arteris s.a. and subsidiaries - ri.arteris.com.brri.arteris.com.br/ptb/5971/arteris 1t16 ingls...

TRANSCRIPT

Arteris S.A. and Subsidiaries Parent Company and Consolidated Interim Financial Information for the Quarter Ended March 31, 2016 Deloitte Touche Tohmatsu Auditores Independentes

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms,

and their related entities. DTTL and each of its member firms are legally separate and independent entities. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms

.© Deloitte Touche Tohmatsu. All the rights reserved.

Deloitte Touche Tohmatsu

Av. Dr. José Bonifácio Coutinho Nogueira, 150 - 5º andar

Campinas - SP - 13091-611 Brasil

Tel: + 55 (19) 3707-3000

Fax:+ 55 (19) 3707-3001

www.deloitte.com.br

REPORT ON THE REVIEW OF QUARTERLY INFORMATION

To the Board of Directors and Shareholders of

Arteris S.A.

São Paulo - SP

We have reviewed the individual and consolidated interim financial statements of Arteris S.A. (“Company”),

contained in the Interim Financial Information – ITR for the quarter ended March 31, 2016, which comprise

the balance sheet as of March 31, 2016 and the related statements of income, comprehensive income,

changes in equity and of cash flows for the three-month period then ended, including the explanatory notes.

The Company’s Management is responsible for the preparation of these individual interim financial

statements, in accordance with Technical Pronouncement CPC 21 (R1) – Interim Financial Information, and

consolidated interim financial statements, in accordance with Technical Pronouncement CPC 21 (R1) and

the international standard IAS 34 – Interim Financial Reporting issued by the International Accounting

Standards Board (IASB), as well as for the presentation of these information in accordance with the

standards issued by the Brazilian Securities and Exchange Commission applicable to the preparation of

Interim Financial Information – ITR. Our responsibility is to express a conclusion on this interim financial

information based on our review.

Scope of review

We conducted our review in accordance with Brazilian and international standards on the review of interim

financial information (NBC TR 2410 – Interim Information Review Performed by the Auditor of the Entity

and ISRE 2410 – "Review of Interim Financial Information Performed by the Independent Auditor of the

Entity" respectively). A review of the interim financial information consists of making inquiries, primarily to

those responsible for financial and accounting matters, and applying analytical and other review procedures.

The review scope is significantly less than that of an audit conducted in accordance with auditing standards

and consequently does not enable us to assure that we have became aware of all significant matters that

might be identified in an audit. Therefore, we do not express an audit opinion.

Conclusion on the individual interim financial information

Based on our review, we are not aware of any fact that could lead us to believe that the individual interim

financial information included in the aforementioned interim financial information was not prepared, in all

material aspects, in accordance with CPC 21 (R1), applicable to the preparation of the Interim Financial

Information – ITR, and presented in accordance with the standards issued by the Securities and Exchange

Commission.

Conclusion on the interim consolidated financial information

Based on our review, we are not aware of any fact that could lead us to believe that the consolidated interim

financial information included in the aforementioned interim financial information was not prepared, in all

material aspects, in accordance with CPC 21 (R1) and IAS 34, applicable to the preparation of the Interim

Financial Information – ITR, and presented in accordance with the standards issued by the Securities and

Exchange Commission.

Deloitte Touche Tohmatsu

© 2015 Deloitte Touche Tohmatsu. All the rights reserved. 3

Emphasis of matter

Difference from individual statements of IFRS

As mentioned in Note 3, the individual financial statements were prepared in accordance with the accounting

practices adopted in Brazil. In the case of Arteris S.A., these practices differ from the IFRS – applicable to

the individual financial statements – solely with respect to the option of maintaining the balance of deferred

assets, as of December 31, 2008, which is being amortized. Our opinion is not qualified under this subject.

Restatement of cash flows related to the interim financial information as of March 31, 2015

On May 14, 2015 we issued a review report on the interim financial information of Arteris S.A., which are

now being restated. As described in Note 5, this interim financial information has been changed and is being

restated in accordance with CPC 23/IAS 8 – Accounting Policies, Changes in Accounting Estimates and

Errors. Our conclusion remains unchanged, given that the interim financial information and their values for

the previous period have been adjusted retrospectively.

Other matters

Statement of value added

We have also revised the statements of value added (DVA) prepared under the Company’s Management

responsibility, individual and consolidated, for the three-month period ended March 31, 2016, the

presentation of which is required by the standards issued by the Securities and Exchange Commission

(CVM) applicable to the preparation of Interim Financial Information (ITR) and considered as supplemental

information for International Financial Reporting Standards – IFRS, which does not require the presentation

of DVA. These statements were subject to the same review procedures described above, and based on our

review, we are not aware of any fact that could lead us to believe that they were not prepared, in all material

aspects, consistently with the interim financial information taken as a whole.

Campinas, May 11, 2016

DELOITTE TOUCHE TOHMATSU Edgar Jabbour

Auditores Independentes Accountant

CRC 2SP 011609/O-8 CRC 1SP 156465/O-9

2

ARTERIS S.A.

(In thousands of Brazilian reais - R$)

Note Note ASSETS 31/03/2016 31/12/2015 31/03/2016 31/12/2015 LIABILITIES AND SHAREHOLDERS' EQUITY 31/03/2016 31/12/2015 31/03/2016 31/12/2015

CURRENT ASSETS CURRENT LIABILITIESCash and cash equivalents 6 188.927 127.362 498.757 488.529 Borrowings and financing 13 361.927 - 604.379 234.496 Trade receivables 7 - - 165.834 153.130 Instrumento financeiro derivativo 25 37.794 37.794 Amounts due from related parties 15 206.422 190.629 260 - Borrowings and financing - related parties 15 136.390 132.218 - - Inventories - - 10.688 8.866 Debentures 14 900.875 859.166 1.730.006 1.726.915 Prepaid expenses 593 302 17.370 18.622 Trade payables 2.742 6.246 121.835 139.391 Taxes recoverable 14.030 17.563 83.696 83.846 Payroll and related taxes 16.354 14.776 80.859 78.487 Advances for new projects - - - - Taxes payable 2.443 5.975 70.528 63.663 Dividends receivable 15 5.674 6.223 5.674 6.223 Amounts due to related parties 15 182 100 152 - Restricted investments 9 23.301 - 40.646 154.171 Contractual guarantees - - 73.969 78.189 Other receivables 825 1.543 5.155 4.977 Inspection fee - - 3.820 3.519 Total current assets 439.772 343.622 828.080 918.364 Dividends proposed 18 33.270 33.270 33.270 33.270

Concession fees 16 - - 82.779 79.765 Provision for contingencies 17 - - 202.897 173.524

NON-CURRENT ASSETS Provision for maintenance in highways 17 - - 61.516 56.711 Restricted investments 9 - - 90.609 85.872 Provision for investments in highways - - - - Taxes recoverable 10.987 7.506 15.390 10.449 Claims received - - 798 3.942 Amounts due from related parties 15 1.987.152 1.941.910 - - Other payables 2.176 4.328 9.971 15.249 Prepaid expenses - - 704 150 Total current liabilities 1.494.153 1.056.079 3.114.573 2.687.121Contractual guarantees - - - 24 Deferred income tax and social contribution 8 - - 285.302 256.591 NON-CURRENT LIABILITIESEscrow deposits 17 6.266 6.266 118.942 111.437 Borrowings and financing 13 - - 2.837.227 2.885.688 Other receivables 7 - - 8.293 8.164 Borrowings and financing - related parties 15 1.418.928 1.391.395 - - Investments in subsidiaries and associates 10 2.927.927 2.593.198 1.053 1.053 Debentures 14 198.646 198.418 1.323.569 1.539.304 Property and equipment 11 9.186 9.621 61.581 62.414 Trade payables - - - 2.824 Intangible assets 12 21.879 21.112 8.856.456 8.627.052 Trade payables - related parties 15 - - - - Diferido - - - - Cauções contratuais - - - - Total non-current assets 4.963.397 4.579.613 9.438.330 9.163.206 Concession fees 16 - - 93.232 108.926

Civil, labor and tax risks 17 - 222 16.634 17.517 Deferred revenue - - - - Deferred income tax and social contribution 8 - - 59.857 62.870 Provision for maintenance in highways 17 - - 482.688 457.361 Provision for investments in highways 17 - - 58.611 63.604 Other payables 4.403 2.390 20.507 11.506 Total non-current liabilities 1.621.977 1.592.425 4.892.325 5.149.600

EQUITYShare capital 18 1.033.198 1.033.198 1.033.198 1.033.198 Profit reserves 1.276.112 1.263.804 1.248.585 1.233.922 Valuation adjustment to equity - foreign exchange differences on capital (22.271) (22.271) (22.271) (22.271)

Total equity 2.287.039 2.274.731 2.259.512 2.244.849TOTAL DOS ATIVOS 5.403.169 4.923.235 10.266.410 10.081.570

TOTAL LIABILITIES AND EQUITY 5.403.169 4.923.235 10.266.410 10.081.570

Parent Company Parent Company

BALANCE SHEET AS AT MARCH 31, 2016

Consolidated Consolidated

3

ARTERIS S.A.

INCOME STATEMENT FOR THE PERIOD ENDED MARCH 31, 2016

(In thousands of Brazilian reais - R$, except basic and diluted earnings per share)

Note 31/03/2016 31/03/2015 31/03/2016 31/03/2015

NET OPERATING REVENUE 19 - - 877.267 918.929

COST OF SERVICES 20 - - (653.071) (656.711)

OTHER REVENUESEquity in the arnings (losseS) of subsidiaries 10 45.575 68.298 - -

GROSS PROFIT 45.575 68.298 224.196 262.218

OPERATING (EXPENSES) INCOME

General and administrative 20 (1.053) (2.192) (33.606) (42.055) Management Compensation 15 (1.257) (1.366) (5.033) (5.671) Tax expenses (57) (572) (111) (854) Amortization - - - - Other operating income, net 778 1.442 1.643 1.105

OPERATING PROFIT BEFORE FINANCE INCOME 43.986 65.610 187.089 214.743

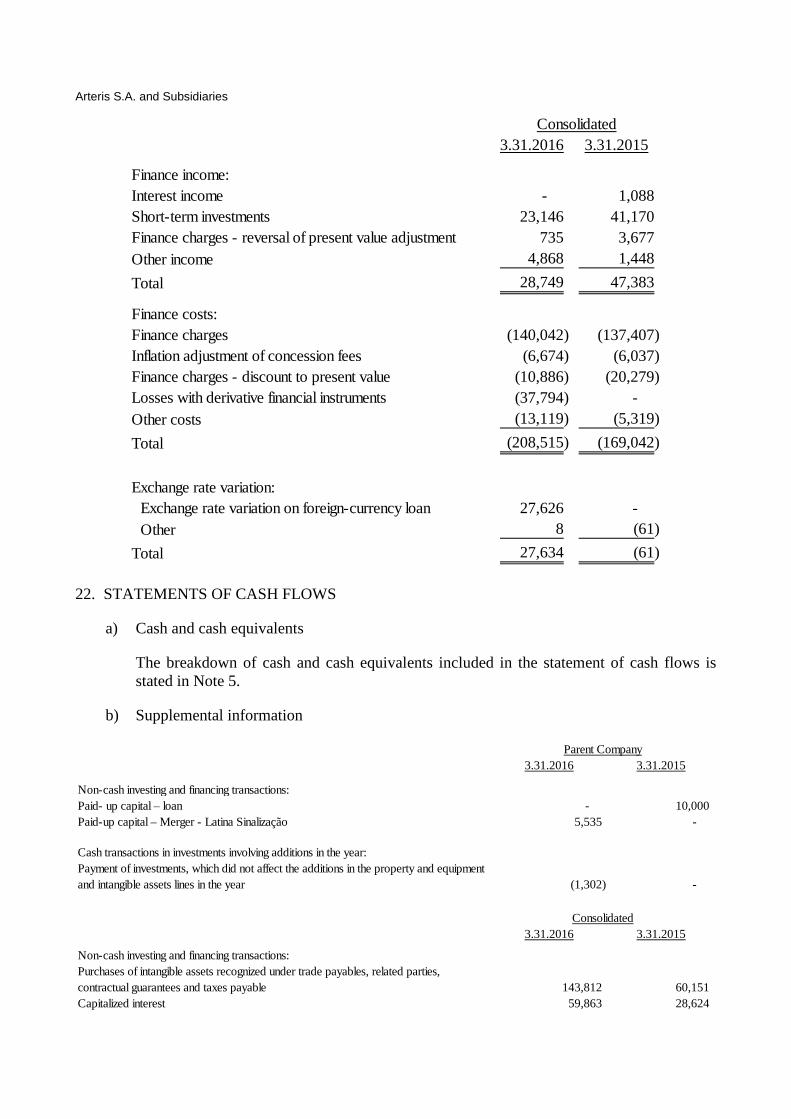

FINANCE INCOME (COSTS)

