apresentação do powerpoint - fibria · pdf filetoday, according to public...

TRANSCRIPT

Corporate PresentationAugust 2014

2

The information contained in this presentation may include statements whichconstitute forward-looking statements, within the meaning of Section 27A of the U.S.Securities Act of 1933, as amended, and Section 21E of the U.S. Securities ExchangeAct of 1934, as amended. Such forward-looking statements involve a certain degree ofrisk and uncertainty with respect to business, financial, trend, strategy and otherforecasts, and are based on assumptions, data or methods that, although consideredreasonable by the company at the time, may turn out to be incorrect or imprecise, ormay not be possible to realize. The company gives no assurance that expectationsdisclosed in this presentation will be confirmed. Prospective investors are cautionedthat any such forward-looking statements are not guarantees of future performanceand involve risks and uncertainties, and that actual results may differ materially fromthose in the forward-looking statements, due to a variety of factors, including, but notlimited to, the risks of international business and other risks referred to in thecompany’s filings with the CVM and SEC. The company does not undertake, andspecifically disclaims any obligation to update any forward-looking statements, whichspeak only for the date on which they are made.

Disclaimer

3

Company Overview1Pulp and Paper Market2Financial and Operational Highlights3

Agenda

Final Remarks4

4

Company Overview

5

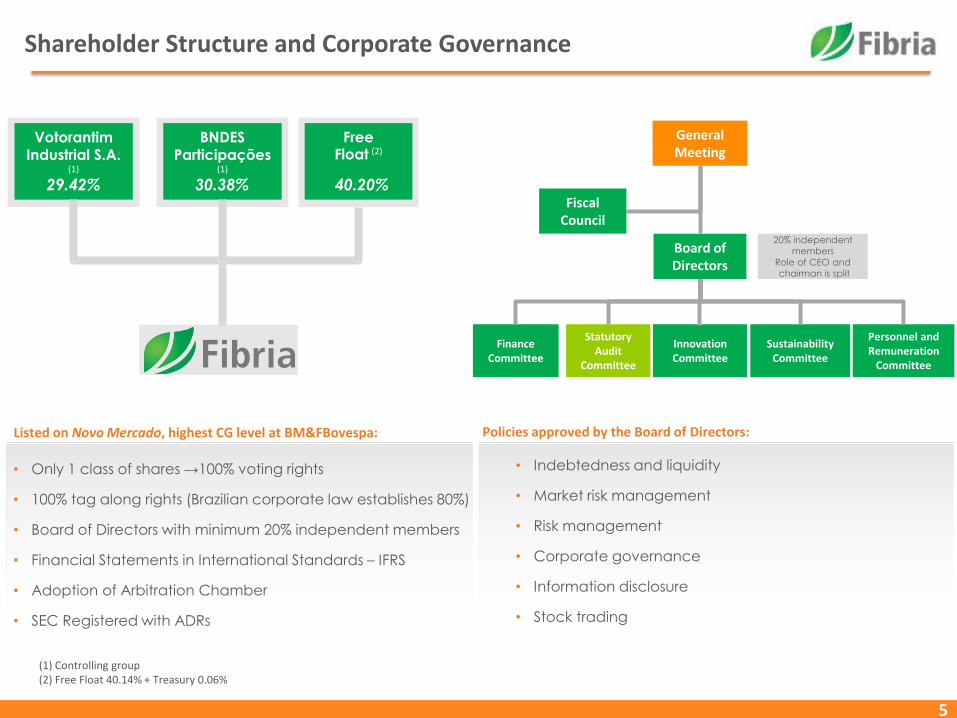

(1) Controlling group(2) Free Float 40.14% + Treasury 0.06%

VotorantimIndustrial S.A.

