audited financial statements - world...

TRANSCRIPT

AUDITED FINANCIAL STATEMENTS

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Republic of the PhilippinesCOMMISSION ON AUDIT

Commonwealth Avenue, Quezon City, Philippines

INDEPENDENT AUDITOR'S REPORT

The SecretaryDepartment of TransportationOrtigas Avenue, Mandaluyong City

We have audited the accompanying financial statements of the Cebu-Bus Rapid Transit

(BRT) Project financed under the International Bank for Reconstruction and

Development (IBRD) Loan No. 8444-PH of the World Bank, including Clean

Technology Fund Loan No. TF017646-PH, and Credit Facility Agreement with the

Agence Francaise de Developpement, and implemented by the Department of

Transportation - Central Office (DOTr - CO), which comprise the Statement of

Financial Position as of December 31, 2016, and the related Statement of Financial

Performance, Cash Flows, Changes in Net Assets/Equity and Comparison of Budget andActual Amounts and Statement of Sources and Uses of Funds for the year then ended,and a summary of significant accounting policies and other explanatory information.

Management's responsibility for the financial statements

Management is responsible for the preparation and fair presentation of these financialstatements in accordance with Philippine Public Sector Accounting Standards (PPSAS),and for such internal control as management determines is necessary to enable thepreparation of financial statements that are free from material misstatements, whether dueto fraud or error.

Auditor's responsibility

Our responsibility is to express an opinion on these financial statements based on ouraudit. We conducted our audit in accordance with the Philippine Public Sector Standardson Auditing. Those standards require that we comply with ethical requirements and planand perform the audit to obtain reasonable assurance about whether the financialstatements are free from material misstatements.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosure in the financial statements. The procedures selected depend on the auditors'judgment, including the assessment of the risks of material misstatements of the financialstatements, whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the entity's preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on the effectiveness of

the internal control. An audit also includes evaluating the appropriateness of accounting

policies used and the reasonableness of accounting estimates made by management, as

well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to

provide a basis for our unqualified audit opinion.

Unqualified Opinion

In our opinion, the financial statements referred to above present fairly in all material

respects, the financial position of the Cebu CBRT Project of Department of

Transportation as of December 31, 2016, and the results of its financial performance,

cash flows, changes in net assets/equity and the comparison of budget and actual amounts

for the year then ended, in accordance with applicable laws, rules and regulations and in

conformity with the PPSAS.

COMMISSION ON AUDIT

By:

AVE LDA B. TORRESS pervising Audito

16 June 2017

~2

Republic of the PhilippinesDEPARTMENT OF TRANSPORTATION

STATEKMENT OF MANAGEMENT RESPONSIRILITYFOR FINANCIAL STATEMENTS

CEBU BUS RAPID TRANSIT PROJECTFUND C1, STER 02

lie management of Department of Transportation - Central Office (DOTr-CO) florthe Cebu-Bus Rapid Transit (Cebu-RRT) Project is responsible lbr all infonnation andrepreseuatioin contained in the accoipanying Statement of Financial Position as of 31Decembr 2016 and tlie related Statement of Financial Performance, Statement ofChanges in Net Assets/Equity, Statement of Cash Flows, Stalement of Comparison ofActual and Budget Amount and Noes to Financial Statements for the Year thenEnded. The financial statements have been prepared in confornity m ith Philippine Public

Setor Accounting Standards and generallt accepted state accounting principles. and

retleet amotnis that are hased on the best estimates and informed judgment of

managenent with an appropriate consideration to materiality.

in this regard. management maintins a system of accounting and reporting which

provides for the necessary internal controls to ensure that transactions are pruperlyatithoriized and recorded, assets are safeguarded against unauthori,cd tise or disposition

and liabilities are recognited.

