asia in a global context - dbs bank in a global context... · pricing power “slacks ... rapid...

TRANSCRIPT

.

Confidential – Not For Redistribution

Asia in a Global Context

2 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Table of Contents

Building Nikko AM’s Investment Capabilities

Asia in a Global Context

Asia in a Historical Context

China Playbook

The Coming “Big Rotation”

Japan: Asia’s Other Giant

The Sun is Rising in Japan

Asia: The 4 Key Themes for Asia

The Prescription: How to Invest in Asia’s Growth

Section 1

Section 2

Section 3

Section 4

Section 5

Section 6

Section 7

Section 8

Section 9

3 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Asia Investment Timeline

Nikko AM’s Investment Professionals: Total 200 as of Mar. 2015

Spectrum of Investment Activeness

Building Nikko AM’s Investment Capabilities

We are an “Asia

based Global Asset

Management firm”

While we have built

out our in-region

capabilities, our 200

investment

professionals span

over all major

markets around the

world

Mar 2011 Acquired Tyndall AM

Sep 2011 Purchased DBS AM

Apr 2007 Acquired 40% stake in “Rong Tong Fund Management

Apr 2015 Apr 2014 Apr 2013 Apr 2012 Apr 2011 Apr 2008 Apr 2007

Oct 2013 New Asian Equity team joins from TAAM

Aug 2012 Invested in Ambit Investment

Advisors

Japan Singapore

& HK

Australia

& NZ Europe US

PMs 49 19 18 10 8

Analysts 24 11 9 5 3

Other 27 6 6 3 2

Total: 200 100 36 33 18 13

China Oceania SG & ASEAN India

Dec 1959

Japan

Dec 1959 Tokyo office opens

4 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Building Nikko AM’s Investment Capabilities (continued)

As of 2014, Nikko

AM’s investment

professionals have

produced more than

50 Thought

Leadership pieces

focusing on all

regions across Asia

5 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Building Nikko AM’s Investment Capabilities (continued)

Product Prioritization

“Barbell” investment capability will capture institutional client needs: high conviction-high alpha active strategies and cost-effective passive strategies

Globally-integrated, dynamic asset allocations will address the needs of both retail and institutional investors

Demand for asset

diversification and

risk mitigation is

driving the industry

to build skill-sets to

address both needs

We have the

solutions to meet

your demands Benchmark

Agnostic

Benchmark

Driven

Investment Philosophy

Distinctively

Active

Efficiently

Passive

6 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Asia in a Global Context

Asia dominated by

two giants: China

and Japan

Although moderate

deflation may seem

abnormal and

therefore dangerous

to investors

accustomed to

secular inflation

since World War II,

short periods of

deflation have been

common in

American history¹

Prices have been

relatively stable over

the long term; they

were actually no

higher in 1940 than

in 1795¹

Deflation does not have to be Great Depression

Lower prices with moderate growth can be very good for the investment market…

“Goldilocks” 1Source: E. Kerschner, “Flations: Inflation and Deflation”, extracted as of 31 May 2015

Inflation is Coming

Monetarist view Zero to negative interest rates Excessive debt incurred by governments

Deflation is Coming

Developed Markets’ population growth = negative growth Pricing Power “slacks” Financial repression

Economists’ Debate:

The answer lies in extending the scope of economic history the last 200 years…

Source: CEIC, Morgan Stanley Research 13 April 2015. *Data as of March 2015 for China, Taiwan and Thailand; 4Q 20114 for HK and February 2015 for others.

Producer Price Deflation Across Asia

Source: Bloomberg, Bank of Singapore, extracted as of 31 May 2015

7 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Asia in a Historical Context

Like China, U.S. in 19th Century was also primarily rural land that increased its urbanization and industrialization - becoming world manufacturing hub

In 1860s-1880s U.S., prices declined but productivity rose following effects of technology, increased reform and competition

Modern Asian economies have all followed similar pattern of growth – wild geese analogy

With Japan as the lead goose

China has become a late 20th Century global growth center following the Information Revolution and growing globalization

Headed in similar direction of increased openness and competitive trend

After around 20 years of secular deflation with low productivity and spending, Japan is finally taking steps to shift to inflationary mindset

China is an example

of Good Deflation –

following path of late

19th Century U.S.:

1) Rise of an

economic

superpower creating

unprecedented

productive capacity

2) Technological

breakthroughs in key

industries causing

oversupply

3) Globalization

U.S. CPI, 1800-1900

Source: Mises Institute, “Deflating the Deflation Myth”,

extracted as of 31 May 2015

China CPI, 1995-Present

Source: www.tradingeconomics.com, National Bureau of Statistics of China, extracted as of 31 May 2015

8 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

China Playbook

British referred to U.S.’ 19th Century growth and production as the “American System

of Manufactures”¹ – but the U.S. should now be switched with China

At end of 1999, China was ranked #7 largest economy with GDP USD $1.0 trn

As of 2013, it ranked #2 with GDP USD $9.2 trn, changing the global economic environment and creating new paradigm

