automotive thermoplastic composites . . . industry ... · pdf fileanalysis m a r k e t e c o n...

TRANSCRIPT

Robert Eller Associates LLC 11

AUTOMOTIVE THERMOPLASTIC COMPOSITES . . .INDUSTRY STRUCTURE AND NEW TECHNOLOGIES

RESPOND TO A GLOBAL RECESSION

ManagementDECISIONS

ANALYSIS

MA

RK

ET

ECO

NO

MIC

TECH

NIC

AL

Robert Eller Associates LLCCONSULTANTS TO THE PLASTICS AND RUBBER INDUSTRIES

PRESENTED BY:

Bob EllerRobert Eller Associates LLCPhone: 001-330-670-9566E-mail: [email protected] site: www.robertellerassoc.com

PREPARED FOR:

SPE AUTOMOTIVE COMPOSITES CONFERENCEDETROIT, MI

SEPTEMBER 15, 2009b/mydox/papers/composites 09.ppt

Robert Eller Associates LLC 22

• Robert Eller Associates LLC is a global plastics con sulting company providing analysis in support of technical, marketing, and economic strategic management decision-making

• Based in Akron, Ohio, with offices in Paris, Shanghai , New Zealand• Asia: Active in China, India, Middle East • Key Focus Areas: Thermoplastic Composites, TPEs, ETP s,

Polyolefins, Automotive, Compounding, and Foams • Multiclient studies:

– China TPE Market– North America/Europe TPE Market

• Single-client decision support analyses • Mergers and Acquisitions:

– Complete management service for small acquisitions– Due diligence support– Technical advisors

Robert Eller Associates LLC

PRESENTATION OUTLINE

• Global Macroeconomic Situation/Automotive Impacts

• Automotive Supply Chain Responses

• Thermoplastic (TP) Composites(a) in the Automotive Market

• Paths to the TP Composite Market

• TP Composite Technology Responses and Opportunities

• Future Vision/Summary

Notes: See abbreviations in Appendix (a) Focus on long fiber reinforced thermoplastics

(LF-RTP)

3

Robert Eller Associates LLC

THE FAMILIES OF AUTOMOTIVE THERMOPLASTIC COMPOSITES

AUTO TP COMPOSITES

MINERAL FILLED

(a)

LG. PARTICLE

MICRO(b)

NANO

CARBON

FIBERS

NANO TUBES

SHORT GLASS (SGF)

GLASS REINFORCED BIOPOLYMERS AND NATURAL FIBER

GMT(s-GMT)

MATRIX FIBERS

NATURAL SYNTHETIC

LONGGLASS (LGF)

MAT(GMT)

Notes:(a) Talc, mica, basalt, etc.(b) Micro-talcs opening new applications (e.g., exte rior panels, hatchback

on Ford Kuga)

SOURCE: ROBERT ELLER ASSOCIATES LLC, 2009 r/mydox/papers/composites09.ppt

MAIN TARGET FOR THIS PRESENTATION LW-GMT

(LW-RT)

Robert Eller Associates LLC 5

MACROECONOMIC SITUATION/AUTOMOTIVE IMPACTS

Robert Eller Associates LLC 66

GLOBAL ECONOMIC GROWTH: 2 YEAR TROUGH

0

1

2

3

4

5

6

7

8

9

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

SOURCE: IMFb/mydox/rapra 2008/rapra 2008.xls

AN

N. %

CH

AN

GE

(A

T P

PP

)ADV. ECON.

EMERG. ECON.

WORLD

SOURCE: IMFB/mydox/papers/jec09.ppt

?

Robert Eller Associates LLC 7

• Global GDP slowdown – 2-year trough in West • Slowed (but continued high) growth in Asia (esp. Ch ina) • Auto overcapacity in West: Europe/U.S. have 53% of

global auto capacity; 12% of global population • Petrodollar export concerns:

- substantial alternative energy investments (esp. battery/electric drive programs)

- CAFE rise in U.S. (still lagging other major natio ns)• Wage deflation/high unemployment• Cash for Clunkers stimulated Europe market (2010

impact?)• Credit lockdown (despite U.S. stimulus) ���� erosion of

consumer purchasing power• OEM market share shift (especially in N. America)

MACROECONOMIC IMPACTS ON GLOBAL AUTO MARKETS

Robert Eller Associates LLC

GLOBAL VEHICLE PRODUCTION DECLINE

8

GLOBAL VEHICLE SALES OUTLOOK

0

10

20

30

40

50

60

70

80

90

1975 1980 1985 1990 1995 2000 2005 2010 2012 2014

SOURCE: ROBERT ELLER ASSOCIATES LLC, 2009r/mydox/Auto Industry/Global Ind Volume.xls

VE

HIC

LE S

ALE

S, M

M U

NIT

S

Annual Growth1990-2000 2.3%2000-2006 2.8%2006-2014 2.2%

2007: 71

2000: 57

2014: 83?

