australia-korea trade: recent structure and future prospects

TRANSCRIPT

AUSTRALIA-KOREA TRADE: RECENT STRUCTURE AND FUTURE PROSPECTS

by ILTAE SON* AND KENNETH WILSON* *

Introduction Korea and Australia are located in the fastest growing region in the world.

Moreover, trade between countries of the Asia-Pacific region is growing faster than trade with the rest of the world and this move to greater regional interdependence is part of a world-wide trend (James 1992). In this paper we analyse the recent trading relationship between Korea and Australia and examine the prospects for further enhancing trade between the two countries. In analysing the nature of international trade between the two countries we take cognisance of the regional trade policy imperatives affecting the countries of the region and explore the possibility of developing a more embracive bilateral relationship between Korea and Australia.

The structure of the paper is as follows. In the next section we describe briefly the recent structure of Korea-Australia trade. We then discuss briefly relevant aspects of international competitiveness of the two economies, in particular, focusing upon the industry sectors where each country has comparative advantage. In the next section we consider the opportunities that exist for trade promotion between Australia and Korea. We then consider the multilateral and regional imperatives which will impact upon the development of any economic co-operation initiatives.

The structure of Korean and Australian "kade Over the past three decades Korea's exports have expanded from a low

base, generating economic growth for Korea and projecting Korea into the big league of trading nations in the world so that by 1993 Korea generated 2.27% of the world's total exports, thereby becoming the world's 13th largest exporting country. By comparison Korea comprised 2.24% of world's total imports and ranked 13th largest importing country in the world in 1993.'

* Associate Professor, Kyung Hee University, Seoul, Korea. ** Associate Professor, Victoria University of 'IBchnology, Melbourne, Australia.

Funding for this research was provided by a grant from the Korean Ministry of Education, 1993 and the research was completed whilst Professor Son was Visiting Fellow in the Department of Applied Economics, Victoria University of lchnology during 1993, funded by a grant from DEET under the 'hrgeted Institutional Links Program.

1. For details of statistics quoted here see IMF, Direction of 'Bade Statistics Yearbook, 1994.

a3

Meanwhile, Australian exports made up 1.15% of the world’s total exports and thereby Australia was the world’s 20th largest exporting country in 1993. By comparison Australian imports comprised 1.12% of the world’s total imports and Australia ranked as 20th largest importing country in the world in 1993. Australia’s trade with Korea has been growing steadily since 1981 when merchandise exports from Australia to Korea comprised only 3.53% of Australia’s total exports, but this had almost doubled by 1993 to be 6.86% of Australia’s total exports.

Korea and Australia have become increasingly important trading partners in terms of t r a m volumes. Table 1 shows recent trade trends between Korea and Australia. The value of Korea’s total merchandise trade with Australia has grown from $US1,203.6 million in 1981 to $US4,532.0 million in 1993 with increases in Australia’s shares of both Korea’s imports and exports, and increases in Korea’s shares of both Australia’s imports and exports. Korea is Australia’s third largest export market after Japan and the USA taking 6.9% of its total exports in 1993. However, Korea ranks eighth in terms of Australia’s imports making up only 3.3% of its total imports in 1993. Australia, on the other hand, is a less significant trading partner for Korea. The value of Korea’s merchandise trade with Australia is smaller in terms of the share of its exports and imports in 1993; Korea’s exports to Australia accounts for only 1.41% of Korea’s total merchandise exports, whilst Korea’s imports from Australia account for about 3.97% of Korea’s merchandise imports. Australia ranks fifteenth in terms of Korea’s exports, but ranks sixth in terms of imports in 1993.

TABLE 1 RECENT TRENDS IN TRADE BETWEEN KOREA AND AUSTRALIA

1981 1985 1988 1991 1993

Korean exports to Australia ($US mil) Annual growth rate (%) Korean Imports from Australia ($US mil) Annual growth rate (%) Bade balance ($US mil) Australia’s share of Korean exports (%) Australia’s share of Korean imports (%) Korea’s share of Australia’s exports (%) Korea’s share of Australia’s imports (%)

293.6 27.4

910.0 33.8

.616.4

1.38

3.48

3.53

1.15

368.8 - 6.0

1116.1 1.9

- 747.3

1.22

3.58

3.81

1.52

864.8 39.6

1797.4 40.5

- 932.6

1.42

3.47

4.72

2.60

990.0 1185.0 3.6 8.2

3009.4 3347.0 16.2 8.5

- 2019 - 2162.0

1.38 1.41

3.69 3.97

6.31 6.86

2.54 3.27 -

Sources: Bank of Korea, Monthly Bulletin. January 1989. November 1992. IMF, Direction of ’Rade Statistics Yearbook 1994.

