antigua and barbuda sales tax (abst): presentation on draft abst law

TRANSCRIPT

Antigua and Barbuda Sales Tax (ABST):

Presentation on draft ABST law

Basic concepts

taxable transactions: taxable supplies of goods or services taxable imports

taxable activities

taxable persons; registration requirements

place of supply (in A & B)

time of supply (when to pay & deduct)

zero-rated (0%) & exemptions (not taxable)

Taxable supplies

must be a supply

made in the course of the taxable activity

in Antigua and Barbuda

by a taxable person(registered or required to be registered)

not exempt

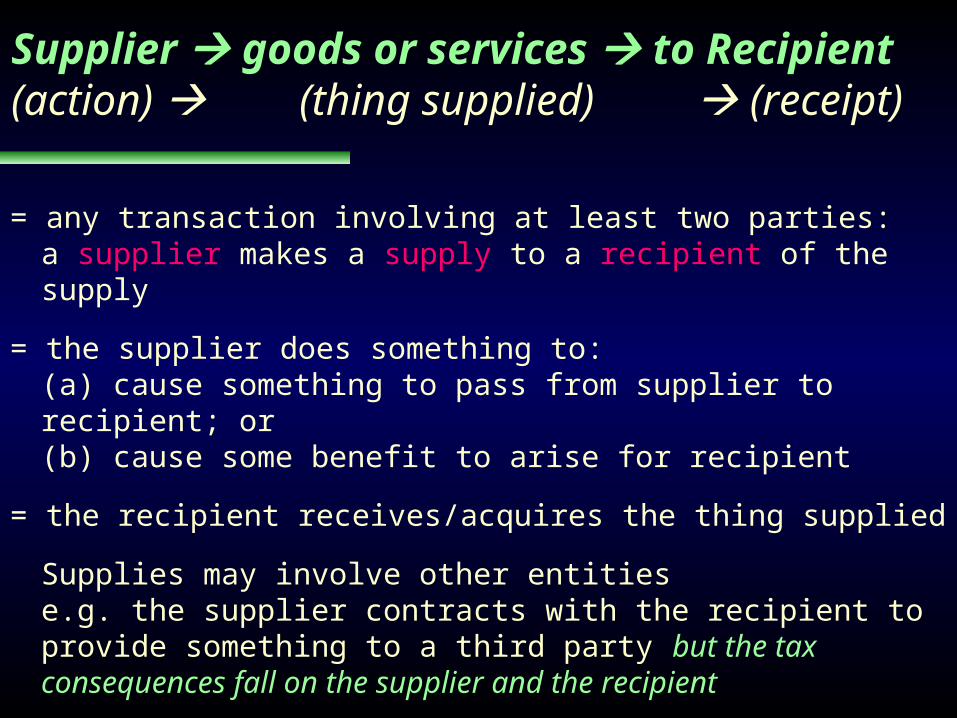

Supplier goods or services to Recipient(action) (thing supplied) (receipt)

= any transaction involving at least two parties:a supplier makes a supply to a recipient of the supply

= the supplier does something to:(a) cause something to pass from supplier to recipient; or(b) cause some benefit to arise for recipient

= the recipient receives/acquires the thing supplied

Supplies may involve other entitiese.g. the supplier contracts with the recipient to provide something to a third party but the tax consequences fall on the supplier and the recipient

Supplies of goods and services

Supplies of goods: goods = tangible property

(real or personal); not only sales – includes leases,

licences, options to purchase, commodity futures

Supplies of services: everything else, e.g. service

industries (including lawyers & accountants), IP,

restrictive covenants, supplies of rights, etc

The distinction is particularly relevant for the

jurisdictional rules (place of supply & exports)

Taxable activity (broader than business)

any activity carried out on a regular or continuous basis & involving the supply of goods or services

includes business, trade, manufacture, commerce, or adventure in the nature of trade

licensing of copyright, leasing of property

includes non-profit activities (because aim is to tax consumption)

one-off activities carried out with a profit-making intent (e.g. acquire property to develop & sell)

Taxable activity (broader than business)

