arvind ltd. - think invert cmp target rating rs.277...

TRANSCRIPT

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY

Stock performance (%)

1m 3m 12m

ARVND 2% -6% -3%

Sensex 8% -1% -13%

BSE CONSDIS 6% -4% -2%

Financial summary

Year Revenues (Rs. mn) EBITDA (Rs. mn) PAT (Rs. mn) EPS (Rs.) P/E(x) ROE (%)

FY16E 83,030 10,560 3,546 13.7 20.2 12.4%

FY17E 96,640 12,825 4,701 18.2 15.2 14.8%

FY18E 1,13,654 15,682 6,824 26.4 10.5 18.9%

Date 15th March 2016

Market Data

Bloomberg ARVND IN

Shares o/s 258mn

Market Cap Rs. 72bn

52-wk High-Low Rs. 366-216

3m Avg. Daily Vol Rs. 627mn

Index member BSEMDCAP

Latest shareholding (%)

Promoters 43.8

Institutions 39.7

Public 16.5

Follow-up noteInvert, always invert: Turn a situation or problem upside down. Look at it backward. What happens if all our plans go wrong?

Where don’t we want to go, and how do you get there? Instead of looking for success, make a list of how to fail instead …..

Tell me where I’m going to die, that is, so I don’t go there. – Charlie Munger

Invert thinking is perhaps the most powerful thinking tool available to neutralise the bias(es) that one may have in their approach to

any investment idea(s). This becomes more imperative where the runway for growth appears extremely long and lucrative. We have

been bullish on Arvind Ltd (ARVND) since our initiation (Click here to read our initiation report) and continue to retain our positive bias

solely for the Brands business, the opportunity of which is humungous. Given the robust brands ARVND has in its portfolio, if their set

‘vision’ is executed properly, it would be one of the best stories ever witnessed in the history of Indian apparel sector.

However, we also believe ARVND in its current avatar, is a complex business with too many moving parts. Hence, this note

broadly focuses on the possible ‘blind spots’ to watch out for and ‘positive triggers’ ahead…

Despite realizing the susceptibility of the textile business and diversifying up the value chain into related ‘brands and retail’ (B&R)

business, the B&R segment still accounts for only ~30% of total revenues and ~12% of EBITDA clearly indicating that the story is still

‘work in progress’ and currently in the transition stage.

The success of any brand story playing out depends on three factors viz. Brand, Resource and Execution. Though the management

has a decent execution history, the pace at which the ‘desired’ vision is fulfilled depends a lot on many other factors as well which are

both within and ‘without’ the control of the management. With already 30+ brands in the portfolio and still counting, capital allocation

and execution needs of the long tail of brands need to be balanced with the already established ones.

Hence, in a bumpy ride it is best to ensure that each one’s ‘Achilles heel’ doesn't further the damage, which in ARVND’s case is its

debt. Though debt currently on ARVND’s books is manageable (debt-equity ratio as on date is ~1.2 times), any deterioration of the

same can significantly dent the financial standing of the company.

….ARVND’s portfolio of brands are rightly placed to make the most out of the evolving trends in lifestyle consumption space

Affinity towards the western brands coupled with increased spending by the new age Indian consumer has also enabled several

western brands, across categories, growing at rapid pace off-late. We believe ARVND’s portfolio comprising of several exciting

western brands and ‘western imitable private brands’ should be a key beneficiary of this trend and ARVND would be the best proxy to

play the trend. Massive success of these brands in other ‘emerging economies’ further reaffirms our stance..

We continue to retain our positive stance on ARVND based on the size of the opportunity and ARVND’s portfolio of brands to

capitalise the same. However, appreciating the complexity of the drivers and execution challenges involved, we believe

monitoring financial leverage level will be extremely crucial during the ‘vision’ fulfilling journey as controlled debt can give

the luxury to accommodate the volatility in the macro cycle, gestation in the evolving consumption habits and any

unaccounted disruptions. We retain BUY with a TP of Rs.323 valuing ARVND on SOTP basis (implied PE of ~18x F17E EPS).

Page 1

Tejash Shah

+91 22 4228 8155

Gnanasundaram S

+91 44 4344 0062

Madhav PVR

+91 44 4344 0060

Executive Summary

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY

Page 2

Blind Spots Vs Positive Triggers

Blind Spots Positive Triggers

#1 Too much is too

thin?

#2 Two decade old

Megamart business

remains a ‘rebellious

child’

#3A Continues to be in a capex mode

across verticals …

#3B – …funded by currently steady

state (but vulnerable) cash flows from

Textiles…

#3C…hence leverage remains

to be crucially monitored #4 Increasing proportion of B2C

segment revenues can lead to

valuation re-rating

#3

Investments into new-gen

businesses…. lottery

tickets

#2 Steady state

textile business to

play a supporting

role

#1 Huge non-linearity in

brands business keeps us

exhilarated

***Achilles’ heel***

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY

23.5

37.0

15.5

4.05

15.0

0.05.0

10.015.020.025.030.035.040.0

Arvind B&R MaduraGarments

Page Industries Kewal Kiran RelaxoFootwear

FY15 Revenues (In Rs.Bn)

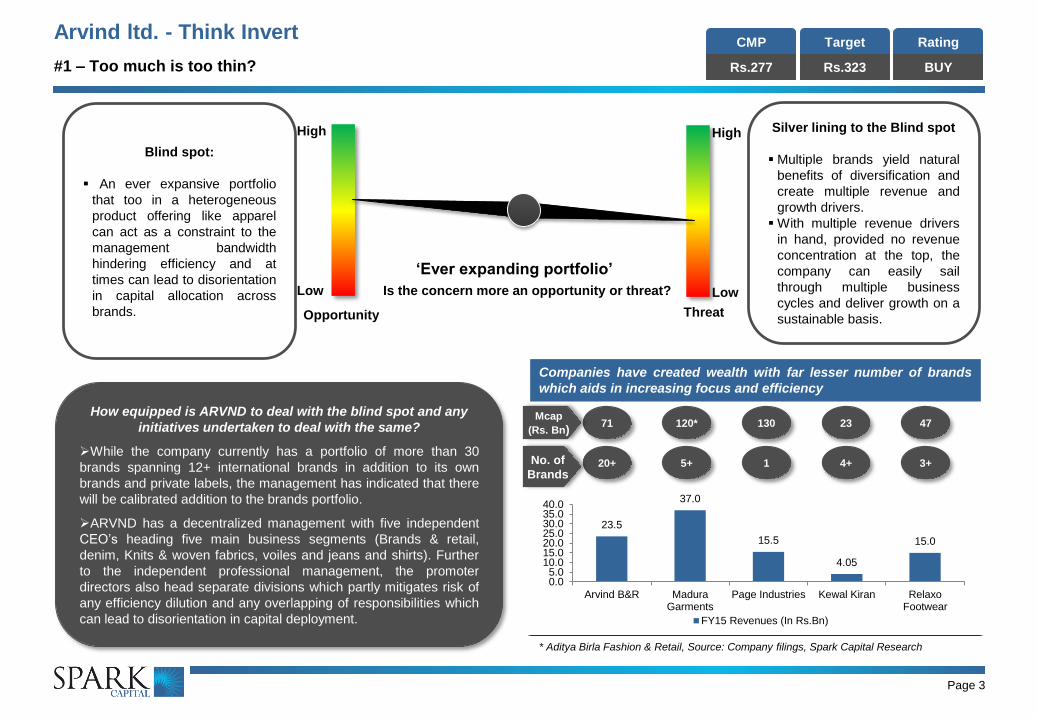

#1 – Too much is too thin?

