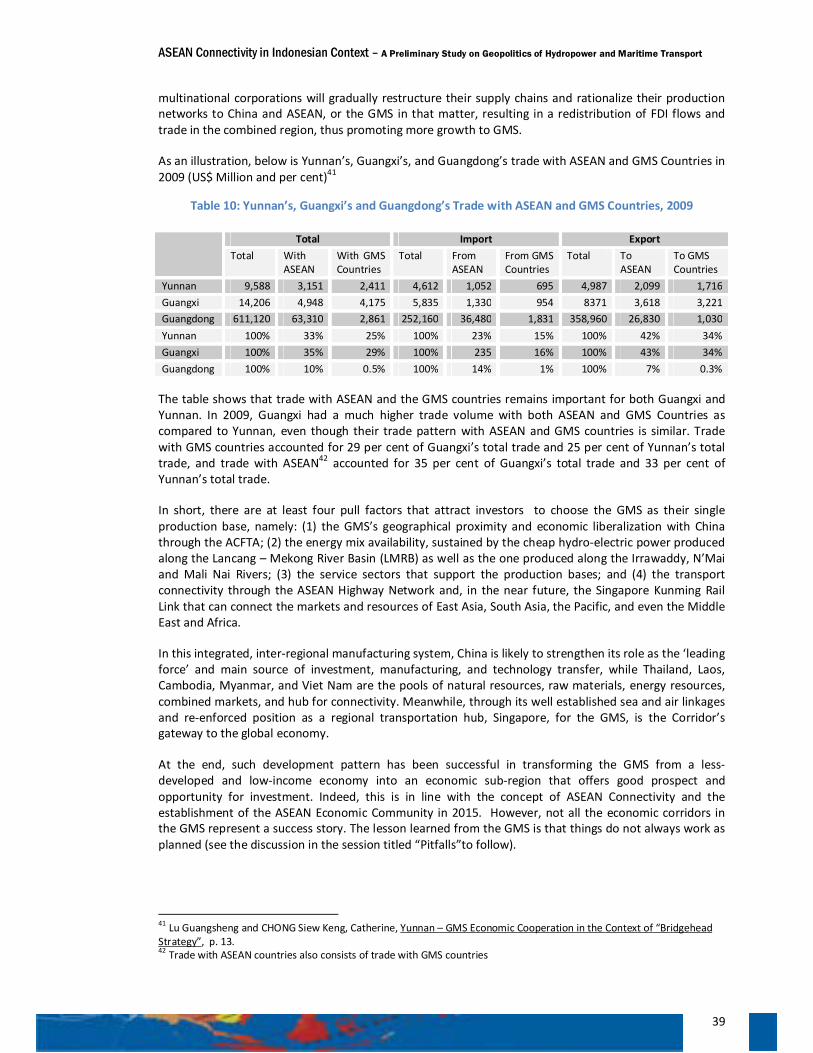

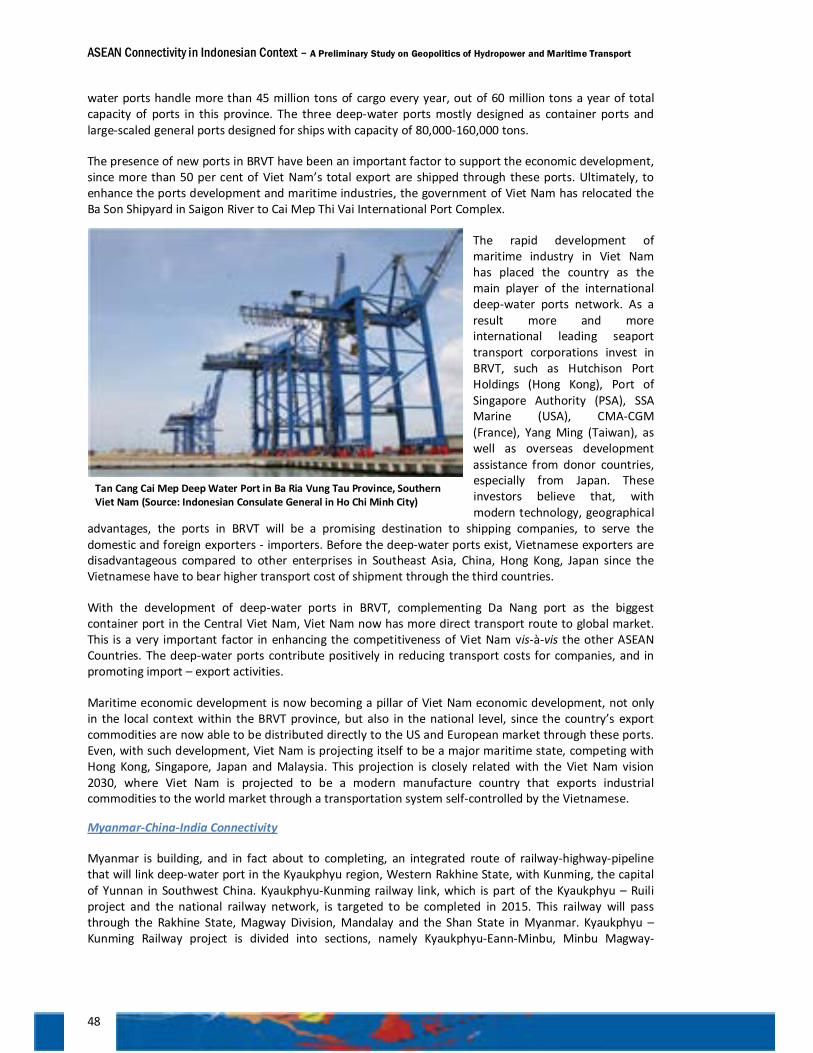

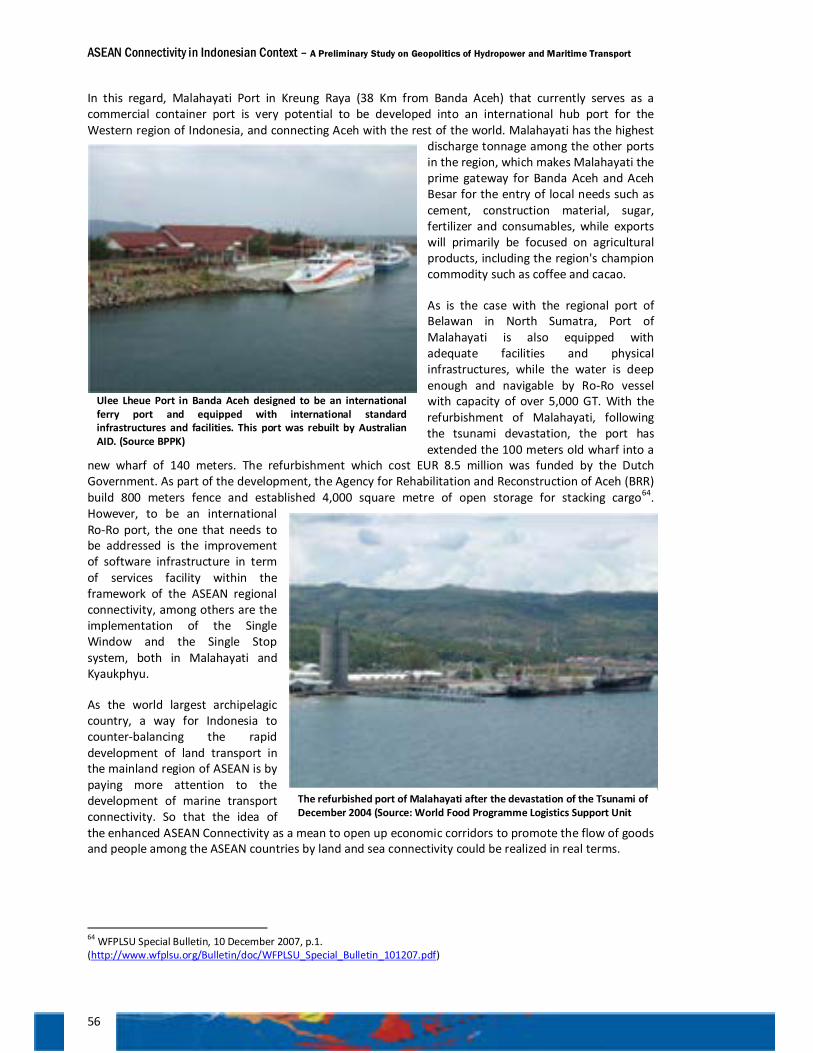

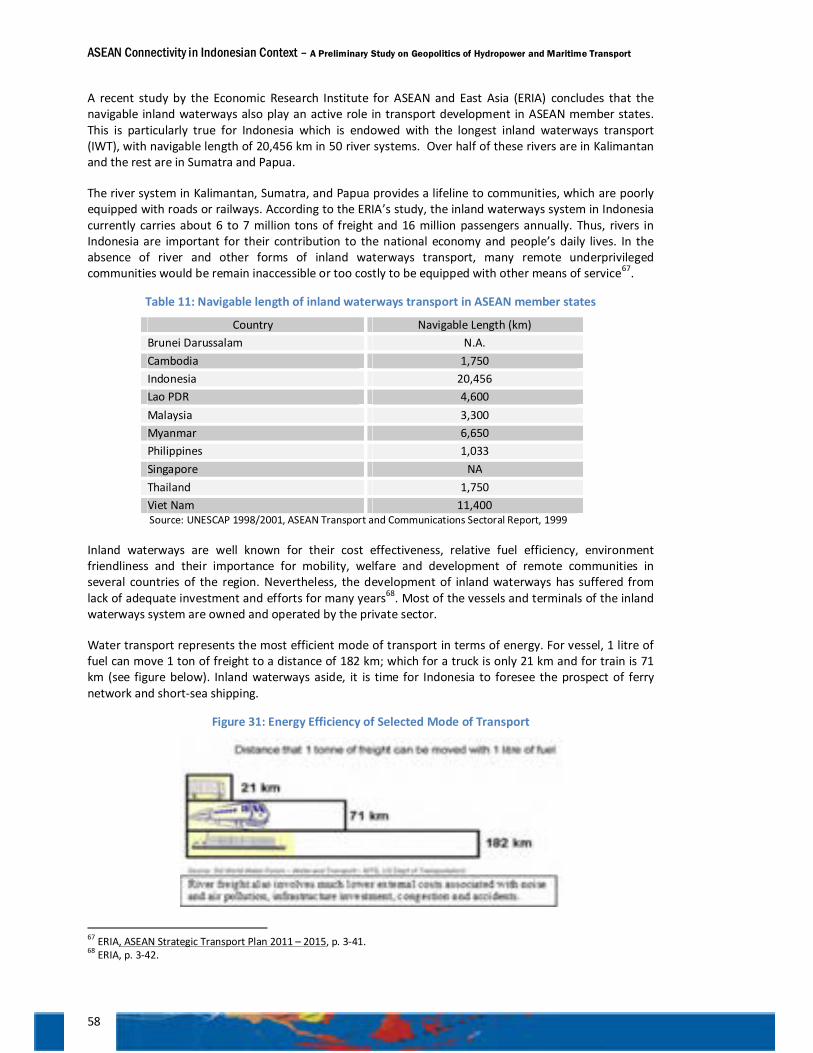

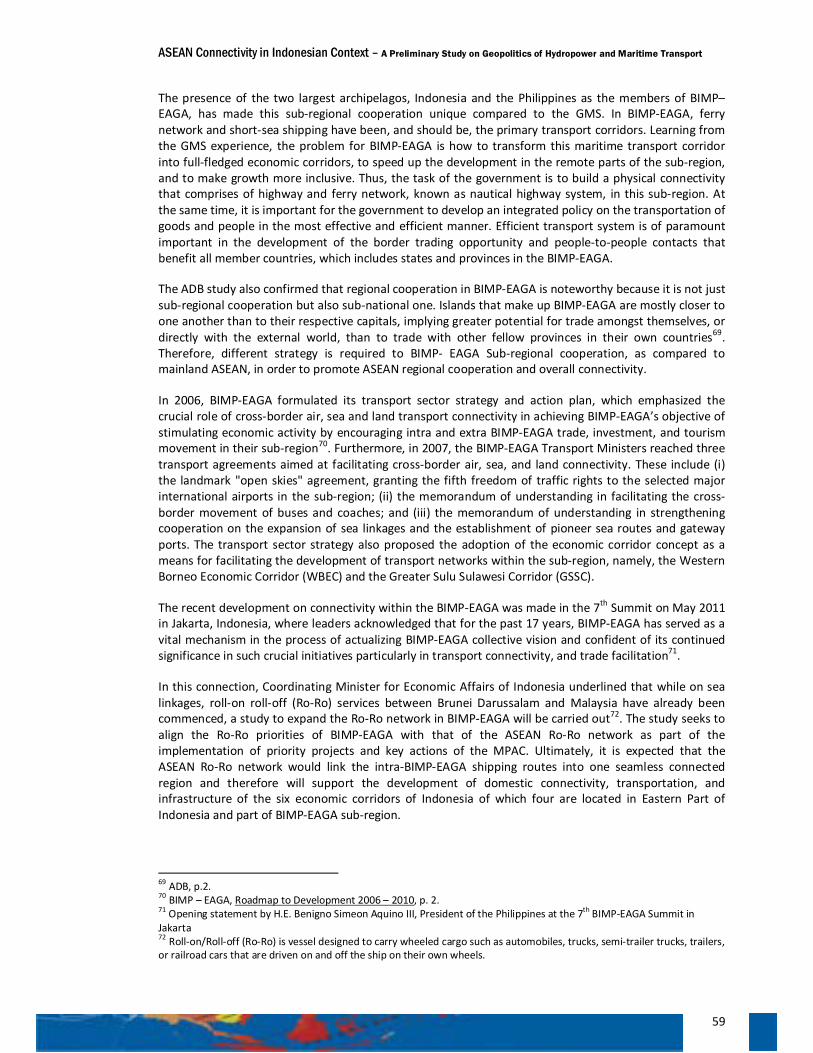

asean connectivity in indonesian...

TRANSCRIPT

ASEAN Connectivity in Indonesian Context

A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

Centre of Policy Analysis and Development for Asia-Pacific and African Regions Policy Analysis and Development Agency

Ministry of Foreign Affairs of the Republic of Indonesia 2011

ASEAN Connectivity in Indonesian Context A Preliminary Study of Geopolitics of Hydropower and Maritime Transport Revised Edition 2011 First Published in Indonesia in 2011 by: Centre of Policy Analysis and Development on Asia-Pacific and African Regions Policy Analysis and Development Agency Ministry of Foreign Affairs of the Republic of Indonesia Jalan Taman Pejambon no.6 Jakarta Pusat 10110 Indonesia Email: [email protected] Editor : Siswo Pramono, et al. Cover Design : Imad Yousry Layout: Donny Warmadewa ©2011 Centre for Policy Analysis and Development on Asia-Pacific and African Regions The responsibility for facts and opinions expressed in this publication rests exclusively with the investigators and their interpretations do not necessarily reflect the views nor the policy of the Ministry of Foreign Affairs of the Republic of Indonesia. Indonesian National book Catalogue (Katalog Dalam Terbitan/KDT) ASEAN Connectivity in Indonesian Context A Preliminary Study on Geopolitics of Hydropower and Maritime Transport, Revised Edition Jakarta: Penerbit P3K2 Aspasaf x+ 150 hlm,; 21 cm x 29 cm ISBN: 978-602-99703-1-9

The views expressed in this book are those of the investigators, and not necessarily those of the Ministry of Foreign Affairs of the Republic of Indonesia

i

Table of Contents Table of Contents ................................................................................................................................. i

List of Figures ................................................................................................................................... iv

List of Tables ................................................................................................................................... vi

Preface .................................................................................................................................. vii

Executive Summary ............................................................................................................................ xi

Chapter 1 | INTRODUCTORY ESSAY: Hydropower as a Pull Factor for Connectivity in Mainland and Archipelagic Regions of ASEAN ............................................................................................................. 1

Background of ASEAN Connectivity ............................................................................................................ 1

Connectivity in ASEAN Context ................................................................................................................... 1

Identification of Issues ................................................................................................................................ 3

Connectivity as the Focus of the Current Research .................................................................................... 3

Aim and Purpose of the Research ............................................................................................................... 4

The Thesis: Pull factors should be determined to promote connectivity ................................................... 4

Why Hydropower? ...................................................................................................................................... 6

Energy Mix ................................................................................................................................................... 8

Hydropower is heavily exploited in the Western Part of ASEAN: China’s role ........................................... 8

Hydropower as a Pull Factor: Ecological approach needed ...................................................................... 11

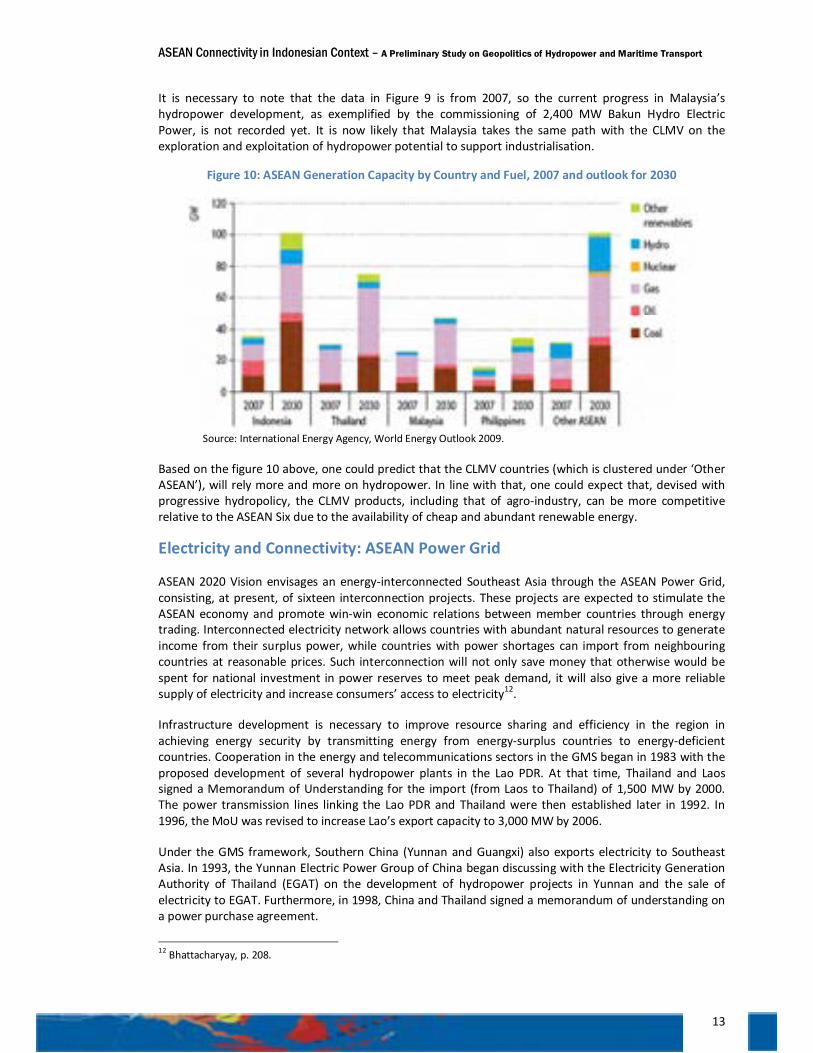

Hydropower Potential in ASEAN ............................................................................................................... 12

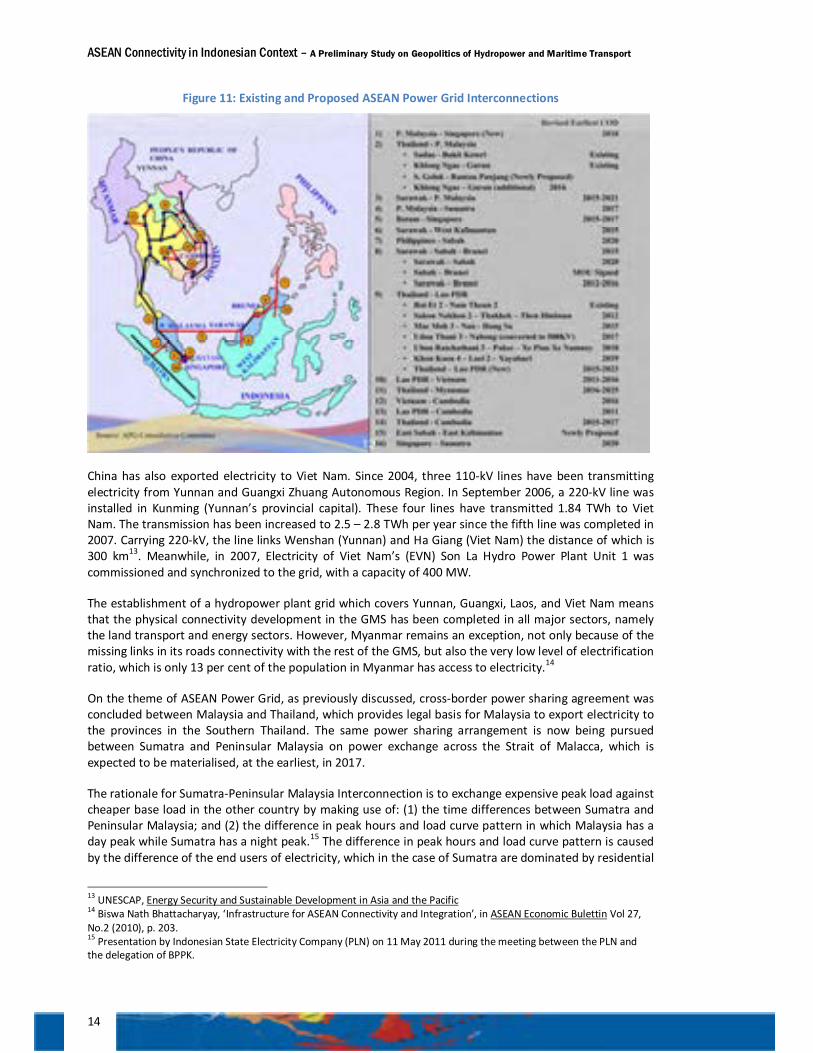

Electricity and Connectivity: ASEAN Power Grid ....................................................................................... 13

Hydropower potential in Indonesian context: the future “trade battles” are also about cheap renewable energy and connectivity ............................................................................................................................ 15

Industry and Connectivity: Public Private Partnership .............................................................................. 16

Progress of ASEAN Integration with Regional and Global Economies ...................................................... 18

The Score Card: Weak competitiveness .................................................................................................... 18

Connectivity and Energy as Key Factors of Competitiveness .................................................................... 19

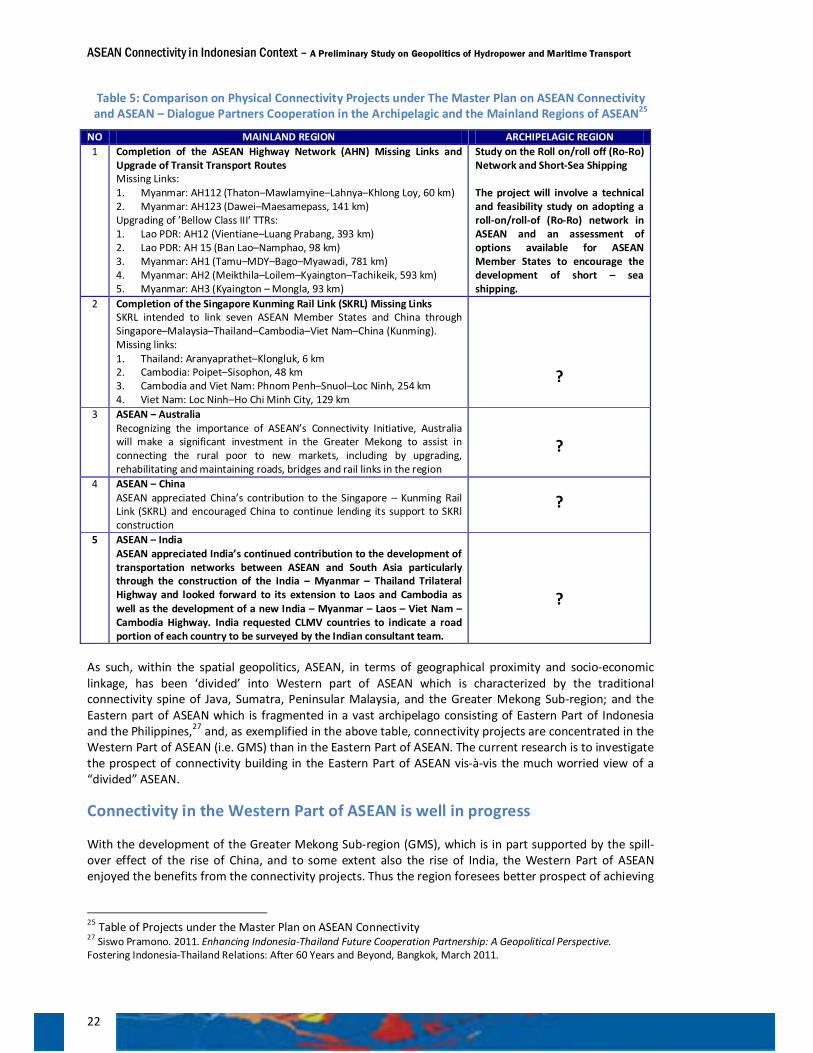

ASEAN must overcome the uneven connectivity ...................................................................................... 21

