“crossroads” · 2018-05-11 · dec-13 y-14 sep-14 jan-15 y-15 sep-15 jan-16 y-16 sep-16 jan-17...

TRANSCRIPT

“Crossroads”

MAY 2018 | ISSUE 65

This document is not valid without disclosure; refer the last page for the disclosure

Alpha Strategist | “Crossroads”

Contents

MAY 2018 | ISSUE 65 2

Executive Summary

Section I………………………………………………………………......................................................………...04-21

ection II…………………………………………………….......................................................………………....22-37

Section III…………………………………………………….........................................................……………….39-67

………………………………………………………………........................................…….......03

(Market through Graphs, Our advisory calls, Model Portfolio & performance, Outlook, Investment

Opportunities & Investment articles)

S

(Detailed views on Equities, Fixed Income, Alternative)

(Advisory approach, 4C Framework, Update on our recommended products)

MAY 2018 | ISSUE 65 3

From a market stand point we are at ”. Markets are witnessing headwinds arising from

concerns over the upcoming state elections, trade spats between major global economies and

spike in global yields. On the other hand, we are witnessing tail winds in the form of increasing

economic traction in the domestic economy resulting in expectation of strong earnings and this

has been complimented by robust domestic flows. Clearly the confluence of the above has

resulted in resurgence of volatility which has been absent for a while now. We see the overall

environment as positive for risky assets, but expect muted returns and higher volatility going

forward.

From a global stand point, optimism appears to be on the rise. A fiscal stimulus for the US economy via tax reform, a

tightening job market combined with substantial increase in Federal borrowing has resulted in a sharp up tick in US

treasury yields. With this development we believe that the tailwind from an accommodative global liquidity condition is

increasingly being challenged, as key central banks tighten monetary policy. This is likely to have a bearing on flows

towards emerging markets.

Growth prospects for the Indian economy continue to look bright. This is evident from various high frequency data

points. Increased economic activity will eventually get reflected in corporate profitability. The building blocks of a

domestic economic recovery seem to be falling in place. This appears to be led by both structural and cyclical factors.

Clearly the visibility of earnings recovery which had been elusive for a while now appears to be turning into reality.

There are early signs of normalization after earnings experienced a subdued trend over the past couple of years. Our

newly launched strategy “Renaissance India Next PMS” aims to capture growth through companies and sectors which

have been head winded in the past but will see good up tick in the coming years. We continue to advise a staggered

approach to investing in equities with a view to commit more during any sharp corrections. In order to capitalize on the

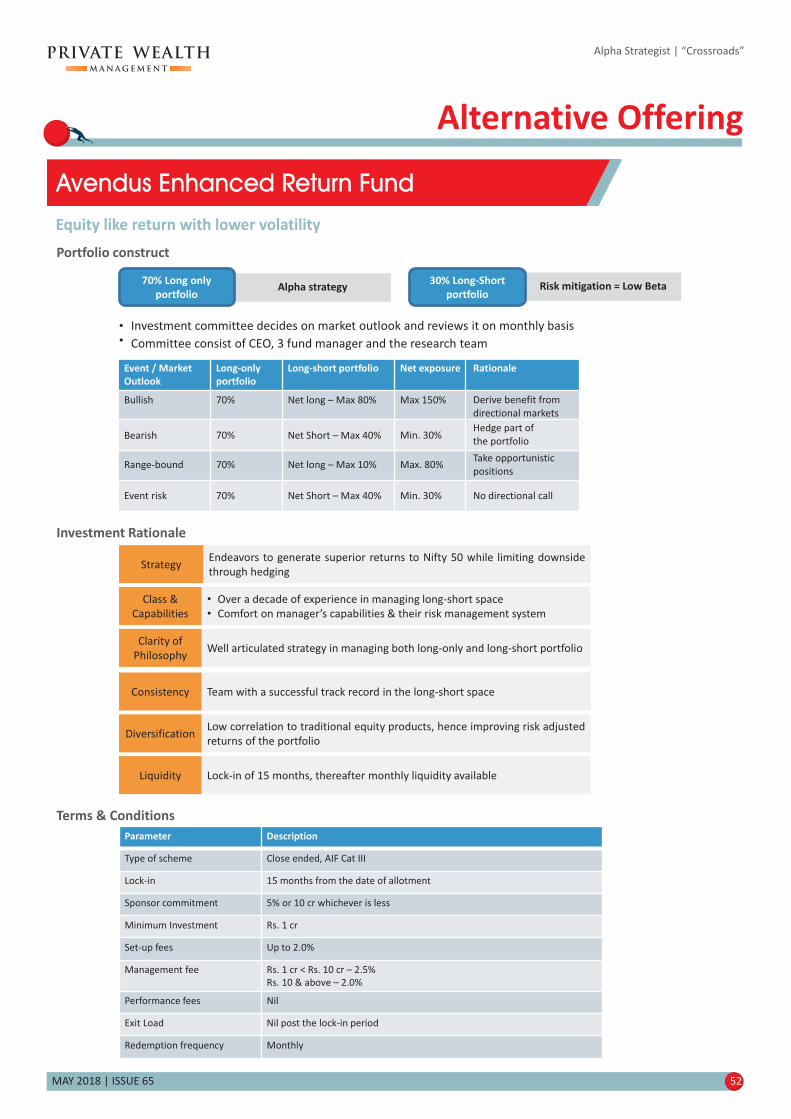

upcoming volatility we are happy to introduce you to “Avendus Enhanced Return Fund” which endeavors to generate

equity like returns while keeping volatility lower than traditional equity strategies. We believe that this proposition

would certainly add value to your portfolio.

Fixed income markets have been quite volatile in the last couple of months with ten year government bond yields

moving between 7.1-7.8%. The government and the RBI have announced a slew of measures to calm the bond markets.

We believe that the RBI will be in an extended state of pause on interest rates. Hence we recommend investors to look at

low maturity high accrual portfolios like short term funds, selected credit portfolios and ultra-short term funds.

At such “ ” it is important to revisit your stated goals as well as asset allocation and stick to it in a disciplined

manner. As usual this edition is rich with several articles to make your investment journey simpler.

Crossroads

Crossroads

“

Happy Investing!

Ashish Shanker

(Head, Investment Advisory – Private Wealth Management)

Executive Summary

Alpha Strategist | “Crossroads”

This document is not valid without disclosure; refer the last page for the disclosure

MAY 2018 | ISSUE 65 4

Section I

Market through Graphs........................................................................................05

Portfolios Commentary........................................................................................08

Model Portfolios .................................................................................................09

.......................................................10

Succession of a Female - Hindu.............................................................................12

Power of Asset Allocation....................................................................................13

Hind-sight investing ............................................................................................15

Decoding Investment Style..................................................................................16

Temperature Gauge.............................................................................................17

Fixed Income Manager Selection Framework

Investment Grid ..................................................................................................19

Our Recommendations .......................................................................................20

Alpha Strategist | “Crossroads”

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2 10-year US Treasury Yield (%)

De

c-1

3

Ma

y-1

4

Se

p-1

4

Jan

-15

Ma

y-1

5

Se

p-1

5

Jan

-16

Ma

y-1

6

Se

p-1

6

Jan

-17

Ma

y-1

7

Se

p-1

7

Jan

-18

Ap

r-1

8

Macro Economy

• The yield on the 10-year Treasury note ended higher in

April, crossing the psychological mark of 3% during the

month

Some encouraging US economic data along with

expectation of more aggressive interest rate hikes

from the US Fed dented sentiment for treasuries

The rise in US treasury yields comes at a time when

there are concerns of widening trade deficit, fiscal

slippage, rising crude prices and the rupee

depreciation in India. This in turn could impact the

foreign flows into India

•

•

• The Indian Meteorological Department (IMD) released

its first forecast for the 2018 southwest monsoon

(June-September) rainfall with expectations of normal

monsoon

It expects monsoon rainfall at 97% of the long period

average (LPA) with very less probability of

experiencing a deficit monsoon

With rising tensions about farmers' distress, general

elections in 2019 and the fact that winter monsoon

(January-February) rainfall in 2018 was the worst in at

least 26 years, 2018 southwest monsoon holds special

significance

•

•

IMD expects normal monsoon in 2018

Source: Indian Meteorological Department (IMD)

MAY 2018 | ISSUE 65 5

Markets through Graphs

Alpha Strategist | “Crossroads”

Source: Bloomberg

US Treasury yield hits its highest level since 2014

• Oil prices rose over 5.2% in April to close at $74/bbl as

compared to $70.3/bbl at the end of the previous

month

Oil prices were hit by a stronger US dollar and a sharp

increase in US crude inventories. However, support

came from lingering uncertainty over the Iranian

nuclear deal

Rising oil prices could have an adverse impact on

India's current account deficit. However, there would

be limited impact on inflation, given its low weightage

in the inflation measure

•

•

Oil prices continue to surge

Source: Bloomberg

9899

98

9593

106

9697

102

92

106

8785

98

95

2011 2012 2013 2014 2015 2016 2017 2018

(% of LPA)IMD's April forecast Actual rainfall

??

