australia _ estudios económicos - coface

DESCRIPTION

Estudio riesgo país de AustraliaTRANSCRIPT

21/10/2015 Australia / Estudios Económicos Coface

http://www.coface.es/EstudiosEconomicos/Australia 1/2

INICIO ESTUDIOS ECONÓMICOS AUSTRALIA

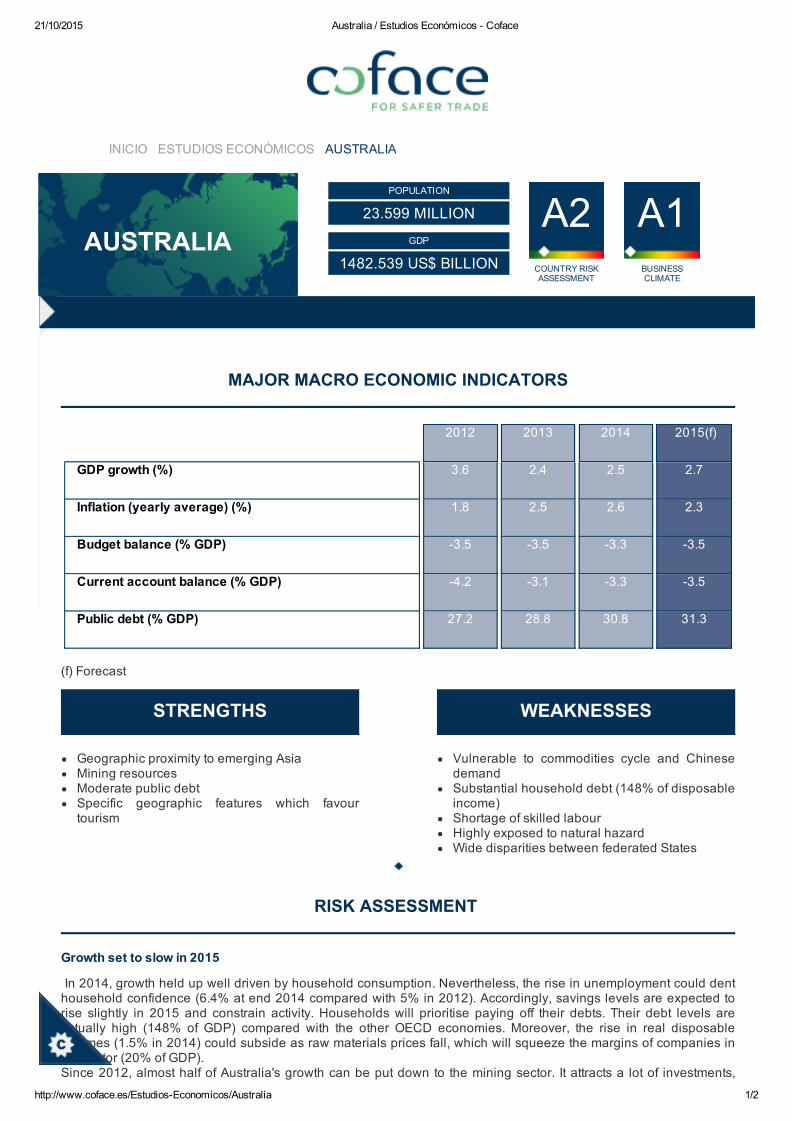

STRENGTHS

Geographic proximity to emerging AsiaMining resourcesModerate public debtSpecific geographic features which favourtourism

WEAKNESSES

Vulnerable to commodities cycle and ChinesedemandSubstantial household debt (148% of disposableincome)Shortage of skilled labourHighly exposed to natural hazardWide disparities between federated States

SYNTHESIS

MAJOR MACRO ECONOMIC INDICATORS

2012 2013 2014 2015(f)