Financial Income 21 80.749 45.663 28.749 47.383

Financial Expenses 21 (140.061) (56.966) (208.515) (169.042) Net Exchange Variation 27.634 (9) 27.634 (61)

(31.678) (11.312) (152.132) (121.720)

OPERATING PROFIT BEFORE INCOME TAX ANDO SOCIAL CONTRIBUTION 12.308 54.298 34.957 93.023

INCOME TAX AND SOCIAL CONTRIBUTIONCurrent 23 - - (53.139) (46.302) Deferred 23 - - 31.684 10.011

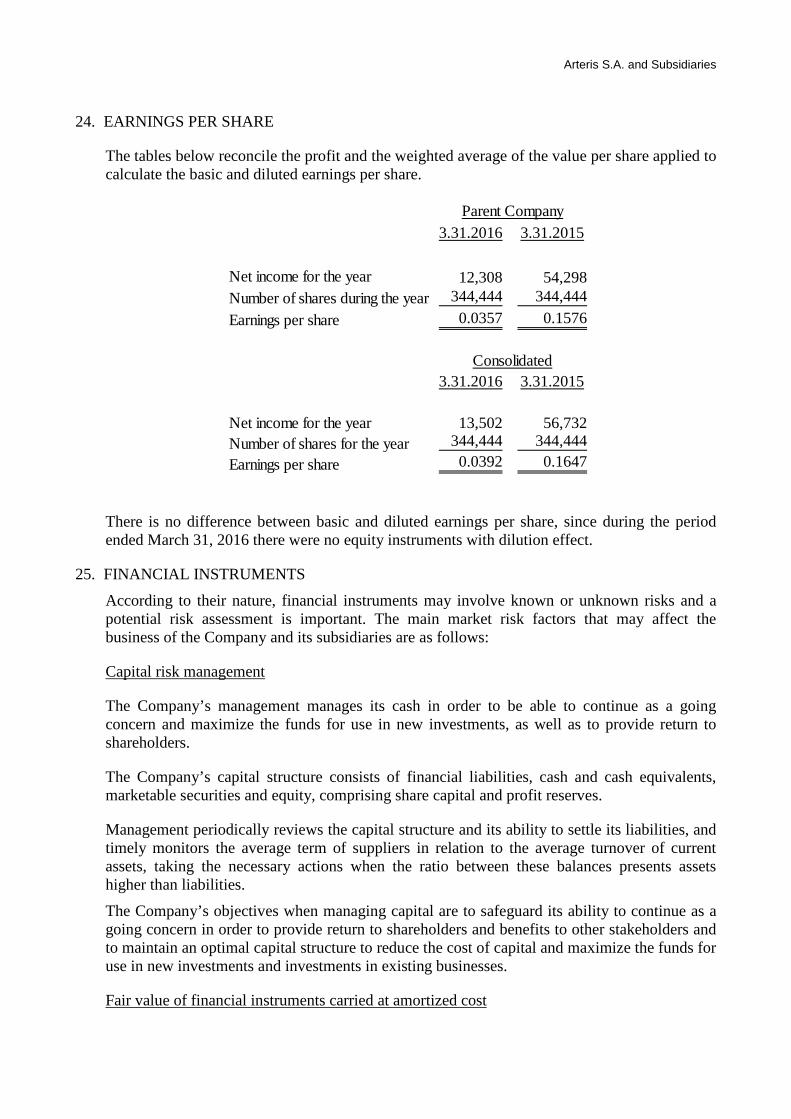

NET PROFIT FOR THE PERIOD 12.308 54.298 13.502 56.732

PROFIT ATTRIBUTABLE TOOwners of the Company 12.308 54.298 13.502 56.732

BASIC AND DILUTED EARNINGS PER SHARE - R$ 24 0,0357 0,1576 0,0392 0,1647

The accompanying notes are an integral part of these financial statements.

Parent Company Consolidated

4

ARTERIS S.A.

Individual statement of comprehensive income for theperiod ended March 31, 2016 and 2015(In thousands of Brazilian reais - R$)

31/03/2016 31/03/2015

Net income for the year from continuing operations 12.308 54.298 Other comprehensive income

Total comprehensive income for the period 12.308 54.298

PROFIT ATTRIBUTABLE TOShareholder controlling participation 12.308 54.298

The accompanying notes are an integral part of these financial statements.

5

ARTERIS S.A.

Consolidated statement of comprehensive income for theperiod ended March 31, 2016 and 2015(In thousands of Brazilian reais - R$)

31/03/2016 31/03/2015

Net income for the year from continuing operations 13.502 56.732 Other comprehensive income

Total comprehensive income for the period 13.502 56.732

PROFIT ATTRIBUTABLE TOShareholder controlling participation 13.502 56.732

The accompanying notes are an integral part of these financial statements.

6

ARTERIS S.A.

(In thousands of Brazilian reais)Ajuste

Valution Adjustmentsto capital - Patrimônio

Share Earnings foreign exchange Retained Consolidatedcapital Legal retention differences on capital earnings equity

BALANCES AT DECEMBER 31, 2014 772.417 101.425 975.225 101.405 (22.271) - 1.928.201

Capital Increase 101.405 (101.405) - Additional proposed dividends (101.405) (101.405)

Net income for the year - - - - 447.370 447.370 Destination if net income Legal Reserve - 22.369 - - (22.369) - Dividends Paid - - - - (79.222) (79.222) Propposed dividends - - - - (27.028) (27.028) Retained income - - 318.751 - (318.751) -

- BALANCES AT DECEMBER 31, 2015 1.033.198 130.798 1.133.006 - (22.271) - 2.274.731

Capital Increase - - - Additional proposed dividends - -

Net income for the year - - - - 12.308 12.308 Destination Of net income Legal Reserve - - - - - - - Propposed dividends - - - - - - - Retained income - - 12.308 - - (12.308) -

- BALANCES AT MARCH 31, 2016 1.033.198 130.798 1.145.314 - (22.271) - 2.287.039

INDIVIDUAL STATEMENT OF CHANGES IN EQUITY FOR THE PERIOD ENDED MARCH 31, 2016 and 2015

Profit reservesAdditional dividend

proposed

9

ARTERIS S.A.

STATEMENTS OF VALUE ADDED FOR THE PERIOD ENDEDMARCH 31, 2015 AND 2016(In thousands of Brazilian reais - R$)

31/03/2016 31/03/2015 31/03/2016 31/03/2015

REVENUESServices provided - - 621.200 599.007 Revenue from construction services - - 301.257 353.041 Other revenues 778 - 12.070 21.993

778 - 934.527 974.041

INPUTS PURCHASED FROM THIRD PARTIESCost of services provided - - (73.457) (74.688) Cost of construction services - - (301.257) (353.041) Materials, energy, outside services and other - - (21.498) (22.713) Cost of concession - - (25.388) (28.620) Cost of provision for maintenance in highways - - (74.209) (26.838) Other - - 11.974 (11.819)

- - (483.835) (517.719)

GROSS VALUE ADDED 778 - 450.692 456.322

DEPRECIATION AND AMORTIZATION (1.543) (535) (141.475) (124.126)

NET VALUE ADDED GENERATED (RETAINED) (765) (535) 309.217 332.196

VALUE ADDED RECEIVED THROUGH TRANSFEREquity in the earnings (losses) of subsidiaries 45.575 68.298 - - Finance income 80.749 45.663 28.749 47.383 Dividends received - 842 - 842 Capitalized interest - - 59.863 28.624 Other 27.636 645 27.637 120

153.960 115.448 116.249 76.969

TOTAL VALUE ADDED TO BE DISTRIBUTED 153.195 114.913 425.466 409.165

DISTRIBUTION OF VALUE ADDEDPersonnel and payroll charges: 222 379 40.160 43.796 Salaries 20 40 11.030 10.700 Benefits 38 39 3.191 2.893 Severance Pay Fund (FGTS)Taxes and contributions: 59 1.632 40.375 71.044 Federal (including tax on financial transactions - IOF) 1 14 13 2.454 State - - 31.449 28.656 Lenders: Interest 41.288 16.923 153.680 138.583 Capitalized interest BNDES - - 27.296 22.628 Capitalized interest Debentures - - 7.701 5.077 Rentals - - 2.524 5.403 Other 44.311 2.674 94.545 21.199 Shareholders: Interest 54.948 38.914 (24.866) - Capitalized interest - - 24.866 - Capital Integralization

12.308 54.298 13.502 56.732

153.195 114.913 425.466 409.165

The accompanying notes are an integral part of these financial statements.

Parent Company Consolidated

7

ARTERIS S.A.

(In thousands of Brazilian reais)Ajuste

Valution Adjustmentsto capital - Patrimônio

Share Earnings foreign exchange Retained Consolidatedcapital Legal retention differences on capital earnings equity

BALANCES AT DECEMBER 31, 2014 772.417 101.425 926.596 101.405 (22.271) - 1.879.572

Capital Increase 101.405 (101.405) - Additional proposed dividends (101.405) (101.405)

Net income for the year - - - - 456.860 456.860 Destination if net income Legal Reserve - 22.843 - - (22.843) - Dividends Paid - - - - (79.222) (79.222) Propposed dividends - - - - (27.028) (27.028) Retained income - - 327.767 - (327.767) -

- BALANCES AT DECEMBER 31, 2015 1.033.198 130.798 1.103.124 - (22.271) - 2.244.849

Capital Increase - - - Additional proposed dividends - -

Net income for the year - - - - 13.502 13.502 Destination Of net income Incorporation - - 1.161 1.161 Legal Reserve - - - - - - Transferencia de Reservas - - - - - - Propposed dividends - - - - - - Retained income - - 13.502 - (13.502) -

- BALANCES AT MARCH 31, 2016 1.033.198 130.798 1.117.787 - (22.271) - 2.259.512

Additional dividend proposed

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE PERIOD ENDED MARCH 31, 2015 and 2016

Profit reserves

8

ARTERIS S.A.

STATEMENT OF CASH FLOWS FOR THE PERIOD ENDED MARCH 31, 2016 And 2015(In thousands of Brazilian reais - R$)

RESUBMITTED

31/03/2016 31/03/2015 31/03/2016 31/03/2015

CASH FLOWS FROM OPERATING ACTIVITIESProfit for the year 12.308 54.298 13.502 56.732 Incorporation - - 1.161 - Adjustments to reconcile profit for the year to net cash (used in) generated by operating activities:

Depreciation and amortization 1.543 535 141.475 124.126 Write-off of permanent assets - - 12.092 13.008 Deferred income tax and social contribution - - (31.684) (10.011) Inflation adjustment and interest on concession fees - - 6.674 6.037 Income from restricted investments - - (7.334) (5.319) Interest and inflation adjustment on mutual (20.874) 38.913 (24.866) (919) Interest and inflation adjustment on borrowings (26.688) - 19.532 32.731 Interest and inflation adjustment on debentures 40.350 16.918 116.823 104.964 Interest and inflation adjustment on derivatives 37.794 - 37.794 - Finance costs / (income) from discount to present value - - 10.151 16.602 Recognition (reversal) of provision for civil, labor and tax risks (222) - 67 1.215 Recognition (reversal) of provision for maintenance in highways - - 74.209 18.397 Equity in the earnings (losses) of subsidiaries (45.575) (68.298) - -

Decrease (increase) in operating assets: Trade receivables - - (11.969) 12.858 Amounts due from related parties 3.414 (114.140) (260) - Inventories - - (1.822) 1.378 Prepaid expenses (291) 263 698 1.276 Taxes recoverable 3.341 14 (2.246) (5.339) Other receivables 718 355 (178) 2.769 Contractual guarantees - - 24 - Escrow deposits - (81) (1.087) (21.117) Other receivables - - (129) (8.200)

Increase (decrease) in operating liabilities: Trade payables (2.269) (1.676) (30.580) 13.709 Other Trade payables 188 - - - Contractual guarantees of suppliers - - (11.092) 833 Payroll and related taxes 1.578 (628) 2.372 (6.581) Taxes payable (3.691) (147) 30.514 34.394 Income tax and social contribution paid - - (32.664) (56.763) Deferred revenue - - - (346) Claims received - - (3.104) 779 Other payables 1.342 (114) 5.859 6.629 Concession fees - - (24) (53) Civil, labor and tax risks - - (950) (966) Payment of interest - - (196.195) (189.643)

Net cash (used in) generated by operating activities 2.966 (73.788) 116.763 143.180

CASH FLOWS FROM INVESTING ACTIVITIESPurchase of property and equipment (19) (624) (2.397) (4.698) Increase in intangible assets (3.094) (1.366) (331.669) (422.761) Restricted investments (23.301) - (84.349) (35.914) Amount redeemed from restricted investments - - 198.086 196.163 Additions to investments (304.000) (20.000) - - Interest on capital received 4.849 5.010 - - Dividends received 10.549 224.974 549 - Net cash generated by (used in) investing activities (315.016) 207.994 (219.780) (267.210)

CASH FLOWS FROM FINANCING ACTIVITIESBorrowings and financing:Funding 388.750 - 388.750 66.675 Payments - - (64.841) (49.030) Payment of interest (135) - - - Payment of debentures - interest - - (191.334) (191.333) Loan related parties - 60.000 - - Payment of principal - related parties - (82.274) - - Payment of interest - related parties (15.000) (5.837) - - Payment of dividends - - - - Payment of concession fees - - (19.330) (18.567) Net cash (used in) generated by financing activities 373.615 (28.111) 113.245 (192.255)

(DECREASE) INCREASE IN CASH AND CASH EQUIVALENTS 61.565 106.095 10.228 (316.285)

CASH AND CASH EQUIVALENTS AT THE BEGINNING OF THE YEAR 127.362 109.516 488.529 1.410.451

CASH AND CASH EQUIVALENTS AT THE END OF THE YEAR 188.927 215.611 498.757 1.094.166

The accompanying notes are an integral part of these financial statements.

