Årsmöteskonferensen 2014 michael menhart the social and economic value of insurance send out

TRANSCRIPT

The Social and Economic Value of Insurance

14 May 2014

Michael Menhart

Chief Economist

Munich Re

The Social and Economic Value of Insurance

Value of insurance for economy and society: obvious, but often

misunderstood

Natural catastrophes: Economic consequences and the role of

insurance

Too important to fail? The systemic risk debate and insurance

2

The social and economic value of insurance goes way

beyond social protection

Source: Munich Re Economic Research 3

• Essential for social protection and financial security

• Knowledge management

• Improvement of risk-resilience through assessment and pricing of risk

• Stabilizing role on capital markets

• Catalyst for economic activity, especially after catastrophes

Insurance addresses fundamental human emotions…

• Risk permeates our lives:

• Property damage

• Natural disaster

• Sickness and disability

• Accidents and death

• Insurance addresses two fundamental interconnected human emotions:

• Hope

• Fear

• Insurance is an intrinsic part of society and social behaviour

Source: Munich Re Economic Research 4

…but is poorly understood and often maligned

(Woody Allen,

Love and Death, 1975)

SourceMunich Re Economic Research 5

“There are worse things

in life than death. Have

you ever spent an

evening with an

insurance salesman?”

Insufficient communication, lack of understanding and natural

conflict between “social welfare” and “for-profit-nature”

• Lack of communication at least in the

past

• Tendency to neglect its image

• Low-profile nature of doing business

• Often conducted locally

• Misinterpretation and lack of

knowledge

• Intrinsic conflict between

• Social welfare underlining insurance

• “For-profit nature” of insurance

business

SourceMunich Re Economic Research 6

Equal importance:

• Value of

insurance

• Values of

insurers

The Social and Economic Value of Insurance

Value of insurance for economy and society: obvious, but often

misunderstood

Natural catastrophes: Economic consequences and the role of

insurance

Too important to fail? The systemic risk debate and insurance

7

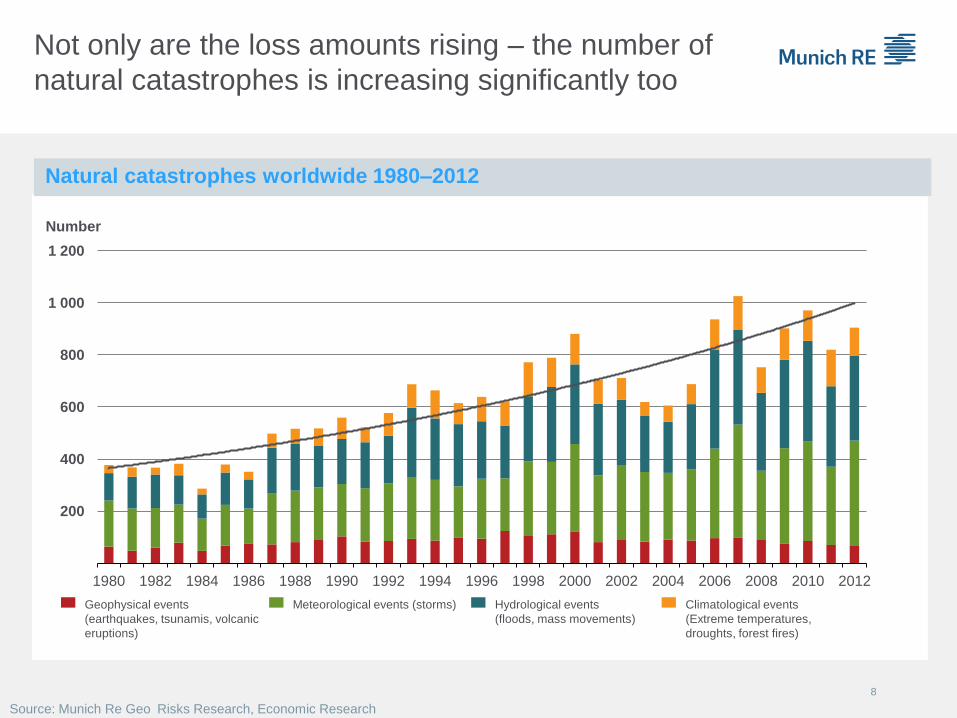

Not only are the loss amounts rising – the number of

natural catastrophes is increasing significantly too

8

Meteorological events (storms) Hydrological events

(floods, mass movements)

Climatological events

(Extreme temperatures,

droughts, forest fires)

Geophysical events

(earthquakes, tsunamis, volcanic

eruptions)

Number

Source: Munich Re Geo Risks Research, Economic Research

200

400

600

800

1 000

1 200

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Natural catastrophes worldwide 1980–2012

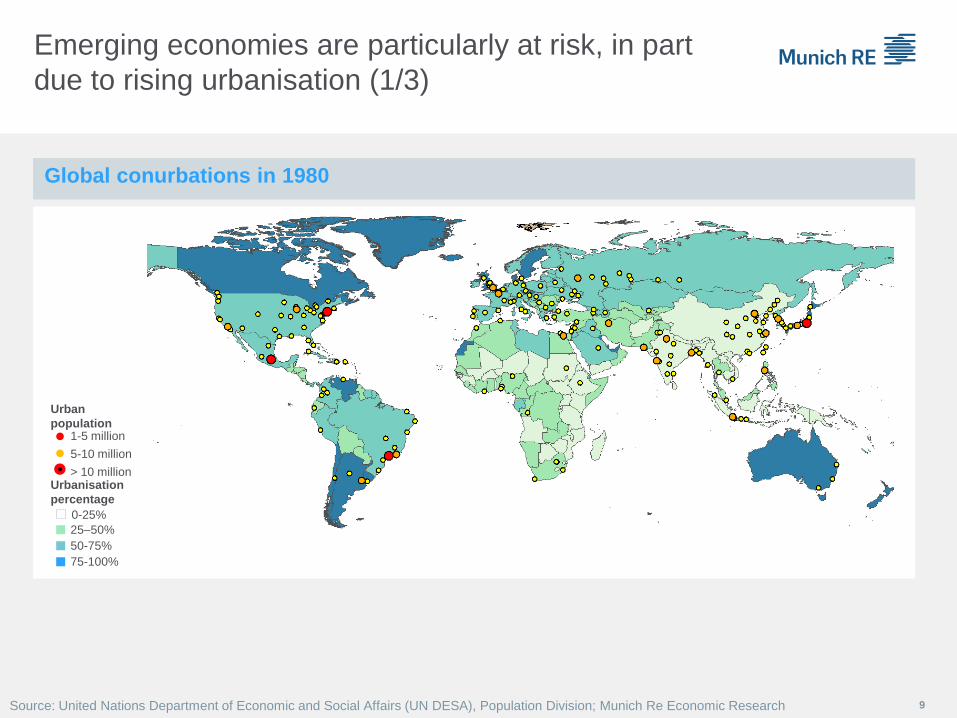

Global conurbations in 1980

9

Emerging economies are particularly at risk, in part

due to rising urbanisation (1/3)