FIRST EVER DECLINE?

(2008/9)

42% IN 15 EMERGING MARKETS; 58% IN EUROPE/U.S./JAPA N

Robert Eller Associates LLC 9

U.S. LIGHT VEHICLE SALES

0

2

4

6

8

10

12

14

16

18

20

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

SOURCE: DEUTSCHE BANK, 2009 b/mydox/auto industry/NA and EUR sales.xls

SA

LES

, M

M U

NIT

S

Robert Eller Associates LLC 10

EUROPE LIGHT VEHICLE SALES

0

2

4

6

8

10

12

14

16

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

SOURCE: DEUTSCHE BANK, 2009 B/mydox/auto industry/NA and EUR sales.xls

SA

LES

, M

M U

NIT

S

Robert Eller Associates LLC 1111

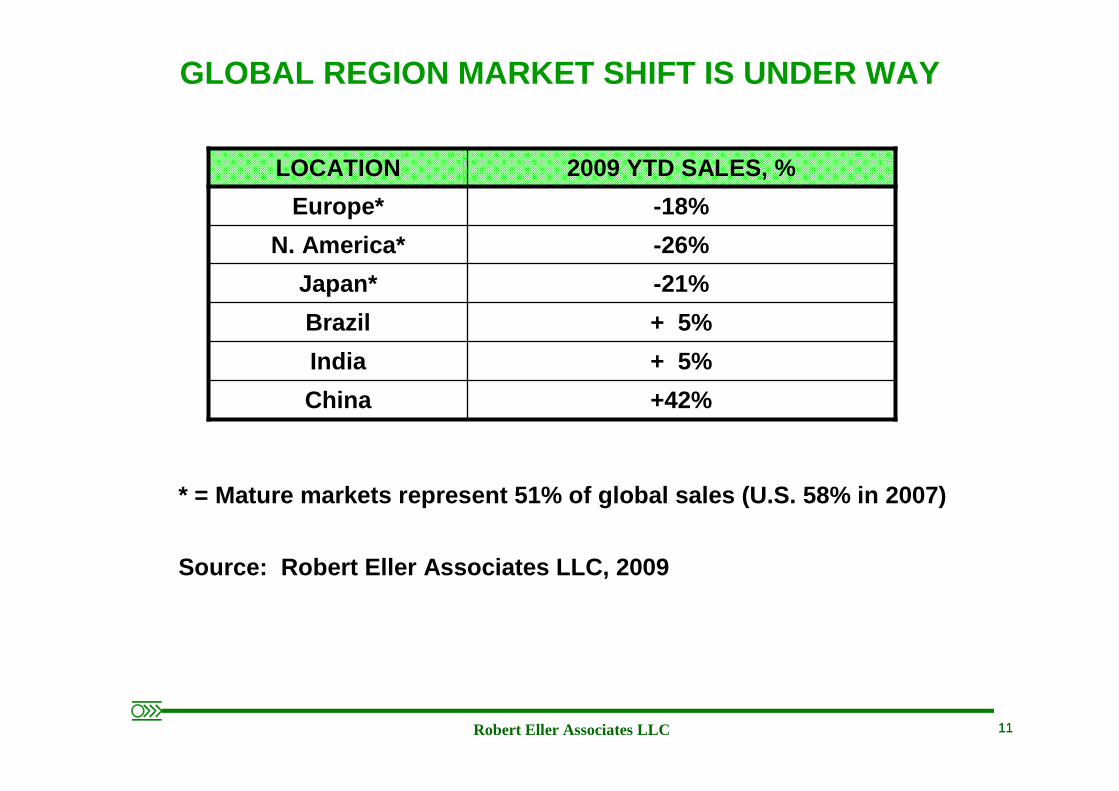

GLOBAL REGION MARKET SHIFT IS UNDER WAY

-18%Europe*

-26%N. America*

-21%Japan*

+ 5%Brazil

+42%China

+ 5%India

2009 YTD SALES, %LOCATION

* = Mature markets represent 51% of global sales (U .S. 58% in 2007)

Source: Robert Eller Associates LLC, 2009

Robert Eller Associates LLC 1212

W. EUROPEAN VEHICLE MARKET SHARE SHIFT

0

10

20

30

40

50

60

A/B C/D

FLEET MARKET SEGMENTb/mydox/ jec 09/euro mix shif t .xls

SA

LES

SH

AR

E,

%

20052009(EST)

Sources: JD Power; Deutsche Bank; Robert Eller Ass oc. LLC, 2009

Sales Shift Toward Smaller Vehicles

• Lower discretionary spending

• Lower residual values• Gov't. incentives favor

smaller cars/hybrids• European/Asian design

imports to U.S.• Probable fuel price

increases

• OEM profitability impact (less profitable product mix)• Intensified weight savings pressure • Increased penetration of TP composites

