asia pacific daily 1 august 2016 - cimb · eye on macau vol.37: jul mass table analysis- ......

TRANSCRIPT

Equity research│August 1, 2016

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Asia Pacific Daily - 1 August 2016

Equity Research Reports…

▌IDEA OF THE DAY | Vietnam Strategy Note - Vietnam’s stock market at an 8-year high | P2 Vietnam’s VN-Index (VNI) broke out of its two-year trading range, while CIMB’s top picks outperformed the VNI by 14% YTD (vs. 30% outperformance in 2015) Sentiment is being boosted by the removal of foreign ownership limits (FOL) on Vinamilk and other stocks, as well as by growing confidence in the new government Valuation is still reasonable at 13x FY16 P/E, versus 13% expected EPS growth The VNI already hit our 648 target price (+12%), so we’re lifting our target price by 7% to 694 (+20%); we expect the VNI to test (but not break) the 700 level in Q4.

———————————————————————————————————————————————————————————————————————————————————————

▌Australia BHP Billiton (ADD, tp:A$26.30) - One offs tipped for result | P3 Byron Energy (ADD, tp:A$0.44▲) - SM71 valuation underpins a higher price | P4 CYBG PLC (HOLD, tp:A$3.75) - 3Q16 trading update | P5 Mineral Deposits (ADD, tp:A$0.96) - June Q production and HY (loss) | P6 ———————————————————————————————————————————————————————————————————————————————————————

▌China/Hong Kong Want Want China (HOLD, tp:HK$5.00▼) - Reporting currency changed to Rmb | P7 Wynn Macau (HOLD, tp:HK$11.93) - Helped by high win rate | P8 ———————————————————————————————————————————————————————————————————————————————————————

▌Indonesia Gudang Garam (ADD, tp:Rp92,000.00▼) - Seasonal pressure | P9 Mayora Indah (ADD, tp:Rp46,000.00) - Recovery intact, margin hit by sugar | P10 Property Devt & Invt (OVERWEIGHT) - 2Q16 results: pressure on earnings remains | P11 ———————————————————————————————————————————————————————————————————————————————————————

▌South Korea Amorepacific Corp (ADD, tp:W520,000.00▼) - Focus on the big picture | P12 Industrial Bank of Korea (HOLD, tp:W12,700.00) - Stable but not attractive | P13 Samsung Card (ADD, tp:W59,000.00▲) - Capturing future growth | P14 ———————————————————————————————————————————————————————————————————————————————————————

▌Malaysia Felda Global Ventures (ADD, tp:RM2.08) - The way forward to improve earnings | P15 Malaysia Airports Holdings (ADD, tp:RM8.30▲) - Golden opportunity to accumulate | P16 Agribusiness (NEUTRAL) - Gauging sentiment on the palm oil sector | P17 Banks (OVERWEIGHT) - Jun 16 tracker – working hard to limit impaired loan ratios | P18 ———————————————————————————————————————————————————————————————————————————————————————

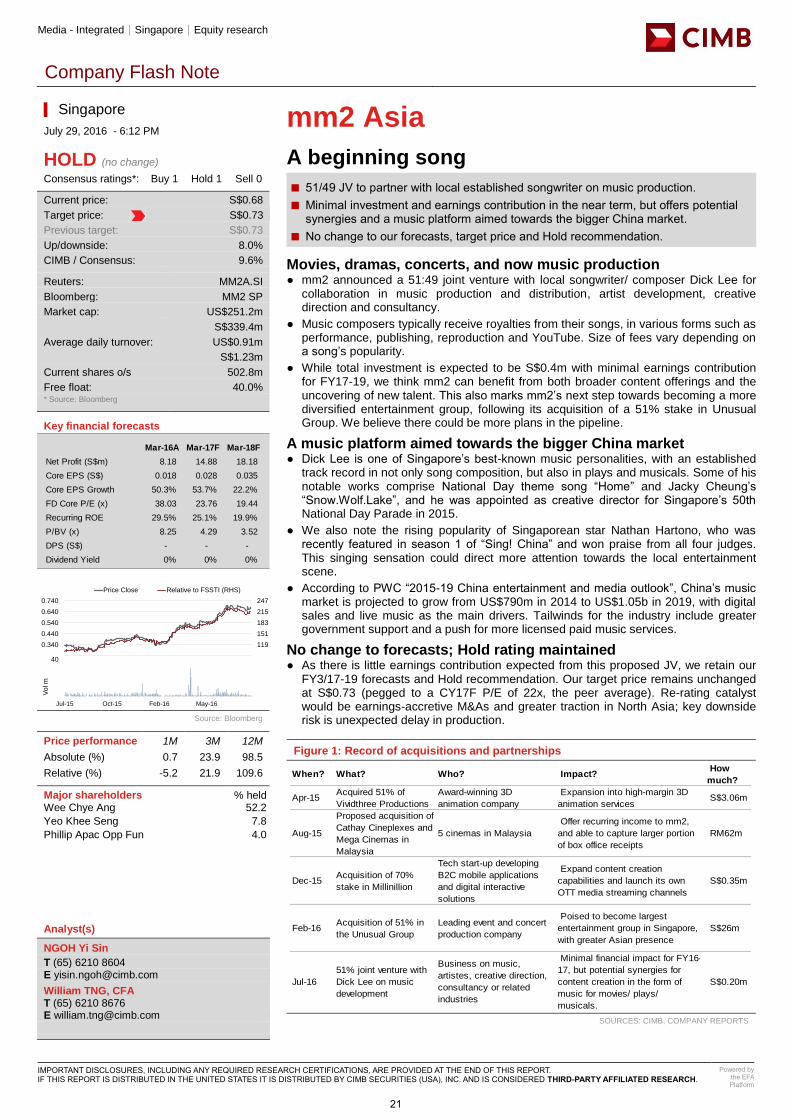

▌Singapore CDL Hospitality Trust (HOLD, tp:S$1.43▼) - 2QFY16: RevPAR decline re-accelerates | P19 Far East Hospitality Trust (HOLD, tp:S$0.65) - Blame it on June and the renovations | P20 mm2 Asia (HOLD, tp:S$0.73) - A beginning song | P21 Singapore Airlines (HOLD, tp:S$12.67▲) - Core earnings continue to be under pressure | P22 ———————————————————————————————————————————————————————————————————————————————————————

▌Taiwan Advanced Semiconductor (ADD, tp:NT$43.00▲) - Getting back on course | P23 Delta Electronics Inc (HOLD, tp:NT$177.00▲) - Steadily improving | P24 Innolux (HOLD, tp:NT$12.90▲) - Panel price hike already priced in | P25 ———————————————————————————————————————————————————————————————————————————————————————

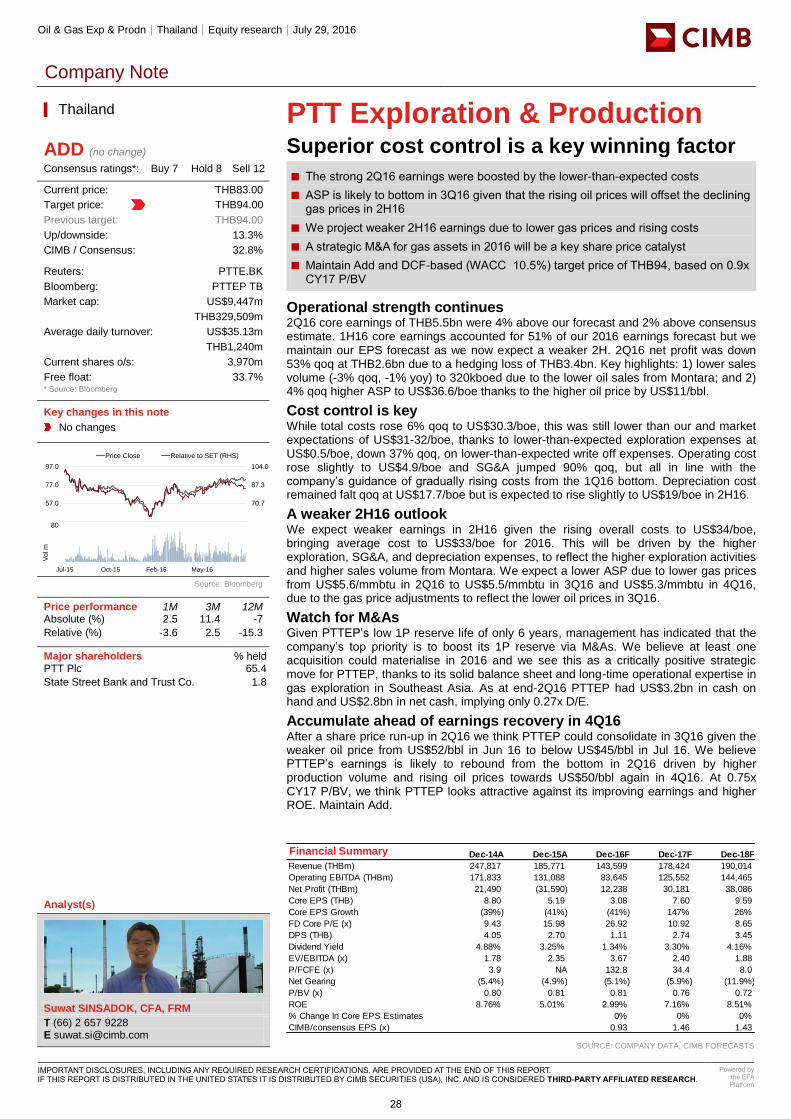

▌Thailand Jasmine Broadband Internet Infrastructure Fund (ADD, tp:THB13.50) - Stable high yield with growth potential | P26 PTT (ADD, tp:THB389.00) - An attractive utilities gas play | P27 PTT Exploration And Production (ADD, tp:THB94.00) - Superior cost control is a key winning factor | P28

Sources: CIMB. COMPANY REPORTS

Showcasing CIMB Research Ideas

HKG: Gaming 28/07 Eye on Macau Vol.37: Jul mass table analysis- premium mass boost >PDF

———————————————————————————————————————————————————————————————————————————————————

THB: WHA Premium Growth Freehold and Leasehold REIT 26/07 Potential shelter from the storm >PDF

———————————————————————————————————————————————————————————————————————————————————

IND: Astra International 25/07 2Q preview: Slippery earnings, bright macro >PDF

———————————————————————————————————————————————————————————————————————————————————

TWN: General Interface Solution 24/07 Exploiting synergy from group consolidation >PDF

———————————————————————————————————————————————————————————————————————————————————

MAL: Strategy Note - Alpha Edge 20/07 Asia turning bullish >PDF

Regional Equity Research Contacts

Michael GREENALL, CFP Regional Head of Research/Head of Research Msia T: (60) 3 2261 9088 E: [email protected]

———————————————————————————————————————————————————————————————————————————————————

Show Style "View Doc Map"

CIMB Conference / Events |

CIMB 10th Annual Indonesia Conference 08-12 August 2016, Bali - Indonesia

———————————————————————————————————————————————————————————————————————————————————

Vietnam│Equity research│July 30, 2016

Strategy Note

THIS REPORT IS PREPARED IN ASSOCIATION WITH VNDIRECT SECURITIES CORPORATION. PLEASE SEE DISCLAIMER AND IMPORTANT NOTICES APPEARING AT THE END OF THIS DOCUMENT. IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE ALSO PROVIDED AT THE END OF THIS REPORT. THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Vietnam Strategy Vietnam’s stock market at an 8-year high

Vietnam’s VN-Index (VNI) broke out of its two-year trading range, while CIMB’s top ■picks outperformed the VNI by 14% YTD (vs. 30% outperformance in 2015)

Sentiment is being boosted by the removal of foreign ownership limits (FOL) on■Vinamilk and other stocks, as well as by growing confidence in the new government

Valuation is still reasonable at 13x FY16 P/E, versus 13% expected EPS growth■The VNI already hit our 648 target price (+12%), so we’re lifting our target price by■7% to 694 (+20%); we expect the VNI to test (but not break) the 700 level in Q4

Strong stock market performance, despite Brexit and weak H1 GDP Vietnam’s 1H16 GDP growth was below expectations, but stock prices continued rising because weak H1 growth ensures ample liquidity (M2 grew 20% yoy in H1), and the H1 economic statistics revealed strength behind the headline figures; growth was held back by low oil prices and Vietnam’s worst drought in decades, but consumer spending grew 8% yoy, buoyed by strong consumer confidence, and manufacturing output grew 10%.