Page 3

How equipped is ARVND to deal with the blind spot and any

initiatives undertaken to deal with the same?

While the company currently has a portfolio of more than 30

brands spanning 12+ international brands in addition to its own

brands and private labels, the management has indicated that there

will be calibrated addition to the brands portfolio.

ARVND has a decentralized management with five independent

CEO’s heading five main business segments (Brands & retail,

denim, Knits & woven fabrics, voiles and jeans and shirts). Further

to the independent professional management, the promoter

directors also head separate divisions which partly mitigates risk of

any efficiency dilution and any overlapping of responsibilities which

can lead to disorientation in capital deployment.

Silver lining to the Blind spot

Multiple brands yield natural

benefits of diversification and

create multiple revenue and

growth drivers.

With multiple revenue drivers

in hand, provided no revenue

concentration at the top, the

company can easily sail

through multiple business

cycles and deliver growth on a

sustainable basis.Opportunity Threat

Is the concern more an opportunity or threat?

Blind spot:

An ever expansive portfolio

that too in a heterogeneous

product offering like apparel

can act as a constraint to the

management bandwidth

hindering efficiency and at

times can lead to disorientation

in capital allocation across

brands.

Companies have created wealth with far lesser number of brands

which aids in increasing focus and efficiency

* Aditya Birla Fashion & Retail, Source: Company filings, Spark Capital Research

20+ 5+ 1 4+ 3+No. of

Brands

71 120* 130 23 47Mcap

(Rs. Bn)

Low

High

Low

High

‘Ever expanding portfolio’

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#1 – Too much is too thin?

Page 4

1980………………………..1995…………………....2000….....................2005….2008.……………...2010…2013…………..……2016

Own brand

‘True

Blue’

Source: Company filings, Media snippets & Spark Capital Research

Exit brands

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#2 – Two decade old Megamart business remains a ‘rebellious child’

Page 5

How equipped is ARVND to deal with the blind spot and any

initiatives undertaken to deal with the same?

ARVND recently undertook another attempt to turnaround its long

ailing retail chain viz. Megamart. In a short span of ~15 days in the

months of August and September, the company converted around ~35

Megamart stores into their newly branded ‘Unlimited’ stores. We

understand that out of the 176 stores which existed till last year, 55

stores were closed in the current year, 35 stores have been converted

into ‘Unlimited’ stores which are expected to generate ~70% of Sales

and the remaining 50 profitable stores operate in the old format.

We understand that the latest revamp in Megamart might be the last

of the changes. While the management believes the business might

take a year before consolidation happens and healthy growth is

witnessed, we believe further delay in revival might lead to

management seriously considering continuation of the retail chain.

Silver lining to the Blind spot

Understanding that its discount-

apparel format Megamart is not

capital efficient, ARVND has

moved to value fashion retail by

revamping Megamart to

‘Unlimited’.

While majority of ARVND’s

brands are targeted at the upper

middle class and the rich,

Megamart/Unlimited ensures the

company benefits from the

evolving Indian middle class by

playing the conversion game of

‘unorganised to organised’.

Blind spot:

Sustainable business model still

not in place for Megamart even

post two decades of operation.

Further, there has been no ‘proof

of concept’ of a successful

discounted retail model in India.

‘Megamart business’

Opportunity Threat

Is the concern more an opportunity or threat?

Tepid growth in Megamart revenues over the last four years with

profitability nowhere close to desired

Source: Company filings, Spark Capital Research

1.89 2.92 3.97 4.99 5.07 5.49 5.600

1

2

3

4

5

6

FY 09 FY 10 FY 11 FY 12 FY 13 FY 14 FY 15

In R

s.B

n

Megamart Revenues (In Bn)

Further to the fact that a

successful discounted retail chain

is yet to emerge in the country, we

believe Megamart is possibly an

unwanted diversion which drains

both management and financial

bandwidth given its history.

Low

High

Low

High

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#3A – Continues to be in a capex mode across verticals …

Page 6

Though a blind spot is it the right way forward?

“Organisation don’t really have a choice; they must adapt or die,” –

Anonymous.

Though we note the fallacies of ARVND in still trying to build a

sustainable business model, we believe, ARVND is ‘effective’ if not

‘efficient’ since it is moving in the right direction of moulding its business

model into that which fits into the future and doesn't fade away in the

past especially in a fast changing sector like fashion. We believe in the

immense opportunity that exists both in ARVND’s B2C businesses and

the apparel sector.

Silver lining to the Blind spot

New and unproved business can

create disproportionate return at a

non-linear pace. In addition to

creating possible future drivers of

the organisation, new initiatives

(Creyate, Technical Textiles,

Arvind Internet) can create a

perception of a ‘young’ firm and

may strike a healthy chord with the

youth.

Blind spot:

Despite its vintage in the

industry ARVND’s business

model continues to be work in

progress. Though we understand

that the company is ‘firing on all

cylinders’ realizing the

susceptibility of its textile

business by diversifying up the

value chain; the vicious cycle of

established segments

compensating for ‘formative’

segments continues.

‘Lack of steady state growth path’

Opportunity Threat

Is the concern more an opportunity or threat?

Incremental capital employed tending clearly towards new and

others business segments

Capital Employed; Source: Company filings, Spark Capital Research

69% 62% 62% 60% 54% 49%

10%13% 14% 16%

19%20%

0%0% 0% 2%

3% 5%3% 3% 6% 2% 5% 6%

18% 21% 19% 20% 20% 20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY 10 FY 11 FY 12 FY 13 FY 14 FY 15

Textiles Brands and Retail Real Estate Others Unallocable

Low

High

Low

High

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#3B – …funded by currently steady state (but vulnerable) cash flows from Textiles…

Page 7

Want to play ARVND for its

brands business…f

…however since still in ‘WIP’

dependant on Textile segment for

cash flows..