0-25%

25–50%

50-75%

75-100%

Urbanisation

percentage

Urban

population 1-5 million

5-10 million

> 10 million

Source: United Nations Department of Economic and Social Affairs (UN DESA), Population Division; Munich Re Economic Research

Global conurbations in 2011

10

Emerging economies are particularly at risk, in part

due to rising urbanisation (2/3)

0-25%

25–50%

50-75%

75-100%

Urbanisation

percentage

Urban

population 1-5 million

5-10 million

> 10 million

Source: United Nations Department of Economic and Social Affairs (UN DESA), Population Division, Munich Re Economic Research

Global conurbations in 2025

11

Emerging economies are particularly at risk, in part

due to rising urbanisation (3/3)

0-25%

25–50%

50-75%

75-100%

Urbanisation

percentage

Urban

population 1-5 million

5-10 million

> 10 million

Source: United Nations Department of Economic and Social Affairs (UN DESA), Population Division; Munich Re Economic Research

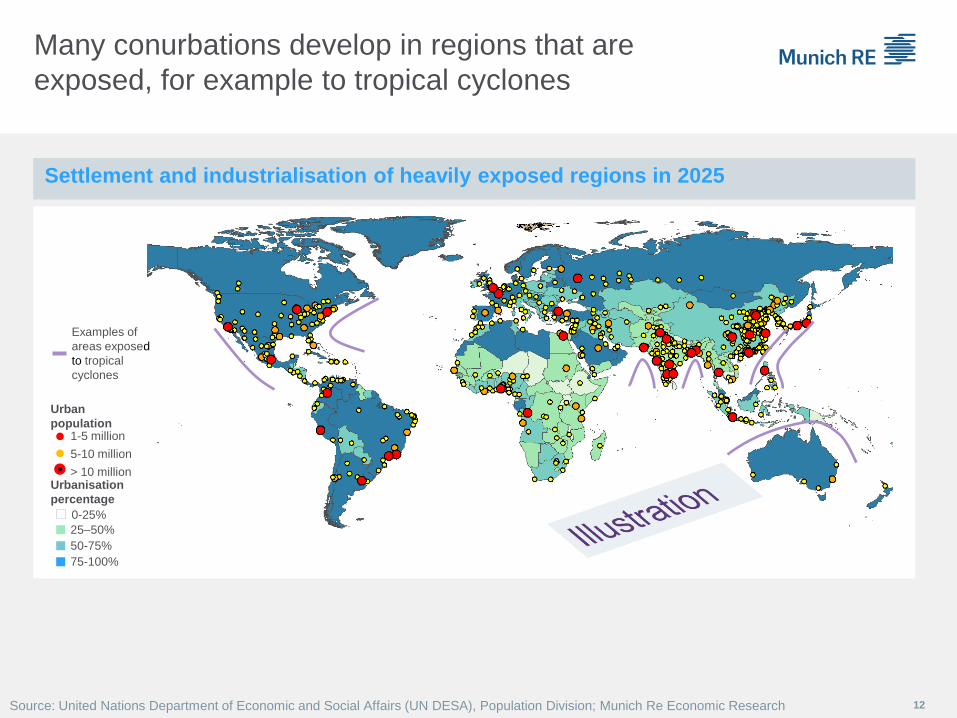

Settlement and industrialisation of heavily exposed regions in 2025

12

Many conurbations develop in regions that are

exposed, for example to tropical cyclones

0-25%

25–50%

50-75%

75-100%

Urbanisation

percentage

Urban

population 1-5 million

5-10 million

> 10 million

Source: United Nations Department of Economic and Social Affairs (UN DESA), Population Division; Munich Re Economic Research

Examples of

areas exposed

to tropical

cyclones

The overall economic effect results from both the direct

and the indirect effects

13

Economic effects of natural catastrophes

Overall effect

Direct losses

Direct consequences of the

forces of nature

Usually not directly evident from

the development of GDP*

Personal injury

Direct economic losses, e.g.

damage to capital assets and

resources

Indirect effects = “positive” + negative indirect effects

All effects not caused directly by the natural catastrophe

but by the resultant direct losses

Indirect effects are usually changes in GDP compared

with the hypothetical development of GDP in the

absence of a natural catastrophe

“Positive” indirect effects,

e.g. through

Reconstruction stimulus

“Prosperity incentives”, e.g.

construction of new, better-

quality houses

“Creative destruction”, e.g.

