asaf cohen department of mathematics university of michigan financial mathematics seminar university...

TRANSCRIPT

PARAMETER ESTIMATION: THE PROPER WAY TO USE BAYESIAN

POSTERIOR PROCESSES WITH BROWNIAN NOISE

Asaf CohenDepartment of Mathematics

University of Michigan

Financial Mathematics SeminarUniversity of Michigan

September 10, 2014

1

Contents

Motivation: Brownian Motion with Unknown Drift

Introduction: Bayesian Parameter Estimation, Examples

Current & Future Work

Scaled Renewal Processes Brownian Motion (with unknown drift)

The Posterior Processes and their Limits

2

Contents

Motivation: Brownian Motion with Unknown Drift

Introduction: Bayesian Parameter Estimation, Examples

Current & Future Work

The Posterior Processes and their Limits

2

Scaled Renewal Processes Brownian Motion (with unknown drift)

A DM (Decision Maker) wants to estimate a parameter . His i.i.d. (given ) observations are

Introduction: Bayesian Parameter Estimation, Examples

Bayesian Parameter Estimation

• has a prior distribution

• The DM chooses an estimator that minimizes the expected loss function

Bayesian

• A fundamental tool is the posterior distribution

Parameter Estimation

3

e.g.,

Sampling is stopped accordance with a stopping rule

• The sample size is not fixed in advance .