LYDIA S. NIALVAR DANTE M. LANTINDirector 1i1 Assistant Sceretarv for Administrative

Coipptrollership Service and Comptroillership Serices

Date Signed DSte Signed

Ti1F VOLUMBIA TOWFe TPE FAX (632) iD 492'S

BRcY WAK wm< K r Ptr AtE TRIL (FII TRE 12 7 ToT / 19

5S%5 MANDhAMuW)NG CHTY, PilU i INFIs BOT AýCTOM CVNlTER IOTI INI- 1'4O

DEPARTMENT OF TRANSPORTATION - CENTRAL OFFICESTATEMENT OF FINANCIAL POSITION

CEBU BUS RAPID TRANSITFund Cluster 02

As at December 31, 2016

Notes 2016 2015

Assets

Current Assets

Cash and Cash Equivalents 5 P 617,812,700.80 P 193,593,736.27

Receivables 6 1,713.29

Other Current Assets 8 11,143,114.62 30,758,493.75

Total Current Assets 628,957,528.71 224,352,230.02

Non - Current Assets

Property, Plant and Equipment 7 125,391,242.14 804,354.74

Total Non-Current Assets 125,391,242.14 804,354.74

Total Assets 754,348,770.85 225,156,584.76

Liabilities

Current Liabilities

Financial Liabilities - 2,104,329.50

Inter-Agency Payables 9 4,149,621.21 20,387.49

Total Current Liabilities 4,149,621.21 2,124,716.99

Total Liabilities 4,149,621.21 2,124,716.99

Total Assets Less Total Liabilities 750,199,149.64 223,031,867.77

Net Assets/Equity

Equity 750,199,149.64 223,031,867.77

Accumulated Surplus/(Deficit) 750,199,149,64 223,031,867.77

Total Net Assets/Equity P 750,199,149.64 P 223,031,867.77

This statement should be read in conjuction with the accompanying notes.

I

DEPARTMENT OF TRANSPORTATION - CENTRAL OFFICESTATEMENT OF FINANCIAL PERFORMANCE

CEBU BUS RAPID TRANSITFund Cluster 02

FOR THE YEAR ENDED DECEMBER 31, 2016

Notes 2016 2015

RevenueService and Business Income 10 P 391,68302 P 131,560.43

Total Revenue 391,683.02 131,560.43

Less Current Operating ExpensesPersonal ServicesMaintenance and Other Operating Expenses - 4,256,958,98

Financial Expenses 11 1,509.76 465.25

Non-Cash Expenses 12 4,235.41 -

Current Operating Expenses 5,745.17 4,257,424.23

Surplus (Deficit) from Current Operations 385,937.85 (4,125,863.80)

Net Financial Assistance/Subsidy 13 479,936,944.52 227,289,292.00

Gains 14 35,762,819.83 -

Surplus (Deficit) for the period P 516,085,702.20 P 223,163,428.20

This statement should be read in conuction with the accompanying notes.

2

DEPARTMENT OF TRANSPORTATION - CENTRAL OFFICE

STATEMENT OF CHANGES IN NET ASSETS/EQUITYCEBU BUS RAPID TRANSIT

Fund Cluster 02

FOR THE YEAR ENDED DECEMBER 31, 2016

Accumulated Surplus/(Deficit)

2016 2015

Balance at January 01 P 223,031,867.77 P

Prior Period Adjustments/Unrecorded Income and Expenses 11,286,815.64 -

Restated balance 234,3 18,683.41

Changes in net assets/equity for Calendar Year 2016

Adjustment of net revenue recognized directly in net assets/equity (205,235.97) (131,560.43)

Surplus for the period 516,085,702.20 223,163,428.20

Total recognized revenue and expense for the period 515,880,466.23 223,031,867.77

Balance at December 31 P 750,199,149,64 P 223,031,867.77

*I - Net revenue deposited with the National Treasry (revenue including construcve receipt of income

and mcome of BIR remitted by agencies thru TRA)

This statement should be read in conjuction with the accompanying notes.

3

DEPARTMENT OF TRANSPORTATION - CENTRAL OFFICE

DETAILED STATEMENT OF CASH FLOWSCEBU BUS RAPID TRANSIT

Fund Cluster 02For the Year Ended December 31, 2016

Note 2016 2015

Cash Flow From Operating/Investing Activities:

Cash Inflows:Receipt of Notice of Cash Allocation P 479,936,944.52 P 226,831,378.56

Collection of Income/Revenues 391,683.02 131,560.43

Total Cash Inflows 480,328,627.54 226,962,938.99

Cash Outflows from Operating Activities

Remittance to National Treasury 2,299,527.97 131,560.43

Payment of Expenses - 1,673,439.45

Remittance of Personnel Benefit Contributions and Mandatory Deductions 10,181,106,31 1,566,004.69

Adjustment - 19,386.56

Total Cash Outfows from Operating Activities 12,480,634.28 3,390,391.13

Net Cash Provided by (Used in) Operating Activities 467,847,993.26 223,572,547.86

