anti money laundering pmla guidelines. contents introduction to money laundering introduction : fatf...

TRANSCRIPT

Anti Money LaunderingPMLA Guidelines

Contents• Introduction to Money Laundering• Introduction : FATF / FIU INDIA / PMLA (2002) • Obligations Under PMLA / AML Workflow• Suspicious Transaction in brief• STR Reporting• Sample / Case Studies • Recordkeeping

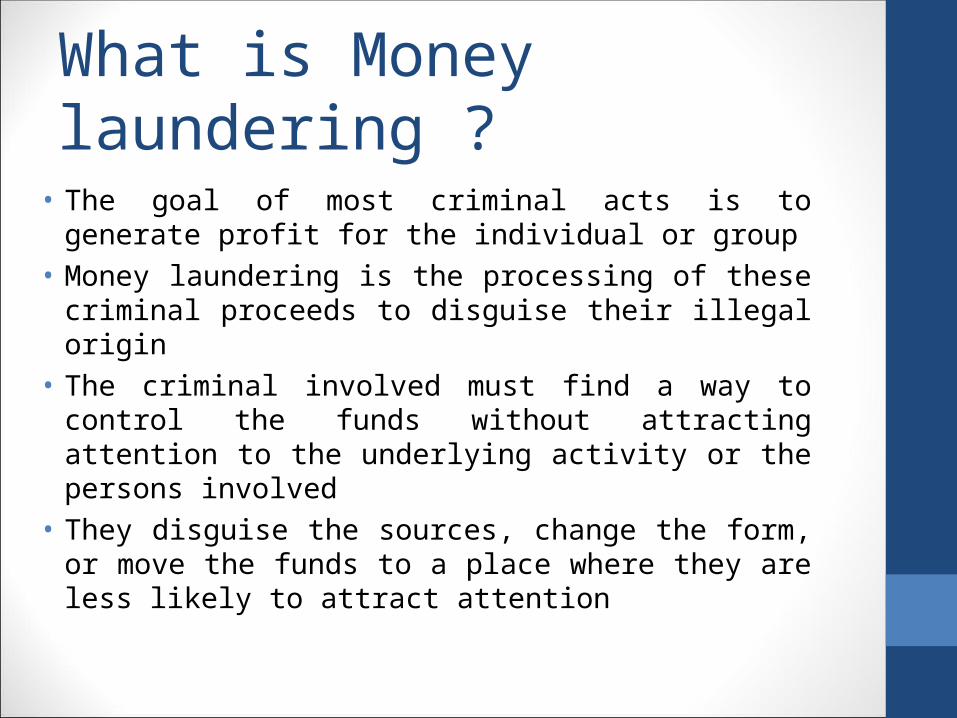

What is Money laundering ?

• The goal of most criminal acts is to generate profit for the individual or group

• Money laundering is the processing of these criminal proceeds to disguise their illegal origin

• The criminal involved must find a way to control the funds without attracting attention to the underlying activity or the persons involved

• They disguise the sources, change the form, or move the funds to a place where they are less likely to attract attention

Where Does Money Laundering occur?

• As money laundering is a consequence of almost all profit generating crime, it can occur practically anywhere in the world

• Because the objective of money laundering is to get the illegal funds back to the individual who generated them, launderers usually prefer to move funds through stable financial systems