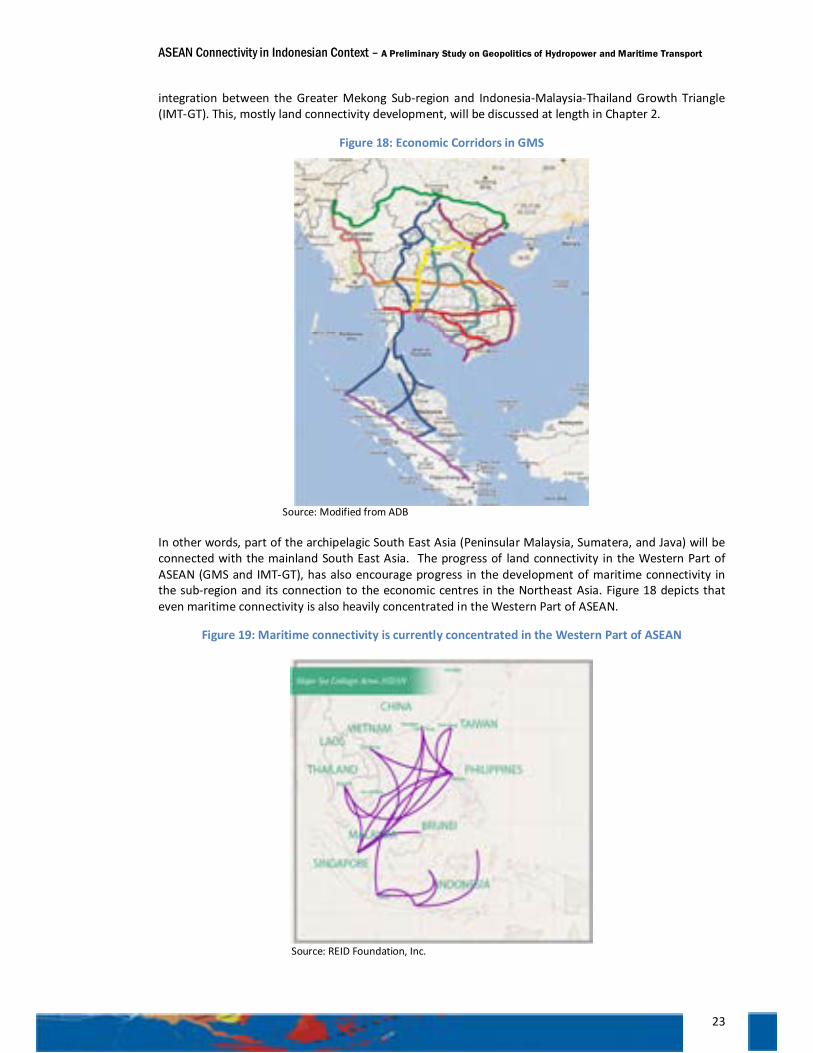

Connectivity in the Western Part of ASEAN is well in progress ................................................................ 22

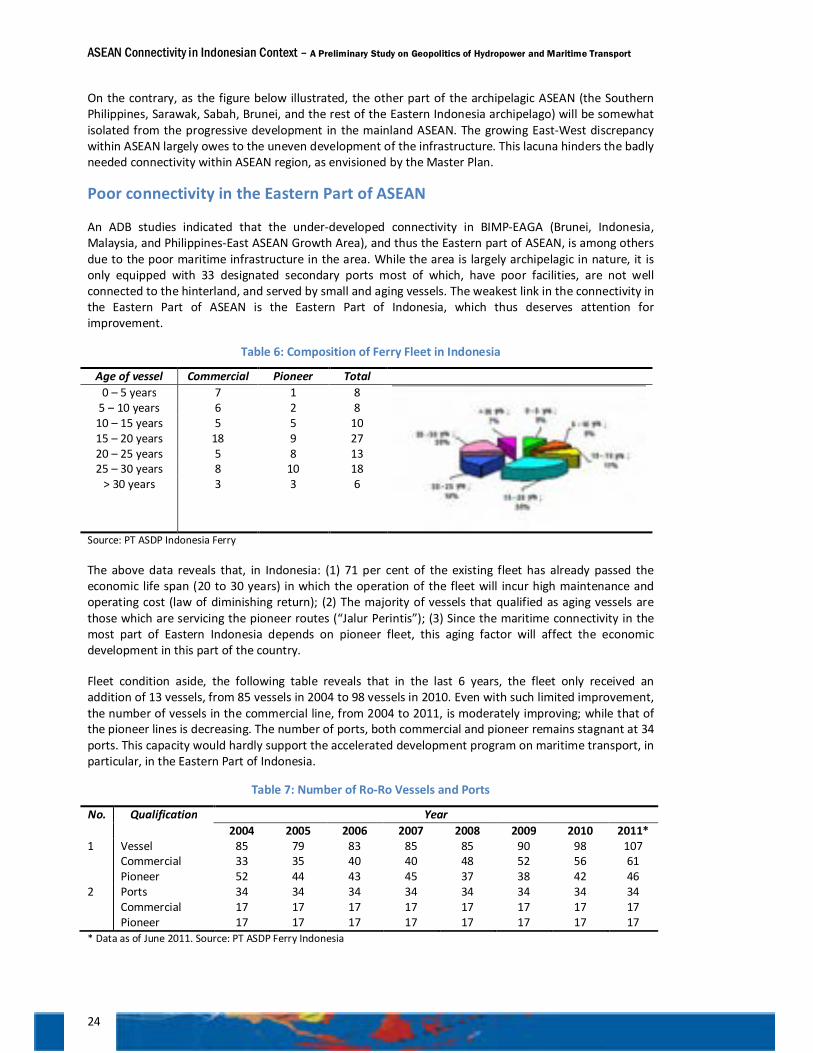

Poor connectivity in the Eastern Part of ASEAN........................................................................................ 24

Chapter 2 | WESTERN PART OF ASEAN: The Making of Land Connectivity and Economic Corridors .. 29

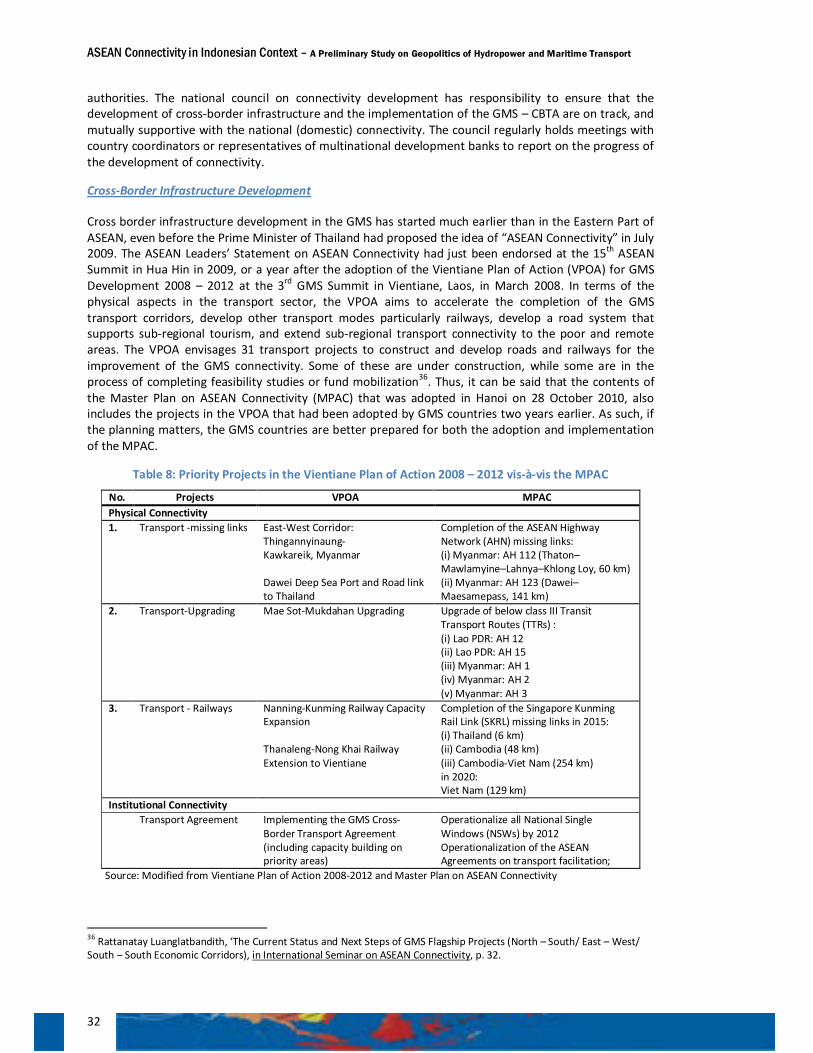

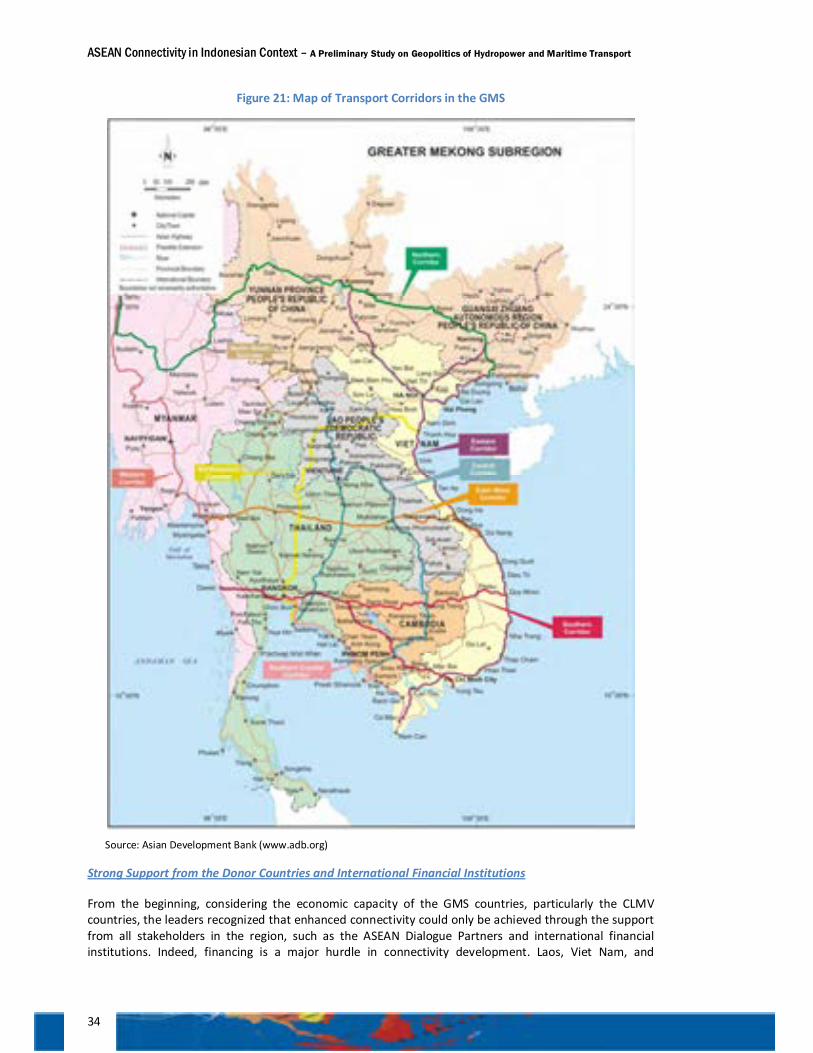

Connectivity in the Greater Mekong Sub-region (GMS) ........................................................................... 29

The Rationale behind the Success Story of the GMS ............................................................................ 30

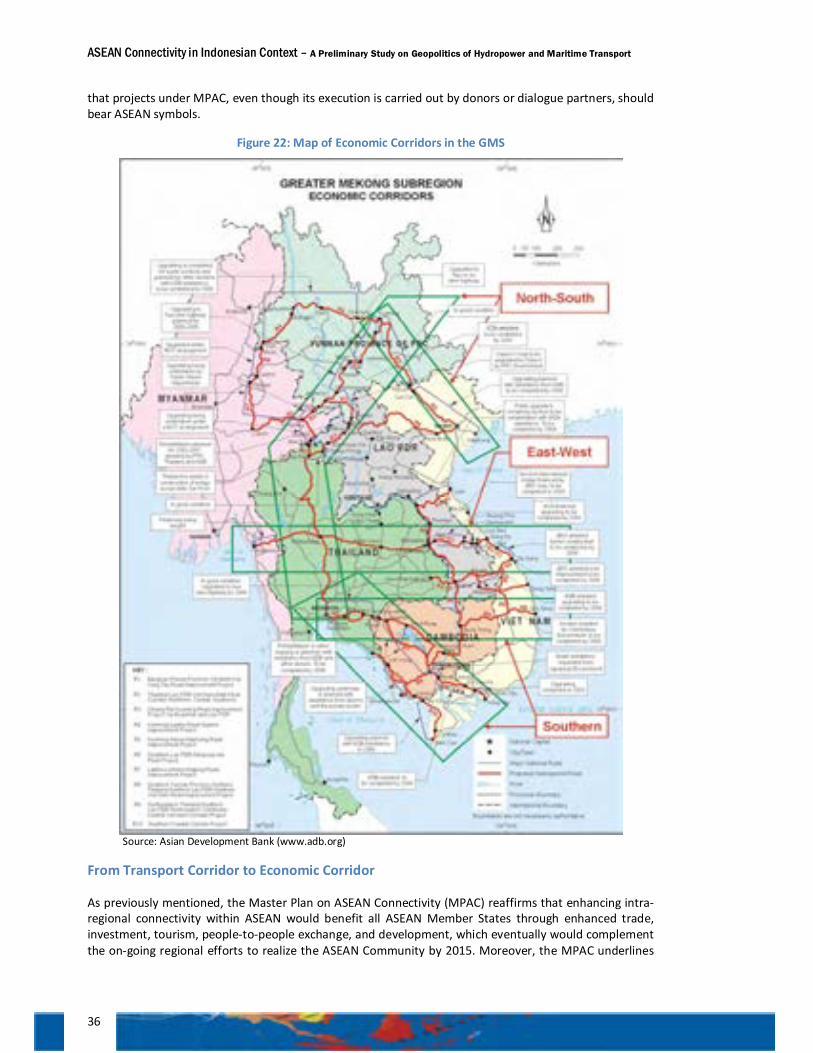

From Transport Corridor to Economic Corridor .................................................................................... 36

The China’s Role .................................................................................................................................... 38

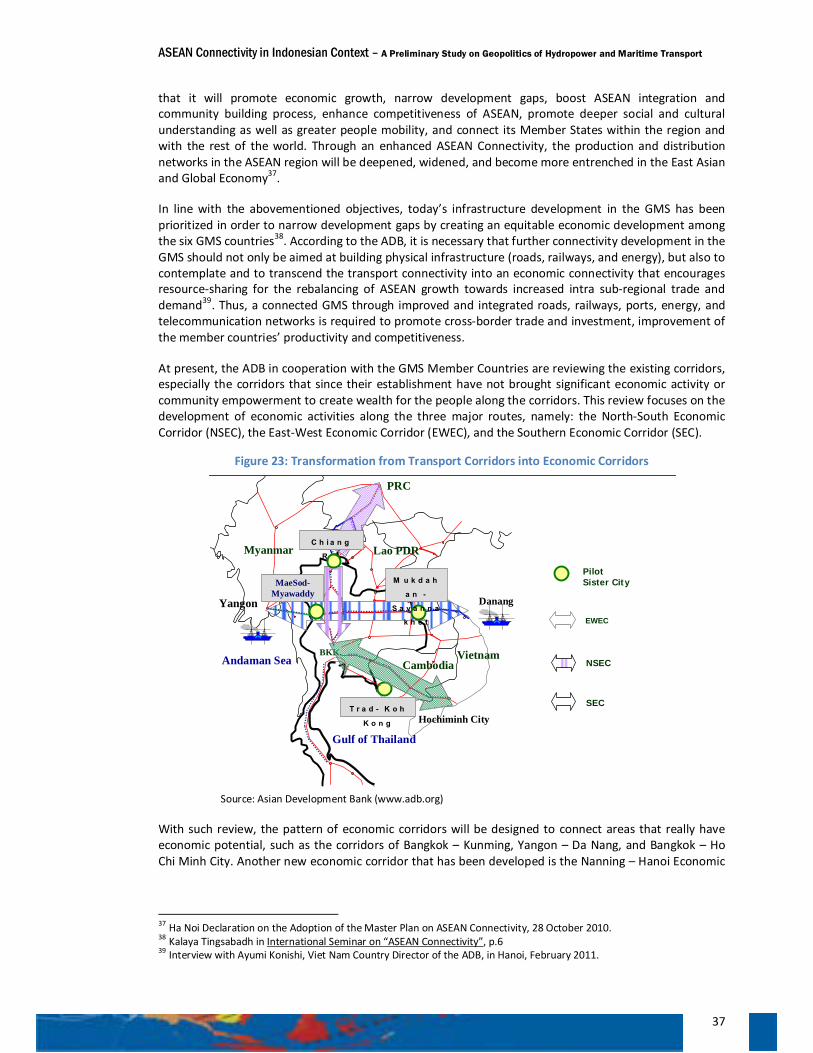

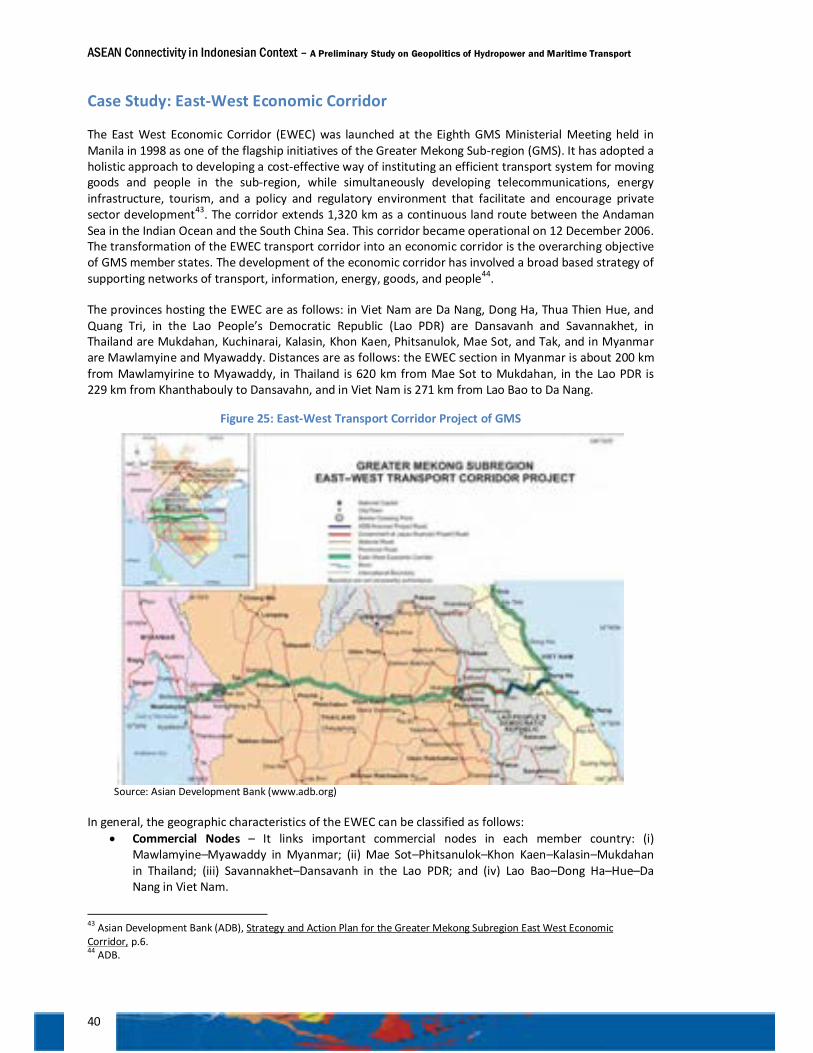

Case Study: East-West Economic Corridor ................................................................................................ 40

Physical Connectivity ............................................................................................................................. 41

People-to-people Connectivity ............................................................................................................. 44

ii

Pitfalls ................................................................................................................................................... 44

GMS Vision on ‘connectivity plus’: Lesson learned from Viet Nam and Myanmar .............................. 47

Connectivity in Indonesia, Malaysia, Thailand – Growth Triangle ............................................................ 49

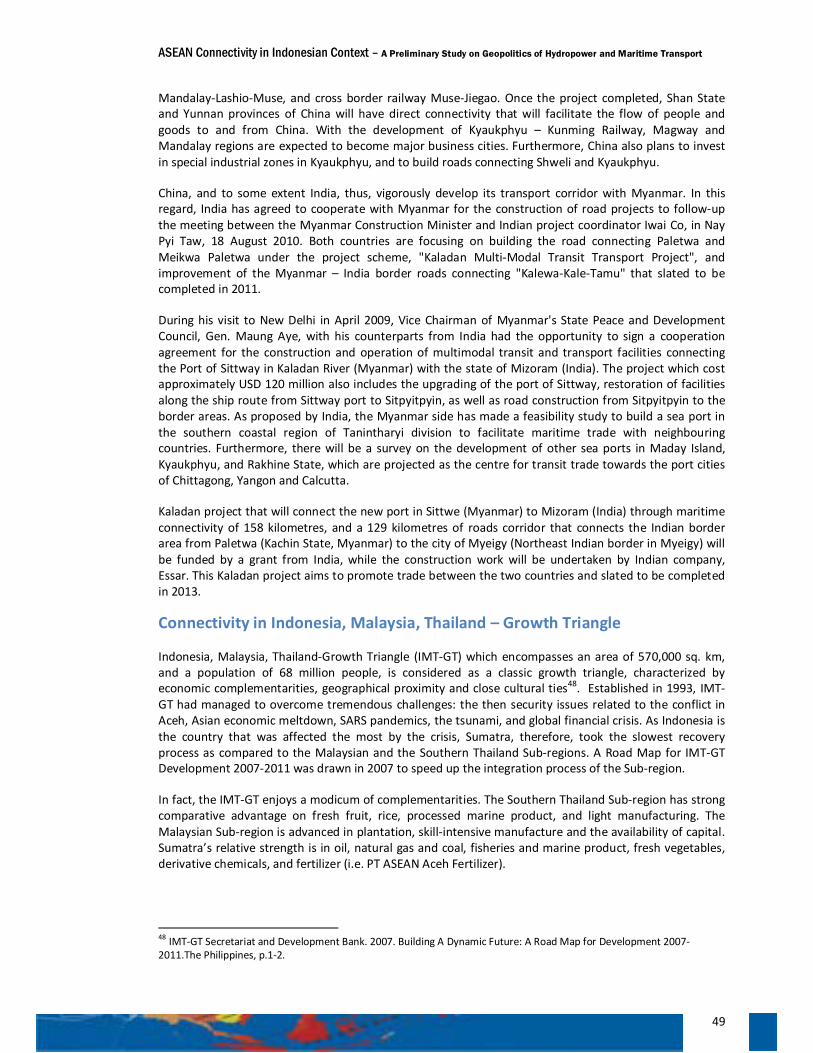

Challenge for Connectivity .................................................................................................................... 50

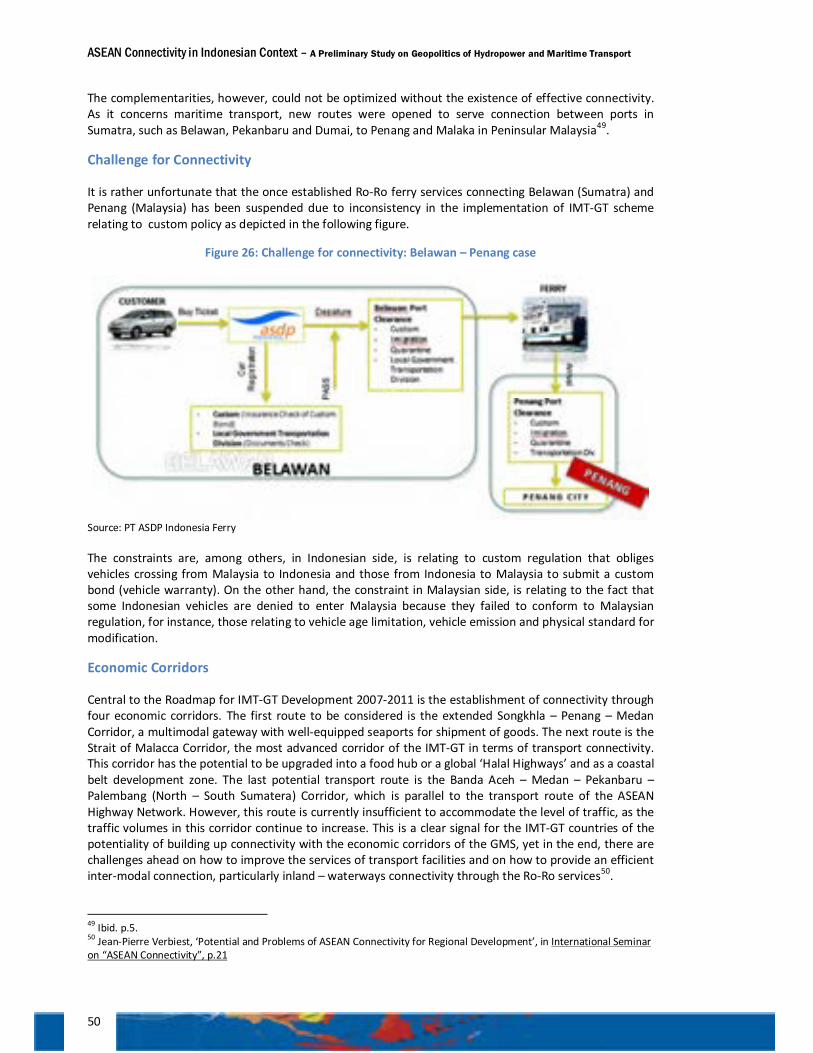

Economic Corridors .............................................................................................................................. 50

