assignment 1 report on the australian economy · pdf filemacroeconomics: theory and...

TRANSCRIPT

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 1

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

Assignment 1 – Report on

the Australian Economy

(25555) Macroeconomics: Theory

and Applications

Karli-Jane Bergamin 10682336

Alessandra Lambides 10779559

Johanan Ottensooser 10873305

Shaambavi Sivasubramanian 10856817

8th September 2010

Word Count: 2653 including internal referencing

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 2

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

MACROECONOMICS: THEORY AND APPLICATIONS (25555)

ASSIGNMENT COVER SHEET

2010- Autumn

Assignment (30%)

TUTOR'S NAME: Alexander Calvo TUTORIAL DAY: Wednesday

TUTORIAL TIME : 4:00pm

Family Name First Name Student

Number

Contribution Signature*

1. Bergamin Karli-Jane 10682336 25%

2. Lambides Alessandra 10779559 25%

3. Ottensooser Johanan 10873305 25%

4. Sivasubramanian Shaambavi 10856817 25%

100 %

*By signing your name, you agree that you have read, understood and followed the advice in

the subject guide concerning cheating and plagiarism.

Follow the submission instructions closely & carefully :

Complete this “coversheet” correctly and submit to your tutor in your class.

Follow the assignment criteria

Conduct a self-assessment on the hardcopy before submitting

Keep a copy of your assignment

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 3

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

Group Report Assignment

25555 – Macroeconomic Theory and Applications

Contents

1 Executive Summary ............................................................................................................... 4

2 Introduction .......................................................................................................................... 5

3 Australia’s current economic situation ................................................................................. 6

4 Fiscal Policy ......................................................................................................................... 10

5 Monetary Policy .................................................................................................................. 12

6 The RBA’s August decision .................................................................................................. 14

7 Conclusion ........................................................................................................................... 17

8 Bibliography ........................................................................................................................ 18

9 Turnitin Report

10 Marking Rubric

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 4

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

1 Executive Summary

This essay will evaluate the RBA’s decision not to change interest rates at the August ’10

monetary policy meeting. This analysis was made by exploring the Australian economic

climate, analysing the current macroeconomic mix and by applying these to the RBA’s

monetary policy goals. In light of the Global Financial Crisis (GFC), Australia has performed

comparably well. Current GDP growth rate to this quarter is 3.2%, whereas as most other

OECD economies have recorded negative growth, the US recording negative growth of -2.4%.

Fiscal and Monetary policy have created and developed a positive economic climate by

targeting any symptoms of a pervading recession through copious government spending and

loosening monetary policy. In spite of its apparent stability, Australia’s economy is still

fragile. Interest rates have been held at 4.5% for the past three months to maintain this

delicate balance. A further reduction in interest rates may have increased growth at the cost

of increasing inflationary pressures. An increase in interest rates may have dampened

consumer confidence too soon. Thus, the RBA’s decision to maintain interest rates is in line

with its goal of maximizing non-inflationary growth.

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 5

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

2 Introduction

A country’s economic situation is determined by both factors out of the control of its

governing body and factors implemented directly through macroeconomic policy. This report

aims to describe Australia’s current economic landscape and outline the Macroeconomic

policies its governing bodies have implemented to try and maintain a level of sustainable

growth. It then strives to analyse the reasoning behind the Reserve Bank Australia’s (RBA)

choice to maintain the current cash rate at 4.5% this month. This report seeks to illustrate the

current relative stability of the Australian economy as driving the current macroeconomic

stance, a combination of a mildly contractionary fiscal and neutral monetary stance. The

paper proposes to analyse the RBA’s decision to take a cautious monetary stance benefit to

the Australian economy in light of its slow recovery post the economic crisis and the potential

inflationary pressures a fall in interest rates could cause.

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 6

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

3 Australia’s current economic situation

Australia’s economic condition is arguably one of stability and economic recovery. Despite

global economic uncertainty, Wayne Swan states that the Australian economy remains in a

strong position with a positive economic future (Australian Government, 2010).

