asia-pacific wealth report(2010)

TRANSCRIPT

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 1/32

AaPa Wealth rept

2010

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 2/32

State of Asia-Pacific Wealth 4

2009 in Review: Asia-Pacific Showed Resilience in the Face 8

of the Global Downturn

Asia-Pacific HNWIs Favored Equities and Real Estate 14

in Portfolios in 2009

Real Estate Was a Preferred Financial Investment 18

for Asia-Pacific HNWIs in 2009

Asia-Pacific HNWIs Seek Out Tangible-Asset Investments 21

Spotlight: Wealth Management Firms in Asia-Pacific Face 24

Unique Challenges in Adapting Their Strategies to Meet

New Client Demands

Methodology 30

Contnts

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 3/32

TO OUR READERS,

Capgemini and Merrill Lynch Global Wealth Management ar plasd to prsnt th 2010 Asia-Pacific Wealth Report ,

or fifth annal in-dpth look at th hih nt worth (HNW) marktplac in th rion. Th rport bilds on th sccss

of th World Wealth Report , now in its 14th yar. Both rports ar th rslt of an xtnsiv collaboration btwn or two

firms, stdyin th ky trnds that affct hih nt worth individals (HNWIs).

Th past yar, 2009, saw a rsrnc in th nmbr and walth of Asia-Pacific HNWIs that fw miht hav prdictd jst a yar bfor. Bt whil many Asia-Pacific markts srd back to lif in 2009, th fallot from th crisis is vidnt

in HNWIs’ nw invstmnt bhaviors and attitds.

This rport xamins th post-crisis shifts in HNWIs’ asst allocations, rflctin an asin of crisis fars and a

catios rtrn to markts. Bt it also looks bhind ths spcifics at th mor fndamntal chans in HNWIs’

invstmnt prioritis.

W find that Asia-Pacific HNWIs, mch lik thir contrparts lobally, want to bttr ndrstand xactly what thy ar

invstin in, whr it is hld and how it is vald, and thy ar dmandin mor val-addd advic and invstmnt

options that proprly alin with thir risk profils and invstmnt oals. For walth manamnt firms, ths nds

translat into nw dmands—and crat challns that ar niq to th Asia-Pacific rion.

W look in particlar at how nw HNW-clint dmands ar pttin intns prssr on prodct and srvic offrins

and clint srvicin modls—and ndrscorin th critical shorta of walth manamnt capabilitis in th rion.

Manain this prssr, and implmntin nw clint-drivn stratis ffctivly, will b critical as walth manamnt

firms position thmslvs to captr th normos potntial that still lis ahad in Asia-Pacific.

It is a plasr to prsnt this yar’s rport, and w hop yo draw val from its insihts.

Asia-Pacific Walth Rport

Sallie Krawcheck

President, Global Wealth &Investment ManagementBank o America

Bertrand Lavayssière

Managing DirectorGlobal Financial ServicesCapgemini

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 4/32

4 2010 AsiA-PAcific WEALTH rEPorT

1 HNWIs are defined as those having investable assets of US$1 million or more, excluding primary residence, collectibles, consumables and consumer durables

ASIA-PACIFIC HNWI POPULATION RECOUPED CRISIS-RELATED LOSSES

Hon Kon and India witnssd th stronst HNWI-

poplation rowth (104.4% and 50.9% rspctivly),followd by Taiwan (42.3%), rcovrin most of thlosss mad in 2008. In 2008, th HNWI poplationsof Hon Kon and India had xprincd th larstprcnta dclins in th rion.

Japan and China still hav th larst HNWI

poplations in th rion. Japan alon accontd for54.6% of Asia-Pacific HNWIs, down only marinally from 56.8% in 2008.

Region’s HNWIs and Their Wealth Are StillHighly Concentrated

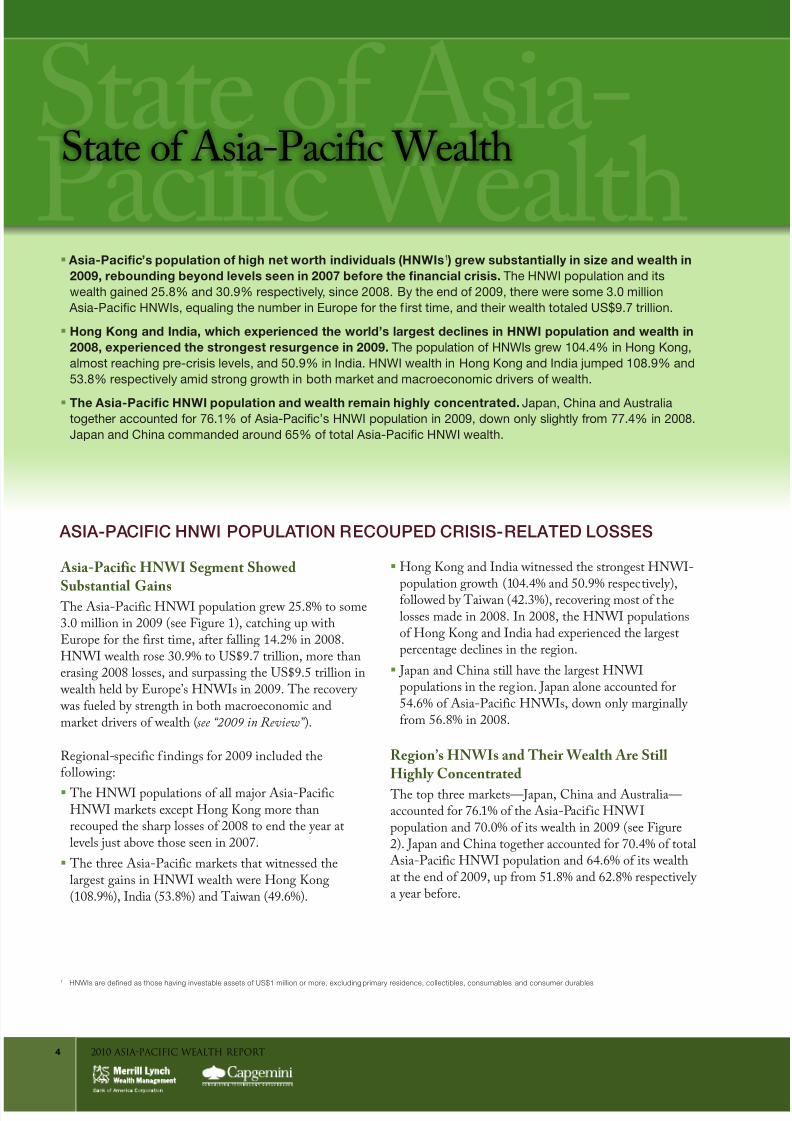

Th top thr markts—Japan, China and Astralia—accontd for 76.1% of th Asia-Pacif ic HNWIpoplation and 70.0% of its walth in 2009 (s Fir2). Japan and China tothr accontd for 70.4% of totalAsia-Pacific HNWI poplation and 64.6% of its walthat th nd of 2009, p from 51.8% and 62.8% rspctivly a yar bfor.

Asia-Pacific’s population of high net worth individuals (HNWIs1 ) grew substantially in size and wealth in

2009, rebounding beyond levels seen in 2007 before the financial crisis. The HNWI population and itswealth gained 25.8% and 30.9% respectively, since 2008. By the end o 2009, there were some 3.0 million Asia-Paciic HNWIs, equaling the number in Europe or the irst time, and their wealth totaled US$9.7 trillion.

Hong Kong and India, which experienced the world’s largest declines in HNWI population and wealth in

2008, experienced the strongest resurgence in 2009. The population o HNWIs grew 104.4% in Hong Kong,almost reaching pre-crisis levels, and 50.9% in India. HNWI wealth in Hong Kong and India jumped 108.9% and53.8% respectively amid strong growth in both market and macroeconomic drivers o wealth.

The Asia-Pacific HNWI population and wealth remain highly concentrated. Japan, China and Australiatogether accounted or 76.1% o Asia-Paciic’s HNWI population in 2009, down only slightly rom 77.4% in 2008.Japan and China commanded around 65% o total Asia-Paciic HNWI wealth.

Stat of Asia-

Pacific WalthStat of Asia-Pacific Walth

Asia-Pacific HNWI Segment Showed

Substantial Gains Th Asia-Pacific HNWI poplation rw 25.8% to som3.0 million in 2009 (s Fir 1), catchin p witherop for th first tim, aftr fallin 14.2% in 2008.HNWI walth ros 30.9% to uS$9.7 trillion, mor thanrasin 2008 losss, and srpassin th uS$9.5 trillion in walth hld by erop’s HNWIs in 2009. Th rcovry was fld by strnth in both macroconomic andmarkt drivrs of walth (see “2009 in Review” ).

Rional-spcific f indins for 2009 incldd thfollowin:

Th HNWI poplations of all major Asia-Pacific

HNWI markts xcpt Hon Kon mor thanrcopd th sharp losss of 2008 to nd th yar atlvls jst abov thos sn in 2007.

Th thr Asia-Pacific markts that witnssd th

larst ains in HNWI walth wr Hon Kon(108.9%), India (53.8%) and Taiwan (49.6%).

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 5/32

52010 AsiA-PAcific WEALTH rEPorT

sTATE of AsiA-PAcific WEALTH

FIguRe 1. Asia-Paciic HNWI Population, 2006–2009 (by Market)

(000s)

2009200820072006

1,484

343

15799

88

20

100

117

149

138

154

169

118123

96

12910584

413

364

477

174

1271278382

1,5171,366

1,650

24

24

19

6668

7871

36

44

5076

42376158

2.6m 2.8m 2.4m 3.0m

CAGR 2006–2008 -3.4% Growth 2008–2009 25.8%

Number

of

HNWIs

(000s)

0

500

1,000

1,500

2,000

2,500

3,000

Other Markets 11.1%

Indonesia 28.3%

Taiwan 42.3%

Singapore 32.7%

Hong Kong 104.4%

Thailand 19.6%

India 50.9%

Japan 20.8%

China 31.0%

Australia 34.4%

South Korea 21.2%

Annual Change

2008−2009

Note: (a) All chart numbers are rounded; (b) “Other Markets” includes Kazakhstan, Malaysia, Myanmar, New Zealand, Pakistan, Philippines, Sri Lanka and VietnamSource: Capgemini Lorenz curve analysis, 2010

FIguRe 2. Distribution o Asia-Paciic HNWI Wealth, 2009 (by Market)

(%)

Total: US$9.7 Trillion

40.3%

24.3%

5.4%

4.9%

3.5%

2.7%

2.4%

0.8%

3.9%

3.8%

7.8%

Japan 3,892

China 2,347

Singapore 369

India 477

Australia 519

South Korea 340

Other Markets 749

Indonesia80

Thailand 232

Taiwan 264

Asia-Pacic HNWIWealth by market, 2009

Annual Change2008–2009

(US$ billion)

Hong Kong 379

22.4%

40.4%

35.6%

53.8%

36.7%

23.2%

11.6%30.6%

22.2%

49.6%

108.9%

Note: (a) All chart numbers are rounded; (b) “Other Markets” includes Kazakhstan, Malaysia, Myanmar, New Zealand, Pakistan, Philippines, Sri Lanka and VietnamSource: Capgemini Lorenz curve analysis, 2010

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 6/32

2010 AsiA-PAcific WEALTH rEPorT6

sTATE of AsiA-PAcific WEALTH

Japan is by far th larst sinl HNWI markt inAsia-Pacific. Alon it accontd for 54.6% of thAsia-Pacific HNWI poplation and 40.3% of its walth at th nd of 2009. Howvr, rowth in Japan’sHNWI smnt was modst compard with othrmarkts in th rion, d to th slowdown in Japan’s

macroconomic rowth and th rlativly wak prformanc of its stock markts. Japan’s qity-marktcapitalization ros jst 6.1% in 2009 compard with anavra of 87.9%2 across othr Asian markts. ThHNWI poplation rw 20.8% to 1.7 million and walth ros 22.4% to uS$3.9 trillion.

