“from the bottom-up” economic outlook – 2018• household spending accounts for 57.6% of...

TRANSCRIPT

MONTREAL | TORONTO | CALGARY | VANCOUVER | NEW YORK

“From the Bottom-Up”Economic Outlook – 2018

FEBRUARY 2018

Mark Fattedad, CFAPortfolio Manager, Institutional and Private Clients

1

FRAMING RISK• There are three types of equity bear markets:

• Event-driven = mildest • Cyclical (recessions) = average drawdown -30%.• Structural (macro imbalances + asset bubbles) = average drawdown -50%

• Our focus is on the cyclical and structural

2

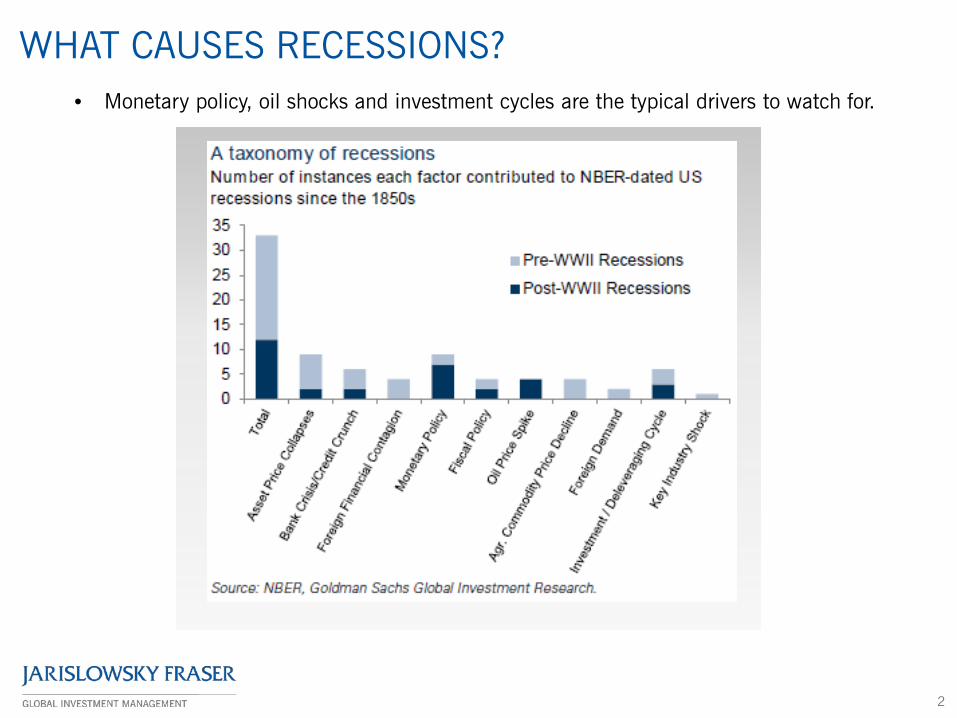

WHAT CAUSES RECESSIONS?• Monetary policy, oil shocks and investment cycles are the typical drivers to watch for.

YIELD CURVE – NOT INVERTED

Source: Bloomberg3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1 5 10 15 20 30

U.S. Yield Curve (Feb 14/ 18 vs Feb 14/ 17)

US Feb 14/17

US Feb 14/18

• Normally would see a period of three months where short-term interest rates are above long-term rates (i.e. an inverted yield curve), prior to a recession.

4

MANUFACTURING IS STRONG Global PMI's

With Developed (DM) and Emerging (EM) Market Subindices

M740 JAN 2018

57 57

56 56

55 55

54 54

53 53

52 52

51 51

50 50

49 49

48 482012 2013 2014 2015 2016 2017 2018

GlobalDMEM

54.4

56.6

52.0

Source: TD Bank

5

UNEMPLOYMENT REMAINS VERY LOW

Source: Bloomberg, Econoday

3

4

5

6

7

8

9

10

11

12Recession US Unemployment Rate US Unemployment Rate 12m MA

• A rise in the unemployment rate by a third of one percent has always preceded U.S. recessions.

6

POTENTIAL RISKS - CONSUMER SPENDING • Household spending accounts for 57.6% of Canadian GDP

• Rising rates and stricter rules for low-ratio mortgages is expected to reduce consumer spending.

• Anti-globalization sentiment on the rise.• Regionally, Ontario looks most at risk from a disruption to NAFTA, with the bulk of the

exports (80%) being in industries that are vulnerable to trade negotiations.

7

POTENTIAL RISKS – TRADE

Source: BMO

8

WHAT ABOUT ESG FACTORS?

• “Scrapping Carbon Taxes Leaves a Gaping Hole in the Ontario PC Platform”– Maclean’s, Feb. 14, 2018

• “Blame Ontario Minimum Wage Hike for Canada Job Plunge. Or Not.” - Bloomberg, February 9, 2018

• “Kinder Pipeline Battle Spirals as Alberta Halts Power-Deal Talks” – Bloomberg, Feb. 2, 2018

No shortage of news headlines………

Funded by the JF Partners Foundation

10 KEY TRENDS FOR THE NEXT DECADE

Funded by the JF Partners Foundation

10 KEY TRENDS FOR THE NEXT DECADE

Investment Outlook

SUMMARY

11

• Near-term, the risk of recession is quite low. A more significant market downturn does not look to be imminent.

• We continue to recommend an overweight position in equities, underweight position in bonds, and overweight position in cash.

• ESG trends unlikely to change the business cycle, but have material implications for long-term business value.

DISCLAIMER

12

This document is prepared by Jarislowsky, Fraser Limited (JFL) and is provided for informationpurposes only, it is not intended to convey investment, legal, tax or individually tailored investmentadvice. All opinions and estimates contained in this report constitute JFL's judgment as of the timeof writing and are provided in good faith. All data, facts and opinions presented in this documentmay change without notification. No use of the Jarislowsky, Fraser Limited name or anyinformation contained in this report may be copied or redistributed without the prior writtenapproval of JFL.