assessment of working capital management rajastan spining & weaving mills ltd

TRANSCRIPT

A Project Report On;

“Commodity Futures”For Prabodh Pvt. Ltd.

SUBMITTED TO,

Dr. B.A.M.U. UNIVERSITY, AURANGABAD

IN PARTIAL FULFILLMENT OF 3 YEARS FULL TIME COURSE OF-

BACHELOR OF BUSINESS ADMINISTRATION

Submitted By:

xrf

A report submitted in partial fulfillment of

The requirement of

Bachelor of Business Administration

{BBA}

DEOGIRI COLLEGE AURANGADAD

Acknowledgement

I have great pleasure to present the project report on “Commodity Futures” for Prabodh, in

partial fulfillment of Master’s Degree in Business Administration, University of Aurrangabad, at

Deogiri Institute of Management & Research,.

I would like to place on records deepest sense of gratitude to Mr. Mohan Chimanlal Gujarathi,

Director of Prabodh, for his inspiring and able guidance which made it possible to bring the best

of my efforts on the project.

I am desirous of placing on record profound indebtedness to Mr. Balachandran, project guide, for

valuable advice, guidance and support he offered.

I also acknowledge the gratitude to Director of Deogiri Institute of Management & Research,.

who motivated us a lot in carrying out this project.

CONTENTS

INTRODUCTION AND SCOPE OF THE PROJECT…………………….…………1

INTRODUCTION TO FUTURES…………………………………………..………... 3

FUTURES TERMINOLOGY

COMMODITY DERIVATIVES

DEFINITION OF COMMODITY FUTURES

PRICING OF COMMODITY FUTURES

INVESTMENT ASSETS VERSUS CONSUMPTION ASSET

PRICING

BASIC PAYOFFS

TRADING IN COMMODITY FUTURES / TRADING SYSTEM

CLEARING AND SETTLEMENT

REGULATORY FRAMEWORK

THE ‘COMMODITY EXCHANGE’ PLATFORM…………………….…………... 18

PROMOTERS & GOVERNANCE

THE NCDEX SYSTEM: HOW TRANSACTION HAPPENS ON THE NCDEX

CLEARING

SETTLEMENT

COMMODITY ANALYSIS…………………….…………………….……………… 20

BULLION (PRECIOUS METALS): GOLD & SILVER

ENERGY: CRUDE OIL

CONCLUSION…………………….…………………….………………………… 105

ECONOMIC FUNCTIONS: LIQUIDITY, RISK TRANSFER, PRICE DISCOVERY

BENEFICIARIES

INVESTMENT IN COMMODITY FUTURES

BIBLIOGRAPHY…………………….…………………….……………………….. 111

ANNEXURE-I…………………….…………………….…………………………… 112

ANNEXURE-II…………………….…………………….…………………………... 119

CONTENTS

INTRODUCTION AND SCOPE OF THE PROJECT…………………….…………1

INTRODUCTION TO FUTURES…………………………………………..………... 3

FUTURES TERMINOLOGY

COMMODITY DERIVATIVES

DEFINITION OF COMMODITY FUTURES

PRICING OF COMMODITY FUTURES

INVESTMENT ASSETS VERSUS CONSUMPTION ASSET

PRICING

BASIC PAYOFFS

TRADING IN COMMODITY FUTURES / TRADING SYSTEM

CLEARING AND SETTLEMENT

REGULATORY FRAMEWORK

THE ‘COMMODITY EXCHANGE’ PLATFORM…………………….…………... 18

PROMOTERS & GOVERNANCE

THE NCDEX SYSTEM: HOW TRANSACTION HAPPENS ON THE NCDEX

CLEARING

SETTLEMENT

COMMODITY ANALYSIS…………………….…………………….……………… 20

BULLION (PRECIOUS METALS): GOLD & SILVER

ENERGY: CRUDE OIL

CONCLUSION…………………….…………………….………………………… 105

ECONOMIC FUNCTIONS: LIQUIDITY, RISK TRANSFER, PRICE DISCOVERY

BENEFICIARIES

INVESTMENT IN COMMODITY FUTURES

BIBLIOGRAPHY…………………….…………………….……………………….. 111

ANNEXURE-I

ANNEXURE-II

CONTENTS

INTRODUCTION AND SCOPE OF THE PROJECT……………………. 1

COMMODITY FUTURES……………………. 3FUTURES TERMINOLOGYCOMMODITY DERIVATIVESDEFINITION OF COMMODITY FUTURESPRICING OF COMMODITY FUTURESINVESTMENT ASSETS VERSUS CONSUMPTION ASSETPRICINGBASIC PAYOFFSTRADING IN COMMODITY FUTURES FUTURES TRADING SYSTEM CLEARING AND SETTLEMENT REGULATORY FRAMEWORK

THE ‘COMMODITY EXCHANGE’ PLATFORM……………………. 18 PROMOTERS & GOVERNANCE THE NCDEX SYSTEM: HOW TRANSACTION HAPPEN ON THE NCDEX CLEARING SETTLEMENT

COMMODITY ANALYSIS……………………. 20BULLION (PRECIOUS METALS): GOLD & SILVERENERGY: CRUDE OIL CONCLUSION……………………. 105 ECONOMIC FUNCTIONS: LIQUIDITY, RISK TRANSFER, PRICE DISCOVERY BENEFICIARIESINVESTMENT IN COMMODITY FUTURES:

ANNEXURE-I

ANNEXURE-II

INTRODUCTION AND SCOPE OF THE PROJECT:

The origin of derivatives can be traced back to the need of farmers to protect themselves against fluctuations in the price of their crop. From the time it was sown to the time it was ready for harvest, farmers would face price uncertainty. Through the use of simple derivative products, it was possible for the farmer to partially or fully transfer price risks by locking in asset prices. These were simple contacts developed to meet the needs of farmers and were basically a means or reducing risk.

A farmer who sowed his crop in June faced uncertainty over the price he would receive for his harvest in September. In years of scarcity, he would probably obtain attractive prices. However during times of oversupply, he would have to dispose off his harvest at a very low price. Clearly this meant that the farmer and his family were exposed to a high risk of price uncertainty.

On the other hand, a merchant with and ongoing requirement of grains too would face a price risk that of having to pay exorbitant prices during dearth, although favorable prices could be obtained during periods of oversupply. Under such circumstances, it clearly made sense for the farmer and the merchant to come together and enter into a contract whereby the price of the grain to be delivered in September could be decided earlier. What they would then negotiate happened to be a futures type contract, which would enable both parties to eliminate the price risk.

In 1848, the Chicago board of trade, or CBOT was established to bring farmers and merchants together. A group of traders got together and created the to arrive contract at proved useful as a device for hedging and speculation on price changes. These were eventually standardized, and in 1925 the first futures clearing house came into existence.

Today, derivative contracts exist on a variety of commodities such as corn, cotton etc. Besides commodities, derivatives contracts also exist on a lot of financial underlying like stocks, exchange rate, interest rate, etc.

Derivatives products today which play an important role in finance world came out as ‘hedging tool’. Volatility in prices of products in cash market has lead to trading in forward or futures markets. Derivatives products include forward, futures and options, swaps etc. The underlying instruments could be financial instruments or commodities. In agricultural dominated country like India trading in commodities is deeply rooted. The price movements in agricultural products have always been a major concern of farmers, manufacturers as well as consumers. Due to development of well organized and more technically advanced market place the Exchanges were evolved where people enter into futures contracts. MCX and NCDEX provide the facility of online trading in commodity futures the same as NSE in case of financial instruments such as shares. Right now options are not available.

The reason behind evolution of commodity futures was hedging against prices movements in commodities such as cotton, sugar, gold, silver, crude oil, etc. Commodity futures play vital role in Price discovery, Liquidity (leverage), and Risk transfer.

This project is carried out to understand the concept and trading of commodity futures and analysis of commodities. In his project commodities taken for analysis are Gold, Silver and Crude oil.

The scope of commodity futures is very wide and so project is carried out on 3 commodities: GOLD, SILVER (BULLION FUTURES) and CRUDE OIL (CRUDE OIL FUTURES) as the volume in these futures are more than other commodities on MCX and NCDEX.

The project work includes:1) Study the evolution of commodity markets in India2) Study the trading system3) Study of commodities (study limited to 3 commodities GOLD, SILVER AND CRUDE

OIL) and commodity analysis for investment purpose4) Finding trading tool for making profit5) Finding investment strategies

The above work is done with help of data collected from ‘PRABODH’ where the project is carried, different web sites (MCX and NCDEX) and material available at ‘PRABODH’.