China rmaind th scond-larst HNWI bas in thrion, with 477,000 HNWIs, p 31.0% from thprvios yar. Stock-markt capitalization in Chinasoard mor than 100% in 2009, as th conomy rw ata rapid 8.6% pac.

Astralia, which still has th third-larst HNWIpoplation amon Asia-Pacific markts, boncd back in 2009 aftr many of thos who had falln into th“mass afflnt”3 catory in 2008 raind thirHNWI stats. Movmnt in and ot of th HNWIcatory is rlativly frqnt in Astralia, whr 91.1%of all HNWIs ar in th lowst (uS$1 million–uS$5million) walth band.

In India, th HNWI poplation and its walth rw

50.9% and 53.8% rspctivly in 2009, mor thanrcopin th losss of 2008, with rsrnt stockshlpin to driv th rcovry. India’s stock-marktcapitalization mor than dobld in 2009 aftr droppin64.1% in 2008. Importantly, thoh, HNWI walth wasalso drivn in India by th strnth in th ndrlyinconomy, which rw 6.8% in 2009.

Taiwan’s HNWI poplation also showd on of thsharpst rowth rats in th rion (42.3%) aftr TaiwanStock exchan capitalization jmpd 84.5%. Thatsharp incras was fld by nws that Taiwan and

China wr notiatin a financial mmorandm of ndrstandin (Mou) that wold lad to ratrcross-straits coopration on trad and invstmnt andlibralization of financial markts.

Hong Kong Saw Strong Gains but Could NotRecoup the Record Losses of 2008

Th HNWI poplations of Hon Kon and Indiaxprincd th stronst rowth in nmbrs and walthin th world in 2009, bt thos ains had followd th

world’s larst dclins in 2008. In India, th HNWIpoplation and its walth flly rcovrd to pr-crisislvls, bt in Hon Kon, th nmbr of HNWIs at thnd of 2009 was still only 79% of th nmbr at th ndof 2007, bcas th starin dclins of 2008otwihd th hfty ains of 2009.

Hon Kon’s HNWI rcovry in 2009 followdsinificant ains in th ky markt drivrs of walth,particlarly qitis and ral stat. Hon Kon’spoplation of HNWIs is spcially snsitiv to pricmovmnts in ths asst classs for a nmbr of rasons.

For on thin, thy hold most of thir walth in ths twoasst classs. In fact, of all Hon Kon HNWI assts in2009, 52% was hld in ithr qitis or ral stat—andanothr 6% was in th form of altrnativ invstmnts. Allthr of ths asst classs tnd to b volatil, rsltin inpotntially lar swins in HNWI walth lvls.

Hon Kon’s HNWI nmbrs also tnd to flctat widly bcas a sinificant nmbr of Hon Kon HNWIs ar inth uS$1 million–uS$5 million walth band. As a rslt, whn asst prics plnd in 2008, many HNWIs in thislowr band qickly droppd into th “mass afflnt”

brackt—bt thn jst as qickly raind thir HNWIstats as asst prics rcovrd in 2009.

Ultra-HNWI Ranks and Wealth Showed Hefty Gains in 2009

Th Asia-Pacific ultra-HNWI4 poplation and its walth xpandd 36.7% and 42.6% rspctivly in 2009(s Fir 3), postin ains that far xcdd th avrarowth amon th nral HNWI poplation.

At th nd of 2009, ultra-HNWIs rprsntd only 0.6%of th total Asia-Pacific HNWI poplation, clos to th

lobal ultra-HNWI/HNWI ratio, bt accontd for24.5% of total HNWI walth in Asia. That is lss thanth lobal avra of 35.5%, bt is consistnt withhistorical trnds. Of th rion’s ultra-HNWIs, 57.0% wr from Japan and China.

2 World Federation of Exchanges, 2010; Capgemini analysis, 20103 The “mass affluent” are defined as individuals with investable assets of US$100,000 to US$1,000,000

4 Ultra-HNWIs are defined as those having investable assets of US$30 million or more, excluding primary residence, collectibles, consumables, and consumer durables

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 7/32

2010 AsiA-PAcific WEALTH rEPorT 7

sTATE of AsiA-PAcific WEALTH

China and India Are Expected to Be the Fastest-Expanding Asia-Pacific HN WI Segments inComing Years

Emerging Asia (China, India, Indonsia and Thailand)is fast bcomin th main nin of rowth in thAsia-Pacific rion (see “2009 in Review” ), and its HNWIpoplation showd robst rowth of 33.2% in 2009, with walth p 40.4%. goin forward, China and India arlikly to rmain th fastst-rowin HNWI smnts inth world, basd on th positiv otlook for markt andmacroconomic drivrs of walth for thos conomisand th Asia-Pacific rion as a whol.

Fastr conomic rowth and th rsltant improvmntin bsinss conditions shold propl xpansion in thHNWI smnt sinc bsinss ownrship and incomtothr accont for th majority (73%) of all HNWI walth in Asia-Pacific xcldin Japan.

elswhr in Asia-Pacific, Newly Industrialized Asia (Sinapor, Hon Kon, Taiwan and Soth Kora) saw th fastst rowth in HNWI poplation and walth in2009 (40.4% and 49.2% rspctivly), mostly bcas of Hon Kon and Taiwan. Th rowth in th Nwly Indstrializd conomis is likly to modrat somwhat,and b otpacd by th rowth in HNWI walth inemrin Asia. In Industrialized Asia (Astralia, Japan

and Nw Zaland), th HNWI poplation and its walth ar likly to kp rowin, bt at a slowr pacthan in th rst of th rion. In 2009, th HNWIpoplation in Indstrializd Asia rw 21.9%, whil its walth ros 23.8%.

FIguRe 3. Number o HNWIs by Wealth Band, 2008–2009 (Global and Asia-Paciic)

Source: Capgemini Lorenz curve analysis, 2010

Number oIndividuals 2009

HNWI PopulationGrowth 2008–2009

HNWI WealthGrowth 2008–2009

% o Total HNWIWealth 2009

Global Asia-

PacifcGlobal

Asia-

PacifcGlobal

Asia-

PacifcGlobal

Asia-

Pacifc

93.1k(0.9%

o Total)

19.6k(0.6%

o Total)19.4% 36.7% 21.5% 42.6% 35.5% 24.5%

896.9k(8.9%

o Total)

240.9k(8.0%

o Total)18.4% 31.9% 18.3% 32.0% 21.9% 23.9%

9,053.4k(90.1%o Total)

2,761.9k(91.4%o Total)

16.9% 25.3% 17.1% 25.9% 42.6% 51.6%US$1m–US$5m

Millionaire “Net Door”

US$5m–US$30m“Mid-Tier Millionaire”

>US$30mUltra-HNWI

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 8/32

8 2010 AsiA-PAcific WEALTH rEPorT

5 The Economist Intelligence Unit, Regional Data, June 20106 Ibid

7 Ibid

8 Ibid

ASIA-PACIFIC ECONOMY KEPTGROWING IN 2009, ALBEIT MORESLOWLY THAN IN 2008

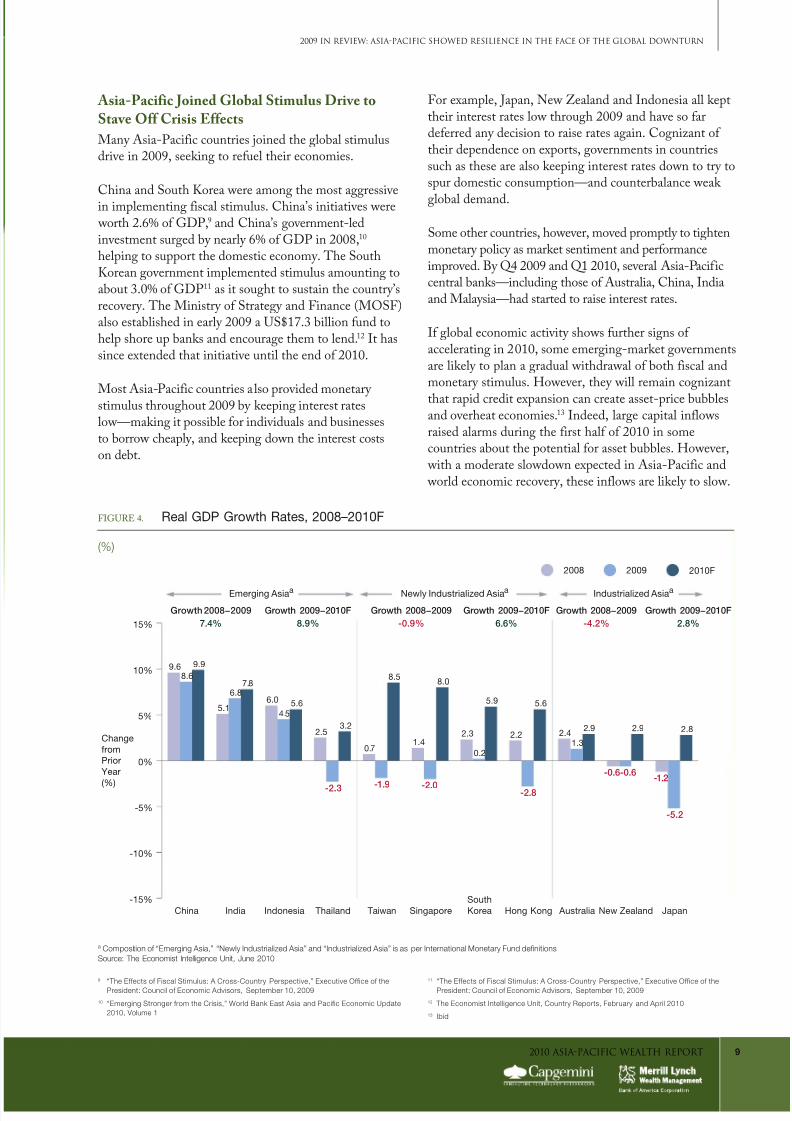

Asia-Pacific Economy Excluding Japan Grew 4.6%in 2009 despite the Contraction in World GDP

Asia-Pacific as a whol provd rsilint in 2009, dspitth 2.0% contraction in World gDP.6 gDP rw 4.6% inAsia-Pacific xcldin Japan, lss than th 5.6% in 2008,bt a stron pac nvrthlss. Howvr, emrin Asia was th primary drivr of rowth, with th standotsbin China and India, whr ral gDP rw 8.6% and6.8% rspctivly.7 Many othr conomis in Asia-Pacificactally contractd, incldin thr of th for Nwly Indstrializd conomis and two of th thr contrisin Indstrializd Asia (s Fir 4).