20

35

50

65

80Oil (Brent) $/bbl

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

• Equity markets witnessed a stellar month with Nifty 50

gaining 6.2% in April as compared to decline of 4.9%

and 3.6% in the month of and March,

respectively

Robust domestic flows and healthy start to Q4FY18

earnings season supported market rally amidst FII

selling, currency depreciation and rising crude prices

The current valuation levels are on the back of

depressed earnings growth over the last few years. We

expect earnings to recover supported by demand

recovery in consumption sectors, low base of

demonetization and commodity price inflation

February

•

•

Equities

MAY 2018 | ISSUE 65 6

Source: Bloomberg

Sensex PE (TTM) trades 31% above average

Alpha Strategist | “Crossroads”

• Both earnings yield to bond yield (EY-BY) and MOVI

which we use to gauge market attractiveness, trades in

the fair value zone

Both indicators suffered on the back of recent market

rally and rise in bond yields. However, even at these

levels investors have made positive returns at least

70% of times for 3-year holding period

Given the current valuations, we suggest investors to

stagger their investments over the next few months

and capitalize on any sharp decline by incremental

deployment

•

•

Valuation indicators trade in fair value zone

Source: MOWM

• The Q4FY18 earnings season has so far been broadly in

line with expectations in terms of revenue. However,

profits have missed estimates, largely dragged by

corporate-focused private banks

Sales, EBITDA and PAT for the 20 Nifty companies have

grown at 19.1%, 14.1% and 2.2%, as against

expectations of 16.0%, 13.6% and 11.9%, respectively

We expect the performance of corporate-focused

private banks and PSU Banks to drag the aggregates in

Q4FY18. However, consumer, cement, autos, private

banks, NBFCs and IT shall provide the necessary

cushion which reinstates our FY19 earnings recovery

story

•

•

Nifty (20 companies) sales growth of 19%

(estimate 16% YoY)

Source: MOSL

Ap

r-0

8

24.1

18.8

5.0

10.0

15.0

20.0

25.0

30.0 Sensex TTM PE 10-year average PE

Ap

r-0

9

Ap

r-1

0

Ap

r-1

1

Ap

r-1

2

Ap

r-1

3

Ap

r-1

4

Ap

r-1

5

Ap

r-1

6

Ap

r-1

7

Ap

r-1

8

10

1

9

12

17

12 12

14

19

Ma

r-1

6

Jun

-16

Se

p-1

6

De

c-1

6

Ma

r-1

7

Jun

-17

Se

p-1

7

De

c-1

7

Ma

r-1

8

Sales growth (%YoY)

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

80.0

90.0

100.0

110.0

120.0

130.0 MOVI (LHS) EY-BY (RHS)

Ap

r-1

5

Oct

-15

Ap

r-1

6

Oct

-16

Ap

r-1

7

Oct

-17

Ap

r-1

8

MAY 2018 | ISSUE 65 7

Summary

Fixed Income

Consumption, Domestic Cyclicals, Rural

High quality Corporate Bond funds,

Credit Opportunities funds, FMPBullish on accrual strategies

& tactical on dynamic bond funds

Sovereign Gold Bonds, Gold ETFsNeutral Neutral

AlternativesGold prices inches up

• Gold prices (-1.8%) saw a slight fall in April to close the

month at $1,315 per ounce as compared with $1,339

per ounce in the previous month

Gold prices started on a high note due to weakness in

the US dollar and fears of a global trade war, however,

gains were offset after the US Fed raised expectations

of a faster pace of rate hikes and as dollar strengthened

We continue to hold our neutral stance on gold, as we

believe there is merit in having allocation to this asset

class as it acts as a hedge against any major geopolitical

risk

•

•

Alpha Strategist | “Crossroads”

Source: Bloomberg

6.06.46.87.27.68.08.48.89.29.6

10.010.4

1 Yr 3 Yr 5 Yr

Yie

ld (

%)

Maturity

Gsec AAA AA AGsec (1 year bck) AAA (1 year bck) AA (1 year bck) A (1 year bck)

Source: Bloomberg

Increase in yields across credit curve

• In lieu of the ongoing concerns, yields across the credit

curve at the shorter end have shifted upwards hence

resulting in spreads of 40–170 bps w.r.t different credit

assets

Quantum of rise in yields of AAA segment has not been

accompanied with a similar rise in yield of lower rated

assets owing to spread compression

From a prudent risk reward perspective, short term

AAA assets offers a value proposition to lock in

investments at higher yields which were prevalent in

lower rated assets

•

•

6.2 6.2

6.7

7.3

7.67.8 7.8 7.9 7.8

8.07.9

7.8 7.88.0 8.0 8.0

5.8

6.0

6.26.4

6.6

6.8

7.07.2

7.4

7.67.8

8.0

8.2

3M 6M 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 11Y 12Y 13Y 17Y

Years

Current 1 mnth back 6 mnths back 1 yr back

Yields remain volatile on confluence of domestic &

global factors

• Indian bond market has kept the stakeholders on toes

due to wide swings in the yields.

While RBI’s dovish stance on inflation, reduced

government borrowing, OMO purchases and easing of

FPI norms supported bond market, hawkish stance

revealed in MPC minutes, rising crude oil prices and

global yields dented market sentiment

In such volatile times, it is prudent to stick to high

quality/credit oriented accrual strategies so as to get a

visibility of risk adjusted returns

•

•

Source: Bloomberg

1000

1050

1100

1150

1200

1250

1300

1350

1400

Ap

r-1

4

Au

g-1

4

De

c-1

4

Ap

r-1

5

Au

g-1

5

De

c-1

5

Ap

r-1

6

Au

g-1

6

De

c-1

6

Ap

r-1

7

Au

g-1

7

De

c-1

7

Ap

r-1

8

GOLD Spot ($/Oz)

MAY 2018 | ISSUE 65 8

Investment Committee

Alpha Strategist | “Crossroads”

Portfolios CommentaryTactical changes and strategies

� – Replaced Income Funds with Dynamic Bond Funds based on the note released -

– Reduced allocation to Gold by 25% and increased to Dynamic Bond Funds based on discussionin the Investment Committee meeting

– Reduced further allocation to Gold by 25% and increased to Dynamic Bond Funds based on discussionin the Investment Committee meeting

– Exited Gilt Fund’s and moved to Short-term Funds (40%), Income Funds (40%) and Dynamic BondFunds (20%) based on the note released -

– Exited Income Funds and other long duration investments and invested the redemption proceeds inUltra Short-term Funds based on the note released –

– Cash allocation brought back to its strategic weight and invested the balance allocation into giltfunds based on the note released –

– Switched 15% of equity allocation to Information Technology (IT) sector funds from large cap andmulti cap funds, based on the note released –

– Reduced 10% of equity allocation and switched to ultra short term funds based on the notereleased –

– Switched 50% of Short-term Funds allocation to Gilt Funds, to increase duration of theportfolio, based on the note released –

– Deployed Cash in Nifty ETFs, based on the note released –

– Switched all cash positions to gilt funds, to further increase duration of the portfolio

– Reduced allocation to Gilts and moved to Ultra Short term Funds to create liquidity in the portfolio

May 23, 2014 – Switched allocation from IT Sector Funds and Nifty ETFs to Infrastructure Funds and Small cap Fundsrespectively, based on the note released –

– Switched allocation from Cash to Gilt funds, to increase the duration of the portfolio based on thenote

– Switched allocation from Small & Midcap funds to Large Cap funds, on the back of relativelyhigher valuations of midcaps as compared to large cap.

– On the fundamental front, demand side continues to be supportive for gold. We have therebyrevised out short term outlook on gold from underweight to neutral stance.

– Reduced Gilt exposure and allocated the proceeds towards Gold, on the back of better risk rewardscenario for gold & bond yields coming below it long term average

December 15, 2012

February 14, 2013

April 1, 2013

May 17, 2013

July 29, 2013

September 20, 2013

September 27, 2013

September 30, 2013

November 20, 2013

November 25, 2013

December 3, 2013

May 5, 2014

September 6, 2014

September 28, 2015

September 24, 2015

February 29 , 2016

“Interest”ing TimesAhead”

“Yields came tumbling after…to plummet further”

“Ride the Tide”

“The Gilt Edge”

“Information Technology – In a position on strength”

“The Bear-nanke Hug – Underweight Equities”

“Time to Rebuild Duration – A Déjà vu”

“Equity Markets – An Update”

“Good Times Ahead!”

“Way Ahead for Duration”.

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

April 22, 2016 – Switched allocation from Duration strategies to Accrual strategies, based on the note released –

March 31, 2018 – In Fixed Income, we reiterate our stance on accrual strategy, however, given the current valuations,tactical allocation to dynamic bond funds can be considered by investors who can withstand interest rate volatility

March 31, 2018 – Increase allocation towards value oriented multi-cap strategies

“Time toShift Gears”

As on April 30, 2018

Committee Members

Mr.

Mr. Vijay Goel – Private Wealth Management

Mr. Ashish Shanker – Head, Investment Advisory

Mr. Kishore Narne – Head, Commodities & Currency

Mr. Nikhil Gupta, Economist, MOSL

Mr. Pradeep Ashok Kumar – Vice President,

Gautam Duggad – Head of Research, Institutional Equities, MOSL

Managing Director & CEO,

Investment Advisory

Products & Advisory Team, Private Wealth Management

Mr. A Balasubramanian, CEO, Aditya Birla Sun Life AMC Ltd.