Sentiment boosted by FOL removal & new government The elimination of foreign ownership limits (FOL) has a profound impact on Vietnam’s stock market because it will enable the participation of a much wider range of investors in the local market, and because foreigners will now be able to directly influence the stock prices of companies like Vinamilk (VNM’s FOL has been full for years). Lifting FOL’s also demonstrates the new government’s commitment to reforms, further solidifying the esteem investors have for the county’s new, technocratic politburo.

The VND exchange is stable The SBV implemented a more flexible currency management regime this year – so the VND only depreciated by about 1% YTD. The currency is also firm because Vietnam ran a US$1.7b trade surplus in 1H16 vs. a US$3.5b deficit in 1H15, and because in CPI inflation is 2.5%. We forecast a 1% C/A surplus and a 3% BoP surplus this year, supported by 6.7%/GDP of overseas remittances and 7.4%/GDP of FDI inflows.

Vietnam has a good “LEVIS” fit - so we’re lifting our target price 7% Vietnam’s stock market scores well on the “LEVIS” stock market analysis framework: (L)iquidity is abundant, FY16 (E)arnings growth prospects continue to look good (note that Vietnamese companies are just starting to report their H1 earnings figures & it’s too soon to look at FY17 earnings in Vietnam), (V)aluation is still reasonable on a PEG basis, (I) interest rates are a bit high – which is the only LEVIS criteria for which Vietnam does not “check the box”, and (S)entiment is very positive – as evidenced by strong consumer survey data. The market already hit our 2016 target for the VNI – so we’re raising our target price by another 7%; we like VNM, MWG, VIC, and PVS.

[ X ]

Figure 1: The VN-Index broke out of its long-standing trading range

SOURCES: CIMB, NEILSEN

▎Vietnam

Highlighted companies

Mobile World (ADD; TP VND144,000)

Vietnam’s leading mobile phone retailer is now aggressively growing its home electronics chain. The total number of its outlets doubled over the last year, so earnings grew 86% yoy in 5M15. MWG is trading at 12X FY16 P/E, versus ~50% expected EPS growth.

Vingroup (ADD; TP VND64,000)

Vietnam’s leading real estate developer is benefitting from the country’s buoyant property market. The company’s pre-sales surged 180% last year, which should drive 180% FY16 EPS growth. VIC is trading at a 20% discount-to-NAV.

Vinamilk (ADD; TP VND177,000)

Vietnam’s leading consumer company is a perpetual favourite with foreign investors – and the foreign ownership limits that previously restricted their VNM share purchases have now been eliminated. VNM is trading at 21x FY16 P/E vs 23% EPS growth

Ample liquidity to fuel asset prices

AC Nielsen’s VN Consumer Confidence

Analyst(s)

Michael KOKALARI, CFA

T (84) 90 797 4408 E [email protected]

Title:

Source:

Please fill in the values above to have them entered in your report

450

500

550

600

650

700

Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

Title:

Source:

Please fill in the values above to have them entered in your report

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2009 2010 2011 2012 2013 2014 2015 5M16

M2 growth (yoy)

Title:

Source:

Please fill in the values above to have them entered in your report

80

85

90

95

100

105

110

115

4Q12 2Q13 4Q13 2Q14 4Q14 2Q15 4Q15

2

Mining│Australia│Equity research│July 29, 2016

IMPORTANT DISCLOSURES REGARDING COMPANIES THAT ARE THE SUBJECT OF THIS REPORT AND AN EXPLANATION OF RECOMMENDATIONS CAN BE FOUND AT THE END OF THIS DOCUMENT. MORGANS FINANCIAL LIMITED (ABN 49 010 669 726) AFSL 235410 - A PARTICIPANT OF ASX GROUP

Powered by EFA

BHP Billiton

One offs tipped for result

BHP has announced it will recognise a provision in the range of US$1.1-$1.3bn for ■the Samarco incident in its upcoming FY16 result.

The provision is equivalent to approximately half of the current estimate for ■Samarco’s funding obligations under the framework entered into in March.

In terms of cash outlays relating for Samarco, we assume approximately ■~US$250m is paid by BHP in FY17.

From FY18 onwards we assume Samarco will restart and self-fund ongoing ■remediation and compensation under the agreed framework.

The complex legal process continues in Brazil. ■

Provision added to expected one offs We have assumed US$1.2bn of provisions is recognised in the upcoming FY16 result, in addition to direct costs of ~US$100m (post tax). This combines with impairments already posted in the interim result in February, when BHP wrote down the book value of Samarco to zero, in addition to a large impairment against its US onshore O&G assets (primarily its gas interests). We now estimate combined one off charges of US$7.3bn in the FY16 earnings result, which we expect will see a reported NLAT of US$6.4bn (was NLAT of US$5.3bn) and underlying NPAT of US$832m (unchanged).

Heartening response We remain encouraged by the high priority BHP has made of the Samarco incident, with its quick and decisive action helping to jumpstart the extensive recovery process. The company has provided a further short-term debt facility of up to US$116m to its part-owned subsidiary Samarco in order to assist in continuing its work on the site.

Our Samarco assumptions In our base case, to be conservative we have assumed that Samarco cannot independently fund the near-term remediation and recovery work under the agreed framework. As a result we assume BHP and Vale split the expenses 50/50 during FY16 (~US$250m) and FY17 (~US$200m). We have estimated the direct costs by setting it in line with the agreed framework with an added (albeit small) contingency. Although there is a great deal of uncertainty around the timeframe for a possible restart of the Samarco operations, we have assumed the operations become active from early FY18 at which point we expect Samarco will start ‘self-funding’ the remediation costs.

No change in our thinking While we have revised our forecast reported NLAT for FY16, there have been no changes to our underlying earnings expectations or SOTP-valuation derived price target of A$26.30 per share. We believe Samarco/BHP/Vale will work through the legal process in Brazil and continue to responsibly support the recovery process. We maintain our Add recommendation, believing there is significant upside risk to BHP’s forward earnings from the stronger commodity price environment. The key risk to our call remains the potential for volatility around commodities in the short term.

SOURCE: MORGANS, COMPANY REPORTS

▎Australia

ADD (no change) Current price: A$19.97

Target price: A$26.30

Previous target: A$26.30

Up/downside: 31.7%

Reuters: BHP.AX

Bloomberg: BHP AU

Market cap: US$75,537m

A$100,342m

Average daily turnover: US$179.4m

A$241.5m

Current shares o/s 5,321m

Free float: 100.0%

Price performance 1M 3M 12M

Absolute (%) 10.8 -2.9 -21.3

Relative (%) 1.9 -9.2 -20.8

Adrian PRENDERGAST

T (61) 3 9947 4134

Financial Summary Jun-14A Jun-15A Jun-16F Jun-17F Jun-18F

Revenue (US$m) 56,762 44,636 31,803 38,098 43,624

Operating EBITDA (US$m) 31,517 21,651 12,264 15,767 20,262

Net Profit (US$m) 13,832 1,910 -6,449 3,360 5,683

Normalised EPS (US$) 2.52 1.21 0.16 0.63 1.07

Normalised EPS Growth 11% (52%) (87%) 304% 69%

FD Normalised P/E (x) 5.96 12.47 96.10 23.81 14.08

DPS (US$) 1.21 1.26 0.24 0.39 0.53

Dividend Yield 8.05% 8.38% 1.59% 2.62% 3.55%

EV/EBITDA (x) 3.56 5.09 8.96 6.63 4.77

P/FCFE (x) 9.41 14.78 9.59 14.66 9.23

Net Gearing 30.2% 34.6% 39.3% 29.4% 16.0%

P/BV (x) 1.01 1.24 1.43 1.36 1.26

ROE 18.0% 8.9% 1.4% 5.9% 9.3%

% Change In Normalised EPS Estimates 0% 0% 0%

Normalised EPS/consensus EPS (x) 1.01 1.40 1.60

64.0

78.1

92.1

106.2

12.0

17.0

22.0

27.0

Price Close Relative to S&P/ASX 200 (RHS)

Source: Bloomberg

10

20

30

40

50

Jul-15 Oct-15 Feb-16 May-16

Vol m

3

Oil & Gas Exp & Prodn│Australia│Equity research│July 29, 2016

IMPORTANT DISCLOSURES REGARDING COMPANIES THAT ARE THE SUBJECT OF THIS REPORT AND AN EXPLANATION OF RECOMMENDATIONS CAN BE FOUND AT THE END OF THIS DOCUMENT. MORGANS FINANCIAL LIMITED (ABN 49 010 669 726) AFSL 235410 - A PARTICIPANT OF ASX GROUP

Powered by EFA

Byron Energy Ltd

SM71 valuation underpins a higher price

Funding has been secured and the development of SM71 is expected to occur ■over the coming year with production anticipated by mid-2017.

BYE has announced two farm-in partners for the drilling of the Bivouac Peak lease ■which is scheduled for 1H17.

Retain Add recommendation on an increased target price of A$0.44 (was A$0.38). ■

South Marsh Island 71 delivers Following the successful drilling of the SM71 well, which intersected hydrocarbons in four sands, BYE has announced a reserve increase. 2P reserves net to BYE stand at 2.271mmboe, up 508% and the well will be brought into production in 2017.

South Marsh Island 6 to not be re-entered Following ongoing drilling issues associated with SM6, BYE has decided not to re-enter the SM6 #2 well to complete the drilling down to the primary target (G20 Sand). BYE will plug and abandon the section of the SM6 #2 well that is below the F Sands and it will undertake an assessment of the SM6 project based solely on the net pay intersected in the F Sands.