Parent Company Consolidated

8

ARTERIS S.A.

STATEMENT OF CASH FLOWS FOR THE PERIOD ENDED MARCH 31, 2016 And 2015(In thousands of Brazilian reais - R$)

Previously issued Adjust Resubmitted31/03/2015 31/03/2015

CASH FLOWS FROM OPERATING ACTIVITIESProfit for the year 56.732 - 56.732 Incorporation - - Adjustments to reconcile profit for the year to net cash (used in) generated by operating activities:

Depreciation and amortization 124.126 - 124.126 Write-off of permanent assets 13.008 - 13.008 Deferred income tax and social contribution (10.011) - (10.011) Inflation adjustment and interest on concession fees 6.037 - 6.037 Income from restricted investments (5.319) - (5.319) Interest and inflation adjustment on mutual (919) - (919) Interest and inflation adjustment on borrowings 32.731 - 32.731 Interest and inflation adjustment on debentures 104.964 - 104.964 Interest and inflation adjustment on derivatives 16.602 - 16.602 Finance costs / (income) from discount to present value 1.215 - 1.215 Recognition (reversal) of provision for civil, labor and tax risks 18.397 - 18.397 Recognition (reversal) of provision for maintenance in highways - - - Participação dos acionistas não controladores

Decrease (increase) in operating assets: 12.858 - 12.858 Trade receivables - - - Amounts due from related parties 1.378 - 1.378 Inventories 1.276 - 1.276 Prepaid expenses (5.339) - (5.339) Adiantamentos para novos projetos 2.769 - 2.769 Other receivables - - - Contractual guarantees (21.117) - (21.117) Escrow deposits (8.200) - (8.200) Other receivables

Increase (decrease) in operating liabilities: 13.709 - 13.709 Trade payables - - - Other Trade payables 833 - 833 Contractual guarantees of suppliers (6.581) - (6.581) Payroll and related taxes 34.394 - 34.394 Taxes payable (56.763) - (56.763) Income tax and social contribution paid (346) - (346) Contas a pagar - partes relacionadas 779 - 779 Claims received 6.629 - 6.629 Other payables (53) - (53) Concession fees (966) - (966) Outros passivos (48.072) (141.571) (189.643) Payment of interest 284.751 (141.571) 143.180 Net cash (used in) generated by operating activities

CASH FLOWS FROM INVESTING ACTIVITIES (4.698) - (4.698) Purchase of property and equipment (422.761) - (422.761) Adiantamentos para novos projetos (35.914) - (35.914) Restricted investments 196.163 - 196.163 Amount redeemed from restricted investments - - - Recebimento de dividendos - exercícios anteriores - - - Interest on capital received - - - Dividends received (267.210) - (267.210) Net cash generated by (used in) investing activities

CASH FLOWS FROM FINANCING ACTIVITIESBorrowings and financing: 66.675 - 66.675 Funding (49.030) - (49.030) Payments (185) 185 - Payment of interest - - - Debentures: (191.333) - (191.333) Payment of debentures - interest (141.386) 141.386 - Pagamentos de debêntures - juros - - - Loan related parties - - - Payment of principal - related parties - - - Payment of interest - related parties - - - Recebimento de Juros - empresas ligadas - - - Distribuição de juros s/ capital próprio - - - Dividendos propostos (18.567) - (18.567) Payment of dividends - - - Payment of concession fees - - - Aumento de Capital (333.826) 141.571 (192.255) Net cash (used in) generated by financing activities

(316.285) - (316.285) (DECREASE) INCREASE IN CASH AND CASH EQUIVALENTS

1.410.451 - 1.410.451 CASH AND CASH EQUIVALENTS AT THE BEGINNING OF THE YEAR

1.094.166 - 1.094.166 CASH AND CASH EQUIVALENTS AT THE END OF THE YEAR

The accompanying notes are an integral part of these financial statements.

Arteris S.A. and Subsidiaries

ARTERIS S.A. AND SUBSIDIARIES

NOTES TO THE INTERIM FINANCIAL INFORMATION FOR THE PERIOD ENDED MARCH 31, 2016 (Amounts in thousands of Brazilian reais - R$, unless otherwise stated)

1. OPERATIONS

Arteris S.A. (“Company”) has its registered office and principal place of business at Avenida Presidente Juscelino Kubitschek, 1.455 - 9º andar, in the city of São Paulo, state of São Paulo, Brazil. The Company’s individual and consolidated interim financial information for the period ended March 31, 2016 includes the Company and its subsidiaries (collectively referred to as “Arteris Group” and individually as “Group entity”). The Company was established on November 9, 1998.

Arteris, through its subsidiaries, mainly state concessionaires, has a solid cash position, robust capital structure and special funding sources to implement its business plan.

The Company allocates the resources generated by operating activities to meet its working capital needs. Additionally, it accesses the capital markets and raises loans and financing with Brazil’s major financial institutions and development agencies to complete its cash needs.

Cash generation added to the Company’s creditworthiness, besides the funds raised through long-term financing lines is appropriate to comply with its short-term liabilities recorded under current liabilities, which includes the financing amortization and to maintain an appropriate leverage level for long-term liabilities.

Once its subsidiaries’ revenue projections in the medium and long terms indicate upward and sustainable levels through the toll traffic involvement and annual tariff increases, at the same time the work plan is supported by the loan with the Brazilian Development Bank (BNDES) and funds raised in the capital markets by means of the issue of infrastructure debentures or other securities in its concessionaires and through the Company itself, Management believes that the Company and its subsidiaries have conditions to honor their current short and medium term commitments.

On March 31, 2016, Latina Sinalização Ltda. (“Latina Sinalização”) was merged into Latina Manutenção de Rodovias Ltda. (“Latina Manutenção”), both of them controlled by Arteris. The merger of Latina Sinalização into Latina Manutenção is part of the Group’s corporate restructuring, which aims at improving the organization of its activities, increasing economic efficiency and synergy gains, reducing operating and financial costs and simplifying the corporate structure.

On April 30, 2015, the controlling shareholder Partícipes en Brasil S.L. informed its intention to hold a Public Tender Offer for the Acquisition of Arteris S.A. Shares with a view to cancelling the Company’s registration as a category A publicly-held company and delisting it from the Novo Mercado.

On March 31, 2016, the Company complied with all the requirements before the competent regulatory agencies.

There were no changes in operations in the quarter ended March 31, 2016, in relation to the year ended December 31, 2015.

Arteris S.A. and Subsidiaries

The parent company and consolidated financial information was approved by the Board of Executive Officers and authorized for issue on May 11, 2016.

2. CONCESSIONS

In conformity with its corporate purposes, as at March 31, 2016, the Company holds interests in highway concessionaires in the State of São Paulo and in federal highway concessionaires.

In comparison with the December 31, 2015, no changes in the interests in concessions were registered in the quarter ended March 31, 2016, except for:

State concessionaires

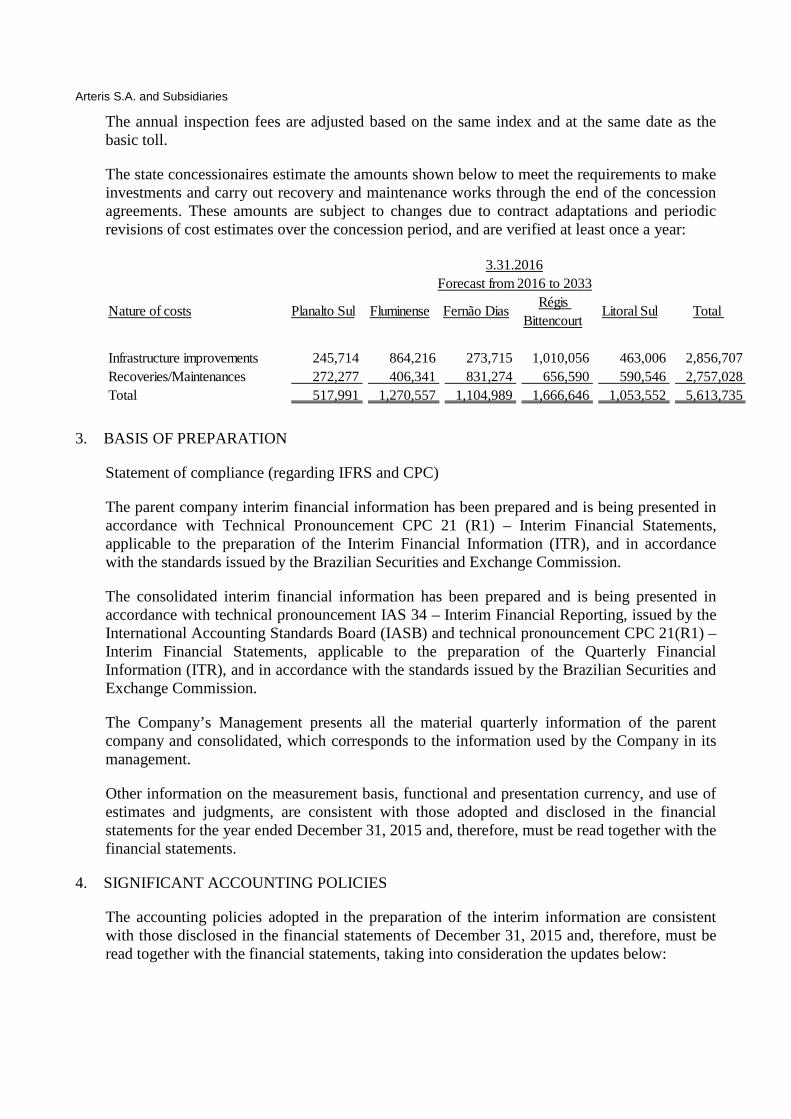

The state concessionaires estimate the amounts shown below to meet the requirements to make investments and carry out recovery and maintenance works through the end of the concession agreements. These amounts are subject to changes due to contract adaptations and periodic revisions of cost estimates over the concession period, and are verified at least once a year:

Federal concessionaires

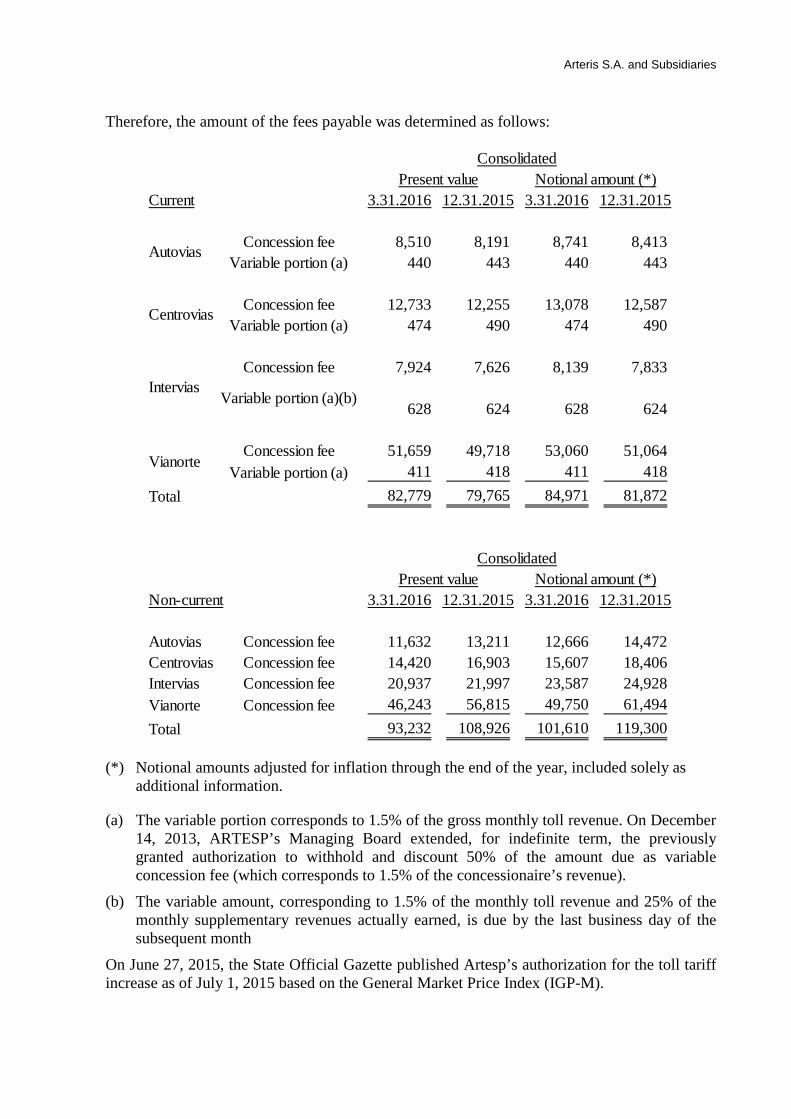

The main commitment made by the federal concessionaires as a result of the concession agreements is the payment to the ANTT of the inspection fees intended to cover expenses on inspecting the concession over the entire period. The nominal amounts of the inspection fees are as follows:

Autovias Centrovias Intervias Vianorte Forecast

from Forecast

from Forecast

from Forecast

from 2016 a 2019 2016 a 2019 2016 a 2028 2016 a 2018

Infrastructure improvements 98,360 1,943 381,530 1,765 483,598 Special upkeep work 189,280 77,702 190,985 43,915 501,882

287,640 79,645 572,515 45,680 985,480

Nature of costs

3.31.2016

Total

Concessionaire Annual amountAmount in the

concession period

Planalto Sul 1,846 31,074 Fluminense 2,665 44,861 Fernão Dias 7,916 133,253 Régis Bittencourt 8,436 142,006 Litoral Sul 6,424 108,137

27,287 459,331

Arteris S.A. and Subsidiaries

The annual inspection fees are adjusted based on the same index and at the same date as the basic toll.