However, it must slow down “catch-up growth” tactics be sustainable and avoid market crisis – opposite of Japan’s collapse of bubble after 1980s

During this Good

Deflationary period,

China is following

the footsteps of

Japan, Taiwan and

Korea

We believe China

will become nexus of

global equity

investing - not

because of growth

rate, but because of

previous trajectories

followed by the other

countries mentioned

However,

normalizing growth

trends leaves us

bearish on

commodities and oil

Source: 1Time, “How China is like 19th Century America”; World Bank; extracted as of 31 May 2015

No. Country GDP in 1999

(USDbn) No. Country

GDP in 2013 (USDbn)

1 U.S. 9,660 1 U.S. 16,768

2 Japan 4,432 2 China 9,240

3 Germany 2,196 3 Japan 4,919

4 U.K. 1,558 4 Germany 3,730

5 France 1,500 5 France 2,806

6 Italy 1,249 6 U.K. 2,678

7 China 1,083 7 Brazil 2,245

2013 China’s GDP greater than Germany, U.K. & France…COMBINED

+753% =9,214

Top 7 Economies by GDP, 1999 vs. 2013

Source: World Bank

9 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

China Playbook (continued)

China seen as following the same two-stage development processes as Japan, Taiwan and Korea did

Stage 1: (Japan 1950s-70s; China 1980s-00s)

Rapid economic growth and high productivity coinciding with capital controls and tightly

managed exchange rates

China’s growth has

been through

mobilizing

resources, moving

labor to cities and

increasing industrial

output

However Stage 1 of

Asia growth cannot

be sustained without

opening market

Source: World Bank, Gavekal, extracted as of 31 May 2015

Per-Capita GDP Per-Capita GDP Growth

Source: Barron’s, The Maddison-Project, 2013 version., Jan 2013 Note: 1990 International Geary-Khamis (GK) dollar: A hypothetical unit of currency that has the same purchasing power parity that the USD had in the U.S. in 1990

10 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

China Playbook (continued)

Stage 2: (Japan 1970s-90s; China now)

Loosened capital controls and freed up exchange rates leading to improved equity

performance

This process has been followed by opening of capital markets and competition – driving productivity

Slow-down will

create equity

investing

opportunities –

reform and market

opening lead to

greater competition,

profitability

Nominal GDP Nikkei Index

1960s 380% 170%

1970s 240% 180%

1980s 90% 510%

Decade-by-decade cumulative gains in Japan

Nominal GDP and the Nikkei Index

Source: Gavekal, extracted as of 31 May 2015

11 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

China Playbook (continued)

Positioning RMB as a global reserve currency

Qualified Foreign Institutional Investor (QFII & RQFII) program to attract capital into RMB-based EQ and FI

Shanghai-Hong Kong Stock Connect for cross-border sales of securities

Limited to mainland institutional or private investors with 500,000 yuan (~USD 80 thousand) on account, there has been recent news of lowering capital requirements for more participants

China is taking key

steps to open its

economy and capital

account

Source: SG Cross Asset Research/Economics, extracted as of 31 May 2015

China’s Reform Timeline

12 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

The Coming “Big Rotation”

Because of capital controls, China’s market cap is not reflected in Global Equity

Indices

China is ~15% of world GDP but only 2.4% of MSCI ACWI

Potentially grossly understated due to its semi-closed nature

If controls were relaxed, China’s weighting would jump from 2.4% to 4.8% of MSCI

AWI and from 18.8% to 37.5% of MSCI EM

As China removes

investment barriers,

it will become a

larger part of global

equity indices

Because of this, we

believe China’s

weighting in MSCI

will increase

significantly as

capital controls are

relaxed

Source: MSCI, The Conference Board Global Economic Outlook 2014, May 2014

Hypothetical Weight of MSCI ACWI Hypothetical Weight of MSCI EM

13 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

The Coming “Big Rotation” (continued)

China has 1,874

listed companies

with market cap

greater than USD

500mn

9x more companies

than in HK, Taiwan

and Korea

Number of Listed Companies Above USD 500mn Market Cap by Country

Source: Factset, Goldman Sachs Investment Research, March 6 2015

14 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Japan: Asia’s Other Giant

Japan suffered from bad deflation for more than two decades

Policy errors, poor QE execution combined with bad demographics trend and strong currency

These all lead to prescription of first two Abenomic arrows

While Abenomics has yet to deliver inflation target of 2%, it created a boom for the stock market

China has seen the

mistakes made by

the lead goose

Japan’s Lost Decade

was the precursor

for Prime Minister

Abe’s first two

Arrows for re-growth

Source: WSJ, extracted as of 31 May 2015

Source: Reuters, extracted as of 31 May 2015

15 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Japan: Asia’s Other Giant (continued)

High correlation between Nikkei and JPY depreciation between 2013-14 evidence

Though correlation starting to break down, we believe market is starting to price in two longer term effects of Abenomics – a “New Goldilocks” market