Doesn’t include:

hobbies & private activities

employment (employee is your value added)

acting as director of a company (except where engaged to do so through a business, e.g. where lawyer or accountant engaged to act as Director)

government activities that don’t involve supplying goods or services to the public

Taxable persons

Person includes non-legal persons such as partnerships, trusts, and unincorporated entities

must be registered if an annual turnover ≥ threshold

persons are registered, not activities:if person has >1 taxable activity, all will count towards threshold, only one registration

Exclude from turnover your exempt supplies, other non-taxable supplies, sales of capital assets, closure of a business… …

Place of supply

Goods:

place where goods are when supplied

Services:

most are where supplier has place of business;

some are where supply effectively used or enjoyed

special rules for rights and options (including vouchers and phone cards)

Some supplies are not taxed

zero-rated (0%) & exemption (no tax)

difference lies in the input tax credit entitlements

no credits for exempt supplies

therefore the supplies are “input taxed”

undeductible input tax passed on in the price of exempt supplies is hidden from consumers

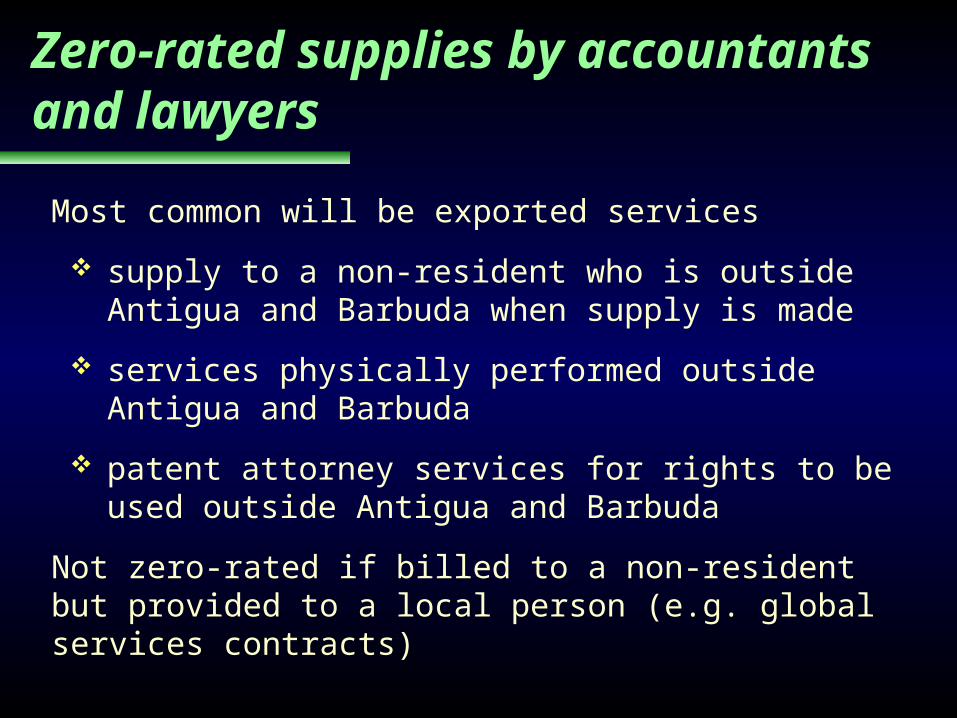

Zero-rated supplies by accountants and lawyers

Most common will be exported services

supply to a non-resident who is outside Antigua and Barbuda when supply is made

services physically performed outside Antigua and Barbuda

patent attorney services for rights to be used outside Antigua and Barbuda

Not zero-rated if billed to a non-resident but provided to a local person (e.g. global services contracts)

Imports

any import by any person registration not required

aim is to tax value of consumption in Antigua and Barbuda taxed charged on:customs value + customs duty & other import taxes + freight & insurance

close links between ABST on imports and customs duties: collection (by Comptroller) administration (under customs laws); time & place of payment (when & where the duty is paid)

