appendix a independent accountants’ report on the …

TRANSCRIPT

APPENDIX A

INDEPENDENT ACCOUNTANTS’ REPORT ON THE PROFIT FORECAST AND

PROFIT PROJECTION

3 August 2012

The Board of DirectorsFEO Hospitality Asset Management Pte. Ltd.(as Manager of Far East Hospitality Real Estate Investment Trust)14 Scotts Road #06-01Far East PlazaSingapore 228213

DBS Trustee Limited(as Trustee of Far East Hospitality Real Estate Investment Trust)12 Marina Boulevard#44-01/04 DBS Asia Central @Marina Bay Financial Centre Tower 3Singapore 018982

Dear Sirs

Letter from the Independent Accountant on the Profit Forecast for the period from

1 August 2012 to 31 December 2012 and Profit Projection for the year ending

31 December 2013

This letter has been prepared for inclusion in the prospectus (the “Prospectus”) to be issuedin connection with the offering of stapled securities in Far East H-Trust, comprising Far EastHospitality Real Estate Investment Trust (“Far East H-REIT”) and Far East HospitalityBusiness Trust at the offering price range of between S$0.86 and S$0.93 per stapled security(the “Offering”).

The directors of FEO Hospitality Asset Management Pte. Ltd. (the “Directors”) areresponsible for the preparation and presentation of the forecast and projected statements oftotal return of Far East H-REIT for the period from 1 August 2012 to 31 December 2012 (the“Profit Forecast”) and the year ending 31 December 2013 (the “Profit Projection”), as setout on page 138 of the Prospectus, which have been prepared on the basis of theassumptions as set out on pages 140 to 153 of the Prospectus.

We have examined the Profit Forecast and Profit Projection as set out on page 138 of theProspectus in accordance with Singapore Standards on Assurance Engagements applicableto the examination of prospective financial information. The Directors are solely responsiblefor the Profit Forecast and Profit Projection including the assumptions set out on pages 140 to153 of the Prospectus on which they are based.

Profit Forecast

Based on our examination of the evidence supporting the assumptions, nothing has come toour attention which causes us to believe that these assumptions do not provide a reasonablebasis for the Profit Forecast. Further, in our opinion, the Profit Forecast is properly prepared

A-1

on the basis of the assumptions, is consistent with the accounting policies set out on pagesB-13 to B-19 of the Prospectus, and is presented in accordance with the relevant presentationprinciples of Recommended Accounting Practice 7 “Reporting Framework for Unit Trusts” (butnot all the required disclosures), issued by the Institute of Certified Public Accountants ofSingapore (“ICPAS”), which is the framework to be adopted by Far East H-REIT in thepreparation of its financial statements.

Profit Projection

The Profit Projection is intended to show a possible outcome based on the statedassumptions. As the length of the period covered by the Profit Projection extends beyond theperiod covered by the Profit Forecast, the assumptions used in the Profit Projection (whichincluded hypothetical assumptions about future events which may not necessarily occur) aremore subjective than would be appropriate for the profit forecast. The Profit Projection doesnot therefore constitute a profit forecast.

Based on our examination of the evidence supporting the assumptions, nothing has come toour attention which causes us to believe that these assumptions do not provide a reasonablebasis for the Profit Projection. Further, in our opinion, the Profit Projection are properlyprepared on the basis of the assumptions, is consistent with the accounting policies set out onpages B-13 to B-19 of the Prospectus, and is presented in accordance with the relevantpresentation principles of Recommended Accounting Practice 7 “Reporting Framework forUnit Trusts” (but not all the required disclosures), issued by the ICPAS which is the frameworkto be adopted by Far East H-REIT in the preparation of its financial statements.

Events and circumstances frequently do not occur as expected. Even if the events anticipatedunder the hypothetical assumptions described above occur, actual results are still likely to bedifferent from the Profit Forecast and Profit Projection since other anticipated eventsfrequently do not occur as expected and the variation may be material. The actual results maytherefore differ materially from those forecasted and projected. For these reasons, we do notexpress any opinion as to the possibility of achievement of the Profit Forecast and ProfitProjection.

Attention is drawn to the risk factors set out on pages 73 to 97 of the Prospectus whichdescribe the principal risks associated with the Offering to which the Profit Forecast and ProfitProjection relate and the sensitivity analysis of the Directors’ Profit Forecast and ProfitProjection as set out on pages 153 to 154 of the Prospectus.

Yours faithfully,

ERNST & YOUNG LLPPublic Accountants andCertified Public AccountantsSingapore

Partner- in-charge: Nelson Chen

A-2

APPENDIX B

INDEPENDENT ACCOUNTANTS’ REPORT ON THE EXAMINATION OF THE

UNAUDITED PRO FORMA FINANCIAL INFORMATION

3 August 2012

The Board of DirectorsFEO Hospitality Asset Management Pte. Ltd.(as Manager of Far East Hospitality Real Estate Investment Trust)14 Scotts Road #06-01Far East PlazaSingapore 228213

DBS Trustee Limited(as Trustee of Far East Hospitality Real Estate Investment Trust)12 Marina Boulevard#44-01/04 DBS Asia Central@ Marina Bay Financial Centre Tower 3Singapore 018982

Dear Sirs

Far East Hospitality Real Estate Investment Trust

We report on the unaudited pro forma financial information of Far East Hospitality Real EstateInvestment Trust (“Far East H-REIT”) set out on pages B-4 to B-24 of the prospectus (the“Prospectus”) to be issued in connection with the offering of stapled securities in Far EastH-Trust, comprising Far East H-REIT and Far East Hospitality Business Trust (the“Offering”). The unaudited pro forma financial information of Far East H-REIT has beenprepared for illustrative purposes only and is based on certain assumptions after makingcertain adjustments:

(i) Unaudited pro forma statements of total return for the years ended 31 December 2009,2010, 2011, and the three months ended 31 March 2011 and 31 March 2012, whichhave been prepared to provide information on the total return of Far East H-REIT had itacquired the properties comprising Albert Court Village Hotel, Changi Village Hotel,The Elizabeth Hotel, Landmark Village Hotel, Oasia Hotel, Orchard Parade Hotel, TheQuincy Hotel, Central Square Village Residences, Hougang Village Residences,Regency House and Riverside Village Residences (collectively, the “Properties”), andentered into master lease agreements with First Choice Properties Pte Ltd, Far EastOrganization Centre Pte. Ltd., Golden Development Private Limited, Golden LandmarkPte Ltd, Transurban Properties Pte. Ltd., Far East Orchard Limited (formerly known asOrchard Parade Holdings Limited), OPH Riverside Pte Ltd, Serene Land Pte Ltd,Oxley Hill Properties Pte Ltd and Riverland Pte Ltd (“Master Lease Agreements”),under the same terms set out in the Prospectus on 1 January 2009;

(ii) Unaudited pro forma cash flow statements for the year ended 31 December 2011 andthe three months ended 31 March 2012, which have been prepared to provide

B-1

information on the cash flows of Far East H-REIT, had it purchased the Properties andentered into the Master Lease Agreements, under the same terms set out in theProspectus on 1 January 2011; and

(iii) Unaudited pro forma balance sheets as at 31 December 2011 and 31 March 2012,which have been prepared to provide information on the financial position of Far EastH-REIT, had it purchased the Properties and entered into the Master LeaseAgreements, under the same terms set out in the Prospectus on 31 December 2011and 31 March 2012, respectively.

The unaudited pro forma financial information has been prepared for illustrative purposes onlyand, because of its nature, may not give a true picture of Far East H-REIT’s actual totalreturns, cash flows or financial position.

The unaudited pro forma financial information is the responsibility of the directors of FEOHospitality Asset Management Pte. Ltd. (the “Directors”). Our responsibility is to express anopinion on the unaudited pro forma financial information based on our work.

We carried out procedures in accordance with Singapore Statement of Auditing Practice 24Auditors and Public Offering Documents (“SSAP 24”). Our work, which involved noindependent examination of the underlying financial information, consisted primarily of:

(i) comparing the financial information used in the preparation of the unaudited pro formafinancial information to the audited financial statements and unaudited managementaccounts of the following companies which owned the Properties prior to theiracquisition by Far East H-REIT: First Choice Properties Pte Ltd, Far East OrganizationCentre Pte. Ltd., Golden Development Private Limited, Golden Landmark Pte Ltd, FarEast Orchard Limited (formerly known as Orchard Parade Holdings Limited), OPHRiverside Pte Ltd, Serene Land Pte Ltd, Oxley Hill Properties Pte Ltd and RiverlandPte Ltd for the years ended 31 December 2009, 2010 and 2011, and the three monthsended 31 March 2011 and 31 March 2012, and Transurban Properties Pte. Ltd. for theyear ended 31 December 2011 and the three months ended 31 March 2011 and31 March 2012. The aforementioned audited financial statements and unauditedmanagement accounts are hereinafter collectively referred to as “the RelevantFinancial Statements”; and

(ii) considering the evidence supporting the pro forma adjustments and discussing theunaudited pro forma financial information with the Directors.

In our opinion:

(i) the unaudited pro forma financial information has been properly prepared based oninformation in the Relevant Financial Statements (which were prepared in accordancewith Singapore Financial Reporting Standards) and is presented in accordance withthe relevant presentation principles of Recommended Accounting Practice 7“Reporting Framework for Unit Trusts” issued by the Institute of Certified PublicAccountants of Singapore;

(ii) the unaudited pro forma financial information has been properly prepared in a mannerconsistent with both the format of the financial statements and the accounting policiesto be adopted by Far East H-REIT;

(iii) each material adjustment to the information used in the preparation of the unauditedpro forma financial information is appropriate for the purpose of preparing suchfinancial information and in accordance with SSAP 24; and

B-2

(iv) the unaudited pro forma financial information has been properly prepared on the basisof the assumptions set out on pages B-5 to B-10 after making the adjustmentsdescribed on pages B-5 to B-10.

Yours faithfully,

ERNST & YOUNG LLPPublic Accountants andCertified Public AccountantsSingapore

Partner- in-charge: Nelson Chen

B-3

(A) INTRODUCTION

The Unaudited Pro Forma Financial Information of Far East H-REIT has been prepared forinclusion in the prospectus (the “Prospectus”) to be issued in connection with the initial publicoffering of the Stapled Securities in Far East H-Trust on the Singapore Exchange SecuritiesTrading Limited (the “Offering”).

Far East H-Trust is a hospitality stapled group comprising Far East H-REIT and Far EastH-BT. Far East H-REIT is a Singapore-based REIT established with the principal investmentstrategy of investing, directly or indirectly, in a diversified portfolio of income-producing realestate in Singapore, used primarily for hospitality and/or hospitality-related purposes, whetherwholly or partially, as well as real estate-related assets in connection to the foregoing. FarEast H-BT is a Singapore-based business trust which will be dormant as at the Listing Date.

Under the proposed initial public offering of the Stapled Securities in Far East H-Trust,329,366,000 Stapled Securities will be offered at an offering price range of between S$0.86and S$0.93 per Stapled Security (the “Offering Price”), payable in full on application. TheOffering consists of an international placement to investors, including institutional and otherinvestors in Singapore and an offering to the public in Singapore.

As at the Listing Date, the initial property portfolio of Far East H-REIT will comprise sevenhotels and four serviced residences, all of which are located in Singapore. The seven hotelsare Albert Court Village Hotel, Changi Village Hotel, The Elizabeth Hotel, Landmark VillageHotel, Oasia Hotel, Orchard Parade Hotel and The Quincy Hotel (together, the “Hotels”). Thefour serviced residences are Central Square Village Residences, Hougang VillageResidences, Regency House and Riverside Village Residences (together, the “Serviced

Residences”, and with the Hotels, the “Properties”).

