appendix i: questionnaire on islamic finance objectives

TRANSCRIPT

Appendix I: Questionnaire onIslamic Finance Objectives andAchievements

Dear Respondent,

I am conducting an academic research on whether the Objectives of Islamic Financeare being achieved or not by Islamic Banks and Financial Institutions. I very humblyrequest you to spend your precious five minutes in filling the questionnaire as per yourperception about the Islamic Finance Industry. Your contribution in this regard will behighly appreciated and will be acknowledged at the time of submission of thesis.

1. Your Name (Optional): Prof./Dr./Mr./Mrs./Miss . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2. Please select your age:a) Under 25 b) 26–35c) 36–45 d) 46 or older

3. Please select your gender?a) Male b) female

4. How are you related with Islamic Finance, please tick any one from thefollowing.a) Customer b) Employee of Islamic Bankc) Shariah Advisor d) Regulatory officere) Others (Please specify . . . . . . . . .

5. By religion you are a?a) Muslim d) Buddhistb) Christian e) Atheist/Secularc) Hindu f) Others please specify

6. Data Collection country:a) Malaysia c) United Arab Emirates

Note: There is no right or wrong answer, all I am interested in knowing is your opinionon a “- point Scale”. Where,

5 = Strongly Agree,4 = Agree,3 = Neutral,2 = Disagree,1 = Strongly Disagree.

157

158 Appendix I: Questionnaire on Islamic Finance Objectives and Achievements

Please tick (√

) the number for each statement.

Do you think Islamic Banking and Financial Services is:

1 True to the teachings of Islam? 5 4 3 2 12 Shariah Based? 5 4 3 2 13 A good vehicle to promote Islamic values? 5 4 3 2 14 Working as per the teachings of Quran and

Sunnah?5 4 3 2 1

5 First in conformity with the norms of Islamand then in accordance with customer’spreferences?

5 4 3 2 1

6 Investing in business where there is no Gharar(more risk)?

5 4 3 2 1

7 Practically not indulged in businesses likegambling, pornographic, alcohol, cinema andother forbidden businesses in Islam?

5 4 3 2 1

8 Not different from other commercial banksexcept in complying with Shariah legalprescriptions with regard to product offering?

5 4 3 2 1

9 Promoting Islamic values and way of lifetowards staff, clients and general public?

5 4 3 2 1

Do you think:

10 Shariah scholars play their role while issuingdifferent products?

5 4 3 2 1

11 Shariah board acts as a watchdog while issuingdifferent products?

5 4 3 2 1

Do you think Islamic banks and financial institutions:

12 Do not exploit its customers in any way? 5 4 3 2 113 Do not indulge in misleading advertisements? 5 4 3 2 114 Do not earn income through unfair means? 5 4 3 2 115 Are free from exploitation, discontentment and

strife?5 4 3 2 1

16 Are in consonance with the principles of fairdealing, justice and benevolence?

5 4 3 2 1

17 Properly reflect the values in which they arebased?

5 4 3 2 1

18 Follow Islamic ethics? 5 4 3 2 1

Appendix I: Questionnaire on Islamic Finance Objectives and Achievements 159

I believe that the following objectives of Islamic finance are being achievedby Islamic Banks and Financial Institutions:

19 Maximizing profits (good percentage of returnto investors).

5 4 3 2 1

20 Help in alleviating poverty (povertyeradication).

5 4 3 2 1

21 Promoting sustainable development projects. 5 4 3 2 122 Providing employment opportunities. 5 4 3 2 123 Minimizing cost of operations. 5 4 3 2 124 Enhancing product and service quality. 5 4 3 2 125 Offering viable and competitive financial

products.5 4 3 2 1

Do you think Islamic Banks and Financial Institutions:

26 Are providing enough retail products? 5 4 3 2 127 Contributing to social welfare? 5 4 3 2 128 Collecting and distributing Zakat? 5 4 3 2 129 Contribute in removing society’s inequalities

and improving general standard of living?5 4 3 2 1

30 Performance cannot be judged only throughgood percentage of profit/return?

5 4 3 2 1

31 Use modern technology in performing bankingtransactions?

5 4 3 2 1

32 Completely serve as an alternative bankingsystem?

5 4 3 2 1

Do you think following products and services of Islamic finance are reallyIslamic:

33 Mudarabah (sleeping partnership)? 5 4 3 2 134 Musharakah (partnership Financing)? 5 4 3 2 135 Sukuk? 5 4 3 2 136 Ijarah (leasing)? 5 4 3 2 137 Takaful (insurance)? 5 4 3 2 138 Murabahah (cost plus financing)? 5 4 3 2 1

160 Appendix I: Questionnaire on Islamic Finance Objectives and Achievements

Your comments and suggestions are welcome, regarding the development ofIslamic Finance Industry in the world . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . If you need additional sheets, please ask.

Thank You

Your Signature please

Appendix II: Islamic FinancialInstitutions (By Region andCountry1)

1. Middle East

1.1 Bahrain1.2 Jordan1.3 Kuwait1.4 Lebanon1.5 Qatar1.6 Syria1.7 Saudi Arabia1.8 United Arab Emirates1.9 Yemen

2. Asia (South and Southeast)

2.1 Bangladesh2.2 Brunei Darussalam2.3 Indonesia2.4 Pakistan2.5 Malaysia2.6 Thailand

3. Africa

3.1 Kenya3.2 South Africa3.3 Sudan

4. Asia (Northern)

4.1 China

5. Australia and Pacific Islands

5.1 Australia

1 Different banks and financial institutions across globe are given. This is not thecomplete list in any way. In this list only those banks and financial institutionshave been taken which the researcher knows from his personal website, which is‘World Database for Islamic Banking and Finance’ (WDIBF), and having websiteURL www.wdibf.com.

161

162 Appendix II: Islamic Financial Institutions (By Region and Country)

6. Commonwealth of Independent States

6.1 Azerbaijan6.2 Kazakhstan6.3 Russia

7. Europe

7.1 France7.2 Germany

163

Co

un

try

No

.of

Isla

mic

Ban

ks

Nam

eo

fth

eB

ank

Yea

ro

fes

tab

lish

men

tSp

ecia

lFe

atu

res

Alg

eria

01A

lBar

aka

Ban

kof

Alg

eria

2M

ay20

,199

1w

ith

aca

pita

lof

500,

000,

000

AD

Ba

hra

in09

Bah

rain

Isla

mic

Ban

k(B

isB

)319

79T

heau

thor

ized

capi

tali

sB

D10

0m

illio

nan

dpa

idup

capi

tali

sB

D66

.235

mill

ion

AB

CIs

lam

icB

ank

(E.C

.)4

1980

Offi

ces

in22

coun

trie

sin

wor

ld

Ithm

aar

Ban

kB

.S.C

.5N

oin

form

atio

nIt

has

apa

id-u

pca

pita

lof

US$

701

mill

ion,

tota

leq

uity

ofU

S$1

billi

on

Gul

fFi

nanc

eH

ouse

(GFH

)6N

oin

form

atio

n61

%in

crea

sein

profi

tsto

US

$340

mill

ion

duri

ng20

07

AlB

arak

aB

ank

Bah

rain

719

84T

wo

bran

ches

inB

ahra

in

AlS

alam

Ban

kB

ahra

in8

19Ja

nuar

y20

06Pa

idup

capi

talU

S$31

8m

illio

n

Cap

inno

vaIn

vest

men

tB

ank9

Janu

ary

2009

fully

owne

dsu

bsid

iary

ofth

eB

ank

ofB

ahra

inan

dK

uwai

t(“

BB

K”)

,

Cit

iIs

lam

icIn

vest

men

tB

ank10

July

1996

100%

owne

dsu

bsid

iary

ofC

itic

orp

Ban

king

Cor

pora

tion

Kha

leej

iCom

mer

cial

Ban

k11N

ovem

ber

2004

paid

-up

capi

talo

fB

D30

mill

ion

2h

ttp

://w

ww

.alb

arak

a-ba

nk.

com

/fr/

tran

slat

edfr

omD

utc

hla

ngu

age

toEn

glis

hth

rou

ghG

oogl

etr

ansl

ator

.3

htt

p:/

/ww

w.b

isb.

com

/Abo

utU

s/h

isto

ry.a

sp.