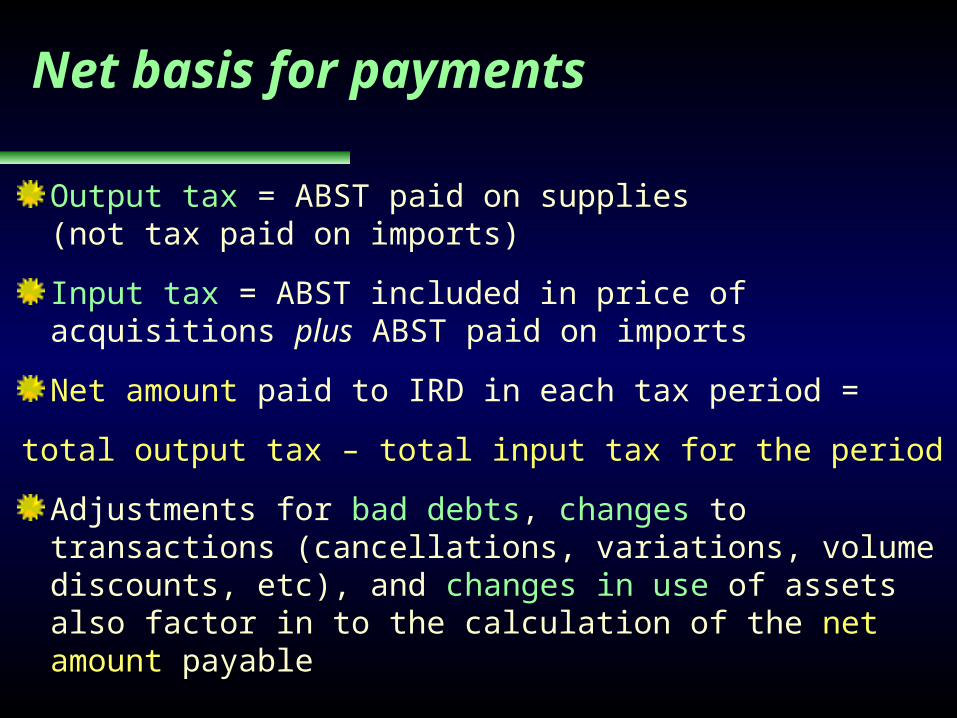

Net basis for payments

Output tax = ABST paid on supplies(not tax paid on imports)

Input tax = ABST included in price of acquisitions plus ABST paid on imports

Net amount paid to IRD in each tax period =

total output tax – total input tax for the period

Adjustments for bad debts, changes to transactions (cancellations, variations, volume discounts, etc), and changes in use of assets also factor in to the calculation of the net amount payable