COMMODITY FUTURES:

Futures markets were designed to solve the problems that exist in forward markets. A futures contract is an agreement between two parties to buy or sell an asset at a certain time in the future at a certain price. But unlike forward contracts, the futures contracts are standardized and exchange traded. To facilitate liquidity in the futures contracts, the exchange specifies certain standard features of the contract. It is standardized contract with standard underlying instrument, a standard quantity and quality of the underlying instrument that can be delivered, and a standard living of such settlement. A futures contract may he offset prior to maturity by entering into an equal and opposite transaction. More than 99% of futures transactions are offset this way.

Definition: “ It is an agreement to buy or sell a specified quantity of commodity in a designated future month at a price agreed upon by the buyer and seller. “

The standardize items in futures contracts are:1) Quantity of the underlying 2) Quality of the underlying3) The date and the month of delivery 4) The units of price quotation and minimum price change 5) Location of settlement

Futures terminology:

1) Spot Price: The price at which an asset trades in the spot market

2) Futures Price: The price at which the futures contract trades in futures market.

3) Contract cycle: The period over which a contract trades. The commodity futures contracts on the NCDEX have one-month, two-months and three months expiry cycles which expire on the 20th day of the delivery month. Thus a Jan expiration contract expires on the 20thjan and a Feb expiration contract ceases trading on the 20th Feb. On the next trading day following the 20th, a new contract having a three-month expiry is introduced for trading.

4) Expiry date: It is the date specified in the futures contract. This is the last day on which the contract will be traded, at the end of which it will cease to exist.

5) Delivery Unit: The amount of asset that has to be delivered under one contract. For instance, the delivery unit for futures on Long Staple Cotton on the NCDEX is 55 bales. The delivery unit of the Gold futures contract is 1 kg.

6) Basis: Basis can be defined as the futures price minus the spot price. There will be a different basis for each delivery month for each contract. In a normal market, basis will be positive. This reflects that futures prices normally exceed spot prices.

7) Cost of Carry: The relationship between futures prices and spot prices can be summarized in terms of what is known as the cost of carry. This measures the storage cost plus the interest that is paid to finance the asset less the income earned on the asset.

8) Initial Margin: The amount that must be deposited in the margin account at the time a futures contract is first entered into is known as initial margin.

9) Marking to market (MTM): In the futures market, at the end of each trading day, the margin account is adjusted to reflect the investors gain or loss depending upon the futures closing price. This is called marking to market.

10) Maintenance Margin: This is somewhat lower than the initial margin. This is set to ensure that the balance in the margin account never becomes negative. If the balance in the margin account falls below the maintenance margin, the investor receives a margin call and is expected to top up the margin account to the initial margin level before trading commences on the next day.

COMMODITY DERIVATIVES:

Derivatives as a tool for managing risk first originated in the commodities markets. They were then found useful as a hedging tool in financial markets as well. In India, trading is commodity futures has been in existence from the 19th century with organized trading in cotton through the establishment of cotton treade4 association in 1875. Over a period of time, other commodities were permitted to be traded in futures exchanges. Regulatory constraints in 1960s resulted in virtual dismantling of the commodities futures markets. It is only in the last decade that commodity future exchanges have been activelyu encouraged. However, the markets have been thin with poor liquidity and have not grown to any significant level.

COMMODITY FUTURES:It is an agreement between two parties to buy or sell the underlying commodity at a future date at today’s future price. Futures contracts differ from forward contracts in the sense that they are standardized and exchange traded.

PRICING OF COMMODITY FUTURES:

The process of arriving at a figure at which a person buys and another sell a futures contract for a specific expiration date is called price discovery. In an active futures market, the process of price discovery continues from the markets opening until its close. The prices are freely and competitively derived. Futures prices are therefore considered to be superior to the administered prices or the prices that are determined privately. Further, the low transaction costs and frequent trading encourages wide participation in futures markets lessening the opportunity for control by a few buyers and sellers.

INVESTMENT ASSETS VERSUS CONSUMPTION ASSET:

While studying futures contracts, it is essential to distinguish between investment assets and consumption assets. An investment asset is an asset that is held for investment purpose by most investors. Stocks and bonds are examples of investment assets. Gold and sliver are also examples of investment assets. Note however that investment assets do no always have to be held exclusively for investment. As we saw earlier, silver, for example have a number of industrial uses. However, to classify as investment assets, these assets do have to satisfy the requirement that they are held by a large number of investors solely for investment. A consumption asset is an asset that is held primarily for consumption. At is not usually held for investment. Examples of consumption assets are commodities such as copper, oil, and pork bellies.

PRICING

Financial Instruments Futures:

There is no cost of carry, but the holding cost is cost of financing (less) Dividend Returns. Therefore the fair value of Future contract can be defined as under: F = Sert

Where, F = Future PriceS = Spot Pricer = Cost of Financing (using continuous compounded interest rate)t = Time till expiratione = 2.71828

Commodities Futures: In commodities you have to carry till it is sold as there is physical delivery. Here the seller so insures ‘holding cost’ which is equal to cost of finance + Storage cost + Insurance. Fair value of Future contract here is defined as under: F = (S + U)ert Where,F = Future PriceS = Spot PriceU = Present Value of Storage r = Cost of Financing (using continuous compounded interest rate) t = Time till expiration e = 2.71828

BASIC PAYOFFS:

PAYOFF FOR COMMODITY FUTURES:Futures contract have linear payoff, just like the payoff of the underlying asset. If the price of the underlying rises, the buyer makes profits. If the price of the underlying falls, the buyer makes losses. The magnitude of profits or losses for a give upward or downward movement is the same. The profits as well as losses for the buyer and the seller for a futures contract are unlimited. These linear payoffs are fascinating as they can be combined with options and the underlying to generate various complex various complex payoffs.

PAYOFF FOR BUYER OF FUTURES: LONG FUTURES:The payoff for a person who buys a futures contract is similar to the payoff for a person who holds an asset. He has a potentially unlimited upside as well as a potentially unlimited downside.

Payoff For A Buyer Of Bold:The figure shows the pro9fits/losses from long position of gold. The investor bought gold at Rs 6000 per 10 grams. If the price of gold rises, he is in profit and if prices of gold fall he is in losses.

+500

0 5500 6000 6500GOLD

-500

Payoff for a Seller of Cotton:

The figure shows the profits/ losses from a short position on cotton. The investopr sold long staple cottonm at Rs. 6500 per Quintal. If the price of cotton falls, he profits. If the price of cotton rises, he looses.

+500

0 6000 6500 7000Long Staple Cotton

-500

Payoff for a Buyer of Gold Futures:

The figure shows the profits/losses for a long futures position. The investor bought futures when gold futures were trading at Rs. 6000 per 10 grams. If the price of the underlying gold goes up, the gold futures price too would go up and his futures position starts making profit. If the price of gold falls, the futures price falls too and his futures position starts making profit. If price of gold falls, the futures price falls too and his futures position starts showing losses.

Profit

0 6000 GOLD future price

Loss

Payoff for seller of futures: Short futures

The payoff for a person who sells a futures contract is similar to the payoff for a person who shorts an sset. He has a potentially unlimited upside as well as a potentially unlimited downside. Take the case of a speculator who sells a two – month cotton futures contract when the contract sells Rs 6500 per quintal. The underlying asset in this is long staple cotton. When the prices of long stale cotton moves down, the cotton futures prices also move down and the short futures position starts making profits. When the prices of long staple cotton move up, the cotton futures price also moves up and the short futures position starts making loses. The following figure shows the pay off diagram for the seller of a futures contract:

The figure shows the profits/ losses for a short futures position. The investor sold cotton futures at Rs 6500 per quintal. If the price of the underlying long staple cotton goes down, the future

price also falls, and the short futures position starts making profit. If the price of underlying long staple cotton rises, the futures too rise, and the short futures position starts showing losses.

Profit

0 6500 Cotton Futures Price

Loss

TRADING IN COMMODITY FUTURES

Futures Trading System:

The trading system on the “exchange” provides a fully automated screen based trading for futures on commodities on a nationwide basis as well as an online monitoring and surveillance mechanism.Here we take NCEDX Platform. It supports an order driven market and provides complete transparency of trading operations.

The NCDEX system supports an order driven market, where orders match automatically. Order matching is essentially on the basis of commodity, its price, time and quantity. All quantity fields are in units and price in rupees. The exchange specifies the unit of trading and the delivery unit for future contracts on various commodities. The exchange notifies the regular lot size and tick size for each of the contracts traded for time to time. When any order enters the trading system, it is an active order. It tires to find a match on the other side of the book. If it finds a match, a trade is generated. It does not find a match; the ordr4 becomes passive and gets queued in the respective outstanding order book in the system. Time stamping is done for each trade and provides the possibility for a complete audit trail if required.