4h

ttp

://w

ww

.ara

bban

kin

g.co

m/E

n/A

bou

tAB

C/P

ages

/Fac

tSh

eet.

asp

x.5

htt

p:/

/ww

w.i

thm

aarb

ank.

com

/ith

maa

r_ab

out_

glan

ce.a

sp.

6h

ttp

://w

ww

.gfh

.com

/en

/abo

ut-

us/

abou

t-u

s-3.

htm

l.7

htt

p:/

/ww

w.b

arak

aon

lin

e.co

m/d

efau

lt.a

sp?a

ctio

n=a

rtic

le&

ID=1

37.

8h

ttp

://w

ww

.als

alam

bah

rain

.com

/abo

ut_

us/

Profi

le.

9h

ttp

://w

ww

.cap

inn

ovab

ank.

com

/.10

htt

p:/

/ww

w.c

itii

slam

ic.c

om/c

iib/

hom

epag

e/.

11h

ttp

://w

ww

.kh

cbon

lin

e.co

m/m

edia

/pd

f/FH

/ban

k’s%

20p

rofi

le.p

df.

164

(Con

tin

ued

)

Co

un

try

No

.of

Isla

mic

Ban

ks

Nam

eo

fth

eB

ank

Yea

ro

fes

tab

lish

men

tSp

ecia

lFe

atu

res

Egy

pt01

Fais

alIs

lam

icB

ank

ofEg

ypt12

5Ju

ly,1

979

firs

tEg

ypti

anIs

lam

ic&

Com

mer

cial

Ban

k

Ira

q01

Iraq

iIsl

amic

Ban

k1319

Dec

embe

r,19

92es

tabl

ishe

dfo

rIn

vest

men

tan

dD

evel

opm

ent

Ira

n09

Ban

kM

elli

Iran

14N

oin

form

atio

nw

hen

star

ted

Isla

mic

bank

ing

Firs

tir

ania

nco

mm

erci

alba

nk

Ban

kM

ella

t15D

ecem

ber

20,1

979

rank

ing

amon

gth

eto

p10

00ba

nks

ofth

ew

orld

Ban

kTe

jara

t1619

87th

efa

cilit

ies

ofT

heEa

stM

oder

nB

ank

was

assi

gned

toB

ank

Shah

ansh

ahi.

Ban

kD

epah

17N

oin

form

atio

nw

hen

star

ted

Isla

mic

bank

ing

pres

ent

paid

-in

capi

talo

fIR

R7,

822

billi

on

Ban

kK

esha

varz

i18N

oin

form

atio

nw

hen

star

ted

Isla

mic

bank

ing

now

cons

ider

edas

api

onee

rba

nkin

offe

ring

vari

ety

ofba

nkin

gse

rvic

esna

tion

wid

e

Mas

kan

Ban

k1919

74st

arte

dit

sop

erat

ions

asa

publ

icco

mpa

ny

Kar

arafi

nB

ank20

Oct

ober

11,1

980

firs

tpr

ivat

ely-

owne

dba

nkin

oper

atio

n

12h

ttp

://w

ww

.fai

salb

ank.

com

.eg/

FIB

/fai

sal_

en/E

lnas

h2a

_1.j

sp.

13h

ttp

://w

ww

.ira

qii

slam

icb.

com

/.Tr

ansl

ated

from

Ara

bic

toEn

glis

hth

rou

ghG

oogl

etr

ansl

ator

.14

htt

p:/

/ww

w.b

mi.

ir/E

n/B

MIH

isto

ry.a

spx?

smn

uid

=100

11.

15h

ttp

://e

n.b

ankm

ella

t.ir

/por

tal.

asp

x?ta

bid

=405

.16

htt

p:/

/ww

w.t

ejar

atba

nk.

ir/.

Tran

slat

edfr

omPe

rsia

nLa

ngu

age

toEn

glis

hth

rou

ghG

oogl

etr

ansl

ator

.17

htt

p:/

/ww

w.b

anks

epah

.ir/

Engl

ish

/def

ault

.asp

x?ta

bid

=450

.18

htt

p:/

/ww

w.a

gri-

ban

k.co

m/S

tati

c/En

glis

h/A

bou

t/Pr

ofile

.asp

.19

htt

p:/

/ban

k-m

aska

n.i

r/d

efau

lt-4

446.

asp

x.20

htt

p:/

/en

.kar

afar

inba

nk.

com

/his

tory

/def

ault

.kb.

165

Sam

anB

ank21

Aug

ust,

2002

shar

eca

pit

alof

US$

1.4

mln

.

Pers

ian

Ban

k22Ju

ly,2

001

regi

ster

edun

der

No.

1780

28on

Sept

embe

r6,

2001

Jord

an

03Jo

rdan

Isla

mic

Ban

k2319

7880

AT

Ms

alov

erth

eco

untr

y

Jord

anD

ubai

Isla

mic

Ban

k2420

07D

ubai

Isla

mic

Ban

kal

ong

wit

hit

spa

rtne

rJo

rdan

Dub

aiC

apit

al

Isla

mic

Inte

rnat

iona

lA

rab

Ban

k259

Febr

uary

,199

8p

ubl

icsh

areh

old

ing

com

pan

yin

acco

rdan

cew

ith

the

com

pan

ies

Law

of19

89

Ku

wa

it04

Inte

rnat

iona

lB

ank

ofK

uwai

t26Ju

ly20

07K

uw

ait

Rea

lEs

tate

Ban

k(i

nco

rpor

ated

in19

73)

has

been

ren

amed

to“K

uw

ait

Inte

rnat

ion

alB

ank

toex

erci

seit

sbu

sin

ess

asan

Isla

mic

ban

k.

Kuw

ait

Fina

nce

Hou

se27

1977

Firs

tIs

lam

icB

ank

inK

uwai

t

Bou

byan

Ban

k28N

oin

form

atio

nFo

urm

ain

bran

ches

are

inD

arw

aza,

Ku

wai

tC

ity,

Mu

bara

kto

wer

,Far

wan

iya,

Daj

eej

and

Qeb

laTo

wer

.

Ahl

iUni

ted

Ban

kK

uwai

29A

pril,

2010

Con

vent

iona

lban

kco

nver

ted

into

Isla

mic

21h

ttp

://w

ww

.sb2

4.co

m/.

22h

ttp

://w

ww

.par

sian

-ban

k.co

m/h

isto

ryof

ban

k_en

.htm

l.23

htt

p:/

/ww

w.j

ord

anis

lam

icba

nk.

com

/en

/?p

id=D

Y&

lan

=1&

pp

i=12

4&p

gi=1

27&

th=1

.24

htt

p:/

/ww

w.j

dib

.jo/

Abo

ut-

JDIB

.asp

x.25

htt

p:/

/ww

w.i

iaba

nk.

com

.jo/

en/H

ome/

Abo

utU

s/ta

bid

/54/

Def

ault

.asp

x.26

htt

p:/

/ww

w.k

ib.c

om.k

w/K

REB

Cli

ent/

Cli

entP

ages

/In

dex

.asp

x?Id

=76.

27h

ttp

://w

ww

.kfh

.com

/en

/abo

ut/

ind

ex.a

spx.