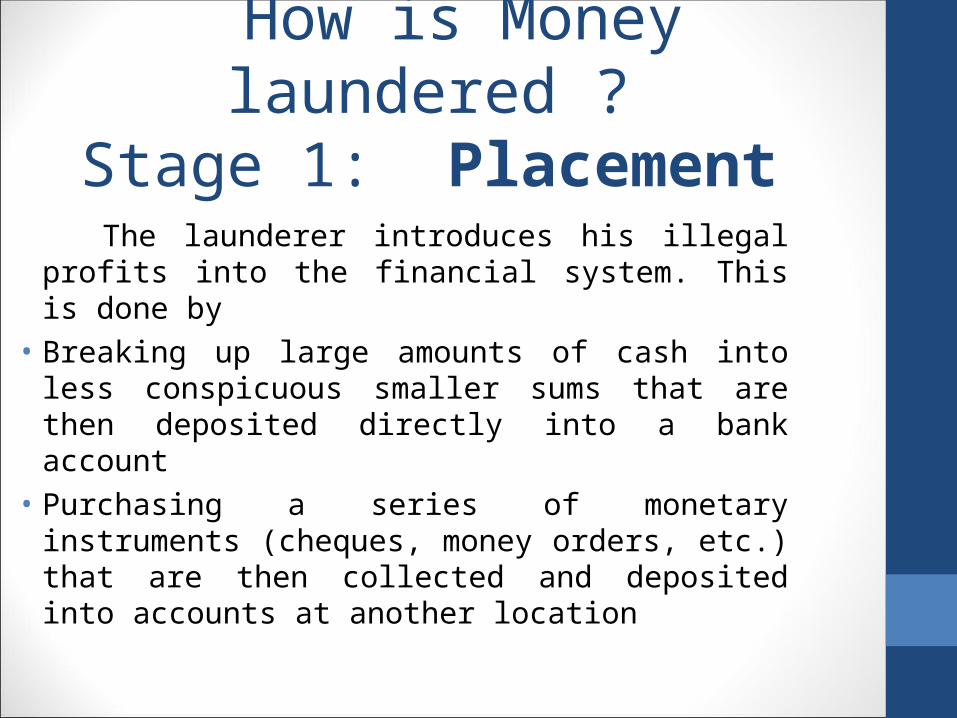

How is Money laundered ? Stage 1: Placement

The launderer introduces his illegal profits into the financial system. This is done by

• Breaking up large amounts of cash into less conspicuous smaller sums that are then deposited directly into a bank account

• Purchasing a series of monetary instruments (cheques, money orders, etc.) that are then collected and deposited into accounts at another location

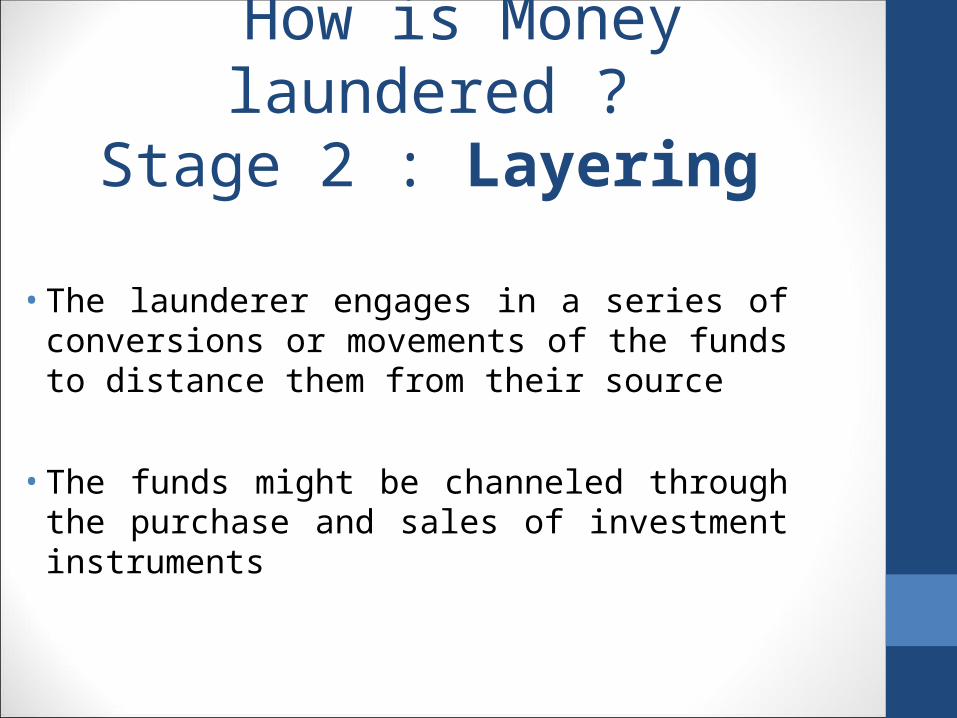

How is Money laundered ? Stage 2 : Layering

• The launderer engages in a series of conversions or movements of the funds to distance them from their source

• The funds might be channeled through the purchase and sales of investment instruments

How is Money laundered ? Stage 3 : Integration

• Having successfully processed his criminal profits through the first two phases the launderer then moves them to the third stage, integration

• The funds re-enter the legitimate economy. The launderer might choose to invest the funds into real estate, luxury assets, or business ventures

Financial Action Task Force

• About FATF An inter governmental policy making body, comprised of around 25 countries, that has a ministerial mandate to establish international standards for combating money laundering and terrorist financing.

• Birth The FATF was created at the 1989 G7 Summit meeting in Paris

• Role of FATF Sets international standards to combat money laundering and terrorist financing.Assesses and monitors compliance with the FATF standards

FATF - Recommendations

• The internationally endorsed global standards for implementing effective AML/CFT measures. In 1990, the FATF issued 40 recommendations to fight money laundering

• In 2001 it issued 8 special recommendations • In 2003 it issued 9th Special recommendation

FATF - Benefits

• Securing a more transparent and stable financial system that is more attractive to foreign investors

• Ensure that financial institutions are not vulnerable to infiltration or abuse by organised crime groups

• Build the capacity to fight terrorism and trace terrorist money

• Meet binding international obligations, and avoid the risk of sanctions or other action by the international community

• Avoid becoming a haven for criminals

FIU India

• Financial Intelligence Unit – India (FIU-IND) was set by the Government of India vide O.M. dated 18th November 2004