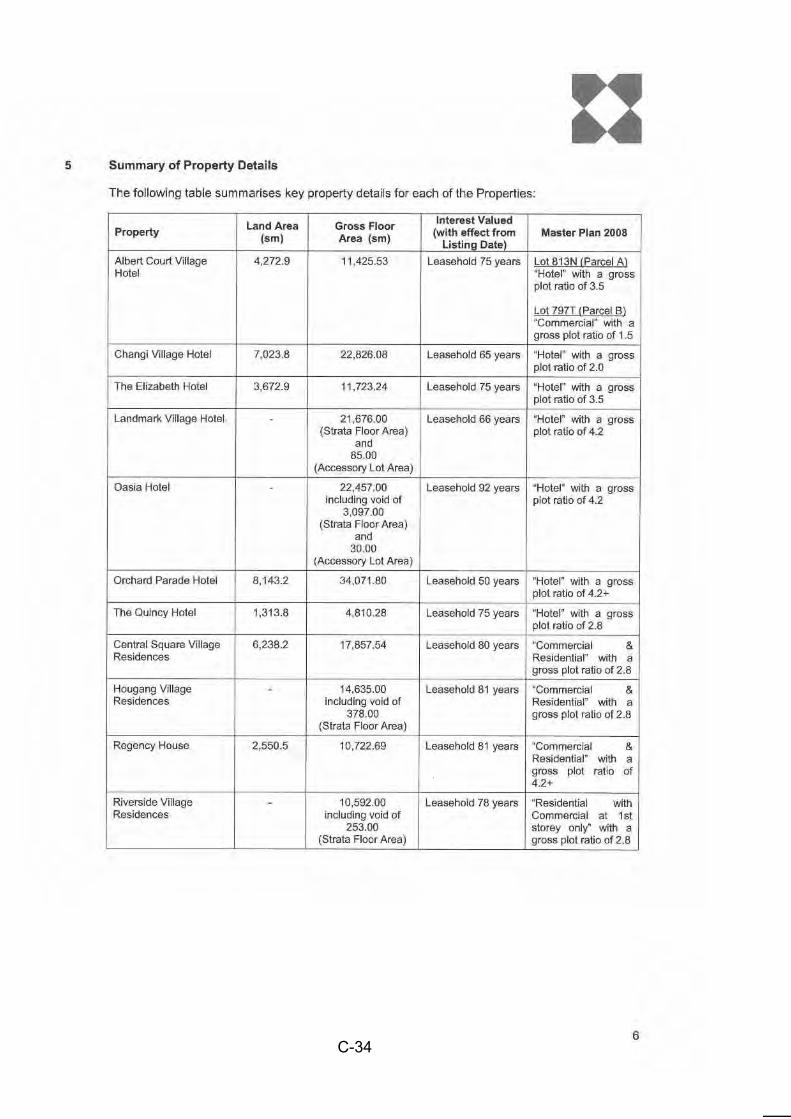

The tenures of the Properties to be acquired by Far East H-REIT from their respectivevendors (the “Vendors”) are set out in the table below.

Name of Property Leasehold Tenure(1) (years) Vendor and Master Lessee

Hotels

Albert Court Village Hotel 75 First Choice Properties Pte Ltd

Changi Village Hotel 65 Far East Organization Centre Pte. Ltd.

The Elizabeth Hotel 75 Golden Development Private Limited

Landmark Village Hotel 66 Golden Landmark Pte Ltd

Oasia Hotel 92 Transurban Properties Pte. Ltd.

Orchard Parade Hotel 50 Far East Orchard Limited

The Quincy Hotel 75 Golden Development Private Limited

Serviced Residences

Central Square Village Residences 80 OPH Riverside Pte Ltd

Hougang Village Residences 81 Serene Land Pte Ltd

Regency House 81 Oxley Hill Properties Pte Ltd

Riverside Village Residences 78 Riverland Pte Ltd

Note:

(1) This commences as at the Listing Date.

As at the Listing Date, the Vendors will also be Master Lessees of the Properties’ hotel andserviced residence operations. The initial term of the Master Lease Agreements for each ofthe Hotels and Serviced Residences will be 20 years with an option to obtain an additional

B-4

lease for a further 20 years on the same terms and conditions save for amendments requireddue to any change in law. Far East H-REIT may, in relation to any Property for which theoption for an additional lease is not exercised, enter into a new master lease agreement, onterms to be agreed, with either the existing Master Lessee or a new master lessee.

Details on the REIT Manager’s management fees, the REIT Trustee’s fee and the leasepayments under the Master Lease Agreements are set out in Section G.

(B) BASES OF PREPARATION OF UNAUDITED PRO FORMA FINANCIAL

INFORMATION

No financial statements of Far East H-Trust have been prepared for the financial years ended31 December 2009, 2010 and 2011 and the three months ended 31 March 2011 and31 March 2012 as Far East H-REIT and Far East H-BT were both constituted on 1 August2012.

Ernst & Young LLP has been appointed as auditors of Far East H-REIT and Far East H-BTsince their respective dates of constitution.

No pro forma financial information of Far East H-BT has been presented as it will be dormantas at the Listing Date. Accordingly, no consolidated pro forma financial information for FarEast H-Trust has been presented.

The Unaudited Pro Forma Financial Information of Far East H-REIT set out in this report,expressed in Singapore dollars, is prepared for illustrative purposes only and is based oncertain assumptions, and shows the Unaudited Pro Forma Statements of Total Return of FarEast H-REIT for each of the three years ended 31 December 2009, 2010 and 2011, and thethree months ended 31 March 2011 and 31 March 2012, the Unaudited Pro Forma BalanceSheets of Far East H-REIT as at 31 December 2011 and 31 March 2012, and the UnauditedPro Forma Cash Flow Statements of Far East H-REIT for the year ended 31 December 2011and the three months ended 31 March 2012. In preparing the Unaudited Pro Forma FinancialInformation, certain assumptions have been applied on the audited financial statements of theVendors. The aforementioned financial statements of the Vendors are hereinafter collectivelyreferred to as the “Relevant Financial Statements”.

B-5

The Relevant Financial Statements are audited by the following auditors:

Name of Auditor

Year End 2009 2010 2011

Hotels

Albert CourtVillage Hotel

31 December PricewaterhouseCoopersLLP

PricewaterhouseCoopersLLP

PricewaterhouseCoopersLLP

Changi VillageHotel

31 December AC Alliances AC Alliances Ernst & Young LLP

The ElizabethHotel

31 December Tan Choon Chye & Co Tan Choon Chye & Co Ernst & Young LLP

LandmarkVillage Hotel

30 September Ernst & Young LLP Ernst & Young LLP Ernst & Young LLP

Oasia Hotel 31 December N.A. N.A. Ernst & Young LLP

OrchardParade Hotel

31 December PricewaterhouseCoopersLLP

PricewaterhouseCoopersLLP

PricewaterhouseCoopersLLP

The QuincyHotel

31 December AC Alliances AC Alliances Ernst & Young LLP

Serviced Residences

Central SquareVillageResidences

31 December PricewaterhouseCoopersLLP

PricewaterhouseCoopersLLP

PricewaterhouseCoopersLLP

HougangVillageResidences

31 December AC Alliances AC Alliances Ernst & Young LLP

RegencyHouse

31 December AC Alliances AC Alliances Ernst & Young LLP

RiversideVillageResidences

30 September PricewaterhouseCoopersLLP

PricewaterhouseCoopersLLP

Ernst & Young LLP

The Unaudited Pro Forma Statements of Total Return of Far East H-REIT for the years ended31 December 2009, 2010 and 2011, and the three months ended 31 March 2011 and31 March 2012 reflect the total return of Far East H-REIT, assuming Far East H-REIT hadpurchased the Properties and entered into the Master Lease Agreements on 1 January 2009under the same terms set out in the Prospectus.

The Unaudited Pro Forma Cash Flow Statements show the cash flows of Far East H-REIT forthe year ended 31 December 2011 and the three months ended 31 March 2012, assumingFar East H-REIT had purchased the Properties and entered into the Master LeaseAgreements on 1 January 2011 under the same terms set out in the Prospectus.

The Unaudited Pro Forma Balance Sheets of Far East H-REIT as at 31 December 2011 and31 March 2012 present the financial position of Far East H-REIT, assuming Far East H-REIThad purchased the Properties and entered into the Master Lease Agreements on31 December 2011 and 31 March 2012, respectively, under the same terms set out in theProspectus.

The Unaudited Pro Forma Financial Information has been prepared on the basis of theaccounting policies as set out in Section F and is to be read in conjunction with Section G. Inaddition, the Unaudited Pro Forma Financial Information has been prepared based on theassumption that the issue price is the Maximum Offering Price and that the Over-AllotmentOption is fully exercised.

B-6

The Unaudited Pro Forma Financial Information is prepared for illustrative purposes only andbecause of its nature, may not give a true picture of Far East H-REIT’s actual total returns,cash flows or financial position.

(i) Unaudited Pro Forma Statements of Total Return

The Unaudited Pro Forma Statements of Total Return have been prepared on the basis thatFar East H-REIT purchased the Properties at their respective purchase prices and enteredinto the Master Lease Agreements on 1 January 2009.

The following assumptions were made for each of the periods presented:

Š Gross revenue for the Hotels and Serviced Residences is assumed to be computedbased on the terms of the Master Lease Agreements as set out in Section G Note 3,which have been applied to the gross operating revenue and gross operating profit inthe Relevant Financial Statements, where applicable, after making certain adjustmentsas set out below:

(S$’000)

AlbertCourtVillageHotel

ChangiVillageHotel

TheElizabeth

Hotel

LandmarkVillageHotel

OasiaHotel

OrchardParadeHotel

TheQuincyHotel Total

Pro FormaAdjustments Adjusted

Gross Operating Revenue

FY2009 9,386 21,590 13,967 17,558 N.A. 26,182 6,795 95,478 (2,594)(1)(2) 92,884

FY2010 12,294 26,666 18,401 23,018 N.A. 33,578 9,570 123,527 (2,659)(1)(2) 120,868

FY2011 12,396 27,963 17,855 24,883 10,862 34,568 10,097 138,624 44(2) 138,668

1Q2011 2,904 6,505 4,787 5,758 N.A. 8,584 2,396 30,934 - 30,934

1Q2012 2,702 6,878 4,475 6,040 6,789 8,787 2,444 38,115 - 38,115

Gross Operating Profit

FY2009 4,699 7,396 7,584 8,387 N.A. 16,126 3,014 47,206 4,371(1)(3)(4) 51,577

FY2010 7,024 12,555 11,653 12,673 N.A. 21,618 4,756 70,279 3,137(1)(3)(4) 73,416

FY2011 6,720 14,261 10,520 13,686 3,989 21,824 5,053 76,053 3,097(3)(4) 79,150

1Q2011 1,618 3,329 3,073 3,165 N.A. 5,695 1,195 18,075 855(3)(4) 18,930

1Q2012 1,085 3,414 2,550 3,023 3,412 5,575 1,164 20,223 913(3)(4) 21,136

(S$’000)

CentralSquareVillage

Residences

HougangVillage

ResidencesRegencyHouse

RiversideVillage

Residences TotalPro Forma

Adjustments Adjusted

Gross Operating Revenue

FY2009 7,029 2,968 5,313 4,557 19,867 93(5) 19,960

FY2010 8,787 4,243 6,074 5,500 24,604 66(5) 24,670

FY2011 9,976 5,487 7,113 6,246 28,822 65(5) 28,887

1Q2011 2,502 1,238 1,668 1,495 6,903 12(5) 6,915

1Q2012 2,380 1,281 1,698 1,533 6,892 22(5) 6,914

Gross Operating Profit

FY2009 3,864 1,181 3,255 2,957 11,257 1,679(4)(5) 12,936

FY2010 5,592 2,471 4,125 3,605 15,793 1,607(4)(5) 17,400

FY2011 6,593 3,293 4,922 4,179 18,987 1,929(4)(5) 20,916

1Q2011 1,741 764 1,190 999 4,694 475(4)(5) 5,169

1Q2012 1,571 809 1,171 1,048 4,599 474(4)(5) 5,073

Notes:

(1) Adjustments to exclude F&B revenue from 2009 to 2010 for outlets outsourced to a related party with effect from 2011.