The state concessionaires estimate the amounts shown below to meet the requirements to make investments and carry out recovery and maintenance works through the end of the concession agreements. These amounts are subject to changes due to contract adaptations and periodic revisions of cost estimates over the concession period, and are verified at least once a year:

3. BASIS OF PREPARATION

Statement of compliance (regarding IFRS and CPC)

The parent company interim financial information has been prepared and is being presented in accordance with Technical Pronouncement CPC 21 (R1) – Interim Financial Statements, applicable to the preparation of the Interim Financial Information (ITR), and in accordance with the standards issued by the Brazilian Securities and Exchange Commission.

The consolidated interim financial information has been prepared and is being presented in accordance with technical pronouncement IAS 34 – Interim Financial Reporting, issued by the International Accounting Standards Board (IASB) and technical pronouncement CPC 21(R1) – Interim Financial Statements, applicable to the preparation of the Quarterly Financial Information (ITR), and in accordance with the standards issued by the Brazilian Securities and Exchange Commission.

The Company’s Management presents all the material quarterly information of the parent company and consolidated, which corresponds to the information used by the Company in its management.

Other information on the measurement basis, functional and presentation currency, and use of estimates and judgments, are consistent with those adopted and disclosed in the financial statements for the year ended December 31, 2015 and, therefore, must be read together with the financial statements.

4. SIGNIFICANT ACCOUNTING POLICIES

The accounting policies adopted in the preparation of the interim information are consistent with those disclosed in the financial statements of December 31, 2015 and, therefore, must be read together with the financial statements, taking into consideration the updates below:

Nature of costs Planalto Sul Fluminense Fernão Dias Régis Bittencourt

Litoral Sul Total

Infrastructure improvements 245,714 864,216 273,715 1,010,056 463,006 2,856,707 Recoveries/Maintenances 272,277 406,341 831,274 656,590 590,546 2,757,028 Total 517,991 1,270,557 1,104,989 1,666,646 1,053,552 5,613,735

Forecast from 2016 to 20333.31.2016

Arteris S.A. and Subsidiaries

Derivative financial instruments

Operations with derivative financial instruments, contracted by the Company, are basically swap operations that aim exclusively to hedge against foreign exchange risks associated with balance sheet items. The Company does not make use of Hedge Accounting for derivative financial instruments.

Derivative financial instruments are measured at fair value and the variations are recorded in profit or loss for the period. The fair value of derivative financial instruments is calculated by the Company’s treasury department, based on information related to each operation contracted and on the corresponding market information on the financial statements’ reporting dates, such as interest rates and exchange rates. This information is compared with the positions informed by the trading desks of each financial institution involved and, if there is no significant difference, the position informed by the financial institution is used to define the fair value.

The fair value of financial instruments actively traded in organized financial markets is established based on the acquisition prices quoted in the market, on the conclusion of trading at the balance sheet date, without deducting transaction costs. The fair value of financial instruments for which there is no active market is established based on appraisal techniques. These techniques may include the use of recent market transactions (with exemption of interests); reference to the current fair value of similar instruments; discounted cash flow analysis or other appraisal models.

Assets and liabilities adjusted to present value

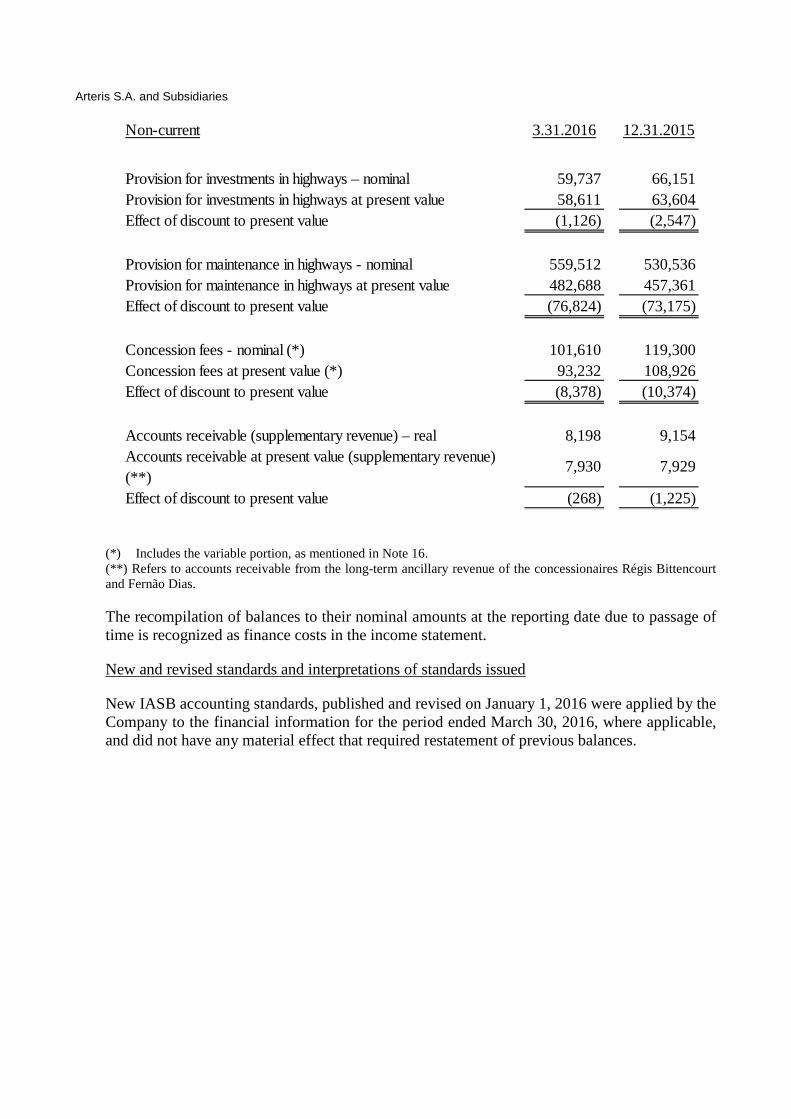

The nominal balances and the present value of current and non-current assets and liabilities, at the end of the reporting period, are as follows:

Current

Provision for investments in highways – nominal 66,134 61,333 Provision for investments in highways at present value 61,516 56,711 Effect of discount to present value (4,618) (4,622)

Provision for maintenance in highways - nominal 224,063 178,476 Provision for maintenance in highways at present value 202,897 173,524 Effect of discount to present value (21,166) (4,952)

Concession fees - nominal (*) 84,971 81,872 Concession fees at present value (*) 82,779 79,765 Effect of discount to present value (2,192) (2,107)

Accounts receivable (supplementary revenue) – real 14,689 - Accounts receivable at present value (supplementary revenue) (**)

13,981 -

Effect of discount to present value (708) -

3.31.2016 12.31.2015

Arteris S.A. and Subsidiaries

(*) Includes the variable portion, as mentioned in Note 16. (**) Refers to accounts receivable from the long-term ancillary revenue of the concessionaires Régis Bittencourt and Fernão Dias.

The recompilation of balances to their nominal amounts at the reporting date due to passage of time is recognized as finance costs in the income statement.

New and revised standards and interpretations of standards issued

New IASB accounting standards, published and revised on January 1, 2016 were applied by the Company to the financial information for the period ended March 30, 2016, where applicable, and did not have any material effect that required restatement of previous balances.

Provision for investments in highways – nominal 59,737 66,151 Provision for investments in highways at present value 58,611 63,604 Effect of discount to present value (1,126) (2,547)

Provision for maintenance in highways - nominal 559,512 530,536 Provision for maintenance in highways at present value 482,688 457,361 Effect of discount to present value (76,824) (73,175)

Concession fees - nominal (*) 101,610 119,300 Concession fees at present value (*) 93,232 108,926 Effect of discount to present value (8,378) (10,374)

Accounts receivable (supplementary revenue) – real 8,198 9,154 Accounts receivable at present value (supplementary revenue) (**)

7,930 7,929

Effect of discount to present value (268) (1,225)

Non-current 3.31.2016 12.31.2015

Arteris S.A. and Subsidiaries

5. RESTATEMENT OF THE STATEMENTS OF CASH FLOWS

The Company’s Management identified a reclassification in the interest amounts disclosed in the statements of cash flows for the period ended March 31, 2015, as shown below. Accordingly, the Company is restating these statements of cash flows for March 31, 2015.

Previously issued Adjustment Notes Restated31.03.2015 31.03.2015

CASH FLOWS FROM OPERATING ACTIVITIESProfit for the year 56,732 - 56,732

Depreciation and amortization 124,126 - 124,126 Write-off of permanent assets 13,008 - 13,008 Deferred income tax and social contribution (10,011) - (10,011) Inflation adjustment and interest on concession fees 6,037 - 6,037 Income from restricted investments (5,319) - (5,319) Interest and inflation adjustment on borrowings 31,812 - 31,812 Interest and inflation adjustment on debentures 104,964 - 104,964 Finance cost / (income) from discount to present value 16,602 - 16,602 Recognition (reversal) of provision for civil, labor and tax risks 1,215 - 1,215 Recognition (reversal) of provision for maintenance 18,397 - 18,397

Consolidated

Adjustments to reconcile profit for the year to net cash (used in) generated by operating activities:

Decrease (increase) in operating assets: Trade receivables 12,858 - 12,858 Inventories 1,378 - 1,378 Prepaid expenses 1,276 - 1,276 Taxes recoverable (5,339) - (5,339) Other receivables 2,769 - 2,769 Escrow deposits (21,117) - (21,117) Other receivables (8,200) - (8,200)

Increase (decrease) in operating liabilities: Trade payables 13,709 - 13,709 Contractual guarantees of suppliers 833 - 833 Payroll and related taxes (6,581) - (6,581) Taxes payable 34,394 - 34,394 Income tax and social contribution paid (56,763) - (56,763) Deferred revenue (346) - (346) Claims received 779 - 779 Other payables 6,629 - 6,629 Concession fees (53) - (53) Civil, labor and tax risks (966) - (966) Payment of interest (48,072) (141,571) (a) (189,643) Net cash (used in) generated by operating activities 284,751 (141,571) 143,180

Arteris S.A. and Subsidiaries

(a) According to the recommendation of CPC 03, the Company reclassified interest paid from financing activity to operating activity.