Asia-Pacific rowth was ndrmind, howvr, by thslowdown in xports of oods and srvics across mostmarkts. exports droppd 19.5% in Indstrializd Asia in2009, sinificantly mor than th 9.0% dclin across thrst of Asia-Pacific,8 bcas Indstrializd Asia ishavily dpndnt on trad with dvlopd nations, which wr sffrin from th conomic slowdown. Japan, for xampl, saw xports pln 24.1% in 2009, hitspcially hard by th drop in ato dmand from thunitd Stats and erop. India and China wr th only

two major Asia-Pacific contris in which indstrialprodction actally ros in 2009, as thy njoyd a mordivrsifid xport markt and broadr domstic dmand.

The economic crisis pervaded the globe in 2009, demonstrating the interdependence o the world’s economies,

but Asia-Pacific proved to be the most resilient, helped in particular by strong gross domestic product

(GDP) growth of 8.6% in China and 6.8% in India.5 In act, GDP across Emerging Asia grew 7.4% in 2009,signiicantly more than in the other economies o the region and world.

Fiscal-stimulus measures were widespread as governments worldwide boosted expenditures to supporttheir economies. Most sizable in Asia-Paciic was the US$586 billion in stimulus commitments by China—anamount that was second only to the U.S. stimulus package (US$787 billion) in absolute terms.

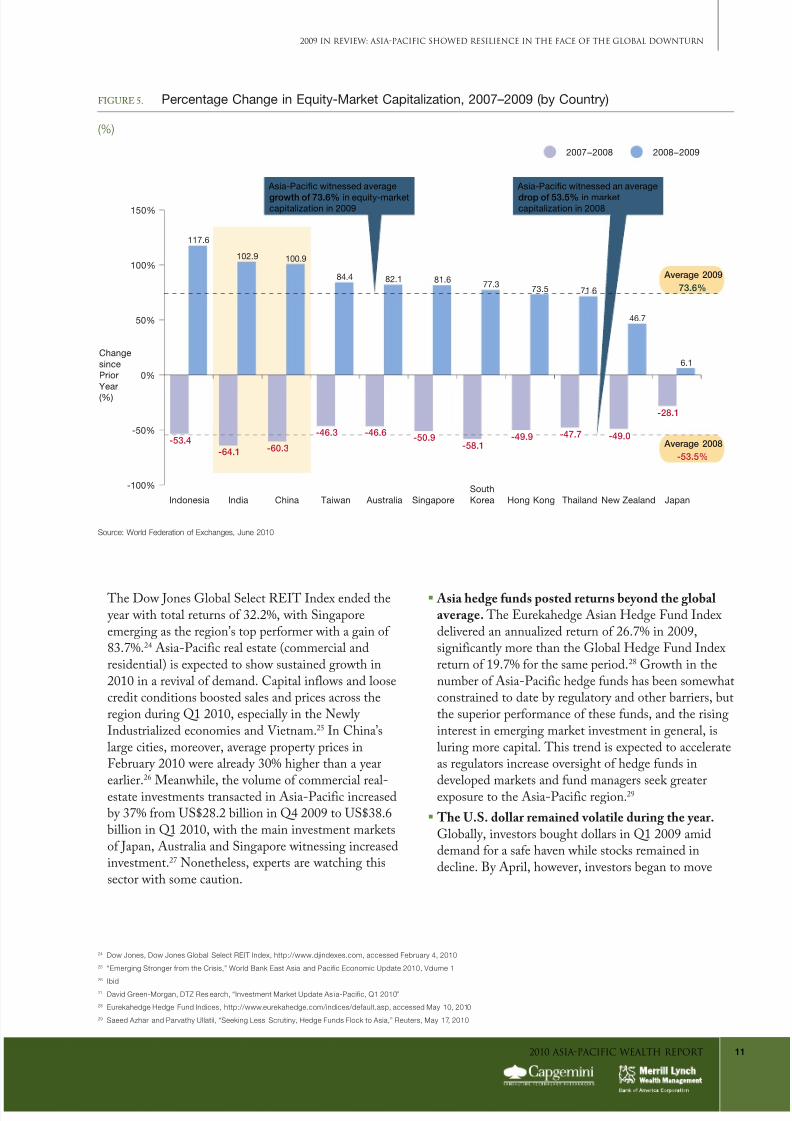

Key market drivers of wealth rebounded strongly in 2009, with Asia-Pacific equity-market capitalization

surging 73.6%, compared with aggregate global growth o 47.1%, as ears over the inancial crisis began toabate and investors cautiously returned to markets. China, Indonesia and India each doubled its equity-marketcapitalization during the year, and the region’s emerging markets showed superior growth overall, even in theirst hal o 2009 when developed markets had yet to revive.

In 2010 and 2011, aggregate Asia-Pacific growth is likely to outpace the world economy, as relatively

resilient domestic demand and intra-regional trade help to offset any ongoing weakness in exports to

advanced economies. Emerging Asia and Newly Industrialized Asia are expected to post GDP growth o 8.9%and 6.6% respectively, in line with pre-crisis levels. Asia-Paciic is likely to experience aster GDP expansionthan the rest o the world, although the nature o the recovery is likely to dier by market.

2009 in Rviw

2009 in Rviw: Asia-PacificShowd Rsilinc in th Fac

of th global Downtrn

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 9/32

2010 AsiA-PAcific WEALTH rEPorT 9

9

“The Effects of Fiscal Stimulus: A Cross-Country Perspective,” Executive Office of thePresident: Council of Economic Advisors, September 10, 2009

10 “Emerging Stronger from the Crisis,” World Bank East Asia and Pacific Economic Update2010, Volume 1

11

“The Effects of Fiscal Stimulus: A Cross-Country Perspective,” Executive Office of thePresident: Council of Economic Advisors, September 10, 2009

12 The Economist Intelligence Unit, Country Reports, February and April 2010

13 Ibid

2009 in rEviEW: AsiA-PAcific sHoWEd rEsiLiEncE in THE fAcE of THE GLobAL doWnTurn

Asia-Pacific Joined Global Stimulus Drive toStave Off Crisis Effects

Many Asia-Pacific contris joind th lobal stimlsdriv in 2009, skin to rfl thir conomis.

China and Soth Kora wr amon th most arssivin implmntin fiscal stimls. China’s initiativs wr worth 2.6% of gDP,9 and China’s ovrnmnt-ldinvstmnt srd by narly 6% of gDP in 2008,10 hlpin to spport th domstic conomy. Th SothKoran ovrnmnt implmntd stimls amontin toabot 3.0% of gDP11 as it soht to sstain th contry’srcovry. Th Ministry of Straty and Financ (MOSF)also stablishd in arly 2009 a uS$17.3 billion fnd tohlp shor p banks and ncora thm to lnd.12 It hassinc xtndd that initiativ ntil th nd of 2010.

Most Asia-Pacific contris also providd montary stimls throhot 2009 by kpin intrst ratslow—makin it possibl for individals and bsinsssto borrow chaply, and kpin down th intrst costson dbt.

For xampl, Japan, Nw Zaland and Indonsia all kptthir intrst rats low throh 2009 and hav so fardfrrd any dcision to rais rats aain. Conizant of thir dpndnc on xports, ovrnmnts in contrissch as ths ar also kpin intrst rats down to try tospr domstic consmption—and contrbalanc wak

lobal dmand.

Som othr contris, howvr, movd promptly to tihtnmontary policy as markt sntimnt and prformancimprovd. By Q4 2009 and Q1 2010, svral Asia-Pacificcntral banks—incldin thos of Astralia, China, Indiaand Malaysia—had startd to rais intrst rats.

If lobal conomic activity shows frthr sins of acclratin in 2010, som mrin-markt ovrnmntsar likly to plan a radal withdrawal of both fiscal andmontary stimls. Howvr, thy will rmain conizantthat rapid crdit xpansion can crat asst-pric bbblsand ovrhat conomis.13 Indd, lar capital inflowsraisd alarms drin th first half of 2010 in somcontris abot th potntial for asst bbbls. Howvr, with a modrat slowdown xpctd in Asia-Pacific and world conomic rcovry, ths inflows ar likly to slow.

FIguRe 4. Real GDP Growth Rates, 2008–2010F

(%)

-15%

-10%

-5%

0%

5%

10%

15%

JapanNew Zealand AustraliaHong Kong

South

KoreaSingaporeTaiwanThailandIndonesiaIndiaChina

Change

from

Prior

Year

(%)

Emerging Asiaa Industrialized AsiaaNewly Industrialized Asiaa

Growth 2008−2009

7.4%

Growth 2009−2010F

8.9%

Growth 2008−2009

-0.9%

Growth 2009−2010F

6.6%

Growth 2008−2009

-4.2%

Growth 2009−2010F

2.8%

9.6 9.9

5.1

6.87.8

6.0

4.5

5.6

2.5

0.71.4

2.3 2.2 2.42.9 2.9 2.8

5.65.9

0.2

8.58.0

3.2

-2.3 -1.9 -2.0 -2.8

1.3

-0.6-0.6-1.2

-5.2

8.6

20092008 2010F

a Composition of “Emerging Asia,” “Newly Industrialized Asia” and “Industrialized Asia” is as per International Monetary Fund definitionsSource: The Economist Intelligence Unit, June 2010

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 10/32

2010 AsiA-PAcific WEALTH rEPorT10

2009 in rEviEW: AsiA-PAcific sHoWEd rEsiLiEncE in THE fAcE of THE GLobAL doWnTurn

National Savings Rate Dipped Slightly

In 2009, national savins14 as a prcnta of gDPdippd to 38.3% from 38.5% in Asia-Pacific xcldin Japan,15 drivn by incrasd ovrnmnt xpnditrs tidto th fiscal-stimls masrs implmntd to stav off dama from th conomic crisis.

Th dclin was only marinal in Asia-Pacific as a whol,and th rion still had th world’s hihst nationalsavins rat. Howvr, th dclin in national savins wasmor sinificant in Indstrializd Asia (-16.5%) than thdclins in emrin Asia and Nwly IndstrializdAsia. This cold sinal fwr fnds will b availabl forftr invstmnt in thos conomis.