…Textile business though steady state

is cyclical in nature…

f

“……But the promised benefits from these textile investments were

illusory. Many of our competitors, both domestic and foreign, were

stepping up to the same kind of expenditures and, once enough

companies did so, their reduced costs became the baseline for reduced

prices industry wide. Viewed individually, each company’s capital

investment decision appeared cost- effective and rational; viewed

collectively, the decisions neutralized each other and were irrational (just

as happens when each person watching a parade decides he can see a

little better if he stands on tiptoes). After each round of investment, all the

players had more money in the game and returns remained anemic” —

Warren Buffet (Letter to Shareholders – 1985 Annual Report)

Textile Segment

‘ Inability to scale

up from fabric to

garmenting’

‘ Excess capacity

absorbing higher

fund flow’

‘Currency

Fluctuations’

‘ New competitive

markets for

sourcing emerge’

‘Exclusion of India

from various FTA’s’

‘Demand tapering in

end user countries’

‘ Product

substitutes/

disruption’

‘Availability of

continued high

quality raw material’

…and is dependant on umpteen factors which

are both within & ‘without’ control of

ARVND’s management

f

‘Factors beyond control of ARVND’

‘Factors within

control of ARVND’

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#3C – …hence leverage remains to be crucially monitored

Page 8

Rescheduling of Debt in 2009

On account of the weak business environment that

prevailed in the textile sector, ARVND had to

reschedule its debt in December 2008-January

2009. We understand that the company had

received approval to reschedule its term loan

obligations from its bankers that included State Bank

of India (SBI), Bank of Baroda, UCO Bank and ICICI

Bank for rescheduling term loan payment worth

Rs.150 million each for January and February 2009.

We also understand that CRISIL had downgraded

the ratings of the bank loan facilities of ARVND in

February 2009 to ‘D/P5’ from ‘BBB-/Negative/P3’ on

account of timeliness of payments stating that ‘it

believed ARVND’s internal accruals were unlikely to

be sufficient to meet its debt obligations and was in

discussion to reschedule its debt’.

Silver lining to the Blind spot

Majority of Textile companies

(refer slide 9) are highly

leveraged given the capital

intensive nature of business and

Arvind’s debt metrics are in-line

with the industry standards.

Natural benefits of having a

leveraged balance sheet

includes cheaper cost of capital,

and tax benefits among others

Blind spot:

ARVND already has reasonable

amount of debt on books which we

believe exerts pressure to

continuously deliver operating profits

to service debt.

Brief of Arvind’s Debt restructuring in 2001

In the mid 1990s, ARVND undertook a massive expansion of its denim capacity

despite the fact that alternate cotton fabrics were gradually replacing the demand

for denim. The expansion plan was funded by loans from both Indian and overseas

financial institutions. With the demand for denim slowing down, ARVND found it

difficult to service its debt obligations, and thus the interest burden on the loans shot

up. Consequently, in the late 1990s, ARVND ran into deep financial problems on

account of its huge debt burden and incurred huge losses. The company’s credit

rating had also been downgraded by CRISIL to “default” rating in October 2000

from “highest safety” in 1997.

Subsequently in 2001, the company announced a Rs.27bn plus debt restructuring

plan which the Gujarat High Court approved. This decision of the HC made the debt

restructuring plan legally binding on the company as well as on all lenders, including

the dissenting ones. The banks agreed to the buyback at a 55% discount on the

principal amount, while some agreed to a five year rollover for which they were

entitled to interest plus the principal. Some banks also agreed to a ten year rollover

for which they would be paid a higher rate of interest plus principal. The debtrevamp was estimated to reduce Arvind interest burden by 50%.

‘Leveraged Balance sheet’

Opportunity Threat

Is the concern more an opportunity or threat?

Though debt currently on

ARVND’s books is manageable, any

deterioration in the cash flow can

dent the financial standing of the

company. We believe an unlevered

balance sheet can give the luxury of

experimentation and ‘search’ for next

set of growth drivers.

Low

High

Low

High

Source: Media snippets and articles, Spark Capital Research

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#3C – …hence leverage remains to be crucially monitored

Page 9

ARVND’s capital outlay has been majorly funded by external

sources over the last many years...

Source: Company filings, Spark Capital Research

ARVND’s capital structure though leveraged in line with many peers

in the textile and apparel segment

Source: Company filings, Spark Capital Research

2.26

4.493.68 3.88

5.975.30

1.652.20 2.48

3.68 3.82 3.70

0

1

2

3

4

5

6

7

FY 11 FY 12 FY 13 FY 14 FY 15 FY 16E

In R

s.B

n

Capex PAT

ARVND’s financial metrics though above average are not as robust

to have nil impact during tail ends as reflected in the past

Source: Company filings, Spark Capital Research

1.26

0.80

1.81

1.10

2.23

1.02

0.00

0.50

1.00

1.50

2.00

2.50

Arvind KPR TextileMills

WelspunIndia

Indo CountIndustry

BombayRayon

Fashion

Raymonds

FY15 Debt-equity ratio

6.085.34

-2.15

5.49

2.34 2.24 2.271.78 1.79

0.10 0.09

0.03

0.10 0.17 0.19 0.20 0.21 0.19

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 FY 14 FY 15

Interest Coverge Ratio Net Cash Accruals to Total debt

...company to remain on capex mode given the nature of business

and formative stage of the new businesses

Source: Company filings, Spark Capital Research

71%

41% 36%

115%

134%

75%

100%107%

0%

20%

40%

60%

80%

100%

120%

140%

160%

FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 FY 14 FY 15

Capex as a % of Cash from operating activities

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY

Page 10

Mitra Adiperkasa: A Case study worthwhile to LOOK with relevance to ARVND

About Mitra Adiperkasa (MAPI): Mitra Adiperkasa is an Indonesian retail company with a diversified portfolio that includes department stores, fashion,

sports equipment, food & beverages, supermarkets as well as lifestyle products. Mitra Adiperkasa has 1792 retail outlets, that contain over 150 brands, in

58 cities across Indonesia. The company is franchise holder of various and numerous well-known global brands such as Starbucks, Zara and Nine West.

What happened to MAPI?

MAPI’s EBITDA in a matter of eighteen months fell 13% in FY15 (for 12 months ending September 2015) Vs FY13 while its net profit dropped drastically to

IDR -4.6 from IDR 327.8 in FY13. The company’s share price correspondingly fell from peak of IDR 9,550 in May 2013 to low of IDR 2,800 in September

2015. The probable reason for the company’s drastic fall was on account of concurrence of multiple unrelated events simultaneously which are explained

below and we have over the next two pages attempted to ‘discuss and understand’ what the impact of the same factors if occurred on ARVND.

Possible Reasons for

MAPI’s crisis?

#4

Sudden unfavorable

government

regulation

#5

Significant

depreciation of

home currency

#6

Aggressive debt-

funded expansion

#1

Rising inflation leading

to declining

purchasing power

#2

Consequences of

economic slowdown

and domestic

recession

#3

Long merchandise

procurement lead time

with majority of goods

sold being imported

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY

Page 11

Possible reasons for MAPI’s crisis & its relevance for ARVND?

