asset building in rural communities: exploring and identifying opportunities rosemary heins jeanne...

TRANSCRIPT

Asset Building in Rural Communities:Exploring and Identifying Opportunities

Rosemary Heins

Jeanne Warning

Cynthia Needles Fletcher

Patricia Olson

andLynette Flage

North Dakota State University

Iowa State University University of Minnesota

Background

• 7-state initiative to build leadership and reduce poverty in rural communities

• 3 phases: learning, leadership, action

• pathways to financial security and opportunity

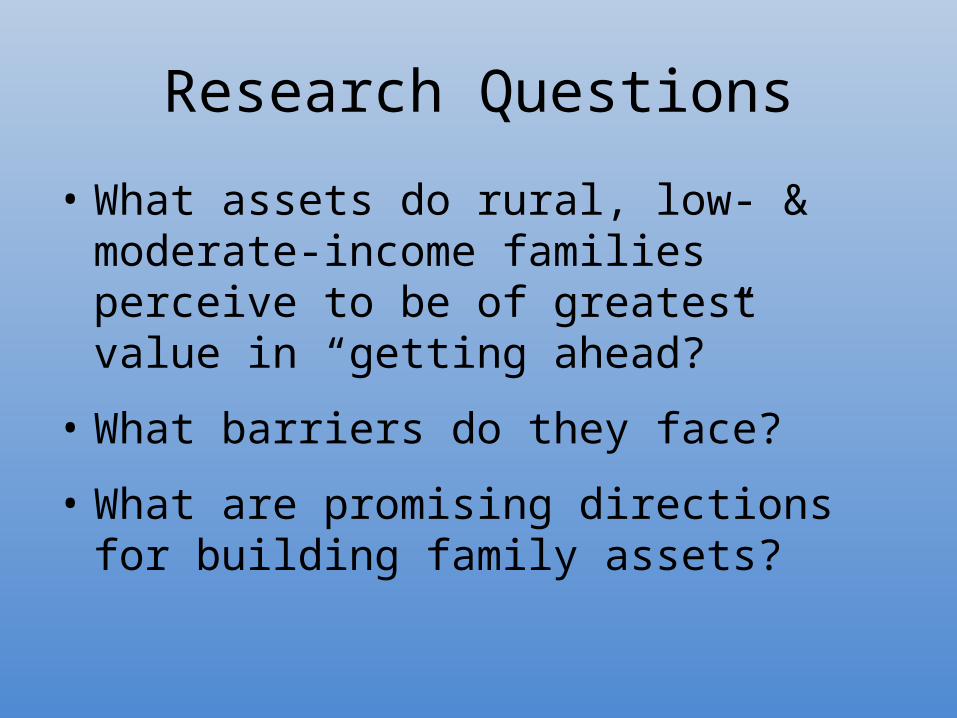

Research Questions

• What assets do rural, low- & moderate-income families perceive to be of greatest value in “getting ahead?”

• What barriers do they face?

• What are promising directions for building family assets?

Bridging Two Asset- Building Paths

• community rural development

• family economics

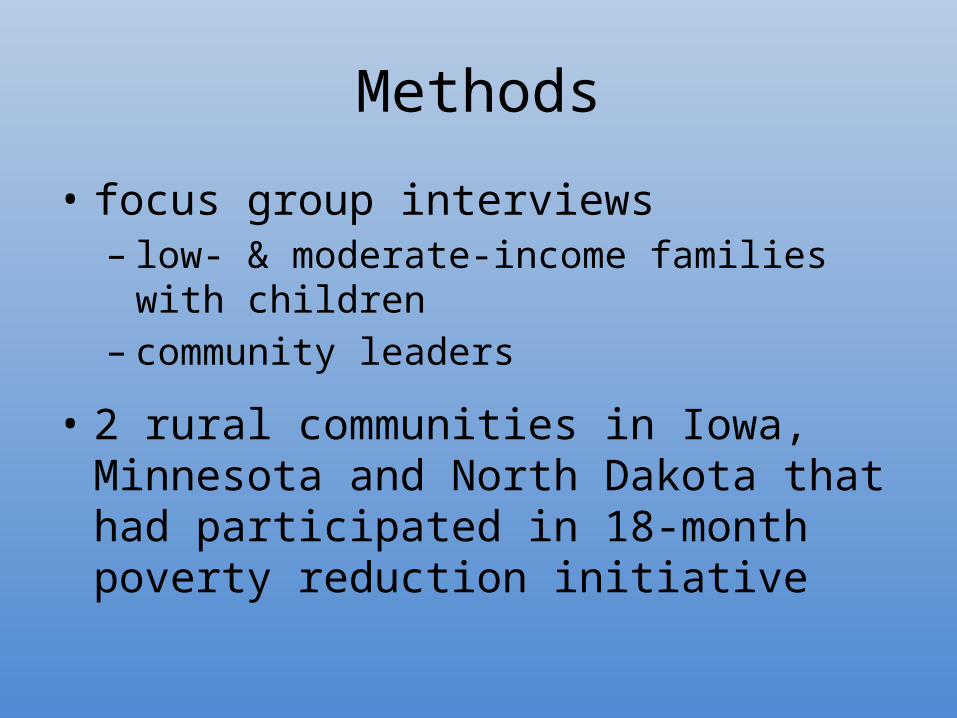

Methods

• focus group interviews– low- & moderate-income families with children– community leaders