(1)

29.42%

BNDESParticipações

(1)

30.38%

FreeFloat (2)

40.20%

• Only 1 class of shares →100% voting rights

• 100% tag along rights (Brazilian corporate law establishes 80%)

• Board of Directors with minimum 20% independent members

• Financial Statements in International Standards – IFRS

• Adoption of Arbitration Chamber

• SEC Registered with ADRs

• Indebtedness and liquidity

• Market risk management

• Risk management

• Corporate governance

• Information disclosure

• Stock trading

Fiscal Council

Board of Directors

20% independent

members

Role of CEO and

chairman is split

Innovation Committee

Statutory Audit

Committee

Finance Committee

Sustainability Committee

Personnel and Remuneration

Committee

General Meeting

Listed on Novo Mercado, highest CG level at BM&FBovespa: Policies approved by the Board of Directors:

Shareholder Structure and Corporate Governance

6

A Winning Player

Port Terminal Pulp Unit

Três Lagoas

Santos

AracruzPortocel

Caravelas

BelmonteVeracel

Jacareí

Superior Asset Combination Main Figures – 2Q14 LTM

Pulp capacity million tons 5,300

Net revenues R$ billion 7.1

Total Forest Base (1) thousand hectares 962

Planted area(1) thousand hectares 555

Net Debt R$ billion 6.7

Net Debt/EBITDA (in Dollars)(2) X 2.4

Net Debt/EBITDA (in Reais) X 2.3

Source: Fibria(1) Including 50% of Veracel, excluding forest partnership areas and excluding the forest base linked to the sale of forest assets in Southern Bahia State and Losango. (2) For covenants purposes, the Net Debt/EBITDA ratio is calculated in Dollars.

7

Fibria’s Units Industrial Capacity

* Veracel is a joint venture between Fibria (50%) and Stora Enso (50%) and the total capacity is 1,120 thousand ton/year

8

Worldwide presence

Strong global customer base

Long-term relationships

Focus on customers with stable business

Customized pulp products and services

Sound forestry and industrial R&D

Focus on less volatile end-use markets such as tissue

Efficient logistics set up

Low dependence on volatile markets such as China

Low credit risk

100% certified pulp (FSC and PEFC/Cerflor)

Sales Mix by End Use - Fibria

Sales Mix by Region - Fibria

Europe42%

N. America

22%

Asia27%

Other9%

Region - 2Q14

Tissue49%

Printing & Writing

33%

Specialty18%

End Use - 2Q14

Highlights

30%20%

29% 29% 24% 18%26% 26% 30%

22% 28% 31% 30%19% 22%

37%46%

46% 41%

35% 44%43% 41% 36%

42%43% 35% 36%

46% 42%

22% 25%14% 20%

31% 28% 20% 23% 25% 26%21% 26% 26% 26% 27%

11% 9% 11% 10% 10% 10% 11% 10% 9% 10% 8% 8% 8% 9% 9%

4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

North America Europe Asia Other

Fibria’s Commercial Strategy

9

Pulp and Paper Market

10

Today, according to public information, there will be a 11% increase of the pulp market capacity between 2014 and 2016

SOFTWOOD(1)

25.5 MT

HARDWOOD(1)

31.1 MT

MARKET PULP(1)

56.6 MT+ =

2014-2016(3):

• New capacities: 6.0 mt

• Announced Closures: (0.13) mt

Net: 5.9 mt

2014-2016(2):

• New capacities: 0.7 mt

• Announced Closures: (0.35) mt

Net: 0.35 mt

2014-2016:

• New capacities: 6.7 mt

• Announced Closures: (0.5) mt

Net: 6.2 mt

(1) Source: PPPC Special Research Note May 2014 – does not include Sulphite and UKP(2) Projects included: Paper Excellence (70kt); UPM Kymi (170kt); Klabin (200kt); Sodra Värö (275kt)| Closures: Birla AV Terrace Bay (350kt)(3) Projects included: Maranhão (1.5mt); Montes del Plata (1.3 mt); Oji Nantong (700kt); Eldorado (200kt); CMPC Guaíba II (1.3 mt); Klabin Ortigueira (1.0mt) | Closures: April Rizhao

(130kt)