28h

ttp

://w

ww

.ban

kbou

byan

.com

/mis

sion

_vis

ion

.htm

l.29

htt

p:/

/ww

w.a

hli

un

ited

.com

.kw

/au

b_kw

.htm

l.

166

(Con

tin

ued

)

Co

un

try

No

.of

Isla

mic

Ban

ks

Nam

eo

fth

eB

ank

Yea

ro

fes

tab

lish

men

tSp

ecia

lFe

atu

res

Leb

an

on03

Al-

Bar

aka

Ban

kLe

bano

n3019

92fi

rst

deve

lopi

ngba

nkin

Leba

non

wor

king

acco

rdin

gto

Fidu

ciar

yC

ontr

act

Law

Num

ber

520

date

dJu

ne6,

1996

infu

llco

mpl

ianc

ew

ith

Isla

mic

Shar

iah

Ara

bFi

nanc

eH

ouse

31N

oin

form

atio

nA

rab

Fin

ance

Hou

se’s

Man

agem

ent

stro

ngl

ysu

pp

orts

this

ince

nti

ve(L

aw31

8)

Leba

nese

Isla

mic

Ban

k32N

oin

form

atio

nba

nk

pro

vid

esza

kat

affi

nit

yca

rd

Pa

lest

ine

01Pa

lest

ine

Isla

mic

Ban

k3316

Dec

embe

r,19

9514

bran

ches

and

the

hea

dof

fice

atD

eir

al-B

alah

Qa

tar

04Q

atar

Isla

mic

Ban

k348

July

1982

Mor

eth

an10

0A

TM

s

Qat

arIn

tern

atio

nal

Isla

mic

Ban

k35Ja

nuar

y1,

1992

12br

anch

esan

d50

AT

Ms

Qat

arIs

lam

icIn

sura

nce

Com

pany

3619

95Q

R60

.5m

illi

onin

2007

30h

ttp

://w

ww

.al-

bara

ka.c

om/a

bou

tus.

ph

p?c

at=h

isto

ry.p

hp

.31

htt

p:/

/ww

w.a

fh.c

om.l

b/p

reve

nti

on.a

sp.

32h

ttp

://w

ww

.leb

anes

eisl

amic

ban

k.co

m.l

b/in

dex

.asp

.33

ww

w.i

slam

icba

nk.

ps.

Tran

slat

edfr

omA

rabi

cto

Engl

ish

thro

ugh

Goo

gle

tran

slat

or.

34h

ttp

://w

ww

.qib

.com

.qa/

engl

ish

/sit

e/to

pic

s/st

atic

228e

228e

.htm

l?cu

_no=

1&ln

g=0&

tem

pla

te_i

d=3

21&

tem

p_t

ype=

42&

par

ent_

id=3

00.

35h

ttp

://w

ww

.qii

b.co

m.q

a/q

iib/

en/q

iibc

ms.

asp

x?q

cid

=6.

36h

ttp

://w

ww

.qii

c.co

m.q

a/En

glis

h_P

ages

/His

tory

/in

dex

.htm

l.

167

Sau

di

Ara

bia

06A

linm

aB

ank37

31Ja

nuar

y,20

07T

he

Shar

iah

boar

dof

Ali

nm

aB

ank

was

form

edp

urs

uan

tto

reso

luti

onN

o.3/

43,

dat

ed12

/01/

1428

Isla

mic

Dev

elop

men

tB

ank38

20O

ctob

er,1

975

Th

ep

urp

ose

ofth

eba

nk

isth

ed

evel

opm

ent

ofM

usl

imco

un

trie

s

AlR

ajhi

Ban

k3919

88M

ore

than

2500

AT

Ms

Nat

iona

lCom

mer

cial

Ban

k40N

oin

form

atio

nPa

idu

pca

pit

alU

S$

8m

illi

on

Ban

kA

lbila

d414

Nov

embe

r,20

04co

rpor

ate

cap

ital

of3,

000,

000,

000

Sau

di

Riy

als.

Ban

kA

lJaz

ira42

June

21,1

975

oper

ates

un

der

com

mer

cial

regi

stra

tion

No.

4030

0105

23

Sud

an

07A

lBar

aka

Ban

kSu

dan43

1984

23br

anch

esan

d65

6em

plo

yees

Isla

mic

Co–

oper

ativ

eD

evel

opm

ent

Ban

k4419

82ce

lebr

ated

its

25th

birt

hd

ayin

2008

AlS

alam

Ban

k45N

oin

form

atio

nd

eter

min

edon

pre

sen

tin

gth

em

ost

adva

nce

dse

rvic

esin

Isla

mic

ban

kin

g

Emir

ates

and

Suda

nB

ank46

No

info

rmat

ion

auth

oriz

edca

pit

alof

USD

200

Mn

37h

ttp

://w

ww

.ali

nm

a.co

m/w

ps/

por

tal/

alin

ma/

!ut/

p/c

5/04

_SB

8K8x

LLM

9MSS

zPy8

xBz9

CP0

os3h

zf2c

LDy9

3A0t

3d1c

3A09

3Ixd

3_yB

fI29

TA_3

g1Lz

40G

D9g

mxH

RQ

C3t

lD5/

.38

htt

p:/

/ww

w.i

sdb.

org/

irj/

por

tal/

anon

ymou

s?N

avig

atio

nTa

rget

=nav

url

://2

4de0

d5f

10d

a906

da8

5e96

ac35

6b7a

f0.

39h

ttp

://w

ww

.alr

ajh

iban

k.co

m.s

a/A

bou

tUs/

Page

s/d

efau

lt.a

spx.

40h

ttp

://w

ww

.ala

hli

.com

/en

-US/

Abo

ut%

20U

s/C

orp

orat

e%20

Profi

le/P

ages

/Cor

por

ateP

rofi

leH

ome_

Page

.asp

x.41

htt

p:/

/ww

w.b

anka

lbil

ad.c

om/e

n/a

bou

t.as

p?T

abId

=1.

42h

ttp

://w

ww

.baj

.com

.sa/

abou

t/d

efau

lt.a

sp?a

b=vi

ew.

43h

ttp

://w

ww

.alb

arak

a.co

m/d

efau

lt.a

sp?a

ctio

n=a

rtic

le&

id=9

6.44

htt

p:/

/ww

w.i

scob

.com

/abo

ut_

E.h

tm.

45h

ttp

://w

ww

.als

alam

ban

k.n

et/h

tml/

abou

t.h

tml.

46h

ttp

://w

ww

.ean

dsb

ank.

com

/abo

utu

s/ab

outu

s.h

tml.

168(C

onti

nu

ed)

Co

un

try

No

.of

Isla

mic

Ban

ks

Nam

eo

fth

eB

ank

Yea

ro

fes

tab

lish

men

tSp

ecia

lFe

atu

res

Expo

rtD

evel

opm

ent

Ban

k47Ja

nuar

y15

,200

3T

he

nat

ion

alp

riva

tese

ctor

hol

ds

abou

t83

.14

%of

the

cap

ital

ofth

eba

nk

Fais

alIs

lam

icB

ank48

May

,197

8h

ead

qu

arte

rof

the

ban

kis

atK

har

tou

mSu

dan

Tada

mon

Isla

mic

Ban

k49M

arch

,198

3go

odre

pu

tati

onat

both

loca

lan

din

tern

atio

nal

leva

l

Syri

a02

Syri

aIn

tern

atio

nal

Isla

mic

Ban

k50Se

ptem

ber

7,20

06D

ecre

eN

o.35

(200

5)