(2) Adjustments to include rental revenue from 2009 to 2011 for areas previously leased out and returned to hotel operation

with effect from 2012.

B-7

(3) Adjustments to exclude MCST Sinking Fund payments to be borne by Far East H-REIT.

(4) Adjustments to:-

(i) Exclude staff costs relating to hospitality core management to be borne by Far East H-REIT as part of Property

Manager Fees.

(ii) Exclude previously charged selling, promotion and administrative expenses, and replace the same based on

agreed charge-out rates.

(5) Adjustments to include revenue and expenses derived from car park operations.

The variable rent component of Far East H-REIT’s gross revenue derived from the MasterLessees is computed as follows:

FY2009 FY2010 FY2011 1Q2011 1Q2012

Pro Forma Pro Forma Pro Forma Pro Forma Pro Forma

(S$’000) (S$’000) (S$’000) (S$’000) (S$’000)

% of adjusted gross operating revenue(1) 37,238 48,027 55,293 12,490 14,859% of adjusted gross operating profit(1) 21,104 29,416 32,298 7,874 9,512(3)

58,342 77,443 87,591 20,364 24,371Less: Fixed Rent 46,000 46,000 49,000(2) 11,500 15,850(3)

Variable Rent 12,409(4) 31,443 38,591 8,864 8,521

FY2009 FY2010 FY2011 1Q2011 1Q2012

Pro Forma Pro Forma Pro Forma Pro Forma Pro Forma

(S$’000) (S$’000) (S$’000) (S$’000) (S$’000)

Far East H-REIT’s gross revenue comprisingthose derived from:(a) Master Lessees based on terms of Master

Lease Agreements- Fixed Rent 46,000 46,000 49,000(2) 11,500 15,850(3)

- Variable Rent 12,409 31,443 38,591 8,864 8,521

58,409 77,443 87,591 20,364 24,371(b) Commercial rental revenue 15,513 15,452 16,805 4,006 4,351

73,922 92,895 104,396 24,370 28,722

Notes:

(1) The adjusted gross operating revenue and adjusted gross operating profit represent the gross operating revenue and

gross operating profit of the Properties on which Far East H-REIT’s gross revenue from the Master Lessees is derived

based on the terms of the Master Lease Agreements as set out in Section G note (c).

(2) Includes pro-rated fixed rent for Oasia Hotel which commenced operations in April 2011 and became fully operational in

October 2011.

(3) Includes pro-rated minimum guarantee for Oasia Hotel.

(4) As Hougang Village Residences’ Variable Rent in FY2009 was a negative S$66,360, the Variable Rent was capped at 0.

Š Property tax, insurance expense and Sinking Fund contributions previously incurred bythe respective Vendors of the Properties to be assumed by Far East H-REIT;

Š Other property expenses comprises property expenses of the commercial units suchas staff costs, property tax, property management fees, marketing expenses, utilities,repair and maintenance expenses, general and administrative expenses and othermiscellaneous operating expenses and are based on the amounts incurred on thecommercial units included in the Relevant Financial Statements;

Š REIT Manager’s management fees are based on the formula as set out in Section GNote 1;

Š REIT Trustee’s fee is based on the formula as set out in Section G Note 2;

Š Other trust expenses comprise annual listing fees, registry fees, audit and tax advisoryfees, valuation fees, legal fees, costs associated with the preparation of annual reports,investor communication costs and other miscellaneous costs. Other trust expenses ofS$18,028,000, S$1,040,000, S$1,082,000, S$270,000 and S$281,000 are assumed to

B-8

be incurred by Far East H-REIT for the years ended 31 December 2009, 2010 and2011, and the three months ended 31 March 2011 and 2012 respectively. Other trustexpenses for the year ended 31 December 2009 includes a one-off non-capitalisedissuance costs of S$17,028,000;

Š Capital expenditure incurred for the respective periods are assumed to be capitalisedas part of the value of the relevant Property and as such, would increase the value ofthe Far East H-REIT Deposited Property for purposes of computation of themanagement fees payable to the REIT Manager and the fees payable to the REITTrustee;

Š Capital expenditure incurred for the respective periods are assumed to be funded byborrowings;

Š The Far East H-REIT Debt Facilities, being $725.0 million unsecured floating ratebanking facilities, were in place at the time of the acquisition of the Properties;

Š Interest expense on borrowings is based on an effective interest rate of approximately2.5% per annum (inclusive of all margins and amortisation of upfront debt financingcost) and an average principal of S$651,594,000, S$654,595,000 and S$660,765,000,S$656,402,000 and S$666,175,000 for the years ended 31 December 2009, 2010 and2011 and the three months ended 31 March 2011 and 31 March 2012 respectively;

Š 100% of taxable income available for distribution to holders of Far East H-REIT Units isdistributed;

Š Far East H-REIT is not taxed on the taxable income that is distributed to holders of theStapled Securities;

Š Properties are acquired at an estimated aggregate purchase price of S$2,104,953,000;

Š The aggregate valuation of the Properties of S$2,139,850,000 remained unchangedthroughout the periods presented except to the extent of the assumed capitalexpenditure described below; and

Š Capital expenditure of S$3,187,000, S$2,815,000, S$9,525,000, S$796,000 andS$1,296,000 were incurred by Far East H-REIT on the Properties for the years ended31 December 2009, 2010 and 2011 and the three months ended 31 March 2011 and31 March 2012 respectively.

(ii) Unaudited Pro Forma Cash Flow Statements

The unaudited Pro Forma Cash Flow Statements for the year ended 31 December 2011 andthe three months ended 31 March 2012 have been prepared assuming Far East H-REIT hadpurchased the Properties and entered into the Master Lease Agreements on 1 January 2011,and is based on the cash flows directly attributable to the Properties and Far East H-REIT’sborrowing and unit structures.

In addition, the following assumptions were made:

Š Properties are acquired at an estimated aggregate purchase price of S$2,104,953,000;

Š Assets (comprising cash) and liabilities (comprising rental deposits of commercial unitsof the Hotels and Serviced Residences) directly attributable to the Properties,amounting to S$4,557,000 and S$4,557,000 respectively, were also acquired by FarEast H-REIT;

B-9

Š The Far East H-REIT Debt Facilities were in place at the time of the acquisition of theProperties;

Š The date that Far East H-REIT’s borrowings were fully drawn down and the StapledSecurities were issued correspond to the timing of the purchase of the Properties on1 January 2011;

Š Interest expense on borrowings is paid on a quarterly basis, in arrears in the followingquarter;

Š Management fees payable to the REIT Manager in the form of Stapled Securities arepaid on a quarterly basis, in arrears in the following quarter. Management fees payableto the REIT Manager in cash are paid on a monthly basis, in arrears in the followingmonth;

Š Capital expenditure of S$9,525,000 and S$1,296,000 incurred for the year ended31 December 2011 and the three months ended 31 March 2012 respectively isassumed to be capitalised as part of the value of the relevant Property and as such,would increase the value of the Far East H-REIT Deposited Property for purposes ofcomputation of the management fees payable to the REIT Manager and the feespayable to the REIT Trustee;

Š Capital expenditure incurred is assumed to be funded by borrowings;

Š Issue costs are assumed to be funded by proceeds raised from the Offering;

Š Proceeds raised, net of issue costs, from the Offering amounted to S$1,458,773,000;

Š Rental deposit remained unchanged at S$4,557,000;

Š 100% of taxable income available for distribution to holders of Far East H-REIT Units isdistributed for each of the periods presented. Distribution to holders of Far EastH-REIT Units are paid on a quarterly basis, in arrears; and

Š Far East H-REIT is not taxed on the taxable income that is distributed to holders of FarEast H-REIT Units.

(iii) Unaudited Pro Forma Balance Sheets

The unaudited Pro Forma Balance Sheets have been prepared on the basis that Far EastH-REIT purchased the Properties at their respective purchase prices and entered into theMaster Lease Agreements on 31 December 2011 and 31 March 2012.

The following assumptions are made:

Š Properties are acquired at an estimated aggregate purchase price of S$2,104,953,000;

Š Assets (comprising cash) and liabilities (comprising rental deposits of commercial unitsof the Hotels and Serviced Residences) directly attributable to the Properties,amounting to S$4,557,000 and S$4,557,000 as at 31 December 2011 and 31 March2012 respectively, were also acquired by Far East H-REIT;

Š Proceeds raised, net of issue costs, from the Offering amounted to S$1,458,773,000;

Š Issue costs relating to the Offering are estimated to be S$32,813,000 and are assumedto be funded by proceeds raised from the Offering; and

Š Borrowings of S$650,000,000 were drawn down by Far East H-REIT on 31 December2011 and 31 March 2012 to partially fund the acquisition of the Properties, issue anddebt related costs.

B-10

(C) UNAUDITED PRO FORMA STATEMENTS OF TOTAL RETURN

The unaudited Pro Forma Statements of Total Return of Far East H-REIT for the years ended31 December 2009, 2010 and 2011 and the three months ended 31 March 2011 and31 March 2012 have been prepared for inclusion in this Prospectus and are presented below.The assumptions used to prepare the unaudited Pro Forma Statements of Total Return areconsistent with those described in Bases of Preparation of Unaudited Pro Forma FinancialInformation.

FY2009 FY2010 FY2011 1Q2011 1Q2012

Note (S$’000) (S$’000) (S$’000) (S$’000) (S$’000)

Gross Revenue 9 73,922 92,895 104,396 24,370 28,722Property Expenses- Property tax (3,721) (3,459) (4,624) (1,091) (1,338)- Insurance expense (163) (142) (147) (29) (38)- Sinking Fund Contributions (276) (237) (46) (11) (11)- Other property expenses (4,315) (5,107) (4,892) (1,178) (1,368)

(8,475) (8,945) (9,709) (2,309) (2,755)

Net Property Income 65,447 83,950 94,687 22,061 25,967REIT Manager’s management fees (9,047) (9,796) (10,254) (2,492) (2,656)Trustee’s Fees (429) (429) (431) (107) (108)Other trust expenses (18,028) (1,040) (1,082) (270) (281)Finance costs (net) 10 (16,288) (16,360) (16,508) (4,101) (4,160)

Net income before tax and fair value change 21,655 56,325 66,412 15,091 18,762Fair value change in investment properties 34,897 - - - -

Net income before tax 56,552 56,325 66,412 15,091 18,762Income tax expense - - - - -

Net income after tax 56,552 56,325 66,412 15,091 18,762Add/(Less): Non-tax (chargable)/deductible items(net)(1) (9,553) 8,916 9,284 2,264 2,395

Income available for distribution to holders of FarEast H-REIT units 46,999 65,241 75,696 17,355 21,157

Note:

(1) “Non-tax (chargeable)/deductible items” comprise the REIT Manager’s management fees paid/payable in Stapled

Securities, Trustees’ fees, amortisation of upfront debt financing cost, fair value change in investment properties and

non-capitalised issuance costs.

B-11

(D) UNAUDITED PRO FORMA CASH FLOW STATEMENTS

The unaudited Pro Forma Cash Flow Statements for the year ended 31 December 2011 andthe three months ended 31 March 2012 have been prepared for inclusion in the Prospectusand presented below. The assumptions used to prepare the unaudited Pro Forma Cash FlowStatement are consistent with those described in Bases of Preparation of Unaudited ProForma Financial Information.