11

476kt

-24kt

101kt

346kt

Total North America Western Europe China

+6.3%

6M2014 vs. 6M2013

-2.9%

+22.3%

+3,2%

400

500

600

700

800

900

1000

1100

0

50

100

150

200

250

jul/

08

de

z/0

8

mai

/09

ou

t/0

9

mar

/10

ago

/10

jan

/11

jun

/11

no

v/1

1

abr/

12

set/

12

fev/

13

jul/

13

de

z/1

3

mai

/14

Spread Avg. Spread BHKP NBSK

Global Pulp Market Demand

Demand growth rateHardwood (BHKP) vs. Softwood (BSKP) (000 ton)

Hardwood demand will continue to increase at a faster pace than Softwood

Source: PPPC Source: PPPC

(1) Source: PPPC World 20 – June/2014

Shipments of Eucalyptus Pulp (1) NBSK vs. BHKP - Prices(1)

(1) Source: FOEX |Average spread in the last 5 years.

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Hardwood Softwood

2013 - 2018 CAGR:Hardwood: +2.8%Softwood: +0.7%

000 ton 1998 2008 2018

Growth

1998-

2008

Growth

2008-

2018

Hardwood 15.0 24.5 32.8 63% 34%

Eucalyptus 6.0 14.2 23.2 137% 63%

Softwood 17.6 21.6 24.8 23% 15%

Market Pulp 32.6 46.1 57.1

Avg. Spread: US$ 101

Spread Jun/14: US$ 184

12

Supply structural changes puts pressure on the industry

MARKET PULP CAPACITY RANKING 20141 (000T) MAIN PROJECTS

Project Country Capacity Timing Fiber Status

Arauco / Stora Uruguay 1.3Mt 2Q2014 BEKP Confirmed

CMPC Guaíba II Brazil 1.3 Mt 2Q2015 BEKP Confirmed

Klabin Paraná Brazil 1.5 Mt 2Q2016BEKP/

BSKP/FluffConfirmed

APP South Sumatra Indonesia 2.0 Mt 4Q2016 BHKP Confirmed

Fibria Três Lagoas II Brazil 1.75 Mt - BEKP Unconfirmed

COST CURVE EVOLUTION

USD

/Ad

t, 2

01

3 c

ost

leve

l

Cumulative Capacity Million t/a

Cost position of marginal

producer

1) Hawkins Wright – Outlook for Market Pulp, August 2014

Source: Hawkins Wright , Poyry and Fibria Analysis

- 1.000 2.000 3.000 4.000 5.000 6.000

Canfor

ENCE

Eldorado

Resolute

Domtar

Mercer

Sodra

Ilim

IP

Weyerhaeuser

Metsa Group

Paper Excellence

Stora Enso

UPM

CMPC

Georgia Pacific

Suzano

Arauco

APRIL

Fibria

Bleached Softwood Kraft Pulp (BSKP)

Bleached Hardwood Kraft Pulp (BHKP)

Unbleached Kraft Pulp (UKP)

Mechanical

5,300

13

Source: Hawkins Wright , Poyry and Fibria Analysis

Gross capacity addition should not be counted as the only factorinfluencing pulp price volatility

BH

KP

pri

ces

-ci

fEu

rop

e (U

S$/t

on

)

Gre

enfi

eld

cap

acit

y (0

00

to

n)

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2,0

0

100

200

300

400

500

600

700

800

900

1.000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Valdivia

APP Hainan

VeracelNueva Aldea

Santa Fé

Mucuri

FrayBentos

KerinciPL3

Três Lagoas

Rizhao

APP Guangxi

ChenmingZhanjiang

EldoradoMontes del

Plata

Maranhão

Guaíba II

14

Capacity closures DO happen…

-910

-85

-1.260

-1.180

-540-500

-105

-1.085

-405

-1400

-1200

-1000

-800

-600

-400

-200

0

2006 2007 2008 2009 2010 2011 2012 2013 2014-2015 E

Source: PPPC and Fibria

Closures of Hardwood Capacity Worldwide000 ton

15

Technical Age and Scale in the Market Pulp IndustryFurther closures are expected due to lack of adequate investments in the industry…