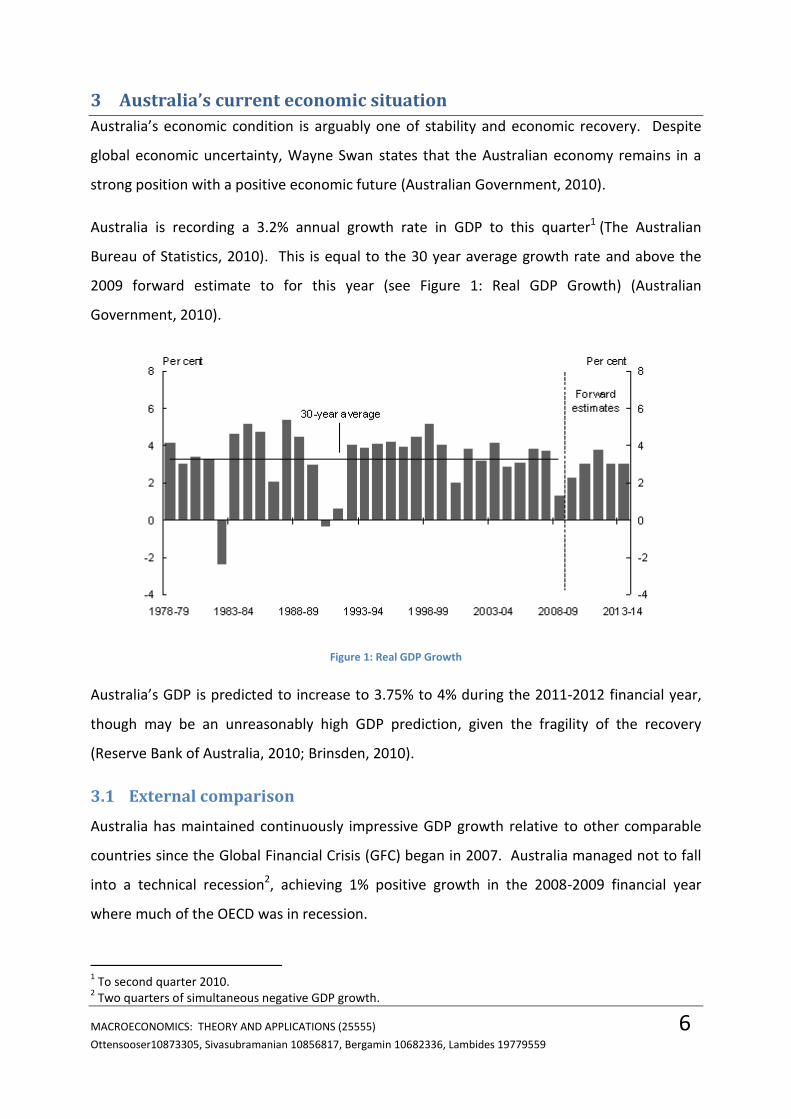

Australia is recording a 3.2% annual growth rate in GDP to this quarter1 (The Australian

Bureau of Statistics, 2010). This is equal to the 30 year average growth rate and above the

2009 forward estimate to for this year (see Figure 1: Real GDP Growth) (Australian

Government, 2010).

Figure 1: Real GDP Growth

Australia’s GDP is predicted to increase to 3.75% to 4% during the 2011-2012 financial year,

though may be an unreasonably high GDP prediction, given the fragility of the recovery

(Reserve Bank of Australia, 2010; Brinsden, 2010).

3.1 External comparison

Australia has maintained continuously impressive GDP growth relative to other comparable

countries since the Global Financial Crisis (GFC) began in 2007. Australia managed not to fall

into a technical recession2, achieving 1% positive growth in the 2008-2009 financial year

where much of the OECD was in recession.

1 To second quarter 2010.

2 Two quarters of simultaneous negative GDP growth.

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 7

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

Figure 2 (Australian Government, 2010; Reserve Bank of Australia, 2010; Bureau of Economic

Analysis, 2010) highlights Australia’s relative economic success.

Figure 2: International GDP Growth

3.2 Australia’s economy by components of GDP

GDP is the aggregate final domestic production of goods and services. It consists of

consumption (C), investment (I), net government fiscal activity (G) and net exports (X-Q), as

delineated by the following equation:

Equation 1: GDP

Any accurate description of Australia’s current economic situation must factor in changes in

the components of GDP.