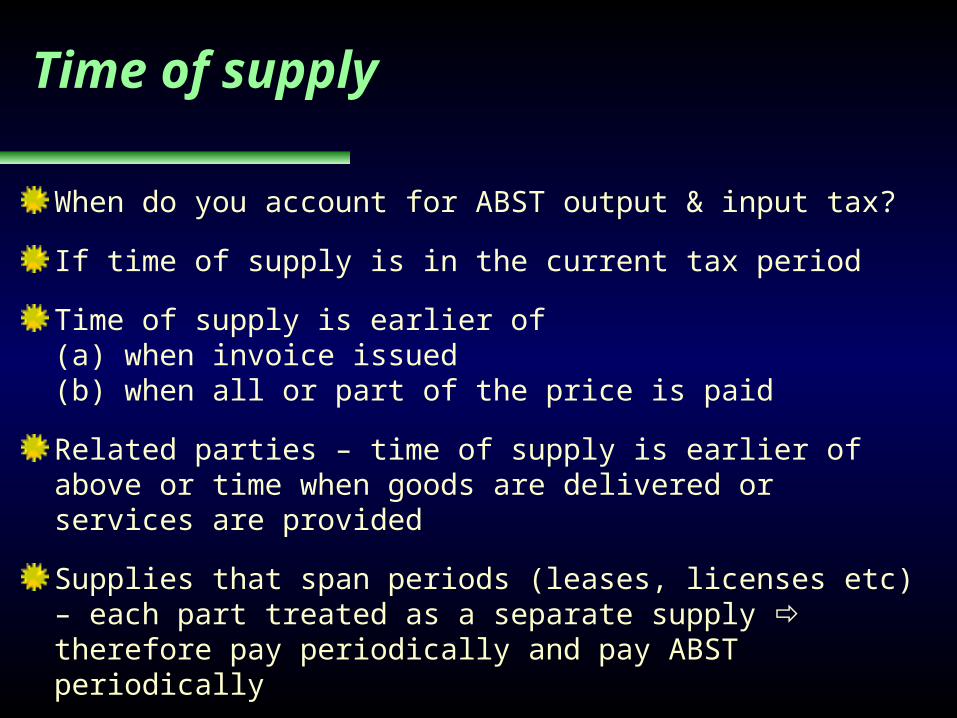

Time of supply

When do you account for ABST output & input tax?

If time of supply is in the current tax period

Time of supply is earlier of(a) when invoice issued(b) when all or part of the price is paid

Related parties – time of supply is earlier of above or time when goods are delivered or services are provided

Supplies that span periods (leases, licenses etc) – each part treated as a separate supply therefore pay periodically and pay ABST periodically

Global basis for calculations

Net ABST payable is calculated for each tax period

Input tax on a particular purchase does not have to be credited when the output tax is paid for the supply to which it relates

Rather, the input tax incurred in a tax period is credited against the output tax collected in that period.

Tracing is only required in a limited sense:for determining whether an acquisition relates to making exempt supplies or private purposes (and therefore is denied an input tax credit)

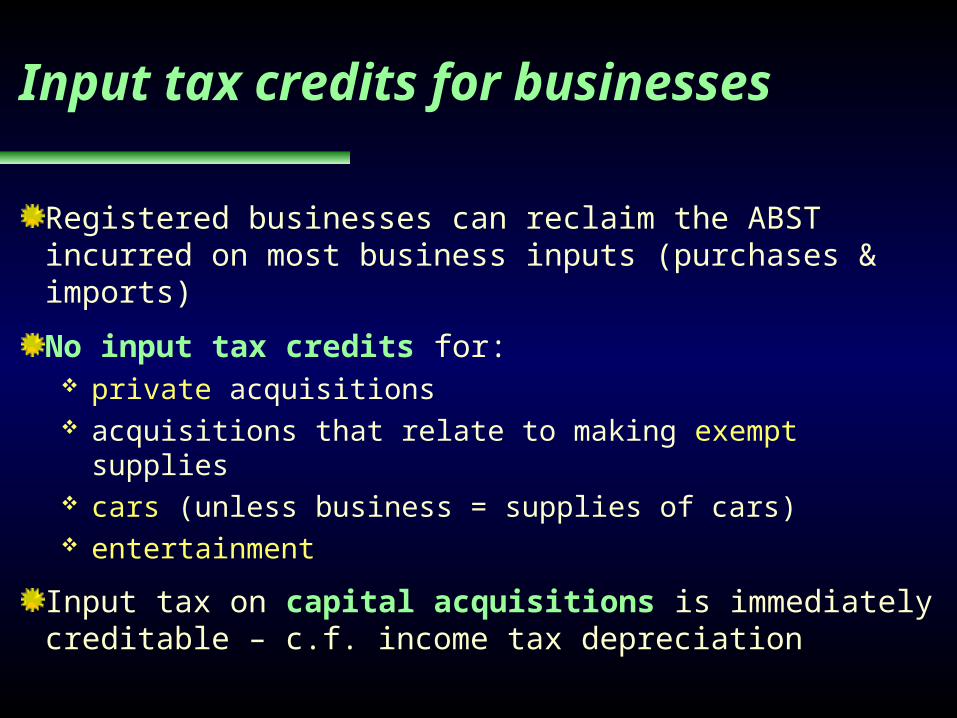

Input tax credits for businesses

Registered businesses can reclaim the ABST incurred on most business inputs (purchases & imports)

No input tax credits for: private acquisitions acquisitions that relate to making exempt supplies cars (unless business = supplies of cars) entertainment

Input tax on capital acquisitions is immediately creditable – c.f. income tax depreciation