the destruction fosters

innovation; new production

facilities are more modern

than those destroyed

*) Exemptions are droughts and heat waves which directly impair GDP

Source: Munich Re Economic Research

Negative indirect effects,

e.g. through

Loss of production due to

destroyed installations

Degradation of human

capital

Damaged and destroyed

infrastructure

Often higher inflation

Frequently, an increase in

government debt

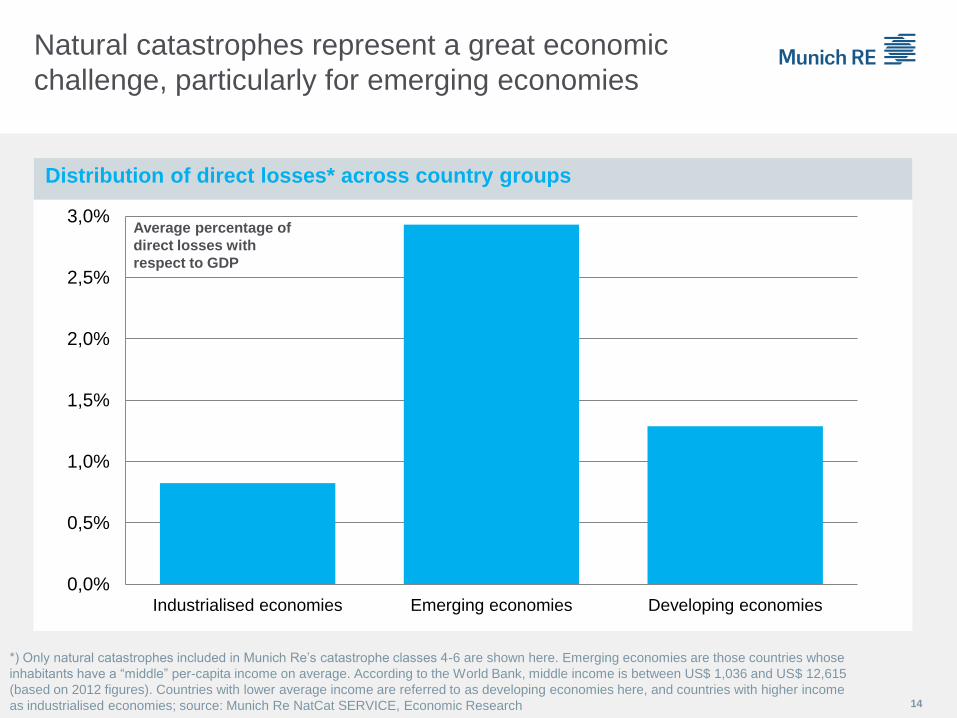

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

Industrialised economies Emerging economies Developing economies

Average percentage of

direct losses with

respect to GDP

14

Natural catastrophes represent a great economic

challenge, particularly for emerging economies

Distribution of direct losses* across country groups

*) Only natural catastrophes included in Munich Re’s catastrophe classes 4-6 are shown here. Emerging economies are those countries whose

inhabitants have a “middle” per-capita income on average. According to the World Bank, middle income is between US$ 1,036 and US$ 12,615

(based on 2012 figures). Countries with lower average income are referred to as developing economies here, and countries with higher income

as industrialised economies; source: Munich Re NatCat SERVICE, Economic Research

15

Example: Hurricane Gustav caused higher absolute damage in the USA,

but lower relative damage than in Jamaica. This is explained, in part, by the countries’

respective absolute economic strength and economic level of development

*) In original values, **) In 2005 values and purchasing power parity; source: Global Insight, “Tropical Cyclone Report: Hurricane Gustav” from the National Hurricane Center; Munich Re Geo Risks Research, Economic Research; Source of photos: Dpa / Picture Alliance

US$ 4.3bn

0.03 %

11

Overall losses*

Overall losses

(relative to GDP)

Fatalities

US$ 14,292bn GDP 2008*

US$ 43,161 GDP per capita

2008**

USA

US$ 0.21bn

1.5%

15

Overall losses*

Overall losses

(relative to GDP)

Fatalities

US$ 14bn GDP 2008*

US$ 7,437 GDP per capita

2008**

Jamaica

The overall economic effect results from both the direct

and the indirect effects

16

Economic effects of natural catastrophes

Overall effect

Direct losses

Direct consequences of the

forces of nature

Usually not directly evident from

the development of GDP*

Personal injury

Direct economic losses, e.g.

damage to capital assets and

resources

Indirect effects = “positive” + negative indirect effects

All effects not caused directly by the natural catastrophe

but by the resultant direct losses

Indirect effects are usually changes in GDP compared

with the hypothetical development of GDP in the

absence of a natural catastrophe

“Positive” indirect effects,

e.g. through

Reconstruction stimulus

“Prosperity incentives”, e.g.

construction of new, better-

quality houses

“Creative destruction”, e.g.

the destruction fosters

innovation; new production

facilities are more modern

than those destroyed

*) Exemptions are droughts and heat waves which directly impair GDP

Source: Munich Re Economic Research

Negative indirect effects,

e.g. through

Loss of production due to

destroyed installations

Degradation of human

capital

Damaged and destroyed

infrastructure

Often higher inflation

Frequently, an increase in

government debt

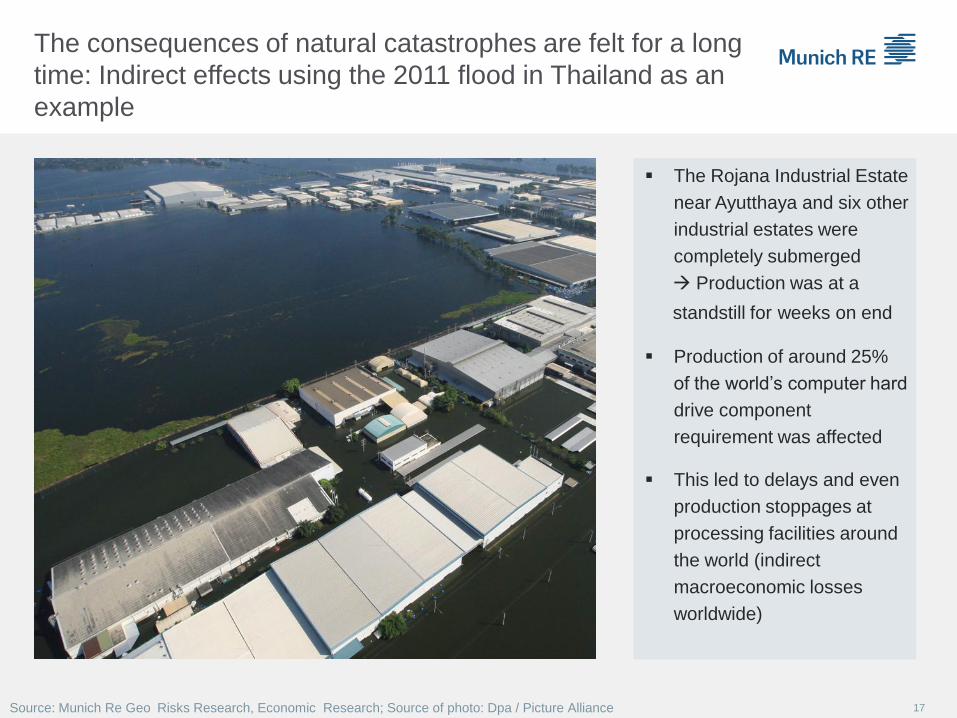

The Rojana Industrial Estate

near Ayutthaya and six other

industrial estates were

completely submerged

Production was at a

standstill for weeks on end

Production of around 25%

of the world’s computer hard

drive component

requirement was affected

This led to delays and even

production stoppages at

processing facilities around

the world (indirect

macroeconomic losses

worldwide)

