assessment for ballarat west growth area

TRANSCRIPT

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

1

PREPARED FOR THE LOCAL GOVERNMENT ASSOCIATION OF SOUTH AUSTRALIA

Economic Assessment for Ballarat West Growth Area Prepared for the City of Ballarat MacroPlan Australia Pty Ltd November 2010

FINAL REPORT

MACROPLAN AUSTRALIA PTY LTDSYDNEY | MELBOURNE | BRISBANE | PERTH

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

2

Signed*

………………………………… DATE: November 2010 [email protected]

www.macroplan.com.au

CONTACT

MacroPlan Australia Pty Ltd Level 4, 356 Collins Street, Melbourne, Vic. 3000 t 03 9600 0500 f 03 9600 1477

© MacroPlan Australia Pty Ltd All Rights Reserved. No part of this document may be reproduced, transmitted, stored in a retrieval system, or translated into any language in any form by any means without the written permission of MacroPlan Australia Pty Ltd. All Rights Reserved. All methods, processes, commercial proposals and other contents described in this document are the confidential intellectual property of MacroPlan Australia Pty Ltd and may not be used or disclosed to any party without the written permission of MacroPlan Australia Pty Ltd

MACROPLAN AUSTRALIA PTY LTD SYDNEY | MELBOURNE | BRISBANE | PERTH

Project Director

Richard Brice General Manager Economics and Research

Project Contact

Jennifer Wong Senior Consultant Activity Centres & Policy

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

3

1 EXECUTIVE SUMMARY ............................................................................................. 4

2 INTRODUCTION ..................................................................................................... 15

2.1 PROJECT OBJECTIVES .......................................................................................................... 15 2.2 THE STUDY AREA ............................................................................................................... 16 2.3 METHODOLOGY ................................................................................................................ 18 2.4 REPORT STRUCTURE ........................................................................................................... 19

3 RETAIL AND COMMERCIAL CENTRE HIERARCHY ..................................................... 20

3.1 DEFINITIONS ..................................................................................................................... 20 3.2 CURRENT AND FUTURE FLOORSPACE SUPPLY ........................................................................... 21

4 RETAIL FLOORSPACE DEMAND ............................................................................... 28

4.1 METHODOLOGY ................................................................................................................ 28 4.2 POPULATION TRENDS AND PROJECTIONS: CITY OF BALLARAT ...................................................... 29 4.3 POPULATION AND DWELLING CAPACITY IN BALLARAT WEST ....................................................... 30 4.4 ACTIVITY CENTRE REQUIREMENTS ......................................................................................... 30 4.5 RETAIL FLOORSPACE DEMAND BY PRECINCT ............................................................................ 31 4.6 SEBASTOPOL REVIEW ......................................................................................................... 33 4.7 RETAIL ALLOCATION TO THE BALLARAT WEST GROWTH AREA .................................................... 35

5 NON‐RETAIL FLOORSPACE DEMAND ...................................................................... 36

5.1 KEY ASSUMPTIONS ............................................................................................................ 36 5.2 IMPLICATIONS ................................................................................................................... 39

6 DELIVERY SCENARIOS............................................................................................. 40

6.1 SCENARIO 1: BALLARAT WEST GROWTH AREA PLAN (BASE CASE) .............................................. 41 6.2 SCENARIO 2: BWGA ELEVATED ROLE .................................................................................... 42 6.3 DELIVERY SCENARIOS: ECONOMIC IMPACTS ............................................................................. 44

7 IMPLEMENTATION AND RECOMMENDATIONS ....................................................... 45

7.1 ECONOMIC PRINCIPLES ....................................................................................................... 45 7.2 RECOMMENDATIONS FOR OPTIMAL DELIVERY OF ACTIVITY CENTRES ............................................. 45 7.3 ACTIONS .......................................................................................................................... 46

8 ATTACHMENT A: LITERATURE REVIEW ................................................................... 47

8.1 STATE PLANNING POLICY FRAMEWORK .................................................................................. 47 8.2 LOCAL PLANNING POLICY FRAMEWORK (LPPF) ....................................................................... 48 8.3 PLANNING DIRECTIONS, CITY OF BALLARAT ............................................................................. 49

9 ATTACHMENT B: DELIVERY SCENARIO MAPS .......................................................... 52

9.1 MAP 1: EXISTING RETAIL HIERARCHY, BWGA ......................................................................... 52 9.2 MAP 2: SCENARIO 1, BASE CASE (2030) ............................................................................... 54 9.3 MAP 3: SCENARIO 2, ELEVATED ROLE (2030) ........................................................................ 56 9.4 MAP 4: SCENARIO 1, BASE CASE (END CAPACITY) .................................................................... 58 9.5 MAP 5: SCENARIO 2, ELEVATED ROLE (END CAPACITY) ............................................................. 60

10 ATTACHMENT C: DEFINITIONS AND ABBREVIATIONS ............................................. 62

Contents

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

4

1 Executive Summary

MacroPlan Australia was commissioned by the City of Ballarat to undertake an economic assessment and understand the future allocation of proposed activity centres in the Ballarat West Growth Area (BWGA), particularly the retail and employment components.

The assessment will be used to assist Council in the preparation of a detailed Precinct Structure Plan (PSP) for the BWGA.

The BWGA forms the south western portion of the Ballarat urban area. It is around 8km from the Ballarat CBD and has been identified by Council as the major location for future growth, including retail and community uses that will meet the needs of a significant number of new households that are expected to accommodate the area. It includes the suburbs of Alfredton, Delacombe and Sebastopol.

The Study Area

For the purposes of estimating retail and commercial requirements across the BWGA, a Study Area has been defined. The Study Area is composed of:

• Precincts 1, 2, 3 and 4 (i.e. the Ballarat West Growth Area as defined in the BWGA Plan)

• The suburb of Alfredton, located to the north of Precinct 4 and the east of Precinct 3.

This boundary recognises that a future activity centre within Precinct 3 will not only serve future residents within the BWGA but also existing residents in the established suburb of Alfredton.

The Study Area does not include existing populations in Sebastopol or Delacombe, as it is acknowledged that these populations are already serviced by existing centres in Sebastopol.

The Ballarat West Growth Area Plan

MacroPlan have reviewed the BWGA Plan that outlines the proposed retail hierarchy of future activity centres across the BWGA.

The BWGA Plan places an emphasis on maintaining the retail hierarchy within the City of Ballarat, in particular by ensuring Ballarat CBD is the main, higher order centre with neighbourhood and local services provided to service residents within the BWGA.

Two types of centres are proposed within the BWGA under the BWGA Plan; the first a Local Activity Centre servicing walkable catchments, the second a Neighbourhood Activity Centre (proposed at Delacombe and Alfredton) that can support higher order retail.

While this represents a good platform from which to consider future retail provision across the BWGA, the realities of population growth, residential timing and impacts on the existing retail hierarchy will need to be considered.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

5

Figure 1. Ballarat West Study Area

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

6

Key considerations

MacroPlan has reviewed the City’s economic, planning and policy context and identified the following key considerations with regards to future delivery options for centres across the BWGA:

• Policy directions identified in the City of Ballarat Economic Development Strategy (2010‐2014), the Interim Activity Centres Strategy, Ballarat CBD strategy, Commercial Development Strategy: Issues and Directions Paper and the Ballarat West Growth Area Plan.

• The importance of supporting the primacy of the Ballarat CBD as addressed in the above policies.

• Allowing for the provision of an appropriate volume of localised employment in the BWGA.

• Consideration of market reality and feasibility in relation to the local catchments of each proposed centre.

• Consideration of an appropriate distribution of retail floorspace across the centres hierarchy including Local, Neighbourhood and Major Activity Centres.

• Consideration of the role of retail floorspace in promoting and encouraging the delivery of complementary land uses, including higher residential densities and employment in non‐retail commercial sectors.

• Potential economic impacts of delivery options for centres across the BWGA, including on the Ballarat community and wider region.

New residential populations will create additional demand for retail tenancies that have a preference to locate on Business Zone 4 land. It will be challenging to locate these tenancies in or adjacent to the CBD, therefore the planning of a new bulky goods precinct either in the BWGA or elsewhere in Ballarat should be considered. There should be a preference to locate bulky goods adjacent to existing centres or industrial related precincts to allow for comparison shopping and delivery of appropriate retail diversity across the Ballarat Urban Area.

The feasibility of delivering non‐retail based employment will be enhanced with relatively larger retail centres. A significant proportion of new residents will work in the office based sector and while many of these jobs should be accommodated in the Ballarat CBD in the short term, it is important to ensure that there are opportunities to deliver some office tenancies in neighbourhood centres across the BWGA.