Stronger economic fundamentals

Corporate earnings growth

First two Arrows

have led yen to fall

by 40%, with stock

market almost

doubling – the best

performance in over

a decade

The percentage of

net cash-firms has

now risen to more

than 50%, which is

an overwhelmingly

high level compared

with past averages

and global trends

Breakdown of Currency-Equity Linkage Growth in Exports and Imports (YoY)

Source: Nikko Asset Management based on data from Bank of Japan as of 31 January 2015 Source: Gavekal Data, Macrobond as of 31 March 2015

16 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

The Sun is Rising in Japan

We are now seeing signs that the third Arrow is making effects in various aspects

Female participation rate - Women in management roles has risen from 6.9% in Jun 2012 to 8.3% in Jun 2014

Trade Agreements – Trans Pacific Partnership agreement expected to be reached by end of 2015 or early 2016

Corporate Governance - reforms leading to higher ROE and lower corporate tax rates, leading to investments

Companies that have announced reforms have recorded strong share price performance

52 companies that announced reforms since 2014 have outperformed TOPIX by average of 5.7% a month after their respective announcements¹

Ex: Yahoo Japan announced doubling year-end dividend on Mar. 19 2015

The third Abenomic

Arrow is underway,

influencing

Japanese companies

to make various

structural reforms

Source: Goldman Sachs, Factset as of 16 April 2015

TOPIX-relative Performance (Equal-weighted) of 52

companies that have announced reforms since 2014 Global Comparison of Net Cash-Firms

Source: Nomura and Nikko AM, based on TSE, MSCI and S&P data extracted as of 31 May 2015

17 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

The Sun is Rising in Japan (continued)

Japan to benefit most from TPP - Only 18% of Japan’s trade falls under free trade

agreements - South Korea’s 43%¹

GPIF has reallocated its weighting of Japanese equities from 12% to 25%¹

Total equity allocation from 24% to 50% - Domestic institutions expected to follow

Corporate Governance reforms leading to higher ROE and lower corporate tax rates – leading to investments²

Bottom-Up: average profit margin for listed companies rose to 4.61% in Q1-15 vs. last peak of 4.64% in Q4-07

Top-Down: Corporate profit margins (ex-financials) hitting a new high of 5.3% in 4Q-14

There are still

skeptics of the

Japanese market,

but they don’t realize

bull market is still

young

“A bull climbs many

walls of worries” –

we believe that the

equity gain is

sustainable

TPP participation,

GPIF reallocation

and Corporate

Governance Code

are catalysts for

Japan’s sustainable

equity growth

Source: 1 BCA Research, 2 Gavekal, extracted as of 31 May 2015 Source: Gavekal, as of 31 May 2015

U.S.

18 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Asia: The 4 Key Themes

Taking into consideration demographics, wage growth and a burgeoning middle class, we have 4 Key investment themes for Asia:

‘Old Asia to New Asia’: Don’t look backwards

As ‘Old Asia’ evolves

into ‘New Asia’,

investors need to

consider where

growth will come

from in the future

We have identified

Four Key Themes

Healthcare Tourism Insurance Environment

Sector represents only 6% of Chinese GDP1

China one of lowest

health spenders as % of GDP, though urbanization creating growth

Medical Tourism: 5 of

Top 10 destinations in Asia2

Asia-Pac 2nd in no. of

tourism arrivals at

28.4%3

No. of outbound Chinese tourists has doubled in past 4 years - we expect it to double in 5 years

Share of total global premiums set to grow

Ageing populations will boost demand for life insurance in Ems4

Non-life insurance will

profit from increased

urbanization,

expanding middle

class and rising

economic wealth4

China & US agreement to tackle carbon dioxide emissions

China has pledged to make clean energy sources, such as solar

power, account for

20% of the country's

total energy

production by 2030

1Source: World Health Organization, as of August 2014 2Source: Medical Travel Quality Alliance. http://www.mtqua.org/providers/top-10-worlds-best-hospitals-for-medical-tourists-new/ 3Source: UN Economic and Social Commission for Asia Pacific Statistical Yearbook 2013, UN World Tourism Organization 4Source: Swiss Re sigma Study on World Insurance 2012

19 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

The Prescription: How to Invest in Asia’s Growth

China

Invest in sectors/companies that will perform well in a deflationary environment with increasing capital openness and competition

Reforms which happen every two decades in China are significant and happening now - Investment

opportunities abound in this environment

Sectors include Insurance, Environmental, Technology, Tourism, Consumption and Healthcare

Stock examples: China Medical System, China Taiping Insurance, CT Environmental, and

Sinopharm

Japan

Turnaround Opportunity: Undervalued global brands that are transforming their business portfolio

for high profitability

Improving Corporate Governance: Upside in capital efficiency (increase in Capex/M&A and

Shareholder Returns)

Stock examples: Sony, Nintendo and Toray

ASEAN

Structural drivers in place and remain bullish: Rise of affluence and consumerization driven by

young and fast growing labor force, rising middle class and increasing urbanization FDI will be ASEAN’s future lever for economic success driven by boom in infrastructure and greater

liberalization and connectivity in trade and services (e.g. ASEAN Economic Community by 2015)

Positive on Philippines, Indonesia and Singapore: Greatest opportunities are in logistics, financial services, consumer and infrastructure

Any securities shown are for illustration purposes only and are not stock recommendations.