Cash Outflows from Investing Activities

Purchase /Construction of Property, Plant and Equipment 88,515,997.22 29,978,811.59

Total Cash Outfows from Investing Activities 88,515,997.22 29,978,811.59

Net Cash Provided by (Used in) Investing Activites (88,515,997.22) (29,978,811.59)

Increase (Decrease) in Cash and Cash Equivalents 379,331,996.04 193,593,736.27

Effects of Exchange Rate Changes on Cash and Cash Equivalents 44,886,968.49 -

Cash and Cash Equivalents, January 1 193,593,736.27 -

Cash and Cash Equivalents, December 31 5 P 617,812,700.80 P 193,593,736,27

This statement should be read in conjuction with the accompanying notes.

4

DEPARTMENT OF TRANSPORTATION - CENTRAL OFFICE

STATEMENT OF COMPARISON OF BUDGET AND ACTUAL AMOUNT

CEBU BUS RAPID TRANSITFund Cluster 02

FOR THE YEAR ENDED DECEMBER 31, 2016

Actual

Particulars Budgeled Amount Amounts on Difference Final

Comparable Budget and ActualBasis

Original Findi

RECEl PTSServices and Business Income 3 6 P 0.00 P 0.00 P 391,683.02 P (391,683.02)

Tax RevenueAssistance and Subsidy 3 7

Shares, Grants and Donations

GainsOthers

Total Receipts 0.00 0.00 0,00 0.00

Total Cash Outfows from Operating Activities

PAYMENTSPersonnel ServicesMaintenance & Other Operating Exp

Capital Outlay 3,7 1,552,906,754.49 2,489,976,031,79 12,440,805.61 2,477,535,226.18

Financial ExpensesOther

Total Cash Outfows fron Investing Activities 1,552,906,754.49 2,489,976,031.79 12,440,805.61 2,477,535,226.18

NET RECEIPTS/PAYMENT P(1,552,906,754.49) P1(2,489,976,031.79) P(12,440,805.61) P (2,477,535,226.18)

This statement should be read in conjuction with the accompanying notes.

5

DEPARTMENT OF TRANSPORTATION - CENTRAL OFFICENotes to Financial Statements

Cebu Bus Rapid TransitFund Cluster 02

For the year ended December 31, 2016

General Information/Agency Profile

1.1 The financial statements of the Department of Transportation of theCEBU BUS RAPID TRANSIT were authorized for issue on April 21,2017 as shown in the Statement of Management Responsibility signed byDirector Lydia S. Malvar and Assistant Secretary Dante M. Lantin, the

authorized representatives of the DOTr-CO.

1.2 The Department (then Ministry) of Transportation and Communications(DOTC) was created by virtue of Executive Order No. 546, series of 1979.

It was later re-organized, both structurally and functionally by the issuanceof subsequent legislations, as follows: (a) Executive Order No. 125 dated

January 30, 1987, which was promulgated in conformance to ExecutiveOrder No. 5, series of 1986; (b) Executive Order No. 125-A dated April13, 1987, to give further impetus to the declared policy of the State

towards the maintenance and expansion of viable, efficient and

dependable transportation and communication systems as effectiveinstruments for the Department's objectives; (c) Executive Order No. 202,dated June 19, 1987, creating the Land Transportation Franchising andRegulatory Board as a sectoral office of the Department; (d) ExecutiveNo. 220, dated October 1988, creating the Cordillera AdministrativeRegion, compelling the DOTC to establish a DOTC-CAR as its regionaloffice; (e) Republic Act No. 7354, dated April 2, 1992, which took effectJune 3, 1992, creating the Philippine Postal Corporation as an attachedcorporation to the DOTC from the former sectoral office, Postal Service

Office; (f) Department Order No. 96-912 dated January 15, 1996,establishing the DOTC-CARAGA as its regional office; (g) Executive

Order No. 477 dated April 15, 1988, transferring the Philippine CoastGuard to the DOTC as a sectoral office; (h) Republic Act No. 9497, datedMarch 4, 2008, creating the Civil Aviation Authority of the Philippines as

an attached corporation to the DOTC from the former sectoral office, Air

Transportation Office; (i) Executive Order No. 780 dated January 29,2009, transferring the sectoral office, Telecommunications Office, from

the DOTC to the Commission of Information and CommunicationsTechnology (CICT); (j) Republic Act No. 9993, dated July 27, 2009,establishing the Philippine Coast Guard as an armed and uniformed

service to the DOTC from a former sectoral office, and (k) Republic ActNo. 10844, dated May 23, 2016 creating the Department of Information

and Communications Technology (DICT) and renaming the DOTC to

Department of Transportation (DOTr).