It is important to recognise that there is a potential risk of a reduction in Ballarat’s employment self sufficiency if required additions to retail and commercial floorspace outside of the Study Area are not adequately planned for. For example, there will be significant leakage of retail expenditure if additional retail cannot be accommodated in the Ballarat CBD and other areas of Ballarat and is not compensated by increases in the size of retail centres in the Study Area.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

7

Demographic and Residential assessment

Capacity assessments prepared by MacroPlan (see the Ballarat Demographic and Residential assessment, Stages 1 and 2) have been used to inform this study. According to these assessments the population of the Study Area can be summarised as follows:

Figure 2. Population forecasts, Ballarat West Study Area, end capacity

Study Area 2010 2020 2030 End Capacity

Precinct 1 – Bonshaw Drive ‐ 503 3,252 19,027

Precinct 2 – Greenhalghs Road ‐ 703 4,286 10,575

Precinct 3 – Alfredton West ‐ 1,025 4,953 8,989

Precinct 4 – Carngham Road ‐ 575 3,238 8,694

Ballarat West Growth Area ‐ 2,806 15,729 47,285

existing population ‐ Alfredton 6,793 9,152 9,420 9,420

Total Study Area 6,793 11,957 25,149 56,704

Source: MacroPlan Australia

The BWGA is estimated to yield an end capacity of around 47,285 residents, with around one third (15,729, or 33.2%) of this growth occurring by 2030. In addition, the existing suburb of Alfredton will reach approximately 9,420 residents by 2030.

This means that centres in the BWGA will need to consider the retail demand generated by a Study Area that totals 56,704 residents. This does not include demand generated from outside the trade catchment from nearby regions such as Golden Plains.

Retail hierarchy and retail supply

Making recommendations as to the future allocation of retail floorspace is only possible once the existing retail context has been established. The supply of retail floorspace by format and the current retail hierarchy across the City of Ballarat has been assessed to obtain an understanding of how floorspace is distributed.

The first step in assessing existing and proposed retail supply has been a consideration of how key centre designations compare to market reality.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

8

Figure 3. Existing and Future Retail Centres, City of Ballarat

Centre Hierarchy Type Total retail

floorspace (m2) Existing Centres

Ballarat CBD Principal Activity Centre 143,220 Stockland Wendouree Major Activity Centre 36,160 Sebastopol North Neighbourhood Activity Centre 9,810 Howitt Street Neighbourhood Activity Centre 20,870 Sebastopol Local Activity Centre 3,960 Ballarat Marketplace Local Activity Centre 4,150 Midvale Shopping Centre Local Activity Centre 1,620 Northway Centre Local Activity Centre 1,470 Alfredton Local Activity Centre 530 Buninyong Local Activity Centre 2,350 Other Out‐of‐Centre 77,630 Total Existing 301,770

Future Centres Alfredton West Neighbourhood Activity Centre 6,500 Delacombe Town Centre Neighbourhood Activity Centre 15,000 Alfredton ‐ Cuthberts Rd Local Activity Centre 2,400 ‐ 3,700 Delacombe North * 2 Local Activity Centre 1,000 ‐ 1,500 Sebastopol West Local Activity Centre 1,000 Total Proposed 26,900‐29,200

Source: City of Ballarat ‐ Interim Activity Centres Strategy (2010)

While the current retail hierarchy supports the existing population of Ballarat, there will be challenges for the existing retail framework to support future economic growth, particularly significant increases to the resident population that is expected to continue across the Study Area.

Retail need in the Study Area

The following table identifies the volumes of additional retail demand (m2) that will be generated across the Study Area based on the existing population of Alfredton and future population growth.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

9

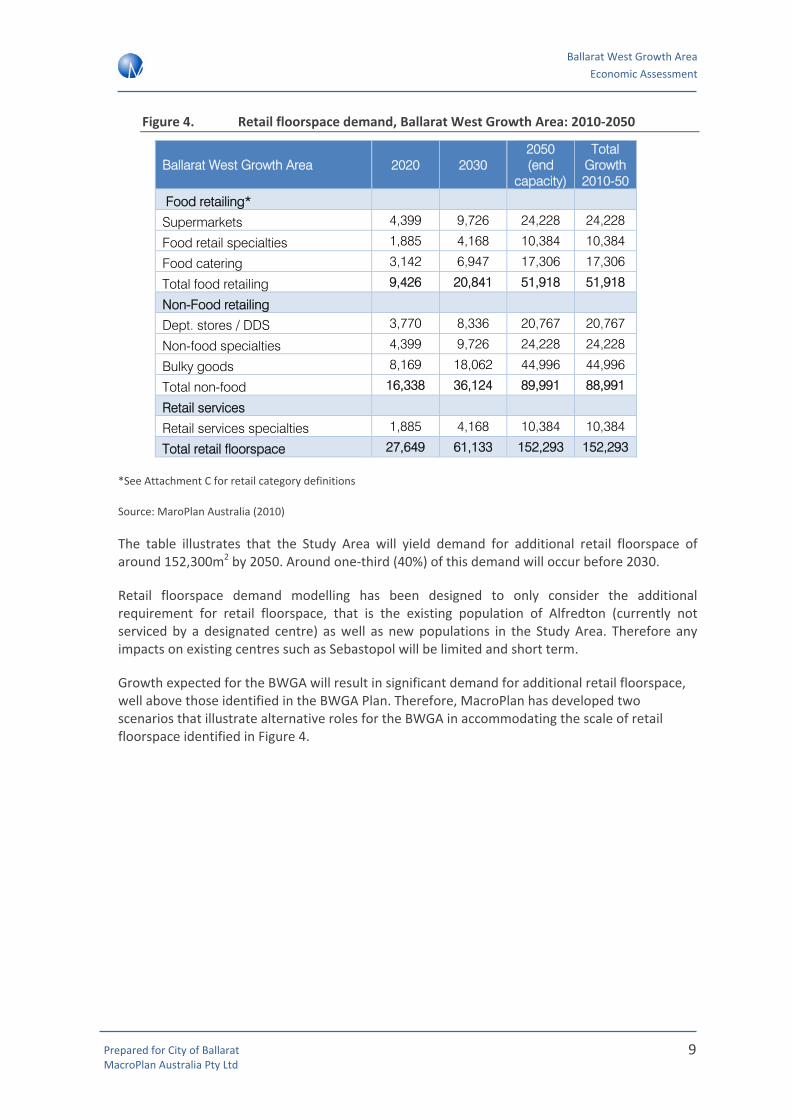

Figure 4. Retail floorspace demand, Ballarat West Growth Area: 2010‐2050

Ballarat West Growth Area 2020 2030 2050 (end

capacity)

Total Growth 2010-50

Food retailing*

Supermarkets 4,399 9,726 24,228 24,228

Food retail specialties 1,885 4,168 10,384 10,384

Food catering 3,142 6,947 17,306 17,306

Total food retailing 9,426 20,841 51,918 51,918

Non-Food retailing

Dept. stores / DDS 3,770 8,336 20,767 20,767

Non-food specialties 4,399 9,726 24,228 24,228

Bulky goods 8,169 18,062 44,996 44,996

Total non-food 16,338 36,124 89,991 88,991

Retail services

Retail services specialties 1,885 4,168 10,384 10,384

Total retail floorspace 27,649 61,133 152,293 152,293

*See Attachment C for retail category definitions

Source: MaroPlan Australia (2010)

The table illustrates that the Study Area will yield demand for additional retail floorspace of around 152,300m2 by 2050. Around one‐third (40%) of this demand will occur before 2030.

Retail floorspace demand modelling has been designed to only consider the additional requirement for retail floorspace, that is the existing population of Alfredton (currently not serviced by a designated centre) as well as new populations in the Study Area. Therefore any impacts on existing centres such as Sebastopol will be limited and short term.

Growth expected for the BWGA will result in significant demand for additional retail floorspace, well above those identified in the BWGA Plan. Therefore, MacroPlan has developed two scenarios that illustrate alternative roles for the BWGA in accommodating the scale of retail floorspace identified in Figure 4.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

10

The gap in supply will be exacerbated if the Ballarat CBD does not supply the volume of ‘non‐food’ retail floorspace to support new residents in the Study Area.

The following figure illustrates how additional retail floorspace demand derived from the Study Area by 2050 should be delivered across the centres hierarchy in Ballarat. This allocation has been developed based on previous experience, a review of benchmark centres and local economic and planning considerations.