6. CASH AND CASH EQUIVALENTS

Broken down as follows:

(*) Represented by highly liquid short-term investments, with insignificant risk of change in value and maturity of less than 90 days from the acquisition date, as follows:

CASH FLOWS FROM INVESTING ACTIVITIESPurchase of property and equipment (4,698) - (4,698) Acquisition of intangible assets (422,761) - (422,761) Restricted investment (35,914) - (35,914) Amount redeemed from restricted investments 196,163 - 196,163 Net cash used in investing activities (267,210) - (267,210)

CASH FLOWS FROM FINANCING ACTIVITIESBorrowings and financing: Funding 66,675 - 66,675 Payments (49,030) - (49,030) Payment of interest (185) 185 (a) - Debentures: - Issue of debentures - - - Payment of debentures - principal (191,333) - (191,333) Payment of debentures - interest (141,386) 141,386 (a) - Payment of concession fees (18,567) - (18,567) Payment of dividends - - - Loans - related parties - - - Other payment of interest - - - Net cash (used in) generated by financing activities (333,826) 141,571 (192,255)

(DECREASE) INCREASE IN CASH AND CASH EQUIVALENTS (316,285) - (316,285)

CASH AND CASH EQUIVALENTS AT THE BEGINNING OF THE YEAR 1,410,451 - 1,410,451

CASH AND CASH EQUIVALENTS AT THE END OF THE YEAR 1,094,166 - 1,094,166

3.31.2016 12.31.2015 3.31.2016 12.31.2015

Cash and banks 2,103 140 15,134 16,105 Short-term investments (*) 186,824 127,222 483,623 472,424 Total 188,927 127,362 498,757 488,529

Parent Company Consolidated

3.31.2016 12.31.2015 3.31.2016 12.31.2015

Bank Certificates of Deposit (CDB) - - - 7,202 Debentures under repurchase agreements - - - 12,614 Investment funds 186,824 127,222 483,623 452,608 Total 186,824 127,222 483,623 472,424

Parent Company Consolidated

Arteris S.A. and Subsidiaries

The financial investments represent the amounts invested in exclusive funds, with daily liquidity and bearing 100.52% of CDI interest rate on average, with characteristics of floating investments in federal government bonds, CDBs, financial bills and repo operations backed by debentures of large-sized financial institutions with low credit risk.

7. TRADE RECEIVABLES

Broken down as follows:

(*) According to Note 25.c.

The Management of the Company and its subsidiaries did not identify the need to recognize a provision for loss on receivables as at March 31, 2016. The average maturity is 30 days, except for ancillary revenues, which have a receivables longer period, according to the negotiation of each agreement referring to the use of concessionaires’ right of way.

Electronic toll(*) 142,041 133,938 Toll tickets 312 1,775 Toll cards 5,275 3,882 Supplementary revenues 16,594 13,535 Other revenues receivable 1,612 -

165,834 153,130 8,293 8,164

Consolidated3.31.2016 12.31.2015

Current Non-current

Current Non-current

- -

7,930 363

- - 7,929 235

- -

Arteris S.A. and Subsidiaries

8. DEFERRED INCOME TAX AND SOCIAL CONTRIBUTION

Broken down as follows:

Noncurrent assets 3.31.2016 12.31.2015

Bases of deferred asset:Tax loss (a) 347,145 310,886 Accrued profit sharing 19,472 14,880 Civil, labor and tax risks(b) 15,337 13,485 Merged concession (c) (16,945) (17,387)Other provisions 2,458 1,759 Provision for highway maintenance 616,393 531,755 Adjustments to financial charges 40,836 28,396 Deferred pre-operating expenses (Federal) 41,711 45,272

Adjustments related to changes in accounting practices - adoption of Law 12,973/14 (d)

Differences in intangible assets, deferred charges and property and equipment, net - assets

85,382 85,381

Amortization of adjustments - changes in accounting practices - assets (35,991) (34,636)Differences of intangible assets, deferred charges and property and equipment, net - liabilities

(298,948) (239,416)

Amortization of adjustments - changes in accounting practices - liabilities 20,932 13,542 Reversal of interest capitalization 1,339 761

Taxable base 839,121 754,678 Combined statutory rate 34% 34%Total deferred income tax and social contribution 285,302 256,591

Consolidated

Non-current liabilities 3.31.2016 12.31.2015

Bases of deferred liability:Tax loss (a) (43,653) (51,544)Accrued profit sharing (2,908) (5,028)Civil, tax and labor risks (b) (1,051) (3,565)Other provisions (363) (1,599)Provision for highway maintenance (69,192) (99,130)Adjustments in financial charges (3,094) (10,688)

Adjustments related to changes in accounting practices - adoption of Law 12,973/14 (e)

Differences in intangible assets, deferred charges and property and equipment, net 318,245 377,843 Amortization of adjustments - changes in accounting practices (21,899) (20,764)Reversal of interest capitalization (34) (612)

Taxable base 176,051 184,913 Combined statutory rate 34% 34%Total deferred income tax and social contribution 59,857 62,870

Consolidated

Arteris S.A. and Subsidiaries

(a) Refers to tax losses and social contribution tax loss carryforwards, whose possibility of offsetting tax credit is supported by future taxable income projections of concessionaires Planalto Sul, Fluminense, Fernão Dias, Régis Bittencourt, Litoral Sul and Latina Manutenção.

(b) Refer to provisions for civil, labor and tax risks related to unsettled claims.

(c) Credit arising from the amortization of the merged concession, recorded up to the base date of the spin-off of OHL do Brasil Participações em Infraestrutura Ltda. – “OHL Participações” in June 2006 and, until then, controlled in “part B” of that company's taxable income book (LALUR). With the merger of the interest of OHL Participações; the Company recognized this credit that, pursuant to tax legislation, will be amortized at the rate of 20% per annum, for tax purposes, and for the term of the concession, for accounting purposes.

(d) On December 31, 2014, the Company’s Management opted for the early adoption of Law 12,973/14 as expected for the fiscal year of 2014, in the following subsidiaries: Autovias and Centrovias. Other subsidiaries applied said law when it took effect as of January 1, 2015. Therefore, the Company’s subsidiaries froze the balances related to changes in accounting practices and started amortizing the residual balance of adjustments referring to the changes in the accounting practices until the end of the concession period.

The Company has tax credits that are not being recognized given that it is a holding company that does not record taxable result.

The future business forecasts of the Company and its subsidiaries and their income projections are prepared by their Management.

The expectation of recovery of all credits and the actual payment of deferred tax debits, indicated by taxable income projections, are as follows:

Period ended on:

Non-current asset2016 48,138 2017 47,050 2018 51,656 2019 16,638 2020 38,017 After 2021 83,803

285,302

Arteris S.A. and Subsidiaries

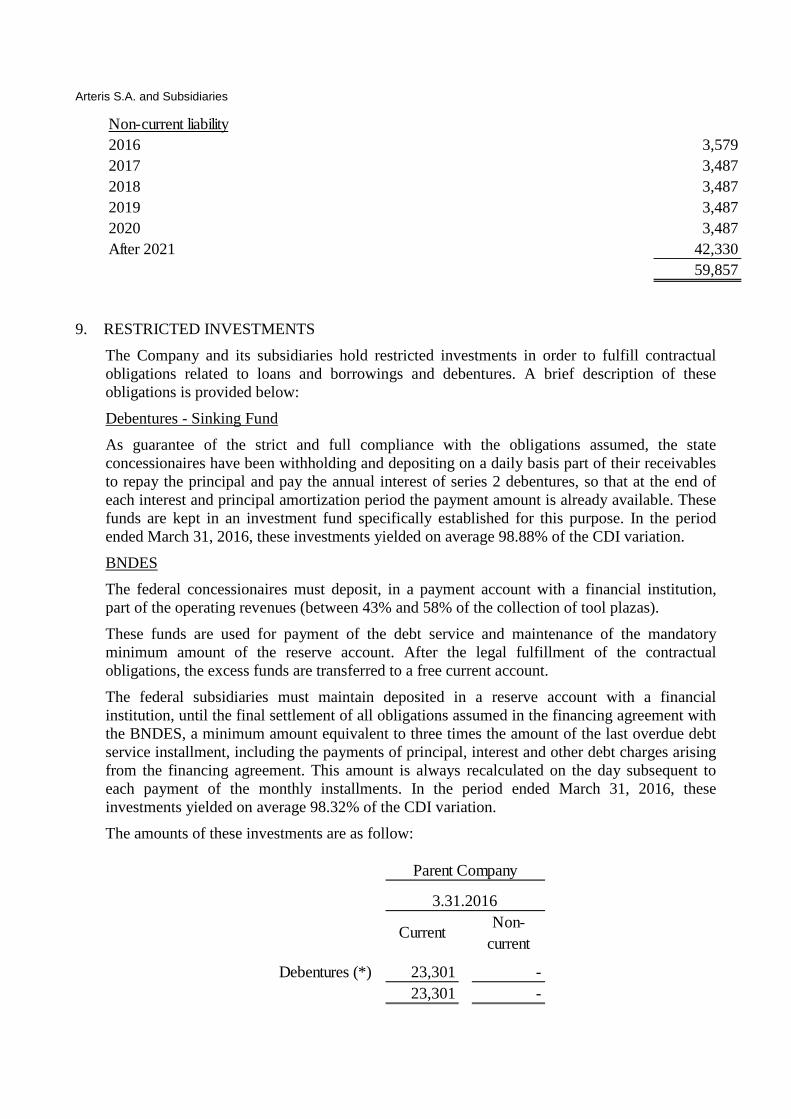

9. RESTRICTED INVESTMENTS

The Company and its subsidiaries hold restricted investments in order to fulfill contractual obligations related to loans and borrowings and debentures. A brief description of these obligations is provided below:

Debentures - Sinking Fund

As guarantee of the strict and full compliance with the obligations assumed, the state concessionaires have been withholding and depositing on a daily basis part of their receivables to repay the principal and pay the annual interest of series 2 debentures, so that at the end of each interest and principal amortization period the payment amount is already available. These funds are kept in an investment fund specifically established for this purpose. In the period ended March 31, 2016, these investments yielded on average 98.88% of the CDI variation.

BNDES

The federal concessionaires must deposit, in a payment account with a financial institution, part of the operating revenues (between 43% and 58% of the collection of tool plazas).

These funds are used for payment of the debt service and maintenance of the mandatory minimum amount of the reserve account. After the legal fulfillment of the contractual obligations, the excess funds are transferred to a free current account.

The federal subsidiaries must maintain deposited in a reserve account with a financial institution, until the final settlement of all obligations assumed in the financing agreement with the BNDES, a minimum amount equivalent to three times the amount of the last overdue debt service installment, including the payments of principal, interest and other debt charges arising from the financing agreement. This amount is always recalculated on the day subsequent to each payment of the monthly installments. In the period ended March 31, 2016, these investments yielded on average 98.32% of the CDI variation.

The amounts of these investments are as follow:

Non-current liability2016 3,579 2017 3,487 2018 3,487 2019 3,487 2020 3,487 After 2021 42,330

59,857

Debentures (*) 23,301 - 23,301 -

3.31.2016

Current Non-current

Parent Company

Arteris S.A. and Subsidiaries

(*) Refers to the value retained by the bank on March 31, 2016 for the payment of interest on the 2nd issue debentures. Payment took place on April 1, 2016.

10. INVESTMENTS IN SUBSIDIARIES AND ASSOCIATES

As at March 31, 2016, the Company held control, directly or indirectly, of the capital stock of the following subsidiaries:

Debentures 40,646 - 154,171 - BNDES - 90,609 - 85,872

40,646 90,609 154,171 85,872

Consolidated

3.31.2016 12.31.2015Non-

currentNon-

currentCurrent Current

Indirect Direct Interest

Autovias - 100%Centrovias - 100%Intervias 49% 51%Vianorte - 100%Planalto Sul - 100%Fluminense - 100%Fernão Dias - 100%Régis Bittencourt - 100%

Litoral Sul - 100%

Latina Manutenção (a) - 100%Arteris Participações (c) - 100%

Subsidiary 3.31.2016

Arteris S.A. and Subsidiaries

Investments in subsidiaries are as follows:

Changes in investments in the parent company for the period ended March 31, 2016 are as follows:

Autovias 125,040,451 100% 186,389 611,458 425,069 80,479 5,296 Centrovias 101,483,834 100% 156,976 636,813 479,837 84,224 29,229 Intervias 2,219,666 51% 183,547 1,389,172 1,205,625 98,485 24,500 Vianorte 1,132,038 100% 175,034 459,795 284,761 71,906 19,084 Planalto Sul 344,677,249 100% 256,565 1,038,861 782,296 69,315 (10,359)Fluminense 249,821,758 100% 429,045 1,578,470 1,149,425 125,124 (3,962)Fernão Dias 542,639,799 100% 389,335 1,714,895 1,325,560 81,133 (22,587)Régis Bittencourt 270,196,214 100% 656,910 2,222,251 1,565,341 144,161 1,275 Litoral Sul 385,905,537 100% 443,953 1,835,555 1,391,602 122,440 (8,512)Latina Manutenção (*) 7,648,344 100% 47,978 111,304 63,326 72,510 10,870 Arteris Participações 63,593 100% - 91,739 91,739 - 11,587 (*) Quotas.