3.2.1 Consumption

Consumption is a major indicator of a country’s economic situation. Australia’s retail

spending increased in June to reach an overall 0.8% increase in volume over the June quarter

(The Australian Bureau of Statistics, 2010). This marks a trend of modestly increasing

confidence in Australia, with both business and consumer confidence greater than the long-

run average.

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 8

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

However, as a result of the recent economic crisis, Australian consumers are now generally

more conservative (Gruen, 2010). This is marked through an increased household savings

rate, up 1.3% in May 2010 (Reserve Bank of Australia, 2010).

This consumption growth contributes more than 1.5% of Australia’s GDP growth (Reserve

Bank of Australia, 2010).

3.2.2 Investment

There has been growth in net investment, driven by mining. There was an expectation that

the mining tax would reduce investment from overseas, but investment in the mining industry

rose by 29% in the June quarter, as compared to the same quarter last year, and almost 50%

above expectations (Pascoe, 2010).

Furthermore, there has been recorded a mildly optimistic investment outlook (Pascoe, 2010).

3.2.3 Net Government Expenditure

Government expenditure rose dramatically in response to the GFC, but is slowing due to fears

of overstimulating the economy, crowding out private investment and placing too great a

debt burden on Australia. For more, see section 4, below.

3.2.4 Net Exports

Net exports have positively affected the GDP, with the current account deficit falling from 16

billion in the first quarter of the year to less than 6 billion currently (Helyar, 2010). Australia is

now running a trade surplus (which is not common for Australia) that has added .4% to the

June quarter’s GDP growth (Stutchbury, 2010). This has largely been caused by increased

Southeast Asian demand for Australian mineral exports. Export quantities are set to

dramatically increase next year due to capital investment easing capacity constraints on

Australia’s mining industry.

3.3 Unemployment rate

Australia’s unemployment rate increased in response to the GFC in 2009, peaking above 6%.

Since then, it has begun to fall and was at 5.1% in June (Minutes of Monetary Policy, August

2010). There is some evidence that shows that some of this decrease in unemployment rate is

due to a decreasing participation rate, which fell to approximately 65%, due to hysteresis and

discouragement of the long term unemployed in the labour force (Reserve Bank of Australia,

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 9

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

2010). Overall, Australia’s unemployment rate is much lower than most OECD countries, with

the US at 9.5% (United States Bureau of Labor Bureau of Labor Statistics, 2010). This bodes

well for the Australian economy.

3.4 Inflation

Australia’ underlying inflation rate is currently at 2.75% (Minutes of Monetary Policy, August

2010), which is the first time in nearly three years it has been under 3%. Australia’s headline

Consumer Price Index was at 3.1%. The upwards pressure on inflation can be explained by

the GDI outpacing the GDP due to increased Asian demand (primarily from India and China)

for Australian minerals. This has been offset by passive consumer demand in recent times,

lower wage growth in 2009, the appreciation of the Australian dollar, retail price discounting

as well as a decline in domestic holiday accommodation pricing and little increase in utility

prices in the last quarter.

3.5 External Stability

Whilst Australia’s net exports are growing fast, Australia still has a problem with external

stability: a rising Australian dollar is decreasing the international competitiveness of

Australian exports and foreign debt servicing counterbalances Australia’s positive net exports

to bring Australia into a growing current account deficit. Whilst the Australian dollar has not

yet dampened demand for Australian primary exports, there has been increased outsourcing

of secondary and tertiary production due to their relative cheapness. Whilst Australia’s

current account deficits, and the level of private foreign debt, are high, investors remain calm,

since the CAD is decreasing at record rates (Martin, 2010).

The RBA continues to stress that external global uncertainty, especially from Europe, remains

an issue. Further, Australia’s reliance on Asian growth and demand (see Figure 2:

International GDP Growth, above) for mining exports are making Australia’s economic future

fragile (Reserve Bank of Australia, 2010).