Entities in the Trading System:

There are two entities in the trading system of NCDEX- trading cum clearing members and professional Clearing members:

1) Trading cum clearing members (TCMs):Trading cum clearing members are members of NCDEX. They can trade and clear either on their own account or on behalf of their clients including participants. The exchange assigns an ID to each TCM. Each TCM can have more than on user. The number of user allowed for each trading member is notified by the exchange from time to time.Each user of TCM must be registered with the exchange and is assigned an unique user ID. The unique TCM ID functions as a reference for all orders/trades of different users. This ID is common for all users of a particular TCM. It is the responsibility of the TCM to maintain adequate control over persons having access to the firm’s User IDs.

2) Professional clearing members:

Professional clearing members are members of NSCCL. The PCM membership entitles the members to clear trades executed through Trading cum Clearing Members (TCMs), both for themselves and or on behalf of their clients. They carry out risk management activities and confirmation inquiry of trades through the trading system.

Some important Commodity Futures Contract and their Symbols:Pure Gold Mumbai GLDPURMUMPure Silver New Delhi SLVPURDELSoybean Indore SYBEANIDRRefined Soya Oil Indore SYOREFIDRRapeseed Mustard Seed Jaipur RMSEEDJPRCrude Palm Oil Kandla KRDPOLKDL

Contracts Specification for Commodity Futures:

NCDEX in the first phase under the category of bullion, it has already started trading in gold and silver, and in agri commodities, trading has commenced in cotton (long and medium staple), soybean, soy oil, rape/mustard seed, rape/mustard oil, crude palm oil an RBD palmolein. In the second phase NCDEX plans to offer the following commodities for trading: Rice, wheat, coffee, tea, edible oil products like groundnut, sunflower, castor, base metals, and commodity indices like agri commodity index and metal commodity index.

Commodity Futures Trading Cycle:

NCDEX trades commodity futures contracts having one- month, two- month, three- month expiry cycles. All contracts expire on the 20th of the expiry month. Thus a Jan expiration contract would expire on the 20the of January and a Feb expiry contract would cease trading on 20th Feb. If the 20th of expiry month is a trading holiday, the contract shall expire on previous trading day.

New contracts will be introduced on the trading day following the expiry of the near month contract. The following figure show contract cycle for futures contracts on NCDEX:As can be seen, at any given point of time, three contracts are available for trading a near month a middle month and far month. As the Jan contract expires on the 20th of the month, a new three-month contract starts trading from the following day, once more making available three index futures contracts for trading

JAN FEB MAR APR

JAN 20 contract

FEB 20 contract

MAR 20 contract

APRIL 20 contract

MAY 20 contract

JUN 20 contract

Order Types and Trading Paramaters:

An electronic trading system allows the trading members t enter ordrs with various conditions attached to them as per their requirements. These conditions are broadly divided into the following categories:1) Time Conditions2) Price Conditions3) Others ConditionsSeveral combinations of the above are possible thereby providing enormous flexibility to users. The order types and conditions are summarized below. Of these, the order types available on the NCDEX system are regular lot order, stop loss order, immediate or cancel order, good till day order, good till cancelled order, good till date order and spread order.

1) Time Conditions:

- Good till day order: Aday order, as the name suggests is an order which is valid for the day on which it is entered. Ifr the order is not executed during the day, the system cancels the ordr automatically at the end of the day. Example: A trader wantsto go long on March 1, 2004 in refined palm oil on the commodity exchange. A day order is placed at Rs 340/ 10kg. If the market does not reach this price the order does not get filled even if thje market toucjhes Rs 341 and closes. In other words day order is for a specific price and if thje order does not get filled that day, one hase to place the order again the next day.

- Good till cancelled (GTC): A GTC order remains in the system until the user cancels it. Consequently, it spans terading days, if not traded on the day the order is entered. The maximum number of days an order can remain in the system is notified by the exchange from time to time after which the order is automatically cancelled by the system. Each day counted is a calendar day inclusive of holidays. The days counted are inclusive of the day on which the order is placed and the order is cancelled from the system at the end of the day of the expiry period.

-Good till date (GTD): A GTD allows the user to specify the date till which the order hould remain in the system if not executed. The maximum days allowed by the system are the same as in GTCorder. At the end of this day/ date, the order is cancelled from the system. Each day /date counted are inclusive of the day/date on which the order is placed and the order is cancelled from the system at the end of the day/date of the expiry period.

-Immediate or Cancel (IOC): An IOC order allows the user to buy or sell a contract as soon as the order is released into the system, failing which the order is cancelled from the system. Partial match is possible for the order, and the unmatched portion of the order is cancelled immediately.

- All or None Order:AON is as limit order, which is to be executed in its entirety, or not all. Unlike a fill or kill order, an all or none order is not cancelled if it is not executed as soon as it is represented in the exchange. An all ore none order position can be closed out with another AON order.

- Fill or Kill Order:FOK is a limit order that is placed to be executed immediately and if the order is unable to be filled immediately, it gets cancelled.

2) Price Condition

- Limit Order:An order to buy or sell a stated amount of a commodity at a specified price, or at a better price, if obtainanle at the time of execution. The disadvantage is that the order may not get filled at all if the price for that day does not reach the specified price.

- Stop-Loss:A stop-loss order is an order, placed with the broker, to buy or sell a particular futures contract at the market price if and whern the pice reaches a specified levelk. Futures traders often use sto-p orders in an effort to limit the amount they might lose if the futures price moves agaist their position. Stop orders are not executed until the price reaches the specifies moves agaist their position. Stop orders are not executed until the price reaches the specified point. When the price reaches that point the stop order bv becomes a market order. Most of the time, stop orders are used to exit trade. But, stop orders can be excuted for buying/selling positions too. A buy stop order is initiated when one wants to buy a contract r go long and a sell stop order when one wants to sell or go short. The order gets filled at the suggested stop order price or at a better price. Example: A trader has purchased crude oil futures at Rs 750 per barrel. He wishes to limit his loss to Rs.50 a barrel. Astop order would then be plac3d to sell an offsetting contract if the price falls to Rs 700 per barrel. When the market touchjes this price, stop order gets executed and the terader would exit the market. For the stop-lss sell order, the trigger price has to be reater than the limit price.

3) Other conditions:

-Market price:Market orders are orders for which no pride is specfified at the time the order is entered (i.e. price ius markert price). For such orders, the system determines the price. Only the position to be taken long/short is stated. When this kind of order is placed, it gets executed irrespective of the current market price of thjat particular asset.

- Market on open: The order will be executed on the market open within the oening range. This trade is used to enter a new trade, or exit an open trade.

- MNarket on close: The order will be executed on the market close. The fill price will be within the closing range, which may, in some markets, be sbutstantially different from the settlement price. This trade ios also used to enter a new trade, or exit an open trade.

- Trigger price: Price at which an order gets triggered fro the stop-loss book.

- Limnit price: Price of the orders after triggering from stop-loss book.

- Spread order: A simple spread order involves two positions, one long and one short. They are taken in the same commodity with different months (calendar spread) or in closely related commodities. Prices of the two futures contract therefore tenn to go up and down together, and gains on one side of the spread are offset by losses on the other. The spreaders

goal I sto profit from a change in the difference between the tow futures prices. The trader is virtually unconcerned whether the entire price structure mmoves up or down, juist so long as the futures contract he bought goes up more (or down less) than the futures contract he sold.

- One cnanels the other order: It is called one cancels the other order (0oco). An order placed so as to take advantage of price movement, which consists of both a stop and a limit price. Once one level is reached, one half of the order will be executed (either stop or limit) and the remaining order cancelled (either limit or stop). This typoe or foder would close the position if the market moved to either the stop rate or the limit rate, thereby closing the trade and at the same timem canceling them othner entry order. Example: A trader has a buy position at Rs 14000/ tonne on Soyabean. He wishes to have both stop and limit orders in order ato fill the order in a particular price range. A stop order is placed at Rs 14100/tonne and a limit order at Rs 13900/tonne. If the markdt trades at Rs 13900/tonne, the limnit order gets filled and the stop order is immeditately gets cancelled. The trader exits the market at Rs 13900/ tonne.

PERMITTED LOT SIZE:The permitted trading lot size for the futures contracts on individual commodities is stipulated by the exchange for time to time. The lot size currently applicable on individual commodity contracts is given below:Commodity futures: Lot Size and other parameters

INSTRUMENTTYPE ASSET

ASSET SYMBOL

MARKET LOT

QUANTITYUNIT

PRICEUNIT

DELIVERYLOT

DELIVERYUNIT

FUTCOM GLDPURMUM

100 GM Rs/10GM 1 KG

FUTCOM SLVPURDEL 5 Kg Rs/Kg 30 KGFUTCOM SYBEANIDR 1 MT Rs/

Quintal10 MT

FUTCOM SYOREFIDR 1 MT Rs/10 Kg 10 MTFUTCOM RMSEEDJPR 1 MT Rs/20 Kg 10 MTFUTCOM RMOEXPJPR 1 MT Rs/10 Kg 10 MTFUTCOM RBDPLNKA

K1 MT Rs/10 Kg 10 MT

FUTCOM CRDPOLKDL

1 MT Rs/10 Kg 10 MT

FUTCOM COTJ34BTD 11 BALES Rs/Quintal

55 BALES

FUTCOM COTS06ABD 11 BALES Rs/Quintal

55 BALES

TICK SIZE FOR CONTRACT:

The tick size is the smallest price change that can occur for the trades on the exchange. The tick size in respect of all futures contracts admitted to dealings on the NCDEX is 5 paise.

