association bookkeeping manual - sustainabilityxchange bookkeeping... · association bookkeeping...

TRANSCRIPT

Association Bookkeeping

Manual

For Use By NASFAM Member Associations In Conjunction With The NASFAM

Bookkeeping Workshop

SDU publication SDU-M102

NASFAM skills development unit

P.O. Box 30716

Lilongwe 3, Malawi

Sk illsDevelopmentU nit

Association Bookkeeping Manual Edition #2

DU Publication SDU-M102

s Association of Malawi (NASFAM)

ages 1-3, 10-13 have been amended with permission from the

EMAS/International Cooperative Alliance publication Cooperative

S

1998 NASFAM Skills Development Unit

National Smallholder Farmer

PO Box 30716

Lilongwe 3, Malawi

P

C

Bookkeeping- Marketing Cooperatives, London, 1977.

Foreword

This manual is intended to assist NASFAM member Smallholder Farmer

Associations to set up and maintain an association accounting system. As we will

discuss in the manual, proper bookkeeping and accounting must be a top priority of

all associations. The manual is designed to introduce the accounting system in a

simple and straightforward manner, and when possible should be used in

conjunction with the NASFAM Skills Development Unit Association Bookkeeping

Workshop. In using this manual please be aware that the manual is not an

exhaustive manual for association accounting, rather it puts the fundamental system

into place for immediate usage. With this in mind, association bookkeepers,

committees, and advisors should feel free to contact the NASFAM Accounting

and Auditing Unit with any questions or problems they may have. The system

is being implemented for the first time and therefore some minor adjustments and

additions will have to be made.

Please be aware that the system outlined in this manual is designed specifically for

usage by NASFAM member associations. It takes into account a Smallholder

Farmers Association’s particular accounting needs, with an eye on simplicity and

accuracy in use. The different members of NASFAM do in fact have different crops

and therefore marketing operations and therefore an accounting system will have to

adjust to their operation. Associations such as the Mulanje Associations will have to

adapt the system outlined in this manual for use with their association’s particular

needs. This exercise will be done in conjunction with the Accounting and Auditing

Unit and the Skills Development Unit.

This manual is one of many services that NASFAM offers member associations. I

hope associations find the manual of assistance in maintaining their accounts so that

NASFAM and area associations can continue to assist member farmers. Once

again, please feel free to submit any comments or question you or your association

may have regarding the manual or the system.

Robert Gibson Skills Development Unit Advisor

Table of Contents

I. The why and what of association bookkeeping

1.1 Why Bookkeeping? 1 - 2

1.2 What is Bookkeeping? 2

1.3 What is the Job Of The Bookkeeper? 2 - 3

1.4 Auditors 3 - 4

1.5 Internal Checkers 5

II. Accounting Basics

2.1 Accounting Terms 5 - 7

2.2 The Double Entry System 7 - 8

III. Introduction to the Smallholder Association Accounting System

3.1 General ledger 12 - 18

3.2 Petty Cash/Expense Ledger 18 - 20

3.3 Sub-Ledgers 21 - 25

3.4 Ledger And Program Identification Numbers 26

IV. Supporting Documents

4.1 Receipts 29 - 31

4.2 Delivery Invoice 32 - 33

4.3 Cash or Cheque Payment Voucher 33 - 34

4.4 Cash Request Form 35 - 36

4.5 Association Cash Count Form 36 - 37

4.6 Bank Reconciliation Statement 37 - 38

V. Association Accounting System in Use

5.1 What Doe the Association Need to Start the System? 41

5.2 Preparing the Accounts to Begin Bookkeeping 41 - 42

5.3 When To Make Entries Into The Accounts 43

5.4 Making Primary Entries

5.4.1 Membership Fee Transactions 43 - 48

5.4.2 Petty Cash Expense Transactions 48 - 51

5.4.3 Fertilizer Program Transactions 51 - 58

5.4.4 Hessian Cloth Program Transactions 58 - 63

5.4.5 Bank Transactions 63 - 65

5.4.6 Donations From Organizations 65 - 66

5.4.7 Payment Of Transport Commissions 66

5.4.8 Retail Sales 67 - 71

5.4.9 Retail Petty Cash Transactions 71

5.5 Easy Reference Transaction Chart 72 - 77

VI. Closing The Accounts And Preparing Financial Reports

5.1 Closing The Accounts- Month End 83 - 84

5.2 Trial Balance 85 - 86

5.3 Stock On Hand And Valuation Report 87 - 88

5.4 Balance Sheet 89 - 90

5.5 Retail Sales Trading Account 91 - 92

5.6 Month End Income Report 93 - 94

5.7 Trading Profit and Loss On Commercial Activities 95 - 96

Report

5.8 Report To Committee 97 - 99

5.9 Year End Financial Reports 100

5.10 Reporting Checklist 101-102

The Why and What of Association Bookkeeping

1.1 Why Bookkeeping? As anybody associated with an association can tell you, large amounts of money

flow through an association within a year. Associations handle millions of Kwacha

annually for the purpose of operating expenses, fertilizer programs, transport service

fees, etc. With such large quantities of cash, there are opportunities for loss of

money, mismanagement, theft, and a variety of other problems that ultimately

threaten the livelihood of the association.

Associations deal with smallholder farmer money, of which the farmer members

depend on for the livelihood of themselves and their families. To date association

accounts have been kept in an often informal manner, with areas for improvement in

receipting, accounts setup, financial reports, etc. Proper association bookkeeping

must be a first priority of associations and management as association move into

the future.

The purpose of bookkeeping is three fold:

� To maintain an accurate financial picture of the business, in such a way, that the state of its finances can be simply, clearly and accurately revealed at any time.

� To make it possible for the accuracy of the accounts to be quickly

checked, to avoid errors or fraud. � To serve as a management tool by providing the information required

for decision making and for planning future activities.

Remember that the member farmers are also the owners of the association. They

need to know how their business is doing and how their funds are being used.

Members elect a committee to direct and control the affairs of their business and a

manager is appointed to run the day to day operations. The committee and the

Guide To Association Bookkeeping 1

manager need information that is complete, accurate, and up to date on the

operations of the association to be able to make decisions. The bookkeeping system

in use must therefore show:

How much the association owns. These are its assets and show the use being made of these funds.

How much the association owes. These are its liabilities and indicate the

source of the funds in use in the association.

Whether the association has financial stability and is able to pay its debts as they arise

Whether the association is operating efficiently covering its costs and

providing a net surplus

1.2 What is Bookkeeping?

Bookkeeping is the process of recording all business transactions. Transactions

involve the exchange of goods and services at a stated price, and therefore an

exchange of money. Stated differently:

Bookkeeping is concerned with correctly entering permanent written

records of financial transactions into the books of account of the

association.

A financial transaction arises in the course of the business when there

is a transfer of money or something having a money value.

1.3 What is the job of the bookkeeper?

The bookkeeper in an association will most often be the association manager, or

perhaps another member of the association staff for larger association. The work of

the bookkeeper is very important and therefore a qualified individual must be in

charge of the duty. Some of the qualities of a good bookkeeper are: 1. Attention to detail and accuracy

2. Mathematical knowledge

3. Knowledge of calculator use Guide To Association Bookkeeping 2

4. Basic accounting knowledge

5. Trustworthy and stable

The bookkeeper has a large responsibility and therefore must be up to the job at

hand. The work of the bookkeeper includes:

Keeping complete and accurate re cords of every financial transaction in which the association is involved.

Checking the accuracy of these records at regular intervals.

Preparing final accounts and a balance sheet at the end of every financial

year, ready for audit and later consideration by the committee and the members.

Preparing reports for the manager and the committee on the financial position

of the association during the financial year.

NOTE: A committee member should not be the bookkeeper that is not their role in the association. We will look later at what their role should be.

1.4 Auditors: An auditor is a skilled accountant whose responsibility it is to check and verify the

accounts of the association at the end of the financial year and at any other time as

NASFAM may consider necessary. The auditor is independent of the association

and reports to the association committee, members, and NASFAM. NASFAM

provides an auditor to area associations as a service that is included in the

association’s yearly membership fees. The NASFAM auditor will make regular

checks of the association accounts, and will assist the association in completing

year-end reports and preparing for annual general meetings. An auditor is there to

assure that accounts are kept accurately and that ‘honest people remain honest’ as

well as to educate the association and the bookkeeper about correct procedures and

to correct any mistakes they may be making.

1.5 Internal Checker: An Internal Checker is appointed by the association to conduct regular checks for the

members on the books, assets, and activities of the association. Whereas an auditor

will do an in depth look at the accuracy of the accounts, the Internal Checker will

Guide To Association Bookkeeping 3

complete a quick regularly scheduled check of the accounts to assure that basic

policy is being followed. The Internal Checker can do a simple cash count to make

sure the cash in the cash box is equal to that in the cash account, as well as

assuring that all receipts have been entered into the accounts. The association

committee should decide the role the internal checker will play, and exactly what

procedures they will follow. After completing regular check the Internal Checker will

report to the committee, and membership. If any suspected anomalies are found,

the matter should be referred immediately to the NASFAM Auditor.

Guide To Association Bookkeeping 4

Accounting Basics

2.1 Accounting Terms

Records of Original Entry: Records of Original Entry as the name implies are the initial documents upon which

a transaction is recorded, and are completed immediately when a financial

transaction occurs. These documents will become the source of future ledger

entries, and therefore they must be completed with great care. At present records

of original entry can be bought at a local stationery stores. NASFAM will look into

purchasing specially printed receipts for associations in the near future. Some

examples of records of original entry are:

-Receipts and Payment Vouchers

-Invoices

-Cheque books, bank deposit and withdrawal books

-Cash sale receipts

All unused receipts must be kept securely in the association cash box, or

another secure place.

Assets:

They are what the association owns, any good or service that can be given a money

value is called an asset. Some examples of assets are:

Cash- Currency, checks, bank drafts.

Accounts Receivable- Money due from association members for merchandise, entrance fees, etc.

Merchandise- Goods produced or bought by the association for sale.

Equipment- Articles expected to last for a period of years, that assist in the

operations of the associations. Guide To Association Bookkeeping 5

Fixed Assets- Those assets which are held for an extended period of time

(land, buildings, equipment, etc.)

Prepaid expenses- Those expenses that have been paid in advance. Such as rent paid in advance for the year.

Liabilities:

Shows what the association owes. They include items such as overdue rent,

overdue transport payments, loans, etc. Liabilities are often recorded as an account

payable.

Account:

A record containing details for a transaction for a specific item (Assets, capital,

liabilities) Some accounts that association will keep are: Cash Account Membership Fees Account Expense/Petty Cash

Account

Bank Account Retail Sales Account Receivables Account

Input Sales Account Service Fees/Revenue Account Etc.