• FIU-IND is an independent body reporting directly to the Economic Intelligence Council (EIC) headed by the Finance Minister

• The main function of FIU-IND is to receive cash/suspicious transaction reports, analyse them and, as appropriate, disseminate valuable financial information to intelligence/enforcement agencies and regulatory authorities

Functions of FIU India

• Collection of Information • Analysis of Information• Sharing of Information• Act as Central Repository• Coordination• Research and Analysis

Prevention of Money Laundering Act (PMLA 2002)

• PMLA 2002 forms the core of the legal framework put in place by India to combat money laundering

• Came into force with effect from July 1, 2005• The PMLA rules impose obligation on banking

companies, financial institutions and intermediaries to verify identity of clients, maintain records and furnish information to FIU-IND

• PMLA defines money laundering offence and provides for the freezing, seizure and confiscation of the proceeds of crime

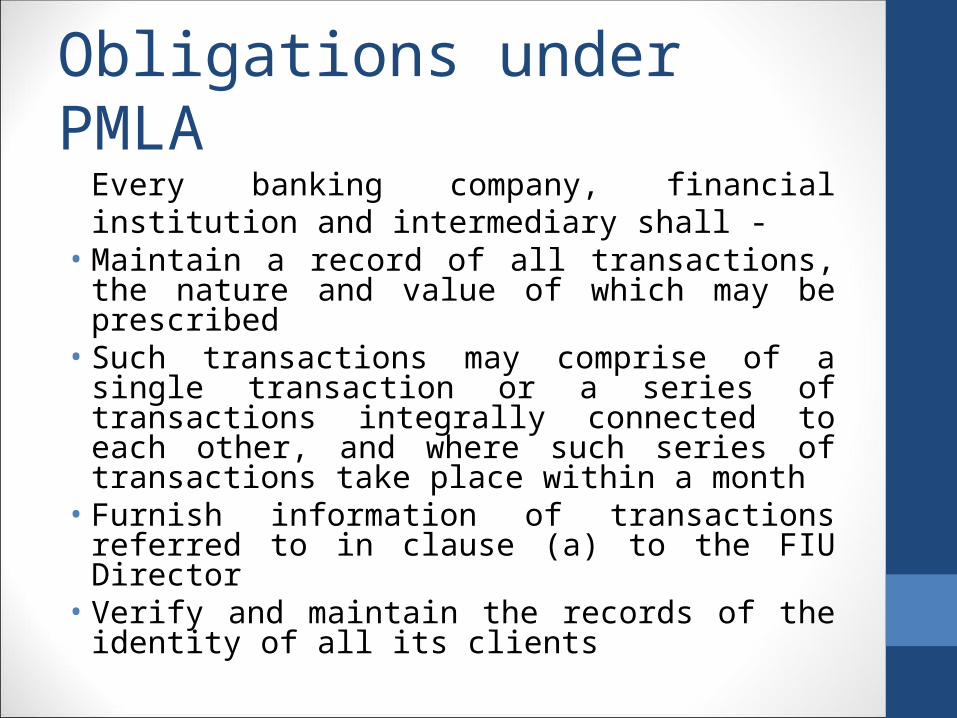

Obligations under PMLAEvery banking company, financial institution and intermediary shall -

• Maintain a record of all transactions, the nature and value of which may be prescribed

• Such transactions may comprise of a single transaction or a series of transactions integrally connected to each other, and where such series of transactions take place within a month

• Furnish information of transactions referred to in clause (a) to the FIU Director

• Verify and maintain the records of the identity of all its clients

Appointing a Principal Officer , Establishing Policies and Procedures, Sending these details to FIU IND

Screening of Client with Known criminal background , Sebi Debarred Database or UNSC

Capture Various Inputs in the Client Master, Client’ Risk Profile

Marking of Client With Special Category Capturing Financial Parameters like Income, Net worth etc..

Monitoring of Transactions and creation of alerts through a systemOnce a transaction crosses the thresh hold limit,

as defined in AML Policy / Risk Profile

Senior Management would consider the suspicious alertsand report the same to FIU if required

