | India | Aviation

Jet Airways (India) Ltd. March 19, 2012

GEPL Capital Research| Initiating Coverage 30

Key Risks

• Fuel costs beyond airlines’ control Aviation turbine fuel (ATF) prices account for 40-45% of an airline’s total revenues. A sharp increase in the ATF prices have dented margins and led to losses across the industry. Any further price rise could result in a significant net loss and hence erosion of net worth for the company.

• Change in landing and navigation charge regulations