20 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

The Prescription: How to Invest in Asia’s Growth (continued)

Buy Asia as your Core Holdings in a global diversified portfolio - Japan should outperform all Developed Markets as catalysts from Abe’s structural reforms unfold.

Asia is on a deflationary path as well as exporting deflation elsewhere. Include

long duration bonds in a balanced portfolio

Best combination: Long duration Asian Bonds and Asian Equity

Buy companies, not indices

Well researched, high conviction portfolios of emerging Asian brands in key sectors will outperform market indices which track the “Old Asia”.

The most effective

way for investing

into Asia involves

accessing the

relevant core

holdings, and

complementing this

with the appropriate

satellite solutions

Appendix

22 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

China Playbook (continued)

While usually strong

correlation between

equity market

returns and nominal

GDP growth, China

is outlier similar to

Japan in the 1980s

Source: Gavekal, extracted as of 31 May 2015

A-Share equity market starting in the 2000s was overvalued in P/E terms – with average ratio of 50

By 2012, the multiple fell in line to the EM average of 12

23 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Reforms – A Key Element for 2015

Short term sacrifice

for sustainable

longer term growth –

India and China

most promising

Source: Goldman Sachs Global Investment Research 23 November 2014.

24 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

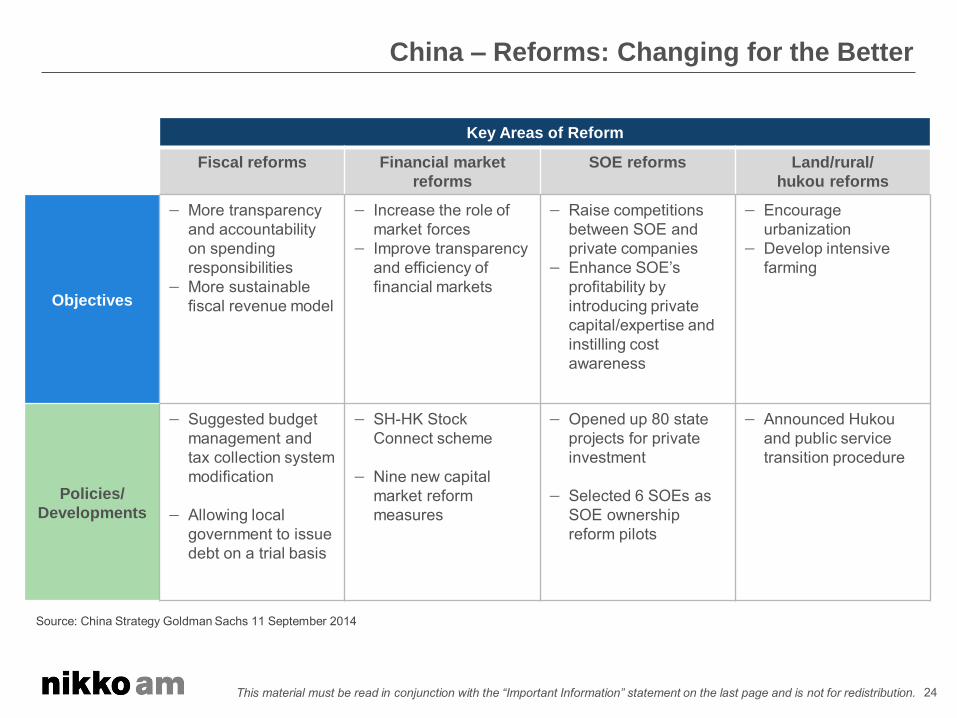

China – Reforms: Changing for the Better

Source: China Strategy Goldman Sachs 11 September 2014

Key Areas of Reform

Fiscal reforms Financial market

reforms

SOE reforms Land/rural/

hukou reforms

Objectives

More transparency and accountability on spending responsibilities

More sustainable fiscal revenue model

Increase the role of market forces

Improve transparency and efficiency of financial markets

Raise competitions between SOE and private companies

Enhance SOE’s

profitability by introducing private capital/expertise and instilling cost awareness

Encourage urbanization

Develop intensive farming

Policies/

Developments

Suggested budget management and tax collection system modification

Allowing local government to issue debt on a trial basis

SH-HK Stock Connect scheme

Nine new capital market reform measures

Opened up 80 state projects for private investment

Selected 6 SOEs as SOE ownership reform pilots

Announced Hukou and public service transition procedure

25 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

China – More Sustainable Future Growth

Share of GDP: More

consumption; less

fixed asset

investment

Less reliance on

factories (Old

China); More on

Healthcare, IT and

consumers (New

China)

Source: China Strategy Morgan Stanley 6 November 2014

Red line shows the relative performance of New China stocks compared to Old China

stocks. Green line shows the MSCI China movement.