MACROECONOMICS: THEORY AND APPLICATIONS (25555) 10

Ottensooser10873305, Sivasubramanian 10856817, Bergamin 10682336, Lambides 19779559

4 Fiscal Policy

Since the late 2008, the approaches taken by our central macroeconomic bodies have been

directed by increased volatility of world markets due to the GFC, a world recession due to the

shortfall of liquidity of investment banks in the United States. As a result, macroeconomic

policies have been implemented with a view to negative the GFC’s effect on the Australian

economy whilst still providing for adequate exit strategies can be executed once stability

returns.

Fiscal Policy is the mechanism by which government alters their spending, either in the form

of government investment (G) and/or transfer payments (TR), or their collections through the

taxation rate (t) to reduce fluctuation in the business cycle and lessen the output gap.

4.1 Discretionary Fiscal Policy

Australia’s current fiscal stance is mildly contractionary with a Budget Deficit of 40.8bil (2.9%

of GDP) for 2010-11 compared to 2008-09 deficit of 57.1bil (4.4% of GDP) (James & Sebastian,

2010). For the past two years, however, the Australian Government has been applying

expansionary fiscal policy through a $42bil Stimulus Package to ward off recession symptoms

due to the GFC (Parliament of Australia, 2010). This stimulus comprised of Government

Investment expenditure and Transfer Payments to influence the level of aggregate-demand

and output, thereby increasing equilibrium income and GDP.

The equilibrium position of the economy lies where AD=Y; as illustrated by Eq1.

Eq1

]

Discretionary strategies outlined by the Stimulus Package include government investment

expenditure on large-scale infrastructure projects and microeconomic reform initiatives.

$14.7billion was spent on school halls extensions, $10.5billion for residential building

projects and ceiling insulation for homes, and $890million for road constructions (Gittins,

2009). This has resulted in job-creation, increased activity in the construction sector and

will continue to improve AD in the medium term. $2.7billion has been spent on business

tax-breaks encouraged risk-averse businesses to continue their activities (Gittins, 2009).

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p11

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

This is in accordance to the simple Keynesian model; output (Y) rises proportionately to the

change in G as a product of the government expenditure multiplier3.

The government plans to return the budget to surplus by 2012-13 a few strategies are being

put in place to slowly withdraw the expenditure. This includes confining annual real growth

to 2% until the budget surplus reaches 1% of GDP (Parliament of Australia, 2010) by limiting

expenditure, and increasing revenues through Super Profits Tax (12billion in tax revenue in

four years) and higher excise on alcohol and cigarettes (Swan & Rudd, 2010).

The Stimulus Package also includes $12.7billion in TR, a one off tax free cash-handouts of up

$950 to income earners, single income two-parent families earning up to $150,000, families

with schoolchildren, students and apprentices, and drought affected famers (Gittins, 2009).

The initiative encouraged individuals to spend money (increase consumption) thereby

providing an immediate stimulus to the economy. These results correspond to the

theoretical notion (Eq1), that an increase in TR will directly affect the consumption function

(Eq2) hence resulting in an increase in AD.

Eq2

4.2 Non-Discretionary Fiscal Policy

Other, non-discretionary fiscal outcomes include the effect of automatic stabilisers. As less

tax receipts are received by the Government during periods of lower output, leakage caused

by income circulation reduces i.e. when Y decreases, tY falls. Hence consumption inevitably

rises (Eq2) and so do outputs (Eq1). During periods of economic recession, uncertain

employment prospects and inconsistent income-flow result in rises in welfare benefit

payments.

3

)1(1

1*

tcdG

dY

i.e. the change in government expenditure effects a change in equilibrium income on a

greater than 1:1 basis because of its further effect on reducing taxes and increasing consumption.

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p12

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

5 Monetary Policy

5.1 Current Monetary Policy Stance

Monetary Policy is the instrument used by the Reserve Bank (of Australia) to influence

inflation and output. Prior to the GFC, the main function of the monetary policy was to

manage economic growth and maintaining target inflation of 2-3% by subtly raising interest

rates to slow the economy or lower rates as a stimulus. Since 2007, monetary policy has

been somewhat contractionary, but has now plateaued at 4.25% (ABC News, 2010).

5.2 Monetary Policy in Relation to the GFC

The Reserve Bank of Australia loosened monetary policy over the last year or so in attempt

to rectify the loss of consumer and business confidence caused by the GFC. This was

achieved by reducing interest rates and increasing the money supply in the economy

thereby increasing consumption by individuals, business investments and hence output .

