asset liability management for life insurance: a...

TRANSCRIPT

Asset Liability Managementfor Life Insurance:

a Dynamic Approach

Dr Gabriele Susinno & Thierry BochudQuantitative Strategies

Capital Management Advisors

CAPITAL MANAGEMENT ADVISORS srlRisk Consulting

Madrid May, 23rd, 2001

2©2000 Arthur Andersen. All rights reserved.

• Capital Management Advisors.• Introduction: Life Insurance• Embedded Options• Actuarial Probabilities• Insurance Market Evolution• Integrated Dynamic ALM• Control Parameters: Dynamic Hedging• Further Developments: Optimal Control, Passport Options, …• Technological and Computational Issues• Final Remarks

Contents

3©2000 Arthur Andersen. All rights reserved.

Capital Management Advisors: who we are

• CAPITAL MANAGEMENT ADVISORS (CMA) is a company providingspecialised advisory services in the field of asset management

• CMA's target clients are institutional investors such as insurancecompanies, asset managers, pension funds, foundations and banks

• CMA is a partnership between Arthur Andersen and a Team ofprofessionals with extensive experience in financial markets. CMA is acompany of Arthur Andersen

4©2000 Arthur Andersen. All rights reserved.

Life Insurance Contracts with Minimum Guaranteed Return

Payout

• At maturity if survival: Endowment• Conditional on death: Term• or Surrender

Premiums

• Single• annual and constant• annual and indexed

Whole life insurance = Endowment + Term

• Insurance Contract:• Entitles the policy holder to earn the maximum between a

guaranteed yield and a participation β on the segregatedfund performance. Given the Lifetime of the contract T andan initial investment I0 (or a periodic payment π).

5©2000 Arthur Andersen. All rights reserved.

Two types of guaranty

Strike resets in thecliquet guaranty

Segregated FundEuropean like Minimum Guaranteed ReturnCliquet Minimum Guaranteed Return

Maturity

• The Company may withdraw hisbenefits during the life of the contract. This is done either on aquarterly or annual basis.

• The insured will receive a finalpayment which is the maximum between a minimum guaratee andthe value of the segregated fund return times his participation rate β.

( ) ( )

−++⋅=Ψ0

00 1;1max

AAArLA TT

gTL β

6©2000 Arthur Andersen. All rights reserved.

Cliquet Dynamics

ΣΣΣΣ

10^3 Scenarios

7©2000 Arthur Andersen. All rights reserved.

Embedded Options

NAV at maturity

K

K K/β

Strike

Premium

1-β

Claim given tothe CompanySeg

regate

d Fun

d

K K/β

1-β

8©2000 Arthur Andersen. All rights reserved.

Insurance Guarantees as Financial Contingent Claims

• Brennan & Schwartz (1976)Pricing of Equity-Linked Life Insurance Policies with Asset Value Guarantee

• Boyle & Schwartz (1977)Equilibrium Prices of Guarantees under Equity-Linked Contracts

• Bacinello & Ortu (1993)Pricing Equity-Linked Life Insurance with Endogenous Minimum Guarantee

• Grosen & Iorgensen (1997)Fair Valuation of Life Insurance Guarantees

• Brys & de Varenne (1997)On the Risk of Life Insurance Liabilities: Debunking Some Common Pitfalls

• Susinno & al (2000)Insurance Optional

• Consiglio, Cocco & Zenios (2001)Scenario Optimization Asset and Liability Modeling for Endowments with Guarantees

9©2000 Arthur Andersen. All rights reserved.

Low Interest rates:Impact on the Interest Margin

0

2

4

6

8

10

12

%

1996 1997 1998 1999 2000

Italian Government Benchmark 10Y

85%Italian Government Benchmark 10Y

Minimum Guaranteed Rate

1996 1997 1998 1999 2000

Average Returns

Policyholder Returns

1996 11.00% 9.05%1997 9.72% 7.91%1998 8.37% 6.89%1999 6.86% 5.59%

10©2000 Arthur Andersen. All rights reserved.

Needs to enhance financial risk exposure

- 1995 -

72%

21%

4%3%

- 1999 -

60%16%

14%

5%5%

Treasury

Corporate

Azioni

Altro

Fondi Comuni

Push towards a majorexposition to financial

risk

(Stocks, Corporate, …)

Push towards a majorexposition to financial

risk

(Stocks, Corporate, …)

Interest Margin Competition

⇒

11©2000 Arthur Andersen. All rights reserved.

Old Eldorado New Mess

12©2000 Arthur Andersen. All rights reserved.