CDD

PROCESS

AML Workflow

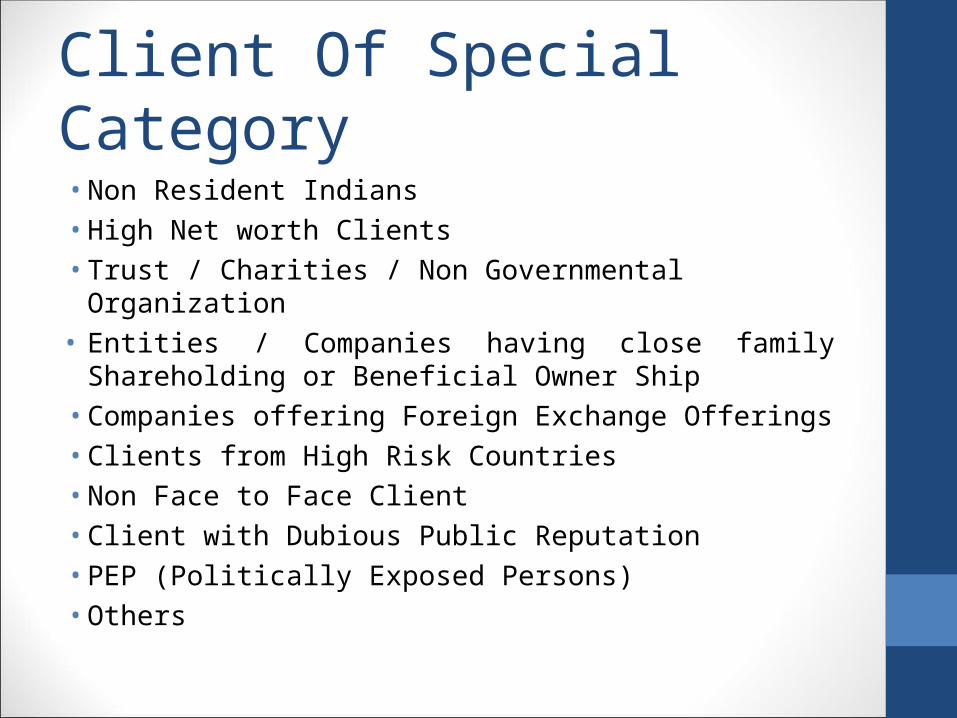

Client Of Special Category

• Non Resident Indians • High Net worth Clients • Trust / Charities / Non Governmental Organization• Entities / Companies having close family Shareholding

or Beneficial Owner Ship • Companies offering Foreign Exchange Offerings • Clients from High Risk Countries• Non Face to Face Client • Client with Dubious Public Reputation• PEP (Politically Exposed Persons)• Others

Suspicious transaction

Suspicious transaction means a transaction or a series of transactions, undertaken by a client or a group clients, that

• gives rise to a reasonable ground of suspicion that it may involve the proceeds of crime; or

• appears to be made in circumstances of unusual or unjustified complexity; or

• appears to have no economic rationale or bonafide purpose

Suspicious Transaction Criteria • Clients whose identity verification seems difficult or clients

that appear not to cooperate• Source of funds of client is not keeping in line with his

apparent standing• Substantial Increase in business without apparent cause• Attempted transfer of investment proceeds to apparently

unrelated parties• Appears to be an agent of an undisclosed principal• Multiple accounts with no apparent reason. • Unexplained high level funds activity with low securities

transactions• Large deposits for long term investments. Immediate

liquidation

Suspicious Trading Common Violations

• Insider trading is unique to the securities industry and generates illicit assets. As a predicate offence for money laundering, and an offence in its own right

• This type of misconduct is reportable on STRs • It has proven useful in assisting law enforcement and

regulators to prosecute such misconduct

Insider Trading Indicators• The customer makes a large purchase or sale of a security, or

option on a security, shortly before news is issued that affects the price of the security

• The customer is known to have friends or family who work at or for the securities issuer

• The customer lives in the locality where the issuer is located• The customer’s purchase does not correspond to his or her

investment profile. For example, the customer may never have invested in equity securities, but does so at an opportune time

• The customer’s account is opened or significantly funded shortly before a purchase; and

• The customer sells his or her position in a security in conjunction with a significant announcement about the security.

Insider Trading : Sample • Indicators: Unusual important transactions; Suspicion of insider trading; and

Securities sold a few months later. • Suspicious transaction/activity report information • In 2004, an ABC institution reported several unusual important purchases of shares of

two quoted companies, belonging to the same group, by company Y represented by Mr. X and a third party also in relation with company Y. Mr. X was manager in the two quoted companies, but also managed company Y.

• Case description • Mr. X, manager of an important group of companies, knew that a reorganisation of

the group was going to be publicly announced. This could have a favourable effect on the share price of two companies of this group after the reorganisation was announced.

• Mr. X used this knowledge to purchase securities of these two companies through another company he managed and through a third party before the reorganisation was announced.

• Once the reorganisation was announced, the share price of these two companies rose sharply. The shares were sold at a high profit.