The recommended distribution above is based on the following proportional allocations of key retail categories (see Attachment C for retail category definitions):

• Total Food (including supermarkets, food specialities and food catering): NACs and LACs (50%), PAC (30%), MACs (20%)

• Non‐food specialities: PAC (60%), MACs (20%), NACs and LACs (20%)

• DDS/Department Store demand: PAC (50%), MACs (50%)

• Bulky goods: homemaker centre/bulky goods precinct

The next step is to consider how the above distribution by hierarchy can be accommodated within and outside the Ballarat West Growth Area.

Delivery Scenarios

MacroPlan has defined two scenarios that illustrate alternative roles for the BWGA in accommodating retail floorspace and associated jobs for future residents. These scenarios assume that the distribution of higher order retailing (i.e. non‐food retail) is a significant driver in the co‐location of non‐retail based employment (i.e. in the professional, health and education sectors).

The first scenario outlines a traditional role for the BWGA in providing convenience neighbourhood centre based retailing and a relatively limited mix of non‐retail jobs, with demand for higher order retailing and employment leaking out of the Study Area to alternative locations across the City.

Distribution by hierarchy

Land use distribution

Additional retail

floorspace demand from the BWGA(2010‐2050)

150,000m2

Core retail (B1Z)106,000m2

PAC (Ballarat CBD)43,000m2

MACs28,000m2

NACs and LACs35,000m2

Bulky goods (B4Z)44,000m2

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

11

The second scenario explores an opportunity for a greater volume of retail floorspace and therefore enhanced opportunities for non‐retail employment in the BWGA. It provides Council with an alternative delivery framework that can allow for the accommodation of a greater volume of jobs in the BWGA in the event that job growth elsewhere in Ballarat may be constrained.

Planning for the second scenario is consistent with a sustainable economic development strategy for the City of Ballarat as it reduces the potential risk that economic development in the BWGA could reduce employment self sufficiency across the City by providing alternative employment opportunities.

Both scenarios have been developed to ensure that, as a minimum, the Study Area should meet the demand generated by NACs and potentially capture demand that would normally be directed at MACs.

Scenario 1: Ballarat West Growth Area Plan (Base Case)

This scenario assumes that NACs are delivered broadly in accord with the existing BWGA Plan and allows for the accommodation of a medium sized bulky goods precinct in the Study Area. The vast majority of food catering (including restaurants and cafes) and non‐food retail floorspace is assumed to be accommodated outside of the BWGA.

Scenario 2: BWGA Elevated role

This scenario considers the possibility whereby BWGA plays a higher order role in accommodating employment growth within the City of Ballarat. The additional population generated by residential development in the BWGA will require additional employment floorspace throughout Ballarat. It is important for Council to consider that the BWGA may therefore need to play a more significant role in accommodating employment in sectors outside of retail services.

Therefore consideration of an alternative scenario should be planned for to ensure that an appropriate volume of retail and commercial floorspace and employment in the retail sector is accommodated in Ballarat.

The end point distribution of retail floorspace under both scenarios at 2050 is illustrated in the following figure:

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

12

Figure 5. Retail floorspace distribution by centre hierarchy, BWGA: 2010‐2050

Centre type Scenario 1: BWGAP Scenario 2: BWGA Elevated Role

Principal Activity Centres

43,000m2

Full distribution to Ballarat CBD

No allocation to BWGA

Additional floorspace delivered by 2030

Full distribution to Ballarat CBD

No allocation to BWGA

Additional floorspace delivered by 2030

Major Activity Centres

28,000m2

Partial distribution to Ballarat CBD (approx. 15,000m2)

Partial distribution elsewhere in Ballarat e.g. Stockland Wendouree (approx. 15,000m2)

Delivery of a MAC at the BWGA by 2030 (e.g. Delacombe)

Neighbourhood Activity Centres/

Local Activity Centres

35,000m2

NACs: Full distribution to BWGA

Total of 20,000m2 distribution to 2 Large NACs (e.g. Delacombe and/or Alfredton)

LACs:20,000m2 allocated to 3‐4 LACs averaging 3,000‐5,000m2 in size

NACs: Up to 15,000m2 to a suitable site within the BWGA (e.g. Delacombe or Alfredton)

LACs: 20,000m2 allocated to 3‐4 LACs averaging 3,000‐5,000m2 in size

Bulky Goods

44,000m2

Partial distribution to the BWGA

Balance to existing centres or new bulky goods precinct elsewhere in Ballarat (50%)

Partial distribution to the BWGA

Balance to existing centres or new bulky goods precinct elsewhere in Ballarat (50%)

Non‐retail commercial

Around 13,500m2 delivered by 2030

Additional 6,500m2 floorspace delivered beyond 2030

Around 29,100m2 delivered by 2030

A further 7,500m2 delivered beyond 2030.

As evident in the above table, the key difference between Scenario 1 and Scenario 2 is partial allocation of MAC retail floorspace to the CBD under Scenario 1 and complete allocation of MAC retail floorspace to a MAC in the BWGA under Scenario 2.

Under both scenarios, employment self sufficiency levels in the BWGA are estimated to remain relatively low as the Ballarat CBD continues to deliver a majority of non‐retail employment opportunities.

However, it is important to ensure that non‐retail floorspace is planned for at centres within the BWGA to service future resident employed generated in the Study Area. This includes consideration of sites for bulky goods retailing that is adjacent to existing centres or industrial

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

13

related precincts to allow for comparison shopping and delivery of appropriate retail diversity across the Ballarat Urban Area.

Creating employment opportunities improves employment self‐sufficiency that will result in a number of net community benefits (social, environmental, economic), including:

• Reducing the level of out‐commuting from the region;

• Environmental benefits from reduced vehicle trips;

• Retained local expenditure; and

• Increased local business profitability.

Economic Principles

The following economic principles were designed to facilitate the allocation of retail and non‐retail commercial floorspace in a way that encourages sustainable economic development and maximise the wealth of residents in Ballarat by reducing the cost of shopping and commuting to work.

• Maximising Economic Development & Employment – The retail sector is a key employer in Ballarat and has significant economic multipliers in other sectors of the economy including wholesale trade, transport and distribution. It is important to ensure enough retail floorspace is provided in the Study Area that maximises economic development and employment in this and other sectors.

• Demonstrating need – Need for retail floorspace should be demonstrated in a particular catchment. Centres should have their own catchment (recognising that trade areas will overlap to some extent) that reflects their position in the retail hierarchy. Applications for retail floorspace need to not only demonstrate minimal impacts but also a market gap.

• Mitigating impacts – Impacts of proposed developments on existing centres with regard to sales should be limited. This principle will be achieved if the market need is demonstrated and a centre has its own defined primary catchment that does not overlap or is minimised with other centres. This balances the benefits of competition without creating negative impacts from a loss of existing business.

• Reducing length and number of vehicle trips – The cost of vehicle trips will have an impact on household budgets in the BWGA. The hierarchy needs to be supported in a way that reduces the length and number of vehicle trips where possible. Retail floorspace that encourages weekly visitation should be co‐located to a walkable catchment where possible.

• Encouraging a mix of uses – Apart from a diversity of retail, other supporting and complementary uses need to be accommodated in MACs and PACs. Land parcels need to be identified for residential accommodation and commercial floorspace to allow opportunities for mixed use activity and development.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

14

• Visibility and Access – where possible, future centre locations should be visible by passing traffic and located along major roads and highways.

Recommendations for optimal delivery of activity centres

According to the economic principles highlighted above, MacroPlan recommends that Council takes steps to maximise the opportunities to deliver Scenario 1 and prioritise the delivery of higher order retail and non‐retail commercial uses at the Ballarat CBD, as well as acknowledging the importance of providing some of these opportunities within the BWGA.

Delivery of non‐retail commercial uses will be critical in the establishment of the hierarchy across the City of Ballarat, particularly within the BWGA.

Actions

MacroPlan has developed a number of key actions to assist in the delivery of the above recommendations.

• Prioritise exploration of potential development locations within the Ballarat CBD

• Prioritise the elevation of Delacombe and Alfredton as the two higher order activity centres within the BWGA, with consideration that Delacombe has the potential to expand from a large NAC to a MAC beyond 2030 from a demand perspective;

• Explore alternative locations across the BWGA that could accommodate additional demand outside of the centres identified in the BWGA Plan. Locations considered should meet the economic principles as detailed above;

• Explore the potential for non‐retail employment across the City of Ballarat as a means of improving future employment self sufficiency;

• Consider locations for non‐centre based retailing such as bulky goods and homemaker centres of up to 44,000m2 to meet demand derived from the Study Area.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

15

2 Introduction

MacroPlan Australia was commissioned by the City of Ballarat to undertake an economic assessment to understand the future allocation of proposed activity centres in the Ballarat West Growth Area (BWGA), particularly the retail and employment components.