26 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Commodity Prices – Fall in Oil Price More Good than Bad

Short term concern for deflation

Positive for consumers

Oil prices – Driven

by supply not post-

crisis demand

decline

Short term concern

for deflation

Positive for

consumers

Source: Bloomberg, BofA Merrill Lynch Global Research 30 October 2014

Impact of 10% decline in oil prices on Current

Account Balance (% GDP)

Declining oil prices pose threat to deflation

27 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Asia and Real Interest Rate

Real interest rates remain generally high in Asia

The largest economy in Asia has room and is poised to further ease monetary conditions

Room for Easier

Monetary Policy

Source: CEIC, Goldman Sachs Global Investment Research 4 March 2015

28 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

China Playbook (continued)

Chinese stocks are

not yet in a bubble

Source: BCA Research, May 2015

29 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

India – Structural Story Remains (Demographic Potential)

Consumption is a

structural theme

Youngest population

globally

Growing middle

class and

aspirations

A revival in

investments

Source: CEIC Data Research Limited, Citi Equity Research 10 September 2014

Consumer and Business Loans (% GDP)

Youngest Population Globally

Source: Edelweiss Research, December 2013

Source: Morgan Stanley 29 April 2015

New Investment Projects (INR Bn)

30 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

India – Stock Picking with Strong Macro Tailwind

Long-term ROE versus PB

Long term Sensex EPS growth versus PE

Market retracement

puts PER and PB

below historical

averages

Multi-year growth –

sectors and stocks

to emerge

Opportunities in

Infrastructure and

Cyclical industries

Source: CLSA May 2015

Source: CLSA September 2014

31 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Tourism – Grown Steadily

Chinese tourist now a global phenomenon and will continue

Increasing disposal incomes, Currency depreciation vis-à-vis Renminbi, Relaxed visa restrictions

Asia-Pacific accounted for 28.4% of the world’s inbound tourists in 2011

Tourism receipts were US$362.6bn, +16.7%

Tourism arrivals were 284m, +8%

International tourism

has recovered to

exceed pre-crisis

(2008-09) levels

Source: UN Economic and Social Commission for Asia Pacific Statistical Yearbook 2013, UN World Tourism Organization.

Outbound tourists:

+16.3% in 2014 to 114m, est.

Source: China National Tourism Administration June 2014. Travel China Guide for 2013.

Any sectors shown are for illustration purposes only and are not to be construed as investment recommendations.

Inbound Tourism Arrivals, World Regions,

1995-2001

32 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Environment

The World needs to change, beginning with the world’s two largest economies

China and US signed bilateral agreement on climate change

Emissions cap by 2030

Target 20% clean energy usage by 2030

Singapore Skyline, 20 Jun 2013 (Top) and 20 Jan 2011

Source: ADB Economics Working Paper Benjamin Sovacool June 2014 News.cn, Xinhuanet..net . APEC Meeting, Beijing November 2014

Share of Greenhouse Gas Emissions of Top 10 countries, 2010

Any sectors shown are for illustration purposes only and are not to be construed as investment recommendations.

33 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Healthcare: 1) Aging population

900mn people of

over 65 years old in

2050 in Asia

Some countries

including Korea,

Thailand and China

are of rapidly ageing

demographics

Any sectors shown are for illustration purposes only and are not to be construed as investment recommendations.

Population of over 65 years, 2015E & 2050E

Source: IMS Institute as of October 2014

0

10

20

30

40

50

60

70

80

90

1990 2010 2030 2050 2070

Republic of Korea

Japan

Thailand

China

Malaysia

Indonesia

India

(%)Estimate

Population trend of over 65 years, 1990-2070E

34 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Healthcare: 2) Current low healthcare spend and poor medical infrastructure

An improved living standard will lift healthcare demands in Asia

The current poor medical infrastructure in Asia implies huge opportunities for the healthcare market

Relationship Between Healthcare Related Expenditure (relative to GDP)

and GDP per capita (2012)

Healt

hcare

rela

ted

exp

en

dit

ure

(re

lati

ve t

o G

DP

)

GDP per capita

Number of Doctors and Beds per 1,000 people (2011)

Source: OECD (Health at a Glance 2013) as of Oct 2014

Source: WHO, IMF (World Economic Outlook, April 2014)

35 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Stock Examples Within the 4 Key Themes

Tourism- Hana Tour

7/13 10/13 1/14 4/14 7/14 10/14 1/15 4/15

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

150,000

Source: FactSet Prices

Closing Price

17-May-2013 to 18-May-2015 (Daily) Price (Local Currency)

Hanatour Service, Inc.