4

Introduction: Bayesian Parameter Estimation, Examples

Bayesian Sequential Parameter Estimation

• A fundamental tool is the posterior process

• The DM chooses an estimator that minimizes the expected loss function

• has a prior distribution

Bayesian Parameter EstimationSequential

e.g.,

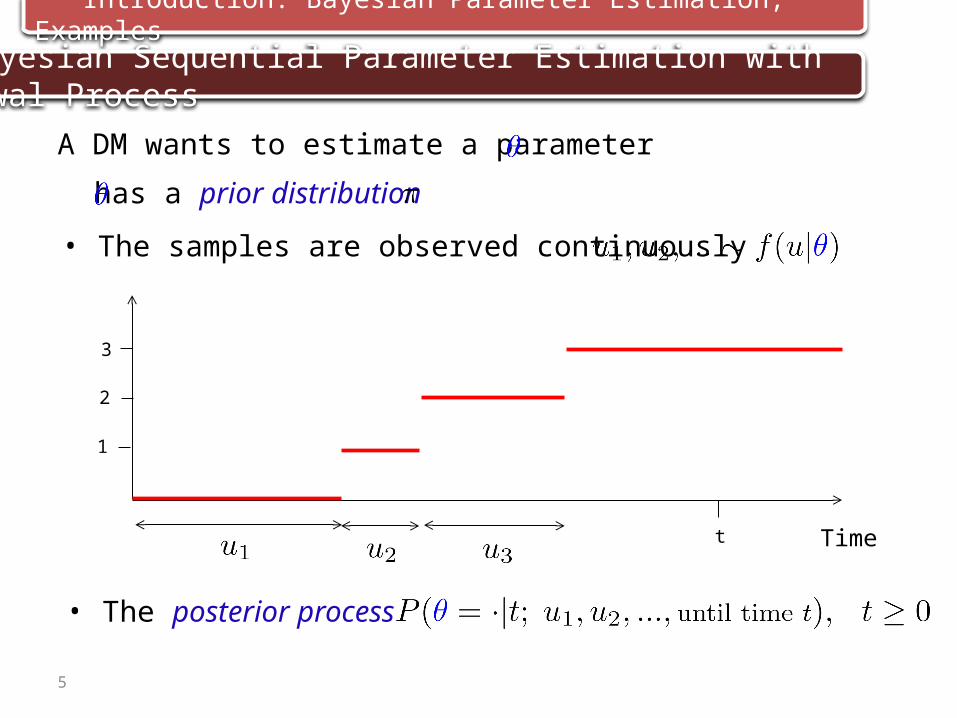

A DM wants to estimate a parameter

• The samples are observed continuously

5

Introduction: Bayesian Parameter Estimation, Examples

Bayesian Sequential Parameter Estimation with Renewal Process

• has a prior distribution

t

2

3

Time

1

• The posterior process

A DM wants to estimate a parameter

• The DM continuously observes

6

Introduction: Bayesian Parameter Estimation, Examples

Bayesian Sequential Parameter Estimation with Brownian Noise

• has a prior distribution

• The posterior process

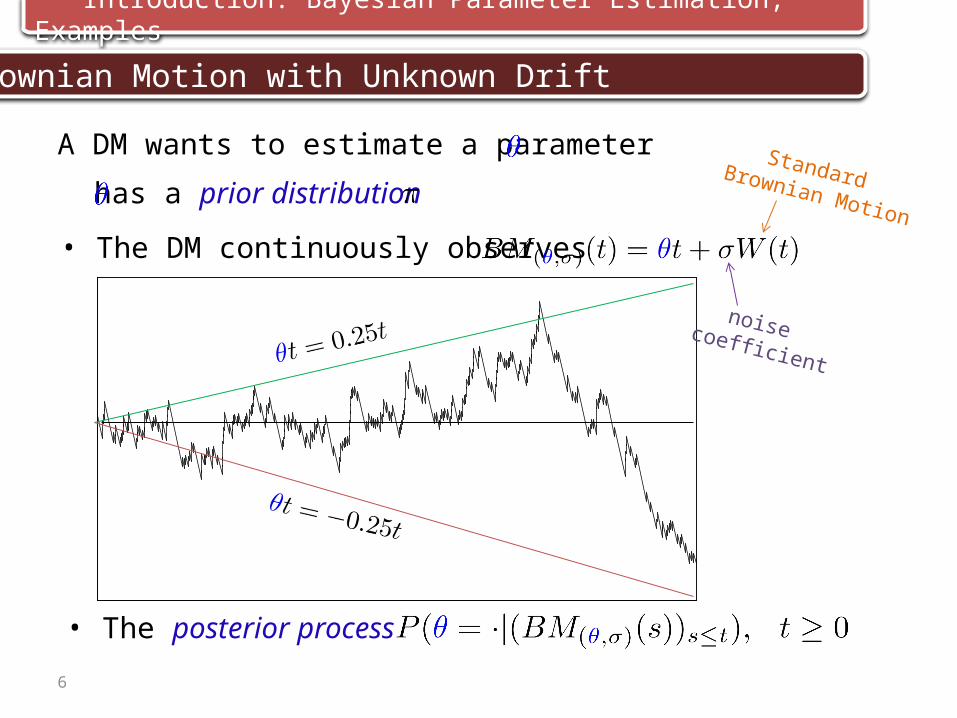

A DM wants to estimate a parameter Standard Brownian Motion

noise coefficient

• The DM continuously observes

6

Introduction: Bayesian Parameter Estimation, Examples

Brownian Motion with Unknown Drift

• has a prior distribution

• The posterior process

A DM wants to estimate a parameter Standard Brownian Motion

noise coefficient

Contents

Motivation: Brownian Motion with Unknown Drift

Introduction: Bayesian Parameter Estimation, Examples

Current & Future Work

The Posterior Processes and their Limits

7

Scaled Renewal Processes Brownian Motion (with unknown drift)