1.3 The mandate of the Department of Transportation (DOTr) is to act as the

primary policy, planning, programming, coordinating, implementing,

regulating and administrative entity of the executive branch of thegovernment in the promotion, development and regulation of a dependableand coordinated networks of transportation and communications systems,as well as, in the fast, safe, efficient and reliable transportation andcommunications services. Its registered office is located in the ColumbiaTower, Brgy. Wack-Wack, Ortigas Avenue, 1555 Mandaluyong City,Philippines.

1.4 The Cebu-BRT Project is the establishment of a transport system witharound 33 bus stations and 176 buses that will run through the 23-kmcorridor from Bulacao to Ayala, with link to Cebu's South RoadProperties (SRP) via dedicated and exclusive bus-ways and mixed traffic

operation from Ayala to Talamban in Cebu City. Its objective is toimprove overall performance of the urban passenger transport system inthe Project Corridor in Cebu City in terms of quality and level of service,safety and environmental efficiency.

2. Statement of Compliance and Basis of Preparation of Financial Statement

The financial statements have been prepared, in accordance with and comply withthe Philippine Public Sector Accounting Standards (PPSAS) issued by theCommission on Audit per COA Resolution No. 2014-003 dated January 24, 2014

The financial statements have been prepared on the basis of historical cost, unless

stated otherwise. The Statement of Cash Flows is prepared using the directmethod.

3. Summary of Significant Accounting Policies

3.1 Basis of Accounting

The financial statements are prepared on an accrual basis in accordancewith the Philippine Public Sector Accounting Standards (PPSAS).

3.2 Cash and cash equivalents

Cash and cash equivalents pertain to cash at bank which are readilyconvertible to known amount of cash and are subject to insignificant risk

of change in value. For the purpose of the statement of cash flows, cashand cash equivalents consist of cash and short term deposits as definedabove, net of outstanding bank overdrafts.

7

3.3 Property, Plant and Equipment

Recognition

An item is recognized as property, plant and equipment (PPE) if it meetsthe characteristics and recognition criteria as a PPE.

The characteristics of PPE are as follows:

* tangible items;* are held for use in the production or supply of goods of services,

for rental to others, or for administrative purposes; and* are expected to be used more than one reporting period.

An item of PPE is recognized as an asset if

* it is probable that future economic benefits or service potential

associated with the item will flow to the entity; and

* the cost of fair value of the item can be measured reliably.

Measurement at Recognifion

An item recognized as property, plant, and equipment is measured at cost.

A PPE acquired through non-exchange transaction is measured at its fair

value as at the date of acquisition.

The cost of the PPE is the cash price equivalent or, for PPE acquired

through non-exchange transaction, its cost is its fair value as at recognitiondate.

Cost includes the following:

o its purchase price, including import duties and non-refundablepurchase taxes, after deducting trade discounts and rebates;

o expenditure that is directly attributable to the acquisition of theitems; and

* initial estimates of the costs of dismantling and removing the item

and restoring the site on which it is located, the obligation for

which an entity incurs either when the item is acquired, or as aconsequence of having used the item during a particular period for

purposes other than to produce inventories during that period.

X

Measurement after Recognition

After recognition, all property, plant and equipment are stated at cost lessaccumulated depreciation and impairment losses

When significant parts of property, plant and equipment are required to bereplaced at intervals, the DOTr recognizes such parts as individual assetswith specific useful lives and depreciates them accordingly. Likewise,when a major repair/replacement is done, its cost is recognized in thecarrying amount of the plant and equipment as a replacement if therecognition criteria are satisfied. All other repair and maintenance costsare recognized as expense in surplus or deficit as incurred.

Depreciation

Each part of an item of property, plant and equipment with a cost that issignificant in relation to the total cost of the item is depreciated separately.

The depreciation charge for each period is recognized as expense unless itis included in the cost of another asset.

Initial Recognition ofDepreciation

Depreciation of an asset begins when it is available for use such as when itis in the location and condition necessary for it to be capable of operatingin the manner intended by management.