Ch

amB

ank51

Sept

embe

r7,

2006

Firs

tIs

lam

icba

nk

inSy

ria

Tu

nis

ia01

Zayt

un

aB

ank52

Oct

ober

,200

9u

niv

ersa

lco

mm

erci

alba

nk

Tu

rkey

04K

uve

ytTu

rkPa

rtic

ipat

ion

Ban

k5319

89K

uw

ait

fin

ance

hou

seh

as62

%sh

ares

inth

isba

nk

AlB

arak

aTu

rk54

1985

fore

ign

par

tner

ssh

are

is66

,16%

,

47h

ttp

://w

ww

.ed

ban

k.sd

/en

_web

/abo

uba

nk1

.asp

x.48

htt

p:/

/ww

w.fi

bsu

dan

.com

/en

/.49

htt

p:/

/ww

w.t

adam

onba

nk-

sd.c

om/e

ngl

ish

/1.p

hp

.50

htt

p:/

/ww

w.s

iib.

sy/i

nd

ex.p

hp

?op

tion

=com

_con

ten

t&vi

ew=a

rtic

le&

id=4

7&It

emid

=66&

lan

g=en

.51

htt

p:/

/ww

w.c

ham

ban

k.co

m/i

nd

ex.p

hp

?op

tion

=com

_con

ten

t&vi

ew=c

ateg

ory&

layo

ut=

blog

&id

=34&

Item

id=6

1&la

ng=

en.

52h

ttp

://w

ww

.ban

qu

ezit

oun

a.co

m.T

ran

slat

edfr

omFr

ench

toEn

glis

hth

rou

ghG

oogl

etr

ansl

ator

.53

htt

p:/

/ww

w.k

uve

yttu

rk.c

om.t

r/en

/Hak

kim

izd

a_Ta

rih

ce.a

spx.

54h

ttp

://w

ww

.ban

qu

ezit

oun

a.co

m.T

ran

slat

edfr

omFr

ench

toEn

glis

hth

rou

ghG

oogl

etr

ansl

ator

.tt

p:/

/en

.alb

arak

atu

rk.c

om.t

r/ab

out_

us/

det

ail.

asp

x?Se

ctio

nID

=YX

L0%

2bp

Pb1Z

Gxu

cFd

8yJz

Iw%

3d%

3d&

Con

ten

tId

=op

Vi0

iuq

7Iu

zLtB

3Mxt

%2f

nQ

%3d

%3d

.

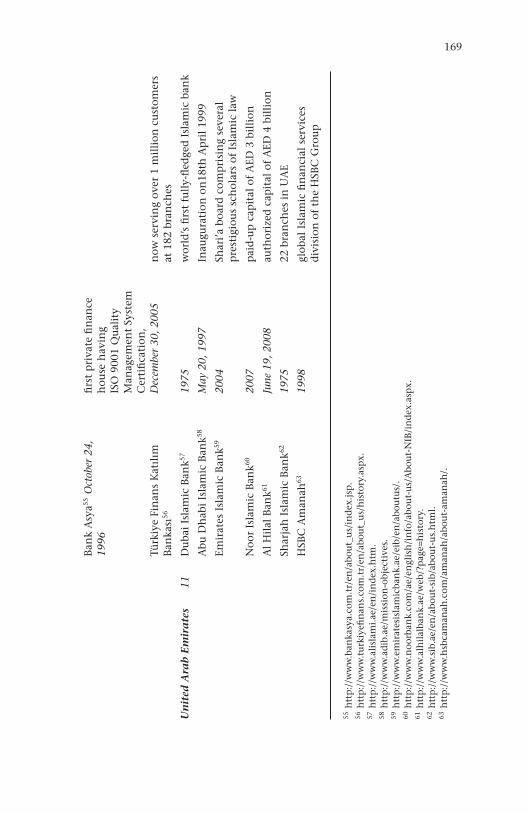

169

Ban

kA

sya55

Oct

ober

24,

1996

firs

tp

riva

tefi

nan

ceh

ouse

hav

ing

ISO

9001

Qu

alit

yM

anag

emen

tSy

stem

Cer

tifi

cati

on,

Türk

iye

Fin

ans

Kat

ılım

Ban

kası

56D

ecem

ber

30,2

005

now

serv

ing

over

1m

illi

oncu

stom

ers

at18

2br

anch

es

Un

ited

Ara

bE

mir

ate

s11

Du

bai

Isla

mic

Ban

k5719

75w

orld

’sfi

rst

full

y-fl

edge

dIs

lam

icba

nk

Abu

Dh

abi

Isla

mic

Ban

k58M

ay20

,199

7In

augu

rati

onon

18th

Ap

ril1

999

Emir

ates

Isla

mic

Ban

k5920

04Sh

ari’a

boar

dco

mp

risi

ng

seve

ral

pre

stig

iou

ssc

hol

ars

ofIs

lam

icla

w

Noo

rIs

lam

icB

ank60

2007

pai

d-u

pca

pit

alof

AED

3bi

llio

n

Al

Hil

alB

ank61

June

19,2

008

auth

oriz

edca

pit

alof

AED

4bi

llio

n

Shar

jah

Isla

mic

Ban

k6219

7522

bran

ches

inU

AE

HSB

CA

man

ah63

1998

glob

alIs

lam

icfi

nan

cial

serv

ices

div

isio

nof

the

HSB

CG

rou

p

55h

ttp

://w

ww

.ban

kasy

a.co

m.t

r/en

/abo

ut_

us/

ind

ex.j

sp.

56h

ttp

://w

ww

.tu

rkiy

efin

ans.

com

.tr/

en/a

bou

t_u

s/h

isto

ry.a

spx.

57h

ttp

://w

ww

.ali

slam

i.ae

/en

/in

dex

.htm

.58

htt

p:/

/ww

w.a

dib

.ae/

mis

sion

-obj

ecti

ves.

59h

ttp

://w

ww

.em

irat

esis

lam

icba

nk.

ae/e

ib/e

n/a

bou

tus/

.60

htt

p:/

/ww

w.n

oorb

ank.

com

/ae/

engl

ish

/in

fo/a

bou

t-u

s/A

bou

t-N

IB/i

nd

ex.a

spx.

61h

ttp

://w

ww

.alh

ilal

ban

k.ae

/web

/?p

age=

his

tory

.62

htt

p:/

/ww

w.s

ib.a

e/en

/abo

ut-

sib/

abou

t-u

s.h

tml.

63h

ttp

://w

ww

.hsb

cam

anah

.com

/am

anah

/abo

ut-

aman

ah/.

170

(Con

tin

ued

)

Co

un

try

No

.of

Isla

mic

Ban

ks

Nam

eo

fth

eB

ank

Yea

ro

fes

tab

lish

men

tSp

ecia

lFe

atu

res

Att

ijar

iAl

Isla

mi64

No

info

rmat

ion

par

tof

Com

mer

cial

Ban

kof

Du

bai

Mas

hre

qA

lIs

lam

i65N

oin

form

atio

nIs

lam

icB

anki

ng

arm

ofM

ash

req

grou

p

Du

bai

Ban

k6620

02m

oder

nIs

lam

icba

nk

ofch

oice

Ajm

anB

ank67

No

info

rmat

ion

pai

du

pca

pit

alof

AED

1bi

llio

n

Yem

en03

Tad

ham

onin

tern

atio

nal

Isla

mic

ban

k68M

ay25

,199

5ba

nk

run

sas

sets

that

are

esti

mat

ed1.

415

mil

lion

US

dol

lars

Saba

Isla

mic

Ban

k69A

pril,

1997

7500

shar

ehol

der

ofal

lse

gmen

tsof

soci

ety

Isla

mic

Ban

kof

Yem

enfo

rFi

nan

cean

dIn

vest

men

t70N

oin

form

atio

np

rovi

des

all

kin

ds

ofm

oder

nfa

cili

ties

toit

scu

stom

ers

like

SMS,

AT

Met

c.