Growth in Private Consumption Slowed in 2009

Th rat of rowth in privat consmption slowd

across most of Asia-Pacific in 2009, bt th aratlvl of privat consmption still ros from 2008,larly bcas ains in China and India mor thanoffst waknss lswhr.

Th otriht lvl of privat consmption16 ros touS$4.1 trillion from uS$3.9 trillion in Asia-Pacificxcldin Japan, bt th rion still only acconts forabot 14% of lobal privat consmption. Nvrthlss,this was th scond straiht yar of halthy ains inprivat consmption in th rion, hlpd by rsilintconsmr confidnc. In fact, consmr confidnc was

srin in Asia-Pacific by th scond half of 2009,17 boyd in part by optimism ovr th mploymntotlook. Bsinss and consmr sntimnt has contindto thriv sinc, and consmr confidnc in India andChina has bn spcially stron, hlpin to boost bothrtail sals and bsinss spndin.

Ral ovrnmnt consmption manwhil ros 10%, fromuS$1.0 tril lion in 2008 to uS$1.1 trill ion18 in Asia-Pacificxcldin Japan, as ovrnmnts in th rion incrasdthir fforts to stimlat rowth and boost th financialsystm whil th lobal conomy soht to riht itslf

from th ffcts of th financial crisis.

ASIA-PACIFIC LED WORLDWIDEREBOUND IN MARKET AND OTHERDRIVERS OF WEALTH

In 2009, Asia-Pacific markt drivrs of walth raind

sinificant rond aftr hfty losss in 2008. Major asstclasss, spcial ly qitis and ral stat, rbonddsharply. Th followin wr amon th notabl marktdvlopmnts in Asia-Pacific in th last yar or so:

Equity-market capitalization surged 73.6% to

US$16.0 trillion in 2009,19 rbondin from a 53.5%dclin in 2008 (s Fir 5) as invstors rtrnd toth markts amid wanin financial-crisis fars. Th2009 Asia-Pacific rbond was far stronr than th47.1% incras in lobal qity-markt capitalization,and was ld by China, Indonsia and India. In fact,mrin markts in th rion showd stllar rowth

as a whol (34.1%20), and vn manad to mak ainsin th first half of 2009 whn mor dvlopd marktshad yt to rviv. Th pac of that rowth slowdsomwhat in th scond half of 2009 whn dvlopdmarkts startd to rbond mor stronly, bt Asia-Pacific qity-markt capitalization had nvrthlssrtrnd to nar pr-crisis lvls by th nd of 2009, whil lobal markts had rcopd only thr of thfiv yars’ worth of losss thy sffrd in 2008.

Housing prices recovered across much of Asia-

Pacific aftr incrrin havy losss drin th crisis. Th stronst ains wr in Hon Kon, whrhosin prics ros 20.8% in 2009,21 drivn partly by amassiv inf lx of byrs from mainland China. InChina itslf, hosin prics and sals ot a dirct boostfrom ovrnmnt action to rvrs many of th policis(.., on taxation and lndin) that it had sd torstrain th markt whn it was ovrhatin in 2007.Incrasd invstmnt dmand also hlpd boost pricsin China, as wll as in Taiwan, which postd an 18.3%ain22 in hosin prics. Astralia a lso saw asinificant rbond in hosin prics, d to incrasdinvstor activity and rnwd intrst from byrs of

scond and third homs.23

14 National savings = GDP – [pr ivate consumption + government consumption]

15 The Economist Intelligence Unit, Regional Data, June 2010

16 Ibid

17 MasterCard Worldwide Index of Consumer Confidence,

http://www.masterintelligence.com, accessed May 2010

18 The Economist Intelligence Unit, Regional Data, June 2010

19 World Federation of Exchanges, market capitalization statistics,http://www.world-exchanges.org/statistics, accessed March 2010

20 MSCI Global Indexes for Select Regions, www.mscibarra.com, January 1, 2009 -December 31, 2009

21 “Global Property Guide,” variation of monthly prices adjusted for i nflation forDecember 2008-December 2009

22 Ibid23 Australian Bureau of Statistics

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 11/32

2010 AsiA-PAcific WEALTH rEPorT 11

2009 in rEviEW: AsiA-PAcific sHoWEd rEsiLiEncE in THE fAcE of THE GLobAL doWnTurn

Th Dow Jons global Slct ReIT Indx ndd th yar with total rtrns of 32.2%, with Sinapormrin as th rion’s top prformr with a ain of 83.7%.24 Asia-Pacific ral stat (commrcial andrsidntial) is xpctd to show sstaind rowth in2010 in a rvival of dmand. Capital inflows and looscrdit conditions boostd sals and prics across thrion drin Q1 2010, spcially in th Nwly Indstrializd conomis and Vitnam.25 In China’slar citis, morovr, avra proprty prics inFbrary 2010 wr alrady 30% hihr than a yar

arlir.26

Manwhil, th volm of commrcial ral-stat invstmnts transactd in Asia-Pacific incrasdby 37% from uS$28.2 billion in Q4 2009 to uS$38.6billion in Q1 2010, with th main invstmnt marktsof Japan, Astralia and Sinapor witnssin incrasdinvstmnt.27 Nonthlss, xprts ar watchin thissctor with som cation.

Asia hedge funds posted returns beyond the global

average. Th erkahd Asian Hd Fnd Indxdlivrd an annalizd rtrn of 26.7% in 2009,sinificantly mor than th global Hd Fnd Indxrtrn of 19.7% for th sam priod.28 growth in thnmbr of Asia-Pacific hd fnds has bn somwhatconstraind to dat by rlatory and othr barrirs, btth sprior prformanc of ths fnds, and th risinintrst in mrin markt invstmnt in nral, islrin mor capital. This trnd is xpctd to acclratas rlators incras ovrsiht of hd fnds in

dvlopd markts and fnd manars sk ratrxposr to th Asia-Pacific rion.29

The U.S. dollar remained volatile during the year. globally, invstors boht dollars in Q1 2009 amiddmand for a saf havn whil stocks rmaind indclin. By April, howvr, invstors ban to mov

24 Dow Jones, Dow Jones Global Select REIT Index, http://www.djindexes.com, accessed February 4, 2010

25 “Emerging Stronger from the Crisis,” World Bank East Asia and Pacific Economic Update 2010, Volume 1

26

Ibid27 David Green-Morgan, DTZ Res earch, “Investment Market Update As ia-Pacific, Q1 2010”

28 Eurekahedge Hedge Fund Indices, http://www.eurekahedge.com/indices/default.asp, accessed May 10, 2010

29 Saeed Azhar and Parvathy Ullatil, “Seeking Less Scrutiny, Hedge Funds Flock to Asia,” Reuters, May 17, 2010

FIguRe 5. Percentage Change in Equity-Market Capitalization, 2007–2009 (by Country)

(%)

JapanNew ZealandThailandHong Kong

South

KoreaSingapore AustraliaTaiwanChinaIndiaIndonesia

-100%

-50%

0%

50%

100%

150%

117.6

-53.4

-64.1 -60.3 -58.1

-28.1

102.9 100.9

84.4 82.1 81.677.3

73.5 71.6

46.7

6.1Change

since

Prior

Year

(%)

Asia-Pacic witnessed average

growth of 73.6% in equity-marketcapitalization in 2009

Asia-Pacic witnessed an average

drop of 53.5% in marketcapitalization in 2008

Average 2008

-53.5%

Average 2009

73.6%

-49.0-50.9 -49.9 -47.7-46.6-46.3

2008−20092007−2008

Source: World Federation of Exchanges, June 2010

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 12/32

2010 AsiA-PAcific WEALTH rEPorT12

30 Ozforex, historical data for select curre ncies against the U.S. dollar,http://www.ozforex.com.au, access ed Februar y 2, 2010

31 “Regional Economic Outlook: Asia and Pacific: Leading the Global Re covery,Rebalancing for the M edium Term,” International Monetary Fund, April 2010

32 Dow Jones, Dow Jones Commodity Index (DJUBS), http://www.djindexes.com,accessed January 29, 2010

33 MSCI Commodity Index Total Returns, http://www.mscibarra.com, accessedJune 1, 2010

34 Carolyn Cui, “Metal Rally Has Legs to Keep Running,” Wall Street Journal,January 3, 2010

35 Kitco, London PM FIX Prices, http://www.kitco.com, accessed February 11, 2010

36 Ibid

37 “Regional Economic Outlook: Asia and Pacific: Leading the Global Re covery,Rebalancing for the Me dium Term,” International Monetary Fund, April 2010

38 Kitco, London PM FIX Prices, http://www.kitco.com, accessed February 11, 2010

39 World Gold Council, “Gold D emand Trends: Fourth Quarter and Full Year 2009,”February 17, 2010

40 World Gold Council, “Gold I nvestment Digest,” April, 2010

41 Ibid

42 U.S. Energy Information Administration, Cushing, OK WTI Spot Price FOB,http://www.eia.doe.gov, acce ssed January 28, 2010

43 “Emerging Stronger from the Crisis,” World Bank East Asia and Pacific Economic Update2010, Volume 1

away from th dollar as cntral banks arond th worldstppd p fforts to spport thir conomis. Thdollar’s slid was compondd by th rlativ waknssof th u.S. conomic rcovry. By Q3 2009, somcontris incldin Astralia wr vn raisin intrstrats, whil th u.S. Fdral Rsrv maintaind ky

rats nar zro. encorad by th availability of chapmony, invstors borrowd dollars to by stocks, old,commoditis and othr crrncis. At th nd of th yar, th dollar was down aainst most majorcrrncis, spcially th Brazilian ral (-25.2%),Canadian dollar (-14.3%) and British pond (-9.9%).30 Within Asia-Pacific too, most crrncis (with thxcption of th yn, Vitnams don and Hon Kondollar) apprciatd aainst th u.S. dollar as rnwdcapital flows wr accompanid by a sharp drop in yilds on local-crrncy bonds in 2009.31

Commodities posted strong gains in 2009, though

they did not recoup all the 2008 losses. Th Dow Jons-uBS Commodity Indx (DJuBS) ros 18.7% in2009 aftr a 36.6% drop in 2008.32 Th 2009commodity rally was drivn by mtals as hops of alobal conomic rcovry sprrd dmand, and fars of inflation ncorad hdin. Th MSCI All Contry Asia xcldin Japan Commodity Prodcrs Indxpostd 89.6% rtrn for th yar.33 globally, copprrcordd ains of 139% as indstrial dmand soard,and ndd th yar at uS$3.3275/pond,34 which wasarond 18% lss than th hihs of 2008. Silvr prics

ros stadily to nd 2009 with a ain of 57.5%.35

Strondmand from atomakrs incrasd lobal dmand forplatinm, which is sd in catalytic convrtrs, andlad, which is sd in car battris. Platinm pricsros 63.3% to nd th yar at uS$1,466/oz,36 and ladmor than dobld in pric to uS$2,416/mtric ton.In Asia-Pacific in particlar, stron commodity pricsand robst dmand in Q1 2010, spcially fromChina,37 is likly to driv incrasd privat invstmntin rsorc-rich conomis sch as Astralia, Indonsiaand Malaysia.