Note: Shares are calculated from data taken from IMF, Direction of ’Rade Statistics Yearbook 1994. Australian imports are valued at FOR

84

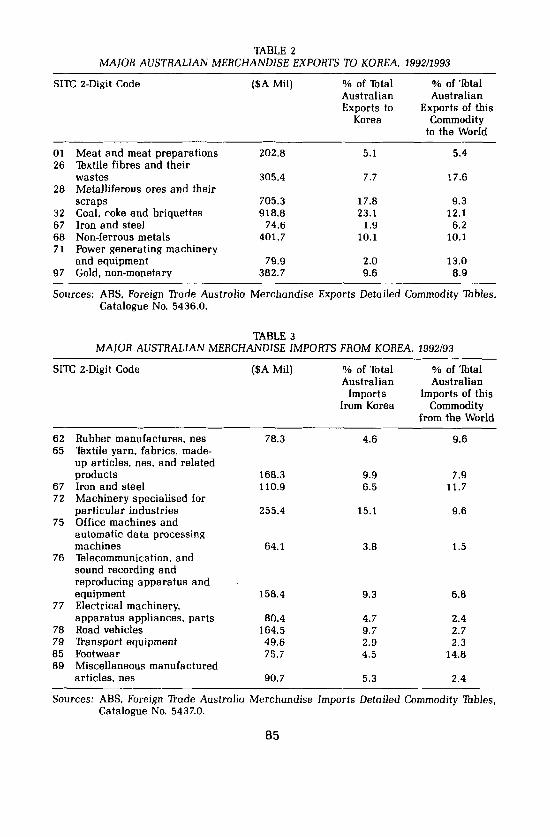

TABLE 2 MAJOR AUSTRALIAN MERCHANDISE EXPORTS TO KOREA, 199211993

S I X 2-Digit Code [$A Mil) % of 'Ibtal % of 'Ibtal Australian Australian Exports to Exports of this

Korea Commodity to the World

~ ~

01 Meat and meat preparations 202.8 5.1 5.4 26 Rxtile fibres and their

28 Metalliferous ores and their scraps 705.3 17.8 9.3

32 Coal, coke and briquettes 918.8 23.1 12.1 67 Iron and steel 74.6 1.9 6.2 68 Non-ferrous metals 401.7 10.1 10.1 71 Power generating machinery

and equipment 79.9 2.0 13.0 97 Gold, non-monetary 382.7 9.6 8.9

wastes 305.4 7.7 17.6

Sources: ABS, Foreign 'Rade Australia Merchandise Exports Detailed Commodity Tables, Catalogue No. 5436.0.

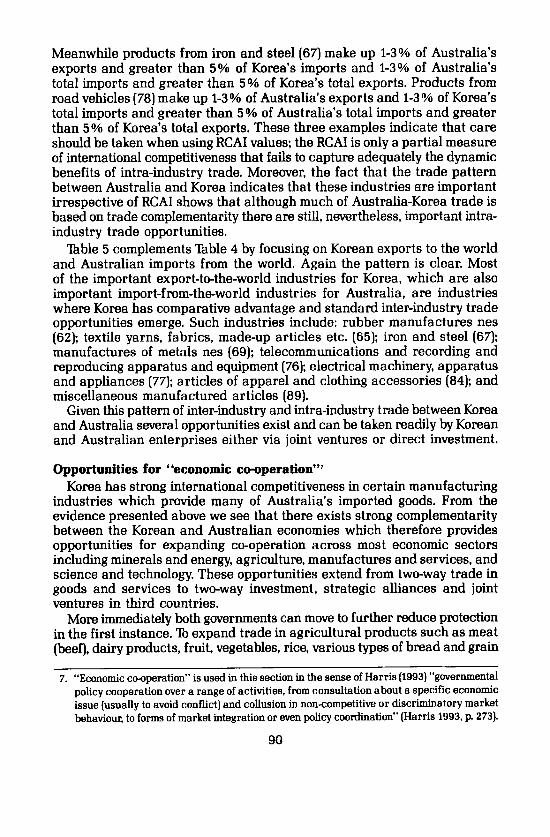

TABLE 3 MAJOR AUSTRALIAN MERCHANDISE IMPORTS FROM KOREA, 1992/93

S I X 2-Digit Code [$A Mil) % of 'Ibtal % of 'Ibtal Australian Australian

from Korea Commodity Imports Imports of this

from the World

62 65

67 72

75

76

77

78 79 85 89

Rubber manufactures, nes Bxtile yarn, fabrics, made- up articles, nes, and related products Iron and steel Machinery specialised for particular industries Office machines and automatic data processing machines Rlecommunication. and sound recording and reproducing apparatus and equipment Electrical machinery, apparatus appliances, parts Road vehicles 'Ransport equipment Footwear Miscellaneous manufactured articles, nes