The consequences of natural catastrophes are felt for a long

time: Indirect effects using the 2011 flood in Thailand as an

example

Source: Munich Re Geo Risks Research, Economic Research; Source of photo: Dpa / Picture Alliance 17

As a consequence of the 2011 earthquake and tsunami in Japan, there were production stoppages

and supply interruptions for many Japanese and foreign firms

The automobile industry was particularly impacted; Toyota, for example, had to close all 12 of its

Japanese plants temporarily. As a result, automobile exports, e.g. to the USA, collapsed

The 2011 earthquake and tsunami in Japan also led

to production stoppages

18

Example of a negative indirect effect: Lost production

Source: Munich Re Economic Research, Reuters; Source of figure: Leckcivilize, A. (2012): The Impact of Supply Chain Disruptions: Evidence from the Japanese Tsunami.

Earthquake and tsunami (March-June 2011)

Car parts and components

Passenger vehicles

Ex

po

rts

(tu

rno

ve

r) t

o t

he

US

A

(in

de

x:

Ja

nu

ary

20

09

= 1

00

)

Exports declined

by more than half

19 Source: Munich Re Economic Research, IMF

In emerging economies, government debt often rises

significantly following natural catastrophes – example Chile

- 40

- 20

0

20

40

60

80

0

2000

4000

6000

8000

10000

12000

14000

16000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Government debt (left axis))

Growth rate of government debt (right axis)

Government debt Chile

in bn pesos

Start of 2010:

Earthquake in Chile

The overall economic effect results from both the direct

and the indirect effects

20

Economic effects of natural catastrophes

Overall effect

Direct losses

Direct consequences of the

forces of nature

Usually not directly evident from

the development of GDP*

Personal injury

Direct economic losses, e.g.

damage to capital assets and

resources

Indirect effects = “positive” + negative indirect effects

All effects not caused directly by the natural catastrophe

but by the resultant direct losses

Indirect effects are usually changes in GDP compared

with the hypothetical development of GDP in the

absence of a natural catastrophe

“Positive” indirect effects,

e.g. through

Reconstruction stimulus

“Prosperity incentives”, e.g.

construction of new, better-

quality houses

“Creative destruction”, e.g.

the destruction fosters

innovation; new production

facilities are more modern

than those destroyed

*) Exemptions are droughts and heat waves which directly impair GDP

Source: Munich Re Economic Research

Negative indirect effects,

e.g. through

Loss of production due to

destroyed installations

Degradation of human

capital

Damaged and destroyed

infrastructure

Often higher inflation

Frequently, an increase in

government debt

21

GDP

level

Time Occurrence of

catastrophe

GDP losses in the wake

of the catastrophe (=indirect

negative effects)

Hypothetical GDP growth

without catastrophe

Actual GDP growth

Rise in GDP due to

the stimulus from

reconstruction

(= indirect positive effects)

End of

reconstruction

Several years

Indirect effects over time: Typical GDP growth after a

natural catastrophe

Illustration: Indirect effects of an average* natural catastrophe in the short and medium term

(up to five years)

*) Relative to average direct losses as a percentage of GDP

Source: Graph based on Hallegatte S. et al. (2010):The Economics of Natural Disasters, Munich Re Economic Research

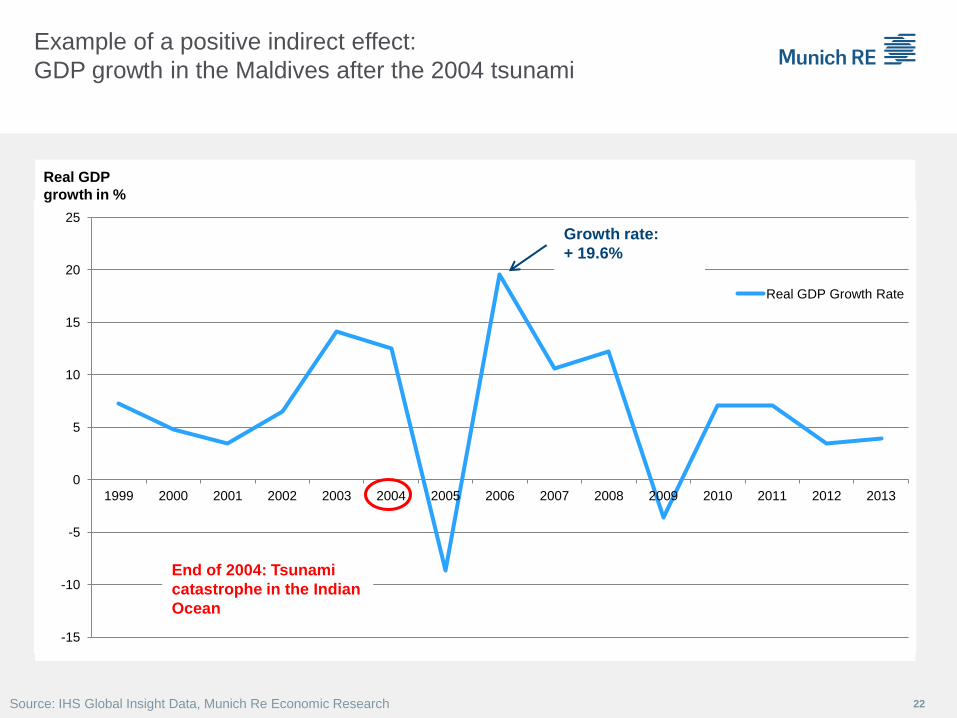

22

Example of a positive indirect effect:

GDP growth in the Maldives after the 2004 tsunami

-15

-10

-5

0

5

10

15

20

25

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Real GDP Growth Rate

Growth rate:

+ 19.6%

End of 2004: Tsunami

catastrophe in the Indian

Ocean

Source: IHS Global Insight Data, Munich Re Economic Research

Real GDP

growth in %

Example: The indirect effects of Hurricane Katrina in Louisiana

Example: Despite the financial crisis that began in 2008,

GDP in Louisiana started growing again soon after Hurricane Katrina

23 Sources: Federal Reserve Economic Data, Munich Re Economic Research

Hurricane

Katrina

-8

-6

-4

-2

0

2

4

6

8

10

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Real G

DP

gro

wth

(in

per

cen

t)

Louisiana USA Differenz

% Louisiana grows faster than

the USA as a whole

(probably the result of

reconstruction)

Louisiana grows more slowly

than the USA as a whole

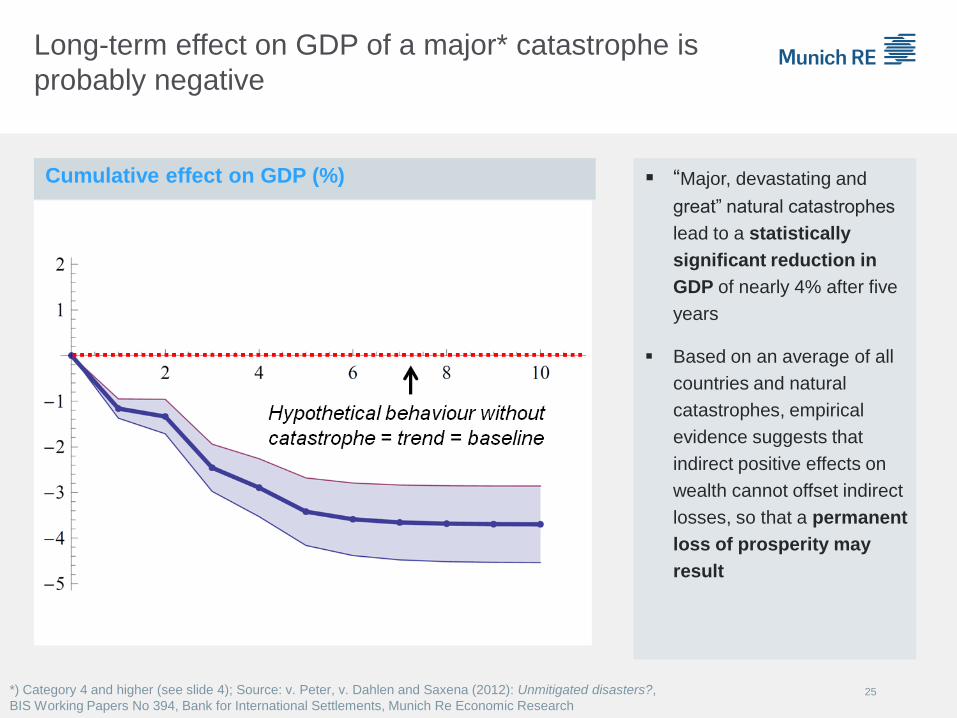

High level of development and interregional interconnection can mitigate negative GDP effects

The overall effect depends on the time horizon under review

24

Source: Munich Re Economic Research

Indirect effects

Short- and medium-term effects (up to 5 years) Long-term effects (over 5 years)

Direct effects +

GDP growth is negatively impacted in the short and medium term by a natural catastrophe

The GDP level declines in the short to medium term compared with the hypothetical trend without

the natural catastrophe

The GDP level also remains below the long-term hypothetical trend without the natural

catastrophe, except if the natural catastrophe increases long-term growth (based on the status of

research as of today, this is rather “unlikely”)

“Major, devastating and

great” natural catastrophes

lead to a statistically

significant reduction in

GDP of nearly 4% after five

years

Based on an average of all

countries and natural

catastrophes, empirical

evidence suggests that

indirect positive effects on

wealth cannot offset indirect

losses, so that a permanent

loss of prosperity may

result

Cumulative effect on GDP (%)

25

Long-term effect on GDP of a major* catastrophe is

probably negative

*) Category 4 and higher (see slide 4); Source: v. Peter, v. Dahlen and Saxena (2012): Unmitigated disasters?,

BIS Working Papers No 394, Bank for International Settlements, Munich Re Economic Research

26

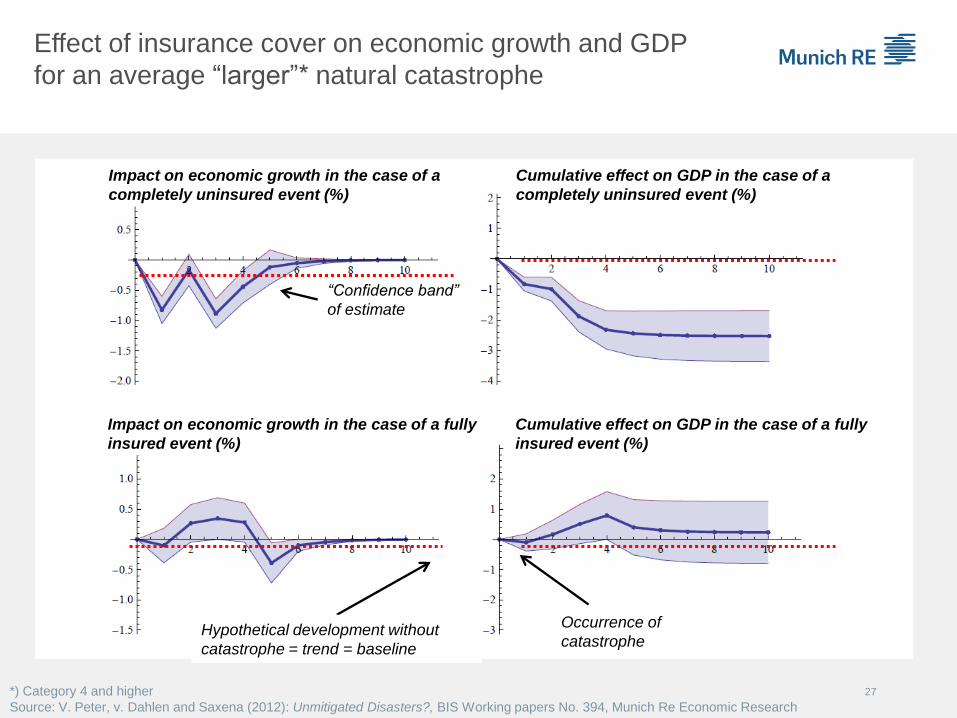

Insurance cover significantly helps economic recovery

following a natural catastrophe

GDP

level

Time Occurrence of

catastrophe

Hypothetical GDP trend

without the disaster

GDP growth in countries

with low insurance

penetration

End of

reconstruction

Several years

GDP growth in countries

with high insurance

penetration

Increase in GDP from the

economic stimulus of

reconstruction (= indirect

positive effects)