Adding Actuarial Probabilities& annual premiums

+

⇓PortfolioPortfolio Egineering Egineering & Dynamic Asset Allocation & Dynamic Asset Allocation

Whole Life Insurance:The Policyholder owns the right to exercise the guaranty at all possible exit times (American like exercise) conditional on acontractually defined event. Due to independence between mortality and financial Assets The exit may not triggered by a market event! ⇒ The portfolio must be continuously re-balanced

( )∑=

⋅=ΠN

iiit tC

1ζ

13©2000 Arthur Andersen. All rights reserved.

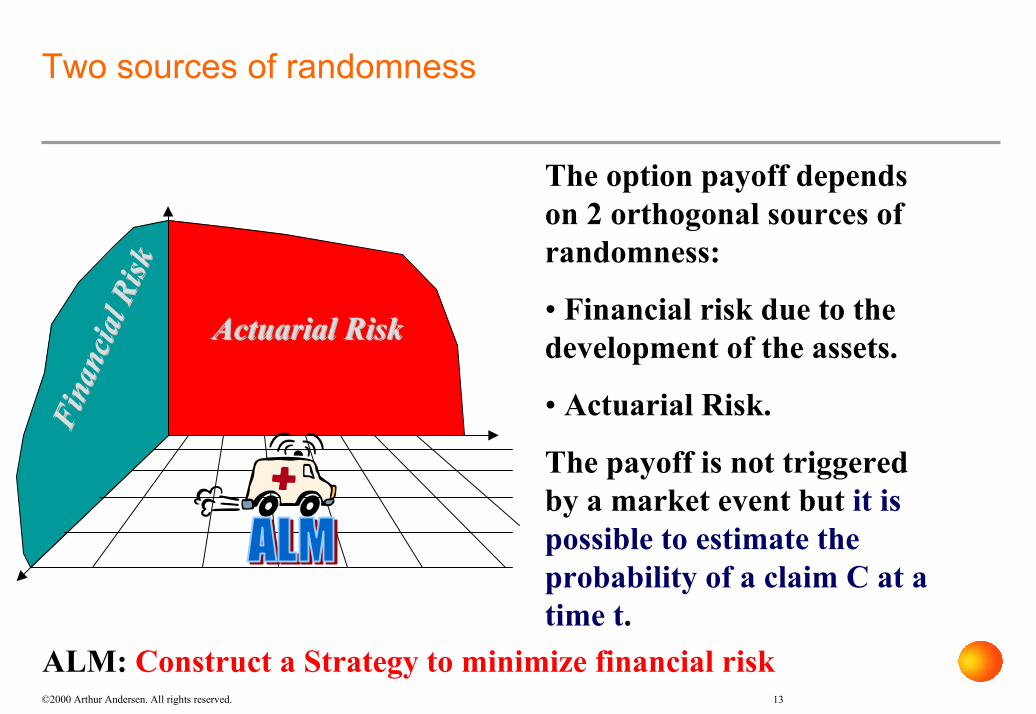

Two sources of randomnessFi

nanc

ial R

isk

Fina

ncia

l Risk

Actuarial RiskActuarial Risk

The option payoff dependson 2 orthogonal sources ofrandomness:

• Financial risk due to thedevelopment of the assets.

• Actuarial Risk.

The payoff is not triggeredby a market event but it ispossible to estimate theprobability of a claim C at atime t.

ALM: Construct a Strategy to minimize financial risk

14©2000 Arthur Andersen. All rights reserved.

Mutual Aspects

• For one insured only a fraction of the guaranteed amount isprotected at each possible exit time while 100% of the payof has tobe given to the insured (Dirac*100%)

• With a large number of insured the uncertainty on the amount ofcapital to cover for each possible exit time is reduced and we are leftwith the volatility of actuarial estimations.

Maturity

T = 0

...

............

15©2000 Arthur Andersen. All rights reserved.

Target

Define investment classes and optimalstrategies.

The control parameter is the mix betweencash and risky assets!!!

Practical Management Actions:

Immunise the downside risk of theshorted put.

⇓

Portfolio InsurancePortfolio Insurance

⇓

16©2000 Arthur Andersen. All rights reserved.

Sensitivity:

• Contract’s Structure

• Actual value of the guaranteed level

• Actuarial probabilities

• Segregated Fund Stat. Prop.

• Transaction Costs and Regulatory Constraints

⇒ ∆

CASH Dynamic Asset Allocation

Strategy!!!Simple Experiment

Dynamic Asset Allocation

17©2000 Arthur Andersen. All rights reserved.