Ledger:

A ledger is a book in which accounts are entered. The ledger is ruled to include all

details of the transaction. The association accounting system will contain accounts

in sub-ledgers and the general ledger. The ledgers will be examined in detail in the

next section.

An account ledger looks like this:

Date Entry #

Details

Rcpt. #

Debit Credit Balance

16-07

01

Mwaiwathu # 63062

500

CR 500-

Most accounts have a column to put the date, details of the transaction, a debit and

a credit column, and finally the balance of the account. We will look at the account in

more detail further in the manual.

Guide To Association Bookkeeping 6

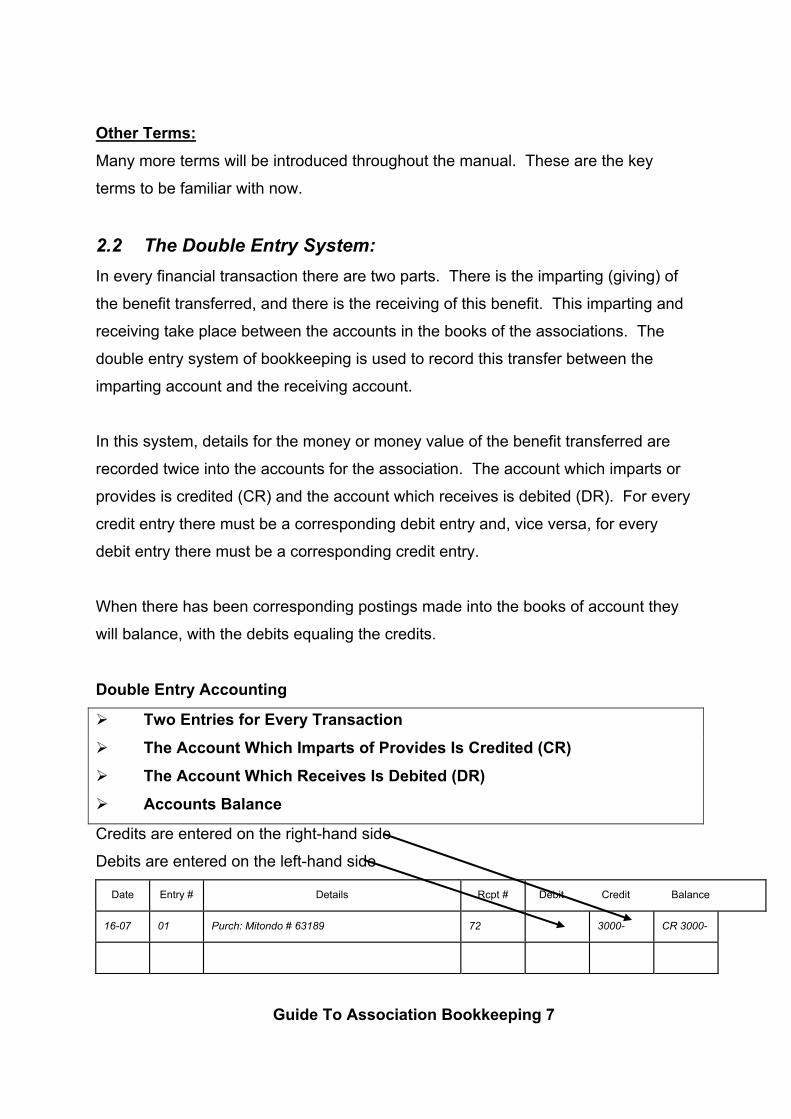

Other Terms:

Many more terms will be introduced throughout the manual. These are the key

terms to be familiar with now.

2.2 The Double Entry System: In every financial transaction there are two parts. There is the imparting (giving) of

the benefit transferred, and there is the receiving of this benefit. This imparting and

receiving take place between the accounts in the books of the associations. The

double entry system of bookkeeping is used to record this transfer between the

imparting account and the receiving account.

In this system, details for the money or money value of the benefit transferred are

recorded twice into the accounts for the association. The account which imparts or

provides is credited (CR) and the account which receives is debited (DR). For every

credit entry there must be a corresponding debit entry and, vice versa, for every

debit entry there must be a corresponding credit entry.

When there has been corresponding postings made into the books of account they

will balance, with the debits equaling the credits.

Double Entry Accounting

Two Entries for Every Transaction

The Account Which Imparts of Provides Is Credited (CR)

The Account Which Receives Is Debited (DR)

Accounts Balance

Credits are entered on the right-hand side

Debits are entered on the left-hand side

Date Entry #

Details

Rcpt #

Debit Credit Balance

16-07

01

Purch: Mitondo # 63189

72

3000-

CR 3000-

Guide To Association Bookkeeping 7

When to debit and when to credit: Debit To:

Credit To:

Increase assets (cash)

Decrease assets (cash)

Increase an expense

Decrease an expense

Increase purchases

Decrease purchases

Increase liability

Decrease liability

Decrease sales or

revenue

Increase sales or

revenue

**If you remember anything from the above chart, remember:

When you increase cash or bank balance a debit entry is made.

When you decrease cash or bank balance, a credit entry is made.

� If you know these entries you will always be able to figure out the

other corresponding entry. In sections III and IV the double entry

system and the correct entries to accounts will be explained in

detail.

Guide To Association Bookkeeping 8

NOTES

Guide To Association Bookkeeping 9

NOTES

Guide To Association Bookkeeping 10

Introduction to the Smallholder Association Accounting System

The association accounting system consists of sub-ledgers and the general ledger.

The various accounts that have been previously mentioned are contained in these

ledgers. The ledgers are arranged as follows:

*Insert: Diagram of ledger system

Guide To Association Bookkeeping 11

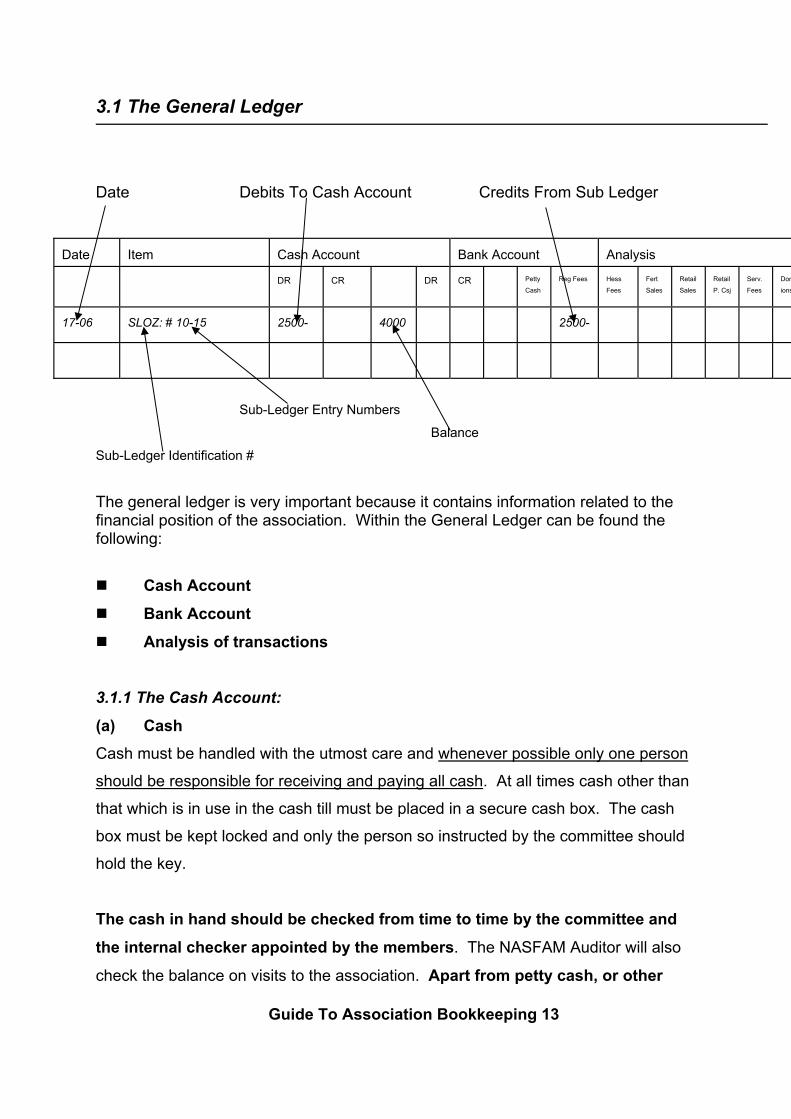

3.1 The General Ledger

Date Debits To Cash Account Credits From Sub Ledger

Date

Item

Cash Account

Bank Account

Analysis

DR

CR

DR

CR

Petty

Cash

Reg Fees

Hess

Fees

Fert

Sales

Retail

Sales

Retail

P. Csj

Serv.

Fees

Don

ions

17-06

SLOZ: # 10-15

2500-

4000

2500-

Sub-Ledger Entry Numbers

Balance

Sub-Ledger Identification # The general ledger is very important because it contains information related to the financial position of the association. Within the General Ledger can be found the following:

Cash Account

Bank Account

Analysis of transactions

3.1.1 The Cash Account:

(a) Cash

Cash must be handled with the utmost care and whenever possible only one person

should be responsible for receiving and paying all cash. At all times cash other than

that which is in use in the cash till must be placed in a secure cash box. The cash

box must be kept locked and only the person so instructed by the committee should

hold the key.

Guide To Association Bookkeeping 13

The cash in hand should be checked from time to time by the committee and

the internal checker appointed by the members. The NASFAM Auditor will also

check the balance on visits to the association. Apart from petty cash, or other

cash held to make expected payments, all cash received should be banked at

the end of every day in its entirety.

Although it is easy to say that cash should be banked daily Smallholder Associations

must address the fact that they may operate in areas where banking facilities are not

readily available. Therefore a banking policy should be developed by the

association, a sample policy would be ‘Once cash box receipts reach K10,000, the

receipts must be banked in their entirety on the next working day’. So if the

Nkhamanga Association receives receipts of K11,230 on Friday, the association

manager must schedule a trip to Mzuzu to bank the cash on the following Monday.

Will this policy work? What policy should NASFAM and local committee set?

(b) Cheques Received:

For bookkeeping purposes all cheques received by the association are treated as

cash. Cheques should only be accepted if the person writing the cheque is known to

be in good financial standing (100% sure that the money is available in the bank). If

the person may not be in good financial standing the association should demand a

cash payment, up front deposit, etc. Generally, post-dated cheques (those with a

date in the future) should not be accepted.