78.3

168.3 110.9

255.4

64.1

158.4

80.4 164.5 49.6 75.7

90.7

4.6

9.9 6.5

15.1

3.8

9.3

4.7 9.7 2.9 4.5

5.3

9.6

7.9 11.7

9.6

1.5

6.8

2.4 2.7 2.3

14.8

2.4 ~~-

Sources: ABS, Foreign n a d e Australia Merchandise Imports Detailed Commodity Tobles, Catalogue No. 5437.0.

85

Tables 2 and 3 provide details about the value and composition of recent bilateral trade flows between the two countries for a selection of SITC 2-Digit industries. Tables 2 and 3 show the value of trade in commodities for 1993, and composition of the bilateral trade flows, in terms of the percentage shares of the major commodities traded between the two countries in 1993.

Table 2 provides information for the most important export items from Australia to Korea. The most important Australian export commodity category to Korea is coal, coke and briquettes (SIX Code 32), representing 23.1% of Australia's total merchandise exports to Korea in 1993*. The second largest export commodity category to Korea in 1993 is iron ores (28) at 17.8% whilst the third most important commodity group contains non-ferrous metals (68) making up 10.1% of Australia's merchandise exports to Korea. Other important export commodity categories from Australia to Korea contain textile fibres, including wool and cotton (26), meat and meat preparations, including beef (Ol), and gold (97).

nb le 3 provides data on S IX 2-Digit Australian merchandise imports from Korea in 1993. From 'Igble 3 we see that Korea is an important source of several commodity categories with machinery specialised for particular industries (72) making up 15.1% of Australia's imports from Korea whereas this commodity group makes up 9.6% of Australia's total imports. Other important imports include road vehicles (78), telecommunications and sound recording and reproducing apparatus and equipment (76), and textile yarn, fabrics, made-up articles and related products (65).

Tables 2 and 3 tend to confirm the view that much of Korea-Australia trade is based on the predictions of the traditional Hecksher-Ohlin-Samuelson (HOS) model of international trade which emphasises the gains from trading products which embody different factor proportions, what is sometimes called the gains from trade complementarity or gains from inter-industry trade. Does this then mean that there are few, if any, possible gains from intra-industry trade to be obtained between Korea and Australia? To help answer this question we calculated Grubel-Lloyd Intra-Industry Tkade Indexes (IITI? for both countries, including bilateral IITI figures for selected SIX 2-Digit manufacturing industries where the share of exports or imports is greater than 1% of total exports or imports between Korea and Australia;

2. Numbers in parentheses throughout the paper refer to S I X 2-Digit categories. 3. We follow accepted practice and measure the Grubel-Lloyd IITI as follows:

IITIij=l-[IXij-Mijll(Xij +Mij)] where Xij and Mij refer to the exports and imports of country j in commodity i, respectively. The Grubel-Lloyd IITIij Index lies in the interval 0 to 1. If exports exactly match imports, i.e. Xij =Mi,. the Grubel-Lloyd IITIi,, becomes unity, which implies that all the trade is IITI; a country both imports and exports products of the same industry. When either exports equal zero or imports equal zero then the Grubel-Lloyd IITIij would also be zero indicating no IIT at all. Therefore, the closer is the value of the index to unity, the greater is the degree of IIT.

86

these are important export-generating manufacturing industries to either or both Korea and Australia in terms of their bilateral trade

Very few SIX 2-Digit industries have Grubel-Lloyd IITI above 0.5, and they are: non-metallic mineral manufactures, not elsewhere specified (nes) (66), iron and steel (67), manufactures of metals, nes (69), and office machines and ADP machines (75). By contrast, the great majority of the bilateral Grubel-Lloyd IIT indexes for these tradeimportant manufacturing industries are below 0.5 and many are below 0.1. This analysis of bilateral Grubel- Lloyd IITI tends to confirm the indications gained from lhbles 2 and 3 that the pattern of trade flows between Korea and Australia is characterised by trade complementarity or inter-industry trade. Intra-industry trade is not an important feature of Korean-Australian trade except in a small range of manufacturing industries, although this is not to deny that intra-industry trade opportunities exist.