QUANTITY FREEZE:

All orders placed by members have to be within the quantity specified by the exchange is this regard. Any order exceeding this specified quantity will not be executed but will lie pending with the exchange as a quantity freeze. The following table gives the quantity freeze for each commodity contract. In respect of orders which have come under quantity freeze, the member is required to confirm to the exchange that there is no inadvertent error in the order entry and that the order is genuine. On such confirmation, the exchange can approve such order. However, in exceptional cases, the exchange may, at its discretion, not allow the orders that have come under quantity freeze for execution for any reason whatsoever including non-availability of exposure limits

INSTRUMENT TYPE ASSET

ASSETSYMBOL

QUANTITYFREEZE UNIT

FUTCOM GLDPURMUM 30000 Grams (gm)FUTCOM SLVPURDEL 1500 kilograms (Kgs)FUTCOM SYBEANIDR 300 Metric Tonnes (MT)FUTCOM SYOREFIDR 300 Metric Tonnes (MT)FUTCOM RMSEEDJPR 300 Metric Tonnes (MT)FUTCOM RMOEXPJPR 300 Metric Tonnes (MT)FUTCOM RBDPLNKAK 300 Metric Tonnes (MT)FUTCOM CRDPOLKDL 300 Metric Tonnes (MT)FUTCOM COTJ34BTD 3300 BalesFUTCOM COTS06ABD 3300 Bales

BASE PRICE:

On introduction of new contracts, the base price is the prvious day’s closing price of thje underlying commodity in the prevailing spot markets. These spot prices are polled across multiple centers and a single spot price is determined by the bootstrapping method. The base price of the contractrs on all subsequent trading days is the dai9ly settlement price of the futures contracts on the previous trading day.

PRICE RANGES OF CONTRACTS:

In order to prevent erroneous order entry by trading members, operating price ranges on the NCDEXZ are dept at =/- 10% from the base price. Orders exceeding the range specified are not executed and lie pending with the exchange as a price freeze. In respect of orders which have come under price freeze, the members are required to confirm to the exchange that there is no inadvertent error in the order entry and that the order is genuine. The exchange can approve or disapprove such orders solely at its own discretion. Unless specifically notified by the exchange, there will be no price ranges applicable I the last half hour of normal market trading.

ORDER ENTRY ON THE TRADING SYSTEM:

The NCDEX trading system has a set of function keys built into the trading front-end. These keys have been provided to facilitate faster operation of the system and enable quicker trading on the system. The function keys can be operated from the keyboard of the user. The set of function keys enable the following:

- Buy open- Sell open - Order cancellation- Order modification - Exercise/Position liquidation - Outstanding orders- Quick order cancel - Spread order entry- Trade modify- trade Cancel- Client master maintenance- Market by order- Market by price- Activity log- Security list/ portfolio steup- portfolio offline order entry - spread market by price- previous trades- contract description- alphabetical sorting of contracts- spread order status- spread activity log- Snap quote- online offline order entry- message log - market movement - full message display- market inquiry- spread outstanding orders- net position upload- order status- liquidity schedule- buy close - sell close

MARGINS FOR TRADING IN FUTURES:

Margin is the deposit money that needs to be paid to buy or sell each contract. The margin required for a futures contract is better described as performance bond or good faith money. The margin levels are set by the exchanges based on volatility (market conditions) and can be changed at any time. The margin requirements for most futures contracts range fr0om 2% to 15% of the value of the contract.In the futures market, there are different types of margins that a trader has to maintain/. We will discuss them in more details when we talk about risk management in the next chapter. At this stage we look at the types of margins as they apply on most futures exchanges.

- Initial margin- Maintenance margin- Additional margin- Mark-to-market margin

Just as a trader is required to maintain a margin account with a broker, a clearing house member is required to maintain a margin account with the clearing house. This is known as clearing margin. In the case of clearing house member, there is only an original margin and no maintenance margin. Clearing house and clearing house margins have been discussed further in detail under the chapter on clearing and settlement.

CHANGERS:Members are liable to pay transaction charges for the trade done through the exchange during rthe previous month. The important provisions are listed below: The billing for athe all trades done during the previous month will be raised in the succeeding month.

- Rate of Charges- Due date- collection process- Registration with BJPL and their services- Adjustment against advances transaction charges- penalty for delayed payments

Finally futures market is zero sum game i.e., the total number of long in any contract always equals the total number of short in any contract. The total number of outstanding contracts (long/short) at any point in time is called the Open interest”. This Open interest figure is a good indicator of the liquidity in every contract. Based on studies carried out in international exchanges, it is found that open interest is maximum in near month expiry contracts.

CLEARING AND SETTLEMENT

Most futures contracts do not lead to the actual physical delivery of the underlying asset. The settlement is done by closing out open positions, physical delivery or cash settlement. All these settlement functions are takes care of by and entity called clearing house or clearing corporation.

CLEARING:Clearing if the trades that take place on an exchange happens through the exchange clearing house. A clearing house is a system by which exchanges grantee the faithful compliance of all trade commitments undertaken on the trading floor or electronically over the electronic trading systems. The main task of the clearing house is to keep track to all the transactions that take place during a day so that the net positions of each of its members can be calculated. It guarantees the performance of the parties to each transaction. Typically it is responsible for the following;1) Effecting timely settlement.2) Trade registration and follow up. 3) Control of the evolution of open interest4) Financial clearing of the payment flow.5) Physical settlement (by delivery) or financial settlement (by price difference) of contracts. 6) Administration of financial guarantees demanded by the participants.

The clearing house has a number of members, who are mostly financial institutions responsible for the clearing and settlement of commodities traded on the exchange. The margin accounts for the clearing house members are adjusted of r gains and losses at the end of each day (in the same way as the individual traders keep margin accounts with the broker) The brokers who are not clearing members need to maintain a margin account with the clearing house member through who they trade in the clearing house.

CLEARING MECHANISM:

Only clearing members including professional clearing members (PCMs) are entitled t clear and settle contracts through the clearing house.The clearing mechanism essentially involves working out open positions and obligations of clearing members. This position is considered for exposure and daily margin purposes. Open positions of PCMs are arrived at by aggregating the open positions of all the TCMs clearing through him, in which they have traded. A TCMs open position is arrived at by the summation of this clients’ open positions, in the contracts in which they have traded. Client positions are netted at the level of individual client and grossed across all clients, at the member level without any set-offs between clients. Proprietary positions are netted at member level without any set=-offs between client and proprietary positions.

CLEARING BANKS:

Every clearing member is required to maintain and operate a clearing account with any one of the designated clearing bank branches. The clearing account is to be user exclusively for clearing operations ie., for settling funds and together obligations to “Exchange” including payments of margins and penal charges. A clearing member can deposit funds into this account, but can withdraw funds from this account only is his self-name. A clearing member having funds

obligation to pay is required to have clear balance is his clearing account on or before the stipulated pay-in day and the stipulated time. Clearing members must authorize their clearing bank to access their clearing account for debiting and crediting their accounts as per the instructions of “exchange”, reporting of balances and other operations as may be required by “exchange” for time to time. The following banks have been designated as clearing banks- ICICI Bank Limited, Canara Bank, UTI Bank Limited and HDFC Bank Limited.

DEPOSITORY PARTICIPANTS:

Every clearing member is reuired to maintain and operate a CM pool account with any of the empanelled depository participants. The CM pool account is to be used exclusively for clearing operations i.e., for effecting and receiving deliveries from “exchange”.

SETTLEMENT:

Futures contracts have two types of settlements, the MTM settleiment which happens on a continuous basis at the end of each day, and the final settlement which happens on the last trading day of the futures contract. On the “exchange” daily MTM settlement fand final MTM settlement in respect of admitted deals in futurex contracts are cash settle dby debiting/creditring athe clearing accounts of CCMs, with the respectigve clearing bank. All positions of a CM, either brought forward, created during the day or closed out during the day are market to market at the daily settlement price or the final settlement price a the close of trading hours on a day.

- Daily mark to market settlement Daily mark to market settlement is done till the date of the contract expiry. This is done to take care of daily \price fluctuations of all traders. All the open positions of the members are marked to market at the end of the day and the profit/loss is determined as below:

1) On the day of entering into the contract, it is the difference between the entry vale and daily settlement price for that day.2) On any intervening days. When the member holds an open position, it is the difference between the daily settlement price for that day and the previous day’s settlement price.