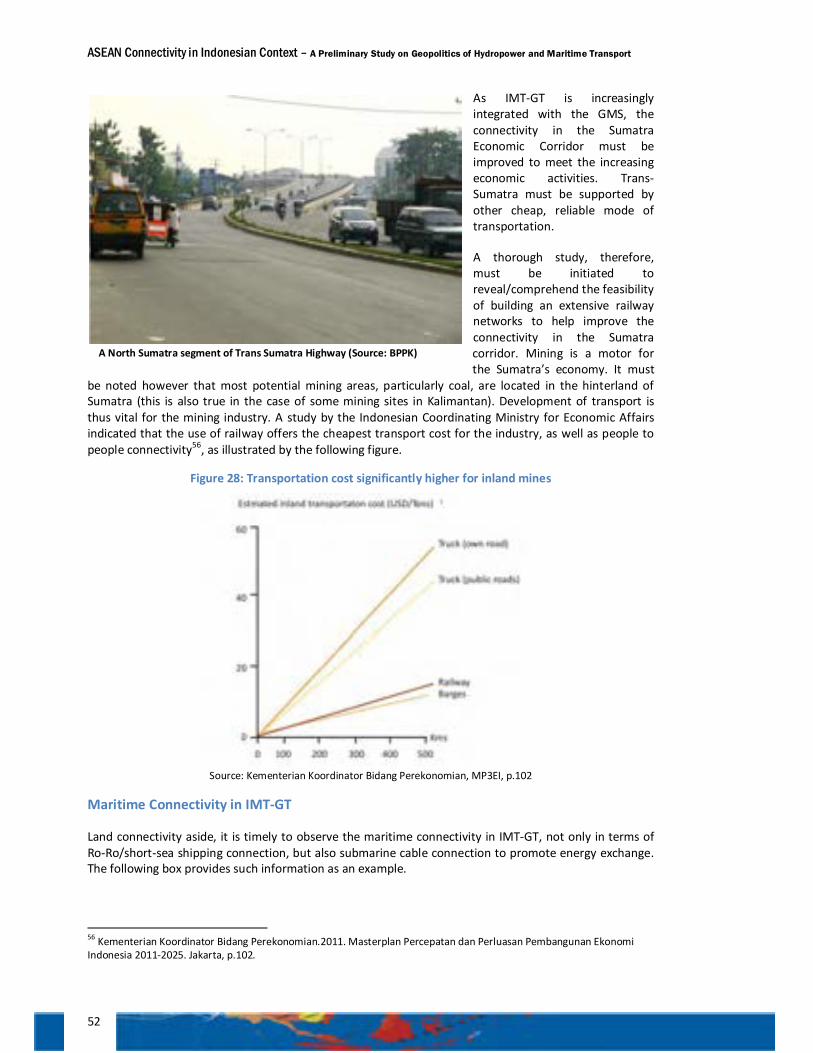

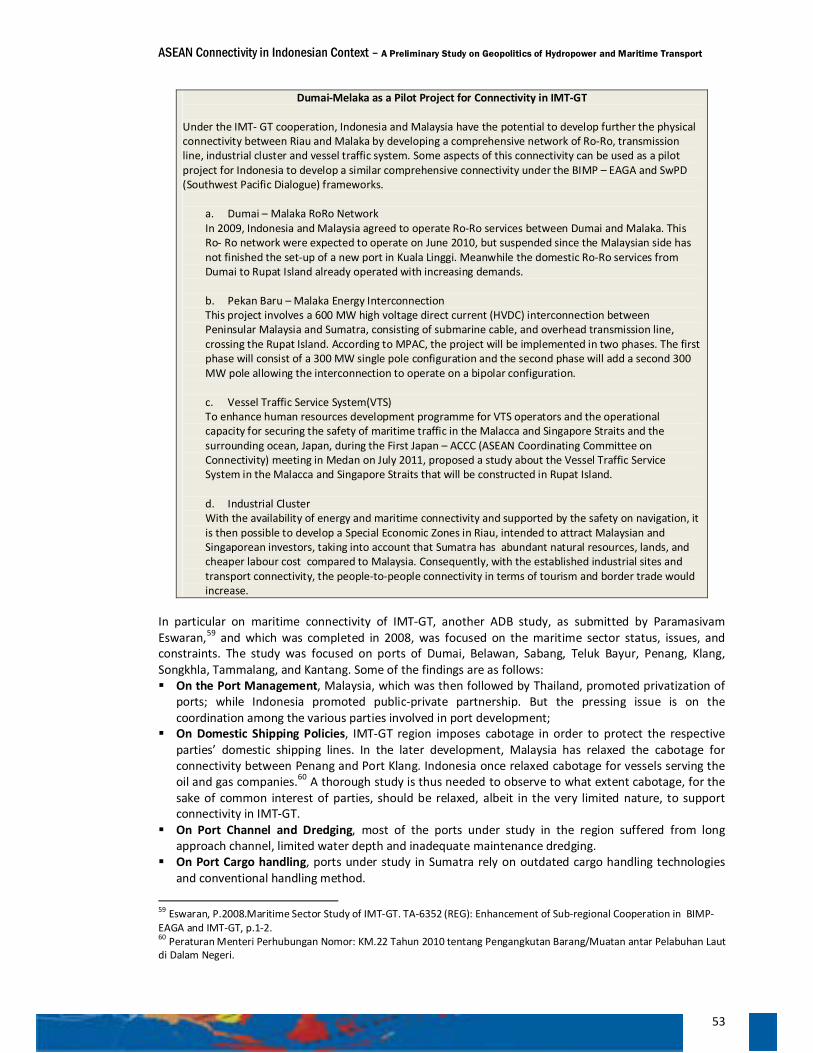

Maritime Connectivity in IMT-GT ......................................................................................................... 52

Chapter 3 | EASTERN PART OF ASEAN: Maritime Connectivity and Economic Corridors ................... 57

ERIA and ADB studies on BIMP-EAGA’s Connectivity ............................................................................... 57

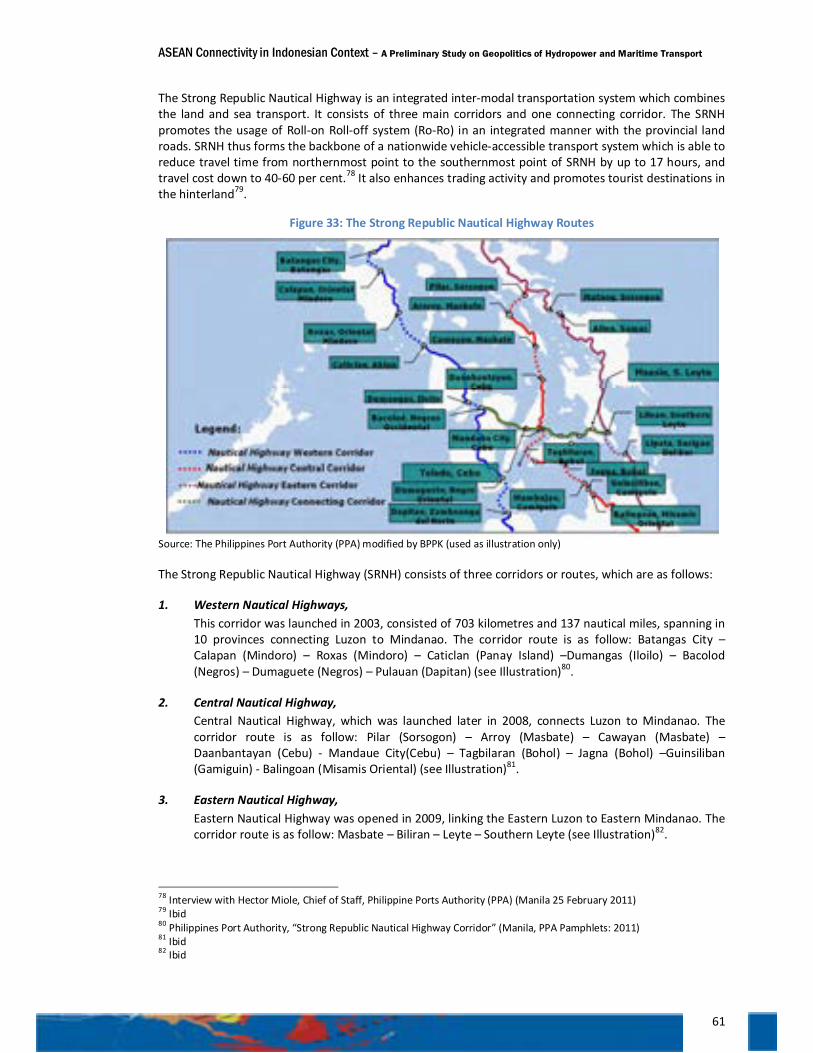

Case Study 1: Strong Republic Nautical Highway ..................................................................................... 60

The Administration of the SRNH ........................................................................................................... 62

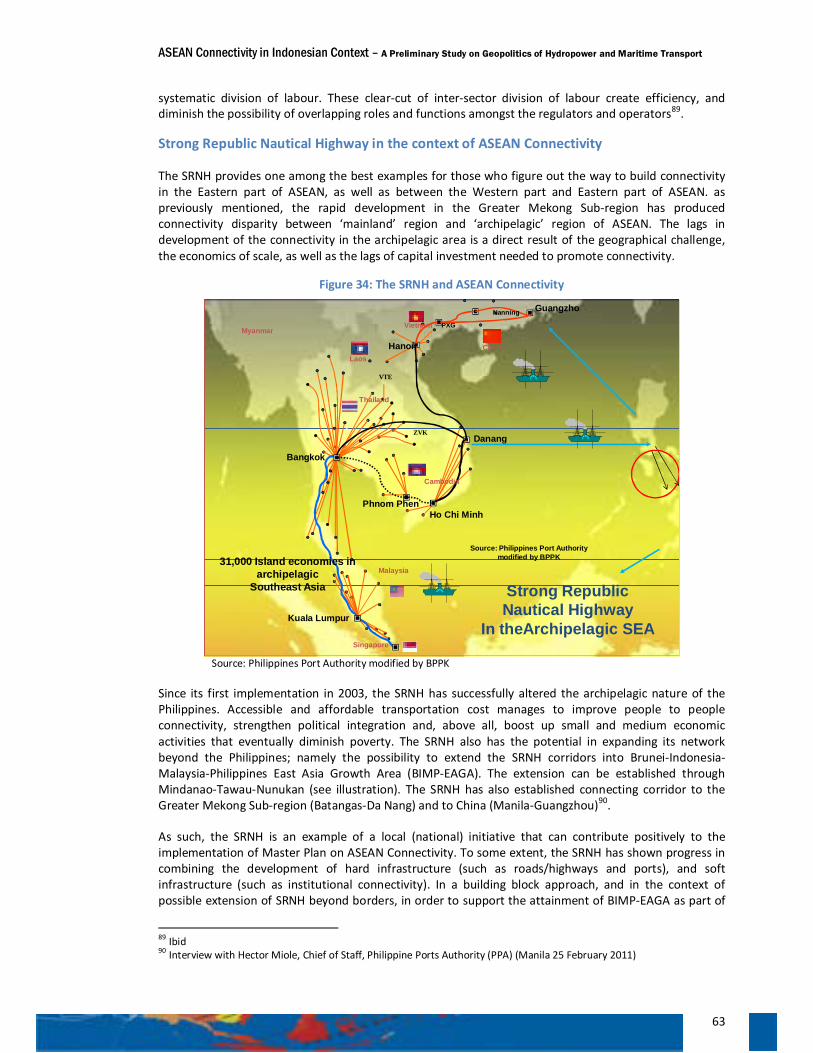

Strong Republic Nautical Highway in the context of ASEAN Connectivity ........................................... 63

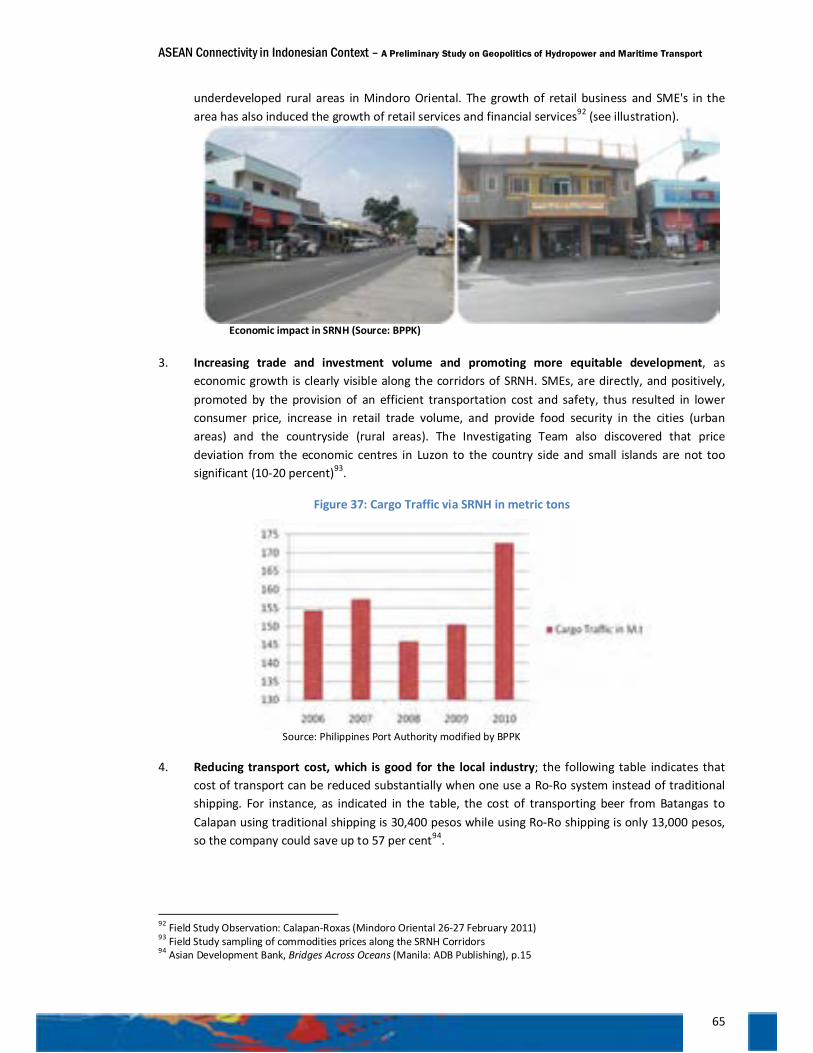

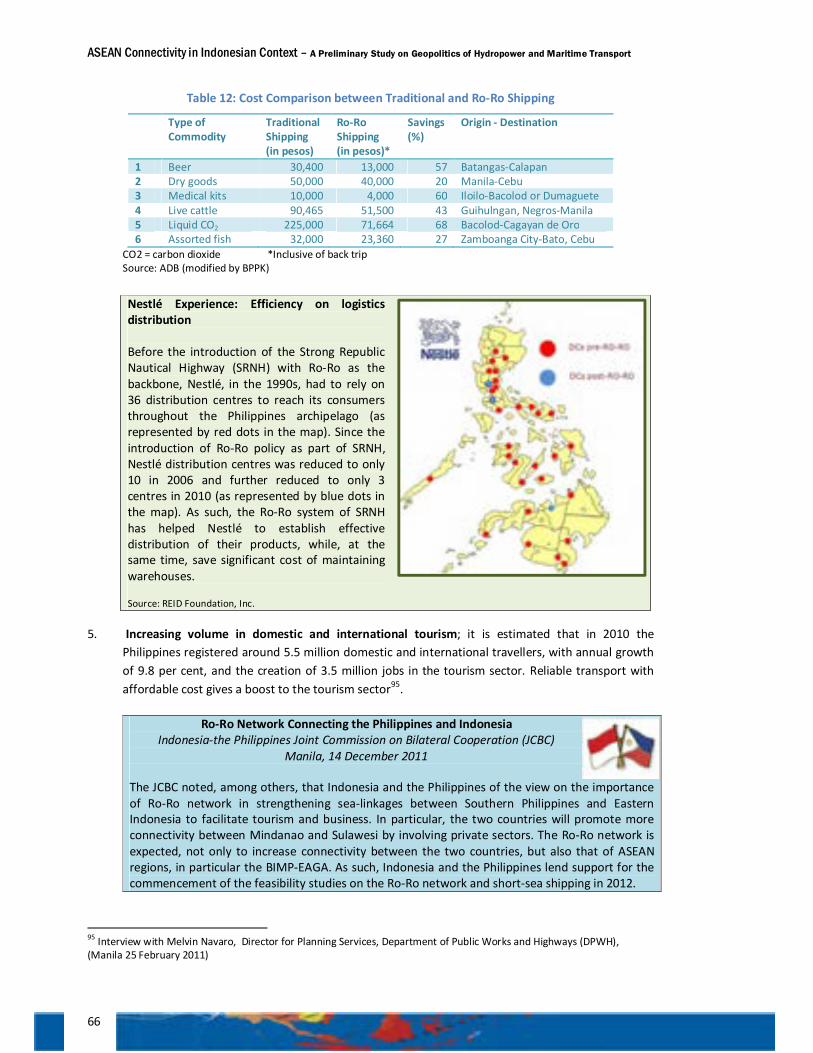

The Economic Significance of SRNH ..................................................................................................... 64

Case Study 2: Indonesian Ferry Belts ........................................................................................................ 67

Current development of Indonesian Ferry – PT ASDP .......................................................................... 67

The potential of Bali-Timor traditional shipping route to become a bridging line connecting Western part and Eastern part of Indonesia ....................................................................................................... 69

Bali – Timor Connection........................................................................................................................ 69

Prospect of ASEAN “connectivity plus” with Southwest Pacific ........................................................... 71

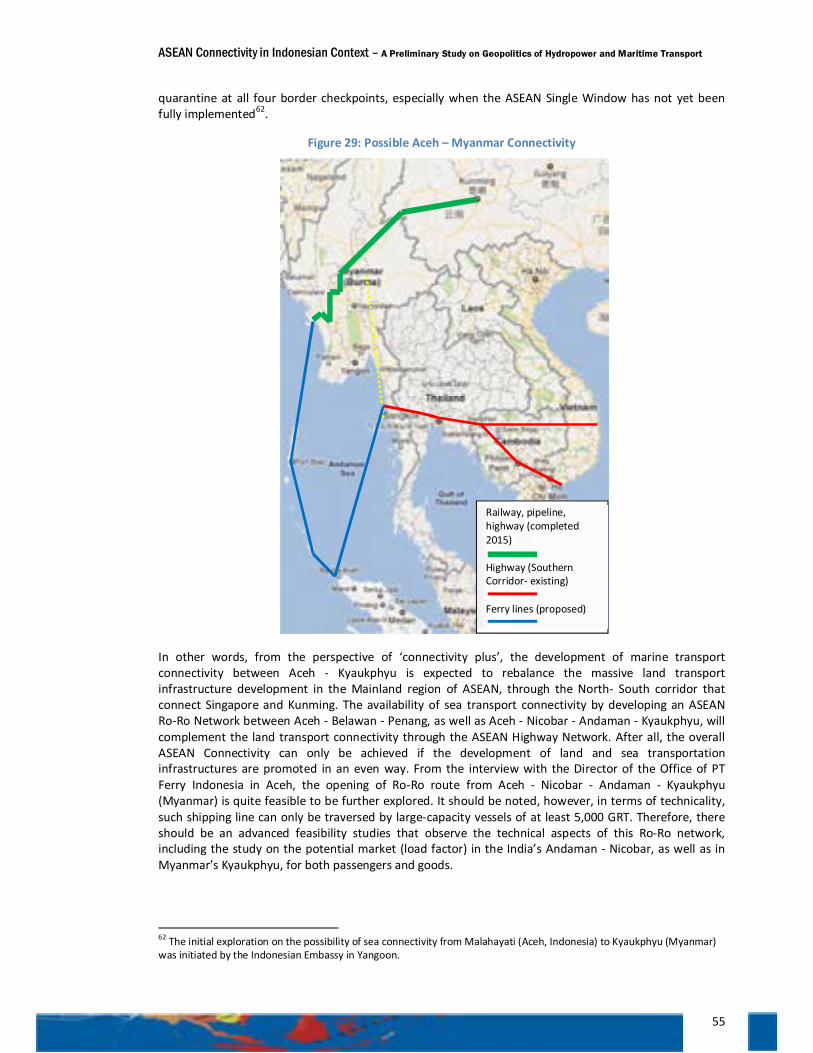

Australia’s Role ..................................................................................................................................... 72

Challenges of “connectivity plus” with Southwest Pacific .................................................................... 73

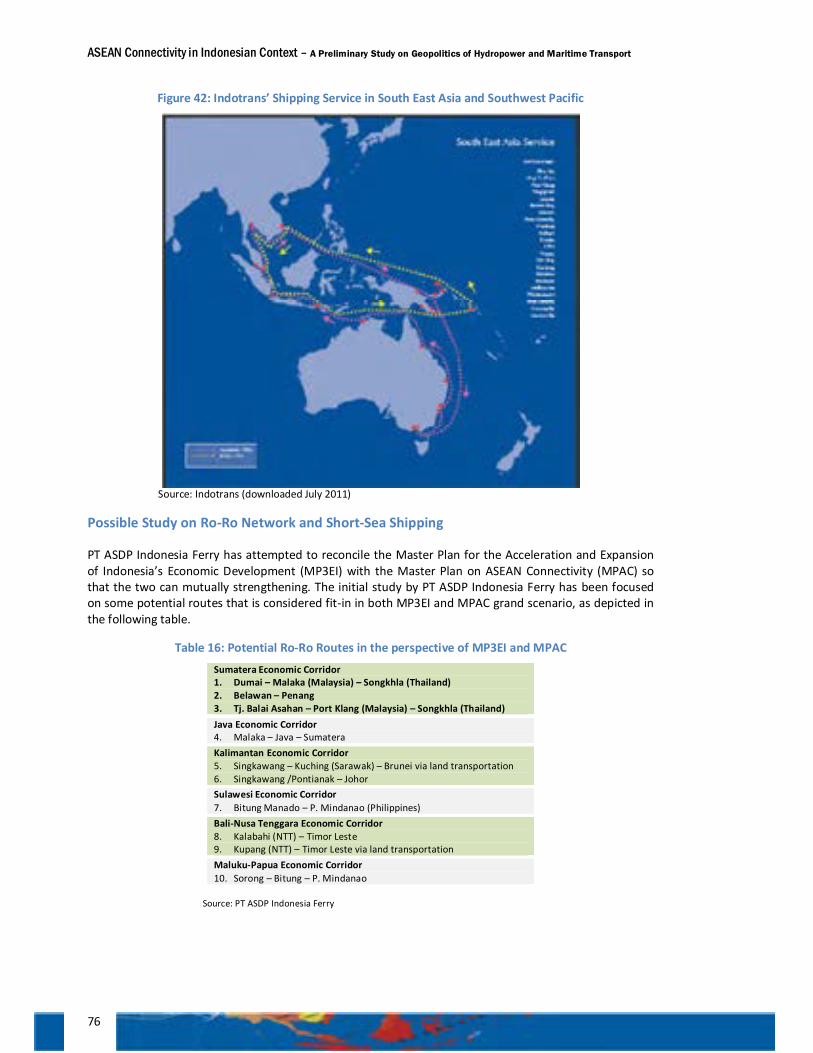

Possible Study on Ro-Ro Network and Short-Sea Shipping .................................................................. 76

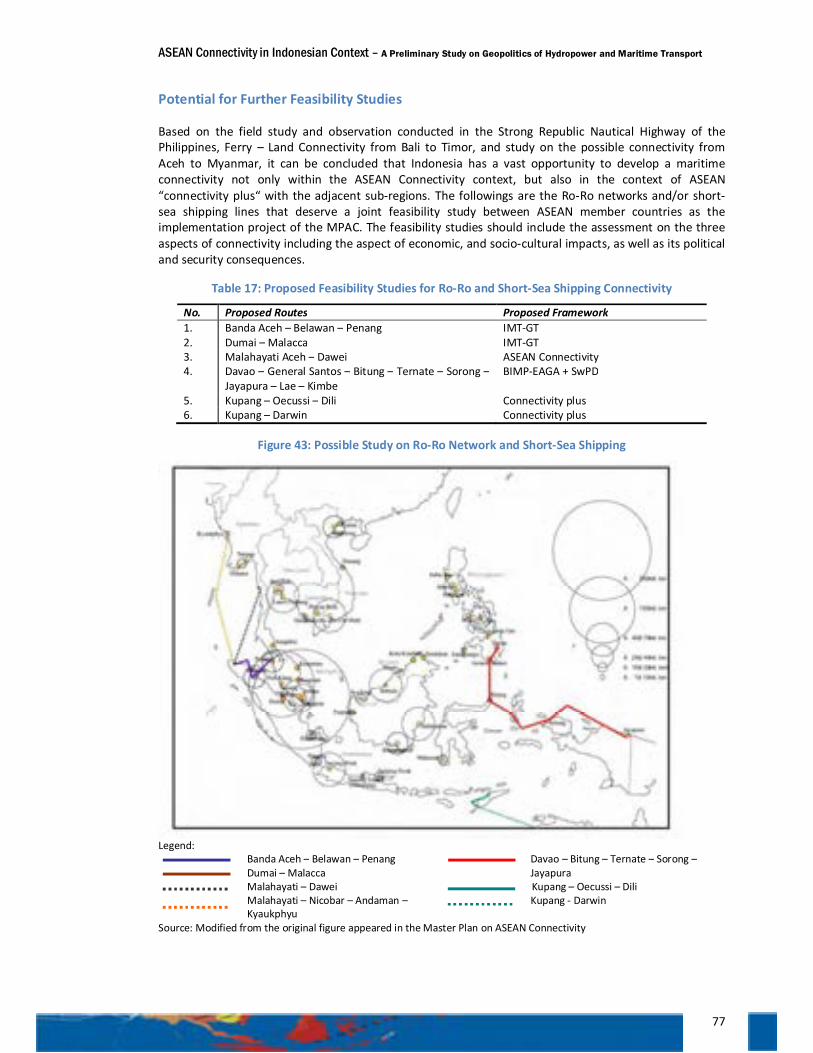

Potential for Further Feasibility Studies ............................................................................................... 77

Pitfalls ................................................................................................................................................... 78

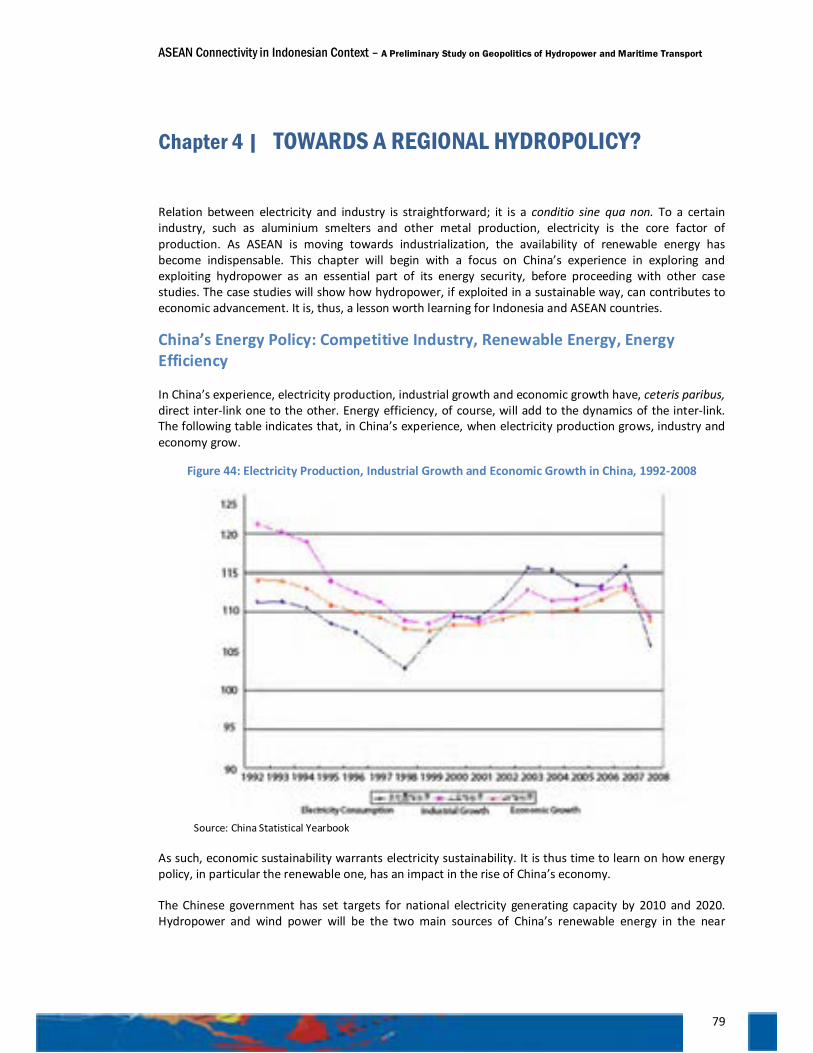

Chapter 4 | TOWARDS A REGIONAL HYDROPOLICY? ...................................................................... 79

China’s Energy Policy: Competitive Industry, Renewable Energy, Energy Efficiency ............................... 79