Robert Eller Associates LLC 1313

U.S. FUEL ECONOMY OBJECTIVES: MINIMAL, BUT WITH SIGNIFICANT FLEET MIX & MATERIALS SELECTION IMPLICA TIONS

AVERAGE FLEET FUEL ECONOMY BY GLOBAL REGION

0

10

20

30

40

50

60

2002 2006 2010 2014 2020

SOURCE: PEW CENTER, 2008b/mydox/papers/RAPRA TPE 08-AvgFleetFuelEcon 08.xls

MP

G

JAPAN

EU

CHINA

AUSTRALIA

USU.S. CAFE LAG CONTINUES

SOURCE: PEW CENTER, 2008

HIGHER CAFE DRIVES COMPOSITES TECH.

Robert Eller Associates LLC 1414

• 2008: $3.50-4.00/gal. ���� 100BN fewer miles driven• Tipping points ���� shifts in vehicle preference • Price will rise and change auto and autoplastics

paradigms: - rising demand/decreasing capacity- economic expansion (eventually)- global population jump by 1.0BN in next 12 years- “middle” class increase by 1.8BN (600MM in China) - U.S.: 750 cars/1,000 peopleChina: 4 cars/1,000 people – If Chinese ���� ½ownership rate of the U.S., adds 400MM cars

- easy-to-get oil has gotten harder to find- gas taxes (remain constant at $0.184/gal.?)

• Plug-in hybrids: emerging, bridge to a (composite intensive) electric car/alternative propulsion worl d

• At $?/gal.: Bioplastics and natural fibers reach pr ice equality with petro-based plastics

FUEL PRICES: THERMOPLASTIC COMPOSITE EFFECTS

Robert Eller Associates LLC 15

AUTOMOTIVE SUPPLY CHAIN RESPONSES

Robert Eller Associates LLC 1616

U.S. AUTOPLASTIC SUPPLY CHAIN PRESSURES/RESPONSES

GLOBALCOMPETITION

OFFSHORECOMPOUNDERS

ENTER

IMPORTEDCOMPETITORS/

SUPPLIERREDUCTION

OEM AGGRESSIVE SUPPLYCHAIN COST SAVE

PRESSURES

TECHNOLOGYTRANSFER

PRICECOMMODITIZATION

ELIMINATION OFEXTRA STEPS

U.S. TPCOMPOSITESTECHNOLOGY

LAG vs. EUROPE

RAW MATERIALS COMPOUNDER TIER 1 FABRICATOR OEM ASSEMBLY

TIER 2, 3SUPPLIERS

OEM OWNERSHIPSHIFT(b)

BANKRUPTCIES

SUPPLY CHAIN GLOBALIZATION

GLOBAL VEHICLE DESIGNS

VEHICLE DEMAND SLOWDOWN

SPECIFICATIONS

GLOBALIZATION PRESSURES

INCREASED EUROPEAN/JAPANESE INFLUENCE

- MULTIPLE UNIT OPERATIONS- EXCESSIVE LOGISTICS- SCRAP GENERATION

SOURCE: ROBERT ELLER ASSOCIATES LLC, 2009r/mydox/papers/Comp09-Implosion 071309.vsd // lg/myfiles/visio/Comp09-Implosion 071309.vsd

PRESSURES PASSED DOWN THE SUPPLY CHAIN

NOTES:(a) STARTED FOR LGF-TPs(b) e.g., MAGNA, BID FOR OPEL, FIAT/CHRYSLER, ETC.

- RESIN SUPPLIER SHIFT TO LOW COST MONOMER REGIONS- REDUCED SERVICE FOR AUTO ACCOUNTS

IN-LINE (D-LFT)COMP'DG. BY

TIER 1s(a)

TRANS-GLOBAL OEMPARTNERING

SHIFT TOEUROPEAN/

ASIANDESIGNS

SHIFT TOSMALLERVEHICLES

SEVEREPRODUCTION

DECLINE

- INEFFICIENT PROCESS TECHNOLOGIES- SALES/MARKETING COSTS- EXCESS LABOR COSTS

ELIMINATE/REDUCE THE INEFFICIENCIES:

BANKRUPTCIES

HYBRID ELECTRICDRIVE SHIFT

Robert Eller Associates LLC 1717

N. AMERICAN AUTOPLASTIC TIER 1s SERVE MULTIPLE OEMs - BANKRUPTCY CAN HAVE INDUSTRY-WIDE IMPLICATIONS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Lear Magna TRW JCI