Gold prices soared in 2009, fueled by broad investor demand. gold prics incrasd stadily throhot2009, ristrin a total incras of 26.9% for th yar. 38 Th pric of old pakd in arly Dcmbr atuS$1,212/oz, bt droppd to uS$1,104/oz at th nd of th yar amid profit-takin. Th challnin conomic

conditions impactd indstrial and jwlry dmand forold, which droppd 16.0% and 20.0% rspctivly in2009.39 Howvr, old saw hfty byin lobally by fnds and individal invstors alik, skin insrancaainst possibl inflation and a dclinin dollar.Notably, th cntral banks of China and India wr ntbyrs of old in 2009 aftr dcads of sllin. China,th world’s scond larst consmr of old in 2009, isxpctd to incras its old consmption vn mor inth nxt fw yars, drivn by nar-trm inflationary xpctations and risin incom lvls.40 Jwlry dmandfrom India was p 27% from a yar arlir in Q4 2009

at 137.8 mtric tons.41 gold prics, which rmaindstron in th first half of 2010, cold fac downwardprssr latr in th yar, d to xpctations thatintrst rats will ris arond th world.

Oil prices ndd 2009 at uS$79.4/barrl, a ain of 78.0% on th yar.42 Prics mor or lss trackd thlobal conomy, fallin at th binnin of th yarbfor movin hihr as fars abot th financial crisisban to as. Prics also ros on xpctations of lon-trm dmand, spcially from mrin marktslik China. Howvr, th otlook for that dmand isnot crtain. China, for instanc, is on of th world’slarst consmrs of crd oil, bt it is not clar xactly what prcnta of its total oil dmand is bin divrtdinto rsrvs. China is also makin lar invstmntsinto altrnativ nris so as to rdc its ftrdpndnc on oil. Abot a third of th invstmnt-basd stimls packa in China drin 2009 was for“rn invstmnts”.43

2009 in rEviEW: AsiA-PAcific sHoWEd rEsiLiEncE in THE fAcE of THE GLobAL doWnTurn

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 13/32

2010 AsiA-PAcific WEALTH rEPorT 13

44 “Global Employment Trends – Up date,” International Labour Organisation, January 2010

45 The Economist Intelligence Unit, April, May and June 2010

46

Ibid47 Ibid

48 As measured by the Economist Intelligence Unit’s Business Environment Rankings (BER)

ASIA-PACIFIC GROWTH IS LIKELYTO OUTPACE GLOBAL ECONOMYIN 2010 AND 2011

Asia-Pacific conomic rowth is likly to otpac WorldgDP xpansion in 2010 and 2011, as fairly rsilint

domstic dmand and intra-rional trad hlp to offstonoin waknss in xports to dvlopd conomis thatar still rcovrin aftr th crisis.

China is xpctd to concntrat on rbalancin itsconomy ovr th nxt fw yars by focsin on boostinth srvic sctor and privat consmption. Chinaannoncd in mid-2010 it was makin its xchan-ratpolicy mor flxibl, bt it is too soon to say how widly th yan will b allowd to mov aainst othrcrrncis, and what th impact miht b on domsticspndin powr and consmption.

Othr contris sch as India, Indonsia andSinapor ar likly to prioritiz capital invstmntand skills dvlopmnt to bttr position thmslvsto boost xports.

employmnt lvls in Asia-Pacific ar also xpctd torbond. Joblss rats in th rion rmain hihr thanbfor th crisis, bt ar still lowr than th lobalavra. ultimatly, data ar xpctd to show 2009nmploymnt rats of 4.4% for east Asia, 5.6% forSothast Asia and th Pacific, and 5.1% for SothAsia—lvls blow initial forcasts.44

Arat indicators asid, not all of Asia-Pacific’sconomis will row in th sam way or at th sam pac.In 2010, emrin Asia and Nwly Indstrializd Asiaar xpctd to xprinc gDP rowth rats of 8.9%and 6.6% rspctivly, in lin with pr-crisis lvls, withemrin Asia—ld by China and India—sparhadinth rion’s conomic rowth and xpansion of indstrialprodction. Indstrializd Asia manwhil is likly torow jst 2.8% drin 2010, a markdly slowr pac than

th othr smnts within Asia-Pacific, bt in lin withothr matr conomis arond th lob.

China’s ral gDP is xpctd to xpand 9.9% in 2010,45 th fastst rat of rowth in th rion. Howvr, thatxpansion is bin boostd by th xtnsiv fiscalstimls implmntd by th ovrnmnt in2009—which fld infrastrctr invstmnt and

hlpd to rviv xpnditrs on proprty dvlopmnt. That xpansion was initially fld too by montary xpansion, bt China has bn radally tihtninmontary policy sinc arly 2010, and contindmontary tihtnin is likly to slow down th rat of conomic rowth. In 2011, China’s rapid gDP rowth is

xpctd to slow a littl to 8.3%.46 goin forward, Chinais xpctd to focs on rbalancin its conomy by boostin th srvic sctor and drivin privatconsmption.

By contrast, India’s rowth is xpctd to kpacclratin, with gDP forcast to xpand 8.1% in 2011aftr a ain of 7.8% in 2010,47 d to th sinificantxpansion of privat consmption and invstmnt. Infact, its cntral bank, th Rsrv Bank of India (RBI), isxpctd to tihtn montary policy prorssivly in 2010to mak sr its conomy dos not ovrhat as th lobal

financial crisis rcds.

Th Asia-Pacific bsinss otlook nrally rmainspromisin, makin th rion a likly mant for lobalcompanis and privat invstmnt. And whil thnvironmnt in som havily trad-xposd Asia-Pacificconomis lik Sinapor and Hon Kon looks lss rosy for ftr invstmnt than in th pr-crisis yars, thotlook for China and India is spcially briht. Forinstanc, China’s bsinss otlook for 2009–2013 shows ah improvmnt ovr 2004–2008,48 rflctin thrlativ strnth of th contry’s ndrlyin conomy.

ultimatly, th financial crisis has dmonstratd thintrdpndnc of th world’s conomis and shownthat Asia-Pacific is not immn to conomic waknss inothr parts of th rion and world. Howvr, Asia-Pacific has provd mor rsilint than othr rions andis xpctd to contin to far wll as part of th lobalrcovry spportd by robst privat dmand, stronintra-rional trad and favorabl consmption lvls— which shold hlp to offst waknss in xports.

2009 in rEviEW: AsiA-PAcific sHoWEd rEsiLiEncE in THE fAcE of THE GLobAL doWnTurn

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 14/32

14 2010 AsiA-PAcific WEALTH rEPorT

ASIA-PACIFIC HNWIS HADMORE THAN HALF THEIR ASSETSIN EQUITIES AND REAL ESTATE BYEND 2009

Asia-Pacific HNWIs had 53% of thir assts in ithrqitis or ral stat by th nd of 2009 (s Fir 6) asa rslt of both incrasd invstmnt and asstapprciation drin th yar. This broht allocationsback to pr-crisis lvls and rvrsd th crisis-drivn

fliht to cash-basd instrmnts. In fact, th strnth inth markts and conomis of Asia-Pacific—and itsmrin markts in particlar—mant th asstallocations of th rion’s HNWIs had shiftd tanibly by th nd of 2009.

Th major shifts incldd th followin:

eqitis accontd for 27% of all Asia-Pacific HNWI

assts by th nd of 2009, p from 23% in 2008, asth rion’s boomin markts attractd invstorsand boostd asst vals. Th qity allocation,howvr, was still blow th avra of 29% amonHNWIs lobally.

Th shar of assts ddicatd to ral stat rivald

qitis—at 26%, p from 22% and considrably abovth 18% lobal avra—as th rion’s proprty boomncorad byin and inflatd prics.

Cash-basd holdins droppd to 22% from 29%, bt

that lvl was still abov th 17% lobal avra.Asia-Pacific HNWIs tnd to favor liqid assts whnth conomic and financial nvironmnt is ncrtain.

Asia-Pacific HNWI investors ended 2009 with 27% of their assets held in equities, up from 23% a year

earlier, as they headed back into the equity markets and equity-asset values rose, especially in emergingmarkets. The allocation to real estate also rose among Asia-Pacific HNWIs, to 26% from 22%, as real-estate prices recovered across major markets in the region.

The proportion of Asia-Pacific HNWI assets allocated to cash-based instruments dropped to 22% in

2009 from 29% in 2008. That level was still ar higher than the 17% global average, as is consistent withlong-term behavior, but the decline relected the unwinding o some sae-haven cash holdings acquired at theheight o the crisis. Fixed-income investments accounted for only 20% of assets, unchanged rom 2008.

This was ar below the 31% global average, but consistent with long-term trends.

Asia-Pacific HNWIs remained primarily invested in their home regions in 2009, though the proportion

invested outside the region rose to 36% from 33% a year earlier. Home-region allocations in China andIndia stood at 85% and 82% o total assets respectively, amid surging growth in those markets and economies.Japanese HNWIs, by contrast, maintained quite geographically diversiied portolios.

By 2011, Asia-Pacific HNWIs’ allocations to equities and fixed-income instruments are expected to

increase and relative holdings of cash-based and real-estate holdings are expected to decline as HNWIsseek to rebalance their portolios. Home-region allocations are expected to decline as Asia-Paciic HNWIspursue returns and opportunities elsewhere, especially in the emerging markets o Latin America and Arica.

Asia-Pacific

HNWIs FavordAsia-Pacific HNWIs Favord eqitisand Ral estat in Portfolios in 2009

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 15/32

2010 AsiA-PAcific WEALTH rEPorT 15

AsiA-PAcific HnWis fAvorEd EQuiTiEs And rEAL EsTATE in PorTfoLios in 2009

Asia-Pacific HNWIs had only 20% of thir holdins in

fixd-incom instrmnts in 2009. That is mch lowrthan th 31% lobal avra, bt is not nsal asmrin markts sch as India hav ndrdvlopdbond markts, so thr ar fwr invstmnt options

than in mor dvlopd markts.

HNWIs’ Exposure to Equities and Real EstateRose as Those Markets Rallied

Th proportion of HNWI assts hld in qitis jmpdto 27% in 2009 as qity-markt capitalization aindlobally and srd in hom-rion markts likChina and India (see “2009 in Review” ). This allocation was hihr than th corrspondin 2007 fir whn thcrisis had not flly mrd. In Japan, Taiwan andIndonsia, howvr, HNWIs maintaind rlativly low qity allocations of 19% or 20%. Ths markts hav wll-stablishd bond markts, and HNWIs havtraditionally favord fixd-incom and ral-statinvstmnts ovr qitis. This hld tr in Taiwanand Indonsia in 2009 vn thoh th domsticstock markts soard. In Japan, th stock marktrtrnd a tpid 6.1% in 2009, so did not draw ndbyin intrst.