GDP losses following the

catastrophe (= indirect

negative effects)

Illustration of indirect effects of an average* natural catastrophe in the short and medium term

*) Relative to average direct losses as a percentage of GDP

Source: Munich Re Economic Research; graph based on Hallegatte S. et al. (2010): The Economics of Natural Disasters.

Impact on economic growth in the case of a

completely uninsured event (%)

Cumulative effect on GDP in the case of a

completely uninsured event (%)

Impact on economic growth in the case of a fully

insured event (%)

Cumulative effect on GDP in the case of a fully

insured event (%)

“Confidence band”

of estimate

Hypothetical development without

catastrophe = trend = baseline

Occurrence of

catastrophe

27

Effect of insurance cover on economic growth and GDP

for an average “larger”* natural catastrophe

*) Category 4 and higher

Source: V. Peter, v. Dahlen and Saxena (2012): Unmitigated Disasters?, BIS Working papers No. 394, Munich Re Economic Research

Development of per-capita debt at different levels of insurance penetration

Low insurance penetration (left) leads to a statistically significant rise in government debt

The insurance penetration of a country has a considerable

influence on its government debt following natural

catastrophes

28

Source: Source: Melecky und Raddatz (2011): How Do Governments Respond after

Catastrophes? World Bank, Munich Re Economic Research

Per-capita debt with low insurance

penetration Per-capita debt with high insurance

penetration

Years after

climatic

catastrophe

“Confidence band”

for estimate

30%

20%

10%

0%

50%

0%

- 50%

- 100% Hypothetical development without

the catastrophe = trend = baseline

29

Source: Munich Re Economic Research; Englmaier and Stowasser (2013): The Effect of

Insurance Markets on Countries’ Resilience to Disasters, Mimeo, University of Würzburg/LMU.

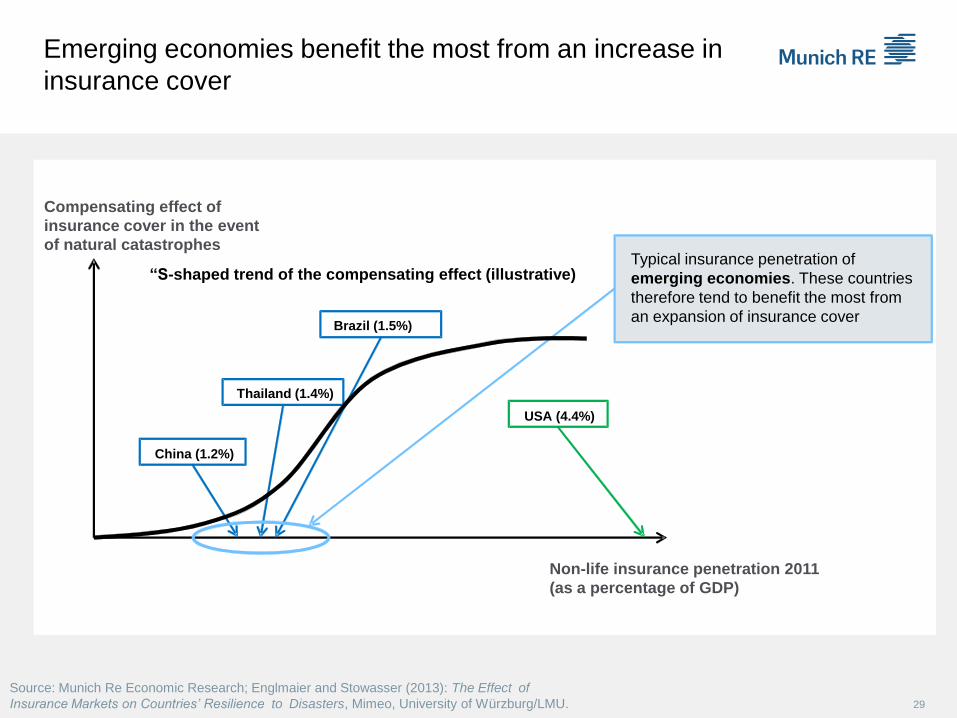

Emerging economies benefit the most from an increase in

insurance cover

Compensating effect of

insurance cover in the event

of natural catastrophes

China (1.2%)

Thailand (1.4%)

Brazil (1.5%)

USA (4.4%)

Non-life insurance penetration 2011

(as a percentage of GDP)

Typical insurance penetration of

emerging economies. These countries

therefore tend to benefit the most from

an expansion of insurance cover

“S-shaped trend of the compensating effect (illustrative)

The Social and Economic Value of Insurance

Value of insurance for economy and society: obvious, but often

misunderstood

Natural catastrophes: Economic consequences and the role of

insurance

Too important to fail? The systemic risk debate and insurance

30

The “AIG case” – sound insurance business, but problems

caused by FP division led to massive public attention

31

Source: Munich Re Economic Research

“SIFIs” (systemically important financial institutions) –

definition according to Financial Stability Board

SIFIs are “…those institutions

whose disorderly failure, because of their

size, complexity and systemic interconnectedness,

would cause significant disruption

to the wider financial system

and economic activity.”