3) On the expiry date if the member has an open position, it is the difference between the final settlement price and the previous day’s settlement price.

- Final Settlement:On the date of expiry, the final settlement price is the spot price on the expiry day. The spot prices are collected from members across the country through polling. The polled bid/ ask prices are bootstrapped and the mid of the two bootstrapped prices is taken as the final settlement price. The responsibility of settlement is on a trading cum blearing member for all trades doing on his own account and his client’s trades. A professional clearing member is responsible for settling all the participants’ trades which he has confirmed to the exchange.

Non fulfillment of either the whole or part of the settlement obligations is treated as a violation of the rules, bye laws and regulations of “exchange” and attracts penal charges as stipulated by “exchange” from time to time.

REGULATORY FRAMEWORK:

At present, there are three tiers of regulations of forward/futures trading system in India, namely, government of India, Forward Markets Commission (FMC) and commodity exchanges. The need for regulation arises on account of the fact that the benefits of futures markets accrue in competitive conditions. Proper regulation is needed to create competitive conditions.

RULES:

It prescribes the following regulatory measures:1) Limit on net open position a son the close of the trading hours. Some times limit is also impoised on intra-day net open position. The limit is imposed operator-wise, and in some cases, also member wise.2) Circuit filter or limit on price fluctuations to allow cooling of market in the event of abrupt upswing or downswing in prices. 3) Special margin deposit to be collected on outstanding purchases or sales when price moves up or down sharply above or below the previous day closing price. By making further purchases/sales relatively costly, the price rise of fall is sobered down. This measure is imposed only or the request of the exchange.4) Circuit breakers or minimum/maximum prices: These are prescribed to prevent futures prices from falling below ass rising above not warranted by respective supply and demand factors. This measure is also imposed on the request of the exchanges.5) Skipping trading in cer5tain derivatives of the contract, closing the market for a specified period and even closing out the contract: These extreme measures are taken only in emergency situations.

RULES GOVERNING INVESTOR GRIEVANCES, ARBITRATION:

In matters where the exchange is a partly to the dispute, the civil courts at Mumbai have exclusive jurisdiction and in all other matters, proper courts within the area covered under the respective regional arbitration center have jurisdiction in respect of the arbitration proceeding s falling/conducted in that regional arbitration center.If the value of claim, difference or dispute is more than Rs. 25Larks on the date of application, the such claim, difference or dispute is up to Rs.25 Lakh, the they are to be referred to a sole arbitrator. Where any claim, difference or dispute arises between agent of the member and client of the agent of the member, in such claim, difference or dispute, the member, to who such agent of the member is affiliated, is impeded as a party. In case the warehouse refuses or fails to communicate to the constituent the transfer of commodities, the date dispute is deemed to have arisen oTHE COMMODITY EXCHANGE PLATFORM:THE NCDEX PLATFORM:

National Commodity and Derivatives Exchange Ltd (NCDEX) is a technology driven commodity exchange. It is public limited company registered under the Companies Act, 1956 with the Registrar of Companies, Maharashtra in Mumbai on April 23, 2003. NCDEX is regulated by Forward Markets Commission is respect of futures trading in commodities. NCDEX currently facilitates trading of 10 commodities.

PROMOTERS:NCDEXis promoted by a consortium of institutions. These include the ICICI Bank Limited (ICICI Bank). LIC, NABARD, and NSE

GOVERNANCE:NCDEX is run by an independent Board of Directors. Promoters do not participate in the day today activities of the exchange. The Directors are appointed in accordance with the provisions of the Articles of Association of the company.

The NCDEX System: How transaction happen on the NCDEX’s market:

TRADING:The Trading system on the NCDEX provides a fully automated Screen-based trading for futures open commodities on a nationwide basis as well as an online monitoring and surveillance mechanism. It supports an order driven market and provides complete transparency of trading operations.

The NCDEX system supports am order driven market, where orders match automatically. Order matching is essentially on the bases of commodity, its price, time and quantity. All quantity fields are in units and price in rupees. The exchange specifies the unit of trading and the delivery unit for futures contracts on various commodities. The exchange notifies the regular lot size and tick size for each of the contracts traded from time to time. When any order enters the trading system, it is an active order. It tries to find a match on the other side of the tool. It finds a match, a trade is generated. If it does not find a match, the order becomes passive and gets queued in the respective outstanding order book in the system.

CLEARING:National Securities Clearing Corporation Limited (NSCCL) undertakes clearing of trades executed on the NNCDWEX. The settlement guarantee fund is maintained and managed by NCCDEX. Only clearing members including professional clearing members (PCMs) only are entitled to clear an dsettle contracts through the clearing house. At NCDEX after the trading hours on the expiry date, based on the available information, the matching for deliveries takes place firstly on the basis of locations and then randomly, keeping in view the factors such as available capacity of the value/ warehouse, commodities already deposited and dematerialized and offered for delivery etc. Matching done by this process is binding on the clearing members. After completion matching process, clearing members are informed of the deliverable/receivable posi9tions and the unmatched positions. Unmatched positions have to be settled in cash. The

cash settlement is only for the incremental gain/loss as determined on the basis of final settlement price.

SETTLEMENT:Futures contracts have two types of settlements, the MTM settlement which happens on a continuous basis at the end of each day, and the final settlement which happens on the last trading day of the futures contract. On the NCDEX, daily MTM settlement and final MTM settlement is respect of admitted deals in futures contracts are cash settle by debiting/ crediting the clearing accounts of CMs with the respective clearing bank. All p9ositions of a CM, either brought forward, created during the day or closed out during the day, are market to market at the daily settlement price or the final settlement price at the close of trading hours on a day.On the date of expiry the final settlement price is the spot price on the expiry day. The responsibility of settlement is on a trading cum clearing member for all trades done on his own account and his client’s trades. A professional clearing member is responsible for settling all the participants trades which he has confirmed to the exchange. On the expiry date of a futures contract, members submit delivery information through delivery request window on the trader workstations provided by NCDEX for all open positions for a commodity for all constituents individually. NCDEX on receipt of such information matches the information and arrives at a delivery position for a member for a commodity.The seller intending to make delivery takes the commodities to the designated warehouse. These commodities have to be assayed by the exchange specified assayer. The commodities have to meet the contract specifications with allowed variances. If the commodities meet the specifications, the warehouse accepts them. Warehouse then ensures that the receipts get updated in the depository system giving a credit in the depositor’s electronic account. The seller the gives the invoice to his clearing member, who would courier the same to the buyer’s clearing member. On an appointed date, the buyer goes to the warehouse and takes physical possession of the commodities.

COMMODITY ANALYSIS:

1) GOLD:

1. Introduction

Gold is a unique asset based on few basic characteristics. First, it is primarily a monetary asset,and partly a commodity. As much as two thirds of gold’s total accumulated holdings relate to“store of value” considerations. Holdings in this category include the central bank reserves,private investments, and high-caratage jewelry bought primarily in developing countries as avehicle for savings. Thus, gold is primarily a monetary asset. Less than one third of gold’s totalaccumulated holdings can be considered a commodity, the jewelry bought in Western markets foradornment, and gold used in industry.

The distinction between gold and commodities is important. Gold has maintained its value inafter-inflation terms over the long run, while commodities have declined.

Some analysts like to think of gold as a “currency without a country’. It is an internationallyrecognized asset that is not dependent upon any government’s promise to pay. This is animportant feature when comparing gold to conventional diversifiers like T-bills or bonds, whichunlike gold, do have counter-party risk.

2. What makes Gold Special?

Timeless and Very Timely Investment: For thousands of years, gold has been prized for itsrarity, its beauty, and above all, for its unique characteristics as a store of value. Nations mayrise and fall, currencies come and go, but gold endures. In today’s uncertain climate, manyinvestors turn to gold because it is an important and secure asset that can be tapped at anytime, under virtually any circumstances. But there is another side to gold that is equallyimportant, and that is its day-to-day performance as a stabilizing influence for investmentportfolios. These advantages are currently attracting considerable attention from financialprofessionals and sophisticated investors worldwide.

Gold is an effective diversifier: Diversification helps protect your portfolio againstfluctuations in the value of any one-asset class. Gold is an ideal diversifier, because theeconomic forces that determine the price of gold are different from, and in many casesopposed to, the forces that influence most financial assets.

Gold is the ideal gift: In many cultures, gold serves as a family treasure or a wealth transfervehicle that is passed on from generation to generation. Gold bullion coins make excellentgifts for birthdays, graduations, weddings, holidays and other occasions. They areappreciated as much for their intrinsic value as for their mystical appeal and beauty. Andbecause gold is available in a wide range of sizes and denominations, you don’t need to bewealthy to give the gift of gold.