Hardwood (BHKP) Market Pulp Softwood (BSKP) Market Pulp

0

500

1.000

1.500

2.000

2.500

3.000

051015202530

PM Capacity, 1000 t/a

Technical Age, years

STRONG

2013/IQ

Weighted average

technical age 14.2 years

Weighted average

capacity 1184 000 t/a

Aracruz

Três Lagoas

Veracel

Jacareí

0

500

1.000

1.500

2.000

2.500

3.000

051015202530

PM Capacity, 1000 t/a

Technical Age, years

WEAK

STRONGWeighted average

technical age 21.2 years

Weighted average

capacity 503 000 t/a

2013/IQ

North American Pulp Mills Other Pulp Mills Closures Grade Switch On & Off

WEAK

16

… and when other expenses are plugged, we see no one but Fibria is generating positive free cash flow in the industry

Total Cash Cost of BHKP

delivered to Europe(US$/t)

528 493 502 453 479 464388 406 426

316 304 306 286 261 227

4840

7170 47 42

112 36 42

50 41 45 5667

6854

117

32

Cash Cost (US$/t) Delivery (US$/t)

Source: Hawkins Wright (Outlook for Market Pulp, March2014) | Fibria’s 2Q14 LTM considering a FX of R$/US$2.29.

501

SG&ATax/Others = 4

CAPEX

Interest

Working Capital = +9

Capacity(k tons): 660 595 1,775 585 565 355 1,005 2,410 1,960 1,095 12,750 = 31,930330 3,680 4,165

FOEX

Net price

809

17

China: Paper capacities expansion continues to go on

China corresponds to 2/3 of global tissue capacity expansion

Ktons 2013 2014E 2015E Total

P&W (woodfree) 385 150 576 1,111

Tissue 1,029 1,831 471 3,331

Cartonboard 2,128 1,650 180 3,958

Total 3,542 3,631 1,227 8,400

Source: Fibria and Independent Consultants

18

World Tissue Consumption, 1991-2013 (3)

Per Capita Consumption of Tissue by World Region (3)China's Share of Market Pulp (2)

24

15 15

12

7 65

1

0

5

10

15

20

25

30

N.America

WestEurope

Japan Oceania EastEurope

LatAm China Africa

9 11 1316

26

1721 20

23

79 10

12

22

1620 19

2110

1012

14

21

17

2223

23

0

2.000

4.000

6.000

8.000

10.000

12.000

2005 2006 2007 2008 2009 2010 2011 2012 2013

Eucaplyptus Hardwood Total

3.200

1.270945

773433

78 27

3.221

1.367

875858

446

16 120

500

1.000

1.500

2.000

2.500

3.000

3.500

BHKPTotal

LatinAmerica

Other* Indonesia USA Canada WesternEurope

5M2013

5M2014

Latin America is the leading exporter of BHKP to China, accounting to approximately 42% of China's total imports in 5M2014.

(Kg/capita/year)

(million t)(‘000s t) (kg/person/year)

Between 2005 and 2013, the Chinese market share of eucalyptus shipments increased by 14 p.p. (total market pulp: + p.p.)

* includes Russia, China, Thailand and New Zealand

0

5

10

15

20

25

30

35

1991 1996 2001 2006 2009 2010 2011 2012 2013N.America W.Europe E.Europe L.AmericaMiddle East Japan China Asia FEOceania Africa

LTM Growth Rate +4.2%

Benefiting From China’s Growth

China’s Hardwood Imports of BHKP by Country (1)

(1) PPPC – Pulp China(2) PPPC – W20. Coverage for chemical market pulp is 80% of world capacity (3) RISI

(In percentage)

19

Internal Consumption and Urbanization

China’s private consumption vs. exports(CNY trillion and annual % change) (1)

Chinese Urbanization Driver of Long-Term Growth(UN Population Projections, Millions)(2)

Sources: (1) the Economist. (2) RISI China Pulp Market Study.