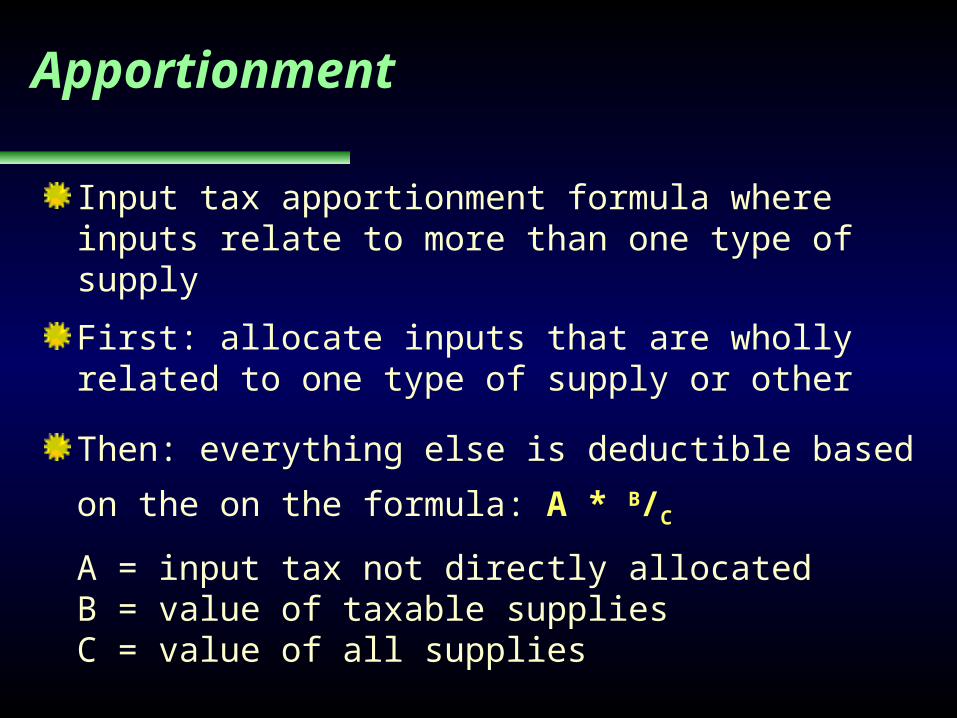

Apportionment

Input tax apportionment formula where inputs relate to more than one type of supply

First: allocate inputs that are wholly related to one type of supply or other

Then: everything else is deductible based on

the on the formula: A * B/C

A = input tax not directly allocatedB = value of taxable suppliesC = value of all supplies

