appraisal report 4356 tamiami trail pc

TRANSCRIPT

Page -1-

Raymond H. Krasinski, MAI, ASA, RAA, GAA State‐Certified General Real Estate Appraiser RZ2720

2018

Raymond H. Krasinski, MAI, ASA, RAA, GAA State‐Certified General Real Estate Appraiser RZ2720

An Automotive Repair / Retail Building 4356 Tamiami Trail Port Charlotte, FL 33980

Restricted Appraisal Report:

2018 - 13576

Peachtree Appraisals 3238 Albin Avenue

North Port, FL 34286 (941) 426-5066 Fax (941) 426-8857

Prepared by:

4356 Tamiami Trail Port Charlotte, Florida Page -1- File # 13576

Peachtree Appraisals

Raymond H. Krasinski, MBA, RAA, GAA, IFA, ASA, MAI

State Certified General Real Estate Appraiser # RZ 2720 Florida General Appraiser Instructor # GA1000104 AQB Certified National USPAP Instructor #10913 E-mail: [email protected]

March 4, 2018 Mr. Greg Dion Dion Signature Realty 957 Dupin Ave Port Charlotte, FL 33948 Re: A Commercial Building 4356 Tamiami Trail Port Charlotte, FL 33980 Peachtree File #13576 Mr. Dion, Pursuant to your request, we submit our analysis on the above-referenced property. The premise of the appraisal assignment is to provide our opinion of the "As Is" Market Value of the subject property based on the effective date of February 26, 2018. The subject property is under contract lease. We have provided the value of the leased fee interest in the subject property. The intent of this appraisal to be in conformity with the Uniform Standards of Professional Appraisal Practice as a Restricted Appraisal Report; as required by the Uniform Standards of Professional Appraisal Practice (USPAP) and as adopted by the Appraisal Institute, the National Association of Independent Fee Appraisers, the American Society of Appraisers, and the Financial Institutions Reform, Recovery and Enforcement Act (FIRREA) as read and interpreted by this office. The Report is restricted to your use. Restricted Appraisal Reports are for one client only with no other intended users. In this respect, restricted reports tend to be for an individual or entity that is knowledgeable about the property and is quite familiar with it. The reporting option allows the appraiser to provide a much more brief and to the point analysis. Indeed, The Uniform Standards requires a notification that any reader of this

NAIFA Designated Member

American Society Appraisers

Designated Member

NAR Designated NAR Designated Residential Appraiser General Appraiser

Peachtree Appraisals

Residential and Commercial Valuations

3238 Albin Ave. North Port, FL. 34286

(941) 426-5066 Fax (941) 426-8857

Appraisal Institute Designated Member

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -2- File # 13576

Peachtree Appraisals

report may have difficulty understanding my opinions and conclusions without access to my (appraiser’s) work file. The following report contains the data, analysis, assumptions and limiting conditions on which we have based our conclusions. Your attention is directed to the "General Assumptions”, “Limiting Conditions" and "Appraiser’s certification" which are considered typical for this type of assignment and have been included within the text of this report. The subject is a commercial building containing a total of 6,600 square feet. As of the effective data, the subject is fully leased under the terms enumerated in the report. The improvements are zoned "CG" (Commercial General according to the zoning ordinances of Charlotte County. Based on the investigation described herein, and subject to the Extraordinary Assumptions cited, Assumptions and Limiting Conditions, the "As Is" Market Value of the Leased Fee Interest in the subject property as of the effective date of February 26, 2018 is:

“AS IS” MARKET VALUE OF THE “LEASED FEE” INTEREST AS OF FEBRUARY 26, 2018

ONE-MILLION-TWO-HUNDRED-FIFTY-THOUSAND-DOLLARS ----$1,250,000----

You are encouraged to read and understand the limiting conditions and both the extraordinary and general assumptions that govern the use and interpretation of this appraisal report. This letter by itself does not constitute an expression of value. It simply conveys the enclosed appraisal report to you and a copy of the report should always accompany this letter. Thank you for the opportunity to be of assistance. Should you require additional assistance on this or any other matter, please call at your convenience. Respectfully submitted:

_____________________________ Raymond H. Krasinski, MBA, RAA, GAA, IFA, ASA, MAI State Certified General Real Estate Appraiser RZ2720

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -3- File # 13576

Peachtree Appraisals

Table of Contents

COVER PAGE LETTER OF TRANSMITTAL SUMMARY OF IMPORTANT FACTS AND CONCLUSIONS SUBJECT PROPERTY PHOTOGRAPHS (EXTERIOR) TABLE OF CONTENTS ....................................................................................................................... 3 SUMMARY OF IMPORTANT FACTS AND CONCLUSIONS .............................................................. 4 PURPOSE AND FUNCTION OF THE ASSIGNMENT RESULTS ..................................................... 10 INTEREST APPRAISED .................................................................................................................... 10 DEFINITIONS ..................................................................................................................................... 10 INTENDED USE AND AUTHORIZED USER OF THE REPORT ...................................................... 12 VALUATION METHODOLOGY .......................................................................................................... 12 CONSIDERATION OF THE THREE APPROACHES TO VALUE ..................................................... 12 SCOPE OF WORK ............................................................................................................................. 13 ASSIGNMENT CONDITIONS ............................................................................................................ 13 EXTENT OF DATA COLLECTION, CONFIRMATION, AND REPORTING ...................................... 14 APPRAISAL CATEGORY .................................................................................................................. 14 PROPERTY RIGHTS/LEGAL CONSTRAINTS ................................................................................. 15 COMPETENCY .................................................................................................................................. 15 IDENTIFICATION OF THE SUBJECT PROPERTY .......................................................................... 16 LEGAL DESCRIPTION ...................................................................................................................... 16 PROPERTY TAX INFORMATION ..................................................................................................... 16 DELINQUENT TAXES ....................................................................................................................... 16 HISTORY OF THE SUBJECT PROPERTY ....................................................................................... 16 CURRENT CONTRACT AND LISTING INFORMATION ................................................................... 16 NEIGHBORHOOD DESCRIPTION .................................................................................................... 19 NEIGHBORHOOD TRENDS AND ANALYSIS CONCLUSIONS ....................................................... 20 LAND AREA ....................................................................................................................................... 22 FLOOD INFORMATION ..................................................................................................................... 23 EASEMENTS/ENCROACHMENTS ................................................................................................... 24 LEGAL RESTRICTIONS .................................................................................................................... 24 SITE ANALYSIS SUMMARY ............................................................................................................. 27 SUMMARY OF IMPROVEMENT ANALYSIS .................................................................................... 31 RETAIL MARKET PERFORMANCE .................................................................................................. 32 MARKETING TIME ............................................................................................................................. 34 REASONABLE EXPOSURE TIME .................................................................................................... 34 INCOME CAPITALIZATION APPROACH.......................................................................................... 41 CONTRACT RENT ............................................................................................................................. 42 EXPENSE ANALYSIS ........................................................................................................................ 43 RECONCILIATION AND FINAL ESTIMATE OF MARKET VALUE ................................................... 49 ADDENDUM ....................................................................................................................................... 50 ASSUMPTIONS AND LIMITING CONDITIONS ................................................................................ 65 APPRAISER’S CERTIFICATION ....................................................................................................... 67 ................................................................................................................................................................

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -4- File # 13576

Peachtree Appraisals

Summary of Important Facts and Conclusions Property Name MaacoLocation 4356 Tamiami Trail Port Charlotte, FL 33980 Property Rights Appraised Leased FeeCounty Charlotte CountyAssessor’s Parcel Number 402226276002Land Area 1.34 Ac. 58,370 SF. Zoning "CG" (Commercial General)Occupancy 100%

Highest & Best Use As Vacant Retail / Commercial As Improved Retail / Commercial

Improvements

Property Type A Commercial Building Number of Buildings Gross Building Area 6,600 sf. Net Rentable Area 6,600 sf. Number of Units Three Year Built 1970 / 46 years Condition Average Estimated Exposure Time 6‐12 months

Final Value Conclusion

Appraisal Premise Interest Appraised Date of Value Value Conclusion

"As Is" Market Value Leased Fee February 26, 2018 $1,250,000

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -5- File # 13576

Peachtree Appraisals

Subject Photos:

Front (West Side)

South Side

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -6- File # 13576

Peachtree Appraisals

Subject Photos:

Rear (East Side)

North Side

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -7- File # 13576

Peachtree Appraisals

Subject Photos:

Tamiami Trail (looking South)

Tamiami Trail (looking North)

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -8- File # 13576

Peachtree Appraisals

Subject Photos:

Office area adjacent main Maaco waiting area Work area for vehicles

Work area for vehicles Work area for vehicles

Restroom Maaco office area

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -9- File # 13576

Peachtree Appraisals

Subject Photos:

Maaco Waiting Area Office area (Gorman tenant)

Work area (Maaco) Small area rented by taxi company

Rear yard storage and parking view West side of building

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -10- File # 13576

Peachtree Appraisals

RESTRICTED APPRAISAL REPORT

A Commercial Building 4356 Tamiami Trail

Port Charlotte, FL 33980

Purpose and Function of the Assignment Results

The purpose of the appraisal is to provide the appraiser’s best estimate of the "As Is" Market

Value of the subject property based on the effective date of February 26, 2018. As of the effective

date, we have provided an opinion of the market value of the leased fee estate based on

stabilized occupancy and the lease in place to the MAACO tenant and others. The date of this

report is March 4, 2018. The function of the appraisal is to assist the client in collateral evaluation

and internal decision making in connection with the acquisition or disposition of real or personal

property.