Ba

ngl

ad

esh

06Is

lam

iB

ank

Ban

glad

esh

Lim

ited

71M

arch

30,1

983

firs

tof

its

kin

din

Sou

thea

stA

sia

ICB

Isla

mic

Ban

kLi

mit

ed72

Ap

ril3

0,19

87ba

nki

ng

oper

atio

ns

com

men

ced

onM

ay20

,19

87

64h

ttp

://w

ww

.cbd

isla

mi.

ae/c

bdis

lam

ic/a

bou

t_bo

ard

.asp

x.65

htt

p:/

/ww

w.m

ash

req

alis

lam

i.co

m/e

ngl

ish

/in

form

atio

n/a

bou

t-u

s/.

66h

ttp

://w

ww

.du

baib

ank.

ae/C

onte

nt/

Def

ault

.asp

x?ID

=43.

67h

ttp

://w

ww

.ajm

anba

nk.

ae/e

n/a

bou

t-u

s/co

mp

any-

pro

file

/Pag

es/C

omp

any-

Profi

le.a

spx.

68h

ttp

://w

ww

.tii

b.co

m/p

ages

.asp

x?id

=67.

69h

ttp

://w

ww

.sab

aban

k.co

m/v

iew

.htm

.Tra

nsl

ated

from

Ara

bic

toEn

glis

hth

rou

ghG

oogl

etr

ansl

ator

.70

htt

p:/

/ww

w.i

by-b

ank.

com

/en

g/d

efau

lt.a

sp.

71h

ttp

://w

ww

.isl

amib

ankb

d.c

om/i

ntr

odu

ctio

n.p

hp

.72

htt

p:/

/ww

w.i

cbis

lam

ic-b

d.c

om/.

171

Al-

Ara

fah

Isla

mi

Ban

k7319

9553

bran

ches

in20

08

Firs

tSe

curi

tyIs

lam

iB

ank

Lim

ited

74Se

pte

mbe

r22

,199

952

bran

ches

fun

ctio

nin

g

Isla

mic

Fin

ance

and

Inve

stm

ent

Lim

ited

(IFI

L)75

Ap

ril

19,2

001

pre

sen

tad

dre

ssat

Ch

and

Man

sion

,66

,D

ilku

sha

C/A

,Dh

aka-

1000

Shah

jala

lIs

lam

iB

ank

Lim

ited

(SJI

BL)

76M

ay10

,200

1h

ead

qu

arte

rof

the

ban

kis

inD

hak

a

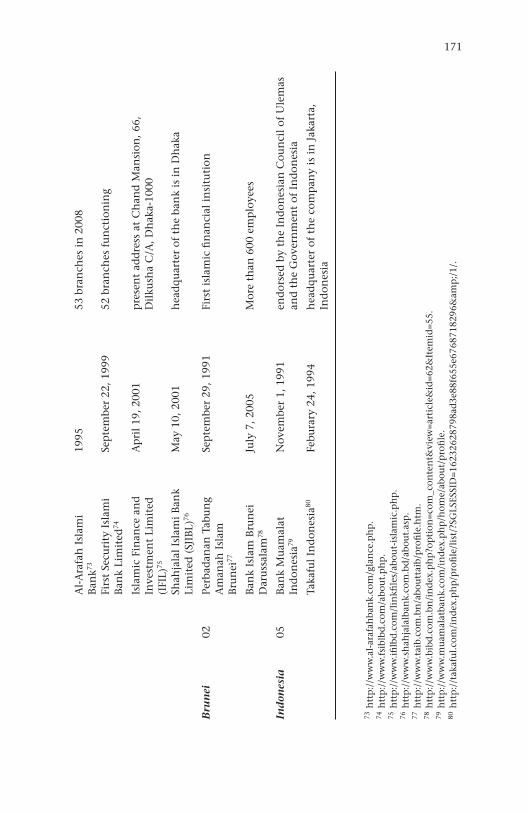

Bru

nei

02Pe

rbad

anan

Tabu

ng

Am

anah

Isla

mB

run

ei77

Sep

tem

ber

29,1

991

Firs

tis

lam

icfi

nan

cial

insi

tuti

on

Ban

kIs

lam

Bru

nei

Dar

uss

alam

78Ju

ly7,

2005

Mor

eth

an60

0em

plo

yees

Ind

ones

ia05

Ban

kM

uam

alat

Ind

ones

ia79

Nov

embe

r1,

1991

end

orse

dby

the

Ind

ones

ian

Cou

nci

lof

Ule

mas

and

the

Gov

ern

men

tof

Ind

ones

ia

Taka

ful

Ind

ones

ia80

Febu

rary

24,1

994

hea

dq

uar

ter

ofth

eco

mp

any

isin

Jaka

rta,

Ind

ones

ia

73h

ttp

://w

ww

.al-

araf

ahba

nk.

com

/gla

nce

.ph

p.

74h

ttp

://w

ww

.fsi

blbd

.com

/abo

ut.

ph

p.

75h

ttp

://w

ww

.ifi

lbd

.com

/lin

kfile

s/ab

out-

isla

mic

.ph

p.

76h

ttp

://w

ww

.sh

ahja

lalb

ank.

com

.bd

/abo

ut.

asp

.77

htt

p:/

/ww

w.t

aib.

com

.bn

/abo

utt

aib/

pro

file

.htm

.78

htt

p:/

/ww

w.b

ibd

.com

.bn

/in

dex

.ph

p?o

pti

on=c

om_c

onte

nt&

view

=art

icle

&id

=62&

Item

id=5

5.79

htt

p:/

/ww

w.m

uam

alat

ban

k.co

m/i

nd

ex.p

hp

/hom

e/ab

out/

pro

file

.80

htt

p:/

/tak

afu

l.co

m/i

nd

ex.p

hp

/pro

file

/lis

t/?S

GLS

ESSI

D=1

6232

6287

98ad

3e88

f655

e676

8718

296&

amp

;/1/

.

172

(Con

tin

ued

)

Co

un

try

No

.of

Isla

mic

Ban

ks

Nam

eo

fth

eB

ank

Yea

ro

fes

tab

lish

men

tSp

ecia

lFe

atu

res

Ban

kSh

aria

hM

and

ari81

Nov

embe

r1,

1999

spre

adov

er26

pro

vin

ces

thro

ugh

out

the

cou

ntr

y

Ban

kSy

aria

hM

ega

Ind

ones

ia82

Au

gust

24,2

004

ban

kw

ases

tabl

ish

edby

dev

elop

ing

ast

ron

gca

pit

alba

se

Ban

kSy

aria

hB

uko

pin

’s83

Oct

ober

24,2

008

PTB

ank

Bu

kop

intr

ansf

erre

dri

ghts

and

obli

gati

ons

ofSh

aria

into

PTB

ank

Syar

iah

Bu

kop

in

Ma

lays

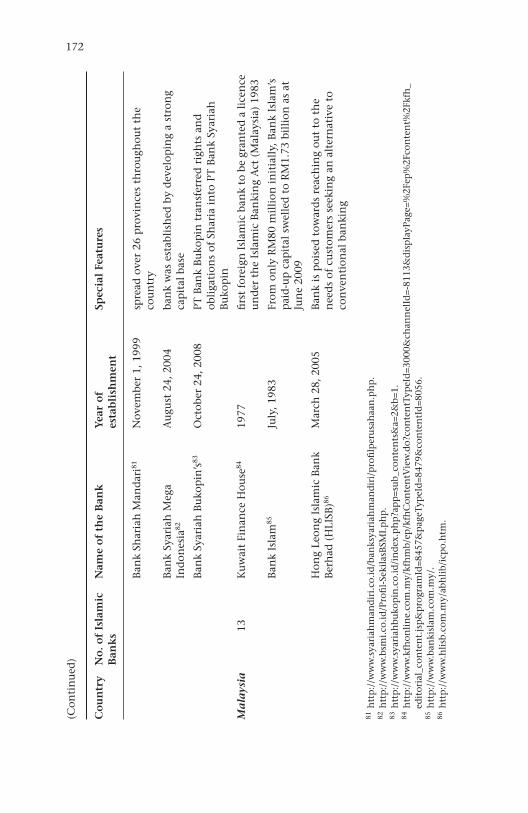

ia13

Ku

wai

tFi

nan

ceH

ouse

8419

77fi

rst

fore

ign

Isla

mic

ban

kto

begr

ante

da

lice

nce

un

der

the

Isla

mic

Ban

kin

gA

ct(M

alay

sia)

1983

Ban

kIs

lam

85Ju

ly,1

983

From

only

RM

80m

illi

onin

itia

lly,

Ban

kIs

lam

’sp

aid

-up

cap

ital

swel

led

toR

M1.