•

Suspicious Trading Common Violations continued• Market manipulation generally refers to conduct that is

intended to deceive investors by controlling or artificially affecting the market for a security

• The simplest form is penny stock manipulation. The widely known scheme is pump and dump

• This scheme involves touting a company’s stock with false or misleading statements, often in conjunction with securities trades that raise the price of the security or make it appear as if the securities trading volume is higher than it actually is. Therefore the security price is artificially raised (“pumped”); the security is then sold (“dumped”) for a profit

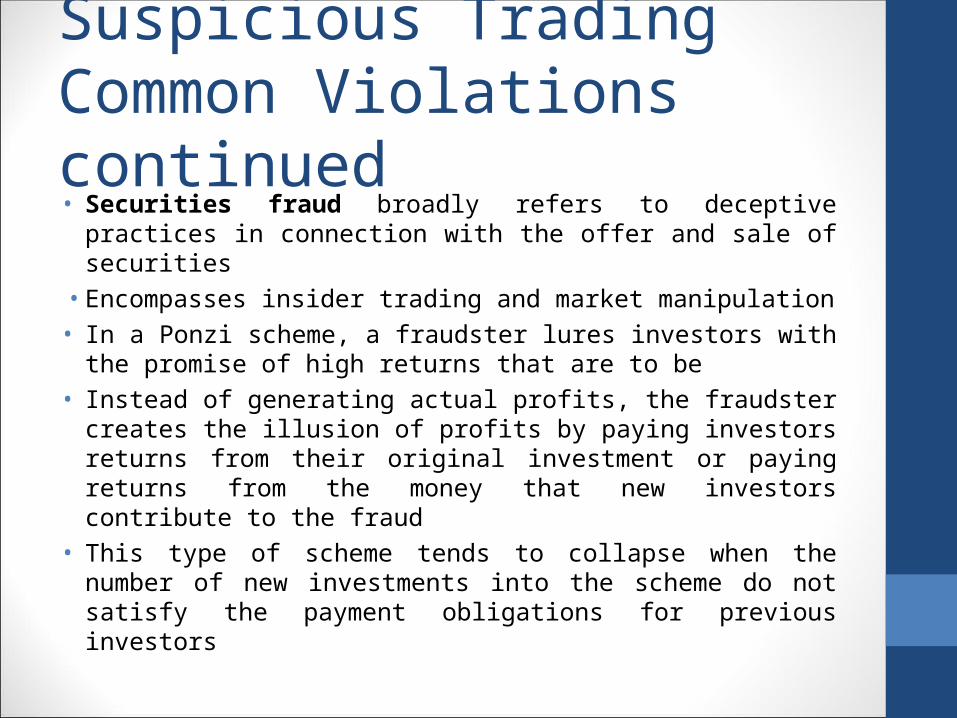

• Securities fraud broadly refers to deceptive practices in connection with the offer and sale of securities

• Encompasses insider trading and market manipulation• In a Ponzi scheme, a fraudster lures investors with the

promise of high returns that are to be• Instead of generating actual profits, the fraudster creates

the illusion of profits by paying investors returns from their original investment or paying returns from the money that new investors contribute to the fraud

• This type of scheme tends to collapse when the number of new investments into the scheme do not satisfy the payment obligations for previous investors

Suspicious Trading Common Violations continued

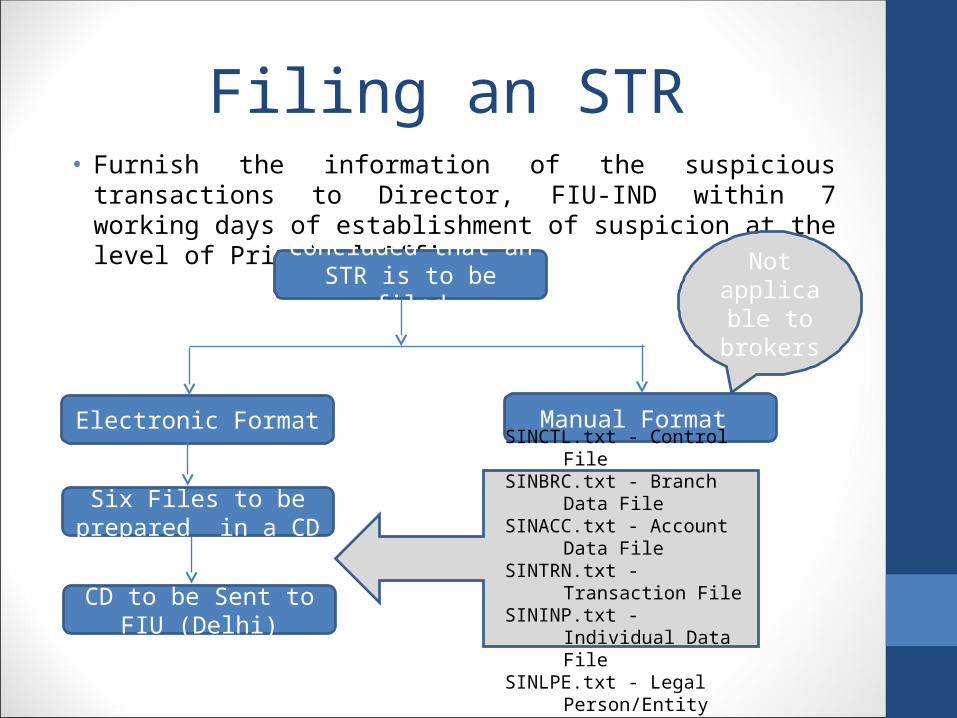

Filing an STR• Furnish the information of the suspicious transactions to Director, FIU-