Source: Industry sources, Spark Capital Research

Factor Affect of external/internal factors on MAPI Probable affect of similar factors on ARVND

#1

Statutory wage increase

as imposed by the

government

The Jakarta government raised the minimum wage by ~44% in 2013

and thereafter risen at a slower pace of around 10% while wages in

other parts of Indonesia rose around ~20 to ~30% levels. Hence with

biggest cost increases being witnessed in payroll not only did the

minimum wages of existing employees increase, the company was also

impacted since it added a lot of new employees as part of its expansion

who were to be paid as per the revised wage levels account of declining

purchasing power.

Though we believe the possibilities of the

central/state governments increasing wages drastically

like in the case of Indonesia is remote; we note that

any significant increase in labour cost can hinder

ARVND’s profitability with employee costs accounting

for ~9% to ~11% of revenues. Further, ARVND derives

more than ~60% of its revenues from the Textile

business which is labour intensive and the USP for

manufacturing in India being ‘cheap labour’.

#2

Consequences of

economic slowdown and

domestic recession

On the back of weak growth, four year low consumption and eight

year low consumer lending (in September 2014), MAPI was affected by

the economic slowdown on back of widespread job losses coupled with

bad festive season leading to weak purchasing power.

Though ARVND has a fair mix of revenues from

exports and domestic sales, any economic slowdown

(both globally or domestically) can affect the company

negatively with majority of the company’s portfolio of

brands (both retail and contract manufacturing)

dependant on disposable income for sales and growth.

#3

Long merchandise

procurement lead time

with majority of goods

sold being imported

MAPI inherently suffers from a long product procurement with a lead

time of 6-9 months, thus the company lacks flexibility to adjust inventory

levels quickly enough to adjust to changes in the external demand

environment. Further, analysis of MAPI’s inventory trends shows that its

inventory intensity rose sharply during periods of economic slowdown.

The procurement cycle is inherent to MAPI’s operating model that

entails imports of merchandize from multiple global brands.

ARVND unlike MAPI manufactures majority of its

goods domestically hence has greater control to adjust

inventory with on the back of lower product

procurement and lead time.

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY

Page 12

Possible reasons for MAPI’s crisis & its relevance for ARVND?

Source: Industry sources, Spark Capital Research

Factor Affect of external/internal factors on MAPI Probable affect of similar factors on ARVND

#4

Sudden unfavorable

government regulation

In 2015, to address the concern of slowing growth in the country the

Indonesian government hiked import tariffs (by 5% to 10%) on import of

clothing from countries [alongside hiking tariff on a array of consumer

goods in a bid to revive domestic manufacturing] with whom Indonesia

did not have a free trade agreement (FTA). With majority of MAPI’s

goods fully imported, the move severely impacted MAPI which was

already facing demand issues.

With majority of ARVND’s foreign label merchandise

being manufactured in India with minimal imports, any

such move by the Indian government to hike tariff on

imported goods is not expected to majorly impact

ARVND.

#5

Significant depreciation of

domestic currency

In between June 2013 and August 2015 Indonesian rupiah declined

~38% against the US dollar to decade low [from the time indications of

tapering of quantitative easing came to light] and lately has been

touching 17-year lows. With MAPI heavily dependant on imports, rupiah

depreciation severely impacted the company’s margin profile and

revenue growth

With majority of ARVND’s foreign label merchandise

being manufactured in India with minimal imports,

depreciation of Indian rupee may not adversely affect

pricing however possibly could impact the royalty paid

though.

#6

Aggressive debt-funded

expansion

During the said period, MAPI aggressively expanded every year, which

led to increase in rents in turn leading to higher costs and losses in FY14.

After its establishment in the 1990s with a handful of stores, MAPI

expanded rapidly through franchise agreements with foreign companies

keen to tap Indonesia's growing consumer base. MAPI currently has

nearly 1,900 stores in 65 cities selling some 150 brands. Further, in

addition to capex with the economy facing an economic slowdown,

increasing prices were not an option and inventories had to be cleared

with heavy discounts leading to negative PAT in FY14.

Though ARVND has not been aggressive on its

capex front in its recent past, a long tail of business in

growth phase entails huge and incessant capex which

does pose a similar kind of threat though not to the

degree of impact on MAPI.

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUYPositive Triggers

Page 13

Positive Triggers

In addition to the positive triggers which can catapult ARVND

significantly, following are the structural pillars on which the

positive triggers are expected to take off:

• Portfolio of strong brands straddled across price points:

ARVND brands encompassing several exciting global brands and

private label offerings are positioned across pricing pyramid which

we believe should enable ARVND to take advantage of consumer

migration at every price point. As the four power brands (Arrow, US

Polo, Flying Machine and Tommy Hilfiger - FY15 turnover Rs.

~13bn) continues to grow at a robust pace, we foresee huge non-

linearity in profitability of the non-power brands portfolio (FY15

turnover Rs. ~4bn) as it comes out of the investment phase from

FY16 onwards. We see an exciting opportunity for ARVND to create

an unparalleled portfolio of apparel brands (30+ brands currently)

which can command an EV of Rs. ~60bn alone by FY18e.

• ‘Preferred’ partner: ARVND being present across the textile value

chain is certainly beginning to emerge as a preferred partner for

several international brands. We also note that entrenched

distribution network of ARVND possessing ~989 key account POS in

India augurs well for them in attracting international brands. Further,

ARVND’s history suggests that seldom have their joint ventures or

licenced agreements ended in sour note, establishing their strong

execution capabilities. ARVND’s focussed initiatives to continuously

innovate across the apparel value chain from ‘fibre to fashion’ in

emerging technologies as technical textiles and e-commerce

underscores the company’s ability to understand emerging consumer

trend in fashion industry.

#4 Increasing proportion of B2C

segment revenues can lead to

valuation re-rating

#3

Investments into new-gen

businesses…. lottery

tickets

#2 Steady state

textile business to

play a supporting

role

#1 Huge non-linearity in

brands business keeps us

exhilarated

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#1 Huge non-linearity in brands business keeps us exhilarated

Page 14

Tommy Hilfiger

Revenues –

CY14

Total Stores

Presence

Casual sportswear

brand for men, women

and kids targeted

primarily at the age

group between 25 years

to 40 years

Others

Description

Retailed in over 90

countries globally

Global Retail Sales:

$6.7bn

Revenues: $3.6bn

~1500+ stores with ~520

stores in Asia

EBIT Margin:14.2%

Derives ~10% of total

retail sales from Asia

Calvin Klein

Calvin Klein has four

brands viz. CK

Collection, CK

(platinum label), CK

(white label), CK Jeans

and CK Underwear; it is

also a licensor for a

range of products,

including fragrance,

women's apparel,

footwear, eyewear,

watches and jewellery

Retailed in over 100

countries globally

Global Retail Sales:

$8.1bn

Revenues: $2.9bn

~2730 stores with ~1600

stores in Asia

EBIT Margin:14.0%

GAP

Leading global

specialty retailer

offering clothing,

accessories and

personal care products

for men, women,

children and

babies.with a portfolio

of five brands viz. GAP,

Banana Republic, Old

Navy, Athleta &

Intermix

Retailed in over ~50

countries and sold online

in ~90+ countries

Net Sales: $16.4bn

~3700+ stores worldwide

with

Operating Margin:

~12.7%

Net Sales/Sq.ft: $361

US Polo

U.S. Polo Assn. brand

is the official brand of

the United States Polo

Association (USPA). It’s

wholly owned

subsidiary partners

with licensees to

provide consumers

with branded apparel,

accessories, luggage,

watches, shoes, small

leather goods, eyewear

and home furnishings.