China’s Grand Strategy on Hydropower ............................................................................................... 80

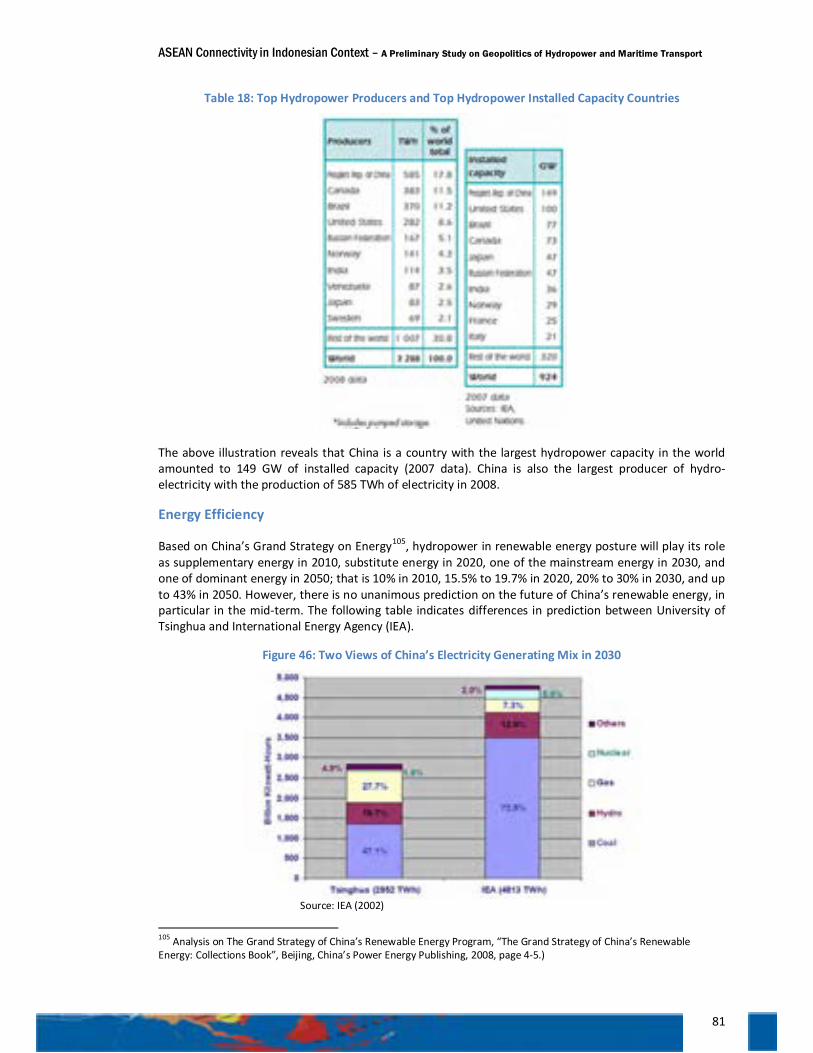

Energy Efficiency ................................................................................................................................... 81

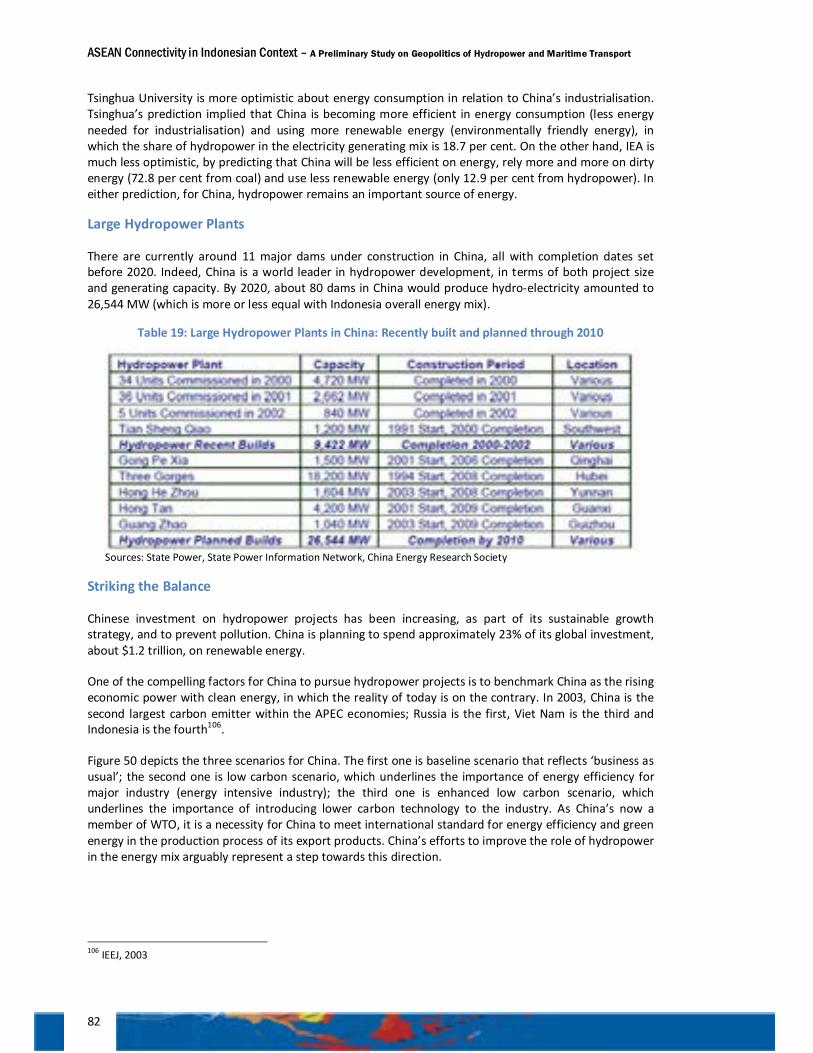

Large Hydropower Plants ..................................................................................................................... 82

Striking the Balance .............................................................................................................................. 82

Challenge .............................................................................................................................................. 83

Ecological and Social Aspects of Conventional Dams: Guangxi’s Longtan Hydropower Project .............. 83

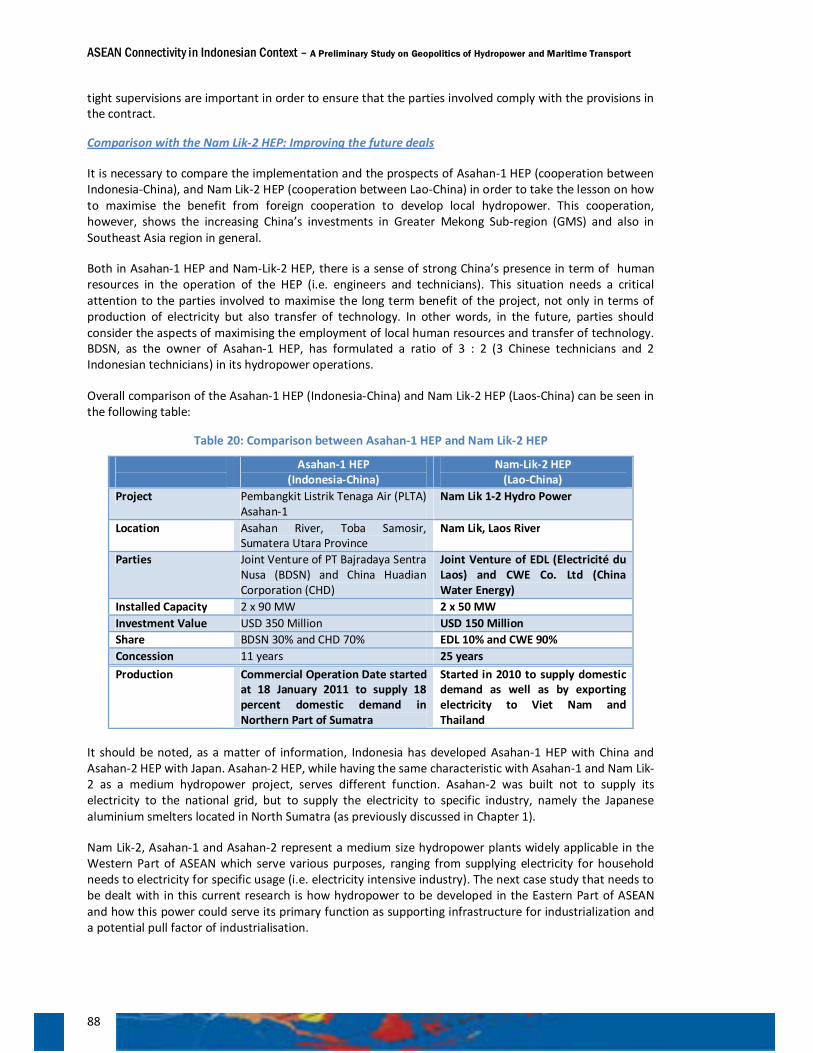

The Business of Medium Hydro: Asahan-1 and Nam Lik-2 Hydropower Projects .................................... 86

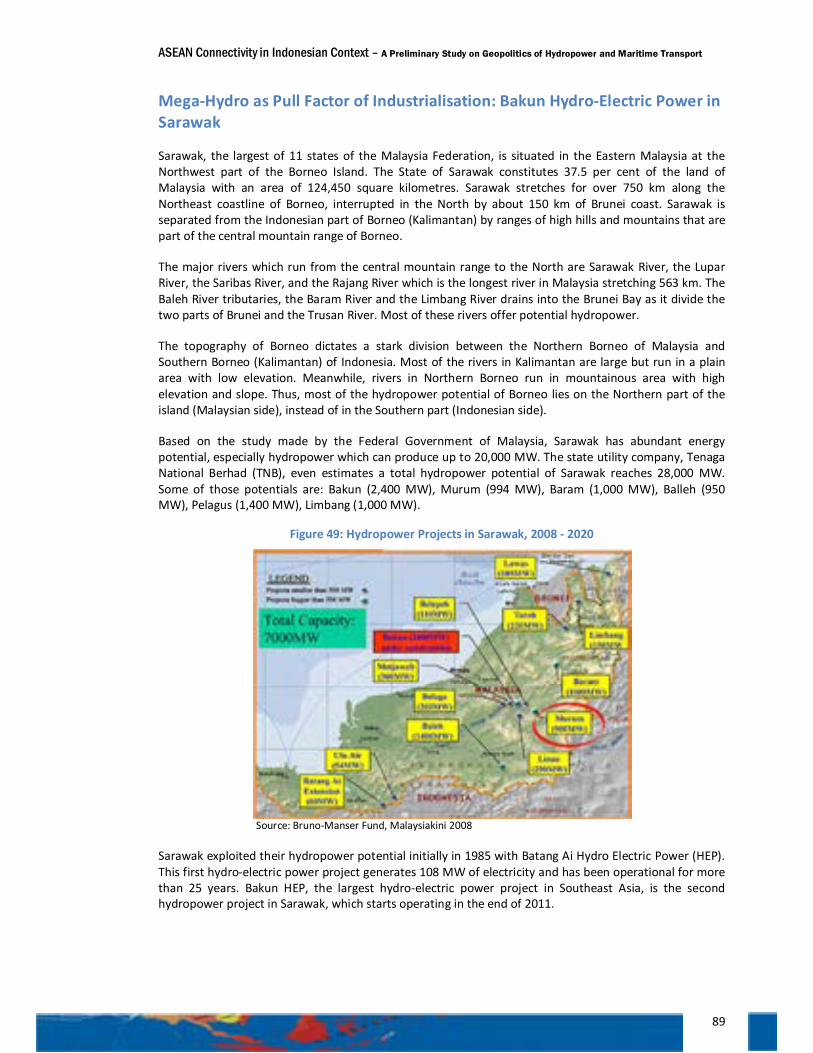

Mega-Hydro as Pull Factor of Industrialisation: Bakun Hydro-Electric Power in Sarawak ....................... 89

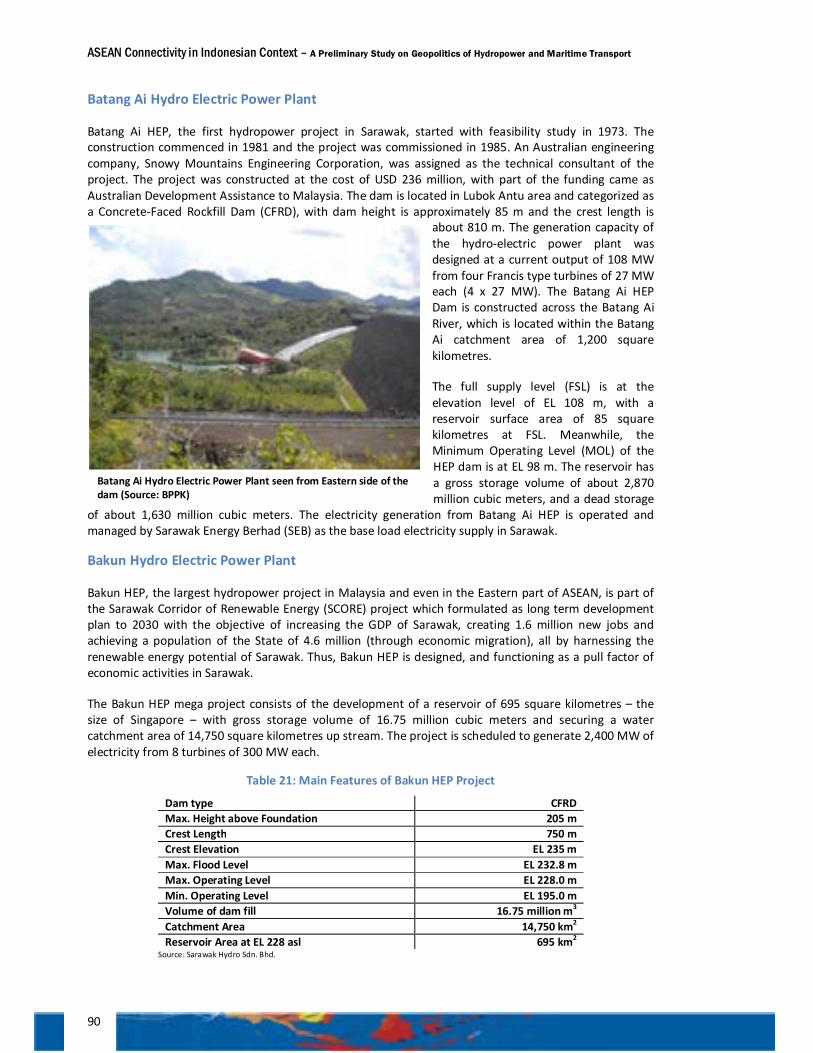

Batang Ai Hydro Electric Power Plant ................................................................................................... 90

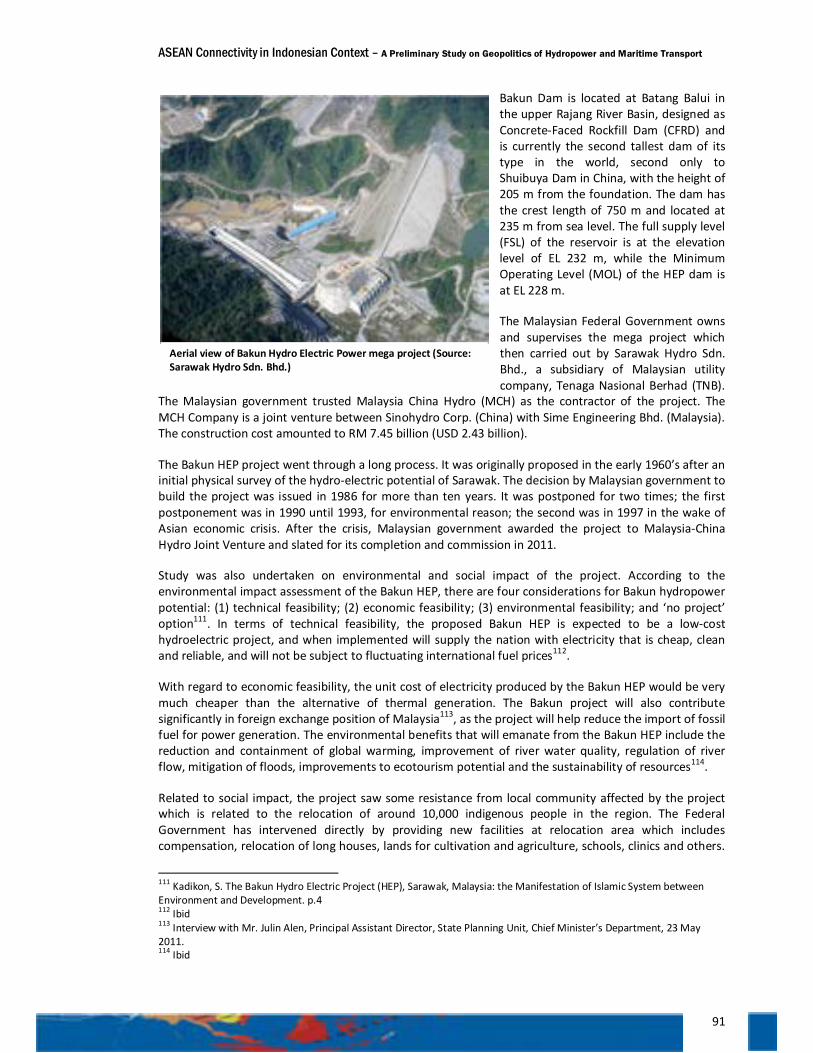

Bakun Hydro Electric Power Plant ........................................................................................................ 90

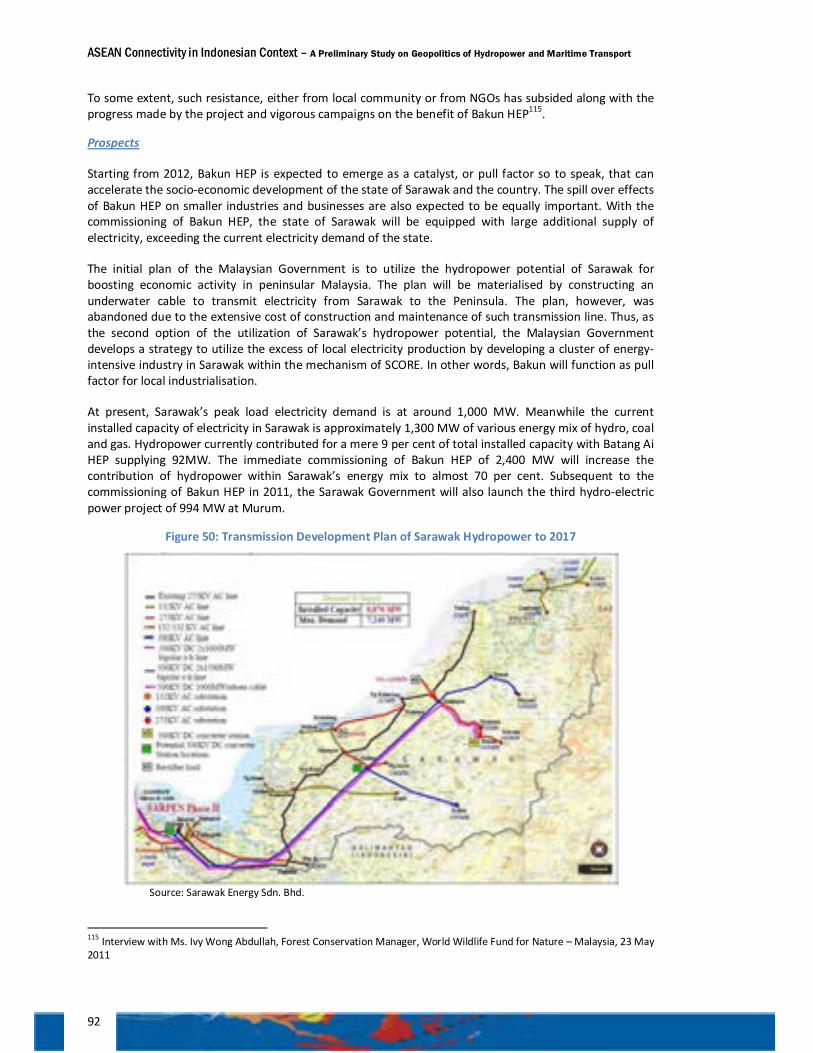

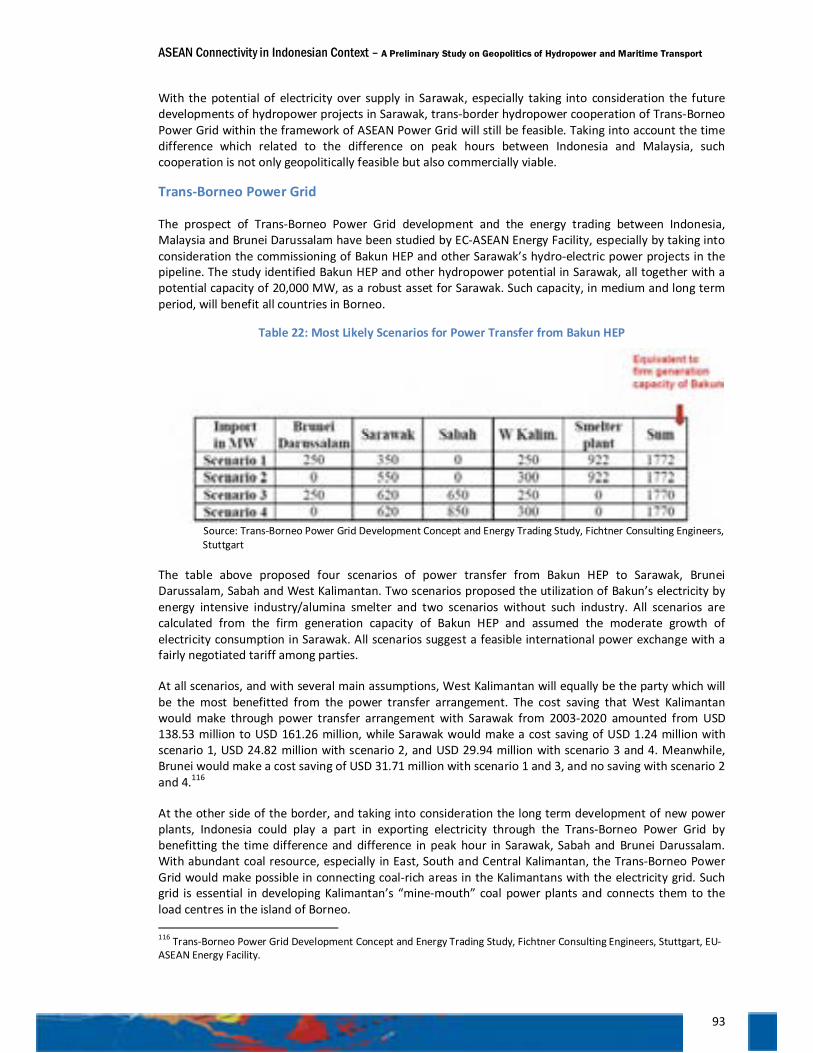

Trans-Borneo Power Grid ..................................................................................................................... 93

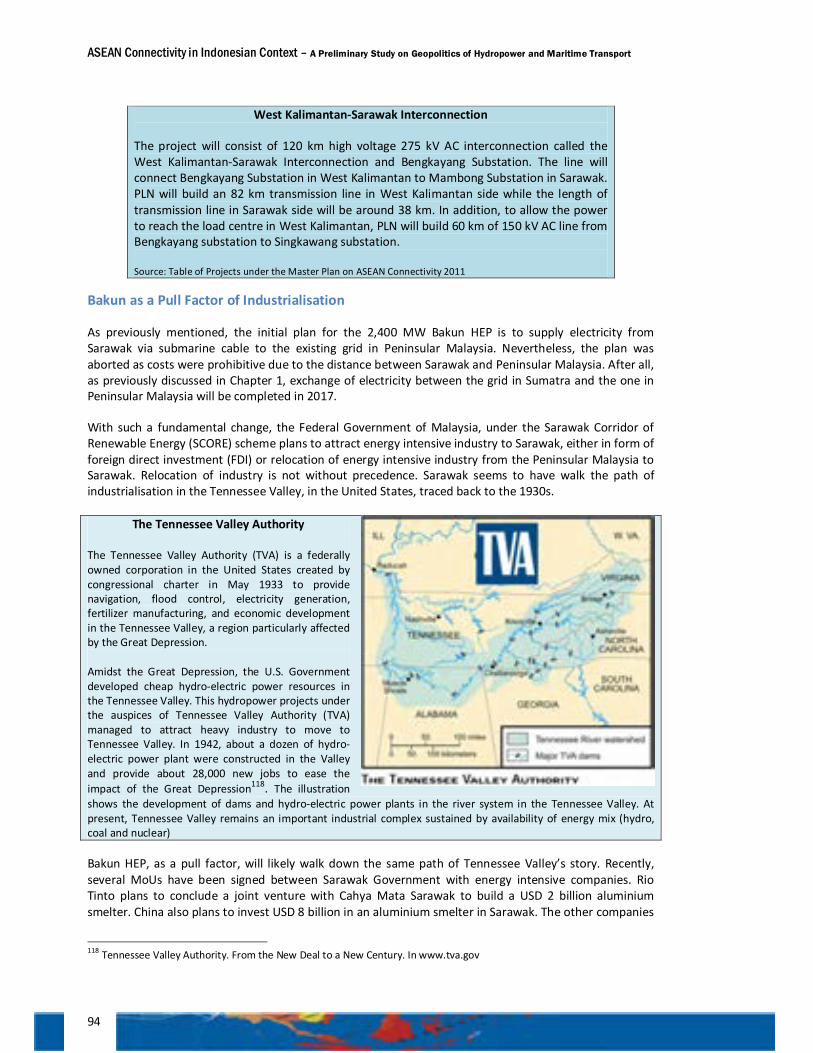

Bakun as a Pull Factor of Industrialisation ............................................................................................ 94