External Invitee

MAY 2018 | ISSUE 65 9

Alpha Strategist | “Crossroads”

Model Portfolios

Note:

Portfolio inception date: October 01, 2012

All ratios calculated for 3 years period. Risk free rate at 6.0%

Performance as on: April 30, 2018

Key Ratios1-year rolling return Max

Drawdown

Draw Down

Period

Jensen's

AlphaInformation

Ratio

Aggressive+

Balanced

Conservative

21.5%

13.3%

9.0%

-12.2%

-4.7%

2.8%

63.2%

34.5%

17.6%

-17.5%

-8.3%

-4.0%

Aug-15 - Feb-16

Aug-15 - Feb-16

Jun-13 - Aug-13

4.1%

1.1%

-0.8%

0.8

1.0

1.4

0.6

0.5

0.4

0.5

0.3

-0.1

Min MaxBeta Sharpe

Average

Client Profile Performance Snapshot

Conservative

55.2%

5.0%

39.8%

Accrual

Gold Fund

Corporate Bond

Balanced

9.0%

12.0%

12.0%

7.0%

26.0%

10.0%

24.0%

Large Cap Funds

Mid Cap Funds

Multi Cap Funds

Balanced Funds

Accrual

Gold Fund

Corporate Bond

Aggressive+

30.0%

22.5%20.0%

27.5%

Equity PMS

Large Cap Funds

Mid Cap Funds

Multi Cap Funds

-0.40.0

0.91.4

5.7

7.3

8.2 8.5

1.4

2.1

5.9

7.58.1 8.0

1 Month 3 Months 6 Months 1 Year 3 Year 5 year Since

Inception

% R

etu

rn

Conservative Portfolio Conservative Index

2.5

-0.3

2.5

9.2 9.3

12.511.6

2.6

-0.2

3.2

10.0

8.3

9.79.2

1 Month 3 Months 6 Months 1 Year 3 Year 5 year Since

Inception

% R

etu

rn

Balanced Portfolio Balanced Index

1 Month 3 Months 6 Months 1 Year 3 Year 5 year Since

Inception

6.0

-0.1

4.2

14.1 13.5

19.717.8

6.2

-2.6

3.9

15.4

9.5

12.6 12.0

% R

etu

rn

Aggressive+ Portfolio Aggressive+ Index

MAY 2018 | ISSUE 65 10

Adding objectivity to fixed income investing

Fixed Income Manager Selection Framework

Alpha Strategist | “Crossroads”

In the above graph, we have taken the Average 1 yr rolling return for 5 years for various funds across categories. The result

was that there was a significant difference between the top performer and bottom performer in almost every category,

making a case for choosing fund managers over the funds. The ability to generate enhanced returns varies from manager

to manager within the same category, thus laying emphasis on the skills of a fund manager. But one must also realize that

past performance cannot be the only criteria to judge a fund. It is almost hazardous to do so. Different market cycles

present different opportunities.

So what strategy will help investors so that their investments are relevant for the ongoing market cycle? Even in fixed

income, there are risks associated with interest rates, credit and liquidity. With the numerous funds at one's disposal,

choosing the correct one can be quite a challenge. Before we venture into the framework of choosing a manager let us

take a sneak-peak into the two kinds of strategies adopted for “enhancing” returns – Credit and Duration.

The credit opportunities style looks for companies that have the ability to repay and mitigates risks such as default and

liquidity. This benefits investors via higher coupons, thus enhancing their overall return. However, the duration style

plays on interest rate cycles and requires an intricate macroeconomic understanding as the manager must get the

interest rate cycles right. Both these strategies play out at various points of time. At a time one anticipates interest rates

to peak, duration strategies would be a preferred option as any subsequent decline in interest rates would enhance the

portfolio returns. Likewise, in a rising interest rate scenario, duration strategies would not augur well, calling for

investment in credit strategies.

The battle of objective vs. subjective decision making often makes appearance in investing. To our mind, having an

objective oriented approach gives purpose to investment which helps in avoiding any impulsive calls. Traditionally, equity

has always been viewed as an asset class for capital appreciation while fixed income is seen as an avenue for capital

preservation. Amongst the fixed income instruments, the most commonly accepted investment avenue is fixed deposits.

There is a psychological comfort that investors draw on account of the fixed return provided by such instruments.

However investors must realize that an instrument like a fixed deposit is tax inefficient. As a result, it does not even meet

the core objective preserving the purchasing power. That raises the obvious question – what kind of fixed income options

should investors seek?

If the veil of ignorance is done away with and the fixed income market is probed into, one will realize that there are

various market linked investment avenues that investors can invest in. To our mind, fixed income mutual funds are one

example of an efficient investment option that investors can avail of as they have various benefits like diversification,

professional management and tax efficiency. However, the question of prudent selection still remains unanswered.

Liq

uid

UST

Sho

rt T

erm

Cre

dit

Op

ps.

Lon

g I

nco

me

Dyn

am

ic

Bo

nd Gilt

6.6 6.77.4

9.2

7.7

6.7 6.9

8.3 8.6 9.0

9.9

8.9 9.29.88.9

9.3

10.310.8 10.8

11.912.6

Avg. 1 Yr RR of worst performing fund Category Average Avg. 1 Yr RR of best performing fund

MAY 2018 | ISSUE 65 11

Alpha Strategist | “Crossroads”

Just like a fast bowler cannot bowl spin and vice versa, a manager cannot mimic both approaches simultaneously. A

manager must be clear on his stance and having experienced two to three market cycles will be of huge significance.

To our mind, good performance is an outcome of a robust process. Hence, one needs to be cognizant of the latter at the

time of evaluation. This thought process has given birth to our . By evaluating the

pilot rather than just the plane, each would enable us to unmask the different hues of investment process from the

performance which is the ultimate outcome.

This framework implies a paradigm shift from the industry norm of ranking funds only on the basis of past performance.

This qualitative and quantitative process would enable us to construct for our clients. In line with

our philosophy of providing better insights to you, we hope you find the same informative.

“4C framework of manager selection”

“C”

“winning portfolios”

MAY 2018 | ISSUE 65 12

Alpha Strategist | “Crossroads”

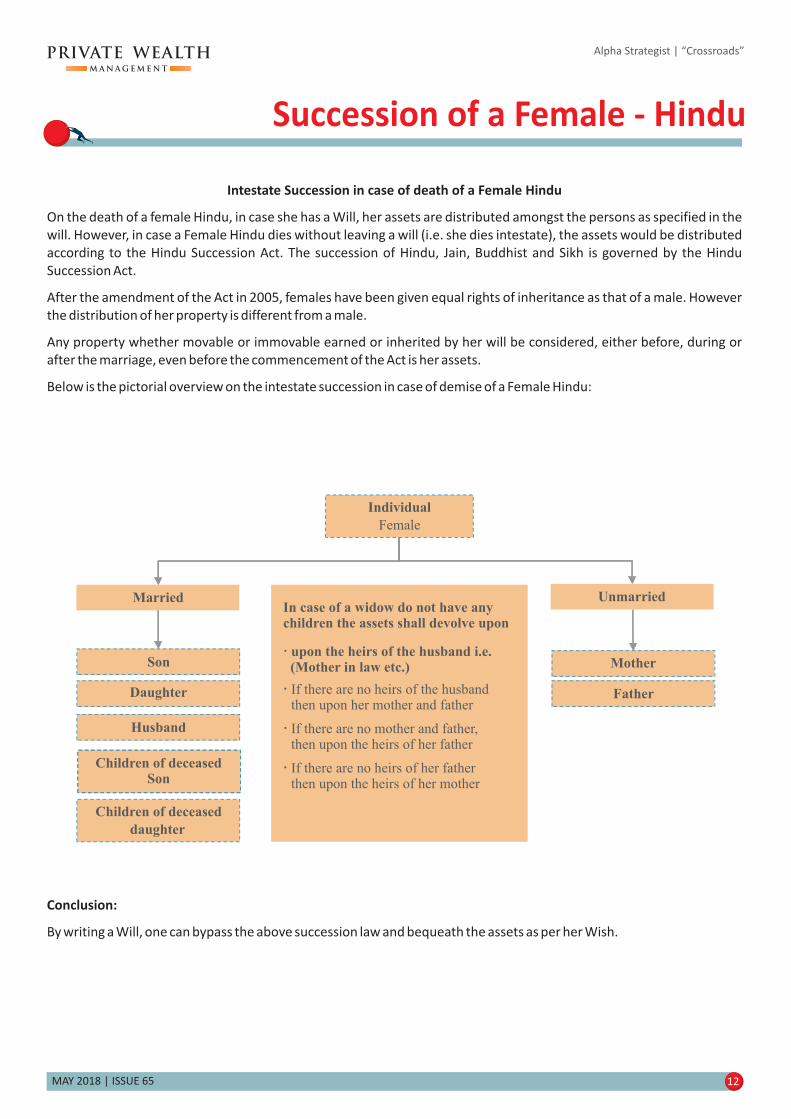

Succession of a Female - Hindu

Son

Married

Individual

Female

Daughter

Husband

Children of deceasedSon

Children of deceased

daughter

Intestate Succession in case of death of a Female Hindu

On the death of a female Hindu, in case she has a Will, her assets are distributed amongst the persons as specified in the

will. However, in case a Female Hindu dies without leaving a will (i.e. she dies intestate), the assets would be distributed

according to the Hindu Succession Act. The succession of Hindu, Jain, Buddhist and Sikh is governed by the Hindu

Succession Act.

After the amendment of the Act in 2005, females have been given equal rights of inheritance as that of a male. However

the distribution of her property is different from a male.

Any property whether movable or immovable earned or inherited by her will be considered, either before, during or

after the marriage, even before the commencement of the Act is her assets.

Below is the pictorial overview on the intestate succession in case of demise of a Female Hindu:

Conclusion:

By writing a Will, one can bypass the above succession law and bequeath the assets as per her Wish.

Mother

Unmarried

Father

In case of a widow do not have anychildren the assets shall devolve upon

upon the heirs of the husband i.e.(Mother in law etc.)�

�

�

�

If there are no heirs of the husbandthen upon her mother and father

If there are no mother and father,then upon the heirs of her father

If there are no heirs of her fatherthen upon the heirs of her mother

MAY 2018 | ISSUE 65 13

Alpha Strategist | “Crossroads”

Power of Asset Allocation

Historically equity has been viewed as a wealth creating asset class and debt and gold being inflation beating asset class.