Source: Company Filingsr/mydox/papers/Comp09-Tier1sOEMs 09.xls

RE

VE

NU

E S

HA

RE BMW

VW

Chrysler

Ford

GM

Other

Robert Eller Associates LLC 18

THE AUTOMOTIVE MARKETand

THERMOPLASTIC (TP) COMPOSITES

Robert Eller Associates LLC 1919

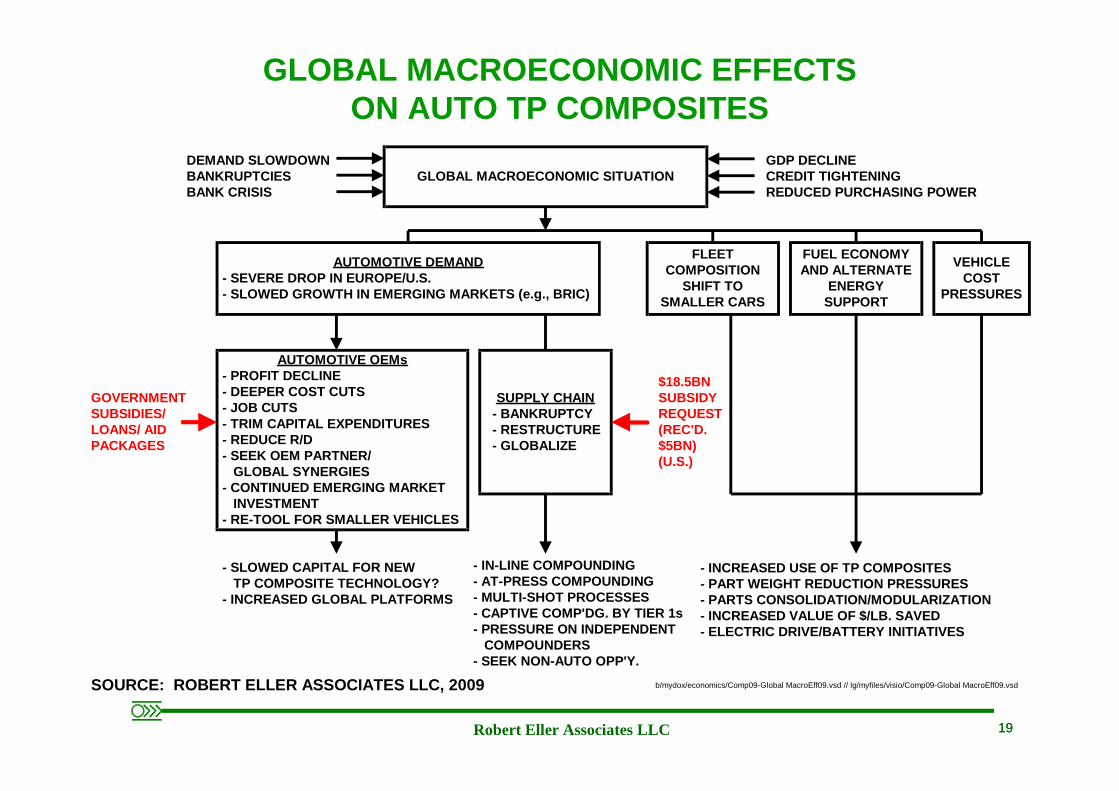

GLOBAL MACROECONOMIC EFFECTS ON AUTO TP COMPOSITES

b/mydox/economics/Comp09-Global MacroEff09.vsd // lg/myfiles/visio/Comp09-Global MacroEff09.vsd

- SLOWED CAPITAL FOR NEW TP COMPOSITE TECHNOLOGY?- INCREASED GLOBAL PLATFORMS

GLOBAL MACROECONOMIC SITUATIONDEMAND SLOWDOWNBANKRUPTCIESBANK CRISIS

AUTOMOTIVE DEMAND- SEVERE DROP IN EUROPE/U.S.- SLOWED GROWTH IN EMERGING MARKETS (e.g., BRIC)

AUTOMOTIVE OEMs- PROFIT DECLINE- DEEPER COST CUTS- JOB CUTS- TRIM CAPITAL EXPENDITURES- REDUCE R/D- SEEK OEM PARTNER/ GLOBAL SYNERGIES- CONTINUED EMERGING MARKET INVESTMENT- RE-TOOL FOR SMALLER VEHICLES

GOVERNMENTSUBSIDIES/LOANS/ AIDPACKAGES

FLEETCOMPOSITION

SHIFT TOSMALLER CARS

FUEL ECONOMYAND ALTERNATE

ENERGYSUPPORT

VEHICLECOST

PRESSURES

SUPPLY CHAIN - BANKRUPTCY - RESTRUCTURE - GLOBALIZE

- IN-LINE COMPOUNDING- AT-PRESS COMPOUNDING- MULTI-SHOT PROCESSES- CAPTIVE COMP'DG. BY TIER 1s- PRESSURE ON INDEPENDENT COMPOUNDERS- SEEK NON-AUTO OPP'Y.