The RBA’s cutting of the cash rate was gradual; an over 4% drop was made within 6 months

(Fig3). The cash rate of 7.25% held from Mar-Aug 08 down to a 49-year low (AAP News,

2009) of 3% by April 2009. This interest rate was held for a 5 month period, only rising

slightly to 3.25% in Oct 09 (ABC News, 2010)

5.3 Effect of Macroeconomic Policy

The policies and strategies imposed by the RBA and Australian Government have been

successful in combating the GFC preventing recession and leading to our apparent recovery.

This is illustrated through Australia’s current economic environment (see section 3), which is

characterised by increases in levels of consumption, investment, and reductions in

unemployment which have reflected favourable on AD and the national output.

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p13

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

Figure 3 CPI

The overall effect of expansionary fiscal and monetary policy has resulted in a GDP growth

rate of 0.9% in Dec09 quarter from -0.8% in Dec08 (ABC News, 2010). According to Treasury

Reports, without the stimulus the economy would have contracted at a rate 0.7% (Gittins,

2010).

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p14

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

6 The RBA’s August decision

The RBA must use monetary policy to address the following considerations:

Limiting “consumer price inflation [to] between 2-3%; the stability of the Australian currency;

the maintenance of full employment within Australia; and the economic prosperity and

welfare of the Australian people” - (Reserve Bank of Australia, 2007; Reserve Bank Act ,

1959)

The primary goal of monetary policy, since 1993, is to maintain stable price levels (Reserve

Bank of Australia, 2007). This must be balanced against the goal of “economic prosperity”

and “full employment”. Together, these goals have been interpreted as maximising

sustainable economic growth, with the requirement for “sustainability” encompassing

consumer price inflation.

As such, all monetary policy decisions, including the August 2010 decision not to raise

interest rates above 4.5%, must have been made in light of the above considerations in

order to be valid.

6.1 Sustainable Economic Growth

Section 3.2, above, discussed the relative strength of Australia’s GDP growth, as shored up

by mining exports, investment, increasingly positive consumer sentiments and government

expenditure (see section 4, above). As such, and in consideration of the predicted high rates

of growth for the next few years, the reserve bank does not really have to use monetary

policy as an expansionary economic tool.

Reducing interest rates would act strongest on consumption spending (due to reduced

mortgage costs increasing disposable income). Consumption is already on a steep rise, with

increased consumer sentiment said to translate into even higher consumption in the next

year or so. Consumer spending has increased by 0.7% and household spending by 1.1% in

the Dec 09 quarter since the recession. As such, this would be over-stimulating the

consumption component of the GDP, potentially creating inflationary pressures.

Consumption spending has experienced a modest increase, despite a higher level of

household savings and low credit growth. Most economists expect that domestic demand

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p15

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

will increase over the next twelve months, but given the current cautious sentiment,

keeping interest rates on hold may encourage positive inter-temporal substitution.

Similarly, the current monetary stance coupled with the stabilization of business credit

should encourage investment and development in line with the expected increase in

demand. The labour market has picked up, with unemployment falling to 5.1% in June and

average work hours have increased, although levels are still far from those reached in 2008.

Further, a decrease in the interest rates would also reduce Australia’s interest rate

differential, potentially reducing foreign investment in Australia by reducing the risk-free

level of growth.

Underlying inflation had continued to fall to 2.75% below 3% for the first time in three

years, and is now within the RBA’s target band. The CPI is at 3.1%, which is partly due to the

increases in tobacco taxes earlier this year and maintenance price of utilities. This rate is

expected to remain steady over the next twelve months while underlying inflation is

expected to increase to 3% due to supply constraints being reached with the expansion of

the resources sector. Due to these inflationary pressures reducing the RBA’s cash rate

would not have been a logical choice.

Despite the Bank’s expectations for global growth to be about trend for the coming year,

expansion has been uneven. Most advanced economies have experienced moderate rates

of growth, and key economic indicators suggest that China is shifting to a more sustainable

rate of development. However the overall strong growth in Asia and Latin America has led

to an increase in the price of Australia's two largest exports, iron ore and coal. As a result,

terms of trade have again risen to the historically high levels experienced in 2008 and

economists expect this to be sustained over the next few years.