Bivouac Peak to be drilled in 1H17 BYE has successfully secured third party funding for the drilling of a well in the Bivouac Peak lease in 1H17 (subject to permitting). Otto Energy (ASX: OEL) and Metgasco (ASX: MEL) have both announced they will farm in to the block which will result in BYE reducing its Working Interest to 35% and its Net Revenue Interest to 26.08%. As a result of these transactions, BYE will be required to fund US$1.4m for the initial well. In addition to announcing the two farm-out deals, BYE has received an independent resource estimate for the Bivouac Peak prospect. The current prospective resource estimate net to BYE is 11.9mmboe.

New loan facility to fund the commencement of production BYE has secured debt funding which will allow the company to bring the SM71 well into production. MEL will subscribe to an A$8.0m three year convertible note with BYE and has also been issued 10m unlisted BYE options with an exercise price of 25c and three year term.

Retain Add recommendation Following the drilling success witnessed at SM71 and the recent reserve and resource upgrades, our target price has increased to A$0.44 (from A$0.38). We believe the market will gain increased confidence following the recent farm-ins and funding agreement and expect upcoming drilling and development activity to attract market interest. Consequently we retain an Add recommendation on BYE.

SOURCE: MORGANS, COMPANY REPORTS

▎Australia

ADD (no change) Current price: A$0.14

Target price: A$0.44

Previous target: A$0.38

Up/downside: 213.1%

Reuters: BYE.AX

Bloomberg: BYE AU

Market cap: US$24.77m

A$32.91m

Average daily turnover: US$0.01m

A$0.01m

Current shares o/s 235.0m

Free float: 80.0%

Price performance 1M 3M 12M

Absolute (%) 21.7 -12.5 -33.3

Relative (%) 12.8 -18.8 -32.8

James LAWRENCE

T (61) 7 3334 4547

Adrian PRENDERGAST

T (61) 3 9947 4134

Financial Summary Jun-14A Jun-15A Jun-16F Jun-17F Jun-18F

Revenue (A$m) - - - - -

Operating EBITDA (A$m) (2.21) (2.46) (2.88) (2.95) (3.05)

Net Profit (A$m) (2.20) (2.49) (2.96) (2.96) (3.06)

Normalised EPS (A$) (0.016) (0.013) (0.013) (0.013) (0.013)

Normalised EPS Growth (18.4%) (2.5%) 0.1% 3.5%

FD Normalised P/E (x) NA NA NA NA NA

DPS (A$) - - - - -

Dividend Yield 0% 0% 0% 0% 0%

EV/EBITDA (x) NA NA NA NA NA

P/FCFE (x) NA NA NA 15.95 16.80

Net Gearing (28.6%) (15.3%) 3.5% 34.6% 49.7%

P/BV (x) 0.88 0.86 0.98 1.08 1.20

ROE (20.0%) (9.3%) (9.1%) (9.3%) (10.6%)

% Change In Normalised EPS Estimates 0% 0% 0%

Normalised EPS/consensus EPS (x) 1.80 1.81 1.87

53

78

103

128

0.090

0.140

0.190

0.240

Price Close Relative to S&P/ASX 200 (RHS)

Source: Bloomberg

1

2

3

Jul-15 Oct-15 Feb-16 May-16

Vol m

4

Banks│Australia│Equity research│July 29, 2016

IMPORTANT DISCLOSURES REGARDING COMPANIES THAT ARE THE SUBJECT OF THIS REPORT AND AN EXPLANATION OF RECOMMENDATIONS CAN BE FOUND AT THE END OF THIS DOCUMENT. MORGANS FINANCIAL LIMITED (ABN 49 010 669 726) AFSL 235410 - A PARTICIPANT OF ASX GROUP

Powered by EFA

CYBG PLC

3Q16 trading update

No revision to guidance. ■

We have made no material changes to our cash EPS forecasts. ■

Our investment view remains unchanged. Cost-out story and potential Internal-■Ratings Based (IRB) accreditation remain the bright spots of the story. The outlook for income growth looks challenging as a result of a softer macroeconomic outlook.

We retain our HOLD recommendation and $3.75 price target. ■

Underlying mortgage growth softer than target The mortgage book grew at an annualised rate of 3.5% over 3Q16, compared with the Company’s target of annualised loan growth of 7-8%. Low growth over 3Q16 was partly the result of strong volume growth over 2Q16 stemming from the stamp duty change on 1 April. However, annualised mortgage book growth over the 9 months to 30 June 2016 was 8% despite assistance in 2Q16 from the change to stamp duty. After stripping out the positive impact this change, mortgage book growth over the same 9 months was likely below the Company’s target range. This belief is also supported by the fact that CYB’s mortgage balances grew 5.5% over the year to 31 May 2016.

NIM assisted by deposit re-pricing The net interest margin (NIM) for 3Q16 was 2.27%, up from 2.25% in 1H16. This increase largely appears to be attributable to the full period impact in 3Q16 of the reduction in liquid assets over 1H16 as well as the full period impact of deposit re-pricing which took place in 1H16. Strong SME loan growth of 13% annualised over 3Q16 also assisted the NIM through a favourable shift in the loan mix. We were expecting some lending margin contraction over 3Q16, however lending margins were likely stable over this period and perhaps this explains the softness in underlying mortgage book growth. We continue to expect the NIM to contract over our forecast period largely due to cuts to the Bank of England’s Bank Rate.

Cost guidance unchanged The Company has said that it is firmly on track to meet full year cost guidance of £730m.

No deterioration in asset quality The credit impairment charge for the 9 months to 30 June 2016 as a percentage of gross loans was 14bps. This compares with 19bps over 1H16 and 21bps over FY15. We continue to expect asset quality to deteriorate over our forecast period particularly in the SME loan book.

Investment view and changes to forecasts We have made no material changes to our cash EPS forecasts. Our 12-month pound target price is unchanged at £2.25. Our target price for the ASX-listed Chess Depository Interests (CDIs) is unchanged at $3.75 based on an AUDGBP cross-rate assumption of 0.600. Despite greater than 10% downside on a 12-month basis, we are maintaining our HOLD recommendation as the Capital Markets Update on September 13 is likely to include positive revisions to cost guidance.

SOURCE: MORGANS, COMPANY REPORTS

▎Australia

HOLD (no change) Current price: A$4.42

Target price: A$3.75

Previous target: A$3.75

Up/downside: -15.2%

Reuters: CYB.AX

Bloomberg: CYB AU

Market cap: US$2,932m

A$3,895m

Average daily turnover: US$23.10m

A$31.22m

Current shares o/s 879.3m

Free float: 100.0%

Price performance 1M 3M 12M

Absolute (%) 7.5 3

Relative (%) -1.4 -3.3

Azib Khan

T (61) 2 9043 7903

Financial Summary Sep-14A Sep-15A Sep-16F Sep-17F Sep-18F

Net Interest Income (£m) 785.0 787.0 809.5 832.4 859.1

Total Non-Interest Income (£m) 197.0 177.0 181.8 185.4 189.9

Operating Revenue (£m) 982 964 991 1,018 1,049

Total Provision Charges (£m) (74.0) (78.0) (63.2) (91.7) (128.8)

Net Profit (£m) (198.0) (225.0) 66.9 100.5 116.8

Normalised EPS (£) 0.19 0.15 0.14 0.18 0.19

Normalised EPS Growth 73.4% (20.9%) (6.4%) 27.7% 10.5%

FD Normalised P/E (x) 13.65 17.24 18.41 14.42 13.05

DPS (£) - - - 0.020 0.020

Dividend Yield 0.00% 0.00% 0.00% 0.79% 0.79%

BVPS (£) 2.89 3.92 4.04 4.15 4.26

P/BV (x) 0.88 0.65 0.63 0.61 0.59

ROE 6.54% 4.31% 3.45% 4.29% 4.61%

% Change In Normalised EPS Estimates 0.061% 0.380% (0.258%)

Normalised EPS/consensus EPS (x) 1.23 1.18 1.00

82.0

92.0

102.0

112.0

122.0

132.0

142.0

3.30

3.80

4.30

4.80

5.30

5.80

6.30

Price Close Relative to S&P/ASX 200 (RHS)

Source: Bloomberg

20

40

60

80

Feb-16 Mar-16 May-16 Jun-16

Vol m

5

Mining│Australia│Equity research│July 29, 2016

IMPORTANT DISCLOSURES REGARDING COMPANIES THAT ARE THE SUBJECT OF THIS REPORT AND AN EXPLANATION OF RECOMMENDATIONS CAN BE FOUND AT THE END OF THIS DOCUMENT. MORGANS FINANCIAL LIMITED (ABN 49 010 669 726) AFSL 235410 - A PARTICIPANT OF ASX GROUP

Powered by EFA

Mineral Deposits

June Q production and HY (loss)

After the first 180° dredge path turnaround and major scheduled maintenance in ■the March quarter, Grande Côte (MDL an effective 45%) returned to production, with 138.9kt of concentrate in the June quarter, with the focus on operational efficiency and consistency. We expect a lift to nameplate output over 2016, an EBITDA-positive December half year, and for the full 2016 year.

Tyssedal Titanium and Iron (MDL 50%) produced its first chloride-route titanium ■slag and high purity iron ore (HPPI) in January after a four-month shutdown, with production of titanium slag in the June quarter of 44.2kt, close to previous levels. TTI was EBITDA positive to the tune of US$6m in the June half. We anticipate increased production for the December half, and stronger cashflow.

Pigment prices have firmed with demand recovery and supply constraint expected ■to lead to stronger ilmenite and rutile pricing. Zircon prices have stabilised after inventory de-stocking. We model prices to strengthen from early 2017.

MDL reported an underlying loss of US$19.2m for the June half year. Our SOTP ■valuation and target remain at A$0.96/share, subject to the usual operational, jurisdictional, commodity price market and exchange rate risks.

GCO – production optimisation continues Heavy Media Concentrate (HMC) production at Grande Côte (TiZir 90%, MDL 50% of TiZir) was at 75% of previous levels for the June half year, after the dredge path turnaround and scheduled maintenance over six weeks in the March quarter and unscheduled stoppages in the June quarter, which limited ilmenite production to 92,783t in the quarter. We model increased production and operational efficiencies in the December half, and a return to EBITDA-positive status for the half, but model a net loss for CY 2016.

TTI – EBITDA positive already The TTI furnace was shut down in mid-September 2015 for a re-line and capacity upgrade, as well as for conversion to production of higher-value Chloride-route titanium slag. Production for the month of March was reported by MDL at 90% of pre-expansion capacity, and by our estimate 75% of the ultimate expanded nameplate. For the June quarter production was 44.2kt of slag. MDL reports that TTI was EBITDA positive for the June half. We model a full year positive NPAT for TTI.

Valuation – target and risk An underlying net loss of US$19.8m was reported for the June half. We have marginally lowered our production forecasts for 2016. Our valuation and target remain at A$0.96. Under the terms of the TiZir agreement with ERAMET (50% of TiZir), ERAMET has now advanced MDL A$7.2m to fund MDL’s contribution to TiZir’s obligations to its bondholders, and will continue to fund up to US$60m in total if necessary. In our view this substantially reduces the risks for TiZir in meeting its debt servicing obligations (US$275.0m) during this weak commodity market as plant optimisation continues. Risks to achieving our price target include operational, commodity price, exchange rate and geographic risks. Efficient operating performance and commodities pricing offers the most upside and downside risks to our target price.