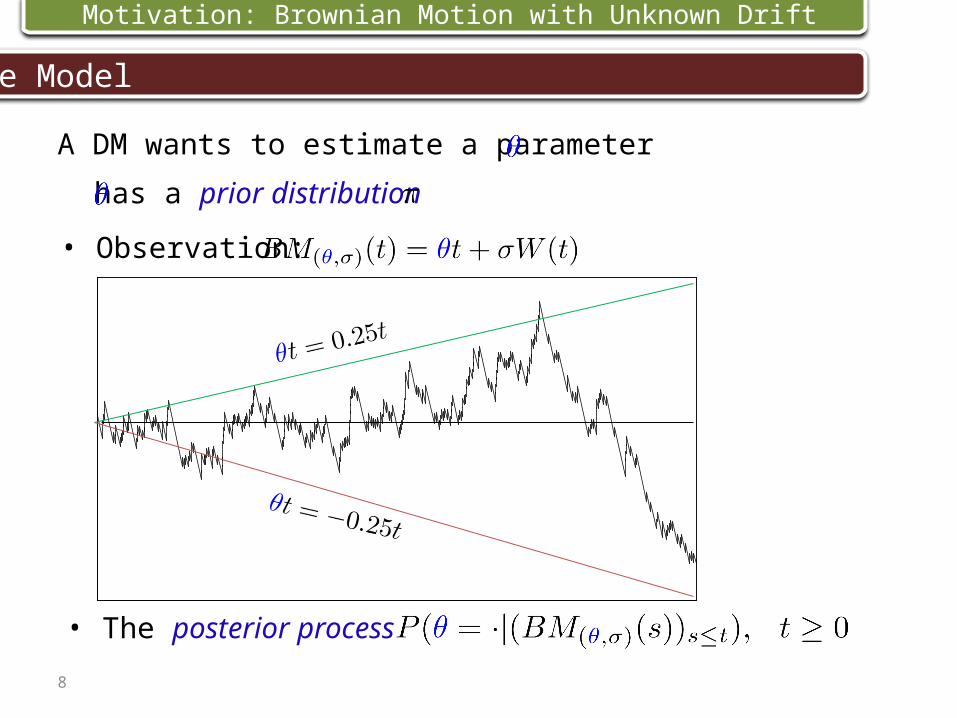

• Observation:

8

The Model

• has a prior distribution

• The posterior process

A DM wants to estimate a parameter

Motivation: Brownian Motion with Unknown Drift

9

Motivation: Brownian Motion with Unknown Drift

The Model

• has a prior distribution

e.g.,

• A common solution: A First Exit Time of

A First Exit Time of the posterior process

A DM wants to estimate a parameter .

• Observation:

10

Literature

Motivation: Brownian Motion with Unknown Drift

• Kalman and Bucy (1961)• Zakai (1969) - Bayesian Posterior Process

Filtering Theory

• Shiryaev (1978) - formulated the problem (discrete and continuous time)• Gapeev and Peskir (2004) - Finite Horizon• Gapeev and Shiryaev (2011) - General Diffusion• Zhitlukhin and Shiryaev (2011) - Three hypotheses• Buonaguidi and Muliere (2013) - Levy Processes

Sequential 2-Hypothesis Testing

• Berry and Friestedt (1985) - formulated the problem• C. and Solan (2013) - Levy Processes

Bayesian Brownian Bandit

EconomicsBolton and Harris (1999), Felli and Harris (1996), Bergemann and Valimaki (1997), Keller and Rady (1999), Moscarini (2005) , Jovanovic (1979)...

11

Motivation: Brownian Motion with Unknown Drift

11

Motivation: Brownian Motion with Unknown Drift

12

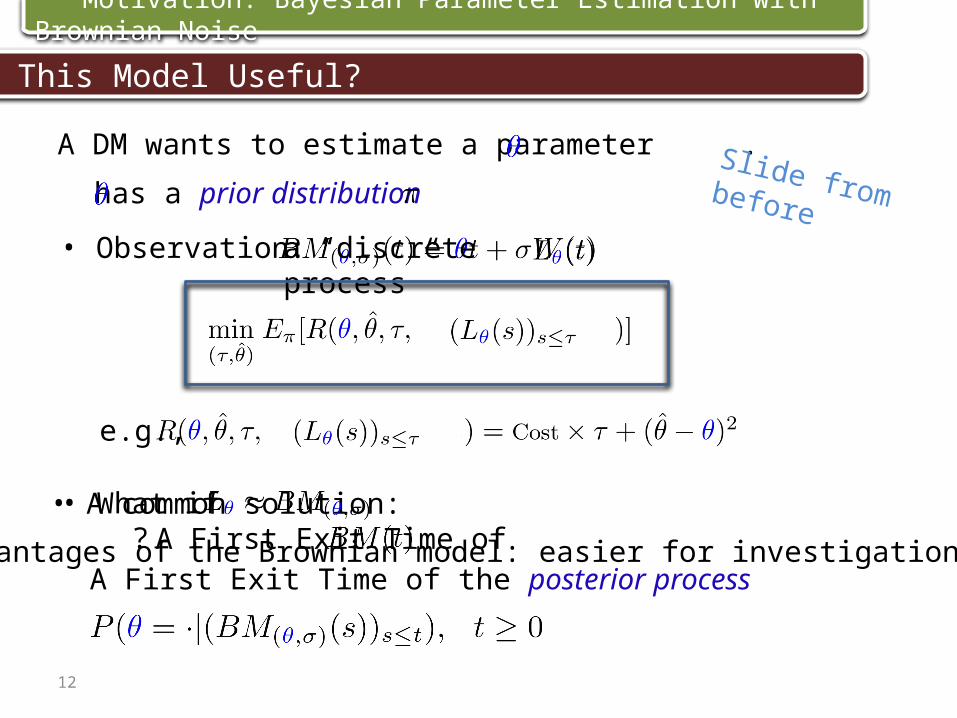

Is This Model Useful?