• 2 rural communities in Iowa, Minnesota and North Dakota that had participated in 18-month poverty reduction initiative

Data

• 12 focus group interviews

• 77 total participants

• 6 communities in 3 states

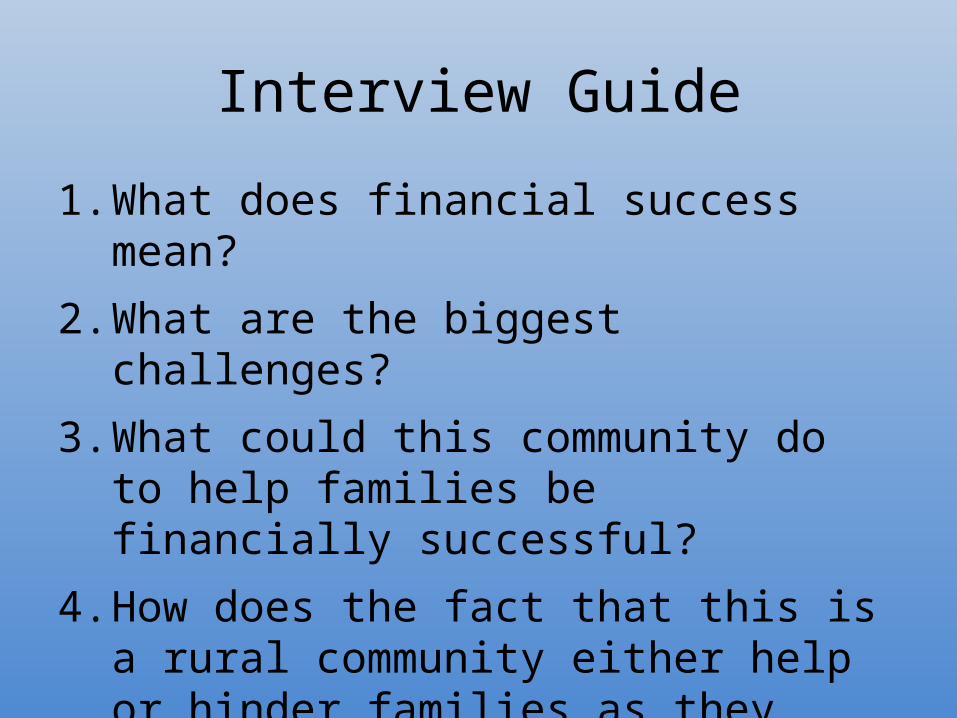

Interview Guide

1. What does financial success mean?

2. What are the biggest challenges?

3. What could this community do to help families be financially successful?

4. How does the fact that this is a rural community either help or hinder families as they manage their finances?

Findings

• Barriers– individual & family– community– societal

• Asset-Building Strategies– youth– adults– other

Barriers to Asset Building in Rural Communities

Question for chat box

• From your own experience, what barriers do rural families face?

• Type in the chat box to share your answers

Individual & Family Barriers

• Personal decisions & lifestyle choices

“we have to careful about saying ‘choices’ because I think not everyone has all the same options available to them or the same resources or skills …….”

Individual & Family Barriers

• Limited financial management skills

“People don’t know how to save.”

Individual & Family Barriers

• Lack of education & job skills

“Education --- they have to have a chance to be educated beyond high school … that will provide a much better job.”

Individual & Family Barriers

• Lack of reliable transportation

“….. You know, I gotta job, and I can’t afford a car, I need a way to get to work every day.”

Community Barriers

• Lack of employment opportunities– low wages– few local part-time jobs for

youth– hard to grow jobs

Community Barriers

• Limited basic goods/ services, as well as– affordable housing– child care– banking – affordable loans– mental health services

Community Barriers

• Lack of adult and youth education programming

• Stigma: “Everybody knows everybody”

Community Barriers

• Building “sense of community” is difficult

“they are here to sleep, and they go out of town, do groceries, go to church out of town. We just don’t know people anymore.”

Societal Barriers

• National economy

• Lack of affordable, accessible work supports– child care– transportation– health insurance/services

Societal Barriers

• Saving is counter-cultural

• Consumer society: easy credit/instant gratification

• Predatory marketplace

• Rising cost of education/debt

Asset-Building Strategies for Youth

Children’s Savings Accounts

Seeded by an initial deposit, accounts grow to age 18.

Savings-in-the-School

In-school banking teaches the savings habit and augments financial education.