That said, little do people know that both debt and gold have rarely beaten inflation. At the same time while equity offers

superior returns in the long run, it also exposes one to certain volatility inherent to the nature of the asset class. Asset

allocation enables you to maximize your return potential while reduce your risk. Industry research has shown that 92% of

the returns are attributable to the correct asset allocation.

We thought it to be prudent to substantiate it with some data. The table below highlights calendar year performance of

different asset classes such as equity, debt, gold and cash. As you would observe no asset class has been a consistent

winner.

Having said that, it is very clear that if one were to do a very simple asset allocation of equal investing in different asset

classes, there would have been only 1 instance in last 15 years where the strategy would have given negative returns. This

includes period of global financial crisis where most of the markets were battered. Thus there is a clear merit in

diversifying assets across different asset classes as it reduces dependency on single asset classes and protect from

market turbulence.

Performance as on: April 30, 2018

Equity is represented by Nifty 50

Debt is represented by CRISIL Short term bond Index,

Cash is represented by CRISIL

Liquid fund Index and Gold – Bloomberg, MOWM

Average: Equal allocation to each asset class in the calendar year

In our mind while return certainly matters, but so does risk. Based on your risk taking appetite, one should decide on how

much money needs to be allocated to different asset classes.There are multiple factors that define your risk tolerance

level such as investment horizon, liquidity needs, investment goals and so on. An investor with high risk tolerance may be

willing to accept greater volatility in pursuit to generate higher potential returns and may allocate higher percentage of

the portfolio towards higher risk assets. On the other hand, an investor with low risk tolerance may have to forego higher

potential returns for a steadier and less volatile portfolio.

11.3%

CAGREquity

16.1%

Gold

11.4%

Debt

6.8%

Cash

6.8%

CAGR of underlying asset classes

Multi-asset approach tends to deliver smoother returns than what is achieved by investing in just a single asset class

2003

Equity

71.9%

2004 2005 2006 2007 2008 2009 2010 2012 2013 20142011 2015 2016 2017

Average

Equity

10.7%

Gold

24.1%

Gold

31.9%

Equity

27.7%

Cash

9.0%

Equity

31.4%

Debt

8.7%

Gold

12.0%

Equity

28.6%

Equity

75.8%

Equity

36.3%

Equity

39.8%

Equity

54.8%

Gold

30.1%

Gold

13.5%

Cash

4.0%

Gold

22.3%

Gold

20.8%

Gold

16.7%

Debt

9.5%

Gold

19.7%

Equity

17.9%

Cash

8.2%

Gold

10.2%

Debt

8.3%

Debt

10.5%

Cash

8.2%

Debt

9.8%

Cash

6.6%

23.8%

Cash

4.6%

Debt

5.4%

Gold

5.9%

Debt

2.7%

Cash

4.6%

Cash

6.0%

Debt

8.0%

Cash

8.4%

Debt

6.6%

Cash

5.1%

Debt

7.9%

Debt

9.1%

Cash

7.5%

Equity

-4.1%

Cash

9.2%

Equity

6.8%

11.6%8.1%1.7%12.9%1.2%13.9%5.8%13.0%26.7%-0.9%21.7%18.0%17.0%4.5%

Debt

%5.4

Gold

0.5%

Debt

4.5%

Debt

5.5%

Cash

7.5%

Equity

-51.8%

Cash

4.9%

Debt

4.7%

Equity

-24.6%

Equity

3.0%

Gold

-6.2%

Gold

0.6%

Gold

-19.2%

Cash

8.5%

2.6%

2018*

Gold

5.4%

Debt

0.7%

Cash

2.4%

Equity

2.0%

MAY 2018 | ISSUE 65 14

Alpha Strategist | “Crossroads”

By selecting a portfolio with equity and fixed income, the potential gains that the equity component can give are much

higher and the associated risk can be well taken care of by the fixed investment portfolio. Thus a portfolio invested across

asset classes has the ability to generate superior risk adjusted return.

To prove our hypothesis, we carried out back-testing with just two asset classes, equity and fixed income. We created

three model portfolios with 75:25, 50:50 and 25:75 exposures to fixed income and equity respectively. Over 5-year

holding period, none of these portfolio generated negative returns. Also, it is worth highlighting that over 3-year holding

period, portfolio which has high exposure to equity (75%) gave positive returns 98.7% of time over the last 12 years.

• Multi-asset class strategies smoothen the ride

• Protects on the downside during extreme falls witnessed from a single asset class

• Makes returns more predictable

The above illustration has been carried out for indices which are passively managed. Our experience has been that

actively managed strategies have been able to generate significant alpha. Thereby, we believe the upside benefit is

higher in case of actively managed strategies. Consequently, the same can be depicted from the below table.

Fixed Income 75%; Equity: 25% Fixed Income 50%; Equity: 50% Fixed Income 25%; Equity: 75%

1 year 3 year 5 year 1 year 3 year 5 year 1 year 3 year 5 year

Period of analysis: March 2002 to April 2018

Equity is represented by Nifty 50 & Debt is represented by CRISIL Short term bond Index

10.4%

28.1%

-8.2%

180

9 (5.%)

41 (22.8%)

10.0%

21.7%

5.2%

158

0.0%

13 (8.2%)

9.8%

20.3%

5.6%

132

0.0%

3 (2.3%)

13.6%

48.9%

-22.7%

180

19 (10.6%)

43 (23.9%)

12.3%

35.2%

2.4%

158

0.0%

27 (17.1%)

11.6%

30.2%

3.6%

132

0.0%

14 (10.6%)

16.7%

70.6%

-37.4%

180

30 (16.7%)

45 (25.0%)

14.3%

46.4%

-0.6%

158

2 (1.3%)

32 (20.3%)

13.2%

37.8%

1.4%

132

0.0%

18 (13.6%)

For indices:

Fixed Income 75%; Equity: 25% Fixed Income 50%; Equity: 50% Fixed Income 25%; Equity: 75%

1 year 3 year 5 year 1 year 3 year 5 year 1 year 3 year 5 year

13.7%

38.3%

-6.2%

179

7 (3.9%)

26 (14.5%)

13.5%

33.9%

6.0%

157

0.0%

0 (0.0%)

13.0%

30.6%

6.9%

131

0.0%

0 (0.0%)

19.8%

70.2%

-21.1%

179

17 (9.5%)

34 (19.%)

18.2%

54.1%

2.7%

157

0.0%

9 (5.7%)

16.8%

44.3%

6.0%

131

0.0%

0 (0.0%)

25.9%

102.2%

-36.2%

179

25 (14.%)

40 (22.3%)

22.3%

70.0%

-1.0%

157

2 (1.3%)

14 (8.9%)

20.0%

54.1%

5.2%

131

0.0%

2 (1.5%)

For actively managed strategies:

For active managers, Franklin India Prima Plus, HDFC Equity Fund and Sundaram Select Midcap have been considered for Equity and Aditya Birla SL Short Term

and SBI Magnum InstaCash Cash has been considered for Debt

Portfolio

Holding Period

Average

Max

Min

Number of observation

Number of times below 0%

Number of times below 6%

Portfolio

Holding Period

Average

Max

Min

Number of observation

Number of times below 0%

Number of times below 6%

MAY 2018 | ISSUE 65 15

Hind-sight Investing

We are well aware of the disclaimer “past performance is no guarantee of future results”. Despite this the most common

method of investing in mutual funds remains by looking at the past performance. It’s quite intuitive to assume that

something that was a good investment in the recent past is still a good investment.

However, it’s not that simple. Our study shows that there is a limited probability of getting investment decisions right

which are solely based on historical data. Let us illustrate this with some examples of the recent past.

The below table comprises of last 17 years of data which to our mind is comprehensive. Funds were ranked based solely

on performance for pre-defined time buckets. As you can see, in the 1 year bucket 36% of the funds continued to be top

performers and 64% could not retain their position. Similarly, in the 3 year bucket 68% of the funds could not retain their

position.

If we translate the above numbers in terms of probability, your chance of selecting a top performing fund basis past

performance is lesser than winning a coin toss!

Just like we don't drive a car looking at the rear view mirror, investment decisions too should not be based on mere past

performance. In fact to our mind one needs to go beyond the norm of return based analysis to arrive at investment

decisions.

As the age old adage goes “bet on the jockey, not the horse”, the same holds true for investment wherein you lay your bet

on the manager and not the fund. So how does one go about it? In line with our philosophy of empowering you, we take

this opportunity to provide you an understanding of our “manager selection methodology”.

(Methodology notes: Date range period 2000-2017, calendar year returns, all open-ended equity schemes, AUM cut off

250cr as on 31st Dec 2017)

Review period: 2000 - 2017

Investments in top performing funds based on 1 – 3 yr track record

Top funds basis

1 yr performance

Rank after1 year

Q1 - 36%

Q2 - 24%

Q3 - 20%

Q4 – 20%

Rank after3 year

Q1 - 33% Q1 - 32%

Top funds basis

1 yr performance

Top funds basis

3 yr performance

Q2 - 34%

Q3 - 16%

Q4 – 17%

Q2 - 33%

Q3 - 18%

Q4 – 17%

Rank after3 year

The top 25% of the funds on basis of performance are assigned Q1, next 25% are assigned Q2 and so on.