Market Cap US$1.4b

Net Debt to

Equity

Net cash

EPS CAGR (’14-

16)

36%

ROE (FY15e) 18.2

P/E Ratio (FY15e) 30 X

Div Yield

(FY154e)

1.1%

Why we bought Hana Tour:

Market leader in Korea with 21% MS

Structural Growth in outbound travel,

driven by aging population, increasing leave entitlements and air seat supply

Recovery in consumption post the Sewel ferry accident

Meetings with management: 6

BUY 7/12 10/12 1/13 4/13 7/13 10/13 1/14 4/14 7/14 10/14 1/15 4/15

20

25

30

35

40

45

50

55

60

Source: FactSet Prices

Closing Price

18-May-2012 to 19-May-2015 (Daily) Price (Local Currency)

AIA Group Limited

Market Cap US$80bn

RBC Solvency

Ratio

430% (regulatory min.

150%)

EPS CAGR (’14-

16)

12.2%

ROE (FY15e) 11.5%

P/E Ratio (FY15e) 19.7 X

Div Yield

(FY154e)

1.1%

Why we bought AIA Group:

Long term structural demand for life

insurance across Asia as societies mature and wealth increases

Leading Life Insurance franchise – focused on highly profitable protection centric products

Most prudent investment allocation framework inline with insurance best principals

Largest capital reserves in Asia to sustain organic growth, dividends and to aid future bancassurance partnerships

Meetings with Management: 4

Insurance – AIA Group

Source: FactSet as of May 19, 2015 Source: FactSet as of May 20, 2015

BUY

Source: FactSet

Source: FactSet Any securities shown are illustration purposes only and are not intended as a recommendation to buy or hold these securities, and their continued inclusion in the Asia ex-Japan strategy’s representative portfolio is not guaranteed. Above information is based on historical data and does not guarantee future investment performance.

36 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Stock Examples Within the 4 Key Themes (continued)

Environment – CT Environmental Group

Market Cap US$2.1b

Net Debt to

Equity

62%

EPS CAGR (’14-

16)

34.5%

ROE (FY15e) 26.5%

P/E Ratio (FY15e) 27 X

Div Yield (FY15e) 0.6%

Why we bought CT Environmental

Group:

Renewed, greater focus on

environment in13th FYP, particularly on water treatment

Dominant 3rd party industrial waste-water treatment player - a sector with high barriers to entry, with demonstrated ability to grow capacity

Reliance on a build-own-operate model offers higher profitability, lower working capital drain, and greater transparency

Meetings with Management: 1

Market Cap US$4.1b

Net Debt to

Equity

2.0%

EPS CAGR (’14-

16)

16.9%

ROE (FY15e) 29.1%

P/E Ratio (FY15e) 23.6x

Div Yield (FY15e) 1.2%

Why we bought China Medical

Systems:

Strong product portfolio established by

management team with track record of identifying drugs with good market potential & exclusivity

Well-established direct sales network with access to more than 12,000 hospitals in China

Key drugs in portfolio treat lifestyle diseases of today: depression, liver cirrhosis, heart failure

Best-in-class profitability and ROE

Meetings with Management: 8

Healthcare – China Medical System

7/13 10/13 1/14 4/14 7/14 10/14 1/15 4/15

0

2

4

6

8

10

12

Source: FactSet Prices

Closing Price

17-May-2013 to 19-May-2015 (Daily) Price (Local Currency)

CT Environmental Group Ltd.

BUY

Source: Bloomberg Source: FactSet

Any securities shown are illustration purposes only and are not intended as a recommendation to buy or hold these securities, and their continued inclusion in the Asia ex-Japan strategy’s representative portfolio is not guaranteed. Above information is based on historical data and does not guarantee future investment performance.

Source: FactSet as of May 20, 2015

7/12 10/12 1/13 4/13 7/13 10/13 1/14 4/14 7/14 10/14 1/15 4/15

2

4

6

8

10

12

14

16

Source: FactSet Prices

Closing Price

18-May-2012 to 20-May-2015 (Daily) Price (Local Currency)

China Medical System Holdings Ltd.

Source: FactSet as of May 20, 2015

BUY

37 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Asia ex-Japan: Investment Approach