(c) Receipt Of Cash and Proper Receipting:

A receipt must be issued whenever cash is received. A receipt must show: 1. Receipt #

2. Name of association

3. Name of person paying the cash

4. Purpose for which cash received

5. Date cash received

7. Signature of person receiving the cash

8. Page # posted to in ledger

Usually the receipt is made out in duplicate using a carbon paper. The top copy is

issued to the person paying the cash. The bottom copy is kept by the association as

the record of original entry from which the ledger will be posted. The entry is made

into the ledger recording the following items:

Guide To Association Bookkeeping 14

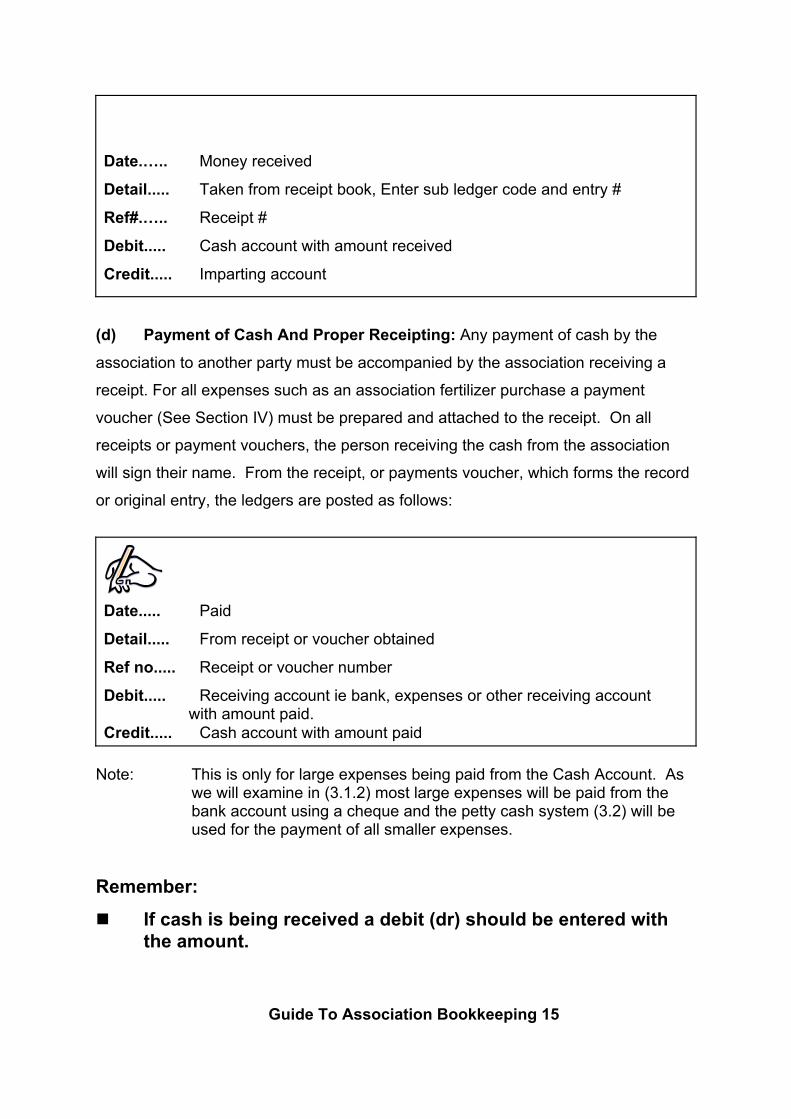

Date.….. Money received

Detail..... Taken from receipt book, Enter sub ledger code and entry #

Ref#.….. Receipt #

Debit..... Cash account with amount received

Credit..... Imparting account

(d) Payment of Cash And Proper Receipting: Any payment of cash by the

association to another party must be accompanied by the association receiving a

receipt. For all expenses such as an association fertilizer purchase a payment

voucher (See Section IV) must be prepared and attached to the receipt. On all

receipts or payment vouchers, the person receiving the cash from the association

will sign their name. From the receipt, or payments voucher, which forms the record

or original entry, the ledgers are posted as follows:

Date..... Paid

Detail..... From receipt or voucher obtained

Ref no..... Receipt or voucher number

Debit..... Receiving account ie bank, expenses or other receiving account with amount paid. Credit..... Cash account with amount paid

Note: This is only for large expenses being paid from the Cash Account. As

we will examine in (3.1.2) most large expenses will be paid from the bank account using a cheque and the petty cash system (3.2) will be used for the payment of all smaller expenses.

Remember:

If cash is being received a debit (dr) should be entered with the amount.

Guide To Association Bookkeeping 15

If cash is being paid out a credit (cr) should be entered with the amount.

3.1.2 The Bank Account

(a) Current account (Same as Checking Account)

Most associations have already opened a current account at their nearest bank in

following with the by laws of the association. The bank will issue deposit slips,

withdrawal forms, and a cheque book to the association. As associations process

larger and larger amounts of money, there is a need that purchases, such as those

for inputs, be issued on association cheques, not through cash or by means of a

third party cheque book. The committee when opening the account should inform

the bank officers of those people authorized to sign cheques and withdrawal slips,

and the bank will take specimen signatures from these officers. The cheque book

must be kept secure in the association cash box at all times. The person

appointed to handle the cash of the association will make the deposits to this current

account at the bank. If an association does not have a current account, they

should do so immediately.

(b) Savings Accounts

Associations may open a savings account with a local bank if they are able to tightly

control the cash flow requirements of the association. Savings accounts offer

associations interest payments for keeping the money with their bank but

withdrawals tend to be much more difficult. Instead of payments being made with a

simple cheque, the association signatories must all travel to the bank to withdrawal

cash or a money order. Such a procedure is costly to the association and is difficult

to control. Therefore associations should only have cash in a savings account if they

are sure that the money will not be needed for an extended period of time (say six

months), at which point they can transfer it to the current account.

(c) Bank Deposits

Pages in the bank deposit book should be processed at the bank and the association

copy retained. From these records of original entry, entries will be made into the

Guide To Association Bookkeeping 16

ledgers.

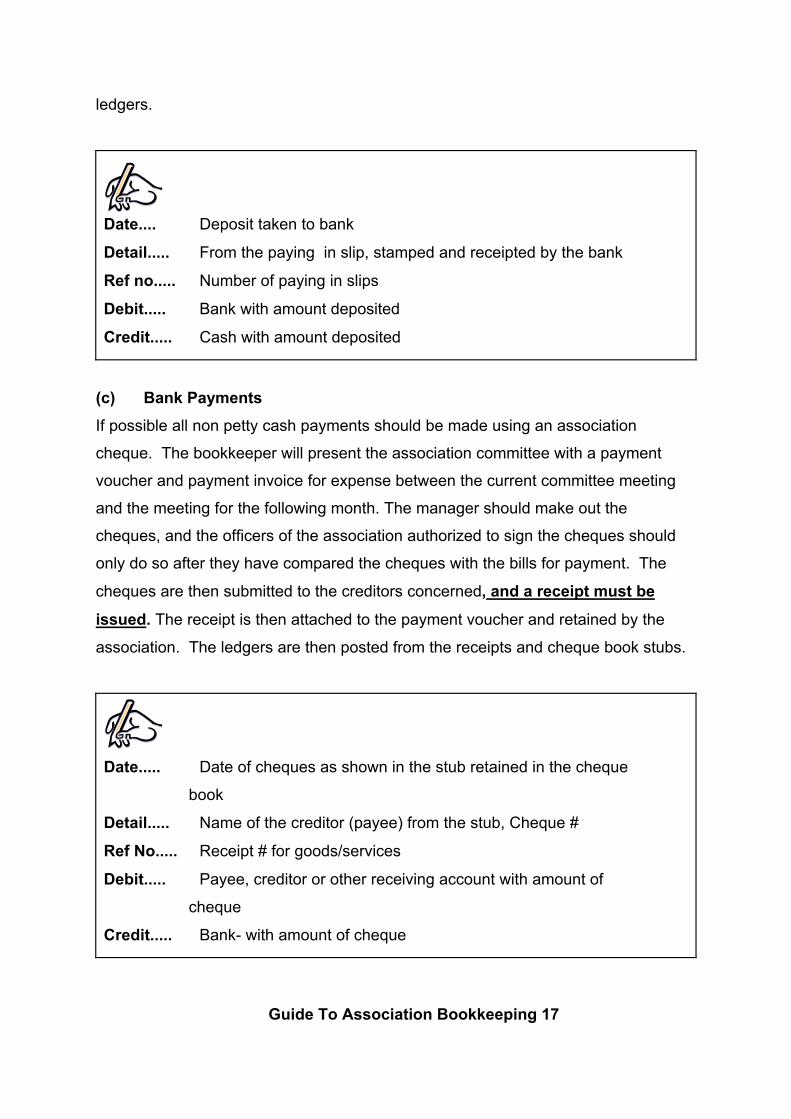

Date.... Deposit taken to bank

Detail..... From the paying in slip, stamped and receipted by the bank

Ref no..... Number of paying in slips

Debit..... Bank with amount deposited

Credit..... Cash with amount deposited

(c) Bank Payments

If possible all non petty cash payments should be made using an association

cheque. The bookkeeper will present the association committee with a payment

voucher and payment invoice for expense between the current committee meeting

and the meeting for the following month. The manager should make out the

cheques, and the officers of the association authorized to sign the cheques should

only do so after they have compared the cheques with the bills for payment. The

cheques are then submitted to the creditors concerned, and a receipt must be

issued. The receipt is then attached to the payment voucher and retained by the

association. The ledgers are then posted from the receipts and cheque book stubs.

Date..... Date of cheques as shown in the stub retained in the cheque

book

Detail..... Name of the creditor (payee) from the stub, Cheque #

Ref No..... Receipt # for goods/services

Debit..... Payee, creditor or other receiving account with amount of

cheque

Credit..... Bank- with amount of cheque

Guide To Association Bookkeeping 17

If a deposit is being made to the bank account a debit (dr) should be

entered with the amount.

If a withdrawal or a payment is being made by check from the bank account a credit (cr) should be entered with the amount.

3.1.3 Analysis

This section of the General ledger allows the association to chart and analyze

transactions. As can be seen, each sub-ledger account is represented in the

analysis section. As entries are written in the general ledger to the cash or bank

account a corresponding entry should be made to the analysis section under the

appropriate heading. To denote whether a credit or a debit is being made to the

account a small (DR) or (CR) should be entered above or to the left of the amount

being entered to the column (See the example below). We will look at the analysis

section in use in section IV and V.