Aspects of international competitiveness and prospects for trade promotion between Korea and Australia

Insight into the international competitiveness of important exporting industries of the Korean and Australian economies can be obtained by considering the Revealed Comparative Advantage Index (RCAI) for each country. The RCAI is determined by calculating the share of a particular commodity group in an economy’s total exports and then dividing by that commodity group’s (or industry’s) share of world exp~r t s .~ If the RCAI of a particular commodity group is greater than unity, the export share of the commodity group in a country exceeds the world average export share of that commodity group. This also means that the country tends to have relatively high comparative advantage in that commodity group. Likewise, a RCAI of less than unity indicates that the country has lower comparative advantage in that commodity group than the world average level.

We have calculated the RCAI for a selection of Korea’s and Australia‘s SIX 2-Digit industries for 1991 (Son and Wilson 1994), which reveal that Australia has strong comparative advantage in industries producing agricultural products, minerals, and non-ferrous metals, but Australia has no comparative advantage in most manufactured products and in some primary products, whilst Korea has comparative advantage in a range of manufacturing industries. We have used this information on RCAI to construct two tables which identify those S IX 2-Digit industries where the best prospects for expanded inter-industry trade, based on trade complementarity and expanded intra-industry trade based on greater integration and “economic co-operation” exist.

4. See Son and Wilson (1994) lhble 14 for details. The bilateral Grubel-Lloyd IIT indexes referred to here were calculated using 1991 data, the most recent data available at the disaggregated bilateral level.

5. The RCAI can be formalised as follows: RCAI = (Xij/Xj)/(WilW) where i = commodity, j = country and W = world.

87

Tables 4 and 5 should be read together and are complementary; they combine information about exports, imports and revealed comparative advantage. Table 4 identifies those S I X 2-Digit industries that are important export industries to the world for Australia, whilst also being important industries from the world to Korea. Alternatively, Table 5 identifies those S I K 2-Digit industries that are important export industries to the world for Korea, whilst also being important import industries from the world to Australia. From Table 4 we see that products from S I K 28, metalliferous ores and metal scrap, made up 5% or more of Australia’s total exports to the world and 3-5% of Korea’s imports from the world and that the RCAI was greater than unity for this industry for Australia and less than 0.3 for Korea; quite clearly this is an important export industry for Australia and is an important market source for Korea since a substantial percentage of its total imports are for products produced by this industry. Not surprisingly Australia has comparative advantage in the products from this industry and Australia’s export trade is based on standard predictions of the HOS model of trade.

A clear pattern emerges from Table 4, most of those industries that are important export industries to the world for Australia are characterised by comparative advantage for Australia; these are industries where there are straightforward inter-industry trade opportunities and they include: cereals and cereal preparations (4); metalliferous ores and metal scrap (28); coal, coke and briquettes (32); and non-ferrous metal (68).

Australian Exports to World

TABLE 4

AUSTRALIA TO WORLD, KOREA FROM WORLD OPPORTUNITIES FOR TRADE PROMOTION SITC-2 DIGIT INDUSTRIES;

1-3 Yo 3-5 yo >5%

1-3 YO 69 Manufactures of metals nes*

67 Iron, Steel

78 Road Vehicles

3 4 % 4 Cereals and Cereal Preparation**

> 5 % 26 Extile Fibres 28 Metalliferous ores 33 Petroleum 32 Coal, coke and and metal scrap** products

6 8 Non-ferrous metals** briquettes**

TABLE 5 OPPORTUNITIES FOR TRADE PROMOTION SIK-2 DIGIT INDUSTRIES:

KOREA TO WORLD, AUSTRALIA FROM WORLD

Total Korean Exports to World

’Ibtal Australia1 Imports from World

1-3 9

3-59

- > 5 9

-

1-3 %

51 Organic chemicals 57 Plastics in primar:

forms 32 Rubber

manufactures nes’ 39 Manufactures of

metals nes* 71 Power generating

machinery and equipment

72 Machinery specialised for particular industries

33 Petroleum product 74 General industrial

machinery and equipment

3-5 % I >5%

67 Iron and steel 84 Articles of apparel

and clothing accessories*

‘5 Office machin and ADP machines*

65 ’IBxtiles, yarns, fabrics, made-up clothes*

76 ’IBlecommunication and recording apparatus etc*

machinery, apparatus and appliances*

78 Road vehicles 79 Other transport

equipment 80 Miscellaneous

manufactured articles*

77 Electrical

Source: Calculated by the authors from data provided by Korean Institute of Economy and

*indicates a RCA Index of greater than unity for this industry in Korea and a value of less than 0.3 for the same industry in Australia.

**indicates a RCA Index of greater than unity for this industry in Australia and a value of less than 0.3 for the same industry in Korea. SI‘K 51.57, 74, 79 have RCAI <0.3 for Australia and SITC 72 has RCAI <0.3 for both Korea and Australia.