Th qity allocation was hihst amon HNWIs inChina (s Fir 7), whr 42% of all HNWI assts wr tid p in stocks at th nd of 2009, and in India(32%). HNWIs from China hav bcom incrasinly drawn to domstic qitis markts, which hav

consistntly otprformd lobal markts, and thy incrasd thir allocations to qitis in 2009 by 13prcnta points. That was th larst incras amonHNWIs in any Asia-Pacific markt. India’s HNWIs,manwhil, wr drivn to invst in qitis by risinasst vals and sins of ndrlyin conomic rowth.India’s gDP rw narly 7% in 2009, whil th combindmarkt capitalization of th National and th Bombay Stock exchans mor than dobld to nd 2009 atuS$2,531.3 billion.

Asia-Pacific ultra-HNWIs wr slihtly mor havily

invstd in qitis (30%) than th rion’s HNWIsovrall, which is consistnt with that rop’s tndncy toprs risk and rtrns mor arssivly ivn thirratr lvls of disposabl incom.

FIguRe 6. Breakdown o Asia-Paciic HNWI Financial Assets, 2006–2011F

(%)

0

25

50

75

100

2011F2009200820072006

24% 26% 23% 27%

20%

22%

26%

5% 8%

18%

19%

25%

31%

20%

29%

22%

6%

21%

25%

20%

8%

15%

24%

29%

8%

%

Equities

Fixed Income

Cash / Deposits

Real Estateb

Alternative Investmentsa

a Includes structured products, hedge funds, derivatives, foreign currency, commodities, private equity and venture capitalb Comprises commercial real estate, real estate investment trusts (REITs), residential real estate (excluding primary residence), undeveloped property, farmland and “other”Note: Percentages may not total 100% due to roundingSource: Capgemini/Merrill Lynch Financial Advisor Surveys, March 2007, April 2008, March 2009 and March 2010

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 16/32

2010 AsiA-PAcific WEALTH rEPorT16

AsiA-PAcific HnWis fAvorEd EQuiTiEs And rEAL EsTATE in PorTfoLios in 2009

HNWIs’ ral-stat holdins also jmpd in 2009. Of allAsia-Pacific HNWI assts, 26% was hld in ral stat in2009, hadin back toward pr-crisis lvls as th rion’sproprty markts contind or rnwd thir ains.

Mor spcifically: Of all ral-stat assts, th shar ddicatd to

rsidntial ral stat49 ros slihtly to 60% from 59%amon HNWIs from Asia-Pacific xcldin Japan. That prcnta is 53% whn incldin Japan. Formany in th rion, rsidntial proprty rmains ahihly attractiv invstmnt bcas tiht spply andstron dmand prsist in most prim locations. Thprics of lxry rsidncs in Asia-Pacific rw by 17.1%50 in 2009, with prics in citis lik Hon Kon,Shanhai and Bijin srin by mor than 40%51 torach rcord lobal lvls.52 China’s HNWIs spcially

favor rsidntial ral stat, which acconts for 70% of all thir ral-stat holdins.

Commrcial ral stat is stadily ainin poplarity in

th rion, bt th allocation to this catory of ral stat(24% amon HNWIs in th rion as a whol) rmainsshort of th 27% lobal avra. Th allocation is hihst(58%) amon HNWIs from Soth Kora for a varity of rasons spcific to that markt, incldin landlord-frindly lasin systms and stabl vacancy rats.

Invstmnt in ral stat invstmnt trsts (ReITs)

rmains low across Asia-Pacific, bcas th markt isstill vry small and th prodct is not availabl in allmarkts. In fact, Japan, Sinapor and Hon Kontothr accont for 91% of total ReIT-markt

capitalization in th rion, and Japans HNWIs’allocation to ReITs is by far th hihst in Asia-Pacific(23% of all ral-stat holdins). Howvr, ReITinvstmnt is xpctd to broadn in th ftr bcasothr contris—incldin boomin China—arprparin to lanch ReITs. govrnmnts hop ReITs will as th pward prssr on hosin prics by providin an altrnativ to dirct ral-stat invstmnt,and Asia-Pacific invstors ar bcomin mor willin toconsidr ths typs of asst classs.53 Asia-PacificReITs also achivd stllar rtrns in 2009 asconomic conditions improvd and xpansionary crdit

conditions spportd ral-stat markts. Th S&PAsia-Pacific ReIT Bnchmark Indx ros 36.0% in2009, marinally mor than th S&P global ReITIndx, which aind 33.7%.54

FIguRe 7. Breakdown o Asia-Paciic HNWI Financial Assets, 2009 (by Market)

(%)

0

25

50

75

100

TaiwanSouth

Korea

SingaporeMalaysiaJapanIndonesiaIndiaHong KongChina Australia

25%

42%

23%

23%

23%

34%37%

1%

32% 30%19%

19%

19%

19%

16%

16%

33%

25%

25%

25%21% 20%

26%

26%

23%

4%

13%

22%22%

22%

22%

22%

10%8%

18%

24%

6%

18%

29%

29%

12%

15%

27%

5%

14%

40%

4% 4% 5%3%

%

Equities

Fixed Income

Cash / Deposits

Real Estateb

Alternative Investments a

a Includes structured products, hedge funds, derivatives, foreign currency, commodities, private equity and venture capitalb Comprises commercial real estate, real estate investment trusts (REITs), residential real estate (excluding primary residence), undeveloped property, farmland and “other”Note: Percentages may not total 100% due to roundingSource: Capgemini/Merrill Lynch Financial Advisor Surveys, March 2007, April 2008, March 2009 and March 2010

49 Not including primary residence

50

Knight Frank’s Prime International Residential Index51 Knight Frank, “The Wealth R eport 2010,” http://www.knightfrank.com

52 Kay Coughlin, President and CEO, Christie’s Great Estates, interview by Capgemini, April 2010

53 “China Poised to Add REITs to Cool Down Simmering Property Market,” China Daily, April26, 2010

54 S&P Indices Market Attributes, Global Property and REIT (Q4 2009)

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 17/32

2010 AsiA-PAcific WEALTH rEPorT 17

AsiA-PAcific HnWis fAvorEd EQuiTiEs And rEAL EsTATE in PorTfoLios in 2009

55

“Rupiah Is Asia’s Top Performing Currency for 2009 as Growth Dr aws Investors,”Jakarta Globe, January 1, 2010

56 “Asia Set to Grab a 5th of Global Hedge Fund Flows,” Reuters, March 1, 2010,http://www.reuters.com/article/idUSTRE6201HJ20100301

Asia-Pacific HNWIs’ Holdings of AlternativeInvestments Remained Limited

Holdins of altrnativ invstmnts wr littl chandamon Asia-Pacific HNWIs at 5% of th aratportfolio in 2009 vs. 6% in 2008. This prcnta is mch

th sam as th avra amon HNWIs lobally, btAsia-Pacific holdins tnd to b concntratd instrctrd prodcts and forin crrncy. Othr optionssch as vntr capital, privat qity and vntr capitalfnds ar rlativly fw in Asia-Pacific, bcas rlationhas so far slowd thir dvlopmnt. Many invstors aralso nfamiliar or ncomfortabl with th associatd risksof ths altrnativs, so tnd not to favor thm.

Strctrd prodcts wr th most poplar altrnativ-invstmnt catory, accontin for 23% of all altrnativinvstmnts amon HNWIs in Asia-Pacific xcldin

Japan. Th rlativ holdins ar hihr (33%) amonHNWIs in Japan, whr intrst rats hav bn low foran xtndd priod, ncorain invstors to prs a varity of options with potntially hihr rtrns.

Forin crrncy was also a poplar altrnativinvstmnt for Asia-Pacific HNWIs, which had 24% of altrnativ-invstmnt holdins in that catory by thnd of 2009, compard with th lobal HNWI avra of jst 13%. That allocation, which nrally rflcts

attmpts to hd aainst local crrncy flctations, wassharply hihr amon HNWIs from Indonsia (46%), whr th rpiah otprformd vry othr Asiancrrncy to ain 16% in 2009 aainst th u.S. dollar.55

Hd-fnd allocations wr also far lowr amon

Asia-Pacific HNWIs (14% of all altrnativ invstmnts)than th lobal HNWI avra (27%). Invstors havfwr hd-fnd choics in Asia-Pacific bcas of varios rlatory and othr barrirs, and th rioncrrntly acconts for lss than 10% of total lobalhd-fnd assts. Howvr, xistin hd fnds in thrion ros narly 40% in 2009, clarly otpacin throwth in u.S. and eropan hd fnds.56 If thisprformanc is sstaind, Asia-Pacific HNWIsmiht wll incras thir allocations to hd fndsin th ftr.

Asia-Pacific HNWIs Still Favored Home-RegionInvestments in 2009

Asia-Pacific HNWIs concntratd 64% of all thirinvstmnts in thir hom rion in 2009, bt thy nvrthlss soht nw opportnitis lswhr too,spcially in th mrin markts of Latin Amrica andth Middl east. As a rslt, hom-rion allocationsdroppd by 3 prcnta points (s Fir 8 for by-markt dtail).

FIguRe 8. Breakdown o Asia-Paciic HNWI Geographic Asset Allocation, 2009 (by Market)

(%)

0

25

50

75

100

TaiwanSingaporeSouth

Korea

MalaysiaJapanIndonesiaIndiaHong KongChina Australia

%

71%

18% 14%

30%

13%

12%10%

18%

5%5%

9% 9% 9%9%

72%

85%

8% 8%8% 8%

15%

6%4% 4% 4%

4%

4%

68%

82%

71%

43%

82% 81% 80%

1%

1%

1%1%

1%

3% 3%

1% 1% 1%1%

2%

2%

2%3%

2%2%

2% 2%

Africa

Middle East

North America

Europe

Asia-Pacic

Latin America

Note: Percentages may not total 100% due to roundingSource: Capgemini/Merrill Lynch Financial Advisor Surveys, March 2007, April 2008, March 2009 and March 2010

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 18/32

2010 AsiA-PAcific WEALTH rEPorT18

Real estate remains a major asset class or Asia-

Paciic HNWIs across the region. Indeed, by the endo 2009, Asia-Paciic HNWIs held 26% o theirportolios in real-estate assets, ar above the globalaverage o 18%, and up rom 22% a year earlier. Whyis this so? The recovery in real-estate prices certainlyueled investment in 2009, but that was only part othe dynamic.

Investment options in Asia-Paciic are more limitedthan in mature North American and Europeanmarkets, so HNWIs requently pursue real estate—both bricks and mortar (“direct” investments) andother real-estate assets—as an important orm o

inancial investment. Also, real estate provides Asia-Paciic HNWIs with an opportunity to invest inamiliar markets, while still diversiying their holdings. As a result, domestic and home-region buyersdominate Asia-Paciic real-estate investment, unlikeother regions o the globe in which one may see moreoverseas real estate investors.