Interest Appraised The subject property is tenant occupied and subject to contract rental agreements as of the effective date. Based on this a leased fee analysis is judged to be applicable. We have analyzed any leases in effect to determine contract rent, and whether contract rent varied from market rent. We have analyzed the value of the leased fee estate.

Definitions Market Value1 means the most probable price, which a property should bring in a competitive, and open market under all conditions requisite to a fair sale, the buyer and seller, each acting prudently, knowledgeably and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale, as of a specified date, and the passing of title from seller to buyer under conditions whereby:

a. Buyer and seller are typically motivated; b. Both parties are well informed or well advised and each acting in what they

consider their own best interest; c. A reasonable time is allowed for exposure in the open market; d. Payment is made in terms of cash in U.S. dollars or in terms of financial

arrangements comparable thereto; and

1 1 OCC 12 C.F.R. Part 34.42(g); 55 Federal Register 34696, August 24, 1990, as amended at 57 Federal Register 12202, April, 9, 1992; 59

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -11- File # 13576

Peachtree Appraisals

e. The price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions granted by anyone associated with the sale.

A leased fee estate “a freehold (ownership interest) where the possessory interest has been granted to another party by creation of a contractual landlord‐tenant relationship (i.e., a lease).2

A fee simple estate "Absolute ownership unencumbered by any other interest or estate, subject only to the limitations imposed by the governmental powers of taxation, eminent domain, police power, and escheat” A leasehold estate "the tenant's possessory interest created by a lease” Subdivision Development Method “A method of estimating land value when subdivision development is the highest and best use of the parcel of land being appraised. When all direct and indirect costs and entrepreneurial incentive are deducted from an estimate of the anticipated gross sales price of the finished lots (or residences), the resultant net sales proceeds are then discounted to the present value at a market‐derived rate over the development and absorption period to indicate the value of the land.” Gross Retail Value "The sum of the separate and distinct market value opinions for each of the units in a condominium, subdivision development, or portfolio of properties, as of the date of valuation. The aggregate of retail values does not represent an opinion of value; it is simply the total of multiple market value conclusions. Also, called the sum of retail values, aggregate retail value, or aggregate retail selling price."

Stabilized Occupancy, “Occupancy at that point in time when abnormalities in supply and demand or any additional transitory conditions cease to exist and the existing conditions are those expected to continue over the economic life of the property; the optimum range of long‐term occupancy that an income‐producing real estate project is expected to achieve under competent management after exposure for leasing in the open market for a reasonable period of time at terms and conditions comparable to competitive offerings.”

2 Appraisal Institute (2010) .Dictionary of Real Estate Appraisal, 5th Ed., Appraisal Institute, Chicago, ILL.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -12- File # 13576

Peachtree Appraisals

Intended Use and Authorized User of the Report The report has been exclusively prepared for the client and may not be used or relied upon by any other party. Any party who uses or relies upon any information in this report, without the preparers’ written consent, does so at his or her own risk. Possession of this report, or a copy thereof, does not carry with it the right of publication. The subject property is a commercial building containing 6,600 square feet, and is located on 58,370 square feet (1.34 acres) of "CG" (Commercial General) zoned land. The function of the appraisal is to assist the client with internal decision making and business planning. The intended user of this report is the client:

Mr. Greg Dion Dion Signature Realty

957 Dupin Ave Port Charlotte, FL 33948

Valuation Methodology There are three classic approaches to determine the value of real property. We considered the intended use of the appraisal assignment results, the needs of the user (the context of use), the complexity of the property, and other pertinent factors such as assignment conditions. The following discussion indicates our rationale and approach to solving the appraisal problem.

Consideration of the Three Approaches to Value In order to estimate the market value of properties that are similar to the subject, the Cost, Sales Comparison, and Income Approaches can be employed. In this appraisal assignment, all three approaches to value have been considered; however, only the income approach to value was considered useful. The premise of the assignment is to determine the effect of a new tenant occupying the bulk of the property. This will result in a "net leased" property that would be offered in the market as an investment. The Income Approach is considered a reliable method as a probable buyer would base a purchase decision on the income generating potential of the property and an anticipated rate of return. The Sales comparison approach is only considered to the extent of identifying rates of return and discount. Substitute sale properties are only analyzed on the basis of "net rental" properties. The available quality and quantity of data for each valuation approach chosen was considered sufficient for development. It is our opinion this approach (these approaches) provide(s) a credible and supportable value estimate within the context of the intended use of the assignment results by the intended users.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -13- File # 13576

Peachtree Appraisals

Scope of Work We have visited the subject property to gather information about the physical characteristics and condition of the improvements that are relevant to the valuation problem and to gain an understanding of the site’s relationship to the neighborhood and general market area. Additionally, we investigated various economic indicators, and other market sources to determine the strengths and weaknesses of the local economy as it affects the value of the subject. Subject attributes that are relevant to the appraisal problem have been assembled and analyzed. These include data and analysis on the subject’s location, quality, and zoning. Market data researched has generally been constrained to the three‐year period immediately prior to the effective date. We conducted market research relevant to the appraisal process, including a survey of competitive properties, collecting comparable sales, and gathering other information pertinent to the valuation. We sought adequate market and economic data and used it if it was found to support market conclusions. We used judgment in the absence of available data or in instances where the collection of data was temporarily uneconomic in relation to its importance to the valuation problem. It is not intended that research for this assignment would be exhaustive; rather that it would produce adequate market data relative to the subject property and the appraisal problem, so that the final value estimate(s) would be accurate to established professional, client, and community standards as considered in conjunction with the intended use of the assignment results, or in other words that the assignment result would reasonably solve the clients appraisal problem given the context of the intended use. The property being appraised is a commercial building, last inspected on February 26, 2018. The appraisal problem to be solved is to estimate the "As Is" Market Value of the subject property based on the effective date of February 26, 2018. The function of the appraisal is to assist the client in collateral evaluation and internal decision making in connection with the acquisition or disposition of real or personal property. The property consists of an improvement of 6,600 square feet on 58,370 square feet or 1.34 acres of "CG" (Commercial General) zoned land. Additional information about the specifics of the assignment and data included in the report is delineated below:

Assignment Conditions The Uniform Standards of Professional Appraisal Practice, Standards Rule 2, requires that an appraisal report clearly and accurately discloses all assumptions, extraordinary assumptions, hypothetical conditions, and limiting conditions used in the assignment. Your attention is directed to the limiting conditions section of the report, which is considered typical for this type of assignment. Extraordinary assumptions presume as fact otherwise uncertain information about physical, legal or economic characteristics of the subject property; or about conditions external to the property, such as market conditions or trends; or about the integrity of the data used in an analysis. The

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -14- File # 13576

Peachtree Appraisals

characteristic that separates an extraordinary assumption from a typical assignment assumption is that if the extraordinary assumption is found to be contrary to the presumed fact, it would most likely affect the assignment results. In this appraisal assignment, there are no extraordinary assumptions. In this appraisal, there are no extraordinary assumptions. Hypothetical Conditions assume conditions contrary to known facts about physical, legal, or economic characteristics of the subject property; or about conditions external to the property, such as market conditions or trends; or about the integrity of the data used in an analysis. Hypothetical conditions are typically employed for the purpose of credible analysis, such as providing a current estimate of market value for a proposed structure that does not actually exist on the date of valuation. In this appraisal assignment, there are no USPAP Hypothetical Conditions.