3.1.4 Note On Entries To the General Ledger

If every transaction had to be written two times in its entirety it would be a lot of work

for the bookkeeper. To make the workload on the bookkeeper lighter, and to save

paper, entries into the general ledger are made as a summary of each sub-ledger,

not as single transactions. Every day the bookkeeper will first make entries into

each sub-ledger from the days transactions, he or she will then summarize each

sub-ledger to the general ledger through a single entry that lists the Sub-Ledger and

the entry numbers. Therefore the number of general ledger entries will equal the

number of sub-ledgers that had a transaction recorded to them. (See our example

at the beginning of the section.)

3.2 Petty Cash/Expense Ledger

Date Entry # Debit Money In Analysis Of Expense

Guide To Association Bookkeeping 18

Transactions

Analysis

Date

Entry

#

Details

DR

CR

Wage

s

Trans

Food

Stat.

Other

16-07

01

Replenish Cheque # 7102 2000

2000

17-08

02

PEM 22, L. Phiri

100- 190-

0

100-

-AND SO ON-

Details Of Transaction Credit Money Out Balance

Guide To Association Bookkeeping 19

As associations grow in size, it is necessary to implement the usage of a petty cash

system. A petty cash system allows for small expense to be paid from the petty cash

account instead of the Cash Account or the Bank Account. Such a system also

allows the association to analyze the types of expense incurred over the course of a

month, or other period of time.

The advantage of a petty cash system is:

• The work of making numerous small expenses could be made by someone other that the bookkeeper, such as the clerk. Maintaining petty cash can be a large job, therefore the association should carefully access whether a clerk is qualified before handing over this task. In most associations the manager should retain this task of keeping the association petty cash (Not to be confused with SADP petty cash).

• The number of entries into the general ledger is significantly reduced. Instead

of posting every expense to the general ledger, posting only needs to be done one or two times per month.

• It follows the amount budgeted for the monthly petty cash expenses and

therefore allows for the expenses of the month to be both controlled and analyzed.

Association bookkeepers use a system called the imprest system to keep the petty

cash account. Each month an amount will be given to the person keeping petty cash

to meet the expense needs of the month. The person keeping petty cash will then

pay out from this money the expenses of the month. At the end of the month the

petty cashier totals the amount spent from the petty cash and this exact amount will

be taken from the cash account and transferred to petty cash, leaving the petty

cashier with the same amount that he or she originally started with. If the need

increases for the month another transaction will also be made to address this. This

system will be looked at in more detail in Section IV and V.

Guide To Association Bookkeeping 20

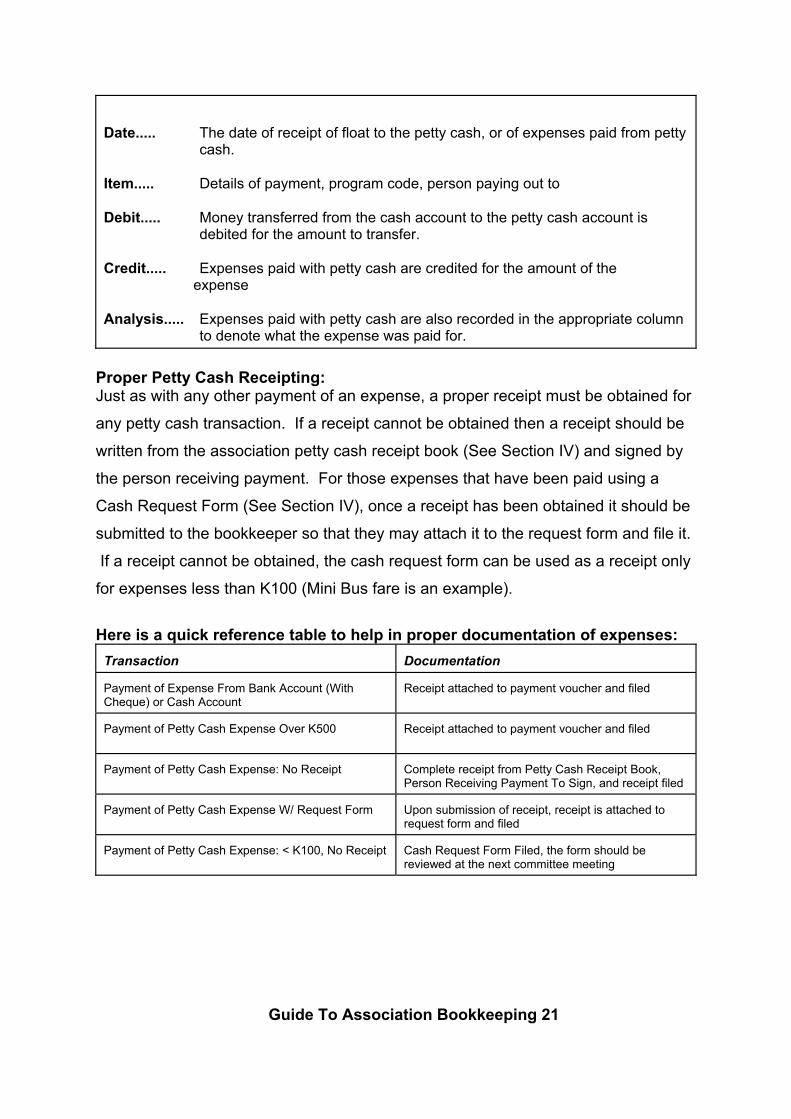

Date..... The date of receipt of float to the petty cash, or of expenses paid from petty cash.

Item..... Details of payment, program code, person paying out to Debit..... Money transferred from the cash account to the petty cash account is

debited for the amount to transfer. Credit..... Expenses paid with petty cash are credited for the amount of the expense Analysis..... Expenses paid with petty cash are also recorded in the appropriate column

to denote what the expense was paid for. Proper Petty Cash Receipting: Just as with any other payment of an expense, a proper receipt must be obtained for

any petty cash transaction. If a receipt cannot be obtained then a receipt should be

written from the association petty cash receipt book (See Section IV) and signed by

the person receiving payment. For those expenses that have been paid using a

Cash Request Form (See Section IV), once a receipt has been obtained it should be

submitted to the bookkeeper so that they may attach it to the request form and file it.

If a receipt cannot be obtained, the cash request form can be used as a receipt only

for expenses less than K100 (Mini Bus fare is an example).

Here is a quick reference table to help in proper documentation of expenses: Transaction

Documentation

Payment of Expense From Bank Account (With Cheque) or Cash Account

Receipt attached to payment voucher and filed

Payment of Petty Cash Expense Over K500

Receipt attached to payment voucher and filed

Payment of Petty Cash Expense: No Receipt

Complete receipt from Petty Cash Receipt Book, Person Receiving Payment To Sign, and receipt filed

Payment of Petty Cash Expense W/ Request Form

Upon submission of receipt, receipt is attached to request form and filed

Payment of Petty Cash Expense: < K100, No Receipt

Cash Request Form Filed, the form should be reviewed at the next committee meeting

Guide To Association Bookkeeping 21

3.3 Sub-Ledgers Date Sub-Ledger Name Details Of Transaction Balance Sub-Ledger: Membership Reg Pg# 1 DATE

ENTR

Y #

DETAILS

RCT#

DEBIT

CREDIT

05-05

01

Alinafe # 20123

0025

500-

CR 500-

Entry # Receipt # Credit Entry (Account is giving

something) Sub-Ledgers contain all those accounts outside of the general ledger and petty cash

ledger. They include a variety of accounts such as input sales accounts, service fee

account, donations account, etc.

3.3.1 Service Fee / Revenue Sub-Ledger: This account keeps a record of all

service fees obtained by the association for a variety of programs such as transport,

hessian cloth, retail sales, green pac sales, input programs, etc. Service fees are

transferred to the service fee account at the end of a particular program from the

specific program Sub-Ledger.

Guide To Association Bookkeeping 22

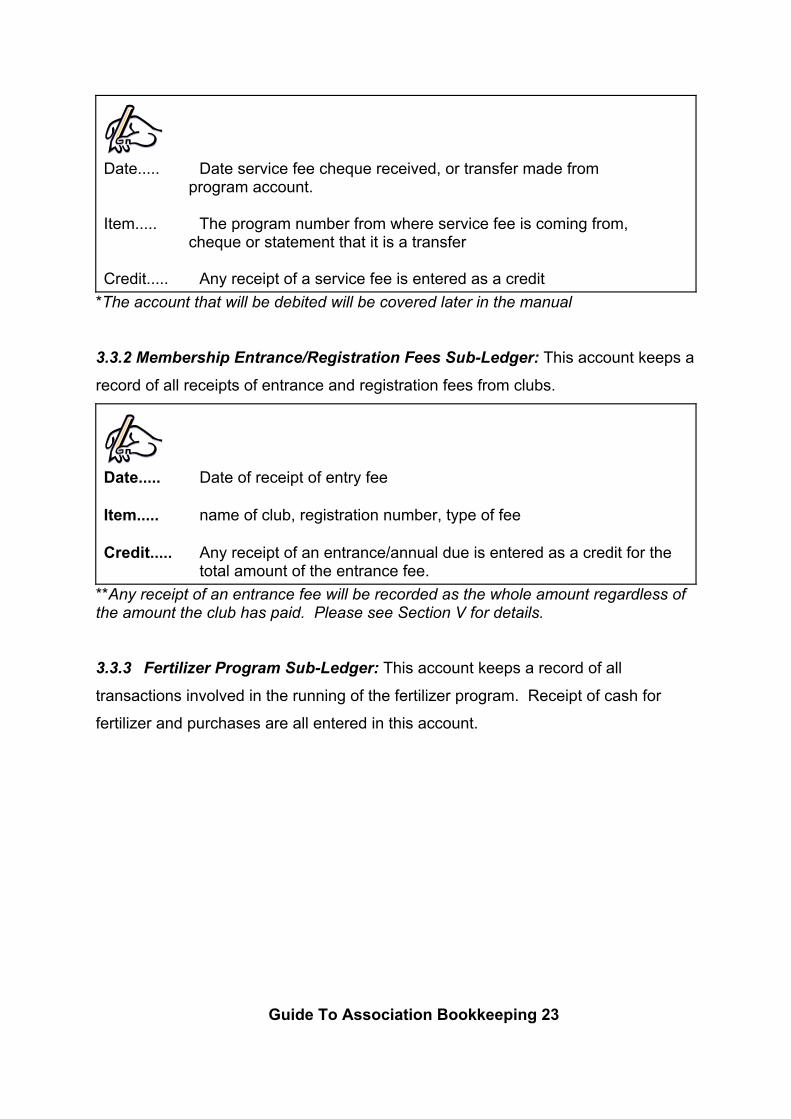

Date..... Date service fee cheque received, or transfer made from program account. Item..... The program number from where service fee is coming from, cheque or statement that it is a transfer Credit..... Any receipt of a service fee is entered as a credit

*The account that will be debited will be covered later in the manual

3.3.2 Membership Entrance/Registration Fees Sub-Ledger: This account keeps a

record of all receipts of entrance and registration fees from clubs. Date..... Date of receipt of entry fee Item..... name of club, registration number, type of fee Credit..... Any receipt of an entrance/annual due is entered as a credit for the

total amount of the entrance fee. **Any receipt of an entrance fee will be recorded as the whole amount regardless of the amount the club has paid. Please see Section V for details. 3.3.3 Fertilizer Program Sub-Ledger: This account keeps a record of all

transactions involved in the running of the fertilizer program. Receipt of cash for

fertilizer and purchases are all entered in this account.