73bi

llio

nas

atJu

ne

2009

Hon

gLe

ong

Isla

mic

Ban

kB

erh

ad(H

LISB

)86M

arch

28,2

005

Ban

kis

poi

sed

tow

ard

sre

ach

ing

out

toth

en

eed

sof

cust

omer

sse

ekin

gan

alte

rnat

ive

toco

nve

nti

onal

ban

kin

g

81h

ttp

://w

ww

.sya

riah

man

dir

i.co

.id

/ban

ksya

riah

man

dir

i/p

rofi

lper

usa

haa

n.p

hp

.82

htt

p:/

/ww

w.b

smi.

co.i

d/P

rofi

l-Se

kila

sBSM

I.p

hp

.83

htt

p:/

/ww

w.s

yari

ahbu

kop

in.c

o.id

/in

dex

.ph

p?a

pp

=su

b_co

nte

nts

&a=

2&b=

1.84

htt

p:/

/ww

w.k

fhon

lin

e.co

m.m

y/kf

hm

b/ep

/kfh

Con

ten

tVie

w.d

o?co

nte

ntT

ypeI

d=3

000&

chan

nel

Id=-

8113

&d

isp

layP

age=

%2F

ep%

2Fco

nte

nt%

2Fkf

h_

edit

oria

l_co

nte

nt.

jsp

&p

rogr

amId

=845

7&p

ageT

ypeI

d=8

479&

con

ten

tId

=805

6.85

htt

p:/

/ww

w.b

anki

slam

.com

.my/

.86

htt

p:/

/ww

w.h

lisb

.com

.my/

abh

lib/

icp

o.h

tm.

173

Asi

anFi

nan

ceB

ank

Ber

had

87N

ovem

ber

28,2

005

Asi

anFi

nan

ceB

ank

isre

gula

ted

and

sup

ervi

sed

byB

ank

Neg

ara

Mal

aysi

au

nd

erth

eIs

lam

icB

anki

ng

Act

,198

3

EON

CA

PIs

lam

icB

ank88

Ap

ril1

,200

6u

thor

ized

and

pai

d-u

pC

apit

alof

RM

1bi

llio

nan

dR

M39

8m

illi

onre

spec

tive

ly

Al

Raj

hi

Ban

k89O

ctob

er,2

006

19br

anch

es

May

ban

kIs

lam

icB

erh

ad90

Jan

uar

y1,

2008

firs

tco

mm

erci

alba

nk

toof

fer

Isla

mic

ban

kin

gp

rod

uct

san

dse

rvic

esth

rou

gha

win

dow

con

cep

tin

1993

Stan

dar

dC

har

tere

dSa

adiq

Ber

had

91N

ovem

ber

12,2

008

hea

dq

uar

ter

ofth

eba

nk

isin

Ku

laLu

mp

ur

HSB

CA

man

ah92

2008

Nov

embe

r20

08,t

he

firs

tbr

anch

ofH

SBC

Am

anah

Mal

aysi

a

Publ

icIs

lam

icB

ank93

Nov

embe

r1,

2008

Isla

mic

Ban

kin

gtr

ansa

ctio

ns

atal

l24

2Pu

blic

Ban

kbr

anch

esan

d26

hir

ep

urc

has

ece

ntr

esin

Mal

aysi

a

All

ian

ceIs

lam

icB

ank94

No

info

rmat

ion

wit

hit

sh

olis

tic

ban

kin

gsc

ope,

focu

ses

onco

nsu

mer

ban

kin

g,co

mm

erci

alba

nki

ng

and

SMEs

tobo

ost

the

busi

nes

s

87h

ttp

://w

ww

.asi

anfi

nan

ceba

nk.

com

/cor

por

ate_

over

view

/cor

por

ate_

orga

niz

atio

n.h

tml.

88h

ttp

://w

ww

.eon

ban

k.co

m.m

y/is

lam

ic/a

bou

tus/

corp

orat

e_p

rofi

le.s

htm

l.89

htt

p:/

/ww

w.a

lraj

hib

ank.

com

.my/

.90

htt

p:/

/ww

w.m

ayba

nk2

u.c

om.m

y/m

ayba

nki

slam

ic/c

orp

orat

e_in

fo/i

nd

ex.s

htm

l.91

htt

p:/

/ww

w.s

tan

dar

dch

arte

red

.com

.my/

isla

mic

-ban

kin

g/en

/.92

htt

p:/

/ww

w.h

sbca

man

ah.c

om/a

man

ah/a

bou

t-am

anah

.93

tran

sact

ion

sat

all

242

Publ

icB

ank

bran

ches

and

26h

ire

pu

rch

ase

cen

tres

inM

alay

sia.

94h

ttp

://w

ww

.all

ian

ceis

lam

icba

nk.

com

.my/

ind

ex_a

bou

tus.

htm

l.

174(C

onti

nu

ed)

Co

un

try

No

.of

Isla

mic

Ban

ks

Nam

eo

fth

eB

ank

Yea

ro

fes

tab

lish

men

tSp

ecia

lFe

atu

res

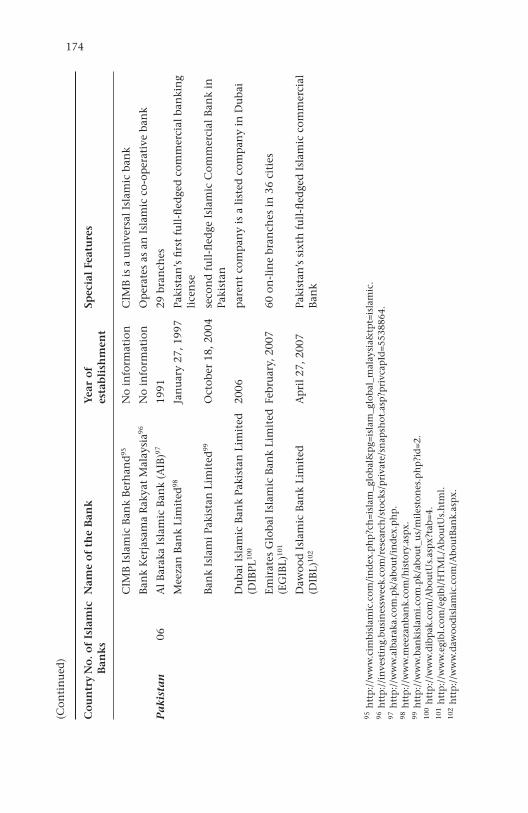

CIM

BIs

lam

icB

ank

Ber

han

d95

No

info

rmat

ion

CIM

Bis

au

niv

ersa

lIs

lam

icba

nk

Ban

kK

erja

sam

aR

akya

tM

alay

sia96

No

info

rmat

ion

Op

erat

esas

anIs

lam

icco

-op

erat

ive

ban

k

Pa

kist

an

06A

lB

arak

aIs

lam

icB

ank

(AIB

)9719

9129

bran

ches

Mee

zan

Ban

kLi

mit

ed98

Jan

uar

y27

,199

7Pa

kist

an’s

firs

tfu

ll-fl

edge

dco

mm

erci

alba

nki

ng

lice

nse

Ban

kIs

lam

iPa

kist

anLi

mit

ed99

Oct

ober

18,2

004

seco

nd

full

-fled

geIs

lam

icC

omm

erci

alB

ank

inPa

kist

an

Du

bai

Isla

mic

Ban

kPa

kist

anLi

mit

ed(D

IBPL

100

2006

par

ent

com

pan

yis

ali

sted

com

pan

yin

Du

bai

Emir

ates

Glo

bal

Isla

mic

Ban

kLi

mit

ed(E

GIB

L)10

1Fe

bru

ary,

2007

60on

-lin

ebr

anch

esin

36ci

ties

Daw

ood

Isla

mic

Ban

kLi

mit

ed(D

IBL)