The company’s brand is

licensed in over 135

countries.

NA

NA

Among Top 50 global

licensors

Aeropostale

Aéropostale, Inc. is a

mall-based, specialty

retailer of casual

apparel and

accessories, principally

targeting 14 to 17 year-

old young women and

men through its

Aéropostale® stores

and 4 to 12 year-old

kids through its P.S.

from Aéropostale™

stores

Outside US & Canada its

licensees operate ~239

stores 13 countries

Net Sales: ~$1.84bn

~1050+ stores across the

world

Net Sales/Sq.ft: $403

Source: Company filings, Spark Capital Research

ARVND’s portfolio includes some of the top brands in the world which clock billions of dollars in revenues worldwide annually

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#1 Huge non-linearity in brands business keeps us exhilarated

Page 15

Source: Spark Capital Research

Luxury

Bridge To

Luxury

Mass Market

Entry Level

Premium

ARVND Brands

Luxury Apparel

brands

synonymous with

Multinational

brands

Premium Apparel

brands space has

a mix of Indian

and Multinational

brands

Brands can be

Indian but to be

positioned and

advertised as a

‘multinational’

brand.

ARVND’s robust portfolio straddled across segments stand out in their respecting categories

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#1 Huge non-linearity in brands business keeps us exhilarated

Page 16

Snapshot of GAP’s journey and success in China; Though India is far away from where China is, GAP’s potential in emerging markets is

displayed

Snapshot of GAP in China:

Year Entered: 2010

Revenues: $300mn in 2013 and expected

to triple by 2016-17

Type of Entry in China: Direct

GAP Journey in China

CY2011

Opened 10 stores during the year and

closed the year with 14 stores totally in

five cities

CY2012Opened 30 stores during the year by

bringing in outlet business

CY2013

Opened over 30 stores including in 5

new additional cities. Ended the year

with presence in 21 cities

CY2014

Company ended the year with119

Stores including Old Navy

Company clocked $500 million of

revenues in just over four years of

entry

GAP entered China in November 2010 Fall with opening of

4 stores

CY2015

116 GAP stores and 10 old navy

stores as of October 2015 – Total

132 stores

Importance of GAP China in the words of Mr. Art Peck (CEO

of GAP Inc.)

“ In China, we opened our 100th store for Gap brand. I think that's

exciting. That's great progress. …Old Navy continues to do very

well inside of China. So with that combination, we feel very good

about as we look at China becoming the second most important

country to Gap, Inc. as we go forward”

“But, yeah, for us if the productivity per foot is better than average,

then in most cases you can assume we can get a better operating

margin for a total country than we have in North America so let's

hope that the sales per foot in China continues at the rates they

are right now.”

“And we think that's going to be by far our second biggest market

sooner rather than later. And I feel good about the performance all

around. And profitability is going to be there because we think that

the economic model as we project forward and look at the

productivity in each one of our stores, we look at the gross margin

rate we think we can achieve based on three years of operating,

how the SG&A is going to flow, what the ROD is going to look like,

we believe the economic model for China is going to be very

attractive to the business.”

E-commerce

opened from

Day 1

Within 2

years of

entry outlet

centres

channel also

commenced

Source: Company filings, Spark Capital Research

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#1 Huge non-linearity in brands business keeps us exhilarated

Page 17

Possible factors which we believe that worked in China & can play out in India as well

What worked in China?Snippets on GAP China in the words of the management

“We want to lead the way in bringing Omni-channel to life

in China. “It’s early days yet, but with the addition of virtual

experiences both in our Gap stores and in other non-

traditional locations, we hope to offer more points of

access to our Chinese customer so she can shop our

brands wherever, whenever and however she wants.”

“I think by the amount of capital we're spending there, the

amount of energy you're getting at the most senior level of

the company, China reports directly to me, I think it's a

real strong indicator to our shareholders and the analysts

that we believe we've got a tiger by the tail. And we think

that's going to be by far our second biggest market sooner

rather than later. And I feel good about the performance

all around. And profitability is going to be there because

we think that the economic model as we project forward

and look at the productivity in each one of our stores, we

look at the gross margin rate we think we can achieve

based on three years of operating, how the SG&A is going

to flow, what the ROD is going to look like, we believe the

economic model for China is going to be very attractive to

the business.”

“Everything in China we've uncovered so far is,

customers love fashion, it is a big family play, which

obviously fits for Old Navy and for Gap, value proposition,

but not discounting, just being money – not overpaying for

quality, which is a good definition of value, which is

important to the Chinese.”

- GAP Inc concalls – 2009-2015

Mix of Distribution Channel

f

Able Managementf

Creating a strong brand with

solid perception management f

Robust assortment mix

f

Tier 2 Cities penetration &

Chinese perception of valuef

The company operated with a different strategy in

China by commencing its online operations from Day

one. Further, within a short span of time GAP started

opening outlet stores in China in addition to specialty

stores having a healthy mix of all forms of retail. With

online channel and outlet format operating profitability

commanding higher profitability, the company’s

operating margins were close US GAP profitability

despite being in early stages of operations in China.

Glocal management : The company struck a balance

between the global marketing that operated out of New

York helping the Chinese team, in addition to having a

separate agency in China to speak and augment its

branding and communication.

The management believed in long term investment in

marketing and branding awareness. In the words of Mr.

Art Peck ‘the company did not sacrifice the near to mid-

term investments for a real great long-term business’.

In China, the kids and baby business index was much

higher into the overall business than the adult business.

Hence, with assortment of products better in China than

in North America with a favourable mix to kids and

baby, the same acted to be more of a relative strength.