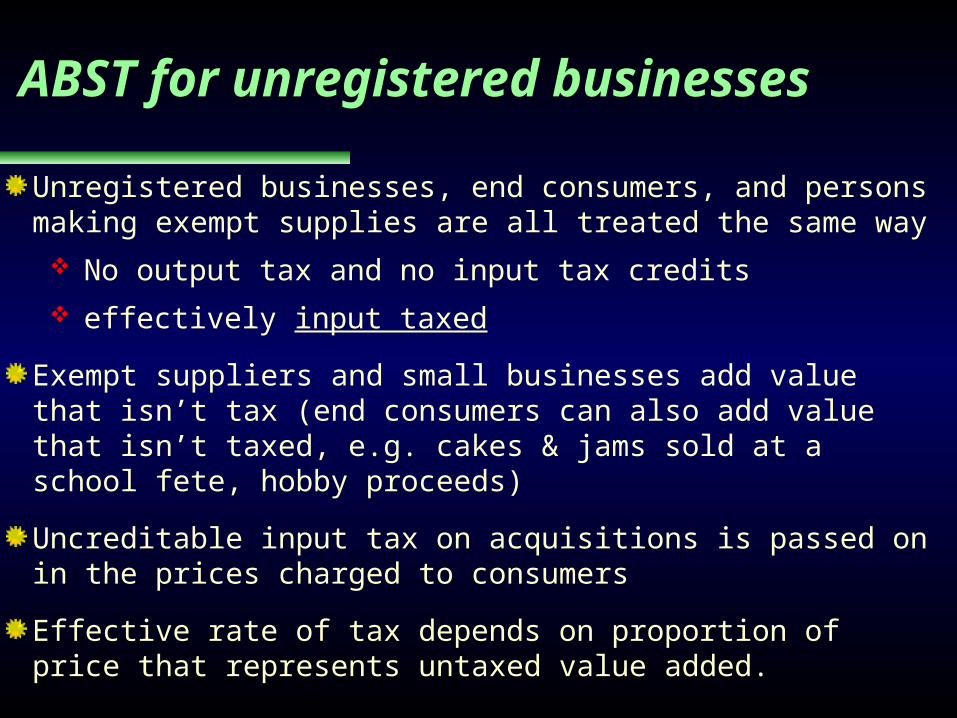

ABST for unregistered businessesUnregistered businesses, end consumers, and persons making exempt supplies are all treated the same way

No output tax and no input tax credits effectively input taxed

Exempt suppliers and small businesses add value that isn’t tax (end consumers can also add value that isn’t taxed, e.g. cakes & jams sold at a school fete, hobby proceeds)

Uncreditable input tax on acquisitions is passed on in the prices charged to consumers

Effective rate of tax depends on proportion of price that represents untaxed value added.

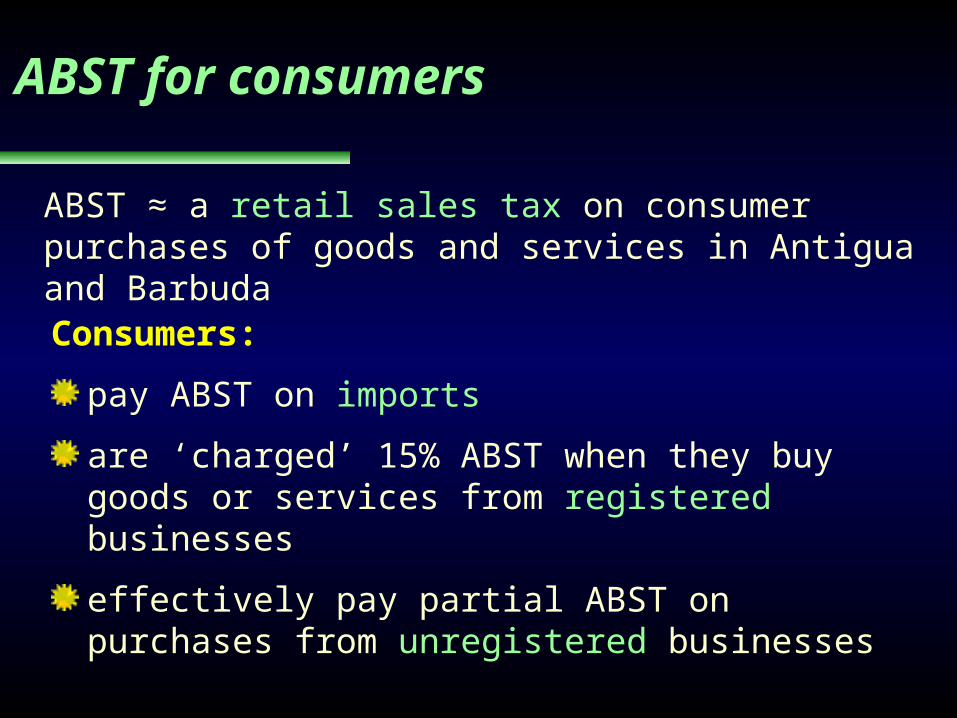

ABST for consumers

Consumers:

pay ABST on imports

are ‘charged’ 15% ABST when they buy goods or services from registered businesses

effectively pay partial ABST on purchases from unregistered businesses

ABST ≈ a retail sales tax on consumer purchases of goods and services in Antigua and Barbuda

Structure of the Act

Basic provisions – definitions then application of

the law

Administrative provisions

Schedules (zero-ratings & exemptions)

Regulations – to cover transitional issues, special

cases, format of tax invoices etc.