- INCREASED USE OF TP COMPOSITES- PART WEIGHT REDUCTION PRESSURES- PARTS CONSOLIDATION/MODULARIZATION- INCREASED VALUE OF $/LB. SAVED- ELECTRIC DRIVE/BATTERY INITIATIVES

SOURCE: ROBERT ELLER ASSOCIATES LLC, 2009

$18.5BNSUBSIDYREQUEST(REC'D.$5BN)(U.S.)

GDP DECLINECREDIT TIGHTENINGREDUCED PURCHASING POWER

Robert Eller Associates LLC 20

TP composite substitution driven by:

• Supply chain restructuring

• Weight save pressures (value weight savings [10% weight reduction yields 7% fuel economy improvement])

• System cost savings potential/parts consolidation

• Material cost savings for D-LFT vs. other LGF processes

• Green pressures and improved capabilities for natural fiber composites

• Other plastic substitution (e.g., exteriors) stimul ates TP composites (e.g., hatchback inner panel)

AUTOMOTIVE MARKET DYNAMICS AND TP COMPOSITE SUPPLY CHAIN RESPONSES

Robert Eller Associates LLC 21

TP COMPOSITE TECHNOLOGY RESPONSES and OPPORTUNITIES

Robert Eller Associates LLC

PATHS TO THE LGF-TP COMPOSITE MARKET

SOURCE: ROBERT ELLER ASSOCIATES LLC, 2009

1. COMPOUND:

COMPOUNDER INJECTION PRESS

IN-LINECOMPOUNDING

EXTRUDER

IN-LINECOMPOUNDING

EXTRUDER

COMPRESSIONPRESS

INJECTION PRESS

INJECTION PRESS

2. D-LFT:

3. LGF CONCENTRATE:

LGF COMPOUND MOLDED PART

ROVING

RESIN

ADDITIVES

MOLDED PART

CONCENTRATE

NEAT RESIN

MOLDED PART

4. GMT OR LW-RT:ROVING

MAT

NEAT RESIN

EXTRUDER PREHEATBLANKS MOLDED PARTCOMPRESSION

PRESS

r/mydox/papers/Comp09-LGFTP Comp Mkt 071309 // lg/myfiles/visio/Comp09-LGFTP Comp Mkt 071309

COMPOUNDING FACILITATED EARLY GROWTH OF LGF-TPs; DO ES NOT REQUIRE CAPEX

HIGH GROWTH POTENTIAL; CAPEX REQUIRED (FAVORED BY M AJOR TIER 1s); LARGE PARTS, HIGH VOLUME REQUIRED FO RCOMPETITIVE ECONOMICS, GOOD FIBER LENGTH RETENTION

EARLY GMT BEING REPLACED BY HIGH QUALITY; LW-RT COM PETES WITH D-LFT IN UNDERBODY SHIELDS

USE EXISTING EQUIPMENT

Robert Eller Associates LLC 2323

INTERMATERIAL/INTERPROCESS COMPETITION IN LONG FIBE R, AUTOMOTIVE THERMOPLASTICS

D-LFT

Target Applications2008 N. America volume ~ 120MM lbs., excluding

S-GMT and LW-RT- Front end carrier- Door hardware module- Instrument panel substrate- Underbody shield- Running board- Hatchback door inner- Overhead console/Headliner structure- Instrument panel structural ducts- Load floor- Spare tire well/Storage module- Seating- Engine covers (start in natural fiber composite)- Lithium-ion battery related

S-GMT

LW-RT

LGF Compound

Concentrate

InjectionCompression

Note: Currently primarily glass; some shift to natural fibers

SOURCE: ROBERT ELLER ASSOCIATES LLC, 2009

Robert Eller Associates LLC 2424

AUTO APPLICATIONS FOR TP COMPOSITES(a)

- Facilitates strong trend towards hardware consolidation

- Brose is early leader

Door hardware module* (7-8)

- Stimulated by changes in overhead design and construction

Overhead console/ Headliner structure

- 2012 Ford Escape (see Ford Kuga photo) - Combination with talc/PP exterior

Hatchback door*

- Started in N. America Running board

-W ill come from Europe with OEM transplants - LW-RT competes with D-LFT - Add-on acoustic layer being offered

Underbody shield* (8)

- Started in Europe (Faurecia and JCI)- Both D-LFT injection and compression

Instrument panel substrate* (7)

- Major near-term D-LFT and LGF-PP pellet driver in N. American market

- Established in Europe

Front end module/ carrier* (6-8)

STATUS / NOTEAPPLICATION

(Cont’d.)

Robert Eller Associates LLC 2525

- Early Chrysler innovation (2007)- Requires vibration welding

Instrument panel structural ducts (15-18)

- Early GMT application Load floor

- Competes with SMC, GMT; natural fiber candidate?