Bchnology.

nb le 4 and Table 5 together indicate those industries where there are some prospects for intra-industry trade: petroleum, petroleum products and related materials (33); iron and steel (67) and road vehicles (78).8 The products of petroleum, petroleum products and related materials (33) make up greater than 5% of Australia’s total exports and greater than 5% of Korea’s total imports, and greater than 5% of Australia’s total imports and 1-3% of Korea’s total exports, even though Korea has RCAI of less than 0.3.

6. Even though Australia has a RCAI of less than 0.3 for S IX 78.

89

Meanwhile products from iron and steel (67) make up 1-3% of Australia’s exports and greater than 5% of Korea’s imports and 1-3% of Australia’s total imports and greater than 5% of Korea’s total exports. Products from road vehicles (78) make up 1-3% of Australia’s exports and 1-3% of Korea’s total imports and greater than 5% of Australia’s total imports and greater than 5% of Korea’s total exports. These three examples indicate that care should be taken when using RCAI values; the RCAI is only a partial measure of international competitiveness that fails to capture adequately the dynamic benefits of intra-industry trade. Moreover, the fact that the trade pattern between Australia and Korea indicates that these industries are important irrespective of RCAI shows that although much of Australia-Korea trade is based on trade complementarity there are still, nevertheless, important intra- industry trade opportunities.

Table 5 complements Table 4 by focusing on Korean exports to the world and Australian imports from the world. Again the pattern is clear. Most of the important export-to-the-world industries for Korea, which are also important import-from-the-world industries for Australia, are industries where Korea has comparative advantage and standard inter-industry trade opportunities emerge. Such industries include: rubber manufactures nes (62); textile yarns, fabrics, made-up articles etc. (65); iron and steel (67); manufactures of metals nes (69); telecommunications and recording and reproducing apparatus and equipment (76); electrical machinery, apparatus and appliances (77); articles of apparel and clothing accessories (84); and miscellaneous manufactured articles (89).

Given this pattern of inter-industry and intra-industry trade between Korea and Australia several opportunities exist and can be taken readily by Korean and Australian enterprises either via joint ventures or direct investment.

Opportunities for “economic ~wperation”~ Korea has strong international competitiveness in certain manufacturing

industries which provide many of Australia’s imported goods. From the evidence presented above we see that there exists strong complementarity between the Korean and Australian economies which therefore provides opportunities for expanding co-operation across most economic sectors including minerals and energy, agriculture, manufactures and services, and science and technology. These opportunities extend from two-way trade in goods and services to two-way investment, strategic alliances and joint ventures in third countries.

More immediately both governments can move to further reduce protection in the first instance. To expand trade in agricultural products such as meat (beef), dairy products, fruit, vegetables, rice, various types of bread and grain

7. “Economic co-operation” is used in this section in the sense of Harris (1993) “governmental policy cooperation over a range of activities, from consultation about a specific economic issue [usually to avoid conflict) and collusion in noncompetitive or discriminatory market behaviour, to forms of market integration or even policy coordination” [Harris 1993, p. 273).

90

based confectionaries, and seafood, the Korean government has to remove or reduce restrictions on imports of agricultural products. The Korean government is currently moving to open its agricultural markets (except for some commodities such as rice), thereby providing opportunities for Australia’s agricultural exports. As a reciprocal gesture there are changes that the Australian government could make. There are some agricultural commodities such as fruits that Korea can export to Australia. However, inspection and quarantine requirements, including phytosanitary restrictions on the part of Australia limits Korea’s exports of some agricultural commodities. In addition to the removal or reduction of most tariff barriers, most non-tariff barriers must also be eliminated or reduced over time. Amongst the more important non-tariff barriers are import quotas. Other non-tariff barriers have to do with structural barriers which take the form of import restrictions and regulations such as import licences, phytosanitary restrictions, and market regulations. Korea and Australia have each complained about each other’s discriminatory trading practices which restrain the trade between the two countries. The non-tariff barriers which are at issue in particular between the two countries are Korea’s import quotas on Australia’s exports of agricultural products (in particular beef) and Australia’s Anti-Dumping actions against Korea’s exports of manu- factured goods. During the period from 1990 to 1993, Australian industries initiated 17 cases of Anti-Dumping proceedings against Korean exporters.B Continued Anti-Dumping actions by Australian industries will not encourage or promote trade nor strengthen the bilateral relationship between Korea and Australia.