FY2011 1Q 2012

(S$’000) (S$’000)

Operating activities

Net income before income tax 84,527 18,825Adjustments for:Finance costs 16,364 4,124Fair value change in investment properties (34,897) -Non-capitalised issuance costs 17,028 -REIT Manager’s management fees paid or payable in Far East H-REIT Units 8,188 2,121

Operating income before working capital changes 91,210 25,070Changes in trade payables 171 6Changes in trade receivables (7,299) (825)Finance costs paid (15,714) (3,961)

Cash flows from operating activities 68,368 20,290

Investing activities

Purchase of investment properties and related assets and liabilities(1) (2,100,396) -Capital expenditure (9,525) (1,296)

Cash flows used in investing activities (2,109,921) (1,296)

Financing activities

Proceeds from issue of Far East H-REIT Units (net of issuance costs) 1,458,773 -Proceeds from borrowings 656,674 1,296Distribution to holders of Far East H-REIT Units (56,944) (18,981)

Cash flows from/(used in) financing activities 2,058,503 (17,685)

Net increase in cash & cash equivalents 16,950 1,309Cash & cash equivalents at beginning of year/ period - 16,950

Cash & cash equivalents at end of year/ period 16,950 18,259

Note:

(1) The effect of acquisition of the Properties and related assets and liabilities of Far East H-REIT’s pro forma cash flows for

the year ended 31 December 2011 is set out below:

FY2011

(S$’000)

Investment properties 2,104,953Cash 4,557Rental deposits (4,557)

Net assets acquired 2,104,953

Purchase price (2,104,953)

Less:Cash acquired 4,557

Net cash outflow (2,100,396)

Significant Non-Cash Transactions

During the year ended 31 December 2011 and the three months ended 31 March 2012,8,804,815 and 2,281,045 Stapled Securities at S$0.93 per Stapled Security, amounting toapproximately S$8,188,000 and S$2,121,000, were issued and accrued as payment for theportion of the REIT Manager’s management fees which is payable in the form of StapledSecurities (see Section G note (1)).

B-12

(E) UNAUDITED PRO FORMA BALANCE SHEETS

The unaudited Pro Forma Balance Sheets as at 31 December 2011 and 31 March 2012 havebeen prepared for inclusion in the Prospectus and is presented below. The assumptions usedto prepare the unaudited Pro Forma Balance Sheet are consistent with those described inBases of Preparation of Unaudited Pro Forma Financial Information.

As at31 December

2011

As at31 March

2012

Note (S$’000) (S$’000)

Non-current assets

Investment Properties 2 2,139,850 2,139,850Current assets

Cash and cash equivalents 5,527 5,527

Total assets 2,145,377 2,145,377

Current liabilities

Rental deposits 3 4,557 4,557Non-current liabilities

Borrowings (net of upfront debt financing costs) 4 647,150 647,150

Total liabilities (excluding net assets attributable to holders of Far

East-H REIT Units) 651,707 651,707

Net assets attributable to holders of Far East H-REIT Units 5 1,493,670 1,493,670

Number of Far East H-REIT Units in issue (’000) 1,603,888 1,603,888

Net asset value per Far East H-REIT Unit (S$) 0.93 0.93

(F) NOTES TO THE UNAUDITED PRO FORMA FINANCIAL INFORMATION

1. Significant Accounting Policies of Far East H-REIT

The significant accounting policies of Far East H-REIT, which have been consistently appliedin preparing the Unaudited Pro Forma Financial Information set out in this report, are asfollows:

Basis of Preparation of the Unaudited Pro Forma Financial Information

The Unaudited Pro Forma Financial Information, which is expressed in Singapore dollars androunded to the nearest thousand, is prepared in accordance with the bases set out in SectionB and applied to financial information prepared in accordance with Singapore FinancialReporting Standards (but not all the required disclosures), which is the accounting frameworkto be adopted by Far East H-REIT, and the provisions of the Trust Deed.

The Unaudited Pro Forma Financial Information is prepared on the historical cost basis,except that investment properties are stated at valuation.

The functional currency of Far East H-REIT is Singapore dollars. Revenue, expenses,receipts and payments are denominated primarily in Singapore dollars.

The preparation of the Unaudited Pro Forma Financial Information requires the REITManager to make judgments, estimates and assumptions that affect the application ofaccounting policies and the reported amounts of assets and liabilities.

Estimates and underlying assumptions are reviewed by the REIT Manager on an ongoingbasis. Revisions to accounting estimates are recognised in the period in which the estimate isrevised and in any future periods affected.

B-13

Investment Properties

Investment properties comprise completed properties and properties under construction orredevelopment to earn rentals or for capital appreciation or both.

Investment properties are measured initially at cost, including transaction costs incurred tobring the property to the condition necessary for it to be capable of operating. The carryingamount includes the cost of replacing part of an existing investment property at the time thatcost is incurred if the recognition criteria are met; and excludes the cost of day-to-dayservicing of an investment property. Subsequent to initial recognition, investment propertiesare stated at fair value, representing open market values, determined by independentprofessional valuers. Gains or losses arising from changes in the fair values of investmentproperties are included in profit or loss in the year in which they arise.

Investment properties are derecognised when either they have been disposed of or when theinvestment properties are permanently withdrawn from use and no future economic benefit isexpected from the disposal. Any gains or losses on the retirement or disposal of aninvestment property are recognised in profit or loss in the period of derecognition. Investmentproperties are subject to renovations or improvements at regular intervals. The cost of majorrenovations and improvements is capitalised and the carrying amounts of the replacedcomponents are recognised in profit or loss. The cost of maintenance, repairs and minorimprovements is recognised in profit or loss when incurred.

Investment properties are not subject to depreciation.

Impairment of non-financial assets

The REIT Manager assesses at each reporting date whether there is an indication that anasset may be impaired. If any indication exists, or when an annual impairment testing for anasset is required, the REIT Manager makes an estimate of the asset’s recoverable amount.

An asset’s recoverable amount is the higher of an asset’s or cash-generating unit’s fair valueless costs to sell and its value in use and is determined for an individual asset, unless theasset does not generate cash inflows that are largely independent of those from other assetsor group of assets. Where the carrying amount of an asset or cash-generating unit exceedsits recoverable amount, the asset is considered impaired and is written down to itsrecoverable amount. In assessing value in use, the estimated future cash flows expected tobe generated by the asset are discounted to their present value using a pre-tax discount ratethat reflects current market assessments of the time value of money and the risks specific tothe asset. In determining fair value less costs to sell, recent market transactions are taken intoaccount, if available. If no such transactions can be identified, an appropriate valuation modelis used. These calculations are corroborated by valuation multiples, or other available fairvalue indicators.

Impairment losses are recognised in profit or loss in those expense categories consistent withthe function of the impaired asset.

For assets excluding goodwill, an assessment is made at each reporting date as to whetherthere is any indication that previously recognised impairment losses may no longer exist ormay have decreased. If such indication exists, the REIT Manager estimates the asset’s orcash-generating unit’s recoverable amount. A previously recognised impairment loss isreversed only if there has been a change in the estimates used to determine the asset’srecoverable amount since the last impairment loss was recognised. If that is the case, the

B-14

carrying amount of the asset is increased to its recoverable amount. That increase cannotexceed the carrying amount that would have been determined, net of depreciation, had noimpairment loss been recognised previously. Such reversal is recognised in profit or lossunless the asset is measured at revalued amount, in which case the reversal is treated as arevaluation increase.

Financial assets

Financial assets are recognised when, and only when, Far East H-REIT becomes a party tothe contractual provisions of the financial instrument. The REIT Manager determines theclassification of financial assets at initial recognition.

Financial assets are initially recognised at fair value plus transaction costs except for financialassets, at fair value through profit or loss, which are recognised at fair value. Transactioncosts for financial assets at fair value through profit or loss are recognised immediately asexpenses.

Non-derivative financial assets with fixed or determinable payments that are not quoted in anactive market are classified as loans and receivables. Subsequent to initial recognition, loansand receivables are measured at amortised cost using the effective interest method, lessimpairment. Gains and losses are recognised in profit or loss when the loans and receivablesare derecognised or impaired, and through the amortisation process.

A financial asset is derecognised where the contractual right to receive cash flows from theasset has expired. On disposal of a financial asset in its entirety, the difference between thecarrying amount and the sum of the consideration received and any cumulative gain or lossthat had been recognised in other comprehensive income is recognised in profit or loss.

All regular way purchases and sales of financial assets are recognised or derecognised onthe trade date i.e., the date that the REIT Manager commits to purchase or sell the asset.Regular way purchases or sales are purchases or sales of financial assets that requiredelivery of assets within the period generally established by regulation or convention in themarketplace concerned.

Impairment of financial assets

The REIT Manager assesses at each end of the reporting period whether there is anyobjective evidence that a financial asset is impaired.

For financial assets carried at amortised cost, the REIT Manager first assesses whetherobjective evidence of impairment exists individually for financial assets that are individuallysignificant, or collectively for financial assets that are not individually significant. If the REITManager determines that no objective evidence of impairment exists for an individuallyassessed financial asset, whether significant or not, it includes the asset in a group offinancial assets with similar credit risk characteristics and collectively assesses them forimpairment. Assets that are individually assessed for impairment and for which an impairmentloss is, or continues to be recognised, are not included in a collective assessment ofimpairment.

If there is objective evidence that an impairment loss on financial assets carried at amortisedcost has incurred, the amount of the loss is measured as the difference between the asset’scarrying amount and the present value of estimated future cash flows discounted at thefinancial asset’s original effective interest rate. If a loan has a variable interest rate, the

B-15

discount rate for measuring any impairment loss is the current effective interest rate. Thecarrying amount of the asset is reduced through the use of an allowance account. Theimpairment loss is recognised in profit or loss.

When the asset becomes uncollectible, the carrying amount of impaired financial assets isreduced directly or if an amount was charged to the allowance account, the amounts chargedto the allowance account are written off against the carrying value of the financial asset.

To determine whether there is objective evidence that an impairment loss on financial assetshas incurred, the REIT Manager considers factors such as the probability of insolvency orsignificant financial difficulties of the debtor and default or significant delay in payments.

If in a subsequent period, the amount of the impairment loss decreases and the decrease canbe related objectively to an event occurring after the impairment was recognised, thepreviously recognised impairment loss is reversed to the extent that the carrying amount ofthe asset does not exceed its amortised cost at the reversal date. The amount of reversal isrecognised in profit or loss.

Cash and cash equivalents

Cash and cash equivalents comprise cash and demand deposits.

Financial liabilities

Financial liabilities are recognised when, and only when, Far East H-REIT becomes a party tothe contractual provisions of the financial instrument. The REIT Manager determines theclassification of financial liabilities at initial recognition.

Financial liabilities are initially recognised at fair value plus transaction costs except forfinancial liabilities, at fair value through profit or loss, which are recognised at fair value.

After initial recognition, financial liabilities other than those designated at fair value throughprofit or loss are subsequently measured at amortised cost using the effective interest ratemethod. Gains and losses are recognised in profit or loss when the liabilities arederecognised, and through the amortisation process.

A financial liability is de-recognised when the obligation under the liability is discharged orcancelled or expires. When an existing financial liability is replaced by another from the samelender on substantially different terms, or the terms of an existing liability are substantiallymodified, such an exchange or modification is treated as a de-recognition of the originalliability and the recognition of a new liability, and the difference in the respective carryingamounts is recognised in profit or loss

Net assets attributable to Holders of Far East H-REIT

Net assets attributable to holders of Far East H-REIT Units represent the holders’ residualinterest in Far East H-REIT’s net assets upon termination.