• has a prior distribution

e.g.,

• A common solution: A First Exit Time of

• Observation:

A First Exit Time of the posterior process

A DM wants to estimate a parameter .

a “discrete process”

• What if ?

• Advantages of the Brownian model: easier for investigation

Motivation: Bayesian Parameter Estimation with Brownian Noise

Slide from before

13

Is This Model Useful?

Motivation: Bayesian Parameter Estimation with Brownian Noise

• Kalman and Bucy (1961)• Zakai (1969) - Bayesian Posterior Process

Filtering Theory

• Shiryaev (1978) - formulated the problem (discrete and continuous time)• Gapeev and Peskir (2004) - Finite Horizon• Gapeev and Shiryaev (2011) - General Diffusion• Zhitlukhin and Shiryaev (2011) - Three hypotheses• Buonaguidi and Muliere (2013) - Levy Processes

Sequential 2-Hypothesis Testing

• Berry and Friestedt (1985) - formulated the problem• C. and Solan (2013) - Levy Processes

Bayesian Brownian Bandit

EconomicsBolton and Harris (1999), Felli and Harris (1996), Bergemann and Valimaki (1997), Keller and Rady (1999), Moscarini (2005) , Jovanovic (1979)...No Justification

Slide from before

14

Is This Model Useful?

Suppose that

1. For a given rule of strategy does the losses satisfy

2. Are the optimal rules of strategies for the observed processes and relatively close?

3. Are the optimal losses relatively close?

Usually not!

Usually not!

Usually not!So… Why to study Bayesian parameter estimation with Brownian noise?

Motivation: Brownian Motion with Unknown Drift

Questions:

14

Is This Model Useful?

Suppose that

1. For a given rule of strategy does the losses satisfy

2. Are the optimal rules of strategies for the observed processes and relatively close?

3. Are the optimal losses relatively close?

Usually not!

Usually not!

Usually not!So… Why to study Bayesian parameter estimation with Brownian noise?

Motivation: Brownian Motion with Unknown Drift

Questions:

Weird phenomena: a different approximation works….

How to calculate?Fundamental tool: posterior processes

Why different?