IND within 7 working days of establishment of suspicion at the level of Principal Officer

Concluded that an STR is to be filed

Electronic Format Manual Format

Six Files to be prepared in a CD

CD to be Sent to FIU (Delhi)

Not applicable to brokers

SINCTL.txt - Control FileSINBRC.txt - Branch Data FileSINACC.txt - Account Data FileSINTRN.txt - Transaction FileSININP.txt - Individual Data FileSINLPE.txt - Legal Person/Entity

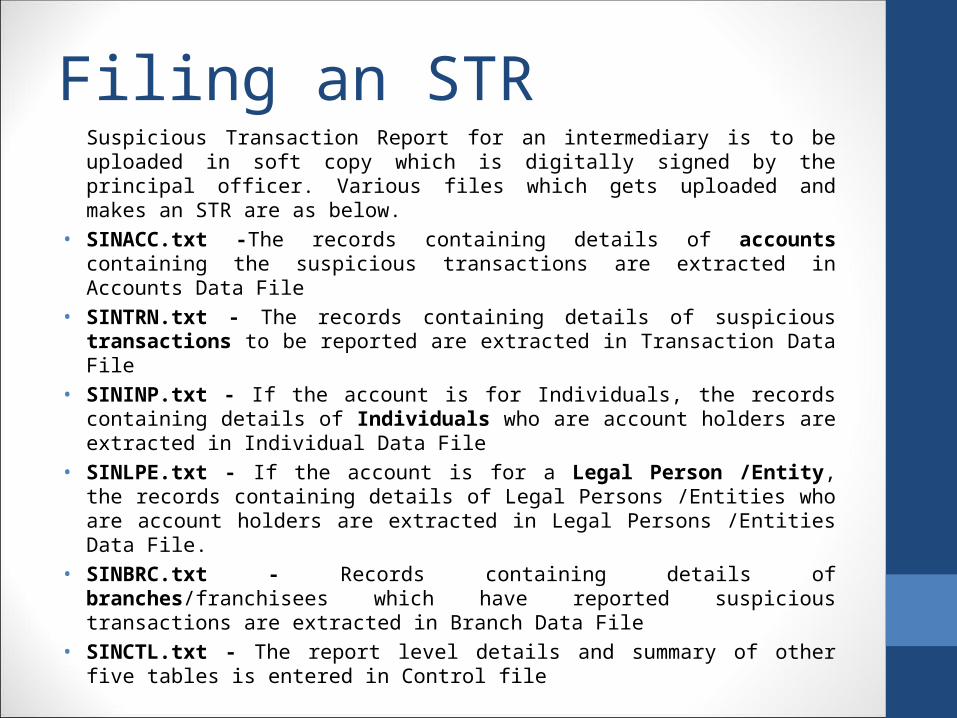

Filing an STRSuspicious Transaction Report for an intermediary is to be uploaded in soft copy which is digitally signed by the principal officer. Various files which gets uploaded and makes an STR are as below.

• SINACC.txt -The records containing details of accounts containing the suspicious transactions are extracted in Accounts Data File

• SINTRN.txt - The records containing details of suspicious transactions to be reported are extracted in Transaction Data File

• SININP.txt - If the account is for Individuals, the records containing details of Individuals who are account holders are extracted in Individual Data File

• SINLPE.txt - If the account is for a Legal Person /Entity, the records containing details of Legal Persons /Entities who are account holders are extracted in Legal Persons /Entities Data File.

• SINBRC.txt - Records containing details of branches/franchisees which have reported suspicious transactions are extracted in Branch Data File

• SINCTL.txt - The report level details and summary of other five tables is entered in Control file