SOURCE: MORGANS, COMPANY REPORTS

▎Australia

ADD (no change) Current price: A$0.46

Target price: A$0.96

Previous target: A$0.96

Up/downside: 111.9%

Reuters: MDL.AX

Bloomberg: MDL AU

Market cap: US$35.51m

A$47.17m

Average daily turnover: US$0.10m

A$0.14m

Current shares o/s 103.7m

Free float: 67.6%

Price performance 1M 3M 12M

Absolute (%) 106.8 56.9 -36.8

Relative (%) 97.9 50.6 -36.3

Chris BROWN

T (61) 7 3334 4885

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (US$m) - - - - -

Operating EBITDA (US$m) (5.48) (3.62) (3.80) (3.99) (4.19)

Net Profit (US$m) (71.73) (42.02) 1.11 66.51 98.03

Normalised EPS (US$) (0.69) (0.41) 0.01 0.64 0.95

Normalised EPS Growth (24%) (41%) 5912% 47%

FD Normalised P/E (x) NA NA 32.10 0.53 0.36

DPS (US$) - - - - -

Dividend Yield 0% 0% 0% 0% 0%

EV/EBITDA (x) NA NA NA NA NA

P/FCFE (x) 0.9 NA NA 174.0 16.9

Net Gearing (7.62%) (1.91%) (2.47%) (2.55%) (3.31%)

P/BV (x) 0.11 0.13 0.13 0.13 0.13

ROE (19.7%) (14.2%) 0.4% 24.9% 36.6%

% Change In Normalised EPS Estimates (91.3%) (4.9%) (3.7%)

Normalised EPS/consensus EPS (x) (0.27) 3.62 2.03

27

38

50

61

73

84

96

107

0.12

0.22

0.32

0.42

0.52

0.62

0.72

0.82

Price Close Relative to S&P/ASX 200 (RHS)

Source: Bloomberg

1

2

3

4

Jul-15 Oct-15 Feb-16 May-16

Vol m

6

Food & Beverages│Hong Kong│Equity research│July 29, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Want Want China Reporting currency changed to Rmb

Want Want announced a change in reporting currency from US$ to Rmb. ■

We expect weak topline growth in 1H16 as cool weather impacted beverage and ■popsicle sales; rice cracker sales also likely underperformed due to earlier CNY.

We expect 1H16 sales to drop 2.8% yoy while earnings to grow 1.7% yoy in Rmb ■terms. In US$, sales and net profit will both fall 7.8% and 3.5% yoy respectively.

We cut FY16-18F earnings by 5.7-14.3% to reflect weaker topline growth. ■

Maintain Hold. While Want Want’s valuation is not expensive, we would like to see a ■recovery in demand for its core product, i.e. Hot Kid Milk.

Change in reporting currency Management announced adoption of Rmb as presentation currency to better reflect the underlying performance of the company, given over 90% of total revenue is generated in mainland China. The first restated financials will be presented in 1H16 results release.

Hot Kid milk sales worsened in 2Q16 According to the management, Hot Kid milk sales were flat yoy in 1Q16, but turned to negative growth in 2Q16 due to the intensified competition and cooler weather. Want Want recently launched room temperature kids’ yoghurt and high-end yoghurt drink in Jun and Jul, which should help to improve milk sales in 2H16. We now expect Hot Kid milk sales to fall 10.0% and 1.1% yoy respectively in US$ terms in 1H16 and 2H16.

Rice cracker to recover in 2H16 Rice cracker segment sales are highly correlated with the timing of the Chinese New Year (CNY). Due to an earlier CNY this year, we expect rice cracker sales to drop 3% yoy in 1H16. However, given CNY in 2017 will be even earlier, rice cracker sales should improve in 2H16. We now expect rice cracker sales to recover 8.7% yoy in 2H16.

Warmer July will help popsicles and jellies sales Cool weather in 2Q16 negatively impacted sales of popsicles and jellies. However, sales have picked up c.30% in Jul as it got increasingly warmer. Management also said it will launch new cake products in 2H16. We now expect snacks sales to drop 7.0% yoy in 1H16, but recover to positive 3.6% yoy growth in 2H16.

To benefit from lower milk powder price According to the management, international milk powder price procured by Want Want fell more than 20% yoy in 1H16. Want Want has accumulated inventories which will be sufficient for use until end-3Q16. We expect GPM expansion of 0.5% pt yoy to 43.0% in 1H16. Want Wat cut over 3,000 sales people in Sep/Oct 2015, hence we expect its distribution expenses ratio to drop 0.4pts yoy to 14.1% in 1H16. Management said it will continue to closely control the expenses ratios in 2H16.

Maintain Hold with lower DCF-based TP of HK$5.0 (WACC: 9.3%) Maintain Hold. Although Want Want’s valuation is not demanding, we would like to see more successful product launches. Want Want had US$1.4bn cash at end-FY15, which could support continuous share buy-back plan and limit further share price downside. Key upside risks include better-than-expected launch of new beverage products; downside risks include slower-than-expected recovery in Hot Kid milk sales and higher-than-expected promotional expenses.

▎Hong Kong

HOLD (no change) Consensus ratings*: Buy 3 Hold 16 Sell 6

Current price: HK$4.75

Target price: HK$5.00

Previous target: HK$5.60

Up/downside: 5.3%

CIMB / Consensus: -12.5%

Reuters: 0151.HK

Bloomberg: 151 HK

Market cap: US$7,784m

HK$60,388m

Average daily turnover: US$12.62m

HK$97.92m

Current shares o/s: 13,101m

Free float: 48.5% * Source: Bloomberg

Key changes in this note

FY16F Revenue decreased by 4.7%.

FY16F EPS decreased by 5.7%.

FY16F ROE decreased by 1.5%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -13.6 -20.6 -41.1

Relative (%) -20.7 -24.5 -30

Major shareholders % held Tsai Eng Meng 48.0

Wen Hsien Cheng 3.5

Analyst(s)

Lei YANG, CFA

T (86) 21 5047 1771 x108 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (US$m) 3,775 3,428 3,333 3,418 3,582

Operating EBITDA (US$m) 894.8 861.3 872.4 907.8 970.0

Net Profit (US$m) 620.5 542.1 572.7 593.6 634.5

Core EPS (US$) 0.047 0.041 0.044 0.045 0.048

Core EPS Growth (9.6%) (12.0%) 5.7% 3.6% 6.9%

FD Core P/E (x) 13.03 14.80 14.01 13.51 12.64

DPS (US$) 0.024 0.018 0.019 0.020 0.021

Dividend Yield 3.90% 2.95% 3.11% 3.23% 3.45%

EV/EBITDA (x) 8.73 9.03 8.60 7.90 7.07

P/FCFE (x) 334.0 20.1 15.6 13.8 13.9

Net Gearing (11.3%) (9.9%) (20.8%) (30.9%) (37.7%)

P/BV (x) 3.92 4.27 3.63 3.14 2.74

ROE 30.9% 27.5% 28.0% 24.9% 23.2%

% Change In Core EPS Estimates (5.7%) (10.9%) (14.3%)

CIMB/consensus EPS (x) 1.02 1.03 1.03

66.0

76.0

86.0

96.0

106.0

4.40

5.40

6.40

7.40

8.40

Price Close Relative to HSI (RHS)

50

100

150

Jul-15 Oct-15 Feb-16 May-16

Vo

l m

7

Gaming│Hong Kong│Equity research│July 29, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Wynn Macau Helped by high win rate

2Q16 property EBITDA of USD190m, 9% above expectations helped by a high VIP ■win rate of 3.98%.

Initial table allocation for new Wynn Palace at 100 tables, below market■expectations of 200-250 tables.

Premium mass segment strong with higher spending players returning.■Maintain hold with target price based on 16x FY16, EV/EBITDA, 1 s.d. above the■stock’s 4 year average. Upside risks include stronger ramp-up at Wynn Palace.

2Q16 EBITDA helped by a high win rate Wynn Macau’s 2Q16 property EBITDA reached USD190m (+10% yoy, flat qoq), 9% higher than consensus expectations. As VIP win rates during the quarter reached an abnormally high rate of 3.98%, this contributed USD20m to EBITDA. On a hold-normalized basis, reported EBITDA would have been about 2% below expectations. EBITDA margins reached 30% during the quarter (+170bp yoy, -160bp qoq). We expect EBITDA to increase 31% yoy with the opening of Wynn Palace.

Premium mass coming back Mass table wins were up 13% yoy which management attributed to the cultivation of new players and the return of premium mass players to the gaming market. This was consistent with our proprietary table analysis which showed that, on an overall market basis, ultra-premium mass tables with a minimum bet of HKD3k+/USD387+ comprised 14% of tables in 2Q16 vs. 12% in 2Q15. The return of premium mass players is a positive indication of recovery in the gaming market.

Lower initial table allocation The government has initially granted Wynn Macau 100 tables for the upcoming Wynn Palace project which is lower than the initial 150 tables granted for Galaxy Phase 2 and the 200 tables for Studio City. The 100-table initial allocation is lower than expected. However, we expect further table allocation in later stages similar to Galaxy Phase 2 and Studio City. With Sands Parisian opening three weeks after Wynn Palace, we believe the government is being prudent with new table grants to control table supply.

Shifting of resources Wynn Palace will open with 350 tables (100 new tables, 250 shifted from Wynn Macau). Wynn Macau will be left with 270 tables. The tables shifted from Wynn Macau will be from the VIP segment and not mass which are better performing tables at the property. Out of the 7,000 employees at Wynn Palace, 5,000 will be new employees and the remaining will be shifted from Wynn Macau. Wynn can save USD20-25m in payroll expenses from the employee shift. Wynn Palace will open on August 22, 2016.

Maintain hold Wynn Macau is the top performing gaming stock +47% YTD and is hence trading at 15x Bloomberg consensus EV/EBITDA, vs. 11x sector average. While Wynn Palace is likely to be the premier new property on Cotai and the lower initial table allocation is not likely to have a significant impact to earnings given table underutilization in Macau, we believe the positives are mostly priced in and hence would wait for a better entry point. Upside risks include stronger than expected ramp up of Wynn Palace.