Later lack of substitutability was added as indicator. (FSB)

32

Source: Financial Stability Board, Munich Re Economic Research

G-SIBs – The systemically relevant banks 2013

33

Source: Financial Stability Board, Munich Re Economic Research

Insurers and banks - differences in business models

important for systemic risk discussion

Economic function of banks

Essential for payment, clearing and settlement

Saving deposits of public always with at least “implicit government

guarantee”

Different economic role of insurers

No comparable interconnectedness (no “inter-banking market”

needed for financing)

Traditional insurance activities have an inverted cycle of

production (pre-funding of liabilities)

Payments depend on occurrence of “insured event”

No risk of “bank-run” on insurers 34

Source: Munich Re Economic Research

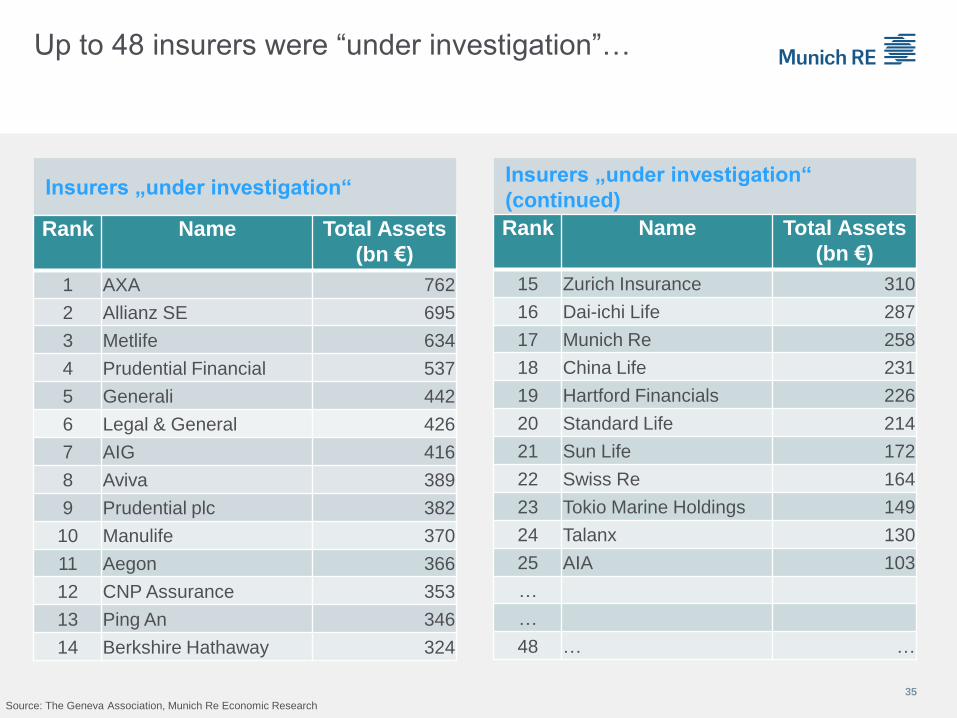

Up to 48 insurers were “under investigation”…

35

Insurers „under investigation“ Insurers „under investigation“

(continued)

Rank Name Total Assets

(bn €)

1 AXA 762

2 Allianz SE 695

3 Metlife 634

4 Prudential Financial 537

5 Generali 442

6 Legal & General 426

7 AIG 416

8 Aviva 389

9 Prudential plc 382

10 Manulife 370

11 Aegon 366

12 CNP Assurance 353

13 Ping An 346

14 Berkshire Hathaway 324

Rank Name Total Assets

(bn €)

15 Zurich Insurance 310

16 Dai-ichi Life 287

17 Munich Re 258

18 China Life 231

19 Hartford Financials 226

20 Standard Life 214

21 Sun Life 172

22 Swiss Re 164

23 Tokio Marine Holdings 149

24 Talanx 130

25 AIA 103

…

…

48 … …

Source: The Geneva Association, Munich Re Economic Research

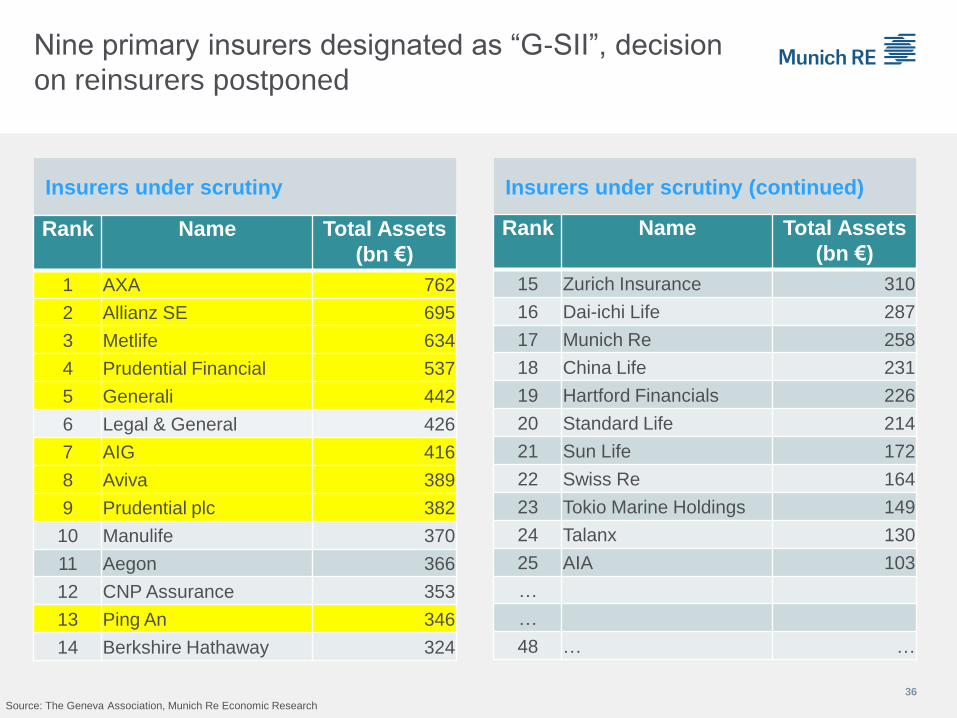

Nine primary insurers designated as “G-SII”, decision

on reinsurers postponed

36

Insurers under scrutiny Insurers under scrutiny (continued)

Rank Name Total Assets

(bn €)

1 AXA 762

2 Allianz SE 695

3 Metlife 634

4 Prudential Financial 537

5 Generali 442

6 Legal & General 426

7 AIG 416

8 Aviva 389

9 Prudential plc 382

10 Manulife 370

11 Aegon 366

12 CNP Assurance 353

13 Ping An 346

14 Berkshire Hathaway 324

Rank Name Total Assets

(bn €)