Quoting GAP’s management from their concalls “Gap

right now is in some, let's call them for argument sake

Tier 4, Tier 5 cities, doing well. Everything in China

we've uncovered so far is, customers love fashion, it is

a big family play,, value proposition, but not

discounting, just being money – not overpaying for

quality, which is a good definition of value, which is

important to the Chinese”

Source: Company filings, Spark Capital Research

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY

PVH despite its vintage still trades in ~14 to ~20 band

Source: Bloomberg, Spark Capital Research

#1 Huge non-linearity in brands business keeps us exhilarated

Page 18

GAP one-year forward PE peaked at ~21 times in 2007

Source: Bloomberg, Spark Capital Research

H&M: With growth rate peaking, 1 year forward PE back to peak

valuations

Source: Bloomberg, Spark Capital Research

…Abercrombie & Fitch too at peak levels of ~26x one year forward

Source: Bloomberg, Spark Capital Research

Globally, apparel companies have traded at rich valuations even in matured markets

9

11

13

15

17

19

21

Dec-0

5

Ma

y-0

6

Oct-

06

Ma

r-07

Au

g-0

7

Jan

-08

Jun

-08

Nov-0

8

Ap

r-09

Se

p-0

9

Fe

b-1

0

Jul-1

0

Dec-1

0

Ma

y-1

1

Oct-

11

Ma

r-12

Au

g-1

2

Jan

-13

Jun

-13

Nov-1

3

Ap

r-14

Se

p-1

4

Fe

b-1

5

Jul-1

5

6

8

10

12

14

16

18

20

Dec-0

5

Ma

y-0

6

Oct-

06

Ma

r-07

Au

g-0

7

Jan

-08

Jun

-08

Nov-0

8

Ap

r-09

Se

p-0

9

Fe

b-1

0

Jul-1

0

Dec-1

0

Ma

y-1

1

Oct-

11

Ma

r-12

Au

g-1

2

Jan

-13

Jun

-13

Nov-1

3

Ap

r-14

Se

p-1

4

Fe

b-1

5

Jul-1

5

13

15

17

19

21

23

25

27

Dec-0

5

Ma

y-0

6

Oct-

06

Ma

r-07

Au

g-0

7

Jan

-08

Jun

-08

Nov-0

8

Ap

r-09

Se

p-0

9

Fe

b-1

0

Jul-1

0

Dec-1

0

Ma

y-1

1

Oct-

11

Ma

r-12

Au

g-1

2

Jan

-13

Jun

-13

Nov-1

3

Ap

r-14

Se

p-1

4

Fe

b-1

5

Jul-1

5

7

9

11

13

15

17

19

21

23

25

27

Dec-0

5

May-…

Oct-

06

Ma

r-07

Au

g-0

7

Jan

-08

Jun

-08

Nov-0

8

Ap

r-09

Se

p-0

9

Fe

b-1

0

Jul-1

0

Dec-1

0

May-…

Oct-

11

Ma

r-12

Au

g-1

2

Jan

-13

Jun

-13

Nov-1

3

Ap

r-14

Se

p-1

4

Fe

b-1

5

Jul-1

5

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#1 Huge non-linearity in brands business keeps us exhilarated

Page 19

6.2 6.9 8.3 9.1 12.5 18.1 22.4 25.2 32.3 37.4

9.4%11.7%

8.1%

0.2% -0.3% 7.6%

8.8% 9.7%12.0% 12.4%11%

20%

29%

64%

72%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

0

5

10

15

20

25

30

35

40

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Rs.b

n

Madura Garments Revenue Madura Garments EBITDA Margin Madura Garments ROACE

As exhibited in Madura garments, we

believe margins and capital

efficiency significantly increase as

brands achieve a certain milestone

revenue mark.

Other Brands expected to start generating profits by FY17…

Source: Company, Spark Capital Research

…leading to massive improvement in overall brands profitability

Source: Company, Spark Capital Research

1,1853,724 5,251 7,904 12,455

-43.5%

-12.4%

-2.0%

6.0% 7.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

0

2000

4000

6000

8000

10000

12000

14000

FY 14 FY 15 FY 16E FY 17E FY 18E

Rs.m

n

Other Brands Revenue Other brands EBITDA%

847 1,058 1,957 3,126 4,239

6.5%

6.2%

9.3%

11.3%11.6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

500

1000

1500

2000

2500

3000

3500

4000

4500

FY 14 FY 15 FY 16E FY 17E FY 18E

Rs.m

n

Brands EBITDA Brands EBITDA%

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#2 Steady state textile business to play a supporting role

Page 20

…without compromising on margins leading…

Source: Company, Spark Capital Research

Arvind’s textiles business has managed to deliver healthy revenue growth across macro-economic cycles…

Source: Company, Spark Capital Research

…to strong cash flow generation over years to fund other businesses

Source: Company, Spark Capital Research

1393 1623

3191

1889 1701

23892879

38504.7%

6.1% 6.3%

9.6%

12.7%13.3% 13.4%

12.6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0

500

1000

1500

2000

2500

3000

3500

4000

4500

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

RO

CE

Rs.m

n

Standalone Free Cash flows (Rs.mn) Standalone ROCE

10.6%

-2.6%

23.7% 24.5%

13.0%

8.1%

25.6%

9.0%

1.8%

9.9% 9.8%

1.5%

-2.0%4.1% 3.0% 2.4% 2.5% 2.6% 2.9% 3.2% 3.2% 3.2%

3.9%

8.5%10.3%

6.6%5.1%

6.9%

7.2%

7.5%7.5% 7.6% 7.7%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

Textiles segment Revenue growth (%) Global GDP growth (%) India GDP growth (%)

3.38 2.90 3.654.94

6.48 6.43

8.56 8.98 8.979.76

10.93

16.7%

14.7% 15.0%16.3%

18.9%17.4%

18.4%17.7% 17.4% 17.2% 17.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

0.00

2.00

4.00

6.00

8.00

10.00

12.00

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16EFY17EFY18E

Textile Segment EBITDA (Rs.bn) Textile segment EBITDA margins (%)

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#3 Investments into new-gen business…. a lottery ticket

Page 21

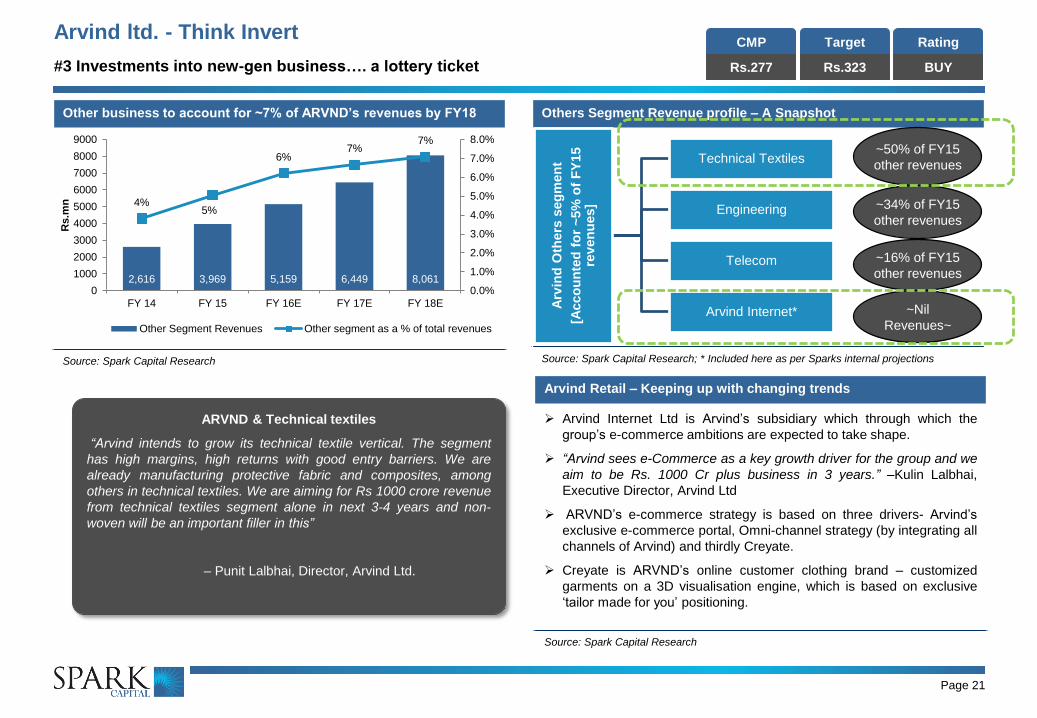

Other business to account for ~7% of ARVND’s revenues by FY18

Source: Spark Capital Research

Others Segment Revenue profile – A Snapshot

Source: Spark Capital Research; * Included here as per Sparks internal projections