Guide To Association Bookkeeping 23

Date..... Date of receipt of cash payment, or date of purchase Item..... Receipt of cash- name of club/person, club registration #

Purchase- name of supplier, cheque number Debit..... All purchase of fertilizer will be debited for the total purchase amount.

At the end of the program the amount remaining in the account will be transferred to the service fee account by entering a debit for the total amount.

Credit..... All sales paid in cash will be credited for the total amount of the order

3.3.4 Retail Sales With Analysis Sub-Ledger: This account records the sales of

various items by the association (bailing paper, hoes, plastic, etc.). Daily

sales receipts are entered into the Sub-Ledger daily. By also making an entry

under the analysis column under the appropriate item sold, the association is

able to analyze the sales of particular items. This system is appropriate only

for sales made on an informal basis. When association open retail supply

shops, an accounting system will have to be designed specifically for that

purpose.

Date Description Of Sale Credit Sales Amount

Date

Entry #

Item

Rct. #

Retail Analysis

DR

CR

Item

Twine

Item

B Paper

Item

Hoes

Item

Item

15-04

12

Sale: 2m B Paper, Mem #

23

14

30-

30-

Entry # Receipt # Item Sold

Guide To Association Bookkeeping 24

Date..... The date of sales or purchase of retail items Item..... The type of product sold and quantity, Member # Debit...... Any purchase of items for sale is debited for the total purchase amount Credit..... Any sales of items is credited for the total sales amount Analysis..... Sales: The total sales amount is entered under the appropriate sales item.

Purchases: The total purchase amount is entered under the appropriate sales item.

3.3.5 Donations Sub-Ledger: All donations to the association are entered in this

account. Some examples of donations would be demo-plot, field days, etc..

Date...... Date the donation is received Item..... Who donation is from, what for, cheque # Credit..... All donations to the association are credited for the total amount of the donation.

3.3.5 Accounts Receivable Sub-Ledger: This account shows the amount of

money that an outside party or a member owes the association. If a member

has only paid part of the membership fee, or an input supplier is to pay a

rebate or levy, these items are called accounts receivable. Although they

have not yet been received by the association they can be included as assets.

Date..... Date the fee, levy, etc.. Was to be paid

Guide To Association Bookkeeping 25

Item..... Name of debtor, who is owing association, and for what

Debit..... Any money owed to the association is debited for the total amount owed - Credit..... Upon receipt of payment the account is credited for the amount received

Guide To Association Bookkeeping 26

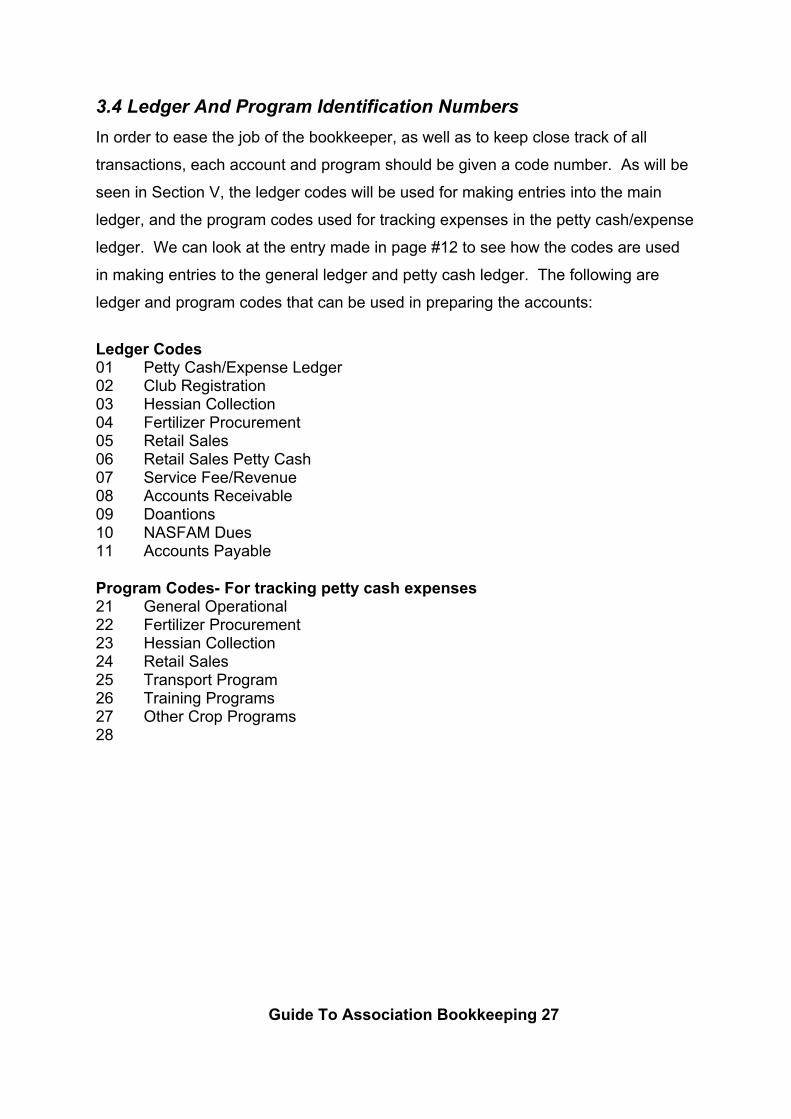

3.4 Ledger And Program Identification Numbers

In order to ease the job of the bookkeeper, as well as to keep close track of all

transactions, each account and program should be given a code number. As will be

seen in Section V, the ledger codes will be used for making entries into the main

ledger, and the program codes used for tracking expenses in the petty cash/expense

ledger. We can look at the entry made in page #12 to see how the codes are used

in making entries to the general ledger and petty cash ledger. The following are

ledger and program codes that can be used in preparing the accounts:

Ledger Codes 01 Petty Cash/Expense Ledger 02 Club Registration 03 Hessian Collection 04 Fertilizer Procurement 05 Retail Sales 06 Retail Sales Petty Cash 07 Service Fee/Revenue 08 Accounts Receivable 09 Doantions 10 NASFAM Dues 11 Accounts Payable Program Codes- For tracking petty cash expenses 21 General Operational 22 Fertilizer Procurement 23 Hessian Collection 24 Retail Sales 25 Transport Program 26 Training Programs 27 Other Crop Programs 28

Guide To Association Bookkeeping 27

Notes

Guide To Association Bookkeeping 28

Notes

Guide To Association Bookkeeping 29

Supporting Documents

A comprehensive accounting system must have a series of documents used to

support the entries into the accounts. Supporting documents such as receipts,

delivery invoices, cash count forms, etc., leave a paper trail so that all transactions

can be tracked to their inception. It must be noted that supporting documents are as

important as entries into the accounts, and therefore it is a requirement that they be

used, and stored for an appropriate amount of time. This is a quick list of supporting

documents and their usage, the documents will be examined more closely and put to

use in Section V. Association Accounting System In Use.

4.1 Receipts

(a) Sales Receipts

Sales receipts record transactions between the association and members. As we

examined in Section II, every transaction that the association carries out involving

cash must include the production of a receipt. If cash is paid by a member for

fertilizer, a receipt must be drawn with the details of that transaction.

Sample Receipt:

Guide To Association Bookkeeping 30

#8 15-07-98 RB 007 Date: 15-07-98 Name: Mambo Club Reg # 271023 Item: 99 Mem Fees

Paid in full 15-07 Total: K500- Rcv. Signature: Gift Phiri

• Date of the transaction • Name of person submitting cash/cheque. Receipt should include the club name

and registration number as well. • Details of transactions. Items being purchased with cash/cheque. Total amount

of purchase per item should be recorded to the left hand side • Total cash received • Signature of person receiving cash/cheque • Write Paid In Full And Date upon full payment • Entry # to Sub-Ledger and date posted **A separate receipt book should be used for each different program. (b) Payment Receipts As we examined in Section III, every payment of an expense must be accompanied

by a receipt. For most expenses the person receiving payment will issue a receipt

Guide To Association Bookkeeping 31

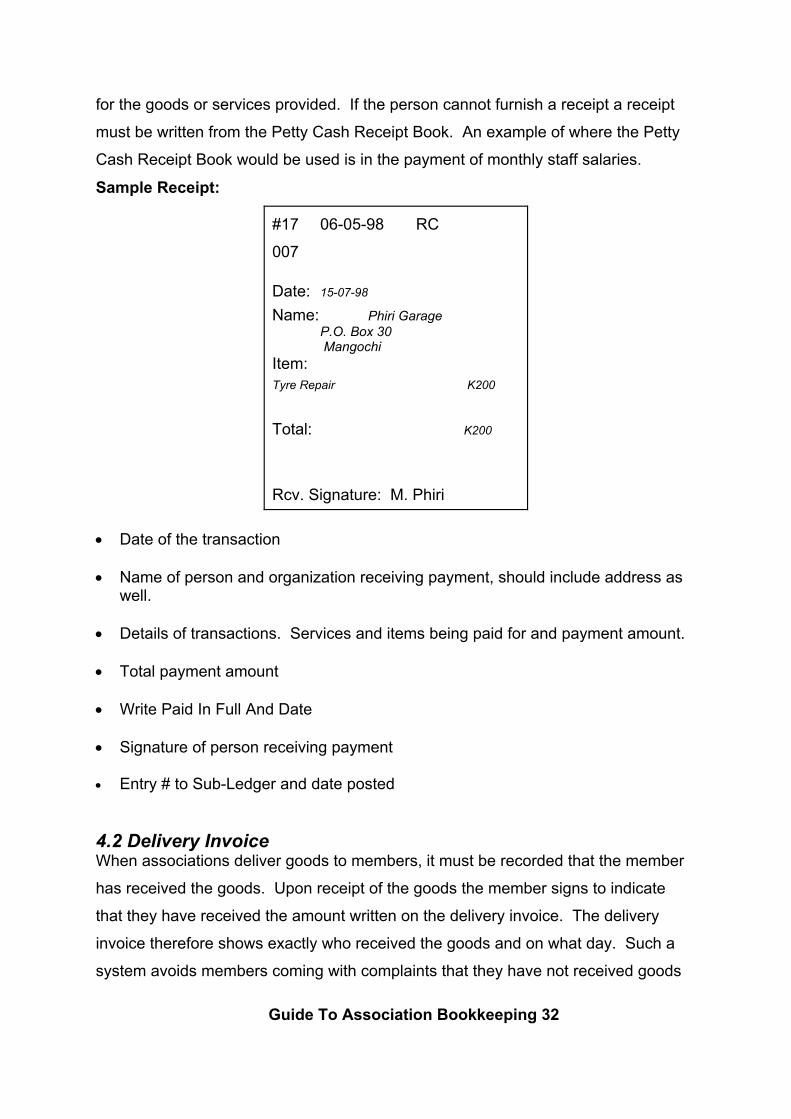

for the goods or services provided. If the person cannot furnish a receipt a receipt

must be written from the Petty Cash Receipt Book. An example of where the Petty

Cash Receipt Book would be used is in the payment of monthly staff salaries.