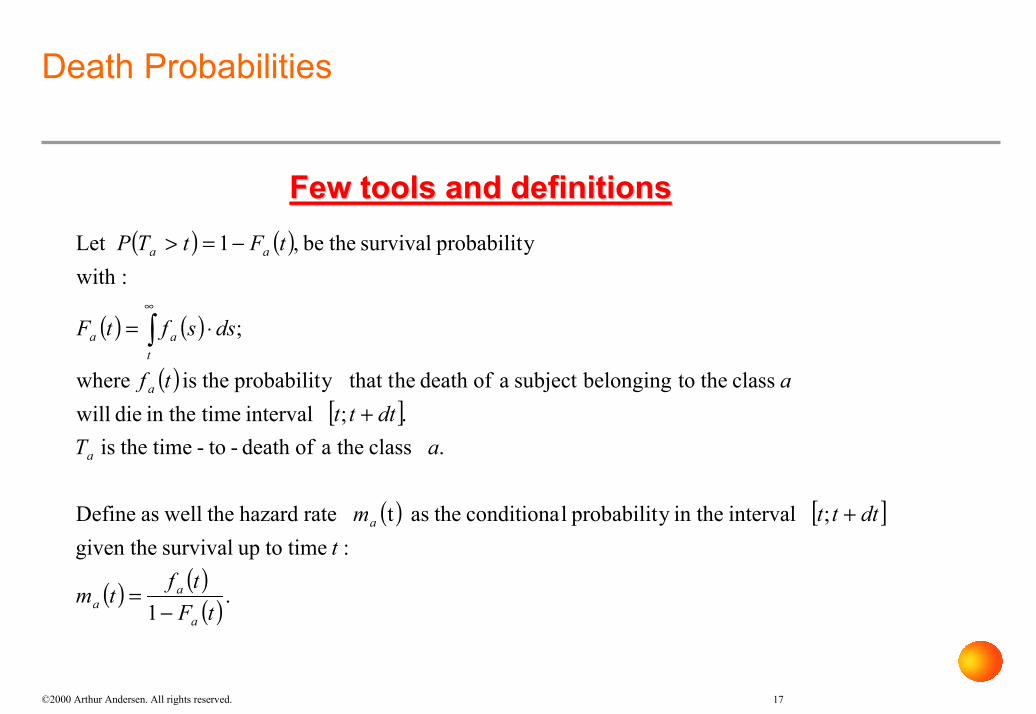

Death Probabilities

( ) ( )

( ) ( )

( )[ ]

( ) [ ]

( ) ( )( ) .

1

: time toup survival given the ; interval in they probabilit lconditiona theas t rate hazard the wellas Define

. class thea ofdeath -to- time theis .; interval timein the die will

class the tobelongingsubject a ofdeath hey that tprobabilit theis where

;

:withyprobabilit survival thebe ,1Let

tFtftm

tdtttm

aTdttt

atf

dssftF

tFtTP

a

aa

a

a

a

taa

aa

−=

+

+

⋅=

−=>

∫∞

Few tools and definitionsFew tools and definitions

18©2000 Arthur Andersen. All rights reserved.

Merging the Two WorldsPayment activated Options

Term• Death in td ∈ [ν,ν+dν] ∀ν ∈

[0,Ta].

⇓B-S Strategy:Hold a weighted portfolio of european

options for each possible time ofdeath ν.

Endowment• Paid if td > T.

⇓

( ) ( ) ( )[ ]

( ) { tTtT

taa

T

ttTt

a

a

adtFtm

>>

+>

=

−−∆=∆ ∫ if 1

otherwise 0 1

11 ννν

( ) ( )[ ]( ) { tT

tT

tattTt

a

a

atTF

>>

+>

=

−−⋅∆=∆ if 1

otherwise 0 1

11~

Much simpler correction

19©2000 Arthur Andersen. All rights reserved.

Application

From Actuarial estimations it is possible to deduce the fraction ξi of contracts maturing at time Ti, ∀ Ti < T.

The event “maturity” can be triggered either by the end of a given contract or by a death event.

Definition: ∆t is the sensitivity at time t of a contingent claim w.r.t. a variation of the underlying value

20©2000 Arthur Andersen. All rights reserved.

A First Approach : Delta-Hedging

Fixed Income

Shares

Cash

Fixed Income

Shares ∆∆∆∆}

Desinvestmentor

Structured Products

21©2000 Arthur Andersen. All rights reserved.

A First Approach : Delta Hedging (Simulations)

• Apply Black&Scholes delta hedging to replicate the put option

• Consider the benchmark as the option’s underlying

22©2000 Arthur Andersen. All rights reserved.