The assessment will be used to assist Council in the preparation of a detailed Precinct Structure Plan (PSP) for the BWGA.

2.1 Project Objectives

The Ballarat West Growth Area Plan (BWGAP) provides guidance on the planning and development of the BWGA for the next 30 years. This economic assessment builds on the findings from the BWGAP.

In addition to informing the PSP the following assessment will:

• identify demand for activity centres and additional retail and employment in the Ballarat BWGA;

• assist in timing and staging of centre delivery by providing retail provision recommendations for the short, medium and long term;

• provide recommendations regarding the hierarchy, role and function, sizing, floorspace requirements and potential land use of the proposed activity centres within the BWGA;

• outline any impacts of proposed centres on nearby existing centres including Sebastopol North and Sebastopol and a strategy to mitigate any impacts of these new activity centres.

Location and Context

The City of Ballarat is approximately 105 kilometres north‐west of Melbourne. The city had an estimated statistical district population of 91,787 at 2008.

Ballarat is renowned for its cultural heritage and decorative arts, especially applied to the built environment. Combined with the gold rush era, this has created a picturesque urban landscape. In 2003, Ballarat was the first of two Australian cities to be registered as a member of the International League of Historical Cities.

Furthermore, the City is notable for its very wide boulevards. The main street is Sturt Street and is considered among one of the finest main avenues in Australia with over 2 kilometres of central gardens known as the Sturt Street Gardens featuring bandstands, fountains, statues, monuments, memorials and lampposts.

Regarding the urban development, the inner established suburbs in Ballarat were initially laid out around the key mining areas and include Ballarat East, Golden Point, Soldiers Hill, Black Hill, Brown Hill, Eureka, Caledonian, Canadian, Redan, Sebastopol and Newington.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

16

Population Growth

More recently, a population boom has been experienced in planned suburbs, particularly to the north and west of the CBD, including Alfredton, Wendouree, Ballarat North and parts of Nerrina, Invermay and Invermay Park, Sebastopol, Delacombe, Mount Clear and Mount Helen.

Geographically, the move to focus on the west of Ballarat as a growth area is ideal due to the difficulty of expanding the hilly terrain situated to the north and high quality agriculture land to the east.

Road and Rail Infrastructure

There are a number of existing arterial roads servicing the BWGA such as the Remembrance Drive, Carngham Road, Glenelg Highway and Dyson Drive. A network of new collector roads and bus services are also proposed to meet future population growth.

In addition, the $505 million Western Highway duplication between Ballarat and Stawell will improve traffic efficiency along the west of Ballarat, particularly connections between Adelaide and Melbourne. The project is planned for completion in 2012.

Ballarat will also benefit from investment into Victoria’s Regional Rail Link that will create a 50 per cent extra capacity across regional Victoria and improve connections to metropolitan Melbourne.

2.2 The Study Area

For the purposes of estimating retail and commercial requirements across the Ballarat West Growth Area, the Study Area has been defined as:

• Ballarat West Growth Area (as defined in the Growth Area Plan); and

• The existing population in Alfredton to the north of the BWGA boundary.

Ballarat West Growth Area

Ballarat West Growth Area is situated approximately 8 kilometres west/south‐west of the Ballarat CBD and is currently used for rural residential and agricultural purposes. The area is highly fragmented with multiple owners.

Figure 6 shows that the BWGA is comprised of four major precincts.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

17

Figure 6. Study area and surrounds

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

18

Figure 7. Ballarat West Growth Area: PSP Precincts by Area

PRECINCT AREA Precinct 1 – Bonshaw Drive 700ha Precinct 2 – Greenhalghs Road 360ha Precinct 3 – Alfredton West 325ha Precinct 4 – Carngham Road 290ha TOTAL 1,675ha

Source: City of Ballarat, 2010

Located to the west of Sebastopol, Precinct 1 is the largest of the growth precincts, comprised of approximately 700 hectares of land. It accommodates mainly rural residential dwellings and farm land and is bounded by low density residential on the northern and eastern aspect.

Precinct 2 sits north of the Glenelg Highway and to the west of the low density residential area of Delacombe. Greenhalghs Road runs east to west through the centre of the precinct. Precinct 2 currently has a small amount of low density residential to the south of the precinct and just north of the Glenelg Highway.

Precinct 3 sits to the west of Alfredton and is the northernmost precinct in the Ballarat West Growth Area. It is bordered to the west by the Ballarat Skipton Rail Trail and to the north by Remembrance Drive.

To the west of the industrial zone on Learmonth Street is Precinct 4, bordered to the north by the established suburb of Alfredton, to the south by Precinct 2. Carngham Road runs east to west through the centre of the precinct.

The City of Ballarat has identified two neighbourhood activity centres and four local activity centres within the Ballarat West Growth Area. These will be discussed in more detail in the following sections of this report.

Alfredton

The Study Area for the purposes of this assessment also includes the established suburb of Alfredton, located to the north‐east of the BWGA. Residents in Alfredton are currently not serviced by any centre. While it is not located within the BWGA boundary as defined in the BWGAP, any proposed activity centre within the BWGA will need to service the needs of existing as well as future Alfredton residents.

2.3 Methodology

The methodology used to conduct this assessment is based on analysis of historical and projected regional employment and job growth using standard approaches. This has been considered across the industries relevant to this study to inform the future retail, commercial and industrial floorspace requirements across the Study Area.

In addition, the economic development potential for growth fronts has been considered as part of this assessment. Within the BWGA, MacroPlan considers that retail developments typically lead to non‐retail employment creation.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

19

Demand for non‐retail uses such as office, community facilities, and higher residential densities (e.g. townhouses, units and apartments) will be largely dependent on the retail and amenity provided at centres. That is, population drives retail expenditure growth; expenditure creates demand for new retail floorspace, critical mass in retail drives residential densities through an active street culture with improved amenity and a wider range of retailing opportunities; and activated streets with high amenity and range in retail will drive demand for office floor space.

Based on this, the following methodology has been employed:

• Estimate future population for the Study Area (2010‐2050)

• Undertake a retail based assessment in the area to estimate retail floorspace potential in the catchment.

• Undertake a centre‐based assessment based on benchmarks to estimate total jobs for each centre.

2.4 Report Structure

This report is divided into the following sections:

• Section 2: Overview of the Study Area

• Section 3: Previous studies and literature review

• Section 4: Socio‐demographic analysis

• Section 5: Retail and commercial hierarchy

• Section 6: The need for activity centre floorspace

• Section 7: Land use need

• Section 8: Conclusions and recommendations

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

20

3 Retail and commercial centre hierarchy

In order to make recommendations on the future of retail floorspace in the Study Area, MacroPlan has considered the existing retail and commercial landscape of the area, including centres that may be impacted by any changes to the current structure.

3.1 Definitions

MacroPlan has defined a preferred activity centres hierarchy as part of this assessment. This hierarchy is outlined as follows:

Principal Activity Centres (PAC)

MacroPlan recommends the following Principal Activity Centre definition is applied and recognised within the Ballarat West PSP:

• These centres are expected to source trade from a maximum trade area of 200,000 persons and a Primary Trade Area of at least 100,000 persons.

• This will support floorspace of between 80,000 and 120,000sqm of retail GLA depending on incomes and market shares.

• If trade areas and market shares are demonstrated to be relatively high (as demonstrated by a survey etc), expansions in floorspace in secondary trade areas will be considered by Council to ensure an equitable distribution of retail activity and limit monopoly trading by an individual centre.

Major Activity Centres (MAC)

MacroPlan also recommends the following Major Activity Centre definition is applied and recognised within Ballarat West PSP:

• These centres support a residential catchment of up to 120,000 persons which will support demand for between 40,000 and 60,000sqm of retail floorspace GLA.

• They should be sub‐ordinate to Principal Activity Centres, particularly in regard to the provision of employment mixes and non‐retail floorspace.

• They will generally be located in the secondary trade area of a Principal Activity Centre or they may enjoy their own distinct trade area, however they would face competition from a supporting network of Neighbourhood Activity Centres (defined below) particularly for food retailing.

• Again if the centre catchment is proven to be significantly higher than 100,000 persons, it is likely that future development in the centres secondary trade areas will restrict the existing catchment.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

21

Neighbourhood Activity Centres (NAC)

This level of the hierarchy supports MACs and provides a mix of grocery (supermarket) and speciality retailing.

Guidelines:

• These centres have a primary role of providing weekly shopping needs to residents principally in regard to food retailing. They are also supported by a network of speciality retailers and other businesses meeting household and business needs.