Sample Receipt: #17 06-05-98 RC

007 Date: 15-07-98 Name: Phiri Garage P.O. Box 30 Mangochi Item:

Tyre Repair K200

Total: K200

Rcv. Signature: M. Phiri

• Date of the transaction • Name of person and organization receiving payment, should include address as

well. • Details of transactions. Services and items being paid for and payment amount. • Total payment amount • Write Paid In Full And Date • Signature of person receiving payment • Entry # to Sub-Ledger and date posted 4.2 Delivery Invoice When associations deliver goods to members, it must be recorded that the member

has received the goods. Upon receipt of the goods the member signs to indicate

that they have received the amount written on the delivery invoice. The delivery

invoice therefore shows exactly who received the goods and on what day. Such a

system avoids members coming with complaints that they have not received goods Guide To Association Bookkeeping 32

(hessian, fertilizer, etc.) Since the delivery invoice can be referred to, and the

member shown the name of the person receiving their goods.

Association Name Invoice Number Depot Delivered To Date Delivered

Delivery Invoice Association:

Henga Valley

Delivery Invoice:

007

Delivery Depot:

Boma

Delivery Date:

07-10-97

Club

Name/Individual

Reg#

Items Receiving In Good

Order

Rcpt#

Signature of Receipt

Masasa

64312

20 Bags D-Compound

72

Mr Phiri

Association Representative Witness To Above Signature M. W. K. Gunda Date: 16-07

Club Receiving Reg/ID # Item Receiving Receipt # Signature Of Receipt

• Delivery Invoice #.. Invoices should be numbered consecutively 001, 002, 003, etc. and kept in a book after completion

• Delivery Depot..... Location that delivery is being made. All deliveries to

the same location can be recorded on the same delivery note.

• Delivery Date..... Date of delivery of goods • Club Name..... Name of club or name of individual and club

• Reg#..... Registration # of club • Items Receiving..... Details of the items which are being received

Guide To Association Bookkeeping 33

• Signature..... Signature of person receiving goods on behalf of club

or individual • Receipt#..... The person receiving the goods should show their

receipt and the number recorded.

• Witness Signature.... Signature of association representative to verify signatures for people receiving goods.

4.3 Cash Or Cheque Payment Voucher

A payment voucher is a document that accompanies the payment of large expenses

or purchases. The voucher is useful for two reasons; it provides a back up to the

receipt issued by the person receiving payment, and it requires authorization by the

appropriate parties before a cheque or cash can be issued. All expenses paid

from the cash account and any petty cash expense over K500 should be

accompanied by a payment voucher. After payment is issued the receipt

should be stapled to the back of the voucher and placed in the appropriate file.

Guide To Association Bookkeeping 34

Sample Payment Voucher

Payment Voucher Cheque # 120

Payable to: Farmers Friendly Fertilizer Date: 23-09 Payees Signature: Mr Solomoni Date: 24-09 Date

Description

Ref#

Amount (Mk)

23-09

100 Bags Comp-D

1234

4000-

Voucher Prepared By: Mr Bandawe Date: 23-09 Voucher Approved By: Mrs Somanje Date: 23-09 Collected By: Mr Giliyoni Date: 24-09 Posted By: Mr Chiwaula Date: 25-09 • Payable To... The name of the person/company that is to receive payment • Payee Signature... Upon receipt of payment the person receiving

payment should sign, and produce a receipt. • Date...... The date that payment will be made • Description..... Details of what the payment is for • Ref no..... The receipt number of the bill • Amount..... Total amount required for the item • Total..... Total being requested for payment • Voucher Prep...Name of person writing the voucher, could be the name

of the bookkeeper or that of a member of the committee • Approved By.... Before payment is made the appropriate authority must

first sign. The association committee should decide who (Can be more than one person) shall be required to approve vouchers. After signature a cheque should be drawn or a cash payment prepared.

• Posted By.... Record of the date and who made the posting to the

accounts. • Collected By... Person receiving payment.

Guide To Association Bookkeeping 35

4.4 Cash Request Form

The cash request form is used by individuals within the association (committee

members, manager) to request for petty cash funds to carry out operations related to

the running of the association. The cash request form serves as an authorization

form as well as a tentative receipt until the person requesting cash furnishes one.

Only requests for petty cash that have been pre-approved at the last committee

meeting should be granted. Any emergency request granted must be reviewed at

the following committee meeting. Cash request forms will be kept by the person

responsible for petty cash, and should be used for small expenses only. After the

person requesting cash has paid the expense, they must furnish a receipt for

the amount used and return any change left from the transaction.

Who Requests Amount Requested Per Item

Date Of Request

Association Petty Cash Request Form

Person Requesting M. Nyirongo

Date 04-06

Purpose Amount

Transport KU – LL – KU approved at committee meeting 04-06

MK100

Lunch LL MK40

Total Requested MK140

Authorized By: M. Munyimbiri

Cash Received By: M. Nyirongo

Details Of Purpose (W/Cmte Approval Date) Total Requested

Signatures

• Person Requesting... Name of person requesting for cash

Guide To Association Bookkeeping 36

• Date.... Date request being made

• Purpose..... Detailed account of what money needed for

(transport to and from, where, food, etc..) • Total Needed..... Total request • Authorized By... Name of person authorizing, committee should

decide who is to authorize expenses. A person should never authorize their own expenses (ie. The manager should not authorize his or her own transport expense to Lilongwe)

• Cash Received By... Signature of person requesting cash to verify that

money is received. Note: *The person requesting must furnish a receipt after payment for the expense after

which time the receipt is attached to the back of the cash request form and stored in

the appropriate place.

**The association committee should decide on standard expenses for various

association activities in advance. For example, how much should a member get for

transport from a location and back, and how much for lunch, etc..

4.5 Association Cash Count Form The cash count form is used by the bookkeeper and committee to keep an exact

record of cash in the cash box, or in the petty cash. The cash count should be

recorded periodically (perhaps one time per week) and done at the end of every

month. A cash count allows for a quick audit of the accounts, to show that the cash

in the cash box equals exactly the amount in the books. The cash count should

always be witnessed by another person other that the bookkeeper.

Sample Cash Count Form

Guide To Association Bookkeeping 37

Mulanje Association Cash Count

Date:

K200 X 2 =400

K100 X 1 = 100

K50 X -- =

K20 X -- =

K10 X 3 = 30

K5 X -- =

K1 X 4 = 4

Other Coins X K7.50 = 7.50

TOTAL CASH ON HAND 541.50

Manager Signature: M. Banda

Witness Signature: T. Nasoro

• Date..... Date of cash count • 500X ..... Number of notes of that denomination • = ..... Total cash in cash box of that denomination • Total Csh On Hnd.. Total cash on hand in the cash box • Bookkeeper Sign.... Signature of bookkeeper verifying cash count • Witness Sign.... Signature of witness to verify Cash count by

bookkeeper 4.6 Bank Reconciliation Statement The Bank Reconciliation Statement is used by the bookkeeper and committee to

check the accuracy of bank statements association accounts. Upon receipt of a

bank statement, the balance is checked against the association Bank Account

Balance to confirm that they equal each other. If they are not equaling, then the

association committee should look into the issue further and possibly call for the

assistance of the NASFAM Auditor.

Guide To Association Bookkeeping 38

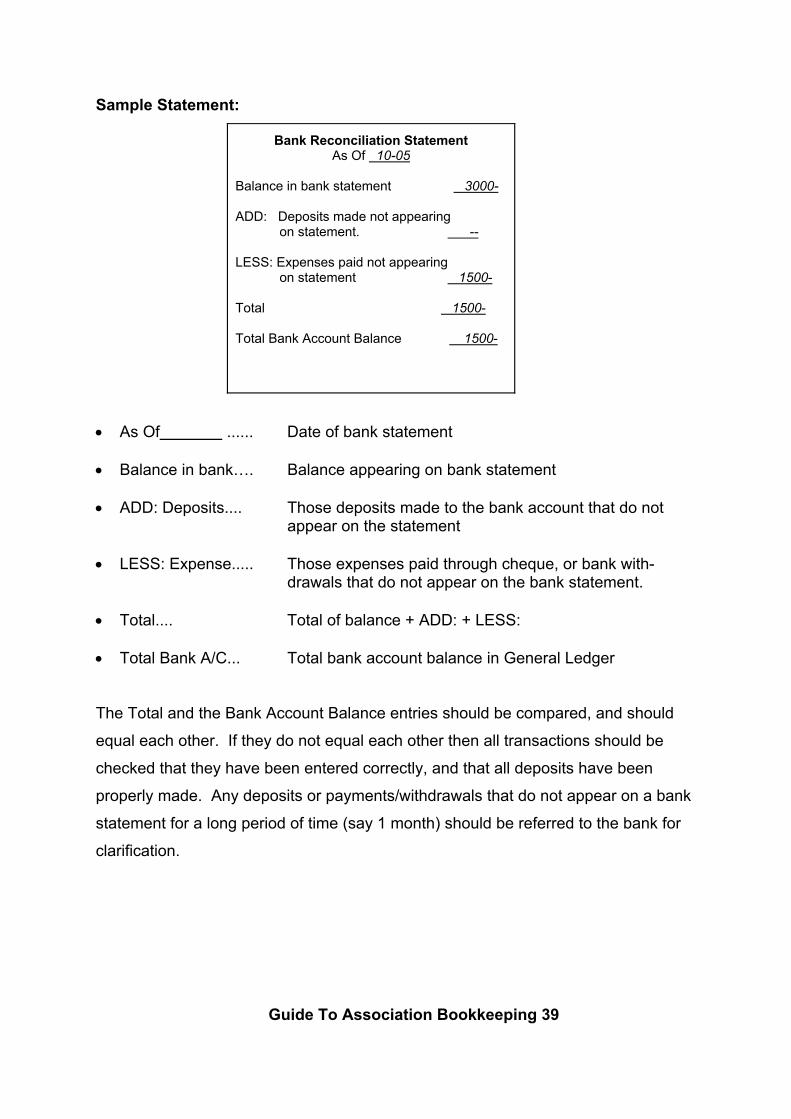

Sample Statement:

Bank Reconciliation Statement As Of 10-05

Balance in bank statement 3000- ADD: Deposits made not appearing on statement. -- LESS: Expenses paid not appearing on statement 1500- Total 1500- Total Bank Account Balance 1500-

• As Of ...... Date of bank statement • Balance in bank…. Balance appearing on bank statement • ADD: Deposits.... Those deposits made to the bank account that do not

appear on the statement • LESS: Expense..... Those expenses paid through cheque, or bank with-

drawals that do not appear on the bank statement. • Total.... Total of balance + ADD: + LESS: • Total Bank A/C... Total bank account balance in General Ledger The Total and the Bank Account Balance entries should be compared, and should

equal each other. If they do not equal each other then all transactions should be

checked that they have been entered correctly, and that all deposits have been

properly made. Any deposits or payments/withdrawals that do not appear on a bank

statement for a long period of time (say 1 month) should be referred to the bank for

clarification.