3.31.2016Common

sharesEquity interest (%) Equity Total assets Total liabilities Net revenue Profit / (Loss)

12.31.2015 3.31.2016

Autovias 183,343 - - (2,250) 5,296 186,389 Centrovias 129,334 - - (1,587) 29,229 156,976 Intervias 82,123 - - (1,009) 12,496 93,610 Vianorte 155,950 - - - 19,084 175,034 Planalto Sul 221,924 - 45,000 - (10,359) 256,565 Fluminense 363,007 - 70,000 - (3,962) 429,045 Fernão Dias 383,922 - 28,000 - (22,587) 389,335 Régis Bittencourt 562,635 - 93,000 - 1,275 656,910 Litoral Sul 384,465 - 68,000 - (8,512) 443,953 Latina Manutenção 30,878 6,230 - - 10,870 47,978 Latina Sinalização 15,072 (6,230) - (10,000) 1,158 - Arteris Participações 79,492 - - - - 79,492 Serviço e Tecnologia de Pagamentos S.A. 1,034 - - - 1,034 Other investments 19 - - - - 19 Total 2,593,198 - 304,000 (14,846) 33,988 2,916,340

Balance at

Parent Company

Capital contribution

Interest on equity/dividends

Equity in the earnings (losses) of subsidiaries in the

Balance at

Arteris S.A. and Subsidiaries

11. PROPERTY AND EQUIPMENT

Changes in property and equipment are as follows:

Balance at 12.31.2015 3,418 2,825 4,587 5,270 586 16,686 Additions - - - 19 - 19 Disposals/write-offs (3) - - - - (3)Balance at 3.31.2016 3,415 2,825 4,587 5,289 586 16,702

Accumulated depreciation

Balance at 12.31.2015 (1,905) (1,320) (1,901) (1,939) - (7,065)Depreciation (70) (72) (55) (258) - (454)Disposals/write-offs 3 - - - - 3 Balance at 3.31.2016 (1,975) (1,392) (1,956) (2,197) - (7,516)

Property and equipment, netBalance at 12.31.2015 1,513 1,505 2,686 3,331 586 9,621 Balance at 3.31.2016 1,440 1,433 2,631 3,092 586 9,186 Depreciation rates - % 10 4 55.5 10

Parent Company

Cost of property and equipment Furniture, fixtures and facilities

Facilities, buildings and premises

Leasehold improvements

Other property and equipment

Land Total

Arteris S.A. and Subsidiaries

(a) Refers to the transfer of property and equipment to intangible assets

Furniture, fixtures and facilities

Computers and peripherals Vehicles

Facilities, buildings and premises Land

Machinery and equipment

Other property and equipment

Property and equipment in

progressTotal

Balance at 12.31.2015 19,844 9,430 20,914 23,943 586 40,486 5,367 1,107 121,677 Additions 494 162 312 21 - 1,061 19 266 2,335 Transfers/Reclassifications (a) - 13 210 - - 18 - - 241 Disposals/write-offs (39) (18) (46) - - (71) - - (174)Balance at 3.31.2016 20,299 9,587 21,390 23,964 586 41,494 5,386 1,373 124,079

Accumulated depreciation

Balance at 12.31.2015 (11,901) (6,556) (14,758) (6,265) - (17,769) (2,014) - (59,263)Depreciation (465) (207) (418) (804) - (1,018) (262) - (3,174)Transfers/Reclassifications (a) 1 - (64) - - (110) - - (173)Disposals/write-offs 28 12 34 - - 38 - - 112 Balance at 3.31.2016 (12,337) (6,751) (15,206) (7,069) - (18,859) (2,276) - (62,498)

Property and equipment, netBalance at 12.31.2015 7,943 2,874 6,156 17,678 586 22,717 3,353 1,107 62,414Balance at 3.31.2016 7,962 2,836 6,184 16,895 586 22,635 3,110 1,373 61,581Depreciation rates - % 9 20 20 13 - 12 16.67

Cost of property and equipment

Consolidated

Arteris S.A. and Subsidiaries

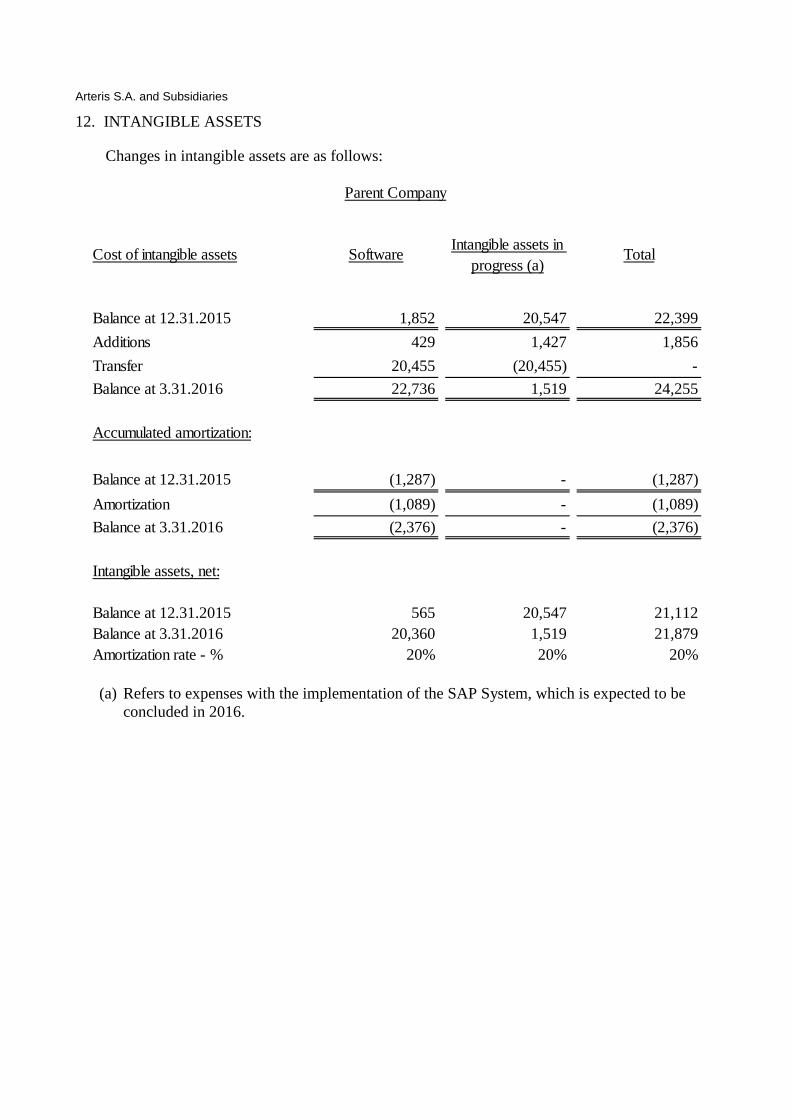

12. INTANGIBLE ASSETS

Changes in intangible assets are as follows:

(a) Refers to expenses with the implementation of the SAP System, which is expected to be concluded in 2016.

Balance at 12.31.2015 1,852 20,547 22,399 Additions 429 1,427 1,856 Transfer 20,455 (20,455) - Balance at 3.31.2016 22,736 1,519 24,255

Accumulated amortization:

Balance at 12.31.2015 (1,287) - (1,287)Amortization (1,089) - (1,089)Balance at 3.31.2016 (2,376) - (2,376)

Intangible assets, net:

Balance at 12.31.2015 565 20,547 21,112 Balance at 3.31.2016 20,360 1,519 21,879 Amortization rate - % 20% 20% 20%

Parent Company

Cost of intangible assets Software Intangible assets in progress (a)

Total

Arteris S.A. and Subsidiaries

(a) Refer to projects and services carried out on the highway, such as paving, duplication, side roads, shoulders, work yards, special structure works, ground leveling, implementing a system for collecting tolls and monitoring traffic, signaling and other such services, amortized on a straight line basis, until the final term of the concession.

(b) Refers to the amount assumed for the operation of the highway system adjusted to present value. See Note 16. (c) Refers to the right of grant deriving from merging the spun-off portion, in June 2006, of OHL Participações, former parent company of Autovias and Centrovias.

This amount is being amortized on a straight line until the final term of the concession. (d) Refers to the amount assumed for using granite and gneiss rocks in infrastructure work in projects for the companies pertaining to the Arteris Group and

installation and safeguarding of equipment to perform the work. (e) Refer to undergoing projects and services on the highway, such as paving, duplication, side roads, shoulders, work yards, special structure works, ground leveling,

implementing a system for collecting tolls and monitoring traffic, signaling and other such services.

Balance at 12.31.2015 8,251,826 351,939 144,380 47,318 12,941 2,688,443 470 11,497,317 Additions 68,483 - - 2,573 - 293,845 14,839 379,740 Transfers/Reclassifications 97,783 - - (1) - (97,788) - (6)Disposals/write-offs (3,206) - - (5) - - (9,139) (12,350)Balance at 3.31.2016 8,414,886 351,939 144,380 49,885 12,941 2,884,500 6,170 11,864,701

Accumulated amortization

Balance at 12.31.2015 (2,468,115) (281,281) (97,795) (16,687) (6,387) - - (2,870,265)Amortization (126,545) (6,400) (2,873) (1,892) (591) - - (138,301)Transfers/Reclassifications - - - 1 - - - 1 Disposals/write-offs 316 - - 4 - - - 320 Balance at 3.31.2016 (2,594,344) (287,681) (100,668) (18,574) (6,978) - - (3,008,245)

Intangible assets, net:

Balance at 12.31.2015 5,783,711 70,658 46,585 30,631 6,554 2,688,443 470 8,627,052Balance at 3.31.2016 5,820,542 64,258 43,712 31,311 5,963 2,884,500 6,170 8,856,456

Consolidated

Intangible asset in progress (e)

Advances to suppliers

TotalCost of intangible assets Intangible assets in highways – works and services (a)

Concession (b) Merged concession (c)

Software Operation right (d)

Arteris S.A. and Subsidiaries

13. BORROWINGS AND FINANCING

Broken down as follows:

Arteris:Working capital(e) Exchange rate var. + 2.6738%p.a. Aug-16 181,282 - - - Working capital(e) Exchange rate var. + 3.1550%p.a. Sep-16 180,645 - - -

361,927 - - -

Parent Company3.31.2016 12.31.2015

Annual charges Maturity Current Non-current Current Non-current

Arteris:Working capital(e) Exchange rate var. + 2.6738%p.a. Aug-16 181,282 - - - Working capital(e) Exchange rate var. + 3.1550%p.a. Sep-16 180,645 - - -

361,927 - - - Autovias:Equipment financing – (FINAME) (b) 6.0% p.a. Oct-17 428 249 428 355

428 249 428 355 Centrovias:Equipment financing – (FINAME) (b) 6.0% p.a. Oct-17 428 249 428 355

428 249 428 355 Vianorte:Equipment financing – (FINAME) (b) 6.0% p.a. Nov-17 428 221 428 327

428 221 428 327

Planalto Sul:Investment financing (BNDES) (a) TJLP + 2.58% p.a. Dec-25 23,202 264,670 22,690 269,474 Investment financing (BNDES) (a) TJLP + 2.62% p.a. Mar-27 121 34,958 121 34,834 Investment financing (BNDES) (a) IPCA + 8.99% p.a. Jan-27 - 17,228 - 16,361

23,323 316,856 22,811 320,669 Transaction cost (127) (1,180) (76) (1,283)

23,196 315,676 22,735 319,386

Current Non-current

Consolidated

Annual charges Maturity Current Non-current

3.31.2016 12.31.2015

Fluminense:Investment financing (BNDES) (a) TJLP + 2.45 p.a. Nov-26 43,657 656,053 36,357 662,578

43,657 656,053 36,357 662,578 Transaction cost (790) (3,850) - -

42,867 652,203 36,357 662,578 Fernão DiasEquipment financing – (FINAME) (b) 6% p.a. Jun-19 236 526 236 584Investment financing (BNDES) (a) TJLP + 2.21% Mar-26 47,386 535,204 48,991 542,041

47,622 535,730 49,227 542,625 Transaction cost (609) (1,260) - -

47,013 534,470 49,227 542,625 Régis BittencourtInvestment financing (BNDES) (a) TJLP + 2.21% p.a. Dec-24 82,477 822,911 80,761 838,719

82,477 822,911 80,761 838,719 Transaction cost (183) (1,393) - -

82,294 821,518 80,761 838,719

Arteris S.A. and Subsidiaries

TJLP - Long-Term Interest Rate.

(a) Credit facility opening agreement entered into with the Brazilian Development Bank (BNDES) to finance the recovery, improvement, maintenance, conservation, expansion, and operation works and services in the highways.

(b) Financing of equipment, guaranteed by the financed assets, collateral signature of shareholders or promissory notes.

(c) Finance lease agreements signed with financial institutions for acquisition of vehicles, information technology equipment and other equipment. The guarantees are the financed assets.

(d) Bank credit notes contracted from the financial institution for purchase of property and equipment for the São José Mill facility, with repayment term of 36 months as from the transaction formalization date, guaranteed by Arteris.