102

Ap

ril

27,2

007

Paki

stan

’ssi

xth

full

-fled

ged

Isla

mic

com

mer

cial

Ban

k

95h

ttp

://w

ww

.cim

bisl

amic

.com

/in

dex

.ph

p?c

h=i

slam

_glo

bal&

pg=

isla

m_g

loba

l_m

alay

sia&

tpt=

isla

mic

.96

htt

p:/

/in

vest

ing.

busi

nes

swee

k.co

m/r

esea

rch

/sto

cks/

pri

vate

/sn

apsh

ot.a

sp?p

rivc

apId

=553

8864

.97

htt

p:/

/ww

w.a

lbar

aka.

com

.pk/

abou

t/in

dex

.ph

p.

98h

ttp

://w

ww

.mee

zan

ban

k.co

m/h

isto

ry.a

spx.

99h

ttp

://w

ww

.ban

kisl

ami.

com

.pk/

abou

t_u

s/m

iles

ton

es.p

hp

?id

=2.

100

htt

p:/

/ww

w.d

ibp

ak.c

om/A

bou

tUs.

asp

x?ta

b=4.

101

htt

p:/

/ww

w.e

gibl

.com

/egi

bl/H

TM

L/A

bou

tUs.

htm

l.10

2h

ttp

://w

ww

.daw

ood

isla

mic

.com

/Abo

utB

ank.

asp

x.

175

Ken

ya02

Gu

lfA

fric

anB

ank10

320

05K

enya

’sfi

rst

full

ySh

ari’a

hco

mp

lian

tba

nk

Firs

tC

omm

un

ity

Ban

k104

Jun

e1,

2008

Alt

ern

ativ

eba

nki

ng

inm

any

pac

es

Sou

thA

fric

a02

AlB

arak

aB

ank10

519

89T

he

ban

kis

join

tly

own

edby

Sou

thA

fric

anin

vest

ors.

DC

DLo

nd

on&

Mu

tual

Plc

Abs

aIs

lam

icB

ank10

619

91R

epu

ted

ban

k

Th

ail

an

d01

Isla

mic

Ban

kof

Th

aila

nd

107

Jun

e,20

03p

aid

-up

cap

ital

of1

bill

ion

bah

t

Au

stra

lia

02Is

lam

icC

o-op

erat

ive

Fin

ance

Au

stra

lia

Pvt.

Ltd

108

1997

star

tin

geq

uit

yof

only

$A20

00

Mu

slim

Com

mu

nit

yC

o-op

erat

ive

(Au

stra

lia)

Lim

ited

109

1989

grou

pw

asto

pro

vid

ea

pra

ctic

alm

odel

ofIs

lam

icfi

nan

cein

Au

stra

lia

Aze

rba

ija

n01

Kau

thar

Ban

k110

1988

Firs

tco

mm

erci

alba

nks

inA

zerb

aija

n.

Ru

ssia

01A

lSh

ams

Cap

ital

111

No

info

rmat

ion

Dr.

Dja

biev

isa

pio

nee

rin

intr

odu

cin

gth

is

Ger

ma

ny

02K

uve

ytTu

rk11

219

89K

uw

ait

Fin

ance

Hou

seh

as62

%sh

ares

103

htt

p:/

/ww

w.g

ulf

afri

can

ban

k.co

m/H

ome/

Abo

ut-

Us.

104

htt

p:/

/ww

w.fi

rstc

omm

un

ityb

ank.

co.k

e/in

dex

.ph

p?o

pti

on=c

om_c

onte

nt&

task

=vie

w&

id=1

26&

Item

id=1

38.

105

htt

p:/

/ww

w.a

lbar

aka.

co.z

a/A

bou

t_al

Bar

aka/

Cor

por

ate_

Profi

le.a

spx.

106

htt

p:/

/ww

w.a

bsa.

co.z

a/A

bsac

oza/

Ind

ivid

ual

/Ban

kin

g/Ex

clu

sive

-Ban

kin

g/Is

lam

ic-B

anki

ng.

107

htt

p:/

/ww

w.i

ban

k.co

.th

/201

0/en

/abo

ut/

abou

t_d

etai

l.as

px?

ID=1

.10

8h

ttp

://w

ww

.icf

al.c

om.a

u/a

bou

t_u

s.h

tm.

109

htt

p:/

/ww

w.m

cca.

com

.au

/Pag

es/A

bou

tus.

htm

l.11

0h

ttp

://w

ww

.kau

thar

ban

k.co

m/e

n/.

111

htt

p:/

/als

ham

scap

ital

.com

/.11

2h

ttp

://w

ww

.ku

veyt

turk

.com

.tr/

en/H

akki

miz

da_

Tari

hce

.asp

x.

176(C

onti

nu

ed)

Co

un

try

No

.of

Isla

mic

Ban

ks

Nam

eo

fth

eB

ank

Yea

ro

fes

tab

lish

men

tSp

ecia

lFe

atu

res

IFIS

Isla

mic

Ban

kin

g113

No

info

rmat

ion

firs

tco

mp

any

inth

eG

erm

anm

arke

tth

atke

eps

stri

ctly

wit

hin

the

fram

ewor

kof

Ger

man

and

Euro

pea

nri

ghts

toth

eru

les

ofIs

lam

.

Un

ited

Kin

gdom

06A

BC

Inte

rnat

ion

alB

ank

plc

114

1980

AB

C’s

net

wor

ksp

read

sov

er22

cou

ntr

ie

Ah

liU

nit

edB

ank11

519

97A

hli

Un

ited

Ban

k(U

K)

PLC

(AU

BU

Kfo

rmer

lykn

own

asT

he

Un

ited

Ban

kof

Ku

wai

tPL

C)

intr

odu

ced

Man

zil

Hom

ePu

rch

ase

Plan

Euro

pea

nIs

lam

icIn

vest

men

tB

ank

PLC

116

Jan

uar

y,20

05Fi

rst

ind

epen

den

tsh

aria

hco

mp

lain

tIs

lam

icin

vest

men

tba

nk

auth

oriz

edby

FSA

QIB

(UK

)117

No

info

rmat

ion

Ass

etm

anag

emen

t,co

rpor

ate

fin

ance

,rea

les

tate

and

trea

sury

.

Gat

ehou

seB

ank

PLC

118

2008

Pion

eeri

ng

FSA

regu

late

dba

nk

offe

rin

gSh

aria

hco

mp

lian

tw

hol

esal

eba

nki

ng

serv

ices

base

din

Lon

don

,UK

.

113

htt

p:/

/ww

w.k

uve

yttu

rk.c

om.t

r/en

/Hak

kim

izd

a_Ta

rih

ce.a

spx.