Style Agnostic

Stock selection and stock weightings driven by view and

conviction, not the benchmark

Mid to large cap, Preference for liquid stocks

Benchmark Unaware

Bottom-up Stock

Pickers

Fundamental

Research Driven

Universe

Focused Portfolios

Investment Horizon

Portfolios are predominantly constructed through bottom-up

stock selection

Identification of mis-priced stocks through fundamental

research

Portfolio holds between 40 to 60 stocks

Generally greater than 3 years

38 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

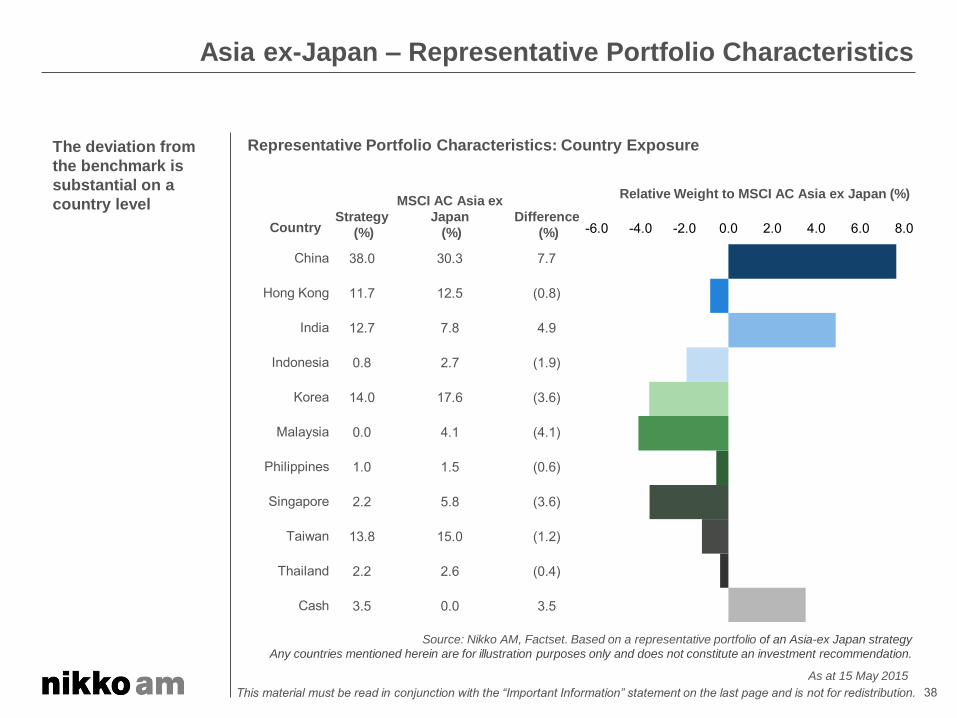

Asia ex-Japan – Representative Portfolio Characteristics

Representative Portfolio Characteristics: Country Exposure

The deviation from

the benchmark is

substantial on a

country level

Country Strategy

(%)

MSCI AC Asia ex

Japan

(%)

Difference

(%)

China 38.0 30.3 7.7

Hong Kong 11.7 12.5 (0.8)

India 12.7 7.8 4.9

Indonesia 0.8 2.7 (1.9)

Korea 14.0 17.6 (3.6)

Malaysia 0.0 4.1 (4.1)

Philippines 1.0 1.5 (0.6)

Singapore 2.2 5.8 (3.6)

Taiwan 13.8 15.0 (1.2)

Thailand 2.2 2.6 (0.4)

Cash 3.5 0.0 3.5

Relative Weight to MSCI AC Asia ex Japan (%)

Source: Nikko AM, Factset. Based on a representative portfolio of an Asia-ex Japan strategy

Any countries mentioned herein are for illustration purposes only and does not constitute an investment recommendation.

As at 15 May 2015

-6.0 -4.0 -2.0 0.0 2.0 4.0 6.0 8.0

39 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Asia ex-Japan - Representative Portfolio Characteristics (continued)

Representative Portfolio Characteristics: Sector Exposure The deviation from

the benchmark is

substantial on a

sector level

Sector Strategy

(%)

MSCI AC

Asia ex

Japan

(%)

Difference

(%)

Consumer Discretionary 5.3 8.0 (2.7)

Consumer Staples 7.5 5.0 2.5

Energy 1.4 5.1 (3.6)

Financials 34.4 34.2 0.2

Healthcare 12.1 1.9 10.1

Industrials 4.2 9.0 (4.8)

Information Technology 20.9 21.8 (0.9)

Materials 0.0 4.7 (4.7)

Telecommunications 3.7 6.4 (2.7)

Utilities 7.0 3.9 3.1

Cash 3.5 0.0 3.5

Relative Weight to MSCI AC Asia ex Japan (%)

Source: Nikko AM, Factset. Based on a representative portfolio of an Asia-ex Japan strategy

Any sectors mentioned herein are for illustration purposes only and does not constitute an investment recommendation.

recommendation As at 15 May 2015

-6.0 -4.0 -2.0 0.0 2.0 4.0 6.0 8.0 10.0 12.0

40 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Stock Examples Within Japan

Sony

Market Cap JPY 34.6bn

Net Debt to

Equity

-2%

EPS CAGR (’14-

16)

Back in black

ROE (FY15e) 6.0%

P/E Ratio (FY15e) 25.4 X

Div Yield (FY15e) 0.25%

Why we bought Sony:

Conviction on aggressive restructuring

under the new leadership (new CEO and CFO)

Sony brand is alive and asset sales have helped finance R&D for future business development.

Now ready to be on the offensive and leverage its capabilities in software, gaming and entertainment businesses.

Financial services business is solid.

New ROE target of 10%.