A Less Naive Approach : Modified Black&Scholes

RiskyAssets Risky

Assets

Option Price

Fund F0with volatility σσσσ

Fund (F0-P0)with volatility

σσσσ

RiskyAssets

Option Price

Cash

Fund (F0-P0)with volatility

σσσσ....(1-∆∆∆∆)

∆∆∆∆

23©2000 Arthur Andersen. All rights reserved.

A Less Naive Approach : Modified Black&Scholes (Simul.)

• Remember that no premium is paid for the put option

• Consider the fund (=benchmark+put) as the underlying

24©2000 Arthur Andersen. All rights reserved.

Proportion of Cash : Comparative Study

Guaranteed minimum

Floor

K

25©2000 Arthur Andersen. All rights reserved.

Tradeoffs

Expected Shortfall Expected Returns

Transaction Costs Discrete Hedging Errors

Precision, Variables Computation Time

26©2000 Arthur Andersen. All rights reserved.

Relative Performance Dynamic/Static Strategy.

27©2000 Arthur Andersen. All rights reserved.

Transaction Costs (Arbitrary Units)

28©2000 Arthur Andersen. All rights reserved.

A general scheme

* ROA= RETURN ONASSETS

SHAREHOLDERS

ROEROE

SEGREGATED FUND

COMPANY insured

MANAGEMENT FEES

Reim

burs

men

ts

NET

PREM

IUM

S

INTERESTMARGIN

SOLVENCYMARGIN

SOLVENCYMARGIN

ADJUSTMENTS

MARKET

ROAROA

COSTS

29©2000 Arthur Andersen. All rights reserved.

Let’s Play with Real World…Static Approach

30©2000 Arthur Andersen. All rights reserved.

Let’s Play with Real World…Dynamic Approach

31©2000 Arthur Andersen. All rights reserved.

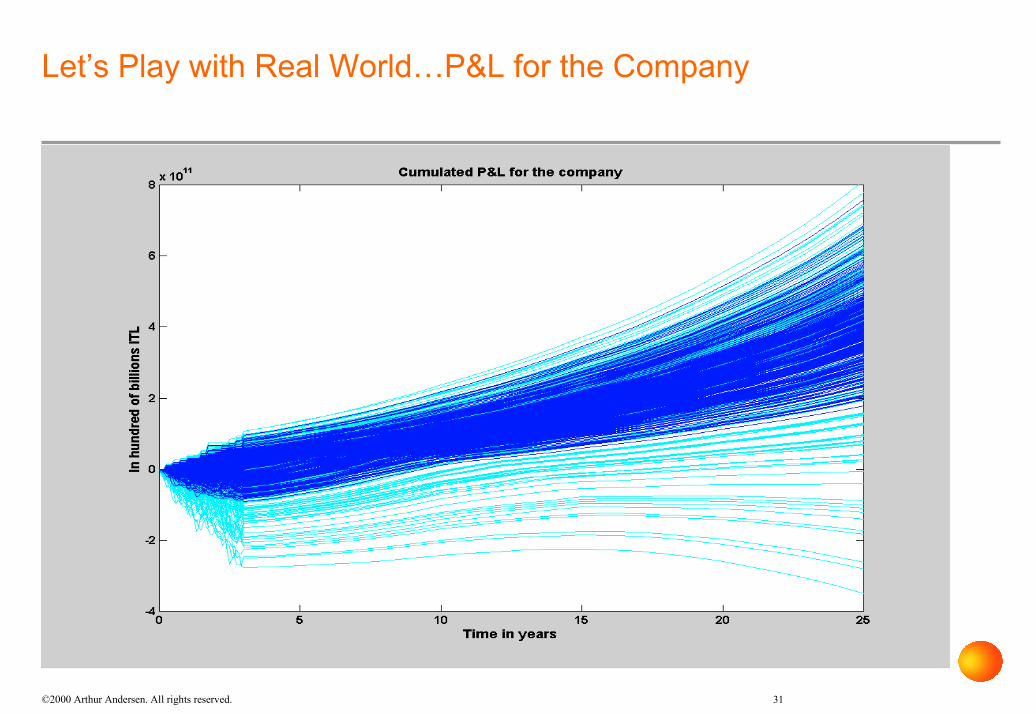

Let’s Play with Real World…P&L for the Company

32©2000 Arthur Andersen. All rights reserved.

Further Analysis

• Stochastic Optimal Control

Maximize a utility function given management constraints for aset of market scenarios

• Passport Options

Option on a trading account

33©2000 Arthur Andersen. All rights reserved.