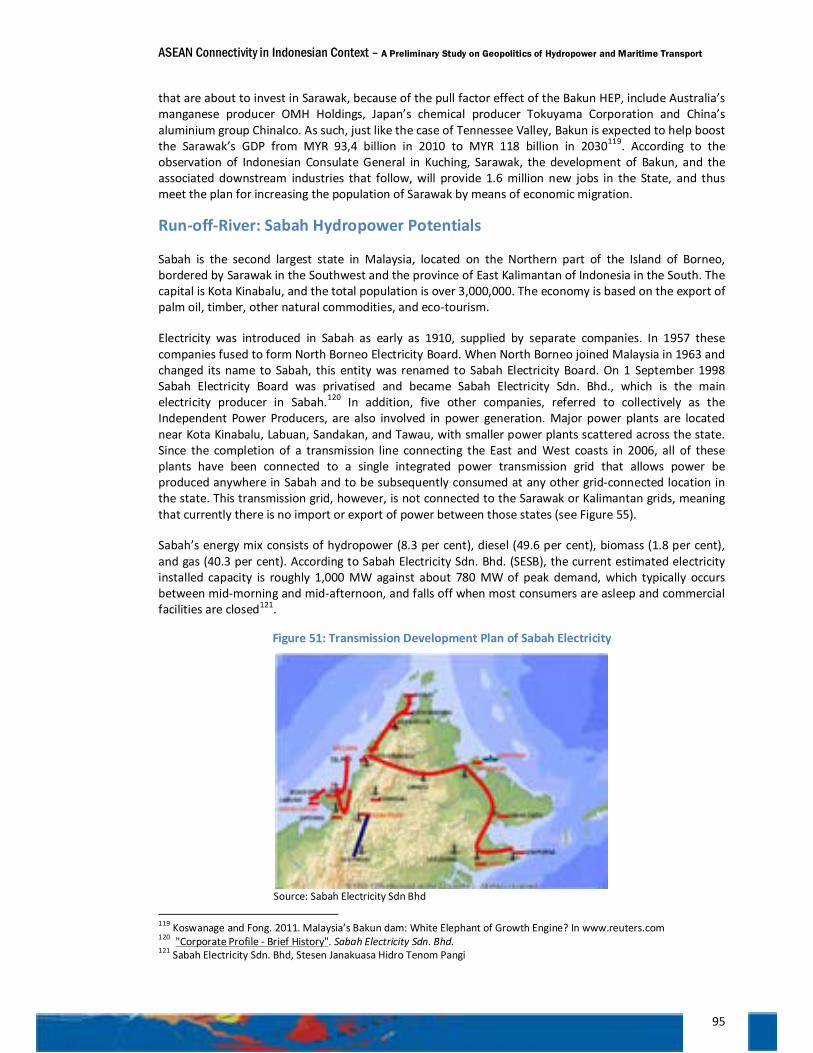

Run-off-River: Sabah Hydropower Potentials ........................................................................................... 95

The prospect of mini-hydropower projects .......................................................................................... 96

iii

Tenom Pangi run-off-river HEP ............................................................................................................. 97

Prospects ............................................................................................................................................... 98

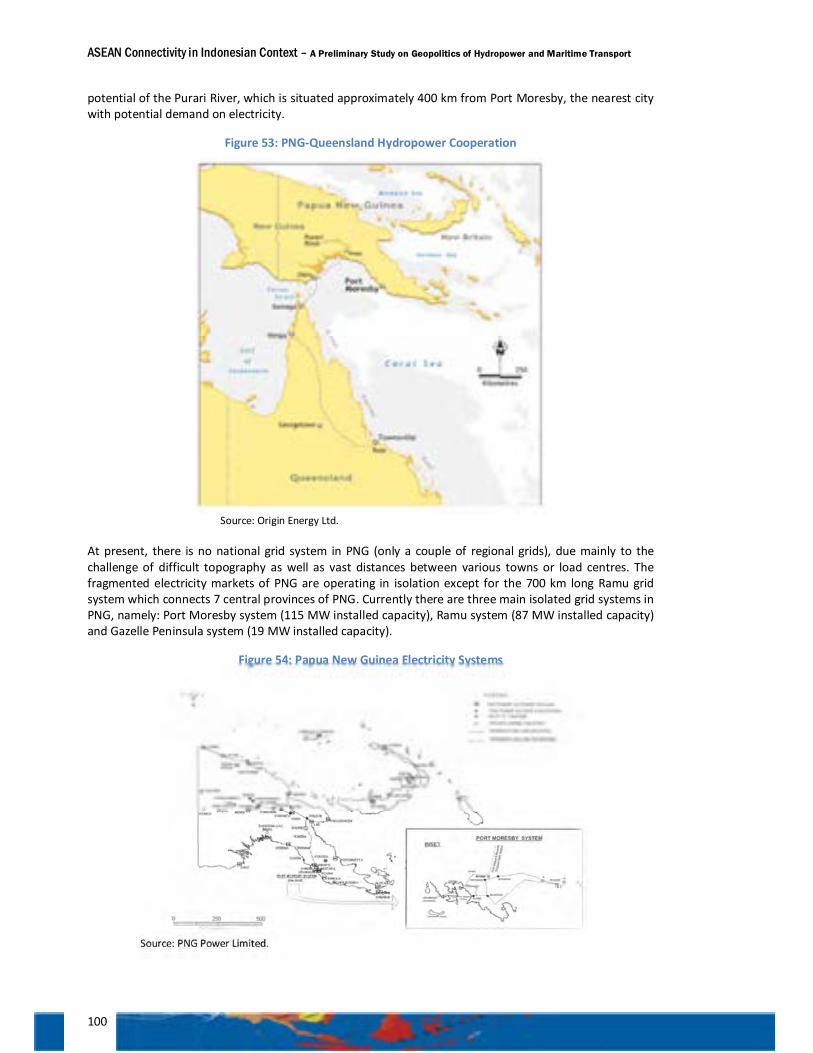

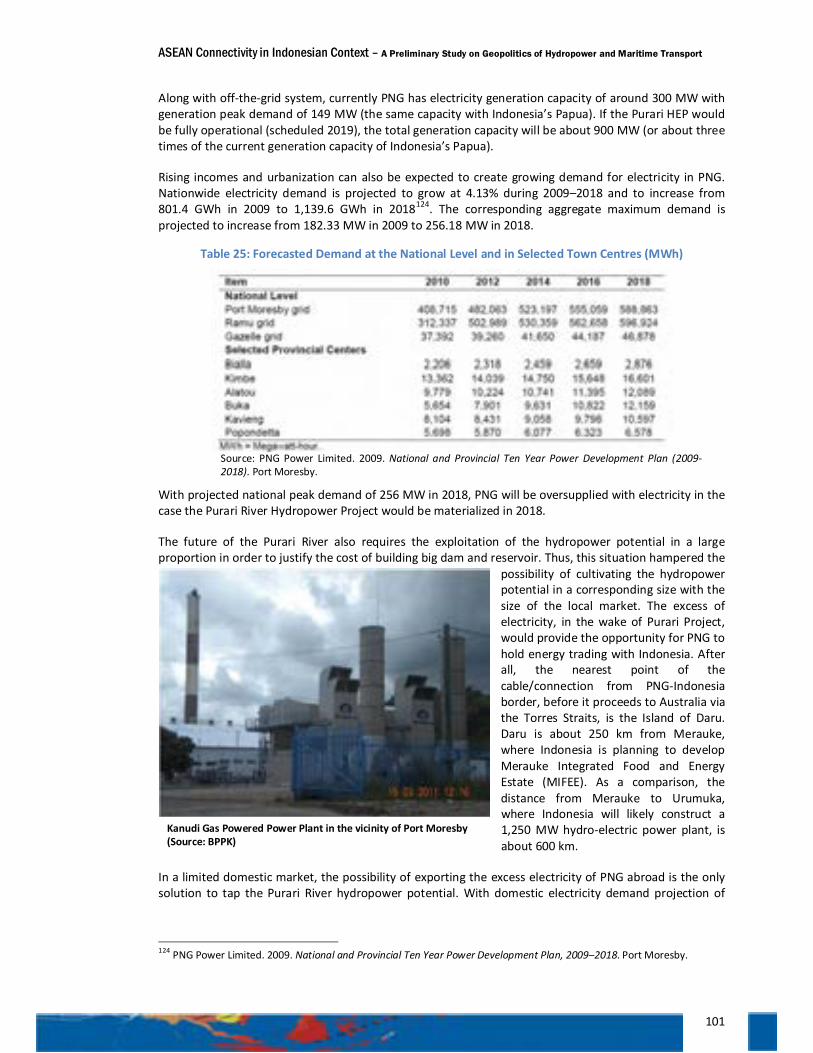

In the Quest of Larger Market: PNG-Australia Cross-border Hydropower Cooperation .......................... 99

Nature of Cooperation: Domestic and Foreign Market ........................................................................ 99

Challenges ............................................................................................................................................. 99

The Cooperation Begins ...................................................................................................................... 103

Prospects ............................................................................................................................................. 104

Papua: An ASEAN Gate to the Pacific with Big Potential of Energy Mix ................................................. 104

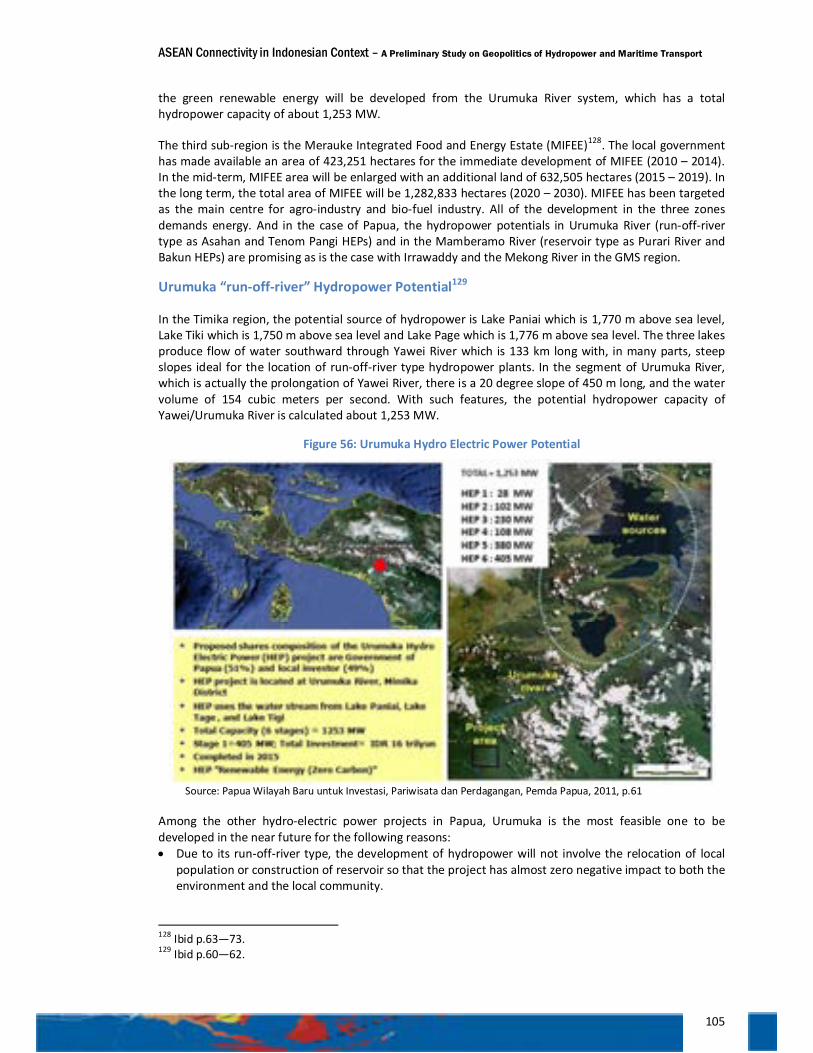

Urumuka “run-off-river” Hydropower Potential ................................................................................. 105

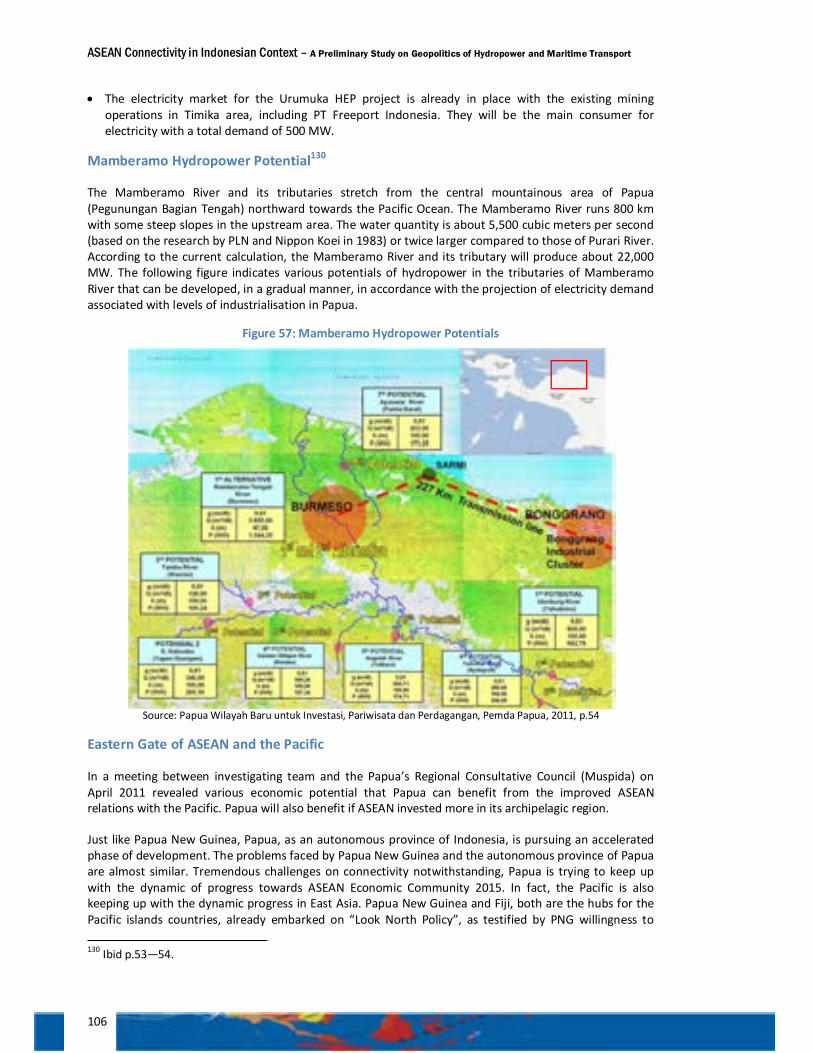

Mamberamo Hydropower Potential ................................................................................................... 106

Eastern Gate of ASEAN and the Pacific ............................................................................................... 106

Lesson Learned from the GMS: what is relevant to IMT-GT and BIMP-EAGA? ...................................... 108

Lesson learned from SRNH: what is relevant to Eastern Part of Indonesia? .......................................... 110

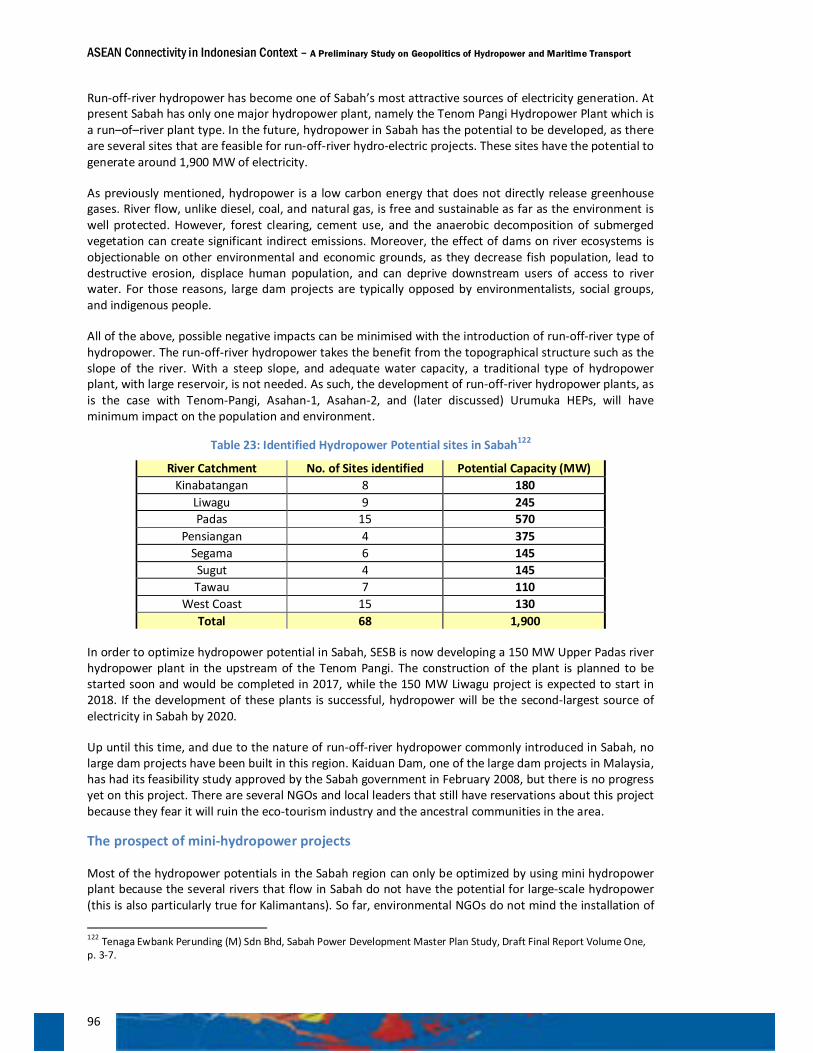

More lessons learned on maritime connectivity ..................................................................................... 111

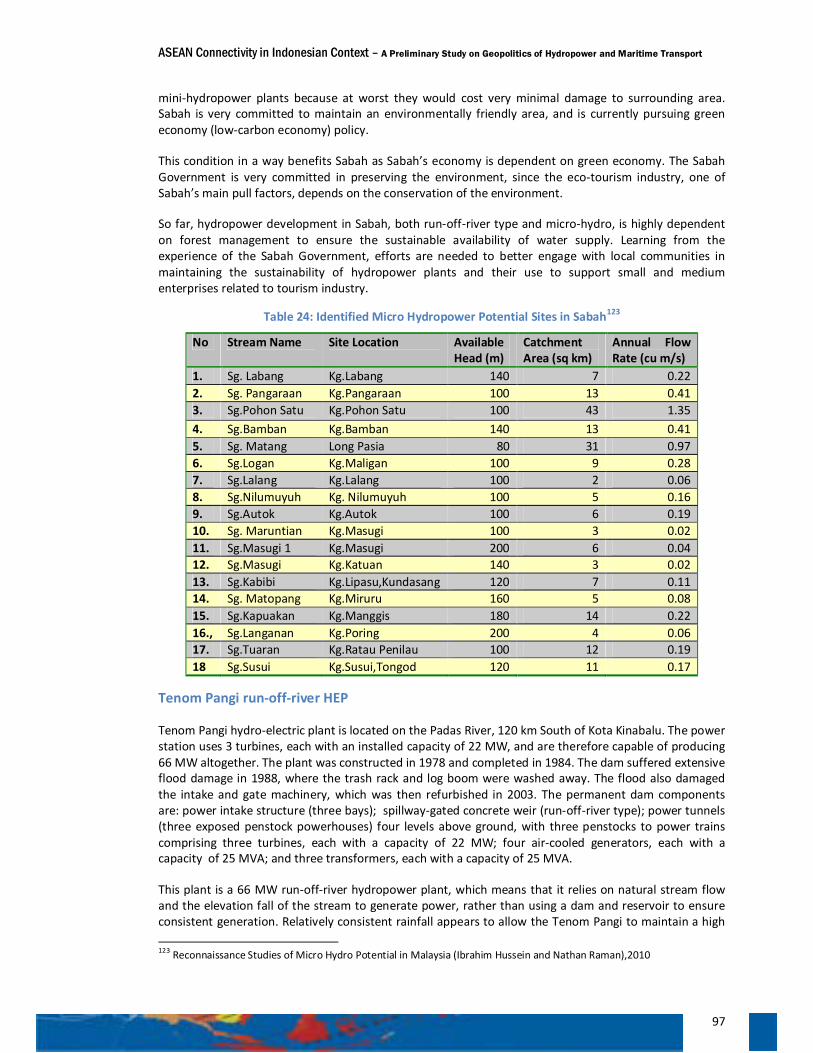

Recommendations .................................................................................................................................. 112

List of Abbreviations ........................................................................................................................ 118

List of Interviewees.......................................................................................................................... 121

About Investigators ......................................................................................................................... 124

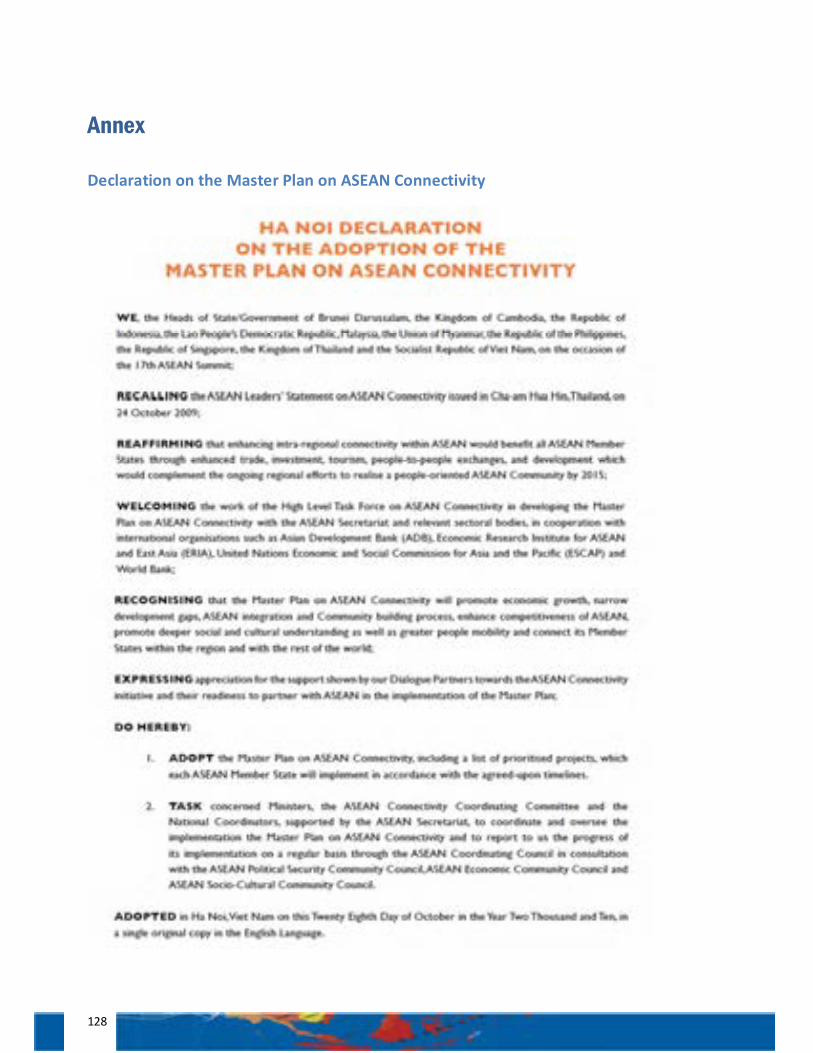

Annex ................................................................................................................................ 128

Declaration on the Master Plan on ASEAN Connectivity ........................................................................ 128

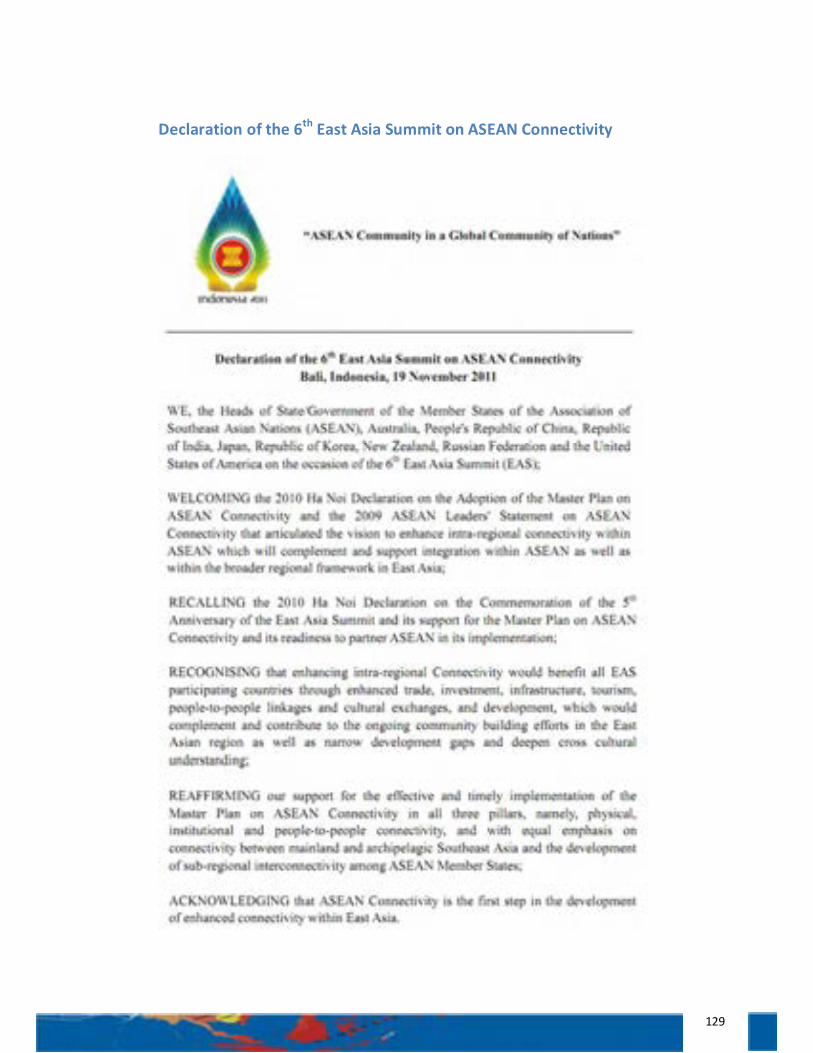

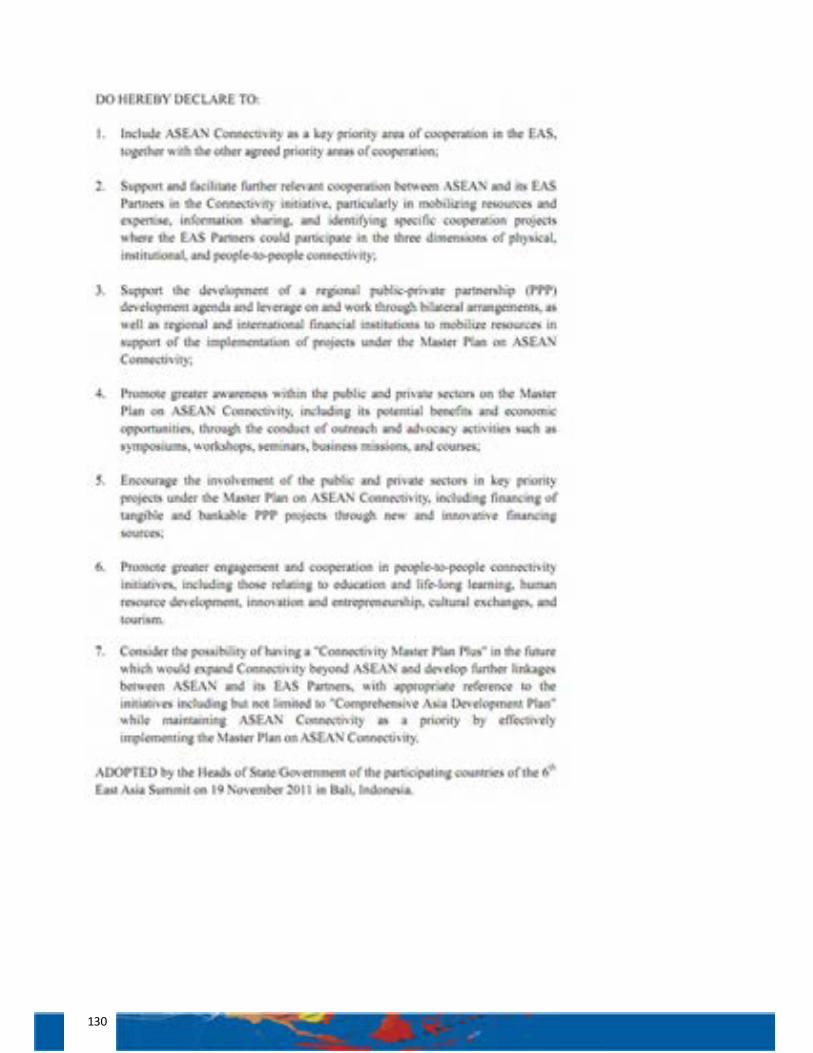

Declaration of the 6th East Asia Summit on ASEAN Connectivity ............................................................ 129