For simplicity and to avoid proportionate computation, the depreciation isfor one month if the PPE is available for use on or before the 15th of themonth. However, if the PPE is available for use after the 15" of the month,depreciation is for the succeeding month.

Depreciated Method

The straight line method of depreciation shall be adopted unless another

method is more appropriate for agency operation.

Estimated Useful Lif

The DOTr uses the Schedule on the Estimated Useful Life of PPE byclassification prepared by COA.

The DOTr uses a residual value equivalent to at least five percent (5%) ofthe cost of the PPE.

Impairment

An asset's carrying amount is written down to its recoverable amount, or

recoverable service amount, if the asset's carrying amount is greater than

its estimated recoverable service amount.

I)erecognition

The DOTr recognizes items of property, plant and equipment and/or any

significant part of an asset upon disposal or when no future economic

benefits or service potential is expected from its continuing use. Any gain

or loss arising on derecognition of the asset (calculated as the difference

between the net disposal proceeds and the carrying amount of the asset) is

included in the surplus or deficit when the asset is derecognized.

3.4 Changes in accounting policies and estimates

The DOTr recognizes the effects of changes in accounting policiesretrospectively. The effects of changes in accounting policy are appliedprospectively if retrospective application is impractical.

The DOTr recognizes the effects of changes in accounting estimatesprospectively by including in surplus or deficit.

The DOTr corrects material prior period errors retrospectively in the firstset of financial statements authorized for issue after their discovery by:

* Restating the comparative amounts for prior period(s) presented inwhich the error occurred; or

* If the error occurred before the earliest prior period presented,restating the opening balances of assets, liabilities and netasset/equity for the earliest prior period presented.

Effective February 2016, the DOTr adopted the Capitalization Thresholdof P15,000.00 policy as one of the criterion for recognition of the cost ofan item of Property, Plant and Equipment Thus, the following newaccounting policies are adopted:

I. Tangible items below the capitalization threshold of Pl 5,000.00 shallbe accounted as semi-expendable property.

2. These items shall be recognized as expenses or capitalized cost, iffunded from capital outlay/infrastructure funds, upon issue to the end-user.

3.5 Foreign currency transactions

Transactions in foreign currencies are initially recognized by applying the

spot exchange rate between the function currency and the foreign currency

at the transaction.

At each reporting date:

* Foreign currency monetary items are translated using the closingrate;

* Nonmonetary items that are measured in terms of historical cost in

a foreign currency shall be translated using the exchange rate at the

date of the transaction; and* Nonmonetary items that are measured at fair value in a foreign

currency shall be translated using the exchange rates at the datewhen the fair value is determined.

Exchange differences arising (a) on the settlement of monetary items, or

(b) on translating monetary items at rates different from those at which

they are translated on initial recognition during the period or in previous

financial statements, are recognized in surplus or deficits in the period in

which they arise, except as those arising on a monetary item that forms

part of a reporting entity's net investment in a foreign operation.

3.6 Revenue from Exchange Transactions

Measurement ofrevenue

Revenue shall be measured at the fair value of the consideration receivedor receivable.

Rendering of services

The DOTr recognizes revenue from rendering of services by reference to

the stage of completion when the outcome of the transaction can be

estimated reliably. The stage of completion is measured by reference to

labor hours.

When the contract outcome cannot be measured reliably, revenue isrecognized only to the extent that the expenses incurred are recoverable.

Sale of(Good

Revenue from the sale of goods are recognized when the significant risk

and reward of ownership have been transferred to the buyer, usually on

delivery of the goods and when the amount of revenue can be measured

reliably and it is probable that the economic benefit and service potentialassociated with the transaction will flow to the DOTr.

Inlerest Income

Interest income is accrued using the effective yield method. The effectiveyield discounts estimated future cash receipts through the expected life ofthe financial asset to that asset's carrying amount. The method applies thisyield to the principal outstanding to determine interest income eachperiod.

3.7 Budget information

The annual budget is prepared on a cash basis and is published in thegovernment website.

As a result of the adoption of the cash basis for budgeting purposes, aseparate Statement of Comparison of Budget and Actual Amounts ispresented showing the basis, timing or entity differences. Explanatorycomments are provided in the notes to the annual financial statements;first, the reason for overall growth or decline in the budget is stated,followed by details of overspending or under spending on line items.

The annual budget figures included in the financial statements are for theDOTr - C.O. and therefore exclude the budget for its attached agencies.These budget figures are those approved by the governing body at thebeginning and during the year following a period of consultation with thepublic.