Extent of Data Collection, Confirmation, and Reporting The value conclusions herein are based upon a review and analysis of the market conditions affecting real property, including vacant land data, recent sales and current listings of competing parcels, sales of individual competing improved properties, absorption data from competing projects, cost data from comparable projects, cost services, and other related data. This information has been obtained from public records, real estate sales people and brokers, commercial real estate databases, and data from company files of previous appraisals of similar projects. In addition, we have viewed both the interior and exterior of the subject to gather information about the physical characteristics and condition of the improvements that are relevant to the valuation problem. Market data investigated for this report was over the time period of the past three years and located in the Port Charlotte area. Data sources used in research included Integrated Realty Information System, Charlotte County public records, Multiple Listing Services, Win2Data, CoStar, LoopNet, and internal appraisal files among others.

Appraisal Category The Appraisal Standards Board of the Appraisal Foundation issued the revised Uniform Standards of Professional Appraisal Practice on January 1, 2016. One of the items covered in these requirements is the identification of appraisal reports in one of the following two categories:

1. Appraisal Report 2. Restricted Appraisal Report

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -15- File # 13576

Peachtree Appraisals

Unless otherwise noted, this report is a Restricted Appraisal Report as categorized under USPAP; as such, the information and conclusions provided are very brief and only intended for the named user. It may be difficult of impossible for a reader to properly understand the appraiser’s opinions and conclusions with access to data contained in the Appraiser’s work file.

Property Rights/Legal Constraints We were not provided with a survey. The subject's land size was obtained from public records. To our knowledge, other than road encumbrances and utility easements there are no encumbrances or easements that would adversely affect the value of the subject property.

Hidden Conditions We assume there are no hidden or unapparent conditions of the property, subsoil or structures that would render it more or less valuable than an otherwise apparently comparable property. We assume no responsibility for such conditions or for engineering that might be required to discover such conditions.

Personal Property No chattel is given consideration in this appraisal report.

Competency Under the Uniform Standards of Professional Appraisal Practice there is a competency provision, which states in part “Prior to accepting an assignment or entering into an agreement to perform any assignment, an appraiser must properly identify the problem to be addressed and have knowledge and experience to complete the assignment competently…”. If the appraiser lacks the knowledge or experience necessary for a particular assignment, this must be disclosed and the all steps necessary to complete the assignment competently must be taken. I Raymond H. Krasinski, MBA, RAA, GAA, IFA, ASA, MAI, have been appraising commercial projects since 1998. I have experience and knowledge regarding the proper methodologies and techniques to value the subject property. I believe that I am competent to accept and complete the assignment for the client given the context of the intended use stated herein.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -16- File # 13576

Peachtree Appraisals

IDENTIFICATION OF THE SUBJECT PROPERTY POSTAL ADDRESS 4356 Tamiami Trail Port Charlotte, FL 33980 COUNTY PROPERTY APPRAISER IDENTIFICATION # 402226276002 LEGAL DESCRIPTION 26 40 22 P-7-6 1.34 AC. M/L GROSS SUB PART LT 7 DESC AS COMM AT NE COR SEC 26 S 1326.74 FT FOR POB CONT W 155.4 FT S 270.21 FT FOR POB TH CONT S 83.55 FT SE 137.15 FT SW 200 FT TO NE ROW US 41 TH SE ALG ROW 49.61 FT TO N ROW SHERRY ST TH E ALG ROW 248.08 FT TO SW COR LOT 1 HARBOR EXEC. PARK TH N 226.51 FT NW 145.54 FT NW 145.88 FT TO POB 223/629 566/1196-1200 DC635/855 851/970851/979 1582/120 CD1774/277 *Source: Charlotte County Property Appraiser's and/or Court Clerk’s online database.

Property Tax Information As of January 1, 2017, (latest tax assessment), the subject property had a “just value” of $519,798. The taxes are estimated at $7,050 with an additional $1,580+‐ in non‐ad‐valorem assessments. There are no delinquent taxes.

Delinquent Taxes As of the effective date of this appraisal, the subject parcel has no delinquent property taxes.

History of the Subject Property A search of the local county records indicates the subject has not transferred in the previous 36‐months.

Current Contract and Listing Information As of the effective date of this report the subject property has an active listing in the amount of $1,400,000. Listing has been active for approximately three weeks. The existing lease has purchase option that is available after the second year of occupancy. The tenant MAACO (James McCulla) has the right to purchase the property for a value derived by appraisal.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -17- File # 13576

Peachtree Appraisals

AREA MAP

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -18- File # 13576

Peachtree Appraisals

Wide Area Aerial

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -19- File # 13576

Peachtree Appraisals

NEIGHBORHOOD DESCRIPTION A neighborhood is defined in Real Estate Appraisal Terminology, First Edition, 1975, page 137, by the American Institute of Real Estate Appraisers and the Society of Real Estate Appraisers, (now called Appraisal Institute), as follows:

"A portion of a larger community, or an entire community in which there is a homogeneous group of inhabitants, buildings, or business enterprises. Inhabitants of a neighborhood usually have a more than casual community of interest and a similarity of economic level or cultural background. Neighborhood boundaries may consist of well‐defined natural or man‐made barriers or they may be more or less well defined by a distance change in land use or in the character of the inhabitants".

A discussion and analysis of these various factors as they affect the value of the subject property follows.

Neighborhood Introduction The subject property is located along the east side of Tamiami Trail (U.S. 41) at the intersection Sherry Street in the unincorporated area of Port Charlotte. The subject’s neighborhood is about ½ mile east of the Palm Beach Boulevard downtown district of Fort Myers. The immediate vicinity of the subject consists primarily of single family residential homes. Commercial activity is relegated to the downtown district and is also spread in a radial spoke pattern along major thoroughfares in the area. The subject’s street is just such a thoroughfare. The general residential improvement in neighborhood is a modest residential home developed between 1960 and the present. The majority of homes are generally well maintained; however, an occasionally an area home will show distinct signs of deferred maintenance. The subject is convenient to community services, houses of worship, shopping, and major transportation routes.

Neighborhood Boundaries

North Olean Blvd.

South Peace River (Punta Gorda)

West Harbor Blvd.

East Kings Highway The boundaries are not exact; however, neighborhood characteristics, land uses, and predominant property types and values tend to change beyond this area.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -20- File # 13576

Peachtree Appraisals

Percentage Built-up and Trend The subject neighborhood is a mixture of commercial properties along the US Route 41 corridor surrounded by residential development consisting primarily of single‐family homes. The subject property is located on the eastern side of US Route 41. US Route 41 (Tamiami Trail) is a six‐lane highway that is in good repair. Most of the commercial property along this highway is separated from the road by a landscape buffer; businesses are accessed via service roads. The surrounding subdivisions consist primarily of single‐family residential homes developed during the 1960’s through the 1980’s. The areas around the US Route 41 corridor represent the original development of Port Charlotte. Subsequently, areas further in on each side of US Route 41 to the north and south have steadily developed with newer residential development. At the present time, commercial development is continuing along the U.S. Route 41 corridor to the north and south of the subject location.

Typical Improvement and Level of Maintenance Most of the commercial buildings in the area have been renovated, updated, and are more or less modern. There are still some older dated properties; however, this is rare. Both commercial and residential buildings are generally in overall average repair and vary from the 1920’s to modern day. Most are within 40 years of age. In general, real estate in the area appears to have average maintenance levels.

Public Services All typical public services are available to the area. Police and fire protection are provided by Charlotte County. Hospitals are located approximately 2 miles northeast of the subject property in Port Charlotte. At the time of appraisal, all public services were judged to be adequate and consistent with those available in the surrounding communities.

Neighborhood Trends and Analysis Conclusions The longer‐term outlook for the subject’s direct vicinity is generally positive. US Route 41 is the central business highway through the area. The subject has good exposure to the highway and is well located. Market activity along US 41 has been robust over the past year. The general outlook for the economy at large is positive.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -21- File # 13576

Peachtree Appraisals

SITE ANALYSIS

Aerial View

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -22- File # 13576

Peachtree Appraisals

Location The subject property is located along the east side of Tamiami Trail (U.S. 41) at the intersection Sherry Street in the unincorporated area of Port Charlotte, Charlotte County, Florida. Postal Address: 4356 Tamiami Trail Port Charlotte, FL 33980

Land Area The subject site consists of a parcel containing a total of 58,370 square feet or 1.34 acres (MOL). The site is irregular. The property has approximately 145’ of frontage along Tamiami Trail, and an average depth of 209’. The dimensions and size are taken from public records. The current improvement provides a land‐to‐building ratio of 4.20:1. Based on an analysis of similar properties, the subject does not appear to have excess or surplus land. The ratio of land area to the improvement appears to be adequate to support the subject’s use as a commercial building. A copy of the subject’s GIS plat is provided below as taken from the Charlotte County geographic information system:

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -23- File # 13576

Peachtree Appraisals

Topography Topography of the site is generally level and about the same as the road grade of Tamiami Trail Based on a visual inspection, drainage of the site appears adequate.