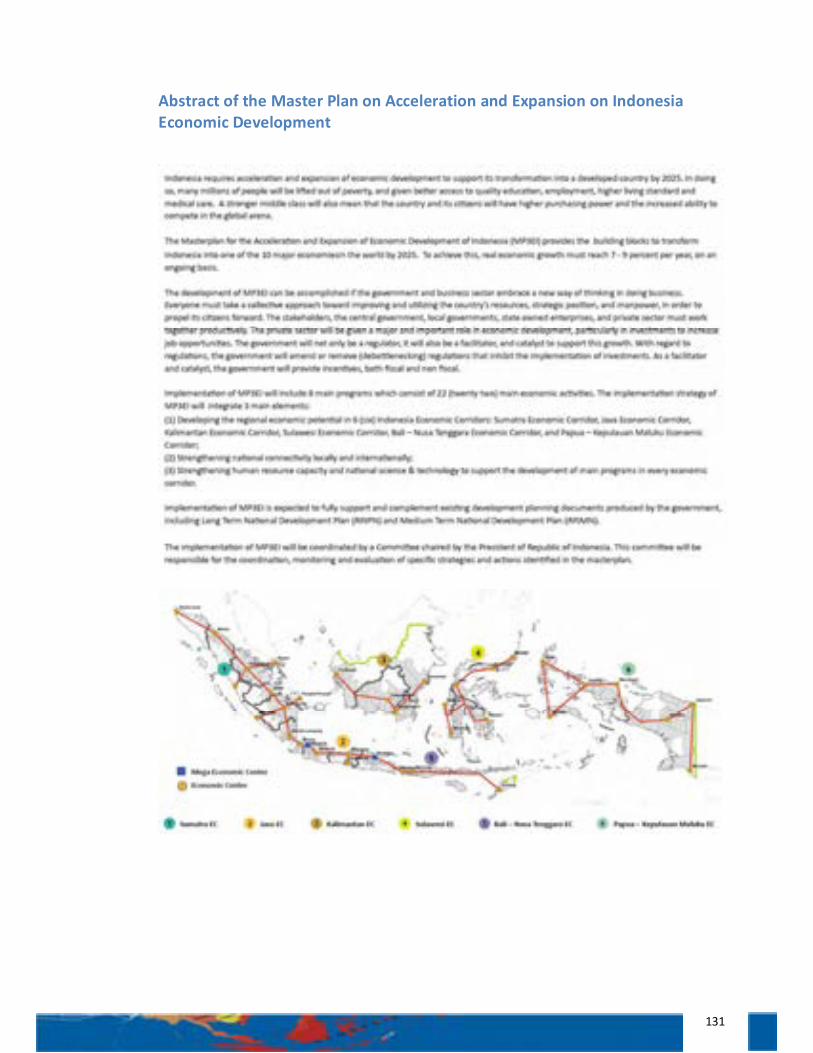

Abstract of the Master Plan on Acceleration and Expansion on Indonesia Economic Development ..... 131

iv

List of Figures Figure 1: Interaction between ASEAN Connectivity and ASEAN Community ................................................. 2 Figure 2: The Western and the Eastern Parts of ASEAN ................................................................................. 3 Figure 3: Connection between connectivity, industry and renewable energy ............................................... 4 Figure 5: Inalum’s Asahan-2 Hydro Electric Power Plant and its Smelting Plant ............................................ 6 Figure 6: Average Power Production Expense per kWh ................................................................................. 7 Figure 7: Mekong Basin Hydropower ............................................................................................................ 10 Figure 7: Heart of Borneo Initiative .............................................................................................................. 11 Figure 8: Identified Hydro Potential (MW) on ASEAN Power Grid ............................................................... 12 Figure 9: ASEAN Generation Capacity by Country and Fuel, 2007 and outlook for 2030 ............................. 13 Figure 10: Existing and Proposed ASEAN Power Grid Interconnections ....................................................... 14 Figure 12: Investing through Public-Private Partnership .............................................................................. 16 Figure 14: Quality of Infrastructure, 2009 .................................................................................................... 20 Figure 15: Toyota Regional Production Base ................................................................................................ 20 Figure 16: Japan’s Vision on ASEAN Connectivity (Vision 2) – “Maritime ASEAN Economic Corridor” ........ 21 Figure 17: Economic Corridors in GMS ......................................................................................................... 23 Figure 18: Maritime connectivity is currently concentrated in the Western Part of ASEAN ........................ 23 Figure 19: GMS location at Heart of Asia ...................................................................................................... 30 Figure 21: Map of Transport Corridors in the GMS ...................................................................................... 34 Figure 22: Transformation from Transport Corridors into Economic Corridors ........................................... 37 Figure 23: Nanning – Singapore Economic Corridor ..................................................................................... 38 Figure 24: East-West Transport Corridor Project of GMS ............................................................................. 40 Figure 25: Challenge for connectivity: Belawan – Penang case .................................................................... 50 Figure 26: IMT-GT Economic Connectivity Corridors .................................................................................... 51 Figure 27: Transportation cost significantly higher for inland mines ........................................................... 52 Figure 29: Map of Brunei, Indonesia, Malaysia, Philippines East ASEAN Growth Area ................................ 57 Figure 30: Energy Efficiency of Selected Mode of Transport ........................................................................ 58 Figure 31: SRNH as an Inter-modal Transportation System (Land-RoRo-Land) ............................................ 60 Figure 32: The Strong Republic Nautical Highway Routes ............................................................................ 61 Figure 33: The SRNH and ASEAN Connectivity .............................................................................................. 63 Figure 34: Vision for Archipelagic ASEAN: BIMP-EAGA-RoRo- Network ....................................................... 64 Figure 35: Passenger Traffic in millions ......................................................................................................... 64 Figure 36: Cargo Traffic via SRNH in metric tons .......................................................................................... 65 Figure 40: Map of Ro-Ro Ports in Bali and the Nusa Tenggaras.................................................................... 69 Figure 41: Prospect of ASEAN Connectivity in the Eastern Part of Indonesia............................................... 72 Figure 42: Sea Lanes of Communication and National Sea Lanes ................................................................. 73 Figure 43: Indotrans’ Shipping Service in South East Asia and Southwest Pacific ........................................ 76 Figure 44: Possible Study on Ro-Ro Network and Short-Sea Shipping ......................................................... 77 Figure 45: Electricity Production, Industrial Growth and Economic Growth in China, 1992-2008 ............... 79 Figure 46: China’s Electricity Generation Capacity by Energy Type, 2000 .................................................... 80 Figure 47: Two Views of China’s Electricity Generating Mix in 2030 ............................................................ 81 Figure 48: CO2 Emissions in China, 2000-2050 ............................................................................................. 83 Figure 49: Map of Guanxi Zhuang Autonomous Region ............................................................................... 84 Figure 50: Hydropower Projects in Sarawak, 2008 - 2020 ............................................................................ 89 Figure 51: Transmission Development Plan of Sarawak Hydropower to 2017............................................. 92 Figure 52: Transmission Development Plan of Sabah Electricity .................................................................. 95 Figure 53: Energy Forecast: Electricity demand is expected to reach 1,500 MW by the year 2020 ............ 98 Figure 54: PNG-Queensland Hydropower Cooperation .............................................................................. 100 Figure 55: Papua New Guinea Electricity Systems ...................................................................................... 100 Figure 56: Australian Electricity Generation by fuel, 2007-2008 ................................................................ 102 Figure 57: Urumuka Hydro Electric Power Potential .................................................................................. 105

v

Figure 58: Mamberamo Hydropower Potentials ......................................................................................... 106 Figure 59: Comparison on Flow of Goods between Containerized Shipping and Ro-Ro Shipping .............. 110

vi

List of Tables Table 1: Estimated Levelized Cost of New Generation Resources, 2016 ........................................................ 7 Table 3: Examples of Public Private Partnership Projects in Indonesia ready for bidding (in USD million) .. 17 Table 5: Comparison on Physical Connectivity Projects under The Master Plan on ASEAN Connectivity and ASEAN – Dialogue Partners Cooperation in the Archipelagic and the Mainland Regions of ASEAN ............ 22 Table 6: Composition of Ferry Fleet in Indonesia ......................................................................................... 24 Table 7: Number of Ro-Ro Vessels and Ports ................................................................................................ 24 Table 8: Priority Projects in the Vientiane Plan of Action 2008 – 2012 vis-à-vis the MPAC ......................... 32 Table 9: Transport Corridors of the GMS ...................................................................................................... 33 Table 10: Yunnan’s, Guangxi’s and Guangdong’s Trade with ASEAN and GMS Countries, 2009 ................. 39 Table 11: Navigable length of inland waterways transport in ASEAN member states ................................. 58 Table 12: Cost Comparison between Traditional and Ro-Ro Shipping ......................................................... 66 Table 13: Comparison of Ro-Ro Network in the Eastern and Western Part of Indonesia ............................ 68 Table 14: Profile of Pacific Island Countries .................................................................................................. 74 Table 15: Indicative Export Freight Rates in Indonesia ................................................................................. 75 Table 16: Potential Ro-Ro Routes in the perspective of MP3EI and MPAC .................................................. 76 Table 17: Proposed Feasibility Studies for Ro-Ro and Short-Sea Shipping Connectivity .............................. 77 Table 18: Top Hydropower Producers and Top Hydropower Installed Capacity Countries ......................... 81 Table 19: Large Hydropower Plants in China: Recently built and planned through 2010 ............................ 82 Table 20: Comparison between Asahan-1 HEP and Nam Lik-2 HEP ............................................................. 88 Table 21: Main Features of Bakun HEP Project............................................................................................. 90 Table 22: Most Likely Scenarios for Power Transfer from Bakun HEP .......................................................... 93 Table 23: Identified Hydropower Potential sites in Sabah ............................................................................ 96 Table 24: Identified Micro Hydropower Potential Sites in Sabah ................................................................. 97 Table 25: Forecasted Demand at the National Level and in Selected Town Centres (MWh) ..................... 101 Table 26: Key Performance Indicators for the Australian Electricity Industry ............................................ 102

vii

Preface

An inter-connected ASEAN through enhanced physical connectivity, institutional connectivity, and people-to-people connectivity looms high as the priority during Indonesian Chairmanship in ASEAN.

In the national context, the issue of connectivity has been the one of priority projects under the Master Plan for Acceleration and Expansion of Indonesia Economic Development (MP3EI), which is intended to attain high, balanced, fair and sustainable economic growth for all Indonesians.

Having the task of undertaking analysis and development in foreign policy and international relations, the Policy Analysis and Development Agency of the Ministry of Foreign Affairs (hereafter called “the Agency”) is committed itself to provide a strategic recommendation to the Foreign Ministry and other stakeholders on how the welfare of the nations can be enhanced by building a better connectivity, both in regional level (ASEAN), and in domestic level (Indonesian Archipelago).

To reach this goal, the Agency charged the Centre for Policy Analysis and Development of Asia Pacific and African Regions (hereafter called “P3K2 Aspasaf”) to undertake research based on field studies in various locations throughout the mainland and the archipelagic regions of ASEAN, and the contiguous areas as well.

It should be noted in advance, that the findings of this research, as documented in the book, titled: “ASEAN Connectivity in Indonesian Context: A Preliminary Study on Geopolitics of Hydropower and Maritime Transport”, have not qualified yet as a policy. Thus this book should not be regarded as the official position of the Indonesian Foreign Ministry.

It is my sincere hope that this research can contribute positively to the discourse of connectivity, both at national and regional level of ASEAN.

Herewith, I would like to appreciate all members of the Investigating Team - diplomats with strong idealism and dedication to their profession - for all the efforts and risks they took in completing this research.

Indeed, this research project cannot be completed without invaluable input and help from the advisors, and reviewers. I would like herewith to convey my highest appreciation to all of the distinguished advisors and reviewers for their generosity and help rendered to the Investigating Team.

Last but not least, allow me to extend my gratitude and appreciation to all of the facilitators and many other parties, who I could not mention one by one, who have made this project possible. For the Agency, this book is not the end of the research on ASEAN Connectivity, since we are going to revise and update it from time to time to meet the dynamic development in Southeast Asia and its immediate regions.

Jakarta, 20 December 2011 Ambassador WARDANA Vice Minister/Director General of Policy Analysis and Development Agency Ministry of Foreign Affairs

viii

PATRON:

Ambassador Wardana

INVESTIGATING TEAM:

The Centre for Policy Analysis and Development on Asia Pacific and African Regions (P3K2 Aspasaf)

Chief Investigator:

Siswo Pramono, LLM., Ph.D.

Investigators:

Lukman Hakim Siregar, M.IS., M.Si.

Arianto Surojo, S.S., M.A.

Donny Warmadewa, S.IP., MM., DEA

Sigit Aris Prasetyo, S.S., M.Hum.

Christine Refina, S.IP, MIS.

Adinda Hutabarat, S.Hum., M.M.

Yudho Priambudi Asruchin, S.H.

Eva K. Situmorang, S.Hum.

M. Reza Adenan, B.A.

Banga Malewa, S.Pd.

Indri Yanuarti, S.Sos.

Adkhilni M.Sidqi, S.IP.

Imad Yousry, S.Hum.

Ivan Namanto, B.A.

CONSULTANT:

Ambassador Amiruddin Noor

ix

ADVISORS: (In Personal Capacity) Ambassador I Gede Ngurah Swajaya, Indonesian Permanent Representative to ASEAN Chair of ASEAN Connectivity Coordinating Committee Drs. Erlangga Mantik, M.A. Deputy for Macroeconomic and Financial Coordination The Coordinating Ministry of Economic Affairs of the Republic of Indonesia

Ir. Bambang Hermawanto, M.Sc. Chairman of ASEAN Power Grid Consultative Committee Dr. Oktorialdi,

The Head of the Center for Data and Information Development Planning The National Development Planning Agency of the Republic of Indonesia Ir. Djoko Prasetijo, Ph.D. Head of System Planning Division of PT PLN (Persero) Drs. Youlman Jamal, Director of Bussiness Ferry Transportation of PT Indonesia Ferry (Persero) Ir. Bambang Purnomo Hidayat, M.BA.

Assistant Vice President of PT Bajra Daya Sentra Nusa (Asahan 1 Hydro Electric Power Plant)

REVIEWERS: (In Personal Capacity) Dr. Ir. Bambang Susantono, MCE. Vice Minister for Transportation of the Republic of Indonesia High Level Task Force on ASEAN Connectivity Mahendra Siregar, SE., MA. Vice Minister for Trade of the Republic of Indonesia Professor Dr. Dewi Fortuna Anwar, MA. Deputy for Political Affairs, Secretariat of the Vice President of the Republic of Indonesia

x

FACILITATORS: H.E. Da'i Bachtiar,

Ambassador of the Republic of Indonesia in Kuala Lumpur

H.E. Kria Fahmi Pasaribu, Ambassador of the Republic of Indonesia in Vientiane

H.E. Mohammad Hatta, Ambassador of the Republic of Indonesia in Bangkok

H.E. Pitono Purnomo, Ambassador of the Republic of Indonesia in Hanoi

H.E. Sebastianus Sumarsono, Ambassador of the Republic of Indonesia in Yangon

H.E. Yohanes Kristiarto Soeryo Legowo, Ambassador of the Republic of Indonesia in Manila

H.E. Handriyo Kusumo Priyo, Ambassador of the Republic of Indonesia in Bandar Seri Begawan

H.E. Soehardjono Sastromihardjo, Ambassador of the Republic of Indonesia in Phnom Penh

Kenssy Dwi Ekaningsih, Chargé d’affaires a.i., Embassy of the Republic of Indonesia in Singapore

H.E. Imron Cotan, Ambassador of the Republic of Indonesia in Beijing

H.E. Eddy Setiabudhi, Ambassador of the Republic of Indonesia in Dili

H.E. Andreas Sitepu, Ambassador of the Republic of Indonesia in Port Moresby

H.E. Aidil Chandra Salim, Ambassador of the Republic of Indonesia in Suva

Bambang Tarsanto, Consul General of the Republic of Indonesia in Ho Chi Minh City

Soepeno Sahid, Consul General of the Republic of Indonesia in Kota Kinabalu

Gary R. M. Jusuf, Consul General of the Republic of Indonesia in Sydney

Edi Yusup, Consul General of the Republic of Indonesia in Guangzhou

Lalu Malik Partawana, Consul General of the Republic of Indonesia in Davao City

Joko Suprapto, Acting Consul General of the Republic of Indonesia in Kuching

xi

Executive Summary The research will focus on two challenges of ASEAN Connectivity, in particular the maritime one. First is the discrepancy in the progress of connectivity between the Western part of ASEAN which is largely a land mass, and the Eastern Part of ASEAN, which is an archipelago. Second is the Eastern Part of ASEAN, which represents a weak link in the overall ASEAN maritime connectivity, despite the sub-region potential. This sub-region largely consists of the Philippines and the Eastern Part of Indonesia. The research concludes that economic pull factors are needed to speed up the development of connectivity in the Eastern Part of ASEAN. Cheap and abundant energy mix of hydro and coal power can become the pull factor to attract energy-intensive processing industries (i.e. smelters) to come to the region. The growing economic activity will eventually, as business dictates, induce development of connectivity in the archipelagic region of ASEAN.

The “ASEAN Connectivity in Indonesian Context: A Preliminary Study on Geopolitics of Hydropower and Maritime Transport” is the fruit of field research conducted by the Centre for Policy Analysis and Development on Asia Pacific and African Regions (P3K2 Aspasaf), the Ministry of Foreign Affairs of the Republic of Indonesia from December 2010 to July 2011. The field research was commenced in the Greater Mekong Sub-region (GMS), followed by field research in Indonesia-Malaysia-Thailand Growth Triangle (IMT-GT) and Brunei-Indonesia-Malaysia-Philippines – East ASEAN Growth Area (BIMP-EAGA) regions. The P3K2 Aspasaf investigating team has also conducted a field observation for the connectivity segments within the Pacific island states, the island of New Guinea (Papua and PNG), and the islands stretched across from Bali to Timor.

The objective of this book is to trigger the discourse regarding the connectivity in the Archipelagic Region of ASEAN (or Eastern Part of ASEAN), aside from being the initial input for the decision makers and general public in ASEAN regions.

It should be noted in advance that this research is not about hydropower and transport policy per se, nor about the Master Plan on the Acceleration and Expansion of Indonesian Economic Development (MP3EI). It is about the geopolitics of connectivity and energy, using maritime transport and hydropower as examples, since connectivity (including the maritime one) and energy represent strategic issues with economic and political implication to ASEAN integration.

The striking character of “connectivity” is its double edge nature. One needs to be careful in designing ASEAN Connectivity, or the national connectivity as expressed by Master Plan for Acceleration and Expansion of Indonesia Economic Development (MP3EI). Connectivity by nature works at both sides. Connectivity might lead into a better economic integration but somehow it might also lead into economic vulnerability, even disintegration, if the region is not well prepared for it. The phenomenon of “ASEAN divides” can be read as a new drive in the part of mainland region of ASEAN to integrate economically, due to geographical proximity, with the rising China. Thus consequently, this might lead into an “isolation” of the archipelagic region of ASEAN from the rest of the ASEAN region.

Assumedly, the more an economy is integrated, the more it becomes vulnerable to the negative impact of integration. The striking example was the Asian economic meltdown in 1997-1998. Most of the CLMV countries (Cambodia, Laos, Myanmar, Viet Nam), which then, had not yet been well integrated economically with the rest of the region, were relatively immune from the devastating, domino effect of the crisis. But, Indonesia and other ASEAN countries which had already been integrated with the economics of the region, suffered the most.

It is not to say that ASEAN should perceive “integration” with a negative tone, apprehensively ASEAN should only be aware of, and be prepared for, the possible unpredictability impact of such connectivity. Connectivity is the natural order of globalisation, what ASEAN needs to do is to maximize efforts to attain positive impact of connectivity while negating the negative impact. This is exactly the perspective of Indonesia should be when it attempts to fit the MP3EI into a broader ASEAN Connectivity, and ASEAN connectivity plus.

xii

One needs also to comprehend the complexity of connectivity. Connectivity might produce an unexpected outcome. It has been observed in the current research how connectivity works in the Philippines as exemplified by the success story of Strong Republic Nautical Highway, but the same connectivity produces less desired impact in the GMS as is the case with the East-West Economic Corridor (while many other corridors in GMS are successful).

ASEAN saw the once widening gap among countries in the mainland region; and now it also sees the gaps within and among economies in the archipelagic side of ASEAN. Therefore ASEAN should be able to address this very multiple challenges. The future of ASEAN Community, ASEAN centrality or ASEAN capacity to play a central role, against the backdrop of the dynamic regional architecture, much also depends on ASEAN capacity to narrow or to bridge the gaps within ASEAN and within ASEAN member countries as well.

It is thus important for the ASEAN strategists to understand the nature of archipelagic-mainland characters of connectivity, and thus the associated perspectives. ASEAN is not either archipelagic or mainland, but consists of the both characteristics. Thus ASEAN should not employ “one size fits all” approach to the problem among or within members. The solution for “land-locked” dis-connectivity in the mainland side is different from the solution for “isolated island” dis-connectivity in the archipelagic side. Building a road or a trail to an isolated land-locked area is different from establishing a shipping line to an isolated island area.

Technology, which will be materialized into the right infrastructure, will change the feature of most isolated islands areas in the archipelagic ASEAN. But technology, and the associated infrastructure, is expensive while most of the isolated regions are poor. But, ASEAN Community would agree that a common action is needed to break all of the dis-connectivity, if integration, economic or otherwise, is the common ideal of all peoples of ASEAN.

In practical level, it is imperative for Indonesia to address the gap within its maritime belts, which is largely the consequence of the economics of scale (i.e. load factors). Most of the maritime belts in the Western Part of Indonesia have already been commercialised due to the high level of economic activity in the West, and thus can easily be integrated into the regional or even global maritime connectivity. Most of the maritime belts in the Eastern Part of Indonesia remains largely pioneered due to the lack of economic activity in the sub-region, and thus cannot be easily integrated with the regional maritime connectivity. In a way, the improvement of maritime belts from the Western Part to the Eastern Part of Indonesia will be great contribution for the connectivity within ASEAN and beyond.

One possibility for ASEAN to help improve its maritime connectivity is by assisting Indonesia and the Philippines, for instance, to interconnect the Eastern belts of the Indonesian archipelago with the Strong Republic Nautical Highway of the Philippines.

On the archipelagic perspective of “connectivity plus”, it is necessary for ASEAN and for Indonesia to undertake feasibility study on the possible connectivity between Aceh, in the Western tip of Indonesian archipelago, with the new hubs of Myanmar’s Dawei, Yangon and Kyaukphyu in the Andaman Sea. On the other end, more study is needed in the possible development of “ASEAN connectivity plus” towards the Pacific, using Papua as the ASEAN Eastern gate to reach Papua New Guinea, Solomon Islands, the Northern part of Australia and the rest of the Pacific island states.

It should be noted, that ASEAN once vigorously pursues cooperation on the development of fertilizer industry to sustain ASEAN’s agriculture. In the light of ASEAN archipelagic perspective, it is necessary for ASEAN to enhance cooperation in the maritime-related strategic industry, which includes, but not limited, to shipping industry, shipyard, and development of maritime science and technology.

As the gap between the Western Part of ASEAN, which is heavily invested with infrastructure to boost economic development, and the Eastern Part of ASEAN which is lacking the supporting infrastructure, is a nowadays reality, ASEAN should devise a strategy for an even connectivity through industrialisation.

Learning from the experience of the Western Part of ASEAN, in particular the GMS region, one may infer that a pull factor is needed to accelerate the industrialisation process. The new government of Myanmar, for instance, is contemplating on a “water law” to support the development of agriculture, mining, and

xiii

power generation industries. For Myanmar, the mighty river such as Irrawaddy is a blessing given by nature to support industrialisation, both in term of its potential development into effective irrigation and prospective hydropower. The mighty Mekong River (or Lancang River) assumes the same role. Mekong River is not only the life vein for agro-industry in the GMS, but also a vital source of hydropower. In other words, in the Western Part of ASEAN, hydropower represents an effective pull factor, if not in a lesser role as a main supporting infrastructure, for industrialisation.

The Eastern Part of ASEAN is also blessed with the mighty rivers. It is time to explore and exploit in the most sustainable way the mighty rivers such as Rajang River in the Island of Borneo or Mamberamo and Purari rivers in the Island of New Guinea as the pull factor to bring energy intensive industry to come to the Eastern Part of ASEAN. Equally important, run-off-rivers such as Urumuka and Asahan, also need to be sustainably explored and exploited.