Guide To Association Bookkeeping 39

NOTES

Guide To Association Bookkeeping 40

NOTES

Guide To Association Bookkeeping 41

The Association Accounting System In Use

5.1 What does the association need to start the system?

Before setting up a new accounting system for the association, the association will

first need to purchase some basic items for the bookkeeper. The expense

associated with purchasing these items is minimal in comparison to the importance

of the items. The following items are needed per association: � Calculator

� Cash Box

� Accounting Ledger, 32 column preferable (1)

� Hard cover notebooks (7-10)

� Receipt Books-1/major program, registration fees, petty cash

(6-7)

� Support Documents (Master copy to be supplied)

� Ruler, Paper Punch, Stapler, Pens, File Folders

5.2 Preparing the accounts to begin bookkeeping

Now that the necessary items have been purchased, the books must be put in a

format suitable for the association accounting system. Preparing the books will take

some time, and needs to be done carefully with attention to detail. A ruler and a

good pen should be used to rule all ledgers to give the accounts a professional look.

To set up the account to begin bookkeeping, the bookkeeper should:

1. Rule several pages of the main ledger using the sample page at the back of this manual. Label the outside of the book and the spine as MAIN LEDGER- Mulanje Smallholder Farmers Association & Address.

2. Rule several pages of a hard cover notebook as a petty cash/expense ledger

using the sample page given at the back of this manual. Label the outside of the book and the spine as Petty Cash/Expense Ledger- Mulanje Smallholder Farmers Association & Address.

3. Rule several pages of a hard cover notebook as the other necessary sub-

ledgers using the sample page given at the back of this manual. For the less Guide To Association Bookkeeping 42

used Sub-Ledgers combine them into one hard cover book. Label the outside of the book and the spine as Service Fees Sub-Ledger- Mulanje Smallholder Farmers Association & Address. The Sub-Ledger should be prepared as follows (The ledgers may differ for non-tobacco associations):

Use (5) hard cover books total � Input Program Ledger

� Hessian Collection Program Ledger

� Service Fees Ledger and Donations Ledger

� Retail Sales ledger

� Accounts Receivable Ledger and Accounts Payable Ledger

� Petty Cash Ledger

4. Label receipt books with the program they will be used for. The books should

be arranged and labeled as follows:

� Petty Cash-Henga Valley Smallholder Farmers Association

� Fertilizer Sales- Henga Valley Smallholder Farmers Association

� Membership Dues- Henga Valley Smallholder Farmers Association

� Retail Sales- Henga Valley Smallholder Farmers Association

� Hessian Collection- Henga Valley Smallholder Farmer

� Etc..

**Remember a separate receipt book should be used for each of the above programs, receipts from different programs should not be combined in the same book.

5.3 When to make entries into the accounts

As we know, smallholder associations do not have the resources to hire a full time

bookkeeper to keep the association accounts. Therefore, the association will usually

ask the manager to act as the manager and the bookkeeper. The manager’s job is

very busy and he or she does not have time to concentrate only on the books each

day. The manager must therefore set aside a certain amount of time each day to

compile the accounts. A recommended practice is that the manager close the office

at 3:30 or 4:00 each day to sit down and complete the entries of the day. Here is a

sample of how the books are kept from transaction to entry into the books:

1. 10:30 in the morning a farmer comes in to complete a transaction (Example- Purchase Bailing Paper)

Guide To Association Bookkeeping 43

2. The manager or clerk writes a receipt for the purchase of bailing paper. 3. The manager or clerk then receives the cash for the bailing paper order

signing on the receipt to show that they have received it. 4. The manager places the cash in a secure place (till, cash box) separate from

the other cash. For very large receipts the receipts should be banked immediately. As discussed in Section II this may not be possible for all associations, therefore follow the policy set forth by the association regarding when to bank receipts.

5. 3:45 the manager closes the office, takes all the receipts of the day and

enters them first into the appropriate sub-ledgers, and then all Sub-Ledger transactions are entered into the main ledger. This will be covered further later in the section.

5.4 Making Primary Entries

The following examples are a comprehensive look at the entries that will be made

into the books each day for different programs, and for different types of

transactions. These transactions have been called primary entries, in that they are

the entries that will be made into the accounts at the end of each day. At the end of

Section VI we will also look at the entries that need to be made at the end of each

month, and the reports to be completed each month.

5.4.1 Membership Fee Transactions

(a) Receipt of full membership/entrance fee payment Example: The association membership fee is K500 per year. Mr. R.

Nyirongo brings in K500 on December 5, 1997 to pay on behalf of the club

he belongs to Mitondo club Reg#63189

Bookkeeping Steps (1) Person receiving money (clerk or manager) completes a detailed

receipt:

Guide To Association Bookkeeping 44

009

011,10-10-98 Date: 10-10-98

Name: Njoka #67302

Mem # 72 Item: 99 Mem Dues K500

Total: K500

Rcv. Signature: S Mwale

(2) Entry is made into the Membership Sub-Ledger of the transaction

Sub-Ledger: Membership SL#02

Date Entry #

Details

Rcpt #

Debit Credit Balance

10-10

011

99Mem Fee, Njoka #67302 (Mem #72)

09

500-

CR 500-

�As we learned in Section III any receipt of cash for memberhip fees is credited to the Membership Sub-ledger

(3) Entry is then made into the General Ledger of the transaction**

General Ledger

Date

Item

Cash Account

Bank Account

Analysis

DR

CR

DR

CR

Petty Cash

Reg Fees

Hess Fees

Fert Sales

Retail Sales

Retail P. Csj

Serv. Fees

A/C Rec.

Donations

10-10

SLO2: #11-11

500-

500-

CR 500-

�Remember as we learned in Section III, any receipt of cash is entered as a debit to the cash account.

�Under ‘Item’ remember to state the sub-ledger name and entry #s

**As we examined in Section III all entries from a sub-ledger each day are made as a single entry to the main ledger.

(b) Receipt of partial membership/entrance fee payment

Guide To Association Bookkeeping 45

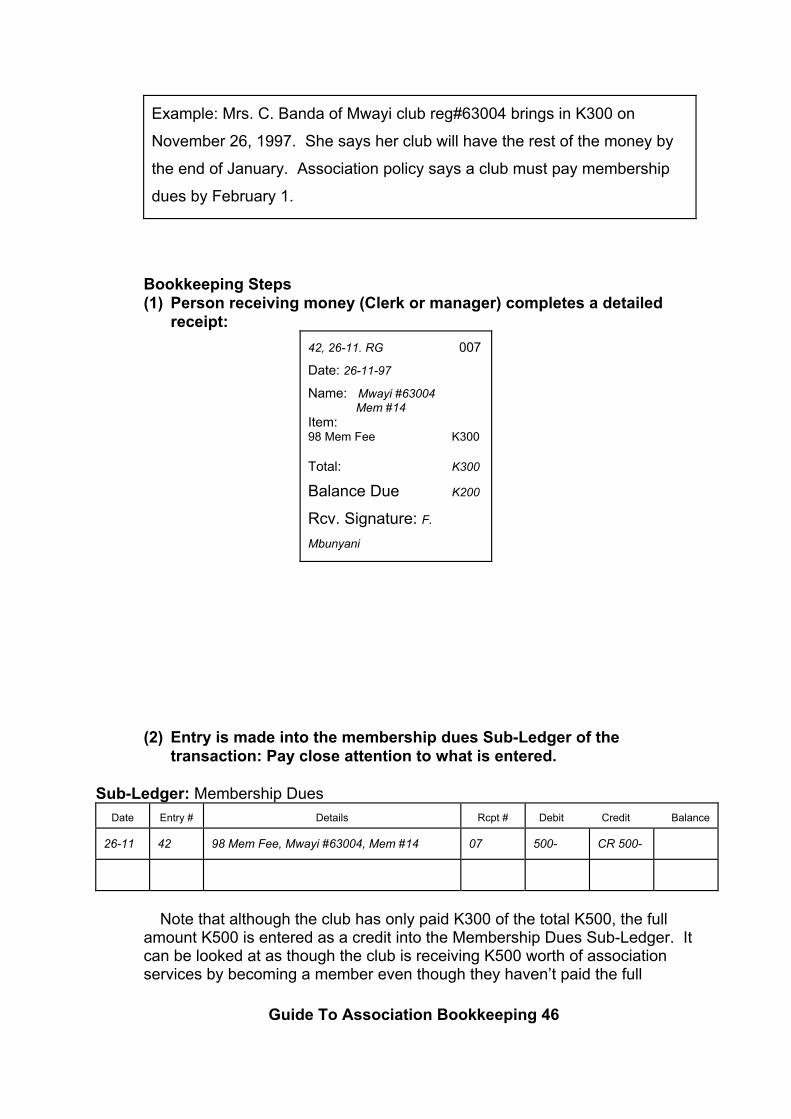

Example: Mrs. C. Banda of Mwayi club reg#63004 brings in K300 on

November 26, 1997. She says her club will have the rest of the money by

the end of January. Association policy says a club must pay membership

dues by February 1.

Bookkeeping Steps (1) Person receiving money (Clerk or manager) completes a detailed

receipt: 42, 26-11. RG 007

Date: 26-11-97

Name: Mwayi #63004 Mem #14

Item: 98 Mem Fee K300 Total: K300 Balance Due K200

Rcv. Signature: F.