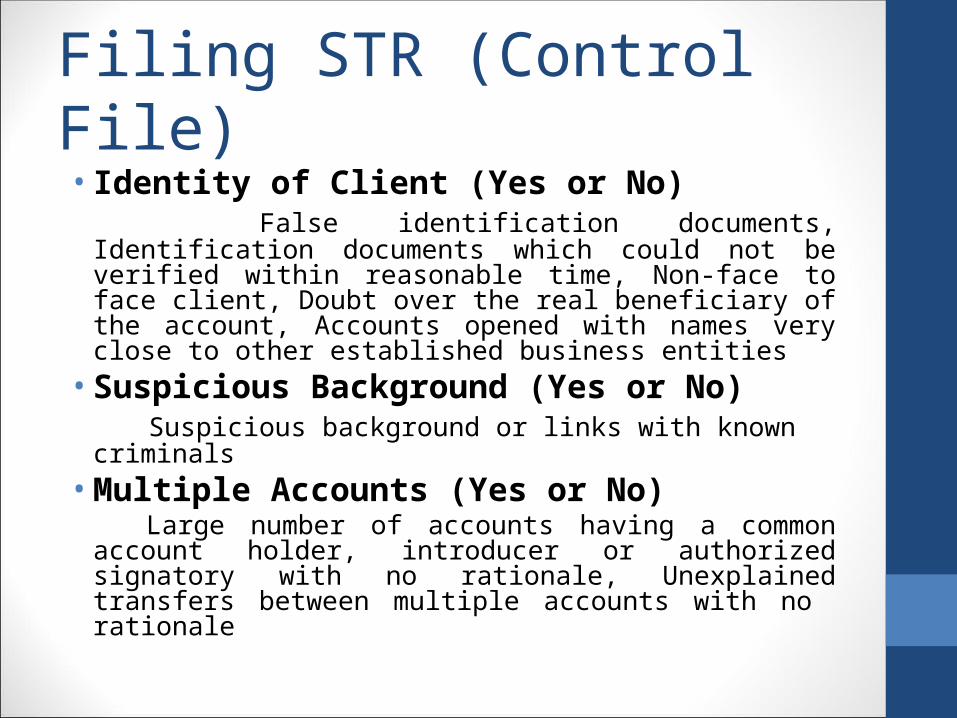

Filing STR (Control File)• Identity of Client (Yes or No) False identification documents, Identification documents which

could not be verified within reasonable time, Non-face to face client, Doubt over the real beneficiary of the account, Accounts opened with names very close to other established business entities

• Suspicious Background (Yes or No) Suspicious background or links with known criminals• Multiple Accounts (Yes or No) Large number of accounts having a common account holder,

introducer or authorized signatory with no rationale, Unexplained transfers between multiple accounts with no rationale

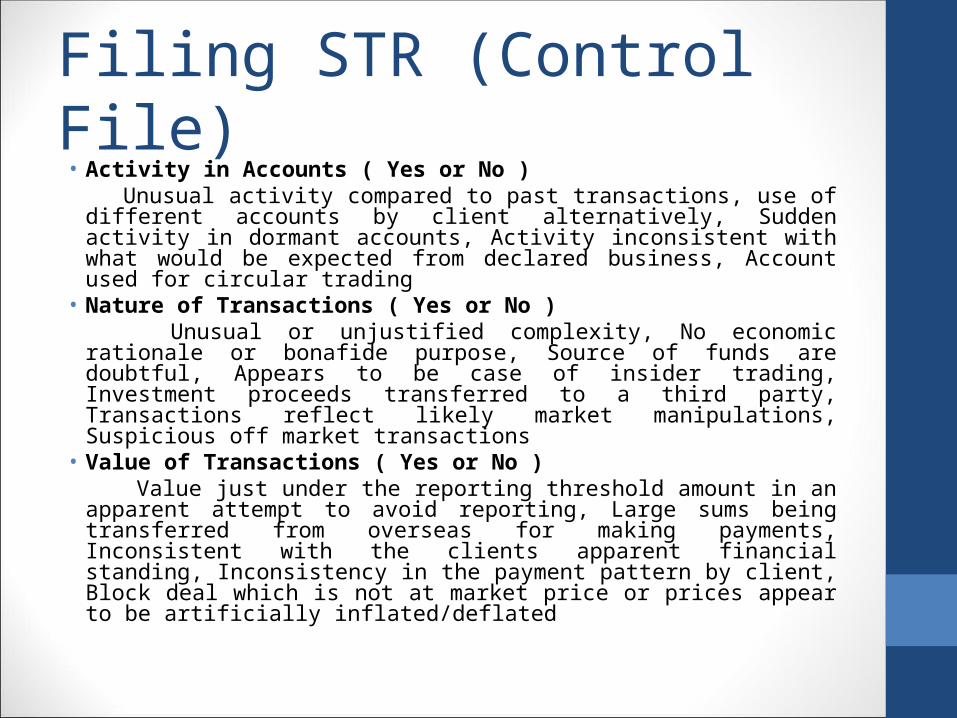

Filing STR (Control File)• Activity in Accounts ( Yes or No ) Unusual activity compared to past transactions, use of different

accounts by client alternatively, Sudden activity in dormant accounts, Activity inconsistent with what would be expected from declared business, Account used for circular trading

• Nature of Transactions ( Yes or No ) Unusual or unjustified complexity, No economic rationale or bonafide

purpose, Source of funds are doubtful, Appears to be case of insider trading, Investment proceeds transferred to a third party, Transactions reflect likely market manipulations, Suspicious off market transactions

• Value of Transactions ( Yes or No ) Value just under the reporting threshold amount in an apparent

attempt to avoid reporting, Large sums being transferred from overseas for making payments, Inconsistent with the clients apparent financial standing, Inconsistency in the payment pattern by client, Block deal which is not at market price or prices appear to be artificially inflated/deflated

STR Important Points• Continuity in dealing with the client as normal until told

otherwise and the client shall not be told of the report/suspicion

• Intermediaries shall not put any restrictions on operations in the accounts where an STR has been made

• Intermediaries and their directors, officers and employees (permanent and temporary) shall be prohibited from disclosing (“tipping off”) the fact that a STR or related information is being reported or provided to the FIU-IND. Thus, it shall be ensured that there is no tipping off to the client at any level.