Flood Information Flood information is taken from public records. The property appears to lie in Zone “9AE” based on the FEMA Flood Maps. The “9AE” zone has the following definition from FEMA: Zone X “Areas determined to be outside 500‐year floodplain determined to be outside the 1% and 0.2% annual chance floodplains.”

Community Map Number: 120061

Community Panel Number: 0229F

Dated: 5/5/2003

Flood Zone: 9AE

Insurance Required: Yes

Soil and Subsoil A visual surface inspection of the property was made. I am not an expert in the field of wetland or subsoil analysis; therefore, assume no responsibility for hidden or unapparent conditions beyond the area of my expertise. We disclaim responsibility for the detection of hidden or unapparent subsoil conditions at the subject property. The assumption that the soil has bearing capacity is based on the existing improvement, if any, or nearby improvements.

Utilities and Services The subject is served by Charlotte County utilities and currently has public water. Public sewer is available; and is in the process of being hooked up. A specific assumption of the appraisal is that the sewer is hooked up as of the effective date. Electrical services are provided by Florida Power & Light. The subject has three phase electric in place. Police and fire protection are provided by Charlotte County. The cost of utilities and services are similar to competing areas within Charlotte County and the general market area.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -24- File # 13576

Peachtree Appraisals

Environmental Nuisances and Hazards The property has been visually inspected for environmental contamination, such as underground storage tanks, drums of known or unknown contents, evidence of waste disposal such as sludge(s), paints, chemical residues, oil spillage, asbestos, etc. I am not an expert in determining the presence or absence of hazardous substances.

Easements/Encroachments The subject property has typical road, drainage and utility easements. No adverse easements or encroachments were observed or are known as of the effective date.

Legal Restrictions No title insurance commitment was included; a copy should be obtained for review. We are not aware of any legal restrictions that would adversely affect the subject’s value or marketability.

Zoning The subject land is zoned Commercial General according to the zoning ordinances of the Charlotte County. The designation allows a wide variety of commercial, retail and light industrial uses. Additionally, the subject is located in the Charlotte Harbor CRA and the highway overlay zone. The building currently complies with zoning and use regulations. The “MAACO” use was approved under the zoning code see letter below:

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -25- File # 13576

Peachtree Appraisals

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -26- File # 13576

Peachtree Appraisals

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -27- File # 13576

Peachtree Appraisals

Zoning – Land Use Summary The subject property is zoned “CG” (Commercial General). The zoning district offers a good array of uses for the subject lot. The maximum height is 70’. The subject’s current improvements appear to conform to the zoning district.

Functional Adequacy of the Site The overall utility of the site appears adequate to support its use as a commercial building. Ingress/egress is accomplished through a curb cut along Tamiami Trail. The parking lot contains about 10 spaces in common. The subject appears to have adequate room for parking and maneuvering.

Street Improvements Tamiami Trail is a six‐lane, two way, divided highway that generally runs northeast/southwest along the southwestern property line of the subject. The road appeared to be maintained in average condition at the time of our property visit.

Site Analysis Summary The subject property is located along the east side of Tamiami Trail (U.S. 41) at the intersection Sherry Street in Port Charlotte, Florida and serves a substantial residential population base in the area. The building has access directly from Tamiami Trail There are no conflicts with adjacent land uses. The site has adequate ingress/egress and room for maneuvering. Site improvements, such as parking areas, landscape, shrubs, trees, and etcetera were in average condition at the time of our property visit. The overall appearance of the site gives the impression of average maintenance. There is no excess or surplus land. Under present market conditions, the marketing‐time, per conversations with Realtors in the area, for buildings similar to the subject is 6‐12 months.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -28- File # 13576

Peachtree Appraisals

Improvement analysis

Building Sketch, first floor

Defined AreasMAACO Auto 5,000Gorman (Office) 1,100Bluebird Cap 500Total Area 6,600

**Layout is approximate and for illustration only.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -29- File # 13576

Peachtree Appraisals

Improvement Description

BUILDING DESCRIPTION

Property Name: OHG Building

Property Address: 4356 Tamiami Trail Port Charlotte, FL 33980

Property Type: Mixed Use

Overview: The subject improvements consist of a commercial building containing 6,600 square feet of area. The main part of the building will be occupied and built out by a MAACO Auto painting franchisee. The right‐hand side of the building includes an 1,100‐square foot office occupied an accounting firm. Additionally, there is an office and storage area of approximately 500 square feet rented to Bluebird taxicab company.

Construction: Single story steel over I‐beam trusses with purlins. Monolithic concrete slab foundation.

Quality: Average

Year Built: 1970 (46 years)

Year Renovated: The subject office area was renovated in 2006.

Condition: Average

Effective Age: 20 years

Remaining Economic Life: 30 years

Deferred Maintenance: No significant deferred maintenance was observed during our inspection of the property. There are minor paint and cosmetic items noted. Nothing that would be significant to value.

Capital Expenditures: As of the effective date, the tenant “MAACO” is anticipated to have substantially completed the build‐out and

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -30- File # 13576

Peachtree Appraisals

installation of components necessary for its business activities.

FOUNDATION AND EXTERIOR

Foundation: Poured monolithic concrete slab on spread footer.

Structural Frame: Steel I‐beam

Exterior Walls: Metal and stucco

Windows: Few windows, single hung and tilt out, glass in metal frames. Metal frame doors (steel clad, solid core).

Roof Cover Metal

INTERIOR Interior Layout See Drawing

Floor Cover: floor covering in the office areas is commercial style

carpeting with tile or linoleum in the restrooms. The warehouse is sealed concrete.

Walls: Interior walls are drywall, taped and painted, generally a “smooth wall” finish.

Ceilings and Ceiling Height: Interior ceiling heights in the office areas is 8 feet with a drywall ceiling. Interior clear height in the warehouse is about 14 feet to the underside of the metal trusses.

Lighting: Various fluorescent fixtures, predominantly mounted on the metal trusses.

Restrooms: Adequate restrooms: average quality fixtures in the offices/

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -31- File # 13576

Peachtree Appraisals

MECHANICAL SYSTEMS: Heating and Cooling: Package HVAC units. Offices each have separate systems.

Electrical: 400 AMP, three phase.

Plumbing: Central water and sewer system.

Fire Sprinkler: None

Elevators/Escalators: None

Security: Central Station.

SITE IMPROVEMENTS AND PARKING Site Improvements: Exterior lighting

Parking: Surface parking, about 20 spaces in common

Average condition.

PROPERTY INSPECTION Level of Inspection The interior and exterior of the subject building(s) were

inspected. We did not inspect the roof or mechanical systems and due to our lack of expertise in engineering and contracting, we are not qualified to ensure the condition of the systems or any other structural components. According to tenants and/or the owner, all structural and mechanical systems are operating efficiently and effectively.

Summary of Improvement Analysis The subject building is classified as a mixed‐use building with 8 marked parking spaces in front of building, with unmarked space (approximately 25) and additional open areas on each side. As of the effective date, the building will be occupied by an auto paint facility, an office use and a taxicab company.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -32- File # 13576

Peachtree Appraisals

MARKETABILITY ANALYSIS The section below discusses the market attributes of the area as well as the subject’s submarket and the marketability of the subject property based on its current use. The section elaborates on the overall market sector that the subject is a part of and discusses the subject and its competitive advantages, disadvantages, economies and diseconomies relevant to the valuation.

MARKETABILITY ANALYSIS The section below discusses the market attributes of the area as well as the subject’s submarket and the marketability of the subject property based on its current use. The section elaborates on the overall market sector that the subject is a part of and discusses the subject and its competitive advantages, disadvantages, economies and diseconomies relevant to the valuation.