• They support a catchment of up to 30,000 persons however most trade is drawn from a Primary trade area of 15,000 persons or less.

• These centres are generally delivered early in a development cycle and should be supported by a network of local activity centres (defined below).

• The Primary Trade Area will support between 6,000 and 8,000m2 of retail floorspace with a further 3,000m2 supported by the secondary trade area due to limited market shares.

• These centres provide an important source of local retail based and commercial employment. Ideally these centres should be located on primary or secondary roads to capture some passing trade.

Local Activity Centres (LAC)

Local Activity Centres provide an opportunity to provide convenience and grocery retailing in walkable catchments in existing and new residential development fronts.

They should be ideally provided on a grid network of streets to support walkable catchments and bicycle access.

Guidelines:

• These centres meet the daily and to a lesser extent weekly shopping needs of residents.

• They will support a 3,000 to 5,000 person Primary Trade Area and should be encouraged in a framework that supports walkable access to a majority of residents.

• They will normally contain a small supermarket with some supporting speciality retail.

• Subject to a Primary Trade Area of 5,000 persons the maximum supportable floorspace would be in the order of 3,000 to 4,000m2 depending on incomes.

3.2 Current and future floorspace supply

In order to understand the potential retail and commercial floorspace requirement for the Study Area, MacroPlan has reviewed the existing Centre hierarchy and floorspace allocations across the City of Ballarat.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

22

Assessing the existing centres framework can determine how the market is currently operating and whether there are significant gaps or surpluses in the existing allocation of retail and commercial floorspace that growth areas such as the BWGA can alleviate through future allocation.

The following table identifies floorspace (m2) including non‐retail components across the City of Ballarat by centre type as defined in Section 4.1.

Figure 8. Total* floorspace in Activity Centres by type: City of Ballarat

Activity Centre type Floorspace (m2)

Principal Activity Centre (Ballarat CBD) 223,410m2

Major Activity Centre 43,290m2

Neighbourhood Activity Centre (Large) 41,440m2

Neighbourhood Activity Centre (Small) 21,540m2

Other (out of centre) 327,560m2

Total 657,240m2

* includes retail and non retail floorspace

Source: City of Ballarat Interim Activity Centres Strategy (2010)

As shown in the figure above, the Ballarat CBD accounts for around one third of the City’s total floorspace (223,410m2). Of this, retail comprises around 143,200m2 of floorspace. Although a large amount of commercial floorspace is also located in the CBD, a high level of ‘out‐of‐centre’ commercial floorspace also exists. Around 52,840m2 of commercial, professional and business services floorspace is located outside a designated activity centre. This tends to arise from businesses locating on the outskirts of centres that have no floorspace provisions for this use.

Existing retail centres hierarchy: City of Ballarat

Currently, the total retail provision across the City of Ballarat is 301,770m2. Ballarat CBD comprises of the largest concentration of retail uses as well as government, community, health and education services.

Large amounts of this supply are within:

• Principal Activity Centre: Ballarat CBD (143,220m2);

• Major Activity Centre: Stockland Wendouree Shopping Centre (36,160m2) represents the only MAC with major tenants (Kmart, Coles and Safeway) as well as specialty stores;

• Neighbourhood Centres: Howitt Street Shopping Centre (20,870m2), Sebastopol North (9,810m2), Sebastopol (3,960m2).

By 2030, it is projected that this total may have to increase by around 50% to meet future demand. As part of the City of Ballarat’s Interim Activity Centres Strategy, an emphasis is placed

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

23

on seeking to estimate the future supportable retail floorspace over the next 15 years and developing a framework to guide future development.

Proposed retail hierarchy, City of Ballarat

MacroPlan has assessed current retail floorspace supply in the City of Ballarat. The figure below displays the hierarchy for current and proposed centres in the region.

Figure 9. Retail Hierarchy, City of Ballarat

Type Location Explanation

Principal Activity Centre Ballarat CBD Major centre with discount departments store, multiple supermarkets and a range of retail and non‐retail outlets

Major Activity Centre Stockland Wendouree Discount department stores and supermarkets with a range of retail and non‐retail outlets

Large Neighbourhood Activity Centre

Sebastopol North

Howitt Street

A larger scale supermarket with specialty retail and non‐retail outlets

Small Neighbourhood Activity Centre

Ballarat Marketplace

Buninyong

Midvale Centre

Smaller scale centre, usually with a supermarket and/or a small number of specialty outlets

Local Activity Centre Alfredton – Cuthberts Road

Sturt Street

Mainly smaller retail shops which catchment comprises mainly local residents and passing traffic

Source: Ballarat Commercial Development Strategy

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

24

Figure 10. Ballarat Activity Centre Network – Current and Proposed

Source: Ballarat Commercial Development Strategy (2008)

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

25

Figure 11. Current and proposed floorspace in Ballarat

Centre Hierarchy Type Retail/Bulky Goods m2

Commercial m2

Trade and Repair m2 Vacant m2 Total

Existing Centres Ballarat CBD Principal Activity Centre 143,220 70,220 4,070 5,900 223,410 Stockland Wendouree Major Activity Centre 36,160 3,610 0 3,520 43,290 Sebastopol North Neighbourhood Activity Centre 9,810 350 100 0 Howitt Street Neighbourhood Activity Centre 20,870 5,690 2,960 1,660 41,440 Sebastopol Local Activity Centre 3,960 610 410 3,630 Ballarat Marketplace Local Activity Centre 4,150 0 220 230 Midvale Shopping Centre Local Activity Centre 1,620 270 0 0 Northway Centre Local Activity Centre 1,470 0 0 0 Alfredton Local Activity Centre 530 710 0 0 Buninyong Local Activity Centre 2,350 1,270 110 0 21,540 Other Out‐of‐Centre 77,630 152,710 80,720 16,500 327,560 Total Existing 301,770 235,440 88,590 31,440 657,240

Proposed Centres Alfredton West Neighbourhood Activity Centre 6,500 Delacombe Town Centre Neighbourhood Activity Centre 15,000 Alfredton ‐ Cuthberts Rd Local Activity Centre 2,400 ‐ 3,700 Delacombe North * 2 Local Activity Centre 1,000 ‐ 1,500 Sebastopol West Local Activity Centre 1,000

Total Proposed 26,900‐29,200

Source: City of Ballarat ‐ Interim Activity Centres Strategy (2010)

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

26

Proposed future retail floorspace allocation: Ballarat West Growth Area

In relation to future retail supply in the BWGA, the BWGA Plan proposes a network of future activity centres including specific locations and prescribed retail floorspace limits. The Plan defines the need for Local Centres and Neighbourhood Centres.

Four Local Centres are recommended in the BWGA that would contain a small group of shops (total floorspace of between 1,000‐ 1,500m2). These would be located at:

• Delacombe North;

• Delacombe front of Glenelg Highway;

• Sebastopol West; and

• Alfredton on Cuthberts Road near Dyson Drive.

The Plan also identifies two future Neighbourhood Centres; Delacombe in the south and Alfredton in the north.

The following table outlines the proposed sizes of these centres. The location of these Centres ensures the Local Centres serve a catchment of 400m walkable distance and the larger Neighbourhood Centres are within reasonable distance from each other.

Figure 12. Proposed retail centres hierarchy: Ballarat West Growth Area

Location Hierarchy Retail floorspace (m2)

Alfredton West Neighbourhood Activity Centre 6,500

Alfredton – Cuthberts Road Local Activity Centre 2,400‐ 3,700

Delacombe North x2 Local Activity Centre 1,000‐1,500

Delacombe Town Centre Neighbourhood Centre 15,000

Sebastopol West Local Activity Centre up to 1,000

Total 26,900‐ 29,200

Proposed Developments

Alfredton West – Neighbourhood Activity Centre

The BWGA Plan proposes to allocate around 6,500m2 of floorspace to this development located on Dyson Drive near the intersection with Sturt Street and Remembrance Drive. Around 8 hectares of land has been set aside for this centre. From a capacity perspective this land could accommodate a centre at least three times the proposed size if required, the equivalent of a sub‐regional centre.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

27

Delacombe ‐ Neighbourhood Activity Centre

The Delacombe development will be the largest of the activity centres proposed for the BWGA. The sites are split across three sides of the Glenelg Highway and Wiltshire Lane. The development is proposed to be spread across 15,000m2 of land however, there is potential that this centre could be significantly larger.

Alfredton (Cuthberts Road) – Local Activity Centre

The central Alfredton development located on Cuthberts Road is a 3.5 hectare site with 3,700m2 allocated for a centre which would likely include a small shopping centre which would capture localised shopping needs from those who don’t travel the further distance to the Alfredton West Primary Neighbourhood Centre.