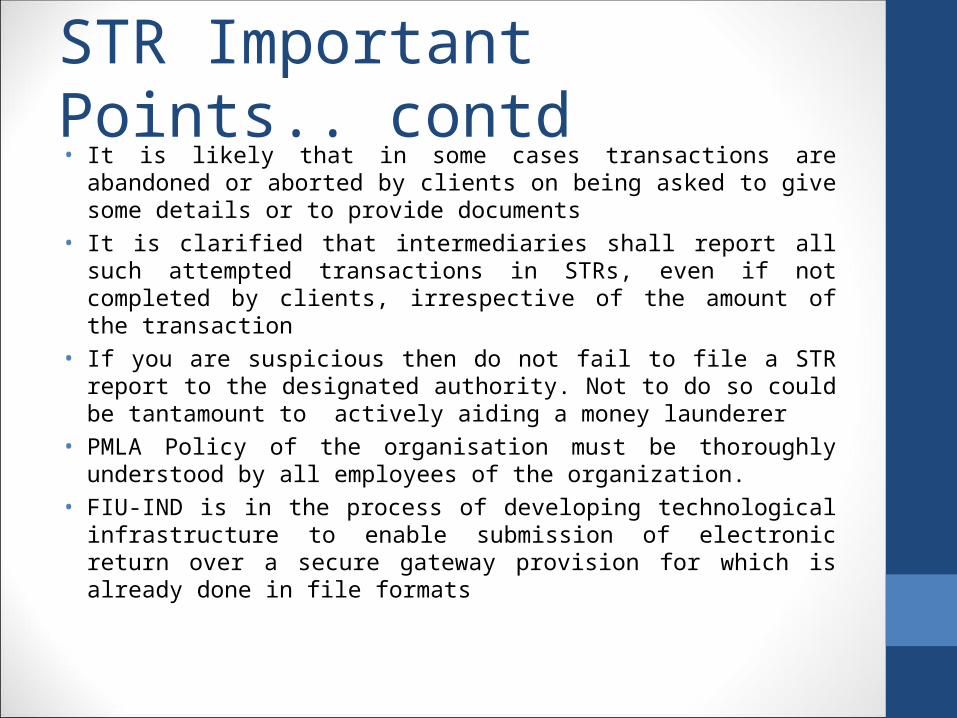

STR Important Points.. contd• It is likely that in some cases transactions are abandoned or

aborted by clients on being asked to give some details or to provide documents

• It is clarified that intermediaries shall report all such attempted transactions in STRs, even if not completed by clients, irrespective of the amount of the transaction

• If you are suspicious then do not fail to file a STR report to the designated authority. Not to do so could be tantamount to actively aiding a money launderer

• PMLA Policy of the organisation must be thoroughly understood by all employees of the organization.

• FIU-IND is in the process of developing technological infrastructure to enable submission of electronic return over a secure gateway provision for which is already done in file formats

Recordkeeping• Maintain such records as are sufficient to permit reconstruction of

individual transactions so as to provide, if necessary, evidence for prosecution of criminal behavior

• Where required by the investigating authority, they shall retain certain records, e.g. client identification, account files, and business correspondence, for periods which may exceed those required under the SEBI Act, Rules and Regulations framed there-under PMLA, other relevant legislations, Rules and Regulations or Exchange bye-laws or circulars

• Maintain records for a period of five years from the date of transactions between the client and intermediary i.e. the date of termination of an account or business

• In situations where the records relate to on-going investigations or transactions which have been the subject of a suspicious transaction reporting, they shall be retained until it is confirmed that the case has been closed relationship between the client and intermediary

Summary : Money Laundering in some Economies• Launderers are continuously looking for new routes for

laundering their funds• Economies with growing or developing financial centers,

but inadequate controls are particularly vulnerable as established financial centre countries implement comprehensive anti-money laundering regimes

• Some might argue that developing economies cannot afford to be too selective about the sources of capital they attract. But postponing action is dangerous. The more it is deferred, the more entrenched organized crime can become.

How does Money Laundering affect business ?

• Hampers economic growth. • Allows anti social elements to damage our society. • Will take investors away from the financial system if they

feel it is unsafe. • A reputation for integrity is the one of the most valuable

assets of a financial institution• The institution could be drawn into active complicity with

criminals and become part of the criminal network itself, if the employees have been involved or for turning blind eye

• Evidence of such complicity will have a damaging effect on the attitudes of other financial intermediaries and of regulatory authorities, as well as ordinary customers

Thank You…