The actual amounts under Receipts pertains to other cash collections anddo not include receipt of NCAs, while Payments pertain tocash/check/ADA disbursements.

4. Prior Period Adjustments

Fundamental errors of prior years are corrected by using the AccumulatedSurplus/(Deficit) account. Errors affecting current year's operation are charged tothe current years accounts.

The Prior Period Adjustment recorded during the year is composed of thefollowing:

Particulars AmountCorrection of Prior Years Expenses P 2,162,666.98Gain on Foreign Exchange 9,124,148.66Total Prior Period Adjustment P11,286$15.64

12

5. Cash and Cash Equivalents

5.1 Cash in Bank - Local Currency, Current Account

Accounts AmountCash in Bank-Local Currency, Current Account P26,444,885.86

Cash in Bank-L/C-Current Account ____ 26.444,885.86

5 1 1 Cash in Bank - Local Currency, Current Account balance as of31 December 2016 amounting to P26,444,885.86 representsbalance of the peso equivalent of the USD1,000,000.00 transferredfrom the Dollar Savings Account authorized per Loan Agreement.

5 2 Cash in Bank - Foreign Currency

Accounts AmountCash in Bank-Foreign Currency P591,367,81494

Cash in Bank-F/C-Savings Account P591,367,814.94

5.2.1 Cash in Bank - Foreign Currency Savings Account balance asof 31 December 2016 amounting to P591,367,814.94 representsbalance of the funding requirement for the CBRT project under the

Expanded Foreign Currency Deposit Unit (EFCDU) and CreditFacility Agreement (CFA).

6. Receivables

6.1 Inter-Agency Receivables

Accounts Current Non-Current Total

(m Php)Due from NGAs 1,713.29 0.00 1,713,29

Totals 1,713.29 0.00 1,713.29

6.1.1 The Due from NGAs Account balance of P1,713,29 as of 31December 2016 represents fund transfer to Procurement Service

(PS) for the 3"' & 4 quarter supply requirements of BRT-NationalProgram Management Office (BRT-NPMO).

7. Property, Plant and Equipment

Machinery and Equipment

7.1 Office Equipment account balance as of 31 December 2016 of

P37,000.00 represents one (1) unit LCD Projector for the use of BRT-

NPMO.