Expenses incurred in connection with the initial public offering of Far East H-REIT Units andlisting on the SGX-ST are deducted directly against net assets attributable to holders of FarEast H-REIT Units.

B-16

Revenue recognition

Rental income receivable under operating leases is recognised on a straight-line basis overthe term of the lease.

Interest income is recognised using the effective interest method.

Expenses

Property expenses are recognised on an accrual basis.

Fees paid and payable to the REIT Manager are recognised on an accrual basis based on theformula stipulated in Section G Note 1.

Trust expenses are recognised on an accrual basis.

Borrowing costs are capitalised as part of the cost of a qualifying asset if they are directlyattributable to the acquisition, construction or production of that asset. Capitalisation ofborrowing costs commences when the activities to prepare the asset for its intended use orsale are in progress and the expenditures and borrowing costs are incurred. Borrowing costsare capitalised until the assets are substantially completed for their intended use or sale. Allother borrowing costs are expensed in the period they occur. Borrowing costs consist ofinterest and other costs that an entity incurs in connection with the borrowing of funds.

Taxes

(i) Current tax

Current income tax assets and liabilities for the current and prior periods are measuredat the amount expected to be recovered from or paid to the taxation authorities. Thetax rates and tax laws used to compute the amount are those that are enacted orsubstantively enacted at the end of the reporting period. Current income taxes arerecognised in profit or loss.

(ii) Deferred tax

Deferred tax is provided using the liability method on temporary differences at the endof the reporting period between the tax bases of assets and liabilities and their carryingamounts for financial reporting purposes.

Deferred tax liabilities are recognised for all temporary differences, except where thedeferred tax liability arises from the initial recognition of goodwill or of an asset orliability in a transaction that is not a business combination and, at the time of thetransaction, affects neither the accounting profit nor taxable profit or loss.

Deferred tax assets are recognised for all deductible temporary differences, carryforward of unused tax credits and unused tax losses, to the extent that it is probablethat taxable profit will be available against which the deductible temporary differences,and the carry forward of unused tax credits and unused tax losses can be utilisedexcept where the deferred tax asset relating to the deductible temporary differencearises from the initial recognition of an asset or liability in a transaction that is not abusiness combination and, at the time of the transaction, affects neither the accountingprofit nor taxable profit or loss.

The carrying amount of deferred tax assets is reviewed at the end of each reportingperiod and reduced to the extent that it is no longer probable that sufficient taxable

B-17

profit will be available to allow all or part of the deferred tax asset to be utilised.Unrecognised deferred tax assets are reassessed at the end of each reporting periodand are recognised to the extent that it has become probable that future taxable profitwill allow the deferred tax asset to be recovered.

Deferred tax assets and liabilities are measured at the tax rates that are expected toapply in the year when the asset is realised or the liability is settled, based on tax rates(and tax laws) that have been enacted or substantively enacted at the end of eachreporting period.

Deferred tax assets and deferred tax liabilities are offset, if a legally enforceable rightexists to set off current income tax assets against current income tax liabilities and thedeferred taxes relate to the same taxable entity and the same taxation authority.

(iii) Sales tax

Revenue, expenses and assets are recognised net of the amount of sales tax except:

(a) Where the sales tax incurred on a purchase of assets or services is notrecoverable from the taxation authority, in which case the sales tax isrecognised as part of the cost of acquisition of the asset or as part of theexpense item as applicable; and

(b) Receivables and payables that are stated with the amount of sales tax included.

The net amount of sales tax recoverable from, or payable to, the taxation authority isincluded as part of receivables or payables in the balance sheet.

Related parties

A related party is defined as follows:

(i) A person or a close member of that person’s family is related to the Trust if thatperson:

(a) Has control or joint control over the Trust;

(b) Has significant influence over the Trust; or

(c) Is a member of the key management personnel of the Trust or REIT Manager orof a parent of the Trust.

(ii) An entity is related to the Trust if any of the following conditions applies:

(i) The entity and the Trust are members of the same group (which means thateach parent, subsidiary and fellow subsidiary is related to the others).

(ii) One entity is an associate or joint venture of the other entity (or an associate orjoint venture of a member of a group of which the other entity is a member).

(iii) Both entities are joint ventures of the same third party.

(iv) One entity is a joint venture of a third entity and the other entity is an associateof the third entity.

(v) The entity is a post-employment benefit plan for the benefit of employees of anentity related to the Trust. If the Trust is itself such a plan, the sponsoringemployers are also related to the Trust;

B-18

(vi) The entity is controlled or jointly controlled by a person identified in (i);

(vii) A person identified in (i)(a) has significant influence over the entity or is amember of the key management personnel of the entity (or of a parent of theentity).

Segment reporting

A segment is a distinguishable component of Far East H-REIT that is engaged in eitherproviding goods or services (business segment), or in providing goods or services within aparticular economic environment (geographical segment), which is subject to risks andrewards that are different from those of other segments.

No business segment information has been presented as the REIT Manager is of the viewthat all the properties are being leased and operated as hotels and serviced residences andthe contribution of the commercial units of the Properties to Far East H-REIT’s results and netassets is insignificant. No geographical segment has been presented as all the properties arelocated in Singapore.

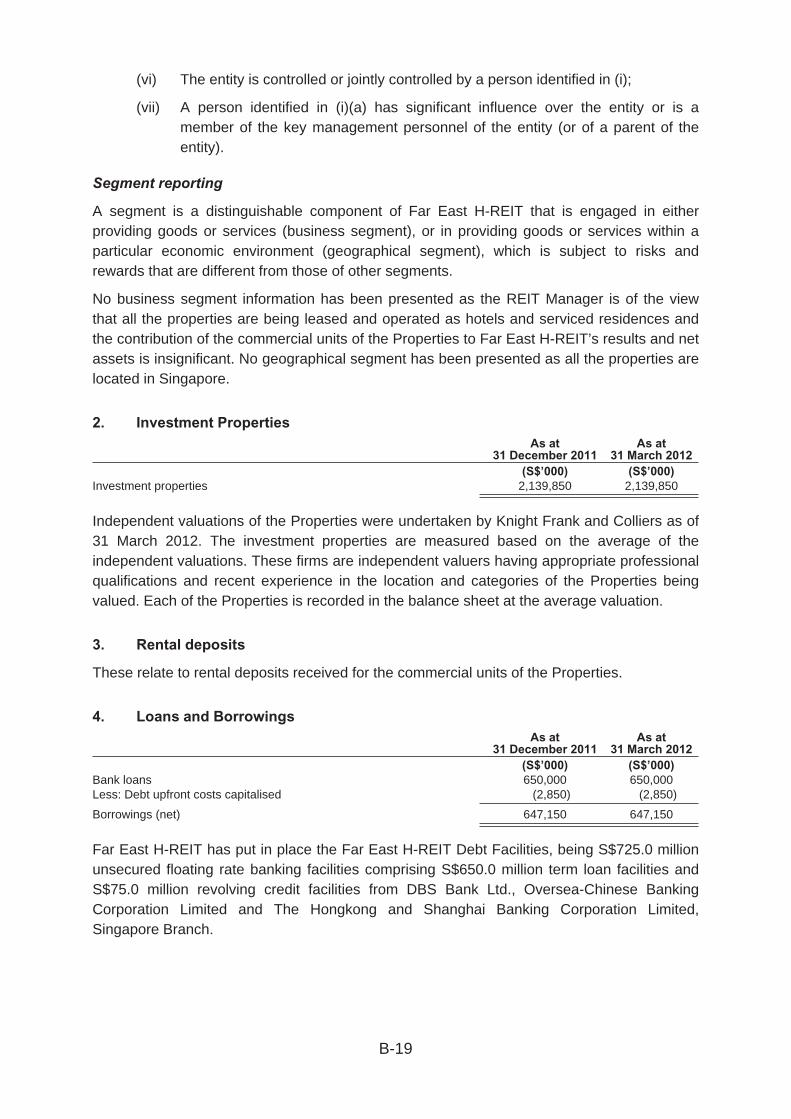

2. Investment Properties

As at31 December 2011

As at31 March 2012

(S$’000) (S$’000)

Investment properties 2,139,850 2,139,850

Independent valuations of the Properties were undertaken by Knight Frank and Colliers as of31 March 2012. The investment properties are measured based on the average of theindependent valuations. These firms are independent valuers having appropriate professionalqualifications and recent experience in the location and categories of the Properties beingvalued. Each of the Properties is recorded in the balance sheet at the average valuation.

3. Rental deposits

These relate to rental deposits received for the commercial units of the Properties.

4. Loans and Borrowings

As at31 December 2011

As at31 March 2012

(S$’000) (S$’000)

Bank loans 650,000 650,000Less: Debt upfront costs capitalised (2,850) (2,850)

Borrowings (net) 647,150 647,150

Far East H-REIT has put in place the Far East H-REIT Debt Facilities, being S$725.0 millionunsecured floating rate banking facilities comprising S$650.0 million term loan facilities andS$75.0 million revolving credit facilities from DBS Bank Ltd., Oversea-Chinese BankingCorporation Limited and The Hongkong and Shanghai Banking Corporation Limited,Singapore Branch.

B-19

5. Net Assets Attributable to Unitholders

As at31 December 2011

As at31 March 2012

Note (S$’000) (S$’000)

Far East H-REIT Units in issue 1,491,616 1,491,616Fair value change in investment properties 34,897 34,897Issue costs 8 (32,813) (32,813)

Net assets attributable to holders of Far East H-REIT Units 1,493,700 1,493,700

1,603,888,000 units in issue as at the Listing Date relate to the number of units in issueimmediately after the completion of the Offering.

Each unit in Far East H-REIT represents an undivided interest in Far East H-REIT. The rightsand interests of holders of Far East H-REIT Units are contained in the Trust Deed and includethe rights to:

(i) receive income and other distributions attributable to the units held;

(ii) participate in the termination of Far East H-REIT by receiving a share of all net cashproceeds derived from the realisation of the assets of Far East H-REIT less anyliabilities, in accordance with their proportionate interests in Far East H-REIT.However, a holder of the Far East H-REIT Units does not have the right to require anyassets (or part thereof) of Far East H-REIT be returned to him;

The restrictions of a holder of the Far East H-REIT Units include the following:

(i) a holder of the right is limited to the right to require due administration of Far EastH-REIT in accordance with the provisions of the Trust Deed; and

(ii) a holder of the Far East H-REIT Units has no right to request to redeem his units whilehis units are listed on SGX-ST.

The liability of a holder of the Far East H-REIT Units is limited to the amount paid or payablefor any unit in Far East H-REIT. The provisions of the Far East H-REIT Trust Deed providethat no holders of the Far East H-REIT Units will be personally liable to indemnify the REITTrustee or any creditor of Far East H-REIT in the event that the liabilities of Far East H-REITexceed its assets.

Under the Far East H-REIT Trust Deed, every Far East H-REIT Unit carries the same votingrights.

6. Financial Instruments

Financial risk management objectives and policies

Exposure to credit, currency, interest rate and liquidity risks arises in the normal course of FarEast H-REIT’s business. Far East H-REIT has written policies and guidelines, which set outits overall business strategies and its general risk management philosophy.

Credit risk

Credit risk is the risk of loss that may arise on outstanding financial instruments should acounterparty default on its obligations.

The REIT Manager’s objective is to seek continual revenue growth while minimising lossesincurred due to increased credit risk exposure. Credit evaluations are performed by the REITManager before lease agreements are entered into with lessees. In addition, Far East H-REIT

B-20

requires lessees to provide tenancy rental deposits. Cash and cash equivalents are placedwith financial institutions which are regulated.

At the pro forma balance sheet date, the investment properties of Far East H-REIT, except forthe commercial units of the Properties, are leased to Master Lessees. The maximumexposure to credit risk is represented by the carrying value of each financial asset on thebalance sheet.