Shift from exports to private consumption;

Positive effects on households income and rising standards of living.

20

Financial and Operational Highlights

21

39% 41%

35%

647679

594

2Q13 1Q14 2Q14

2Q14 Results

21

Cash Production Cost (R$/t)

1.669 1.6421.694

2Q13 1Q14 2Q14

1.291 1.277 1.271 1.269 1.188 1.334

2Q13 1Q14 2Q14

Production Sales

488 524

486 546 549 559

2Q13 1Q14 2Q14

Cash cost ex-maintenance downtimes Cash Cost

Pulp Production and Sales (‘000 t) Net Revenue (R$ million)

EBITDA (R$ million) and EBITDA Margin (%)

22

593 593 605 584648 645

900826

766678 699

2009* 2010* 2011 2012 2013 2Q14 LTM

4,600

5,0545,184

5,299 5,271 5.253

2009* 2010* 2011 2012 2013 2Q14 LTM

The maturity of synergies captured since Fibria’s creation improved its operating indicators…

+14%

PRODUCTION VOLUME (000 t)BEST PRACTICES AND OPERATING STABILITY

Historical Value Inflation Effect**

-21%

CASH COST (R$/ton)

Historical Value Inflation Effect**

-28%

SG&A (R$ million)STRUCTURE AND PROCESS SIMPLIFICATION

1,522

2,526

1,964 2,253

2,796 2.857

2009* 2010* 2011 2012 2013 2Q14 LTM

29%

40%34% 36%

40% 40%

EBITDA (R$ million) - EBITDA MARGIN (%)

* Excludes Conpacel | ** IPCA index considered to calculate the inflation effect

432 448 471 473 505 519

656 624 596549 545

2009* 2010* 2011 2012 2013 2Q14 LTM

23

Cash Production Cost (R$/t) – 2Q14

23

Utilities results boosted by energy sales.

(2Q14: R$ 36/t I 1Q14: R$ 18/t I 2Q13: R$ 14/t)

546

559

14

13

5 4

(27) 4

2Q13 Maintenancedowntimes

Wood FX Maintenance Utilities Others 2Q14

+ 2.2%

24

Indebtedness

Net Debt (Million)

3.3

2.4

2.3

3.02.4

2.4

9.9368.445 8.457

4.485 3.732 3.840

Jun/13 Mar/14 Jun/14

R$ US$

Total Debt and Interest Expenses (Million)

8.2536.970 6.681

3.725 3.080 3.033

Jun/13 Mar/14 Jun/14

R$ US$

Net Debt/EBITDA (US$)Net Debt/EBITDA (R$)

Debt Amortization Schedule (R$ million) Average Tenor (months) and Cost of US$ Debt (%p.a.)

4.7

4.13.8

140 137

109

Interest (R$)

1,776

1,467

3,243

1,068773 769

1,3551,215

923

545 453

48 6

1,302

Liquidez 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Pre-payment BNDES ECN ACC/ACE Voto IV Bonds

(cash)

(revolver)

5747 52

Jun/13 Mar/14 Jun/14

25

Fibria delivered the most significant leverage reduction in the LTM

Net Debt/EBITDA (x)(1)

7.2

6.3

5.6

4.7

3.93.6

2,9

3.2

4.24.8

5.2

4.74.5

3.4

3.1

3.33

2.82.4

2,3

2.5

2.0

3.33.0

4.2

4.8

4.8

5.7

4.75.0 5.0 5.1 5.1 5.2

4.8

2.2

2.2 2.12.0

2.4

2.5

2.32.5

2.3 2.42.2

2.4 2.4 2.6

1.7

1.1

1.9 1.81.9

2.0 2.3 2.5

2.8 2.93.3

3.4

2.9 3.02.8

2.9

1.7

1.4 1.61.8

2.7

2.2

2.7

3.44.1

4.6 4.3

3.73.1

3.8

Sep/09 Dec/09 Mar/10 Jun/10 Sep/10 Dec/10 Mar/11 Jun/11 Sep/11 Dec/11 Mar/12 Jun/12 Sep/12 Dec/12 Mar/13 Jun/13 Sep/13 Dec/13 Mar/14 jun/14