Alpha Strategist | “Crossroads”

MAY 2018 | ISSUE 65 16

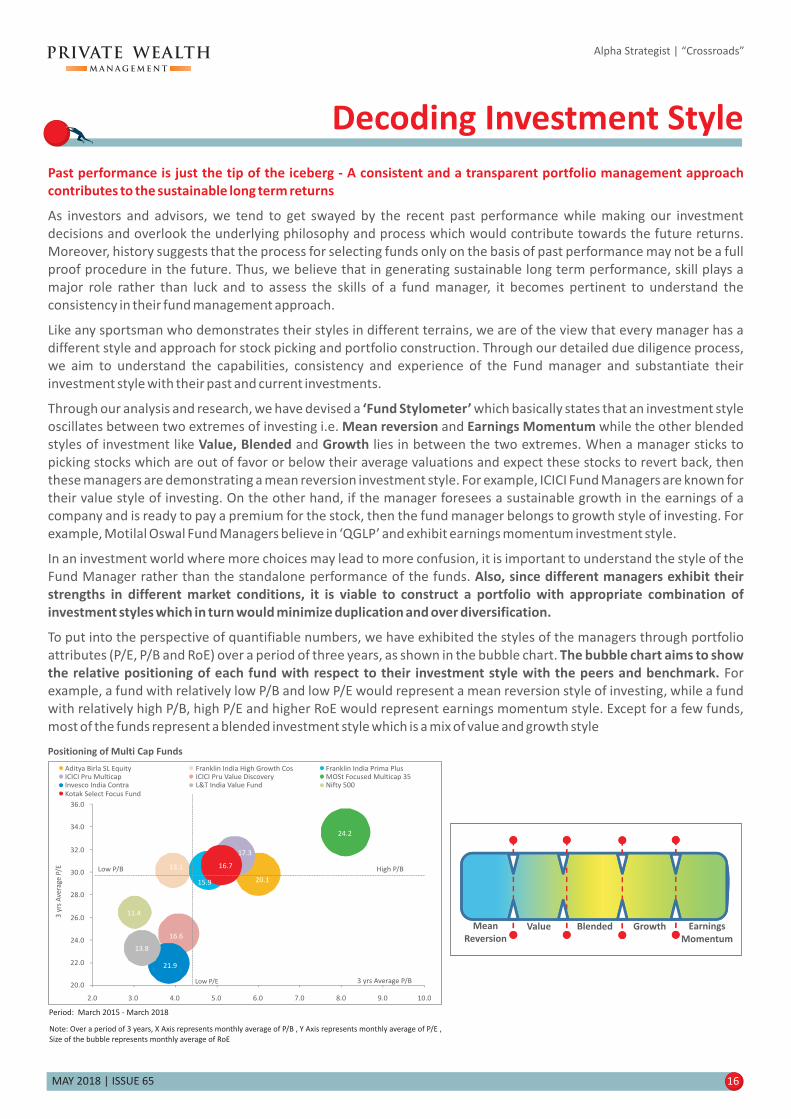

Decoding Investment Style

Past performance is just the tip of the iceberg - A consistent and a transparent portfolio management approach

contributes to the sustainable long term returns

As investors and advisors, we tend to get swayed by the recent past performance while making our investment

decisions and overlook the underlying philosophy and process which would contribute towards the future returns.

Moreover, history suggests that the process for selecting funds only on the basis of past performance may not be a full

proof procedure in the future. Thus, we believe that in generating sustainable long term performance, skill plays a

major role rather than luck and to assess the skills of a fund manager, it becomes pertinent to understand the

consistency in their fund management approach.

Like any sportsman who demonstrates their styles in different terrains, we are of the view that every manager has a

different style and approach for stock picking and portfolio construction. Through our detailed due diligence process,

we aim to understand the capabilities, consistency and experience of the Fund manager and substantiate their

investment style with their past and current investments.

Through our analysis and research, we have devised a which basically states that an investment style

oscillates between two extremes of investing i.e. and while the other blended

styles of investment like and lies in between the two extremes. When a manager sticks to

picking stocks which are out of favor or below their average valuations and expect these stocks to revert back, then

these managers are demonstrating a mean reversion investment style. For example, ICICI Fund Managers are known for

their value style of investing. On the other hand, if the manager foresees a sustainable growth in the earnings of a

company and is ready to pay a premium for the stock, then the fund manager belongs to growth style of investing. For

example, Motilal Oswal Fund Managers believe in ‘QGLP’ and exhibit earnings momentum investment style.

In an investment world where more choices may lead to more confusion, it is important to understand the style of the

Fund Manager rather than the standalone performance of the funds.

To put into the perspective of quantifiable numbers, we have exhibited the styles of the managers through portfolio

attributes (P/E, P/B and RoE) over a period of three years, as shown in the bubble chart.

For

example, a fund with relatively low P/B and low P/E would represent a mean reversion style of investing, while a fund

with relatively high P/B, high P/E and higher RoE would represent earnings momentum style. Except for a few funds,

most of the funds represent a blended investment style which is a mix of value and growth style

‘Fund Stylometer’

Mean reversion Earnings Momentum

Value, Blended Growth

Also, since different managers exhibit their

strengths in different market conditions, it is viable to construct a portfolio with appropriate combination of

investment styles which in turn would minimize duplication and over diversification.

The bubble chart aims to show

the relative positioning of each fund with respect to their investment style with the peers and benchmark.

Alpha Strategist | “Crossroads”

Mean

Reversion

Value Blended Growth Earnings

Momentum

Note: Over a period of 3 years, X Axis represents monthly average of P/B , Y Axis represents monthly average of P/E ,

Size of the bubble represents monthly average of RoE

Positioning of Multi Cap Funds

Period: March 2015 - March 2018

20.1

13.1

15.9

17.3

16.6

24.2

21.9

13.8

11.4

16.7

20.0

22.0

24.0

26.0

28.0

30.0

32.0

34.0

36.0

2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0 10.0

3 yrs Average P/B

Aditya Birla SL Equity Franklin India High Growth Cos Franklin India Prima PlusICICI Pru Multicap ICICI Pru Value Discovery MOSt Focused Multicap 35Invesco India Contra L&T India Value Fund Nifty 500

Kotak Select Focus Fund

High P/B

Low P/E

Low P/B

3 y

rs A

vera

ge P

/E

MAY 2018 | ISSUE 65 17

With markets making historical highs there is a lot of time and ink getting consumed giving views on valuations. One of

the views being that valuations are above long term average and the parameter used to arrive at this view is price

earning multiple. To our mind formulating views solely based on this parameter has certain pitfall. For instance

historically higher price earning phases have been backed by high growth momentum which in today’s scenario is

different. Earnings seem to be the missing ingredient over the past couple of years. Thus there is a need to use multiple

parameters rather than confining oneself to a single variable in order to make investment decisions more full proof. In

our view one needs to take into account risk reward in order to arrive at margin of safety which is critical and forms the

basis for any investment decision.

We are cognizant of the fact that investments are tuned to meet your objectives and thus calling for a suitable asset mix

basis your investment objective. In addition we believe that investors should have a disciplined investment approach

with respect to asset allocation and should not get swayed by market sentiments to avoid accidents. Deviation from the

strategic asset mix should be under circumstances having favorable risk reward. Ideally a prudent investment decision

revolves around the principle of increasing equity exposure when markets are cheap and allocate less when markets are

expensive. However the challenge always remains to accurately estimate when the market is cheap or expensive. In

order to arrive at the decision of preferring equity over debt or vice versa, we believe earning yield to bond yield is an

excellent parameter to consider. This ratio indicates the perceived risk differential between equity and bonds.

Historically whenever earnings yield and bond yield spreads are above 0.8, equities are considered to be undervalued.

For instance at the time of demonetization which coincided with U.S election, one witnessed a sharp fall in yields

making investment in equity compelling on the back of relative valuations. Likewise, any number below .6 suggests

merit in having the portfolio tinted towards debt.

The earning yield to bond yield parameter along with our in-house indicator of market valuations named as MOVI – The

Motilal Oswal Valuation Index enables us to arrive at a well-researched and thought through asset class outlook. So

what is MOVI and what are the variables considered? MOVI is basically an index which is calculated based on the Price to

Earnings (PE), Price to Book Value (PB) and Dividend Yield (DY) on the components of Nifty 50. By means of an algorithm

the weighted average PE, PB and DY of the components of Nifty 50, one arrives at index. A higher level on the MOVI

means markets are expensive and hence one should reduce equity exposure while a lower level on the MOVI means

markets are attractive and hence one should overweight equity exposure.

With the above mentioned input variables we have crafted a unique model coined as temperature gauge which help in

making investment choices across asset classes. The objective of the strategy is to reduce volatility and keep investors

shielded from the sharp falls that are sometimes seen after sustained rise in equity prices.

So how has this fared in the past?

Temperature Gauge

Alpha Strategist | “Crossroads”

MAY 2018 | ISSUE 65 18

Alpha Strategist | “Crossroads”

In the above graph the earning yield is plotted against the x axis and MOVI on the Y axis. The data considered is

represented from the bottom of the market in 2002 till date which basically encompasses two full market cycles of

boom and bust. It is quite evident from the above graph that as the market tends to move towards top right corner,

there are several instances of negative returns and a cautious approach is recommended. However, as the market

moves towards bottom left corner, there are more instances of 18%+ returns from a 3-year forward perspective and

recommend investors to invest aggressively.

This qualitative and quantitative process would enable us to construct “winning portfolios” for our clients. In line with

our philosophy of providing better insights to you, we hope you find the same informative.