Interest rate risk

Far East H-REIT’s exposure to changes in interest rates relate primarily to interest-earningfinancial assets and interest-bearing financial liabilities.

Currency risk

Far East H-REIT’s investment strategy is to invest, directly or indirectly, in a diversifiedportfolio of income-producing real estate in Singapore, used primarily for hospitality and/orhospitality purposes, whether wholly or partially, as well as real estate-related assets inconnection to the foregoing. As such, Far East H-REIT’s exposure to currency risk isinsignificant.

Liquidity risk

The REIT Manager monitors the liquidity of Far East H-REIT and maintains a level of cashand cash equivalents deemed adequate to finance Far East H-REIT’s operations. In addition,the REIT Manager also monitors and observes the Code on Collective Investment Schemesissued by the MAS concerning limits on total borrowings.

Fair values

The carrying amounts of financial assets and liabilities are reasonable approximation of fairvalues, either due to their short-term nature or that they are floating rate instruments that arere-priced to market interest rates on or near the end of the reporting period.

7. Commitments

Far East H-REIT entered into leases on its investment properties. Future minimum rentalreceivable under non-cancellable operating leases at the end of the reporting period are asfollows:

As at31 December 2011

As at31 March 2012

(S$’000) (S$’000)

Receivable- After 1 financial year 77,413 58,217- After 1 financial year but within 5 financial years 235,652 235,984- After 5 financial years 810,000 810,000

1,123,065 1,104,201

The above operating lease rental receivables comprise amounts receivable under the MasterLeases and the leases relating to the commercial units of the Properties.

Rental receivable under the Master Leases are based on the terms of the Master LeaseAgreements as set out in Section G Note 3. The amounts receivable for such leases arebased on the fixed rent as set out in the Master Leases.

B-21

The REIT Trustee has granted an option to each of the Master Lessees to obtain anadditional lease for another 20 years on expiry of the initial 20-year leases based on the sameterms as described above save for amendments required due to any changes in law.

8. Issue Costs

As at31 December 2011

As at31 March 2012

(S$’000) (S$’000)

Underwriting and selling commission 21,527 21,527Professional and other fees 5,394 5,394Miscellaneous issue expenses 5,892 5,892

Total issue costs 32,813 32,813

9. Gross Revenue

Gross revenue represents rental income received/receivable on Far East H-REIT’sinvestment properties.

10. Finance costs (net)

FY2009 FY2010 FY2011 1Q2011 1Q2012

(S$’000) (S$’000) (S$’000) (S$’000) (S$’000)

Interest paid and payable to banks 15,638 15,710 15,858 3,938 3,997Amortisation of debt upfront costs 650 650 650 163 163

16,288 16,360 16,508 4,101 4,160

(G) REIT MANAGER’S MANAGEMENT FEES, REIT TRUSTEE’S FEES AND LEASE

PAYMENTS UNDER MASTER LEASE AGREEMENTS

1. REIT Manager’s Management Fees

The REIT Manager is entitled under the Far East H-REIT Trust Deed to the followingmanagement fees:

(i) Base Fee of 0.03% per annum of the value of the Far East H-REIT’s DepositedProperty (being the gross assets of Far East H-REIT, as stipulated in the Far EastH-REIT Trust Deed); and

(ii) Performance Fee of 4.0% per annum of the Net Property Income (as defined in the FarEast H-REIT Trust Deed) of Far East H-REIT in the relevant financial year (calculatedbefore accounting for this additional fee in that financial year).

For Forecast Period 2012 and Projection Year 2013, 80.0% of the management fees payableto the REIT Manager will be paid in the form of Stapled Securities or (in the event thatUnstapling of the Far East H-REIT Units and Far East H-BT Units has taken place) Far EastH-REIT Units issued at the market price (as defined in the Far East H-REIT Trust Deed)prevailing at the date of issue and 20.0% of the management fees will be paid in the form ofcash.

Any increase in the maximum permitted rate or any change in the structure of the REITManager’s management fees must be approved by an Extraordinary Resolution at a meetingof holders of the Far East H-REIT Units duly convened and held in accordance with theprovisions of the Far East H-REIT Trust Deed.

B-22

The portion of the management fees payable in the form of Stapled Securities will be madeon a quarterly basis, in arrears. The portion of the management fees payable in the form ofcash will be made on a monthly basis, in arrears.

The aforementioned basis has been used to compute the REIT Manager’s management feesfor the purposes of the unaudited pro forma financial information of Far East H-REIT.

2. REIT Trustee’s Fees

The REIT Trustee’s fee is presently charged on a scaled basis of up to 0.02% per annum ofthe value of the Far East H-REIT Deposited Property, subject to a minimum of S$20,000 permonth, excluding out-of-pocket expenses and GST. The actual fee payable will be determinedbetween the REIT Manager and the REIT Trustee from time to time. The REIT Trustee willalso be paid a one-time inception fee of S$50,000. The REIT Trustee’s fee is payable out ofthe Deposited Property of Far East H-REIT on a monthly basis, in arrears.

Under the Far East H-REIT Trust Deed, the maximum fee which the REIT Trustee maycharge is 0.02% per annum of the Far East H-REIT Deposited Property. Any increase in theREIT Trustee’s fee beyond the current scaled basis of up to 0.02% per annum of the value ofthe Far East H-REIT Deposited Property will be subject to agreement between the REITManager and the REIT Trustee.

Any increase in the maximum permitted amount or any change in the structure of the REITTrustee’s fee must be approved by an Extraordinary Resolution at a meeting of holders of theFar East H-REIT Units duly convened and held in accordance with the provisions of the FarEast H-REIT Trust Deed.

The aforementioned basis has been used to compute the REIT Trustee’s fee for the purposeof the Unaudited Pro Forma Financial Information.

B-23

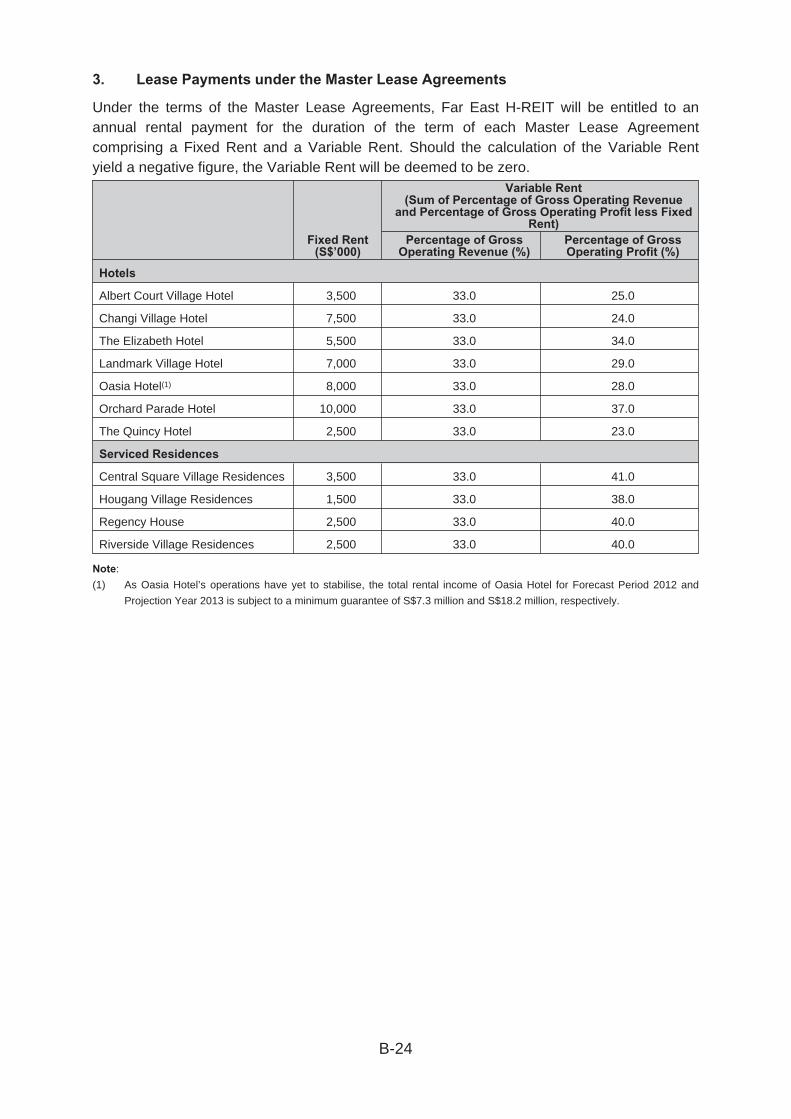

3. Lease Payments under the Master Lease Agreements

Under the terms of the Master Lease Agreements, Far East H-REIT will be entitled to anannual rental payment for the duration of the term of each Master Lease Agreementcomprising a Fixed Rent and a Variable Rent. Should the calculation of the Variable Rentyield a negative figure, the Variable Rent will be deemed to be zero.

Variable Rent(Sum of Percentage of Gross Operating Revenue

and Percentage of Gross Operating Profit less FixedRent)

Fixed Rent(S$’000)

Percentage of GrossOperating Revenue (%)

Percentage of GrossOperating Profit (%)

Hotels

Albert Court Village Hotel 3,500 33.0 25.0

Changi Village Hotel 7,500 33.0 24.0

The Elizabeth Hotel 5,500 33.0 34.0

Landmark Village Hotel 7,000 33.0 29.0

Oasia Hotel(1) 8,000 33.0 28.0

Orchard Parade Hotel 10,000 33.0 37.0

The Quincy Hotel 2,500 33.0 23.0

Serviced Residences

Central Square Village Residences 3,500 33.0 41.0

Hougang Village Residences 1,500 33.0 38.0

Regency House 2,500 33.0 40.0

Riverside Village Residences 2,500 33.0 40.0

Note:

(1) As Oasia Hotel’s operations have yet to stabilise, the total rental income of Oasia Hotel for Forecast Period 2012 and

Projection Year 2013 is subject to a minimum guarantee of S$7.3 million and S$18.2 million, respectively.