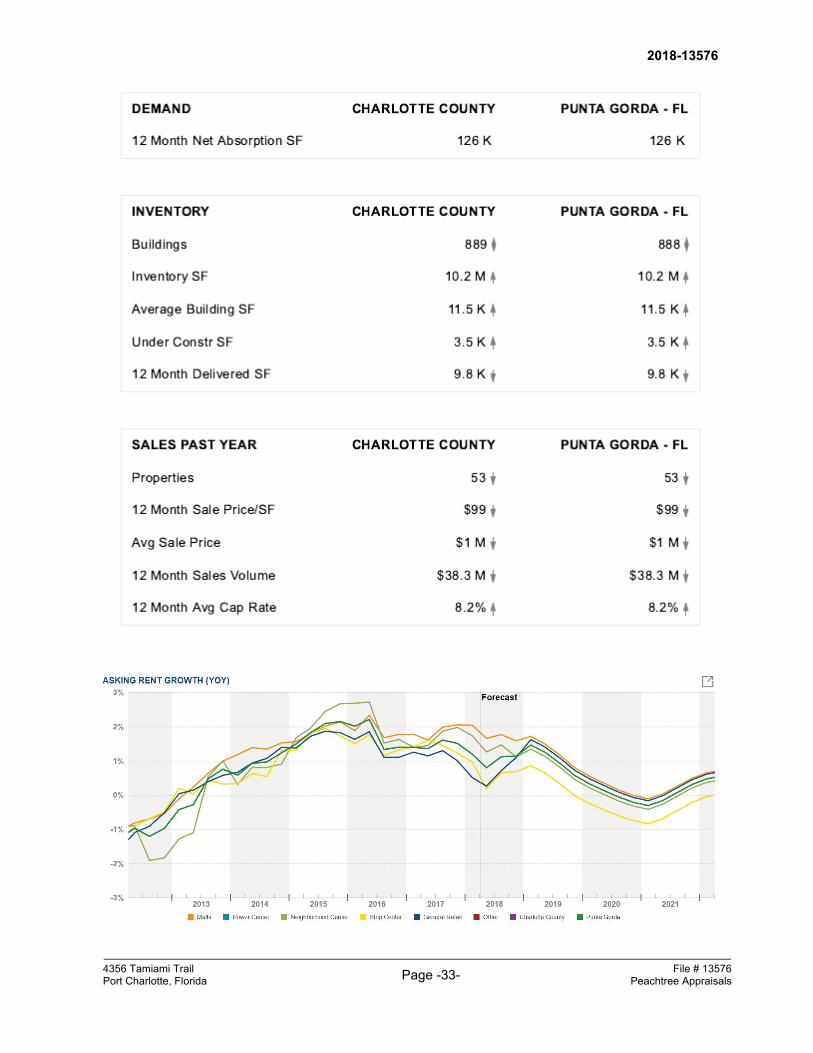

Retail Market Performance The following report is from CoStar and delineates the Charlotte County / Punta Gorda market performance for retail properties. The subject is classified as retail/automotive service.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -33- File # 13576

Peachtree Appraisals

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -34- File # 13576

Peachtree Appraisals

CONCLUSION: The initial part of the summary shows average rents at $14.93 per square foot and rising. The vacancy rate at 4.3% is declining, and availability is declining. The 12‐month absorption was 126,000 square feet. Forecast rent growth is between 1% and 2% per annum. The 12‐month outlook for the Punta Gorda / Port Charlotte Retail market looks fairly stable. CoStar predicts a cyclical pattern to rent growth with a high near the end of 2018 and a slight decline over 2019 into 2020. This is asking rent, which is following a cyclically stable pattern. Absorption is anticipated to remain positive. The overall outlook for the retail market in the subject’s locale is considered positive.

Marketing Time Conversations with local Realtors and real estate appraisers confirm the general weakness throughout the market and indicated that properties of this nature have previously sold within a 6‐12 months month period. Typical lease‐up time for similar properties is estimated at 3 to 6 months. Based on our observations we estimate a sale marketing time for the subject between 6‐12 months.

Reasonable Exposure Time Per the Appraisal Standards Board of the Appraisal Foundation – Statement #6 as contained in the Uniform Standards of Professional Appraisal Practice, exposure time may be defined as the estimated length of time the property interest being appraised would have been offered on the market prior to the hypothetical consummation of a sale at market value on the effective date of the appraisal. Exposure time is a retrospective estimate based on an analysis of past events in a competitive open market. Thus, reasonable exposure time is not synonymous with a marketing time estimate as it is assumed to have occurred prior to the date of valuation. Inherent in the market value estimate is not that the property will sell within the estimated marketing time, but that it would have sold assuming prudent marketing within some reasonable exposure time prior to date of valuation. In this instance, we have concluded that the reasonable exposure time occurring prior to the date of valuation that would have resulted in a consummation of a sale at the market value estimate would have been approximately 6‐12 months.

Marketing Expenses Marketing expense varies in the process of its disposition (i.e., owner’s sale, and or Realtor assistance). Typical charge for professional marketing skills ranges from a low of 5% to a high of 10% of the gross selling price. Selling costs for the subject are estimated at 10%.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -35- File # 13576

Peachtree Appraisals

Purchasers Typically, investors and individual users are purchasers of this type of real estate. There is risk which is anticipated in the acquisition of real estate, therefore, the return on the investment is expected to exceed that of more conservative investment opportunities such as, saving accounts, bonds, CD's, IRA's etc. In general, real estate with proper management techniques, has a tendency to appreciate via increasing its effective gross income and thereby increasing its overall net operating income proportionally, providing further incentive for the investor.

Financing Financing may be obtained from numerous sources within the market place such as local lending institutions and owner financing. Although since the economic downturn, a credit crunch of sorts has occurred. This had made financing more difficult to obtain. The financing parameters are typically 60% to 90% loan‐to‐value ratios, a 1.10 to 1.35 debt coverage ratio, 15 to 30 year amortization, with an interest rate of around 5.25% to 9.50%. Discussions with representatives of local lending institutions and analysis of national market trends indicate that these are typical loan parameters for a property such as the subject. In general, properties similar to the subject have done well in the Charlotte County market over the previous five years and have experienced reasonable market absorption in the general region.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -36- File # 13576

Peachtree Appraisals

HIGHEST AND BEST USE ANALYSIS The highest and best use is defined as:

“The reasonable and probable use that supports the highest present value, as defined, as of the effective date of the appraisal. Alternatively, that use, from among reasonably probable and legal uses, is found to be physically possible, appropriately supported, and financially feasible and which results in highest land value."

The definition immediately above applies specifically to the highest and best use of the land. It is to be recognized that in a case where a site has existing improvements on it, the highest and best use may very well be determined to be different from the existing use. The existing use will continue, however, unless and until land value at its highest and best use exceeds the total value of the property in its existing use. Implied within these definitions is recognition of the contribution that specific use to community environment or to community development goals in addition to wealth maximization of individual property owners. Also implied is that the determination of highest and best use results from the appraiser's judgment and analytical skill, i.e., that the use determined represents an opinion, not a fact to be found. In appraisal practice, the concept of highest and best use represents the premise upon which value is based. In the context of most probable selling price (market value) another appropriate term to reflect highest and best use would be most probable use. In the context of investment value an alternative term would be most profitable use."

Highest and Best Use as Vacant This analysis assumes that a parcel of land is vacant or can be made vacant through demolition of the improvements. The question this analysis answers are what type of improvement should be constructed. To represent the highest and best use (as vacant or improved), a use must meet four criteria. The four tests that a use must meet to qualify as the highest and best use are: 1. Legally permissible 2. Physically possible 3. Financially feasible 4. Maximally productive The highest and best use, as vacant, is to develop the site under the zoning code. Development of the site with a consumer‐oriented use will take advantage of its exposure to traffic and the business district of Port Charlotte.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -37- File # 13576

Peachtree Appraisals

Highest and Best Use as Improved Legally Permissible: The subject property is 1.34 acres in size, it is improved with a commercial building containing 6,600 square feet. The subject property as improved complies with current zoning regulations and is legally permissible. Physically Possible: The improvements were built in 1970 and have been maintained in average fashion over the years. The design, layout, construction materials and overall market appeal are generally consistent with other similar use properties in the area. The subject as it exists is obviously physically possible. The lot coverage and layout of the improvements provide an adequate use of the land that is consistent with other improved properties in the immediate vicinity. There is no surplus or excess land indicated. Financially Feasible: The existing improvement complies with legal restrictions and is physically adequate for its use. Analysis of vacant parcels in the area indicate the current improvement adds value well beyond that of the vacant land; therefore, the current improvements are financially feasible. Maximally Productive: Based on the current zoning, location, physical attributes and condition of the subject, it is clear that the improvements add value well beyond that of only the raw land, and there is no alteration or additional improvement that would significantly increase the return to the land. Additionally, there is no change in zoning, or other legal use that provides a cost/benefit greater than the existing structure. Thus, by definition, the highest and best use of the subject as improved is to remain a commercial building.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -38- File # 13576