3-yr forward NiftyActive

Manager

Average

Max

Min

% times >0%

10%

46%

-9%

97%

19%

54%

-8%

97%

<0%

0-10%

10-18%

18%+

Current

MOVI

40

60

80

100

120

140

160

0.81.01.21.41.61.8

1.53 1.2 0.62 0.54

68%

95%

Fair Value ZoneAttractive Zone

Expensive

Zone

52% of the

observation

lies in this area

0.6

Temperature Gauge – Our internal market thermometer

0.4

EY-BY 0.4-

0.6-

0.8-

1.0-

1.2-

1.4-

1.6-

-

-

-

-

-

-

140

120

100

80

60

40

EY-BY

0.54

MOVI

115.6

Period of analysis: Jan 2002 to April 2018

MOTILAL OSWAL PRIVATE WEALTH MANAGEMENT (MOPWM) - INVESTMENT GRID (May 2018)

Asset Class Holding Period Theme Strategy Managed Solutions

1 Year

< 3 Years

Equity

Fixed Income

Alternatives

Valuations (TTM) trading slightly above its long term average

Revival in rural economy & consumption, deep value,

cyclical recovery

Growth through diversification

Low duration, taxation benefit

Play on short term rates coming off, Capital Preservation

(low credit risk)

Large caps, Dynamic Equity Funds

Multi-cap

Diversified Strategy

Arbitrage/Ultra Short Term Funds/ Low

Duration Funds Long-short funds

High Quality Shot Term Funds,

Structured Products

> 3 Years Coupon + Capital Appreciation Credit Opportunties Funds

3 Years & above

Accommodative central bank policies and reduced likelihood of

US rate hikeSovereign Gold Bonds, Gold ETFs> 3 Years --

M0 NTDOP PMS, ASK Indian Entrepreneur Portfolio, ASK Select

Portfolio, Renaissance All Cap, Franklin India High Growth Cos, Franklin

India Prima Plus, MOSt Focused Multicap 35, M0 NTDOP PMS, Aditya

Birla Equity

MAY 2018 | ISSUE 65 19

Investment GridAlpha Strategist | “Crossroads”

MO Value PMS, Motilal Oswal F25, Aditya Birla SL Top 100, Aditya Birla

SL Focused Eq, ICICI Pru BlueChip Eq, SBI Bluechip , Motilal Oswal

Dynamic, Avendus Enhanced Return

IDFC Arbitrage, Kotak Equity Arbitrage , Invesco India Arbitrage, ICICI

Pru Equity Arbitrage, ABSL Savings, Franklin India Ultra Short, Franklin

Low Duration, ICICI Pru Savings, UTI Treasury Advantage

BNP Paribas Corporate Bond, IDFC Corprate Bond, Aditya Birla

Corporate Bond, IDFC SSIF-ST, ICICI Pru ST Plan, 1-3 yr Fixed Income

Structured Products, FMPs

IDFC Credit Opps, HDFC Credit Risk Bond, ICICI Pru Credit Risk,Reliance

Credit Risk, Franklin STIP, BOI Axa Credit Risk, ABSL Medium Term, LnT

Resurgent India Bond, Reliance Classic Bond, Franklin India Income Opp

Renaissance India Next, Ashmore India Opportunities Fund, Invesco

RISE & DAWN Portfolio, DHFL Pramerica Deep Value PMS, Invesco India

Contra Fund, L&T India Value Fund, ICICI Pru Value Discovery

10-12 YearsHigh equity upside based Alternative

Investment FundsIndia Business Excellence Fund III

Investment in mid-market enterprises that are typically market

leaders which are generally managed by first-generation

entrepreneurs specially from consumer, financial services,

pharma & niche manufacturing sectors

5 - 7 yearsInvesting in early stage mezzanine/

structured equity transactions with

reputed developers from top 6 citiesIndia Realty Excellence Fund IV

Affordable Housing space

MAY 2018 | ISSUE 65 20

Our Recommendations

Alpha Strategist | “Crossroads”

Portfolio Management Services (PMS)

* PMS performance are net of all expenses & fees

Absolute

1 Year 3 Years 5 Years

MOPWM

RatingScheme Name

CAGRStd Dev Beta Alpha

Info.

Ratio

Avg 1 yr

rolling

return

Mααα 12.6

14.8

18.8

14.0

10.5

28.9

3.5

Mααα

Mααα

9.4

19.6

15.4

15.4

10.8

—

19.0

PMS Strategies*

16.6

10.8

6.6

12.1

8.7

24.3

12.7

14.6

8.2

14.1

15.3

15.5

19.1

14.6

9.3

11.5

9.2

17.4

17.9

15.9

12.2

21.3

13.5

12.0

—

21.1

22.1

19.5

21.5

24.4

26.5

22.6

18.8

22.4

19.7

15.4

18.6

14.6

10.1

11.7

9.6

17.3

17.9

15.9

12.4

20.6

—

12.2

14.1

13.6

15.6

12.8

13.0

14.9

15.8

14.6

12.9

15.5

—

13.9

0.90

0.95

1.04

0.90

0.89

1.04

1.07

0.99

0.85

1.03

—

1.00

7.0

4.9

-2.3

0.1

-1.9

4.8

5.3

3.7

1.1

8.2

—

—

1.0

1.0

-0.4

-0.2

-0.6

1.3

1.0

0.8

0.0

1.4

—

—

Mααα

Mααα

Mαα

Mαα

Mαα

2.8

14.1

16.2

33.6

12.1

13.0

15.8

11.1

15.8

12.2

Mααα

Mαα

Mαα

Mααα

12.2

18.2

18.6

23.9

15.8

18.4

18.1

19.7

17.1

16.9

—

27.7

27.8

25.8

26.4

27.7

31.0

34.2

27.3

21.0

12.6

17.9

18.3

23.0

15.7

18.4

17.7

19.7

—

16.7

14.5

15.2

15.4

16.7

13.7

16.7

14.3

17.6

—

16.2

0.77

0.89

0.92

0.95

0.80

0.96

0.82

0.98

—

1.00

-1.7

2.4

2.5

6.8

1.1

2.1

3.0

3.2

—

—

-0.5

0.2

0.4

1.0

-0.2

0.3

0.2

0.4

—

—

Mααα

Absolute

1 Year 3 Years 5 Years

MOPWM

RatingScheme Name

CAGRStd Dev Beta Alpha

Avg 1 yr

rolling

return

AUM

(in Rs. Cr.)Info.

Ratio

Mααα 14.3

15.7

10.5

11.3

11.8

12.5

15.4

Mααα

Mαα

Mαα

Large Cap Funds

12.6

12.3

11.2

11.8

11.6

10.5

9.5

18.7

17.1

17.8

—

17.3

15.6

12.6

12.7

12.5

11.5

12.0

11.8

—

9.8

12.5

13.1

13.1

13.0

13.0

—

13.5

0.88

0.94

0.93

0.81

0.94

—

1.00

3.3

2.9

1.9

2.9

2.2

—

—

0.7

0.8

0.4

0.3

0.6

—

—

Mαα

—

—

—

10.1

11.0

9.6

12.0

10.9

12.4

Balanced Funds

Aditya Birla SL Equity Hybrid ’95 Fund

ICICI Pru Equity & Debt Fund

Franklin India Balanced Fund

HDFC Hybrid Fund

Mααα

Mααα

Mαα

Mαα

Category Average

CRISIL Balanced - Agg Index

11.7

12.6

9.5

12.5

10.1

11.2

17.2

18.2

16.2

19.5

15.7

13.5

11.7

12.4

9.5

12.3

—

11.1

10.2

10.3

8.9

10.4

—

9.0

1.10

1.09

0.96

1.14

—

1.00

0.1

0.9

-1.3

0.6

—

—

0.2

0.4

-0.7

0.5

—

—

14,662

28,806

2,087

21,779

—

—

—

—

Mααα

Mα

—

Mααα

Mααα

Mααα

18.0

31.0

27.0

27.4

—

—

22.4

9.9

19.4

15.3

15.3

11.2

—

19.3

13.5

17.8

13.4

13.4

13.7

—

18.1

0.89

0.94

0.75

0.77

0.92

—

0.92

0.5

3.4

4.7

5.8

-0.5

—

3.4

0.0

0.3

0.3

0.5

-0.2

—

0.2Mααα

AUM

(in Rs. Cr.)

Mααα

Mαα

Mααα

Mαα

Arbitrage Funds

Mααα

Mαα

—

—

Mααα

—

MOSt Value Strategy

MOST NTDOP Strategy

ASK IEP Strategy

ASK SELECT Strategy

DHFL DV

RISE Strategy

MOST IOP Strategy

Equity Mutual Funds

2,767

8,012

6,361

3,013

598

447

4,355

15,236

17,142

4,212

1,003

20,451

—

—

Category Average

NIFTY 50

SBI BlueChip Fund

ICICI Pru BlueChip Equity Fund

Aditya Birla SL Focused Equity Fund

Motilal Oswal Focused 25 Fund

Aditya Birla SL Frontline Equity Fund

12,213

17,853

7,602

11,848

16,652

1,450

8,073

9,251

2,856

2,606

—

—

Multi Cap Funds

Motilal Oswal Multicap 35 Fund

Kotak Select Focus Fund

Franklin India Focused Equity

Franklin India Prima Plus Fund

ICICI Pru Value Discovery Fund

Invesco India Contra Fund

L&T India Value Fund

Aditya Birla SL Equity Fund

ICICI Pru Multicap Fund

Sundaram Rural & Consumption Fund

Category Average

NIFTY 500

1,279

3,005

21,357

3,647

6,686

6,551

7,517

6,248

—

—

Small & Mid Cap Funds

Motilal Oswal Midcap 30 Fund

Kotak Emerging Opportunites Fund

HDFC Mid-Cap Opportunities Fund

HDFC Small Cap Fund

Franklin India Prima Fund

Sundaram Midcap Fund

Franklin India Smaller Cos Fund

DSPBR Small Cap Fund

Category Average

Nifty Free Float Midcap 100

IDFC Arbitrage Fund

ICICI Pru Equity-Arbitrage Fund

Kotak Equity Arbitrage Scheme

Invesco India Arbitrage Fund

Category Average

Crisil Liquid Fund Index

Mαα

Mααα

Mααα

-3.1

-2.7

-2.7

-2.5—

—

-0.9

-0.9

-0.8

-0.8—

—

2,288

8,686

11,257

347—

—

5.8

5.86.1

5.95.86.9

6.1

6.3

6.4

6.26.37.3

7.2

7.3

7.3

7.07.18.1

6.0

6.1

6.2

6.1—

—

0.4

0.4

0.4

0.5—

—

0.79

0.97

0.92

0.84—

—

MAY 2018 | ISSUE 65 21

Alpha Strategist | “Crossroads”