13

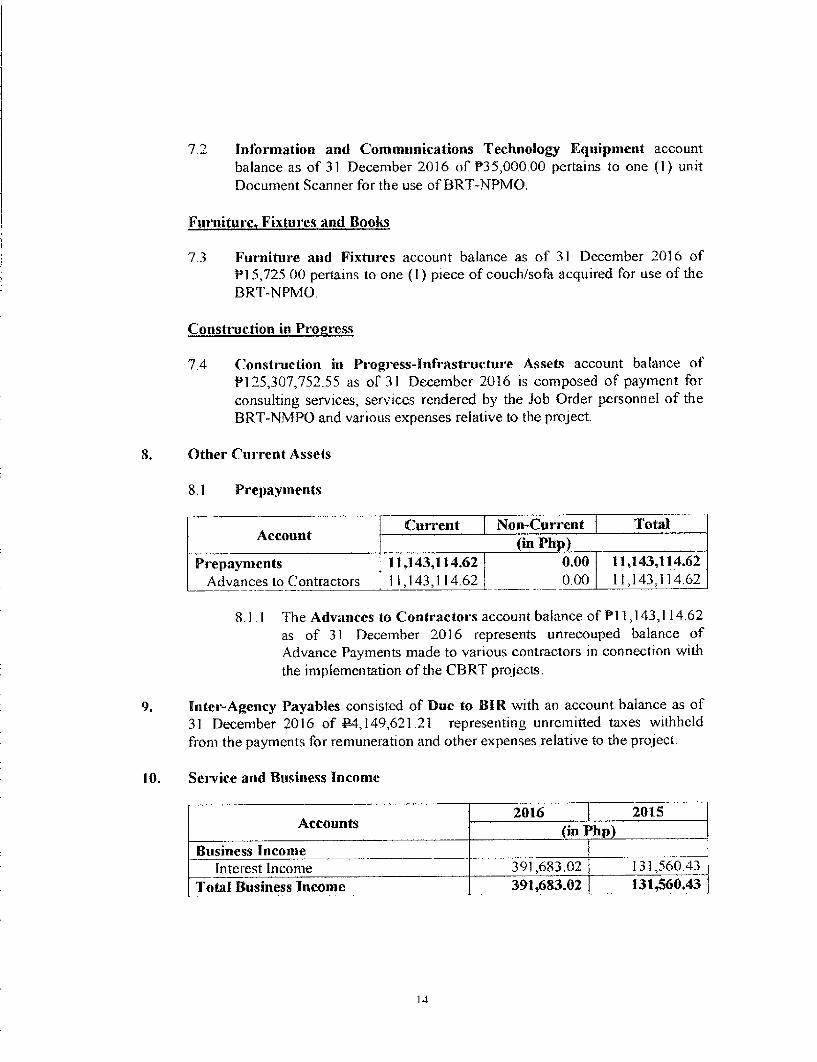

7.2 Information and Communications Technology Equipment accountbalance as of 31 December 2016 of P35,000.00 pertains to one (1) unitDocument Scanner for the use of BRT-NPMO.

Furniture, Fixtures and Books

7 3 Furniture and Fixtures account balance as of 31 December 2016 ofPI 5,725.00 pertains to one (1) piece of couch/sofa acquired for use of theBRT-NPMO.

Construction in Progress

7.4 Construction in Progress-Infrastructure Assets account balance ofP125,307,752.55 as of 31 December 2016 is composed of payment forconsulting services, services rendered by the Job Order personnel of the

BRT-NMPO and various expenses relative to the project.

8. Other Current Assets

8.1 Prepayments

Accn -Current Non-Current TotalAccount (nFi

(in Php)Prepayments 11,143,114.62 0.00 11,143,114.62

Advances to Contractors 11,143,114.62 0.00 11,143,114.62

8.1.1 The Advances to Contractors account balance of P11,143,114.62as of 31 December 2016 represents unrecouped balance ofAdvance Payments made to various contractors in connection with

the implementation of the CBRT projects.

9. Inter-Agency Payables consisted of Due to BIR with an account balance as of

31 December 2016 of P4,149,621.21 representing unremitted taxes withheld

from the payments for remuneration and other expenses relative to the project.

10. Service and Business Income

2016 2015Accounts in Ph

Business IncomeInterest Income 391,683.02 131,560.43

Total Business Income 391,683.02 131,560.43

14

11. Financial Expenses

11.1 Bank Charges

2016 2015Accounts

mPhBank Charges 1,509.76 465.25Total Financial Expenses 1,509.76 465.25

Since the project is still on-going, the above expense shall be capitalizedand reclassified to Construction-in-Progress.

12. Non-Cash Expenses

12.1 Depreciation

2016 2015

Accounts (in Php)

Depreciation-Machinery and Equipment 4,235.41 0.00Total Depreciation 4,235.41 0.00

13. Net Financial Assistance/Subsidy

Accounts 2016 2015(in Php)

Subsidy from National Government 479,936,944.52 227,289,292.00Less: Financial Assistance/Subsidy toLGUs, GOCCs NGOs/POs 0.00 0.00Net Financial Assistance/Subsidy 479,936,944.52 227,289,292.00

14. Gains

The Gain on Foreign Exchange (FOREX) account amounting toP35,762,819.83 as of 31 December 2016 represents gain on foreign exchangerealized from the account of the Cebu Bus Rapid Transit EFCDU and CreditFacility Agreement (CFA) dollar account.

15. Allotments, Obligations and Balances

Allotment OlgtosUnobligated Balance

Categorys, Current Extended.I Total Olgtos Total Reverted IExtended(in Php)

C'apiftal()dy 1,336,2(g)M)X LJ53,776,032 2 8 976,032 945,538,433 1%4,3,9 0,237"9 36.(U

15.1 Allotments released in 2016 amounted to P1,336,200,000.00, noobligation for the year, the balance is extended to CY 2017.

16. Reconciliation of SCBAA and Statement of Cash Flows

Particular AmountActual Amount on Comparable Basis as presented in the (12,049,122.59)Statement of Comparison of Budget and Actual Amount _

Basis DifferencesReceipt of Notice of Cash Allocation I 479,936,94452Payment of Prior Years Accounts Payable : (88,555,825.89)Total Basis Differences , 391,381,118.63

Timing Differences 0.00Entity Differences 0.00

Actual Amount presented in the Statement of Cash Flows 379,331,996.04

1It