Arvind Retail – Keeping up with changing trends

Arvind Internet Ltd is Arvind’s subsidiary which through which the

group’s e-commerce ambitions are expected to take shape.

“Arvind sees e-Commerce as a key growth driver for the group and we

aim to be Rs. 1000 Cr plus business in 3 years.” –Kulin Lalbhai,

Executive Director, Arvind Ltd

ARVND’s e-commerce strategy is based on three drivers- Arvind’s

exclusive e-commerce portal, Omni-channel strategy (by integrating all

channels of Arvind) and thirdly Creyate.

Creyate is ARVND’s online customer clothing brand – customized

garments on a 3D visualisation engine, which is based on exclusive

‘tailor made for you’ positioning.

Source: Spark Capital Research

ARVND & Technical textiles

“Arvind intends to grow its technical textile vertical. The segment

has high margins, high returns with good entry barriers. We are

already manufacturing protective fabric and composites, among

others in technical textiles. We are aiming for Rs 1000 crore revenue

from technical textiles segment alone in next 3-4 years and non-

woven will be an important filler in this”

– Punit Lalbhai, Director, Arvind Ltd.A

rvin

d O

thers

seg

men

t

[Acco

un

ted

fo

r ~

5%

of

FY

15

rev

en

ues]

Technical Textiles

Engineering

Telecom

Arvind Internet*

~50% of FY15

other revenues

~34% of FY15

other revenues

~16% of FY15

other revenues

~Nil

Revenues~

2,616 3,969 5,159 6,449 8,061

4%5%

6%7%

7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

FY 14 FY 15 FY 16E FY 17E FY 18E

Rs.m

n

Other Segment Revenues Other segment as a % of total revenues

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY#4 Increasing proportion of B2C segment revenues can lead to valuation re-rating

Page 22

B&R segment growth driving the company’s growth trajectory…

Source: Spark Capital Research

…to further increase with increasing proportion of B&R revenues

Source: Spark Capital Research

10%3%

23%

3%

19%25%

21%

7%

30%

14%

39%

28%

68%

14%

5%

40%

33%

6%

36%

23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Revenue growth B&R growth

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Textiles Brands & Retail Real Estate Others

Brands & Retail business to grow at ~24% CAGR over next 3 years

Source: Company, Spark Capital Research

Brands & Retail business is expected to grow at ~24% CAGR in 3

years led by

(1) Steady growth of power brands

(2) Non-linear growth of non-power and other new brands,

with some of them expected to ‘graduate’ to power brand

‘status’

(3) Incremental growth of power brands once some of them

reach inflection point of ‘Rs.8bn to Rs.10bn’ in company

revenues.

14.0419.15

23.5027.07

34.40

44.38

5.3% 5.2% 5.2%

6.8%

8.9%

10.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

5

10

15

20

25

30

35

40

45

50

FY 13 FY 14 FY 15 FY 16E FY 17E FY 18E

In R

s.B

n

Brands & Retail Revenues Brands & Retail EBITDA %

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY

Page 23

Valuations – B2B to B2C shift can trigger re-rating

Valuing it on SOTP, we arrive at a TP of Rs.323 (17% upside from CMP)

Source: Spark Capital Research

Segments Parameter FY18E

Multiple (x) EV (Rs. mn) % Share Particulars Rs. mn

Textiles EV EBITDA 10,929 4.0 43,715 37%

Power Brands EV EBITDA 3,367 18.0 60,603 52%

Growth Brands EV Sales 12,455 1.0 12,455 11%

Retail / Mega Mart EV EBITDA 273 1.0 273 0%

Others EV Sales 8,061 0.0 0 0%

Land Value*

Summarised EV (Rs.mn) 1,17,045

Net Debt (Rs.mn) 33,680

MCAP (Rs.mn) 83,365

Nos of shares 258

TP 323

UPSIDE 17%

CMP 277

Implied P/E 18

Implied EV/EBIDTA 9

We continue to retain our positive stance on ARVND

based on the size of the opportunity and ARVND’s

portfolio of brands to capitalise the same. However,

appreciating the complexity of the drivers and

execution challenges involved, we believe

monitoring financial leverage level will be extremely

crucial during the ‘vision’ fulfilling journey as

controlled debt can give the luxury to accommodate

the volatility in the macro cycle, gestation in the

evolving consumption habits and any unaccounted

disruptions. We retain BUY with a TP of Rs.323

(implied PE of 15x F17E EPS).

* Arvind posses a land bank of ~250 acres near Ahmedabad and ~25 acres in Ahmedabad

which are estimated by market participants at Rs.~5bn, we have not ascribed any value to the

same. Any realisation in this aspect could impact financials positively

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUY

Page 24

Financial Summary

Abridged Financial Statements Key Metrics

Rs.mn FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E

Profit & Loss Growth Ratios (%)

Revenue 78,514 83,030 96,640 1,13,654 Revenues 14% 6% 16% 18%

EBIDTA 10,129 10,560 12,825 15,682 EBIDTA 11% 4% 21% 22%

Other Income 932 900 1,000 1,150 PAT 4% -7% 33% 45%

Depreciation 2,124 2,438 2,901 3,220 Margins (%)

EBIT 8,937 9,022 10,924 13,612 EBIDTA 12.9% 12.7% 13.3% 13.8%

Interest 3,946 4,073 4,270 4,221 EBIT 11.4% 10.9% 11.3% 12.0%

PBT 4,991 4,949 6,654 9,391 PAT 4.9% 4.3% 4.9% 6.0%

Tax 1,072 1,435 1,996 2,629 Return Ratios (%)

Normalised PAT 3,823 3,546 4,701 6,824 RoCE 11.9% 10.2% 11.3% 13.9%

EPS (Rs.) 14.8 13.7 18.2 26.4 RoE 14.4% 12.4% 14.8% 18.9%

Balance Sheet Total Asset Turnover (x) 1.3 1.2 1.4 1.6

Net Worth 27,239 29,945 33,557 38,826 Leverage Ratios (x)