Spare tire well/storage module* (9-10)

- Stimulated by trend to electric drive vehicles?Battery carriers

- Starting in natural fiber composites in EuropeEngine covers*

- Competes with SGF-TPs Seating*

STATUS / NOTEAPPLICATION

Notes:

Numbers in ( ) indicate typical weights per vehicle

* = technology transfer from Europe

(a) Includes both LFTs and GMTs

Sources: Dieffenbacher; Robert Eller Associates LL C

AUTO APPLICATIONS FOR TP COMPOSITES(a) (Cont’d.)

Robert Eller Associates LLC

Source: Dieffenbacher

LFT-D-ILC COMPRESSION

Fully automated material handling

Robert Eller Associates LLC

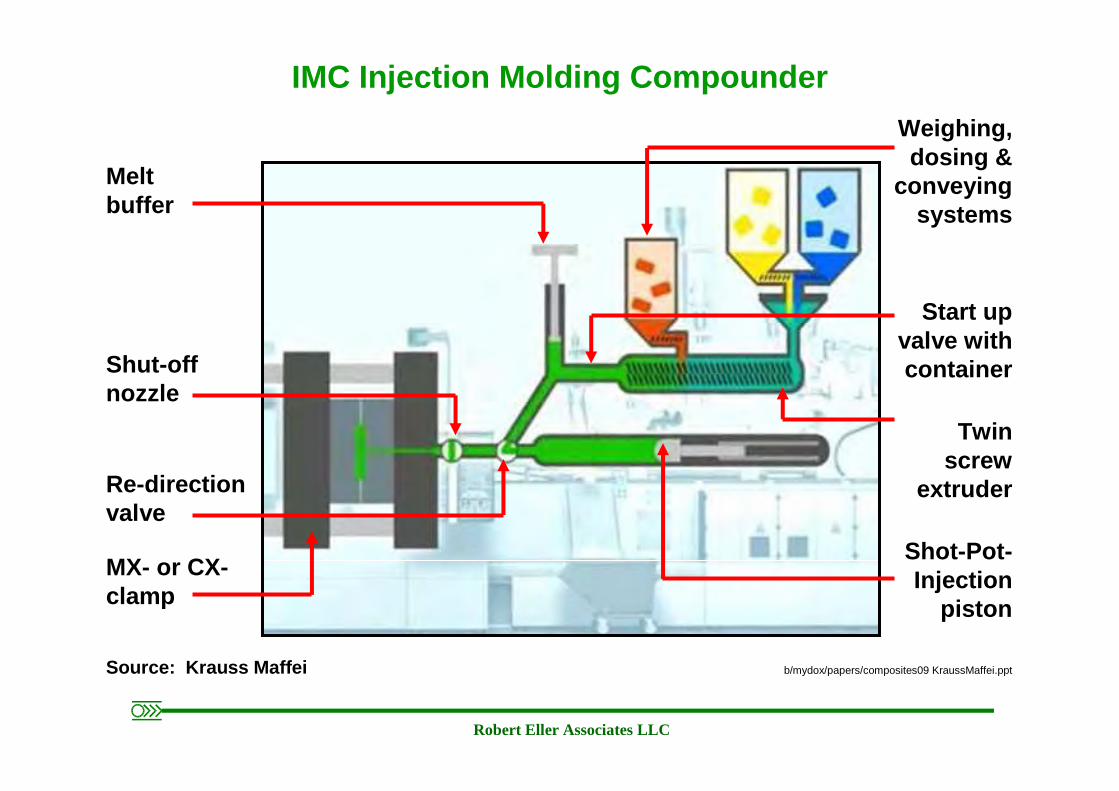

b/mydox/papers/composites09 KraussMaffei.ppt

Melt buffer

Shut-off nozzle

Re-direction valve

MX- or CX-clamp

Weighing, dosing &

conveying systems

Start up valve with container

Twin screw

extruder

Shot-Pot-Injection

piston

Source: Krauss Maffei

IMC Injection Molding Compounder

Robert Eller Associates LLC

Plasticomp Pushtrusion TM Direct In-Line Compounding

Source: PlastiComp

Robert Eller Associates LLC 2929

LFT COMPOSITE OPPORTUNITY TARGETS

SOURCE: ROBERT ELLER ASSOCIATES LLC, 2009

INSTRUMENT PANEL XCARBEAM SUBSTRATE

STRUCTURAL DUCTS SEAT STRUCTURE(b)

HEADLINER (LW-RT)(a) HATCHBACKDOOR INNER

FENDER

FLOOR MODULE/LOAD FLOOR/

SPARE TIRE CARRIER

BUMPERBEAM

BUMPERBEAM

r/mydox/papers/Compo09-LFT Comp Oppy 09.vsd // lg/myfiles/visio/Compo09-LFT Comp Oppy 09.vsd

DOOR HARDWAREMODULE

UNDER BODYSHIELDS(a)(c)

ENGINE THERMALCONTROL*

FRONT END MODULE/CARRIER

NOTES: = HIGH PERFORMANCE MINERAL FILLED(a) MAY CONTAIN ADDED ACOUSTIC ELEMENTS(b) COMPETES WITH SGF-TP(c) D-LFT AND LW-RT COMPETE FOR UNDERBODY SHIELD

HATCHBACKDOOR OUTER* *

*

OVERHEAD CONSOLE/HEADLINER STRUCTURE

Robert Eller Associates LLC 30

• Current methods for making instrument panels are inefficient:

• Multiple step process• Multi-materials vs. a single material • Difficulty of recycling• High scrap rate• High labor content• Use of coatings• Multiple step process• Multi-materials vs. a single material • Difficulty of recycling

• D-LFT (combined with 2-shot molding): • Saves unit operations • Improves recyclability • Will be growth trend • Can be from same materials family • Started in Europe; moving to the U.S.