IDFC Coporate Bond Fund

BNP Paribas Corp Bond Fund

IDFC SSIF-ST Fund

Aditya Birla SL Corporate Bond

Franklin India IBA-A*

Crisil Composite Bond Fund Index

4.5

1.8

4.0

4.7

5.4

0.8

3.2

2.5

3.0

3.7

4.5

-1.2

5.8

5.5

5.3

6.0

6.8

3.7

—

7.6

7.1

8.0

7.9

7.6

—

7.9

7.8

8.6

8.6

7.9

1.7

3.1

1.6

1.6

2.0

—

8.1

8.3

8.1

8.2

9.1

—

96.3

90.4

96.4

79.2

14.4

—

—

7.7

—

16.4

80.4

—

—

—

—

—

0.8

—

3.7

1.9

3.6

4.5

4.4

—

11,456

91

4,344

17,330

885

—

Accrual Funds - High Quality

M

M

M

M

M

M

M

ααα

ααα

αα

ααα

ααα

αα

αα

M

M

M

ααα

ααα

αα

Category Average

Crisil Composite Bond Fund Index

6.3

4.8

7.0

4.5

6.2

4.2

2.3

4.6

5.5

2.8

4.7

0.8

5.0

3.9

6.8

3.2

5.3

3.4

1.4

3.6

4.1

2.0

3.9

-1.2

7.7

6.7

8.3

5.8

7.6

5.9

4.9

5.5

6.4

5.5

6.3

3.7

8.2

8.5

9.7

—

8.3

8.0

8.1

8.1

7.9

8.2

8.3

7.6

9.1

9.5

—

—

9.0

8.6

—

8.5

8.4

—

8.8

7.9

9,769

11,536

1,495

11,456

3,466

10,752

2,495

5,205

10,409

8,131

—

—

Credit Opportunities Fund

Category Average

Dynamic Bond Fund

Crisil Composite Bond Fund Index

7,477

1,435

1,970

3,160

—

—

M

M

M

M

ααα

ααα

αα

αα

0.1

4.9

0.9

-0.1

1.1

0.8

2.6

4.0

3.0

1.6

3.4

3.7

-3.5

-0.3

-1.7

-2.8

-1.0

-1.2

6.5

8.1

7.4

6.4

6.5

7.6

8.1

10.6

7.2

7.4

7.3

7.9

48.5

80.1

92.3

98.0

—

—

43.5

12.2

7.6

—

—

—

2.0

—

—

—

—

—

6.0

7.8

0.2

2.0

—

—

Franklin India ST Income Plan *

Aditya Birla SL Medium Term Fund

BOI AXA Credit Risk Fund

IDFC Corp Bond Fund

Franklin India Income Opportunities Fund

Reliance Credit Risk Fund

L&T Resurgent India Corp Bond Fund

HDFC Credit Risk Bond Fund

ICICI Pru Credit Risk Fund

Reliance Classic Bond Fund

Aditya Birla SL Dynamic Bond Fund

UTI Dynamic Bond Fund

SBI Dynamic Bond

IDFC Dynamic Bond Fund

—

—

—

—

Category Average

Ultra Short Term

Crisil Liquid Fund Index

21,053

19,753

5,421

12,880

9,845

—

—

M

M

M

M

M

ααα

ααα

ααα

αα

αα

6.6

6.9

7.5

7.9

6.4

6.4

7.3

6.7

6.9

7.8

7.9

6.6

6.5

6.9

5.7

6.0

6.3

7.1

6.0

5.6

6.9

8.0

8.2

9.0

9.0

7.9

7.5

7.3

8.6

8.7

9.3

9.4

8.9

8.1

8.1

80.4

66.5

24.6

27.1

81.6

—

—

17.5

31.2

68.6

70.2

15.7

—

—

—

—

5.0

—

—

—

—

2.1

2.3

1.9

2.7

2.7

—

—

ICICI Pru Saving Fund

Aditya Birla SL Savings Fund

Franklin India Low Duration Fund

Franklin India Ultra Short Bond Fund

UTI Treasury Advantage Fund

—

—

M

M

—

ααα

αα

M

M

M

αα

αα

αα

9.7

20.8

32.0

96.3

11.9

4.3

78.1

30.8

9.0

16.6

—

—

75.5

66.1

51.6

—

78.2

87.2

19.3

62.1

83.1

80.0

—

—

12.4

8.8

12.9

—

7.6

5.3

—

—

3.8

—

—

—

2.5

4.2

3.5

3.7

2.2

3.3

2.6

5.7

4.1

3.4

—

—

1.9

1.8

1.5

1.7

1.8

1.9

2.8

1.5

1.7

2.5

—

—

10.1

9.9

11.3

8.1

9.8

9.8

8.7

8.8

9.8

9.2

—

—

3.5

2.2

1.9

3.1

—

—

8.9

8.4

7.1

8.0

—

—

0.9

0.7

1.3

0.7

0.7

—

—

8.0

8.0

8.8

8.9

8.0

—

—

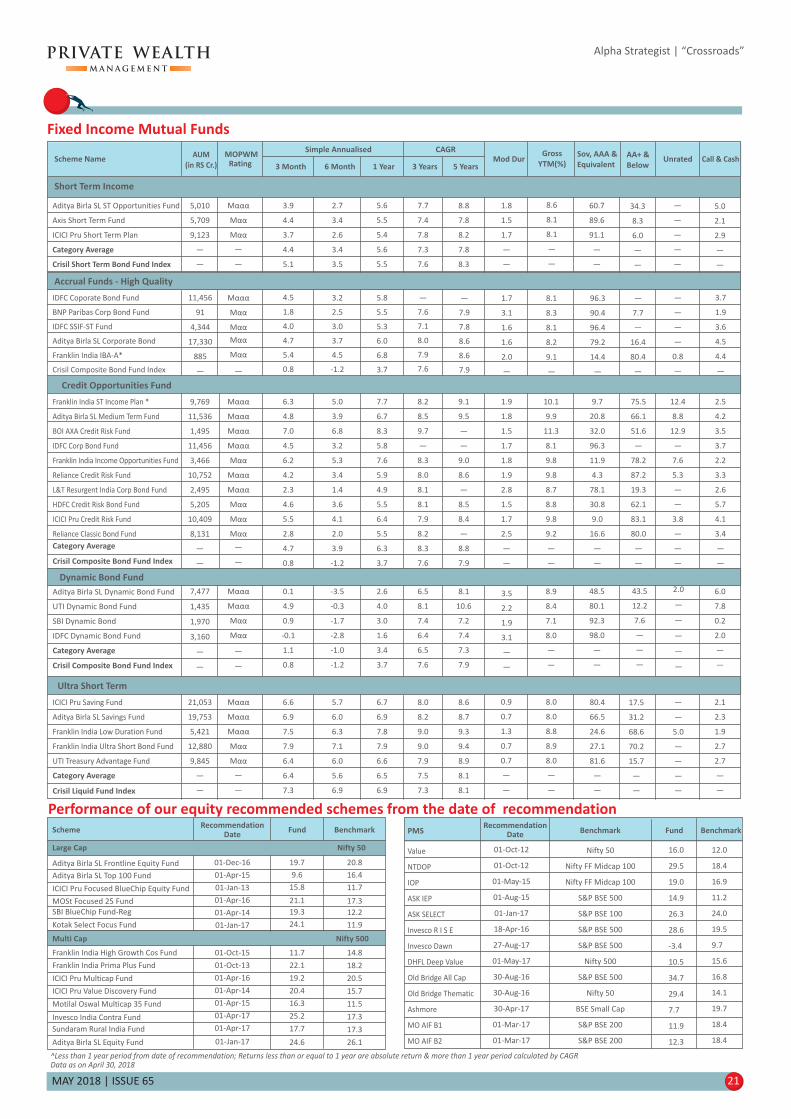

Fixed Income Mutual Funds

3 Month 6 Month 1 Year 3 Years 5 YearsMod Dur

Gross

YTM(%)

Sov,

Equivalent

AAA & AA+ &

BelowUnratedScheme Name

MOPWMRating

Simple Annualised CAGRCall & Cash

AUM

(in RS Cr.)