Sarawak offers good example about the use of hydropower as a pull factor for industrialisation. The development of Bakun Hydro Electric Power mega project in Sarawak has induced the relocation of industry from Peninsular Malaysia to Sarawak or the establishment of completely new industry in Sarawak. The industrialisation of Sarawak will give economic and social impact in the neighbouring regions of Kalimantans and beyond. It is yet to see, however, how the commissioning of Bakun in 2011, which means the availability of an additional 2,400 MW of electricity in Sarawak, which will provide a considerable surplus to be absorbed by the coming energy intensive industry, will be able to bring economic progress, industrialisation and otherwise, in the Northern Part of Borneo.

In the same way, the commencement of Purari project which is adjacent to Merauke, will bring more economic activity in the Southern Part of PNG. As previously mentioned, the main problem of development of the Eastern Part of ASEAN and hence the Eastern Part of Indonesia, is the economics of scale. The market is too small to sustain durable economic activities. The development of electricity generation has always been hampered by the very limited domestic demand, since the users are largely, scattered households. To develop a project like Bakun would prerequisite a larger market, and thus a higher demand of electricity. Compared with other commodities, electricity has a specific characteristic that is the electricity is produced and consumed at the same time. The fact that PNG is able to beneficially combine PNG’s market and Queensland’s market to sustain the development of electric power industry, poses a challenge for Papua to be creative in finding the way to break the vicious circle of the “chicken and egg” phenomenon. The question for Papua is: what should be developed first. It is the basic infrastructure including electricity to attract industry; or the business activity to encourage the development of basic infrastructure, including electricity?

The exportation (or exchange) of electricity aside, mega projects like Bakun in the Northern Part of Borneo, and Purari across the border of Papua, should bring awareness for those in the Eastern Part of ASEAN, on the importance of energy exchange as the efficient way to provide industry with reliable source of electricity. In Borneo Island, interchange is possible, as it has been proved nowadays, albeit limited, between Kalimantans and Sarawak or Sabah. In the future, with the development of coal-rich Kalimantan Corridor as the source of fossil energy, wider interchange between coal-based and hydro-based across Borneo is possible. The industrialisation of the Eastern Part of ASEAN should take this possibility, and opportunity, into consideration.

At the end of the day, the ASEAN competitiveness, in the long-term, in particular when the labour pools in the region are exhausted, will also much depend on the availability of cheap, reliable source of energy, such as hydropower, in ASEAN industry. The presence of hydro mega projects in the Southern Part of China, in the GMS region, and recently in Sarawak, is not without thorough calculation. It represents the quest for competitive energy, for competitive industry.

As such, it is timely and important for ASEAN to devise the region with a common platform that enable it to develop a regional understanding to support development of ASEAN as a single, competitive production base with supporting infrastructure such as maritime connectivity and competitive energy mix (including hydro and coal).

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

1

Chapter 1 | INTRODUCTORY ESSAY: Hydropower as a Pull Factor for Connectivity in Mainland and Archipelagic Regions of ASEAN

Background of ASEAN Connectivity

Before discussing the role of hydropower and connectivity in the economic development and economic integration in the mainland and archipelagic regions of ASEAN, the introductory essay will start with the background of ASEAN Connectivity.

The idea of ASEAN connectivity was first proposed by Thai Prime Minister Abhisit Vejjajiva at the Opening Ceremony of the 42nd ASEAN Foreign Ministers’ Meeting on 20 July 2009 in Phuket. As the Chairman of ASEAN, Prime Minister Abhisit proposed that a “Community of Connectivity” should be one of the objectives of ASEAN Community 2015. It means that goods and peoples, investment and initiatives, can travel obstacle-free throughout the region. A fully integrated ASEAN economy as a single market and production base must have such connectivity built into both its hardware and software1. It is expected that through a well-connected Community, ASEAN can realize its full economic potentials as well as take maximum advantage of the strategic location linking the massive economies of South Asia on the West and Northeast Asia to the North.

This initiative was endorsed with the adoption of the ASEAN Leaders’ Statement on ASEAN Connectivity at the 15th ASEAN Summit held in Hua Hin on 24 October 2009. ASEAN Leaders mandated the creation of a High Level Task Force (HLTF) on ASEAN Connectivity to devise a Master Plan on ASEAN Connectivity by the 17th ASEAN Summit 2010. The Master Plan is both a strategic document for achieving overall ASEAN Connectivity and a plan of action for immediate implementation for the period 2011 – 2015 to connect ASEAN through enhanced physical infrastructure development (physical connectivity), effective institutional arrangement (institutional connectivity) and empowered people (people–to–people connectivity)2.

On 28 October 2010, ASEAN Leaders adopted the Ha Noi Declaration of the Adoption of the Master Plan on ASEAN Connectivity. In this Declaration, the ASEAN Leaders recognized that the Master Plan on ASEAN Connectivity will promote economic growth, narrow development gaps, speed up ASEAN integration and Community building process, enhance competitiveness of ASEAN, promote deeper social and cultural understanding, smooth people mobility, and connects its Member States within the region and with the rest of the world.

The Leaders also tasked the Ministers, the ASEAN Connectivity Coordinating Committee and the National Coordinators, supported by the ASEAN Secretariat, to coordinate and oversee the implementation of the Master Plan on ASEAN Connectivity and to report to the ASEAN Leaders about the progress of the implementation on a regular basis through the ASEAN Coordinating Council.

Connectivity in ASEAN Context

As such, ‘connectivity’, according to the document of the Master Plan on ASEAN Connectivity, refers to the physical, institutional and people-to-people linkages that comprise the foundational support and

1 Statement of Prime Minister of Thailand, H.E. Mr. Abhisit Vejjajiva at the Opening Ceremony of the 42nd ASEAN Foreign Ministers’ Meeting in Phuket, 20 July 2009. 2 Master Plan on ASEAN Connectivity, Executive Summary, p.i.

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

2

facilitative means to achieve the political-security, economic, and socio-cultural pillars towards realizing the vision of an integrated ASEAN Community.

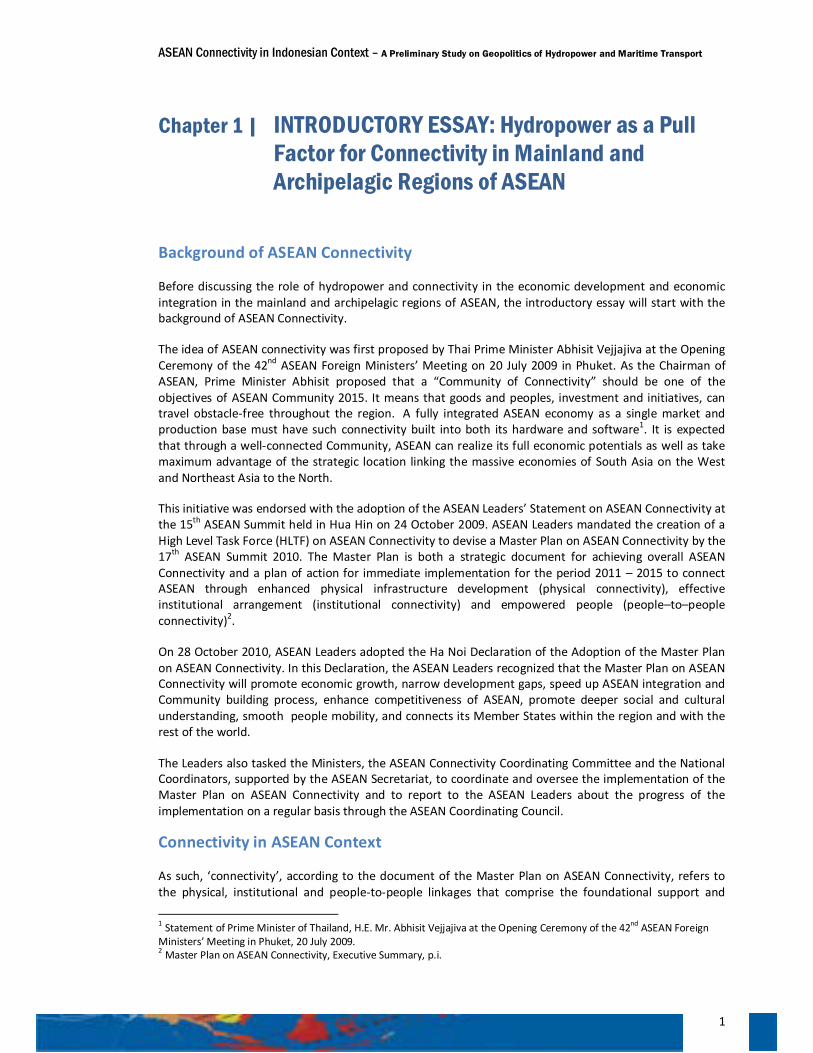

Figure 1: Interaction between ASEAN Connectivity and ASEAN Community

Source: Modified from ERIA

According to the document, the key elements of ASEAN Connectivity include: (1) physical connectivity (i.e. transport, energy, and information and communications technology); (2) institutional connectivity (i.e. trade liberalization and facilitation, investment and services liberalization and facilitation, mutual recognition agreements/arrangements, regional transport agreements, cross-border procedures, capacity building programs); and (3) people-to-people connectivity (i.e. education and culture, as well as tourism).

The global community is expected to contribute to the implementation of the Master Plan since a well-connected Southeast Asia, due to its geostrategic values, will be better for the regional and global security, stability and welfare. As such, it is time for ASEAN Dialogue Partners to help ASEAN implement the Master Plan, especially since resource is an important part of the implementation. According to a study by ADB, it is estimated that ASEAN countries will require infrastructure investment of USD 596 billion during 2006-2015 or about USD 60 billion a year. The ASEAN Infrastructure Fund (AIF) was then established to help address the resource mobilisation problem. The AIF is being set up with an initial equity contribution of USD 485.2 million, of which USD 335.2 million is from ASEAN while the remaining USD 150 million is from ADB. About six projects each year are expected to be carried out starting 2012. The Fund’s total lending commitment through 2020 will be around USD 3.6 billion. It will provide financing for selected public-private partnership (PPP) projects. It is hope that this will attract even greater foreign capital inflows to the region. Foreign direct investment flows in the region doubled to USD 75.8 billion in 2010 from USD 37.8 billion in 2009, and for the first time more than USD 12 billion of those flows were sourced within ASEAN.

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

3

The 6th East Asia Summit, held in Bali, 19 November 2011, has declared its support to the implementation of the Master Plan on ASEAN Connectivity. As such, it is time for the governments of the ASEAN Member States to work closely together with the private sectors and the governments of (in alphabetical order) Australia, China, India, Japan, Republic of Korea, New Zealand, Russia and the United States to materialize, in a comprehensive manner, the ASEAN Connectivity. EAS notwithstanding, cooperation with other members of global community of nation is well expected. Such cooperation should be focused particularly in mobilization of resources and expertise, information sharing, and identification of specific cooperation projects where the EAS Partners could participate in the three dimensions of physical, institutional, and people-to-people connectivity. EAS aside, the UN has also lent supports to the implementation of the ASEAN Connectivity.

Identification of Issues

Among the main issues in the ASEAN connectivity are discrepancy and dis-connectivity. First, there is a discrepancy in the progress of connectivity between the Western Part of ASEAN, which is landmass in nature, and the Eastern Part of ASEAN, which is archipelago. Second, as it concerns maritime transport, connectivity between the Western Part of ASEAN and the Eastern Part of ASEAN is poor (thus, this represents an issue of dis-connectivity). Third, the Eastern Part of ASEAN, which largely consists of the Eastern Part of Indonesia, represents the weakest link in the overall ASEAN Connectivity. Fourth, pull factors are needed to speed up the process of connectivity building. These four issues must be addressed accordingly by ASEAN.

Figure 2: The Western and the Eastern Parts of ASEAN

For the purpose of this research, the area identified as “the Western Part of ASEAN” includes the Greater Mekong Sub-region (GMS) minus Yunnan and Guangxi, and Indonesia-Malaysia-Thailand Growth Triangle (IMT-GT), as well as Singapore and Java. GMS, IMT-GT, Singapore and Java are well connected one to the others. The area identified as “the Eastern Part of ASEAN” includes the Philippines archipelago, Sarawak, Sabah, Brunei and the Indonesian economic corridors (as identified in the “Master Plan of Accelerated Economic Development of Indonesia – MP3EI) of Kalimantan, Bali – NTT, Sulawesi, and Maluku-Papua. The core area of the Eastern Part of ASEAN is the Brunei-Indonesia-Malaysia-the Philippines - East ASEAN Growth Area (BIMP-EAGA). Connectivity in this sub-region is relatively poor

Connectivity as the Focus of the Current Research

This research will focus on physical connectivity in the Eastern Part (archipelagic region) of ASEAN, in particular in the sector of maritime transport and renewable energy, and, to some extent will also look at the relevant institutional connectivity. The main assumptions are these: first, the connectivity in the

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

4

archipelagic region of ASEAN can be achieved by enhancing maritime connectivity and the related institutional connectivity, thereby reducing the costs of investment and the cost of international trade in goods and services, including services link costs and network set-up costs. Second, enhanced physical and institutional connectivity can contribute to narrowing development gaps in the archipelagic region as well as the gap between the archipelagic and the mainland regions of ASEAN, by expanding the frontiers of production/distribution networks. Yet, the augmenting people-to-people connectivity, will further nurture a sense of community in ASEAN as a whole.

Aim and Purpose of the Research

The aim of this research is three-folds. The first one is to observe the current state of affairs in the implementation of the Master Plan on ASEAN Connectivity, which is, as previously mentioned, marked by the stark discrepancy between the rapid infrastructure development in the mainland region of ASEAN and the slow, if not neglected, infrastructure development in the archipelagic region of ASEAN. The second one is to study how the two main regions of ASEAN, the mainland and the archipelago, could enhance, and thus benefit from, an even, yet effective, regional connectivity. Third, is to investigate the pull factors that can be used as a leverage to draw connectivity from the mainland region to the archipelagic regions of ASEAN.

The purpose of this research is to provoke public opinion moulders (i.e. the general public, academicians, and decision makers) to pay more attention, to have more debates, to undertake more feasibility studies, and thus to devise better policy dedicated to the development of maritime connectivity in the Eastern Part of ASEAN. Having set the aim and purpose of the research, a thesis thus needs to be formulated.

The Thesis: Pull factors should be determined to promote connectivity

The main thesis of this research is as follows: the hydropower potentials in the Eastern Part of ASEAN, in particular in the islands of New Guinea and Borneo, should be carefully explored and sustainably developed in order to support the availability of the cheap, competitive energy mix, that is able to function as a pull factor to drive economic activity, that will eventually drive an even connectivity within the archipelagic region of ASEAN, as well as between the archipelagic and the mainland regions of ASEAN.

As such, the research will focus on the inter-link between hydropower as potential renewable energy in the energy mix (and thus part of a potential pull factor for trade and industrialisation projects) and the development of maritime connectivity.

In modern time, electricity is the backbone of industrialisation. All of acceleration strategy can only be attained if ASEAN is able to promote synergy in the development of industry/natural resources, connectivity, and availability of competitive energy mix, as illustrated as follows:

Figure 3: Connection between connectivity, industry and renewable energy

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

5

The point is this: first the government needs to develop power plants, or otherwise to make electricity available, in the area projected as industrial zone. The availability of competitive energy mix will attract investors to invest on energy intensive industry and in that particular industrial zone. As the energy-intensive industry flourishes, investors are keen to invest further in the related downstream industries. Investors, too, are likely interested in connecting such industrial areas with the market or other production centres. It should be noted that the reference of “industry/natural resources” is used, because in Indonesia’s perspective as expressed in the Master Plan of Acceleration and Expansion of Indonesia Economic Development (MP3EI), the type of industry developed in the eastern corridors (i.e. Kalimantan, Sulawesi, Maluku-Papua) is the one which is correlated with the existing main natural resources (i.e. Kalimantan as a centre for production and processing of national mining and energy reserves; Sulawesi as a centre for production and processing of agriculture, plantation, fishery, oil and gas, and mining; Maluku-Papua as a centre for development of food, fishery, energy, and national mining).

In BIMP-EAGA context, for instance, the development of 2,400 MW hydro-electric power plant in Bakun (Sarawak), adding to Sarawak’s generating capacity of 1,300 MW, which will be discussed in Chapter 4, will incite the relocation of industry from Peninsular Malaysia to Sarawak and the establishment of new industry in Sarawak. Because of the availability of cheap hydro-electric energy, investors are interested in developing energy intensive industry, such as aluminium smelters, in Sarawak. At present, some MoUs have been concluded between the Government of Sarawak and some smelters. And in the later stage, the investors will likely be interested in developing connectivity between Peninsular Malaysia to Sarawak and from Sarawak to other regional and global markets. Thus, in this case, Bakun has functioned as the pull factor for industrialisation in Sarawak.

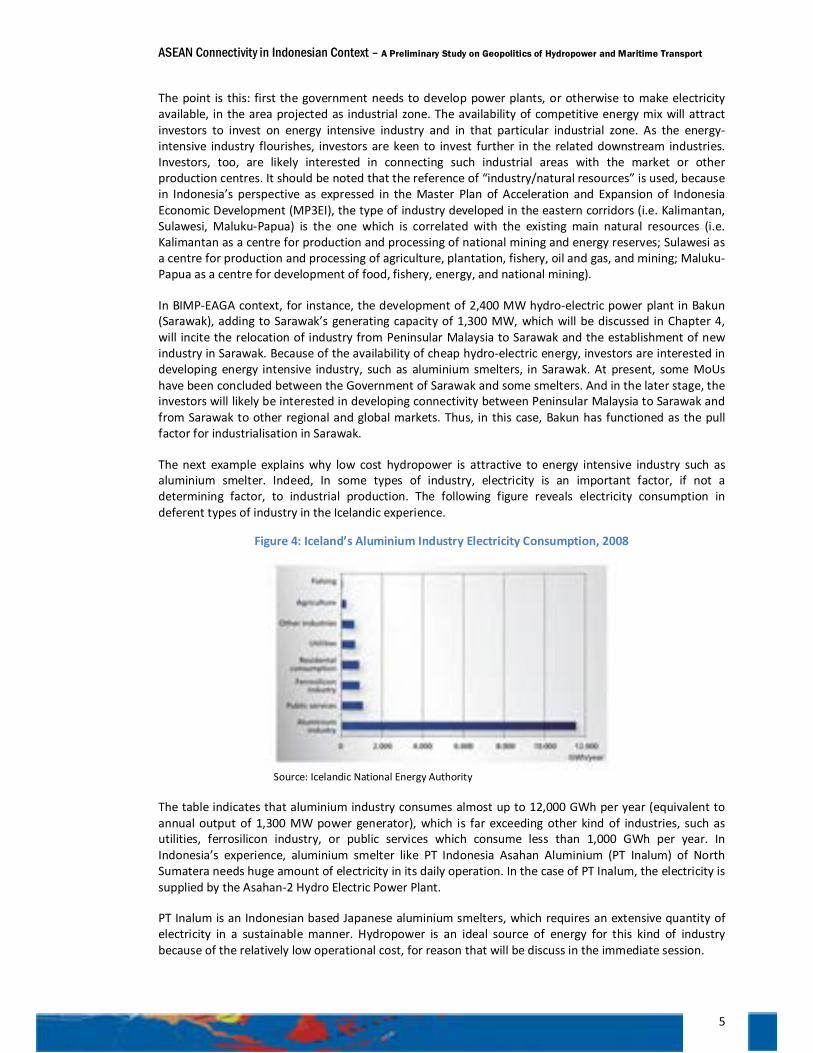

The next example explains why low cost hydropower is attractive to energy intensive industry such as aluminium smelter. Indeed, In some types of industry, electricity is an important factor, if not a determining factor, to industrial production. The following figure reveals electricity consumption in deferent types of industry in the Icelandic experience.

Figure 4: Iceland’s Aluminium Industry Electricity Consumption, 2008

Source: Icelandic National Energy Authority

The table indicates that aluminium industry consumes almost up to 12,000 GWh per year (equivalent to annual output of 1,300 MW power generator), which is far exceeding other kind of industries, such as utilities, ferrosilicon industry, or public services which consume less than 1,000 GWh per year. In Indonesia’s experience, aluminium smelter like PT Indonesia Asahan Aluminium (PT Inalum) of North Sumatera needs huge amount of electricity in its daily operation. In the case of PT Inalum, the electricity is supplied by the Asahan-2 Hydro Electric Power Plant.

PT Inalum is an Indonesian based Japanese aluminium smelters, which requires an extensive quantity of electricity in a sustainable manner. Hydropower is an ideal source of energy for this kind of industry because of the relatively low operational cost, for reason that will be discuss in the immediate session.

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

6

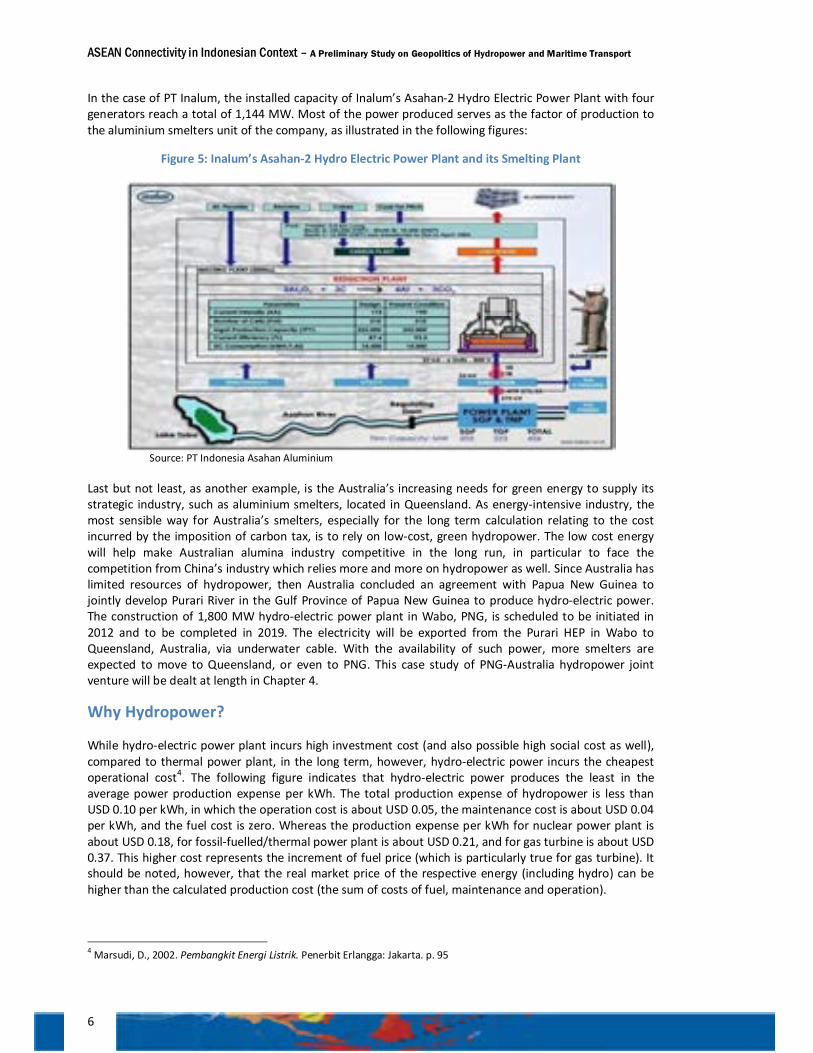

In the case of PT Inalum, the installed capacity of Inalum’s Asahan-2 Hydro Electric Power Plant with four generators reach a total of 1,144 MW. Most of the power produced serves as the factor of production to the aluminium smelters unit of the company, as illustrated in the following figures:

Figure 5: Inalum’s Asahan-2 Hydro Electric Power Plant and its Smelting Plant

Source: PT Indonesia Asahan Aluminium

Last but not least, as another example, is the Australia’s increasing needs for green energy to supply its strategic industry, such as aluminium smelters, located in Queensland. As energy-intensive industry, the most sensible way for Australia’s smelters, especially for the long term calculation relating to the cost incurred by the imposition of carbon tax, is to rely on low-cost, green hydropower. The low cost energy will help make Australian alumina industry competitive in the long run, in particular to face the competition from China’s industry which relies more and more on hydropower as well. Since Australia has limited resources of hydropower, then Australia concluded an agreement with Papua New Guinea to jointly develop Purari River in the Gulf Province of Papua New Guinea to produce hydro-electric power. The construction of 1,800 MW hydro-electric power plant in Wabo, PNG, is scheduled to be initiated in 2012 and to be completed in 2019. The electricity will be exported from the Purari HEP in Wabo to Queensland, Australia, via underwater cable. With the availability of such power, more smelters are expected to move to Queensland, or even to PNG. This case study of PNG-Australia hydropower joint venture will be dealt at length in Chapter 4.

Why Hydropower?