Fibria Arauco¹ CMPC Klabin Suzano

S&P BB+/Positive BBB-/Stable BBB-/Stable BBB-/Stable BB/Negative

Moody’s Ba1/Positive Baa3/Negative Baa3/Negative - Ba2/Stable

Fitch BBB-/Stable BBB/Stable BBB+/Stable BBB-/Stable BB-/Positive

(1) Fibria’s historical data in BRL.

Ratings

26

Interest expense and cost on foreign currency debt

Fonte: Fibria e Bloomberg

143

126

133137

123 125 123 122126

120

134

120 117109

94 9387 85

57

4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

6.3

6.8

6.0 6.0 5.9

6.3

5.85.5 5.5 5.5 5.4

5.2 5.2 5.2

4.7 4.5 4.6

4.13,8

4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

27

2.857

1.125 (1,409)

(386)

111

(20) (28)

Adjusted EBITDA Capex Interest(paid/received)

Working Capital Taxes Others Free Cash Flow

Fibria delivers one of the highest EBITDA/t and FCF/t of the industry

¹ Does not include asset sales, expenses on bonds repurchase, expenses related to the REFIS on subsidiaries profits abroad and tax credits from the BEFIEX program.

Free cash flow generation(1) - 2Q14 LTM (R$ Million)

Free Cash Flow per ton - 2Q14 LTM (R$/ton)

543

214

(268) (73)

21

(4) (5)

Adjusted EBITDA Capex Interest(paid/received)

Working Capital Taxes Others Free Cash Flow

28

2.00 1.76 1.67

1.95 2.16 2,22

562

844 810751 791

752

FX and Pulp Price explain 80% of Fibria’s EBITDA Margin

Average PriceFOEX (US$/t)

Exchange Rate Average (R$/US$)

EBITDA Margin

EBITDA (R$ million)