For industries such as manufactures of metals, nes (69). textile yarn, fabrics, made-up articles, and related products (65) and iron and steel (67), further reductions of tariffs on trades of intermediate inputs and trades of finished goods made from imported intermediate inputs will increase the trade between the two countries. It may also be possible for both govern- ments to further develop importlexport links in certain industries charac- terised by intra-industry trade by providing for preferential treatment for imports used for re-export.

In order to further promote tourism trade between the two countries, the procedures in place for the granting of visas must be devoid of difficulties for potential travellers in the two countries. The Agreement on Visa Exemption which allows for travel for limited periods without the need for a visa should be considered by both government^.^ The introduction of such an agreement would further expand tourism trade between Korea and Australia.

8. See Anti-Dumping Authority for details of the more than 100 total antidumping actions considered by the Authority.

9. The Agreement on Visa Exemption which allows for entry into a country for up to 90 days without the need for a visa has been effective in promoting tourism between Korea and New Zealand.

91

Some bilateral cooperation initiatives already exist in such areas as minerals and energy, quarantine, transport, communication, science and technology, and education. An innovative Arrangement on Industrial Technology Cooperation was signed during the visit of Australia's Prime Minister to Korea in June 1993. Under the Arrangement, Australian and Korean companies and research institutes will be encouraged to cooperate in commercialising the industrial technologies such as information, semi- conductor, new materials, energy, resources and food-processing tech- nologies. The formation of a Joint Economic Committee of senior officials will also contribute to the further development of the bilateral economic relationship between the two countries.

Both countries have been increasing their efforts to develop more diversified l inks through the bilateral co-operation in a range of regional and multilateral economic forums. Australia and Korea have a number of common interests and are dialogue partners in a range of regional and multilateral arrangements in the Asia-Pacific region. Korea and Australia are participating in the development of the Asia Pacific Economic Co- operation forum (APEC),'O the Economic and Social Commission for Asia and Pacific (ESCAP), the Pacific llade and Development Conference (PAFTAD), the Pacific Basin Economic Council (PBEC), and the Pacific Economic Cooperation Council (PECC).

Finally, bilateral trade agreements for Australia's supply to Korea of minerals and energy based resources such as coal, iron ore, and aluminium would also promote trade between the two countries and should be encouraged.

made liberalisation: regional and multilateral considerations The foregoing discussion demonstrates things about Korean-Australian

trade. First, there has been a considerable increase in trade between the two countries over the past decade or so. Secondly, this trade is based squarely upon trade complementarity between the economies of the two countries, though there exists considerable intra-industry trade and opportunities for further expansion in this area. Thirdly, the prospects for increased trade seem good based on the foregoing analysis of underlying trade fundamentals. However, this increased bilateral trade between Korea and Australia forms part of a trend toward increased regionalisation of trade flows observed recently. The extent to which international trade has increased in the Asia-Pacific region over the past two decades is analysed by Yamazawa (1992) James (1992) and Anderson (1993).

An immediate question arises: is the increased intra-regional trade in the Asia-Pacific region a direct reaction to reduced trading opportunities outside the region due to a rise in regional integration agreements elsewhere, or

10. For an excellent discussion of the origins and political imperatives of APEC see Kim (1992).

92

is it simply the result of typical rent-seeking behaviour and the recognition of trading advantages combined with imaginative trade-promoting policy? A related question is: does this increase in regional trade undermine, to any extent, the multilateral trading system as supported by the General Agree- ment on Tariffs and Bade (GATT)?

Simple, straightforward answers to these questions are not possible but consideration of these matters is important when considering what policy initiatives might be introduced and pursued in order to promote Korean- Australian trade. The policy framework must be put into perspective; bilateral initiatives in a regional context as part of a multilateral trading system. In the same way that analysts question the growth of regional integration agreements (do they lower global welfare? do they divert resources away from activities that would promote multilateral trade?), we must be cognisant of the broader context in which we discuss policies aimed at promoting and increasing Korean-Australian trade volumes. Beggar-thy- neighbour policies that simply divert trade away from other trading partners and lead to no net gains in total trade will be questioned as being unable to generate increases in global welfare because they have tradediverted rather than trade-created.

Doubts about the future of multilateral trade make bilateral initiatives more attractive. Such agreements might be necessary to protect market access. However, it is unlikely that there will be a complete collapse of the multilateral system now that the Uruguay Round has been concluded successfully. Nevertheless, opportunities for significant barrier reductions may be possible on a bilateral basis. Australia already operates one detailed bilateral agreement, the Closer Economic Relationship (CER) with New Zealand.”