Technical Issues From Theory to Practice:

• Parameter Estimators Accuracy →→→→ Number of Scenarios

• Optimization →→→→ Number of Parameter Estimations

• Number of Key Variables Nvar (Liabilities, Assets, RF, …)

Nscenarios X Ntimesteps X Npolicies X Nvar

(e.g. 10000 X 400 X 26 X Nvar)

NEED:

Dynamic redistribution of the workload among nodes of a computercluster to prevent memory depletion.

34©2000 Arthur Andersen. All rights reserved.

Technical Issues

Optimization problems may betackled at different levels ofcomplexity.

Operational Computer AidedAsset & Liability Managementmay benefit from up to datecomputing technologies.

HPC is today an attainablesolution which could bring tothe risk management field anew powerful instrument.

35©2000 Arthur Andersen. All rights reserved.

Flowchart

36©2000 Arthur Andersen. All rights reserved.

How to use the hidden power

37©2000 Arthur Andersen. All rights reserved.

CMA ALM engine

DBAssets

Portfolio

DBLiabilitiesPortfolio

DBMarketDatas

ALM Computational Engine

Aggregation

38©2000 Arthur Andersen. All rights reserved.

Network Structure.

39©2000 Arthur Andersen. All rights reserved.

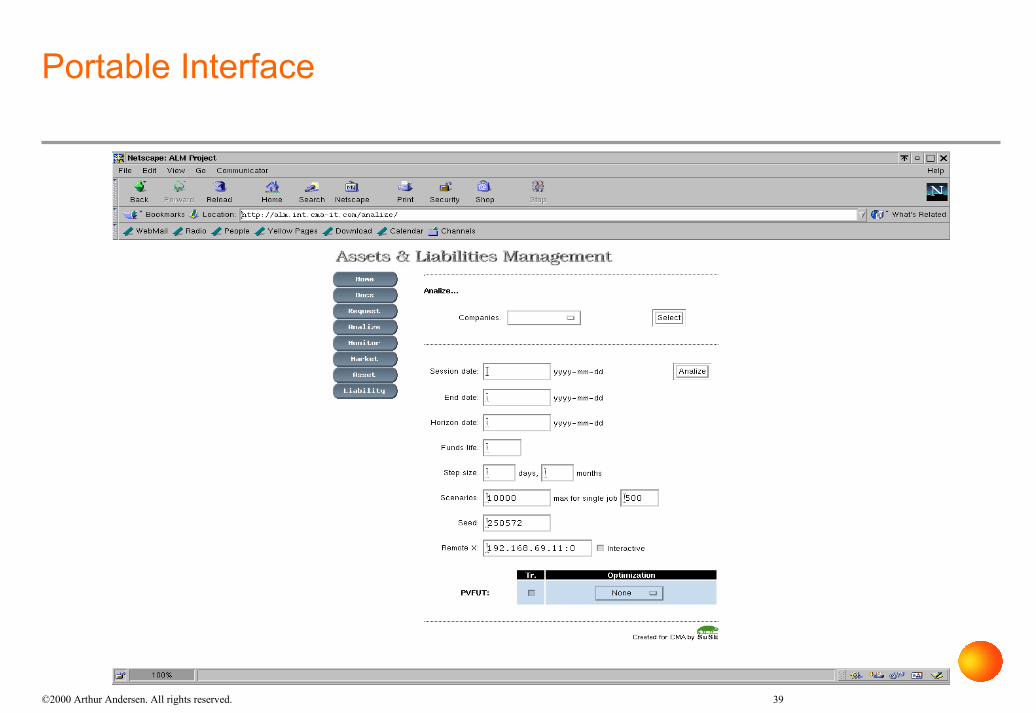

Portable Interface

40©2000 Arthur Andersen. All rights reserved.

Final Remarks

• Hedging of volatility risk shouldn’t hide othermanagement risks : credit, liquidity, ...

• Portfolio’s manager monitoring (tracking error)

• Less volatility in ROE => better public image

41©2000 Arthur Andersen. All rights reserved.

Managed Risk

• Compliance with regulatory constraints andrating agencies

• Lower capital requirements

• Better rating and lower cost of capital

Final Remarks

Asset Liability Managementfor Life Insurance:

a Dynamic Approach Dr Gabriele Susinno & Thierry Bochud

Quantitative StrategiesCapital Management Advisors

CAPITAL MANAGEMENT ADVISORS srlRisk Consulting

Madrid May, 23rd, 2001