Peachtree Appraisals

THE APPRAISAL PROCESS The estimation of a real property's market value involves a systematic process in which the problem is defined, the work necessary to solve the problem is planned, and the data required; is acquired, classified, analyzed and interpreted into an estimate of value. In this process, three approaches are used by the appraiser to estimate value. They are: THE COST APPROACH THE SALES COMPARISON APPROACH THE INCOME APPROACH The cost approach is a method in which the value of a property is derived from creating a substitute property with the same utility as the subject property. In the Cost Approach, the appraiser must estimate the market value of the subject site as if vacant, by using the direct sales comparison approach, then estimate the reproduction cost new of the improvements. Depreciation from all sources is estimated and subtracted from the reproduction cost new of the improvements. The depreciated reproduction cost of all improvements is then added to the estimated site value with the results being an indicated value by the cost approach. The sales comparison approach also referred to as the market approach, involves the comparison of similar properties that have recently sold or similar properties that are currently offered for sale, with the subject property. The basic principle of substitution underlies this approach as it implies that an informed purchaser would not pay more for a property than the cost to acquire a satisfactory substitute property with the same utility as the subject property in the current market. These properties are compared to the subject with regard to differences or similarities in time, age, location, physical characteristics, and the conditions influencing the sale. The notable differences in the comparable properties are then adjusted to the subject property to indicate a value range for the property being appraised. The principle of increasing and decreasing returns is important in identification of comparable properties and the principle of contribution is the heart of the adjustment process in determining the effect that the presence or absence of some characteristic has on the sale price. When sufficient sales data is available, these adjustments are best determined by the actions of typical buyers and sellers in the subject’s market place. This value range, as indicated by the adjusted comparable properties, is then reconciled into a final indicated value for the subject property by this approach. The income capitalization approach is a process that discounts anticipated income streams (whether in dollar income or amenity benefits) to a present worth figure through the capitalization process. The appraiser is again faced with obtaining certain data related to the subject and comparing it to similar physical, functional and economic properties. Comparable rental information is analyzed to estimate potential gross income (actual and/or comparative) to determine a projected net income stream. The appraiser must then estimate a capitalization rate,

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -39- File # 13576

Peachtree Appraisals

either through extraction from the market or using other available techniques. The net income stream is then capitalized into an indicated value by this approach. The value estimates as indicated by the three approaches are then reconciled into a final estimate of the property's value. In the final reconciliation, the appraiser must weigh the relative significance, defensibility, amount and accuracy of data, and applicability of each approach as it pertains to the type of property being appraised and that best approximates the type of value being sought in the appraisal.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -40- File # 13576

Peachtree Appraisals

This page intentionally left blank

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -41- File # 13576

Peachtree Appraisals

INCOME CAPITALIZATION APPROACH The income capitalization approach relates to an investor's thinking and motivation, as to the future benefits of ownership, and is the basic tool for the valuation of income producing real estate. It is based on the principle of substitution, which are the rights to future benefits accruing to ownership. The income producing property is typically purchased for investment purposes and the projected net income stream is the critical factor affecting this market value. The income capitalization approach is practical only when the income stream can be estimated. This income estimate may be developed and supported by a comparison in the local market. An investor purchasing income producing real estate is, in effect, trading a sum of present dollars for a right to the stream of future dollars. There is a relationship between the two, and the connecting link is the process of capitalization. The function of capitalization is to translate an income projection into a present capital value indication. The valuation by the income capitalization approach consists of the following steps: 1. Estimate the economic rent for the subject property through a market analysis of

competitive projects to arrive at a gross income estimate; 2. Estimate the vacancy and collection losses for the income projection period; 3. Deduct the estimated vacancy and collection losses and the annual operating expenses

from the gross income estimate for an estimated net income before recapture; 4. Determine the appropriate capitalization technique and gather market supported data

for its application. 5. Capitalize the resulting net income figure by an appropriate capitalization rate in order to

obtain an indicated value of the property.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -42- File # 13576

Peachtree Appraisals

Contract Rent The subject’s net rentable area is 6,600 square feet. As of the prospective date, the building is anticipated to be 100% occupied by three tenants. The subject’s rent roll is reproduced below:

Tenant Gorman is on a rolling annual lease, and the cab company is month to month. MAACO is on a 5‐year lease with two, 5‐year renewal options. The lease is anticipated to renew as there was a significant expense in tenant improvements, and the zoning to allow an automotive repair along the main road is fairly rare. The lease is level over the term and increases 10% with each renewal. Terms are generally “net, net”. The owner is responsible for upkeep and repair of the structural roof and foundation of the building, and the annual property taxes. All other costs and maintenance are carried by the tenants. The MAACO lease carried a $4,000 per month concession ($24,000 total) over the first 6‐months. This does not re‐occur in the renewal options.

Vacancy & Collection Loss

The income potential estimated above is what one would expect to receive at 100% occupancy. In practice, a building is not expected to be fully occupied throughout its useful life or any major portion of it. Frequently, a new tenant is not found after an old tenant vacates, resulting in a loss of rental income due to vacancy. Additionally, rental loss from a tenant’s inability or unwillingness to pay may accumulate before the owner can resort to remedial measures, resulting in effective vacancy. With occasional exceptions, we recognize an allowance, which is usually estimated as a percentage of potential gross income, and which varies according to the type of property, the tenancy and general conditions of the property and the market. Credit allowance takes into consideration the loss in rent due to collections of rent. Given the subject’s current occupancy and status as well as its history and market trends, we estimate the subject property to have fairly consistent experience going forward. Therefore, it seems reasonable to reconcile only for frictional vacancy at a rate of 5.0% overall.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -43- File # 13576

Peachtree Appraisals

Expense Analysis An integral part of the income approach is an estimate of the operating expenses for the property. The expense estimates are based on the data provided by the property owner, income statements of similar properties, conversations with people who are familiar with properties similar to the subject and discussions with firms, governments, and individuals that service the subject property and similar properties. Expenses typically include fixed expenses such as real estate taxes and insurance, as well as variable expenses such as, management, repairs/maintenance, utilities, reserves, and administrative expenses.

Real Estate Taxes

The subject’s 2016, the total property taxes are estimated at $8,580. We have used that figure with an annual 2% estimated increase. Under the current lease, this expense is the responsibility of the property owner.

Insurance

Structural and liability insurance for properties similar to the subject varies based on the construction type, size, fire resistance, security measures such as alarms and fire sprinklers as well as many other factors. In general, similar properties have exhibited rates between $0.25 and $1.10 per square foot, with most between the $0.30 to $0.75 per square foot range. We have estimated a cost of $0.58 per square foot or $3,800 per year. This cost is reimbursed by the tenants.

Management

A management expense, for outside management, is generally based on a percentage of effective gross income. This is generally a fee for a management agent as well as costs of leasing commissions. Typically, leasing commissions run from 1% to 5% in the local market. The subject has zero cost history in this category over the last year and only a small portion of the property may become available for lease in the near future. We have estimated the cost near 2.2% of the annual effective gross income; which equates to $2,500 per year.

Reserves

A prudent manager should establish a fund for replacement of certain components. However, this is rarely actually done on buildings of the subjects’ size in this market. We have not allocated any costs in this section.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -44- File # 13576

Peachtree Appraisals

Utilities

Utilities include electric service, water, sewer, and trash removal. Under a lease, the tenant would be responsible for all utilities. Therefore, no estimate is provided for this factor.

Maintenance and Repairs / Lawncare and Landscaping

Maintenance and Repairs account for all items of general and common area maintenance and repair, to include lawn care, landscaping, exterior painting, cleaning, HVAC contracts, and roof repairs. The owner is responsible for repairs to the roof and foundation. We have estimated an average annual cost basis of $1,000. This is not a reimbursed expense. We have estimated the $3,500 for general maintenance and lawn care / landscaping. The general maintenance and lawn care is a reimbursed expense.

Operating Expenses Summary

The foregoing operating expenses have been taken from market estimates and data contained within our appraisal files as well as actual data supplied on the expense history of the subject. The operating expenses we have enumerated indicate a total of $19,380 per year, $2.94 per square foot which is 17.1% of the effective gross income. The operating expenses include some costs that are recaptured pass through costs and some that are not. The following section elaborates on pass through costs.