114

htt

p:/

/wik

i.is

lam

icfi

nan

ce.d

e/in

dex

.ph

p/A

BC

_In

tern

atio

nal

_Ban

k_p

lc.

115

htt

p:/

/ww

w.i

ibu

.com

/.11

6h

ttp

://w

ww

.eii

b.co

.uk/

htm

l/ab

outu

s.as

p.

117

htt

p:/

/ww

w.q

ib-u

k.co

m/.

118

htt

p:/

/ww

w.g

ateh

ouse

ban

k.co

m/a

bou

t-u

s/h

isto

ry/.

177

Isla

mic

Ban

kof

Bri

tain

119

Sep

tem

ber,

2004

aun

ched

onth

eLo

nd

onSt

ock

Exch

ange

–A

IMm

arke

t–

onO

ctob

er12

,200

4.C

an

ad

a06

An

sar

Co-

Op

erat

ive

Hou

sin

gC

orp

orat

ion

Ltd

.120

No

info

rmat

ion

Th

eB

oard

Dec

lare

d6%

Patr

onag

eD

ivid

end

for

2009

An

-Nu

r(O

nta

rio)

Hou

sin

gC

oop

erat

ive

Cor

p.L

td.12

1N

oin

form

atio

nC

han

ces

for

grow

than

dd

iver

sifi

cati

on

Qu

rtu

baH

ousi

ng

Coo

per

ativ

e&

Al-

Itti

had

Inve

stm

ent

Inc12

2

1991

Tocr

eate

anIs

lam

icfi

nan

cial

base

for

shar

iaco

mp

lian

tin

vest

men

ts.

UM

Fin

anci

al12

320

04aw

ard

edB

est

Bu

sin

ess

Lead

ersh

ipin

Nor

thA

mer

ica

byW

orld

Fin

ance

Mag

azin

eIs

lam

icFi

nan

ceA

war

ds

in20

09

fron

tier

Alt

Cap

ital

Cor

por

atio

n12

4N

ovem

ber

1,20

06Sh

aria

hco

mp

lain

tm

utu

alfu

nd

s

Glo

bal

Pros

per

ata

Fun

ds12

5N

oin

form

atio

nPr

ovid

esgl

obal

iman

fun

d

119

htt

p:/

/ww

w.i

slam

ic-b

ank.

com

/abo

ut-

us/

.12

0h

ttp

://w

ww

.an

sarh

ousi

ng.

com

/mai

n.h

tm.

121

htt

p:/

/ww

w.n

urc

oop

.com

/.12

2h

ttp

://q

urt

uba

.ca/

en/p

rese

nta

tion

.htm

l.12

3h

ttp

://w

ww

.um

fin

anci

al.c

om/i

nd

ex.p

hp

?pag

e=co

nte

nt&

pid

=43.

124

htt

p:/

/ww

w.f

ron

tier

alt.

com

/fro

nti

eral

t-oa

sis-

irc.

htm

l.12

5h

ttp

://w

ww

.glo

balc

aree

rs.c

a/en

/abo

ut.

htm

.

178

(Con

tin

ued

)

Co

un

try

No

.of

Isla

mic

Ban

ks

Nam

eo

fth

eB

ank

Yea

ro

fes

tab

lish

men

tSp

ecia

lFe

atu

res

Un

ited

Sta

tes

14B

ank

ofW

hit

tier

126

Dec

embe

r20

,19

82O

nly

Tru

eC

omm

un

ity

Com

mer

cial

Ban

kH

ead

qu

arte

red

Wit

hin

Th

eC

ity

Of

Wh

itti

er

Dev

onB

ank12

7N

oin

form

atio

nPr

ovid

esm

ura

bah

ahan

dij

ara

pro

du

cts

only

Un

iver

sity

Isla

mic

Fin

anci

alC

orp

128

No

info

rmat

ion

Com

ple

teIs

lam

icba

nki

ng

solu

tion

assl

ogan

.

Am

een

Hou

sin

gC

oop

erat

ive

ofC

alif

orn

ia12

919

96Pr

ovid

esgo

odn

um

ber

ofp

rod

uct

s

Lari

baA

mer

ican

Fin

ance

Hou

se13

019

87se

rves

clie

nts

inal

lst

ates

eith

erd

irec

tly

orth

rou

ghit

saf

filia

te.

Gu

idan

ceR

esid

enti

al13

1N

oin

form

atio

nPr

ovid

esth

ree

sim

ple

step

sto

hom

eow

ner

ship

Zaya

nFi

nan

ceN

oin

form

atio

nPr

ovid

esfi

nan

cin

gfr

om$5

00,0

00to

$25

mil

lion

and

abov

ep

ertr

ansa

ctio

n

126

htt

ps:

//w

ww

.ban

kofw

hit

tier

.com

/abo

ut.

htm

.12

7h

ttp

://w

ww

.dev

onba

nk.

com

/isl

amic

/in

dex

.htm

l.12

8h

ttp

://w

ww

.un

iver

sity

isla

mic

fin

anci

al.c

om/I

BD

Mai

n.h

tml.

129

htt

p:/

/ww

w.a

mee

nh

ousi

ng.

com

/hom

e/ab

out-

us.

130

htt

ps:

//w

ww

.lar

iba.

com

/def

ault

.htm

.13

1h

ttp

://w

ww

.gu

idan

cere

sid

enti

al.c

om/.

179

All

ied

Ass

etA

dvi

sors

–Im

anFu

nd

132

Jun

e20

00M

arke

tsFl

uct

uat

e..

.Pri

nci

ple

sD

on’t

,is

the

slog

anof

this

ban

k

Azz

adA

sset

Man

agem

ent13

319

97Pr

ovid

esaz

aad

eth

ical

mid

cap

fun

d

JET

SD

JIM

Inte

rnat

ion

alIn

dex

Fun

d13

4Ju

ly1,

2009

ceas

edtr

adin

gon

Oct

ober

19,2

010.

Am

ana

Mu

tual

Fun

dTr

ust

135

1989

Prov

ides

Am

ana

Inco

me,

Am

ana

Gro

wth

and

Am

ana

Dev

elop

ing

wor

ld

Arc

apit

a136

No

info

rmat

ion

Op

erat

esin

Bah

rain

,Atl

anta

,Lon

don

and

Sin

gap

ore

Shar

iah

cap

ital

Inc.

137

No

info

rmat

ion

awar

ded

the

pre

stig

iou

sM

aste

rof

Isla

mic

Fun

ds

Aw

ard

in20

07

Un

icor

nIn

vest

men

tB

ank13

820

04in

tern

atio

nal

pre

sen

cein

the

Un

ited

Stat

es,

Mal

aysi

a,Tu

rkey

and

Sau

di

Ara

bia

132

htt

p:/

/ww

w.i

nve

staa

a.co

m/.

133

htt

p:/

/azz

ad.n

et/n

ew/a

bou

tus_

wh

yazz

ad.a

spx.

134

htt

p:/

/ww

w.j

avel

infu

nd

s.co

m/j

ets-

dji

m.p

hp

.13

5h

ttp

://w

iki.

isla

mic

fin

ance

.de/

ind

ex.p

hp

/Sat

urn

a_C

apit

al_C

orp

.13

6h

ttp

://w

ww

.arc

apit

a.co

m/a

bou

t/co

rpin

fo/o

verv

iew

.htm

l.13

7h

ttp

://w

ww

.sh

aria

hca

p.c

om/i

nd

ex.p

hp

.13

8h

ttp

://w

ww

.un

icor

nin

vest

men

tban

k.co

m/e

n/a

bou

t/st

rate

gic-

busi

nes

s-ov

ervi

ew.h

tml.

Appendix III: Glossary on IslamicFinance