Gold is highly liquid: Gold can be readily bought or sold 24 hours a day, in largedenominations and at narrow spreads. This cannot be said of most other investments,including stocks of the world’s largest corporations. Gold is also more liquid than manyalternative assets such as venture capital, real estate, and timberland. Gold proved to be themost effective means of raising cash during the 1987 stock market crash, and again duringthe 1997/98 Asian debt crisis. So holding a portion of your portfolio in gold can be invaluablein moments when cash is essential, whether for margin calls or other needs.

Gold responds when you need it most: Recent independent studies have revealed thattraditional diversifiers often fall during times of market stress or instability. On theseoccasions, most asset classes (including traditional diversifiers such as bonds and alternativeassets) all move together in the same direction. There is no “cushioning” effect of adiversified portfolio — leaving investors disappointed. However, a small allocation of gold hasbeen proven to significantly improve the consistency of portfolio performance, during bothstable and unstable financial periods. Greater consistency of performance leads to adesirable outcome — an investor whose expectations are met.

3. What makes Gold different from other commodities?

The flow demand of commodities is driven primarily by exogenous variables that are subject tothe business cycle, such as GDP or absorption. Consequently, one would expect that a suddenunanticipated increase in the demand for a given commodity that is not met by an immediateincrease in supply should, all else being equal, drive the price of the commodity upwards.However, it is our contention that, in the case of gold, buffer stocks can be supplied with perfect

elasticity. If this argument holds true, no such upward price pressure will be observed in the goldmarket in the presence of a positive demand shock.

The existence of a sophisticated liquid market in gold has, over the past 15 years, provided amechanism for gold held by central banks and other major institutions to come back to themarket. Although the demand for gold as an industrial input or as a final product (jewellery) differsacross regions, it is argued that the core driver of the real price of gold is stock equilibrium ratherthan flow equilibrium. This is not to say that exogenous shifts in flow demand will have noinfluence at all on the price of gold, but rather that the large supply of inventory is likely todampen any resultant spikes in price. The extent of this dampening effect depends on thegestation lag within which liquid inventories can be converted in industrial inputs. In the goldindustry such time lags are typically very short.

Gold has three crucial attributes that, combined, set it apart from other commodities: firstly,assayed gold is homogeneous; secondly, gold is indestructible and fungible; and thirdly, theinventory of aboveground stocks is astronomically large relative to changes in flow demand. Oneconsequence of these attributes is a dramatic reduction in gestation lags, given low search costsand the well-developed leasing market. One would expect that the time required to convert bullioninto producer inventory is short, relative to other commodities which may be less liquid and lesshomogenous than gold and may require longer time scales to extract and be converted intousable producer inventory, making them more vulnerable to cyclical price volatility. Of course,because of the variability of demand, the price responsiveness of each commodity will depend inpart on precautionary inventory holdings.

There is low to negative correlation between returns on gold and those on stock markets,whereas it is well known that stock and bond market returns are highly correlated with GDP. Thisis because, generally speaking, GDP is a leading indicator of productivity: during a boom,dividends can be expected to rise. On the other hand, the increased demand for credit, countercyclical monetary policy and higher expected inflation that characterize booms typically depress bond prices.

The fundamental differences between gold and other financial assets and commodities give riseto the following “hard line” hypothesis: the impact of cyclical demand using as proxies GDP,inflation, nominal and real interest rates, and the term structure of interest rates on returns ongold, is negligible, in contrast to the impact of cyclical demand on other commodities and financialassets.

Using the gold price and US macroeconomic and financial market quarterly data from January1975 to December 2001, the following conclusions may be drawn:

There is no statistically significant correlation between returns on gold and changes inmacroeconomic variables, such as GDP, inflation and interest rates; whereas returns on

other financial assets, such as the Dow Jones Industrial Average, Standard & Poor’s 500index and 10-year government bonds, are highly correlated with changes inmacroeconomic variables.

Macroeconomic variables have a much stronger impact on other commodities (such asaluminum, oil and zinc) than they do on gold.

Returns on gold are less correlated with equity and bond indices than are returns onother commodities.

Assets that are not correlated with mainstream financial assets are valuable when it comes tomanaging portfolio risk. This research establishes a theoretical underpinning for the absence of arelationship that has been demonstrated empirically for a number of years; namely, that betweenreturns on gold and those on other financial assets.

4. International Scenario:

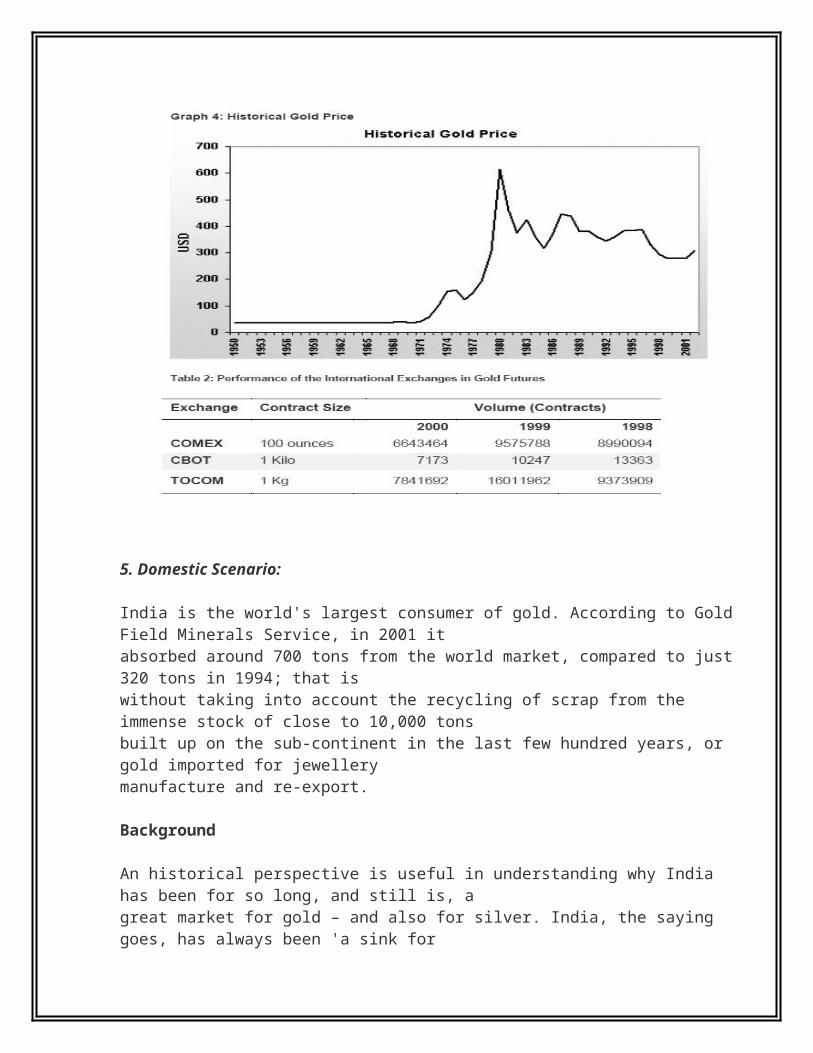

World SupplyAccording to Gold Field Mineral Services, world gold output in 2001 was 2,604 tons, moderatelyhigher than 2,584 ton in 2000. By comparison, it was only 1,311 tons, including estimatedcommunist output, in 1980. Effectively it has doubled. Western world output, excluding the oldcommunist block, increased even faster, from 959 tons in 1980 to 2,112 tons in 2001. Totalproduction throughout history topped 142,500 metric tons by the end of 2001.

Graph 1:

Graph 2:

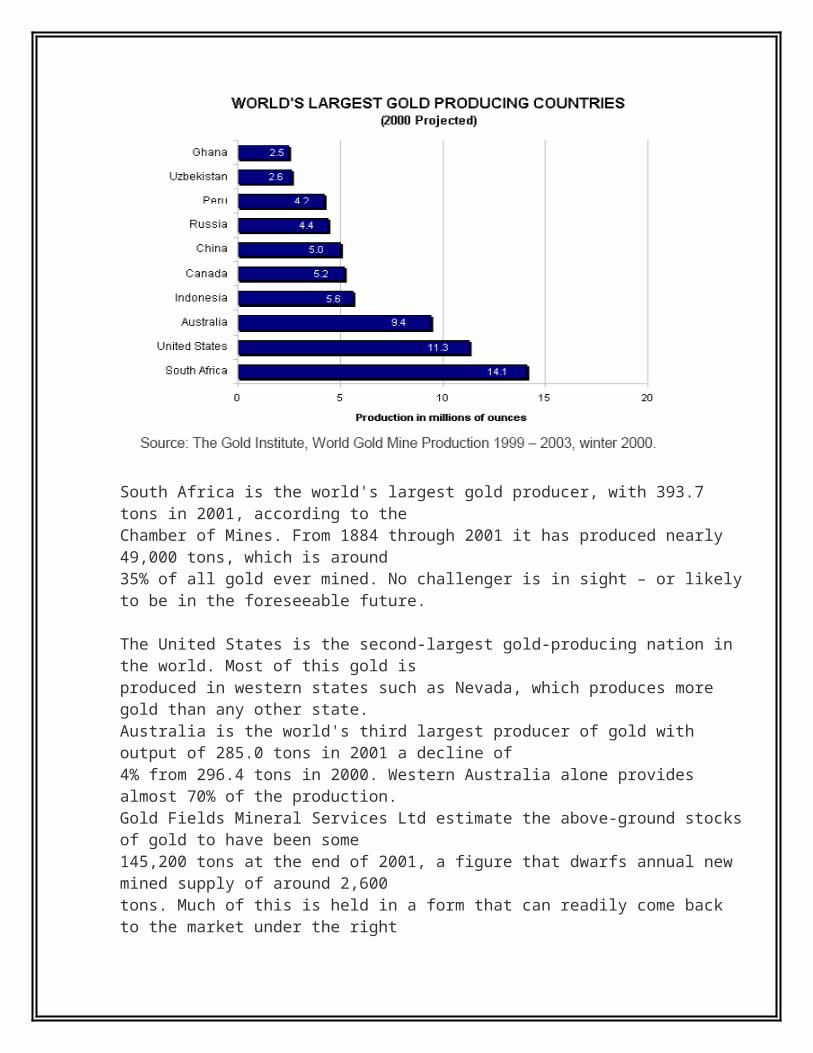

South Africa is the world's largest gold producer, with 393.7 tons in 2001, according to the

Chamber of Mines. From 1884 through 2001 it has produced nearly 49,000 tons, which is around35% of all gold ever mined. No challenger is in sight – or likely to be in the foreseeable future.

The United States is the second-largest gold-producing nation in the world. Most of this gold isproduced in western states such as Nevada, which produces more gold than any other state.Australia is the world's third largest producer of gold with output of 285.0 tons in 2001 a decline of4% from 296.4 tons in 2000. Western Australia alone provides almost 70% of the production.Gold Fields Mineral Services Ltd estimate the above-ground stocks of gold to have been some145,200 tons at the end of 2001, a figure that dwarfs annual new mined supply of around 2,600tons. Much of this is held in a form that can readily come back to the market under the rightconditions. This is obviously true for investment forms of gold but it is also true for much jewelleryin Asia and the Middle East. In these regions jewellery traditionally fulfills a dual role, both as ameans of adornment and as a means of savings. Notably, it is particularly important for women inMuslim and Hindu cultures where traditionally a woman’s jewellery was often in practice her onlyfinancial asset. Such jewellery is of high caratage (21 or 22 carats), and is traded by weight andsold at the current gold price plus a moderate mark-up to allow for dealing and making costs. It isalso fairly common for jewellery to be bought or part-bought by the trading in of another piece ofequivalent weight; the traded-in piece will either be resold by the jeweller or melted down tocreate a new piece.

In Asia and the Middle East both gold investments and gold jewellery are considered as financialor semi-financial assets. It is not known how much of the total stocks of gold lie in these regionsbut in recent years they have accounted for approximately 60% of total demand; while the long held cultural affinity to gold would suggest that the majority of stocks in private hands lie in thisarea. Consumers are very aware of price movements and very sensitive to them. Gold will besold in times of financial need but holders will frequently take profits and sell gold back to themarket if the price rises. Thus the supply of scrap gold will normally automatically rise if the goldprice rises. Even gold used for industrial purposes such as electrical contacts in electronicequipment is frequently recovered as scrap and a rise in the gold price will increase the incentivefor such recovery.

World Gold Fabrication and ConsumptionFabrication statistics measure the amount of gold used in various countries to manufacture endproducts. Consumption figures measure where these gold products were consumed.

World Markets

Today's gold market is a round-the-world, round-the-clock business, played out largely ondealers' trading screens. The core of the business, however, remains in the key markets ofLondon, as the great clearing house, New York as the home of futures trading, Zurich as aphysical turntable, Istanbul, Dubai, Singapore and Hong Kong as doorways to importantconsuming regions and Tokyo where the Commodity Exchange (TOCOM) sets the mood ofJapan. Even Paris still has a small market, a reminder of the days when the French were greathoarders, while Mumbai has increasing importance under India's liberalised gold regime thatpermits official imports through local markets.

5. Domestic Scenario:

India is the world's largest consumer of gold. According to Gold Field Minerals Service, in 2001 itabsorbed around 700 tons from the world market, compared to just 320 tons in 1994; that iswithout taking into account the recycling of scrap from the immense stock of close to 10,000 tonsbuilt up on the sub-continent in the last few hundred years, or gold imported for jewellerymanufacture and re-export.

Background

An historical perspective is useful in understanding why India has been for so long, and still is, agreat market for gold – and also for silver. India, the saying goes, has always been 'a sink forprecious metals'. Both metals are closely woven into the social fabric, especially in the rural areaswhere they are the basic form of saving. Ever since Roman times the 'east' has been a source of silk and spices, and later diamonds, tea and cotton, sought by Mediterranean and European merchants. The first gold ducats struck by the mint in Venice in 1285, which became a staple form of international payment for over three hundred years, went to the Levant and on to India. The gold and silver from the Americas, after Columbus discoveries, mostly just passed through Spain on its way to the east. In the 17th century the Dutch and English East India companies sent

gold and silver to India and Java to pay for goods. The English East India Company shipped 20 tons, almost three years' world output then, to India between 1660 and 1690. Mocatta, the oldest member of the London gold market, first sent gold to India in 1676 to pay for diamonds, the beginning of a long relationship between London and Bombay (now Mumbai) merchants. During the American Civil War in the 1860s India imported almost 420 tons in payment for cotton exports because of disrupted American cotton crops.

Only once has India been a significant dishoarder, when 1,244 tons was shipped out in the 1930sdue to distress selling from famine and the new high price for gold (up from $20.67 to $35).In recent times India has remained faithful to gold. While demand has increased substantiallysince the early 1980s due to general economic growth, annual consumption is dictated both bythe monsoon, with its effect on the harvest, and the marriage season. In an auspicious year thereare upwards of ten million marriages, at which between 20 and 200 grams may be worn by thebride. The status of a family in its community is still often judged by the gold exchanged as thebride's dowry.

The official import of gold into India, however, was banned from 1947. The Gold Control Act of1962 also forbade private holding of gold bars. With local production of less than two tons fromtwo small mines, Bharat and Hutti, together with recycling, the main demand was met bysmuggling from the regional markets of Dubai, Singapore, and Hong Kong, usually as ten tolabars, uniquely preferred in India. The smuggling was a highly professional business, involving upto 200 tons, encouraged by a premium of 30 per cent over the London price. Over 3,000 tons hasentered India unofficially since 1947.

Until 1990, the Gold Control Act forbade the private holding of gold bars in India. There wasphysical investment in smuggled ten tola bars, but it was limited and often amounted to keeping afew bars ready to be made into jewellery for a family wedding. Gold investment essentially was in22 carat jewellery.

In the 1990s, however, deregulation of the market has finally taken place, ushering in the modernmarket of today. Since 1990, investment in small bars, both imported ten tolas and locally-madesmall bars, which have proliferated from local refineries, has increased substantially. GFMSestimate that investment has exceeded 100 tons in some years, although it is hard to segregatetrue investment from stocks held by the 16,000 or more gold dealers spread across India.Certainly gold has been used to conceal wealth, especially during the mid-1990s, when the localrupee price increased steadily. It was also augmented in 1998 when over 40 tons of gold frombonds originally issued by the Reserve Bank of India were restituted to the public.

Graph 5:

India and Global Gold Economy

Estimates vary, but it is believed that at least 13,000 tons of gold rest in India – or approximatelynine per cent of the world’s cumulative mine production. This should be viewed against our sharein land area at 2.4 per cent, in population at 16.4 per cent and in GDP at 1.2 per cent.Mining and production of gold in India is negligible, now placed around 2 tons as against a totalworld production of about 2,272 tons in 1995.

During 1990-95, India’s share in global gold demand is placed at about 402 tons (16.4 per cent) ayear, including imports into India. This should be viewed against its share of 0.6 per cent in worldtrade. On the other hand, India exported about 23 tons in 1995 accounting for a negligible part ofworld trade.

The world gold trading is concentrated in the U.K., Switzerland, Dubai, Hong Kong, etc. and Indiadoes not figure among them.