6.2 Maximum Employment

Unemployment, though reducing from its all-time high of 5.8% (The Australian Bureau of

Statistics, 2010) October 09 to 5.1% in June 10 (The Australian Bureau of Statistics, 2010), is

slowly recovering (with approximately 200,000 jobs being added to the workforce in since

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p16

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

last August). This may be explained by the hysteresis4 brought about by the pro-cyclical

nature of output and participation rate, and labour productivity keeping the unemployment

rate up in spite of the increase in income.

Whilst reducing the interest rate might increase employment, the unemployment rate is low

enough, and close enough to the natural rate of unemployment, that targeting this with

monetary policy would have diminished returns, and would directly increase inflationary

pressures.

6.3 External Stability

External stability is a secondary goal of the RBA’s monetary policy. Australia’s relatively

sound external stability (excluding her massive private international debt): a high Australian

dollar, increasing terms of trade and growing net exports (see s3.3.3 above) would be

inappropriately targeted by monetary policy.

The goals of monetary policy are clearly delineated. There is high, almost peak non-

inflationary growth, the unemployment rate is falling as the participation rate is increasing

and Australia is enjoying record external stability. As such, the RBA’s decision to keep cash-

rates as-is is sound, protecting current growth without adding inflationary pressure.

4 Hysteris is cyclical unemployment becoming long-term unemployment or a reduction of the participation rate

via deskilling or workers no longer “willing” and “actively seeking” employment.

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p17

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

7 Conclusion

Evidently, there are a multitude of factors that determine Australia’s current relative

economic stability. This report primarily identified that Australia was able to avoid being

unduly affected by the global economic recession due to its government expenditure

bolstering consumption, and a healthy export sector bolstered by increasing commodity

prices. These factors have led to Australia’s economic resurgence leaving Australia in a good

position to lead the global economic recovery. This report stresses a neutral monetary

stance will benefit the Australian economy as increasing the cash rate may simmer

Australia’s feel consumption demand whilst a reduction in the cash rate could see the

reappearance of inflationary pressures. Maintaining the cash rate served the RBA’s goals,

and are, thus, a reasonable response to the economic climate.

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p18

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

8 Bibliography AAP News. (2009, September 14). GFC and policy response as unusual as the crisis itself. Retrieved August 27, 2010, from Industry Search News: http://www.industrysearch.com.au/News/GFC-and-policy-response-as-unusual-as-the-crisis-itself-40928

ABC News. (2010). Global Financial Crisis Coverage. Retrieved August 29, 2010, from http://www.abc.net.au/news/events/global-financial-crisis/

Australian Government. (2010, June 1). Economic Statement. Retrieved September 4, 2010, from budget.gov.au: http://www.budget.gov.au/2010-11/content/economic_statement/html/index.htm

Brinsden, C. (2010, August 31). SMH - Business Day. Retrieved September 3, 2010, from Swan upbeat on Australian economy: http://news.smh.com.au/breaking-news-business/swan-upbeat-on-australian-economy-20100831-14avc.html

Bureau of Economic Analysis. (2010, August 27). National Income and Product Accounts Gross Domestic Product, 2nd Quarter 2010 ... Retrieved September 3, 2010, from Bureau of Economic Analysis - National Economic Accounts: http://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm

Central Intelligence Agency. (2009). The World Factbook. Retrieved September 2, 2010, from Field Listing: GDP: https://www.cia.gov/library/publications/the-world-factbook/fields/2195.html

Gittins, R. (2010). Cash splash tap is turning off. Sydney Morning Herald .

Gittins, R. (2009). It may be costly, but it will work. Sydney Morning Herald .