(e) Contracting of two foreign loans totaling fifty million dollars (US$50,000) each, from The Bank of Nova Scotia. In order to hedge against the foreign exchange variation, on the same date the Company also entered into a swap agreement with Scotia Bank do Brasil in order to convert the US dollar to the CDI+1.85% p.a. and CDI+2.15% p.a., respectively. The proceeds will be allocated to the group’s investment plan.

As at March 31, 2016, the maturities of the borrowings and financing are as follows:

As at March 31, 2016, there were no changes to the restrictive covenants contained in the financial statements of December 31, 2015.

Item “h” to the restrictive covenants of the agreement entered into with the BNDES provides for:

The Company shall not distribute dividends, pay interest on capital, pay interest on loans or repay the principal of these loans when the Debt Service Coverage Ratio (ICSD) is lower than 1.3, calculated under the following formula:

Litoral Sul:Investment financing (BNDES) (a) TJLP + 2.32% p.a. Jun-26 41,360 514,217 37,898 516,416

41,360 514,217 37,898 516,416 Transaction cost (1,878) (6,504) - -

39,482 507,713 37,898 516,416 Latina Manutenção:Equipment financing – (FINAME) (b) TJLP + 4.5% p.a. Mar-16 - - 141 - Working capital (d) 112.5% CDI May-17 6,316 4,928 5,919 4,927 Leasing (c ) 2.10% to 3.7% + CDI and 15.8% Feb-16 - - 174 -

6,316 4,928 6,234 4,927

Total 604,379 2,837,227 234,496 2,885,688

Maturity year2017 207,026 2018 283,320 2019 305,627 2020 651,612

1,389,642 2,837,227

After 2021

Arteris S.A. and Subsidiaries

ICSD = Cash Generation from the Activity Debt Service

Where:

Cash Generation from the Activity Debt Service EBITDA

(+) EBITDA (+) Repayment of principal (+) Profit for the year

(-) Income tax (+) Payment of interest (+) Finance cost/income, net

(-) Social contribution (+) Depreciation and amortization

(+) Provision for income tax and soci contribution

(+) Other non-operating expenses/income, net

As at March 31, 2016, the Debt Service Coverage Ratio (ICSD) of the federal concessionaires was below 1.3. However, these companies did not undertake any action that did not comply with this restrictive clause.

The Company is compliant with all restrictive covenants at the end of the reporting period. The fair value of borrowings recognized in current and non-current liabilities approximates their carrying amount, since the impact of the discount is not significant, considering that the discount rates are substantially similar to the contracted rates.

14. DEBENTURES

Broken down as follows:

Contractualyield rates (%)

2nd issue (g) 30,000 CDI + 2.00% p.a. Oct-17 - 200,010 - 198,418

3rd issue (i) 75,000 CDI + 2.00% p.a. Dec-16 904,497 - 864,146 -

105,000 904,497 200,010 864,146 198,418 Transaction cost (3,622) (1,364) (4,980) -

900,875 198,646 859,166 198,418

Parent Company

3.31.2016 12.31.2015

Series Number issued Maturities Current Non-current Current Non-current

Arteris S.A. and Subsidiaries

Contractualyield rates (%)

Arteris:2nd issue (g) 30,000 CDI + 2% p.a. Oct-17 - 200,010 - 198,418

3rd issue (i) 75,000 CDI + 2.00% p.a. Dec-16 904,497 - 864,146 -

105,000 904,497 200,010 864,146 198,418 Transaction cost (3,622) (1,364) (4,980) -

900,875 198,646 859,166 198,418

Autovias:1st issue - series 2 (a) 120,000 IPCA + 8% p.a. Mar-17 60,282 - 74,662 49,518

3rd issue (c) 30,000 CDI + 0.83% p.a. Aug-17 104,365 54,000 106,616 108,000

150,000 164,647 54,000 181,278 157,518 Transaction cost (309) (40) (371) (106)

164,338 53,960 180,907 157,412

Centrovias:1st issue - series 2 (a) 120,000 IPCA + 8% p.a. Mar-17 60,282 - 77,438 46,742 2nd issue (d) 40,000 CDI+0.99%p.a Jun-18 125,406 171,520 115,370 171,520

160,000 185,688 171,520 192,808 218,262 Transaction cost (501) (227) (574) (325)

185,187 171,293 192,234 217,937

Intervias:

3rd issue (c ) 60,000 CDI + 1.09% p.a. Sep-18 199,022 402,000 220,909 402,000

4th issue - series 1 (e) 15,000 CDI+1.10% p.a. Oct-19 10,035 150,000 4,586 150,000

4th issue - series 2 (e) 22,500 IPCA+5.96% p.a. Oct-19 41,882 225,000 30,301 225,000

97,500 250,939 777,000 255,796 777,000 Transaction cost (1,322) (2,019) (1,384) (2,313)

249,617 774,981 254,412 774,687

Vianorte:1st issue - series 2 (a) 100,000 IPCA + 8% p.a. Mar-17 50,235 - 61,935 41,509

2nd issue (b) 15,000 CDI + 0.86% p.a. Mar-17 60,235 - 63,590 30,000

115,000 110,470 - 125,525 71,509 Transaction cost (168) - (219) (33)

110,302 - 125,306 71,476

Planalto Sul:

2nd issue (h) 10,000 IPCA+8.17% p.a. Dec-25 701 125,597 - 120,472

10,000 701 125,597 - 120,472 Transaction cost (105) (908) - (1,098)

596 124,689 - 119,374

Fernão Dias

2nd issue (f) 10,000 CDI + 1.15% p.a. Jun-16 119,200 - 115,127 -

10,000 119,200 - 115,127 - Transaction cost (109) - (237) -

119,091 - 114,890 -

Total 1,730,006 1,323,569 1,726,915 1,539,304

12.31.20153.31.2016

Consolidated

Series Number issued Maturities Current Non-currentCurrent Non-current

Arteris S.A. and Subsidiaries

(a) 1st issue of debentures, series 2 of state concessionaires, on March 15, 2010 with nominal unit amount of R$1,000 each.

(b) 2nd issue of debentures, in a single series, of Vianorte on March 20, 2014 with unit face value of R$10,000 each.

(c) 3rd issue of debentures, in a single series, of Intervias, on September 25, 2013 with unit face value of R$10,000 each, and 3rd issue of debentures, in a single series, of Autovias, on December 18, 2013 with unit face value of R$10,000 each.

(d) 2nd issue of Centrovias’ debentures, in a single series, on March 20, 2014, with unit face value of R$10,000 each.

(e) 4th issue of Intervias’ debentures, in two series, the agreement was issued on October 15, 2014, with unit face value of R$10,000s.

(f) 2nd issue of Fernão Dias’ debentures, in a single series, on December 15, 2014, with unit face value of R$10,000 each.

(g) 2nd issue of the Parent Company’s debentures on October 1, 2014, with unit face value of R$10,000 each.

(h) 2nd issue of Planalto Sul's debentures, on December 15, 2014, with unit face value of R$10,000 each. The payment of this issue was on April 2015.

(i) 3rd issue of the Parent Company’s debentures on June 19, 2015, with unit face value of R$10,000 each.

(j) The Company classified interest paid on debentures as cash flow from financing activities in the parent company, since these debentures were raised and transferred through inter-company loan agreements to meet the working capital needs of its federal subsidiaries.

(k) Debentures were subscribed by their unit face value plus, for second series debentures, the corresponding adjustment for inflation and, for all debentures, the interest charged from the issue date through their actual payment date, as described below:

The yield on series 2 series debentures of 1st issue of concessionaires Autovias, Centrovias and Vianorte is paid yearly, every March 15, as of 2011, and amortized yearly, as of March 15, 2015.

Issue Date Nominal value Payment date Amount subscribed1st issue - State

Series 2 03.15.10 340,000 04.27.10 345,382 2nd issue - Centrovias and Vianorte 03.20.14 550,000 03.25.14 550,722

3rd issue - Autovias and Intervias 09.25.13 and 12.18.13 900,000 10.07.13 and 12.26.13 902,168 4th issue - Intervias 10.15.14 375,000 11.05.14 377,640 2nd issue - Federal 12.15.14 100,000 12.23.14 100,530 2nd issue - Federal 12.15.14 100,000 04.08.15 100,000 1st issue - Arteris 10.04.13 200,000 10.08.13 200,156 2nd issue - Arteris 10.01.14 300,000 10.01.14 302,486 3rd issue - Arteris 06.19.15 750,000 07.03.15 754,408

3,615,000 3,633,492

Consolidated

Arteris S.A. and Subsidiaries

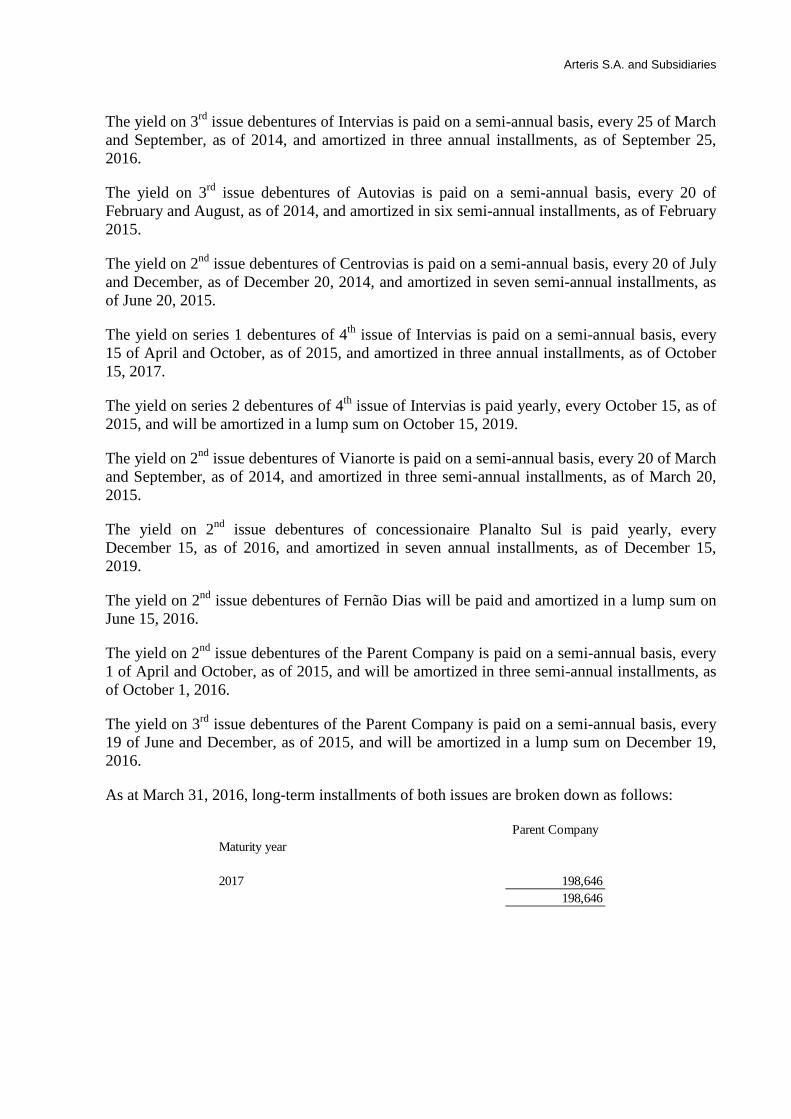

The yield on 3rd issue debentures of Intervias is paid on a semi-annual basis, every 25 of March and September, as of 2014, and amortized in three annual installments, as of September 25, 2016.

The yield on 3rd issue debentures of Autovias is paid on a semi-annual basis, every 20 of February and August, as of 2014, and amortized in six semi-annual installments, as of February 2015.

The yield on 2nd issue debentures of Centrovias is paid on a semi-annual basis, every 20 of July and December, as of December 20, 2014, and amortized in seven semi-annual installments, as of June 20, 2015.

The yield on series 1 debentures of 4th issue of Intervias is paid on a semi-annual basis, every 15 of April and October, as of 2015, and amortized in three annual installments, as of October 15, 2017.

The yield on series 2 debentures of 4th issue of Intervias is paid yearly, every October 15, as of 2015, and will be amortized in a lump sum on October 15, 2019.

The yield on 2nd issue debentures of Vianorte is paid on a semi-annual basis, every 20 of March and September, as of 2014, and amortized in three semi-annual installments, as of March 20, 2015.

The yield on 2nd issue debentures of concessionaire Planalto Sul is paid yearly, every December 15, as of 2016, and amortized in seven annual installments, as of December 15, 2019.

The yield on 2nd issue debentures of Fernão Dias will be paid and amortized in a lump sum on June 15, 2016.

The yield on 2nd issue debentures of the Parent Company is paid on a semi-annual basis, every 1 of April and October, as of 2015, and will be amortized in three semi-annual installments, as of October 1, 2016.

The yield on 3rd issue debentures of the Parent Company is paid on a semi-annual basis, every 19 of June and December, as of 2015, and will be amortized in a lump sum on December 19, 2016.