M

M

M

ααα

αα

αα

3.9

4.4

3.7

4.4

5.1

2.7

3.4

2.6

3.4

3.5

5.6

5.5

5.4

5.6

5.5

7.7

7.4

7.8

7.3

7.6

8.8

7.8

8.2

7.8

8.3

—

—

—

—

—

5.0

2.1

2.9

—

—

5,010

5,709

9,123

—

—

Short Term Income

Aditya Birla SL ST Opportunities Fund

Axis Short Term Fund

ICICI Pru Short Term Plan

Category Average

Crisil Short Term Bond Fund Index

60.7

89.6

91.1

—

—

34.3

8.3

6.0

—

—

—

—

1.8

1.5

1.7

—

—

8.6

8.1

8.1

—

—

^Less than 1 year period from date of recommendation; Returns less than or equal to 1 year are absolute return & more than 1 year period calculated by CAGRData as on April 30, 2018

Performance of our equity recommended schemes from the date of recommendation

Benchmark

Value

NTDOP

IOP

ASK IEP

ASK SELECT

Invesco R I S E

Invesco Dawn

DHFL Deep Value

Old Bridge All Cap

Old Bridge Thematic

Ashmore

MO AIF B1

MO AIF B2

FundBenchmark

12.0

18.4

16.9

11.2

24.0

19.5

9.7

15.6

16.8

14.1

19.7

18.4

18.4

01-Oct-12

01-Oct-12

01-May-15

01-Aug-15

01-Jan-17

18-Apr-16

27-Aug-17

01-May-17

30-Aug-16

30-Aug-16

30-Apr-17

01-Mar-17

01-Mar-17

16.0

29.5

19.0

14.9

26.3

28.6

-3.4

10.5

34.7

29.4

7.7

11.9

12.3

Nifty 50

Nifty FF Midcap 100

Nifty FF Midcap 100

S&P BSE 500

S&P BSE 100

S&P BSE 500

S&P BSE 500

Nifty 500

S&P BSE 500

Nifty 50

BSE Small Cap

S&P BSE 200

S&P BSE 200

RecommendationDatePMS

Large Cap Nifty 50

Multi Cap Nifty 500

20.8

16.4

11.7

17.3

12.2

11.9

BenchmarkScheme FundRecommendation

Date

01-Dec-16

01-Apr-15

01-Jan-13

01-Apr-16

01-Apr-14

01-Jan-17

19.7

9.6

15.8

21.1

19.3

24.1

Aditya Birla SL Frontline Equity Fund

Aditya Birla SL Top 100 Fund

ICICI Pru Focused BlueChip Equity Fund

MOSt Focused 25 Fund

SBI BlueChip Fund-Reg

Kotak Select Focus Fund

14.8

18.2

20.5

15.7

11.5

17.3

17.3

26.1

01-Oct-15

01-Oct-13

01-Apr-16

01-Apr-14

01-Apr-15

01-Apr-17

01-Apr-17

01-Jan-17

11.7

22.1

19.2

20.4

16.3

25.2

17.7

24.6

Franklin India High Growth Cos Fund

Franklin India Prima Plus Fund

ICICI Pru Multicap Fund

ICICI Pru Value Discovery Fund

Motilal Oswal Multicap 35 Fund

Invesco India Contra Fund

Sundaram Rural India Fund

Aditya Birla SL Equity Fund

This document is not valid without disclosure; refer the last page for the disclosure

MAY 2018 | ISSUE 65 22

Section II

Macro Economy...................................................................................................23

Equities...............................................................................................................29

Fixed Income.......................................................................................................34

Alternatives.........................................................................................................37

Alpha Strategist | “Crossroads”

MAY 2018 | ISSUE 65 23

Macro Economy

Alpha Strategist | “Crossroads”

US Fed’s outlook remains

positive and rate hikes

remain on course

The US Fed left rates unchanged in their recent meet but going by their outlook, rate hikes

remain on course. The recent spike in inflation means that the next hike is expected in the

central bank’s June meeting. US GDP data was released recently and it was lower than the

previous quarter. The slowdown is likely caused by the reduced pace of consumer spending

and residential fixed investment. Yet, the economy is growing at a decent pace and looks on

track for continued expansion. Also, the US is expected to receive a substantial amount of

fiscal stimulus this year through tax reform and the passing of another federal bill.

Despite the China trade spat, the Fed remains optimistic on economic growth. A full blown

trade war scenario between the US and China still looks unlikely and negotiations should

prove to be a diffuser but as long as the issue remains unsettled, uncertainty will keep a cap

on global markets. Meanwhile US treasury yields went past the 3% mark and the dollar

rallied subsequently.

US expansion remains on track despite lower GDP

GDP YoY

Inflation rate

10yr Gsec

Policy rate

2.90%

2.40%

2.94%

1.75%

2.00%

1.10%

0.05%

-0.10%

6.80%

2.10%

3.68%

4.35%

2.90%

1.60%

0.56%

0.00%

2.10%

1,6%

0.78%

0.00%

1.20%

2.50%

1.43%

0.50%

2.50%

1.30%

-0.44%

0.00%

US Japan China Germany FranceUnited

KingdomEuro Area

Major Economies - Snapshot

Emerging Economies - Snapshot

GDP YoY

Inflation rate

10yr Gsec

Policy rate

7.20%

4.28%

7.76%

6.00%

5.10%

3.41%

6.96%

4.25%

2.10%

2.68%

9.87%

6.50%

1.20%

5.04%

7.54%

7.50%

2.80%

1.60%

2.75%

1.50%

3.40%

2.60%

2.20%

2.00%

0.90%

2.40%

7.27%

7.25%

India Indonesia Brazil Mexico South Korea RussiaHong Kong

US Trade deficit with China continues to balloon

Source: U.S. Bureau of Economic Analysis

0.6

2.2

2.8

1.8

1.2

3.1 3.22.9

2.3

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2016 2016 2016 2017 2017 2017 2017 2018

US GDP (annualized % growth)

After expanding for twenty straight quarters, the Euro zone recorded its slowest growth in a

year and a half, causing concern for investors. A stronger euro currency and slower

economic activity are making investors question if the central bank could stick to their plan.

The cause for the slowdown has not been pinpointed yet but the suspects are lower exports

and bad weather conditions.

Slower Eurozone growth stokes concerns

Alpha Strategist | “Crossroads”

MAY 2018 | ISSUE 65 24

ECB’s stance in

question in the

face of slowdown

Meanwhile concerns surrounding the impact of the US-China trade spat and Brexit have

bubbled up. The ECB, which was planning to end its bond buying program this year, is

viewing upcoming data with caution. The central bank was relying on growth to eventually

boost inflation. Yet Eurozone’s purchasing managers’ index, which tracks activity such as

order books and inventory, signaled that the slowdown is likely to be temporary and

expansion could return soon.

Despite continued growth, Japan faces testing year ahead

Japan’s recovery continues to remain robust and growth is likely to continue through the

year, albeit at a slower pace. The slowdown was caused by a hit to exports and lower

consumer spending due to increased prices of daily goods. Some important factors will test

the economy’s resilience this year. A potential increase in sales tax is likely to be levied

which could cause the nation’s growth to slow down. Japan will be cautious this time

around because the last time taxes were raised, the country was hit by a recession as a

result. Also, the Bank of Japan is likely to wind down stimulus if it hits its inflation target. It is

already halfway to the target and is showing signs of increased growth.

Meanwhile Japan and China are holding an economic dialogue after eight years on the

back of the US trade threats. This could set the stage for new trade dialogues between

Japan and China at an important time, as they both will be directly or indirectly affected by

the US trade spat.

With inflation increasing,

the BoJ is likely to

withdraw stimulus

China’s service sector shines in April

Amidst trade negotiations with the US, China’s service sector was boosted in April by faster

new business and employment growth. This is a testament to China’s reduced dependency

on their manufacturing sector and rise in their services sector. This will in turn boost the

domestic demand in the country at an important time. Rising wages are giving consumers

more spending power at home. Meanwhile, new business orders accelerated further due

to better market conditions. Both manufacturing and service sectors are showing

increased signs of firming growth.

Concern remains around the US trade talks. After a round of discussions, no substantial

outcome was achieved but discussions are likely to continue. While some undisclosed

trade issues were resolved, disagreement has been mentioned on other matters.

China’s economy shows

signs of firming growth

amidst US trade talks

China’s trade advantage over the US

Source: United States Census Bureau

0

100,000

200,000

300,000

400,000

500,000

600,000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

in $ mn US Goods Exports to China US Goods Imports from China

Alpha Strategist | “Crossroads”

MAY 2018 | ISSUE 65 25

Indian Economy

IMD expects normal monsoon in 2018

The Indian Meteorological Department (IMD) released its first forecast for the 2018

southwest monsoon (June-September) rainfall with expectations of normal monsoon. It

expects monsoon rainfall at 97% of the long period average (LPA) with very less probability

of experiencing a deficit monsoon. Earlier, Skymet, a private weather forecasting agency,

also predicted southwest monsoon rainfall at 100% of LPA.

These, however, are early forecasts. Timely arrival of monsoons, followed by healthy

monthly and regional distribution, would be crucial. Meanwhile, storage levels in

reservoirs are showing faster depletion. As of mid-April, water storage at 91 major

reservoirs in the country stood at 84% of what is considered normal, compared with 90%

for the same period last year.

Importantly though, the IMD's April forecasts for rainfall are not very reliable. The actual

rainfall has deviated significantly from the forecasts in four out of the last five years and the

deviation has been a downward revision during the three years, 2014 to 2016. With rising

tensions about farmers' distress, general elections in 2019 and the fact that winter

monsoon (January-February) rainfall in 2018 was the worst (only ~38% of normal rainfall)

in at least 26 years, 2018 southwest monsoon holds special significance.

Low probability of

a deficient rainfall

Only 14% probability of deficient rainfall Deviation of actual rainfall from initial forecasts

Source: IMD Source: IMD

CRISIL: Credit quality of Indian firms improved in FY18

As per the latest report by CRISIL, debt rating upgrades outpaced downgrades in FY18.

There were 1402 upgrades against 839 downgrades in FY18, leading to a credit ratio of 1.67

times, better than 1.22 times reported in FY17. Also, debt weighted credit ratio for FY18

stands at 2.31 times much higher than 0.88 times recorded in the previous financial year.

The downgrade rate for FY18 stands at 5.9%, the lowest in the past five fiscals, indicating a