B-24

Colliers International Consultancy & Valuation (Singapore) Pte Ltd 1 Raffles Place #45-00, One Raffles Place Singapore 048616 RCB No. 198105965E

MAIN +65 6223 2323 FAX +65 6222 4901 URL www.colliers.com

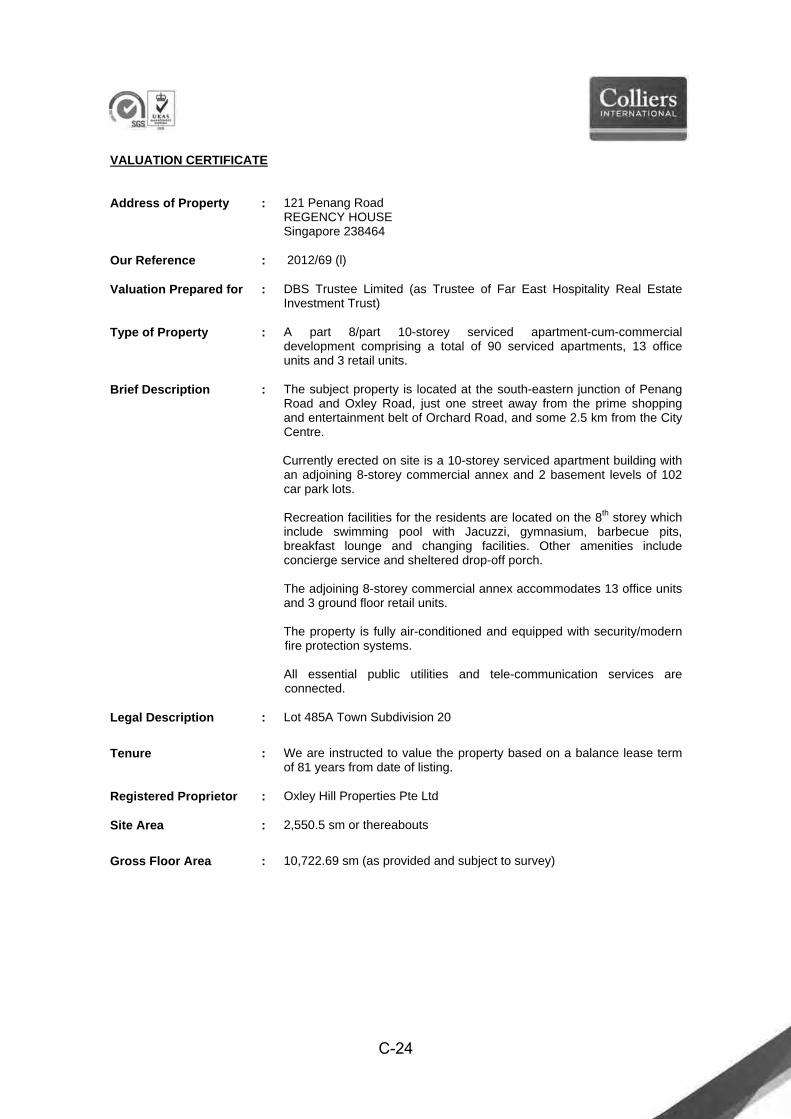

Our Ref: 2012/69 26 July 2012 DBS Trustee Limited (as Trustee of Far East Hospitality Real Estate Investment Trust) 12 Marina Boulevard Level 44 DBS Asia Central @ Marina Bay Financial Centre Tower 3 Singapore 018982 Manager of Far East H-Reit FEO Hospitality Asset Management Pte. Ltd. 14 Scotts Road #06-01 Far East Plaza Singapore 228213 Trustee-Manager of Far East H-BT FEO Hospitality Trust Management Pte. Ltd. 14 Scotts Road #06-01 Far East Plaza Singapore 228213 Dear Sirs, VALUATION OF: (1) ALBERT COURT VILLAGE HOTEL, 180 Albert Street, Singapore 189971 (2) CHANGI VILLAGE HOTEL, 1 Netheravon Road, Singapore 508502 (3) THE ELIZABETH HOTEL, 24 Mount Elizabeth, Singapore 228518 (4) LANDMARK VILLAGE HOTEL, 390 Victoria Street, Singapore 188061 (5) OASIA HOTEL, 8 Sinaran Drive, Singapore 307470 (6) ORCHARD PARADE HOTEL, 1 Tanglin Road, Singapore 247905 (7) THE QUINCY HOTEL, 22 Mount Elizabeth, Singapore 228517 (8) CENTRAL SQUARE VILLAGE RESIDENCES, 20 Havelock Road, Singapore 059765 (9) HOUGANG VILLAGE RESIDENCES, 1 Hougang Street 91, Singapore 538692 (10) REGENCY HOUSE, 121 Penang Road, Singapore 238464 (11) RIVERSIDE VILLAGE RESIDENCES, 30 Robertson Quay, Singapore 238251 Instructions We refer to your instructions to carry out a valuation in respect of the abovementioned properties for listing purposes. Our instructions are to provide our opinion of the market value of the unexpired leasehold interest in the properties as at 31 March 2012, on ‘as is’ basis and subject to the proposed master lease arrangement and existing tenancies. We confirm that we have inspected the subject properties and have prepared full valuation reports (“Reports”) in accordance with the requirements of the instructions. The valuation has been carried out in accordance with The Singapore Institute of Surveyors And Valuers’ Valuation Standards and Guidelines. Our valuation is on the basis of Market Value which is intended to mean “the estimated amount for which a property should exchange on the date of valuation between a willing buyer and a willing seller in an arm’s length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently and without compulsion”. In adopting this definition of value, we are of the opinion that it is consistent with the international definition of Market Value as advocated by the Royal Institution of Chartered Surveyors (RICS) and the International Valuation Standards (IVS).

/Volumes/data folders/~ DTP Job In Progress/R/RR Donnelley/Project Goldstar Prelims_Case ID_5435/final PDF/Appendix C_EDIT_R3.pdf, Page Count: 1 of 50, July 31, 2012, 19:43:30

C-1

APPENDIX C

2

Our valuation has been made on the assumption that the properties are sold in the open market without the benefit of a deferred term contract or any similar arrangement which could serve to affect the value of the property. No allowance has been made in our valuation for any charges, mortgages or amounts owing on the properties, nor for any expenses or taxation which may be incurred in effecting a sale. It is assumed that the properties are free from any major or material encumbrances, restrictions and outgoings of an onerous nature which could affect their values. Reliance on This Letter For the purpose of this Prospectus, we have prepared this letter and the enclosed valuation certificates which summarise our Reports and outline key factors which we have considered in arriving at our opinion of values. This letter and the valuation certificates do not contain all the necessary data and information included in our Reports. For further information, reference should be made to the Reports. The valuations and market information are not guarantees or predictions and must be read in consideration of the following: • The estimated value is based upon the factual information provided by the owner. Property

data/information provided is assumed to be correct. Whilst Colliers International has endeavoured to ensure the accuracy of the information, it has not independently verified all information provided by the owner. Colliers International also accepts no responsibility for subsequent changes in information as to areas, income, expenses or market conditions.

• The methodologies adopted in valuing the properties are based upon estimates of future results and are

not predictions. Each methodology is based on a set of assumptions as to income and expenses of the properties and future economic conditions in the local market.

Summary of Property Information

No. Property Balance

Lease Term (years)

No. of Rooms/Units

Gross Floor Area/Strata Area*

(sm)

1 180 Albert Street, ALBERT COURT VILLAGE HOTEL 75 210 11,425.5

2 1 Netheravon Road, CHANGI VILLAGE HOTEL 65 380 22,826.1

3 24 Mount Elizabeth, THE ELIZABETH HOTEL 75 256 11,723.2

4 390 Victoria Street, LANDMARK VILLAGE HOTEL 66 393 21,761.0*

5 8 Sinaran Drive, OASIA HOTEL 92 428 22,487.0*

6 1 Tanglin Road, ORCHARD PARADE HOTEL 50 388 34,072.0

7 22 Mount Elizabeth, THE QUINCY HOTEL 75 108 4,810.3

8 20 Havelock Road, CENTRAL SQUARE VILLAGE RESIDENCES 80 128 17,857.5

9 1 Hougang Street 91 HOUGANG VILLAGE RESIDENCES 81 78 14,635.0*

10 121 Penang Road, REGENCY HOUSE 81 90 10,722.7

11 30 Robertson Quay, RIVERSIDE VILLAGE RESIDENCES 78 72 10,592.0*

/Volumes/data folders/~ DTP Job In Progress/R/RR Donnelley/Project Goldstar Prelims_Case ID_5435/final PDF/Appendix C_EDIT_R3.pdf, Page Count: 2 of 50, July 31, 2012, 19:43:30

C-2

3

We have been advised that the subject hotels and serviced residences will be leased under master lease arrangements. The master lease will have an initial term of 20 years with an option exercisable by the master lessee to obtain a further term of 20 years. The annual gross rents will comprise a Fixed Rent component plus a Variable Rent component. The Variable Rent refers to an amount computed based on a fixed percentage of Gross Operating Revenue and a fixed percentage of Gross Operating Profit less the Fixed Rent. We are of the opinion that based on the proposed lease structure, the resultant rental amounts are at market levels and the terms of the lease agreement made known to us are typical of market norms. Valuation Rationale In determining the market value of the properties, we have considered relevant general and economic factors and examined available market evidence. We have used the Income Capitalisation Method and the Discounted Cash Flow Analysis as the primary methods. These approaches have in turn been checked by the Sales Comparison Method. In the Income Capitalisation Method, the estimated annual net income of the property after deducting all necessary outgoings is capitalized at an appropriate rate of return for the balance term of the lease tenure to arrive at the market value. The adopted rate reflects the nature, location, tenure, tenancy profile of the property together with the prevailing property market condition. We have also carried out a 10-year Discounted Cash Flow (DCF) Analysis with respect to Net Present Value Method on the properties. Briefly, this method entails comparison of all future receipts from an investment with all future outgoings and the application of an appropriate discounted rate to this flow of net income to determine the net present value (NPV) of this income stream. The property is hypothetically assumed to be sold after the end of the tenth year. In undertaking this method, a wide range of assumptions are made including rental growth and outgoings escalation throughout the cash flow period as well as sale price (or terminal value) of the property at the end of the investment horizon. The future estimates adopted for rents and costs are projections only formed on the basis of information currently available to us and are not representations of what the value of the property will be as at a future date. These assumptions have been based on the current market conditions and current expectations as to property values, income and yield. Summary of Values Summarised below are our opinion of values:

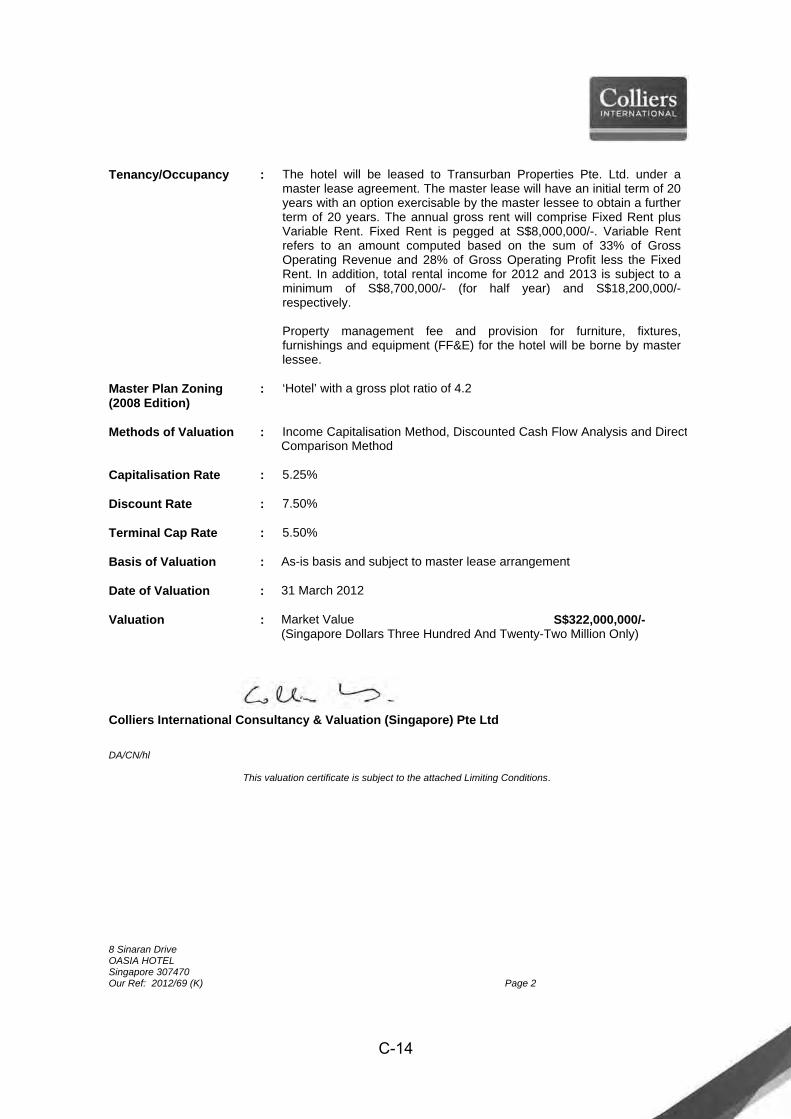

No. Property Market Value (S$) as at 31 March 12

1 180 Albert Street, ALBERT COURT VILLAGE HOTEL 126,000,000/-

2 1 Netheravon Road, CHANGI VILLAGE HOTEL 257,000,000/-

3 24 Mount Elizabeth, THE ELIZABETH HOTEL 193,000,000/-

4 390 Victoria Street, LANDMARK VILLAGE HOTEL 227,000,000/-

5 8 Sinaran Drive, OASIA HOTEL 322,000,000/-

6 1 Tanglin Road, ORCHARD PARADE HOTEL 419,000,000/-

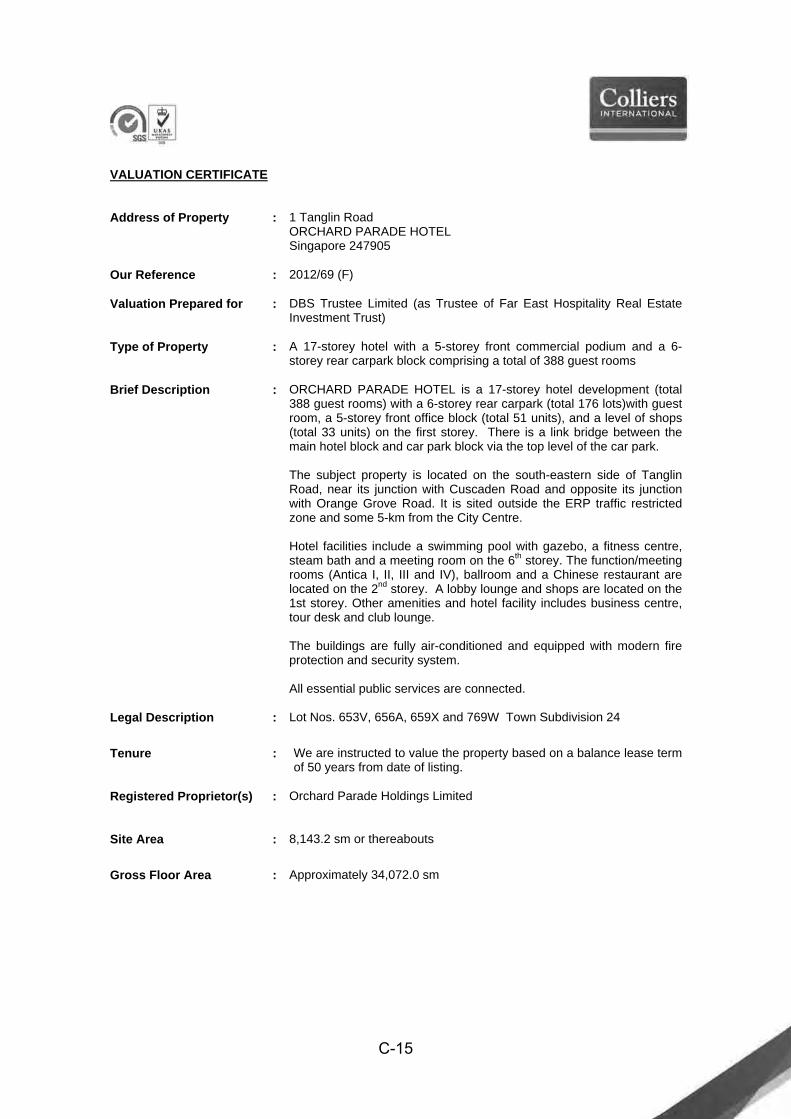

7 22 Mount Elizabeth, THE QUINCY HOTEL 84,000,000/-

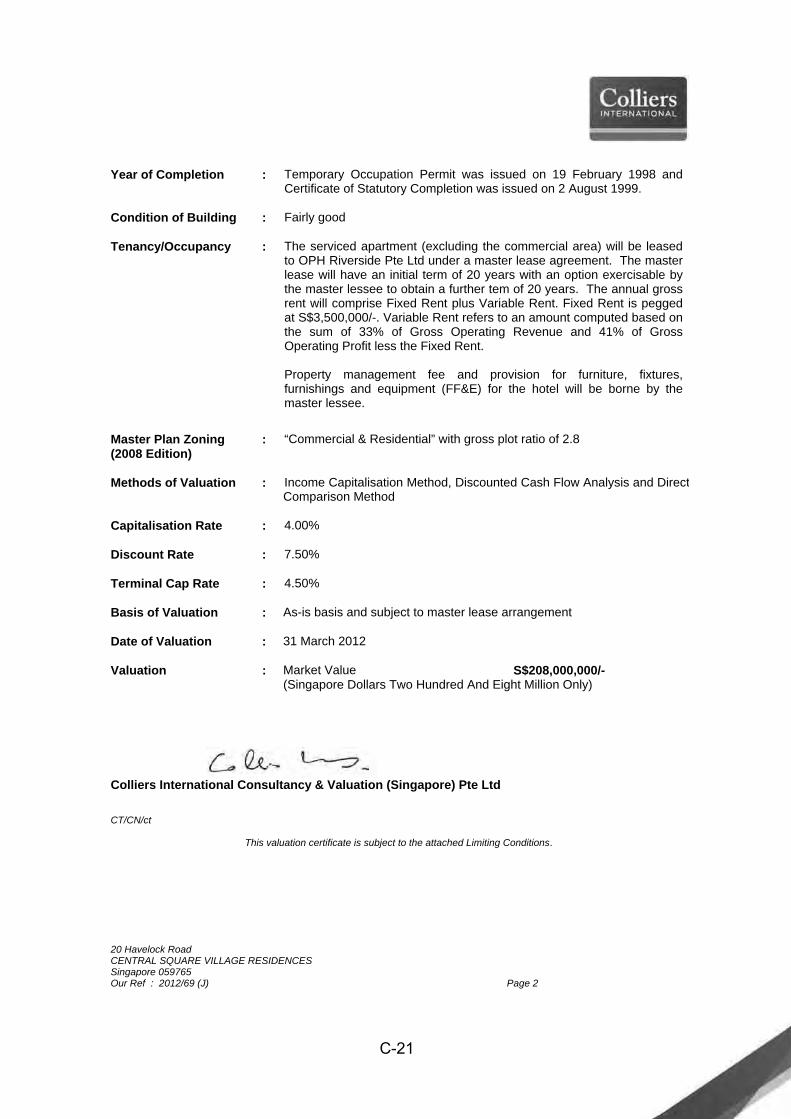

8 20 Havelock Road, CENTRAL SQUARE VILLAGE RESIDENCES 208,000,000/-

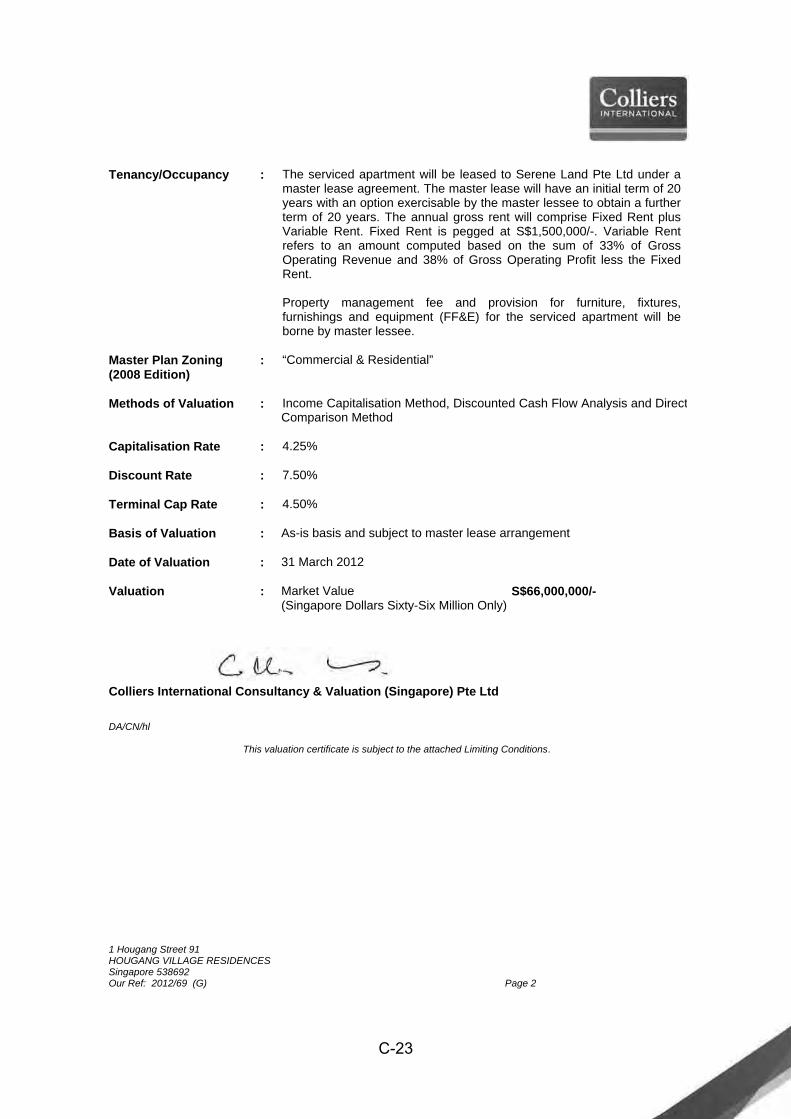

9 1 Hougang Street 91 HOUGANG VILLAGE RESIDENCES 66,000,000/-

/Volumes/data folders/~ DTP Job In Progress/R/RR Donnelley/Project Goldstar Prelims_Case ID_5435/final PDF/Appendix C_EDIT_R3.pdf, Page Count: 3 of 50, July 31, 2012, 19:43:30

C-3

4

Disclaimer We have prepared this Valuation Summary Letter and the enclosed Valuation Certificates for inclusion in the prospectus and specifically disclaim liability to any person in the event of any omission from or false or misleading statement included in the prospectus, other than in respect of the information provided within the Reports and this Valuation Summary Letter.

The reported analysis, opinion and conclusion are limited only by the reported assumptions and limiting conditions and is our personal, unbiased professional analyses, opinions and conclusions. The valuers’ compensation is not contingent upon the reporting of a predetermined value or direction in value that favours the cause of the client, the amount of the value estimate, the attainment of a stipulated result, or the occurrence of a subsequent event. Colliers International Consultancy and Valuation (Singapore) Pte Ltd has relied upon the property data supplied by the owner/manager which we assume to be true and accurate. Colliers International Consultancy and Valuation (Singapore) Pte Ltd takes no responsibility for inaccurate data supplied by the owner/manager and subsequent conclusions related to such data.

We also confirm that we do not have a pecuniary interest that would conflict with a proper valuation of the property and the valuers undertaking the valuation are authorised to practise as valuers and have at least 15 years continuous experience in valuation.

Our Valuation Certificates are appended. Yours faithfully Colliers International Consultancy & Valuation (Singapore) Pte Ltd Cynthia Ng Goh Seow LengB Sc (Est Mgt), FSISV B Sc (Est Mgt), MSISV Appraiser’s Licence No. AD041-2003388A Appraiser’s Licence No. AD041-2003809B Deputy Managing Director Executive Director

Valuation

Encl

No. Property Market Value (S$) as at 31 March 12

10 121 Penang Road, REGENCY HOUSE 170,000,000/-

11 30 Robertson Quay, RIVERSIDE VILLAGE RESIDENCES 117,000,000/-

TOTAL 2,189,000,000/-

/Volumes/data folders/~ DTP Job In Progress/R/RR Donnelley/Project Goldstar Prelims_Case ID_5435/final PDF/Appendix C_EDIT_R3.pdf, Page Count: 4 of 50, July 31, 2012, 19:43:30

C-4