Contents

Motivation: Brownian Motion with Unknown Drift

Introduction: Bayesian Parameter Estimation, Examples

Current & Future Work

The Posterior Processes and their Limits

15

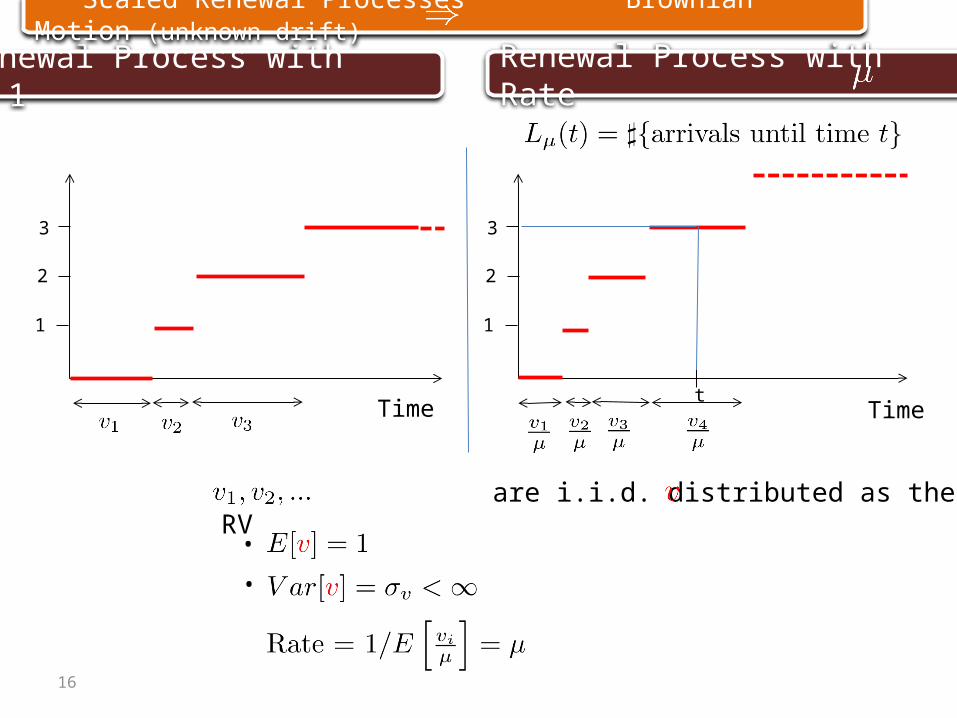

Scaled Renewal Processes Brownian Motion (with unknown drift)

are i.i.d. distributed as the RV

16

Renewal Process with Rate 1

Scaled Renewal Processes Brownian Motion (unknown drift)

2

3

Time

1

•

•

Renewal Process with Rate

2

3

1

tTime

17

High Rate

Take . How behaves?

By proper scaling:Similar to Brownian Motion

FCLT

Scaled Renewal Processes Brownian Motion (unknown drift)

18

High and Unknown Rate - The Proper Scaling

Assumption

• is chosen at time

• The DM continuously observes

FCLT

Why ?

Scaled Renewal Processes Brownian Motion (unknown drift)

Contents

Motivation: Brownian Motion with Unknown Drift

Introduction: Bayesian Parameter Estimation, Examples

Current & Future Work

The Posterior Processes and their Limits

19

Scaled Renewal Processes Brownian Motion (with unknown drift)

20

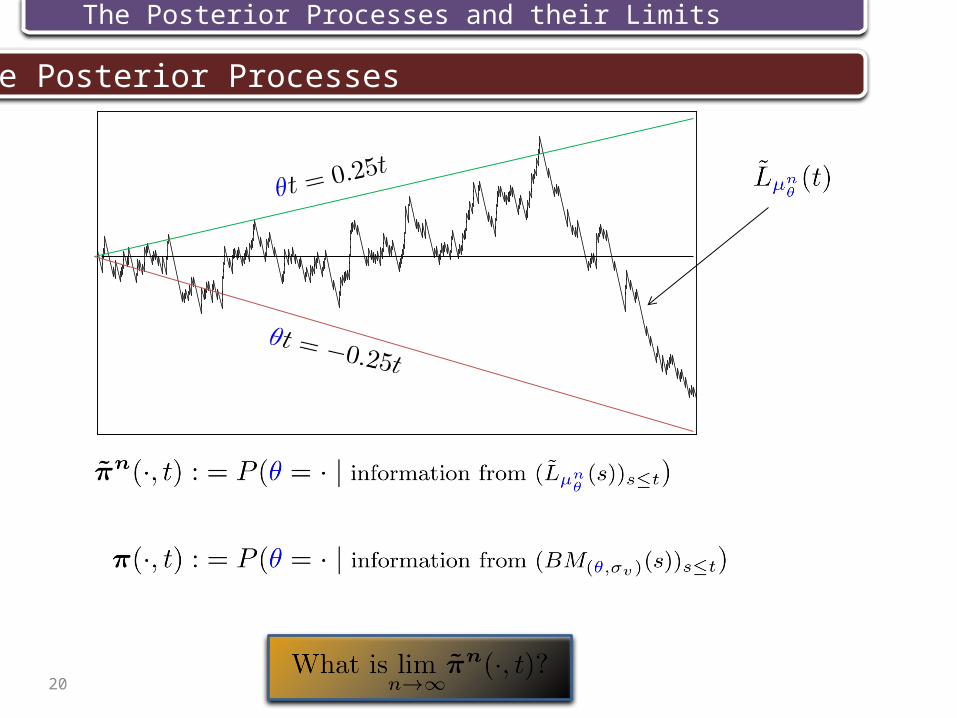

The Posterior Processes and their Limits

The Posterior Processes

21

The Posterior Processes and their Limits

Diffusion Limits

Assumption

has a density with the support

2

3

Time

1 •

•

•

22

The Posterior Processes and their Limits

Diffusion Limits

Assumption

has a density with the support

Theorem 1

Why ?