▎Hong Kong

HOLD (no change) Consensus ratings*: Buy 12 Hold 9 Sell 4

Current price: HK$13.34

Target price: HK$11.93

Previous target: HK$11.93

Up/downside: -10.6%

CIMB / Consensus: -0.2%

Reuters: 1128.HK

Bloomberg: 1128 HK

Market cap: US$8,936m

HK$69,308m

Average daily turnover: US$16.00m

HK$124.2m

Current shares o/s: 5,196m

Free float: 27.7% * Source: Bloomberg

Key changes in this note

No changes

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 21.9 17.6 -12.2

Relative (%) 12 13.9 -2.7

Major shareholders % held WM Cayman Holdings 72.2

Capital Group Companies 4.9

JP Morgan Chase 5.0

Analyst(s)

Michael TING

T (852) 2532 1121 E [email protected]

Jensen POON T (852) 25391350 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (HK$m) 29,445 19,096 22,395 25,460 26,079

Operating EBITDA (HK$m) 7,952 4,032 5,279 6,806 7,051

Net Profit (HK$m) 6,445 2,433 2,264 3,420 3,655

Core EPS (HK$) 1.24 0.47 0.44 0.66 0.70

Core EPS Growth (16.4%) (62.3%) (7.0%) 51.1% 6.9%

FD Core P/E (x) 10.74 28.49 30.62 20.26 18.96

DPS (HK$) 1.75 0.60 0.43 0.65 0.70

Dividend Yield 13.1% 4.5% 3.2% 4.9% 5.2%

EV/EBITDA (x) 9.69 23.28 18.56 14.39 13.89

P/FCFE (x) 11.35 25.90 23.19 13.91 13.62

Net Gearing 111% 599% 659% 643% 627%

P/BV (x) 9.84 16.90 15.92 15.58 15.17

ROE 79.3% 43.7% 53.5% 77.7% 81.1%

% Change In Core EPS Estimates 0% 0% 0%

CIMB/consensus EPS (x) 1.03 1.02 0.96

62.0

82.8

103.7

5.9

10.9

15.9

Price Close Relative to HSI (RHS)

50

100

Jul-15 Oct-15 Feb-16 May-16

Vol m

8

Tobacco│Indonesia│Equity research│July 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Gudang Garam Seasonal pressure

GG’s 1H16 core net profit formed 41% of our FY16 forecast and 42% of consensus, ■below expectations, given seasonal average of 48% in FY11-15.

The deviation stemmed from lower-than-expected operating margin due to higher■advertising and promotion (A&P) spending, likely for its GG Mild brand.

Stripping out excise costs, GG’s 2Q16 gross margin (GPM) was resilient, rising by■1.4% yoy.

Maintain Add, with a lower target price of Rp92,000, still based on 21.5x CY17 P/E■(1 s.d. above 10-year mean).

Sales rose at a robust pace, thanks to favourable base GG’s 2Q16 revenue rose 10% yoy on the back of c.12% yoy price increase, suggesting negative volume growth, which was weaker than the industry’s flattish revenue growth in Jan-Jun 16 (based on two data surveys from third-party sources). GG’s domestic machine-made cigarette (SKM) revenue rose 11% qoq, higher than the 10% in 1Q16. SKM remains GG’s major revenue contributor (90% of 1H16 revenue).

Margins tanked due to excise duties and slow ASP increase GPM weakened 3.8% pts qoq and 60bp yoy in 2Q16, as the full impact of the excise duty increase (+14% yoy, 58% of COGS in 2Q16) weighed on margins. Furthermore, the company only increased ASP by c.2% (Feb 2016) in 1H16. Stripping out excise costs, GG’s 2Q16 GPM would have dipped by 90bp qoq but risen by 1.4% yoy. Ex-excise 2Q16 GPM was resilient and shows no wild fluctuations in raw material prices. We expect GPM to normalise on the back of ASP hike (typically in 2H).

Operating profit under seasonal pressure 2Q16 opex rose at a faster rate than revenue, increasing by 27% qoq and 21% yoy to 10.9% of revenue (vs. 9.1% in 1Q16). Consequently, operating margin (OPM) in 2Q16 fell to 9%, the lowest level in more than six years. Further scrutiny revealed that higher wages were the culprit behind the OPM weakness in 2Q16. Labour cost rose by 34% qoq and 33% yoy in 2Q16, probably because the company paid the 13

th month salary in

Jun 16, compared to Jul 15.

Balance sheet position 2Q16 capex tapered by 12% qoq and 24% yoy to Rp576bn (US$43.3m). This represents 49-62% of the company’s FY16 capex guidance of Rp2.0tr-2.5tr (US$150-188m), vs. CIMB FY16 estimate of Rp2tr, US$150m). GG continued to pay down its short-term debt, as 1H16 gross gearing declined by Rp750bn (US$56m) qoq to Rp11.8tr (US$887m), implying debt-to-equity ratio of 0.33x (vs. 0.54x in FY15). We expect debt to rise in 2H as: 1) GG paid dividends (Rp5tr in Jul 16) and 2) raw materials stocking up typically occurs in 2H (harvest time).

Maintain Add We cut our FY16-18 EPS forecasts by 3-5% to incorporate higher A&P spending. This lowers our target price to Rp92,000, still based on 21.5x CY17 /E (1 s.d. above 10-year mean). GG currently trades at 19x CY16 P/E and 16x CY17 P/E, making it one of the cheapest consumer staple stocks under our coverage. The risk is a lower-than-expected ASP hike as we estimate it to contribute c.10% revenue growth.

▎Indonesia

ADD (no change) Consensus ratings*: Buy 17 Hold 3 Sell 2

Current price: Rp67,525

Target price: Rp92,000

Previous target: Rp95,000

Up/downside: 36.2%

CIMB / Consensus: 20.0%

Reuters: GGRM.JK

Bloomberg: GGRM IJ

Market cap: US$9,909m

Rp129,924,040m

Average daily turnover: US$6.99m

Rp92,630m

Current shares o/s: 1,924m

Free float: 26.9% * Source: Bloomberg

Key changes in this note

FY16F EPS decreased by 4.86%.

FY17F EPS decreased by 2.91%.

FY18F EPS decreased by 3.35%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -0.6 -2.5 43.7

Relative (%) -5.3 -10.3 33.2

Major shareholders % held Suryaduta Investama 66.8

Suryamitra Kusuma 6.3

Analyst(s)

Linda LAUWIRA

T (62) 21 3006 1734 E [email protected]

Margaretta OCTIANA T (62) 21 3006 1738 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (Rpb) 65,186 70,366 78,159 88,237 99,632

Operating EBITDA (Rpb) 10,067 11,654 12,790 14,717 16,384

Net Profit (Rpb) 5,406 6,436 6,735 8,250 9,671

Core EPS (Rp) 2,803 3,317 3,500 4,288 5,026

Core EPS Growth 24.3% 18.3% 5.5% 22.5% 17.2%

FD Core P/E (x) 24.09 20.36 19.29 15.75 13.43

DPS (Rp) 800 800 2,609 1,750 2,144

Dividend Yield 1.18% 1.18% 3.86% 2.59% 3.17%

EV/EBITDA (x) 14.56 12.69 11.50 9.72 8.54

P/FCFE (x) 64.59 47.87 30.16 31.47 48.41

Net Gearing 50.0% 46.9% 42.9% 29.0% 19.7%

P/BV (x) 3.94 3.43 3.28 2.92 2.60

ROE 17.3% 18.0% 17.4% 19.6% 20.5%

% Change In Core EPS Estimates (4.86%) (2.91%) (3.35%)

CIMB/consensus EPS (x) 0.97 1.04 1.06

86.0

101.6

117.1

132.7

148.2

36,000

46,000

56,000

66,000

76,000

Price Close Relative to JCI (RHS)

2

4

6

Aug-15 Nov-15 Feb-16 May-16

Vol m

9

Food & Beverages│Indonesia│Equity research│July 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Mayora Indah Recovery intact, margin hit by sugar

We deem 1H16 core net profit of Rp696bn (US$53m, +27% yoy) in line, at 53/54% ■of our/consensus FY16 estimates, given the earlier festive season.

MYOR posted domestic sales recovery of 34% in 1H16 (vs. -16% in 1H15), which ■was strong even after taking into account the festivities in Jul.

2Q16 gross margin (GPM) declined by 250bp qoq due to the sugar price spike, the ■margin improvement remained evident in pushing for the sharp core profit rebound.

We maintain our FY16-18 EPS estimates, Add call and target price, still based on 3-■year mean forward rolling P/E of 29x.

Strong topline growth 1H16 sales rose 23% yoy, while 2Q16 sales increased 13% yoy (but -2% qoq). The yoy sales improvement was underpinned by domestic sales recovery, as it accounted for 57% of 1H16 revenue (vs. 53% in 1H15) and 60% of 2Q16 revenue (vs. 55% in 1Q16). This was partly due to the earlier timing of the Eid period on 6-7 Jul 2016. Management concurs with our view that domestic sales are firming up in 2016, after a soft 2015.

Sales mix changed slightly There was a slight change in 2Q16 sales mix, as the food processing contributed 53% of revenue (vs. 48% in 2Q15), while coffee/cocoa processing accounted for 47% (vs. 52% in 2Q15). Again, the change in the domestic festive celebration affected the mix.

Margin hurt by sugar price surge 2Q16 GPM declined by 250bp qoq and 330bp yoy, following margin contraction in food processing (-560bp yoy) and coffee/cocoa processing (-70bp yoy). The sugar price spike of c.25% YTD was the main culprit, as it accounted for c.26% of COGS. We estimate a 5% increase in sugar price would lower GPM by c.94bp. Weaker wheat price and improving coffee GPM (as price war subsides) are likely to offset margin pressure.

Forex loss in 1H16 versus gain in 1H15 MYOR had a cash hoard of Rp1.4tr (US$109.9m) in 2Q16, of which 64% was in US$. However, its entire gross debt amounting to Rp4.3tr (US$331.2m) is denominated in Rp. Hence, it recorded forex loss of Rp142bn (US$10.9m) in 1H16 vs forex gain of Rp112bn (US$8.5m) in 1H15. Note that export sales were Rp3.9tr (US$301.4m) in 1H16.

Balance sheet position largely unchanged 1H16 OCF was negative Rp400bn (US$30.5m), mainly due to: 1) higher labour costs as the 13

th month salary was paid in 2Q16, 2) higher working capital, due to the Eid period.

This pushed gross debt up 3% qoq, yet, net gearing declined to 51% in 2Q16 (vs. 58% in 2Q15). 1H16 capex was Rp150bn (US$11.5m), posting 23% of FY16 guidance.

Add rating and target price maintained MYOR will continue to benefit from the catalyst of improving mass consumers’ purchasing power, in our view. We maintain our EPS estimates but note that our FY16 sales forecast is 4% lower than MYOR’s guidance. Our target price is unchanged. Key risk is spike in raw material costs that could curtail margin recovery.