Plain English drafting

Wholesaler

Importer

Retailer

Consumer

Cost: $60Value added: $40

Sell for:$100plus ABST: $10

Taxed Price: $110

Cost: $100Value added: $20

Sell for: $120plus ABST: $12

Taxed Price: $132

Cost: $120Value added:

$80Sell for: $200

plus ABST: $20Taxed Price:

$220

Cost: $220(includes $20

tax)

ABST Treatment:taxable supplies and imports

$6

$10- 6$4

$4

$12- 10

$2

$20- 12

$8

$2 $8

To customs To IRD

$4 $2 $8+ + + = $20$6

Wholesaler

Importer

Retailer

Consumer

Cost: $60Value added: $40

Sell for:$100plus ABST: $10

Taxed Price: $110

Cost: $100Value added:

$20Sell for: $120

plus ABST: $12Taxed Price:

$132

Cost: $120Value added: $80

Sell for: $200plus ABST: $0

Taxed Price: $200

Cost: $200(no tax)

ABST: Supply to consumer is zero-ratede.g. electricity subject to the basic charge

$6

$10- 6$4

$4

$12- 10

$2

$ 0- 12

-$12

$2 - $12

To customs To IRD

$4 $2 - $12+ + + = $0$6

Wholesaler

Importer Retailer

Consumer

Cost: $60Value added: $40

Sell for:$100

Cost: $100Value added:

$20Sell for: $120

Cost: $120Value added:

$80Sell for: $200

plus ABST: $20Taxed Price:

$220

Cost: $220(includes $20

tax)

ABST Treatment:Supplies zero-rated until retailer taxede.g. macaroni sold by a registered restaurant

$20- 0

$20

$20

To IRD

$20 = $20

Wholesaler

Importer Bank Consumer

Cost: $60Value added: $40

Sell for:$100plus ABST: $10

Taxed Price: $110

Cost: $100Value added: $20

Sell for: $120plus ABST: $12

Taxed Price: $132

Cost: $132Value added: $80

Sell for: $212plus ABST: $0

Taxed Price: $212

Cost: $212(includes $12

tax)

ABST: Supply to consumer is exempt(e.g. financial services)

$6

$10- 6$4

$4

$12-

10$2

$2

To customs

To IRD

$4

$2

+ + = $12

$6

BankImporter

Retailer

Consumer

Cost: $60Value added: $40

Sell for:$100plus ABST: $10

Taxed Price: $110

Cost: $110Value added:

$20Sell for: $130

Cost: $130Value added:

$80Sell for: $210

plus ABST: $21Taxed Price:

$231

Cost: $231(includes $31

tax)