Gruen, D. D. (2010, February 19). The economic outlook and challenges for the Australian economy - Address to the American Chamber of Commerce. Retrieved September 3, 2010, from Australian Government - The Treasury: http://www.treasury.gov.au/documents/1783/HTML/docshell.asp?URL=02_Gruen_Speech.htm

Helyar, S. (2010, September 3). SMH - National Times. Retrieved September 3, 2010, from All Australians deserve a dividend from good economic times: http://www.smh.com.au/opinion/society-and-culture/all-australians-deserve-a-dividend-from-good-economic-times-20100902-14rjr.html

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p19

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

James, C., & Sebastian, S. (2010, May 11). Economic Insights Australia’s Budget 2010/11. Retrieved September 4, 2010, from Commsec Economics: http://images.comsec.com.au/ipo/UploadedImages/budget101aa3c77dac76401fa4dc488e7c778b6c.pdf

Martin, P. (2010, September 1). SMH - Federal Election. Retrieved September 2, 2010, from Current account deficit shrinks: http://www.smh.com.au/federal-election/current-account-deficit-shrinks-20100831-14fko.html

Parliament of Australia. (2010, May 11). Budget at a Glance 2010-11. Retrieved September 4, 2010, from http://www.aph.gov.au/budget/2010-11/content/at_a_glance/download/Budget_at_a_Glance_2010_11.pdf

Pascoe, M. (2010, August 26). SMH - Business Day. Retrieved September 1, 2010, from Forget the tax, mining investment powers on: http://www.smh.com.au/business/forget-the-tax-mining-investment-powers-on-20100826-13t8y.html

Reserve Bank Act . (1959).

Reserve Bank of Australia. (2010, June 27). Chart Pack - Output Expenditure Activity Fincon. Retrieved September 3, 2010, from Reserve Bank of Australi: http://www.rba.gov.au/chart-pack/output-expenditure-activity-fincon.pdf

Reserve Bank of Australia. (2010, July 7). Chart Pack. Retrieved September 1, 2010, from Labour Market Developments: http://www.rba.gov.au/chart-pack/labour-market-developments.pdf

Reserve Bank of Australia. (2010, July 29). Chart-Pack, Interest Rates Australia. Retrieved September 3, 2010, from Reserve Bank of Australia: http://www.rba.gov.au/chart-pack/interest-rates-australia.pdf

Reserve Bank of Australia. (2010, August 3). Minutes of the Monetary Policy Meeting of the Reserve Bank Board. Retrieved Sepember 1, 2010, from Reserve Bank of Asutrali: http://www.rba.gov.au/monetary-policy/rba-board-minutes/2010/03082010.html

Reserve Bank of Australia. (2007). Reserva Bank of Australia. Retrieved September 4, 2010, from About Monetary Policy: http://www.rba.gov.au/monetary-policy/about.html#objectives

Reserve Bank of Australia. (2010, August). Statement on Monetary Policy - August 2010. Retrieved September 1, 2010, from RBA: http://www.rba.gov.au/publications/smp/2010/aug/pdf/0810.pdf

Stutchbury, M. (2010, September 2). The Australian - Business With the Wall St Journal. Retrieved September 3, 2010, from Export prices add value to strong GDP growth: http://www.theaustralian.com.au/business/opinion/export-prices-add-value-to-strong-gdp-growth/story-e6frg9p6-1225913019338

MACROECONOMICS: THEORY AND APPLICATIONS (25555) p20

10873305, 10856817, 10682336 Ottensooser, Sivasubramanian, Bergamin, Lambides

Swan, W., & Rudd, K. (2010, May 2). Press Release: Stronger, Fairer, Simpler: A Tax Plan for Our Future. Retrieved Sep 4, 2010, from Australian Treasury: http://www.treasurer.gov.au/DisplayDocs.aspx?doc=pressreleases/2010/028.htm&pageID=&min=wms&Year=&DocType=0

The Australian Bureau of Statistics. (2010, August 31). 8501.0 - Retail Trade. Retrieved September 3, 2010, from The Australian Bureau of Statistics: http://www.abs.gov.au/ausstats/[email protected]/mf/8501.0

The Australian Bureau of Statistics. (2010, June). Australian Bureau of Statistics. Retrieved September 3, 2010, from 5206.0 - Australian National Accounts: National Income, Expenditute and Product: http://abs.gov.au/ausstats/[email protected]/mf/5206.0?OpenDocument

United States Bureau of Labor Bureau of Labor Statistics. (2010, September 3). United States Bureau of Labor Bureau of Labor Statistics. Retrieved September 4, 2010, from Labor Force Statistics from the Current Population Survey: http://www.bls.gov/cps/