15 Zurich Insurance 310

16 Dai-ichi Life 287

17 Munich Re 258

18 China Life 231

19 Hartford Financials 226

20 Standard Life 214

21 Sun Life 172

22 Swiss Re 164

23 Tokio Marine Holdings 149

24 Talanx 130

25 AIA 103

…

…

48 … …

Source: The Geneva Association, Munich Re Economic Research

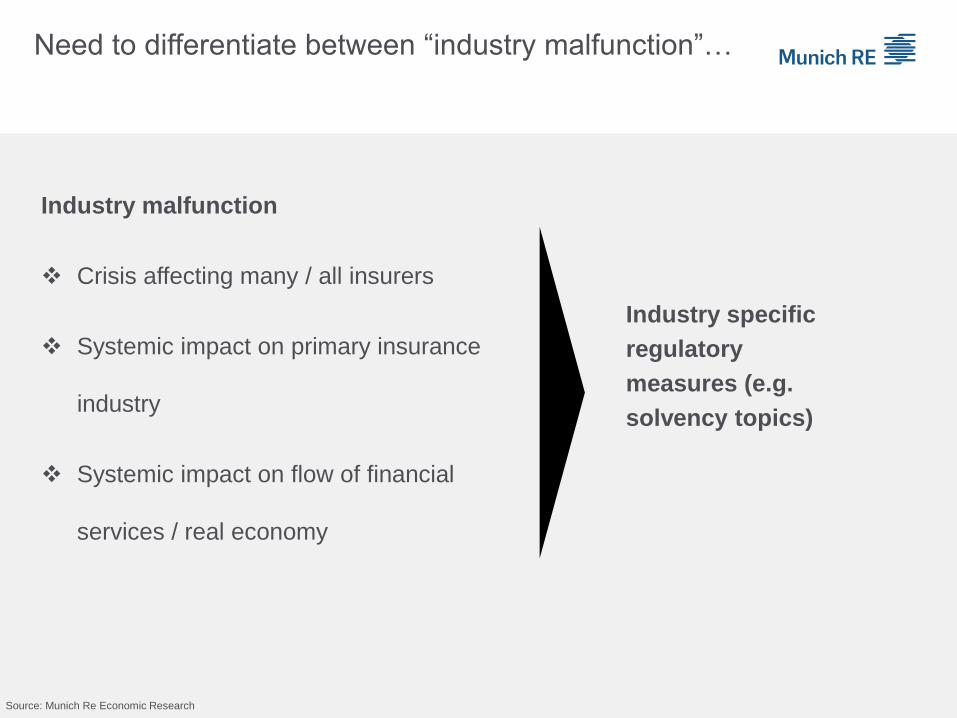

Need to differentiate between “industry malfunction”…

Industry specific

regulatory

measures (e.g.

solvency topics)

Industry malfunction

Crisis affecting many / all insurers

Systemic impact on primary insurance

industry

Systemic impact on flow of financial

services / real economy

Source: Munich Re Economic Research

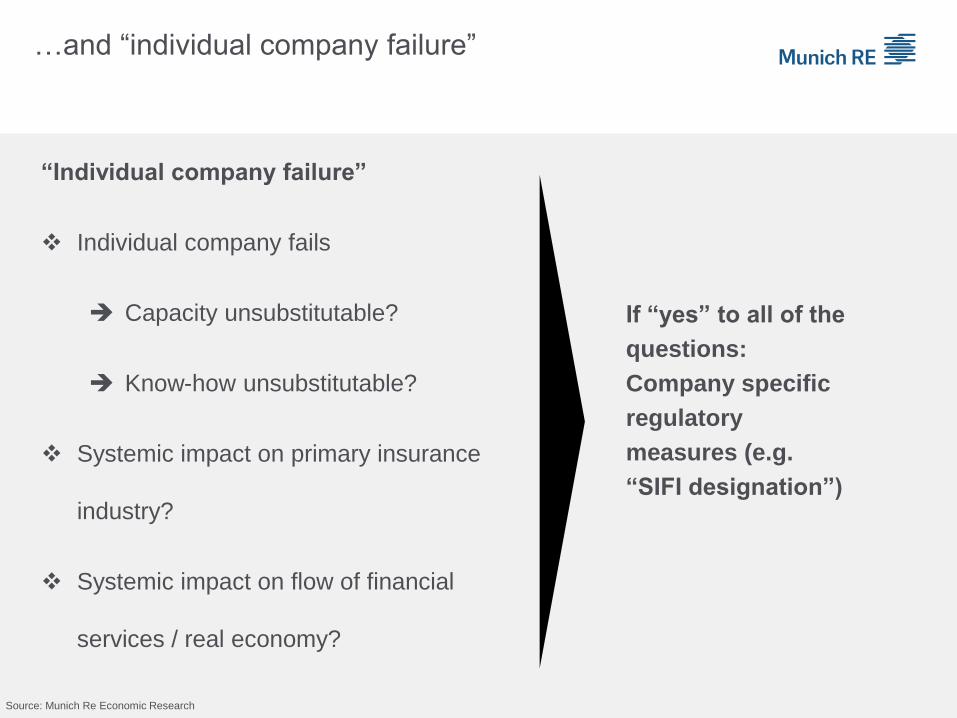

…and “individual company failure”

If “yes” to all of the

questions:

Company specific

regulatory

measures (e.g.

“SIFI designation”)

“Individual company failure”

Individual company fails

Capacity unsubstitutable?

Know-how unsubstitutable?

Systemic impact on primary insurance

industry?

Systemic impact on flow of financial

services / real economy?

Source: Munich Re Economic Research

Summary: The social and economic value of insurance

39

Source: Munich Re Economic Research

• The insurance industry is of utmost importance for the

functioning of any economy

• However, this does not imply systemic relevance of

individual insurance companies

1

• Insurance coverage is key for economic recovery after

natural catastrophes

• Especially emerging market economies would benefit from

increasing insurance penetration

2

• The social and economic value of insurance is obvious, but

often misunderstood

• Having, communicating and living values will be key 3