Academic incentives

Rewarding academic success for good grades or scholarships at graduation

Financial literacy/career mentoring

Adult volunteers mentor financial skill-building & career decision-making

Innovations in 529 plans

Financial incentives to encourage lower-income families’ participation

Asset-Building Programs for Adults

Financial Education for Adults

Integrating adult financial education into existing venues – pre-school settings, worksites and other community organizations

Scholarships for non-traditional students

Grants for higher education focused on those who did not go directly to post-secondary education.

Mentoring

Mentoring or coaching programs train professionals or volunteers who, in turn, help consumers clarify financial goals and problem solve

Small business support and education

Training and technical assistance can help small business owner understand employee benefits and proven strategies that facilitate asset building among employees.

Affordable car programs

Example: Ways to Workhttp://www.waystowork.org

Programs help families get and maintain a reliable car by acquiring a used, donated car, obtaining an affordable loan, and/or saving for a vehicle through a matched savings program.

Other Strategies in Asset Building

Indirect Strategies to Family Asset Building

• Health care

• Child care

• Transportation

• Community event

Health Care

• Impact of health care on ability to build assets and wealth

• Potential solutions?

Child Care and Assets

• Access

• Cost

• Potential Solutions?

Transportation

• Access

• Cost

• “…there’s not a lot of good-paying jobs in the community…so it’s easier to seek work elsewhere, outside of our community.”

• Creative solutions?

Community Events

Support Structure

Get to Know Each

Other

Event

Question for chat box

• What additional ideas are you aware of that rural communities have used to support asset building in their community?

• Type in the chat box to share your answers

Future Directions

• There is growing evidence to support the asset-building approach

• Grow the evidence to support the asset-building approach

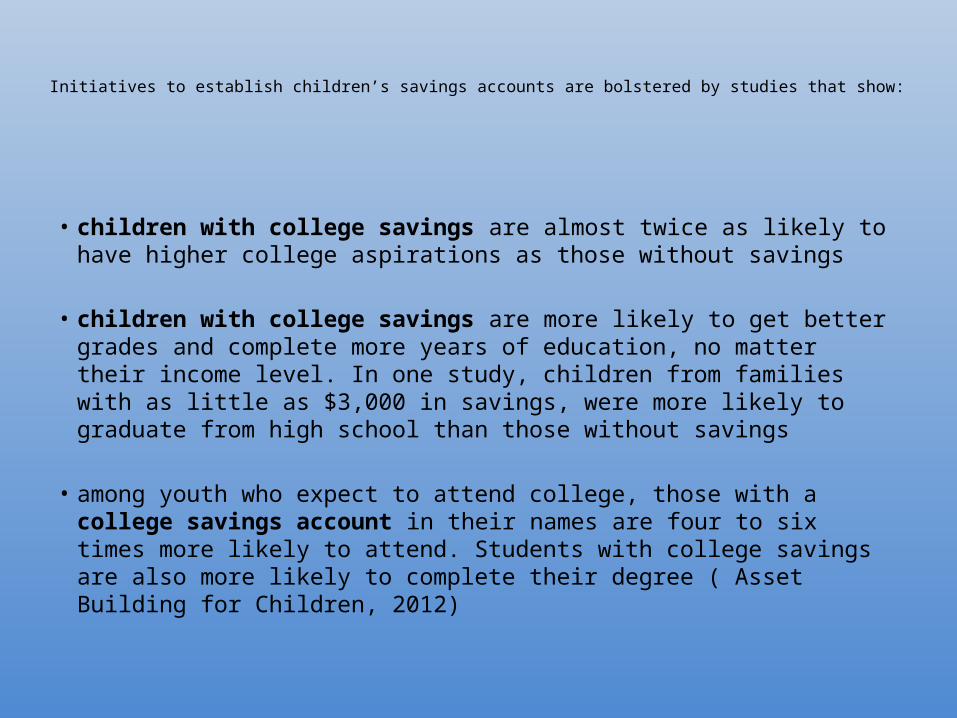

Initiatives to establish children’s savings accounts are bolstered by studies that show:

• children with college savings are almost twice as likely to have higher college aspirations as those without savings

• children with college savings are more likely to get better grades and complete more years of education, no matter their income level. In one study, children from families with as little as $3,000 in savings, were more likely to graduate from high school than those without savings

• among youth who expect to attend college, those with a college savings account in their names are four to six times more likely to attend. Students with college savings are also more likely to complete their degree ( Asset Building for Children, 2012)

Question for chat box

• Describe next steps in our respective fields to community based approaches to asset building?

• Type in the chat box to share your answers

Community-based approaches to asset building

• priorities for new asset-building efforts that are perceived to be of greatest benefit to rural families in building financial stability;

• barriers faced by rural families in their attempts to build assets

• opportunities that could be shaped by collaborations among individuals and families, and community leaders to enhance asset building in rural communities

Questions? Please type in the chat box.

Thank You

Asset Building in Rural Communities: Exploring Barriers and Identifying Opportunities

Cynthia Needles Fletcher ([email protected])

Jeanne Warning ([email protected]) Iowa State University

Rosemary Heins ([email protected])Patricia Olson ([email protected])

University of Minnesota