▎Indonesia

ADD (no change) Consensus ratings*: Buy 7 Hold 3 Sell 0

Current price: Rp39,700

Target price: Rp46,000

Previous target: Rp46,000

Up/downside: 15.9%

CIMB / Consensus: 21.8%

Reuters: MYOR.JK

Bloomberg: MYOR IJ

Market cap: US$2,708m

Rp35,505,616m

Average daily turnover: US$0.13m

Rp1,689m

Current shares o/s: 894.4m

Free float: 66.9% * Source: Bloomberg

Key changes in this note

No change

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 1.9 12.6 45

Relative (%) -2.8 4.8 34.5

Major shareholders % held Unita Branindo 32.9

Public & others

Analyst(s)

Margaretta OCTIANA

T (62) 21 3006 1738 E [email protected]

Linda LAUWIRA T (62) 21 3006 1734 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (Rpb) 14,169 14,819 16,860 19,154 22,199

Operating EBITDA (Rpb) 1,302 2,331 2,535 2,887 3,426

Net Profit (Rpb) 404 1,220 1,306 1,526 1,861

Core EPS (Rp) 464 1,244 1,460 1,706 2,081

Core EPS Growth (47%) 168% 17% 17% 22%

FD Core P/E (x) 85.49 31.91 27.20 23.27 19.07

DPS (Rp) 230.0 160.0 341.0 364.9 426.4

Dividend Yield 0.58% 0.40% 0.86% 0.92% 1.07%

EV/EBITDA (x) 30.32 16.19 14.80 12.99 10.90

P/FCFE (x) NA 37.9 NA 573.1 166.9

Net Gearing 95.4% 40.9% 29.8% 24.1% 17.6%

P/BV (x) 8.91 6.99 5.84 4.88 4.05

ROE 10.7% 24.6% 23.4% 22.8% 23.2%

CIMB/consensus EPS (x) 0.97 0.95 1.01

86.0

103.5

121.0

138.5

156.0

23,000

28,000

33,000

38,000

43,000

Price Close Relative to JCI (RHS)

100

200

300

400

Aug-15 Nov-15 Feb-16 May-16

Vol th

10

Property│Indonesia│Equity research│July 29, 2016

Sector Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

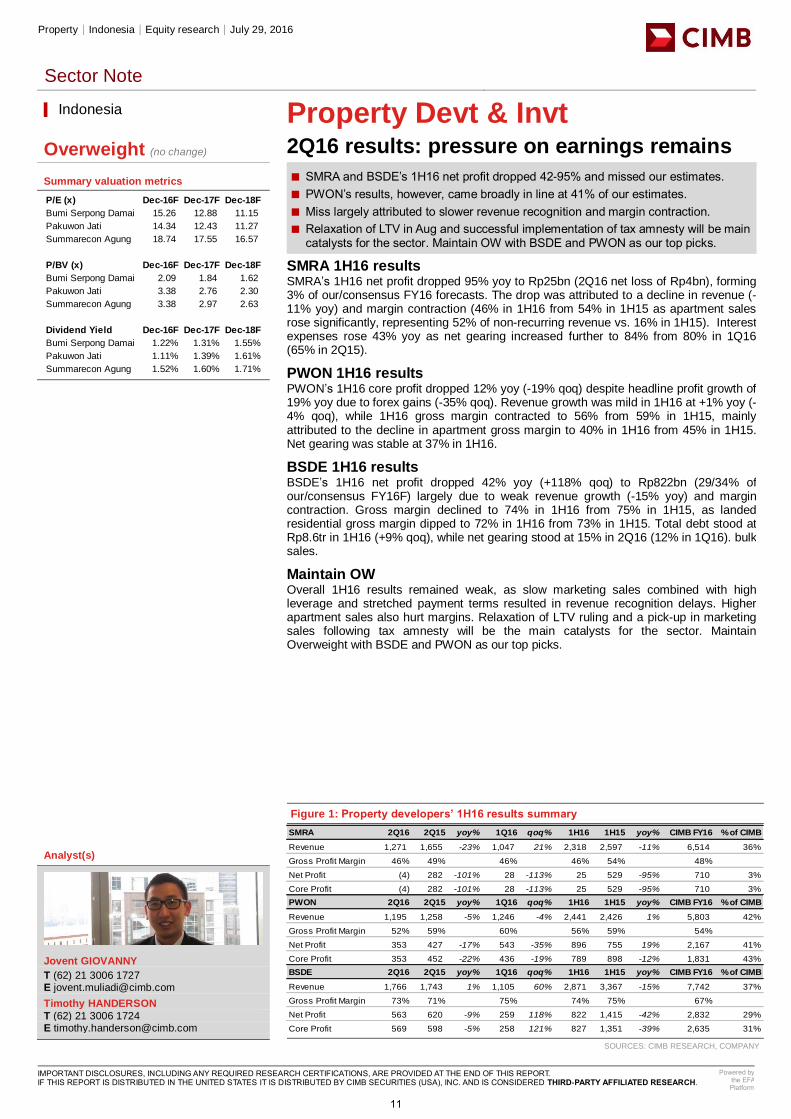

Property Devt & Invt 2Q16 results: pressure on earnings remains

SMRA and BSDE’s 1H16 net profit dropped 42-95% and missed our estimates. ■ PWON’s results, however, came broadly in line at 41% of our estimates. ■ Miss largely attributed to slower revenue recognition and margin contraction. ■ Relaxation of LTV in Aug and successful implementation of tax amnesty will be main ■catalysts for the sector. Maintain OW with BSDE and PWON as our top picks.

SMRA 1H16 results SMRA’s 1H16 net profit dropped 95% yoy to Rp25bn (2Q16 net loss of Rp4bn), forming 3% of our/consensus FY16 forecasts. The drop was attributed to a decline in revenue (-11% yoy) and margin contraction (46% in 1H16 from 54% in 1H15 as apartment sales rose significantly, representing 52% of non-recurring revenue vs. 16% in 1H15). Interest expenses rose 43% yoy as net gearing increased further to 84% from 80% in 1Q16 (65% in 2Q15).

PWON 1H16 results PWON’s 1H16 core profit dropped 12% yoy (-19% qoq) despite headline profit growth of 19% yoy due to forex gains (-35% qoq). Revenue growth was mild in 1H16 at +1% yoy (-4% qoq), while 1H16 gross margin contracted to 56% from 59% in 1H15, mainly attributed to the decline in apartment gross margin to 40% in 1H16 from 45% in 1H15. Net gearing was stable at 37% in 1H16.

BSDE 1H16 results BSDE’s 1H16 net profit dropped 42% yoy (+118% qoq) to Rp822bn (29/34% of our/consensus FY16F) largely due to weak revenue growth (-15% yoy) and margin contraction. Gross margin declined to 74% in 1H16 from 75% in 1H15, as landed residential gross margin dipped to 72% in 1H16 from 73% in 1H15. Total debt stood at Rp8.6tr in 1H16 (+9% qoq), while net gearing stood at 15% in 2Q16 (12% in 1Q16). bulk sales.

Maintain OW Overall 1H16 results remained weak, as slow marketing sales combined with high leverage and stretched payment terms resulted in revenue recognition delays. Higher apartment sales also hurt margins. Relaxation of LTV ruling and a pick-up in marketing sales following tax amnesty will be the main catalysts for the sector. Maintain Overweight with BSDE and PWON as our top picks.

[ X ]

Figure 1: Property developers’ 1H16 results summary

SOURCES: CIMB RESEARCH, COMPANY

▎Indonesia

Overweight (no change) Summary valuation metrics

Analyst(s)

Jovent GIOVANNY

T (62) 21 3006 1727 E [email protected]

Timothy HANDERSON

T (62) 21 3006 1724 E [email protected]

SMRA 2Q16 2Q15 yoy% 1Q16 qoq% 1H16 1H15 yoy% CIMB FY16 % of CIMB

Revenue 1,271 1,655 -23% 1,047 21% 2,318 2,597 -11% 6,514 36%

Gross Profit Margin 46% 49% 46% 46% 54% 48%

Net Profit (4) 282 -101% 28 -113% 25 529 -95% 710 3%

Core Profit (4) 282 -101% 28 -113% 25 529 -95% 710 3%

PWON 2Q16 2Q15 yoy% 1Q16 qoq% 1H16 1H15 yoy% CIMB FY16 % of CIMB

Revenue 1,195 1,258 -5% 1,246 -4% 2,441 2,426 1% 5,803 42%

Gross Profit Margin 52% 59% 60% 56% 59% 54%

Net Profit 353 427 -17% 543 -35% 896 755 19% 2,167 41%

Core Profit 353 452 -22% 436 -19% 789 898 -12% 1,831 43%

BSDE 2Q16 2Q15 yoy% 1Q16 qoq% 1H16 1H15 yoy% CIMB FY16 % of CIMB

Revenue 1,766 1,743 1% 1,105 60% 2,871 3,367 -15% 7,742 37%

Gross Profit Margin 73% 71% 75% 74% 75% 67%

Net Profit 563 620 -9% 259 118% 822 1,415 -42% 2,832 29%

Core Profit 569 598 -5% 258 121% 827 1,351 -39% 2,635 31%

P/E (x) Dec-16F Dec-17F Dec-18F

Bumi Serpong Damai 15.26 12.88 11.15

Pakuwon Jati 14.34 12.43 11.27

Summarecon Agung 18.74 17.55 16.57

P/BV (x) Dec-16F Dec-17F Dec-18F

Bumi Serpong Damai 2.09 1.84 1.62

Pakuwon Jati 3.38 2.76 2.30

Summarecon Agung 3.38 2.97 2.63

Dividend Yield Dec-16F Dec-17F Dec-18F

Bumi Serpong Damai 1.22% 1.31% 1.55%

Pakuwon Jati 1.11% 1.39% 1.61%

Summarecon Agung 1.52% 1.60% 1.71%

11

Personal Products│South Korea│Equity research│July 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Amorepacific Corp Focus on the big picture

2Q OP was 11.1% below our estimate, mainly due to retrospective booking of ■increased payroll cost (W8bn) and weak earnings in the hypermarket channel.

We expect exponential growth in the Chinese subsidiary, after it posted more than a ■50% yoy sales growth in 2Q, with higher OPM.

2Q net profit came in 7.3% below our forecast. Considering a comfortable base and ■strong China sales, earnings growth is likely to accelerate in 3Q.

We maintain our Add rating, with a lower target price of W520,000, based on a ■FY17F P/E of 31.0x (a 20% premium over the global cosmetics company average)

Mixed 2Q16, OP below our estimate and consensus AP’s 2Q operating profit (OP) was 11.1% below our estimate due to: 1) weak domestic hypermarket channel sales (-15% yoy), and 2) retrospective booking of increased payroll cost. However, despite tighter limits on the number of products each shopper is allowed to purchase across all brands, DFS sales jumped 40%, backed by strong overseas and online DFS sales which accounted for around 30% of DFS revenue. Sales from Aritaum increased only 2% yoy due to the revamping and relocation of some stores.

Surprisingly strong sales growth in Chinese subsidiary Its Chinese subsidiary’s 2Q16 earnings were impressive. Sales from the unit rose by more than 50% yoy. A major surprise was brisk sales for the major 3 brands (Innisfree, Sulwhasoo, Etude). Despite aggressive store expansion, OPM improved yoy backed by 1) robust growth in online sales (more than 80% yoy, accounting for 17% of total China revenue) 2) completion of restructuring in the Mamonde brand, 3) strong SSSG, and 4) full-scale growth by new brands (Ryo, IOPE).

High visibility for strong 3Q earnings Considering a comfortable comparison base in DFS and retrospective increased payroll cost in 3Q15, we expect OP growth to accelerate in 3Q. We also expect to see a strong recovery from Momonde in China, backed by aggressive store expansion (1,573 in 1Q16 to 1,764 in 2Q16) and successful brand renovation. While restructuring in Aritaum and weak hypermarket sales could weigh on domestic earnings, we believe this can be offset by a recovery in lucrative DFS and digital sales.