ABST: supply to retailer is exempte.g. financial services

$6

$10- 6$4

$4

$21- 0

$21

$21

To customs To IRD

$4 $21+ + + = $31$6

Wholesaler

Importer Retailer

Consumer

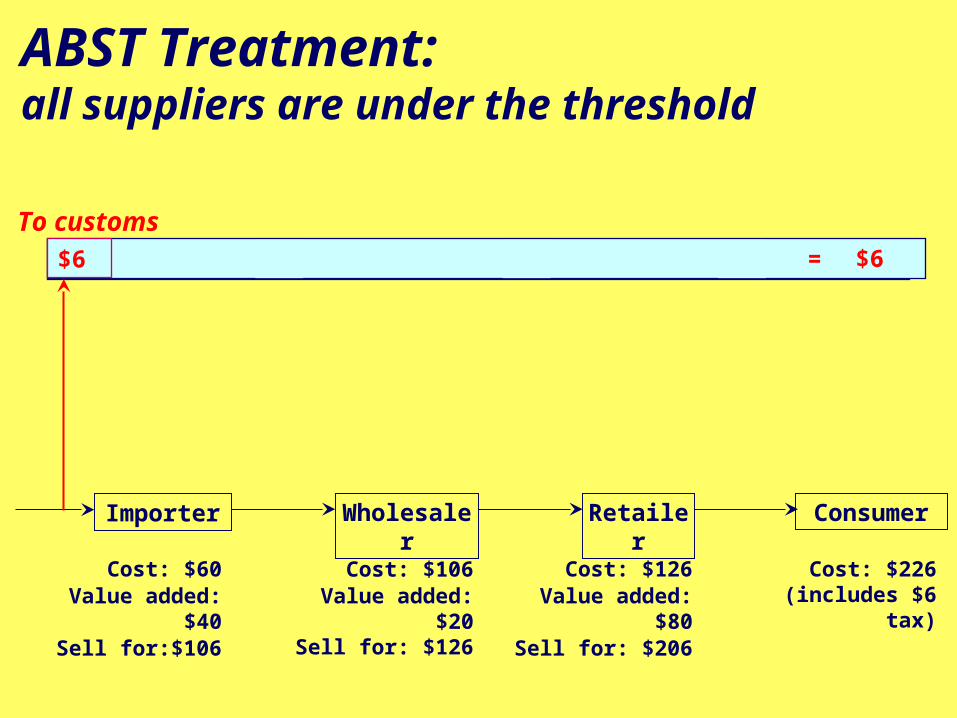

Cost: $60Value added:

$40Sell for:$106

Cost: $106Value added:

$20Sell for: $126

Cost: $126Value added:

$80Sell for: $206

Cost: $226(includes $6

tax)

ABST Treatment:all suppliers are under the threshold

$6

To customs= $6$6

What do you need to do?

identify whether you will exceed the threshold

if yes: will your supplies be taxable, exempt, zero-rated, out-of-scope, or a combination

implement systems to ensure ABST is charged on the right kinds of supplies

work out how your prices should change: subtract taxes saved and then add ABST

get ready to print invoices and documents

be prepared for submitting ABST returns

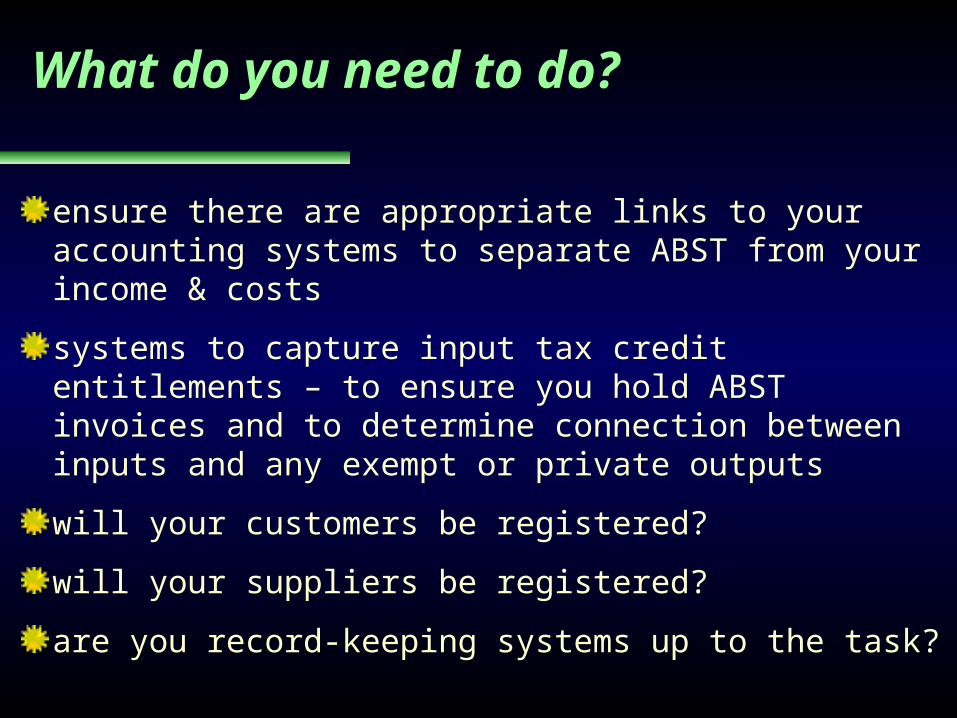

What do you need to do?

ensure there are appropriate links to your accounting systems to separate ABST from your income & costs

systems to capture input tax credit entitlements – to ensure you hold ABST invoices and to determine connection between inputs and any exempt or private outputs

will your customers be registered?

will your suppliers be registered?

are you record-keeping systems up to the task?