29%

40%

34% 36%40% 40%

1,522

2,526

1,964 2,253

2,796 2.857

2009 (1) 2010 (1) 2011 (1) 2012 2013 2Q14 LTM

(1) Excludes Conpacel

29

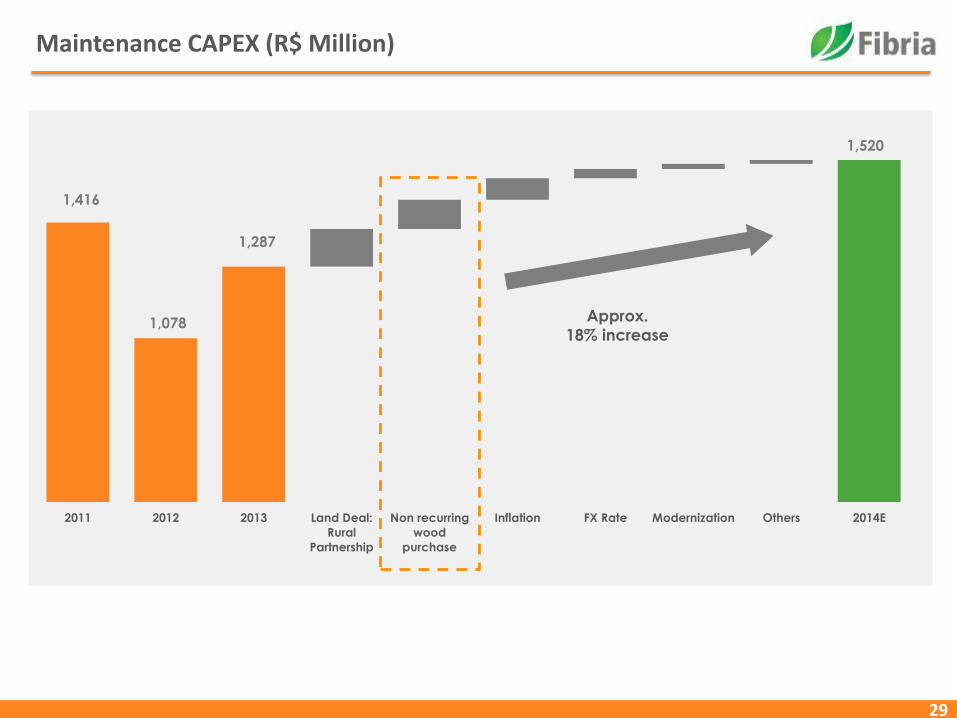

Maintenance CAPEX (R$ Million)

1,416

1,078

1,287

1,520

2011 2012 2013 Land Deal:

Rural

Partnership

Non recurring

wood

purchase

Inflation FX Rate Modernization Others 2014E

Approx.

18% increase

Cash Production Cost saw an increase of 17% over the past 5 years

Cash Production Cost (1) (R$/ton)

432448

471 473

505

2009 (2) 2010 (2) 2011 2012 2013

CAGR: + 4% 2014 Cash Production Cost:

• Wood costs will represent the main impact

• Non recurring increase mainly due to third party wood

• Operating excellence actions focused on keeping cash cost below inflation

• In 2015 the wood impact will be structurally eliminated

(1) Excludes Conpacel

Target to have the cash cost increase below inflation

30

31

Cash Production Cost (R$/t) – 2Q14

31

Utilities results boosted by energy sales.

(2Q14: R$ 36/t I 1Q14: R$ 18/t I 2Q13: R$ 14/t)

546

559

14

13

5 4

(27) 4

2Q13 Maintenancedowntimes

Wood FX Maintenance Utilities Others 2Q14

+ 2.2%

32

IPCA vs FX 2004 – 2014

32

(2Q14: R$ 36/t I 1Q14: R$ 18/t I 2Q13: R$ 14/t)

+ 2.2%0

20

40

60

80

100

120

140

160

180

200

IPCA USD

33

Final Remarks

34

PULP

- Growth with discipline

- Best portfolio of projects

BIO-ENERGY

- Complementary to pulp

- Ensyn

INDUSTRY

CONSOLIDATION ?

OTHER OPPORTUNITIES

- Portocel

- Land and forest

Potential Growth

Prospects

Fibria is seeking value creation for its shareholders with capital discipline

35

Key Highlights

Sound credit profile, with decreasing leverage ratios

Market leader with the lowest cash cost below industry average

Highly experienced and qualified management team

Highly recognized and awarded by industry specialists

36

Back up

37

Fibria 2024 – New Bond Issuance

Principal: US$ 600 millon

Issuance Date: May/2014

Coupon: 5.25% a.a.

Bookbuilding: 11.5x

Spread over T10Y: 275.0 bps

Issuance

US$ 600 million

Highlights

- SEC registered;

- IG document;

- Stretch Debt maturities;

- Fibria 2021 early redemption of US$430 million (78% of the total). Remaining outstanding : US$118 million.

Fibria 2024

- For liability management purposes only;

- Savings of US$ 5.5 MM in interest per year.

38

Hedge

Hedging Strategy

• Debt Hedge:

- Swap operations (currency and rate)

- Maturity aligned with original debt

- No margin call

• Operating Hedge:

- Net FX exposure protection in US$ in up to 18 months

- Current strategy: Zero Cost Collar

- No leverage

- No margin call

- 03/31/2014 data:

- Notional: US$ 932 million

- 41% of protected net exposure

- Maturity: up to 12 months

• All Fibria operations are registered at CETIP

Governance

• Hedging Policy approved by the Board of Directors and available at the Investor Relations website.