China business, differentiated growth likely to continue The growth of Korean-style stand-alone stores has been clearly proven again by AP’s 2Q earnings. Faster than expected growth in the number of stores is apparent in both Innisfree and Etude, where Innisfree has already opened all the stores initially targeted for this year (265 stores) through expansion into 2nd-tier cities. We expect to see positive earnings upside from these two brands with higher OPM backed by 1) robust growth in online channel, 2) faster than expected store expansion, and 3) strong SSSG.

Maintain Add, with lower target price of W520,000 We cut 16-17F EPS by 2-3% to factor in weaker than expected earnings in the MC&S and hypermarket channel. Despite robust growth in China, AP’s shares are trading range-bound since 2015. We expect an OP CAGR of 25% into FY18F, which we consider impressive for a consumer staple name. A strong long-term growth outlook with high visibility should support a high valuation premium, and we believe the recent pullback in 2Q16 presents a good buying opportunity for this high quality stock.

▎South Korea

ADD (no change) Consensus ratings*: Buy 33 Hold 2 Sell 0

Current price: W388,000

Target price: W520,000

Previous target: W530,000

Up/downside: 34.0%

CIMB / Consensus: 4.1%

Reuters: 090430.KS

Bloomberg: 090430 KS

Market cap: US$20,247m

W22,681,894m

Average daily turnover: US$34.60m

W40,009m

Current shares o/s: 58.46m

Free float: 50.7% * Source: Bloomberg

Key changes in this note

FY16-17F EPS decreased by 2-3%

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -9.6 -4.8 -8.4

Relative (%) -12.7 -5.9 -7.3

Major shareholders % held Amore Pacific Group 35.4

Kyungbae Suh 10.7

National Pension Service 8.2

Analyst(s)

Hyunah JO

T (82) 2 6730 6132 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (Wb) 3,874 4,767 5,928 7,048 8,128

Operating EBITDA (Wb) 700 920 1,489 1,762 1,792

Net Profit (Wb) 379 578 799 986 1,147

Normalised EPS (W) 6,482 9,878 13,637 16,799 19,537

Normalised EPS Growth 43.1% 52.4% 38.0% 23.2% 16.3%

FD Normalised P/E (x) 59.85 39.28 28.45 23.10 19.86

DPS (W) 650 1,350 1,700 1,900 2,100

Dividend Yield 0.17% 0.35% 0.44% 0.49% 0.54%

EV/EBITDA (x) 31.42 23.58 14.14 11.64 10.90

P/FCFE (x) 245.0 56.2 53.0 41.5 22.7

Net Gearing (25.0%) (30.5%) (40.8%) (44.6%) (52.8%)

P/BV (x) 7.93 6.78 5.60 4.57 3.78

ROE 14.0% 18.6% 21.6% 21.8% 20.9%

% Change In Normalised EPS Estimates (3.09%) (1.58%) (1.52%)

Normalised EPS/consensus EPS (x) 1.13 1.14 1.12

82.0

91.4

100.8

110.1

300,000

350,000

400,000

450,000

Price Close Relative to KOSPI (RHS)

200

400

600

Aug-15 Nov-15 Feb-16 May-16

Vol th

12

Banks│South Korea│Equity research│July 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Industrial Bank of Korea Stable but not attractive

1H16 PPOP came in line at 54% of our full-year forecast but lower credit costs led ■to a better-than-expected net profit (68% of our full-year forecast).

Steep SME growth was achieved in 1H but this is likely to slow down in 2H. ■

Cautious asset quality outlook ahead, in our view. ■

We expect continued uncertainties on the macro front to weigh on the share price. ■

We maintain a Hold rating with an unchanged target price of W12,700. ■

Core earnings broadly in line IBK reported a PPOP of W689bn (US$614m) and net profit of W287bn (US$256m) in 2Q16. PPOP was broadly in-line, but net profit was boosted by lower-than-expected credit costs which fell to 70bps, from 76bps in 1Q16. SG&A increased slightly due to the seasonal compensation (W61bn), resulting in a cost/income ratio of 41.9% vs. 36.5% in 1Q16. Similar to other banks, IBK’s cost control and provision charges were stable.

Lending growth likely to slow Revenue growth was stronger than expected as NIM was sustained qoq while loan growth at 2.9% qoq was the sector’s highest; SME loans grew 2.8% and household loans expanded 3.5% on a qoq basis. Considering its consistently high loan growth (4.6% year-to-date), the incremental loan growth in 2H16 would be limited, in our view. We expect risk weighted assets (RWA) to likely rise in 2H16.

The good and the bad in 2H16 Despite the BOK rate cut in Jun 16, the high proportion of debenture funding (49.5% of total funding in 2Q16) should provide IBK with some support on margin compression compared to the large banks. On the other hand, IBK saw its write-backs slashed by 6% yoy and NPL sales losses expanding by 63% yoy in 2Q16. This indicates rising credit risks in 2H16.

Lingering concerns There is no change to our view of the underlying earnings of IBK. However, uncertainty around the macro outlook for SMEs increase the mid/long-term earnings risks. We acknowledge that IBK’s fundamental earnings trend looks better than expected. However, in terms of share price momentum, we expect the government policy to re-capitalise policy banks (KDB and KEXIM) to continue to be a swing factor to IBK’s earnings.

Maintain Hold After being appointed for a conduit bank, IBK’s share price has corrected and it now trades at 0.41x 16F P/BV. Its stable earnings trend should support the current share price, but we think upside potential is limited. We maintain Hold, with no change to our P/BV based target price. A sudden deterioration/improvement of NPLs and government policy changes to SME loans are risks to our call.

▎South Korea

HOLD (no change) Consensus ratings*: Buy 18 Hold 10 Sell 3

Current price: W11,850

Target price: W12,700

Previous target: W12,700

Up/downside: 7.2%

CIMB / Consensus: -15.9%

Reuters: 024110.KS

Bloomberg: 024110 KS

Market cap: US$5,924m

W6,635,749m

Average daily turnover: US$12.93m

W15,018m

Current shares o/s: 631.8m

Free float: 48.3% * Source: Bloomberg

Key changes in this note

No change.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 5.8 -2.5 -8.1

Relative (%) 2.7 -3.6 -7

Major shareholders % held Ministry of Strategy and Finance 59.8

National Pension 8.21

Analyst(s)

Kathy PARK

T (82) 2 6730 6124 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Net Interest Income (Wb) 4,511 4,631 4,756 5,078 5,419

Total Non-Interest Income (Wb) 44.9 158.7 190.4 205.7 222.1

Operating Revenue (Wb) 4,556 4,790 4,946 5,283 5,641

Total Provision Charges (Wb) (1,162) (1,193) (1,484) (1,672) (1,729)

Net Profit (Wb) 984 1,099 969 983 1,137

Normalised EPS (W) 1,521 1,697 1,478 1,495 1,739

Normalised EPS Growth 23.7% 11.5% (12.9%) 1.2% 16.3%

FD Normalised P/E (x) 7.79 6.98 8.02 7.92 6.81

DPS (W) 430.0 450.0 500.0 550.0 600.0

Dividend Yield 3.63% 3.80% 4.22% 4.64% 5.06%

BVPS (W) 24,234 26,606 27,554 28,683 29,916

P/BV (x) 0.49 0.45 0.43 0.41 0.40

ROE 6.54% 6.67% 5.46% 5.32% 5.94%

Normalised EPS/consensus EPS (x) 0.80 0.78 0.86

76.0

82.0

88.0

94.0

100.0

106.0

10,000

11,000

12,000

13,000

14,000

15,000

Price Close Relative to KOSPI (RHS)

2

4

6

Aug-15 Nov-15 Feb-16 May-16

Vo

l m

13

Finance Companies│South Korea│Equity research│July 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Samsung Card Capturing future growth

2Q16 results surpassed our estimates and were in line with upbeat consensus. ■

The beat came from above-industry volume growth and lower credit costs. ■

A surge in market share thanks to the alliance with SC bank and active marketing. ■

Capital management and high yielding asset growth should catalyse the stock. ■

Maintain Add and raise our SOP-based target price to W59,000. ■

Ahead of expectations SSC reported 2Q16 PPOP and net profit of W172bn (US$154m) and W84bn (US$75m) respectively, beating our estimates (10%) but largely in line with upbeat consensus. Its delinquency ratios continued to fall, keeping its credit costs at a low level of 1.4% (vs. 1.6% in 1Q16). Its interest expense also came down with average funding rate of 2.7% in 2Q16 vs. 2.8% in 1Q16. We believe the robust 2Q16 results reaffirmed our bullish call on Samsung Card given its strong volume growth and well managed credit costs.

Volume over price The market credit transaction volume reached its highest growth level since 2014 in 2Q16 (+10.1% yoy), according to Credit Finance Association. Individual consumption tax cuts and more merchants adopting credit card payments led the strong growth. SSC also reported a sharp rise in transaction volume (+14.9% yoy for personal credit cards), far outpacing the industry volume growth in 2Q16. We expect healthy volume growth to continue in 2H16, thanks to rising online shopping and expanded merchant coverage.

A key beneficiary of low interest rate SSC continued to expand its high yielding lending with the soaring instalment & auto-leasing in 2Q16 (+22% qoq, +84% yoy on a volume basis) as we expected. We acknowledge SSC has expanded its high yielding portfolio in its asset mix since 4Q15 (Fig. 5). SSC is a key beneficiary of low interest rates as it not only benefits from funding cost savings but also from improving asset quality.

Taking share The strategic alliance with SC (Standard Chartered) Bank and SSC’s active marketing initiatives led its credit purchase MS to jump up to 17.2% in 2Q16 (16.7% in 1Q16 and 16.4% in 2Q15). Credit cards’ merchant fee, fully implemented from Mar 16, was largely offset by robust high volume growth in 1H16. We are of view that SSC is clearly changing its growth strategies with more focus on high yielding products and volume growth.

Stay invested – Top pick in Korea financials SSC’s active growth strategy prompted us to revise up our EPS estimates by 8-22% and lower our payout assumptions to 74-90% in FY16-18F. Strong capital management and high-yielding assets growth will continue to serve as key catalysts. We maintain our Add rating and raise our SOP-based target price to W59,000. Key downside risks include a sudden rate hike and unexpected changes in Samsung Group’s restructuring.

▎South Korea

ADD (no change) Consensus ratings*: Buy 15 Hold 4 Sell 0

Current price: W43,150

Target price: W59,000

Previous target: W56,400

Up/downside: 36.7%

CIMB / Consensus: 28.7%

Reuters: 029780.KS

Bloomberg: 029780 KS

Market cap: US$4,463m

W4,999,311m

Average daily turnover: US$4.20m

W4,864m

Current shares o/s: 115.4m

Free float: 27.6% * Source: Bloomberg

Key changes in this note

FY16-18F Revenue increased by 9-10%.

FY16-18F EPS increased by 8-22%.