GDP growth (%) 3.6 2.4 2.5 2.7

Inflation (yearly average) (%) 1.8 2.5 2.6 2.3

Budget balance (% GDP) 3.5 3.5 3.3 3.5

Current account balance (% GDP) 4.2 3.1 3.3 3.5

Public debt (% GDP) 27.2 28.8 30.8 31.3

(f) Forecast

RISK ASSESSMENT

Growth set to slow in 2015

In 2014, growth held up well driven by household consumption. Nevertheless, the rise in unemployment could denthousehold confidence (6.4% at end 2014 compared with 5% in 2012). Accordingly, savings levels are expected torise slightly in 2015 and constrain activity. Households will prioritise paying off their debts. Their debt levels areactually high (148% of GDP) compared with the other OECD economies. Moreover, the rise in real disposableincomes (1.5% in 2014) could subside as raw materials prices fall, which will squeeze the margins of companies inthe sector (20% of GDP). Since 2012, almost half of Australia's growth can be put down to the mining sector. It attracts a lot of investments,

POPULATION

23.599 MILLION

GDP

1482.539 US$ BILLION COUNTRY RISKASSESSMENT

BUSINESSCLIMATE

A2 A1AUSTRALIA

21/10/2015 Australia / Estudios Económicos Coface

http://www.coface.es/EstudiosEconomicos/Australia 2/2

especially foreign, which will be forced to slow down in 2015. To counter the downturn in prices, the Australiancentral bank has announced that it will maintain an accommodative monetary policy. The key rate is, therefore, likelyto remain at 2.5% in 2015. Investment in infrastructure will contribute to growth needed as it is aging andinadequate, especially in the large towns and cities. In 2014, the Federal government introduced incentives tostimulate investment by the states pledging a bonus of 15% of the proceeds from the sale of public infrastructureassets, provided the income is reinvested in new infrastructure projects. The construction sector will remain sound in 2015, as property prices continued to grow strongly in 2014 (+10%)encouraging investors not to rein in spending. However, the Australian market needs to be watched, as according tothe OECD house prices were 31% too high in 2013. Public deficit on the rise

The government could push back these adjustment objectives: public spending cuts at a time of rising unemploymentwill curb activity. At 30% of GDP in 2014,the level of public debt was the lowest of the large OECD economies. Exports hampered by the Chinese slowdown

On the exports side, activity in the mining (coal and iron ore) and energy sectors (coal seam gas and natural gas) islargely dependent on demand from China (21% for goods and services, 60% for iron). Although Australia has signeda freetrade agreement with China, which allows it to position itself as a privileged partner, the country has to adapt tothe Chinese slowdown. The fall in imports, especially capital goods, is however expected to limit the decline in thetrade balance.Exports of services (tourism, education) will be at a disadvantage in terms of price competitiveness due to theAustralian dollar's high exchange rate against the euro. Apart from the deterioration of the trade balance, the balanceof transfers and of revenues is also posting a deficit. This is the result of large outflows of investment income,especially as regards the mining sector. Moreover, Australia is dependent on expatriate workers due to low birthrates. Emigrants' income transfers to their families also put pressure on the current account balance. The Australian banking system is exposed to property risk

The sector is highly developed, with assets representing three times the size of the economy (340% of GDP). Itobserves Basel III norms and therefore appears capable of resisting a largescale economic shock. Nonetheless, it isvery concentrated, as it is dominated by 4 large banks with very similar operating systems. They hold 80% of totalassets and 90% of mortgages. They are financed mainly through the international markets and are interdependent(provide finance to each other). Two thirds of the real estate stock is backed by a mortgage. Outstanding loansrepresent 1,150 AUD (75% of GDP). A property crisis could, therefore, seriously weaken the banks and the economy. Little political change in 2015

Elected in September 2013, Tony Abbott is the 28th Australian prime minister. With 88 seats out of 150 in the Houseof Representatives, the liberal coalition has a large majority. The next elections are scheduled for 2016, giving theleaders time to implement their programme. Internationally, Australia is conducting a balanced foreign relations policy regarding two poles of power. On theeconomic front, it is seeking to improve relations with the Member States of ASEAN, while, on the diplomatic front, itwill remain very close to the United States given China's rising power in the Asia Pacific region.