23

The Posterior Processes and their Limits

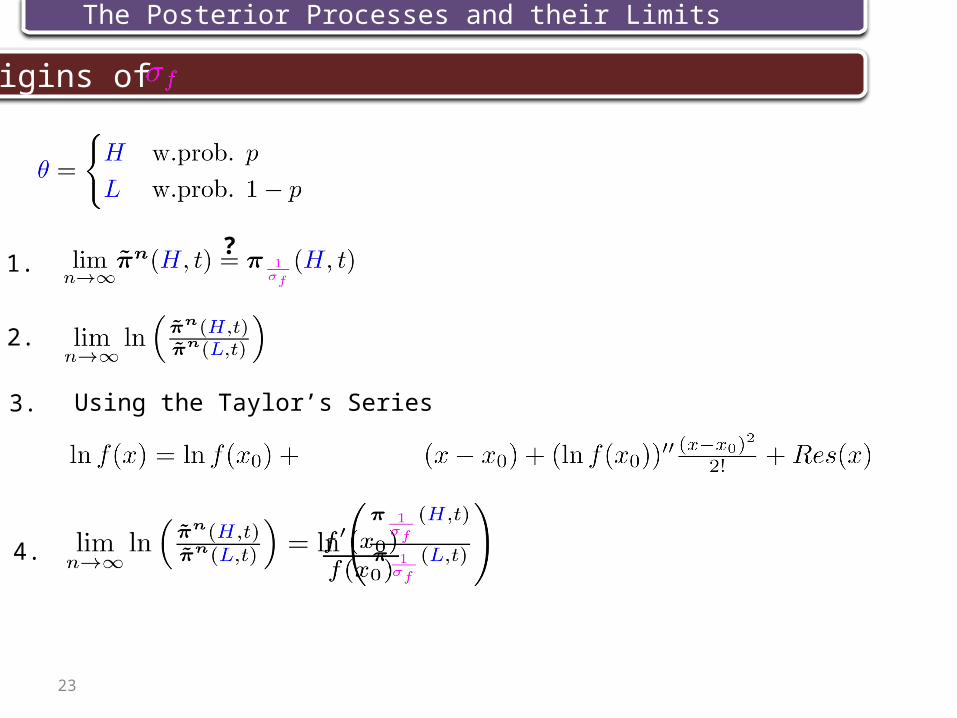

1.

2.

?

Using the Taylor’s Series3.

4.

Origins of

24

The Posterior Processes and their Limits

Heuristics for

Why ?

Recall that

The smaller : “easier” to estimate larger

When is a “large” R.V.?

• The interarrival time

for the discussion, or

The Posterior Processes and their Limits

Why ?

recall that

the smaller : “easier” to estimate larger

When is a “large” R.V.?

• The interarrival time

for the discussion, or

“easier” to estimate ? ?

x25

Heuristics for

26

The Posterior Processes and their Limits

The New

Theorem 2

, and equality holds iff .

What is the relation between and ?

In fact can be arbitrary large

So, can be very different from

27

The Posterior Processes and their Limits

Intuition (Theorem 2)

• is a sufficient statistic for :

• Usually is not a sufficient statistic for :

• However, if , it is sufficient!

and since, then .

28

The Posterior Processes and their Limits

Proof (Theorem 2)

Cauchy–Schwarz

Equality iff and are linearly dependent

iff

29

The Posterior Processes and their Limits

Back to the Motivation

Theorem 3

Since can be arbitrary large

can be very different from

Contents

Motivation: Brownian Motion with Unknown Drift

Introduction: Bayesian Parameter Estimation, Examples

The Posterior Processes and their Limits

Current & Future Work

30

Scaled Renewal Processes Brownian Motion (with unknown drift)

2. - replace FCLT with stable FCLT.

31

Current & Future Work

A) Behavior of posteriors in more general frameworks:

B) The Disorder Problem

1. General diffusions (e.g., Zakai Equation type).

Assume that at some unobservable random time the drift of a Brownian motion (rate of an arrival process) changes.

similar structure.Find the posterior belief that the change has already occurred?

32

Current & Future Work

C) Apply the results in context of queues with uncertainty about the service/arrival rates, asymptotic solution using Bayesian bandits.

D) Apply the results in context of risk processes.

Arrival processGeneral CDF • customers: Bandit (index solution)

• customers: non-classical Bandit (empty periods)

Asymptotic solution under heavy traffic using BM with unknown driftrouter

THANK YOU!

33