EXAMPLE OF TP COMPOSITE TECHNOLOGY RESPONSES TO AUTOMOTIVE MARKETPLACE PARADIGM SHIFTS:

INSTRUMENT PANEL

Robert Eller Associates LLC 313131

•• FASCIAFASCIA

•• BUMPER BEAMBUMPER BEAM

•• ENERGY ABSORBERENERGY ABSORBER

•• CARRIERCARRIER

•• HOOD LATCH POINTHOOD LATCH POINT

•• RADIATOR/HEATRADIATOR/HEATEXCHANGERSEXCHANGERS

•• COOLING COOLING FANSFANS

FRONT END MODULES: PROVEN HIGH GROWTH TECH

SGF-PP CHALLENGING SGF-PA

Robert Eller Associates LLC 323232

VEHICLE: Audi A3MATERIAL: 30% LGF-PPPROCESS: D-LFT (injection)WEIGHT: 3 kgEQUIPMENT: Krauss MaffeiPHOTO: Krauss Maffei

FRONT END CARRIERS: STRONG GROWTH DRIVER FOR D-LFT PROCESSES AND LGF-PP COMPOUND

VEHICLE: Ford FusionMATERIAL: 40% LGF-PPPROCESS: D-LFT (compression)EQUIPMENT: DieffenbacherPHOTO: Dieffenbacher

Robert Eller Associates LLC 33

• Established in Europe. Shifting to N. America. (G erman OEM shift accelerates N.A. penetration)

• Substitution driven by:- Component protection - Lithium-ion battery/electric drive share gain- Improved aerodynamics- Acoustics improvement (new target/value add zone)

• Many process/materials contenders:- GMT - LW-RT (lightweight GMT gaining share, approvals in

place)- LGF-PP pellets- D-LFT processes/examples (Compression, Injection, Krauss Maffei, PlastiComp Pushtrusion TM, others)

- Aluminum, steel- Thermoset composites

UNDERBODY PANELS

Robert Eller Associates LLC 3434

UNDERBODY PANELS

Vehicle: BMW 7-SERIESPart: Underbody ShieldMaterial: 30% LGF-PPSupplier: SABIC - Stamax 30YK430Weight: 6.7 kg (total)Drivers: - Acoustics

- Aerodynamics- Component protection- Cost (vs. GMT)

Note: Most European BMW passenger cars have LW-RT UB shields

Robert Eller Associates LLC 3535

EXAMPLE UNDERBODY SHIELD

Part: Typical underbody shieldProcess: D-LFT compressionEquipment: DieffenbacherMaterial: 25-30% LGF-PPNotes: - LW-RTP competes

- Acoustic function being added (e.g., by Rieter, Ca rcoustics, others)Photo: Dieffenbacher

Robert Eller Associates LLC 3636

• Filled and fiber-reinforced TPs compete for substrate• LGF-PP pellets and D-LFT compete • Combo with 2-shot D-LFT molding saves unit operation s• Integrated cross-car beam/structural duct potential • Example shown: Ford C-Max, Mazda 3, Volvo S40• Material supplier: Quadrant Plastic Composites AG• System supplier: Faurecia

INSTRUMENT PANEL CARRIER: GROWTH TARGET

Robert Eller Associates LLC 37

SPARE TIRE WELL: SUBSTITUTION TARGET

Vehicle: Mercedes C-Class

Weight: 4.3 kgSubstitution drivers:

- Impact strength for crash resist.- Ability to integrate shape features - Corrosion resistance

Material: GMT-PP combination (random glass mat & fab ric)

Robert Eller Associates LLC 38

SPARE TIRE WELL: NATURAL FIBER TARGET

Vehicle: Mercedes A-Class

Material: Abaca fiber/PPSubstitution drivers:

- Good stiffness weight balance- Green solution- Energy saving (natural fiber vs. glass roving)

Robert Eller Associates LLC 39

Front

• LGF-PP• Front Door Carrier plate wt. = 1042 grams• Rear Door Carrier plate wt. = 670 grams