As at March 31, 2016, long-term installments of both issues are broken down as follows:

Parent CompanyMaturity year

2017 198,646 198,646

Arteris S.A. and Subsidiaries

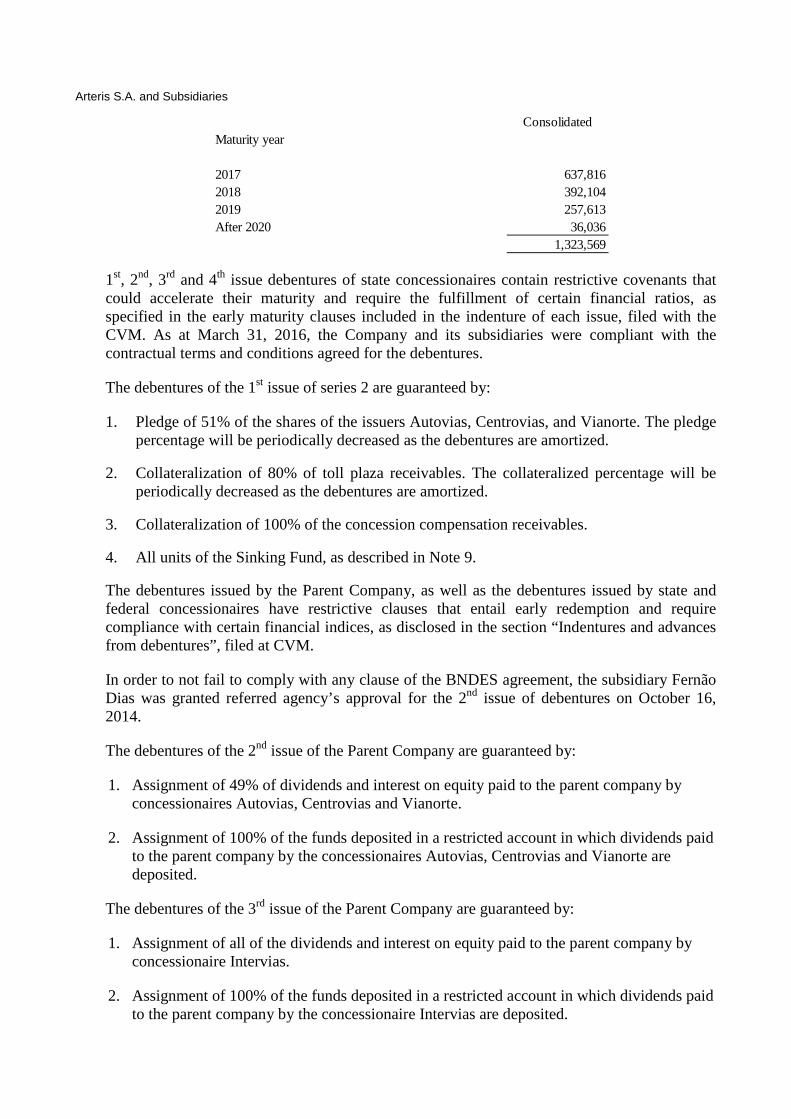

1st, 2nd, 3rd and 4th issue debentures of state concessionaires contain restrictive covenants that could accelerate their maturity and require the fulfillment of certain financial ratios, as specified in the early maturity clauses included in the indenture of each issue, filed with the CVM. As at March 31, 2016, the Company and its subsidiaries were compliant with the contractual terms and conditions agreed for the debentures.

The debentures of the 1st issue of series 2 are guaranteed by:

1. Pledge of 51% of the shares of the issuers Autovias, Centrovias, and Vianorte. The pledge percentage will be periodically decreased as the debentures are amortized.

2. Collateralization of 80% of toll plaza receivables. The collateralized percentage will be periodically decreased as the debentures are amortized.

3. Collateralization of 100% of the concession compensation receivables.

4. All units of the Sinking Fund, as described in Note 9.

The debentures issued by the Parent Company, as well as the debentures issued by state and federal concessionaires have restrictive clauses that entail early redemption and require compliance with certain financial indices, as disclosed in the section “Indentures and advances from debentures”, filed at CVM.

In order to not fail to comply with any clause of the BNDES agreement, the subsidiary Fernão Dias was granted referred agency’s approval for the 2nd issue of debentures on October 16, 2014.

The debentures of the 2nd issue of the Parent Company are guaranteed by:

1. Assignment of 49% of dividends and interest on equity paid to the parent company by concessionaires Autovias, Centrovias and Vianorte.

2. Assignment of 100% of the funds deposited in a restricted account in which dividends paid to the parent company by the concessionaires Autovias, Centrovias and Vianorte are deposited.

The debentures of the 3rd issue of the Parent Company are guaranteed by:

1. Assignment of all of the dividends and interest on equity paid to the parent company by concessionaire Intervias.

2. Assignment of 100% of the funds deposited in a restricted account in which dividends paid to the parent company by the concessionaire Intervias are deposited.

ConsolidatedMaturity year

2017 637,816 2018 392,104 2019 257,613 After 2020 36,036

1,323,569

Arteris S.A. and Subsidiaries

3. Fiduciary sale of all of the shares issued by a wholly owned subsidiary of the parent company which, in turn, will directly hold 49% of Intervias shares.

The 2nd issue debentures of concessionaire Fernão Dias are guaranteed by “aval” guarantee by Arteris S.A., in favor of the debenture holders.

The 1st issue debentures of the federal concessionaires and the and 2nd issue debentures of concessionaire Fernão Dias are guaranteed by “aval” guarantee by Arteris S.A., in favor of the debenture holders.

The 2nd issue debentures of concessionaire Planalto Sul are guaranteed by:

1. Fiduciary assignment of receivables held by the Company.

2. Pledge of all the shares held by the Company.

3. Fiduciary assignment of concession’s rights.

As at March 31, 2016, the Company and its subsidiaries were compliant with the contractual terms and conditions agreed for the debentures.

15. RELATED-PARTY TRANSACTIONS

Related-party transactions refer to administrative expenses, inter-company working capital loans and execution of the group’s investment plan.

The balances at March 31, 2016 and December 31, 2015 and related-party transactions in the periods ended March 31, 2016 and 2015, are stated below:

Arteris S.A. and Subsidiaries

Current assets 3.31.2016 12.31.2015

Amounts due from related parties: Subsidiaries: Autovias (a) 904 1,568 Centrovias (a) 796 1,518 Intervias (a) 842 1,588 Vianorte (a) 692 1,314 Planalto Sul (a) 241 473 Fluminense (a) 799 1,186 Fernão Dias (a) 1,201 1,722 Régis Bittencourt (a) 667 1,731 Litoral Sul (a) 509 930 Latina Manutenção (a) 724 3,234 Latina Sinalização (a) - 151 Autovias (d) 6,237 4,324 Centrovias (d) 4,331 2,982 Intervias (d) 5,535 4,679 Arteris Paricipações (a) 247 - Vianorte (d) 5,508 5,508 Planalto Sul (b) 32,630 22,229 Fluminense (b) 23,986 22,607 Fernão Dias (b) 47,403 44,678 Régis Bittencourt (b) 20,893 19,692 Litoral Sul (b) 52,017 48,515 Related parties:Other 260 - Total 206,422 190,629

-

Parent Company

3.31.2016 12.31.2015Dividends receivable - subsidiaries:

Serviço e Tecnologia de Pagamentos S.A. 5,674 6,223 Total 5,674 6,223

Parent Company

Arteris S.A. and Subsidiaries

Non-current assets3.31.2016 12.31.2015

Amounts due from related parties - borrowings from subsidiaries: Planalto Sul (b) 181,681 176,898 Fluminense (b) 186,823 181,961 Fernão Dias (b) 370,061 360,455 Régis Bittencourt (b) 166,002 161,772 Litoral Sul (b) 403,800 393,767 Total 1,308,367 1,274,853

Parent Company

Amounts receivable from related parties - Debentures subsidiaries: Planalto Sul (e) 21,588 29,710 Fluminense (f) 131,113 127,151 Fernão Dias (i) 21,588 20,938 Régis Bittencourt (g) 279,434 270,998 Litoral Sul (h) 225,062 218,260 Total 678,785 667,057

Total non-current 1,987,152 1,941,910

Current liabilities3.31.2016 12.31.2015

Borrowings and financing from subsidiaries: Autovias (c) 24,385 28,669 Centrovias (c) 35,264 32,062 Intervias (c) 52,092 48,256 Vianorte (c) 24,649 23,231 Total 136,390 132,218

Parent Company

3.31.2016 12.31.2015 3.31.2016 12.31.2015Accounts payable: Related parties:

Intervias (a) 9 - - -Fluminense (a) - 44 - -Fernão Dias (a) - 13 - -Régis Bittencourt (a) - 43 - -Litoral Sul (a) 19 - - -Latina Manutenção (a) 2 - - -Participes en Brasil S.L. 152 - 152 -

Total 182 100 152 -

Parent Company Consolidated

Arteris S.A. and Subsidiaries

(a) Refer to the apportionment of administrative costs and expenses among Arteris Group companies.

(b) Intercompany loan agreements with an interest rate equivalent to 100% of the CDI variation plus 1.037% to 1.4% per year with interest rates maturing as of December 2015 and principal as of December 2017.

(c) Intercompany loan agreements with an interest rate equivalent to 100% of the CDI variation plus 1.037% to 1.4% per year with interest rates maturing as of December 2015 and principal as of December 2017.

(d) Refers to interest on equity receivable.

(e) Refers to the indenture of the 3rd issue of non-convertible, subordinated debentures, in a single series, entered into between Autopista Planalto Sul S.A (Issuer) and Arteris S.A (Debenture Holder), whose proceeds will be allocated to the Issuer’s Capex plan. Referred debentures will bear interest rates corresponding to 100% of CDI variation plus spread of 1.4% per year, with principal amount and interest rates expected to mature on March 29, 2017.

(f) Refers to the indenture of the 2nd issue of non-convertible, subordinated debentures, in a single series, entered into between Autopista Fluminense S.A. (Issuer) and Arteris S.A (Debenture Holder), whose proceeds will be allocated to the Issuer’s Capex plan. Referred debentures will bear interest rates corresponding to 100% of CDI variation plus spread of 1.5% per year, with principal amount and interest rates expected to mature on April 10, 2017.

(g) Refers to the indenture of the 2nd and 3rd issues of non-convertible, subordinated debentures, in a single series, entered into between Autopista Régis Bittencourt S.A (Issuer) and Arteris S.A (Debenture Holder), whose proceeds will be allocated to the Issuer’s Capex plan. Referred debentures will bear interest rates corresponding to 100% of CDI variation plus spread of 1.5% per year, with principal amount and interest rates of the 2nd issue expected to mature on April 27, 2017, and of the 3rd issue expect to mature on June 25, 2017.

(h) Refers to the indenture of the 3rd issue of non-convertible, subordinated debentures, in a single series, entered into between Autopista Litoral Sul S.A (Issuer) and Arteris S.A (Debenture Holder), whose proceeds will be allocated to the Issuer’s Capex plan. Referred debentures will bear interest rates corresponding to 100% of CDI variation plus spread of 1.5% per year, with principal amount and interest rates expected to mature on April 28, 2017.

Non-current liabilities 3.31.2016 12.31.2015Borrowings and financing from subsidiaries - Loans: Autovias (c) 250,896 253,201 Centrovias (c) 303,439 296,580 Intervias (c) 412,945 403,239 Vianorte (c) 186,698 181,696 Total 1,153,978 1,134,716

Parent Company

Amounts due from related parties - Debentures subsidiaries: Intervias (j) 264,950 256,679 Total 264,950 256,679

Total 1,418,928 1,391,395

Arteris S.A. and Subsidiaries

(i) Refers to the indenture of the 3rd issue of non-convertible, subordinated debentures, in a single series, entered into between Autopista Fernão Dias S.A (Issuer) and Arteris S.A (Debenture Holder), whose proceeds will be allocated to the Issuer’s Capex plan. Referred debentures will bear interest rates corresponding to 100% of CDI variation plus spread of 1.5% per year, with principal amount and interest rates expected to mature on August 19, 2017.

(j) Refers to the indenture of the 4th issue of non-convertible, subordinated debentures, in a single series, entered into between Concessionária de Rodovias do Interior Paulista S.A (Issuer) and Arteris S.A (Debenture Holder), whose proceeds will be allocated to the Issuer’s Capex plan. Referred debentures will bear interest rates corresponding to 100% of CDI variation plus spread of 2.0% per year, with principal amount and interest rates expected to mature on June 25, 2017.

During the period ended March 31, 2016, the Company recognized R$1,257 (R$1,366 as at March 31, 2015), Parent Company, and R$5,033 (R$5,671 as at March 31, 2015), Consolidated, as management compensation. Management neither received nor granted loans to the Company and its subsidiaries, and are not entitled to significant fringe benefits.