FY16-18F DPS decreased by 12-33%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 5.2 11.2 16

Relative (%) 2.1 10.1 17.1

Major shareholders % held Samsung Life Insurance 71.9

Analyst(s)

Kathy PARK

T (82) 2 6730 6124 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Net Interest Income (Wb) 2,727 2,960 3,173 3,447 3,703

Total Non-Interest Income (Wb) 794.4 341.8 235.9 191.7 205.4

Operating Revenue (Wb) 3,522 3,302 3,409 3,639 3,908

Total Provision Charges (Wb) (303.1) (272.6) (264.9) (294.2) (330.7)

Net Profit (Wb) 656.0 333.7 342.9 407.2 452.6

Normalised EPS (W) 5,685 2,892 2,971 3,529 3,922

Normalised EPS Growth 140% (49%) 3% 19% 11%

FD Normalised P/E (x) 7.59 14.92 14.52 12.23 11.00

DPS (W) 1,000 1,500 2,200 3,000 3,501

Dividend Yield 2.32% 3.48% 5.10% 6.95% 8.11%

BVPS (W) 55,375 57,957 58,995 62,524 66,446

P/BV (x) 0.78 0.74 0.73 0.69 0.65

ROE 10.4% 5.1% 5.1% 5.8% 6.1%

% Change In Normalised EPS Estimates 8.2% 22.4% 21.6%

Normalised EPS/consensus EPS (x) 1.01 1.16 1.21

74.0

85.3

96.5

107.8

119.0

27,000

32,000

37,000

42,000

47,000

Price Close Relative to KOSPI (RHS)

1

2

3

Aug-15 Nov-15 Feb-16 May-16

Vo

l m

14

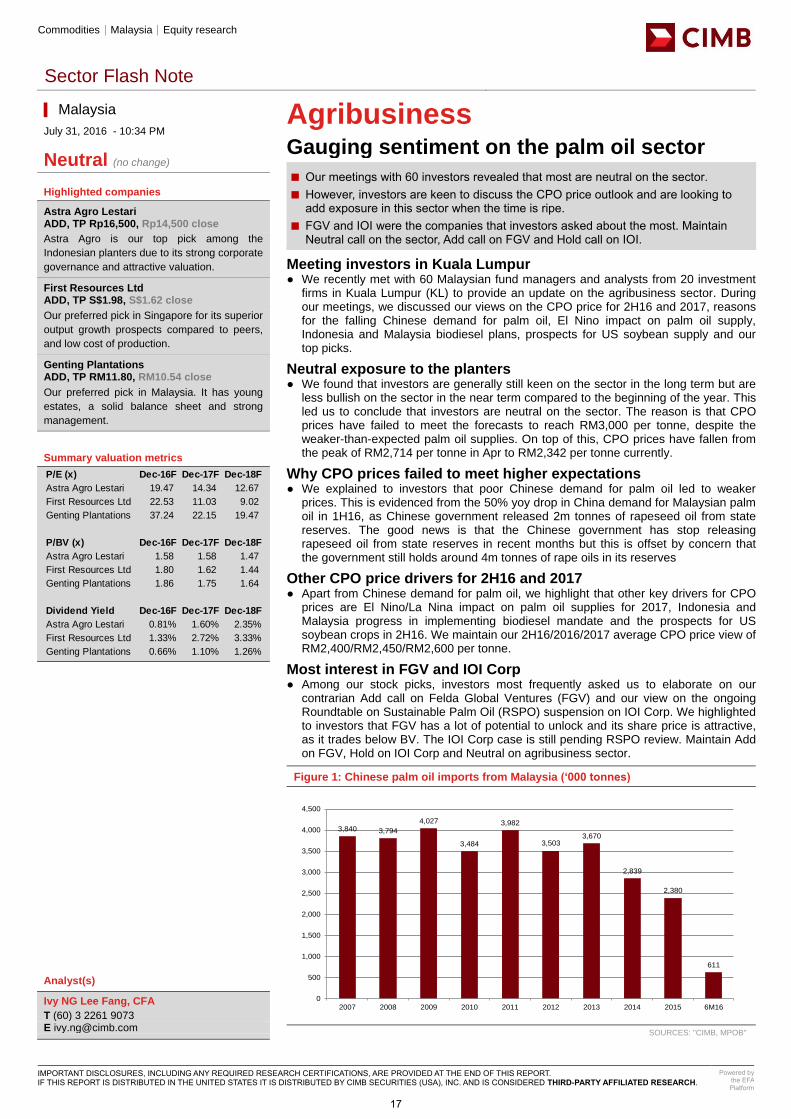

Agribusiness│Malaysia│Equity research│July 30, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Felda Global Ventures The way forward to improve earnings

In an interview with the media, FGV’s CEO shared his plans for improving the ■group’s earnings and investors’ confidence in FGV shares

He also clarified that the group is not aware of any potential suitors for FGV ■

He also revealed potential plans to negotiate for lower land lease expenses ■

We are positive on the group’s plans to boost earnings via improved efficiency ■

We maintain our non-consensus Add call, with SOP target price of RM2.08 ■

Key highlights from interview with CEO In an interview with The Edge Weekly and Starbiz, Felda Global Ventures Holdings’ (FGV) President and CEO Datuk Zakaria Arshad said: (1) he plans to realise the full potential of FGV’s internal capabilities; (2) his biggest challenge is managing organisational behavior; (3) the focus this year is not M&A, reiterating that FGV is no longer in discussions on Eagle High; (4) he is not aware of any potential suitors from Tradewinds or any other companies; and (5) FGV is committed to 50% dividend payout.

Plans to improve earnings and boost investor confidence FGV’s CEO revealed that his mission is to improve the group’s bottomline and investors’ confidence in FGV shares. To achieve this, he is working to enhance the FFB yields for its estates, oil extraction rate of the group’s mills and contain administrative costs. FGV plans to consolidate 2 of its 71 palm oil mills to boost utilisation rate and cut RM100m administrative costs by this year. There are also plans to monetise non-core assets.

Looking at ways to reduce land lease costs The group is also exploring and negotiating for the best land lease agreements with its parent company, FELDA, in a bid to lower costs. This is still in progress, with nothing formulated yet. One possibility could involve reducing the land acreage that are marginal to reduce lease expenses. To recap, under the land lease agreement with FELDA, FGV pays a fixed lease of RM250 per annum and a 15% share of operating profit from the estates.

Some of the key targets for the estates FGV is targeting OER of 20.2% and FFB yield of 19 tonnes/ha. The group achieved its OER target but not FFB due to the El Nino impact. It also plans to reduce its costs of production for crude palm oil (CPO), which was RM1,824 per tonne in 1Q16 to an average of RM1,450 per tonne for 2016. The group withdrew its RSPO certificates due to issues with FELDA’s contractors. It plans to recertify 15 out of its 71 mills this year, and the remainder within the next three years

Positive on CEO’s plans; maintain Add The positive takeaways from the interview are FGV’s plans to lower lease expenses; and improve its estates’ productivity, both of which will help boost future earnings. We are neutral on the news that FGV is not aware of any potential suitors. We maintain our non-consensus Add rating, with unchanged SOP target price of RM2.08. Our SOP implies a P/BV of 1.2x for the group, which is still attractive relative to its Malaysian sector peers’ average of 1.9x. Downside risks include failure to execute plans to improve earnings.

▎Malaysia

ADD (no change) Consensus ratings*: Buy 1 Hold 6 Sell 9

Current price: RM1.85

Target price: RM2.08

Previous target: RM2.08

Up/downside: 12.2%

CIMB / Consensus: 55.3%

Reuters: FGVH.KL

Bloomberg: FGV MK

Market cap: US$1,660m

RM6,749m

Average daily turnover: US$2.99m

RM12.11m

Current shares o/s: 3,648m

Free float: 58.6% * Source: Bloomberg

Key changes in this note

No changes

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 20.1 27.6 12.1

Relative (%) 19.4 28.8 14.8

Major shareholders % held Federal Land Development Authority 20.0

Felda Asset Holdings 13.7

Lembaga Tabung Haji 7.8

Analyst(s)

Ivy NG Lee Fang, CFA

T (60) 3 2261 9073 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (RMm) 16,462 15,700 15,738 16,769 17,725

Operating EBITDA (RMm) 1,269 973 1,069 1,316 1,592

Net Profit (RMm) 306.4 139.6 162.5 334.1 516.0

Core EPS (RM) 0.10 (0.02) 0.04 0.09 0.14

Core EPS Growth 200% (123%) 106% 54%

FD Core P/E (x) 19.14 NA 41.53 20.20 13.08

DPS (RM) 0.10 0.04 0.03 0.06 0.10

Dividend Yield 5.41% 2.16% 1.62% 3.24% 5.41%

EV/EBITDA (x) 6.43 12.40 11.38 9.35 7.41

P/FCFE (x) 34.29 20.08 5.43 5.22 5.57

Net Gearing (9.2%) 33.4% 30.3% 27.7% 18.8%

P/BV (x) 1.06 1.05 1.04 1.02 1.00

ROE 5.45% (1.25%) 2.51% 5.10% 7.71%

CIMB/consensus EPS (x) 1.04 1.31 1.63

74.0

84.0

94.0

104.0

114.0

124.0

1.10

1.30

1.50

1.70

1.90

2.10

Price Close Relative to FBMKLCI (RHS)

50

100

Jul-15 Nov-15 Feb-16 May-16

Vo

l m

15

Airports│Malaysia│Equity research│July 29, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Malaysia Airports Holdings Golden opportunity to accumulate

MAHB’s group 1H16 core net profit of RM110m almost touched our previous full-■year forecast of RM121m, due to better-than-expected performance in Malaysia.

Turkey delivered a small 1H16 core net loss that was in line with our forecasts which ■had already been significantly reduced in our 15 May and 16 July reports.

This is an opportune time to accumulate MAHB, as the current share price does not ■factor in any PSC tariff hike, and prices ISG at an 80% discount to its intrinsic value.

We maintain Add, and raise our DCF-based target price to RM8.30, as we model ■higher Malaysian passenger traffic growth with price competition heating up.

Highlights of 2Q16 MAHB’s Malaysian operations delivered a RM54m core profit in 2Q16 vs. a loss of RM29m during last year’s 2Q. This exceeded our forecasts as lower bonus provisions kept a lid on staff costs. Istanbul Sabiha Gokcen (ISG) incurred a small core net loss of €1.2m in 2Q16, which was in line with expectations given the worsening security situation in Turkey, but disappointing against our expectations at the start of this year.

Traffic growth not particularly inspiring Malaysian 2Q16 pax traffic was flat against last year, but the pax mix improved with higher growth at KLIA MTB compared to klia2 (due to Malindo transferring to MTB from 15 March), and with international traffic growing as opposed to the decline seen in domestic traffic. The latter was related to Ramadan falling squarely in June this year. ISG saw its traffic growth slow down significantly to just 6% yoy in 2Q16, as tourist arrivals fell and airline expansion became more difficult with a congested runway.

What is in the share price? The current share price of RM5.85 implies an equity valuation of RM9.7bn for the group. Our DCF valuation of the Malaysian business is RM9.3bn assuming no PSC hikes, leaving a residual value of RM406m for ISG based on the current market cap. This compares against our DCF value of RM1.9bn for ISG. The market is therefore pricing ISG at an 80% discount to its long-term intrinsic value. We do not think such a large discount is appropriate or necessary, even in the face of near-term demand weakness.