FORD FIESTA

Rear

DOOR HARDWARE MODULES: GROWTH APPLICATION

Robert Eller Associates LLC 40

DOOR HARDWARE MODULE: GROWTH APPLICATION

VEHICLE: Chrysler Sebring convertible MATERIAL: 40% LGF-PPPROCESS: D-LFT (injection compression)EQUIPMENT: Krauss MaffeiPHOTO: Krauss Maffei

Robert Eller Associates LLC 41

VEHICLE: Ford Kuga (2010)APPLICATION: Roof spoiler and tailgate outer

panelGRADE: LyondellBasell Hifax TRC 280X MOLDER: PlastalREA NOTES: - Inner panel is Stamax (SABIC)- Potential for design transfer to the U.S. (2010)

PHOTO: Robert Eller Associates LLC

HATCHBACK DOOR INNER: GROWTH APPLICATION

PART: Hatchback door inner panelMATERIAL: 40% LGF-PPSTATUS: PrototypePROCESS: D-LFT (injection)EQUIPMENT: Krauss MaffeiCOMPETITION: LGF-PP compound

PHOTO: Krauss Maffei

Robert Eller Associates LLC 42

BIOPOLYMER CANDIDATES FOR AUTOMOTIVE APPLICATIONS

BIOPOLYMERS

MATRIX

HC-BASED(E.G., PP)

BIOPOLYMER-PLA-POLYAL- KANOATE-SOY

NATURAL

FIBERS

SYNTHETIC

VEGETABLE ANIMAL(E.G., WOOL, HAIR)

HC-BASED BIO-BASED(BIOFIBERS)

VIRGIN REGEN-ERATED

-FLAX-HEMP-KENAF-HENNEQUIN-JUTE

-SISAL-CURANA-BANANA-BAMBOO

-COTTON-KAPOTE

-COCONUT -PINE-OTHERS

BASTFIBERS

LEAF SEED FRUIT WOOD

WOODFLOUR

WOODFIBER

SOURCE: ROBERT ELLER ASSOCIATES LLC, 2009

NOTE: (a) USED IN BRAZIL, RECENT U.S. INTRODUCTION IN NYLON

PLA POLYAL-KANOATE

b/mydox/biopolymers/BioBased Composites Auto 09.vsdlg/myfiles/visio/BioBased Composites Auto 09.vsd

BRO-MELIAD

-CURAUA(a)

Robert Eller Associates LLC 43

FUTURE VISION/SUMMARY

Robert Eller Associates LLC 44

FUTURE VISION/SUMMARY

• Like other auto plastics, TP composites (especially LF-RTPs) are affected by:

• The global economic downturn

• Market growth shift to Asia

• Sharp global automotive production downturn

• European/Asian OEM share gain in N. America

• Share gain for smaller vehicles in the global fleet

• Expected fuel price increase and slow penetration o f hybrids and electric drive vehicles

Robert Eller Associates LLC 45

FUTURE VISION/SUMMARY (Cont’d.)

• The LF-RTPs have strong growth potential:

• Substitution on multiple (high weight) applications

• Growth in modular construction

• Renewed weight/cost save pressures

• Supply chain restructuring/direct fabrication savin gs

• Parts consolidation potential

• Front end modules/carriers, door hardware modules, and underbody shields will be near-term growth driv er

• European/Asian share gain in N. America brings technology and designs to accommodate vehicle market shifts

Robert Eller Associates LLC 46

FUTURE VISION/SUMMARY (Cont'd.)

• Intermaterial and inter-process competition:

• Multiple materials/processes are competing.

• D-LFT will make rapid share gains due to raw materi al cost savings but could be restricted by capex requirements in a difficult investment environment.

• Natural fiber reinforcement will gain some share.

• TP composites bring opportunities for adding value, e.g.,

• Parts consolidation in most applications

• Adding acoustic functionality to underbody shields

• Crosscar beam/structural duct integration in instru ment panels

TP COMPOSITES: PART OF MANAGING IN A DOWNTURN

Robert Eller Associates LLC 47

D-LFT – direct long-fiber thermoplastics ETP – engineering thermoplasticGMT – glass mat thermoplastic ILC – in-line compoundingLF-RTP – long fiber reinforced thermoplasticsLGF-PP – long-glass fiber polypropylene LGF-RTP – long-glass fiber reinforced thermoplastic LW-RT – lightweight GMT (GM’s designation), also

LW-GMTPA – polyamide PP – polypropylene s-GMT – structural GMTSGF-PP, PA – short-glass fiber polypropylene or nylo nTP – thermoplastic

ABBREVIATIONS

Robert Eller Associates LLC 48

ACKNOWLEDGEMENTS

• Roger Young (REA-Asia) for Asian inputs

• Myriam Massiani (REA-Europe) for European inputs

• Conrad Zumhagen (The Zumhagen Co. LLC) for inputs on fiber-reinforced examples

• Dieffenbacher – photos

• Krauss Maffei - photos

Robert Eller Associates LLC 4949

Thank You!