• Periodical follow up of the hedge portfolio by the Finance Committee

• Maximum % of exposed operational flow is defined according to the FX risk management policy.

• Governance, Risk and Compliance (GRC) Team:

- Report to CEO

- Responsible for monitoring policies compliance

- Independent from Treasury

ZeroCostCollar x NDF – Payoff

39

Fibria’s tax structure

Tax benefits (R$)

Fiscal - annual adjustment

Benefit Amount Maturity

Goodwill

(Aracruz

acquisition)

Annual tax deduction:

~R$89 million (tax)

Remaining Balance Jun/14:

R$1,228 million (base)

2018

Forestry Capex in

Mato Grosso do

Sul state

2014’s tax deduction related

to depletion: R$ 12,4 million

(tax)

Undefined

Tax loss carry forward and tax credits

Benefit Amount

Tax loss

carryforward

Balance up to Jun./14:

R$385 million (base)

Accumulated tax

credits

Balance Jun./2014:

-PIS/COFINS: R$535 million

- withholding tax (IR and CSLL):

R$242 million

- Befiex : R$ 897,6 million

Actual tax payment (cash basis)

2009 2010 2011 2012 2013

R$7 million R$16 million R$4 million R$15 million R$31 million

40

Liquidity Events: delivered as promised

1,361

5,715

1,045

850

836

1,403

1,268

1,851

1,625

EQUITY OFFERING FOREST SALE 2012 (1) FCF 2012 LAND DEAL FCF 2013 TOTAL

4.8 5.2 4.7 4.53.4 3.1 3.3 3.0 2.8 2.4 2,3

Dec/11 Mar/12 Jun/12 Sep/12 Dec/12 Mar/13 Jun/13 Sep/13 Dec/13 Mar/14 Jun/14

Net Debt/EBITDA (x) R$

(1) Losango and forestry assets and land in the south of Bahia State

2012 Bond prepayment

2013 Bond prepayment

Available

Sources (R$ Million) Uses (R$ Million)

2014 Bond prepayment

REFIS

41

Due to productivity gains in its forests, Fibria had the opportunity to explore this new ownership model

MAI* Pulp: (adt/ha/year)

10.6 10.9

12.1

15.0 15.0 15.0 15.0 15.0

2010 2015 2020 2025 2030 2035 2040 2045

FIBRIA’S GAINS IN IMACEL DUE TO INVESTMENTS IN BIOTECHNOLOGY (TONS OF PULP/HA/YEAR)

2012 field trials = 11.9

Conservative assumption

*MAI: Mean annual increment

Actions: • Genetic improvement• Excellence in forestry management• Superior industrial efficiency

42

Leadership position

(1) Fiber Consumption, Recycled Fiber and Pulp: RISI | Market Pulp, Hardwood and Eucalyptus: PPPC Special Research Note - May 2014

Recycled Fiber 234 million t

49% 51%

60%

18% 82%

58% 42%

40%

35% 65%

29%71%

Fiber Consumption403 million t

Pulp 169 million t

Chemical139 million t

Mechanical31 million t

Integrated Mills 84 million t

Market Pulp 56 million t

Hardwood29 million t

Other Eucalyptus Pulp producers:

13 million t

Softwood/Other 27 million t

Acacia/Other 10 million t

Eucalyptus19 million t

Industry Outlook(1)

43

Global Paper Consumption

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Developed Markets Emerging Markets

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Developed Markets Emerging Markets

CAGR 1996 – 2006Developed Markets: + 1.7%Emerging Markets : + 6.0%

85,291

117,611

15,548

37,474

P&W Consumption (000 tons)(1)

Tissue Consumption (000 tons)(1)

114,507

CAGR 2007 – 2016Developed Markets: - 4.0%Emerging Markets : + 4.1%

CAGR 1996 – 2006Developed Markets: + 2.4%Emerging Markets : + 6.9%

CAGR 2007 – 2016Developed Markets: + 1.4%Emerging Markets : + 6.7%

26,877

Source: RISI