Market Cap JPY4.0bn

Net Debt to

Equity

68%

EPS CAGR (’14-

16)

48.8%

ROE (FY15e) 8.1%

P/E Ratio (FY15e) 18.1x

Div Yield (FY15e) 1.2%

Why we bought Toray:

Positive outlook on carbon fiber

demand and the company’s

competitive advantage.

Sole supplier to Boeing for its 787 Dreamliner. Recently won business from BMW, with plans to expand capacity.

New ROE target of 10%.

Toray

BUY

Source: Bloomberg Source: Bloomberg

Any securities shown are illustration purposes only and are not intended as a recommendation to buy or hold these securities, and their continued inclusion in the Japan Value equity strategy’s representative portfolio is not guaranteed. Above information is based on historical data and does not guarantee future investment performance.

Source: Bloomberg as of May 25, 2015 Source: Bloomberg as of May 25, 2015

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Closing Price 30-Dec-2013 to 22-May-2015 (Daily)

0

200

400

600

800

1,000

1,200

Closing Price 30-Dec-2013 to 22-May-2015 (Daily)

41 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Japan Value Equity: Investment Approach

Style Fundamental/Contrarian, Active Management

Mid to large cap, preference for liquid stocks

Bottom-up Stock

Pickers

Fundamental

Research Driven

Universe

Focused Portfolios

Investment Horizon

Portfolios are predominantly constructed through bottom-up

stock selection

Identification of mis-priced stocks and turnaround

opportunities through fundamental research

Portfolio holds approximately 80 to 100 stocks

Generally 3-5 years

.

42 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Japan Value Equity– Strategy Characteristics

The data above is based on a representative account of the Japan Value Equity Strategy The graph and table are based on past data and do not guarantee future returns.

Any sectors mentioned herein are for illustration purposes only and does not constitute an investment recommendation.

The portfolio

maintains an

overweight position

in the Materials,

Industrials and

Consumer

Discretionary

sectors, while it is

underweight

Consumer Staples,

Health Care and

Financials

As at 31 March 2015

GICS10 Sectors 201503 Sector Allocation Vs. Benchmark QoQ Active Sector Exposure

SectorNo. of

StocksPortfolio TOPIX Difference

Energy 2 1.45% 0.89% 0.55%

Materials 15 13.04% 6.92% 6.12%

Industrials 24 23.21% 20.87% 2.34%

Consumer Discretionary 22 25.13% 21.72% 3.41%

Consumer Staples 2 3.27% 7.89% -4.62%

Health Care 2 1.72% 6.51% -4.79%

Financials 12 13.61% 17.42% -3.81%

Information Technology 12 11.01% 10.94% 0.07%

Telecommunication Services 2 3.00% 4.84% -1.84%

Utilities 2 2.37% 2.00% 0.38%

Other* 2.20% 0.00% 2.20%

Total 95 100.00% 100.00%

0% 5% 10% 15% 20% 25%

Portfolio TOPIX

-5% 0% 5% 10%

201412 201503

* Includes cash

43 This material must be read in conjunction with the “Important Information” statement on the last page and is not for redistribution.

Summary

Favorable macro environment for Asian equity active managers

Uneven growth

Lower inflation

Lower oil price

Better prepared for the US interest rate hike

Long term strong equity market performance and current cheap level of valuation

Reform is a key in 2015. Positive for China and India

Wage growth, demographics and growing middle class implies four

promising sectors in particular healthcare

Asia is still growing

strongly

Any sectors shown are for illustration purposes only and are not to be construed as investment recommendations.

44

Nikko Asset Management Asia Limited

12 Marina View, #18-02 Asia Square Tower 2, Singapore 018961 Tel: (65) 6500 5700 Fax: (65) 6534 5183 Co. Registration No. 198202562H

This document is prepared by Nikko Asset Management Co., Ltd. This document is for information only with no consideration given to the specific investment objective, financial situation and particular needs of any specific person. Any securities mentioned herein are for illustration purposes only and should not be construed as a recommendation for investment. You should seek advice from a financial adviser before making any investment. In the event that you choose not to do so, you should consider whether the investment selected is suitable for you. Investments in unit trusts are not deposits in, obligations of, or guaranteed or insured by Nikko Asset Management Asia Limited (“Nikko AM Asia”). Past performance or any prediction, projection or forecast is not indicative of future performance. The portfolios may use or invest in financial derivative instruments. The value of portfolios and income from them may fall or rise. Investments in the portfolios are subject to investment risks, including the possible loss of principal amount invested. The information contained herein may not be copied, reproduced or redistributed without the express consent of Nikko AM Asia. While reasonable care has been taken to ensure the accuracy of the information as at the date of publication, Nikko AM Asia does not give any warranty or representation, either express or implied, and expressly disclaims liability for any errors or omissions. Information may be subject to change without notice. Nikko AM Asia accepts no liability for any loss, indirect or consequential damages, arising from any use of or reliance on this document.

Important Information