Mbunyani

(2) Entry is made into the membership dues Sub-Ledger of the transaction: Pay close attention to what is entered.

Sub-Ledger: Membership Dues

Date Entry #

Details

Rcpt #

Debit Credit Balance

26-11

42

98 Mem Fee, Mwayi #63004, Mem #14

07

500-

CR 500-

� Note that although the club has only paid K300 of the total K500, the full amount K500 is entered as a credit into the Membership Dues Sub-Ledger. It can be looked at as though the club is receiving K500 worth of association services by becoming a member even though they haven’t paid the full

Guide To Association Bookkeeping 46

amount. The other entries we make show us why this is so.

�Some associations do not allow clubs who have not paid their dues in full to obtain any services. In its financial policies, an association can decide whether or not to receive payments in installments from clubs (Assuming that no services will be rendered until full payment received.)

(3) Entry is made into the Accounts Receivable Sub-Ledger of the

transaction: Sub-Ledger: Accounts Receivable (SL308)

Date Entry #

Details

Rcpt #

Debit Credit Balance

26-11

14

SLOZ: Mwayi # 63004

67

200-

DR 200-

�A debit is made to the Accounts Receivable Sub-Ledger for K200, the amount the club is still owing. This is done because it must be shown somewhere that the club is owing the association money. They have signed up to be a member haven’t they? Recording the transaction in the bookkeeper’s head or on a sheet of loose paper is not proper accounting procedure.

(4) The cash received is entered into the General ledger, and the

analysis completed General Ledger

Date

Item

Cash Account

Bank Account

Analysis

DR

CR

DR

CR

Petty Cash

Reg Fees

Hess Fees

Fert Sales

Retail Sales

Retail P. Csj

Serv. Fees

A/C Rec.

Donations

26-11

SL02: #42-42

300

300

CR 500-

SL08: #14-14

DR 200

�The K300 received as cash must be debited to the Cash Account. Under the Analysis column we have made entries of K500 to entrance fees and K200 to show the details of the transaction

�If we add up the entries we have made we can see we have made K500 in

Guide To Association Bookkeeping 47

debits and K500 in credits. This is in line with the double entry accounting system.

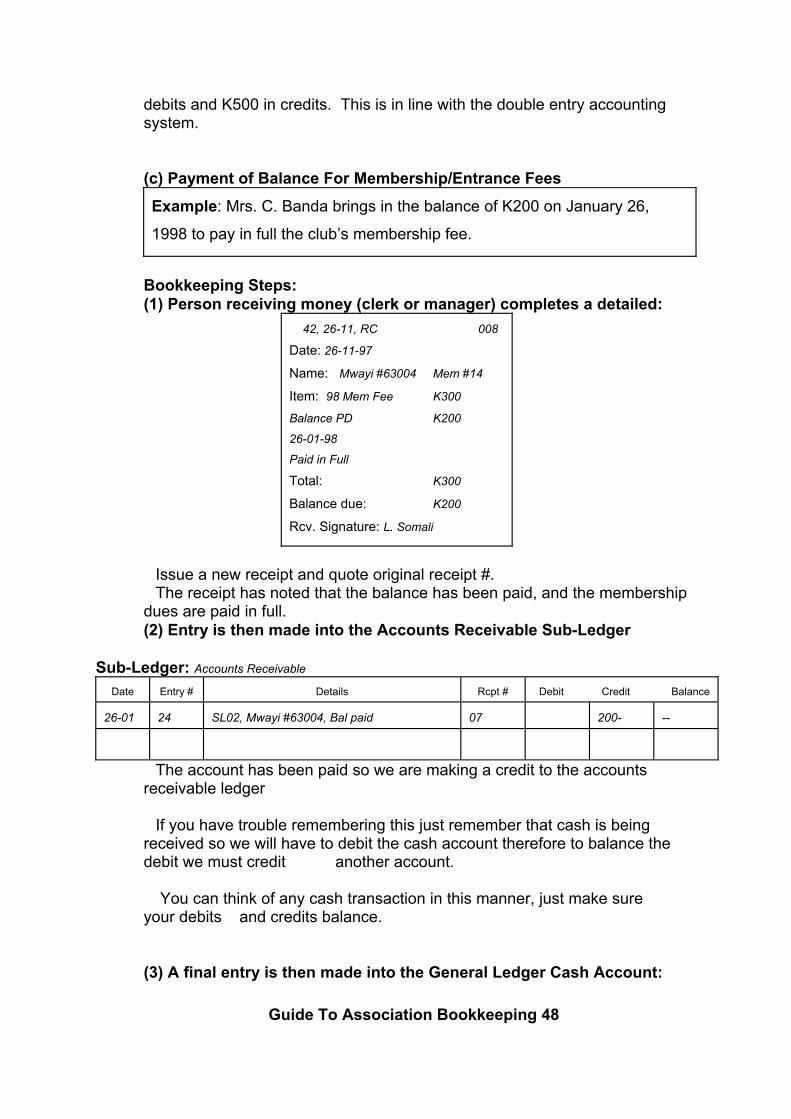

(c) Payment of Balance For Membership/Entrance Fees Example: Mrs. C. Banda brings in the balance of K200 on January 26,

1998 to pay in full the club’s membership fee.

Bookkeeping Steps: (1) Person receiving money (clerk or manager) completes a detailed:

42, 26-11, RC 008 Date: 26-11-97

Name: Mwayi #63004 Mem #14

Item: 98 Mem Fee K300

Balance PD K200

26-01-98

Paid in Full Total: K300

Balance due: K200

Rcv. Signature: L. Somali

�Issue a new receipt and quote original receipt #. �The receipt has noted that the balance has been paid, and the membership dues are paid in full. (2) Entry is then made into the Accounts Receivable Sub-Ledger

Sub-Ledger: Accounts Receivable

Date Entry #

Details

Rcpt #

Debit Credit Balance

26-01

24

SL02, Mwayi #63004, Bal paid

07

200-

--

�The account has been paid so we are making a credit to the accounts receivable ledger

�If you have trouble remembering this just remember that cash is being received so we will have to debit the cash account therefore to balance the debit we must credit another account. �You can think of any cash transaction in this manner, just make sure your debits and credits balance.

(3) A final entry is then made into the General Ledger Cash Account: Guide To Association Bookkeeping 48

General Ledger

Date

Item

Cash Account

Bank Account

Analysis

DR

CR

DR

CR

Petty Cash

Reg Fees

Hess Fees

Fert Sales

Retail Sales

Retail P. Csj

Serv. Fees

A/C Rec.

Donations

26-01

SL08: #24-24

200-

200

CR 200

Guide To Association Bookkeeping 49

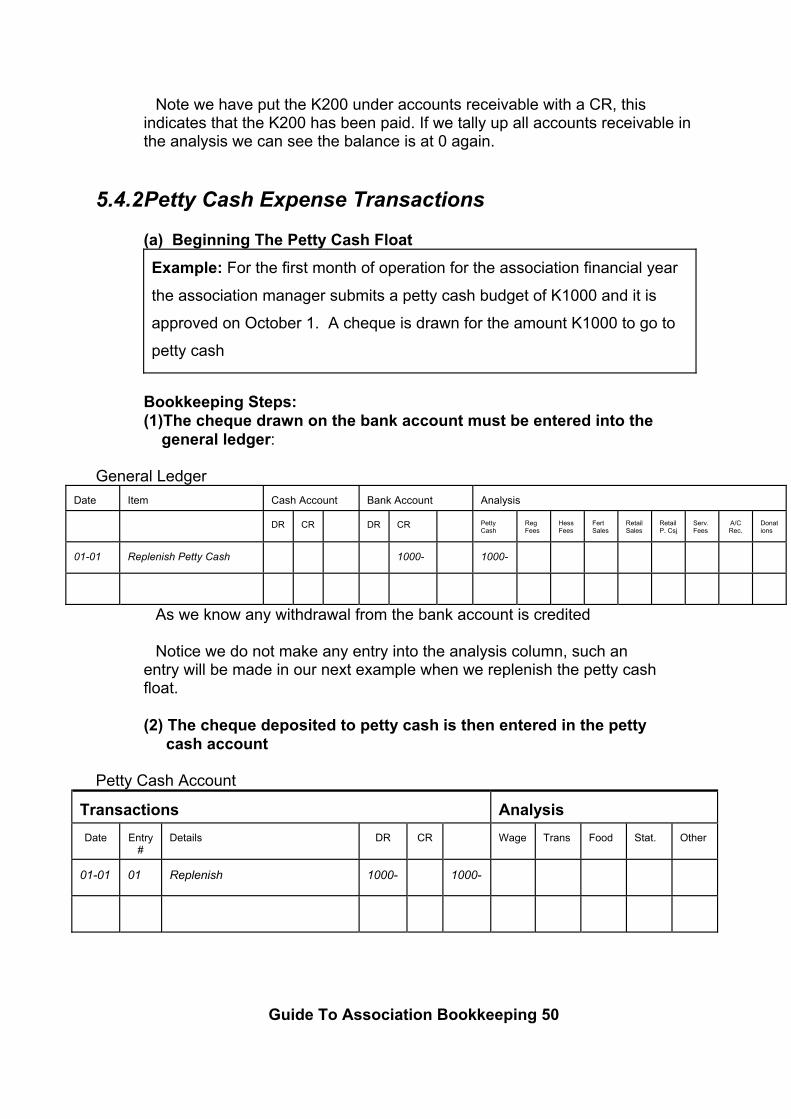

�Note we have put the K200 under accounts receivable with a CR, this indicates that the K200 has been paid. If we tally up all accounts receivable in the analysis we can see the balance is at 0 again.

5.4.2 Petty Cash Expense Transactions

(a) Beginning The Petty Cash Float Example: For the first month of operation for the association financial year

the association manager submits a petty cash budget of K1000 and it is

approved on October 1. A cheque is drawn for the amount K1000 to go to

petty cash

Bookkeeping Steps: (1)The cheque drawn on the bank account must be entered into the general ledger:

General Ledger

Date

Item

Cash Account

Bank Account

Analysis

DR

CR

DR

CR

Petty Cash

Reg Fees

Hess Fees

Fert Sales

Retail Sales

Retail P. Csj

Serv. Fees

A/C Rec.

Donations

01-01

Replenish Petty Cash

1000-

1000-

�As we know any withdrawal from the bank account is credited

�Notice we do not make any entry into the analysis column, such an entry will be made in our next example when we replenish the petty cash float.

(2) The cheque deposited to petty cash is then entered in the petty cash account

Petty Cash Account

Transactions

Analysis

Date

Details

DR

CR

Wage

Trans

Food

Stat.

Other

01-01

01

Replenish

1000-

1000-

Entry #

Guide To Association Bookkeeping 50