An APEC integration agreement probably provides the best alternative to a healthy multilateral trading system for both Korea and Australia. It must be remembered that the rapid economic growth of East Asian economies over the past two decades resulted directly from the adoption of outward- looking growth strategies by countries within the region, combined with access to world markets and declining levels of trade protection obtained by GAIT. A more open multilateral system would benefit both Australia and Korea, but such a system has been placed under pressure from the twin developments of, firstly, the move to regional economic integration, and secondly, the growth in the use of non-tariff barriers outside the GATT framework. This “new-protectionism’’ has placed increased strain on the GATT and encouraged the move toward consideration of bilateral trade remedies. Whilst both the Korean and Australian governments favour an open multilateral trading system, it may nevertheless be convenient, expedient and beneficial to their mutual advantage to use APEC in the first instance, or a more formal bilateral framework along the lines of the CER

11. For a comprehensive discussion of the CER see Lloyd (1991).

93

to extend Gm-based trade policy into the Asia-Pacific region. However, CER is in many respects a special case and may not provide a general model for bilateral agreements between Australia and its other trading partners. Australia and New Zealand have in common many social, sporting, political and economic institutions; language, history, legal and political systems are similar.

As with most bilateral agreements questions still arise as to whether the removal of trade barriers between partners to agreements simply trade- divert to the advantage of the members to the agreement at the expense of non-member countries. A bilateral agreement between Korea and Australia would inevitably raise such questions. Preference given to Australian exports would inevitably displace US exports of agricultural products in the Korean economy. Bade diversion at the expense of the US is likely in a range of markets including beef and wheat in particular. Bade diversion is likely at the expense of some other APEC countries and Asia’s newly industrialising economies (ANIEs) in other markets, particularly primary commodities. Alternatively, preferential treatment given to Korean industrial products at the expense of imports from other trading partners is also likely to lead to reaction by those trading partners. It is unlikely that either Korea or Australia would like to upset the US government or incur the wrath and retaliation of important trading partners in pursuit of a comprehensive bilateral trade agreement. Does this then mean that there is little use in pursuing bilateral trade initiatives between Korea and Australia? Not necessarily, bilateral policy initiatives aimed at liberalising trade opportunities, breaking down barriers and harmonising trade between the two countries may lead to more general application.

In arguing for a bilateral agreement between Korea and Australia we argue such a bilateral agreement should be seen as part of a trade liberalisation strategy. The East Asian countries that have been so successful in expanding both their international trade and their incomes have used a range of policies, often selected pragmatically to achieve their objectives of expanded industrial production and exports. Frequently these strategies involve policies that do not fit neatly into the traditional list of trade liberalisation measures, particularly where the policy measure is aimed at increasing intra-industry trade, good examples of which include the use of export processing zones (EPZs) and import/export links. Much of the growth in intra-industry trade in the region has been facilitated by the use of these non-traditional policy measures which in some cases may be anathema to GATT rules.

Gruen (1994) provides a very useful taxonomy of trade liberalisation policies used by East Asian economies over the past two decades which includes seven different types of trade liberalisation and their related policies or “paths to free trade”. The types of trade liberalisation most relevant to Korea-Australia trade are: (i) inter-industry trade liberalisation which is best achieved by tariff reduction and quota expansion; (ii) intra- industry trade liberalisation best achieved by exportlimport links including

94

import for reexport and export for re-import concessions: (iii) firm specific trade liberalisation achieved by negotiating import rights with individual firms; and (iv) regional trade liberalisation to create free trade areas.*Z

The important point is that trade liberalisation may be achieved by a range of different routes: unilateral, multilateral and bilateral. In the end the success or otherwise of a particular trade liberalisation policy becomes an empirical matter and cannot be determined “in principle”. The only real constraint to the use of a bilateral agreement to achieve trade liberalisation should be its compatibility with other multilateral initiatives. Where a bilateral agreement is aimed at trade liberalisation and is compatible with multilateral agreements it should be encouraged.

Concluding comment The previous discussion has identified the prospects for increased

economic cooperation between Korea and Australia. We have focused upon the underlying economic fundamentals of the trade relationship between the two countries. Korea-Australia trade is growing and has grown considerably from a very low base during the past two decades and the prospects for further growth are very good. The observed complementarity between the Korean and Australian economies provide openings for expansions of both inter-industry and intra-industry trade. Based on an observed synergy in the trading relationship we have argued that the move to a more formal method of economic co-operation to further promote trade between the two countries along the lines of a bilateral agreement, should be encouraged. Such a bilateral agreement must be consistent with both countries’ support for APEC and the promotion of trade liberalisation strategies to further the growth of regional trade.

BIBLIOGRAPHY Anderson, K. (1993). “NAFTA. Excluded Pacific Rim Countries and the Multilateral Bading

System”, in Cushing. R.G. et al. (eds), The Challenge of NAFTA: North America, Australia, New Zealand and the World Zkade Regime, University of Texas at Austin, Austin.