Loan Funds 31,275 35,500 34,500 32,500 Debt to Equity 1.15 1.19 1.03 0.84

Other Long Term Liabilities 1,026 994 951 889 Current Ratio 1.97 2.05 2.02 2.02

Sources of Funds 59,539 66,438 69,008 72,214 Working Capital Ratios

Net Block 30,964 33,826 34,725 35,505 Debtor Days 54 54 52 52

Intangible Assets 2,118 2,118 2,118 2,118 Inventory days 86 86 90 90

Investments 6,775 8,775 7,275 5,275 Creditor Days 63 62 64 64

Total Current Assets 39,900 42,365 49,272 58,112 Per Share

Total Current Liabilities 20,217 20,645 24,382 28,795 Face Value 10.0 10.0 10.0 10.0

Net Current Assets 19,682 21,719 24,890 29,316 Dividend 2.5 2.7 3.5 5.0

Application of Funds 59,539 66,438 69,008 72,214 Valuation Metrics

Cash Flow Shares Outstanding (mn) 258 258 258 258

Cash Flow from Pre-Working Cap 8,726 9,125 10,829 13,052 Market Cap. (Rs. mn) 71,533 71,533 71,533 71,533

Working Capital -3,142 -1,627 -3,594 -4,117 Enterprise Value (Rs. mn) 95,126 96,997 97,921 97,611

Cash Flow from Operations 5,584 7,497 7,235 8,936 EV /Sales (x) 1.2 1.2 1.0 0.9

Capex -5,967 -5,300 -3,800 -4,000 Price/Earnings (x) 18.7 20.2 15.2 10.5

Cash Flow from Investments -5,874 -6,400 -1,300 -850 Price/Book (x) 2.6 2.4 2.1 1.8

Free Cash Flow 198 2,197 3,435 4,936 EV/EBIDTA (x) 9.4 9.2 7.6 6.2

Cash Flow from Financing -485 -688 -6,359 -7,776 FCF Yield (%) 0.2% 2.3% 3.5% 5.1%

Closing Cash Balance 889 1,243 819 1,129 Dividend Yield 0.9% 1.0% 1.3% 1.8%

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUYDisclaimer

Page 25

Spark Disclaimer

Spark Capital Advisors (India) Private Limited (Spark Capital) and its affiliates are engaged in investment banking, investment advisory and institutional equities and

infrastructure advisory services. Spark Capital is registered with SEBI as a Stock Broker and Category 1 Merchant Banker.

We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in the last five years. We

have not been debarred from doing business by any Stock Exchange/SEBI or any other authorities, nor has our certificate of registration been cancelled by SEBI at any point of

time.

Spark Capital has a subsidiary Spark Investment Advisors (India) Private Limited which is engaged in the services of providing investment advisory services and is registered

with SEBI as Investment Advisor. Spark Capital has also an associate company Spark Infra Advisors (India) Private Limited which is engaged in providing infrastructure

advisory services.

This document does not constitute or form part of any offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Nothing in this document should

be construed as investment or financial advice, and nothing in this document should be construed as an advice to buy or sell or solicitation to buy or sell the securities of

companies referred to in this document.

Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies

referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. This

document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published,

copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in

any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Spark Capital

and/or its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to

a certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such applicable restrictions. This

material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Spark Capital makes no representation or warranty, express or implied, as to the accuracy, completeness or fairness of the information and opinions contained in this

document. Spark Capital , its affiliates, and the employees of Spark Capital and its affiliates may, from time to time, effect or have effected an own account transaction in, or

deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit

investment banking or other business from, any company referred to in this report.

This report has been prepared on the basis of information, which is already available in publicly accessible media or developed through an independent analysis by Spark

Capital. While we would endeavour to update the information herein on a reasonable basis, Spark Capital and its affiliates are under no obligation to update the information.

Also, there may be regulatory, compliance or other reasons that prevent Spark Capital and its affiliates from doing so. Neither Spark Capital nor its affiliates or their respective

directors, employees, agents or representatives shall be responsible or liable in any manner, directly or indirectly, for views or opinions expressed in this report or the contents

or any errors or discrepancies herein or for any decisions or actions taken in reliance on the report or the inability to use or access our service in this report or for any loss or

damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits that may arise from or in connection with the use of

or reliance on this report.

Absolute

Rating

Interpretation

BUY Stock expected to provide positive returns of >15% over a 1-year horizon REDUCEStock expected to provide returns of <5% – -10% over a 1-year

horizon

ADDStock expected to provide positive returns of >5% – <15% over a 1-year

horizonSELL Stock expected to fall >10% over a 1-year horizon

Arvind ltd. - Think InvertCMP

Rs.277

Target

Rs.323

Rating

BUYDisclaimer (Cont’d)

Page 26

Spark Capital and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency,

Spark Capital has incorporated a disclosure of interest statement in this document. This should however not be treated as endorsement of views expressed in this report:

Disclosure of interest statement Yes/No

Analyst financial interest in the company No

Group/directors ownership of the subject company covered No

Investment banking relationship with the company covered No

Spark Capital’s ownership/any other financial interest in the company covered No

Associates of Spark Capital’s ownership more than 1% in the company covered No

Any other material conflict of interest at the time of publishing the research report No

Receipt of compensation by Spark Capital or its Associate Companies from the subject company covered for in the last twelve months:

Managing/co-managing public offering of securities

Investment banking/merchant banking/brokerage services

products or services other than those above

in connection with research report

No

Whether Research Analyst has served as an officer, director or employee of the subject company covered No

Whether the Research Analyst or Research Entity has been engaged in market making activity of the Subject Company; No

Analyst Certification of Independence

The views expressed in this research report accurately reflect the analyst’s personal views about any and all of the subject securities or issuers; and no part of the research

analyst’s compensations was, is or will be, directly or indirectly, related to the specific recommendation or views expressed in the report.

Additional Disclaimer for US Institutional Investors

This research report prepared by Spark Capital Advisors (India) Private Limited is distributed in the United States to US Institutional Investors (as defined in Rule 15a-6 under

the Securities Exchange Act of 1934, as amended) only by Auerbach Grayson, LLC, a broker-dealer registered in the US (registered under Section 15 of Securities Exchange

Act of 1934, as amended). Auerbach Grayson accepts responsibility on the research reports and US Institutional Investors wishing to effect transaction in the securities

discussed in the research material may do so through Auerbach Grayson. All responsibility for the distribution of this report by Auerbach Grayson, LLC in the US shall be borne

by Auerbach Grayson, LLC. All resulting transactions by a US person or entity should be effected through a registered broker-dealer in the US. This report is not directed at you

if Spark Capital Advisors (India) Private Limited or Auerbach Grayson, LLC is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available

to you. You should satisfy yourself before reading it that Auerbach Grayson, LLC and Spark Capital Advisors (India) Private Limited are permitted to provide research material

concerning investment to you under relevant legislation and regulations;