Expense Pass-through (Reimbursement)

The expenses we have analyzed are typical and similar for commercial style buildings in the subject’s condition. The overall expenses equate to $2.94 per square foot. We estimate the subject will typically rent on double net lease terms. Under those terms most of the costs will be recaptured with the exception of the management fees and taxes. The owner is also responsible for repairs and maintenance to the building foundation and roof. The recaptured costs amount to $1.11 per square foot or $7,326 in total. This is reflected as an expense reimbursement in the income proforma.

Potential Gross Income, Effective Gross Income, Net Operating Income

I have previously calculated the subject’s base rent at $17.00 per square foot. Additionally, the estimated passthrough expense recapture is $1.11 per square foot. This is an effective rent of $18.11 per square foot providing a Potential Gross Income estimate of $119,526. Vacancy and collection loss is estimated at 5% or $5,976 per year. Removing this figure from the Potential Gross Income yields the Subject’s estimate of Effective Gross Income at $113,550 per year. This is the revenue the property owner can expect to receive. The total estimate of Operating Expenses on an annual basis is $19,380 per year, $1.11 per square foot, 17.1% of the effective

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -45- File # 13576

Peachtree Appraisals

gross income. The remaining Net Operating Income, which is the income to the owner after the cost of operating the property but prior to any mortgage obligations is $94,170.

Net Operating Income (NOI)

We have previously estimated the operating expenses. The total estimate of operating expenses on an annual basis is $19,380, this provides a stabilized net operating income of $94,170. As the income is stabilized, we have used a direct capitalization methodology.

Discounted Cash Flow Analysis (DCF)

Discounted cash flow analysis analyzes the attractiveness of the subject property based on a yield rate to the investor. The analyst calculates the income and expenses over the holding period as well as a reversion (sale of the property). We have estimated a 7‐year hold for the typical investor. For our analysis, we have consulted Realty Rates, a published survey of investor discount rates for specific property types. The following list is from the 2nd quarter 2017 survey:

We find the most similar investment types on the list are the warehouse/distribution and R/D flex under the industrial, this accounts for the subject’s use as a body paint shop. These rates are range from 5.45% to 13.33% respectively with an average 8.86% to 10.10% respectively. Additionally, we considered suburban office, which aligns with the subject’s office uses as well as retail, which is the subject’s major draw. Finally, we considered convenience class gas stations

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -46- File # 13576

Peachtree Appraisals

and freestanding buildings which are somewhat allied with the subject’s vehicular use and its freestanding nature. In the end, we reconciled a discount / yield rate of 8.50%. A terminal capitalization rate of 7.25% was estimated for the reversion at the end of year seven. This is supported by the net sale pages in the addenda. Our DCF analysis follows:

4356 Tamiami Trail Port Charlotte, Florida Page -47- File # 13576

Peachtree Appraisals

Year

RevenuePotential Rental Income 112,200 112,200 112,200 112,200 123,420 123,420 123,420 # 123,420 Loss to lease ‐ ‐ ‐ Expense Reimbursement 7,326 7,473 7,622 7,774 7,930 8,088 8,250 8,415 Assumptions

Adjusted Rental Income 119,526 119,673 119,822 119,974 131,350 131,508 131,670 131,835 Current Lease term is five‐years with four years remaining.

Vacancy & Credit Loss (5,976) (5,984) (5,991) (5,999) (6,567) (6,575) (6,584) (6,592) There are two, Five‐year options. Reversion (Sale) occurs at

Other Income (Exp. Recap) ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ the end of the seventh year with two years left on

Effective Gross Income 113,550 113,689 113,831 113,976 124,782 124,933 125,087 125,244 the first renewal option.

Expenses Lease terms are double net, owner is responsible for

Real Estate Taxes 8,580 8,752 8,927 9,105 9,287 9,380 9,474 9,569 foundation and roof of structure and taxes only.

Property Insurance 3,800 3,876 3,954 4,033 4,113 4,196 4,279 4,365 Natural Gas ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ Electricity ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ Water & Sewer ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ Telephone/Internet/Cable ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ Trash Removal ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ Administrative & General 500 510 520 531 541 552 563 574 Repairs & Maintenance 2,500 2,550 2,601 2,653 2,706 2,760 2,815 2,872 Painting & Decorating ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ Grounds & Landscaping 1,500 1,530 1,561 1,592 1,624 1,656 1,689 1,723 Other ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ Management Fee 2,500 2,550 2,601 2,653 2,706 2,760 2,815 2,872 Reserves for Replacement ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐

Total Expenses 19,380 19,768 20,163 20,566 20,978 21,304 21,636 21,974

Net Operating Income 94,170 93,921 93,668 93,409 103,805 103,629 103,450 103,269

AssumptionsIncome Growth N/A 0.0% 0.0% 0.0% 10.0% 0.0% 0.0% 0.0%

Concessions 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Vacancy & Credit Loss 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0%

Tax Expense Growth 0.0% 2.0% 2.0% 2.0% 2.0% 1.0% 1.0% 1.0%

Oper. Expense Growth N/A 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0%

Management Fee 0.0%

Cost of Sale 7.0%

Year 1 2 3 4 5 6 7 8

Discounted Cash Flow Analysis ‐ 7 year hold4360 Tamiami Trail (OHG ‐ MAACO) Start Date: 2/2018

1 2 3 4 5 6 7 Reversion

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -48- File # 13576

Peachtree Appraisals

Reconciled Value Indication:

Immediate Costs

As‐Is Value Indication (Rounded)

1,246,659

‐

1,273,3868.50%1,290,3448.25% 1,237,8311,263,182

1,246,659

1,230,4161,256,7168.75%

Effective Gross Income (EGI), Expense, Net Operating Income (NOI) Sale / Yield Matrix

Terminal Capitalization Rate

7.00% 7.50%7.25%IRR

$1,250,000

1,221,714

1,205,869

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

1 2 3 4 5 6 7

Year

Expenses EGI NOI

The primary lease has a 10% increase at the end of year 4. The assumption is that the other two small leases will keep pace with that. Expense ratios are assumed to rise 2.0% per year both for property taxes and normal operational expenses. The table at right provides a sensitivity analysis for varying yield rates and terminal capitalization rates. The overall conclusion is the center rate at a 7.25% terminal capitalization rate with an 8.5% yield. This results in an indicated value of $1,246,659; rounded say $1,250,000.

4356 Tamiami Trail Port Charlotte, Florida Page -49- File # 13576

Peachtree Appraisals

Reconciliation and Final Estimate of Market Value The premise of the appraisal assignment is to estimate the current market value of the leased fee interest in the subject property. The report is for the client who is the current owner of the property and is familiar with the property to the extent that a restricted use appraisal is sufficient for their purposes. Based on this there is little necessity for elaborate analysis and explanation of the property itself. We have focused on the leased fee value of the property. Estimation of the real property's market value involves a systematic process in which the problem is defined. The necessary steps to solve the problem are planned, and the data required is acquired, classified, analyzed and interpreted into an estimate of value. We have relied totally on the income capitalization approach; however, provide some closed sales in the addendum to support the range of capitalization rates and as a check of reasonableness. The “net sales” indicate a range of value per square foot between $134.66 and $462.22 with an average of $307.01. The subject’s reconciled value is $189.39 per square foot. Therefore, based upon the foregoing data and analysis, in our opinion, the current Market Value of the Leased Fee Interest in the subject property as of the effective date of February 26, 2018 is:

MARKET VALUE OF THE “LEASED FEE” INTEREST AS OF FEBRUARY 26, 2018

ONE-MILLION-TWO-HUNDRED-FIFTY-THOUSAND-DOLLARS ----$1,250,000----

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -50- File # 13576

Peachtree Appraisals

ADDENDUM

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -51- File # 13576

Peachtree Appraisals

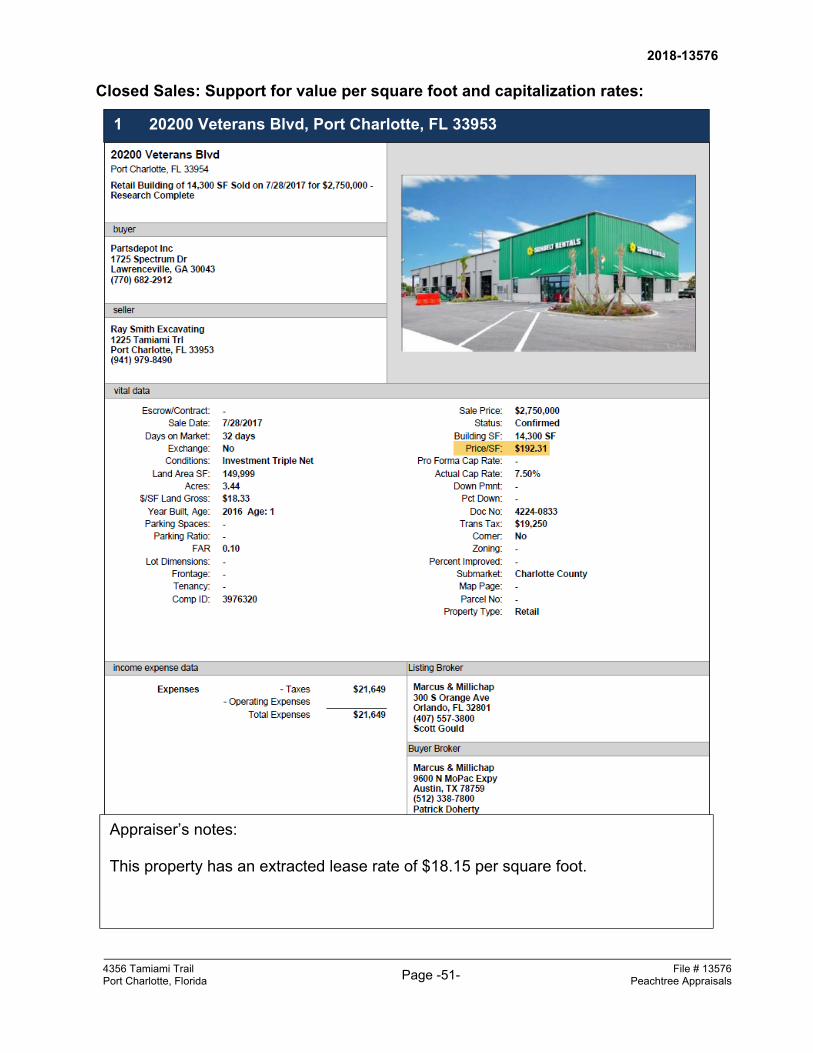

Closed Sales: Support for value per square foot and capitalization rates:

Appraiser’s notes:

This property has an extracted lease rate of $18.15 per square foot.

1 20200 Veterans Blvd, Port Charlotte, FL 33953

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -52- File # 13576

Peachtree Appraisals

2

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -53- File # 13576

Peachtree Appraisals

3

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -54- File # 13576

Peachtree Appraisals

4

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -55- File # 13576

Peachtree Appraisals

5

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -56- File # 13576

Peachtree Appraisals

6 19650 Cochran Blvd, Port Charlotte, FL 33948

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -57- File # 13576

Peachtree Appraisals

8 1820 Del Prado Blvd S, Cape Coral, FL 33990

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -58- File # 13576

Peachtree Appraisals

8 4260 Cleveland Ave, Fort Myers, FL 33901

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -59- File # 13576

Peachtree Appraisals

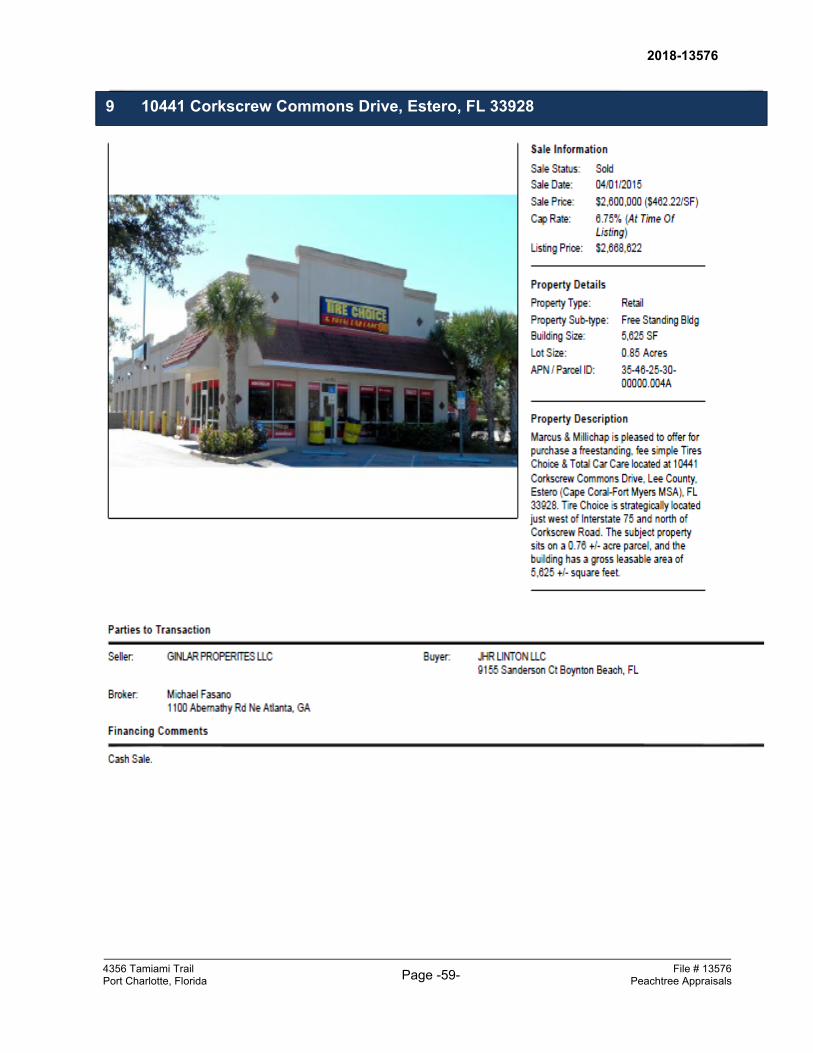

9 10441 Corkscrew Commons Drive, Estero, FL 33928

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -60- File # 13576

Peachtree Appraisals

10 3626 S Dale Mabry Hwy, Tampa, FL 33629

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -61- File # 13576

Peachtree Appraisals

11 8833 State Road 52, Hudson, FL 34667

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -62- File # 13576

Peachtree Appraisals

12 13360 US Highway 301, Riverview, FL 33578

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -63- File # 13576

Peachtree Appraisals

13 3808 14th St W, Bradenton, FL 34205

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -64- File # 13576

Peachtree Appraisals

The following table provides a summary of the auto related sales. The high and low of the comparable transactions is identified. The estimate of the subject’s value $1,250,000 or $189.39 per square foot. This is well within the range of the indicated values below:

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -65- File # 13576

Peachtree Appraisals

ASSUMPTIONS AND LIMITING CONDITIONS The Market Value estimate of the property or properties appraised is subject to the following assumptions and limiting conditions: 1. The legal description furnished is assumed to be correct. 2. No responsibility is assumed for matters legal in character nor is any opinion rendered

herein as to title that is assumed to be good and merchantable. It is assumed that the property is free and clear of liens and encumbrances and under responsible ownership and management on the appraised date.

3. It is assumed that surveys and/or plats furnished to or acquired by the appraiser and used

in the making of this report are correct. The appraiser has not made a land survey or caused one to be made and, therefore, assumes no responsibility for their accuracy.

4. Certain data used in compiling this report was given to the appraiser from sources he

considers reliable; however, he does not guarantee the correctness of such data, although as far as is reasonably possible the data has been checked and is believed to be correct.

5. The soil and the area under appraisement appear to be firm and solid, unless otherwise

stated. Subsidence in the area is unknown or uncommon but the appraiser does not warrant against this condition or occurrence.

6. Subsurface rights (mineral and oil) were not considered in making this report, unless

otherwise stated. 7. Any riparian rights and/or littoral rights indicated by survey, map or plat are assumed to go

with the property unless the appraiser found easements or deeds of record to the contrary. 8. Possession of this report, or copy thereof, does not carry with it the right of publication or

reproduction nor may it be used by anyone but the applicant without prior written consent of the applicant and the appraiser and in any event only in its entirety.

9. The appraiser, by reason of this report, is not required to give testimony in court with

reference to the property herein appraised nor is he obligated to appear before any governmental body, board or agent unless arrangements have been previously made thereof. Court testimony for any reason will require that a fee of $150.00 per hour be paid for our testimony.

2018-13576

4356 Tamiami Trail Port Charlotte, Florida Page -66- File # 13576

Peachtree Appraisals