Facilities for refining, assaying, making them into standard bars in India, as compared to the restof the world, are insignificant, both qualitatively and quantitatively.Of the total gold reserves estimated to be on the books of the Central Banks (subject to someBanks not declaring them) of 28,225.4 tons, the holdings of Reserve Bank of India are only amodest 397.5 tons. Government of India has in its possession some amount of gold mainly out ofconfiscation of smuggled gold remaining after transferring it to the Reserve Bank of India fromtime to time. RBI is neither a speaking purchaser nor a seller of gold reserves, unlike many other

countries including some developing economies, especially in Asia. A part of gold was used byRBI (in parallel with gold with Government) for raising foreign currency resources during thebalance of payments crisis in the early 'nineties. These overseas gold holdings are being used aspart of reserve management to yield a return.

Use of gold as a financial product is virtually non-existent in India except to a limited extent ofissuing ‘Gold Bonds’ by Government of India from time to time coupled with occasional taxamnesty. Commercial banks, however, accept gold as security, but no advances are permitted forpurchase of gold by their customers for non-productive use.

Gold as Investment Vehicle

Gold is valued in India as a savings and investment vehicle and is the second preferredinvestment behind bank deposits. India is the world’s largest consumer of gold in jewellery (muchof which is purchased as investment).The hoarding tendency is well ingrained in Indian society, not least because inheritance laws inthe middle of the twentieth century lent a great desirability to anonymity. Indian people arerenowned for saving for the future and the financial savings ratio is strong, with a ratio of financialassets-to-GDP of 93%.

Gold’s circulates within the system and roughly 30% of gold jewellery fabrication is from recycledpieces. India is typically also the largest purchaser of coins and bars for investment (>80tpa),although last year it had to concede first place to Japan in the wake of the heavy buying in thefirst quarter due to fears for the stability of the Japanese banking system.In 1998-2001 inclusive, annual Indian demand for gold in jewellery exceeded 600 tons; in 2002,however, due to rising and volatile prices and a poor monsoon season, this dropped back to 490tons, and coin and bar demand dropped to 67 tons. Indian jewellery offtake is sensitive to priceincreases and even more so to volatility, although this decline in tonnage since 1998 is also duein part to increasing competition from white and brown goods and alternative investment vehicles,but is also a reflection of the increase in price. The Indian bride’s “Streedhan”, the wealth shetakes with her when she marries and which remains hers, is still gold, however (thus giving goldan important role in the “empowerment” of women in India).

Local expenditure, in terms of the value of the gold content purchased, peaked at Rs 302 billion(Rs 311 per capita) in 1998, when total Indian demand was almost 775 tons, and since then hasdropped to Rs 279 Bn in 2002 (Rs 284 per capita), a decline of almost 9%. This peak in 1998came in the wake of the main liberalisation step, which was the freeing of imports in November1997.

Typically, India accounts for 20% of global gold offtake in any one year. Its GDP (as measured bythe World Bank) in 2001 was 1.5% of the world’s total, ranking twelfth – although if this is

measured on Purchasing Power Parity, then India ranks fourth with 6.4% of the world total. Whilechanges in total demand per capita, in terms both of tonnage and expenditure show how Indianjewellery demand in 2002 compared with the rest of the world in terms of offtake per capita andagainst GDP. Offtake per capita is still very low, reflecting the widespread distribution of the ruralpopulation and the social infrastructure of the country (the rural population accounts forapproximately 70% of national gold demand), but offtake in terms of GDP is high. At just over onegramme of demand per thousand dollars of GDP, India stands third in the world, behind only theUAE (just over two grammes) and Bahrain (almost 1.5g) – although these two are both enhancedby tourist purchases.

It was not always thus. As recently as 1991, Indian gold demand was a little over 230 tons, oronly 8% of world offtake. The deregulation of the market during the 1990s brought about adramatic change. Jewellery demand increased from 208 tons in 1991 to peak at 658 tons in 1998,while demand for investment bars grew from ten tons in 1991 to 116 tons in 1998, and registered85 tons in 2002. These figures reflect average growth rates of 16% and 30% per annumrespectively between 1991 and 1998. While both have eased since 1998, there is still afascination in India for gold and there is significant scope for the development of further demandin the country. In the cities, however, gold is having to compete with the stock market, investment in internet industries, and a wide range of consumer goods. In the rural areas 22 carat jewellery remains the basic investment.

The World Gold Council, which was involved in the deregulation of the market in the 1990s,continues to work closely with Indian gold market stakeholders to foster increased demand, partlythrough the development of new gold instruments that can be bought through banks, as anadditional set of distribution channels, although the rural community does still tend to prefer touse jewelers.

Jewellery

India is the world's foremost gold jewellery fabricator and consumer with fabricator andconsumption annually of over 600 tons according to GFMS. Measures of consumption andfabrication are made more difficult because Indian jewellery often involves the re-making bygoldsmiths of old family ornaments into lighter or fashionable designs and the amount of goldthus recycled is impossible to gauge. Estimates for this recycled jewellery vary between 80 tonsand 300 tons a year. GFMS estimates are that official gold bullion imports in 2001 were 654 tons.

Graph 6:

Exports have increased dramatically since 1996, and in 2001 stood at over 60 tons. The USaccounted for about one third of total official exports. Manufacturers located in Special ExportZones can import gold tax-free through various registered banks under an Export Replenishmentscheme.

Recent Developments in India

World Gold Council (WGC) has estimated that the annual Indian demand for the precious metalin recent years has been in excess of 800 tons. Most of it appears to be meant for jewelleryfabrication, and the rest, estimated at 10 to 15 percent, is possibly meant to meet demand onaccount of investment and industrial processes. A major step in the development of gold marketsin India was the authorization in July 1997 by the RBI to commercial banks to import gold for saleor loan to jewellers and exporters. Initially, 7 banks were selected for this purpose on the basis ofcertain specified criteria like minimum capital adequacy, profitability, risk management expertise,previous experience in this area, etc. The number of banks later went upto 18. On a review,since five banks had not evinced adequate interest in this business in terms of activity, the RBIdid not find it appropriate to renew their licences for this purpose. At present, 13 banks are activein the import of gold. The quantum of gold imported through these banks has been in the rangeof 500 tons per year.

Import of gold by banks authorised by the RBI has succeeded to a large extent in curbing illegaloperations in gold and in foreign exchange markets. It has also resulted in reducing the disparitybetween international and domestic prices of gold from 57 per cent during 1986 to 1991 to 8.5 percent in 2001.

The import duty on gold, which was Rs.220 per ten grams upto January 1999, was increased toRs.400 per ten grams, and with effect from April 2001 has been reduced to Rs.250 per tengrams. The estimates of duty realised from gold imports indicate an annual amount varying fromabout Rs. 1,000 to Rs. 2,000 crore per annum since 1997.

Even though the country consumes more than 800 tons of the metal every year, the system ofassaying and hallmarking has not gained the desired importance. The low quality of goldjewellery being sold in the country and the resultant losses being incurred by the consumers arebeing recognized now. Recent surveys conducted by the Bureau of Indian Standards (BIS) jointlywith Central Consumer Protection Council in 5 major cities reveal that more than 80 per cent ofthe jewellery being sold in the market was of lower purity than claimed and charged for. In somecases, the gold articles sold were 38.6 per cent short in purity in monetary terms. The low purityresults in a loss of around 16 per cent to gold jewellery.

In the recent past, RBI has been actively pursuing the issue of upgrading the quality of trade andproducts through a system of assaying and hallmarking with Government of India and BIS. Themajor objectives of introducing a proper assaying and hallmarking system in the country areenabling consumer protection, developing export competitiveness of the gold jewellery industry,introducing gold based financial products, which will help in mopping up the vast dormant goldresources with the domestic sector and developing India into a leading gold market centre in theworld.

The Government of India announced the Gold Deposit Scheme in 1999 and RBI issuedguidelines to the banks intending to launch the scheme in October 1999. Five banks havelaunched their schemes under the guidelines and the quantum of gold mobilised so far has beenabout 7 tonnes. Unfortunately, the scheme has not evoked the expected response. A number ofreasons can be cited for the low response, prominent among them being depositors’ losing themaking charges spent on jewellery (as the banks would convert them into primary form beforeaccepting as deposits), the low caratage of jewellery, low rate of return on deposit (as seen by thedepositors) and the absence of any amnesty.

6. Role Played by International Authorities:

The authorities of different countries, have on the other hand, played significant roles in furtheringthe development of gold markets. Here one could see three patterns:Producer nations like South Africa, Australia and Brazil have shown keen interest in thedevelopment of spot and forward market in their respective countries mainly with the intention ofproviding financial products to the producers. Also, since a liquid forward market in gold (forenabling the producers to sell their product forward) presupposes the existence of a leasingmarket, these authorities have promoted this market also.Financial centers like the U.K., the USA, Switzerland, Hong Kong and Singapore have activelypromoted gold related products to be traded at these Centers. While in the UK and the USA, themarket is designed to be used by residents and non-residents alike the focus in Singapore is onproviding service to off-shore entities in Singapore and non-residents. There are direct benefits tothe countries concerned in the form of value-addition in the products, employment etc.