Asia-Paciic real estate was not immune to the eectso the global economic downturn, especially in the irsthal o 2009. However, prices recovered sharply in thesecond hal as economic conditions improved and

many governments in the region pursued expansionary

policies to keep borrowing rates low. Additional iscalmeasures in the orm o stimulus spending alsounneled monies into property and inrastructureacross the region, supporting real-estate prices.

In act, some property prices escalated so quickly,especially in China, that observers have voicedconcern that a housing bubble may be looming.Others, however, argue rising prices are not likely toturn into a ully ledged bubble as Asia-Paciicgovernments tend to intervene directly in their real-estate markets. In act, some governments—China andSingapore in particular—have already acted to cool

prices (see below).

More generally, though, the market conditions or Asia-Paciic real estate depend on a variety o actors,rom macroeconomic and political conditions toregulations and capital costs. Accordingly, HNWIspreer one type o real estate over another in any givenmarket largely because o domestic market conditions,such as interest rates and regulation, and speciics likeleasing laws. In act, individual real-estate markets in Asia-Paciic can dier markedly rom one another,creating dierent levels o investment interest.

Ral estat Was a Prfrrd FinancialInvstmnt for Asia-Pacific HNWIs in 2009

Amon hom-rion invstmnts, HNWIs fromAsia-Pacific xcldin Japan invstd 36% in China, 19%in Hon Kon and 10% in India, attractd by th arly rbond in thos qity markts in 2009. Japan’s HNWIscontind to favor domstic invstmnts (63% of allhom-rion holdins), bt wr th most oraphically

divrsifid HNWIs in th rion. Asia-Pacific HNWIs’allocations to th dvlopd markts of North Amricaand erop ros only slihtly—p jst 1 prcnta pointto 28% of all invstmnts—amid th slow conomicrbond in thos rions.

By 2011, Asia-Pacific HNWIs’ Allocations toEquities and Fixed-Income Are Likely to Rise

Lookin ahad to 2011, allocations to qitis andfixd-incom invstmnts ar xpctd to ris amonAsia-Pacific HNWIs to 31% and 25% rspctivly of all

holdins. This incras will likly b fld by stron

conomic rowth in th rion and a stron dsir amonHNWIs to rbalanc thir portfolios. Howvr, thrlativ shar of ral-stat holdins is xpctd todclin, by 8 prcnta points to 18%, as HNWIs look to liqidat som of thir holdins and tak profits aftrth rn-p in prics.

Hom-rion allocations ar also xpctd to dclin asAsia-Pacific HNWIs prs rtrns and opportnitislswhr, spcially in th mrin markts of LatinAmrica and Africa. For instanc, invstmnts in LatinAmrica ar xpctd to ris to 9% of all holdins by 2011 from 6% in 2009. Allocations to th dvlopdrions of North Amrica and erop ar xpctd tormain littl chand from 2009 lvls (19% and 9%rspctivly) as Asia-Pacific HNWIs sk to maintaindivrsifid portfolios.

AsiA-PAcific HnWis fAvorEd EQuiTiEs And rEAL EsTATE in PorTfoLios in 2009

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 19/32

192010 AsiA-PAcific WEALTH rEPorT

FIguRe 9. Asian Real Estate Markets – Levels o Investment Interest, 2009

0

0%-20%-40%-60% 20% 40% 60%

10

20

30

40

50

R e a l - E s t a t

e I n v e s t m e n t I n t e r e s t S c o r e

Avg. Annual Real-Estate Investment Returns (%), 2004−2009

India *

Australia

Japan

Hong Kong

Malaysia

Singapore

Thailand

China

Taiwan

Indonesia

Markets with High Investment

Interest Score but lower

real-estate investment returns

Markets with High Investment

Interest Score and higher

real-estate investment returns

The nancial crisis has

hit hard in Japan's

developed economy,

undermining real-estate

development and

buying interest.

Taiwan’s real-estate investment

interest is expected to decline

after the recent run-up,

especially as the government

seeks to take measures to

check rising prices.

The Malaysian

government is intervening

to support and expand

investment in real-estate,

likely increasing future

investment interest.

China’s government is

already intervening to cool

frothing real-estate prices,

likely leading to a decline

in the investment interest

in the future.

The past three years’

average annual return for

India has been considered

in this report. The effect ofthe nancial crisis has

shifted India’s average

returns to the extreme left

side. India would have

fared relatively better, on a

ve-year average return

basis, shifting it to the right.

Note: (a) *Average annual return for India has been considered for last three years due to unavailability of data; (b) Average annual real-estate returns (%) for various Asian marketsas per the S&P Global Property IndexSource: Capgemini analysis, 2010; S&P Global Property Index, “S&P Indices Market Attributes, Q4 2009”

REAL ESTATE MARKETS IN ASIA-PACIFIC DISPLAY DIFFERENTLEVELS OF INVESTMENT INTEREST

Figure 9 oers a graphical representation o theinvestment interest and returns in dierent Asia-Paciic

real-estate markets over the past ive years. We scoredthe strength o various actors that drive investmentinterest in real estate, including product and capitalavailability, government policies, regulations andmacroeconomic actors.

Figure 9 shows the relative size o real-estate marketsin Asia-Paciic (the size o the “bubbles” relectsmarket capitalization), the level o interest in thosemarkets and the returns (y and x axis respectively).Not surprisingly, Hong Kong, Japan, Australia andChina experienced the greatest level o interest in realestate investment, nonetheless with distinct

dierences among markets. In taking a closer look atsome key markets, we see the ollowing:

In China, the 2009 real-estate recovery was more

pronounced than in any other market in the region.

Urbanization and economic reorms helped to drive

up prices, spurring strong domestic demand or both

residential and commercial real estate. The real-

estate allocation o China’s HNWIs rose to 27% at the

end o 2009 rom just 18% a year earlier, putting

HNWI real-estate allocations among the highest in the

region. However, while the China real-estate segment

is expected to remain strong, the government

regularly intervenes in the domestic market, using

policies on taxation, lending, investment and housing

to discourage or encourage buying. It took a more

expansionary approach in early 2009 in a bid to osetthe eects o the global economic crisis. By

December 2009, however, it was already moving to

cool prices and discourage speculation by returning

to more restrictive policies it had deployed when the

real-estate market showed signs o overheating

beore the crisis. Moreover, the government continues

to keep barriers to oreign investment high, with

regulations increasing the complexity and costs o

any real-estate transaction. Amid these constraints,

investment interest in China real estate will likely stay

strong, but prices could waver.

Hong Kong , conversely, has airly simple and liberal

real-estate laws and is a relatively transparent

market—certainly compared with mainland China. In

act, the strong gains in housing prices in 2009 were

driven partly by an inlux o wealthy mainland

Chinese, who made up 18.1% o luxury home

buyers.57 Concerned about a possible asset bubble,

the Hong Kong government tried to counter the

market’s upswing by tightening lending practices. It

57 Property Wire, “Wealthy Chinese Snap Up Luxur y Property in Hong Kong,” February 5, 2010

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 20/32

20 2010 AsiA-PAcific WEALTH rEPorT

58 Joyce Li, “Luxury Property Buoyant in Hong Kong,” Wall Street Journal, March 17, 2010

59 Property Wire, “Demand Soaring in Singapore Real Estate Market,” March 17, 2010

60 Global Real Estate Transparency Index, Jones Lang Las alle, 2010

61 Global Real Estate Transparency Index, Jones Lang Las alle, 2010; Global PropertyGuide, “The State of Japan’s Real Estate Market,” October 29, 2009; NuWire Investor,“Japan Unveils New Stimulus To Boost Struggling Economy,” December 09, 2009

also raised stamp duties, particularly or luxury

property transactions.58 More broadly, though, the

real-estate market is underpinned by airly limited

supply and steadily growing demand, resulting in

some o the highest real-estate prices in the world.

As the Hong Kong real-estate market is relatively

open to domestic, Asia-Paciic and oreign investors,

investment interest is expected to stay strong.

In Singapore, the real-estate market is also

developed and transparent, with a stable socio-

political environment helping to attract investment.

The share o Singapore HNWIs’ portolios dedicated

to real estate jumped to 34% o all holdings at the

end o 2009 rom 24% a year earlier as property

prices rallied ater a brie crisis-related downturn.

Direct real-estate investment also relected strong

buying interest rom HNWIs within the region and

rom oreign investors, who ace ew barriers to entry.

Singapore is also the second-largest REIT market in Asia-Paciic ater Japan, and REITs recovered

strongly ater the inancial crisis. Like China, though,

Singapore moved quickly to cool the rothing real-

estate segment by, or example, increasing taxes and

stamp duties.59 Nevertheless, investment interest is

likely to remain high, given the underlying stability in

the market.

Australia is considered one o the world’s most

transparent real estate markets,60 making it a

preerred location or oreign investors. Recent

government-policy changes promise to enhance

cross-border investment even urther. During thecrisis, to ensure a stable market, the government

lowered interest rates and increased inrastructure-

related stimulus spending. At the end o 2009,

Australian HNWIs held 40% o all their holdings

in real-estate assets, little changed rom a year

earlier, and up rom 28% at the end o 2007. Going

orward, real estate prices are expected to keep

rising given the rapidly growing population and

limited housing supply.

In Taiwan, HNWIs’ real-estate holdings accounted

or 23% o portolios at the end o 2009, up rom 15%

a year earlier. Real estate in Taiwan got a boost rom

monetary easing and improving regional economic

conditions, as well as news that Taiwan and China

were designing a inancial memorandum o

understanding that could boost cross-straits trade

and investment. Real-estate investment interest is

expected to decline in the uture, however, due to

government measures intended to check prices,

which are perceived to be overvalued.

Malaysia is a market in which investment interest is

expected to grow, ueled by government measures

that will support the real-estate sector. These include

avorable real-estate regulations, low interest rates

and liberalization o oreign-ownership limits.

Japan has a very large and well-developed real-

estate market, but transparency is relatively low

despite its economic maturity, which can deter

investment interest. The Japanese economy was

hit hard by the inancial crisis, undermining real-

estate development and buying interest. As a result,

experts anticipate a cooling o investment interest

in that market.61

CONCLUSION: REAL ESTATE TOREMAIN A KEY FINANCIAL ASSETCLASS IN ASIA-PACIFIC

Since the height o the crisis, Asia-Paciic HNWIs haveallocated more to real-estate investments on a globalas well as regional basis. Real estate is expected toremain a top asset category or Asia-Paciic HNWIsand HNW investors will increasingly be looking toadvisors and wealth management irms to handle andintegrate their real-estate holdings into an overallportolio discussion—especially as they seek todiversiy and optimize risk-adjusted returns.

As HNW investors look to ully integrate and understandthe entirety o their portolios in the risk analysisprocess, wealth management irms will need to developtheir oerings to cater to these demands. Firms will

need to ocus on three imperatives in particular:

Product innovation. Firms will need to provide

better accessibility, advice, products and services

around real estate, not just locally, but regionally and

globally. This extends beyond the obvious inancing

aspects and into managing indirect investment

opportunities, including private equity real estate,

unds o unds, etc. Firms will succeed i they can

provide innovation and accessibility to this important

asset class, while navigating changing regulations

and market conditions across the region. Demand or

real-estate assets is expected to remain high so whilesome major global institutions may have centers o

excellence in real estate, local and regional irms may

need to shore up their product availability and

services around real estate.