Australian Bureau of Statistics (1992). Australia’s Merchandise ”kade with the Republic of Korea: A Dual Perspective. September.

Cushing, R.G.. et al. (eds) (1993). The Challenge of NAFTA: North America, Australia, New Zealand and the World a a d e Regime, University of ’kxas at Austin, Austin.

Department of Foreign Affairs and Bade (1991). Australia-Korea Forum: Proceedings, Australian Government Publishing Services, Canberra, April.

Department of Foreign Affairs and Bade (1992). Country Economic Brief: Korea, AGPS, Canberra, December.

Department of Foreign Affairs and Bade (1993). The APEC Region: a a d e and Investment, Canberra.

12. Gruen (1994) points out that the Australian automotive industry proved resistant to traditional (tariff) trade liberalisation, but exportlimport links have been successful in promoting intra-industry trade leading to improved international competitiveness.

95

Drysdale, P. and Ross Garnaut (1989). “A Pacific Free ’bade Area?”, Pacific Economic Popers,

East Asia Analytical Unit, Department of Foreign Affairs and ’bade (1992). Australia and

East Asia Analytical Unit, Department of Foreign Affairs and ’bade (1992). Korea to the Year

Garnaut. R. (1990), Australia and the Northeast Asian Ascendancy, Australian Government

Grubel. H.G. and P.J. Lloyd (1975). Intra-Industry 7kade. MacMillan, London. Gruen, N. (19941, “Asian ”kade and Industry Policies-Western Economics? ’Ibwards a more

general approach to trade liberalisation”, Centre for Economic Policy Research Discussion Paper no. 313, A N . Canberra.

Harris, S. (1993). “Economic Cooperation and Institution Building in the Asia-Pacific Region”, in Higgott, R. et al. (eds). Pacific Economics Relations in the 1990s: Cooperation of Conflict?, Allen & Unwin, Sydney.

no. 17. Research School of Pacific Studies, A N , Canberra, May.

North-East Asia in the 1900s: Accelerating Change, AGPS. Canberra.

2000: Implications for Australia, Canberra.

Publishing Service, Canberra.

IMF (1994). Direction of ’bade Statistics Yearbook, IMF, Washington, DC. James, W.E. (19921, “Basic Directions and Areas for Cooperation: Structural Issues and the

Asia-Pacific Economies”, in Suh. J.-W. and 7.-R Ro, Asia-Pacific Economic Cooperation: the Way Ahead, KIEP, Seoul.

Kim. C. (1992). “Regional Economic Cooperation Bodies in the Asia-Pacific: Working Mechanism and Linkages”, in Suh, J.W and J.-B. Ro, Asia-Pacific Economic Cooperation: the Way Ahead, KIEP, Seoul.

Koo, R (1990). “Korea‘s Perspective on Asia-Pacific Economic Cooperation”, in Hardt. J.P. and Y.C. Kim (eds). Economic Cooperation in the Asia-Pacific Region, Westview Press.

Lee. Duk-Hoon (1992), “East Asia: The External Policy of Korea”, Economics Division Working Papers, Research School of Pacific Studies, ANU.

Lee. Y. (1987). “Intra-Industry ’bade in the Pacific Basin”, International Economic Journal, Spring.

Lloyd, P.J. (1991). The Future of CER: A Single Market for Australia and New Zealand, CEDA Monograph No. 96, Victoria University Press, Wellington, NZ.

McDonnell. J. (1991), “’bade Liberalization in the Asia-Pacific Region: Why It Is Important and How It Can Be Achieved”, The First APEC Bade Promotion ’baining Course, Korea Institute for Industrial Economics and ’bade, October.

Son. I. and K Wilson. (1994). “”kade Promotion and Economic Cooperation Between Korea and Australia”, Paper presented to a seminar on “Australian and Korean Perspectives on Regional Cooperation and the Future of APEC” at Monash Asia Institute, Monash University, June 9.

Suh, Jang-Won and Jae-Bong Ro (1992). Asian-Pacific Cooperation: the Way Ahead, Korea Institute for International Economic Policy, Seoul.

The Committee for Review of Export Market Development Assistance (1989). Australian Exports: Performance, Obstacles, and Issues of Assistance, AGPS, Canberra, July.

Whitelaw. R. and J. Howe (1992). “Australia’s External Constraint in the 1990s”. Economic Planning Advisory Committee Research Paper no. 1, Economic Planning Advisory Committee, May.

Yamazawa. I. (1992). “On Pacific Economic Integration”, Economic Journal, November.

96