Delacombe North (x2) – Local Activity Centre

Two LACs of up to 1,500m2 have been identified to service future residents in Delacombe North. One will be located adjoining the school site, another fronting the Glenelg Highway.

Sebastopol West ‐ Local Activity Centre

One smaller LAC of up to 1,000m2 has been identified to service the future neighbourhood opposite MR Power Park.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

28

4 Retail floorspace demand

The objective for this project is to identify the economic potential particularly within identified activity centres across each of the four precincts characterising the BWGA. In particular, this involves assessment of the likely level of retail floorspace demand generated in the area. It is important to note that retail catchments for each centre are not discrete and are likely to overlap.

In order to arrive at these outcomes it is necessary to examine the regional trends in terms of resident population and labour force growth.

4.1 Methodology

The following methodology reviews the future retail potential in the Ballarat West Growth Area and has a focus on examining the potential for residential growth outcomes:

• Estimate the likely residential outcomes in each precinct, including estimates of dwelling yields and resident population. This has been completed in a previous study prepared by MacroPlan.

• Estimate the potential demand for local retail facilities, based on the following approach:

o Estimate the average per capita retail expenditure by residents in each precinct, based on current benchmarks and with real growth in average spending applied.

o Apply per capita spending estimates to the projected population at capacity in order to calculate total retail floorspace demand by residents in each precinct.

o Confirm the potential supportable retail floorspace, based on the expenditure projections, and adopting a relevant average turnover level per square metre of retail floorspace.

• Estimate the extent to which retail floorspace would be retained within the precinct.

• Calculate total local retail floorspace provision from above.

• Estimate the potential for accommodating major tenants i.e. supermarkets.

• Estimate the potential to accommodate non‐retail activities in activity centres.

• Identify an appropriate activity centre network for the precinct on the basis of the retail and non‐retail floorspace analysis.

The timeframe for the analysis is the period between 2010 and 2050 which is considered to be an appropriate period over which the proposed activity centre hierarchy (as identified in Figure 3) and the BWGA will be fully developed.

It is important to appreciate that the activity centre floorspace estimates prepared for each precinct are provided as broad indications of the potential scale of development. The actual size of centres and their components (including supermarkets) will be subject to more detailed

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

29

analysis at the planning permit stage and may need to be adjusted according to changes to activity centre formats and innovation.

4.2 Population trends and projections: City of Ballarat

In 2009, the City of Ballarat had an estimated resident population (ERP) of around 94,000 persons, according to Victoria in Future estimates. Between 2001 and 2009, the majority of Ballarat growth occurred in the Ballarat – Inner North (60% of total growth, or 6,276 people) and Ballarat‐South (35% of total growth, or 3,638 people) while the population of Ballarat – North declined slightly (‐56 people).

Population projections by SLA are detailed as follows. It is expected that population expansion in the City of Ballarat will be comprised of growth in the following Statistical Local Areas (SLAs):

• Ballarat‐Central SLA: is forecast to expand from 36,145 persons in 2010 to 39,972 persons in 2030, averaging +0.5% p.a.

• Ballarat–Inner North SLA: is forecast to expand from 33,061 persons in 2010 to 49,487 persons in 2030, averaging +2.0% p.a.

• Ballarat‐North SLA: is forecast to expand from 1,057 persons in 2010 to 1,234 persons in 2030, averaging +0.8% p.a.

• Ballarat‐South SLA: is forecast to expand from 25,737 persons in 2010 to 36,285 persons in 2030, averaging +1.7% p.a.

These population trends by SLA are summarised in the following table.

Figure 13. Estimated Resident Population, City of Ballarat by SLA, 2010‐2030

2010 2015 2020 2025 2030 Growth 2010‐2030

Ballarat (C) ‐ Central 36,145 37,007 38,159 39,075 39,972 3,827 0.5%

Ballarat (C) ‐ Inner North 33,061 36,859 40,897 45,010 49,487 16,426 2.0%

Ballarat (C) ‐ North 1,057 1,118 1,168 1,201 1,234 177 0.8%

Ballarat (C) ‐ South 25,737 28,265 30,895 33,498 36,285 10,548 1.7%

Total City of Ballarat 96,000 103,249 111,119 118,784 126,978 30,978 1.4%

Source: ABS Department of Health and Ageing, MacroPlan Australia 2010

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

30

4.3 Population and dwelling capacity in Ballarat West

Future population levels have also been estimated for the Study Area using a capacity based approach.

The following table highlights capacity for additional residents in the Ballarat West Growth Area, as estimated in the report titled ‘Demographic and Residential Assessment’ also prepared by MacroPlan Australia.

Figure 14. Study Area Population Projections

2020 2030 End capacity

Precinct 1 – Bonshaw Creek 503 3,252 19,027

Precinct 2 – Greenhalghs Road 703 4,286 10,575

Precinct 3 – Alfredton West 1,025 4,953 8,989

Precinct 4 – Carngham Road 575 3,238 8,694

existing population ‐ Alfredton 9,152 9,420 9,420

Total Study Area 11,957 25,149 56,704

Source: Ballarat Demographic and Residential Assessment, MacroPlan Australia 2010

According to capacity‐based assessments, population will grow in accordance with an increase in dwelling stock. Increasing dwelling stock is directly related to household and family composition which will impact the potential retail spend for particular types of goods.

4.4 Activity Centre Requirements

Opportunities for retail development will be determined by the eventual residential population, and to a lesser extent by the needs of workers and other visitors to the area.

Growth and end capacity dwelling estimates for each precinct were estimated for the Residential and Demographic Assessment prepared by MacroPlan in 2010. Using this information, a detailed analysis has been undertaken based on the application of the methodology described in Section 4.1, with allowance for retail demand generated by non‐residents, such as employees and other visitors to the area.

In planning activity centres in the Ballarat West Growth Area, a number of factors need to be considered:

• Centres in the area will act as centres of convenience and local activity for the surrounding residential population.

• Potential exists for more significant retail facilities to further support the sub‐region of south western Ballarat.

• The retail mix of centres is envisaged to include full‐line supermarkets (above 2,500m2), and a range of specialties that reflects the likely expenditure patterns of residents.

• There will be a range of supportable non‐retail floorspace such as business services for example banks, printing services, accountancy, post office, etc.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

31

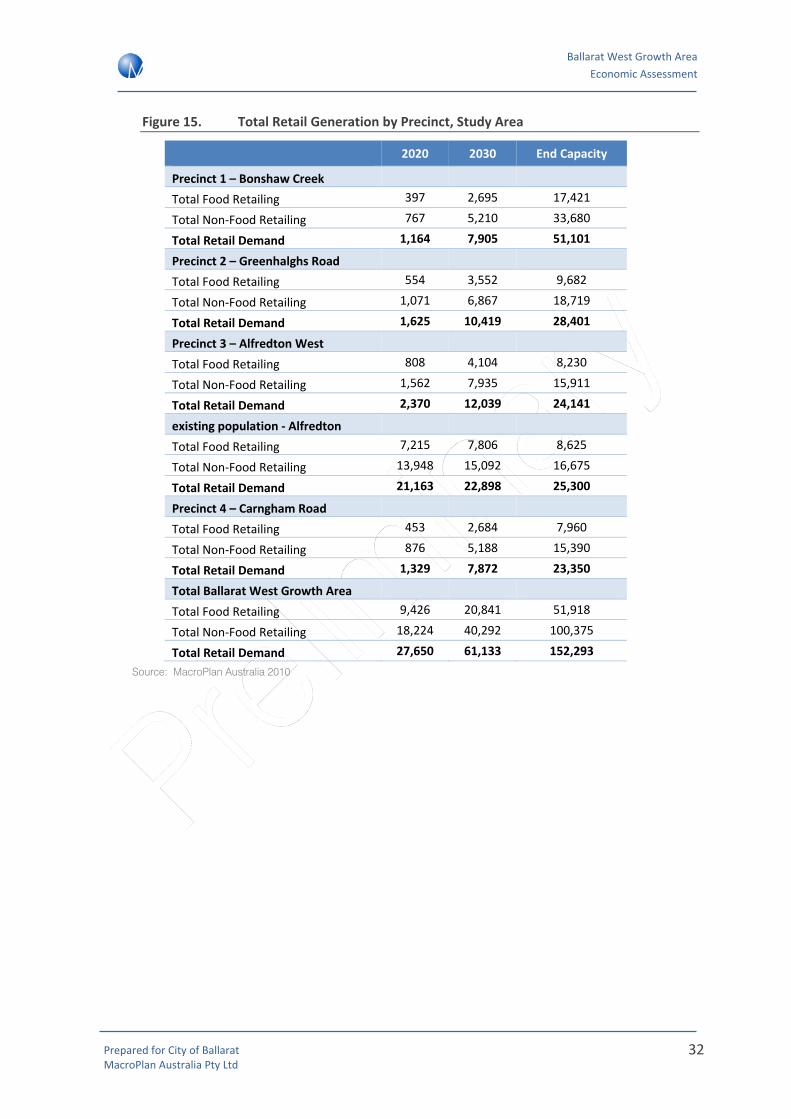

4.5 Retail floorspace demand by Precinct

The amount of floorspace sustained by the forecast population is calculated using per capita ratios. The ratios used in this assessment are organised by major retail categories and based on previous experience and a number of sources, including the Census of Land Use and Employment (CLUE) and ABS retail data. These ratios have been assumed to increase over the forecast period, due to population growth that result in growth in total retail spending as well as increases in real spending over time:

• Food retail: increases from 0.75 m2 per capita in 2010, to 0.83 m2 per capita by 2030 and 0.92 m2 per capita in 2050;

• Non food retail: increases from 1.3 m2 per capita in 2010, to 1.4 m2 per capita by 2030 and 1.6 m2 per capita in 2050;

• Retail services: increases from 0.15 m2 per capita in 2010 to 0.16 m2 per capita by 2030 and 0.18 m2 per capita in 2050;

Using the above ratios, the following figure summarises demand generated by the future population across each precinct in the Study Area:

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

32

Figure 15. Total Retail Generation by Precinct, Study Area

2020 2030 End Capacity

Precinct 1 – Bonshaw Creek Total Food Retailing 397 2,695 17,421

Total Non‐Food Retailing 767 5,210 33,680

Total Retail Demand 1,164 7,905 51,101

Precinct 2 – Greenhalghs Road Total Food Retailing 554 3,552 9,682

Total Non‐Food Retailing 1,071 6,867 18,719

Total Retail Demand 1,625 10,419 28,401

Precinct 3 – Alfredton West Total Food Retailing 808 4,104 8,230

Total Non‐Food Retailing 1,562 7,935 15,911

Total Retail Demand 2,370 12,039 24,141

existing population ‐ Alfredton Total Food Retailing 7,215 7,806 8,625

Total Non‐Food Retailing 13,948 15,092 16,675

Total Retail Demand 21,163 22,898 25,300

Precinct 4 – Carngham Road Total Food Retailing 453 2,684 7,960

Total Non‐Food Retailing 876 5,188 15,390

Total Retail Demand 1,329 7,872 23,350

Total Ballarat West Growth Area Total Food Retailing 9,426 20,841 51,918

Total Non‐Food Retailing 18,224 40,292 100,375

Total Retail Demand 27,650 61,133 152,293 Source: MacroPlan Australia 2010

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

33

Total allocations across the BWGA can be summarised by retail category as follows:

Figure 16. Ballarat West Growth Area –Total Retail Floorspace Demand

Ballarat West Growth Area 2020 2030

2050 (End

capacity)

Total Growth 2010-50

Food retailing

Supermarkets 4,399 9,726 24,228 24,228

Food retail specialties 1,885 4,168 10,384 10,384

Food catering 3,142 6,947 17,306 17,306

Total food retailing 9,426 20,841 51,918 51,918

Non-Food retailing

Dept. stores / DDS 3,770 8,336 20,767 20,767

Non-food specialties 4,399 9,726 24,228 24,228

Bulky goods 8,169 18,062 44,996 44,996

Total non-food 16,339 36,124 89,992 89,992

Retail services

Retail services specialties 1,885 4,168 10,384 10,384

Total retail floorspace 27,650 61,132 152,293 152,293

Source: MacroPlan Australia 2010

The above table highlights that by 2050, the future resident population in the Study Area generates a total retail floorspace of around 152,000m2. Around one third (52,000m2) of this will be comprised of food retailing, a further 60% will be comprised of non‐food retail, including Department Stores, Discount Department Stores, Bulky goods retailing and other specialities (90,000m2), while the remaining 10,000m2 of the study area population’s future retail floorspace requirements should be comprised of retail services.

4.6 Sebastopol Review

Sebastopol is an existing activity centre located to the south east of the BWGA. It represents the closest centre to the BWGA boundary. While it is envisaged that some of the future residents within the BWGA will utilise services in the existing Sebastopol centre, it is expected that a majority of the trade will come from outside the BWGA boundary.

Figure 17 illustrates the Primary and Secondary Trade Area catchments of the existing Sebastopol centre. It highlights that there is minimal overlap with the Primary Trade Area and the BWGA (where around 60%‐70% of the Centre’s trade is sourced from). Therefore it is unlikely that future centres in the BWGA would have a significant impact on the existing Sebastopol shopping centre.

In addition, retail floorspace demand modelling has been designed to only consider the additional requirement for retail floorspace subject to the existing population of Alfredton (currently not serviced by a designated centre) as well as new populations in the Study Area. Therefore impacts on existing centres such as Sebastopol will be limited and short term.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

34

Figure 17. Sebastopol Trade Area

Source: MacroPlan Australia

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

35

4.7 Retail allocation to the Ballarat West Growth Area

As indicated in the previous section, growth expected for the BWGA will result in significant demand for additional retail floorspace, well above those identified in the BWGA Plan. Therefore, MacroPlan has developed two scenarios that illustrate alternative roles for the BWGA in accommodating the scale of retail floorspace identified in Figure 4.

The gap in supply will be exacerbated if the Ballarat CBD does not supply the volume of ‘non‐food’ higher order retail floorspace required by new residents in the Study Area.

The following figure illustrates how additional demand derived from the Study Area by 2050 should be delivered across the retail hierarchy in Ballarat. This allocation has been developed based on previous experience and consideration of the issues highlighted above.

Figure 18. Future retail distribution, 2010‐2050

Source: MacroPlan Australia

The recommended distribution above is based on the following proportional allocations of key retail categories

• Total Food (including supermarkets, food specialities and food catering): NACs and LACs (50%), PAC (30%), MACs (20%),

• Non‐food specialities: PAC (60%), MACs (20%), NACs and LACs (20%)

• DDS/Department Store demand: PAC (50%), MACs (50%)

• Bulky goods: homemaker centre/bulky goods precinct

The next step will be to consider how the above distribution by hierarchy can be accommodated within and outside the BWGA.

Distribution by hierarchy

Land use distribution

Additional retail demand in Ballarat(2050)

150,000m2

Core retail (B1Z)106,000m2

PAC (Ballarat CBD)43,000m2

MACs28,000m2

NACs and LACs35,000m2

Bulky goods (B4Z)44,000m2

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

36

5 Non‐retail floorspace demand

In addition to retail activities, activity centres also accommodate a range of non‐retail shopfront businesses. In some circumstances, home‐based businesses may also seek small office spaces in Neighbourhood Activity Centres.

State government policy generally seeks to expand the range of uses in activity centres to include a wider variety of commercial office uses, particularly for higher order centres (i.e. Major Activity Centres), in an attempt to improve employment self sufficiency and sustainability by encouraging local job provision in close proximity to residential neighbourhoods.

MacroPlan has undertaken a high level labour force needs assessment for the Study Area. The purpose of this analysis is to confirm the need and quantum for non‐retail commercial floorspace within the BWGA.

It is also expected that employment in other non‐retail sectors, including education and health could also be accommodated across the BWGA.

Supplying an inadequate mix of jobs across all professions in the City of Ballarat will lead to a leakage of jobs out of the region as residents seek employment elsewhere. This leads to unsustainable outcomes in relation to private motor vehicle use and exacerbates the demands on existing and future planned transport infrastructure, especially roads.

5.1 Key Assumptions

Proportion of non‐retail floorspace

The proportion of non‐retail commercial (office) floorspace in NACs and MACs can vary depending on centre structure and ownership. For example, a NAC with one owner typically has a relatively low proportion of non‐retail floorspace in the order of 20% of total centre floorspace. In contrast, established areas tend to have a greater provision and diversity of uses within a main street context. Generally these centres have a higher provision of non‐retail uses in the order of 35% ‐ 40%. Provision of non‐retail floorspace increases with higher order shopping centres, with a Major Activity Centre typically providing around 80% of total centre floorspace is in non‐retail commercial formats.