Specialization. Firms may need to involve

specialists/advisors in their advisory and product-

development processes. Advisors will also need to

be well-inormed about regulations, tax implications

and other issues contingent to buying and selling

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 21/32

212010 AsiA-PAcific WEALTH rEPorT

62 Asian Public Real Estate Association (APREA), 2010 – excludes figures from Australia

63

Michael Plummer and Jef f Rabin, Artvest Par tners, interviewed by Capgemini, New York, April-June 201064 Categories of passion investment researched for the World Wealth Report series

65 Michael Plummer and Jef f Rabin, Artvest Par tners, interviewed by Capgemini, New York, April-June 2010

real-estate assets in any given market. Increasingly,

strategic partnerships between global advisory and

local consulting irms are springing up to provide

specialized services in this ield.

REITs. The Asian REIT market, while still developing,

has nevertheless seen capitalization grow to US$70

billion in 2009 rom just US$2 billion in 2001.62 With

many more markets considering REIT legislation,

including China, investment demand is expected to

rise. Deregulation in countries such as Malaysia could

also make it easier or both domestic and oreign

investors to buy REITs. Firms have a good

opportunity to transer knowledge rom more

developed REIT markets into their Asia-Paciic

operations, and develop regional REIT platorms/

strategies in line with local REIT legislation to provide

customized oerings to their HNWI clients.

Asia-Pacific HNWIs Sk Ot Tanibl-Asst Invstmnts

Luxury goods makers and auction houses arereporting booming demand rom Asia-Paciic asthe region continues to see HNWI wealth grow asterthan in other regions. However, these purchasesby HNWIs are indicative o the broader ainity Asia-Paciic investors have or tangible goods—and theestablished role o physical assets in inancial-investment strategies.

In the 2010 World Wealth Report, we looked at anemerging global trend in which some HNWIs areapproaching their passion investments as “investor-collectors.”63 These HNWIs see purchases o Art,

Jewelry, Gems and Watches and other categories otangible assets64 as good alternatives to purely inancialinvestments, and they acquire tangible assets partly ortheir potential to gain value. This is certainly part o thepsyche or Asia-Paciic HNWIs, who have long pursuedphysical investments such as gold and jewelry becauseo their tangible value, proven returns and relativesaety—and their potential to hedge against inancialpressures such as inlation and currency risk.

In act, while many inancial markets around the globehave begun to recover ater the crisis, Asia-PaciicHNWIs have continued to broaden their interests in

investments outside o inancial markets. HNWIs’interests in tangible assets now include a wide rangeo passion investments, including Art, Wine and manyOther Collectibles. Notably, though, while Asia-PaciicHNWIs are acting partly as “investor-collectors”65 inmaking these acquisitions, they also have along-standing ainity or tangible assets as part oa diverse portolio.

HNWIs ARE DRIVEN TO INVEST INTANGIBLE ASSETS BY MORE THANECONOMICS

Economic considerations, such as inancial returns,ear o inlation and currency risk, have clearlycontributed to the increase in HNWI investments intangible-asset classes worldwide. Some Asia-Paciicmarkets also lack the array o investment optionsavailable in more developed markets, making tangibleassets an easy choice. But some sociocultural actorsalso drive the partiality Asia-Paciic HNWIs have orsome o these assets. For example:

In some parts o Emerging Asia (China, India,

Indonesia and Thailand), the wealthy are wary o

sophisticated inancial instruments and are more

conservative in their investment strategies. Investing

in tangible assets is also key to ensuring true

diversiication and protecting against certain orms o

risk or many HNWIs in markets where the inancial

markets are more volatile or less predictable.

Rising aluence in the region has boosted demand or

all types o tangible assets in recent years, attracting

more auction houses and luxury goods retailers to sella broader array o assets into the market, and

providing more options or Asia-Paciic HNWIs.

Among the newly wealthy, status is oten revered,

prompting some HNWIs to acquire luxury assets such

as Art, luxury automobiles, etc., to enhance their

reputation and provide a means to display their wealth.

Traditions and cultural underpinnings inluence the

buy-and-hold approach o gold investments rom

HNWIs in countries such as India and China.

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 22/32

22 2010 AsiA-PAcific WEALTH rEPorT

66 Brook Larmer, “The Real Price of Gold,” National Geographic, January 200967 Refers only to India, China, Hong Kong, Taiwan, Japan, Indonesia and Vietnam

68 Capgemini analysis, 2010

69 “Antwerp Diamond Day Celebrated,” China Daily, June 8, 2010, http://www.chinadaily.com.cn/china/2010expo/2010-06/08/content_9947489.htm

70 “2009 Art Market Trends,” March 2010, Artprice.com

71 The International Art Mar ket 2007-2009, Trends in Ar t Trade during Recession, TEFAF

In 2009, auction houses rom all over the world alsoreported strong buying interest rom Asia-PaciicHNWIs or tangible assets such as high-end jewelry,gems, Art, and Fine Wine. That buying interest hasincreased so much that both Sotheby’s and Christie’snow count Hong Kong as their No. 3 auction center,ollowing London and New York. Indeed, Asia-Paciic

investors have clearly become a orce in these markets,as evidenced by the ollowing:

While Hong Kong is still the region’s predominant

buyer o polished diamonds, retail demand is surging

in China, where diamonds have become revered as

wedding tokens and sought ater by the young and

newly wealthy. For example, Belgian oicials recently

said they expected one in every two polished

diamonds rom Antwerp to be sold to a Chinese

buyer within ive years.69 (Antwerp is a major global

distribution center or diamonds.)

China has become the third-largest Art auction

market globally ater increasing its share rom 7.2%

o the global Fine Art auction market in 2008 to 17.4%

in 2009.70 Elsewhere in Asia-Paciic, other Art markets

are smaller in size, but have been growing steadily.

India’s market, or example, grew 6% in 2009.71

Traditionally, Art markets in Asia-Paciic have largely

been conined to China, India, Indonesia and more

recently Hong Kong. However, recent auctions in

Singapore have been very successul and with good

government support or Art, Singapore is increasingly

becoming the hub o South East Asia Art auctions.

Sotheby’s Asia reported that 57% o the wine sold at

its auctions in 2009 was acquired by Asian buyers,

mostly rom mainland China. Wine is an attractive

category or many new “investor-collectors” as it has

a lower entry point and is more readily accessible.

TANGIBLE ASSETS OFFER NEWOPPORTUNITY FOR WEALTHMANAGEMENT FIRMS

Asia-Paciic HNWIs have clearly become seriousbuyers o all kinds o tangible assets in recent years,

giving wealth management irms an opportunity tooer more services related to these asset classes,including storage services, diversiication services andadvice on regulatory and tax implications.

For wealth management irms, the main challenge liesin building requisite expertise, since their experiencewith these services has oten been limited to date.Some irms have started to oer more advice oninvestments such as art and gold as a way or

GOLD HOLDS SPECIAL APPEAL FOR ASIA-PACIFIC HNWIs

Asia-Paciic HNWIs have long valued gold because it isa relatively liquid asset and has the potential to hedgeagainst inlation and currency risk, but it also holdsspecial cultural appeal. It is widely used in celebrations,

including weddings and religious observances incertain countries, which uels continual demand. InIndia, or instance, gold is equated with ortune, anddespite meager per-capita income levels, thepopulation has hoarded up to 18,000 tons o gold—more than 40 times the amount held in the country’scentral bank.66

In act, Asia-Paciic67 is the largest gold-consumingregion in the world, accounting or 44% o the world’sconsumer demand in 2009. India and China togetheraccounted or more than one-third. Notably, while 72%o global consumer demand is or jewelry, Asian

HNWIs also invest heavily in bullion (bars and coins),which can be easily stored yet readily bought or sold.

This also relects the general preerence Asia-PaciicHNWIs have or buying physical assets, rather thanexchange-traded unds (ETFs) or gold options, eventhough these alternatives are available. Asian HNWIs,more so than their global counterparts, are more likelyto take physical delivery o gold.

HNWIs FROM DEVELOPING ASIAPREFER “JEWELRY, GEMS AND

WATCHES” AS A CATEGORY; THOSEFROM INDUSTRIALIzED ECONOMIESFAVOR “LUxURY COLLECTIBLES”

Asia-Paciic HNWIs’ preerence or durable, tangibleinvestments is evident too in their purchases o passioninvestments. O Asia-Paciic HNWIs’ total suchinvestments in 2009, 61% was dedicated to thecategories o Jewelry, Gems and Watches, Art andOther Collectibles, up rom 52% in 2006.68 However,preerences are not uniorm across Asia-Paciic.

For example, HNWIs rom the Industrialized economiesin Asia-Paciic (e.g., Australia, Japan) avor LuxuryCollectibles such as jets, yachts and luxuryautomobiles. Those rom Emerging Asia are more likelyto esteem Jewelry, Gems and Watches (see Figure 10).

Notably, HNWIs rom the Newly Industrializedeconomies o Hong Kong, Singapore and Taiwanallocated as much as 20% o their passion investmentsin 2009 to Other Collectibles, the category thatincludes wines, coins, memorabilia, antiques, etc.

8/8/2019 Asia-Pacific Wealth Report(2010)

http://slidepdf.com/reader/full/asia-pacific-wealth-report2010 23/32

232010 AsiA-PAcific WEALTH rEPorT

investors to diversiy their portolios and hedgeagainst risks such as inlation and currency exposure.But this is new territory or many o them, as HNWIshave typically turned to domain experts in the past tomanage their speciic tangible-assets interests. Anassociated challenge or irms is the measurementand attribution o portolio perormance. As tangible-

asset holdings become more diverse, or instance, itbecomes more diicult to value these holdings, andincorporate those valuations into portolio-perormance tracking.

Ultimately, wealth management irms may considerestablishing stronger partnerships with auctionhouses, storage acilities and trading irms to expandtheir oerings in this area. Indeed, the SingaporeFreePort, which has its own state-o-the-artmaximum-security vault, equipped to housecollections and other valuables, oers even non-residents and investor-collectors a place to store

valuables, collections and other tangible assets.

Asia-Paciic HNWIs are likely to continue investing intangible-asset classes to diversiy their portolios incoming years, even as inancial markets eventuallyrecover. Wealth management irms need to plan theirstrategy or serving these clients well—especiallysince the ranks o the wealthy are likely to expandgiven the region’s positive economic outlook andrising levels o wealth.

In particular, irms will need to:

Understand the drivers o demand (cultural, inancial,

etc.) and the role o tangible assets in HNWI

portolios (diversiication, saety, hedge, etc.).

Take proper account o tangible assets in portolio

measurement and management, as well as in