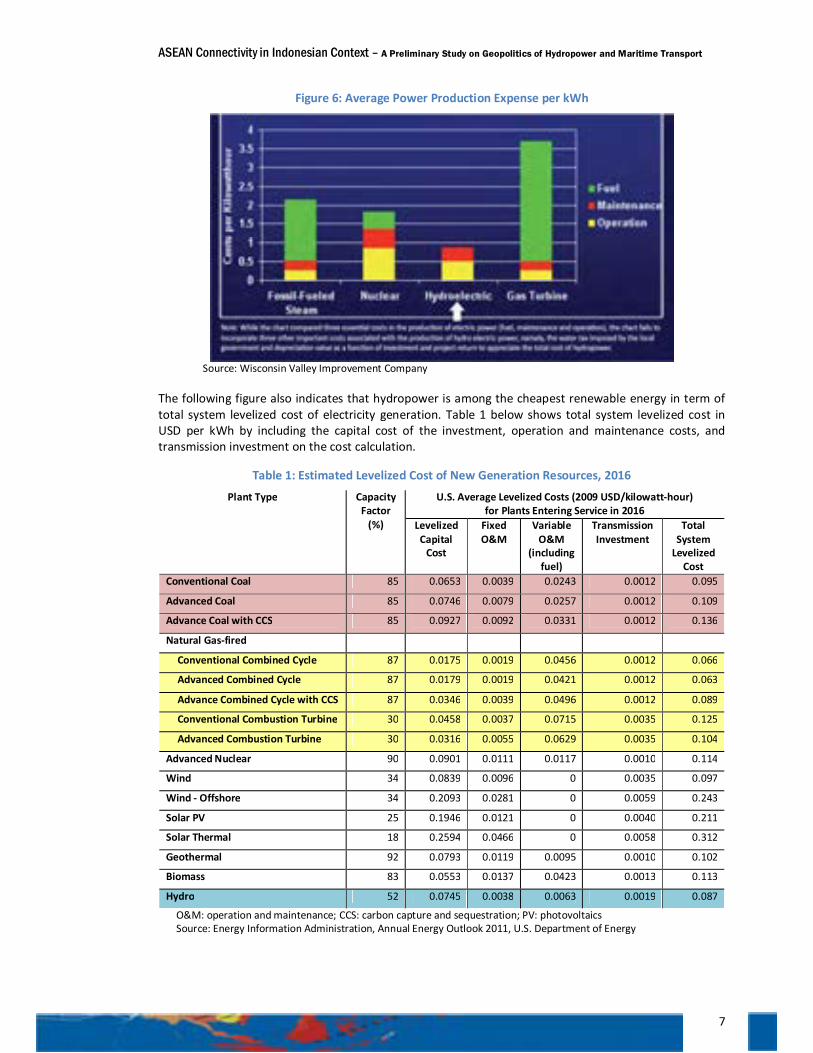

While hydro-electric power plant incurs high investment cost (and also possible high social cost as well), compared to thermal power plant, in the long term, however, hydro-electric power incurs the cheapest operational cost4. The following figure indicates that hydro-electric power produces the least in the average power production expense per kWh. The total production expense of hydropower is less than USD 0.10 per kWh, in which the operation cost is about USD 0.05, the maintenance cost is about USD 0.04 per kWh, and the fuel cost is zero. Whereas the production expense per kWh for nuclear power plant is about USD 0.18, for fossil-fuelled/thermal power plant is about USD 0.21, and for gas turbine is about USD 0.37. This higher cost represents the increment of fuel price (which is particularly true for gas turbine). It should be noted, however, that the real market price of the respective energy (including hydro) can be higher than the calculated production cost (the sum of costs of fuel, maintenance and operation).

4 Marsudi, D., 2002. Pembangkit Energi Listrik. Penerbit Erlangga: Jakarta. p. 95

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

7

Figure 6: Average Power Production Expense per kWh

Source: Wisconsin Valley Improvement Company

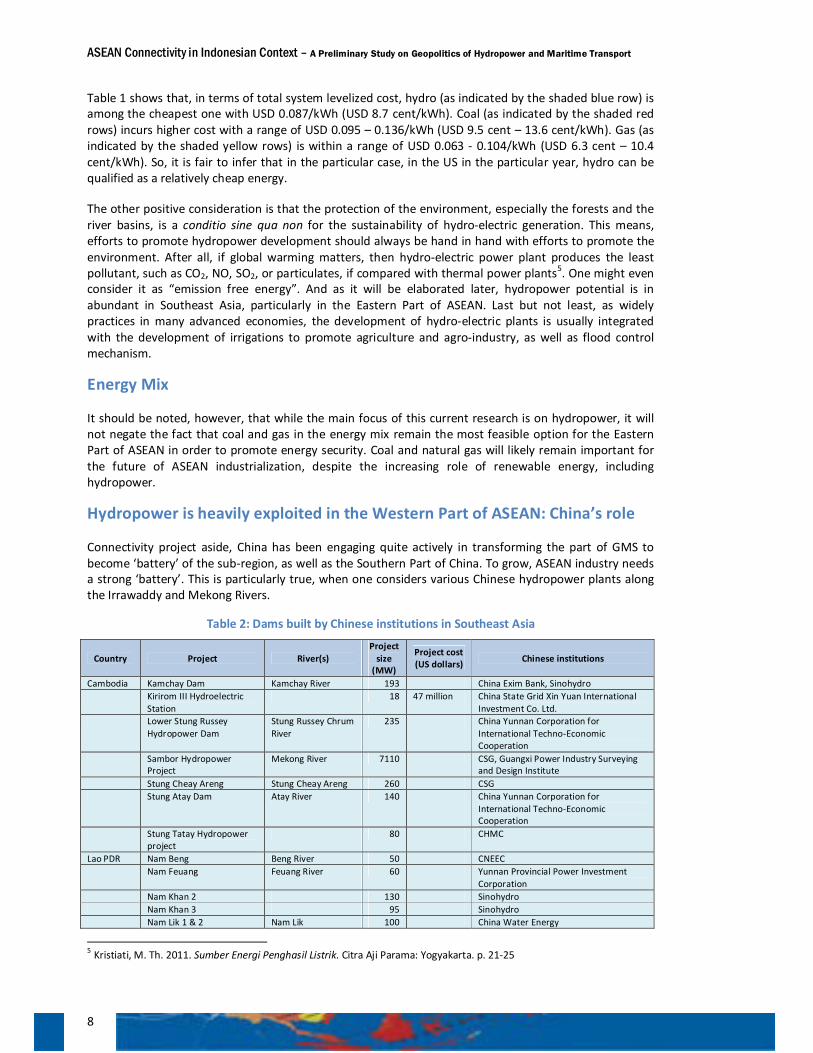

The following figure also indicates that hydropower is among the cheapest renewable energy in term of total system levelized cost of electricity generation. Table 1 below shows total system levelized cost in USD per kWh by including the capital cost of the investment, operation and maintenance costs, and transmission investment on the cost calculation.

Table 1: Estimated Levelized Cost of New Generation Resources, 2016

Plant Type Capacity Factor

(%)

U.S. Average Levelized Costs (2009 USD/kilowatt-hour) for Plants Entering Service in 2016

Levelized Capital

Cost

Fixed O&M

Variable O&M

(including fuel)

Transmission Investment

Total System

Levelized Cost

Conventional Coal 85 0.0653 0.0039 0.0243 0.0012 0.095

Advanced Coal 85 0.0746 0.0079 0.0257 0.0012 0.109

Advance Coal with CCS 85 0.0927 0.0092 0.0331 0.0012 0.136

Natural Gas-fired

Conventional Combined Cycle 87 0.0175 0.0019 0.0456 0.0012 0.066

Advanced Combined Cycle 87 0.0179 0.0019 0.0421 0.0012 0.063

Advance Combined Cycle with CCS 87 0.0346 0.0039 0.0496 0.0012 0.089

Conventional Combustion Turbine 30 0.0458 0.0037 0.0715 0.0035 0.125

Advanced Combustion Turbine 30 0.0316 0.0055 0.0629 0.0035 0.104

Advanced Nuclear 90 0.0901 0.0111 0.0117 0.0010 0.114

Wind 34 0.0839 0.0096 0 0.0035 0.097

Wind - Offshore 34 0.2093 0.0281 0 0.0059 0.243

Solar PV 25 0.1946 0.0121 0 0.0040 0.211

Solar Thermal 18 0.2594 0.0466 0 0.0058 0.312

Geothermal 92 0.0793 0.0119 0.0095 0.0010 0.102

Biomass 83 0.0553 0.0137 0.0423 0.0013 0.113

Hydro 52 0.0745 0.0038 0.0063 0.0019 0.087

O&M: operation and maintenance; CCS: carbon capture and sequestration; PV: photovoltaics Source: Energy Information Administration, Annual Energy Outlook 2011, U.S. Department of Energy

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

8

Table 1 shows that, in terms of total system levelized cost, hydro (as indicated by the shaded blue row) is among the cheapest one with USD 0.087/kWh (USD 8.7 cent/kWh). Coal (as indicated by the shaded red rows) incurs higher cost with a range of USD 0.095 – 0.136/kWh (USD 9.5 cent – 13.6 cent/kWh). Gas (as indicated by the shaded yellow rows) is within a range of USD 0.063 - 0.104/kWh (USD 6.3 cent – 10.4 cent/kWh). So, it is fair to infer that in the particular case, in the US in the particular year, hydro can be qualified as a relatively cheap energy.

The other positive consideration is that the protection of the environment, especially the forests and the river basins, is a conditio sine qua non for the sustainability of hydro-electric generation. This means, efforts to promote hydropower development should always be hand in hand with efforts to promote the environment. After all, if global warming matters, then hydro-electric power plant produces the least pollutant, such as CO2, NO, SO2, or particulates, if compared with thermal power plants5. One might even consider it as “emission free energy”. And as it will be elaborated later, hydropower potential is in abundant in Southeast Asia, particularly in the Eastern Part of ASEAN. Last but not least, as widely practices in many advanced economies, the development of hydro-electric plants is usually integrated with the development of irrigations to promote agriculture and agro-industry, as well as flood control mechanism.

Energy Mix

It should be noted, however, that while the main focus of this current research is on hydropower, it will not negate the fact that coal and gas in the energy mix remain the most feasible option for the Eastern Part of ASEAN in order to promote energy security. Coal and natural gas will likely remain important for the future of ASEAN industrialization, despite the increasing role of renewable energy, including hydropower.

Hydropower is heavily exploited in the Western Part of ASEAN: China’s role

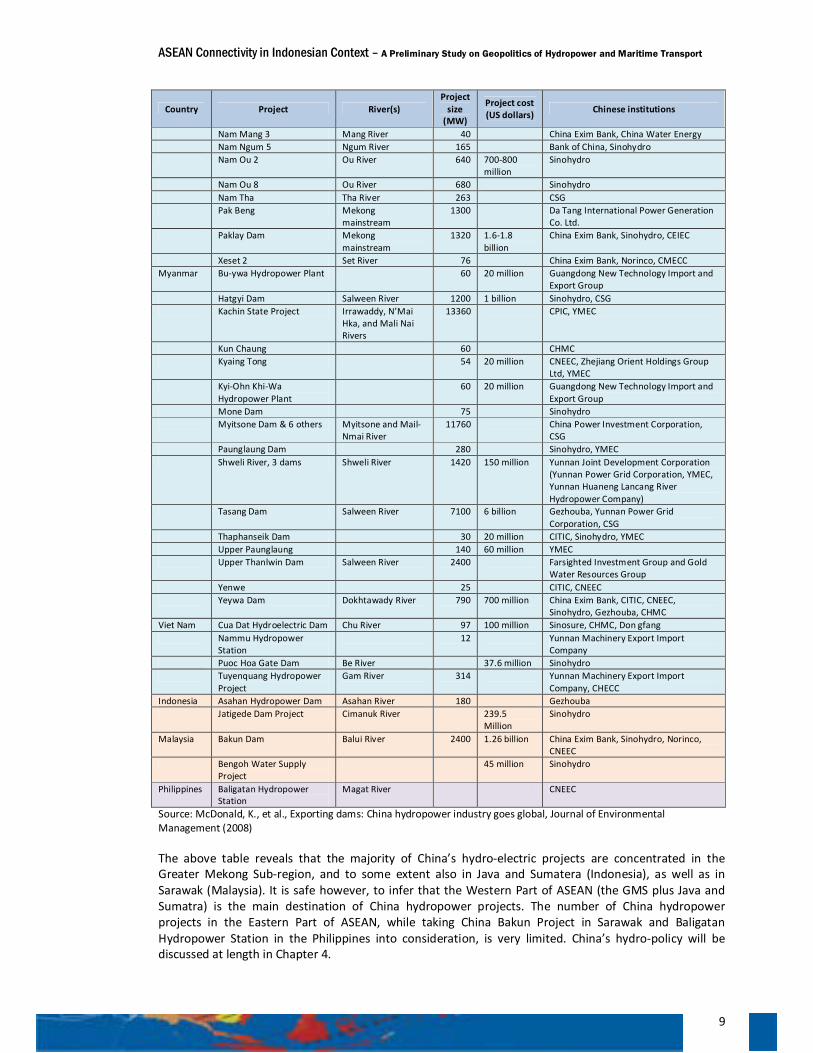

Connectivity project aside, China has been engaging quite actively in transforming the part of GMS to become ‘battery’ of the sub-region, as well as the Southern Part of China. To grow, ASEAN industry needs a strong ‘battery’. This is particularly true, when one considers various Chinese hydropower plants along the Irrawaddy and Mekong Rivers.

Table 2: Dams built by Chinese institutions in Southeast Asia

Country Project River(s) Project

size (MW)

Project cost (US dollars) Chinese institutions

Cambodia Kamchay Dam Kamchay River 193 China Exim Bank, Sinohydro Kirirom III Hydroelectric

Station 18 47 million China State Grid Xin Yuan International

Investment Co. Ltd. Lower Stung Russey

Hydropower Dam Stung Russey Chrum River

235 China Yunnan Corporation for International Techno-Economic Cooperation

Sambor Hydropower Project

Mekong River 7110 CSG, Guangxi Power Industry Surveying and Design Institute

Stung Cheay Areng Stung Cheay Areng 260 CSG Stung Atay Dam Atay River 140 China Yunnan Corporation for

International Techno-Economic Cooperation

Stung Tatay Hydropower project

80 CHMC

Lao PDR Nam Beng Beng River 50 CNEEC Nam Feuang Feuang River 60 Yunnan Provincial Power Investment

Corporation Nam Khan 2 130 Sinohydro Nam Khan 3 95 Sinohydro Nam Lik 1 & 2 Nam Lik 100 China Water Energy

5 Kristiati, M. Th. 2011. Sumber Energi Penghasil Listrik. Citra Aji Parama: Yogyakarta. p. 21-25

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

9

Country Project River(s) Project

size (MW)

Project cost (US dollars) Chinese institutions

Nam Mang 3 Mang River 40 China Exim Bank, China Water Energy Nam Ngum 5 Ngum River 165 Bank of China, Sinohydro Nam Ou 2 Ou River 640 700-800

million Sinohydro

Nam Ou 8 Ou River 680 Sinohydro Nam Tha Tha River 263 CSG Pak Beng Mekong

mainstream 1300 Da Tang International Power Generation

Co. Ltd. Paklay Dam Mekong

mainstream 1320 1.6-1.8

billion China Exim Bank, Sinohydro, CEIEC

Xeset 2 Set River 76 China Exim Bank, Norinco, CMECC Myanmar Bu-ywa Hydropower Plant 60 20 million Guangdong New Technology Import and

Export Group Hatgyi Dam Salween River 1200 1 billion Sinohydro, CSG Kachin State Project Irrawaddy, N’Mai

Hka, and Mali Nai Rivers

13360 CPIC, YMEC

Kun Chaung 60 CHMC Kyaing Tong 54 20 million CNEEC, Zhejiang Orient Holdings Group

Ltd, YMEC Kyi-Ohn Khi-Wa

Hydropower Plant 60 20 million Guangdong New Technology Import and

Export Group Mone Dam 75 Sinohydro Myitsone Dam & 6 others Myitsone and Mail-

Nmai River 11760 China Power Investment Corporation,

CSG Paunglaung Dam 280 Sinohydro, YMEC Shweli River, 3 dams Shweli River 1420 150 million Yunnan Joint Development Corporation

(Yunnan Power Grid Corporation, YMEC, Yunnan Huaneng Lancang River Hydropower Company)

Tasang Dam Salween River 7100 6 billion Gezhouba, Yunnan Power Grid Corporation, CSG

Thaphanseik Dam 30 20 million CITIC, Sinohydro, YMEC Upper Paunglaung 140 60 million YMEC Upper Thanlwin Dam Salween River 2400 Farsighted Investment Group and Gold

Water Resources Group Yenwe 25 CITIC, CNEEC Yeywa Dam Dokhtawady River 790 700 million China Exim Bank, CITIC, CNEEC,

Sinohydro, Gezhouba, CHMC Viet Nam Cua Dat Hydroelectric Dam Chu River 97 100 million Sinosure, CHMC, Don gfang Nammu Hydropower

Station 12 Yunnan Machinery Export Import

Company Puoc Hoa Gate Dam Be River 37.6 million Sinohydro Tuyenquang Hydropower

Project Gam River 314 Yunnan Machinery Export Import

Company, CHECC Indonesia Asahan Hydropower Dam Asahan River 180 Gezhouba Jatigede Dam Project Cimanuk River 239.5

Million Sinohydro

Malaysia Bakun Dam Balui River 2400 1.26 billion China Exim Bank, Sinohydro, Norinco, CNEEC

Bengoh Water Supply Project

45 million Sinohydro

Philippines Baligatan Hydropower Station

Magat River CNEEC

Source: McDonald, K., et al., Exporting dams: China hydropower industry goes global, Journal of Environmental Management (2008)

The above table reveals that the majority of China’s hydro-electric projects are concentrated in the Greater Mekong Sub-region, and to some extent also in Java and Sumatera (Indonesia), as well as in Sarawak (Malaysia). It is safe however, to infer that the Western Part of ASEAN (the GMS plus Java and Sumatra) is the main destination of China hydropower projects. The number of China hydropower projects in the Eastern Part of ASEAN, while taking China Bakun Project in Sarawak and Baligatan Hydropower Station in the Philippines into consideration, is very limited. China’s hydro-policy will be discussed at length in Chapter 4.

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

10

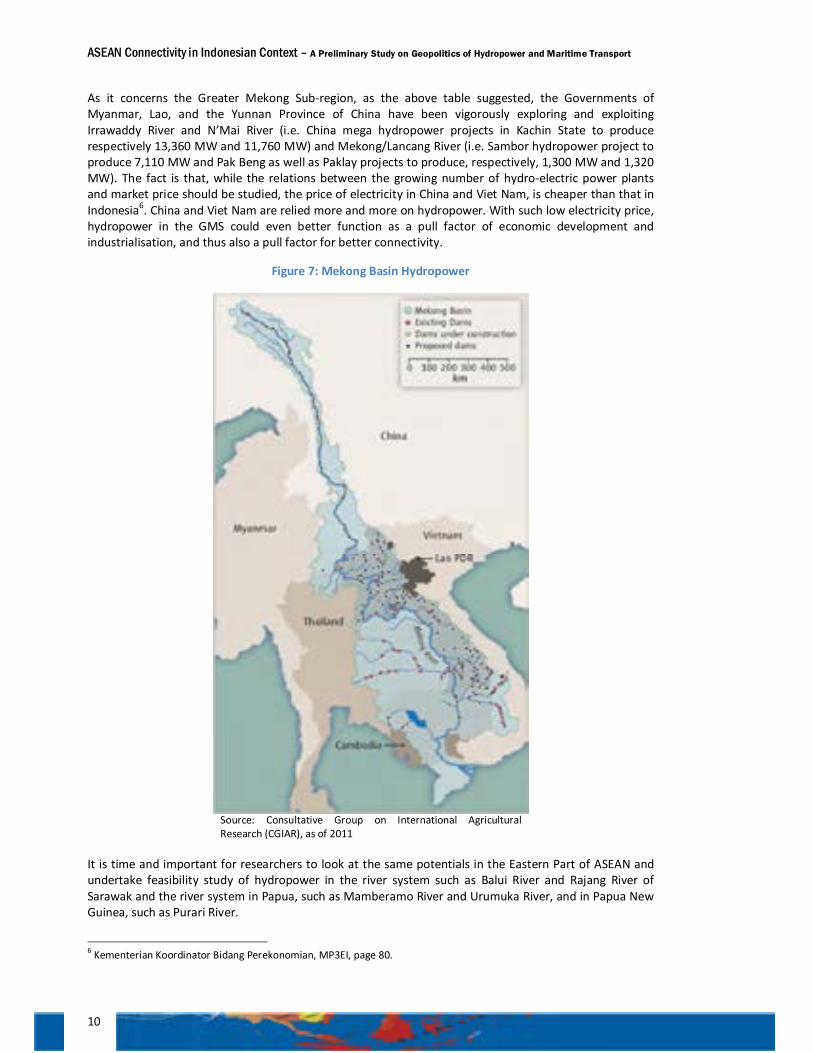

As it concerns the Greater Mekong Sub-region, as the above table suggested, the Governments of Myanmar, Lao, and the Yunnan Province of China have been vigorously exploring and exploiting Irrawaddy River and N’Mai River (i.e. China mega hydropower projects in Kachin State to produce respectively 13,360 MW and 11,760 MW) and Mekong/Lancang River (i.e. Sambor hydropower project to produce 7,110 MW and Pak Beng as well as Paklay projects to produce, respectively, 1,300 MW and 1,320 MW). The fact is that, while the relations between the growing number of hydro-electric power plants and market price should be studied, the price of electricity in China and Viet Nam, is cheaper than that in Indonesia6. China and Viet Nam are relied more and more on hydropower. With such low electricity price, hydropower in the GMS could even better function as a pull factor of economic development and industrialisation, and thus also a pull factor for better connectivity.

Figure 7: Mekong Basin Hydropower

Source: Consultative Group on International Agricultural Research (CGIAR), as of 2011

It is time and important for researchers to look at the same potentials in the Eastern Part of ASEAN and undertake feasibility study of hydropower in the river system such as Balui River and Rajang River of Sarawak and the river system in Papua, such as Mamberamo River and Urumuka River, and in Papua New Guinea, such as Purari River.

6 Kementerian Koordinator Bidang Perekonomian, MP3EI, page 80.

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

11

Hydropower as a Pull Factor: Ecological approach needed

Learning from the experience of China and the GMS countries, the nagging issue is how the development of hydropower will not be prejudicial to the environment, and hence, the interest of sustainable development. As is noted, hydropower development along the Lancang/Mekong River has created disputes between countries in the upper stream and countries in the lower stream. The development of Lao’s hydropower project in Xayaboury Province, in the lower Mekong River which has been disputed between Lao in the one side, and Viet Nam, Cambodia, and Thailand in the other side, is the case in point7. Such dispute is less likely to happen in Myanmar, since most of the main river system is within the territory of Myanmar. Yet, disputes might not be avoidable within Myanmar, and particular between government and the environmentalist NGOs, against the backdrop of Myanmar new political environment.

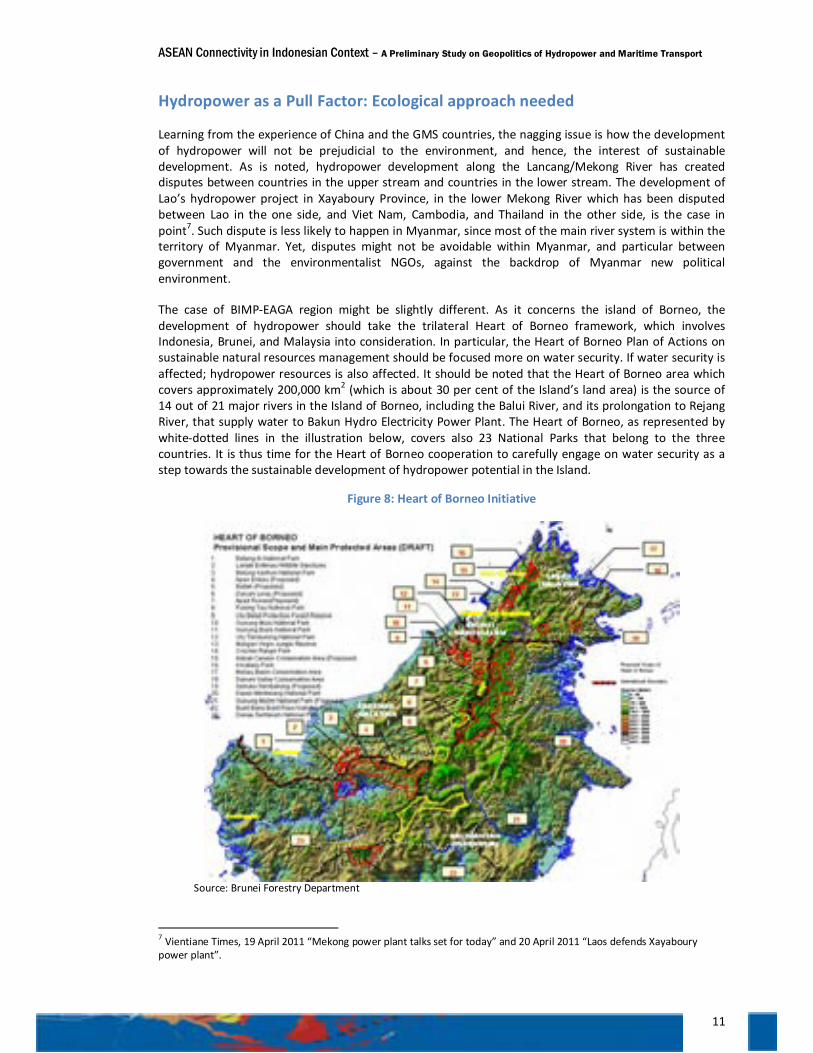

The case of BIMP-EAGA region might be slightly different. As it concerns the island of Borneo, the development of hydropower should take the trilateral Heart of Borneo framework, which involves Indonesia, Brunei, and Malaysia into consideration. In particular, the Heart of Borneo Plan of Actions on sustainable natural resources management should be focused more on water security. If water security is affected; hydropower resources is also affected. It should be noted that the Heart of Borneo area which covers approximately 200,000 km2 (which is about 30 per cent of the Island’s land area) is the source of 14 out of 21 major rivers in the Island of Borneo, including the Balui River, and its prolongation to Rejang River, that supply water to Bakun Hydro Electricity Power Plant. The Heart of Borneo, as represented by white-dotted lines in the illustration below, covers also 23 National Parks that belong to the three countries. It is thus time for the Heart of Borneo cooperation to carefully engage on water security as a step towards the sustainable development of hydropower potential in the Island.

Figure 8: Heart of Borneo Initiative

Source: Brunei Forestry Department

7 Vientiane Times, 19 April 2011 “Mekong power plant talks set for today” and 20 April 2011 “Laos defends Xayaboury power plant”.

ASEAN Connectivity in Indonesian Context – A Preliminary Study on Geopolitics of Hydropower and Maritime Transport

12

The case of Bakun is a testimony of how hydropower has been used as a pull factor of industrialisation. With the operation of Bakun by the end of 2011, Sarawak managed to conclude agreements or MoUs with international energy intensive industries. The example includes the plan of the Australian’s Rio Tinto to conclude a joint venture with Cahya Mata Sarawak in building a USD 2 billion aluminium smelter in Sarawak; a Chinese main power grid operator is planning to invest USD 8 billion in an aluminium smelter. Many companies such as Australian’s manganese produces OMH Holdings, chemical maker Tokuyama Corporation and China’s aluminium group Chinalco will follow suit8. It is estimated that the industrialisation of Sarawak will open a new opportunity for 1.6 million new jobs in Sarawak9.

Likewise, Papua, which has prepared a plan to develop hydropower in Mamberamo River and Bongrang Industrial Estate, should, through the national investment board (BKPM), be able to strike a preliminary deal with partner countries to relocate some of their energy intensive industry to Papua. With such a deal, the market for the Mamberamo Hydro Electric Power would be secured.

The development of hydropower potential in the island of New Guinea, which consists of the Indonesian Provinces of Western Papua and Papua, and the State of Papua New Guinea, should take the principle of single island ecosystem approach into consideration.

Hydropower Potential in ASEAN