Centre Proportion of non‐retail (office) floorspace

Neighbourhood Activity Centre 20% ‐ 40%

Major Activity Centre 60% ‐ 80%

The extent to which non‐retail uses can be accommodated in the BWGA depends on a number of factors such as:

• Design format – main‐street, enclosed or stand alone shopping centre

• Demographic, employment composition and business environment – the extent to which the surrounding population demographic is conducive for business service generation,

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

37

and the potential to locate these facilities at other locations, such as industrial precincts within the growth area.

Land requirement assumption

Figure 19. Land Requirement Assumption

Industry Total floorspace (m2) per job

Core Retail 30m2

Bulky Goods Retailing 70m2

Non‐retail commercial (office)* 20m2

Source: MacroPlan Australia, 2010

Population and Labour Force Growth

Projected employment in the Study Area has been assessed by analysing historical employment trends within Ballarat along with projected changes in participation rates and occupation mix.

Understanding the trends in the Ballarat region will indicate commercial floorspace requirements for each of the activity centres.

At the 2006 Census, Ballarat had a labour force of 40,101 persons, or 58.7% of the resident population. In 2008, the unemployment rate was estimated at 7.1% or 3,308 persons, indicating a labour force of 46,592 persons and approximately 50.8% of the population1. Given population growth, the number of persons employed remained above 2006 levels.

Based upon the latest employment data, 65.1% of the Australian population is in the labour force (as of June 2010).2 Given macroeconomic indicators and recovery from the GFC, this level is not expected to decrease within the short to medium terms. Wyndham LGA has been reviewed as a benchmark for the area going forward. Wyndham retained approximately 66% of its population within the labour force at the 2006 Census.3

Thus, a realistic estimate of 60% of residents entering the labour force has been used to prepare labour force estimates by precinct listed below based upon the population projections in Section 5.

1 ABS National Regional Profile: Ballarat (C) (Local Government Area) 2 ABS Cat No. 6202.0, Labour Force, Australia, June 2010. 3 ABS Cat. No. 2068.0, Census of Population and Housing, Wyndham (C) (Local Government Area)

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

38

Figure 20. Ballarat West Growth Area – Employment Projections

Ballarat West Growth Area

2020 2030 2050 (End Capacity)

Population Employment Population Employment Population Employment

Precinct 1 – Bonshaw Creek 503 302 3,252 1,951 19,027 11,416

Precinct 2 – Greenhalghs Road

703 422 4,286 2,572 10,575 6,345

Precinct 3 – Alfredton West 1,025 615 4,953 2,972 8,989 5,393

Precinct 4 ‐ Carngham Road 575 345 3,238 1,943 8,694 5,216

Total 2,805 1,683 15,729 9,438 47,284 28,371

Source: MacroPlan Australia, 2010

Business location assumptions

Business location preferences have a very significant influence on the demand for land within a retail framework. The importance of business location preferences is evident, particularly when considering the main retail locations which are to be developed within the BWGA.

The key centres which will be the focus for non‐core retail activities in the BWGA are the two activity centres of Alfredton West and Delacombe.

Ballarat CBD will remain the dominant employment location including private and public sector activities given its central location to meet markets and suppliers.

Non‐core retail business establishing with activity centres in the Ballarat West Growth Area are likely to be seeking more affordable options for business development. These location patterns can change with time as a business establish and seek out optimal locations for their activities.

The most important influences on encouraging business activity within activity centres include:

• Competition from other office locations, such as campus office on industrial land;

• Opportunities for business specialisation / clustering;

• Access to labour, especially surrounding residents;

• Flexibility with floor plates and configuration;

• Competitive leasing arrangements;

• Good access to the main road network;

• Visibility (including potential highway frontage);

• Surrounding retail network, including location of key retail anchors; and

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

39

• Amenity setting in terms of building design, landscaping and natural environment.

5.2 Implications

The delivery of high order centres creates greater opportunities to deliver non‐retail based employment such as in the professional, health and education sectors thereby improving employment self sufficiency for a region.

The following section details the two delivery scenarios that have been developed to assess the future implications of two alternative roles for the BWGA in accommodating jobs for future residents. The implications for non‐retail formats to be accommodated within the BWGA will be acknowledged in this assessment.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

40

6 Delivery scenarios

MacroPlan has defined two scenarios that illustrate alternative roles for the BWGA in accommodating jobs for future residents. These scenarios assume that the distribution of higher order retailing (i.e. non‐food retail) is a significant driver in the co‐location of non‐retail based commercial employment (i.e. in the professional, health and education sectors).

The first scenario outlines a traditional role for the BWGA in providing convenience neighbourhood centre based retailing and a relatively limited mix of non‐retail jobs, with demand for higher order retailing and employment leaking out of the study area to alternative locations across the City.

The second scenario explores an opportunity for a greater volume of retail floorspace and therefore enhanced opportunities for non‐retail commercial employment in the BWGA. It provides Council with an alternative delivery framework that can allow for the accommodation of a greater volume of jobs in the BWGA in the event that job growth elsewhere in Ballarat may be constrained.

Planning for the second scenario is consistent with a sustainable economic development strategy for the City of Ballarat as it reduces the potential risk that economic development in the BWGA could reduce employment self sufficiency across the City by providing alternative employment opportunities.

Both scenarios have been developed to ensure that, that as a minimum, the Study Area should meet the demand generated by NACs and potentially capture demand that would normally be directed at MACs.

Figure 21 summarises the floorspace distribution recommendations between 2010 and 2050 under both delivery scenarios. These recommendations are based on the volume of retail floorspace that can be sustained by the future resident population at Ballarat West.

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

41

Figure 21. Retail floorspace distribution by centre hierarchy, 2010‐2050

Centre type Scenario 1: BWGAP Scenario 2: BWGA Elevated Role

Principal Activity Centres

43,000m2

Full distribution to Ballarat CBD

No allocation to BWGA

Additional floorspace delivered by 2030

Full distribution to Ballarat CBD

No allocation to BWGA

Additional floorspace delivered by 2030

Major Activity Centres

28,000m2

Partial distribution to Ballarat CBD (approx. 15,000m2)

Partial distribution elsewhere in Ballarat e.g. Stockland Wendouree (approx. 15,000m2)

Delivery of a MAC at the BWGA by 2030 (e.g. Delacombe)

Neighbourhood Activity Centres/

Local Activity Centres

35,000m2

NACs:Full distribution to BWGA

Total of 20,000m2 distribution to 2 Large NACs (e.g. Delacombe and/or Alfredton)

LACs:20,000m2 allocated to 3‐4 LACs averaging 3,000‐5,000m2 in size

NACs: Up to 15,000m2 to a suitable site within the BWGA (e.g. Delacombe or Alfredton)

LACs: 20,000m2 allocated to 3‐4 LACs averaging 3,000‐5,000m2 in size

Bulky Goods

44,000m2

Partial distribution to the BWGA

Balance to existing centres or new bulky goods precinct elsewhere in Ballarat (50%)

Partial distribution to the BWGA

Balance to existing centres or new bulky goods precinct elsewhere in Ballarat (50%)

Non‐retail commercial

Around 13,500m2 delivered by 2030

Additional 6,500m2 floorspace delivered beyond 2030

Around 29,100m2 delivered by 2030

A further 7,500m2 delivered beyond 2030.

As evident in the above table, the key difference between Scenario 1 and Scenario 2 is partial allocation of MAC retail floorspace to the CBD under Scenario 1 and complete allocation of MAC retail floorspace to a MAC in the BWGA under Scenario 2.

Both scenarios are described in greater detail as follows.

6.1 Scenario 1: Ballarat West Growth Area Plan (Base Case)

This scenario assumes that NACs are delivered broadly in accord with the existing BWGA Plan and allows for the accommodation of a medium sized bulky goods precinct in the Study Area. The

Ballarat West Growth Area Economic Assessment

Prepared for City of Ballarat MacroPlan Australia Pty Ltd

42

vast majority of food catering (including restaurants and cafes) and non‐food retail floorspace is assumed to be accommodated in the Ballarat CBD.

Maps 2 and 4 in Attachment B illustrate the location of centres across the BWGA under Scenario 1. In particular, Map 2 highlights that by 2030, Precinct 3 (Alfredton West) could accommodate a Small Neighbourhood Activity Centre and Precinct 4 (Carngham Road) could accommodate 2 Local Activity Centres.

The small NAC in Precinct 3 could be elevated to a larger NAC by 2050 to cater for the population expected in the Alfredton West area.

End capacity population will support the delivery of a second large NAC at Delacombe (servicing precincts 1 and 2) to meet the convenience needs of the 7,540 residents expected in the two precincts by 2030. This will allow for the delivery of a fourth LAC south‐west of the site, in precinct 1.